mtg q12013 presentation final

Post on 21-Oct-2014

8.623 views

DESCRIPTION

TRANSCRIPT

1

First Quarter 2013

Financial Results

2

Forward looking statements

Forward-looking information and Safe Harbour Statement under the U.S. Private Securities Litigation

Reform Act of 1995

This report contains forward-looking information based on the current expectation of MTG management.

Although management deems that the expectations presented by such forward-looking information are

reasonable, such forward-looking information is subject to risks and uncertainties and no guarantee can be

given that these expectations will prove correct. Accordingly, the actual future outcome could vary considerably

when compared to what is stated in the forward-looking information, due to such factors as described above in

the Risks & Uncertainties section.

3

Strong Growth in

Emerging Markets

4

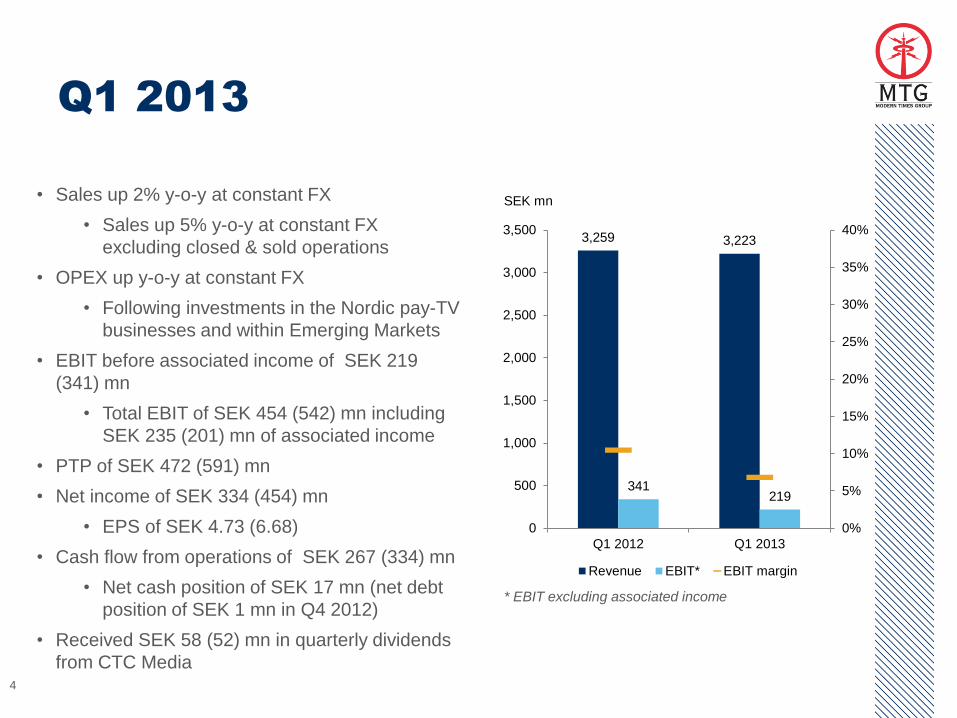

Q1 2013

• Sales up 2% y-o-y at constant FX

• Sales up 5% y-o-y at constant FX

excluding closed & sold operations

• OPEX up y-o-y at constant FX

• Following investments in the Nordic pay-TV

businesses and within Emerging Markets

• EBIT before associated income of SEK 219

(341) mn

• Total EBIT of SEK 454 (542) mn including

SEK 235 (201) mn of associated income

• PTP of SEK 472 (591) mn

• Net income of SEK 334 (454) mn

• EPS of SEK 4.73 (6.68)

• Cash flow from operations of SEK 267 (334) mn

• Net cash position of SEK 17 mn (net debt

position of SEK 1 mn in Q4 2012)

• Received SEK 58 (52) mn in quarterly dividends

from CTC Media

SEK mn

* EBIT excluding associated income

3,259 3,223

341 219

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Q1 2012 Q1 2013

Revenue EBIT* EBIT margin

Forward Expectations

As previously announced, the Group continues to expect its Nordic pay-TV business to

grow its revenues at constant exchange rates in 2013, and to report an operating (EBIT)

margin of approximately 10-12% for the full year 2013. The segment margin is expected

to increase in 2014.

The Group also continues to expect its Emerging Market pay-TV operations to achieve a

breakeven EBIT result for the full year 2013 with rising profitability levels in 2014.

5

6

Operating Review

7

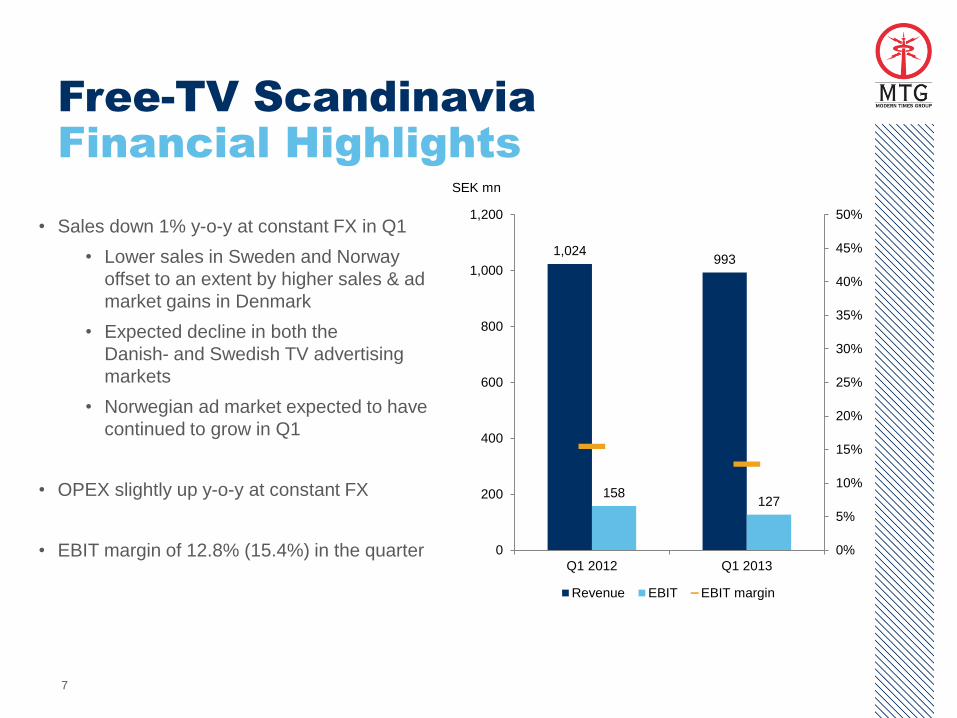

Free-TV Scandinavia

Financial Highlights

• Sales down 1% y-o-y at constant FX in Q1

• Lower sales in Sweden and Norway

offset to an extent by higher sales & ad

market gains in Denmark

• Expected decline in both the

Danish- and Swedish TV advertising

markets

• Norwegian ad market expected to have

continued to grow in Q1

• OPEX slightly up y-o-y at constant FX

• EBIT margin of 12.8% (15.4%) in the quarter

SEK mn

1,024 993

158 127

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

200

400

600

800

1,000

1,200

Q1 2012 Q1 2013

Revenue EBIT EBIT margin

8

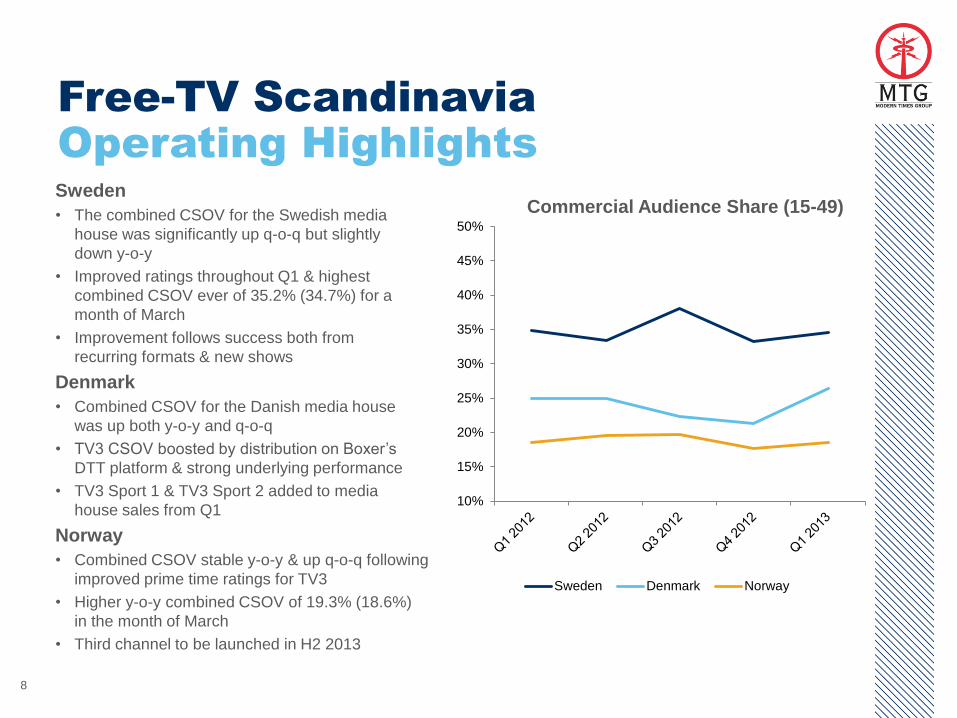

Free-TV Scandinavia

Operating Highlights

Sweden

• The combined CSOV for the Swedish media

house was significantly up q-o-q but slightly

down y-o-y

• Improved ratings throughout Q1 & highest

combined CSOV ever of 35.2% (34.7%) for a

month of March

• Improvement follows success both from

recurring formats & new shows

Denmark

• Combined CSOV for the Danish media house

was up both y-o-y and q-o-q

• TV3 CSOV boosted by distribution on Boxer’s

DTT platform & strong underlying performance

• TV3 Sport 1 & TV3 Sport 2 added to media

house sales from Q1

Norway

• Combined CSOV stable y-o-y & up q-o-q following

improved prime time ratings for TV3

• Higher y-o-y combined CSOV of 19.3% (18.6%)

in the month of March

• Third channel to be launched in H2 2013

Commercial Audience Share (15-49)

10%

15%

20%

25%

30%

35%

40%

45%

50%

Sweden Denmark Norway

9 9

Nordic traffic levels growing & AVOD

services are growing rapidly

Key free-TV brands go online to drive

viewing & strengthen engagement

Free-TV Scandinavia

Focused AVOD development

• Nordic traffic levels are growing

• Danish Q1 AVOD traffic higher than

total FY12 traffic

• Launch of clip site Viasatsport.se in

January 2013 & new music video portal

online

• Like.tv Second Screen app growing & to

be rolled out on more platforms in 2013

• MTG adapting content commission

strategies to leverage linear & online

assets

10

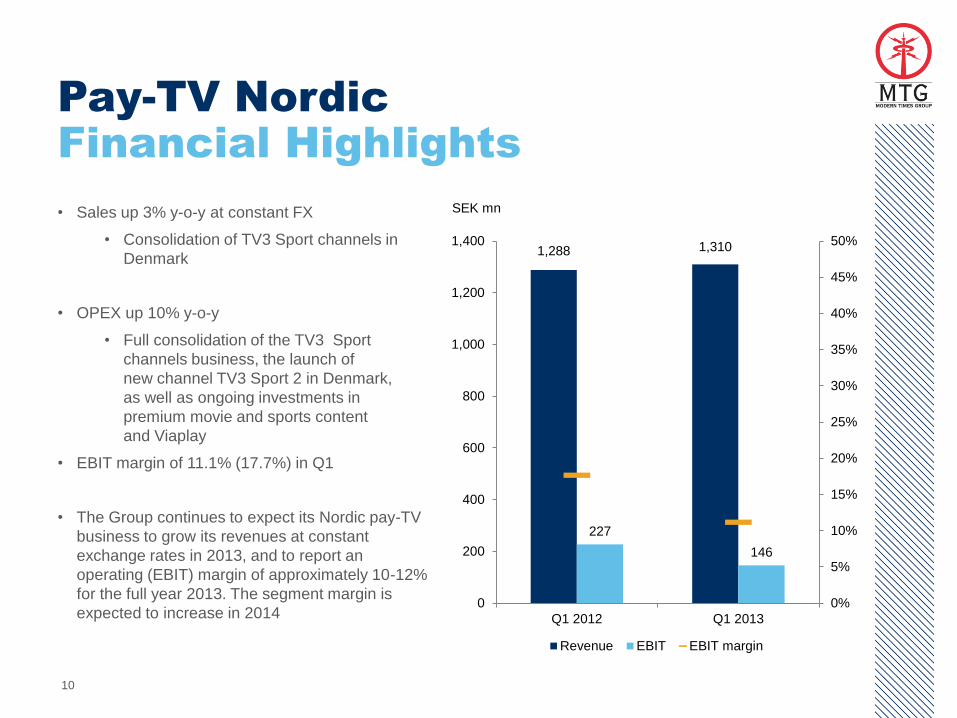

Pay-TV Nordic

Financial Highlights

• Sales up 3% y-o-y at constant FX

• Consolidation of TV3 Sport channels in

Denmark

• OPEX up 10% y-o-y

• Full consolidation of the TV3 Sport

channels business, the launch of

new channel TV3 Sport 2 in Denmark,

as well as ongoing investments in

premium movie and sports content

and Viaplay

• EBIT margin of 11.1% (17.7%) in Q1

• The Group continues to expect its Nordic pay-TV

business to grow its revenues at constant

exchange rates in 2013, and to report an

operating (EBIT) margin of approximately 10-12%

for the full year 2013. The segment margin is

expected to increase in 2014

SEK mn

1,288 1,310

227

146

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

200

400

600

800

1,000

1,200

1,400

Q1 2012 Q1 2013

Revenue EBIT EBIT margin

11

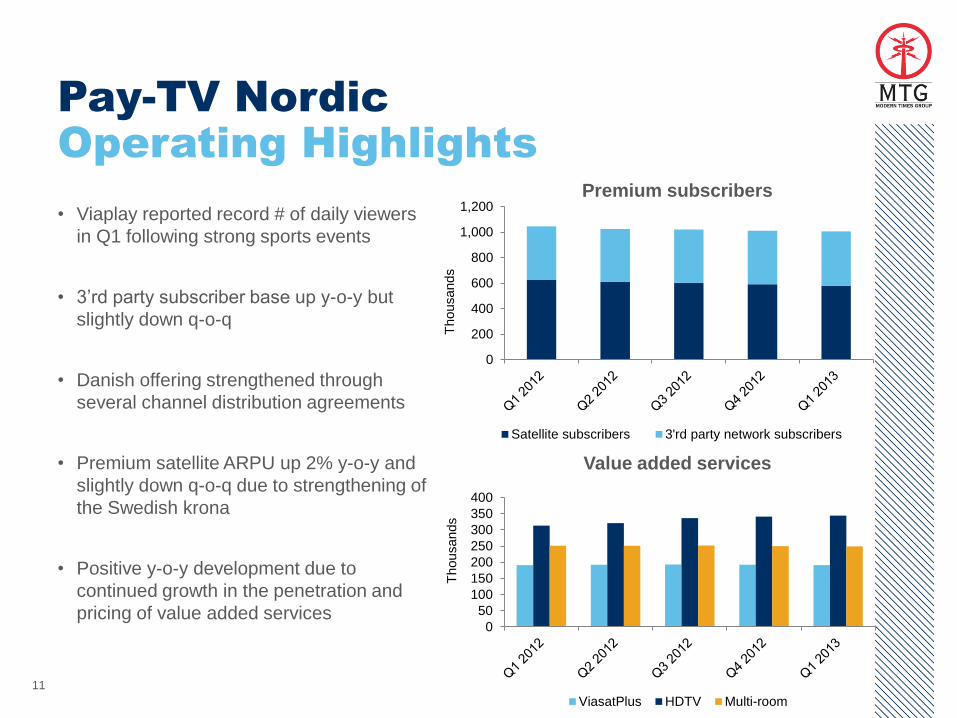

Pay-TV Nordic

Operating Highlights

• Viaplay reported record # of daily viewers

in Q1 following strong sports events

• 3’rd party subscriber base up y-o-y but

slightly down q-o-q

• Danish offering strengthened through

several channel distribution agreements

• Premium satellite ARPU up 2% y-o-y and

slightly down q-o-q due to strengthening of

the Swedish krona

• Positive y-o-y development due to

continued growth in the penetration and

pricing of value added services

Thousands

Thousands

Premium subscribers

Value added services

0

200

400

600

800

1,000

1,200

Satellite subscribers 3'rd party network subscribers

0

50

100

150

200

250

300

350

400

ViasatPlus HDTV Multi-room

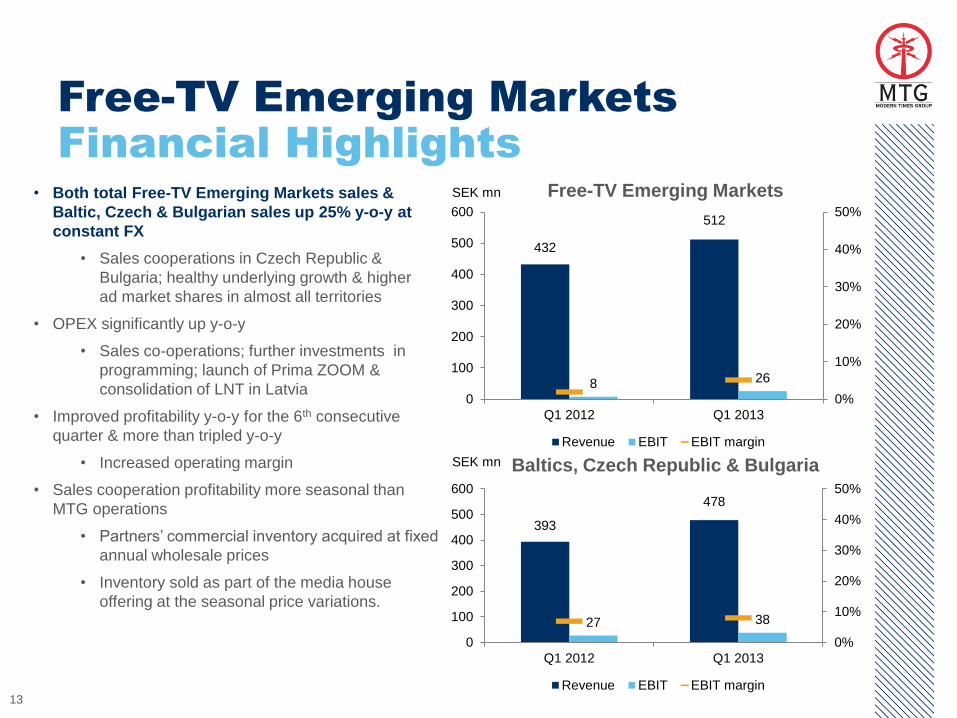

• Both total Free-TV Emerging Markets sales &

Baltic, Czech & Bulgarian sales up 25% y-o-y at

constant FX

• Sales cooperations in Czech Republic &

Bulgaria; healthy underlying growth & higher

ad market shares in almost all territories

• OPEX significantly up y-o-y

• Sales co-operations; further investments in

programming; launch of Prima ZOOM &

consolidation of LNT in Latvia

• Improved profitability y-o-y for the 6th consecutive

quarter & more than tripled y-o-y

• Increased operating margin

• Sales cooperation profitability more seasonal than

MTG operations

• Partners’ commercial inventory acquired at fixed

annual wholesale prices

• Inventory sold as part of the media house

offering at the seasonal price variations.

13

Free-TV Emerging Markets

Financial Highlights

Free-TV Emerging Markets

Baltics, Czech Republic & Bulgaria

SEK mn

SEK mn

432

512

8 26

0%

10%

20%

30%

40%

50%

0

100

200

300

400

500

600

Q1 2012 Q1 2013

Revenue EBIT EBIT margin

393

478

27 38

0%

10%

20%

30%

40%

50%

0

100

200

300

400

500

600

Q1 2012 Q1 2013

Revenue EBIT EBIT margin

14

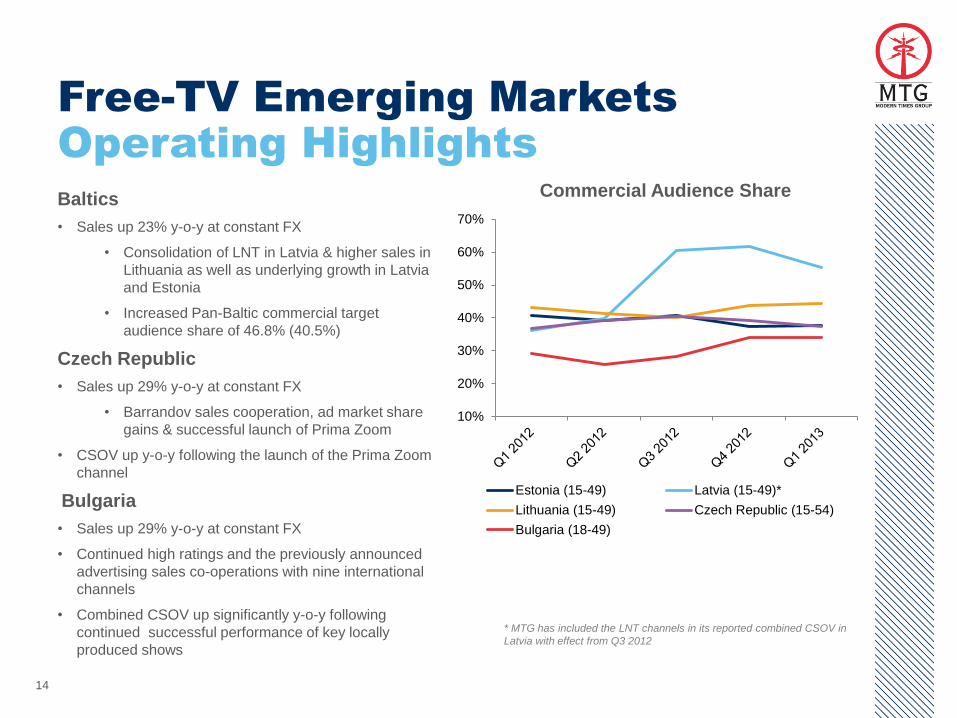

Free-TV Emerging Markets

Operating Highlights

Baltics

• Sales up 23% y-o-y at constant FX

• Consolidation of LNT in Latvia & higher sales in

Lithuania as well as underlying growth in Latvia

and Estonia

• Increased Pan-Baltic commercial target

audience share of 46.8% (40.5%)

Czech Republic

• Sales up 29% y-o-y at constant FX

• Barrandov sales cooperation, ad market share

gains & successful launch of Prima Zoom

• CSOV up y-o-y following the launch of the Prima Zoom

channel

Bulgaria

• Sales up 29% y-o-y at constant FX

• Continued high ratings and the previously announced

advertising sales co-operations with nine international

channels

• Combined CSOV up significantly y-o-y following

continued successful performance of key locally

produced shows

Commercial Audience Share

* MTG has included the LNT channels in its reported combined CSOV in

Latvia with effect from Q3 2012

10%

20%

30%

40%

50%

60%

70%

Estonia (15-49) Latvia (15-49)*

Lithuania (15-49) Czech Republic (15-54)

Bulgaria (18-49)

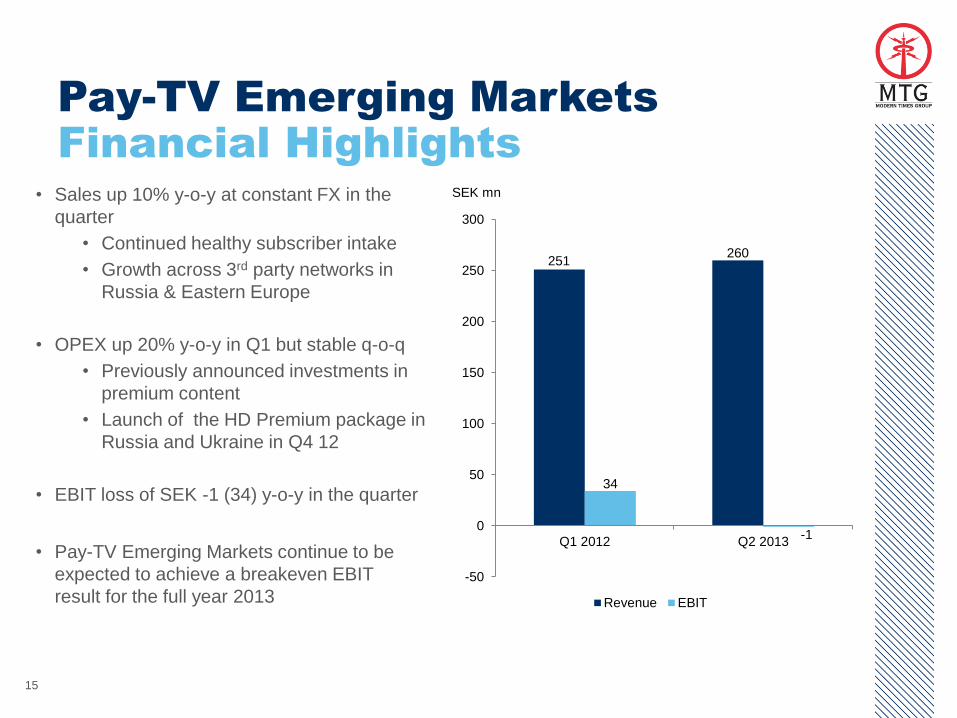

• Sales up 10% y-o-y at constant FX in the

quarter

• Continued healthy subscriber intake

• Growth across 3rd party networks in

Russia & Eastern Europe

• OPEX up 20% y-o-y in Q1 but stable q-o-q

• Previously announced investments in

premium content

• Launch of the HD Premium package in

Russia and Ukraine in Q4 12

• EBIT loss of SEK -1 (34) y-o-y in the quarter

• Pay-TV Emerging Markets continue to be

expected to achieve a breakeven EBIT

result for the full year 2013

15

Pay-TV Emerging Markets

Financial Highlights

SEK mn

251 260

34

-1

-50

0

50

100

150

200

250

300

Q1 2012 Q2 2013

Revenue EBIT

16

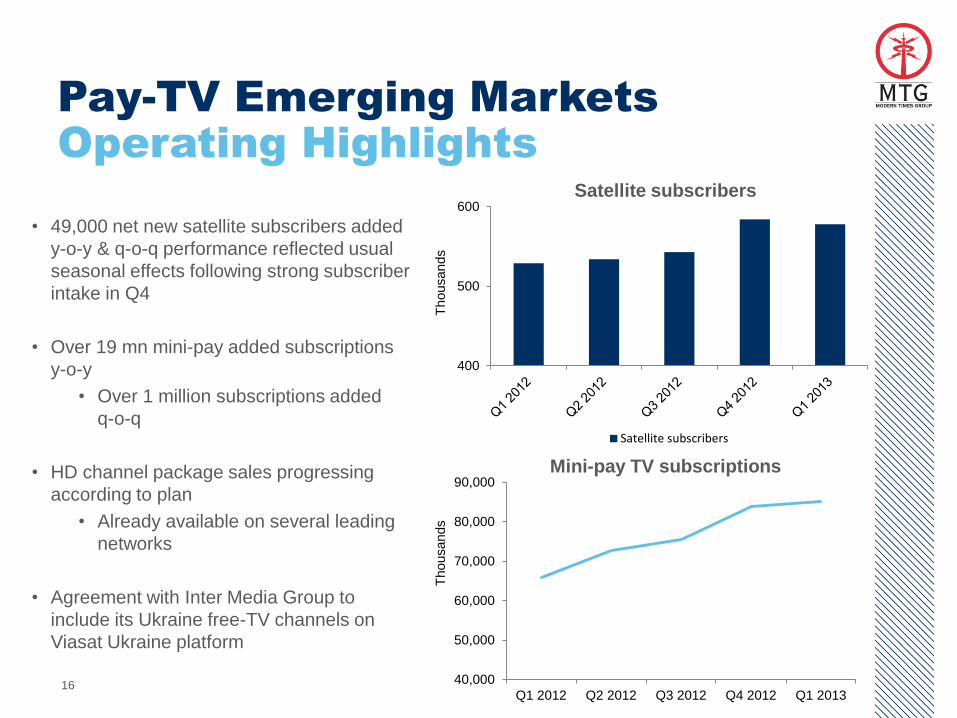

Pay-TV Emerging Markets

Operating Highlights

• 49,000 net new satellite subscribers added

y-o-y & q-o-q performance reflected usual

seasonal effects following strong subscriber

intake in Q4

• Over 19 mn mini-pay added subscriptions

y-o-y

• Over 1 million subscriptions added

q-o-q

• HD channel package sales progressing

according to plan

• Already available on several leading

networks

• Agreement with Inter Media Group to

include its Ukraine free-TV channels on

Viasat Ukraine platform

Satellite subscribers

Mini-pay TV subscriptions

Thousands

Thousands

400

500

600

Satellite subscribers

40,000

50,000

60,000

70,000

80,000

90,000

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

0

2

4

6

8

10

12

14

16

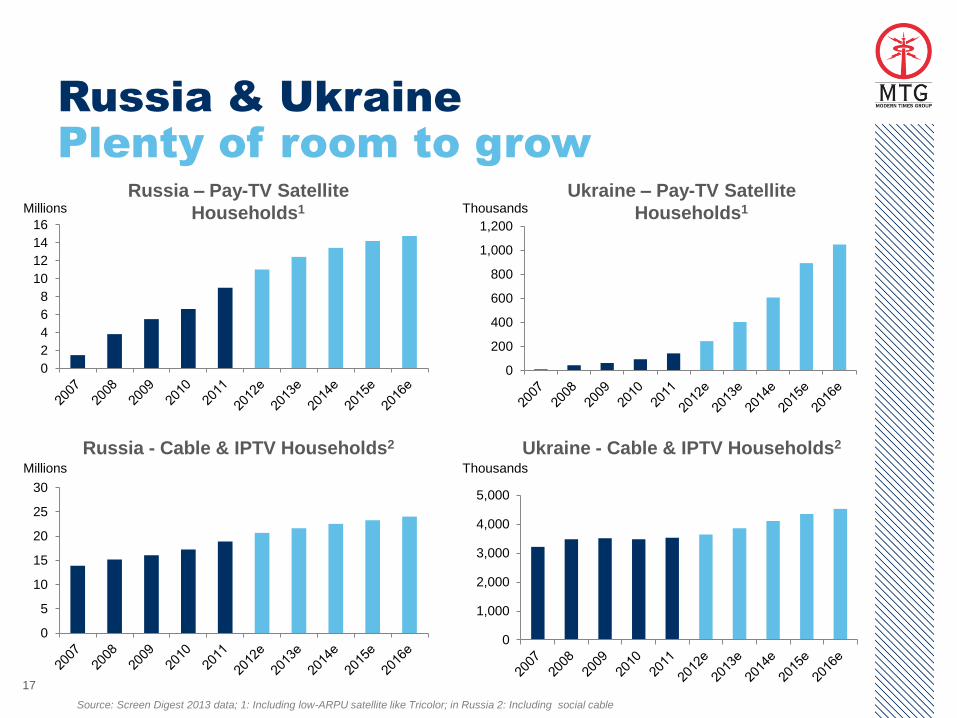

Russia & Ukraine

Plenty of room to grow

17

Millions

Russia – Pay-TV Satellite

Households1

Russia - Cable & IPTV Households2

0

5

10

15

20

25

30

Millions

Ukraine – Pay-TV Satellite

Households1

Ukraine - Cable & IPTV Households2

0

200

400

600

800

1,000

1,200

Thousands

Thousands

0

1,000

2,000

3,000

4,000

5,000

Source: Screen Digest 2013 data; 1: Including low-ARPU satellite like Tricolor; in Russia 2: Including social cable

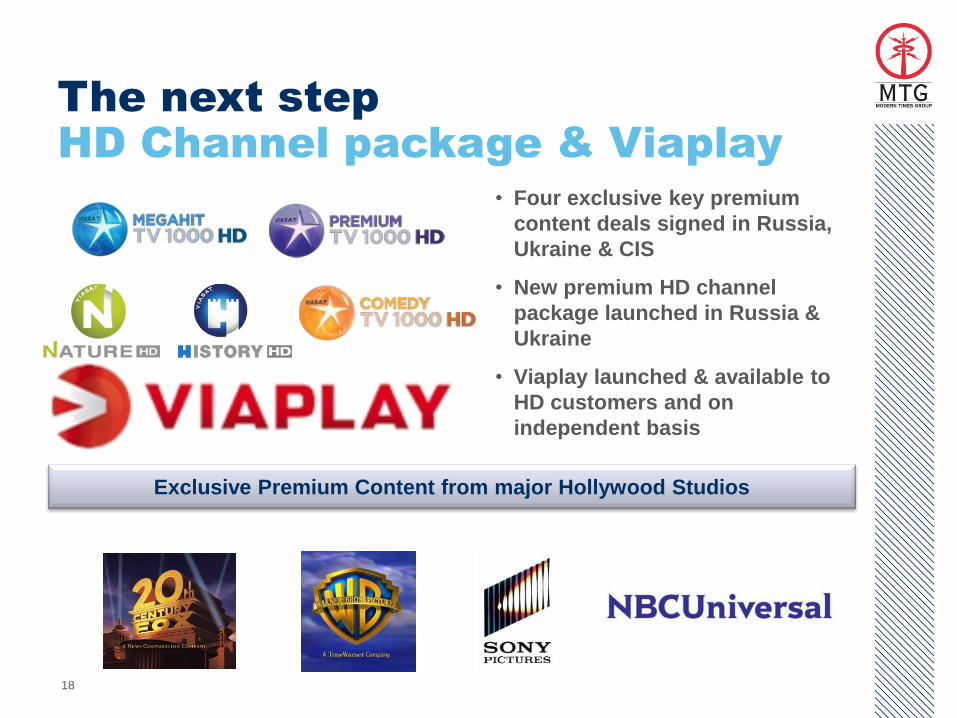

The next step

HD Channel package & Viaplay

18

• Four exclusive key premium

content deals signed in Russia,

Ukraine & CIS

• New premium HD channel

package launched in Russia &

Ukraine

• Viaplay launched & available to

HD customers and on

independent basis

Exclusive Premium Content from major Hollywood Studios

19

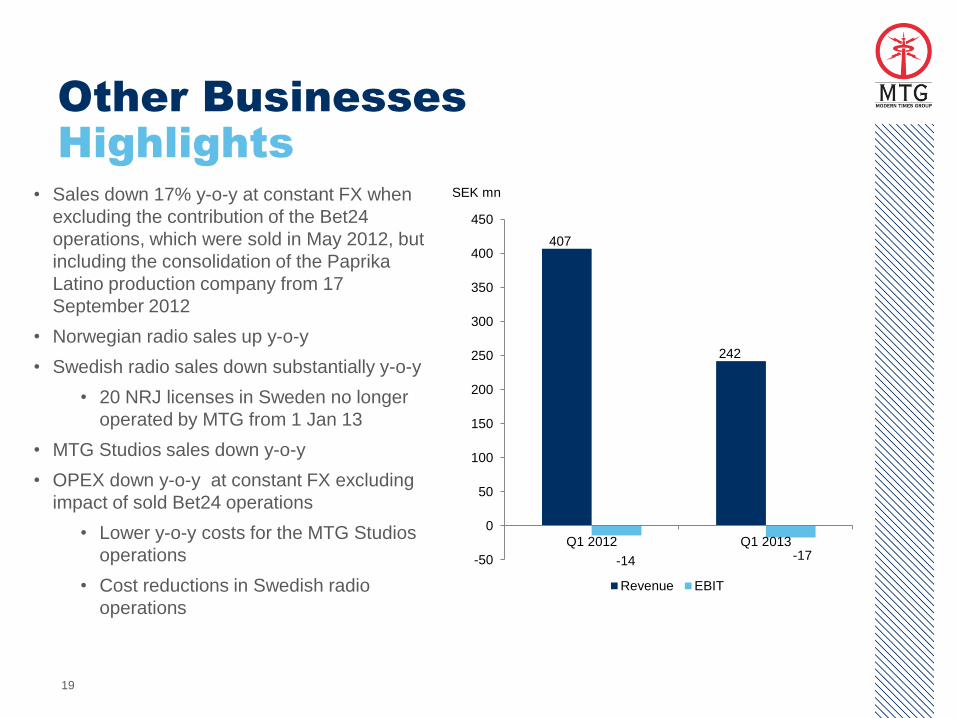

Other Businesses

Highlights

• Sales down 17% y-o-y at constant FX when

excluding the contribution of the Bet24

operations, which were sold in May 2012, but

including the consolidation of the Paprika

Latino production company from 17

September 2012

• Norwegian radio sales up y-o-y

• Swedish radio sales down substantially y-o-y

• 20 NRJ licenses in Sweden no longer

operated by MTG from 1 Jan 13

• MTG Studios sales down y-o-y

• OPEX down y-o-y at constant FX excluding

impact of sold Bet24 operations

• Lower y-o-y costs for the MTG Studios

operations

• Cost reductions in Swedish radio

operations

SEK mn

407

242

-14 -17 -50

0

50

100

150

200

250

300

350

400

450

Q1 2012 Q1 2013

Revenue EBIT

20

Financial Review

21

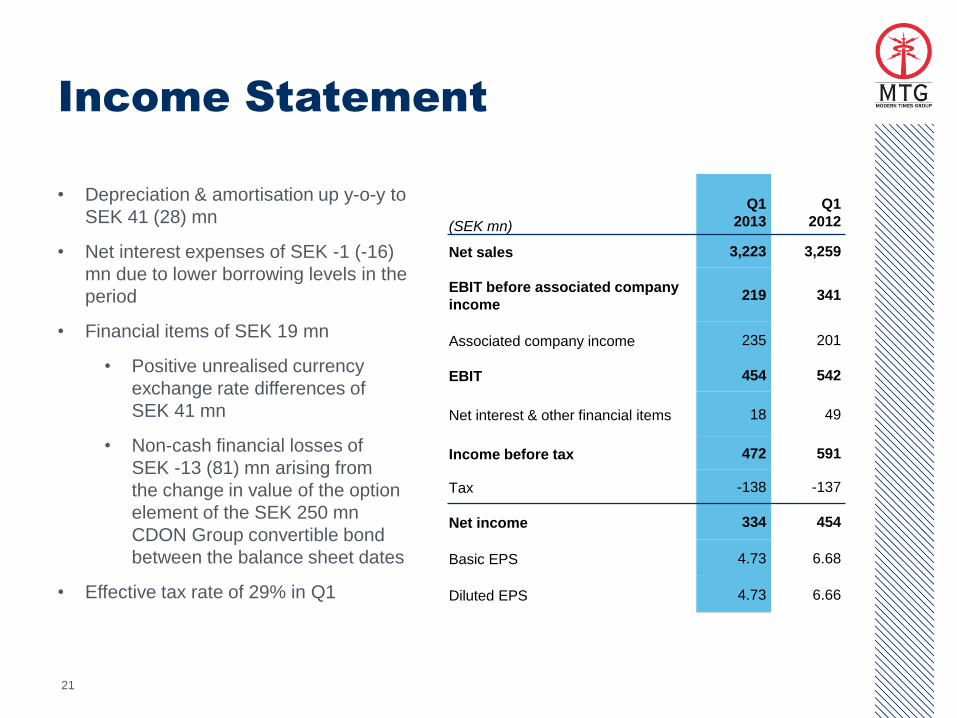

Income Statement

• Depreciation & amortisation up y-o-y to

SEK 41 (28) mn

• Net interest expenses of SEK -1 (-16)

mn due to lower borrowing levels in the

period

• Financial items of SEK 19 mn

• Positive unrealised currency

exchange rate differences of

SEK 41 mn

• Non-cash financial losses of

SEK -13 (81) mn arising from

the change in value of the option

element of the SEK 250 mn

CDON Group convertible bond

between the balance sheet dates

• Effective tax rate of 29% in Q1

(SEK mn)

Q1

2013

Q1

2012

Net sales 3,223 3,259

EBIT before associated company

income 219 341

Associated company income 235 201

EBIT 454 542

Net interest & other financial items 18 49

Income before tax 472 591

Tax -138 -137

Net income 334 454

Basic EPS 4.73 6.68

Diluted EPS 4.73 6.66

22

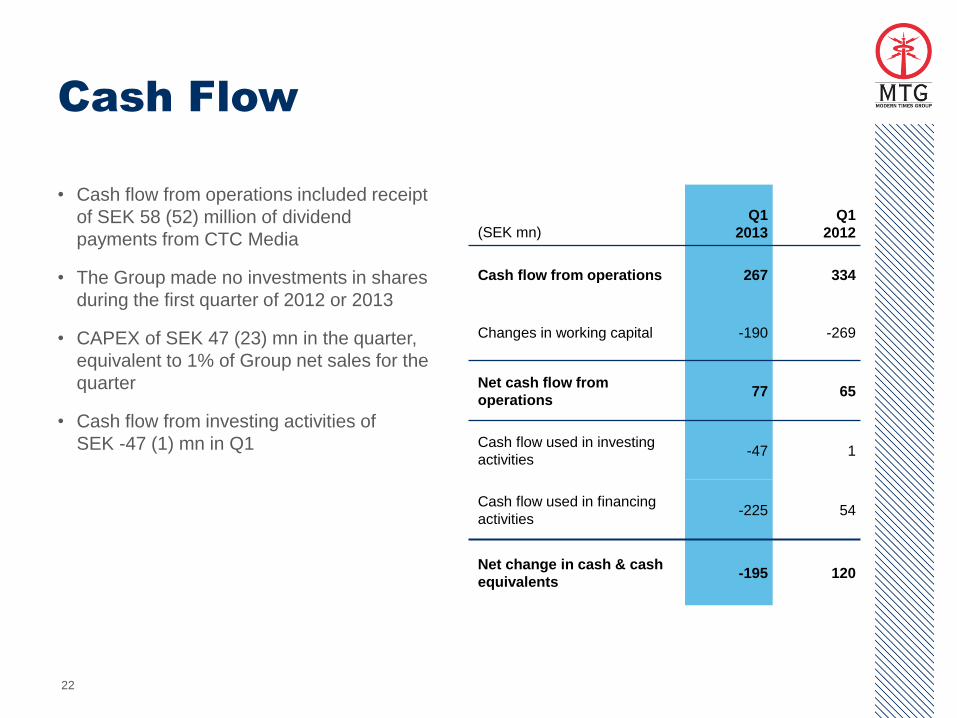

Cash Flow

• Cash flow from operations included receipt

of SEK 58 (52) million of dividend

payments from CTC Media

• The Group made no investments in shares

during the first quarter of 2012 or 2013

• CAPEX of SEK 47 (23) mn in the quarter,

equivalent to 1% of Group net sales for the

quarter

• Cash flow from investing activities of

SEK -47 (1) mn in Q1

(SEK mn)

Q1

2013

Q1

2012

Cash flow from operations 267 334

Changes in working capital -190 -269

Net cash flow from

operations 77 65

Cash flow used in investing

activities -47 1

Cash flow used in financing

activities -225 54

Net change in cash & cash

equivalents -195 120

23

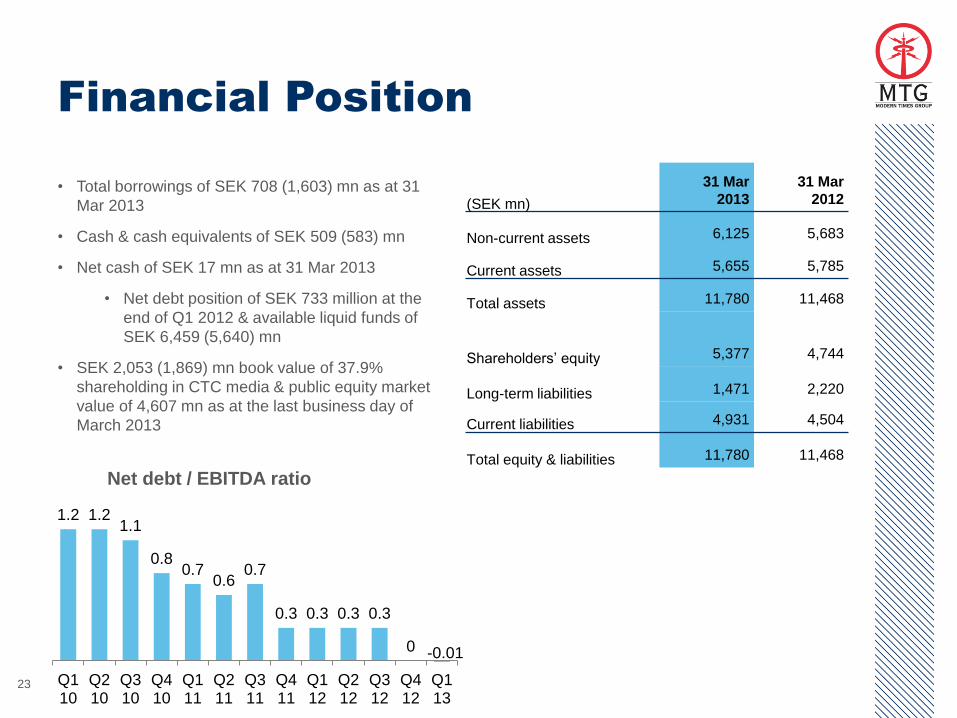

Financial Position

• Total borrowings of SEK 708 (1,603) mn as at 31

Mar 2013

• Cash & cash equivalents of SEK 509 (583) mn

• Net cash of SEK 17 mn as at 31 Mar 2013

• Net debt position of SEK 733 million at the

end of Q1 2012 & available liquid funds of

SEK 6,459 (5,640) mn

• SEK 2,053 (1,869) mn book value of 37.9%

shareholding in CTC media & public equity market

value of 4,607 mn as at the last business day of

March 2013

(SEK mn)

31 Mar

2013

31 Mar

2012

Non-current assets 6,125 5,683

Current assets 5,655 5,785

Total assets 11,780 11,468

Shareholders’ equity 5,377 4,744

Long-term liabilities 1,471 2,220

Current liabilities 4,931 4,504

Total equity & liabilities 11,780 11,468

Net debt / EBITDA ratio

1.2 1.2 1.1

0.8 0.7

0.6 0.7

0.3 0.3 0.3 0.3

0 -0.01

Q110

Q210

Q310

Q410

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

24

First Quarter 2013

Financial Results

25

Summary

• Strong sales performance in free-TV Emerging Markets driven by

sales cooperations, underlying growth & new channel

• Largest free-TV media house on a quarterly basis in the Czech

Republic for the first time

• Continued investments in pay-TV operations & outlook reiterated

• Audience shares stabilising across the board & improvements in

March

• Taking advertising & audience shares in Denmark

• Viaplay subscriber base is growing & record viewing levels for key

sports events during Q1

• Net cash position provides flexibility for both organic and M&A driven

growth

26

For further information, please visit www.mtg.se or contact:

MTG Investor Relations

Tel: +46 (0) 73 699 2714

Email: [email protected]