mro forecast and market trends - iata · pdf file0 mro forecast and market trends presented...

TRANSCRIPT

0

MRO Forecast and Market Trends

Presented by:

Martin HarrisonManaging Director ICF International

11

Today’s Agenda

Follow the Money

MRO Forecast

Impact of New Technology Aircraft

Trends to Watch:

The Mod Squad

March of the Middle East Titans

Amazon the Disrupter

Training 2.0: Virtual Reality

22

Follow the Money

33

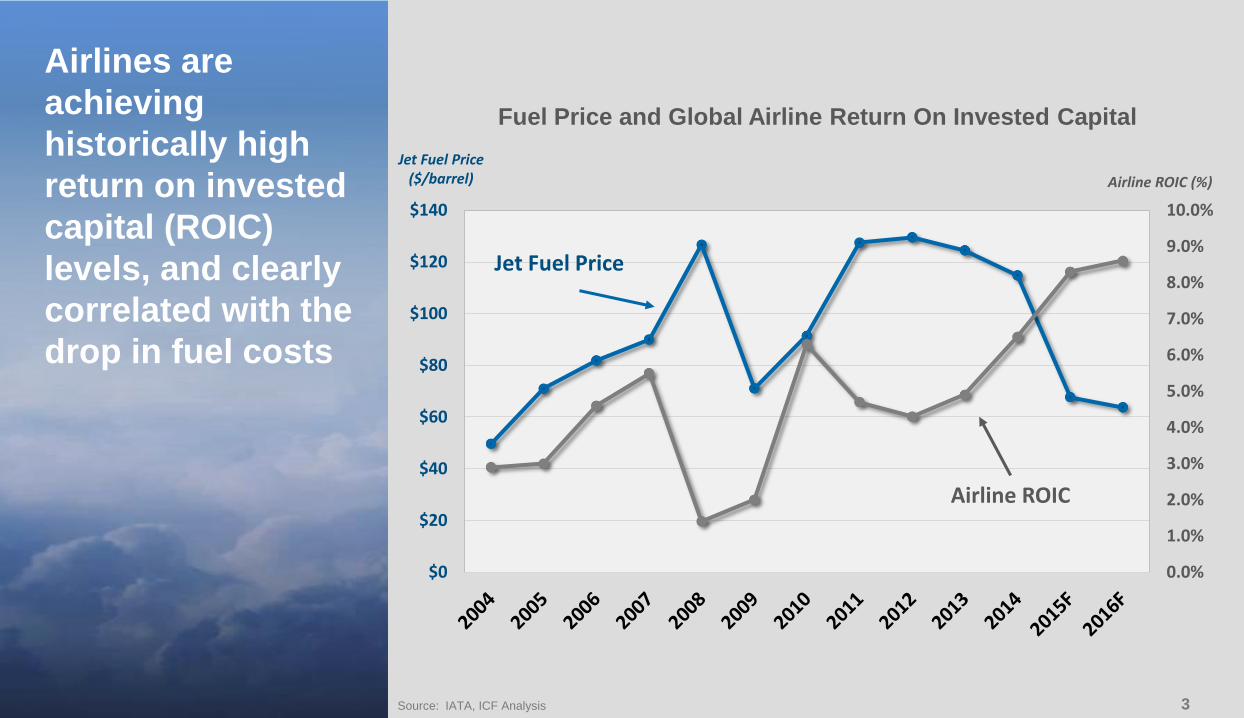

Airlines are

achieving

historically high

return on invested

capital (ROIC)

levels, and clearly

correlated with the

drop in fuel costs

Source: IATA, ICF Analysis

Fuel Price and Global Airline Return On Invested Capital

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

$0

$20

$40

$60

$80

$100

$120

$140

Jet Fuel Price ($/barrel) Airline ROIC (%)

Airline ROIC

Jet Fuel Price

44

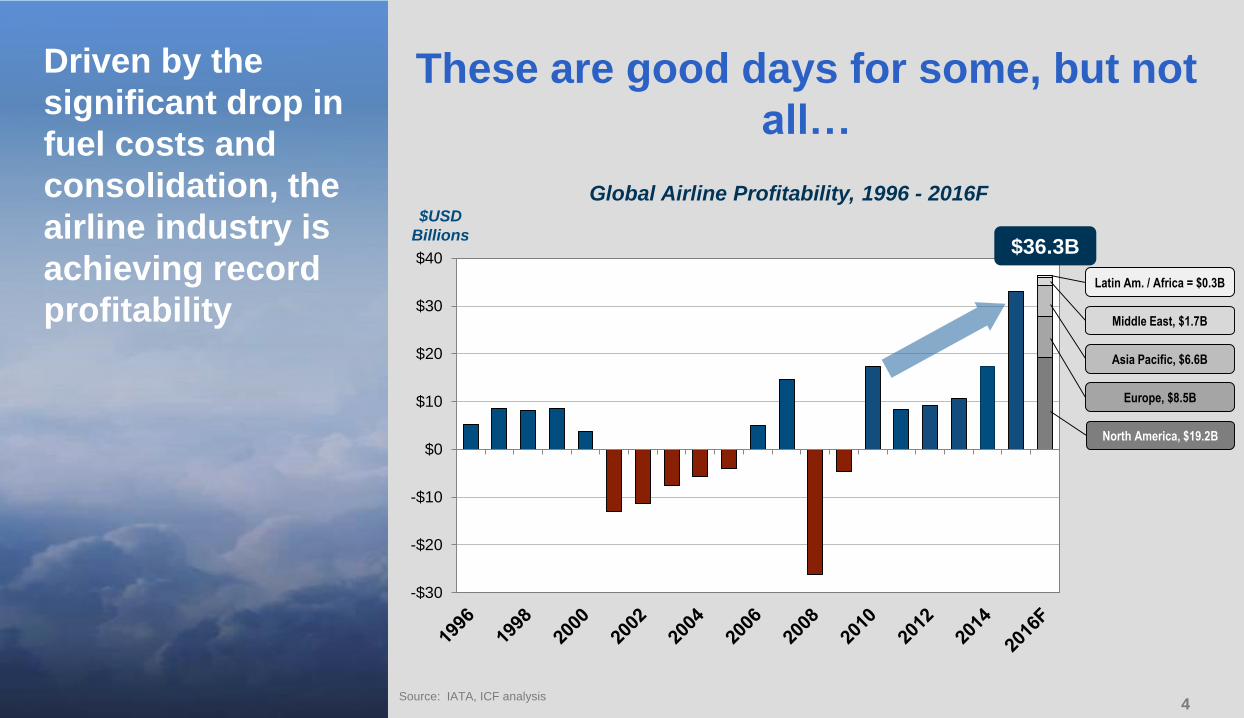

Driven by the

significant drop in

fuel costs and

consolidation, the

airline industry is

achieving record

profitability

Source: IATA, ICF analysis

These are good days for some, but not

all…

Global Airline Profitability, 1996 - 2016F

-$30

-$20

-$10

$0

$10

$20

$30

$40

$USD

Billions$36.3B

Asia Pacific, $6.6B

North America, $19.2B

Europe, $8.5B

Middle East, $1.7B

Latin Am. / Africa = $0.3B

55

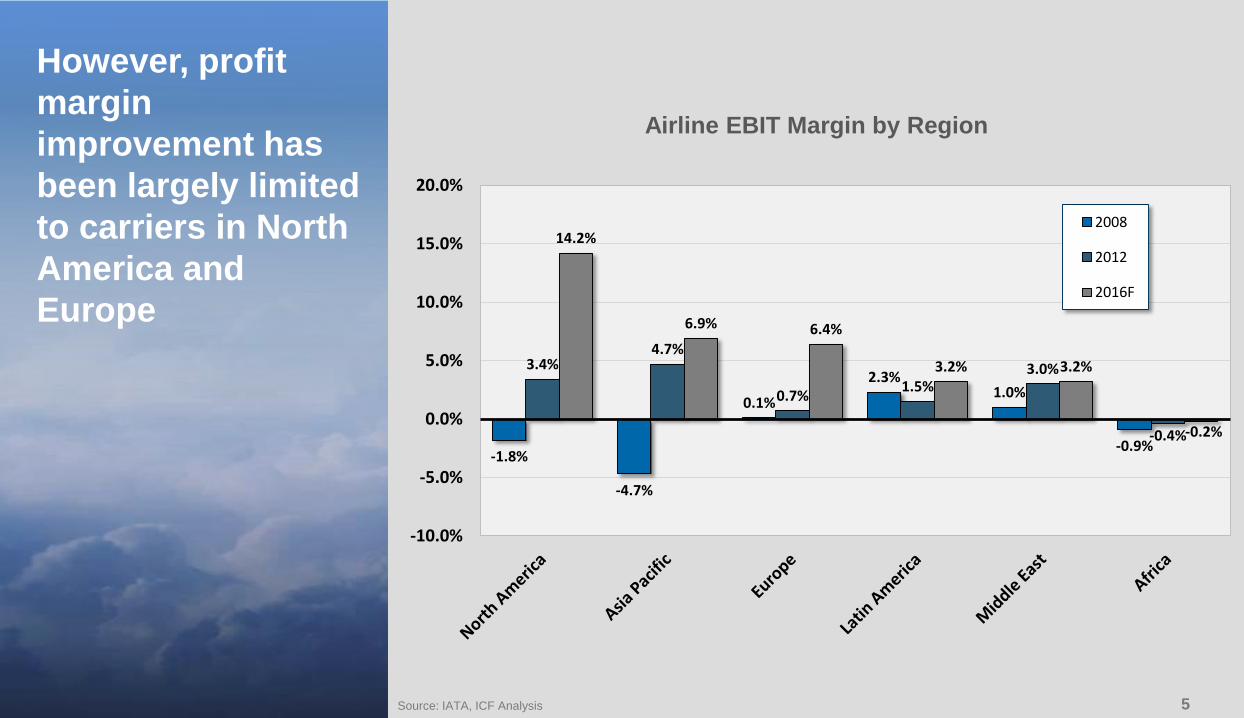

However, profit

margin

improvement has

been largely limited

to carriers in North

America and

Europe

Source: IATA, ICF Analysis

-1.8%

-4.7%

0.1%

2.3%1.0%

-0.9%

3.4%4.7%

0.7%1.5%

3.0%

-0.4%

14.2%

6.9% 6.4%

3.2% 3.2%

-0.2%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

2008

2012

2016F

Airline EBIT Margin by Region

66

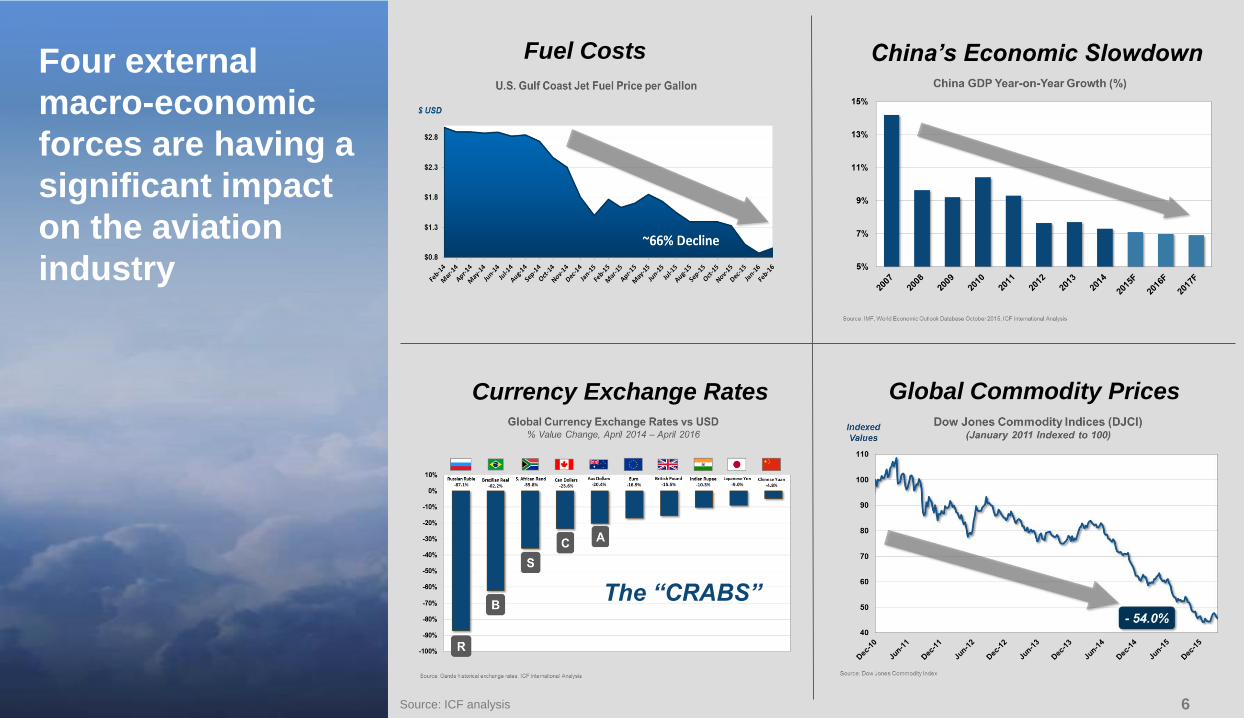

Four external

macro-economic

forces are having a

significant impact

on the aviation

industry

The “CRABS”

Currency Exchange Rates Global Commodity Prices

China’s Economic SlowdownFuel Costs

Source: ICF analysis

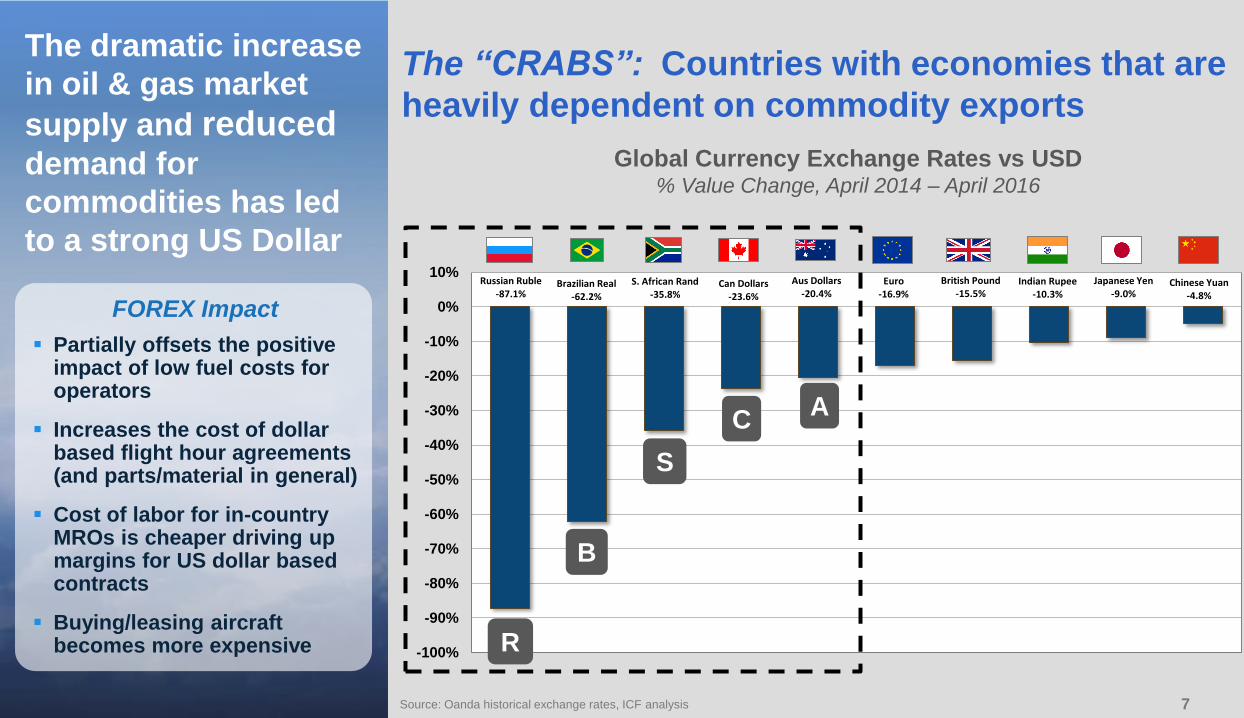

77

The dramatic increase

in oil & gas market

supply and reduceddemand for

commodities has led

to a strong US Dollar

Partially offsets the positive impact of low fuel costs for operators

Increases the cost of dollar based flight hour agreements (and parts/material in general)

Cost of labor for in-country MROs is cheaper driving up margins for US dollar based contracts

Buying/leasing aircraft becomes more expensive

FOREX Impact

Source: Oanda historical exchange rates, ICF analysis

The “CRABS”: Countries with economies that are

heavily dependent on commodity exports

Global Currency Exchange Rates vs USD% Value Change, April 2014 – April 2016

Russian Ruble-87.1%

Brazilian Real-62.2%

S. African Rand-35.8%

Can Dollars-23.6%

Aus Dollars-20.4%

Euro-16.9%

British Pound-15.5%

Indian Rupee-10.3%

Japanese Yen-9.0%

Chinese Yuan-4.8%

-100%

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

B

R

C

S

A

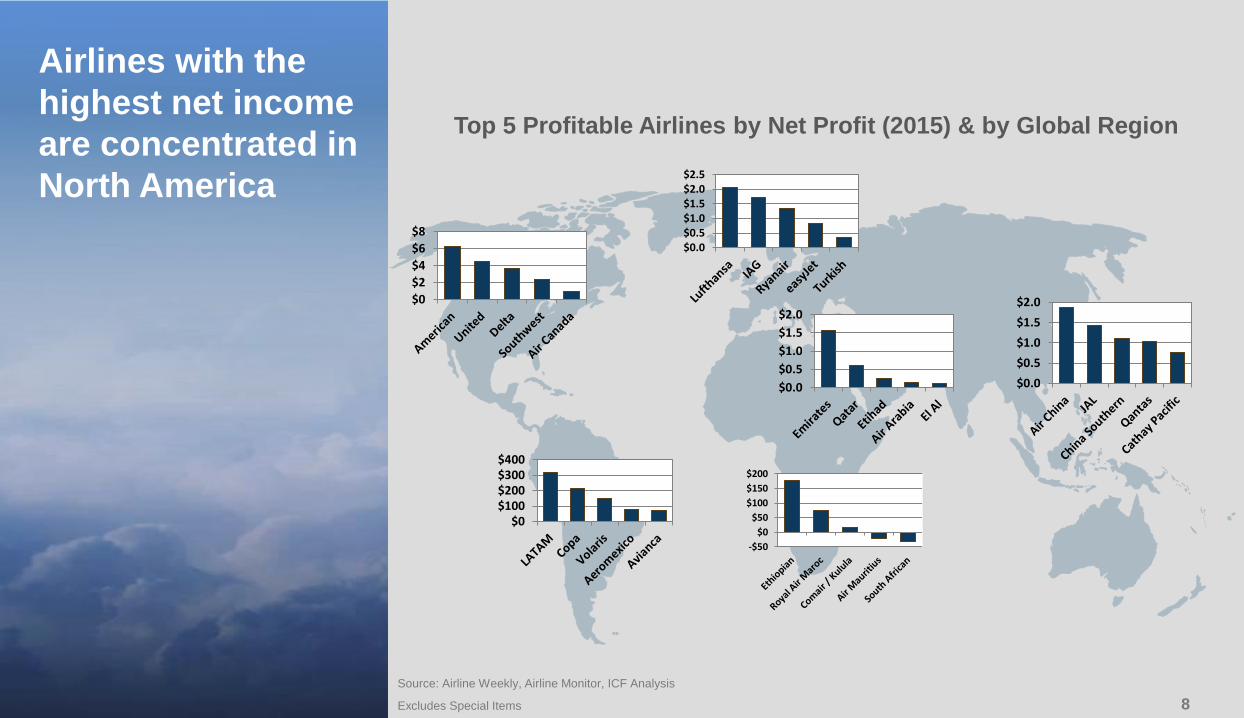

88

Airlines with the

highest net income

are concentrated in

North America

Source: Airline Weekly, Airline Monitor, ICF Analysis

Excludes Special Items

$0

$2

$4

$6

$8

$0$100$200$300$400

$0.0$0.5$1.0$1.5$2.0$2.5

$0.0

$0.5

$1.0

$1.5

$2.0

-$50

$0

$50

$100

$150

$200

$0.0

$0.5

$1.0

$1.5

$2.0

Tho

usa

nd

s

Top 5 Profitable Airlines by Net Profit (2015) & by Global Region

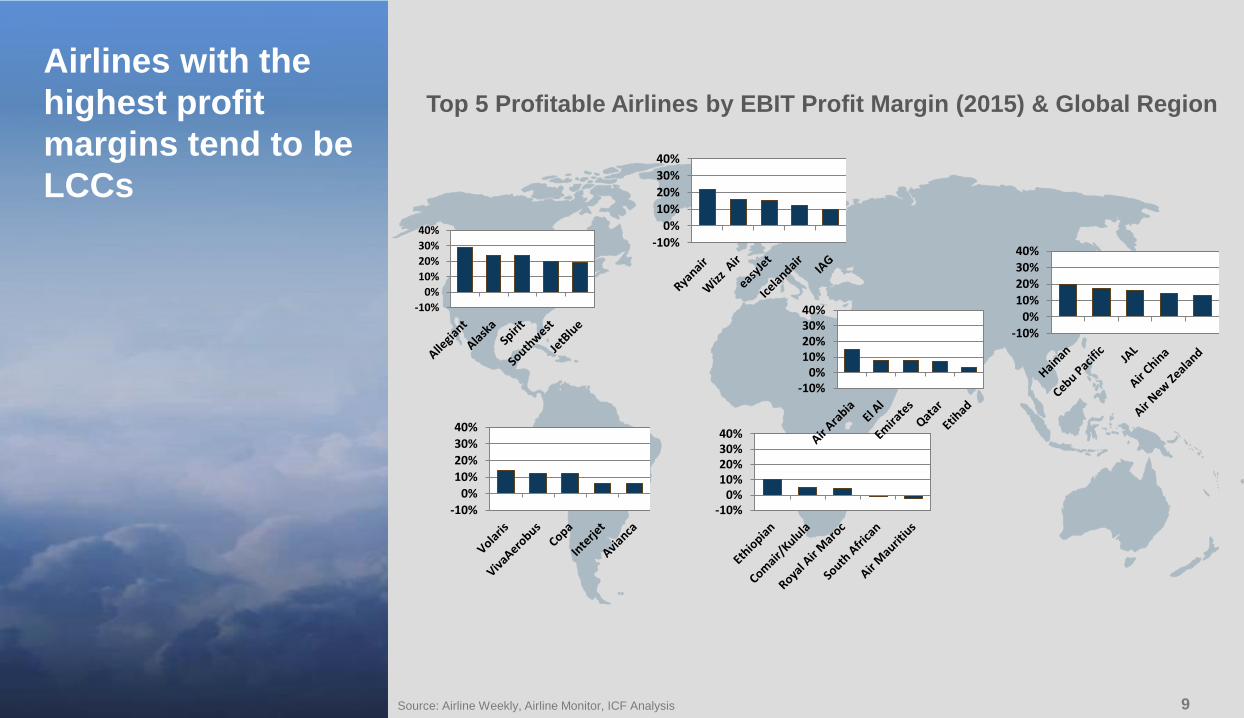

99

Airlines with the

highest profit

margins tend to be

LCCs

Source: Airline Weekly, Airline Monitor, ICF Analysis

-10%

0%

10%

20%

30%

40%

-10%0%

10%

20%

30%

40%

-10%0%

10%20%30%40%

-10%0%

10%20%30%40%

-10%

0%

10%

20%

30%

40%

-10%0%

10%20%30%40%

Top 5 Profitable Airlines by EBIT Profit Margin (2015) & Global Region

1010

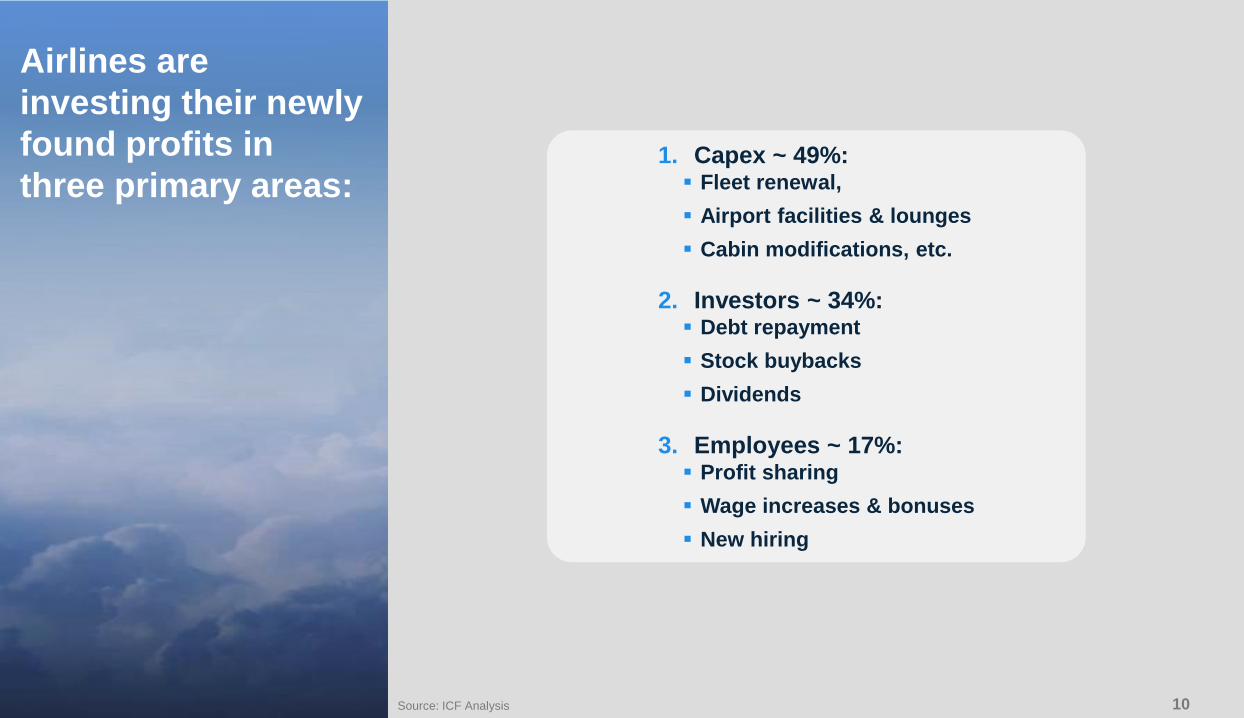

Airlines are

investing their newly

found profits in

three primary areas:

Source: ICF Analysis

1. Capex ~ 49%: Fleet renewal,

Airport facilities & lounges

Cabin modifications, etc.

2. Investors ~ 34%: Debt repayment

Stock buybacks

Dividends

3. Employees ~ 17%: Profit sharing

Wage increases & bonuses

New hiring

1111

MRO Forecast

1212

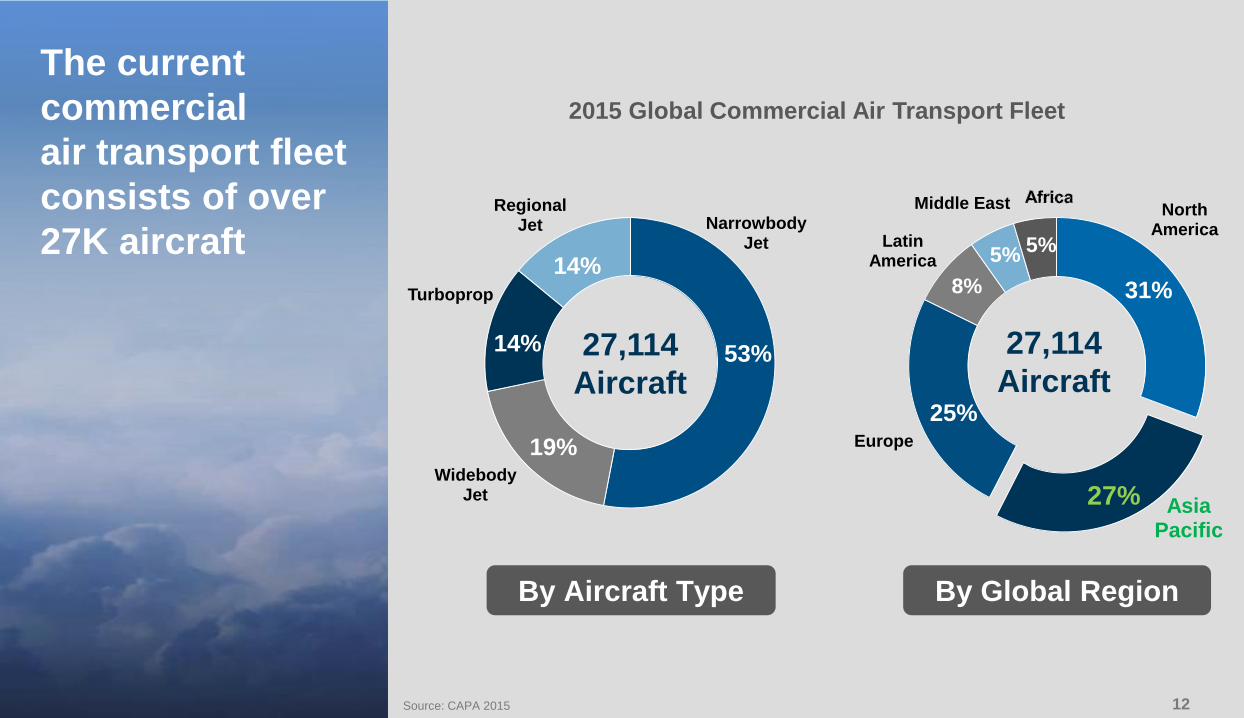

The current

commercial

air transport fleet

consists of over

27K aircraft

Source: CAPA 2015

NarrowbodyJet

WidebodyJet

Turboprop

Regional Jet

27,114

Aircraft

14%

53%14%

19%

By Aircraft Type By Global Region

North America

Asia Pacific

Europe

Latin America

Middle East

31%

27%

25%

8%

5% 5%

27,114

Aircraft

2015 Global Commercial Air Transport Fleet

1313

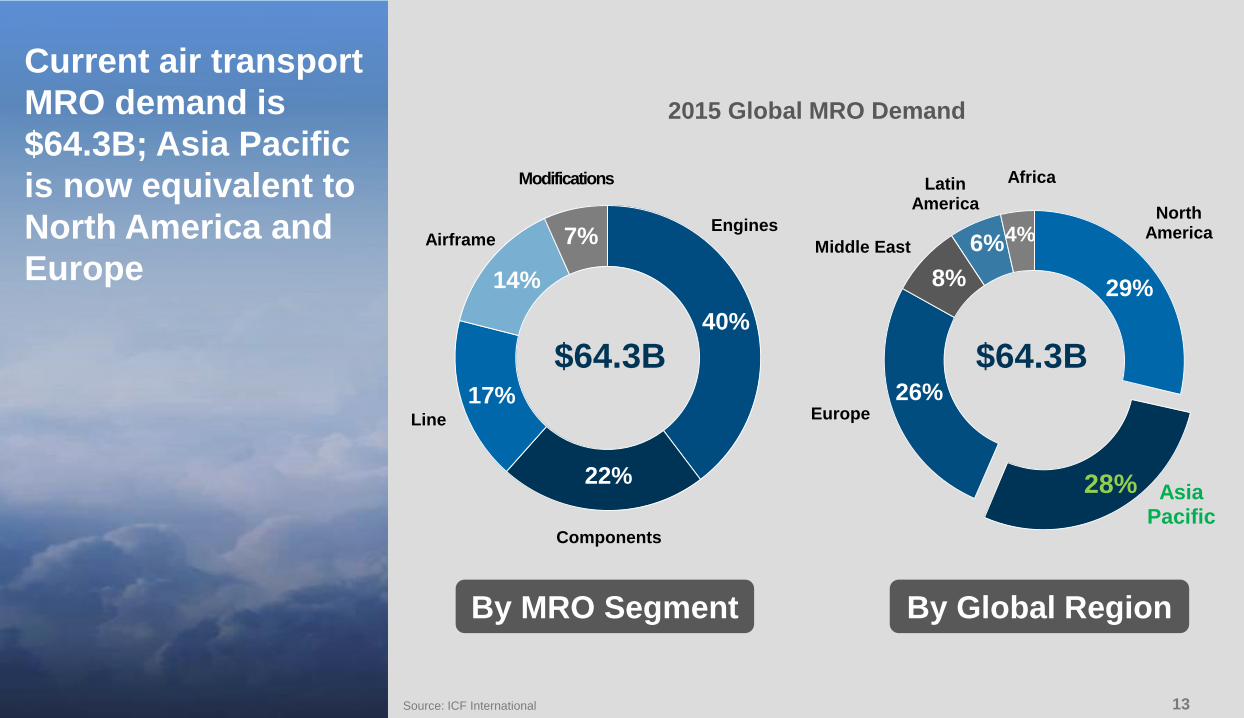

Current air transport

MRO demand is

$64.3B; Asia Pacific

is now equivalent to

North America and

Europe

Source: ICF International

Engines

Components

Line

Airframe

Modifications

14%

17%

22%

40%

7%North

America

Asia Pacific

Europe

Middle East

Latin America

Africa

29%

28%

26%

8%

6%4%

$64.3B$64.3B

By MRO Segment By Global Region

2015 Global MRO Demand

1414

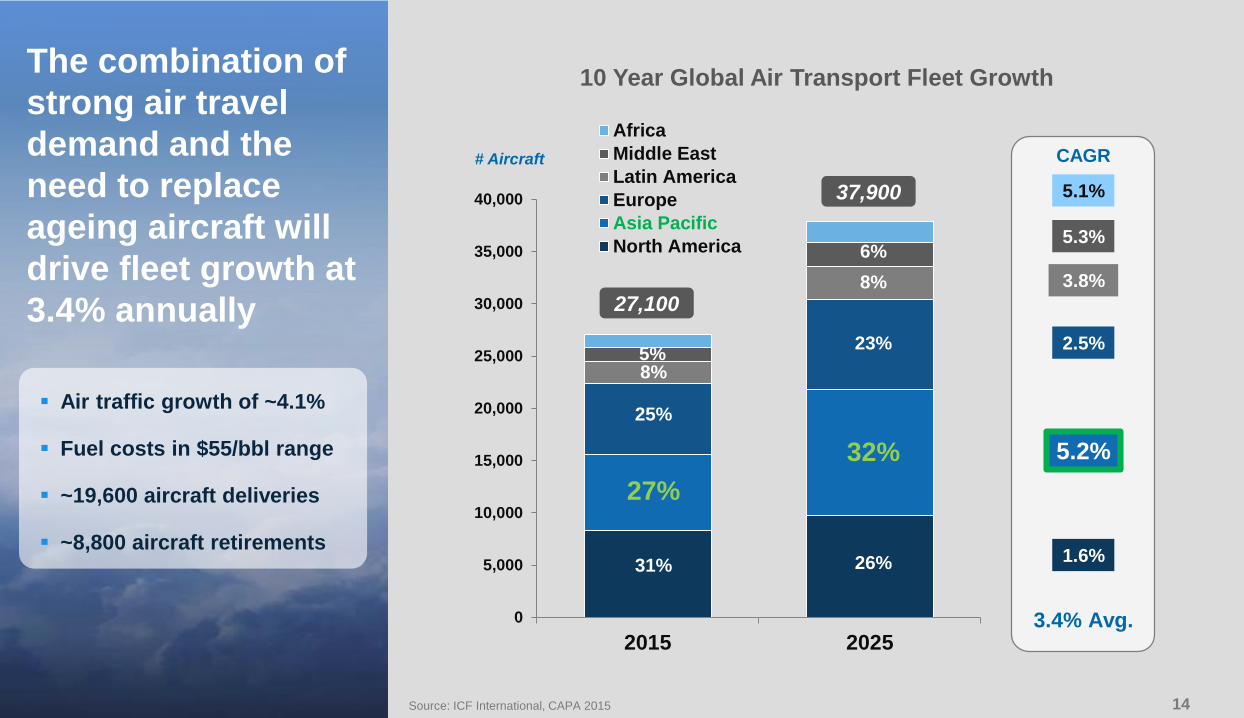

The combination of

strong air travel

demand and the

need to replace

ageing aircraft will

drive fleet growth at

3.4% annually

Source: ICF International, CAPA 2015

Air traffic growth of ~4.1%

Fuel costs in $55/bbl range

~19,600 aircraft deliveries

~8,800 aircraft retirements

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2015 2025

Africa

Middle East

Latin America

Europe

Asia Pacific

North America

27,100

31% 26%

37,900

27%

25%

8%

32%

23%

8%

# Aircraft

3.8%

2.5%

1.6%

5.2%

5.3%

5.1%

CAGR

3.4% Avg.

5%

6%

10 Year Global Air Transport Fleet Growth

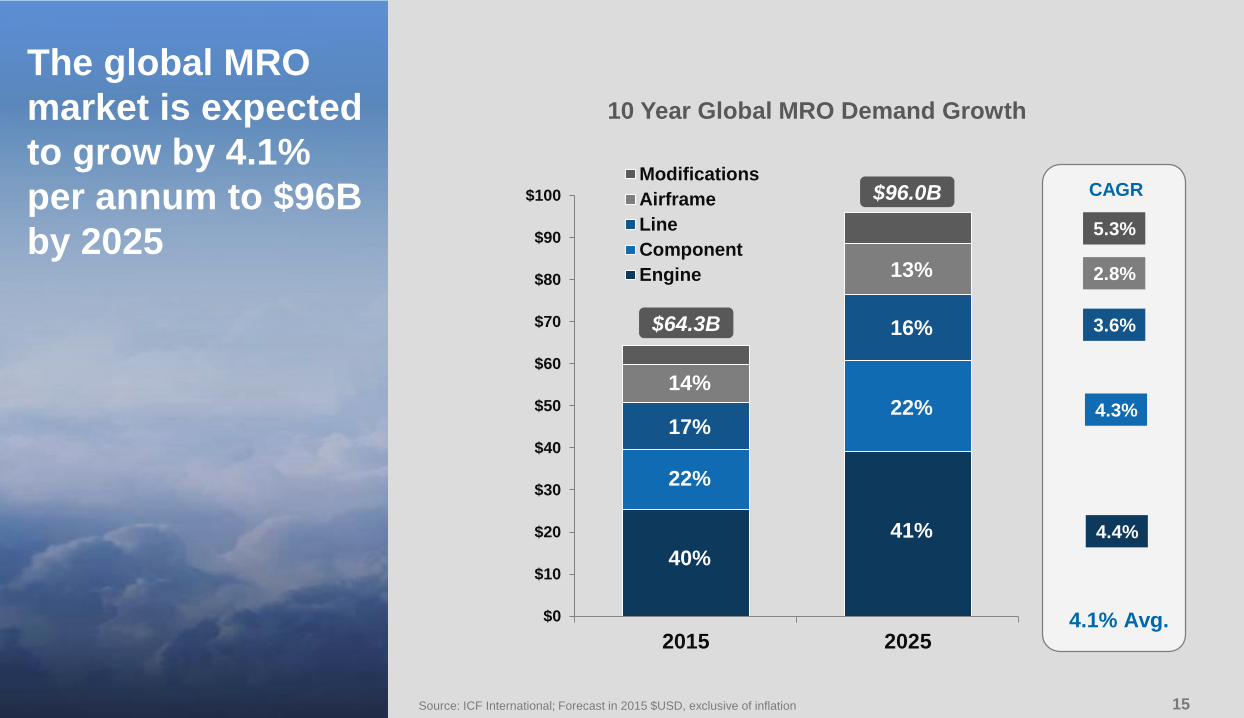

1515

The global MRO

market is expected

to grow by 4.1%

per annum to $96B

by 2025

Source: ICF International; Forecast in 2015 $USD, exclusive of inflation

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

2015 2025

Modifications

Airframe

Line

Component

Engine

40%

22%

14%

17%

$64.3B

$96.0B

2.8%

3.6%

4.3%

4.4%

CAGR

4.1% Avg.

5.3%

41%

22%

16%

13%

10 Year Global MRO Demand Growth

1616

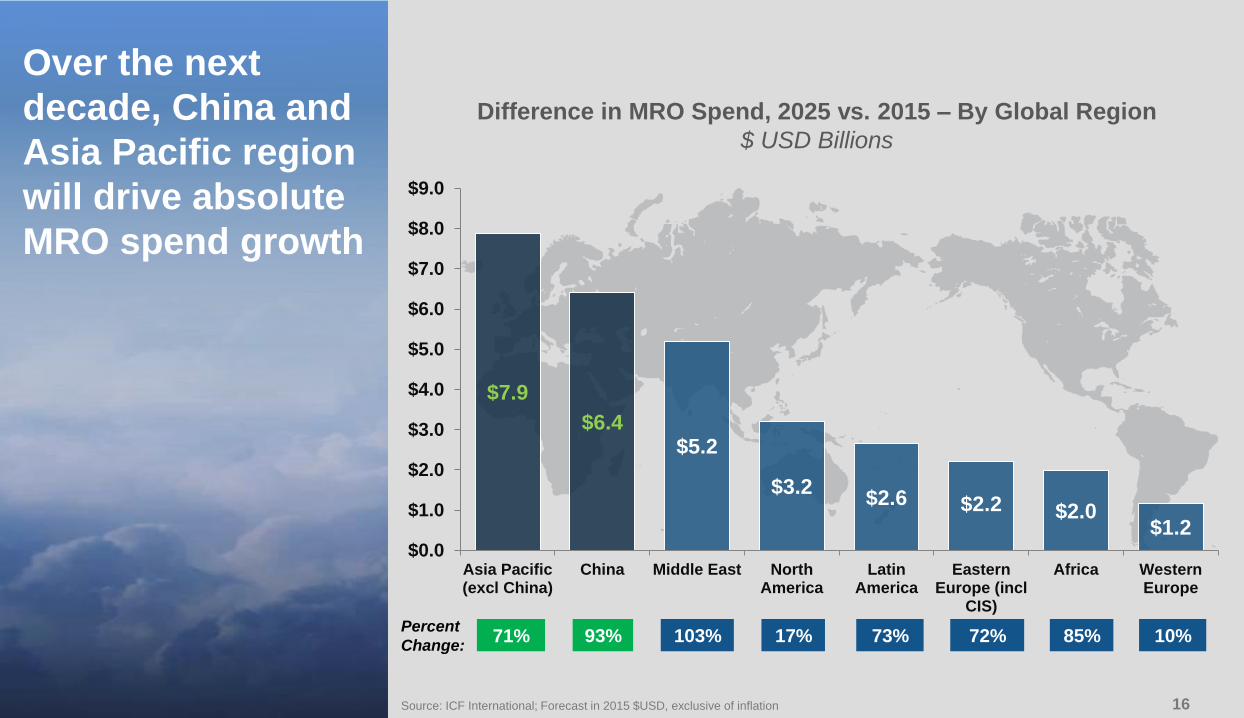

Over the next

decade, China and

Asia Pacific region

will drive absolute

MRO spend growth

Source: ICF International; Forecast in 2015 $USD, exclusive of inflation

Difference in MRO Spend, 2025 vs. 2015 – By Global Region

$ USD Billions

$7.9

$6.4$5.2

$3.2$2.6 $2.2 $2.0

$1.2$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

$9.0

Asia Pacific(excl China)

China Middle East NorthAmerica

LatinAmerica

EasternEurope (incl

CIS)

Africa WesternEurope

71% 93% 103% 17% 73% 72% 85% 10%Percent

Change:

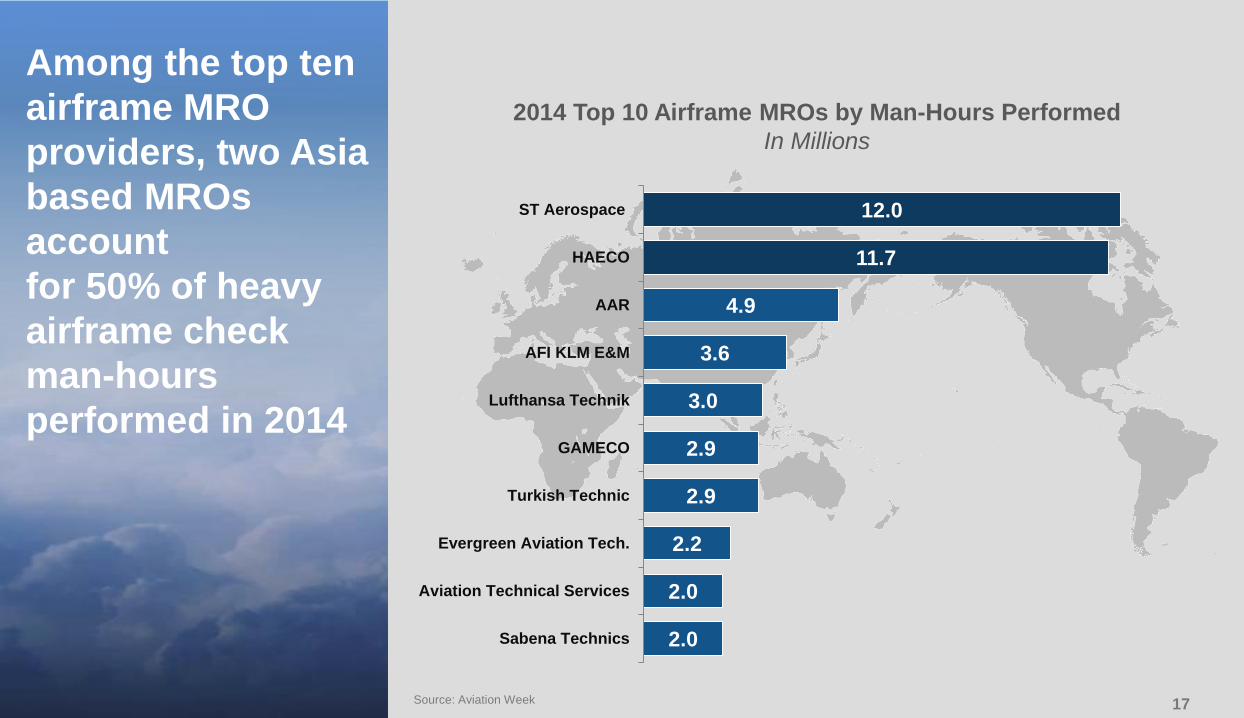

1717

2014 Top 10 Airframe MROs by Man-Hours Performed

In Millions

Among the top ten

airframe MRO

providers, two Asia

based MROs

account

for 50% of heavy

airframe check

man-hours

performed in 2014

Source: Aviation Week

12.0

11.7

4.9

3.6

3.0

2.9

2.9

2.2

2.0

2.0

ST Aerospace

HAECO

AAR

AFI KLM E&M

Lufthansa Technik

GAMECO

Turkish Technic

Evergreen Aviation Tech.

Aviation Technical Services

Sabena Technics

1818

Impact of

New Technology Aircraft

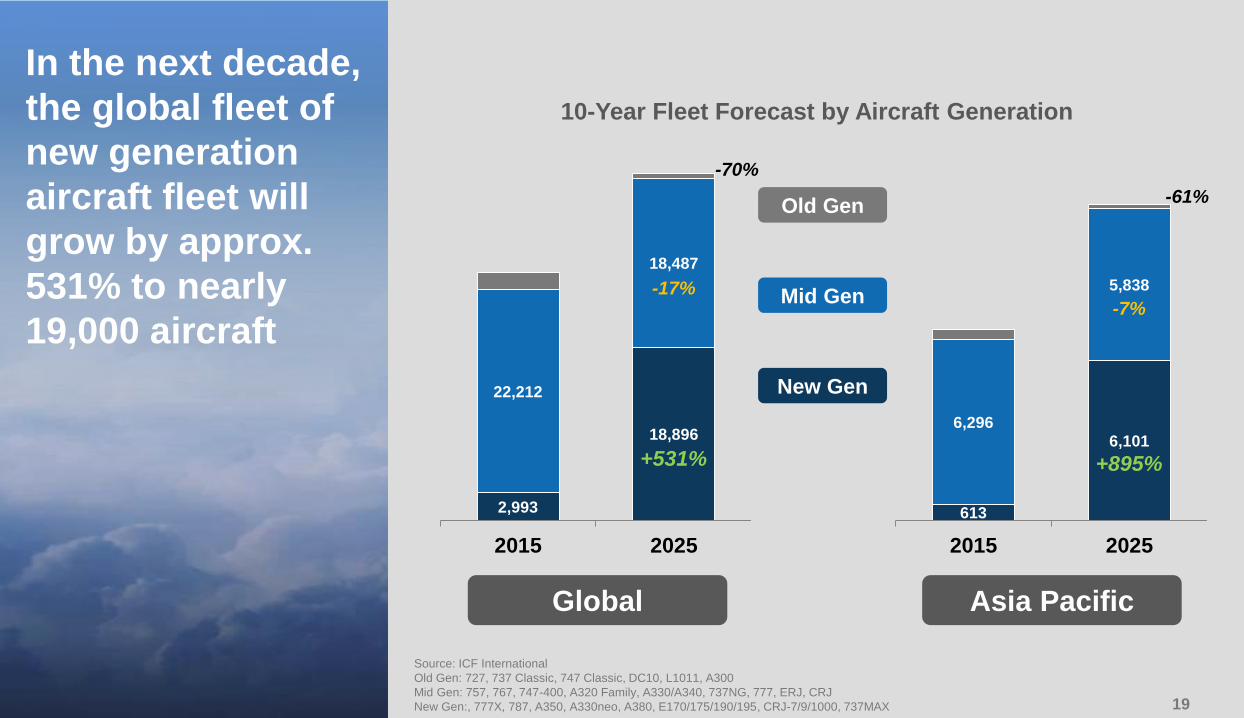

1919

In the next decade,

the global fleet of

new generation

aircraft fleet will

grow by approx.

531% to nearly

19,000 aircraft

10-Year Fleet Forecast by Aircraft Generation

2,993

18,896

22,212

18,487

2015 2025

Global

New Gen

Mid Gen

Old Gen

Source: ICF International

Old Gen: 727, 737 Classic, 747 Classic, DC10, L1011, A300

Mid Gen: 757, 767, 747-400, A320 Family, A330/A340, 737NG, 777, ERJ, CRJ

New Gen:, 777X, 787, A350, A330neo, A380, E170/175/190/195, CRJ-7/9/1000, 737MAX

Asia Pacific

+531%

-70%

-17%

613

6,1016,296

5,838

2015 2025

+895%

-7%

-61%

2020

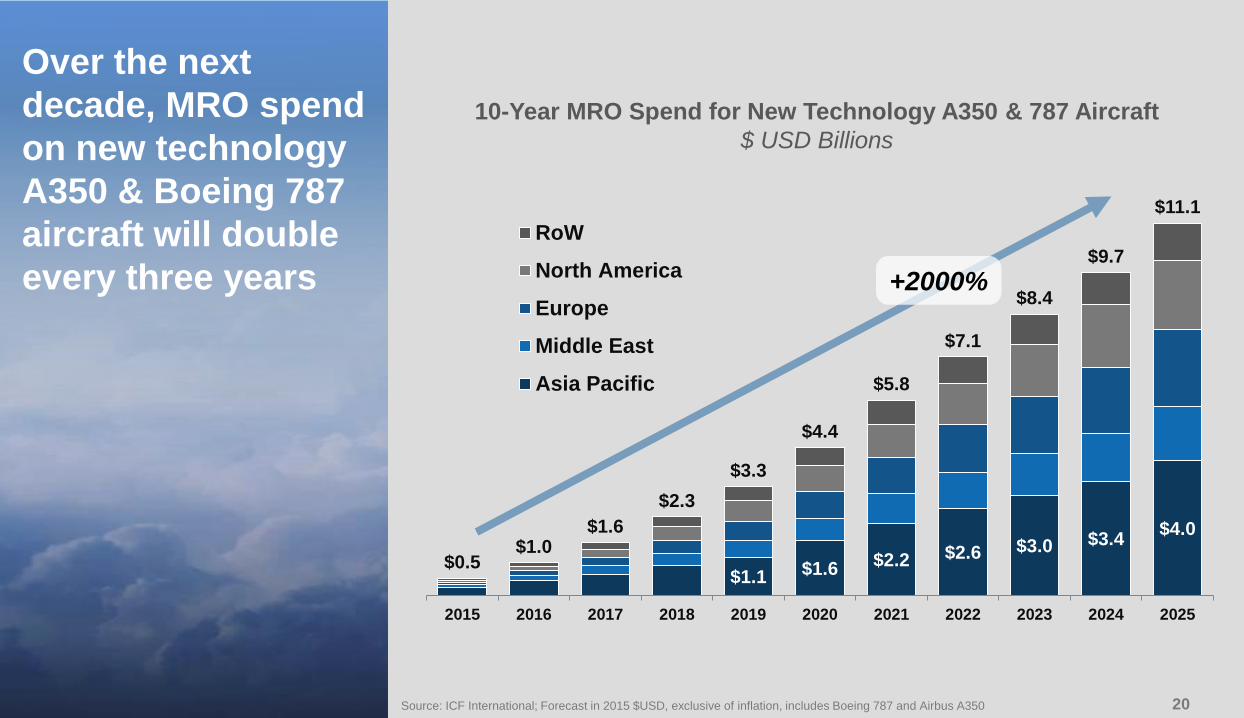

Over the next

decade, MRO spend

on new technology

A350 & Boeing 787

aircraft will double

every three years

Source: ICF International; Forecast in 2015 $USD, exclusive of inflation, includes Boeing 787 and Airbus A350

10-Year MRO Spend for New Technology A350 & 787 Aircraft

$ USD Billions

$1.1 $1.6 $2.2 $2.6 $3.0 $3.4$4.0

$0.5$1.0

$1.6

$2.3

$3.3

$4.4

$5.8

$7.1

$8.4

$9.7

$11.1

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

RoW

North America

Europe

Middle East

Asia Pacific

+2000%

2121

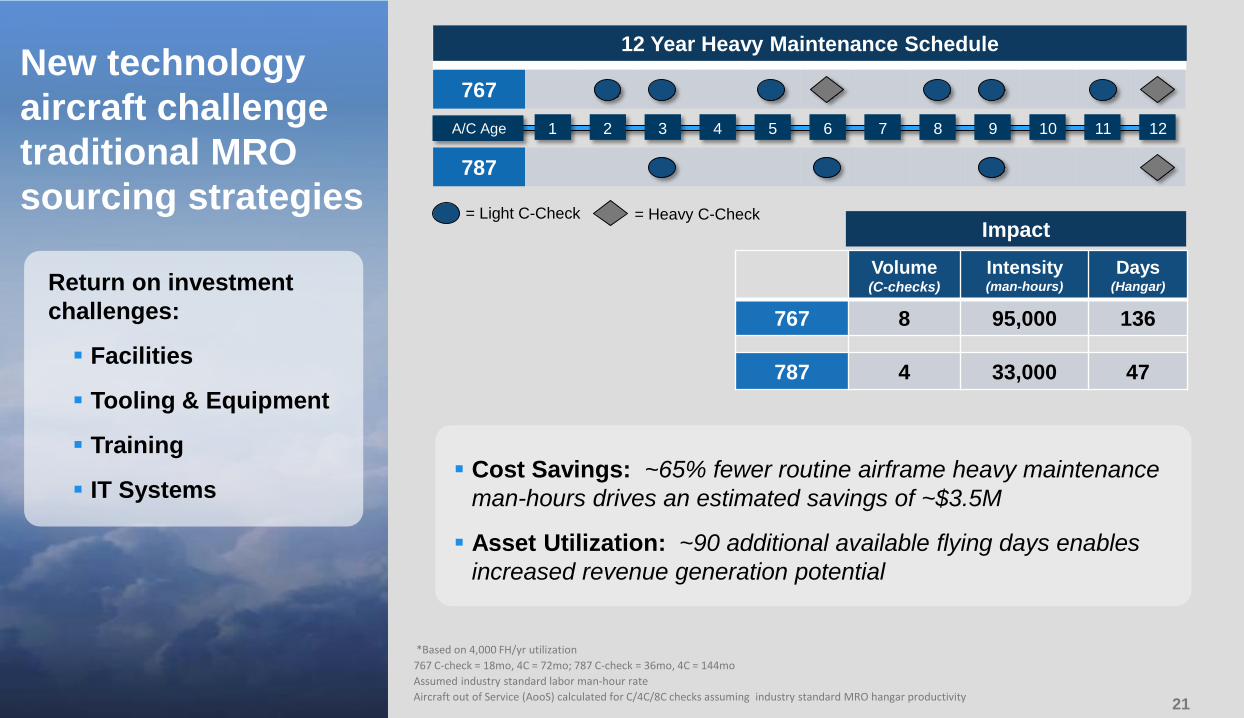

New technology

aircraft challenge

traditional MRO

sourcing strategies= Heavy C-Check= Light C-Check

767

A/C Age 1 2 3 4 5 6 7 8 9 10 11 12

787

Volume(C-checks)

Intensity(man-hours)

Days(Hangar)

767 8 95,000 136

787 4 33,000 47

Impact

Cost Savings: ~65% fewer routine airframe heavy maintenance

man-hours drives an estimated savings of ~$3.5M

Asset Utilization: ~90 additional available flying days enables

increased revenue generation potential

12 Year Heavy Maintenance Schedule

*Based on 4,000 FH/yr utilization

767 C-check = 18mo, 4C = 72mo; 787 C-check = 36mo, 4C = 144mo

Assumed industry standard labor man-hour rate

Aircraft out of Service (AooS) calculated for C/4C/8C checks assuming industry standard MRO hangar productivity

Return on investment

challenges:

Facilities

Tooling & Equipment

Training

IT Systems

2222

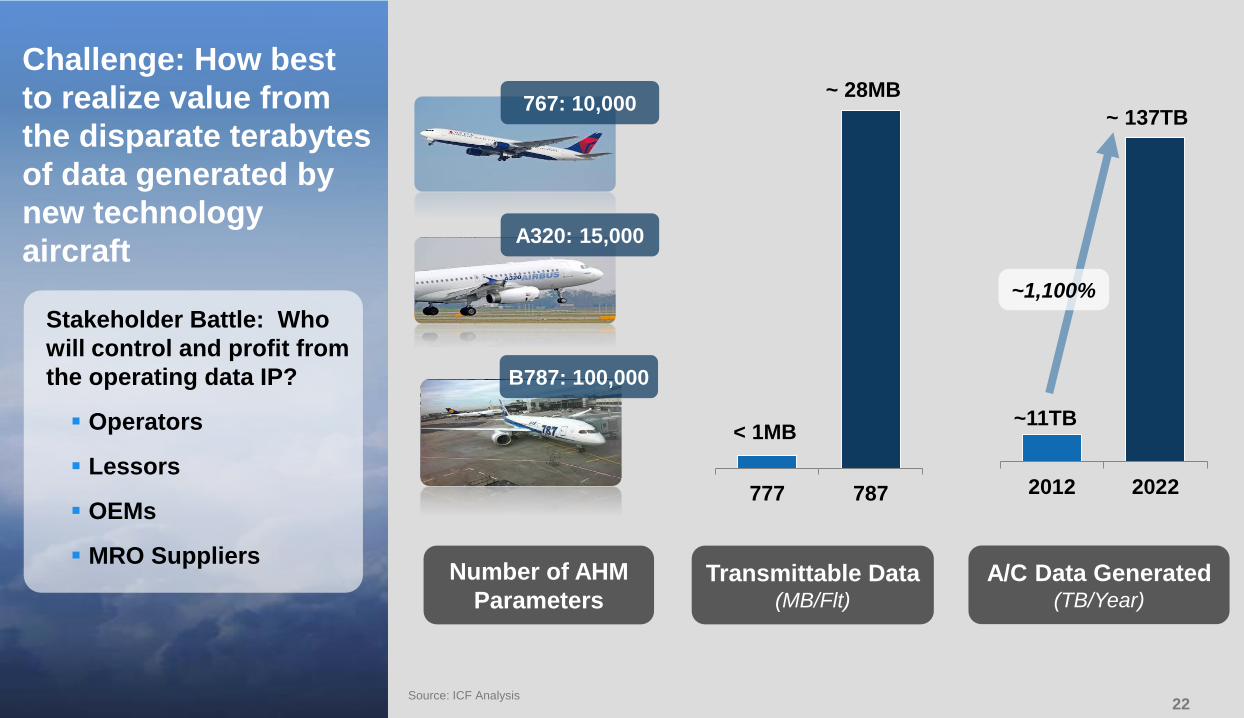

Challenge: How best

to realize value from

the disparate terabytes

of data generated by

new technology

aircraft

Source: ICF Analysis

Number of AHM

Parameters

A320: 15,000

B787: 100,000

2012 2022

~ 137TB

~11TB

777 787

~ 28MB

< 1MB

Stakeholder Battle: Who

will control and profit from

the operating data IP?

Operators

Lessors

OEMs

MRO SuppliersTransmittable Data

(MB/Flt)

A/C Data Generated(TB/Year)

767: 10,000

~1,100%

2323

Trends to Watch…

2424

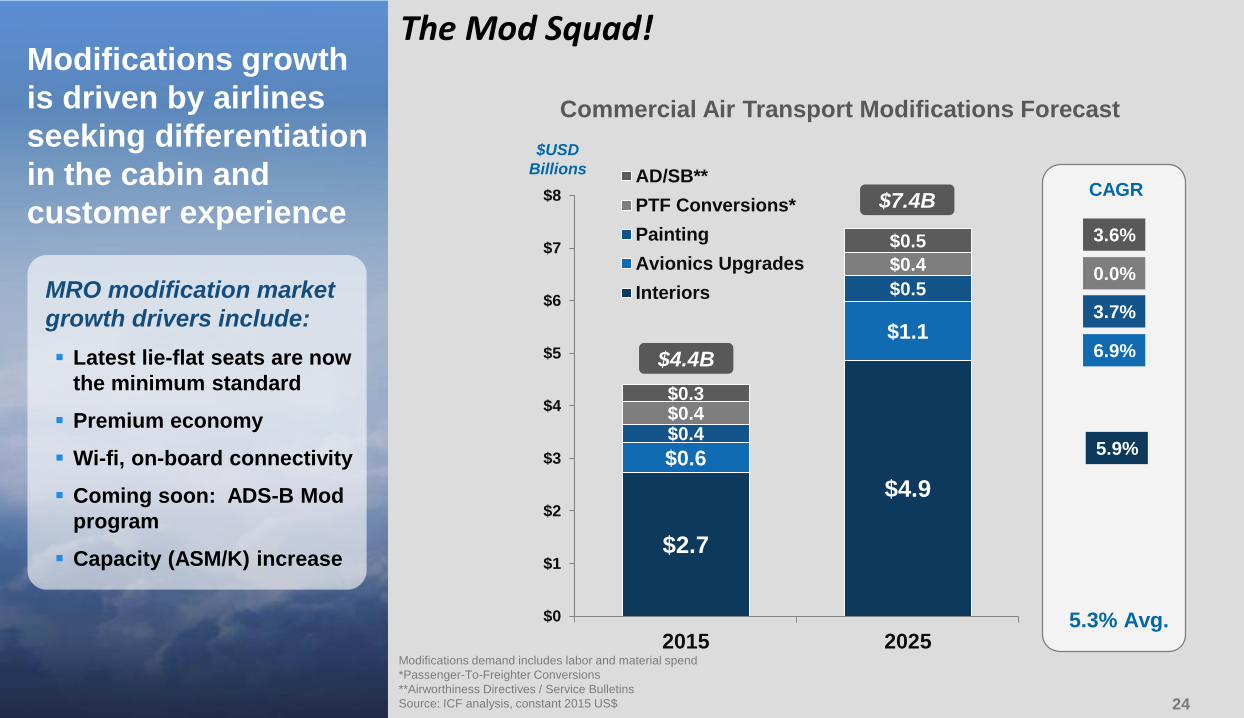

Modifications growth

is driven by airlines

seeking differentiation

in the cabin and

customer experience

Modifications demand includes labor and material spend

*Passenger-To-Freighter Conversions

**Airworthiness Directives / Service Bulletins

Source: ICF analysis, constant 2015 US$

MRO modification market

growth drivers include:

Latest lie-flat seats are now

the minimum standard

Premium economy

Wi-fi, on-board connectivity

Coming soon: ADS-B Mod

program

Capacity (ASM/K) increase

Commercial Air Transport Modifications Forecast

$2.7

$4.9

$0.6

$1.1

$0.4

$0.5

$0.4

$0.4

$0.3

$0.5

$0

$1

$2

$3

$4

$5

$6

$7

$8

2015 2025

AD/SB**

PTF Conversions*

Painting

Avionics Upgrades

Interiors

$4.4B

$7.4B

0.0%

3.7%

6.9%

5.9%

CAGR

5.3% Avg.

3.6%

$USD

Billions

The Mod Squad!

2525

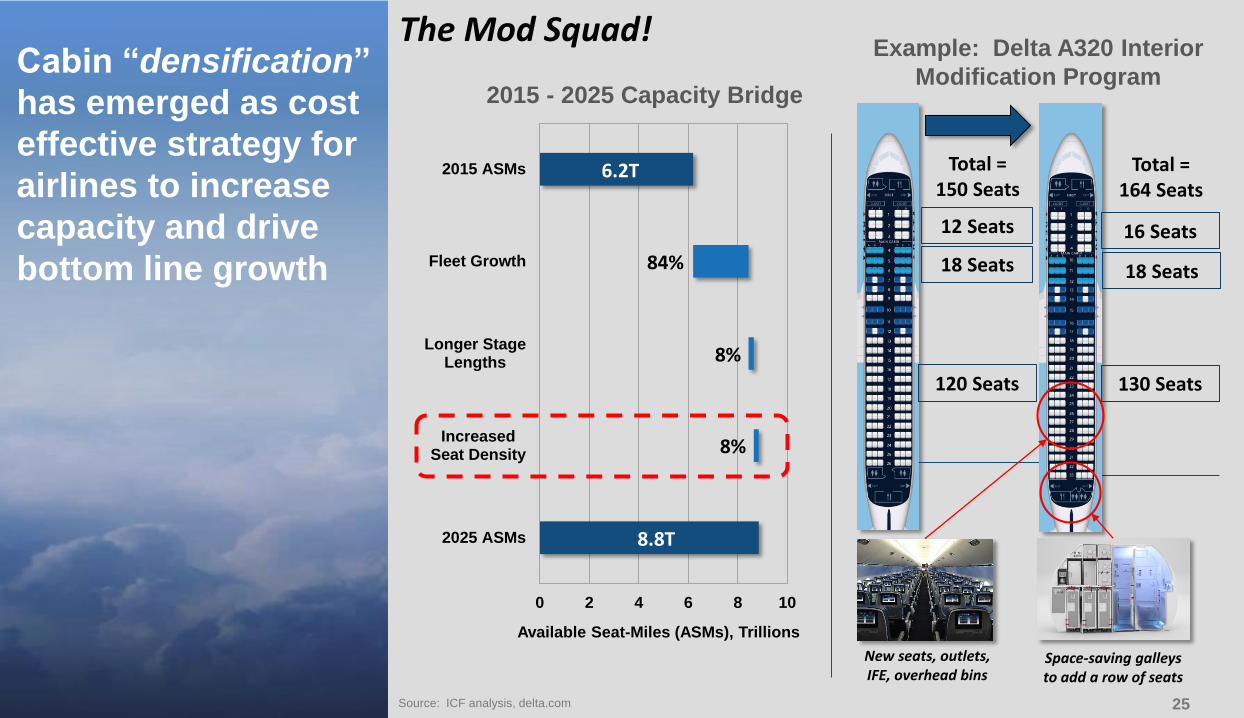

Cabin “densification”

has emerged as cost

effective strategy for

airlines to increase

capacity and drive

bottom line growth

2015 - 2025 Capacity Bridge

0 2 4 6 8 10

2025 ASMs

IncreasedSeat Density

Longer StageLengths

Fleet Growth

2015 ASMs

Available Seat-Miles (ASMs), Trillions

6.2T

8.8T

84%

8%

8%

12 Seats 16 Seats

130 Seats120 Seats

Total = 150 Seats

Total = 164 Seats

Example: Delta A320 Interior

Modification Program

New seats, outlets, IFE, overhead bins

Space-saving galleys to add a row of seats

Source: ICF analysis, delta.com

18 Seats18 Seats

The Mod Squad!

2626

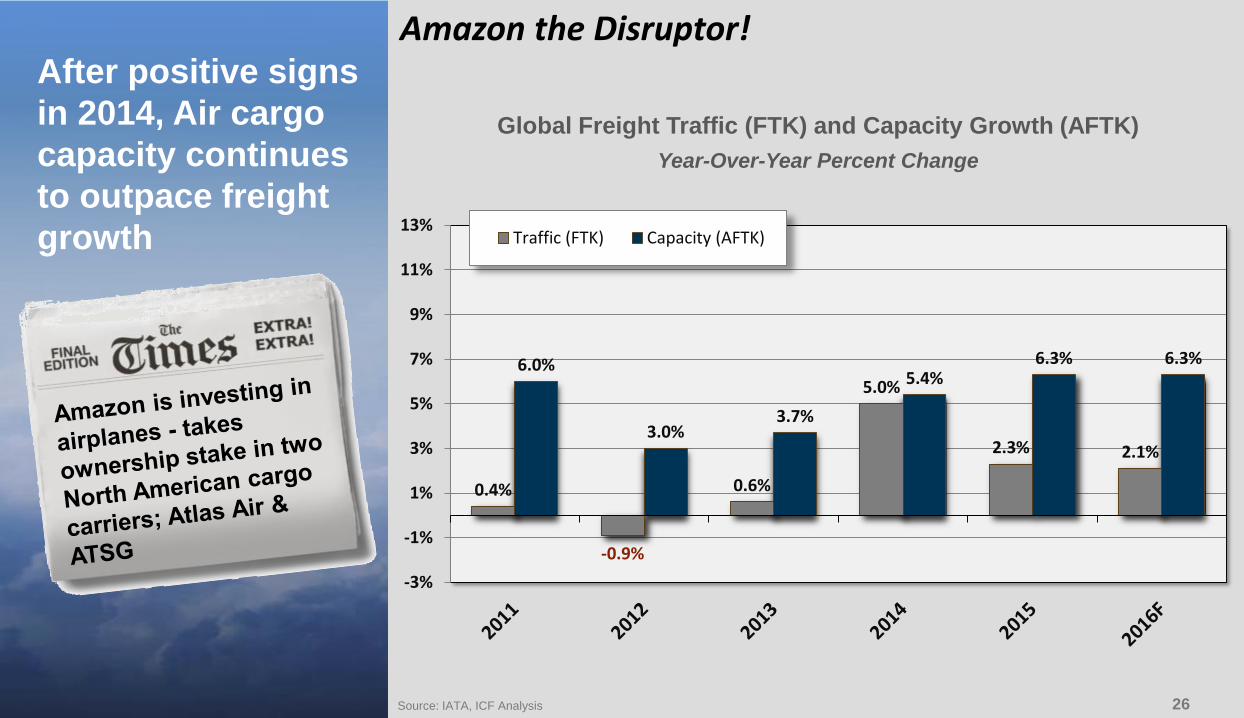

After positive signs

in 2014, Air cargo

capacity continues

to outpace freight

growth

Source: IATA, ICF Analysis

0.4%

-0.9%

0.6%

5.0%

2.3% 2.1%

6.0%

3.0%3.7%

5.4%6.3% 6.3%

-3%

-1%

1%

3%

5%

7%

9%

11%

13%Traffic (FTK) Capacity (AFTK)

Global Freight Traffic (FTK) and Capacity Growth (AFTK)

Year-Over-Year Percent Change

Amazon the Disruptor!

2727

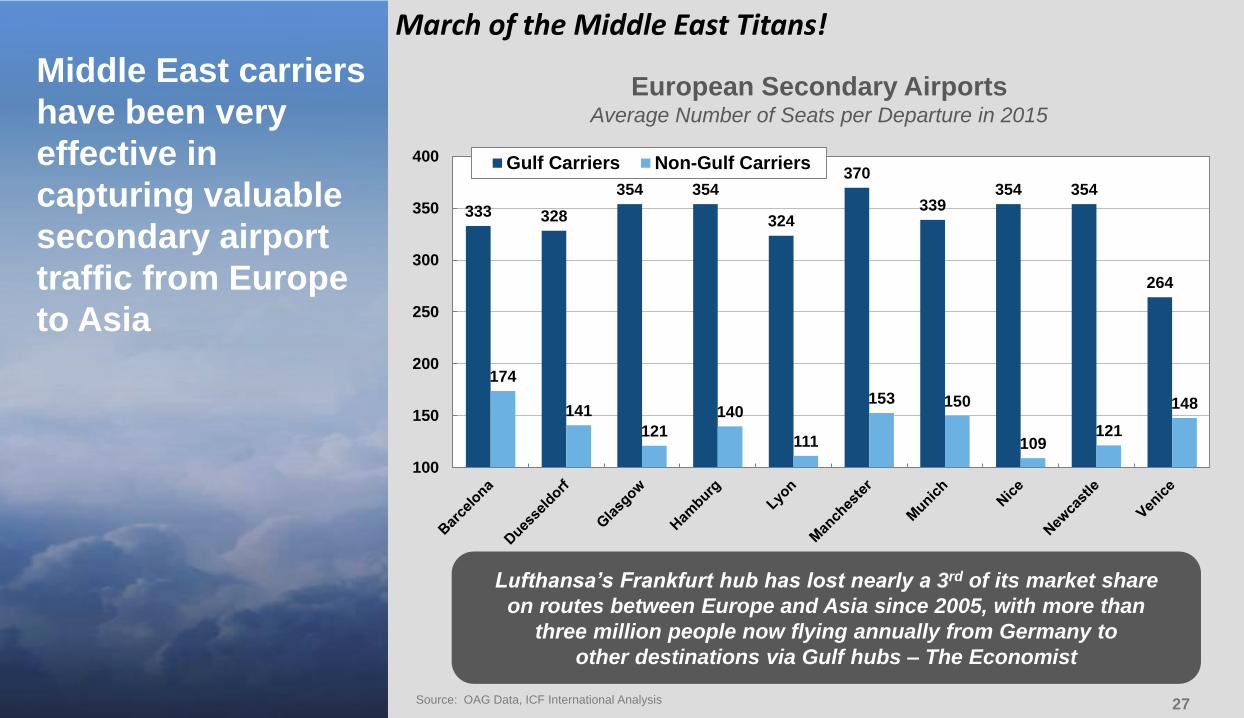

Middle East carriers

have been very

effective in

capturing valuable

secondary airport

traffic from Europe

to Asia

Source: OAG Data, ICF International Analysis

European Secondary AirportsAverage Number of Seats per Departure in 2015

Lufthansa’s Frankfurt hub has lost nearly a 3rd of its market share

on routes between Europe and Asia since 2005, with more than

three million people now flying annually from Germany to

other destinations via Gulf hubs – The Economist

333 328

354 354

324

370

339354 354

264

174

141

121

140

111

153 150

109121

148

100

150

200

250

300

350

400 Gulf Carriers Non-Gulf Carriers

March of the Middle East Titans!

2828

ICF believes that

virtual reality (VR)

technology will be

as disruptive to

MRO training as 3D-

printing is to parts

manufacturing

Training 2.0: Virtual Reality

29

For questions regarding this

presentation, please contact:

Martin Harrison / Jonathan BergerVice President Aerospace & MRO

[email protected] +1 404.819.7669

THANK YOU!

3030

Market Research & Analysis

Airline Maintenance Benchmarking

M&A Commercial Due Diligence

OEM Aftermarket Strategy

Aviation Asset Valuations & Appraisals

MRO Information Technology (IT) Advisory

Strategic Sourcing & Supply Chain Mgt.

LEAN Continuous Process Improvement

Military Aircraft Sustainment

ICF provides a full range of MRO

advisory services

3131

ICF is one of the

world’s largest and

most experienced

aviation and

aerospace

consulting firms

Airports • Airlines • Aerospace & MRO • Aircraft

53 years in business (founded 1963)

80+ professional staff

− Dedicated exclusively to aviation and aerospace

− Blend of consulting professionals and experienced aviation executives

Specialized, focused expertise and proprietary knowledge

Broad functional capabilities

More than 10,000 private sector and public sector assignments

Backed by parent ICF International (2015 revenue: 1.13 billion USD)

Global presence –– offices around the world

joined in 2011joined in 2007 joined in 2012 joined in 2014

New York • Boston • Ann Arbor • London • Singapore • Beijing • Hong Kong