mortgage bankers of florida secondary marketing … · private & confidential mortgage bankers...

TRANSCRIPT

Private amp Confidential

Mortgage Bankers of FloridaSecondary Marketing Conference 2018 Understanding the Secondary Market

Secondary Marketing Conference 2018Understanding the Secondary Market

Overviewbull

bull Loan Production

bull Warehousing QC Delivery

bull Secondary Marketing

bull Loan Administration (Servicing)

Source School of Mortgage Banking I - Introduction to Mortgage Banking

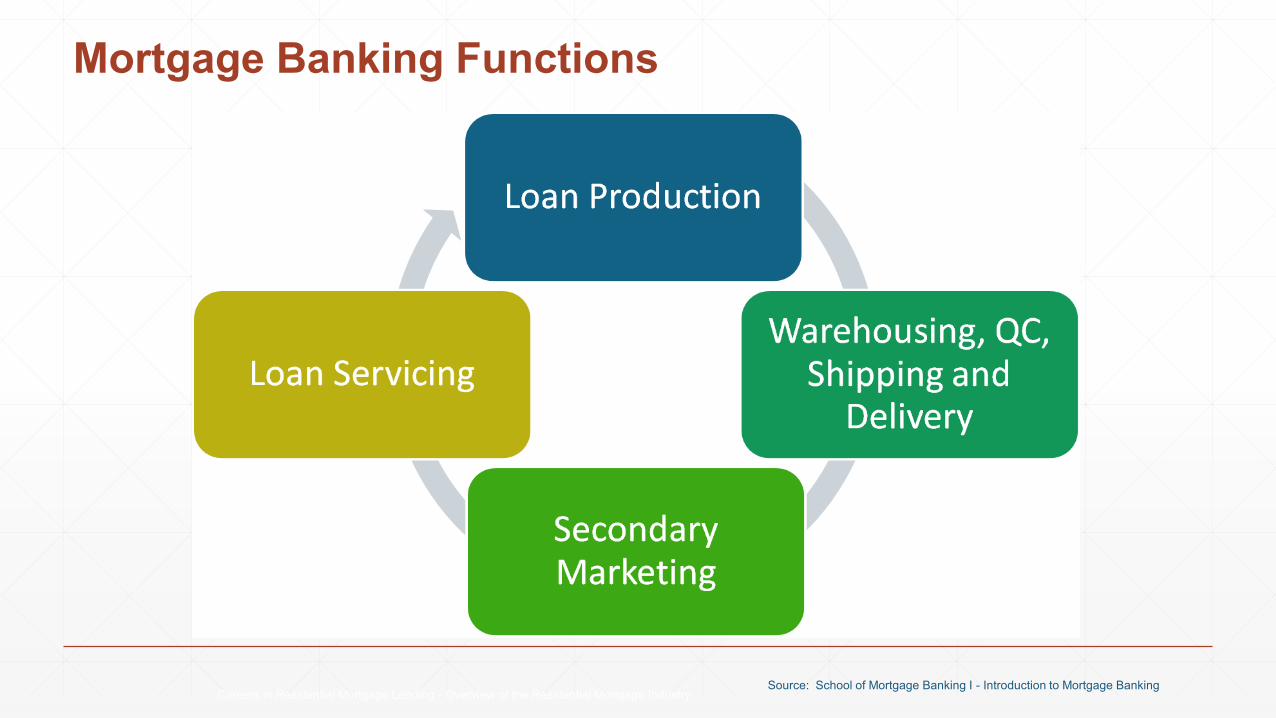

Loan Production

252018 Private and Confidential

3

What Is Mortgage Lending The Higher Purpose

bull Homeownership is an integral part of the American Dream

bull

bull Dedicated mortgage lending professionals take their role in helping people realize that dream seriously and take pride in it

bull

bull Homeownership helps people local communities and the economy to thrive Mortgage lending plays a key role

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Mortgage Banking Functions

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Loan Production

bull Focus is on the borrower (and the borrower experience)

bull Heavily regulated

bullbull Federal or state agencies responsible for control and supervision of a particular

activity or area of public interest

bull Objective is a mortgage loan ldquoproductrdquo comprised of 2 valuable saleable assets

bullbull Stream of loan payments

bull Mortgage servicing rights

School of Mortgage Banking I - Introduction to Mortgage Banking

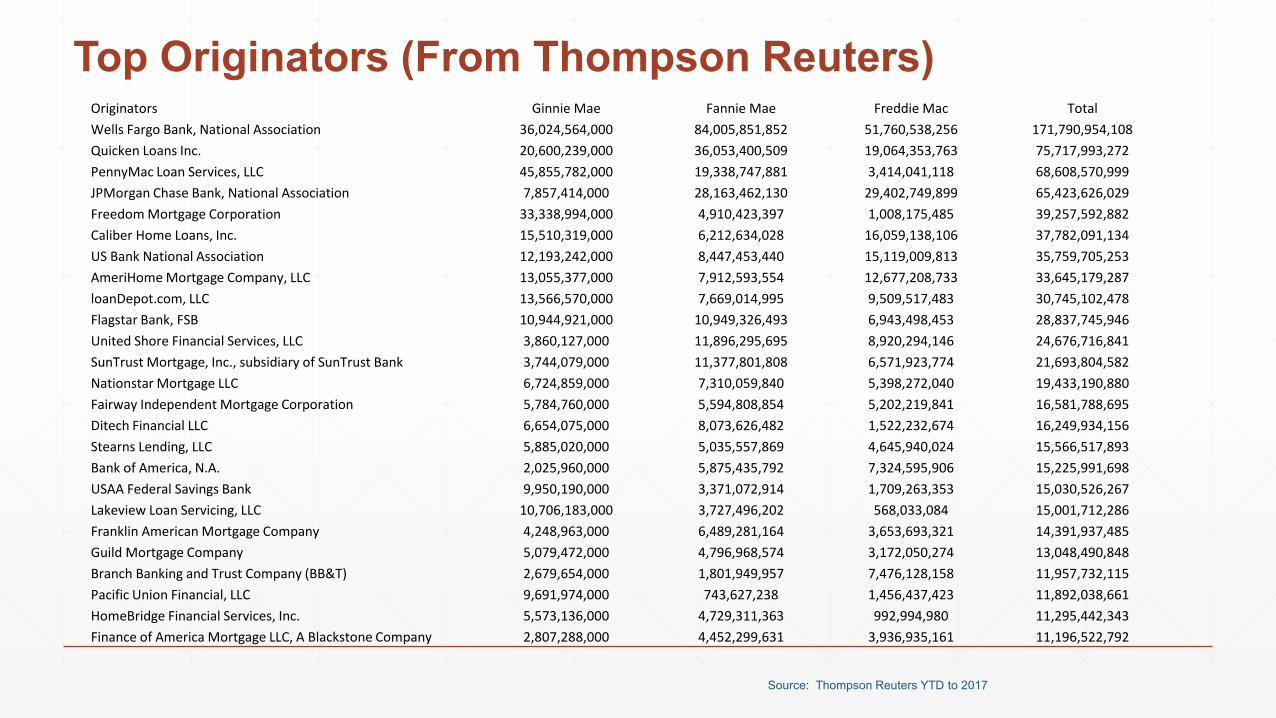

Top Originators (From Thompson Reuters) Originators Ginnie Mae Fannie Mae Freddie Mac Total

Wells Fargo Bank National Association 36024564000 84005851852 51760538256 171790954108

Quicken Loans Inc 20600239000 36053400509 19064353763 75717993272

PennyMac Loan Services LLC 45855782000 19338747881 3414041118 68608570999

JPMorgan Chase Bank National Association 7857414000 28163462130 29402749899 65423626029

Freedom Mortgage Corporation 33338994000 4910423397 1008175485 39257592882

Caliber Home Loans Inc 15510319000 6212634028 16059138106 37782091134

US Bank National Association 12193242000 8447453440 15119009813 35759705253

AmeriHome Mortgage Company LLC 13055377000 7912593554 12677208733 33645179287

loanDepotcom LLC 13566570000 7669014995 9509517483 30745102478

Flagstar Bank FSB 10944921000 10949326493 6943498453 28837745946

United Shore Financial Services LLC 3860127000 11896295695 8920294146 24676716841

SunTrust Mortgage Inc subsidiary of SunTrust Bank 3744079000 11377801808 6571923774 21693804582

Nationstar Mortgage LLC 6724859000 7310059840 5398272040 19433190880

Fairway Independent Mortgage Corporation 5784760000 5594808854 5202219841 16581788695

Ditech Financial LLC 6654075000 8073626482 1522232674 16249934156

Stearns Lending LLC 5885020000 5035557869 4645940024 15566517893

Bank of America NA 2025960000 5875435792 7324595906 15225991698

USAA Federal Savings Bank 9950190000 3371072914 1709263353 15030526267

Lakeview Loan Servicing LLC 10706183000 3727496202 568033084 15001712286

Franklin American Mortgage Company 4248963000 6489281164 3653693321 14391937485

Guild Mortgage Company 5079472000 4796968574 3172050274 13048490848

Branch Banking and Trust Company (BBampT) 2679654000 1801949957 7476128158 11957732115

Pacific Union Financial LLC 9691974000 743627238 1456437423 11892038661

HomeBridge Financial Services Inc 5573136000 4729311363 992994980 11295442343

Finance of America Mortgage LLC A Blackstone Company 2807288000 4452299631 3936935161 11196522792

Source Thompson Reuters YTD to 2017

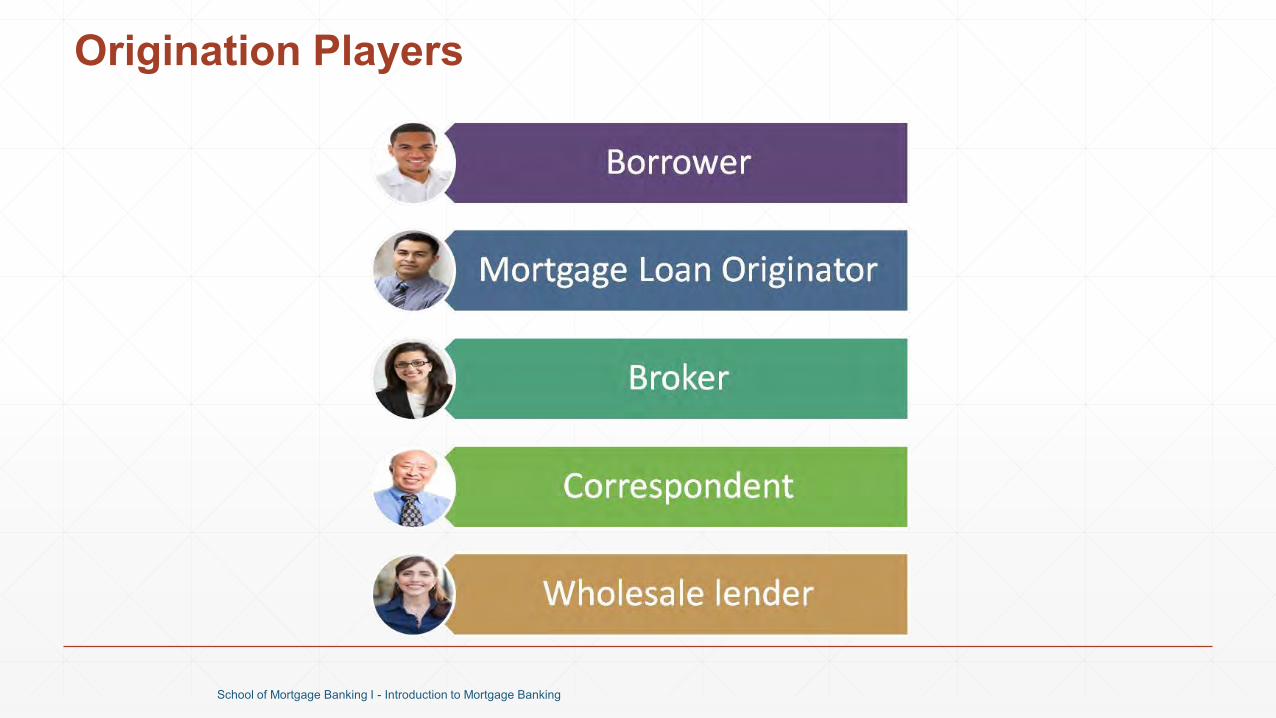

Origination Players

School of Mortgage Banking I - Introduction to Mortgage Banking

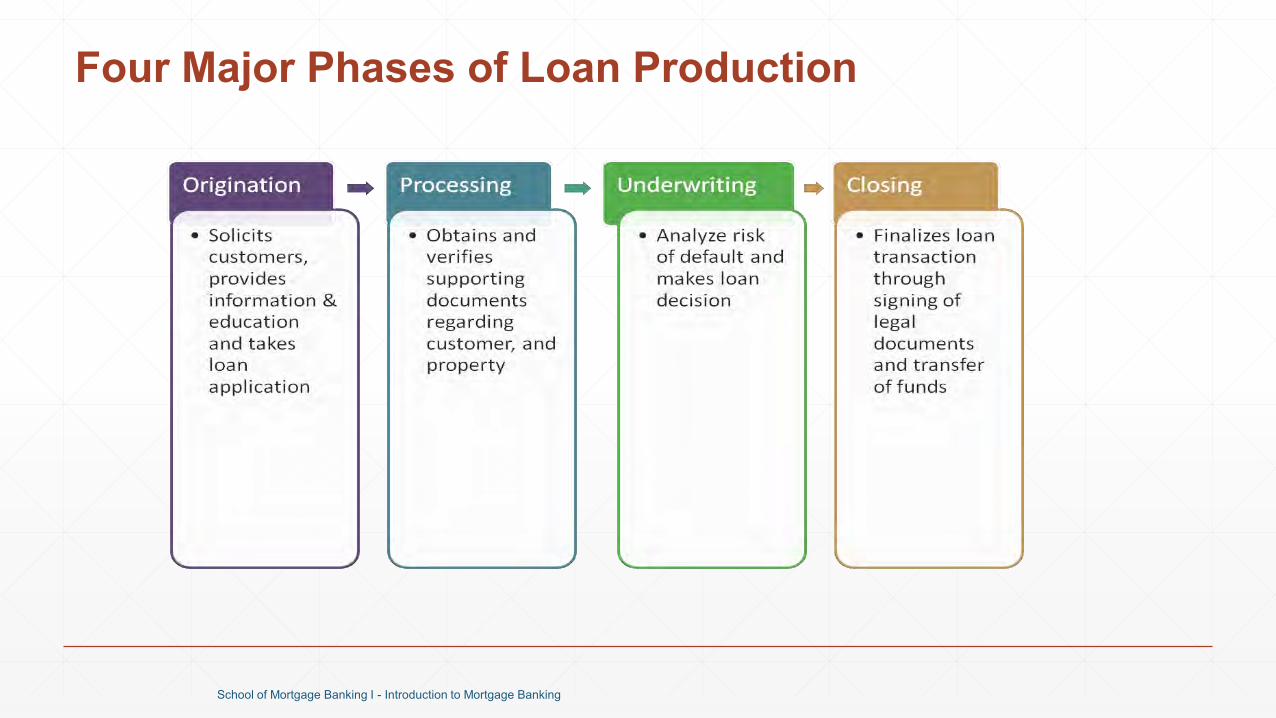

Four Major Phases of Loan Production

School of Mortgage Banking I - Introduction to Mortgage Banking

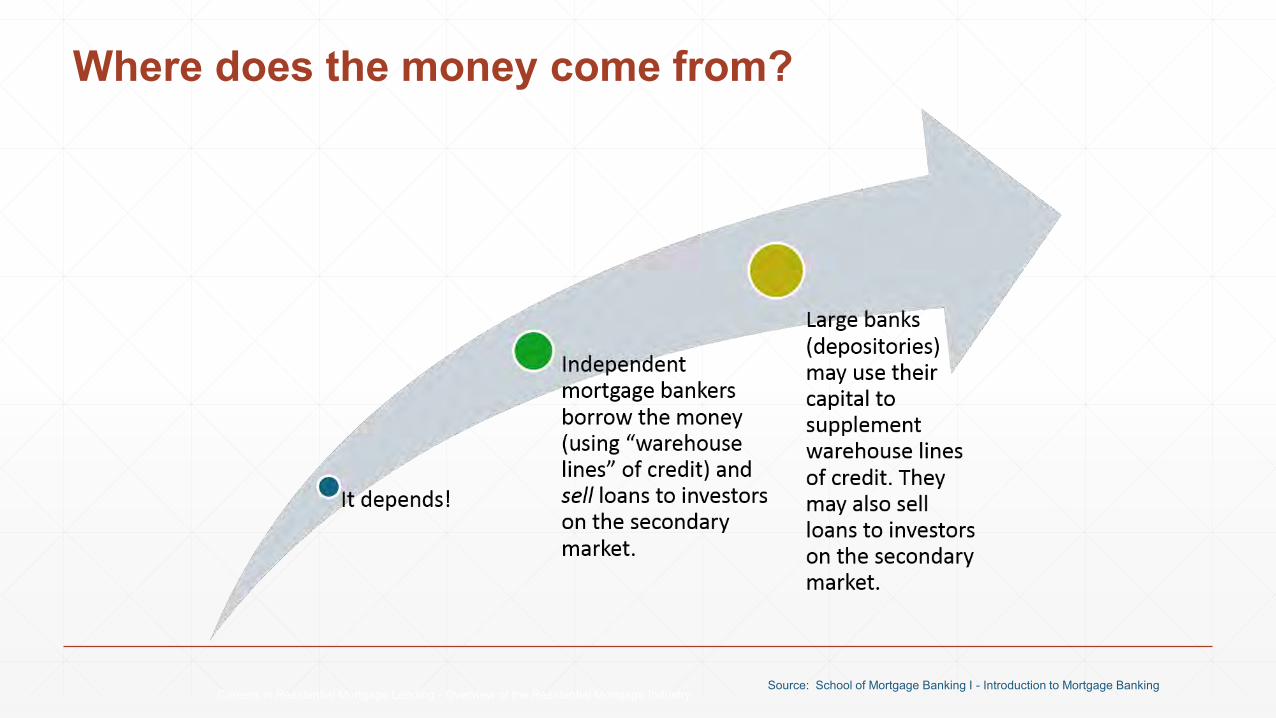

Where does the money come from

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

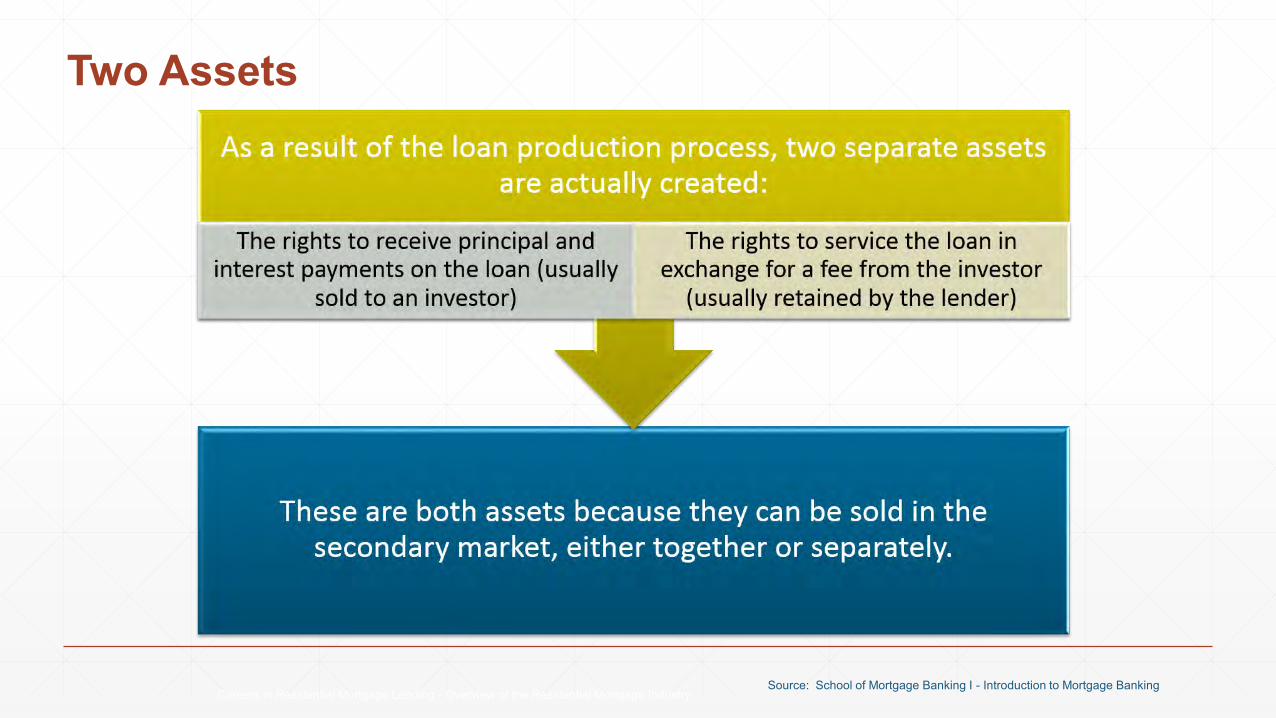

Two Assets

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

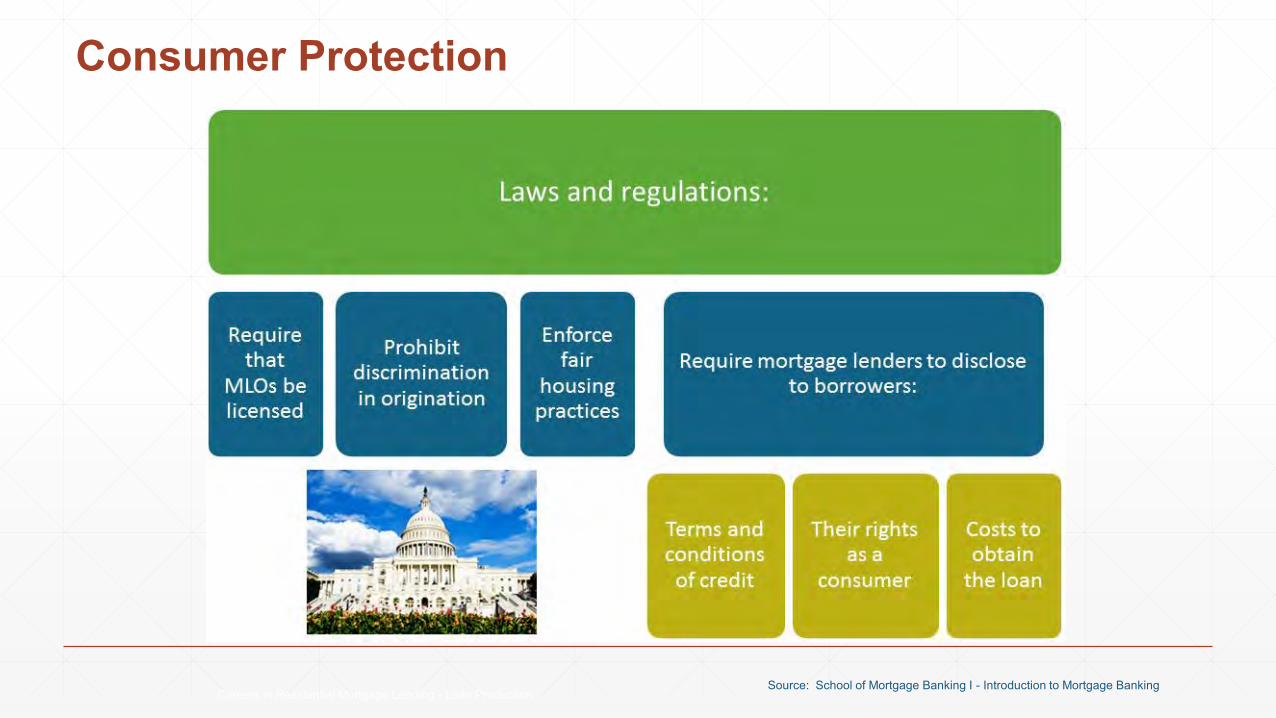

Consumer Protection

Careers in Residential Mortgage Lending - Loan ProductionSource School of Mortgage Banking I - Introduction to Mortgage Banking

Understanding Your BusinessCompanies must focus their origination efforts on products that fit best within their business model

bull Conventional Lending

bull Traditional Agency

bull Specialty Products

bull Government Lending

bull FHA VA USDA FHA Streamline VA IRRRL loans

bull Non-Conforming (True Jumbo)

bull Are you in an area that requires you to offer True Jumbo to remain competitive

bull Non QM

Warehousing QC and Delivery

252018 Private and Confidential

14

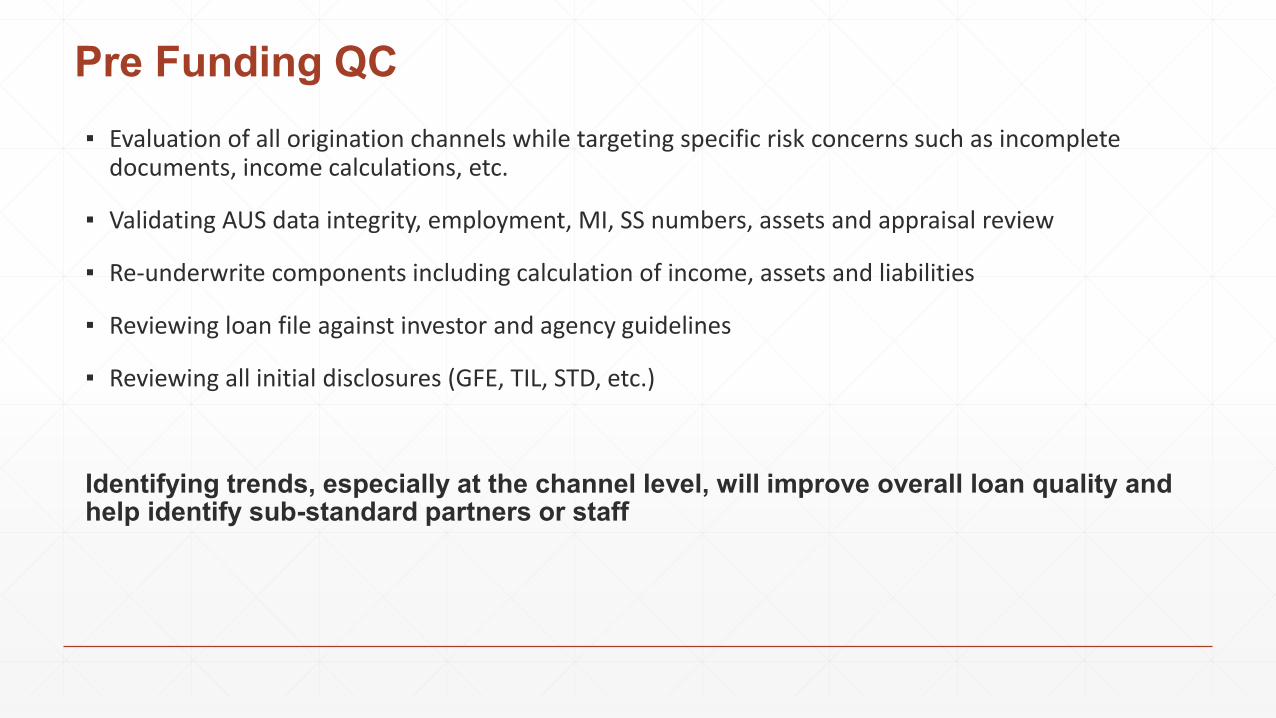

Pre Funding QC Evaluation of all origination channels while targeting specific risk concerns such as incomplete

documents income calculations etc

Validating AUS data integrity employment MI SS numbers assets and appraisal review

Re-underwrite components including calculation of income assets and liabilities

Reviewing loan file against investor and agency guidelines

Reviewing all initial disclosures (GFE TIL STD etc)

Identifying trends especially at the channel level will improve overall loan quality and help identify sub-standard partners or staff

Post Funding QCbull Review of all collateral documents to ensure existence and completeness

bull Re-calculation of income

bull Verification of assets and liability

bull Re-verification of critical information to the AUS data integrity including borrowerco-borrower income employment property type assets SSN address loan terms etc

bull Compliance review

bull Review of appraisal

bull Review of credit reports

bull Summary report highlighting all critical exceptions including current and historical trending

Core processes can be customized to dive deeper into income taxes credit or compliance

The Aggregators

As a mortgage originator there are numerous options where mortgage loans can be sold

bull Over 100 aggregators with multiple deliver options

bull Depository Institutions

bull Examples include ndash Wells Fargo JP Morgan Chase BBampT etc

bull Non-Depository Institutions

bull Examples include ndash Pennymac Amerihome Freedom Mortgage etc

bull The Agencies

bull Fannie Mae Freddie Mac and Ginnie Mae

Choosing the ldquoRightrdquo Aggregators

Numerous options exist to deliver loans choosing the right combination of Aggregators is critical

bull Evaluate an Aggregatorrsquos product offering and pricing

bull Align their product suite with your origination needs

bull Compare pricing across aggregators

bull Compare delivery requirements

bull Review approval requirements

bull Each aggregator has their own set of requirements

bull Net worth warehouse providers policies and procedures etc

Defining Best ExecutionAs a mortgage company matures from Best Efforts to Mandatory Deliveries the profit (and risks change)

bull Best Efforts Delivery

bull LenderOriginator has no financial responsibility to the investoraggregator

bull Mandatory Delivery

bull LenderOriginator is required to deliver committed loans to investoraggregator

bull Failure to deliver usually requires the LenderOriginator to pay for any market costs incurred by the investoraggregator

bull Certainty of Delivery

bull LenderOriginator incurs more responsibility in a Mandatory commitment

bull InvestorAggregator no longer incurs any hedge costs from pull through fluctuations

bull InvestorAggregators pay substantial premium for this certainty

bull Historically there is a 35 basis point premium paid for Mandatory delivery

Best Efforts Deliveries

Most mortgage companies begin their secondary life cycle by delivering closed loans to investors on a best efforts basis (selling servicing released)

bull Established warehouse lines of credit to close in-house

bull Managing warehouse lines of credit

bull Net worth and cash flow

bull Moved underwriting in-house

bull Pros and Cons

bull Overlays

bull Pricing

252018Private and Confidential 20

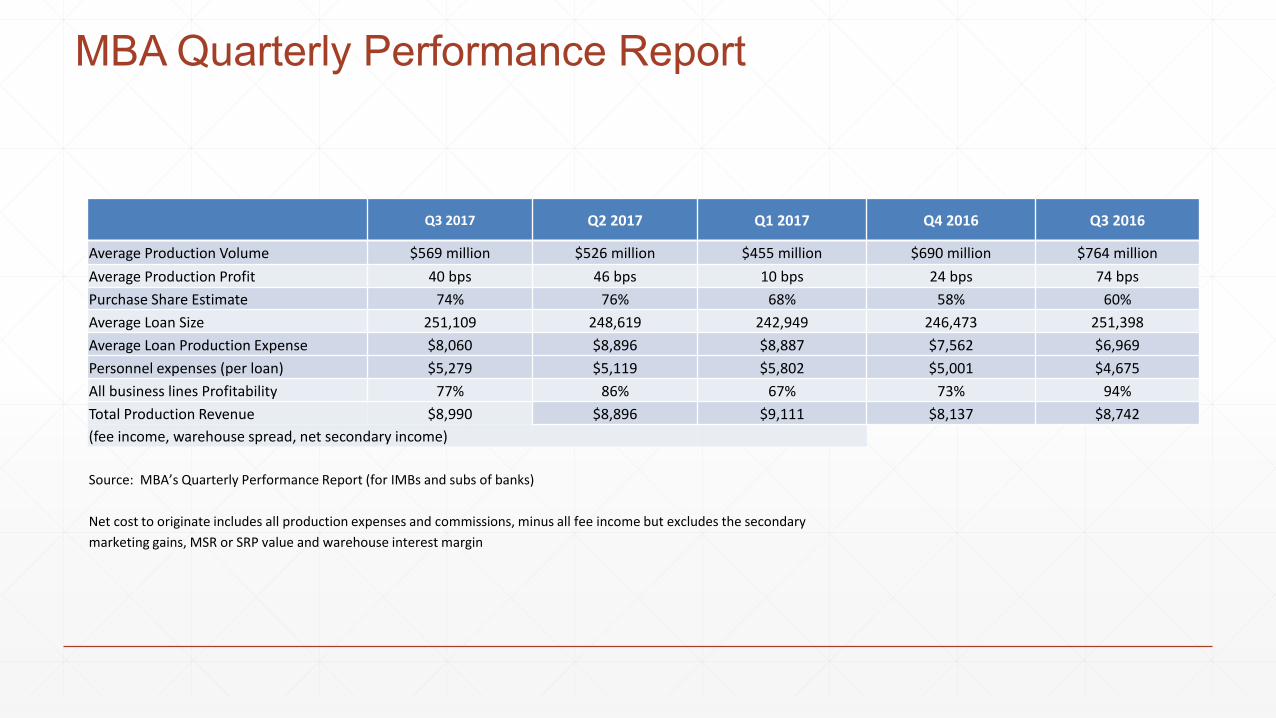

MBA Quarterly Performance Report

Q3 2017 Q2 2017 Q1 2017 Q4 2016 Q3 2016

Average Production Volume $569 million $526 million $455 million $690 million $764 million

Average Production Profit 40 bps 46 bps 10 bps 24 bps 74 bps

Purchase Share Estimate 74 76 68 58 60

Average Loan Size 251109 248619 242949 246473 251398

Average Loan Production Expense $8060 $8896 $8887 $7562 $6969

Personnel expenses (per loan) $5279 $5119 $5802 $5001 $4675

All business lines Profitability 77 86 67 73 94

Total Production Revenue $8990 $8896 $9111 $8137 $8742

(fee income warehouse spread net secondary income)

Source MBArsquos Quarterly Performance Report (for IMBs and subs of banks)

Net cost to originate includes all production expenses and commissions minus all fee income but excludes the secondary

marketing gains MSR or SRP value and warehouse interest margin

Secondary Marketing

252018 Private and Confidential

22

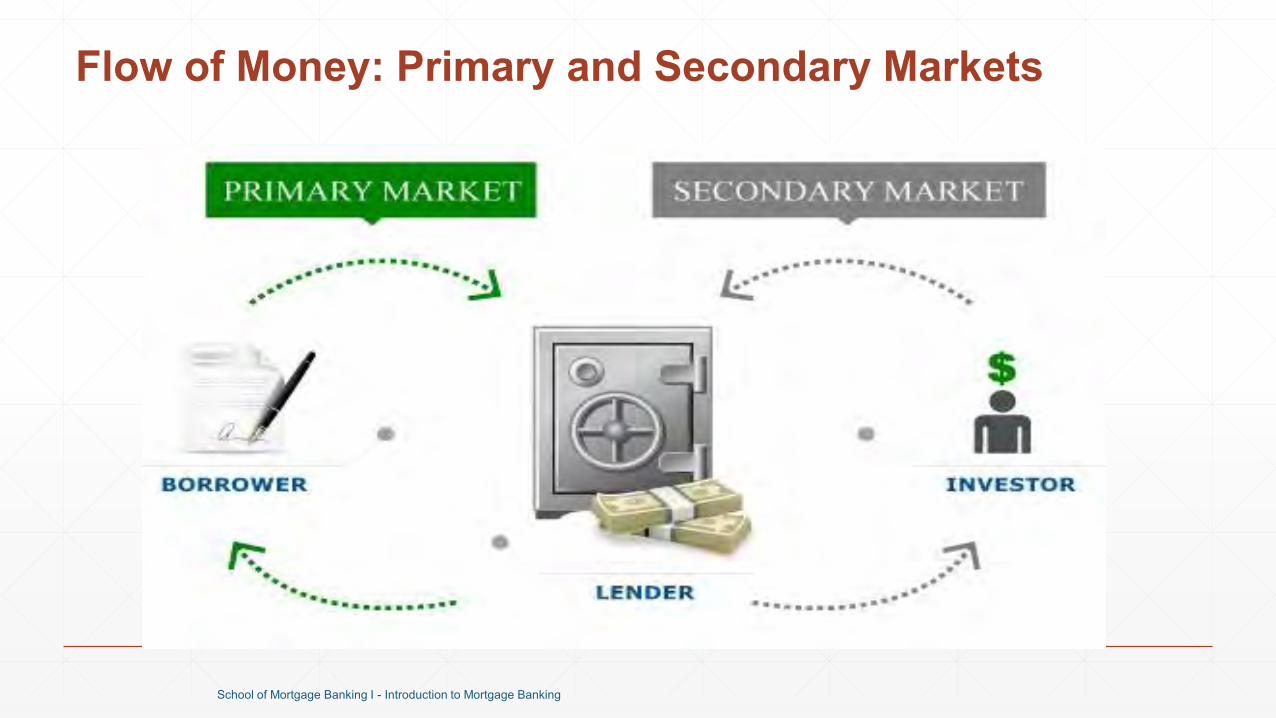

Flow of Money Primary and Secondary Markets

School of Mortgage Banking I - Introduction to Mortgage Banking

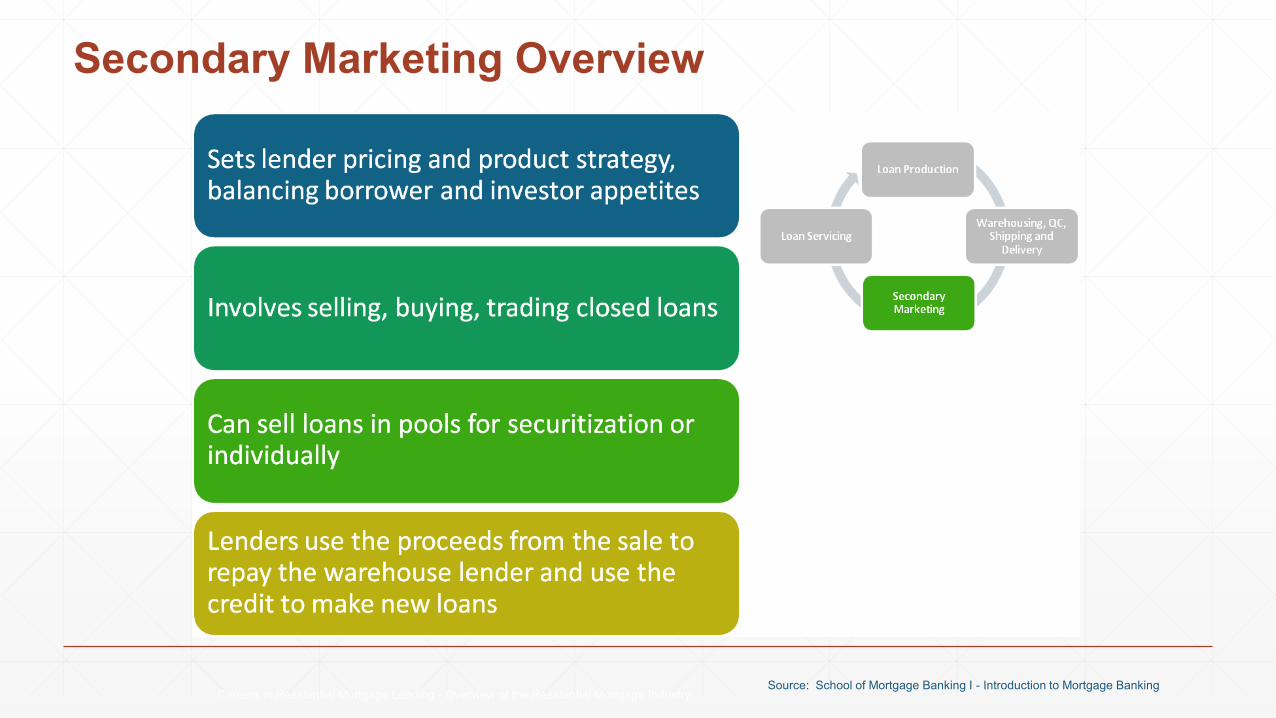

Secondary Marketing Overview

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

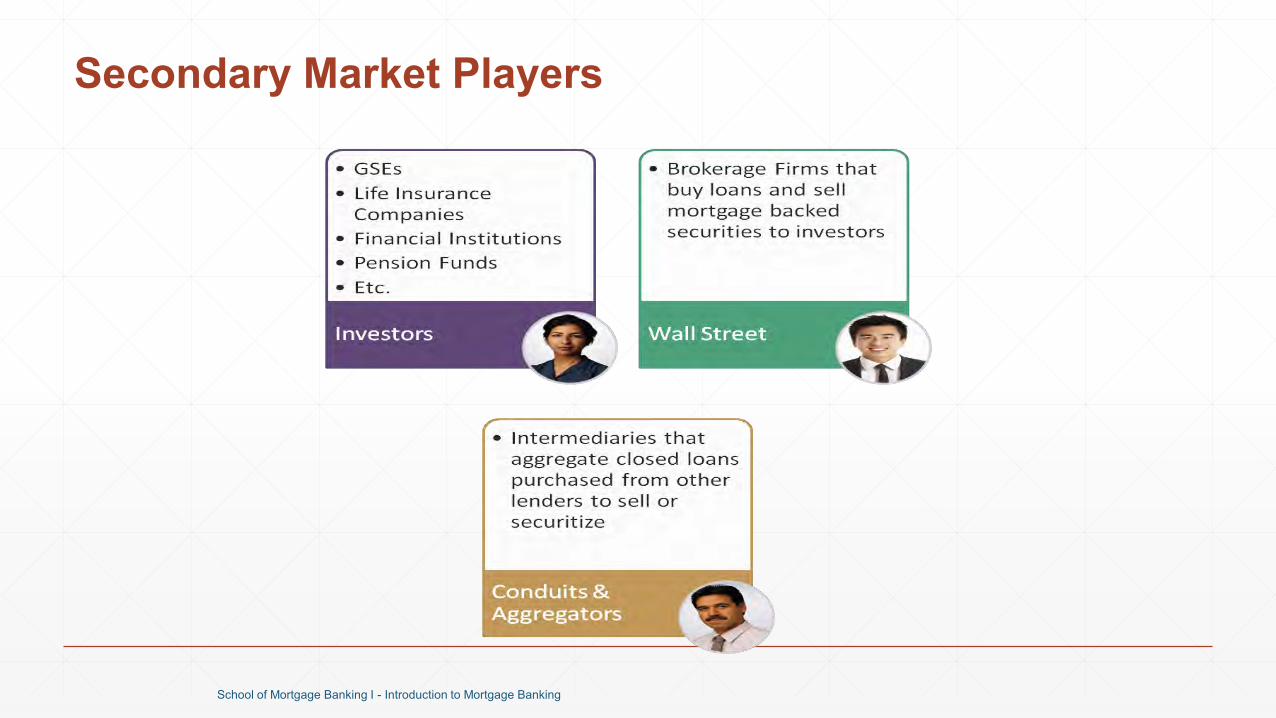

Secondary Market Players

School of Mortgage Banking I - Introduction to Mortgage Banking

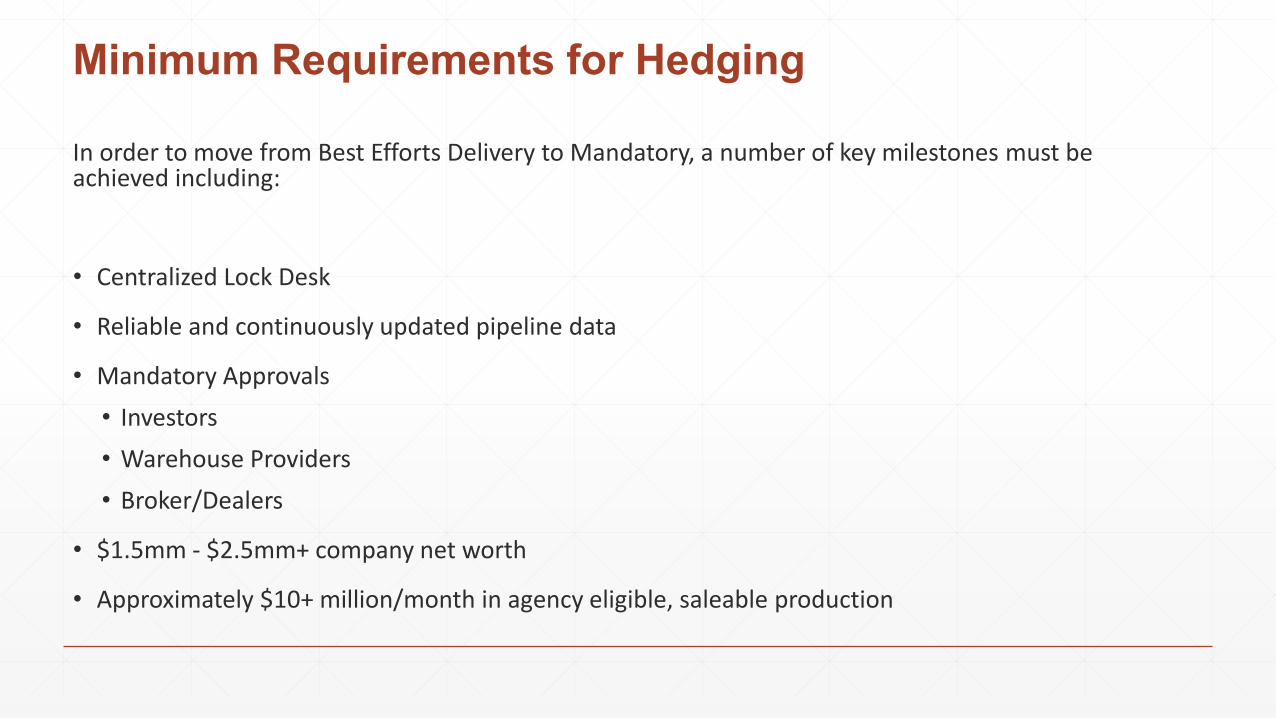

Minimum Requirements for Hedging

In order to move from Best Efforts Delivery to Mandatory a number of key milestones must be achieved including

bull Centralized Lock Desk

bull Reliable and continuously updated pipeline data

bull Mandatory Approvals

bull Investors

bull Warehouse Providers

bull BrokerDealers

bull $15mm - $25mm+ company net worth

bull Approximately $10+ millionmonth in agency eligible saleable production

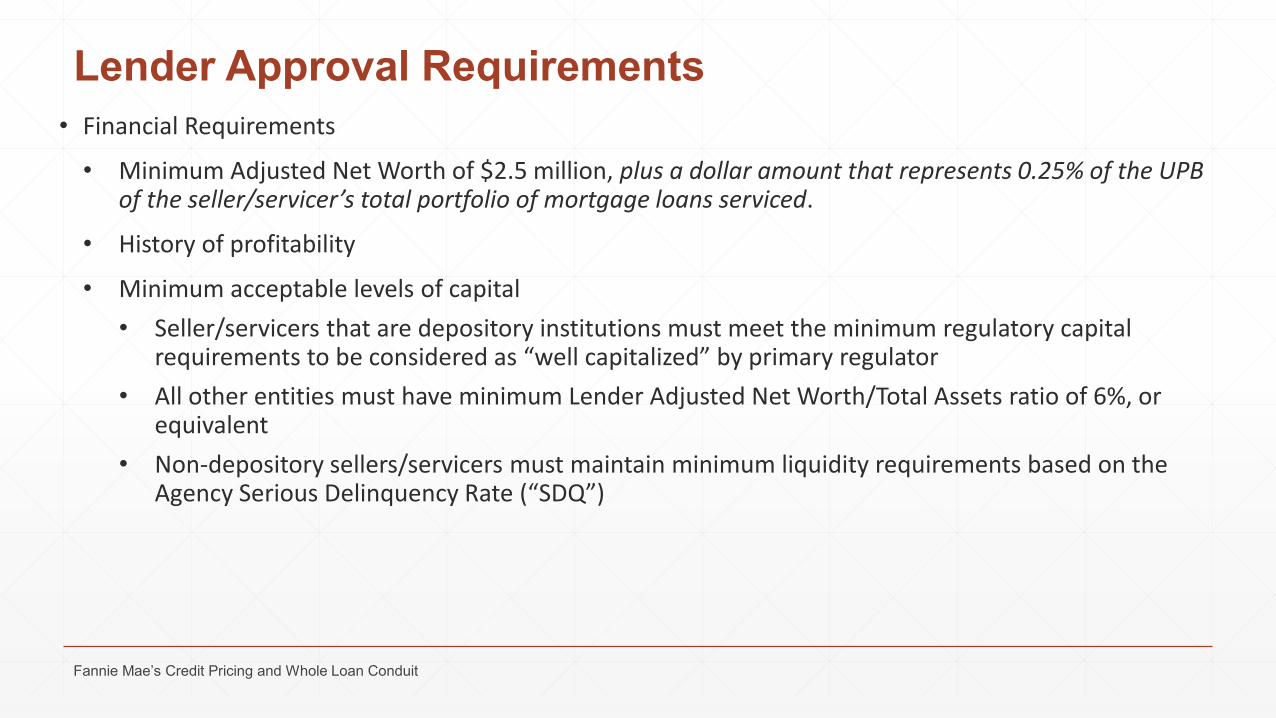

Lender Approval Requirementsbull Financial Requirements

bull Minimum Adjusted Net Worth of $25 million plus a dollar amount that represents 025 of the UPB of the sellerservicerrsquos total portfolio of mortgage loans serviced

bull History of profitability

bull Minimum acceptable levels of capital

bull Sellerservicers that are depository institutions must meet the minimum regulatory capital requirements to be considered as ldquowell capitalizedrdquo by primary regulator

bull All other entities must have minimum Lender Adjusted Net WorthTotal Assets ratio of 6 or equivalent

bull Non-depository sellersservicers must maintain minimum liquidity requirements based on the Agency Serious Delinquency Rate (ldquoSDQrdquo)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

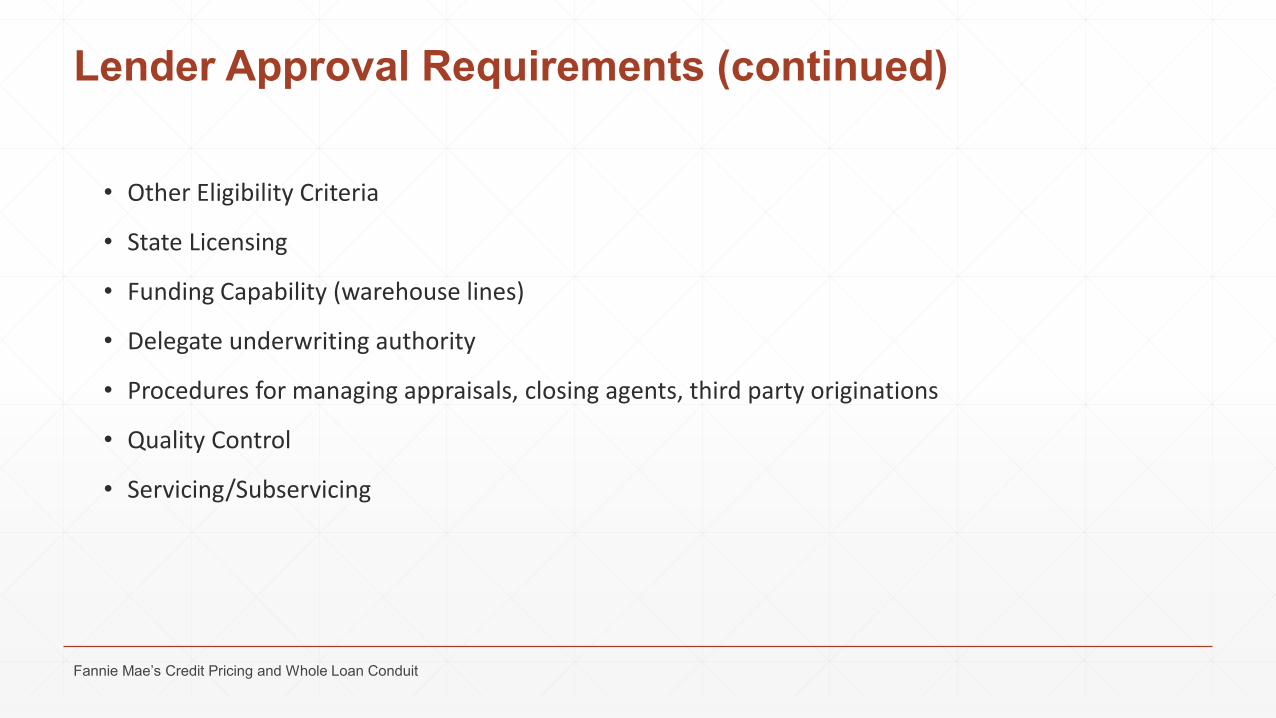

bull Other Eligibility Criteria

bull State Licensing

bull Funding Capability (warehouse lines)

bull Delegate underwriting authority

bull Procedures for managing appraisals closing agents third party originations

bull Quality Control

bull ServicingSubservicing

Lender Approval Requirements (continued)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Interest Rate Risk

bull Definition

bull The risk that an investmentrsquos value will change due to a change in the absolute level of interest rates

bull Tools to hedge

bull Best Efforts Committing

bull Mandatory Committing

bull Hedging with TBAs

Fannie Maersquos Credit Pricing and Whole Loan Conduit

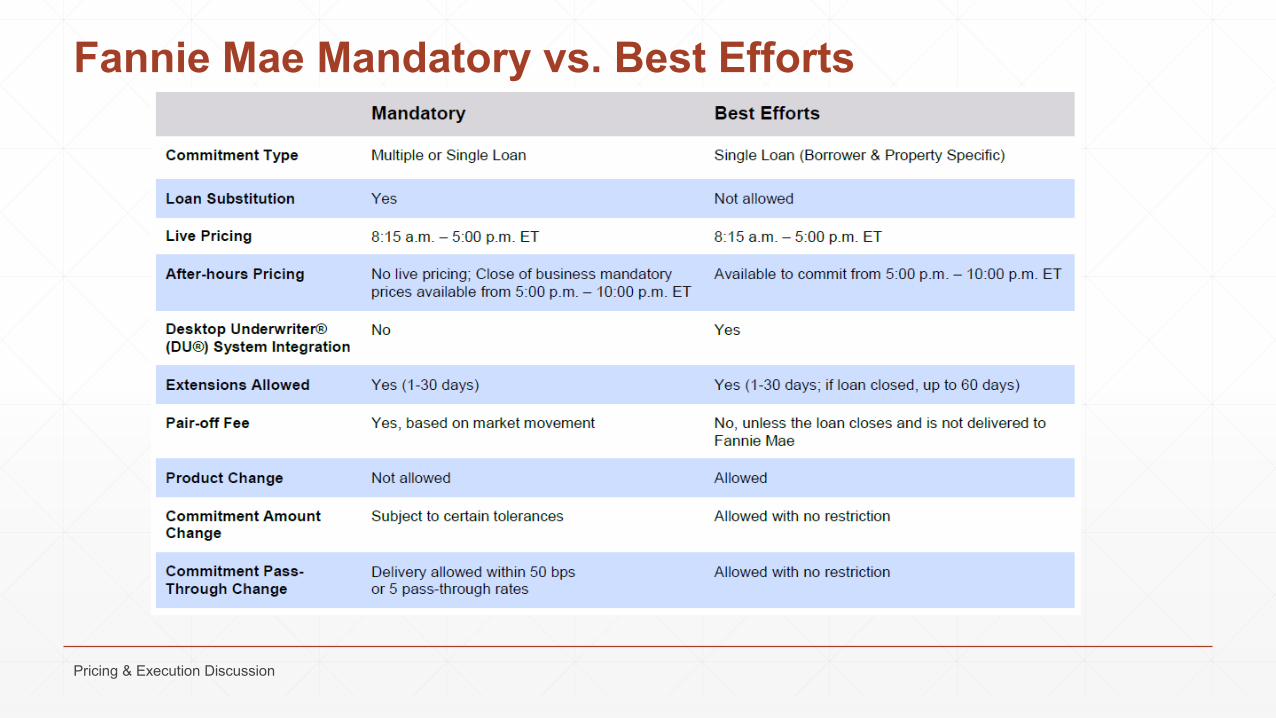

Fannie Mae Mandatory vs Best Efforts

Pricing amp Execution Discussion

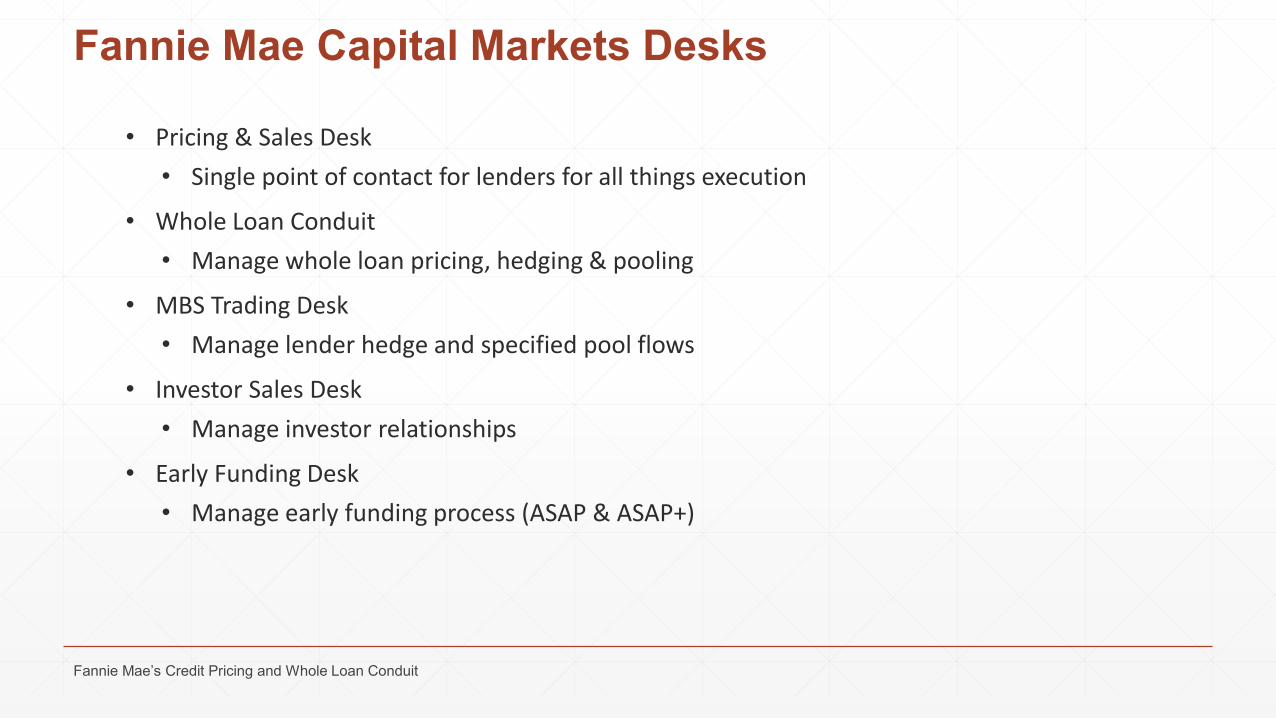

Fannie Mae Capital Markets Desks

bull Pricing amp Sales Desk

bull Single point of contact for lenders for all things execution

bull Whole Loan Conduit

bull Manage whole loan pricing hedging amp pooling

bull MBS Trading Desk

bull Manage lender hedge and specified pool flows

bull Investor Sales Desk

bull Manage investor relationships

bull Early Funding Desk

bull Manage early funding process (ASAP amp ASAP+)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

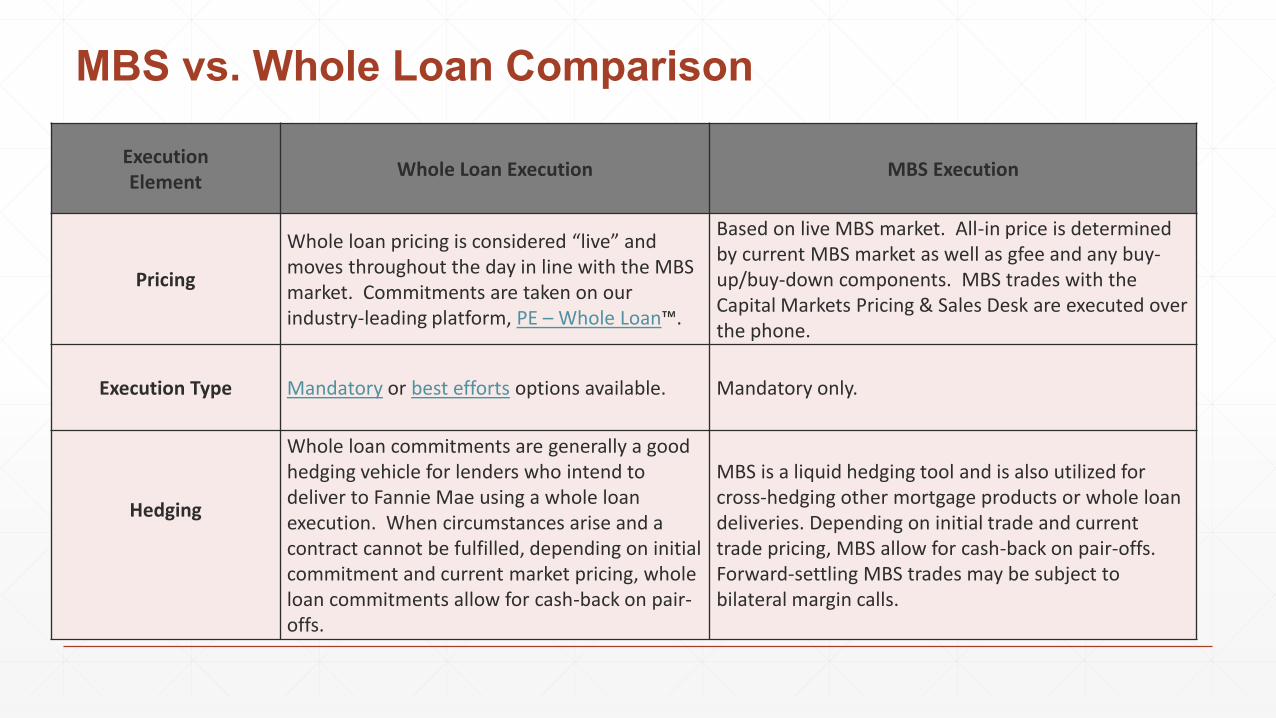

MBS vs Whole Loan Comparison

ExecutionElement

Whole Loan Execution MBS Execution

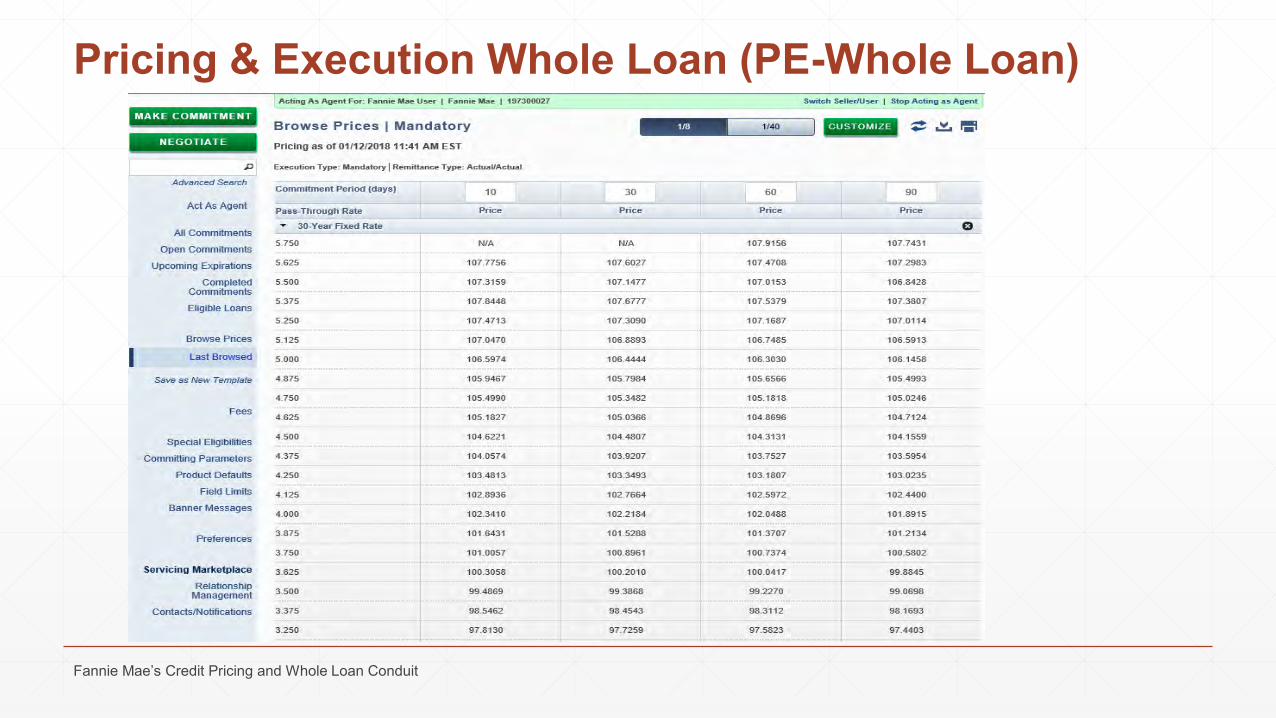

Pricing

Whole loan pricing is considered ldquoliverdquo and moves throughout the day in line with the MBS market Commitments are taken on our industry-leading platform PE ndash Whole Loantrade

Based on live MBS market All-in price is determined by current MBS market as well as gfee and any buy-upbuy-down components MBS trades with the Capital Markets Pricing amp Sales Desk are executed over the phone

Execution Type Mandatory or best efforts options available Mandatory only

Hedging

Whole loan commitments are generally a good hedging vehicle for lenders who intend to deliver to Fannie Mae using a whole loan execution When circumstances arise and a contract cannot be fulfilled depending on initial commitment and current market pricing whole loan commitments allow for cash-back on pair-offs

MBS is a liquid hedging tool and is also utilized for cross-hedging other mortgage products or whole loan deliveries Depending on initial trade and current trade pricing MBS allow for cash-back on pair-offs Forward-settling MBS trades may be subject to bilateral margin calls

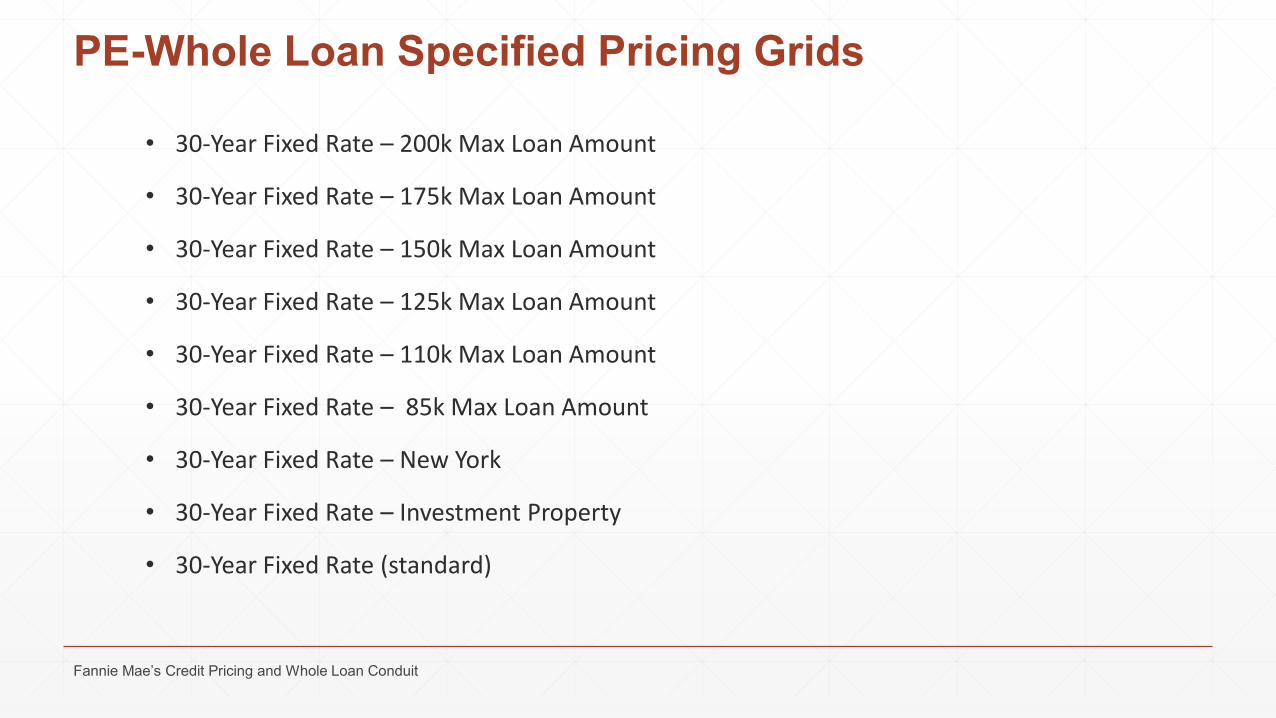

PE-Whole Loan Specified Pricing Grids

bull 30-Year Fixed Rate ndash 200k Max Loan Amount

bull 30-Year Fixed Rate ndash 175k Max Loan Amount

bull 30-Year Fixed Rate ndash 150k Max Loan Amount

bull 30-Year Fixed Rate ndash 125k Max Loan Amount

bull 30-Year Fixed Rate ndash 110k Max Loan Amount

bull 30-Year Fixed Rate ndash 85k Max Loan Amount

bull 30-Year Fixed Rate ndash New York

bull 30-Year Fixed Rate ndash Investment Property

bull 30-Year Fixed Rate (standard)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

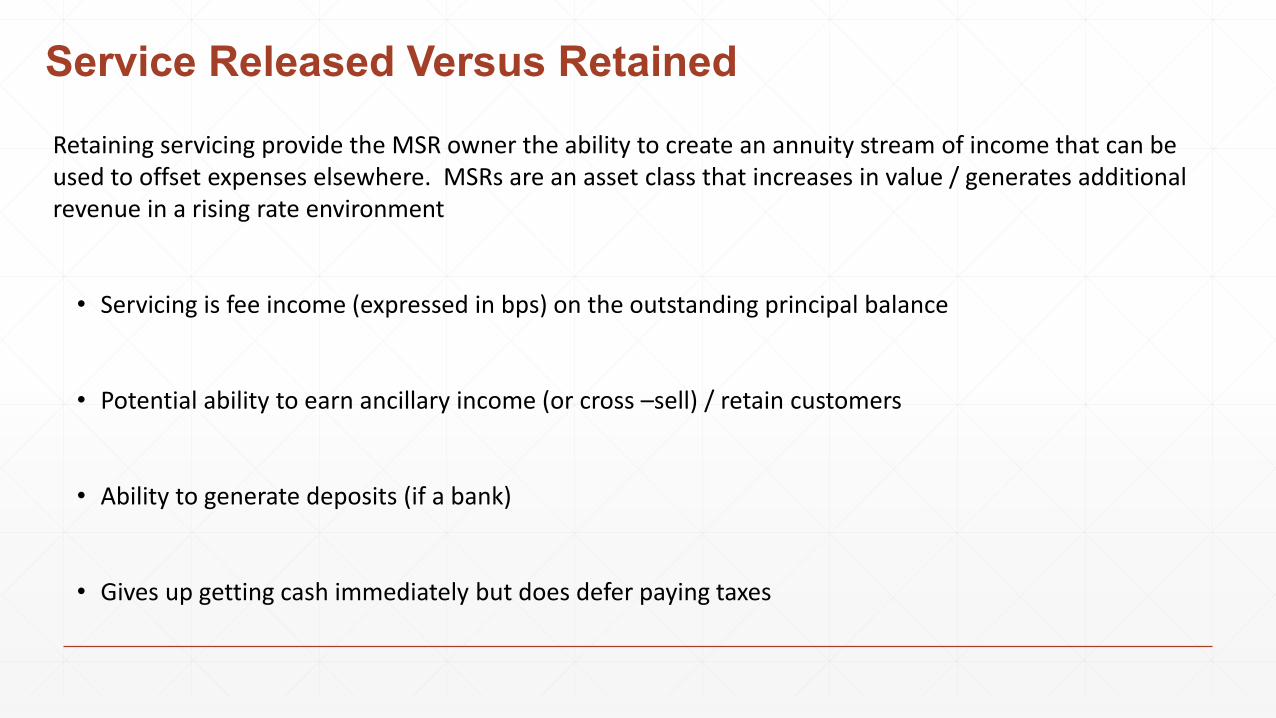

Service Released Versus Retained

Retaining servicing provide the MSR owner the ability to create an annuity stream of income that can be used to offset expenses elsewhere MSRs are an asset class that increases in value generates additional revenue in a rising rate environment

bull Servicing is fee income (expressed in bps) on the outstanding principal balance

bull Potential ability to earn ancillary income (or cross ndashsell) retain customers

bull Ability to generate deposits (if a bank)

bull Gives up getting cash immediately but does defer paying taxes

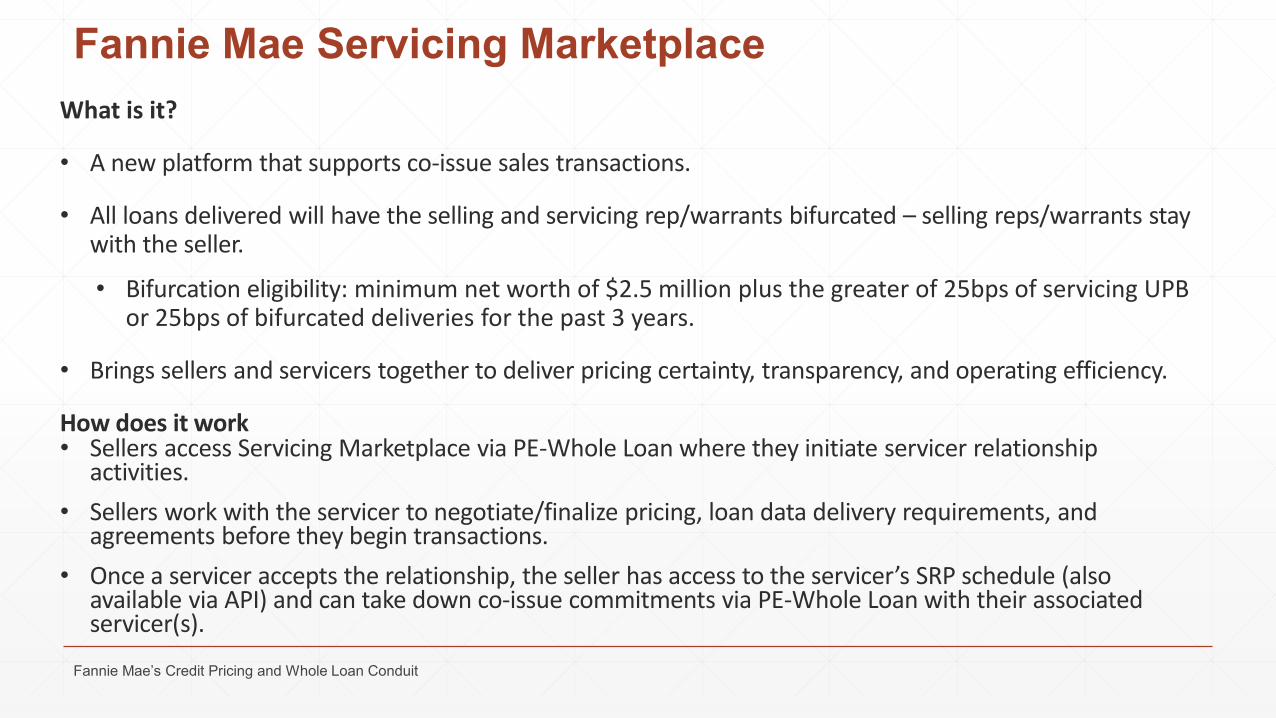

Fannie Mae Servicing MarketplaceWhat is it

bull A new platform that supports co-issue sales transactions

bull All loans delivered will have the selling and servicing repwarrants bifurcated ndash selling repswarrants stay with the seller

bull Bifurcation eligibility minimum net worth of $25 million plus the greater of 25bps of servicing UPB or 25bps of bifurcated deliveries for the past 3 years

bull Brings sellers and servicers together to deliver pricing certainty transparency and operating efficiency

How does it workbull Sellers access Servicing Marketplace via PE-Whole Loan where they initiate servicer relationship

activities

bull Sellers work with the servicer to negotiatefinalize pricing loan data delivery requirements and agreements before they begin transactions

bull Once a servicer accepts the relationship the seller has access to the servicerrsquos SRP schedule (also available via API) and can take down co-issue commitments via PE-Whole Loan with their associated servicer(s)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Fannie Mae Servicing Marketplace

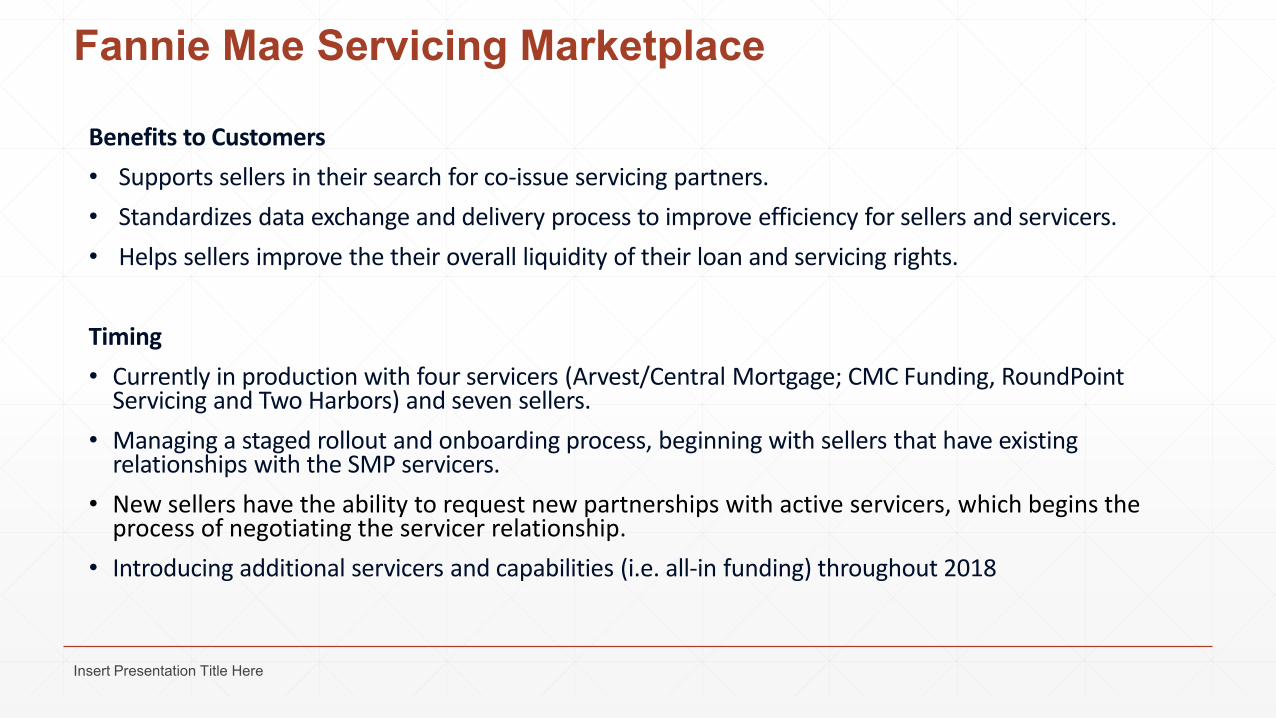

Benefits to Customers

bull Supports sellers in their search for co-issue servicing partners

bull Standardizes data exchange and delivery process to improve efficiency for sellers and servicers

bull Helps sellers improve the their overall liquidity of their loan and servicing rights

Timing

bull Currently in production with four servicers (ArvestCentral Mortgage CMC Funding RoundPointServicing and Two Harbors) and seven sellers

bull Managing a staged rollout and onboarding process beginning with sellers that have existing relationships with the SMP servicers

bull New sellers have the ability to request new partnerships with active servicers which begins the process of negotiating the servicer relationship

bull Introducing additional servicers and capabilities (ie all-in funding) throughout 2018

Insert Presentation Title Here

Pricing amp Execution Whole Loan (PE-Whole Loan)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Single SecurityDescription

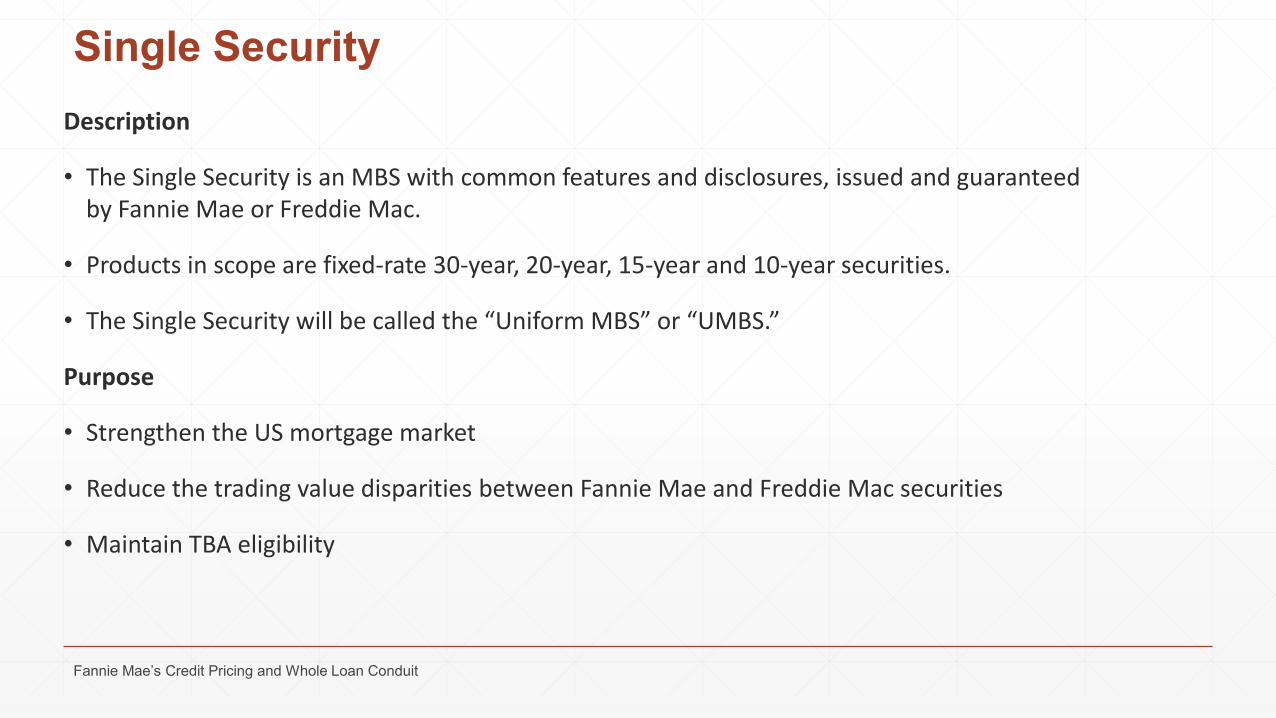

bull The Single Security is an MBS with common features and disclosures issued and guaranteed by Fannie Mae or Freddie Mac

bull Products in scope are fixed-rate 30-year 20-year 15-year and 10-year securities

bull The Single Security will be called the ldquoUniform MBSrdquo or ldquoUMBSrdquo

Purpose

bull Strengthen the US mortgage market

bull Reduce the trading value disparities between Fannie Mae and Freddie Mac securities

bull Maintain TBA eligibility

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Single SecurityDetails

bull Features of the Single Security will be based generally on Fannie Mae MBS

bull Fannie Mae MBS will be fungible with the new Single Security

bull Freddie Mac is creating a mechanism to allow investors to exchange legacy PCs for Single Securities

bull The guarantor of the Single Security will be the issuing Enterprise

bull Both Fannie Mae amp Freddie Mac issued Single Securities will be TBA eligible

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Single SecurityHow will it affect you

bull The single security is expected to be issued in Q2 2019 when both Fannie Mae and Freddie Mac are on the Common Securitization Platform (CSP)

bull The CSP will act as agent for the issuance bond administration and disclosures for all newly-issued single securities

bull Lenders will continue to interact with Fannie Mae and will not interact with the CSP

bull All servicer interaction will continue to occur directly with Fannie Mae

bull Single security will not cause changes to DU eligibility requirements

bull Fannie Mae will not be making any changes to our SellerServicer guide in response to single security

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Responding to the Market Dynamic solutions to bring process efficiency and Day 1 Certaintytrade

Day 1 Certaintytrade

Industry Status QuoPaper-intensive Inefficient ProtractedBorrowers and lenders suffer from amultitude of pain points brought on bytraditional paper-based processes

Fannie Maersquos VisionStreamlined Efficient DynamicBy leveraging borrower and property data applying advanced analytics and bringing key quality control processes up front Fannie Mae is helping lenders transform their business

Wersquore introducing capabilities that address lender feedback by driving greater transparency and a more streamlined mortgage origination process

The result Day 1 Certainty

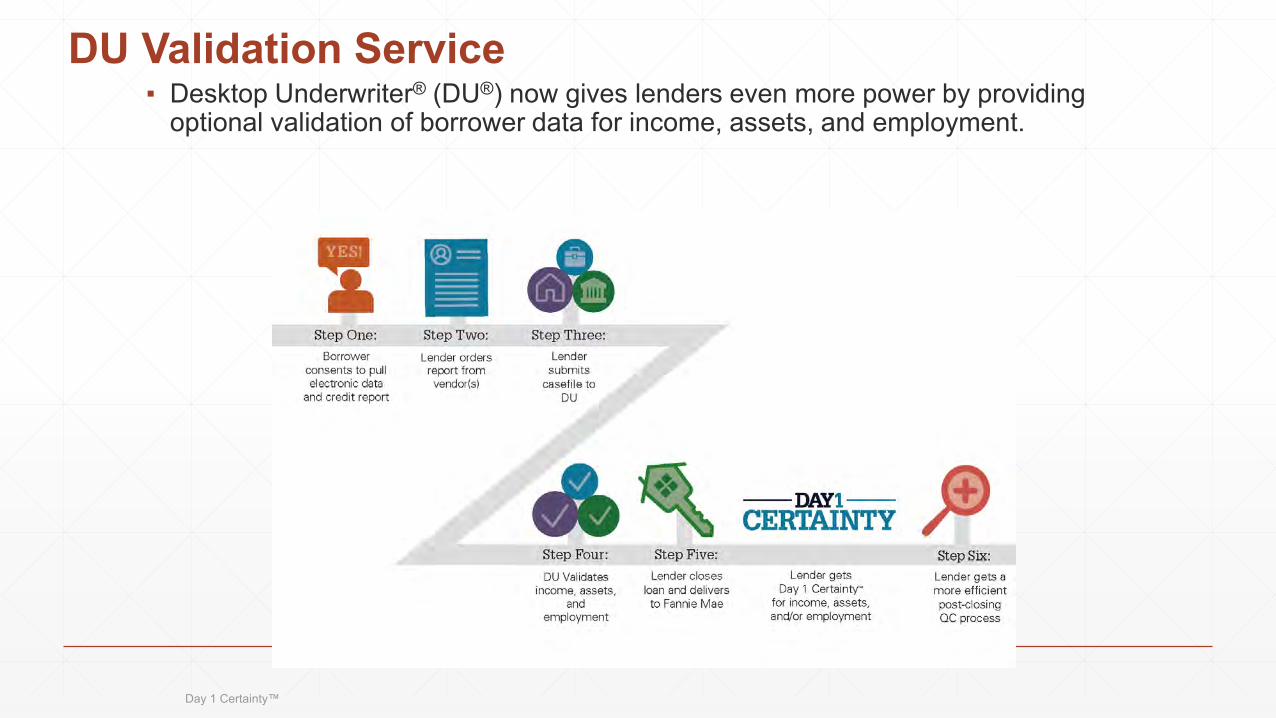

DU Validation Service Desktop Underwriterreg (DUreg) now gives lenders even more power by providing

optional validation of borrower data for income assets and employment

Day 1 Certaintytrade

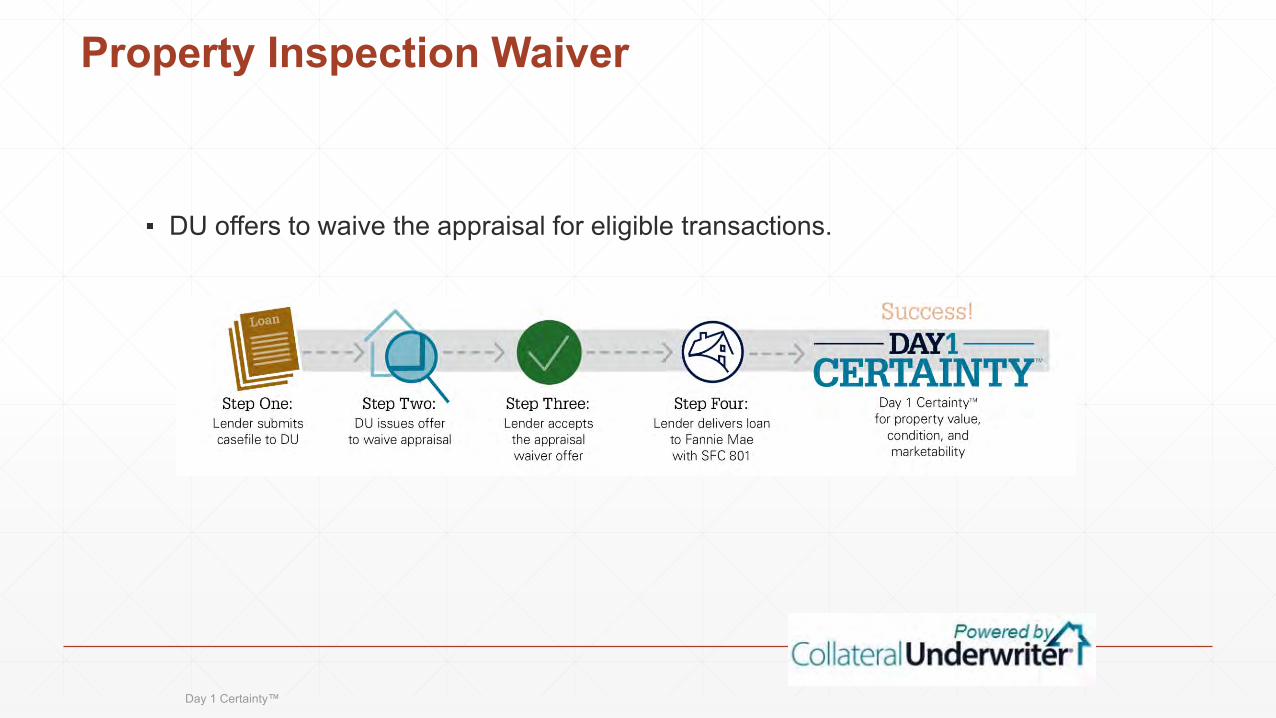

Property Inspection Waiver

DU offers to waive the appraisal for eligible transactions

Day 1 Certaintytrade

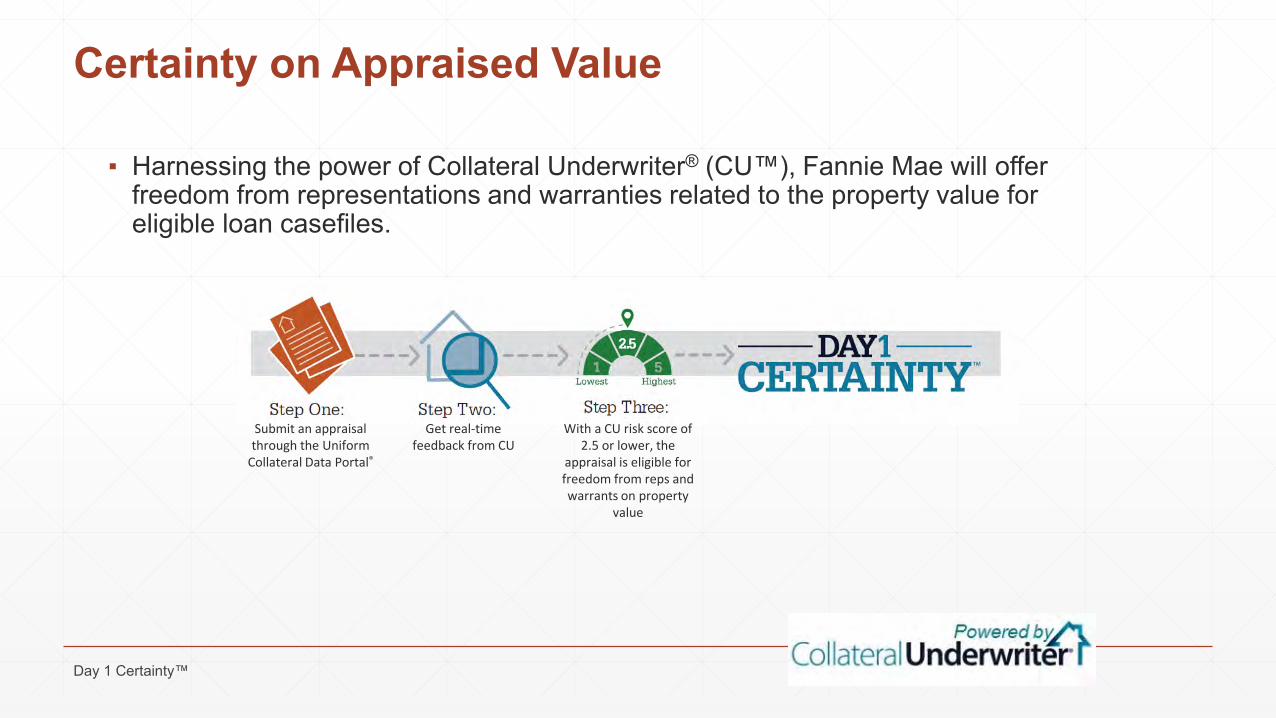

Certainty on Appraised Value

Harnessing the power of Collateral Underwriterreg (CUtrade) Fannie Mae will offer freedom from representations and warranties related to the property value for eligible loan casefiles

Day 1 Certaintytrade

Submit an appraisal through the Uniform

Collateral Data Portalreg

Get real-time feedback from CU

With a CU risk score of 25 or lower the

appraisal is eligible for freedom from reps and warrants on property

value

Loan Administration Servicing

252018 Private and Confidential

46

Tax Reform Bill 2017

The House and Senate passed HR1 the Tax Cuts and Jobs Act and the President signed the bill into legislation right before the Holiday Break (effective for the 2018 tax year)

bull Change in Corporate Tax Rate from 35 to 21

bull Will impact the ldquoCrdquo Corp Bank as the MSR asset is net of the deferred tax liability for BASEL III the lower the tax rate the more than the MSR asset counts toward BASEL III limits

bull A cap on the Interest Deduction (ldquoMIDrdquo)

bull Maintains the mortgage interest deduction for existing mortgages but limits deduction to $750K on mortgages made after December 15th 2017

bull Debt on first and second under $750K but suspends deductibility of home equity lines

bull State and Local tax deductions (ldquoSALTrdquo) allows up to $10000 in state and local tax deductions

bull Maintained current tax treatment for MSRs

bull Preserved the Capital gains treatment for home sales allowing homeowners ability to exclude up to $500K on gain on sale of primary residence

47

BASEL III Update Today [November 21 2017] the Federal banking regulators finalized the pause on Basel III implementation to allow banks that are not subject to Basel IIIs advanced approaches to extend the current regulatory capital treatment of mortgage servicing assets (MSAs) Advanced approaches banking organizations (those with over $250 billion in assets or more than $10 billion in foreign exposure) are required to apply the capital rulesrsquo fully phased-in treatment for these capital items beginning January 1 2018

For example the transitions NPR [now finalized] would require a non-advanced approaches banking organization with an amount of MSAs above the 10 percent common equity tier 1 capital deduction threshold in the capital rules to deduct from common equity tier 1 capital 80 percent of the amount of MSAs above this threshold and to apply a 100 percent risk weight to the MSAs that are not deducted from common equity tier 1 capital including the MSAs that otherwise would be deducted but for the transition provisions

48

Source MBA Loan Administration Email 11212017

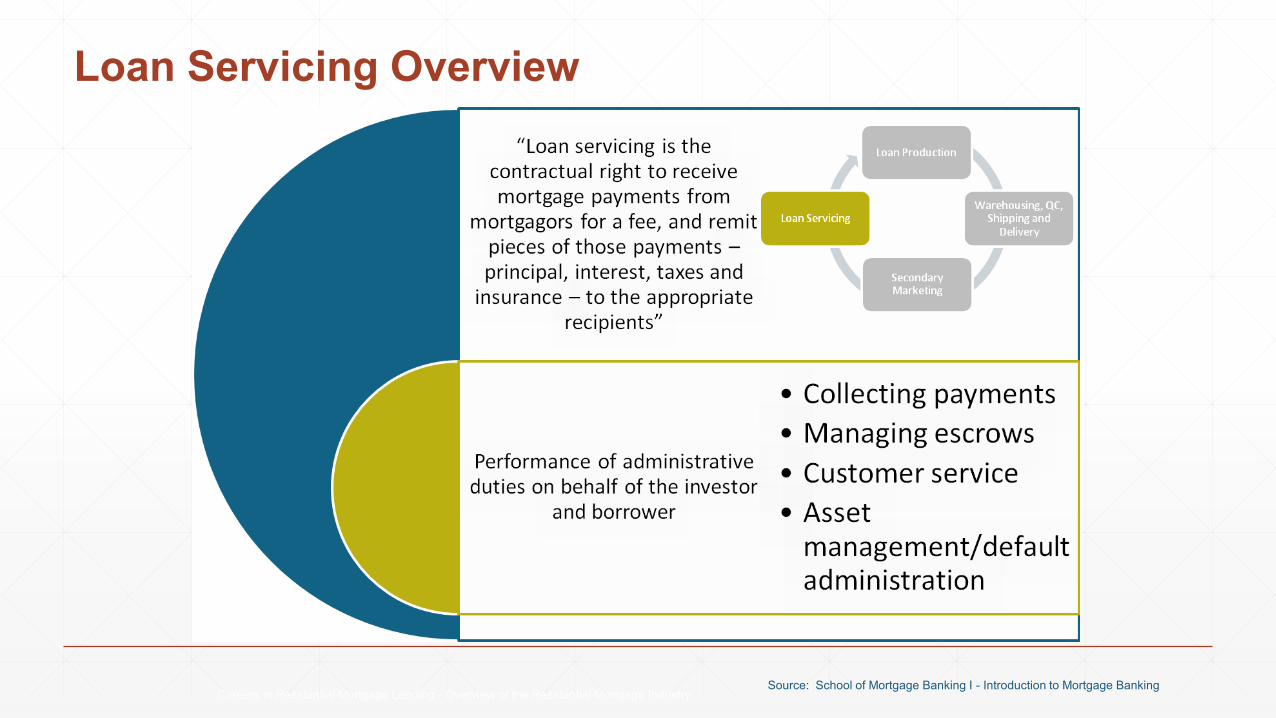

Loan Servicing Overview

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

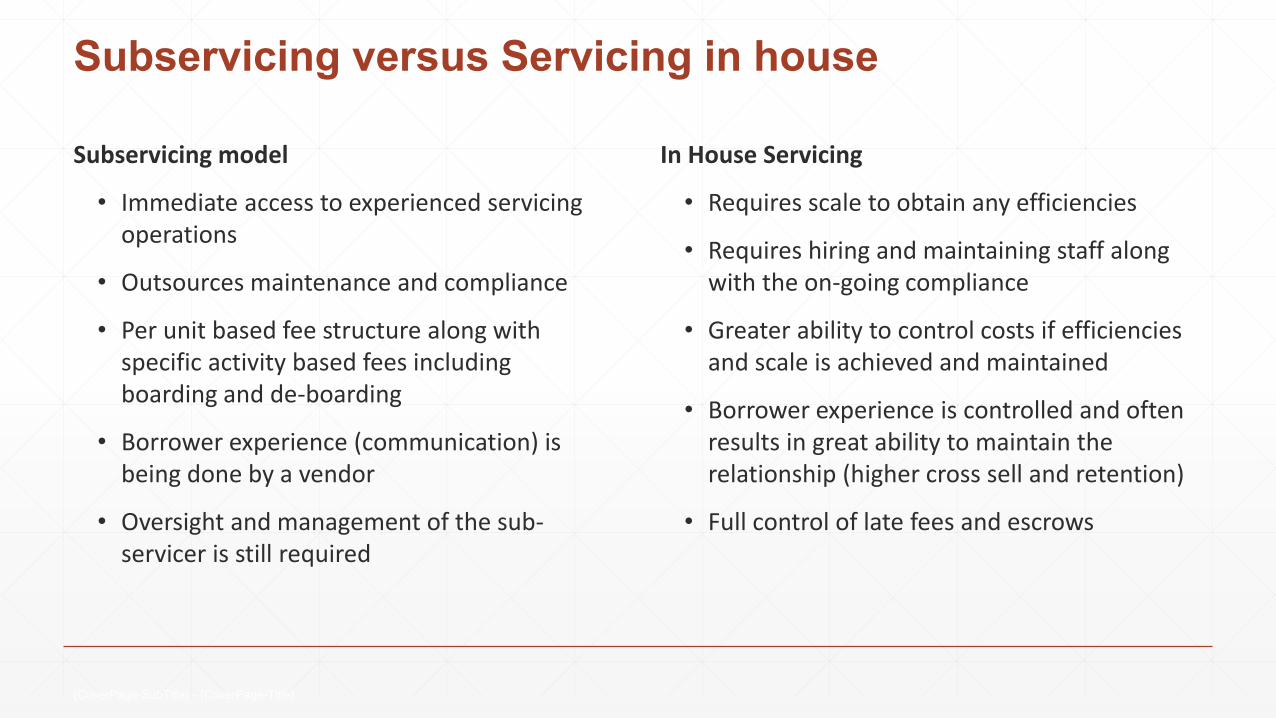

Subservicing versus Servicing in house

Subservicing model

bull Immediate access to experienced servicing operations

bull Outsources maintenance and compliance

bull Per unit based fee structure along with specific activity based fees including boarding and de-boarding

bull Borrower experience (communication) is being done by a vendor

bull Oversight and management of the sub-servicer is still required

In House Servicing

bull Requires scale to obtain any efficiencies

bull Requires hiring and maintaining staff along with the on-going compliance

bull Greater ability to control costs if efficiencies and scale is achieved and maintained

bull Borrower experience is controlled and often results in great ability to maintain the relationship (higher cross sell and retention)

bull Full control of late fees and escrows

CoverPage-SubTitle - CoverPage-Title

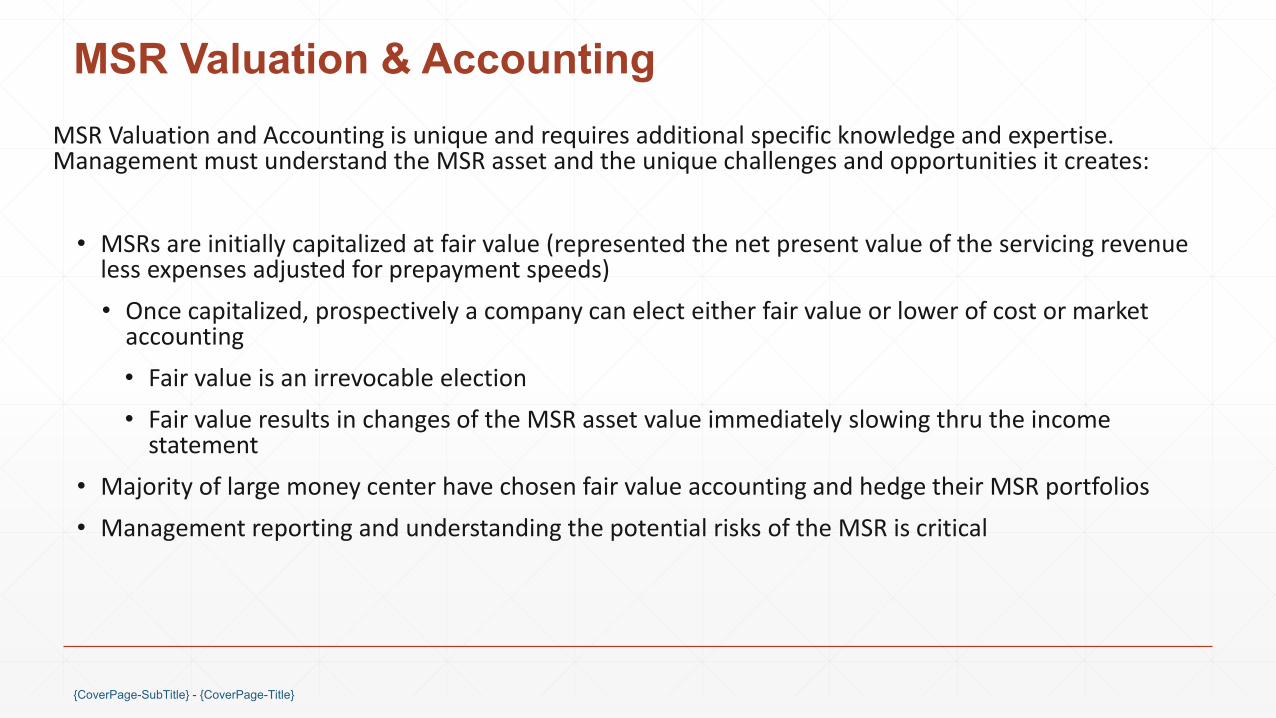

MSR Valuation amp AccountingMSR Valuation and Accounting is unique and requires additional specific knowledge and expertise Management must understand the MSR asset and the unique challenges and opportunities it creates

bull MSRs are initially capitalized at fair value (represented the net present value of the servicing revenue less expenses adjusted for prepayment speeds)

bull Once capitalized prospectively a company can elect either fair value or lower of cost or market accounting

bull Fair value is an irrevocable election

bull Fair value results in changes of the MSR asset value immediately slowing thru the income statement

bull Majority of large money center have chosen fair value accounting and hedge their MSR portfolios

bull Management reporting and understanding the potential risks of the MSR is critical

CoverPage-SubTitle - CoverPage-Title

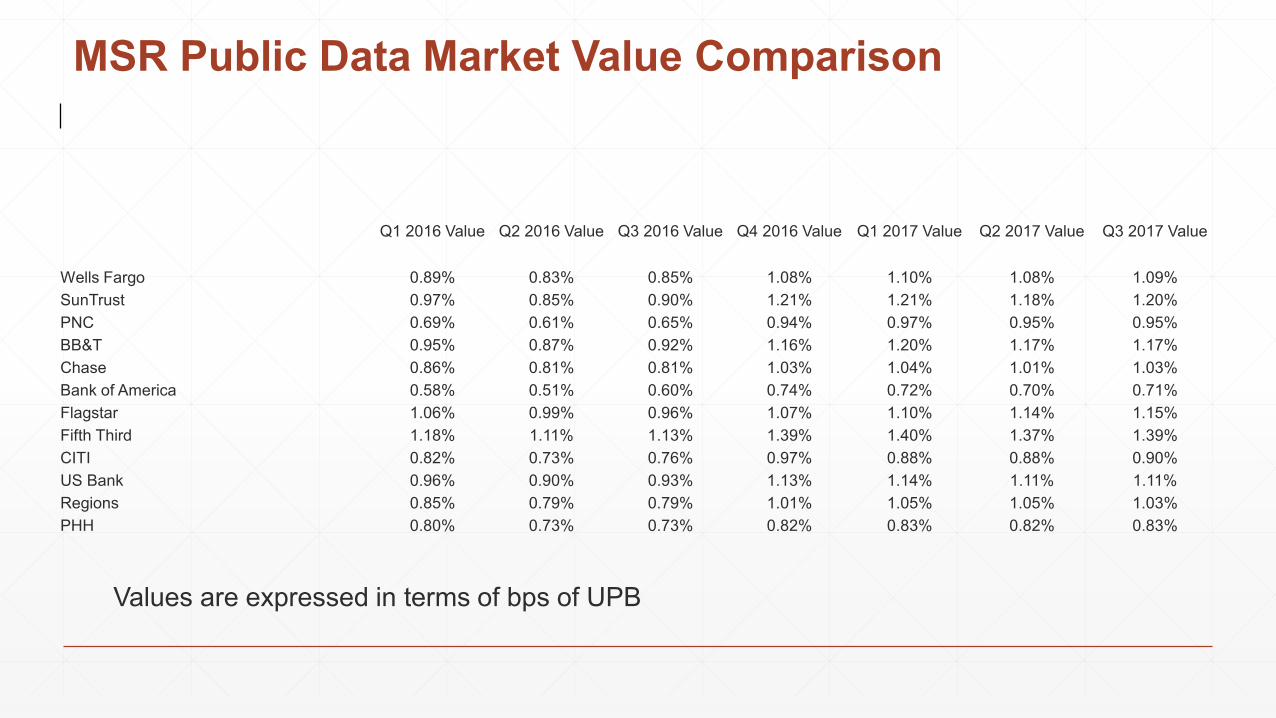

MSR Public Data Market Value Comparison

Q1 2016 Value Q2 2016 Value Q3 2016 Value Q4 2016 Value Q1 2017 Value Q2 2017 Value Q3 2017 Value

Wells Fargo 089 083 085 108 110 108 109SunTrust 097 085 090 121 121 118 120PNC 069 061 065 094 097 095 095BBampT 095 087 092 116 120 117 117Chase 086 081 081 103 104 101 103Bank of America 058 051 060 074 072 070 071Flagstar 106 099 096 107 110 114 115Fifth Third 118 111 113 139 140 137 139CITI 082 073 076 097 088 088 090US Bank 096 090 093 113 114 111 111Regions 085 079 079 101 105 105 103PHH 080 073 073 082 083 082 083

Values are expressed in terms of bps of UPB

Cash and Non Cash Elements of ServicingThe MSR asset in unique in that contains a number of cash and non cash elements that impact the financial statement

bull Initial capitalization (non cash)

bull Changes in MSR values (under fair value) (non cash)

bull Impairment (under LOCOM) (non cash)

bull Amortization expense (LOCOM) (non cash)

bull Actual servicing fee revenue earned cash

bull Actual late fee ancillary earned cash

bull Credit for escrows often internal credit non cash

bull Actual servicing expenses cash

bull Servicing Advances cash

bull Taxes are paid based on the cash received (less any expenses)

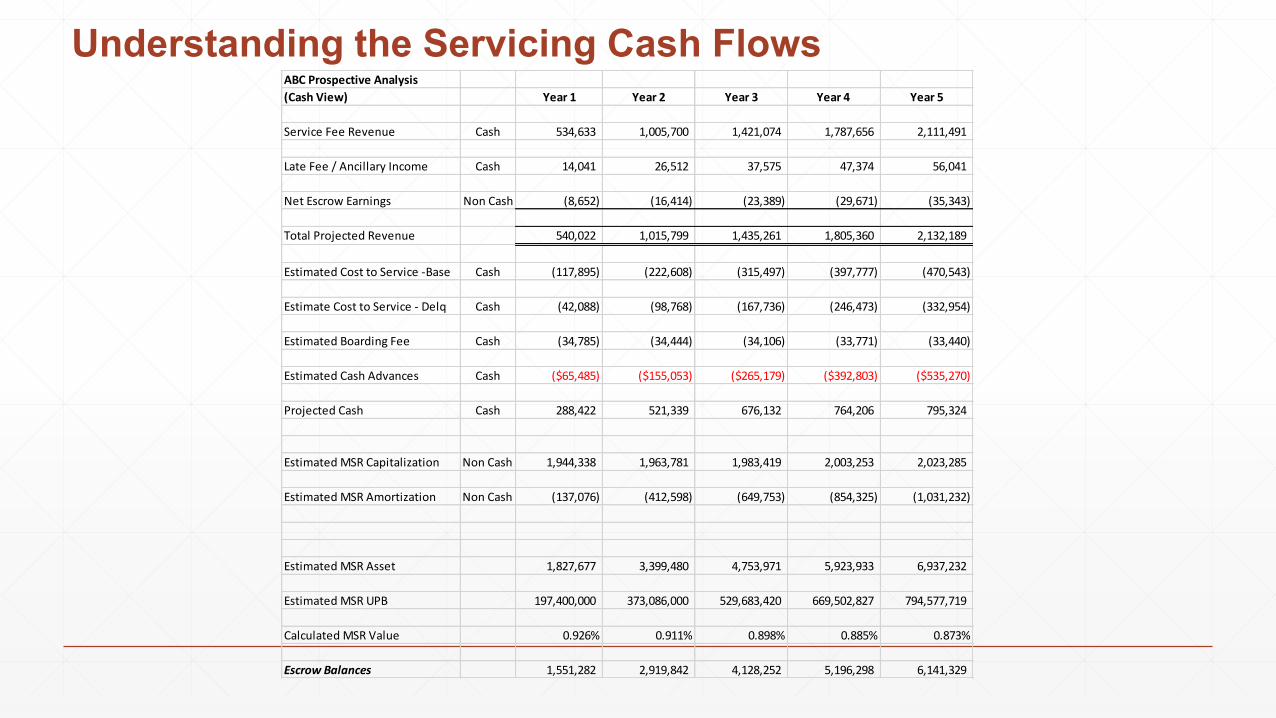

Understanding the Servicing Cash FlowsABC Prospective Analysis

(Cash View) Year 1 Year 2 Year 3 Year 4 Year 5

Service Fee Revenue Cash 534633 1005700 1421074 1787656 2111491

Late Fee Ancillary Income Cash 14041 26512 37575 47374 56041

Net Escrow Earnings Non Cash (8652) (16414) (23389) (29671) (35343)

Total Projected Revenue 540022 1015799 1435261 1805360 2132189

Estimated Cost to Service -Base Cash (117895) (222608) (315497) (397777) (470543)

Estimate Cost to Service - Delq Cash (42088) (98768) (167736) (246473) (332954)

Estimated Boarding Fee Cash (34785) (34444) (34106) (33771) (33440)

Estimated Cash Advances Cash ($65485) ($155053) ($265179) ($392803) ($535270)

Projected Cash Cash 288422 521339 676132 764206 795324

Estimated MSR Capitalization Non Cash 1944338 1963781 1983419 2003253 2023285

Estimated MSR Amortization Non Cash (137076) (412598) (649753) (854325) (1031232)

Estimated MSR Asset 1827677 3399480 4753971 5923933 6937232

Estimated MSR UPB 197400000 373086000 529683420 669502827 794577719

Calculated MSR Value 0926 0911 0898 0885 0873

Escrow Balances 1551282 2919842 4128252 5196298 6141329

Cash and Capital RequirementsThe decision to retain servicing requires the entity to maintain certain capital (cash) and also defers the immediate ability to turn the servicing into cash

bull FHFA has established minimum capital requirements that must be maintained

bull Portfolios will a high level of delinquencies are subject to maintain additional capital

bull Banks are subject to the capital requirement established by BASEL III

bull Changes to the BASEL III limits are in process of being finalized

bull Non Banks must evaluate the amount of their net worth that is tied up in the MSR asset

bull Warehouse lenders and mortgage guarantors monitor the MSR to net worth calculation

MSR Market

The MSR market is made up two distinct types of transactions

bull Co ndash Issue

bull Entering into a relationship with an MSR buyer to sell future production

bull Complex grid based approach

bull Originator often does not collect any payments and sells the MSR as soon as the loan is sold to guarantor (Fannie Freddie or GNMA)

bull Bulk

bull Servicing operational function is performed for a period of time (could be performed by a subservicer)

bull Servicing data is known at time of marketing selling bulk

bull MSR transactions take time to complete (often 90 days)

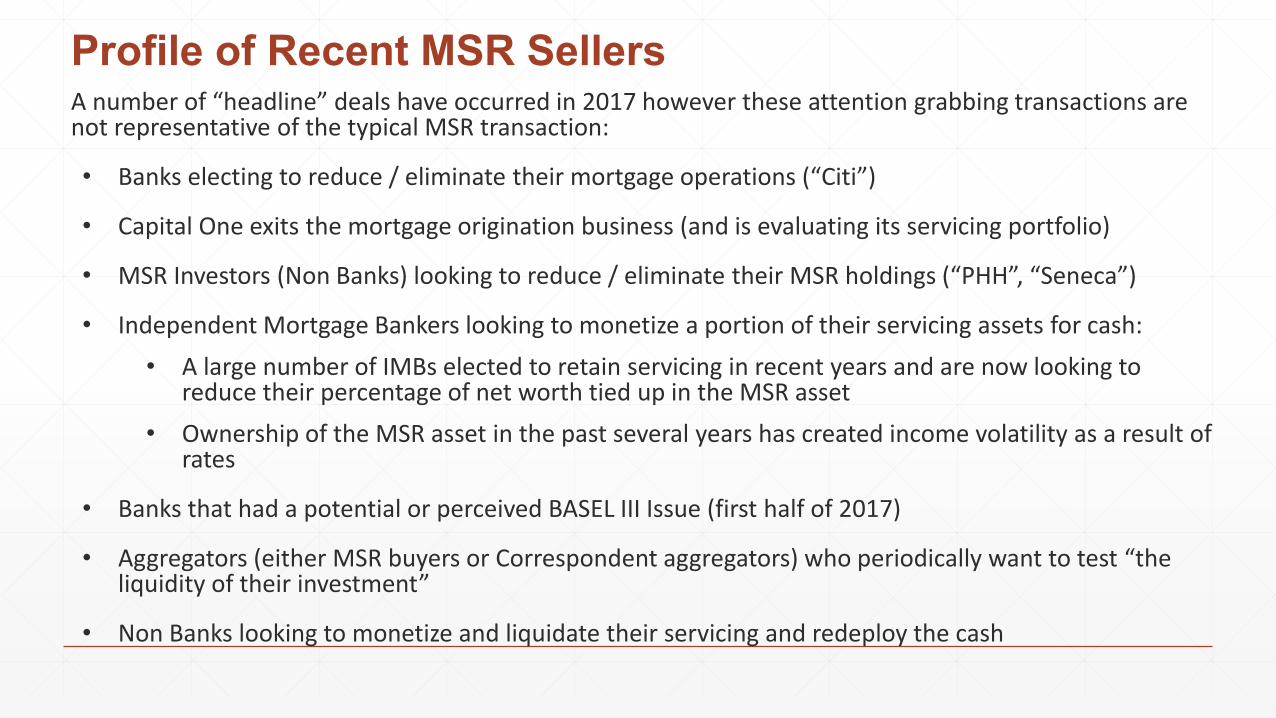

Profile of Recent MSR SellersA number of ldquoheadlinerdquo deals have occurred in 2017 however these attention grabbing transactions are not representative of the typical MSR transaction

bull Banks electing to reduce eliminate their mortgage operations (ldquoCitirdquo)

bull Capital One exits the mortgage origination business (and is evaluating its servicing portfolio)

bull MSR Investors (Non Banks) looking to reduce eliminate their MSR holdings (ldquoPHHrdquo ldquoSenecardquo)

bull Independent Mortgage Bankers looking to monetize a portion of their servicing assets for cash

bull A large number of IMBs elected to retain servicing in recent years and are now looking to reduce their percentage of net worth tied up in the MSR asset

bull Ownership of the MSR asset in the past several years has created income volatility as a result of rates

bull Banks that had a potential or perceived BASEL III Issue (first half of 2017)

bull Aggregators (either MSR buyers or Correspondent aggregators) who periodically want to test ldquothe liquidity of their investmentrdquo

bull Non Banks looking to monetize and liquidate their servicing and redeploy the cash

57

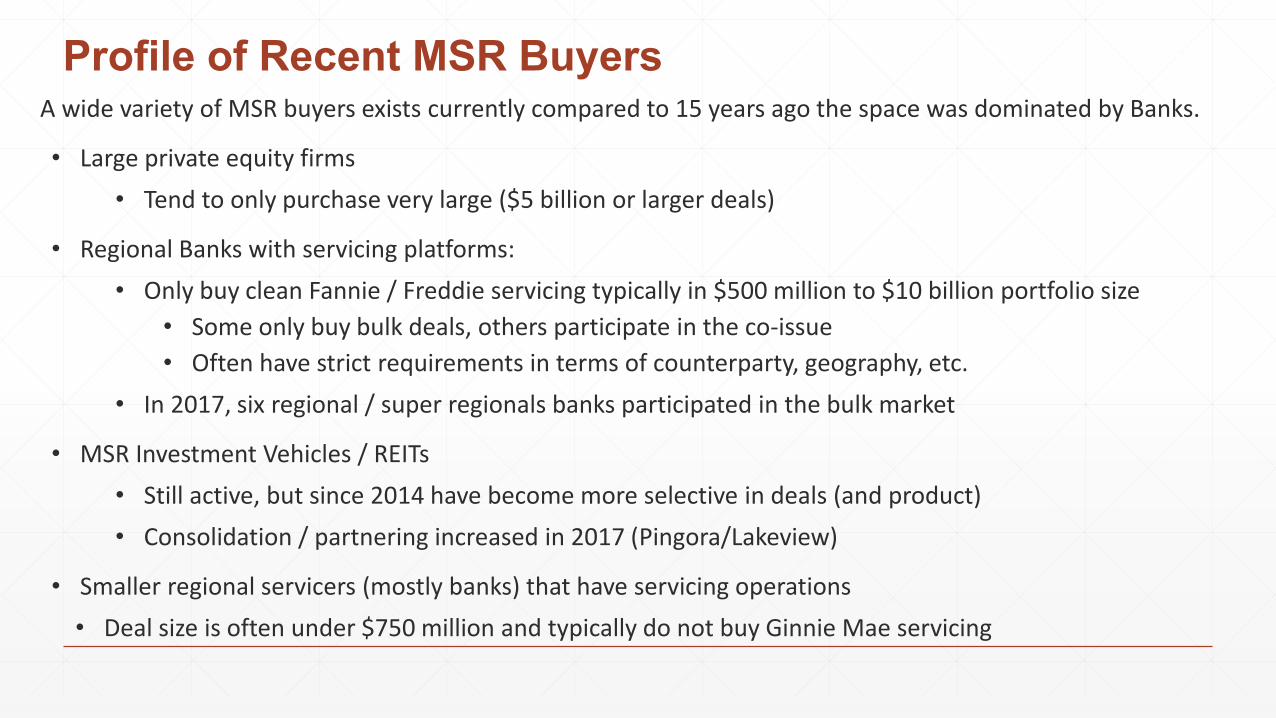

Profile of Recent MSR BuyersA wide variety of MSR buyers exists currently compared to 15 years ago the space was dominated by Banks

bull Large private equity firms

bull Tend to only purchase very large ($5 billion or larger deals)

bull Regional Banks with servicing platforms

bull Only buy clean Fannie Freddie servicing typically in $500 million to $10 billion portfolio size

bull Some only buy bulk deals others participate in the co-issue

bull Often have strict requirements in terms of counterparty geography etc

bull In 2017 six regional super regionals banks participated in the bulk market

bull MSR Investment Vehicles REITs

bull Still active but since 2014 have become more selective in deals (and product)

bull Consolidation partnering increased in 2017 (PingoraLakeview)

bull Smaller regional servicers (mostly banks) that have servicing operations

bull Deal size is often under $750 million and typically do not buy Ginnie Mae servicing

58

Contact Info

Rhonda Beck CMBMCT Trading

rbeckmctradenet

Nitin DaveResMac

NitinDaveresmaccom

Art SchultzFannie Mae

arthur_p_Schultzfanniemaecom

Seth Sprague CMBPhoenix Capital Inc

sspraguephnxcapcom

Overviewbull

bull Loan Production

bull Warehousing QC Delivery

bull Secondary Marketing

bull Loan Administration (Servicing)

Source School of Mortgage Banking I - Introduction to Mortgage Banking

Loan Production

252018 Private and Confidential

3

What Is Mortgage Lending The Higher Purpose

bull Homeownership is an integral part of the American Dream

bull

bull Dedicated mortgage lending professionals take their role in helping people realize that dream seriously and take pride in it

bull

bull Homeownership helps people local communities and the economy to thrive Mortgage lending plays a key role

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Mortgage Banking Functions

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Loan Production

bull Focus is on the borrower (and the borrower experience)

bull Heavily regulated

bullbull Federal or state agencies responsible for control and supervision of a particular

activity or area of public interest

bull Objective is a mortgage loan ldquoproductrdquo comprised of 2 valuable saleable assets

bullbull Stream of loan payments

bull Mortgage servicing rights

School of Mortgage Banking I - Introduction to Mortgage Banking

Top Originators (From Thompson Reuters) Originators Ginnie Mae Fannie Mae Freddie Mac Total

Wells Fargo Bank National Association 36024564000 84005851852 51760538256 171790954108

Quicken Loans Inc 20600239000 36053400509 19064353763 75717993272

PennyMac Loan Services LLC 45855782000 19338747881 3414041118 68608570999

JPMorgan Chase Bank National Association 7857414000 28163462130 29402749899 65423626029

Freedom Mortgage Corporation 33338994000 4910423397 1008175485 39257592882

Caliber Home Loans Inc 15510319000 6212634028 16059138106 37782091134

US Bank National Association 12193242000 8447453440 15119009813 35759705253

AmeriHome Mortgage Company LLC 13055377000 7912593554 12677208733 33645179287

loanDepotcom LLC 13566570000 7669014995 9509517483 30745102478

Flagstar Bank FSB 10944921000 10949326493 6943498453 28837745946

United Shore Financial Services LLC 3860127000 11896295695 8920294146 24676716841

SunTrust Mortgage Inc subsidiary of SunTrust Bank 3744079000 11377801808 6571923774 21693804582

Nationstar Mortgage LLC 6724859000 7310059840 5398272040 19433190880

Fairway Independent Mortgage Corporation 5784760000 5594808854 5202219841 16581788695

Ditech Financial LLC 6654075000 8073626482 1522232674 16249934156

Stearns Lending LLC 5885020000 5035557869 4645940024 15566517893

Bank of America NA 2025960000 5875435792 7324595906 15225991698

USAA Federal Savings Bank 9950190000 3371072914 1709263353 15030526267

Lakeview Loan Servicing LLC 10706183000 3727496202 568033084 15001712286

Franklin American Mortgage Company 4248963000 6489281164 3653693321 14391937485

Guild Mortgage Company 5079472000 4796968574 3172050274 13048490848

Branch Banking and Trust Company (BBampT) 2679654000 1801949957 7476128158 11957732115

Pacific Union Financial LLC 9691974000 743627238 1456437423 11892038661

HomeBridge Financial Services Inc 5573136000 4729311363 992994980 11295442343

Finance of America Mortgage LLC A Blackstone Company 2807288000 4452299631 3936935161 11196522792

Source Thompson Reuters YTD to 2017

Origination Players

School of Mortgage Banking I - Introduction to Mortgage Banking

Four Major Phases of Loan Production

School of Mortgage Banking I - Introduction to Mortgage Banking

Where does the money come from

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Two Assets

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Consumer Protection

Careers in Residential Mortgage Lending - Loan ProductionSource School of Mortgage Banking I - Introduction to Mortgage Banking

Understanding Your BusinessCompanies must focus their origination efforts on products that fit best within their business model

bull Conventional Lending

bull Traditional Agency

bull Specialty Products

bull Government Lending

bull FHA VA USDA FHA Streamline VA IRRRL loans

bull Non-Conforming (True Jumbo)

bull Are you in an area that requires you to offer True Jumbo to remain competitive

bull Non QM

Warehousing QC and Delivery

252018 Private and Confidential

14

Pre Funding QC Evaluation of all origination channels while targeting specific risk concerns such as incomplete

documents income calculations etc

Validating AUS data integrity employment MI SS numbers assets and appraisal review

Re-underwrite components including calculation of income assets and liabilities

Reviewing loan file against investor and agency guidelines

Reviewing all initial disclosures (GFE TIL STD etc)

Identifying trends especially at the channel level will improve overall loan quality and help identify sub-standard partners or staff

Post Funding QCbull Review of all collateral documents to ensure existence and completeness

bull Re-calculation of income

bull Verification of assets and liability

bull Re-verification of critical information to the AUS data integrity including borrowerco-borrower income employment property type assets SSN address loan terms etc

bull Compliance review

bull Review of appraisal

bull Review of credit reports

bull Summary report highlighting all critical exceptions including current and historical trending

Core processes can be customized to dive deeper into income taxes credit or compliance

The Aggregators

As a mortgage originator there are numerous options where mortgage loans can be sold

bull Over 100 aggregators with multiple deliver options

bull Depository Institutions

bull Examples include ndash Wells Fargo JP Morgan Chase BBampT etc

bull Non-Depository Institutions

bull Examples include ndash Pennymac Amerihome Freedom Mortgage etc

bull The Agencies

bull Fannie Mae Freddie Mac and Ginnie Mae

Choosing the ldquoRightrdquo Aggregators

Numerous options exist to deliver loans choosing the right combination of Aggregators is critical

bull Evaluate an Aggregatorrsquos product offering and pricing

bull Align their product suite with your origination needs

bull Compare pricing across aggregators

bull Compare delivery requirements

bull Review approval requirements

bull Each aggregator has their own set of requirements

bull Net worth warehouse providers policies and procedures etc

Defining Best ExecutionAs a mortgage company matures from Best Efforts to Mandatory Deliveries the profit (and risks change)

bull Best Efforts Delivery

bull LenderOriginator has no financial responsibility to the investoraggregator

bull Mandatory Delivery

bull LenderOriginator is required to deliver committed loans to investoraggregator

bull Failure to deliver usually requires the LenderOriginator to pay for any market costs incurred by the investoraggregator

bull Certainty of Delivery

bull LenderOriginator incurs more responsibility in a Mandatory commitment

bull InvestorAggregator no longer incurs any hedge costs from pull through fluctuations

bull InvestorAggregators pay substantial premium for this certainty

bull Historically there is a 35 basis point premium paid for Mandatory delivery

Best Efforts Deliveries

Most mortgage companies begin their secondary life cycle by delivering closed loans to investors on a best efforts basis (selling servicing released)

bull Established warehouse lines of credit to close in-house

bull Managing warehouse lines of credit

bull Net worth and cash flow

bull Moved underwriting in-house

bull Pros and Cons

bull Overlays

bull Pricing

252018Private and Confidential 20

MBA Quarterly Performance Report

Q3 2017 Q2 2017 Q1 2017 Q4 2016 Q3 2016

Average Production Volume $569 million $526 million $455 million $690 million $764 million

Average Production Profit 40 bps 46 bps 10 bps 24 bps 74 bps

Purchase Share Estimate 74 76 68 58 60

Average Loan Size 251109 248619 242949 246473 251398

Average Loan Production Expense $8060 $8896 $8887 $7562 $6969

Personnel expenses (per loan) $5279 $5119 $5802 $5001 $4675

All business lines Profitability 77 86 67 73 94

Total Production Revenue $8990 $8896 $9111 $8137 $8742

(fee income warehouse spread net secondary income)

Source MBArsquos Quarterly Performance Report (for IMBs and subs of banks)

Net cost to originate includes all production expenses and commissions minus all fee income but excludes the secondary

marketing gains MSR or SRP value and warehouse interest margin

Secondary Marketing

252018 Private and Confidential

22

Flow of Money Primary and Secondary Markets

School of Mortgage Banking I - Introduction to Mortgage Banking

Secondary Marketing Overview

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Secondary Market Players

School of Mortgage Banking I - Introduction to Mortgage Banking

Minimum Requirements for Hedging

In order to move from Best Efforts Delivery to Mandatory a number of key milestones must be achieved including

bull Centralized Lock Desk

bull Reliable and continuously updated pipeline data

bull Mandatory Approvals

bull Investors

bull Warehouse Providers

bull BrokerDealers

bull $15mm - $25mm+ company net worth

bull Approximately $10+ millionmonth in agency eligible saleable production

Lender Approval Requirementsbull Financial Requirements

bull Minimum Adjusted Net Worth of $25 million plus a dollar amount that represents 025 of the UPB of the sellerservicerrsquos total portfolio of mortgage loans serviced

bull History of profitability

bull Minimum acceptable levels of capital

bull Sellerservicers that are depository institutions must meet the minimum regulatory capital requirements to be considered as ldquowell capitalizedrdquo by primary regulator

bull All other entities must have minimum Lender Adjusted Net WorthTotal Assets ratio of 6 or equivalent

bull Non-depository sellersservicers must maintain minimum liquidity requirements based on the Agency Serious Delinquency Rate (ldquoSDQrdquo)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

bull Other Eligibility Criteria

bull State Licensing

bull Funding Capability (warehouse lines)

bull Delegate underwriting authority

bull Procedures for managing appraisals closing agents third party originations

bull Quality Control

bull ServicingSubservicing

Lender Approval Requirements (continued)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Interest Rate Risk

bull Definition

bull The risk that an investmentrsquos value will change due to a change in the absolute level of interest rates

bull Tools to hedge

bull Best Efforts Committing

bull Mandatory Committing

bull Hedging with TBAs

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Fannie Mae Mandatory vs Best Efforts

Pricing amp Execution Discussion

Fannie Mae Capital Markets Desks

bull Pricing amp Sales Desk

bull Single point of contact for lenders for all things execution

bull Whole Loan Conduit

bull Manage whole loan pricing hedging amp pooling

bull MBS Trading Desk

bull Manage lender hedge and specified pool flows

bull Investor Sales Desk

bull Manage investor relationships

bull Early Funding Desk

bull Manage early funding process (ASAP amp ASAP+)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

MBS vs Whole Loan Comparison

ExecutionElement

Whole Loan Execution MBS Execution

Pricing

Whole loan pricing is considered ldquoliverdquo and moves throughout the day in line with the MBS market Commitments are taken on our industry-leading platform PE ndash Whole Loantrade

Based on live MBS market All-in price is determined by current MBS market as well as gfee and any buy-upbuy-down components MBS trades with the Capital Markets Pricing amp Sales Desk are executed over the phone

Execution Type Mandatory or best efforts options available Mandatory only

Hedging

Whole loan commitments are generally a good hedging vehicle for lenders who intend to deliver to Fannie Mae using a whole loan execution When circumstances arise and a contract cannot be fulfilled depending on initial commitment and current market pricing whole loan commitments allow for cash-back on pair-offs

MBS is a liquid hedging tool and is also utilized for cross-hedging other mortgage products or whole loan deliveries Depending on initial trade and current trade pricing MBS allow for cash-back on pair-offs Forward-settling MBS trades may be subject to bilateral margin calls

PE-Whole Loan Specified Pricing Grids

bull 30-Year Fixed Rate ndash 200k Max Loan Amount

bull 30-Year Fixed Rate ndash 175k Max Loan Amount

bull 30-Year Fixed Rate ndash 150k Max Loan Amount

bull 30-Year Fixed Rate ndash 125k Max Loan Amount

bull 30-Year Fixed Rate ndash 110k Max Loan Amount

bull 30-Year Fixed Rate ndash 85k Max Loan Amount

bull 30-Year Fixed Rate ndash New York

bull 30-Year Fixed Rate ndash Investment Property

bull 30-Year Fixed Rate (standard)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Service Released Versus Retained

Retaining servicing provide the MSR owner the ability to create an annuity stream of income that can be used to offset expenses elsewhere MSRs are an asset class that increases in value generates additional revenue in a rising rate environment

bull Servicing is fee income (expressed in bps) on the outstanding principal balance

bull Potential ability to earn ancillary income (or cross ndashsell) retain customers

bull Ability to generate deposits (if a bank)

bull Gives up getting cash immediately but does defer paying taxes

Fannie Mae Servicing MarketplaceWhat is it

bull A new platform that supports co-issue sales transactions

bull All loans delivered will have the selling and servicing repwarrants bifurcated ndash selling repswarrants stay with the seller

bull Bifurcation eligibility minimum net worth of $25 million plus the greater of 25bps of servicing UPB or 25bps of bifurcated deliveries for the past 3 years

bull Brings sellers and servicers together to deliver pricing certainty transparency and operating efficiency

How does it workbull Sellers access Servicing Marketplace via PE-Whole Loan where they initiate servicer relationship

activities

bull Sellers work with the servicer to negotiatefinalize pricing loan data delivery requirements and agreements before they begin transactions

bull Once a servicer accepts the relationship the seller has access to the servicerrsquos SRP schedule (also available via API) and can take down co-issue commitments via PE-Whole Loan with their associated servicer(s)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Fannie Mae Servicing Marketplace

Benefits to Customers

bull Supports sellers in their search for co-issue servicing partners

bull Standardizes data exchange and delivery process to improve efficiency for sellers and servicers

bull Helps sellers improve the their overall liquidity of their loan and servicing rights

Timing

bull Currently in production with four servicers (ArvestCentral Mortgage CMC Funding RoundPointServicing and Two Harbors) and seven sellers

bull Managing a staged rollout and onboarding process beginning with sellers that have existing relationships with the SMP servicers

bull New sellers have the ability to request new partnerships with active servicers which begins the process of negotiating the servicer relationship

bull Introducing additional servicers and capabilities (ie all-in funding) throughout 2018

Insert Presentation Title Here

Pricing amp Execution Whole Loan (PE-Whole Loan)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Single SecurityDescription

bull The Single Security is an MBS with common features and disclosures issued and guaranteed by Fannie Mae or Freddie Mac

bull Products in scope are fixed-rate 30-year 20-year 15-year and 10-year securities

bull The Single Security will be called the ldquoUniform MBSrdquo or ldquoUMBSrdquo

Purpose

bull Strengthen the US mortgage market

bull Reduce the trading value disparities between Fannie Mae and Freddie Mac securities

bull Maintain TBA eligibility

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Single SecurityDetails

bull Features of the Single Security will be based generally on Fannie Mae MBS

bull Fannie Mae MBS will be fungible with the new Single Security

bull Freddie Mac is creating a mechanism to allow investors to exchange legacy PCs for Single Securities

bull The guarantor of the Single Security will be the issuing Enterprise

bull Both Fannie Mae amp Freddie Mac issued Single Securities will be TBA eligible

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Single SecurityHow will it affect you

bull The single security is expected to be issued in Q2 2019 when both Fannie Mae and Freddie Mac are on the Common Securitization Platform (CSP)

bull The CSP will act as agent for the issuance bond administration and disclosures for all newly-issued single securities

bull Lenders will continue to interact with Fannie Mae and will not interact with the CSP

bull All servicer interaction will continue to occur directly with Fannie Mae

bull Single security will not cause changes to DU eligibility requirements

bull Fannie Mae will not be making any changes to our SellerServicer guide in response to single security

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Responding to the Market Dynamic solutions to bring process efficiency and Day 1 Certaintytrade

Day 1 Certaintytrade

Industry Status QuoPaper-intensive Inefficient ProtractedBorrowers and lenders suffer from amultitude of pain points brought on bytraditional paper-based processes

Fannie Maersquos VisionStreamlined Efficient DynamicBy leveraging borrower and property data applying advanced analytics and bringing key quality control processes up front Fannie Mae is helping lenders transform their business

Wersquore introducing capabilities that address lender feedback by driving greater transparency and a more streamlined mortgage origination process

The result Day 1 Certainty

DU Validation Service Desktop Underwriterreg (DUreg) now gives lenders even more power by providing

optional validation of borrower data for income assets and employment

Day 1 Certaintytrade

Property Inspection Waiver

DU offers to waive the appraisal for eligible transactions

Day 1 Certaintytrade

Certainty on Appraised Value

Harnessing the power of Collateral Underwriterreg (CUtrade) Fannie Mae will offer freedom from representations and warranties related to the property value for eligible loan casefiles

Day 1 Certaintytrade

Submit an appraisal through the Uniform

Collateral Data Portalreg

Get real-time feedback from CU

With a CU risk score of 25 or lower the

appraisal is eligible for freedom from reps and warrants on property

value

Loan Administration Servicing

252018 Private and Confidential

46

Tax Reform Bill 2017

The House and Senate passed HR1 the Tax Cuts and Jobs Act and the President signed the bill into legislation right before the Holiday Break (effective for the 2018 tax year)

bull Change in Corporate Tax Rate from 35 to 21

bull Will impact the ldquoCrdquo Corp Bank as the MSR asset is net of the deferred tax liability for BASEL III the lower the tax rate the more than the MSR asset counts toward BASEL III limits

bull A cap on the Interest Deduction (ldquoMIDrdquo)

bull Maintains the mortgage interest deduction for existing mortgages but limits deduction to $750K on mortgages made after December 15th 2017

bull Debt on first and second under $750K but suspends deductibility of home equity lines

bull State and Local tax deductions (ldquoSALTrdquo) allows up to $10000 in state and local tax deductions

bull Maintained current tax treatment for MSRs

bull Preserved the Capital gains treatment for home sales allowing homeowners ability to exclude up to $500K on gain on sale of primary residence

47

BASEL III Update Today [November 21 2017] the Federal banking regulators finalized the pause on Basel III implementation to allow banks that are not subject to Basel IIIs advanced approaches to extend the current regulatory capital treatment of mortgage servicing assets (MSAs) Advanced approaches banking organizations (those with over $250 billion in assets or more than $10 billion in foreign exposure) are required to apply the capital rulesrsquo fully phased-in treatment for these capital items beginning January 1 2018

For example the transitions NPR [now finalized] would require a non-advanced approaches banking organization with an amount of MSAs above the 10 percent common equity tier 1 capital deduction threshold in the capital rules to deduct from common equity tier 1 capital 80 percent of the amount of MSAs above this threshold and to apply a 100 percent risk weight to the MSAs that are not deducted from common equity tier 1 capital including the MSAs that otherwise would be deducted but for the transition provisions

48

Source MBA Loan Administration Email 11212017

Loan Servicing Overview

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Subservicing versus Servicing in house

Subservicing model

bull Immediate access to experienced servicing operations

bull Outsources maintenance and compliance

bull Per unit based fee structure along with specific activity based fees including boarding and de-boarding

bull Borrower experience (communication) is being done by a vendor

bull Oversight and management of the sub-servicer is still required

In House Servicing

bull Requires scale to obtain any efficiencies

bull Requires hiring and maintaining staff along with the on-going compliance

bull Greater ability to control costs if efficiencies and scale is achieved and maintained

bull Borrower experience is controlled and often results in great ability to maintain the relationship (higher cross sell and retention)

bull Full control of late fees and escrows

CoverPage-SubTitle - CoverPage-Title

MSR Valuation amp AccountingMSR Valuation and Accounting is unique and requires additional specific knowledge and expertise Management must understand the MSR asset and the unique challenges and opportunities it creates

bull MSRs are initially capitalized at fair value (represented the net present value of the servicing revenue less expenses adjusted for prepayment speeds)

bull Once capitalized prospectively a company can elect either fair value or lower of cost or market accounting

bull Fair value is an irrevocable election

bull Fair value results in changes of the MSR asset value immediately slowing thru the income statement

bull Majority of large money center have chosen fair value accounting and hedge their MSR portfolios

bull Management reporting and understanding the potential risks of the MSR is critical

CoverPage-SubTitle - CoverPage-Title

MSR Public Data Market Value Comparison

Q1 2016 Value Q2 2016 Value Q3 2016 Value Q4 2016 Value Q1 2017 Value Q2 2017 Value Q3 2017 Value

Wells Fargo 089 083 085 108 110 108 109SunTrust 097 085 090 121 121 118 120PNC 069 061 065 094 097 095 095BBampT 095 087 092 116 120 117 117Chase 086 081 081 103 104 101 103Bank of America 058 051 060 074 072 070 071Flagstar 106 099 096 107 110 114 115Fifth Third 118 111 113 139 140 137 139CITI 082 073 076 097 088 088 090US Bank 096 090 093 113 114 111 111Regions 085 079 079 101 105 105 103PHH 080 073 073 082 083 082 083

Values are expressed in terms of bps of UPB

Cash and Non Cash Elements of ServicingThe MSR asset in unique in that contains a number of cash and non cash elements that impact the financial statement

bull Initial capitalization (non cash)

bull Changes in MSR values (under fair value) (non cash)

bull Impairment (under LOCOM) (non cash)

bull Amortization expense (LOCOM) (non cash)

bull Actual servicing fee revenue earned cash

bull Actual late fee ancillary earned cash

bull Credit for escrows often internal credit non cash

bull Actual servicing expenses cash

bull Servicing Advances cash

bull Taxes are paid based on the cash received (less any expenses)

Understanding the Servicing Cash FlowsABC Prospective Analysis

(Cash View) Year 1 Year 2 Year 3 Year 4 Year 5

Service Fee Revenue Cash 534633 1005700 1421074 1787656 2111491

Late Fee Ancillary Income Cash 14041 26512 37575 47374 56041

Net Escrow Earnings Non Cash (8652) (16414) (23389) (29671) (35343)

Total Projected Revenue 540022 1015799 1435261 1805360 2132189

Estimated Cost to Service -Base Cash (117895) (222608) (315497) (397777) (470543)

Estimate Cost to Service - Delq Cash (42088) (98768) (167736) (246473) (332954)

Estimated Boarding Fee Cash (34785) (34444) (34106) (33771) (33440)

Estimated Cash Advances Cash ($65485) ($155053) ($265179) ($392803) ($535270)

Projected Cash Cash 288422 521339 676132 764206 795324

Estimated MSR Capitalization Non Cash 1944338 1963781 1983419 2003253 2023285

Estimated MSR Amortization Non Cash (137076) (412598) (649753) (854325) (1031232)

Estimated MSR Asset 1827677 3399480 4753971 5923933 6937232

Estimated MSR UPB 197400000 373086000 529683420 669502827 794577719

Calculated MSR Value 0926 0911 0898 0885 0873

Escrow Balances 1551282 2919842 4128252 5196298 6141329

Cash and Capital RequirementsThe decision to retain servicing requires the entity to maintain certain capital (cash) and also defers the immediate ability to turn the servicing into cash

bull FHFA has established minimum capital requirements that must be maintained

bull Portfolios will a high level of delinquencies are subject to maintain additional capital

bull Banks are subject to the capital requirement established by BASEL III

bull Changes to the BASEL III limits are in process of being finalized

bull Non Banks must evaluate the amount of their net worth that is tied up in the MSR asset

bull Warehouse lenders and mortgage guarantors monitor the MSR to net worth calculation

MSR Market

The MSR market is made up two distinct types of transactions

bull Co ndash Issue

bull Entering into a relationship with an MSR buyer to sell future production

bull Complex grid based approach

bull Originator often does not collect any payments and sells the MSR as soon as the loan is sold to guarantor (Fannie Freddie or GNMA)

bull Bulk

bull Servicing operational function is performed for a period of time (could be performed by a subservicer)

bull Servicing data is known at time of marketing selling bulk

bull MSR transactions take time to complete (often 90 days)

Profile of Recent MSR SellersA number of ldquoheadlinerdquo deals have occurred in 2017 however these attention grabbing transactions are not representative of the typical MSR transaction

bull Banks electing to reduce eliminate their mortgage operations (ldquoCitirdquo)

bull Capital One exits the mortgage origination business (and is evaluating its servicing portfolio)

bull MSR Investors (Non Banks) looking to reduce eliminate their MSR holdings (ldquoPHHrdquo ldquoSenecardquo)

bull Independent Mortgage Bankers looking to monetize a portion of their servicing assets for cash

bull A large number of IMBs elected to retain servicing in recent years and are now looking to reduce their percentage of net worth tied up in the MSR asset

bull Ownership of the MSR asset in the past several years has created income volatility as a result of rates

bull Banks that had a potential or perceived BASEL III Issue (first half of 2017)

bull Aggregators (either MSR buyers or Correspondent aggregators) who periodically want to test ldquothe liquidity of their investmentrdquo

bull Non Banks looking to monetize and liquidate their servicing and redeploy the cash

57

Profile of Recent MSR BuyersA wide variety of MSR buyers exists currently compared to 15 years ago the space was dominated by Banks

bull Large private equity firms

bull Tend to only purchase very large ($5 billion or larger deals)

bull Regional Banks with servicing platforms

bull Only buy clean Fannie Freddie servicing typically in $500 million to $10 billion portfolio size

bull Some only buy bulk deals others participate in the co-issue

bull Often have strict requirements in terms of counterparty geography etc

bull In 2017 six regional super regionals banks participated in the bulk market

bull MSR Investment Vehicles REITs

bull Still active but since 2014 have become more selective in deals (and product)

bull Consolidation partnering increased in 2017 (PingoraLakeview)

bull Smaller regional servicers (mostly banks) that have servicing operations

bull Deal size is often under $750 million and typically do not buy Ginnie Mae servicing

58

Contact Info

Rhonda Beck CMBMCT Trading

rbeckmctradenet

Nitin DaveResMac

NitinDaveresmaccom

Art SchultzFannie Mae

arthur_p_Schultzfanniemaecom

Seth Sprague CMBPhoenix Capital Inc

sspraguephnxcapcom

Loan Production

252018 Private and Confidential

3

What Is Mortgage Lending The Higher Purpose

bull Homeownership is an integral part of the American Dream

bull

bull Dedicated mortgage lending professionals take their role in helping people realize that dream seriously and take pride in it

bull

bull Homeownership helps people local communities and the economy to thrive Mortgage lending plays a key role

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Mortgage Banking Functions

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Loan Production

bull Focus is on the borrower (and the borrower experience)

bull Heavily regulated

bullbull Federal or state agencies responsible for control and supervision of a particular

activity or area of public interest

bull Objective is a mortgage loan ldquoproductrdquo comprised of 2 valuable saleable assets

bullbull Stream of loan payments

bull Mortgage servicing rights

School of Mortgage Banking I - Introduction to Mortgage Banking

Top Originators (From Thompson Reuters) Originators Ginnie Mae Fannie Mae Freddie Mac Total

Wells Fargo Bank National Association 36024564000 84005851852 51760538256 171790954108

Quicken Loans Inc 20600239000 36053400509 19064353763 75717993272

PennyMac Loan Services LLC 45855782000 19338747881 3414041118 68608570999

JPMorgan Chase Bank National Association 7857414000 28163462130 29402749899 65423626029

Freedom Mortgage Corporation 33338994000 4910423397 1008175485 39257592882

Caliber Home Loans Inc 15510319000 6212634028 16059138106 37782091134

US Bank National Association 12193242000 8447453440 15119009813 35759705253

AmeriHome Mortgage Company LLC 13055377000 7912593554 12677208733 33645179287

loanDepotcom LLC 13566570000 7669014995 9509517483 30745102478

Flagstar Bank FSB 10944921000 10949326493 6943498453 28837745946

United Shore Financial Services LLC 3860127000 11896295695 8920294146 24676716841

SunTrust Mortgage Inc subsidiary of SunTrust Bank 3744079000 11377801808 6571923774 21693804582

Nationstar Mortgage LLC 6724859000 7310059840 5398272040 19433190880

Fairway Independent Mortgage Corporation 5784760000 5594808854 5202219841 16581788695

Ditech Financial LLC 6654075000 8073626482 1522232674 16249934156

Stearns Lending LLC 5885020000 5035557869 4645940024 15566517893

Bank of America NA 2025960000 5875435792 7324595906 15225991698

USAA Federal Savings Bank 9950190000 3371072914 1709263353 15030526267

Lakeview Loan Servicing LLC 10706183000 3727496202 568033084 15001712286

Franklin American Mortgage Company 4248963000 6489281164 3653693321 14391937485

Guild Mortgage Company 5079472000 4796968574 3172050274 13048490848

Branch Banking and Trust Company (BBampT) 2679654000 1801949957 7476128158 11957732115

Pacific Union Financial LLC 9691974000 743627238 1456437423 11892038661

HomeBridge Financial Services Inc 5573136000 4729311363 992994980 11295442343

Finance of America Mortgage LLC A Blackstone Company 2807288000 4452299631 3936935161 11196522792

Source Thompson Reuters YTD to 2017

Origination Players

School of Mortgage Banking I - Introduction to Mortgage Banking

Four Major Phases of Loan Production

School of Mortgage Banking I - Introduction to Mortgage Banking

Where does the money come from

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Two Assets

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Consumer Protection

Careers in Residential Mortgage Lending - Loan ProductionSource School of Mortgage Banking I - Introduction to Mortgage Banking

Understanding Your BusinessCompanies must focus their origination efforts on products that fit best within their business model

bull Conventional Lending

bull Traditional Agency

bull Specialty Products

bull Government Lending

bull FHA VA USDA FHA Streamline VA IRRRL loans

bull Non-Conforming (True Jumbo)

bull Are you in an area that requires you to offer True Jumbo to remain competitive

bull Non QM

Warehousing QC and Delivery

252018 Private and Confidential

14

Pre Funding QC Evaluation of all origination channels while targeting specific risk concerns such as incomplete

documents income calculations etc

Validating AUS data integrity employment MI SS numbers assets and appraisal review

Re-underwrite components including calculation of income assets and liabilities

Reviewing loan file against investor and agency guidelines

Reviewing all initial disclosures (GFE TIL STD etc)

Identifying trends especially at the channel level will improve overall loan quality and help identify sub-standard partners or staff

Post Funding QCbull Review of all collateral documents to ensure existence and completeness

bull Re-calculation of income

bull Verification of assets and liability

bull Re-verification of critical information to the AUS data integrity including borrowerco-borrower income employment property type assets SSN address loan terms etc

bull Compliance review

bull Review of appraisal

bull Review of credit reports

bull Summary report highlighting all critical exceptions including current and historical trending

Core processes can be customized to dive deeper into income taxes credit or compliance

The Aggregators

As a mortgage originator there are numerous options where mortgage loans can be sold

bull Over 100 aggregators with multiple deliver options

bull Depository Institutions

bull Examples include ndash Wells Fargo JP Morgan Chase BBampT etc

bull Non-Depository Institutions

bull Examples include ndash Pennymac Amerihome Freedom Mortgage etc

bull The Agencies

bull Fannie Mae Freddie Mac and Ginnie Mae

Choosing the ldquoRightrdquo Aggregators

Numerous options exist to deliver loans choosing the right combination of Aggregators is critical

bull Evaluate an Aggregatorrsquos product offering and pricing

bull Align their product suite with your origination needs

bull Compare pricing across aggregators

bull Compare delivery requirements

bull Review approval requirements

bull Each aggregator has their own set of requirements

bull Net worth warehouse providers policies and procedures etc

Defining Best ExecutionAs a mortgage company matures from Best Efforts to Mandatory Deliveries the profit (and risks change)

bull Best Efforts Delivery

bull LenderOriginator has no financial responsibility to the investoraggregator

bull Mandatory Delivery

bull LenderOriginator is required to deliver committed loans to investoraggregator

bull Failure to deliver usually requires the LenderOriginator to pay for any market costs incurred by the investoraggregator

bull Certainty of Delivery

bull LenderOriginator incurs more responsibility in a Mandatory commitment

bull InvestorAggregator no longer incurs any hedge costs from pull through fluctuations

bull InvestorAggregators pay substantial premium for this certainty

bull Historically there is a 35 basis point premium paid for Mandatory delivery

Best Efforts Deliveries

Most mortgage companies begin their secondary life cycle by delivering closed loans to investors on a best efforts basis (selling servicing released)

bull Established warehouse lines of credit to close in-house

bull Managing warehouse lines of credit

bull Net worth and cash flow

bull Moved underwriting in-house

bull Pros and Cons

bull Overlays

bull Pricing

252018Private and Confidential 20

MBA Quarterly Performance Report

Q3 2017 Q2 2017 Q1 2017 Q4 2016 Q3 2016

Average Production Volume $569 million $526 million $455 million $690 million $764 million

Average Production Profit 40 bps 46 bps 10 bps 24 bps 74 bps

Purchase Share Estimate 74 76 68 58 60

Average Loan Size 251109 248619 242949 246473 251398

Average Loan Production Expense $8060 $8896 $8887 $7562 $6969

Personnel expenses (per loan) $5279 $5119 $5802 $5001 $4675

All business lines Profitability 77 86 67 73 94

Total Production Revenue $8990 $8896 $9111 $8137 $8742

(fee income warehouse spread net secondary income)

Source MBArsquos Quarterly Performance Report (for IMBs and subs of banks)

Net cost to originate includes all production expenses and commissions minus all fee income but excludes the secondary

marketing gains MSR or SRP value and warehouse interest margin

Secondary Marketing

252018 Private and Confidential

22

Flow of Money Primary and Secondary Markets

School of Mortgage Banking I - Introduction to Mortgage Banking

Secondary Marketing Overview

Careers in Residential Mortgage Lending - Overview of the Residential Mortgage IndustrySource School of Mortgage Banking I - Introduction to Mortgage Banking

Secondary Market Players

School of Mortgage Banking I - Introduction to Mortgage Banking

Minimum Requirements for Hedging

In order to move from Best Efforts Delivery to Mandatory a number of key milestones must be achieved including

bull Centralized Lock Desk

bull Reliable and continuously updated pipeline data

bull Mandatory Approvals

bull Investors

bull Warehouse Providers

bull BrokerDealers

bull $15mm - $25mm+ company net worth

bull Approximately $10+ millionmonth in agency eligible saleable production

Lender Approval Requirementsbull Financial Requirements

bull Minimum Adjusted Net Worth of $25 million plus a dollar amount that represents 025 of the UPB of the sellerservicerrsquos total portfolio of mortgage loans serviced

bull History of profitability

bull Minimum acceptable levels of capital

bull Sellerservicers that are depository institutions must meet the minimum regulatory capital requirements to be considered as ldquowell capitalizedrdquo by primary regulator

bull All other entities must have minimum Lender Adjusted Net WorthTotal Assets ratio of 6 or equivalent

bull Non-depository sellersservicers must maintain minimum liquidity requirements based on the Agency Serious Delinquency Rate (ldquoSDQrdquo)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

bull Other Eligibility Criteria

bull State Licensing

bull Funding Capability (warehouse lines)

bull Delegate underwriting authority

bull Procedures for managing appraisals closing agents third party originations

bull Quality Control

bull ServicingSubservicing

Lender Approval Requirements (continued)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Interest Rate Risk

bull Definition

bull The risk that an investmentrsquos value will change due to a change in the absolute level of interest rates

bull Tools to hedge

bull Best Efforts Committing

bull Mandatory Committing

bull Hedging with TBAs

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Fannie Mae Mandatory vs Best Efforts

Pricing amp Execution Discussion

Fannie Mae Capital Markets Desks

bull Pricing amp Sales Desk

bull Single point of contact for lenders for all things execution

bull Whole Loan Conduit

bull Manage whole loan pricing hedging amp pooling

bull MBS Trading Desk

bull Manage lender hedge and specified pool flows

bull Investor Sales Desk

bull Manage investor relationships

bull Early Funding Desk

bull Manage early funding process (ASAP amp ASAP+)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

MBS vs Whole Loan Comparison

ExecutionElement

Whole Loan Execution MBS Execution

Pricing

Whole loan pricing is considered ldquoliverdquo and moves throughout the day in line with the MBS market Commitments are taken on our industry-leading platform PE ndash Whole Loantrade

Based on live MBS market All-in price is determined by current MBS market as well as gfee and any buy-upbuy-down components MBS trades with the Capital Markets Pricing amp Sales Desk are executed over the phone

Execution Type Mandatory or best efforts options available Mandatory only

Hedging

Whole loan commitments are generally a good hedging vehicle for lenders who intend to deliver to Fannie Mae using a whole loan execution When circumstances arise and a contract cannot be fulfilled depending on initial commitment and current market pricing whole loan commitments allow for cash-back on pair-offs

MBS is a liquid hedging tool and is also utilized for cross-hedging other mortgage products or whole loan deliveries Depending on initial trade and current trade pricing MBS allow for cash-back on pair-offs Forward-settling MBS trades may be subject to bilateral margin calls

PE-Whole Loan Specified Pricing Grids

bull 30-Year Fixed Rate ndash 200k Max Loan Amount

bull 30-Year Fixed Rate ndash 175k Max Loan Amount

bull 30-Year Fixed Rate ndash 150k Max Loan Amount

bull 30-Year Fixed Rate ndash 125k Max Loan Amount

bull 30-Year Fixed Rate ndash 110k Max Loan Amount

bull 30-Year Fixed Rate ndash 85k Max Loan Amount

bull 30-Year Fixed Rate ndash New York

bull 30-Year Fixed Rate ndash Investment Property

bull 30-Year Fixed Rate (standard)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Service Released Versus Retained

Retaining servicing provide the MSR owner the ability to create an annuity stream of income that can be used to offset expenses elsewhere MSRs are an asset class that increases in value generates additional revenue in a rising rate environment

bull Servicing is fee income (expressed in bps) on the outstanding principal balance

bull Potential ability to earn ancillary income (or cross ndashsell) retain customers

bull Ability to generate deposits (if a bank)

bull Gives up getting cash immediately but does defer paying taxes

Fannie Mae Servicing MarketplaceWhat is it

bull A new platform that supports co-issue sales transactions

bull All loans delivered will have the selling and servicing repwarrants bifurcated ndash selling repswarrants stay with the seller

bull Bifurcation eligibility minimum net worth of $25 million plus the greater of 25bps of servicing UPB or 25bps of bifurcated deliveries for the past 3 years

bull Brings sellers and servicers together to deliver pricing certainty transparency and operating efficiency

How does it workbull Sellers access Servicing Marketplace via PE-Whole Loan where they initiate servicer relationship

activities

bull Sellers work with the servicer to negotiatefinalize pricing loan data delivery requirements and agreements before they begin transactions

bull Once a servicer accepts the relationship the seller has access to the servicerrsquos SRP schedule (also available via API) and can take down co-issue commitments via PE-Whole Loan with their associated servicer(s)

Fannie Maersquos Credit Pricing and Whole Loan Conduit

Fannie Mae Servicing Marketplace

Benefits to Customers

bull Supports sellers in their search for co-issue servicing partners

bull Standardizes data exchange and delivery process to improve efficiency for sellers and servicers

bull Helps sellers improve the their overall liquidity of their loan and servicing rights

Timing

bull Currently in production with four servicers (ArvestCentral Mortgage CMC Funding RoundPointServicing and Two Harbors) and seven sellers

bull Managing a staged rollout and onboarding process beginning with sellers that have existing relationships with the SMP servicers