more stained glass

TRANSCRIPT

More Stained Glass – or – Sorry Seems to be the Hardest Word

A very perceptive attorney associate of OFGI pointed out an omission on the article

recently sent out entitled “Stained Glass – or – How We Got Where We Are”. His point is

well taken, and is well expressed by the article we found quoted in its entirety below (bold

& underline added for emphasis – parenthetic expressions added for commentary):

“The Roots of the Subprime Mortgage Mess Have Clinton All Over Them

By Jimmie on Sep 21, 2008 in The Economy and Your Money

There has been a lot of talk recently about subprime mortgages and the thought occurred to me that something had to happen in the financial market to make subprime mortgages so attractive for companies to offer.. First is this tidbit from the USA Today, in 2004.

Subprime mortgage activity grew an average 25% a year from 1994 to 2003, outpacing the rate of growth for prime mortgages (jeessss – and we wonder why we’re in a mess now???). The industry accounted for about $330 billion, or 9%, of U.S. mortgages in 2003, up from $35 billion a decade earlier. (Hummm, how did that happen, Mr. Clinton???).

Where did this come from? It’s not as if subprime mortgages were brand new things in 1994. They’ve existed for quite a long time, but mortgage companies didn’t offer them very often. Something had to happen to generate such a marked increase. Financial markets don’t just shift to a new lending practice without a darned good reason. For there to be a tenfold increase in subprime mortgages means that something dramatic had to happen. So what was it?

In this case, it was the Clinton administration.

In 1994, the administration pushed through some fundamental changes to the Community Reinvestment Act of 1977. The goal of these changes was to make sure that banks were “serving low and moderate income geographies” and making sure that these banks “economically

empowered persons of low and moderate income”. (In other words, make bad loans to people who would not otherwise qualify in areas that are not of interest against real estate that can’t be moved when the need comes to foreclose). Regulators were then given more power to punish banks that did not comply with the new rules These changes led directly, to the explosion of subprime mortgages and contributed heavily to our current financial debacle (as we have pointed out before, so what Clinton balanced the budget – look what other great things he did for the Nation!!!).

The changes did two basic things. First, the government changed the measure by which the regulators decided whether a bank was in compliance with the act or not. Prior to 1994, the ratings were determined in large part by what efforts banks were taking to reach into these neighborhoods - what advertising they were doing, how many bank branches they opened, what sort of outreach they made into offering loans and mortgages. The new rules made the rating dependent on outcome-based numbers - how many mortgages were signed, how much money was loaned, and so on. Those numbers were broken down on racial lines, as well as by neighborhood, and by financial status. In other words, for a bank to get a good rating under the CRA it had to actually start writing mortgages to low-income lenders instead of simply offering mortgages and advertising its services. This was not merely a matter of paperwork. As the Comtroller said in 1994, non compliance would bring out “the full panoply of all our enforcement armorarium”. In other words, the government had a couple brand-new hammers and they intended to use them if banks didn’t make low-income loans.

The second thing that happened is that the Clinton administration made it easier for groups to make complaints against banks for perceived under-performance. That put an immense amount of pressure on banks to cut deals with largely left-wing political groups who then turned that money toward more advocacy and dodgy loans. As a rather prescient article in the City Paper put it:

Crucially, the new CRA regulations also instructed bank examiners to take into account how well banks responded to complaints. The old CRA evaluation process had allowed advocacy groups a chance to express their views on individual banks, and publicly available data on the lending patterns of individual banks allowed activist groups to target institutions considered vulnerable to protest. But for advocacy groups that were in the complaint business, the Clinton administration regulations offered a formal invitation. The National Community Reinvestment Coalition—a foundation-funded umbrella group for community activist groups that profit from the CRA—issued a clarion call to its members in a leaflet entitled “The New CRA

Regulations: How Community Groups Can Get Involved.” “Timely comments,” the NCRC observed with a certain understatement, “can have a strong influence on a bank’s CRA rating.”

The Clinton administration’s get-tough regulatory regime mattered so crucially because bank deregulation had set off a wave of mega-mergers, including the acquisition of the Bank of America by NationsBank, BankBoston by Fleet Financial, and Bankers Trust by Deutsche Bank. Regulatory approval of such mergers depended, in part, on positive CRA ratings. “To avoid the possibility of a denied or delayed application,” advises the NCRC in its deadpan tone, “lending institutions have an incentive to make formal agreements with community organizations.” By intervening—even just threatening to intervene—in the CRA review process, left-wing nonprofit groups have been able to gain control over eye-popping pools of bank capital, which they in turn parcel out to individual low-income mortgage seekers. A radical group called ACORN Housing has a $760 million commitment from the Bank of New York; the Boston-based Neighborhood Assistance Corporation of America has a $3-billion agreement with the Bank of America; a coalition of groups headed by New Jersey Citizen Action has a five-year, $13-billion agreement with First Union Corporation. Similar deals operate in almost every major U.S. city. Observes Tom Callahan, executive director of the Massachusetts Affordable Housing Alliance, which has $220 million in bank mortgage money to parcel out, “CRA is the backbone of everything we do.”

It’s not a real mystery to see what happened next. Lending institutions, under the gun to give out loans, started extending loans to people who would not have qualified for them otherwise. Those loans, called subprime because they are made to people who are not prime credit risks, carried higher interest rates (because the lender needs to make sure that it makes money out of a loan that is far more likely to go into default) and other costly attachments that mitigated the risk to the lender and the people whose money the lender was using for these loans (i.e. folks like you and me). The more pressure that was put on banks from these advocacy groups and government regulators, the more subprime mortgages they issued to keep their CRA score high enough to remain in compliance.

Now, the Clinton administration is not solely responsible for our current financial woes, but it did contribute greatly to the explosion of subprime mortgages, which helped drive us to where we are now. If we’re going to eventually untangle this mess, the CRA and Clinton’s 1994 regulation expansion is a good place to start.”

This is typical over-regulatory policies by Democratic regimes. The more government oversight you pile on things the better, right? The entire Liberal

attitude, is that the “unwashed masses” (that is us) are not bright enough to handle our own business, so we need layers upon layers of Governmental bureaucracy to tell us what to do (for our own good of course). Well, just show even ONE instance where that was true!!! In this case, not only over-regulation by the Executive Branch, but over-regulation with an AGENDA.

No Regrets – or – Just Before Yom Kippur, Clinton Still Unrepentant:

Just days before Yom Kippur (the Day of Judgment & Repentance) Slick Willy is quoted to have still not felt any regret or remorse (imagine that) about his campaign to overturn Glass-Steagall back in 1999:

Bill Clinton Revisits His Economic Legacy (by Dana Goldstein at Tapped, The American Prospect)

on September 22, 2008 - posted - 10:37 PM

“One policy Clinton said he doesn’t regret is his repeal of the Glass-Steagall Act in 1999, which, for the first time since the Depression, allowed commercial banks to engage

in investment banking activities. Clinton said the commercial banks were an important moderating force on the risk-taking of the big investment firms that collapsed this week. “In the case of the current crisis, I believe the bill I signed allowed Bank of America to take over

Merrill Lynch,” he said.”

So, there you have it. Just like they used to say on Saturday Night Live “I’m not sorry, I’m glad I did it”. Yea, it did alright. What he neglected to mention is, that his repeal of Glass-Steagall MADE THE BANK OF AMERICA TAKE OVER OF MERRILL LYNCH NECESSARY IN THE FIRST PLACE.

Just Before the House Bailout Vote, a Democrat Congress Woman just had to open her Mouth:

House Speaker Nancy Pelosi,D-Calif., is seen during a news conference on Capitol Hill in Washington, DC, just minutes to an almost lead pipe synched House Vote to Bailout the economy, our dear friend Nancy had to get up and tell the Nation that the House Democrats had put together this wonderful bill, and that the Republicans had done not a darn thing.

As a result, the bill went down, 228-205. Thirteen of the 19 most vulnerable Republicans and Democrats in

an Associated Press analysis voted against the bill despite the pleas from President Bush and their party

leaders to pass it.

In all, 65 Republicans joined 140 Democrats in voting "yes," while 133 Republicans and 95 Democrats voted

"no."

The final stock carnage was 777 points, far surpassing the 684-point drop on the first trading day after the Sept. 11, 2001, terror attacks. This was the largest single drop in one day – EVER. All because some liberal from California couldn’t keep her d-mn mouth shut!

Stocks plummet in largest one-day point drop

ever AP - 2 minutes ago

NEW YORK - The failure of the bailout package in Congress literally dropped jaws on Wall Street and

triggered a historic selloff — including a terrifying decline of nearly 500 points in mere minutes as the

vote took place, the closest thing to panic the stock market has seen in years.

How are we going to deal with this? Is the proposed bailout of the culprits that took advantage of the Congressional and Presidential idiocy really the right thing to do? What about all of the folks that had (bad) loans made to them that have lost or are losing their homes? Is there an alternative that would actually work better????

Actually, although the House Speaker (boy, is THAT a good title for that gal), had all the wrong motives, and, it is quite unfortunate that it caused the biggest drop in the market EVER; it is probably a good thing that that thing on the top of her shoulders started moving and making noise that resulted in the failure of the passage of this bill.

Frankly, they are bailing out the wrong folks! Why bail out the culprits that got greedy when the folks that really need a bail out are those that were sold (often by unscrupulous mortgage brokers that forged signatures, changed documents, padded incomes, etc.) and got themselves into an ARM that they ultimately could not pay for???

There is some real reform needed, but it is uncertain that bailing out the folks that took a great windfall under the Clinton Administration are the folks that need bailing out. What about reforms? Let’s take a look at another Democratic Party invention – the Federal Reserve…..

The Federal Reserve was established in 1913 by the Federal Reserve Act. Congressional Republicans opposed this law. In fact, Congressman Charles Lindbergh (yea, your remember right, he is the fellow that flew the ‘Spirit of Saint Luis’ over the pond) was one of the strongest opponents to the Federal Reserve, and do you know what happened to him? If no, go look it up, as it is a very interesting story….

http://en.wikipedia.org/wiki/Charles_August_Lindbergh

http://www.charleslindbergh.com/kidnap/index.asp

Republican Congressman Lindbergh said on that historic day, to the House: "This Act establishes the most gigantic trust on earth. When the President signs this bill, the invisible government by the Monetary Power will be legalized. The people may not know it immediately, but the day of reckoning is only a few years removed.

The trusts will soon realize that they have gone too far even for their own good. The people must make a declaration of independence to relieve themselves from the Monetary Power. This they will be able to do by taking control of Congress. Wall Streeters could not cheat us if you Senators and Representatives did not make a humbug of Congress. . . . If we had a people’s Congress, there would be stability.”

What did the Federal Reserve Act do exactly?

Well, frankly, Congress literally gave over the Constitutional power of the U.S. Treasury to manage the U.S. money supply and economy.

The “Federal Reserve” is NEITHER. It is NOT a Federal institution (and NEVER has been) and THERE IS NO RESERVE.

The Fed is actually just a gentlemen’s club of member banks, governed by 12 regional banks, and a CENTRAL bank.

THE ONLY THING FEDERAL ABOUT THE FED IS THAT EVERY SIX YEARS, THE CHAIRMAN IS APPOINTED BY THE PRESIDENT OF THE United States.

Don’t just believe the above – take a look for yourself. Here is a quote from the Fed’s web site:

“

The Structure of the Federal Reserve System

Skip to content

The Board of Governors of the Federal Reserve System

On December 23, Appointments to the Board

1913, the Federal Reserve System, which serves as the nation's central bank, was created by an act of Congress. The System consists of a seven member Board of Governors with headquarters in Washington, D.C., and twelve Reserve Banks located in major cities throughout the United States.

The seven members of the Board of Governors are appointed by the President and confirmed by the Senate to serve 14-year terms of office. Members may serve only one full term, but a member who has been appointed to complete an unexpired term may be reappointed to a full term. The President designates, and the Senate confirms, two members of the Board to be Chairman and Vice Chairman, for four-year terms.

Representation Only one member of the Board may be selected from any one of the twelve Federal Reserve Districts. In making appointments, the President is directed by law to select a "fair representation of the financial, agricultural, industrial, and commercial interests and geographical divisions of the country." These aspects of selection are intended to ensure representation of regional interests and the interests of various sectors of the public.

Responsibilities The primary responsibility of the Board members is the formulation of monetary policy. The seven Board members constitute a majority of the 12-member Federal Open Market Committee (FOMC), the group that makes the key decisions affecting the cost and availability of money and credit in the economy. The other five members of the FOMC are Reserve Bank presidents, one of whom is the president of the Federal Reserve Bank of New York. The other Bank presidents serve one-year terms on a rotating basis. By statute the FOMC determines its own organization, and by tradition it elects the Chairman of the Board of Governors as its Chairman and the President of the New York Bank as its Vice Chairman.

The Board sets reserve requirements and shares the responsibility with the Reserve Banks for discount rate policy. These two functions plus open market operations constitute the monetary policy tools of the Federal Reserve System.

In addition to monetary policy responsibilities, the Federal

Reserve Board has regulatory and supervisory responsibilities over banks that are members of the System, bank holding companies, international banking facilities in the United States, Edge Act and agreement corporations, foreign activities of member banks, and the U.S. activities of foreign-owned banks. The Board also sets margin requirements, which limit the use of credit for purchasing or carrying securities.

In addition, the Board plays a key role in assuring the smooth functioning and continued development of the nation's vast payments system [see Fedwire and Payment System Risk Policy].

Another area of Board responsibility is the development and administration of regulations that implement major federal laws governing consumer credit such as the Truth in Lending Act, the Equal Credit Opportunity Act, the Home Mortgage Disclosure Act and the Truth in Savings Act [see Consumer Information and Community Development].

Meetings The Board usually meets several times a week. Meetings are conducted in compliance with the Government in the Sunshine Act, and many meetings are open to the public. If the Board has convened to consider confidential financial information, however, the sessions are closed to public observation.

Contacts within Government As they carry out their duties, members of the Board routinely confer with officials of other government agencies, representatives of banking industry groups, officials of the central banks of other countries, members of Congress and academicians. For example, they meet frequently with Treasury officials and the Council of Economic Advisers to help evaluate the economic climate and to discuss objectives for the nation's economy. Governors also discuss the international monetary system with central bankers of other countries and are in close contact with the heads of the U.S. agencies that make foreign loans and conduct foreign

financial transactions.

The Structure of the Federal Reserve

Home | About the Fed Accessibility | Contact Us Last update: July 8, 2003

”

I think the man that wrote the bill summed it up best:

"Whoever controls the volume of money in any country is absolute master of all industry and commerce."(Paul Warburg, drafter of the Federal Reserve Act)

So, how did we get saddled with this non-Governmental entity made up of wealthy banks (and the families that owned them at the time) anyway???

Woodrow Wilson was elected President as a Democrat in 1912.

The legislation was originally sponsored in 1913 by the two chairmen of House and Senate Banking and Currency committees, Representative Carter Glass, a Democrat from Virginia and Senator Robert Latham Owen, a Democrat from Oklahoma.

“The House, on December 22, 1913, agreed to the conference report on the Federal Reserve Act by a vote of 298 yeas to 60 nays with 76 not voting. The Senate, on December 23, 1913,

agreed to it by a vote of 43 yeas to 25 nays with 27 not voting. The record shows that there were no Democrats voting "nay" in the Senate and only two in the House. The record also shows that almost all of those not voting on the bill had previously declared their intentions and were paired with members of opposite intentions (See v. 51 Cong. Record, pages 1464,

1487-88).”

When the new Congress convened in 1935, there were only twenty-five Republican senators. The Democratic Party rode roughshod over Congress in both Houses.

Yep, FDR had a New Deal for the U.S. alright. Give the control of the U.S. economy and money supply over to the bankers in a BIGGER way.

The Banking Act of 1935 renewed and extended many of the 1933 provisions to banks outside the Federal Reserve System. However, this act is of particular note because it finally clarified several of the institutional tensions designed into the Federal Reserve System. Under the act, the Federal Reserve Board became the supreme institution; it was renamed the Board of Governors of the Federal Reserve System, and members of the Board were given the title of "Governor," the traditional title for central bankers. In addition, the act ended the ex officio membership of the Secretary of the Treasury and Comptroller of the Currency on the Board. Finally, the act formally recognized the Federal Open Market Committee (FOMC) as a separate legal entity.

The ten year terms of office of the members of the Board were lengthened by the Banking Act of 1935 to fourteen years, which meant that these directors of the nation’s finances, although not elected by the people, held office longer than three presidents.

The Federal Open Market Committee (FOMC), a component of the Federal Reserve System, is charged under U.S. law with overseeing open market operations in the United States, and is the principal tool of US national monetary policy. (Open market operations are the buying and selling of government securities.) The Committee sets monetary policy by specifying the short-term objective for those operations, which is currently a target level for the federal funds rate (the rate that commercial banks charge on overnight loans among themselves). The FOMC also directs operations undertaken by the Federal Reserve System in foreign exchange markets, although any intervention in foreign exchange markets is coordinated with the U.S. Treasury, which has responsibility for formulating U.S. policies regarding the exchange value of the dollar.

The most important policy making body of the Federal Reserve System is the Federal Open Market Committee (FOMC). It is composed of the seven Governors, the president of the Federal Reserve Bank of New York, and four other Reserve Bank presidents that serve on a rotating basis. The FOMC can effect monetary policy through the use of three tools:

1. Open market operations--the buying and selling of U.S. government securities. 2. Altering reserve requirements--the amount of funds that commercial banks must

hold in reserve against deposits. 3. Adjusting the discount rate--the interest rate charged to commercial banks.

These tools can be used to tighten or expand the money supply. For example, if the FOMC wanted to control inflation, it could restrict the nation's money supply by selling government securities and raising the amount of money that banks need to set aside for reserve requirements. Both of these actions would take money out of circulation. In theory, a smaller supply of money would lead to less spending which would lead to lower prices. The FOMC can also raise interest rates to help control inflation. By making money more expensive to borrow, consumers would be more likely to save money rather than spend it. This could also lead to lower prices.

So, what is a potential solution???

How about we REFORM the FED, huh???

EXCERPTS FROM THE SEPTEMBER 28, 2008 BROADCAST OF “TAKE NO PRISONERS “ Dr. Sam Kennedy’s 4 Point Common Sense Economic Recovery Plan ("About all a Federal Reserve note can legally do is wipe out one debt and replace it with itself another debt, a note that promises nothing. If anything's been paid, the payment occurs only in the minds of the parties..." Tupper Saucy, “Miracle on Main Street.”) From Dr. Kennedy: So, they tell us there’s an economic crisis. Let me ask you a question. If America has the most powerful economy in the world, then why does it collapse upon news of a couple of bankruptcies? Why does it collapse at the first sign of trouble? How strong can it be if a misspoken word by the chairman of the Fed of the President can cause a run on the banks? Do you get the feeling that something’s rotten in Washington? My friends, mountains last millions of years until nature whittles them down. Mountains don’t collapse. Gold doesn’t change its properties - it’s immutable. But a house of cards which is based upon promissory notes backed by nothing – promises to pay nothing – empty promises disguised by statutes and regulations to look valuable to the casual observer – then you have built a pseudo an economy that is destined to fail. It must fail; it cannot stand forever. The inevitable end of that economy is coming now or later, and Scripture tells us it is wise to face the pain now.

An economy whose currency: Federal reserve Notes, and investments such as bonds, stocks, mutual funds, and all of these screwy derivatives that no one understands, consisting exclusively of arbitrary floating value assigned to instruments of liability, where all gold and silver backing has been withdrawn by government statutes and regulations back in 1933 (there are the Democrats again) and 1964 (and Democrats AGAIN), is absolute insanity. It’s delusion on a frightening scale. And that’s why the politicians who are blanketing the airwaves sound like disinterested third parties at best, and morons at worst, when they try to analyze the problem and are forced to admit that they do not understand it, cannot estimate the total liability, and have no credible plan for recovery. Only an insane person could understand the myriad layers of economic Tomfoolery. And so, we find ourselves struggling to concoct through this bailout yet another palatable charade to obscure from our own sensibilities that we have wandered way off course, down a suicidal pathway, and not one among us has the courage to step forward and say This must end or we will surely condemn our children to purgatory for the sins of the fathers and their fathers before them.”

So let me ask you a couple of obvious questions. 1. Are you aware that a barrel of oil costs approximately a sixth to a tenth of an ounce of gold – just as it has for decades? In 1974 when the price of oil shot up to $40 a barrel after the Yom Kippur war, the price of gold also increased from $35 an ounce to $183 an ounce. In other words, the perceived value of the dollar is all that really changed. Did it ever occur to you that we haven’t had a gas crisis since 2003? We’ve had a dollar crisis? 2. Are you aware that in 1912, a dollar bought a steak dinner for two JUST AS IT HAD IN 1789? You can confirm this information on the internet. For 120 years, we experienced a natural course of slight deflation as the cost of equipment to produce our products was paid off. Until 1913. What you’ve never been told in school or by the media or by the endless procession of self-anointed television experts, is that inflation is a contrived managed scheme concocted to steal your money, by men who do not wish you good tidings. So what happened in 1913 that raised the price of a steak dinner fifty to one hundred times? We’ll answer that in just a minute. 3. My final question is this: are you aware that the Federal Reserve Bank is a private bank owned by a dozen banking family cartels around the world including the Rothchild, Rockefeller and Morgan families? Here’s what the 9th circuit court said about the Federal Reserve Bank in Lewis v United States, June 24, 1982: ".. we conclude that the [Federal] Reserve Banks are not federal ... but are independent privately owned and locally controlled corporations... without day to day direction from the federal government." Lewis v United States, June 24, 1982 For more information on the Fed, you might consider ordering “The Money Masters” on DVD, or read Tupper Saucy’s miraculous “Miracle on Main Street” which you can order at Amazon.com. What happened in 1913? Congress passed the Federal Reserve Act in the dead of night, giving this private bank the power to print our money at a cost of four cents per bill which it uses to buy Treasury securities. Let’s say the Fed prints ten, one thousand dollar bills at a total cost of forty cents which it uses to purchase a ten thousand dollar Treasury bond. When the bond matures, the Fed returns the bond to the United States and the United States pays the Fed the ten thousand dollar face value. That’s right. The Fed collects ten thousand dollars on a forty cent investment - twenty-five thousand percent interest on a forty cent investment. Now multiply that by the billions of dollars in money the Fed prints every year. Those Treasury securities comprise the bulk of the nine trillion dollars in public debt you read about in the papers that the United States owes. Money conveniently owed to the banking cartels for the privilege of printing our money. That’s what happened in 1913.

Something else happened in 1913. Congress passed the income tax act of 1913 to pay the interest to the Fed for America becoming an instant debtor nation at the stroke of a pen.

(The commentary below has been added. The remaining article continues below)

Income Tax of 1913

In his inaugural address in March 1913, newly elected Democratic President Woodrow Wilson quickly took advantage of a new amendment to the U.S. Constitution, by calling for tariff reduction and the adoption of an income tax. Within a month, during an emergency session of Congress, House Ways and Means Chair Oscar Underwood, a Democrat from Alabama, introduced a tariff reform bill that provided for an income tax with progressive rates. Underwood and the income tax section's principal drafter, Representative Cordell Hull of Tennessee, had originally sought to introduce a flat rate income tax to ensure judicial approval, but pressure from other Democrats, including future Vice-President John Nance Garner of Texas, led them to opt for the graduated rates.

The ensuing debates over the income tax primarily centered on the rate and exemption amount for an income tax, rather than the propriety of the income tax itself. Regular Republicans pushed for flatter rates and lower exemptions. Since they did not concede that the tariff was itself a tax, they viewed any exemption to the income tax to be class legislation and, in the words of Michigan Senator Charles E. Townsend, a "danger to the Republic." When combined with progressive rates, Senator Henry Cabot Lodge of Massachusetts argued, the exemption would "set a class apart and say they are to be pillaged, their property is to be confiscated."

Insurgents and members of the newer Progressive party saw the income tax very differently from Republicans. They advocated steeply progressive rates as a method of redistributing wealth. In the most extreme example, Representative Ira Copley proposed an income tax with a top marginal rate of 68 percent on incomes exceeding one million dollars. Others, such as Senator Robert La Follette of Wisconsin, proposed rates as high as 11 percent to reach what he called the "menace" of "great accumulation of wealth."

Standing between these two extremes were the Democrats, who proposed a more mild progression of rates to offset the burden of tariff taxes on the poor. Senator John Sharp Williams from Mississippi, one of the Democratic caucus's spokesmen in the Senate, rebuked the Insurgent and Progressive position by stating "[n]o honest man can make war upon great fortunes per se.... I am not going to make this tariff bill a great panacea for all the inequalities of fortune existing in this country." Nevertheless, he recognized that a modicum of progressivity, accompanied by a high exemption, was necessary as long as tariff taxes remained in place. According to Williams, the regular Republicans' plea for flat rates and low exemptions should be left for "when the good day comes—the golden day—when there will be no taxes upon consumption at all."

The Democrats' position carried the day. The Underwood/Simmons Tariff Act, which went into effect on October 3, 1913, levied an income tax that imposed mildly progressive rates and was accompanied by a healthy exemption. The graduated rate feature was later challenged, but the Supreme Court upheld it in Brushaber v. Union Pacific R.R. Co. (1916) on the ground that it did not "transcend the conception of all taxation" so as "to be a mere arbitrary abuse of power."

Although the income tax act of 1913 instituted only mild progressivity and raised a relatively small amount, it was still a monumental development. It began the process of converting the tax system from a regressive consumption-based system to a system

that levied taxes based on the ability to pay. Moreover, it offered the vehicle for a rapid expansion of the tax system during World War I (1914–1918) when consumption taxes proved inadequate. It was not until World War II (1939–45), however, when Congress permitted payroll deduction and a significant cut in the exemption, that the income tax truly became a tax for all people. Nevertheless, it was in the income tax act of 1913 that the seeds were planted for this development.

(back to the article quoted above) According to the grace commission report submitted to Ronald Regan in 1984: “With two-thirds of everyone's personal income taxes wasted or not collected, 100 percent of what is collected is absorbed solely by interest on the Federal debt and by Federal Government contributions to transfer payments. In other words, all individual income tax revenues are gone before one nickel is spent on the services which taxpayers expect from their Government.” J. Peter Grace, Cover letter, Grace Commission Report, January 12, 1984 Let me read to you from a speech made to Congress by Republican Congressman Louis McFadden, chairman of the House Banking and Currency committee in 1934 after FDR engineered a government confiscation of all private wealth using tactics similar to the strong-arming of the present Paulson bailout. McFadden brought formal charges against the Board of Governors of the Federal Reserve Bank system, the Comptroller of the Currency and the Secretary of Treasury for conspiracy, fraud, conversion and treason: "Mr. Chairman, we have in this Country one of the most corrupt institutions the world has ever known. I refer to the Federal Reserve Board and the Federal Reserve Banks. The Fed has cheated the Government of these United States and the people of the United States out of enough money to pay the Nation's debt several times over. "This evil institution has impoverished and ruined the people of these United

States, has bankrupted itself, and has practically bankrupted our Government. It has done this through the defects of the law under which it operates, through the maladministration of that law by the Fed and through the corrupt practices of the moneyed vultures who control it. "Some people think that the Federal Reserve Banks are United States Government institutions. They are private monopolies which prey upon the people of these United States for the benefit of themselves and their foreign customers; foreign and domestic speculators and swindlers; and rich and predatory money lenders. In that dark crew of financial pirates there are those who would cut a man's throat to get a dollar out of his pocket; there are those who send money into states to buy votes to control our legislatures; there are those who maintain International propaganda for the purpose of deceiving us into granting of new concessions which will permit them to cover up their past misdeeds and set again in motion their gigantic train of crime. "These twelve private credit monopolies were deceitfully and disloyally foisted upon this Country by the bankers who came here from Europe and repaid us our hospitality by undermining our American institutions. Those bankers took money out of this Country to finance Japan in a war against Russia. They created a reign of terror in Russia with our money in order to help that war along. They instigated the separate peace between Germany and Russia, and thus drove a wedge between the allies in World War. They financed Trotsky's passage from New York to Russia so that he might assist in the destruction of the Russian Empire. They fomented and instigated the Russian Revolution, and placed a large fund of American dollars at Trotsky's disposal in one of their branch banks in Sweden so that through him Russian homes might be thoroughly broken up and Russian children flung far and wide from their natural protectors. They have since begun breaking up of American homes and the dispersal of American children. "Mr. Chairman, there should be no partisanship in matters concerning banking and currency affairs in this Country, and I do not speak with any. Folks, the Federal Reserve Act was written in 1909 by a cartel headed by Senator Nathan Aldrich, grandfather to the wife of John D. Rockefeller the second. At that secret meeting, Aldrich gave the United States twenty years to pay its debts from the Civil and Revolutionary Wars, and appointed a receiver to oversee collection of the debt if the United States defaulted, which was inevitable in light of their ability to contrive limitless liability. The receiver for the debt was the Federal Reserve Bank, and the trustee of the receivership was the Secretary of the Treasury. So let’s not be surprised that twenty years later, all the gold was moved out of U.S. banks into the hands of the Fed, during the so-called Great Depression, giving a pretext to FDR, whose family by the way owned German bonds, to issue executive order 6102, ordering all privately held gold – your family’s gold other than jewelry and $100 – to be turned in to a Federal Reserve Bank branch near you in return for worthless pieces of paper backed by nothing.

That’s when the house of cards began. FDR also ram-rodded through Congress the Emergency Banking Act under contrived “emergency” conditions similar to today’s “crisis,” without providing Congress with a copy of the bill, and permanently facilitating the takeover of all wealth in the united States by the Federal Reserve Bank. If I sound crazy, then why does your deed call you

a tenant? Have you ever asked your attorney? And now you know why Henry Paulson, Secretary of the Treasury, trustee for the bankruptcy, the man who is generally recognized as architect of mortgage derivatives when he was Chairman of Goldman Sachs – the only Wall Street brokerage house which was unmolested by the mortgage meltdown - shamelessly (which is how they always operate), outrageously demands seven hundred billion dollars for a so-called bailout. And where will that money come from? Paulson’s plan calls for Treasury to borrow the money by issuing Treasury bonds. And who is likely to buy them up? The Fed, with freshly printed money. The Treachery Secretary’s plan for your economic welfare calls for a transfer of an addition $700 billion dollars to the Fed. As in 1933, a crisis manufactured in whole by the Fed is being used to consolidate it’s wealth and subjugate the people into dependency through poverty. Wake up America. It’s happening again. Right under your nose. You’re asleep at the wheel and your children are being left scraps on the table if they’re lucky to have a table. All last week, the pundits were asking: what’s the alternative? We have to do something! And…we…can. A single stroke of the pen on a one page “bill.” We can eliminate the so called credit crisis as if it never happened, restore the economy to vibrancy and legitimacy, restore permanent value to our money, return dignity and independence to the American people, and while we’re at it, return gas prices to the pre-1973 levels. One page. One stroke. The solution could not be more obvious to any who will take the time to look. Number 1. Repeal the Federal Reserve Act of 1913. Return the printing and minting of money to the people. This one move will instantly wipe out nine trillion (or so) dollars in debt and provide immediate liquidity and solvency. America will return to being a creditor nation. Number 2. Confiscate the assets of the Fed Reserve Bank, all of its gold, it’s buildings, fixtures, notes and fickle securities. The country will be instant restored to pre-eminence, flush in enough capital to replace our currency with currency backed by gold and silver. All the Feds security interests in the American people will be instantly satisfied The United States will hold no paper on its creators. Americans will become instant owners of their own homes, cars and businesses. All outstanding foreign debts will be satisfied. The assets of the banking cartels include most of the assets of the world at large. The only debts that will not be forgiven are the debts incurred by the Federal Reserve Bank and the World Bank to the people for having stolen their property for 107 years.

Number 3. Repeal the Income Tax Act of 1913 and IRS. This one step will end the tyranny, restore dignity to the American people, and immediately restore hundreds of dollars a week to most people’s paychecks. The need to have four, five and six jobs per family will end. We will have the time and assets to restore our families and enjoy their lives instead of working until we drop, shopping on Sunday, and hunting for bargains. The vast sums of money paid to accountants and attorneys will stay in our pockets. The vast amount of time spent in the deviant calculations of the tax code under the point of a gun will end. And perhaps America can once again be respected around the world. Number 4. Forgive the members of the Federal Reserve Board, the complicit politicians, and the banking families for their inhumanity for their crimes against mankind. Instead, we will confiscate their mansions, their yachts, their holdings, assets and possessions after proper civil trials or pursuant to statute. We will rely on the will of the people to shame their treason publicly and turn them into pariahs around the world until they confess their sins and ask for forgiveness. In this way, we will bring rapid closure, testify to our high intentions, and remain true to the Word of the Creator. Is the loss of a fraudulent stock market where value is established by speculative gambling and greed for the stock rather than the performance of the company, not a worthy price to instantly own your own home, car and business, be free of loan payments, restore your paycheck, and bring truth back to your economy? If the answer is yes, then we should circulate this message during this time of contrived crisis, using the awesome power of the internet as a bulwark against tyranny by governments and the bankers who control them. Thank you for reading. _________________________________________

History’s most important quotations: "Whoever controls the volume of money in any country is absolute master of all industry and commerce." President James A. Garfield "I believe that banking institutions are more dangerous to our liberties than standing armies.” - Thomas Jefferson

"Give me control over a nation's currency and I care not who makes its laws" - Baron M.A. Rothschild (1744 - 1812) "when you or I write a check there must be sufficient funds in our account to cover that check, but when the Federal Reserve writes a check, it is creating money". -Boston Federal Reserve Bank in a publication titled "Putting It Simply" "We make money the old fashioned way. We print it". -Art Rolnick, former Chief Economist, Minneapolis Federal Reserve Bank "History shows that the money changers have used every form of abuse, intrigue, deceit and violent means possible to maintain control over governments by controlling the money and the issuance of it." President James A. Madison "... You are a den of vipers and thieves. I intend to rout you out, and by the grace of the Eternal God, will rout you out". -President Andrew Jackson, upon evicting a delegation of international bankers from the Oval Office "If the American people ever allow private banks to control the issue of their currency first by inflation and then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children will wake up homeless on the continent their fathers conquered". -Thomas Jefferson in 1802 in a letter to then Secretary of the Treasury, Albert Gallatin

"... the privilege of creating and issuing money... is the government's greatest creative opportunity... [saving] the taxpayers immense sums of money...". -Abraham Lincoln "Of all contrivances for cheating the laboring classes of mankind, none has been more effective than that which deludes them with paper money". - Daniel Webster "All the perplexities, confusion and distress in America rise, not from defects in their Constitution or Confederation, not from want of honor or virtue, so much as from downright ignorance of the nature of coin, credit and circulation". -John Adams, in a letter to Thomas Jefferson in 1787 "The money power preys on the nation in times of peace, and conspires against it in times of adversity. It is more despotic than monarchy, more insolent than autocracy, more selfish than bureaucracy. It denounces, as public enemies, all who question its methods or throw light upon its crimes." Abraham Lincoln "I see in the near future a crisis approaching. It unnerves me and causes me to tremble for the safety of my country... the Money Power of the country will endeavor to prolong its reign"' by working upon the prejudices of the people, until the wealth is aggregated in a few hands and the Republic is destroyed. I feel at this moment more anxiety for the safety of my country than ever before, even in the midst of war." -Abraham Lincoln, - In a letter written to William Elkin just after the passage of the National Banking Act of 1863 and less than five months before he was assassinated. "Gold is still the ultimate store of wealth. It's the world's only true money. And there isn't much of it to go around. All of it ever mined would fit into a small building - a 56 foot cube. The annual world production would fit into a 14 foot cube, roughly the size of an ordinary living room. If each Chinese citizen were to buy just one ounce, it would take up the annual supply for the next 200 years".

- Mark Nestmann, author of "How To Achieve Personal And Financial Privacy In A Public Age "Under the surface, the Rothschilds long had a powerful influence in dictating American financial laws. The law records show that they were powers in the old Bank of the United States [abolished by Andrew Jackson]". -Gustav Myers, author of "History of the Great American Fortunes" "If Congress has the right under the Constitution to issue paper money, it was given to be used by themselves, not to be delegated to individuals or corporations". - Andrew Jackson "The few who can understand the system (Federal Reserve) will either be so interested in its profits, or so dependent on its favors, that there will be no opposition from that class, while on the other hand, the great body of the people, mentally incapable of comprehending the tremendous advantages that capital derives from the system, will bear its burdens without complaint and perhaps without even suspecting that the system is inimical to their interests". - John Sherman, protege of the Rothschild banking family, in a letter sent in 1863 to New York Bankers, Morton, and Gould, in support of the then proposed National Banking Act ".. we conclude that the [Federal] Reserve Banks are not federal ... but are independent privately owned and locally controlled corporations... without day to day direction from the federal government." - 9th Circuit Court in Lewis vs United States, June 24, 1982

"Some people think the Federal Reserve Banks are US government institutions They are not... they are private credit monopolies which prey upon the people of the US. for the benefit of themselves and their foreign and domestic swindlers, and rich and predatory money lenders. The sack of the United States by the Fed is the greatest crime in history. Every effort has been made by the Fed to conceal its powers, but the truth is the Fed has usurped the government. It controls everything here and it controls all our foreign relations. It makes and breaks governments at will". -Congressman Louis McFadden, Chairman, House Banking and Currency Committee, June 10, 1932 "This is a staggering thought. We are completely dependent on the commercial Banks. Someone has to borrow every dollar we have in circulation, cash or credit. If the Banks create ample synthetic money we are prosperous; if not, we starve. We are absolutely without a permanent money system. When one gets a complete grasp of the picture, the tragic absurdity of our hopeless position is almost incredible, but there it is. It is the most important subject intelligent persons can investigate and reflect upon. It is so important that our present civilization may collapse unless it becomes widely understood and the defects remedied very soon." -Robert Hemphill, Credit manager of Federal Reserve Bank in Atlanta. "Historically, the United States has been a hard money country. Only [since 1913] has the United States operated on a fiat money system. During this period, paper money has depreciated over 87%. During the preceding 140 year period, the hard currency of the United States had actually maintained its value. wholesale prices in 1913... were the same as in 1787". -Kenneth Gerbino, former chairman of the American Economic Council "About all a Federal Reserve note can legally do is wipe out one debt and replace it with itself another debt, a note that promises nothing. If anything's been paid, the payment occurs only in the minds of the parties...". - Tupper Saucy, author of" The Miracle On Main Street"

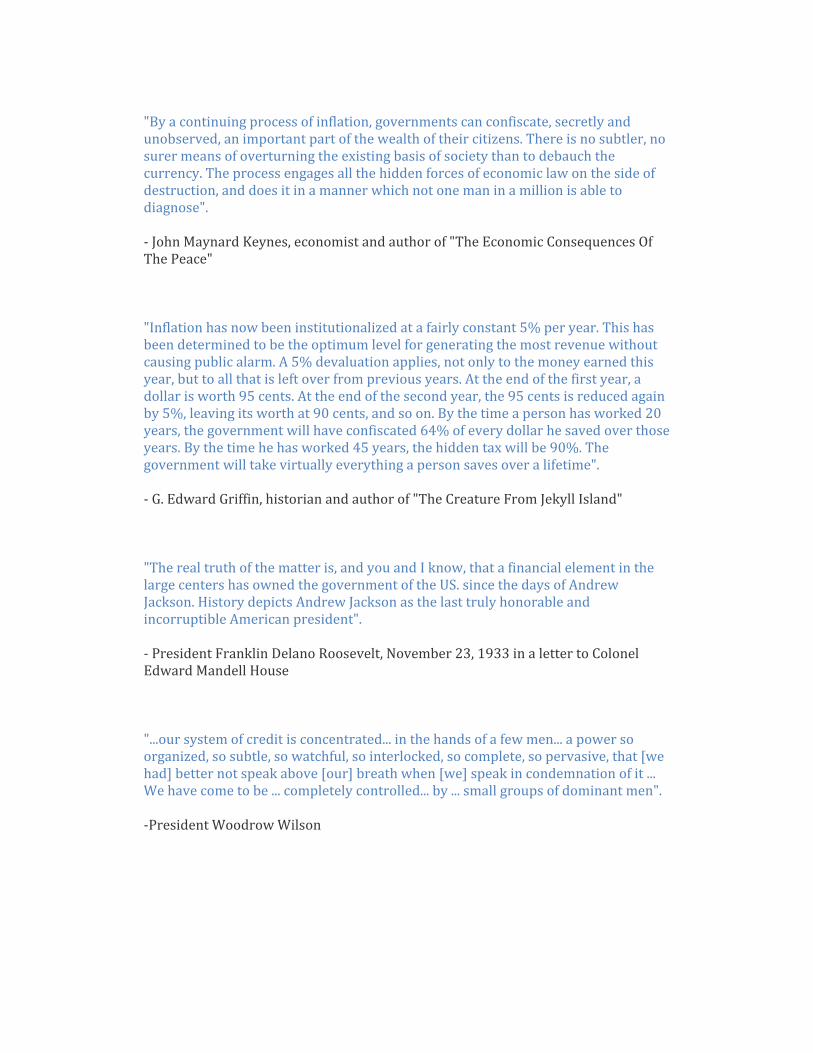

"By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose". - John Maynard Keynes, economist and author of "The Economic Consequences Of The Peace" "Inflation has now been institutionalized at a fairly constant 5% per year. This has been determined to be the optimum level for generating the most revenue without causing public alarm. A 5% devaluation applies, not only to the money earned this year, but to all that is left over from previous years. At the end of the first year, a dollar is worth 95 cents. At the end of the second year, the 95 cents is reduced again by 5%, leaving its worth at 90 cents, and so on. By the time a person has worked 20 years, the government will have confiscated 64% of every dollar he saved over those years. By the time he has worked 45 years, the hidden tax will be 90%. The government will take virtually everything a person saves over a lifetime". - G. Edward Griffin, historian and author of "The Creature From Jekyll Island" "The real truth of the matter is, and you and I know, that a financial element in the large centers has owned the government of the US. since the days of Andrew Jackson. History depicts Andrew Jackson as the last truly honorable and incorruptible American president". - President Franklin Delano Roosevelt, November 23, 1933 in a letter to Colonel Edward Mandell House "...our system of credit is concentrated... in the hands of a few men... a power so organized, so subtle, so watchful, so interlocked, so complete, so pervasive, that [we had] better not speak above [our] breath when [we] speak in condemnation of it ... We have come to be ... completely controlled... by ... small groups of dominant men". -President Woodrow Wilson

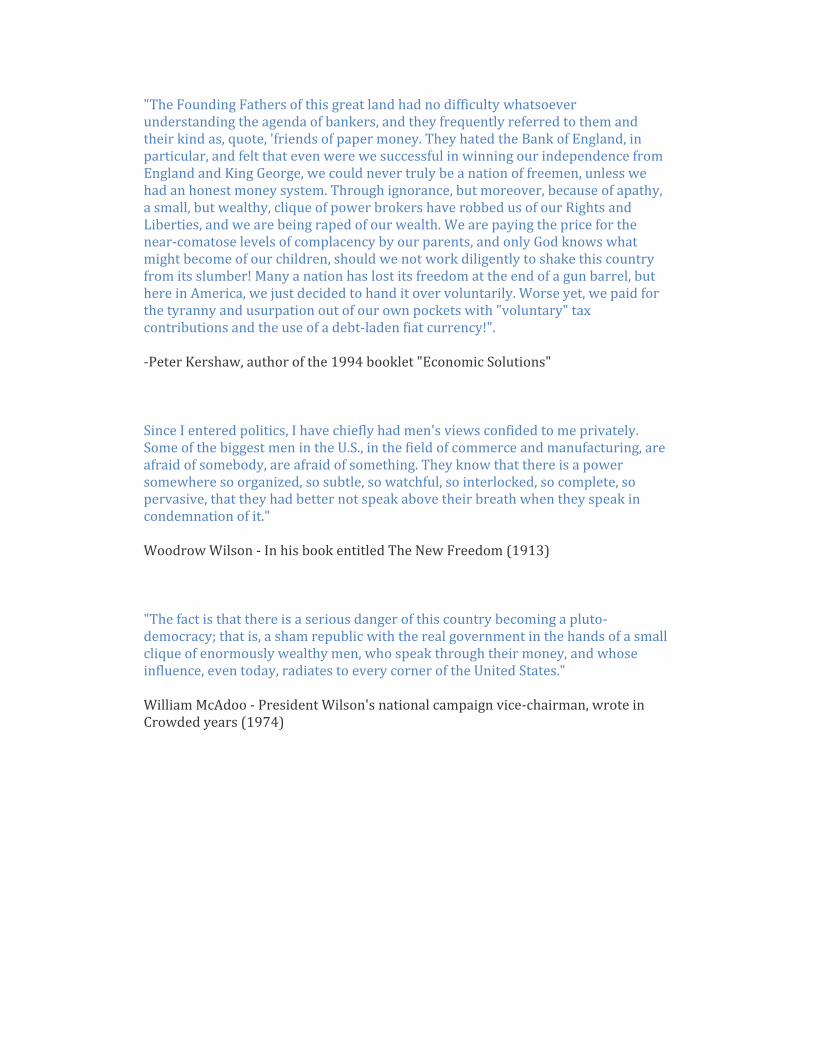

"The Founding Fathers of this great land had no difficulty whatsoever understanding the agenda of bankers, and they frequently referred to them and their kind as, quote, 'friends of paper money. They hated the Bank of England, in particular, and felt that even were we successful in winning our independence from England and King George, we could never truly be a nation of freemen, unless we had an honest money system. Through ignorance, but moreover, because of apathy, a small, but wealthy, clique of power brokers have robbed us of our Rights and Liberties, and we are being raped of our wealth. We are paying the price for the near-comatose levels of complacency by our parents, and only God knows what might become of our children, should we not work diligently to shake this country from its slumber! Many a nation has lost its freedom at the end of a gun barrel, but here in America, we just decided to hand it over voluntarily. Worse yet, we paid for the tyranny and usurpation out of our own pockets with "voluntary" tax contributions and the use of a debt-laden fiat currency!". -Peter Kershaw, author of the 1994 booklet "Economic Solutions" Since I entered politics, I have chiefly had men's views confided to me privately. Some of the biggest men in the U.S., in the field of commerce and manufacturing, are afraid of somebody, are afraid of something. They know that there is a power somewhere so organized, so subtle, so watchful, so interlocked, so complete, so pervasive, that they had better not speak above their breath when they speak in condemnation of it." Woodrow Wilson - In his book entitled The New Freedom (1913) "The fact is that there is a serious danger of this country becoming a pluto-democracy; that is, a sham republic with the real government in the hands of a small clique of enormously wealthy men, who speak through their money, and whose influence, even today, radiates to every corner of the United States." William McAdoo - President Wilson's national campaign vice-chairman, wrote in Crowded years (1974)

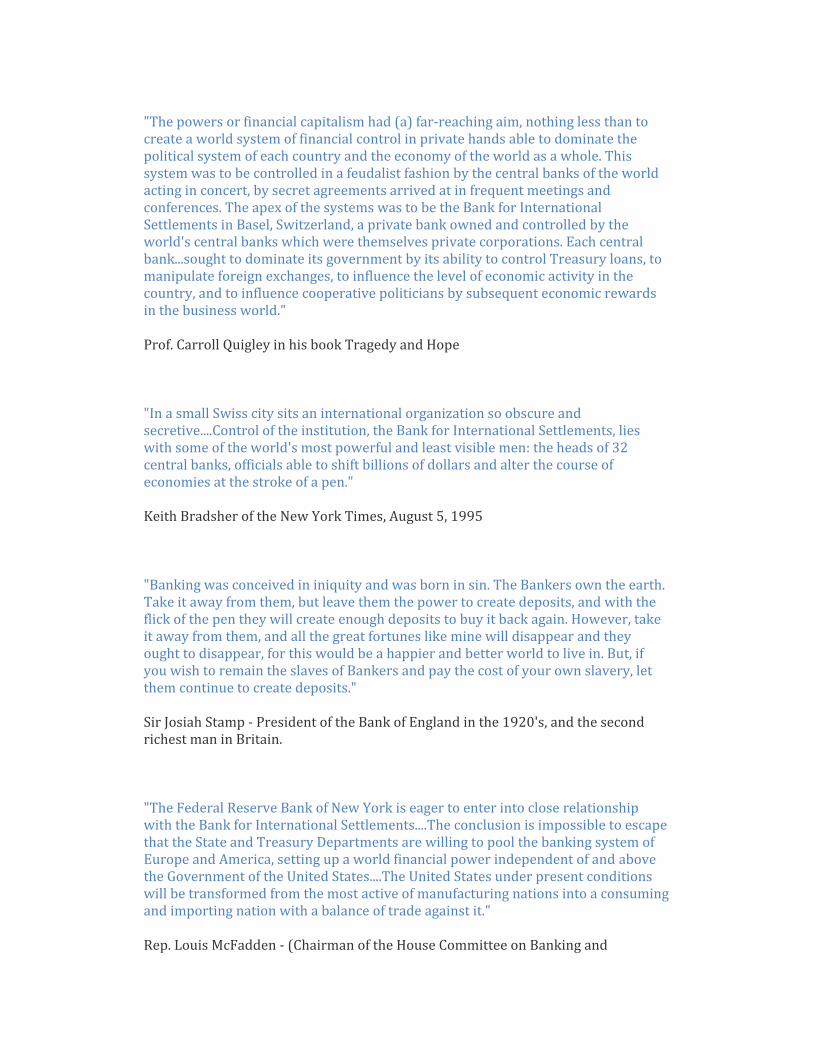

"The powers or financial capitalism had (a) far-reaching aim, nothing less than to create a world system of financial control in private hands able to dominate the political system of each country and the economy of the world as a whole. This system was to be controlled in a feudalist fashion by the central banks of the world acting in concert, by secret agreements arrived at in frequent meetings and conferences. The apex of the systems was to be the Bank for International Settlements in Basel, Switzerland, a private bank owned and controlled by the world's central banks which were themselves private corporations. Each central bank...sought to dominate its government by its ability to control Treasury loans, to manipulate foreign exchanges, to influence the level of economic activity in the country, and to influence cooperative politicians by subsequent economic rewards in the business world." Prof. Carroll Quigley in his book Tragedy and Hope "In a small Swiss city sits an international organization so obscure and secretive....Control of the institution, the Bank for International Settlements, lies with some of the world's most powerful and least visible men: the heads of 32 central banks, officials able to shift billions of dollars and alter the course of economies at the stroke of a pen." Keith Bradsher of the New York Times, August 5, 1995 "Banking was conceived in iniquity and was born in sin. The Bankers own the earth. Take it away from them, but leave them the power to create deposits, and with the flick of the pen they will create enough deposits to buy it back again. However, take it away from them, and all the great fortunes like mine will disappear and they ought to disappear, for this would be a happier and better world to live in. But, if you wish to remain the slaves of Bankers and pay the cost of your own slavery, let them continue to create deposits." Sir Josiah Stamp - President of the Bank of England in the 1920's, and the second richest man in Britain. "The Federal Reserve Bank of New York is eager to enter into close relationship with the Bank for International Settlements....The conclusion is impossible to escape that the State and Treasury Departments are willing to pool the banking system of Europe and America, setting up a world financial power independent of and above the Government of the United States....The United States under present conditions will be transformed from the most active of manufacturing nations into a consuming and importing nation with a balance of trade against it." Rep. Louis McFadden - (Chairman of the House Committee on Banking and

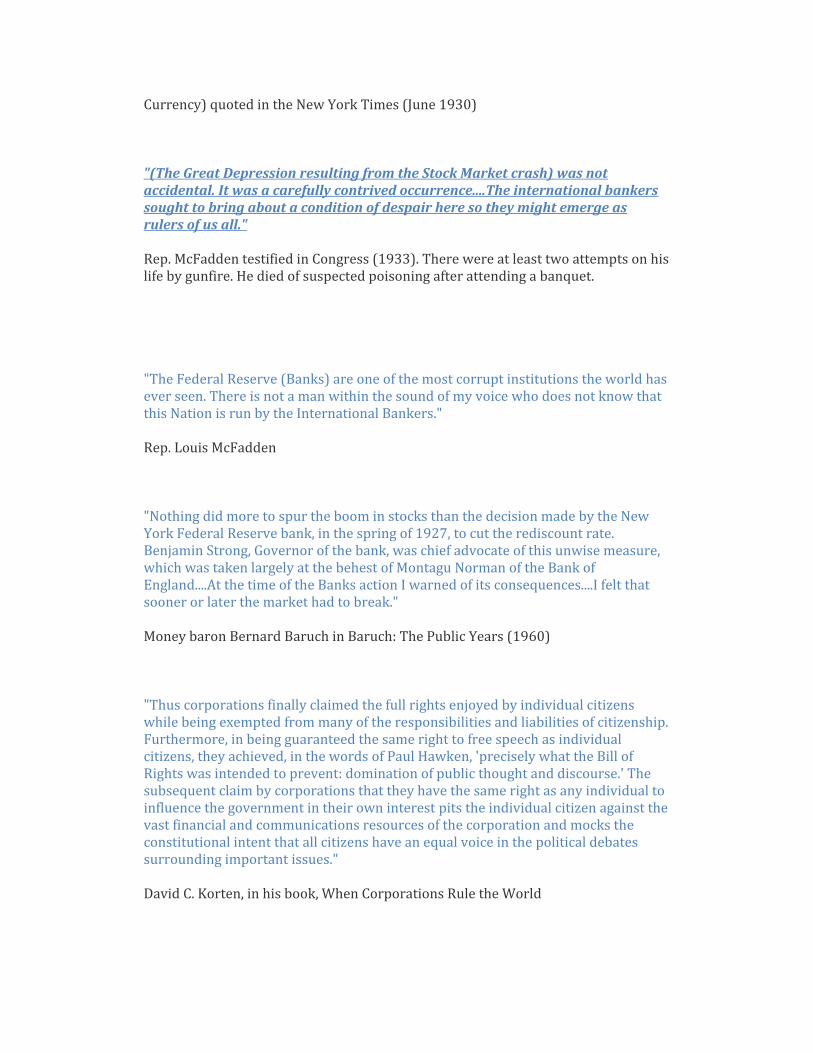

Currency) quoted in the New York Times (June 1930) "(The Great Depression resulting from the Stock Market crash) was not accidental. It was a carefully contrived occurrence....The international bankers sought to bring about a condition of despair here so they might emerge as rulers of us all." Rep. McFadden testified in Congress (1933). There were at least two attempts on his life by gunfire. He died of suspected poisoning after attending a banquet. "The Federal Reserve (Banks) are one of the most corrupt institutions the world has ever seen. There is not a man within the sound of my voice who does not know that this Nation is run by the International Bankers." Rep. Louis McFadden "Nothing did more to spur the boom in stocks than the decision made by the New York Federal Reserve bank, in the spring of 1927, to cut the rediscount rate. Benjamin Strong, Governor of the bank, was chief advocate of this unwise measure, which was taken largely at the behest of Montagu Norman of the Bank of England....At the time of the Banks action I warned of its consequences....I felt that sooner or later the market had to break." Money baron Bernard Baruch in Baruch: The Public Years (1960) "Thus corporations finally claimed the full rights enjoyed by individual citizens while being exempted from many of the responsibilities and liabilities of citizenship. Furthermore, in being guaranteed the same right to free speech as individual citizens, they achieved, in the words of Paul Hawken, 'precisely what the Bill of Rights was intended to prevent: domination of public thought and discourse.' The subsequent claim by corporations that they have the same right as any individual to influence the government in their own interest pits the individual citizen against the vast financial and communications resources of the corporation and mocks the constitutional intent that all citizens have an equal voice in the political debates surrounding important issues." David C. Korten, in his book, When Corporations Rule the World

"Give me control over a man's economic actions, and hence over his means of survival, and except for a few occasional heroes, I'll promise to deliver to you men who think and write and behave as I want them to." Benjamine A. Rooge " The Federal Reserve Bank is nothing but a banking fraud and an unlawful crime against civilization. Why? Because they "create" the money made out of nothing, and our Uncle Sap Government issues their "Federal Reserve Notes" and stamps our Government approval with NO obligation whatever from these Federal Reserve Banks, Individual Banks or National Banks, etc. H.L. Birum, Sr. American Mercury, August 1957, p. 43 "I consider the foundation of the Constitution as laid on this ground that "all powers not delegated to the United States by the Constitution, nor prohibited by it to the states, are preserved to the states or to the people. " ... To take a single step beyond the boundaries thus specially drawn around the powers of Congress is to take possession of a boundless field of power, no longer susceptible of any definition. The incorporation of a bank, and the powers assumed by this bill (chartering the first Bank of the United States), have not, been delegated to the United States by the Constitution." Thomas Jefferson - in opposition to the chartering of the first Bank of the United States (1791). "This is a staggering thought. We are completely dependent on the commercial Banks. Someone has to borrow every dollar we have in circulation, cash or credit. If the Banks create ample synthetic money we are prosperous; if not, we starve. We are absolutely without a permanent money system. When one gets a complete grasp of the picture, the tragic absurdity of our hopeless position is almost incredible, but there it is. It is the most important subject intelligent persons can investigate and reflect upon. It is so important that our present civilization may collapse unless it becomes widely understood and the defects remedied very soon." -Robert Hemphill, Credit manager of Federal Reserve Bank in Atlanta. Well. It is clear that although there has been corruption and blame enough to go around on BOTH sides of the isle; the Democratic Party has carried the day over a period of decades with regard to specific watershed Acts of Congress & Presidents that have resulted in the rights of individuals being overtaken by big impersonal Government, and the money of the very People of the United States & the Treasury of the U.S. Government being literally given over to private banking institutions.

It is incredibly ironic that although the Democratic Party has creatively obtained the reputation of being the “Party of the People” that they themselves, apparently with full knowledge, have been the agents of having sold the American system into the hands of the very wealthy.

Another email sent to us, written by an associate:

“Hi Gregg, Just a new highlight on the bank saving program bail out plan. Ted

China police here to foreclose property to recover losses: Russian economists are expressing shock today over a new United States law that will allow for the first time in that nation’s history the police forces of a foreign Nation to have law enforcement powers over their citizens. These powers are specifically being granted to China’s State Security Police who operate under the Ministry of State Security for the Peoples Republic of China by the United States as a precondition for the Chinese Governments continued purchasing of US debt as the Americans continue their desperate actions to avert their total economic collapse. China had previously ordered its banks to halt all lending to the United States, an action that would totally cripple the American banking system, and as we can read as reported by the Reuters News Service: “Chinese regulators have told domestic banks to stop interbank lending to U.S. financial institutions to prevent possible losses during the financial crisis, the South China Morning Post reported on Thursday. The Hong Kong newspaper cited unidentified industry sources as saying the instruction from the China Banking Regulatory Commission (CBRC) applied to interbank lending of all currencies to U.S. banks but not to banks from other countries. "The decree appears to be Beijing's first attempt to erect defenses against the deepening U.S. financial meltdown after the mainland's major lenders reported billions of U.S. dollars in exposure to the credit crisis," the SCMP said.” Not being understood by the American people is that China is the holder of over $1.4 Trillion of US debt backed by the mortgages on the homes and property of tens of millions these people which, in essence, makes the Chinese one of the largest holders of land in the United States, and which the Chinese government has stated they will protect ‘at all costs’. In rapid response to China’s demands that they be granted immediate access to their American properties to protect their ‘investments’, the United States is enacting a

new law titled the Emergency Economic Stabilization Act of 2008, and which in Section 101, Paragraph 7:3 chillingly states: “Designating financial institutions as financial agents of the Federal Government, and such institutions shall perform all such reasonable duties related to this Act as financial agents of the Federal Government as may be required.” The United States Federal Reserve has further notified the China Development Bank, the second largest bank in Asia and the main holder of US mortgage debt instruments, that they will be designated by the US Secretary of the Treasury as one of the financial institutions protected by this extraordinary new law, and which, according to these reports, will empower Chinese policing authorities the right to act as law enforcement officers in the United States including granting them the right to evict American citizens from homes whose mortgage debt is held by China. Unfortunately for these American people, their own public officials have totally abandoned them as the American Center for Responsive Politics has reported that the staggering amount of $2 Billion has been paid by the perpetrators of this Global financial crisis to US Lawmakers, of both political parties, to sell out their fellow countrymen as virtual economic slaves to the all powerful International corporate cartels who now rule over them. Even worse for these people is that the plan instituted and carried out over these past 40 years to erase their true history leaves virtually none of them today with the full, and monstrous, century old plan to destroy their Nation, and which began with almost the exact same economic crisis they are experiencing today, and was called the Panic of 1907, and of which we can read: “The Panic of 1907, also known as the 1907 Bankers' Panic, was a financial crisis which occurred in the United States when the stock market fell close to 50% from its peak in the previous year. At the time the economy was in recession and there were numerous runs on banks and trust companies. The panic's primary cause was a retraction of loans by a number of banks in New York City, and the sentiment quickly spread across the nation leading to the closures of both state and local banks and businesses.” So shocked were the American people by the Panic of 1907 that they allowed for the first time since their Nations founding, their lawmakers to begin the process of establishing a Central Banking System, and of which one of their founding fathers, and writer of the Declaration of Independence, Thomas Jefferson, warned all future generations of Americans: “The central bank is an institution of the most deadly hostility existing against the Principles and form of our Constitution. I am an Enemy to all banks discounting bills or notes for anything but Coin. If the American People allow private banks to control the issuance of their currency, first by inflation and then by deflation, the banks and corporations that will grow up around them will deprive the People of all their Property until their Children will wake up

homeless on the continent their Fathers conquered.” Today, and sadly, the World is now witnessing these prophetic words of Thomas Jefferson coming true. Even worse, these American people, whose ancestors laid the foundation for what was once the greatest and freest Nation on Earth, have now been reduced to what is now commonly referred to as “sheeple”, “a term of disparagement, a portmanteau created by combining the words "sheep" and "people." It is often used to denote persons who acquiesce to authority, and thus undermine their own human individuality. The implication of sheeple is that as a collective, people believe whatever they are told, especially if told so by authority figures, without processing it to be sure that it is an accurate representation of the real world around them.” It goes without saying, of course, that these Americans do not see themselves in this most truest of lights as they continue living their lives in near total ignorance of the greater catastrophes soon to befall them, all of which they have been, and are continued to be, warned about. But, they continue to laugh off, and spurn, these warnings as they continue to believe the lies being fed them by their propaganda media organs they never seem to realize are nothing but the mouthpieces for the fascist corporate forces delivering them to the slaughterhouses they will come to know all too soon. [Ed. Note: The United States government actively seeks to find, and silence, any and all opinions about the United States except those coming from authorized government and/or affiliated sources, of which we are not one. No interviews are granted and very little personal information is given about our contributors, or their

sources, to protect their safety.]”

Congressional Attempts to Control the Fed In 1937, Rep. Charles G. Binderup of Nebraska, realizing the consequences of the Federal Reserve System, called for the Government to buy all the stock, and to create a new Board controlled by Congress to regulate the value of the currency and the volume of bank deposits, thus eliminating the Fed's independence. He was defeated for re-election. Others have also tried to introduce various Bills to control the Federal Reserve: Rep. Goldborough (1935), Rep. Jerry Voorhis of California (1940, 1943), Sen. M. M. Logan of Kentucky, and Rep. Usher L. Burdick of North Dakota . Rep. Wright Patman of Texas (who was the House Banking Chairman until 1975), said in 1952: "In fact there has never been an independent audit of either the twelve banks of the Federal Reserve Board that has been filed with the Congress ... For 40 years the system, while freely using the money of the government, has not made a proper accounting." Patman said that the Federal Open Market Committee (who, in addition to the Board of Governors,

decides the country's monetary policy) is "one of the most secret societies. These twelve men decide what happens in the economy ... In making decisions they check with no one -- not the President, not the Congress, not the people." Patman also said: "In the United States we have, in effect, two governments ... We have the duly constituted Government ... Then we have an independent, uncontrolled and uncoordinated government in the Federal Reserve System, operating the money powers which are reserved to Congress by the Constitution." During his career, Patman sought to force the Fed to allow an independent audit, lessen the influence of the large banks, shorten the terms of the Fed Governors, expose it to regular Congressional review just like any other Federal agency, and to have only officials nominated by the President and confirmed by Congress to be on the Federal Open Market Committee. In 1967, Patman tried to have them audited, and on January 22, 1971, introduced H.R. 11, which would have altered its organization, diminishing much of its power. He was later removed from the Chairmanship of the House Banking and Currency Committee, which he held for years. On January 22, 1971, Rep. John R. Rarick of Louisiana introduced H.R. 351: "To vest in the Government of the United States the full, absolute, complete, and unconditional ownership of the twelve Federal Reserve Banks." He said: "The Federal Reserve is not an agency of government. It is a private banking monopoly." He was later defeated for re-election. During the 1980's, Rep. Phil Crane of Illinois introduced House Resolution H.R. 70 that called for an annual audit of the Fed (which never came to a full vote), and Rep. Henry Gonzales of Texas introduced H.R. 1470, that called for the repeal of the Federal Reserve Act. The Federal Reserve System has never been audited, and their meetings, and minutes of those meetings, are not open to the public. They have repelled all attempts to be audited. In 1967, Arthur Burns, the Chairman of the Federal Reserve, said that an audit would threaten the "independence" of the Reserve. The Fed in the 1970s and 1980s In 1979, after dismissing Secretary of Treasury Michael Blumenthal, President Jimmy Carter offered the position to American Illuminati chief David Rockefeller, the CEO of Chase Manhattan Bank, but he turned it down [as he had previously turned down the offer from Nixon]. He also turned down the nomination for the Chairmanship of the Federal Reserve Board. Carter then appointed Paul Volcker as Chairman. Volcker graduated from Princeton with a degree in Economics, and from Harvard with a degree in Public Administration. He was an economist with the Federal Reserve Bank of New York (1952-57), worked at the Chase Manhattan Bank (1957-61), was with the U.S. Treasury Department (1961-65), Deputy Under Secretary for Monetary Affairs (1963-65), Under Secretary for Monetary Affairs (1969-74), and President of the New York Federal Reserve Bank (1975-79). When Volcker was in the Nixon Administration as the Under Secretary for Monetary Policy and International Affairs, the executive branch official who works most closely with the Federal Reserve, he and Treasury Secretary John Connally helped formulate the policy that took us off the gold standard in 1971, because of the dwindling gold reserves at Fort Knox. Volcker was chosen

because he was the "candidate of Wall Street." He was a member of the Trilateral Commission, and a major Rockefeller supporter. Bert Lance, the Georgia banker and political advisor to Carter who became his Budget Director and was later forced to resign...said that if Volcker was appointed he would be "mortgaging his re-election to the Federal Reserve." Lance predicted that he would bring high interest rates and high unemployment. He was confirmed by the Senate Banking Committee in August, 1979, replacing Arthur Burns, an Austrian-born economist who was a CFR member with close ties to the Rockefellers. Volcker was against a gold-backed dollar or gold being used as a form of currency. He attempted to tighten the money situation in order to curb the 10% annual growth in the money supply, and to ease the pressure of loan demand. The result [of his policy] was a dramatic increase in interest rates, which climbed to 13.5% by September, 1979, and then soared to 21.5% by December, 1980. [We may speculate] that this economic decline was purposely engineered to cause the political decline of Carter. In response to the rising interest rates, Carter said: "As you well know, I don't have control over the Fed, none at all. It's carefully isolated from any influence by the President or the Congress. This has been done for many generations and I think it's a wise thing to do." During the 1970's, many banks had left the Federal Reserve, and in December, 1979, Volcker told the House Banking Committee that "300 banks with deposits of $18.4 billion have quit the Fed within the past 4-1/2 years," and that another 575 of the remaining 5,480 member banks, with deposits of $70 billion, had indicated that they intended to withdraw. He said that this would curtail their control over the money supply, and that led Congress, in 1980, to pass the Monetary Control Act, which gave the Federal Reserve control of all banking institutions, regardless if they are members or not. Even though inflation had skyrocketed to all-time highs, Reagan kept Volcker on. It was Volcker who started the collapse of the U.S. economy. Alan Greenspan, who became the Chairman of the Federal Reserve Board in 1987, is [also] a member of the Council on Foreign Relations. He has a bachelor's and master's degree, and a doctorate in Economics from New York University. He met Ayn Rand, the author of Atlas Shrugged, in 1952 and they became friends. It is from her that he learned that capitalism "is not only efficient and practical, but also moral." In February, 1995, the seventh increase in the interest rate, within the period of a year, took place. This put Greenspan in the limelight, as well as the Federal Reserve. It was very interesting how the media spin doctors churned out information that totally skirted the issue concerning the Fed's actual role in controlling our economy.

Is it any wonder that within 15 years of the establishment of the Federal Reserve and Federal Taxation, that the U.S. was plunged into what is known as the “Great Depression”???

Republicans will probably again go unheeded:

Rep. Michael Burgess - “we are under Martial Law”

September 28th, 2008 | Breaking News, Constitutional Crisis, Economy, Federal

Reserve

By: D. H. Williams @ 4:20 PM - EST

Rep. Michael Burgess (R-TX) reports from the floor of the House that the

Republicans have been cut out of the process and called unpatriotic for not

blindly supporting the fraudulent bailout. He says the only debate has been

about what talking points to use on the American people. The most ominous

revelation is when he claims the Speaker has declared martial law.

“I have been thrown out of more meetings in this capital in the last 24 hours

than I ever thought possible, as a duly elected representative of 825,000

citizens of north Texas.” Said Congressman Burgess.

Burgess asks the Speaker of the House to post the bailout bill on the internet for

at least 24 hours instead of passing the largest piece of legislation in US

financial history in the “dark of night.”

The most frightening part of Rep. Burgess’ one-minute floor speech is when he

says, “Mr. Speaker I understand we are under Martial Law as declared by the

speaker last night.”

The “Party of the People”.

You have to hand it to the Democratic Party. Somehow, systematically, and over several decades, the Democrats have successfully captured the minds and hearts of the American media and duped much of the general populous into believing that they are the Party that has the American poor and middle-class in mind; whereas the Republicans are for “big corporations” and “the wealthy”.

As you can clearly see, from President Wilson to President Franklin Roosevelt, to President Clinton, it has been Democratic Presidents and Congressional leaders that have taken the American economy and banking system deeper and deeper into darkness.

Discussion Draft of yet unnumbered House Resolution Bill to turn your life and liberty over to

the elitist who really control this country. Think of it as the Emancipation Proclamation in

reverse.