monthly asset class performance & outlook

TRANSCRIPT

Hedge research & strategies group

Hedge Research & strategies GroupHedge Research & Strategies GroupAdvisory Solutions

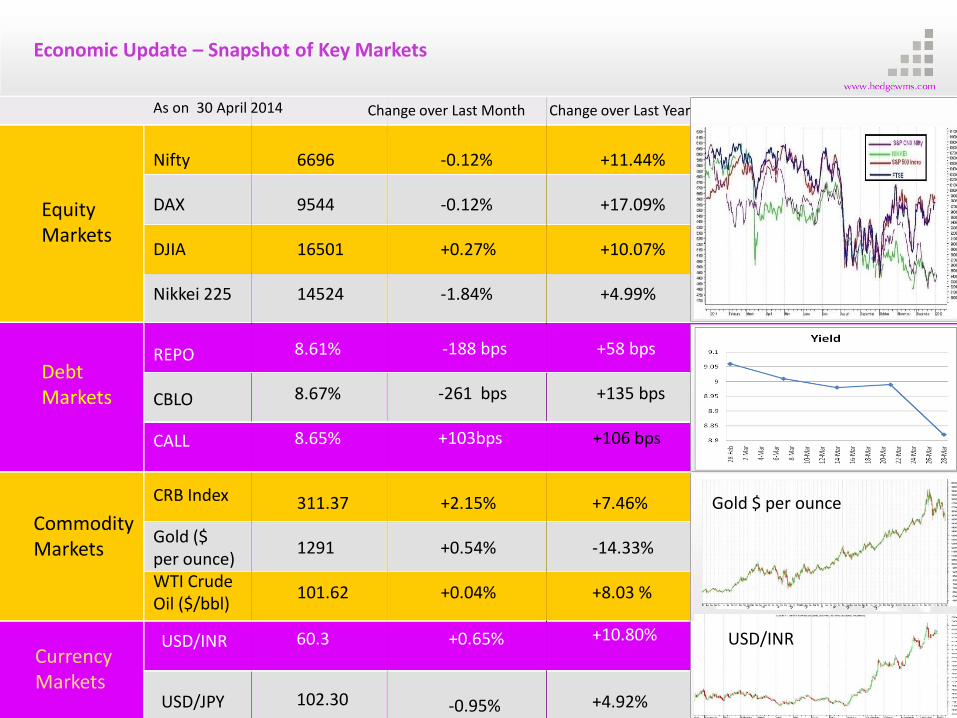

Economic Update – Snapshot of Key Markets

EquityMarkets

DebtMarkets

CommodityMarkets

CurrencyMarkets

Nifty

DAX

DJIA

Nikkei 225

REPO

CBLO

CALL

CRB Index

Gold ($ per ounce)WTI Crude Oil ($/bbl)

USD/INR

USD/JPY

60.3

102.30

+0.65%

-0.95%

+10.80%

+4.92%

6696

9544

16501

14524

8.61%

8.67%

8.65%

311.37

1291

101.62

+2.15%

+0.54%

+0.04%

+7.46%

-14.33%

+8.03 %

-188 bps

-261 bps

+103bps

+58 bps

+135 bps

+106 bps

-0.12%

-0.12%

+0.27%

-1.84%

+11.44%

+17.09%

+10.07%

+4.99%

As on 30 April 2014 Change over Last Month Change over Last Year

Gold $ per ounce

USD/INR

10 year G-Sec (8.15%) 2022 benchmark Yield10 year G-Sec (8.15%) 2022 benchmark Yield

10 year G sec 8.83% bond yield

Economic Update (Global) – April 2014

Emerging Economies

Japan

Europe

US

• • The Federal chair Jannet Yellen commented in an event that length of time the Federal Reserve keeps itskey interest rate near zero will depend on how far the U.S. economy remains from the central bank'semployment and inflation goals, and how long it will likely take to meet them.

•Initial claims for state unemployment benefits ticked up 2,000 to a seasonally adjusted 304,000 for the week ended April 12, Philadelphia Federal Reserve Bank said its business activity index increased to 16.6 this month from 9.0 in March, Retail sales and industrial production were robust in March. surge in new orders and shipments also showed the recovery of world’s largest economy.

•The European Central Bank president said , is ready to deploy anything in its monetary policy toolbox if inflation stays too low for too long despite keeping interest rates steady .

• Euro zone private sector started the second quarter on its strongest footing since 2011. Growth in the euro zone was again led by Germany, the bloc's largest economy, where the PMI jumped from March and was just shy of February's 32-month high. Markit's flash composite PMI, widely regarded as a good gauge of growth, jumped to 54.0 in April from March's 53.1

• Japan raised its sales tax rate from 5 percent to 8 percent, marking the first sales tax hike in 17 years. First step of the two-stage tax hike is aimed at covering swelling social security costs for the country's aging society, which would help increase government tax revenues and restore the nation's fiscal health.

• Japan’s Trade Deficit Widens as Export Growth Weakens. Japan’s weakest export growth in a year spurred a wider-than-forecast trade deficit in March, adding to challenges for Prime Minister Shinzo Abe in steering the economy through the aftermath of sales-tax rise.

• China acted for the first time this year to steady its stumbling economy by cutting taxes for small firms on and announcing plans to speed up the construction of railway lines.

• China Manufacturing Gauge Signals Economic Weakness for the past few months. China is trying to balance supporting growth with curbing shadow banking, eliminating overcapacity and reducing pollution

US

EUROPE

ASIA

CHINA

U.S

EUROPE

ASIA

CHINA

Equity Market Review – April 2014

Indian markets are witnessing a bullish trend for the month as Opinion polls stating a Modi led BJP government in power is attracting

strong capital Inflows into the country . RBI in its bi-monthly meet kept the key rates unchanged. Geopolitical tension in Ukraine ,

uncertainty over the fed interest rates slow growth in China have been the major events in the global front. RBI gave banking license to

Bandhan financial services and IDFC after it got node from election commission .

• Reserve Bank of India (RBI) in its first Bi-monthly Monetary Policy statement 2014-15 announced on 1 April 2014, kept the policy repo rate unchanged at 8.0%. Other policy instruments such as cash reserve ratio also remain unchanged at 4%. Increase the liquidity provided under 7-day and 14-day term repos from 0.5 per cent of net demand and time liabilities (NDTL) of the banking system to 0.75 per cent

•India's annual consumer price inflation in March inched up to 8.31 per cent from 8.03 in February, mainly on account of a rise in fruit

and vegetable prices. India's wholesale prices-based inflation accelerated to a three-month high of 5.70 percent in March, driven up

by increases in food and fuel costs.

• India's Index of industrial production (IIP) dipped 1.9% in February 2014, snapping 0.8% growth recorded in the previous month.

Driven by a decline in consumer goods ,capital goods and manufacturing goods growth . Mining sector, basic goods ,intermediate

goods and electricity rose for the month.

• India's trade deficit widened in March on a sharp fall in exports, which would further ease pressure on the country's current account

balance. The trade deficit stood at $ 10.50 billion, almost five months high.

• Foreign institutional investors (FIIs) have bought stocks worth a net $ 1.19 billion (around Rs 7,191 crore) till 23 April.

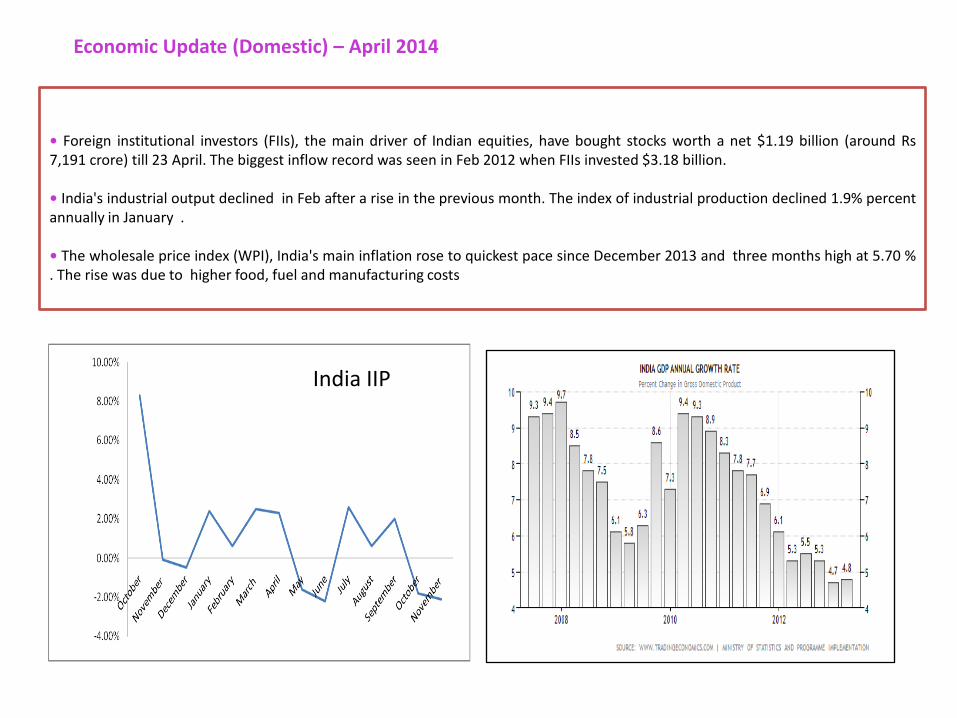

Economic Update (Domestic) – April 2014

• Foreign institutional investors (FIIs), the main driver of Indian equities, have bought stocks worth a net $1.19 billion (around Rs7,191 crore) till 23 April. The biggest inflow record was seen in Feb 2012 when FIIs invested $3.18 billion.

• India's industrial output declined in Feb after a rise in the previous month. The index of industrial production declined 1.9% percentannually in January .

• The wholesale price index (WPI), India's main inflation rose to quickest pace since December 2013 and three months high at 5.70 %. The rise was due to higher food, fuel and manufacturing costs

INDIA IIPIndia IIP

Sectors Under our Research Radar

• Metal

• Banking & Financial Services.

• IT & IT Enabled Services

• FMCG

• Automobiles & Ancillaries

• Capital Goods

• Telecom

• Oil & Gas

• Pharma

Metal sector

• Metal sector is sluggish on global economic scenario and on concerns of decline in industrial demand because of falling Purchasing managers Index (PMI’s) & slowing global growth.

• Indian metal companies are affected because of low demand as high inflation rates & tight monetary policy along with low government spending affects the sector. The international metal prices has turned lower and the other input costs have rose which is putting more pressure on companies which will reduce the operating margin.

Metals & Mining Sector

Global Scenario• Metal sector has lately seen some green shoots in global economy. This is boosting sentiment that economicrecovery is on the cards and demand is set to improve. Strong manufacturing PMI from China and Europe ispositive for the sector. On the LME and other metal markets, base metal have fallen sharply since the start ofthis year. However off late it is seeing some stability on the back of positive economic data from majordeveloped economies.

Indian Scenario• The metal & mining companies has been struggling because of subdued demand. The prices of metals havedropped on the LME as well. However sharp depreciation in Indian rupee is expected to benefit thesecompanies.

• India steel sector is said to grow by 3% this year. An added advantage is that the court has ordered theopening of the B grade mines in Karnataka. With the new import tax of 2.5%, the opening of the mines willoffer some support to the prices.

STOCK IN FOCUS : Hindalco

• Hindalco is advisable for aggressive long term investors because of its attractive valuations. With itssubsidiary Novelis performing well and immune to metal prices is positive for the company in the currentweak economic scenario. Though some concerns prevail in domestic business, it is expected to be in shortterm and over long term its growth is intact. Investors can start buying the stock at the current levels andaccumulate at the lower levels for investment target of Rs. 150.

Banking & Financial Services sector

Current Scenario

• RBI’s steps has been reflecting in currency markets where rupee has strengthened and stability is seen. RBIhas eased Marginal standing facility rates to ease the borrowing cost for banks and companies.

• RBI increased the repo rate by 25 bps in January meet to keep a check on rising core inflation and tostimulate growth in the economy.

STOCK IN FOCUS: Union Bank

• Aggressive investors can consider an investment in the UBIL stock. The bank posted decent results forQ2FY14. The pace of loan growth only came in at 17% yoy for Q4 vs 21% yoy for Q3. This led to NII growth of11% yoy. NIMs saw a decline from 3% to 2.89% and the management attributed this to high cost of funds andinterest rate cuts on the base rate and the sectoral rates. Other income growth came in at 8% but this wasmainly led by treasury income growth of 79% yoy, The bank was boosted by profits on the sale of itsinvestments that grew by 85% yoy. However the core fee based income declined by 4% yoy. Operating costsrose by 13% yoy. The asset quality performance was mixed. NPA position continues to improve and this bodeswell going forward as there will be less interest income reversals and lower credit costs Infact Gross NPAs havebeen trending lower since Q1FY13. Absolute Gross NPAs which stood at Rs. 6541 crores in Q1FY13 havedeclined every quarter since and in Q4FY13 came in at Rs. 6313 crores (In Q3FY13 it stood at Rs. 3168 crores)..With regards to valuations we continue to maintain our BUY rating with price target of Rs.150

Information Technology & IT enabled service Sector

Current scenario

• Indian IT Industry is expected to benefit for short term from Indian Rupee which depreciated close to 6% inJune. Economic conditions are lot better now as Euro zone is stabilizing and on improved economic data fromUnited States.

• gradual revival in the outsourcing demand in the US and the European market helped Indian IT players toresume on the growth path. This strong momentum in the business is reflected in their valuations, which havesoared sharply compared with their year-ago levels . First, the December and the March quarters aretraditionally weak for IT companies due to the festive holidays and the annual exercise carried by client firms toascertain IT budgets for the next year. IT players typically report a sequential volume growth of 1.5-3% duringthis period, compared with more than 3% increase in the first two quarters.

STOCK IN FOCUS:

We are not profiling any stock in the IT sector.

Auto & Ancillary sector

Current Scenario

• Auto sector is facing the worst sales streak in over a decade.

• Auto is also facing multiple headwinds such as an increase in raw material cost, increase in cost of operationsand high interest costs. Increase in excise duty on vehicles was impose during the budget.

• In the recent credit policy meet RBI has decided to leave the rates unchanged, but the lending rates are notlowered by backs. Auto companies posted lower than expected results this quarter.

STOCK IN FOCUS : Maruthi Suzuki

The company posted strong results for Q4FY13 buoyed by higher sales of new models such as Ertiga, Dzire andSwift, operating efficiencies and the benefit of a favourable exchange rate. As was the case with other playersMSIL’s sales volume declined by 4.6% yoy but average price realizations grew by an impressive 14.4% yoy and0.2% qoq taking total sales growth rate to 9.4% yoy. Diesel vehicles now account for 58% of MSIL’s sales mix andhelped boost realizations. Besides discounts for the quarter dropped from the Q3 level of Rs. 12000 to Rs.10000.Traditionally MSIL has been able to perform rather well in a falling market and FY13 was no exception. Whileindustry volumes declined by 2.2% for the full year, MSIL’s sales volumes rose by 4.4%. The company alsoimproved its market share by 1% to 39.5% in FY13. Operating profits rose by a whopping 108% yoy whileoperating profit margins rose by 3% yoy to reach 10.7% The company received a boost by way of yendepreciation relative to the dollar and this added 1.3% to the operating profit margin. PAT growth came in at79% yoy. With regard to valuations we maintain our HOLD rating with our target price of Rs.1885.

Fast Moving Consumer Goods (FMCG)

Current scenario

• Fast moving consumer goods sector is in neutral to positive mode as investors are already churning out stocks

from defensive to cyclical on positive sentiment into the new year. Valuation wise, FMCG is currently on the

higher side compared to forward earnings and with high input costs the margins are expected to be squeezed.

• Good volume numbers in last quarter is however indicating strong demand for FMCG companies and the

easing inflation is big positive for the FMCG companies as the margins for the company will improve in future.

STOCK IN FOCUS :

• FMCG companies are currently over valued and major FMCG companies are trading around 35 times to its FY

14 earnings. Volumes saw a growth below market expectations in the second quarter of FY 13 and their

promotional and advertisement expenses are expected to inch up higher in next couple of quarters however

the decline in the input costs will aid margins to improve.

Capital Goods &, Engineering & power

Current scenario

• Capital goods & Power sector has been affected by macro economic headwinds such as availability of coal,high cost of raw materials & weak order book.

• Capital goods & Engineering sector is expected to benefit form the FY 14 infra targets of Rs.1.15 lakh croreset by Prime minister. Target is to roll out projects worth Rs 1.15 lakh crore in public-private-partnershipmode by the end of this calendar year, including setting up 60 airports. The other major projects includemonitoring the construction of Mumbai's Rs 30,000 crore elevated rail corridor and power and transmissionprojects worth Rs 40,000 crore.

STOCK IN FOCUS: L&T

•Larsen & Toubro Limited is an Indian multinational conglomerate headquartered in Mumbai, India. Thecompany has business interests in engineering, construction, manufacturing, information technology andfinancial services. Larsen is a company which has a strong brand name and track record mainly on theengineering and construction. Larsen and Toubro posted net sales went up by 26.11% to Rs.12078.33crore infirst quarter of FY13 from Rs.9577.87crore in the same quarter FY12. Engineering & Construction segment,which contributing 86.87% to the total revenue, increased for the period by 30% to Rs.10489.76 crore. Evenafter the other income increased by 124.64% to Rs.605.84crore the operating profit margin contracted andreported only 19.37% growth. Valuation based on the DCF method suggesting a fair value of Rs.1379/share.An investor with moderate profile can consider a buy at Rs.1104 with 20% margin of safety.

Telecom Sector

Current Scenario

• The Department of Telecom is hoping to announce the new M&A guidelines next month as it attempts toinfuse life into a sector battered by controversies. Telecom sector now looks stable and seems back on itsfeet with initial investment proposal of over Rs 11,000 crore received in 2013.

• While government is hopeful of announcing mergers and acquisitions guidelines in January and a newpolicy on machine-to-machine communications in first quarter of 2014, in 2013 it was able to implementnew licensing regime of Unified Licences, open up telecom sector for foreign investment by raising FDI limitto 100 percent from 74 percent.

• The government is gradually addressing concerns related to the industry but at the same time there has tobe a balance between compliance with rules and consumers interests.

STOCK IN FOCUS

• Currently we do not advise any stock for the month in telecom sector because of regulatory uncertanity.

Oil & Gas Sector

Current Scenario• Government increased the gas prices to $8.4/mmbtu from April next year will incentivise investment inthe oil & gas sector which will reduce the energy import bill. The revision in gas price will bring in muchrequired technology and risk capital from foreign majors to tap vast unexplored resources in deep and ultradeep water frontiers basins.

• India plans to relax rules for oil and gas exploration licenses in time for the next bidding round, so as toattract global companies. In the past, regulatory uncertainty discouraged many of them from bidding forexploration blocks.

STOCK IN FOCUS :Petronet LNG

• PLL has showcased a good performance over the last couple of quarters on the back of good numbers itdisclosed. The company’s strong business model (stable re-gasification margins and term con-tracts),expanding volumes on account of strong demand estimates, higher marketing margin for spot cargoes due tohuge demand-supply gap in natural gas, expected long-term contracts from Gaz-prom and other sources forKochi terminal and Dahej expansion hold it in good stead and make an impressive bet for the long term. PLLposted net sales for the second quarter of FY 13 went up by 41.03% to Rs.7487.89crore from Rs.5309.40crore in the previous year same quarter. EBIDT margin excluding Other income decreased from 8.35% to5.36% due to 46.76% rise in the raw material cost but Rs.138.87crore other income (forex gain –Rs.114.10)helped the company to post highest quarterly net profit of Rs.314.79crore against Rs.260.34crore in thesecond quarter last fiscal. Commissioning of Kochi terminal is expected to be in the last quarter of currentfiscal but the operation will be in full capacity by the second half of FY14 due to delay in pipelineconstruction. We had a buy rating in the stock previously and reached target level. Based on our DCFvaluation, we have a 12 month price target for the stock of Rs 186/ share. An investor with moderate riskprofile can consider a buy on this stock at or below Rs.143 levels which provides a 20% margin of safety to itscurrent fair Value.

Pharmaceutical Sector

Current Scenario

• Pharma sector is highly linked to government regulations as structural changes are undergoing in the

sector. Pharma sector is growing at a good phase compared to global pharma sector and the production

costs are almost 50 percent lower in India than in Western nations, while overall R&D costs are about one-

eighth and clinical trial expenses are around one-tenth of Western levels which are positive for the sector.

• In long term, the pharma sector is one of the preferred sector as it offers huge scope for development as

low production costs give India an edge over other generics-producing nations, especially China.

STOCK IN FOCUS: Dr. Reddy

• We are not profiling any stock for the sector.

Debt Overview & Outlook

Debt Market update

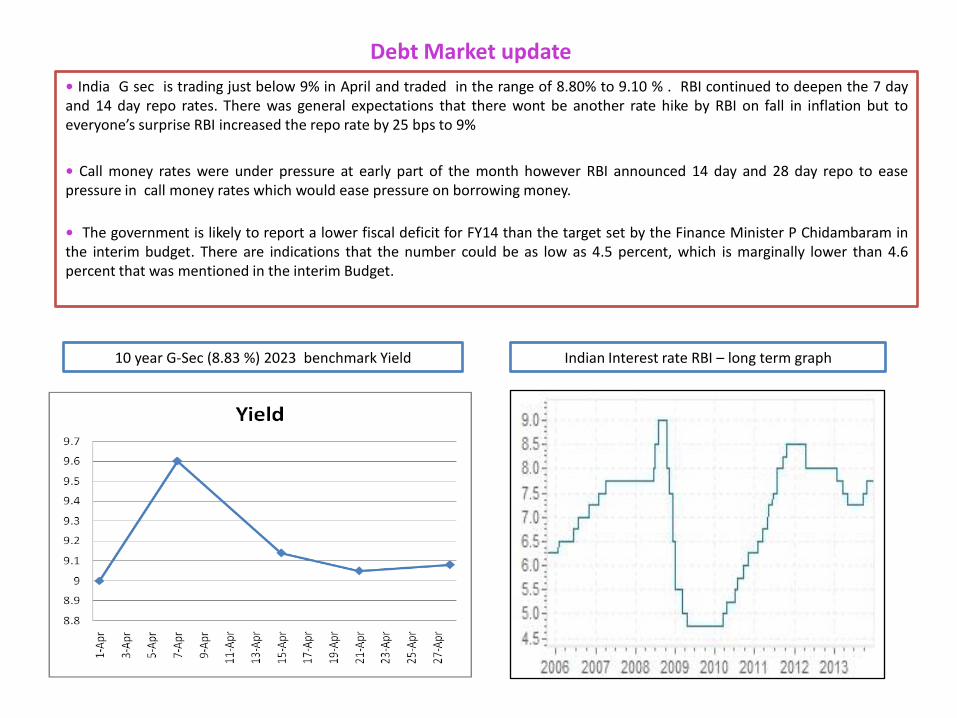

• India G sec is trading just below 9% in April and traded in the range of 8.80% to 9.10 % . RBI continued to deepen the 7 dayand 14 day repo rates. There was general expectations that there wont be another rate hike by RBI on fall in inflation but toeveryone’s surprise RBI increased the repo rate by 25 bps to 9%

• Call money rates were under pressure at early part of the month however RBI announced 14 day and 28 day repo to easepressure in call money rates which would ease pressure on borrowing money.

• The government is likely to report a lower fiscal deficit for FY14 than the target set by the Finance Minister P Chidambaram inthe interim budget. There are indications that the number could be as low as 4.5 percent, which is marginally lower than 4.6percent that was mentioned in the interim Budget.

Indian Interest rate RBI – long term graph10 year G-Sec (8.83 %) 2023 benchmark Yield

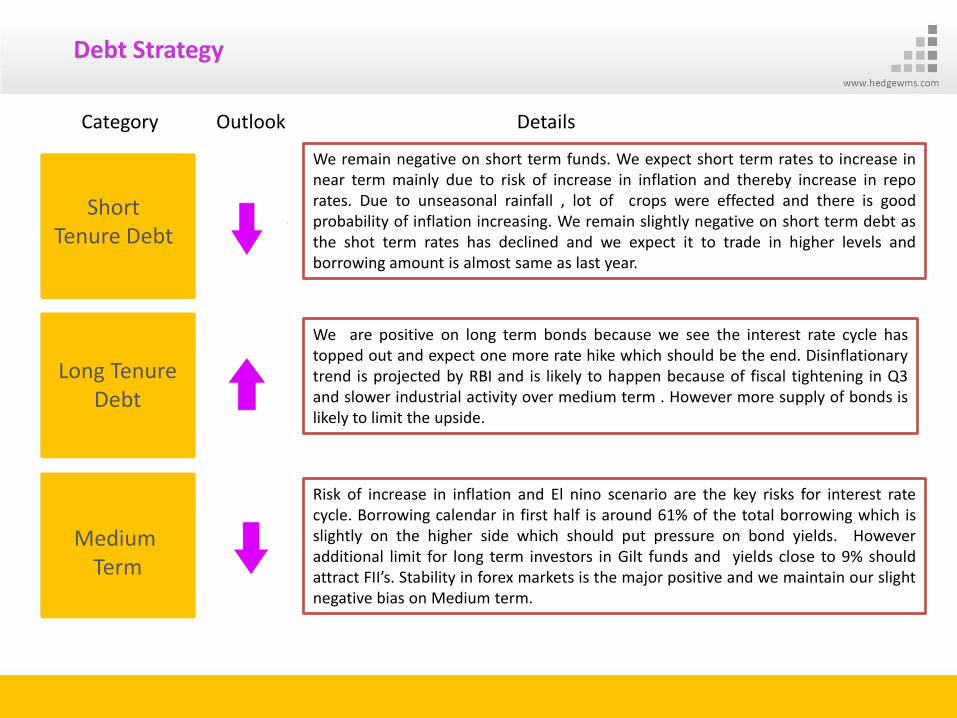

Debt Strategy

We remain negative on short term funds. We expect short term rates to increase innear term mainly due to risk of increase in inflation and thereby increase in reporates. Due to unseasonal rainfall , lot of crops were effected and there is goodprobability of inflation increasing. We remain slightly negative on short term debt asthe shot term rates has declined and we expect it to trade in higher levels andborrowing amount is almost same as last year.

We are positive on long term bonds because we see the interest rate cycle hastopped out and expect one more rate hike which should be the end. Disinflationarytrend is projected by RBI and is likely to happen because of fiscal tightening in Q3and slower industrial activity over medium term . However more supply of bonds islikely to limit the upside.

Risk of increase in inflation and El nino scenario are the key risks for interest ratecycle. Borrowing calendar in first half is around 61% of the total borrowing which isslightly on the higher side which should put pressure on bond yields. Howeveradditional limit for long term investors in Gilt funds and yields close to 9% shouldattract FII’s. Stability in forex markets is the major positive and we maintain our slightnegative bias on Medium term.

ShortTenure Debt

Long Tenure Debt

Medium Term

Category Outlook Details

Commodities – Outlook & Strategy

BULLIONS – Outlook & Strategy

• Spot gold prices in international market reached levels close

to $1280 levels however it s was unable to breach the level of

1400 on the the back of negative news flow for Gold. Federal

reserve decision to hike interest rate hike sooner than expected

was set back for bullion. Easing tensions between Russia and

West was also other reason for the gold to decline.. Outlook:

Gold is expected to remain weak and volatile due to issues on

the back of strong economic data from US after weather related

issues. Fed’s decision to withdraw QE 3 from the market is also

concern.

• Silver prices declined with negative bias. Silver on technical

side trading just below the important level of 20 and is trading

around $19.39 an ounce. Bargain hunting is expected to

provide some support to the falling silver prices. Strong

manufacturing activity in Euro zone is supporting silver prices.

Outlook: Silver is expected to remain volatile due to issues

such as Fed’s decision to withdraw QE3 from the market and

recent weakness in Global economic data. . Bargain hunting is

expected to arise after steep decline in prices on strong

manufacturing demand.

As on 31 April 2014

SILVER

GOLD

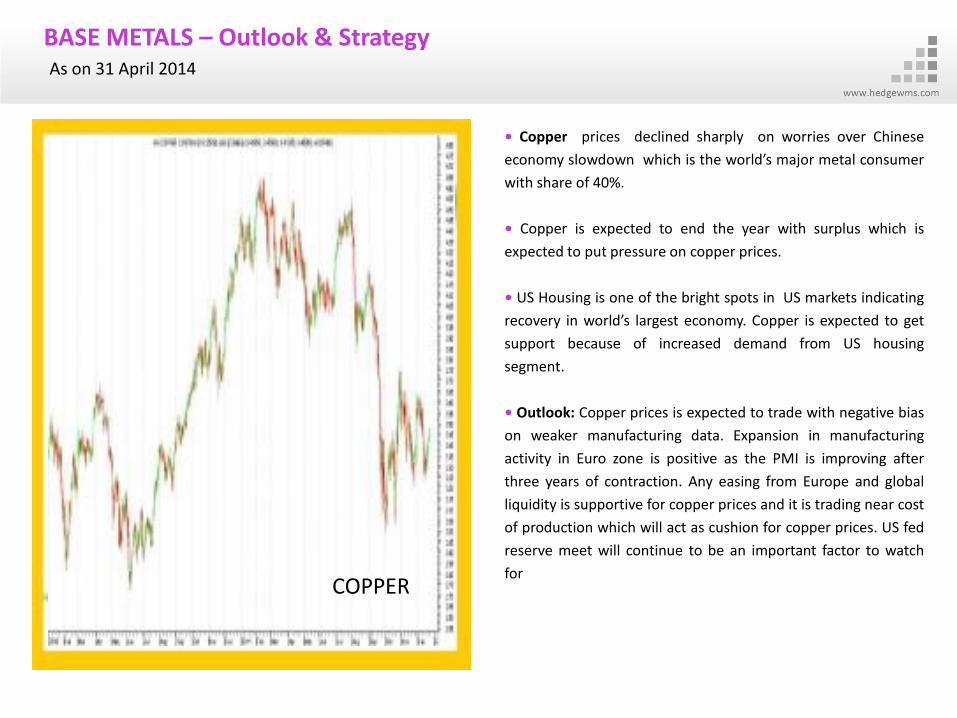

BASE METALS – Outlook & Strategy

• Copper prices declined sharply on worries over Chinese

economy slowdown which is the world’s major metal consumer

with share of 40%.

• Copper is expected to end the year with surplus which is

expected to put pressure on copper prices.

• US Housing is one of the bright spots in US markets indicating

recovery in world’s largest economy. Copper is expected to get

support because of increased demand from US housing

segment.

• Outlook: Copper prices is expected to trade with negative bias

on weaker manufacturing data. Expansion in manufacturing

activity in Euro zone is positive as the PMI is improving after

three years of contraction. Any easing from Europe and global

liquidity is supportive for copper prices and it is trading near cost

of production which will act as cushion for copper prices. US fed

reserve meet will continue to be an important factor to watch

for

As on 31 April 2014

COPPER

ENERGY & AGRI – Outlook & Strategy

• WTI Crude oil prices consolidated with positive bias. It is

supported by launch of TransCanada pipeline which is push more

crude from Cushing Oklahoma to the southern refineries which

will increase the usage of WTI crude oil and reduce the import of

Brent crude. Tension eased between Russia and west which lead

to cooling off prices however strong economic data and pipeline

supported the prices. Outlook: Crude price is expected to be

volatile for the coming months. Positive economic data from US

and Geo political tensions is expected to support oil prices . US

federal reserve decision is expected to have effect on oil prices.

• Rubber prices saw a drop in global prices. This was mainly due

to supply concerns as the tapping season is set to come to a halt

by the end of the month. Rubber prices rose last month following

the government decision to hike the import duty to 20% or Rs 30

per kg from the earlier Rs 20 per kg. Rubber growers had feared

that rubber prices may fall below cost of production if the

situation continued and even the Rubber Board had

recommended a temporary ban on imports. Outlook : We expect

rubber prices to trade with negative bias concerns over global

growth. Especially after recent disappointing growth data from

big economies.

As on 31 April 2014

CRUDE OIL

RUBBER

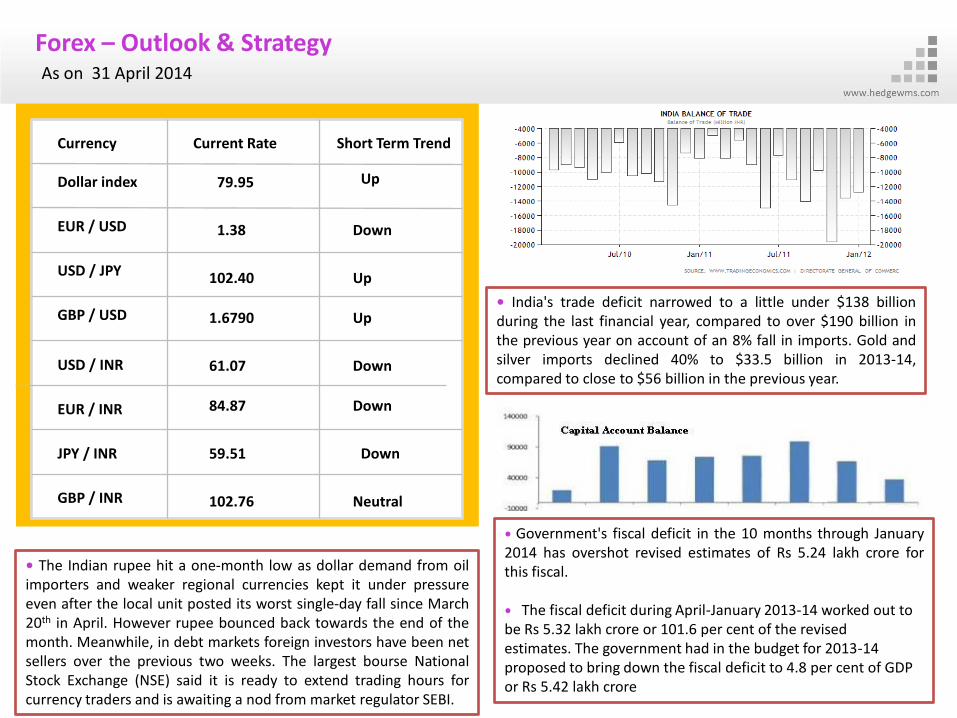

Forex - Outlook & Strategy

Forex – Outlook & StrategyAs on 31 April 2014

• Government's fiscal deficit in the 10 months through January2014 has overshot revised estimates of Rs 5.24 lakh crore forthis fiscal.

• The fiscal deficit during April-January 2013-14 worked out to be Rs 5.32 lakh crore or 101.6 per cent of the revised estimates. The government had in the budget for 2013-14 proposed to bring down the fiscal deficit to 4.8 per cent of GDP or Rs 5.42 lakh crore

Cu

Currency Current Rate Short Term Trend

Dollar index 79.95 Up

EUR / USD 1.38 Down

USD / JPY 102.40 Up

GBP / USD 1.6790 Up

USD / INR 61.07 Down

EUR / INR 84.87 Down

JPY / INR 59.51 Down

GBP / INR 102.76 Neutral

• The Indian rupee hit a one-month low as dollar demand from oilimporters and weaker regional currencies kept it under pressureeven after the local unit posted its worst single-day fall since March20th in April. However rupee bounced back towards the end of themonth. Meanwhile, in debt markets foreign investors have been netsellers over the previous two weeks. The largest bourse NationalStock Exchange (NSE) said it is ready to extend trading hours forcurrency traders and is awaiting a nod from market regulator SEBI.

• India's trade deficit narrowed to a little under $138 billionduring the last financial year, compared to over $190 billion inthe previous year on account of an 8% fall in imports. Gold andsilver imports declined 40% to $33.5 billion in 2013-14,compared to close to $56 billion in the previous year.

Trade balance and export - import data

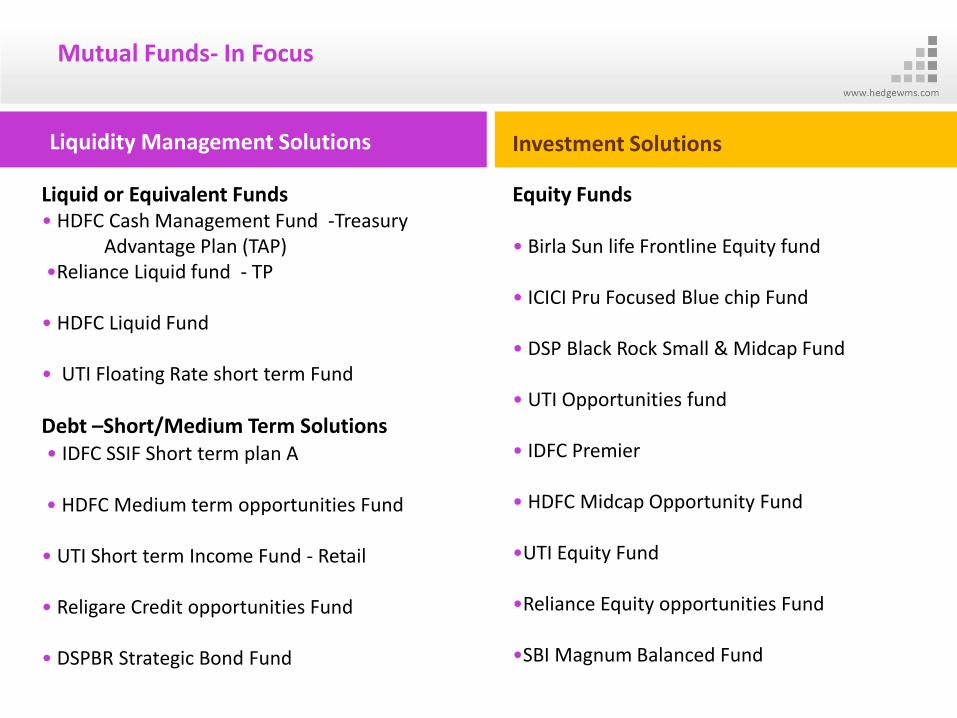

Mutual Funds- In Focus

Liquidity Management Solutions Investment Solutions

Liquid or Equivalent Funds• HDFC Cash Management Fund -Treasury

Advantage Plan (TAP)•Reliance Liquid fund - TP

• HDFC Liquid Fund

• UTI Floating Rate short term Fund

Debt –Short/Medium Term Solutions• IDFC SSIF Short term plan A

• HDFC Medium term opportunities Fund

• UTI Short term Income Fund - Retail

• Religare Credit opportunities Fund

• DSPBR Strategic Bond Fund

Equity Funds

• Birla Sun life Frontline Equity fund

• ICICI Pru Focused Blue chip Fund

• DSP Black Rock Small & Midcap Fund

• UTI Opportunities fund

• IDFC Premier

• HDFC Midcap Opportunity Fund

•UTI Equity Fund

•Reliance Equity opportunities Fund

•SBI Magnum Balanced Fund

Hedge Equities is an established retail and institutional financial service provider in India, with Head Quarters at Kochi with PAN –India presence of more than 130 retail outlets and an overseas office in Dubai. The service folio of Hedge Equities include Equity, Mutual Funds, Derivatives, Commodities, Currency, Fixed Income Securities, Depository Services, Clearing Services, Margin Funding, Fundamental and Technical Research Support & Wealth Management Services (Hedge WMS)

SEBI Registered Portfolio Manager

Dedicated Team of Portfolio Managers & Dealers

Strong in - house Research Team

Investment options across the full risk - reward scale

Disciplined & Rational Investment approach

Hedge Wealth Management Services (WMS)

Hedge WMS is designed exclusively for the discerning investor who desires customized & research oriented rational investment solutions. As a SEBI Registered Portfolio Manager, Hedge Equities through its WMSdivision helping investors to Build, Manage & Grow their Wealth. The company ushers investors to higher growth terrains by formulating novel investment option across full risk- reward scale. Disciplined, Rational & Objective investment approach derived from intensive research are hallmark of Hedge WMS.

The foundation of Hedge WMS is our belief that our customer’s needs are of paramount importance and investments should be tailored to meet their unique needs, requirements & risk appetite. We know that our approach to the management of wealth must reflect our investor’s depth and breadth of needs.

To this end, we help develop a strategy that evaluates your complete financial needs and provide solutions through efficient cash & asset allocation, dynamic rebalancing, strong research & a diversified investment portfolio to minimize risk and maximize return. It is our conviction that we can combine our research insights, market reach and a culture of information sharing with an unwavering focus on risk management to deliver a real return to investors after inflation and taxes

Hedge Equities Research reports

• Morning Report

• Monthly Report

• Company Analysis Reports

• Daily Economic Reports

• Daily Commodities Report

• Daily Currency Report

Hedge Equities Research & Strategies Team

Head of Research: Krishnan Thampi K

Sr. Technical Analyst: Anish .C

Jr. Fundamental Analyst : Jasna

Fundamental Analyst : Shajan. KS

Economic & Commodity Analyst: Vignesh SBK

Reach us at [email protected]

Disclaimer

This document does not solicit any action based on the material contained herein, Hedge Equities Ltd ("the Portfolio Manger") will nottreat recipients as clients by virtue of their receiving this presentation. The recipient of this material alone shall be responsible / liablefor any decision taken on the basis of this material The distribution of this presentation in certain jurisdictions may be restricted ortotally prohibited to registration requirements and accordingly, persons who come into possession of this presentation are required toinform themselves about and to observe any such restrictions and/ or legal compliance requirements Persons who may receive thispresentation should consider and independently evaluate whether it is suitable for his/ her/ their particular circumstances and arerequested to seek professional financialadvice. Past performance is not a guide for future performance Future returns are notguaranteed and a loss of principal may occur The company and its affiliates accept no liabilities for any kind of damage arising out ofthis presentation With respect to all information found in this presentation, the company and its directors, officers, agents, oremployees and its affiliates make no warranty, express or implied, including the usefulness of any information contained therein andthe presentation shall not be liable for any indirect, incidental or consequential damages sustained or incurred in connection with theuse, operation, or usability to use this presentation and information contained therein Under no circumstances will the company beliable for any loss or damage caused by anyone's reliance on information contained in this presentation

RISK FACTORS -All securities investments are subject to market risks and there can be no assurance that the Objectives of the portfolio (s) will beachieved Each portfolio will be exposed to various risks depending on the investment Objective, investment philosophy, investmentstrategy and the capital markets, interest rates, currency exchange rates, changes in laws/policies of the government, taxation laws,political, economic or other developments, general decline in the Indian Markets, which may have adverse impact on individualsecurities, a specific sector or all sectors. Further, the investments by the portfolio shall involve investment risks such as tradingvolumes, settlement risk, liquidity risk, default risk including the possible loss of capital, The portfolio with investment objective toinvest in a specific sector/ industry would be exposed to risk associated with such sector/ industry and its performance will bedependent on performance of such sector/ industry The decisions of Portfolio manager may not always be profitable. Investors of thePortfolio Management Services are not offered by guaranteed assured returns. The Portfolio Manager may invest in shares, debt, unitsof mutual funds, deposits or other financial instruments of associate/ group companies, The name of the portfolios does not in anymanner indicate either the of the product or their future prospects and returns, Investors are advised to read the risk factors given inthe Portfolio management Services Agreement and Disclosure Document before investments

Hedge Research View & January 2012 Monthly Outlook

Economic Update – Domestic & Global

Equity

Debt

Commodity

Mutual Funds & Liquidity Solutions

Currency

Real Estate

You can reach us at [email protected]