money & central banks chapter 2, 15,16. quantity theory simplest monetary theory is the quantity...

TRANSCRIPT

Money & Central Banks

Chapter 2, 15,16

Quantity Theory

• Simplest monetary theory is the Quantity Theory of Money.– Purchasing power of money is equal to the

quantity of money (Mt) times the speed of circulation (V, # of transactions)

– Purchasing power means # of goods (Yt) multiplied by price per good (Pt)

Moneyt * Velocity = Pt * Yt

Rule of Thumb

• Rule of Thumb The growth rate of product is approximately equal to the sum of the growth rates of the elements of a product.

Z X Yt t t t t tZ X Y g g g

1

1

Z t tt

t

Z Zg

Z

Money and Inflation

• Assuming stable velocity

• Inflation occurs when money growth speeds ahead of output growth. The unbounded creation of fiat money leads to inflation which ultimately will make the money worthless.

M Y Pt t t t tg g g

Money & Inflation: 1975-1994

Inflation & Money OECD Countries

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18

Average Money Growth

Ave

rag

e In

flat

ion

Rat

e

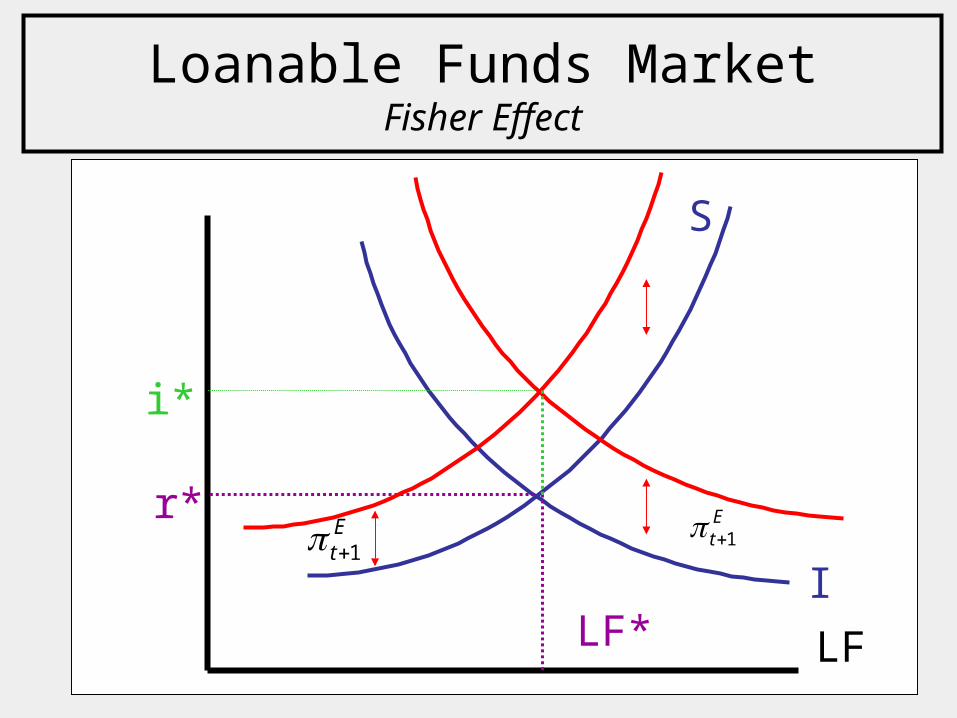

Ex Ante Rate and the Fisher Effect• Savings and investment decisions must be

made before future inflation is known so they must be made on the basis of an ex ante (predicted) real interest rate.

• Fisher Hypothesis: Ex ante real interest rate is determined by forces in the financial market. Money interest rate is just the real ex ante rate plus the market’s consensus forecast of inflation.

1EA FORECAST

t t ti r

Great Inflation of the 1970’sUS Inflation Rates & Interest Rates

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00M

ar-5

5

Mar

-58

Mar

-61

Mar

-64

Mar

-67

Mar

-70

Mar

-73

Mar

-76

Mar

-79

Mar

-82

Mar

-85

Mar

-88

Mar

-91

Mar

-94

Mar

-97

Mar

-00

Mar

-03

%

Interest Rates

Inflation

Source: St. Louis Federal Reserve http://research.stlouisfed.org/fred2/

Fisher Effect: OECD Economies Great Inflation of 1970’s

0

2

4

6

8

10

12

14

16

18

20

0 2 4 6 8 10 12 14 16 18

Average Inflation 1970-1984

Inte

rest

Rat

es-1

984

Loanable Funds MarketFisher Effect

S

I

LF

r*

LF*

1Et

1Et

i*

Ex Ante vs. Ex post

• We can also examine the ex post real return on a loan as the money interest rate less the actual outcome for inflation.

• The gap between actual and forecast inflation determines the gap between the ex post (actual) and ex ante (forecast) return.

1ExP ACTUAL

t t tr i

1 1ExP ExA FORECAST ACTUAL

t t t tr r

Unexpected Inflation Winners and Losers

– Higher than expected inflation means ex post real rates are lower than ex ante. Borrowers are winners/lenders are losers.

– Lower than expected inflation means ex post real rates are higher than ex ante. Lenders are winners/borrowers are losers.

Inflation Risk

• When inflation is variable, lenders will demand some premium for inflation risk. This will put cost on borrowers.

• High inflation rates tend to be associated with unpredictable inflation.

Costs of Anticipated Inflation

• Shoe Leather Costs – Money is a technology for engaging in transactions. The greater is inflation, the greater the cost for individuals of holding money. Individuals must make efforts as a substitute for the convenience of holding money.

• Menu Costs – Firms must engage in costs of changing posted prices. More generally, when prices change rapidly over time, more time and effort must be put into calculating relative prices.

The Inflation Tax

• Banknotes do not pay interest. • The real interest rate on banknotes is

• If inflation is high, currency has sharply negative returns. People will avoid holding money leading to society losing the convenience of money transactions.

1CASH

t tr

Inflation Tax

• Government prints money which can be used to finance expenditures: Mt – Mt-1 .

• What fraction of GDP can be collected?1 1

11

1

1

Mt t t t

t t t Mt t t

M M M gM M M GDP

M M g V

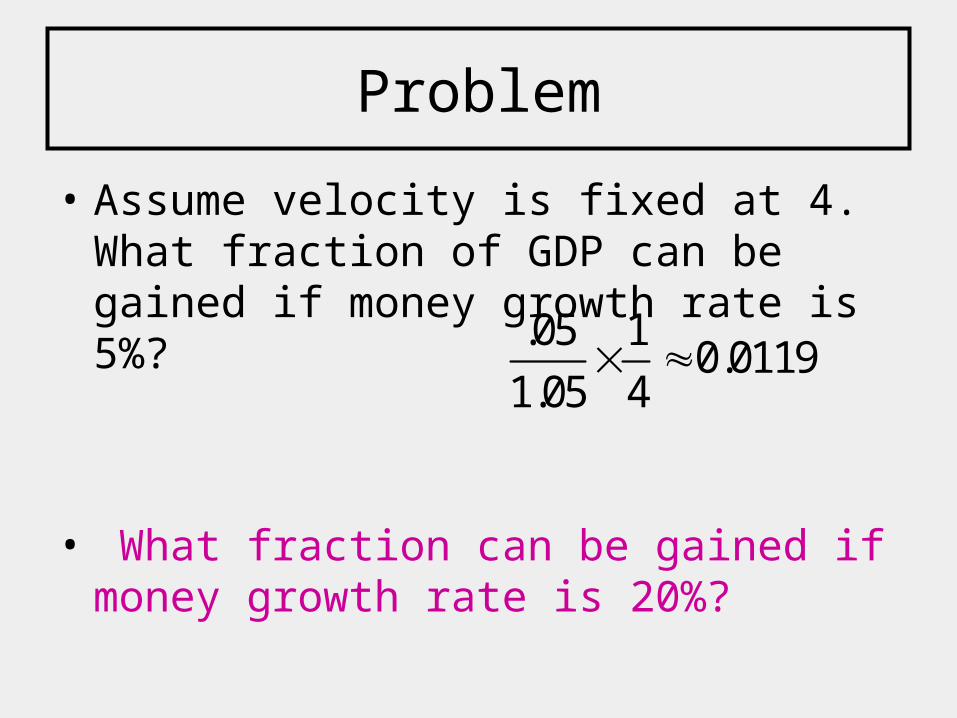

Problem

• Assume velocity is fixed at 4. What fraction of GDP can be gained if money growth rate is 5%?

• What fraction can be gained if money growth rate is 20%?

.05 10.0119

1.05 4

Causes of Extremely Rapid Inflation

• Government generates revenues by printing new money (referred to as seignorage).

• Government facing borrowing constraints may be forced to rely on inflation tax for deficit financing and real returns to owning money.

• Explain the link between deficits and inflation.

Israel 1970-1990

Inflation

0

50

100

150

200

250

300

350

400

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

Israel 1970-1990Surplus (% of GDP)

-30.00%

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

P

Y

AD

A Bias toward Expansionary monetary policy

P*

SRAS

YP

AD′1

2

Inflationary Gap

1. Central Bank repeatedly expands the money supply

2. Inflation recurs

3. After a time, as inflation becomes expected it will cease to impact output even in the short run.

3

SRAS′

45

Discretion vs. Rules

• Central bank can use monetary policy to fight recessionary and inflationary conditions, but they might have a bias toward getting the economy out of a recession because of short-term-ism.

• Some economists suggest that the government create rules that restrict the ability of policy makers to act in a biased manner.

• Others believe that it is necessary for the central bank to act using discretion.

Features of Inflation TargetingA medium term communication strategy

• Commitment to price stability as goal of monetary policy.

• Clear statement of numerical target for inflation over the medium (1-2 year) term.

• Communication with public about current forecasts of inflation and policy actions used to achieve target.

• Central Bankers accountable for achieving goals.

Trend toward Independence

• In late 1998, the Bank of Japan, and the Bank of England, were removed from the direct control of the Ministry of Finance and the Chancellor and the Exchequer respectively.

• In 1997 and 2003 revisions of the Bank of Korea Act, the Bank of Korea were removed from the direct and indirect control of the Ministry of Economy and Finance.

Stabilization Policy ConsensusCan expansionary monetary/fiscal policy affect output in the long run?

No

Is expansionary monetary policy helpful in fighting recessions?

Yes

Is expansionary fiscal policy helpful in fighting recessions?

Yes

Should we use discretionary fiscal policy?

No

Should we use discretionary monetary policy?

Maybe

Discussion Topic

• Yield Curves

• Monetary Policy

• Business Cycles

Learning Outcome

• Calculate the impact of inflation on long-term nominal interest rates using the theory of the Fisher effect.

• Calculate real return on debt as a function of inflation and expected inflation.

• Use velocity and money growth to calculate the share of GDP that can be collected as revenue.

• Calculate real return on money as a function of inflation.