module 3 the financial statements - chartered … of resources. the implications of these objectives...

TRANSCRIPT

Page 131

MODULE 3

The Financial Statements

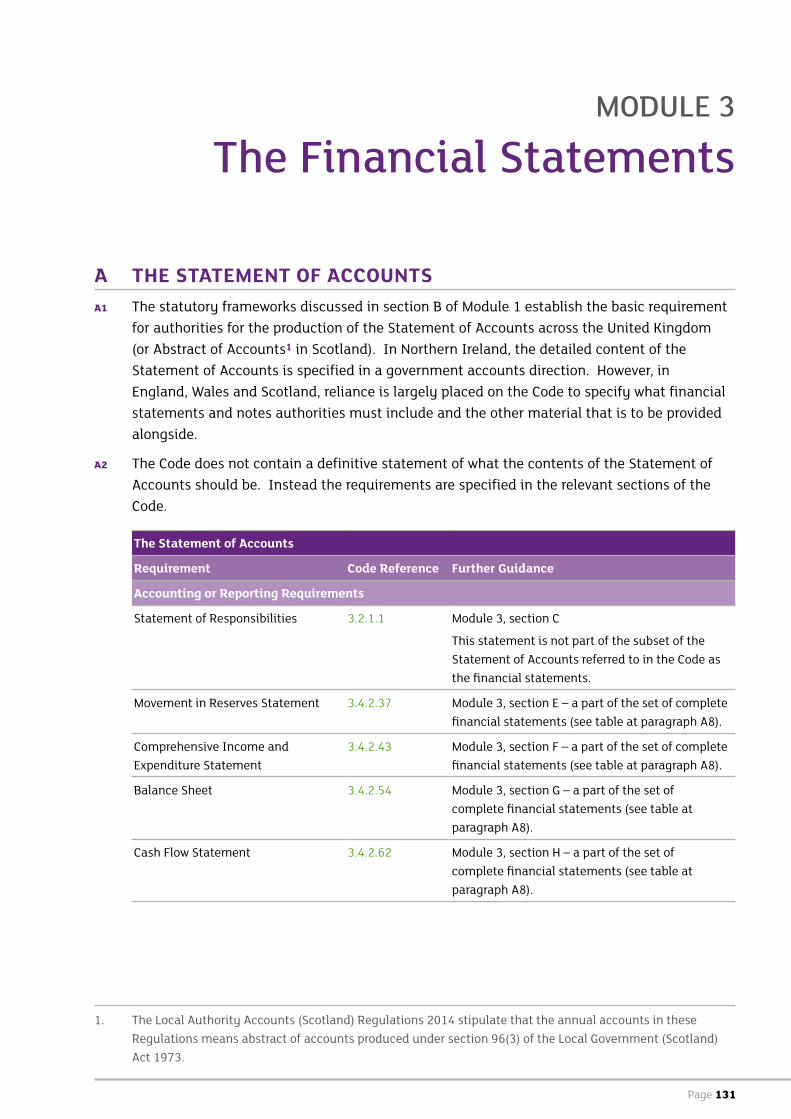

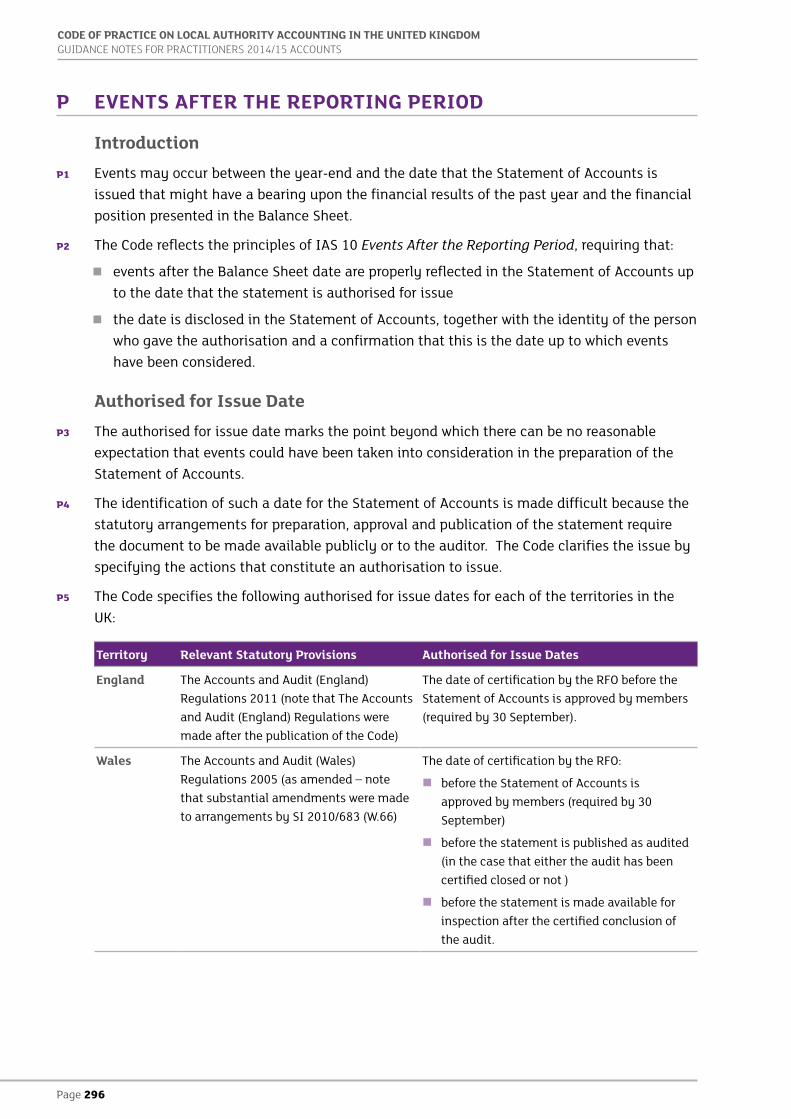

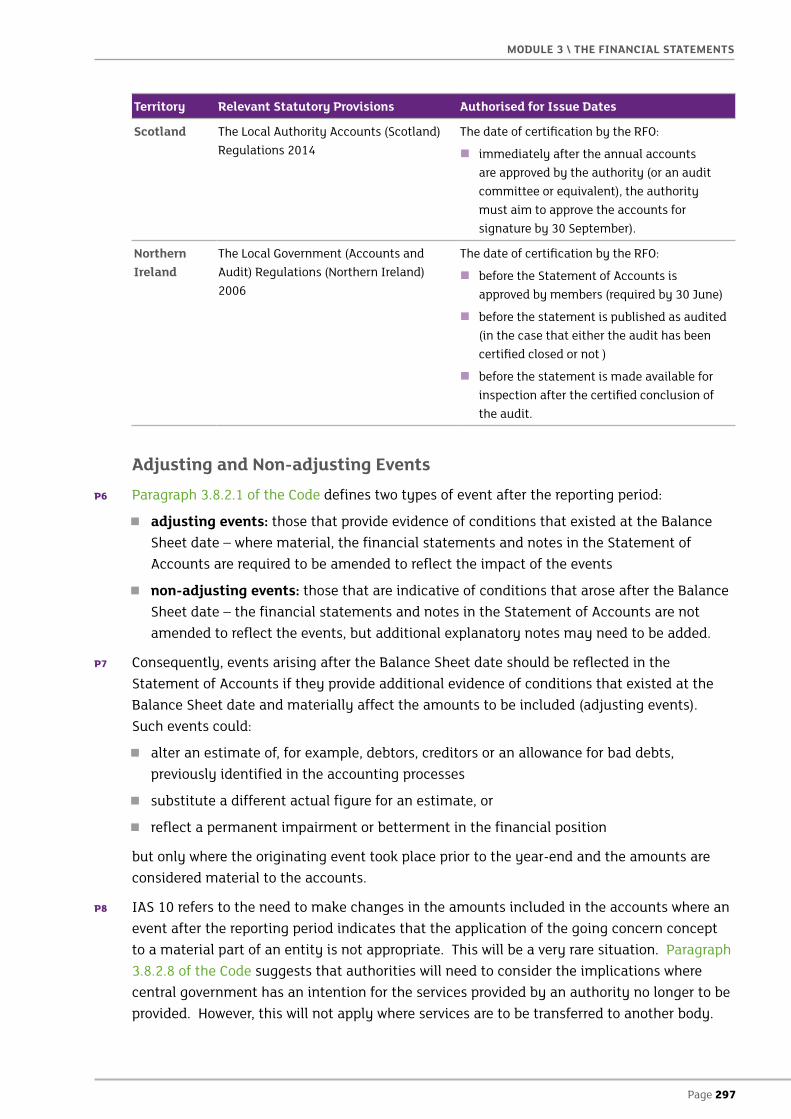

A THE STATEMENT OF ACCOUNTSA1 The statutory frameworks discussed in section B of Module 1 establish the basic requirement

for authorities for the production of the Statement of Accounts across the United Kingdom (or Abstract of Accounts1 in Scotland). In Northern Ireland, the detailed content of the Statement of Accounts is specified in a government accounts direction. However, in England, Wales and Scotland, reliance is largely placed on the Code to specify what financial statements and notes authorities must include and the other material that is to be provided alongside.

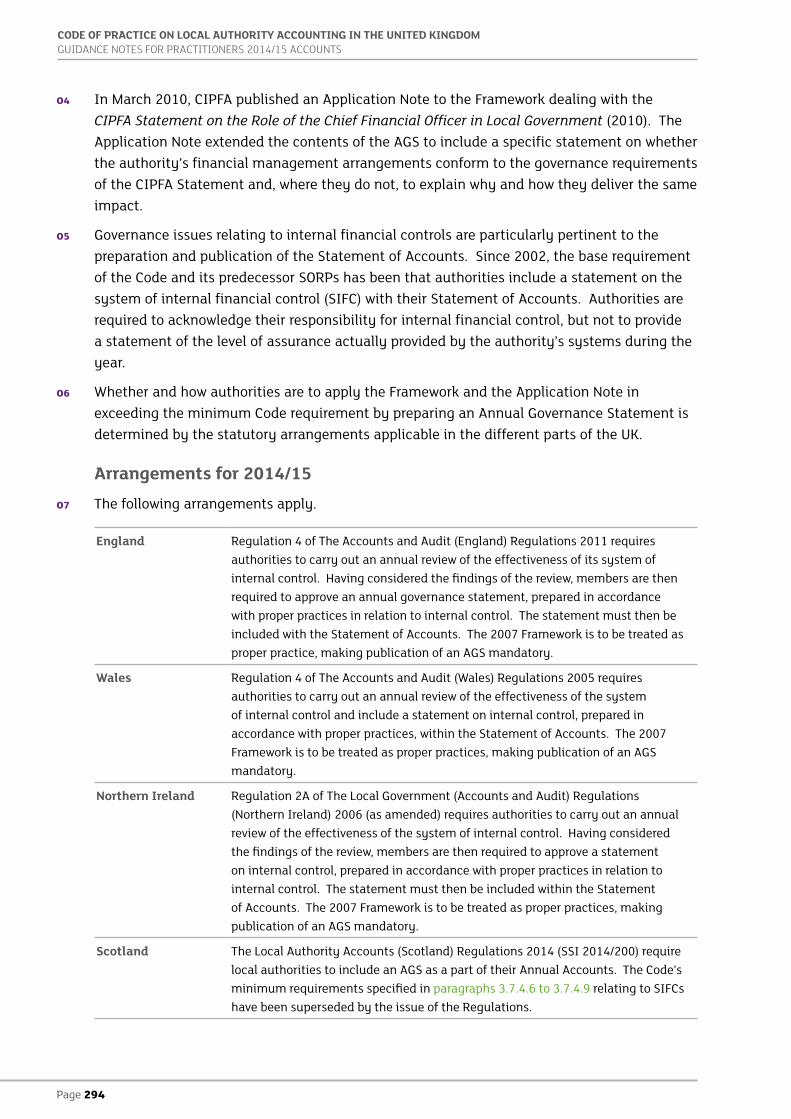

A2 The Code does not contain a definitive statement of what the contents of the Statement of Accounts should be. Instead the requirements are specified in the relevant sections of the Code.

The Statement of Accounts

Requirement Code Reference Further Guidance

Accounting or Reporting Requirements

Statement of Responsibilities 3.2.1.1 Module 3, section C

This statement is not part of the subset of the Statement of Accounts referred to in the Code as the financial statements.

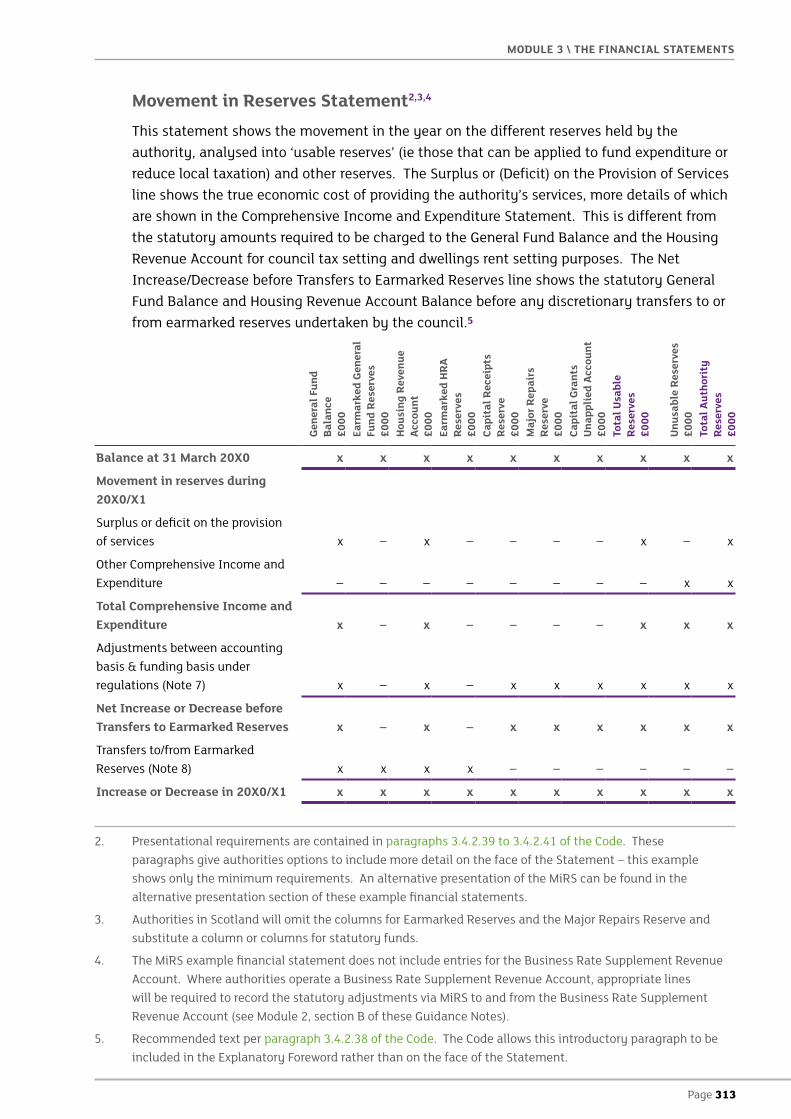

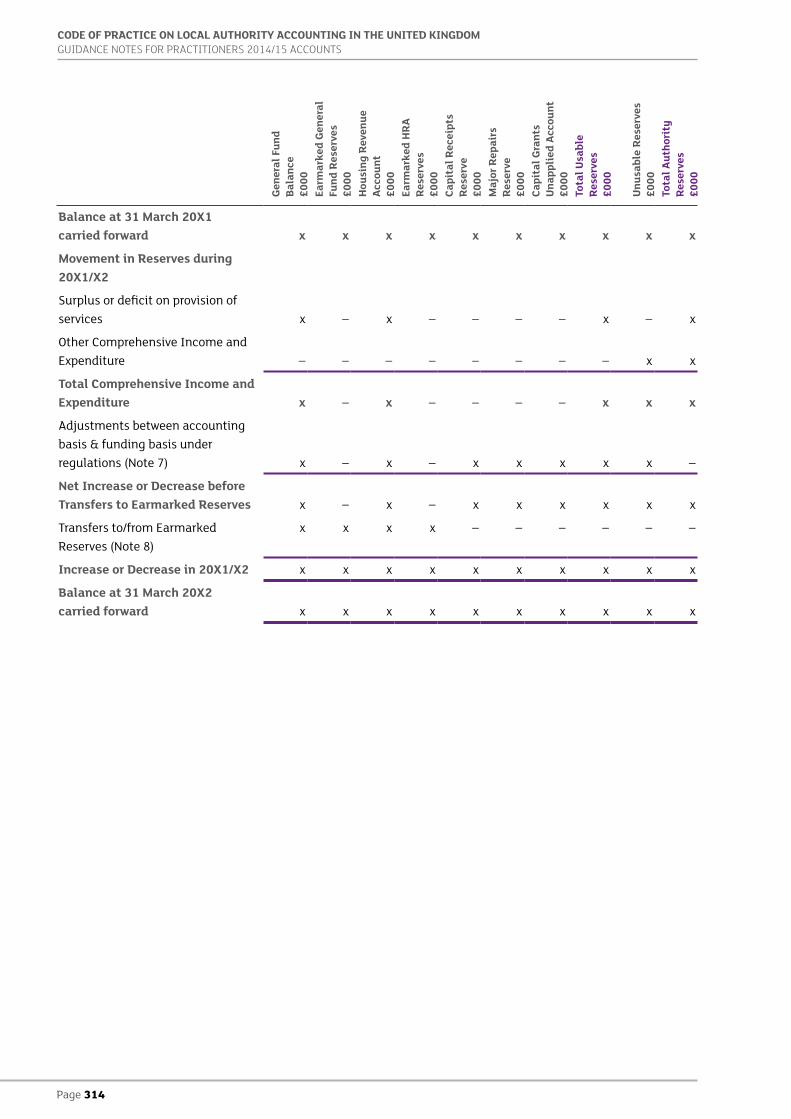

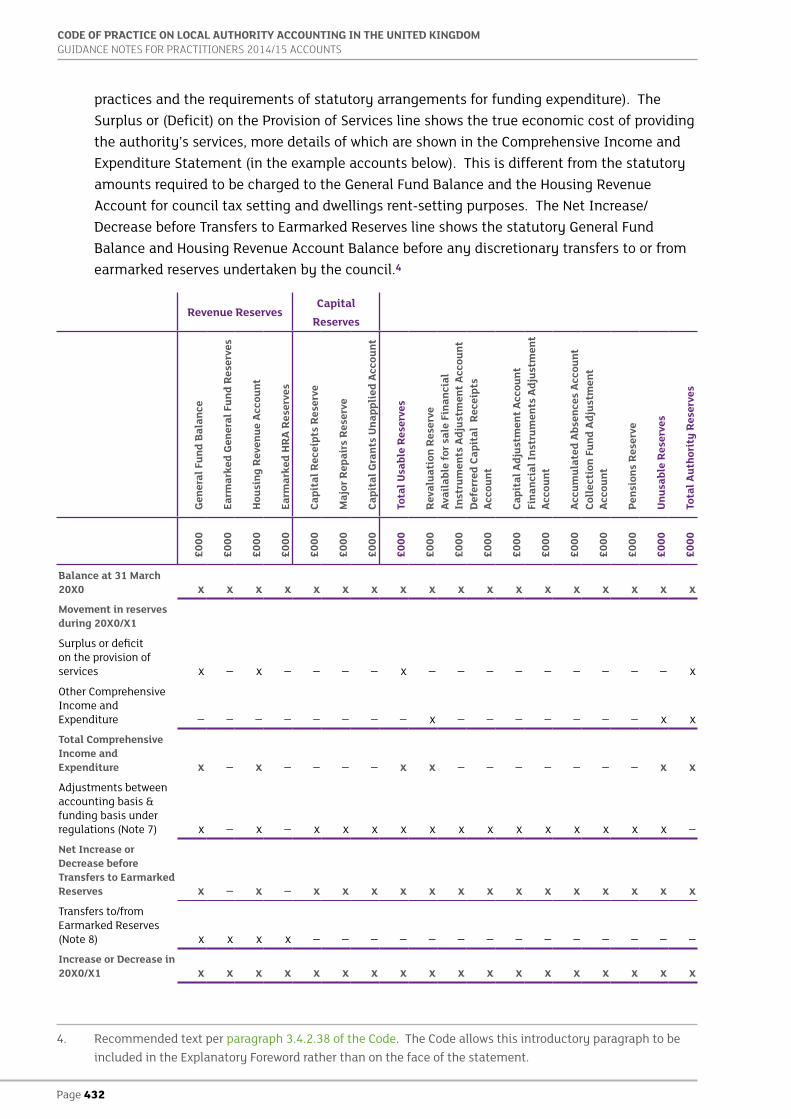

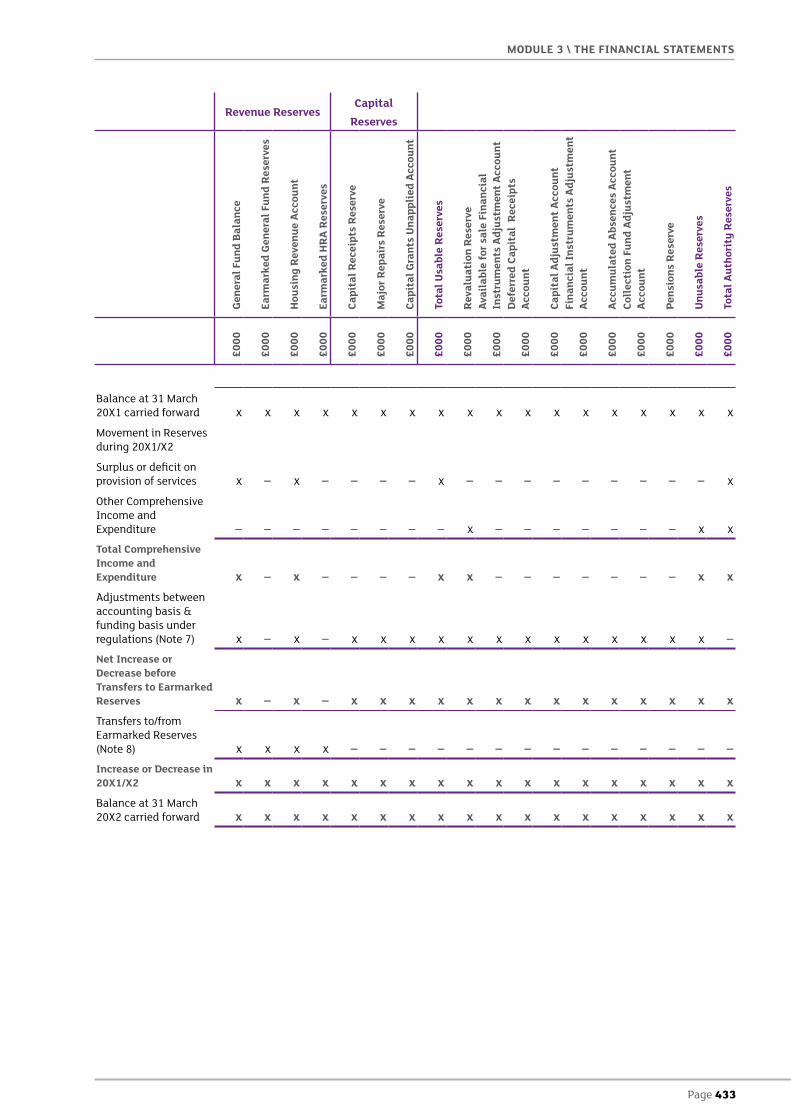

Movement in Reserves Statement 3.4.2.37 Module 3, section E – a part of the set of complete financial statements (see table at paragraph A8).

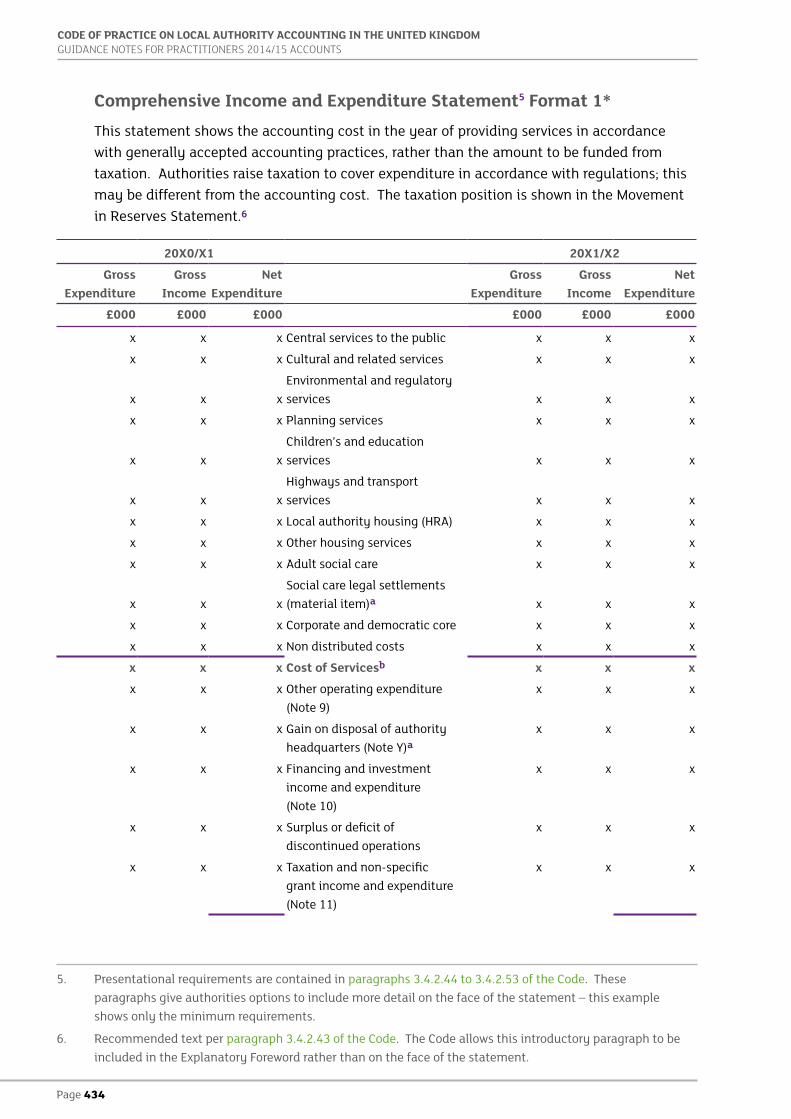

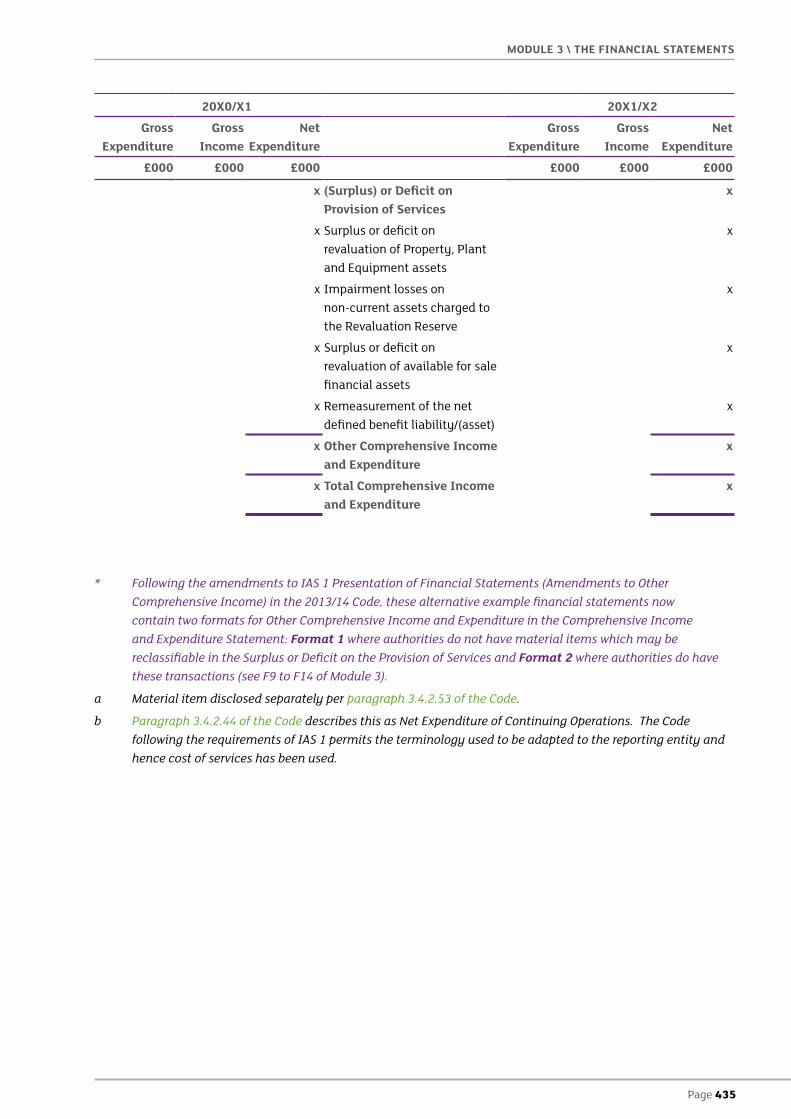

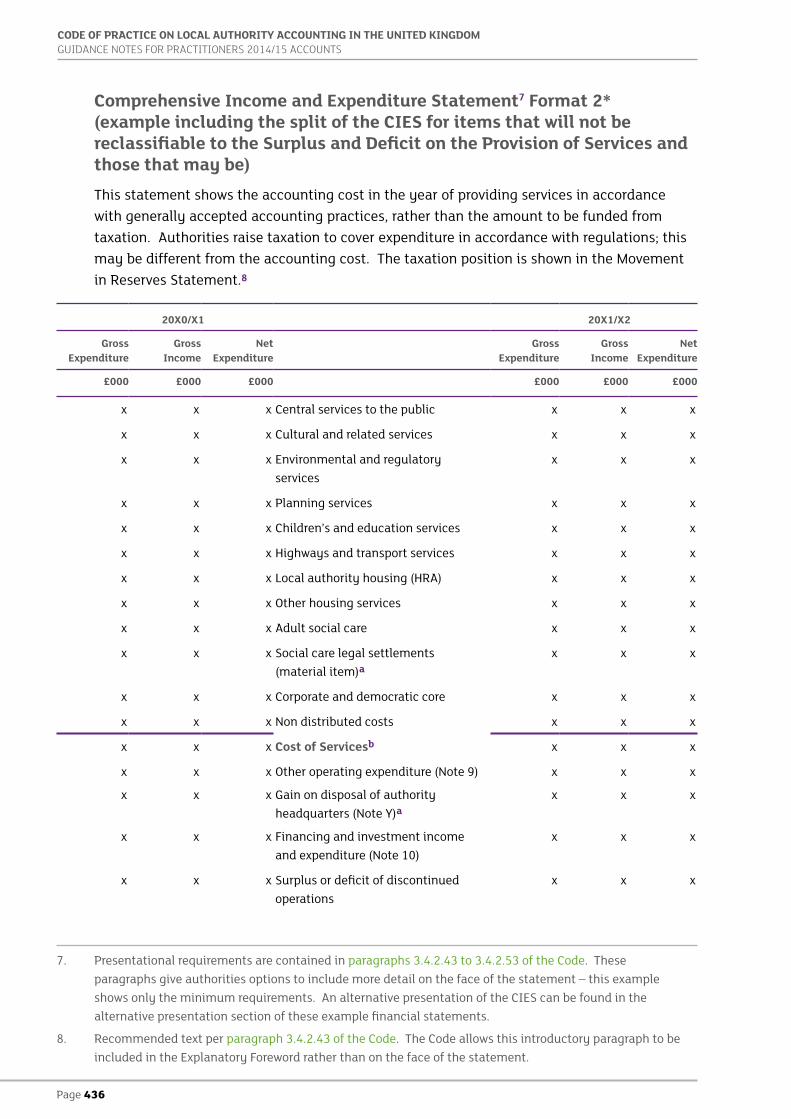

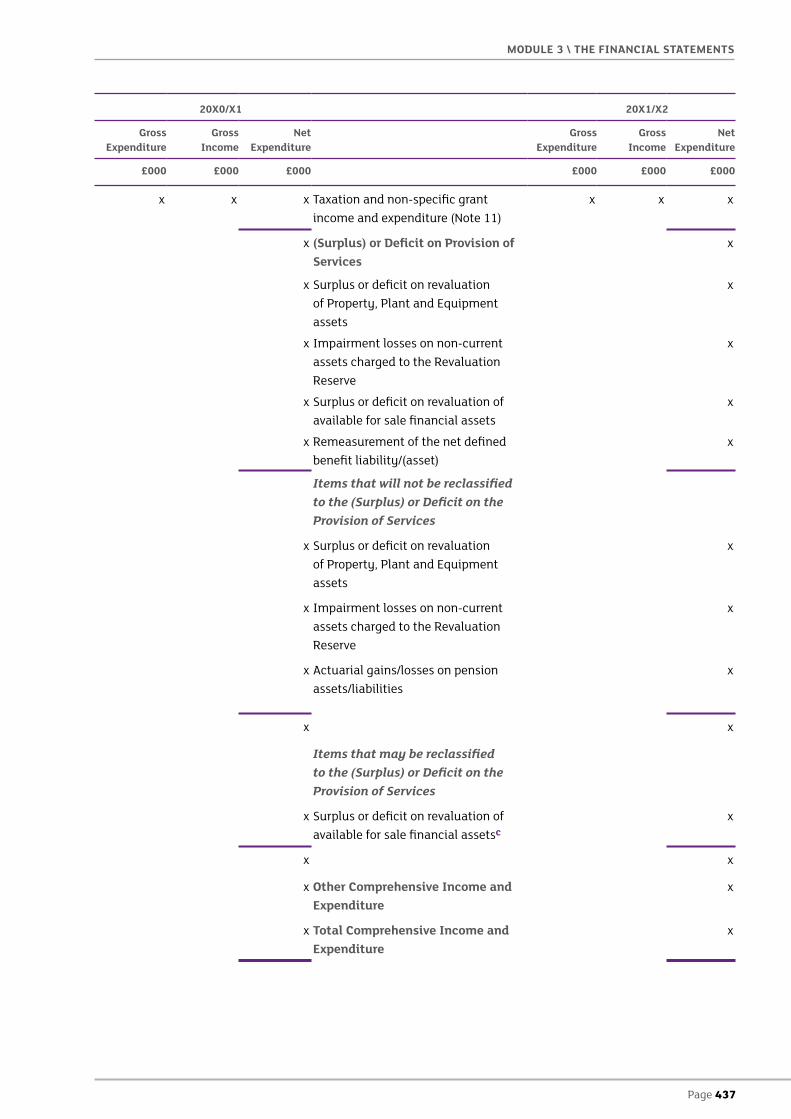

Comprehensive Income and Expenditure Statement

3.4.2.43 Module 3, section F – a part of the set of complete financial statements (see table at paragraph A8).

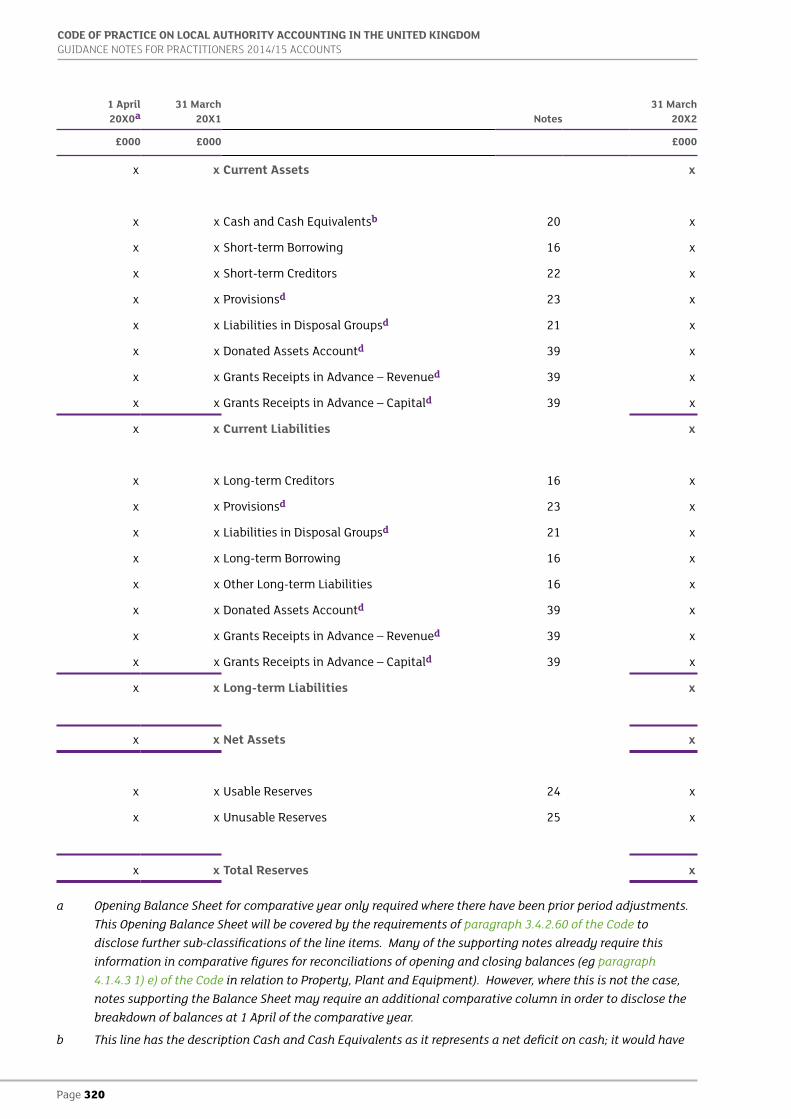

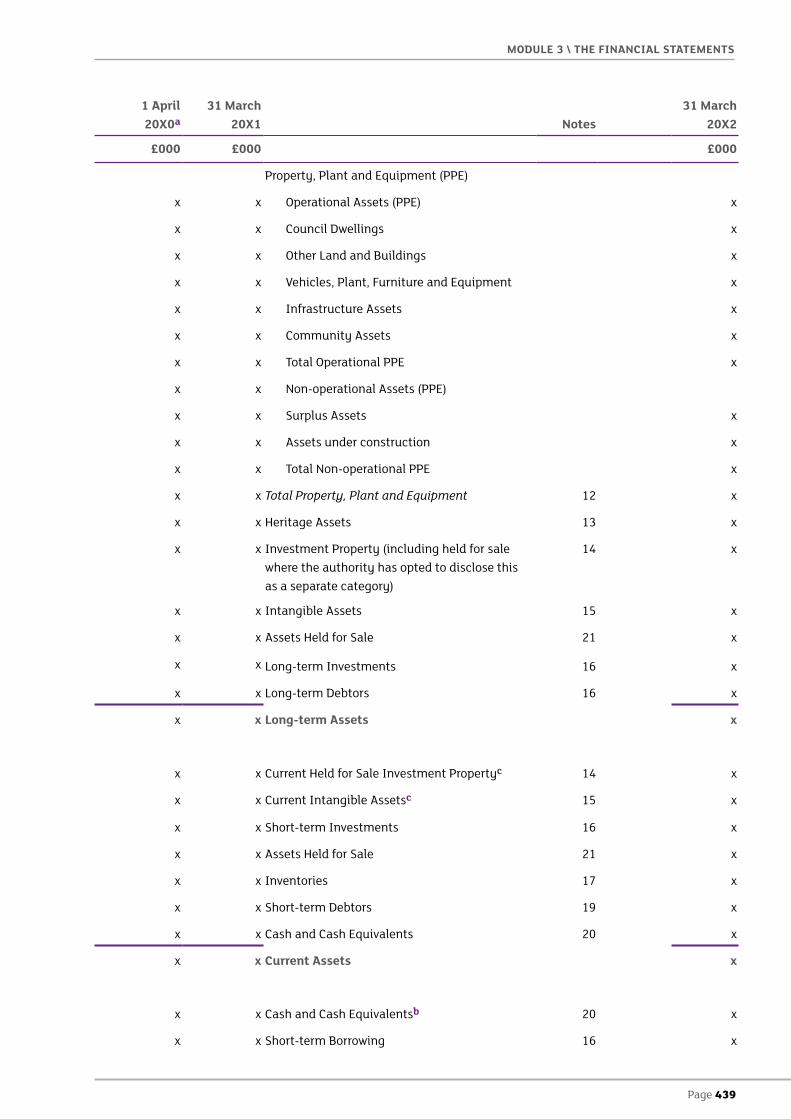

Balance Sheet 3.4.2.54 Module 3, section G – a part of the set of complete financial statements (see table at paragraph A8).

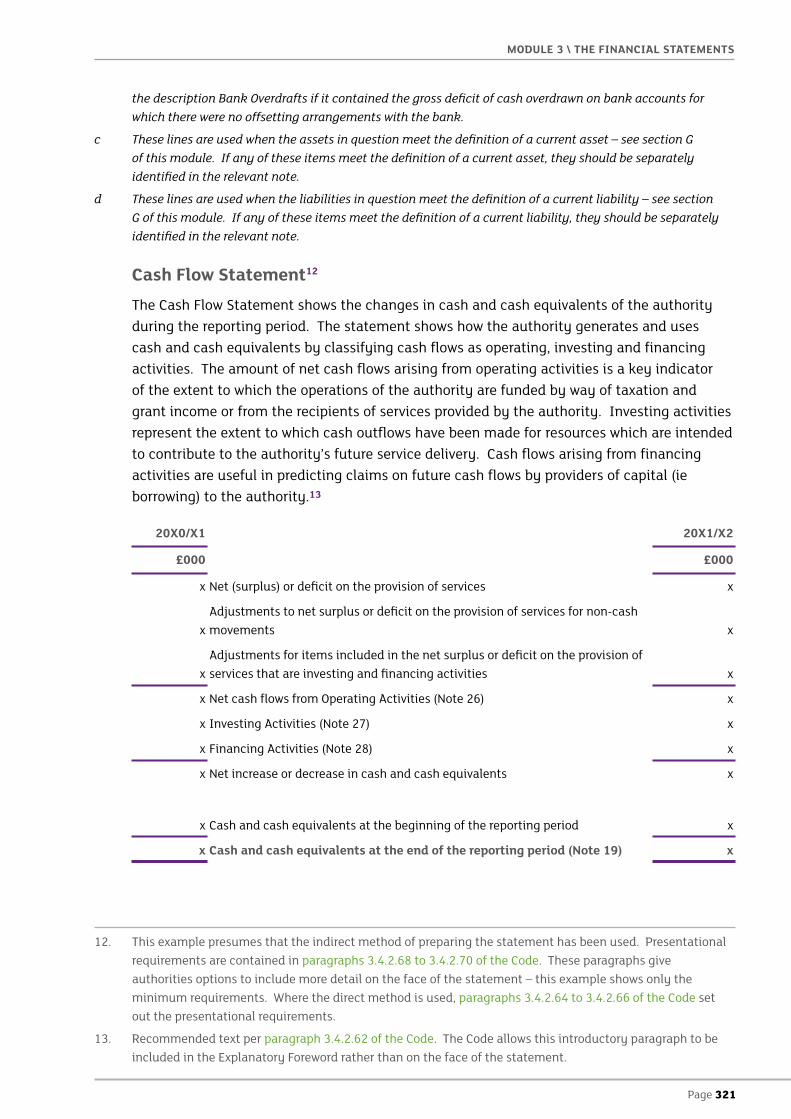

Cash Flow Statement 3.4.2.62 Module 3, section H – a part of the set of complete financial statements (see table at paragraph A8).

1. The Local Authority Accounts (Scotland) Regulations 2014 stipulate that the annual accounts in theseRegulations means abstract of accounts produced under section 96(3) of the Local Government (Scotland)Act 1973.

Page 132

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

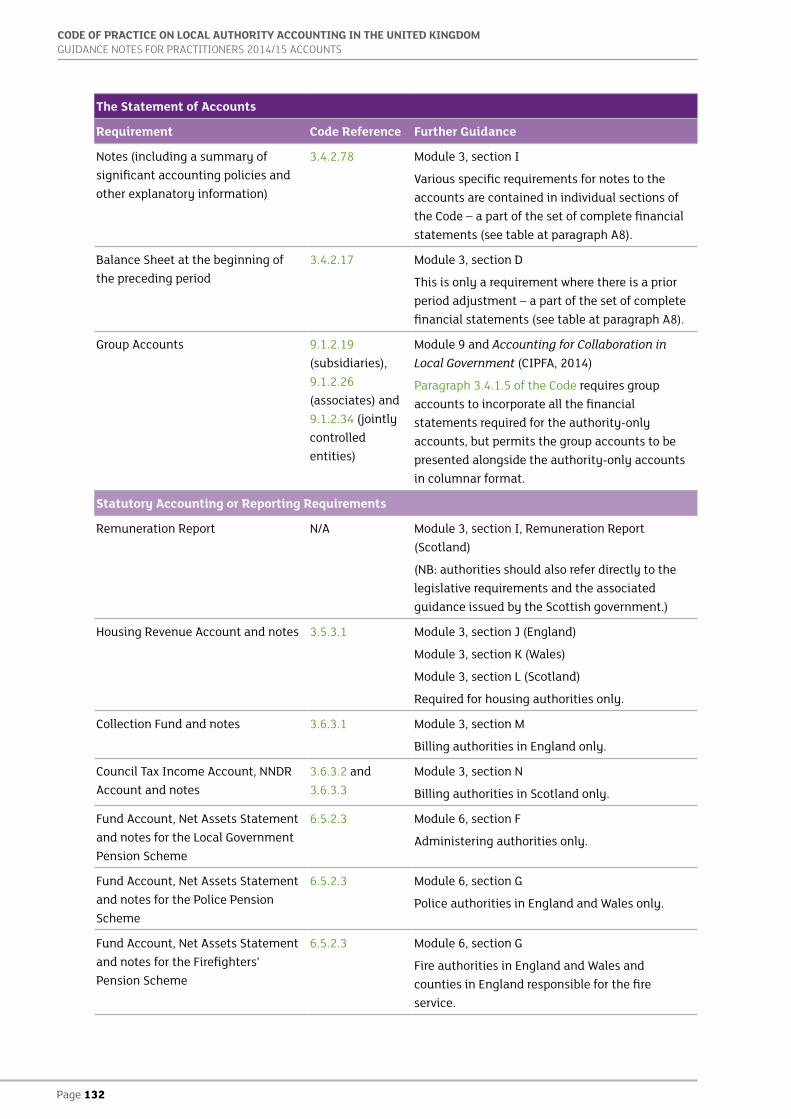

The Statement of Accounts

Requirement Code Reference Further Guidance

Notes (including a summary of significant accounting policies and other explanatory information)

3.4.2.78 Module 3, section I

Various specific requirements for notes to the accounts are contained in individual sections of the Code – a part of the set of complete financial statements (see table at paragraph A8).

Balance Sheet at the beginning of the preceding period

3.4.2.17 Module 3, section D

This is only a requirement where there is a prior period adjustment – a part of the set of complete financial statements (see table at paragraph A8).

Group Accounts 9.1.2.19 (subsidiaries), 9.1.2.26 (associates) and 9.1.2.34 (jointly controlled entities)

Module 9 and Accounting for Collaboration in Local Government (CIPFA, 2014)

Paragraph 3.4.1.5 of the Code requires group accounts to incorporate all the financial statements required for the authority-only accounts, but permits the group accounts to be presented alongside the authority-only accounts in columnar format.

Statutory Accounting or Reporting Requirements

Remuneration Report N/A Module 3, section I, Remuneration Report (Scotland)

(NB: authorities should also refer directly to the legislative requirements and the associated guidance issued by the Scottish government.)

Housing Revenue Account and notes 3.5.3.1 Module 3, section J (England)

Module 3, section K (Wales)

Module 3, section L (Scotland)

Required for housing authorities only.

Collection Fund and notes 3.6.3.1 Module 3, section M

Billing authorities in England only.

Council Tax Income Account, NNDR Account and notes

3.6.3.2 and 3.6.3.3

Module 3, section N

Billing authorities in Scotland only.

Fund Account, Net Assets Statement and notes for the Local Government Pension Scheme

6.5.2.3 Module 6, section F

Administering authorities only.

Fund Account, Net Assets Statement and notes for the Police Pension Scheme

6.5.2.3 Module 6, section G

Police authorities in England and Wales only.

Fund Account, Net Assets Statement and notes for the Firefighters’ Pension Scheme

6.5.2.3 Module 6, section G

Fire authorities in England and Wales and counties in England responsible for the fire service.

Page 133

MODULE 3 \ THE FINANCIAL STATEMENTS

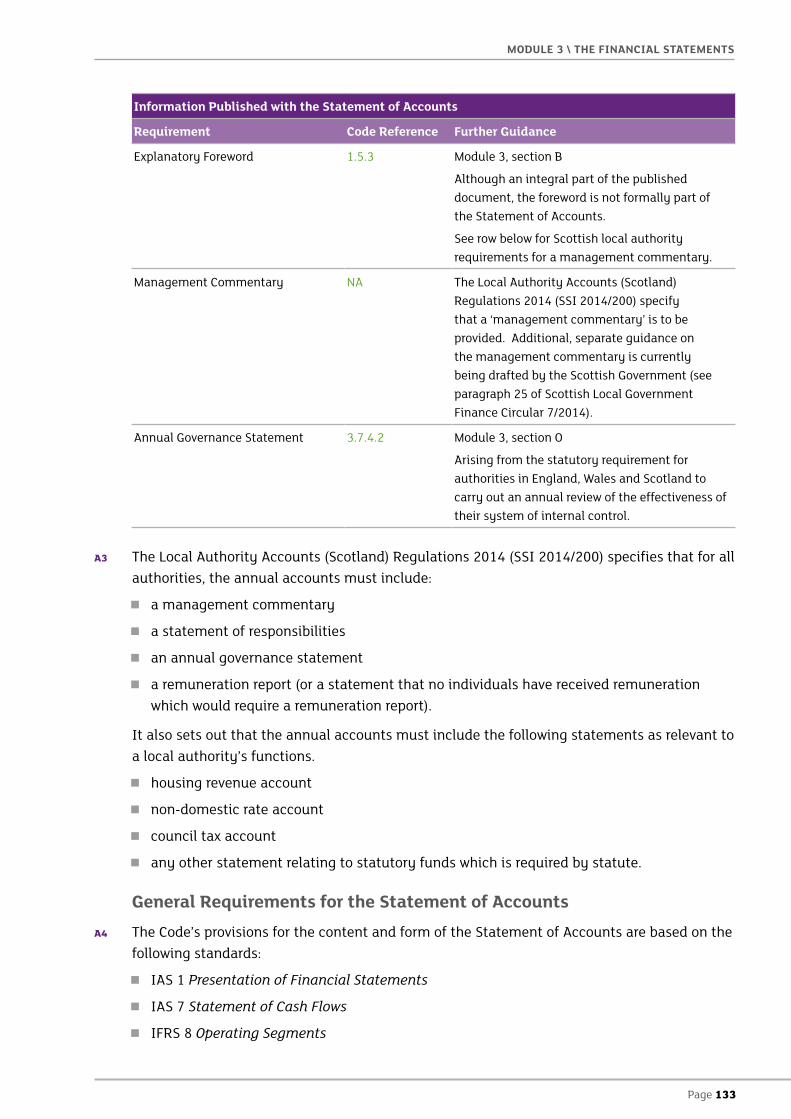

Information Published with the Statement of Accounts

Requirement Code Reference Further Guidance

Explanatory Foreword 1.5.3 Module 3, section B

Although an integral part of the published document, the foreword is not formally part of the Statement of Accounts.

See row below for Scottish local authority requirements for a management commentary.

Management Commentary NA The Local Authority Accounts (Scotland) Regulations 2014 (SSI 2014/200) specify that a ‘management commentary’ is to be provided. Additional, separate guidance on the management commentary is currently being drafted by the Scottish Government (see paragraph 25 of Scottish Local Government Finance Circular 7/2014).

Annual Governance Statement 3.7.4.2 Module 3, section O

Arising from the statutory requirement for authorities in England, Wales and Scotland to carry out an annual review of the effectiveness of their system of internal control.

A3 The Local Authority Accounts (Scotland) Regulations 2014 (SSI 2014/200) specifies that for all authorities, the annual accounts must include:

� a management commentary

� a statement of responsibilities

� an annual governance statement

� a remuneration report (or a statement that no individuals have received remuneration which would require a remuneration report).

It also sets out that the annual accounts must include the following statements as relevant to a local authority’s functions.

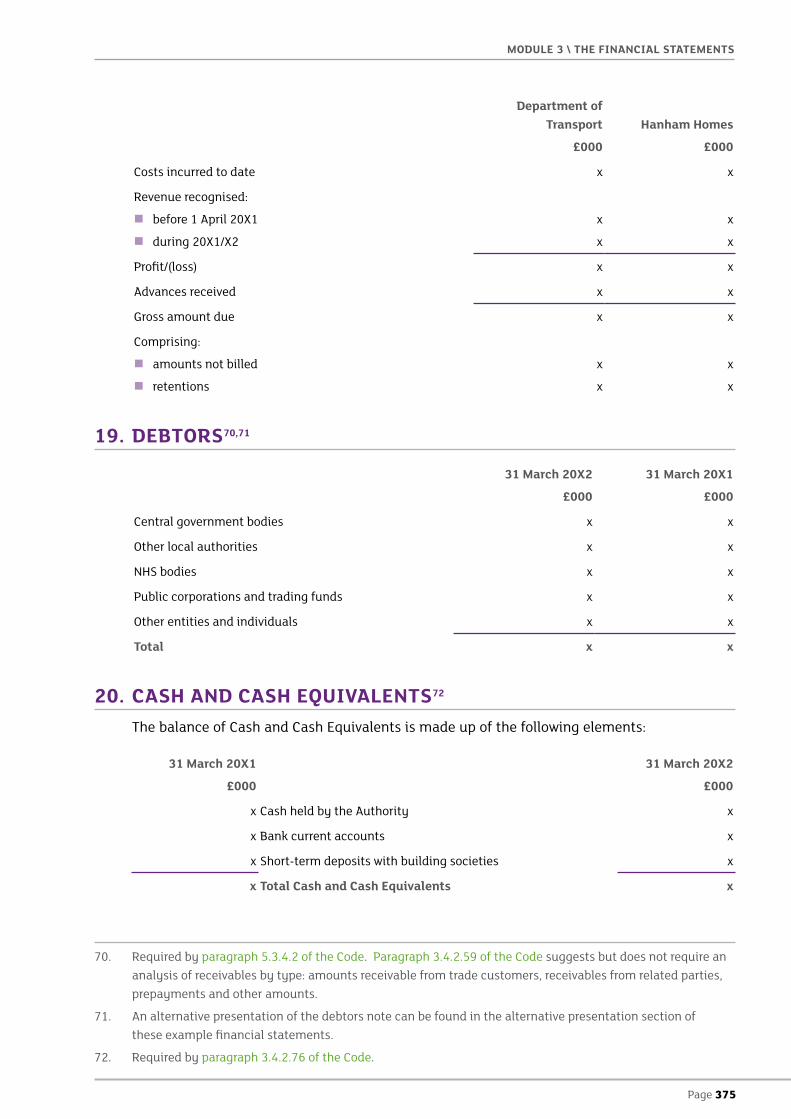

� housing revenue account

� non-domestic rate account

� council tax account

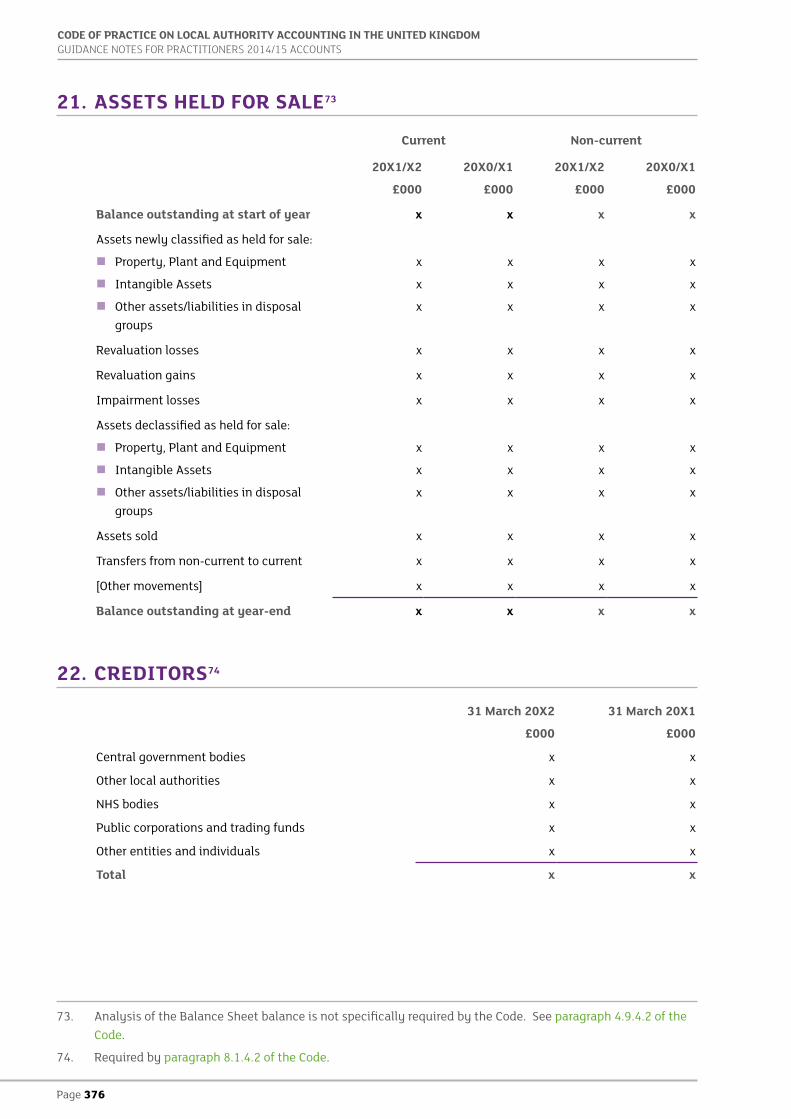

� any other statement relating to statutory funds which is required by statute.

General Requirements for the Statement of AccountsA4 The Code’s provisions for the content and form of the Statement of Accounts are based on the

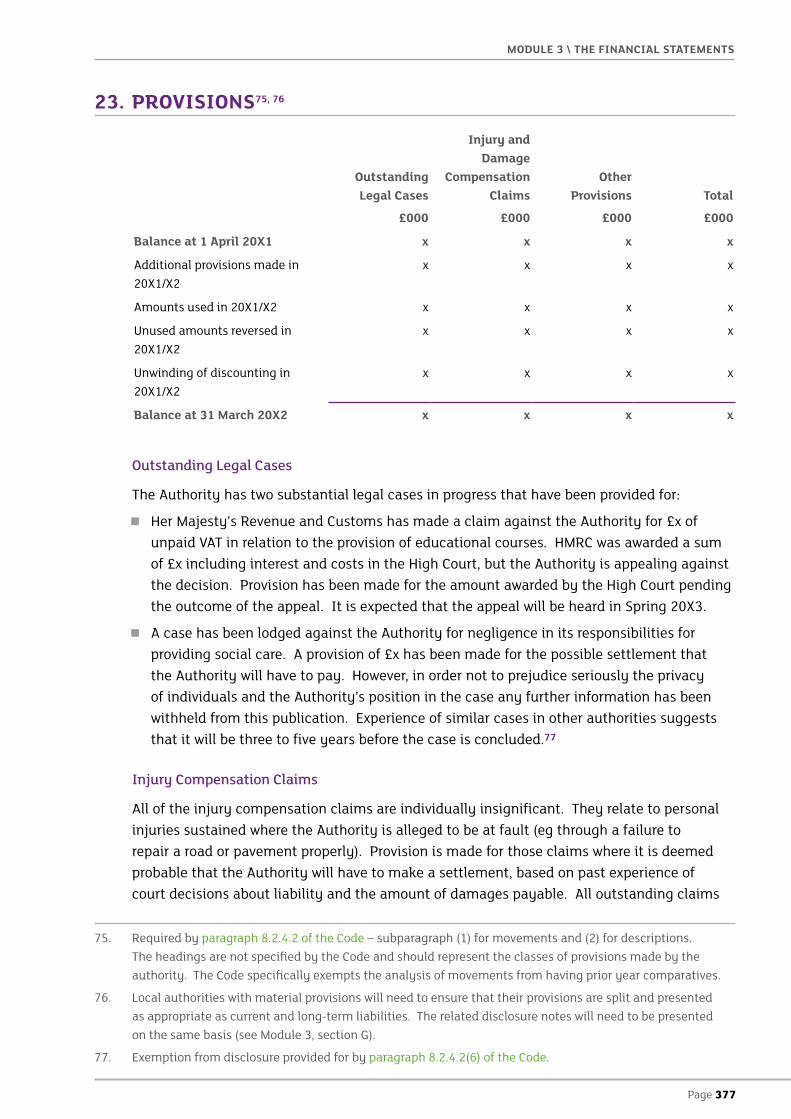

following standards:

� IAS 1 Presentation of Financial Statements

� IAS 7 Statement of Cash Flows

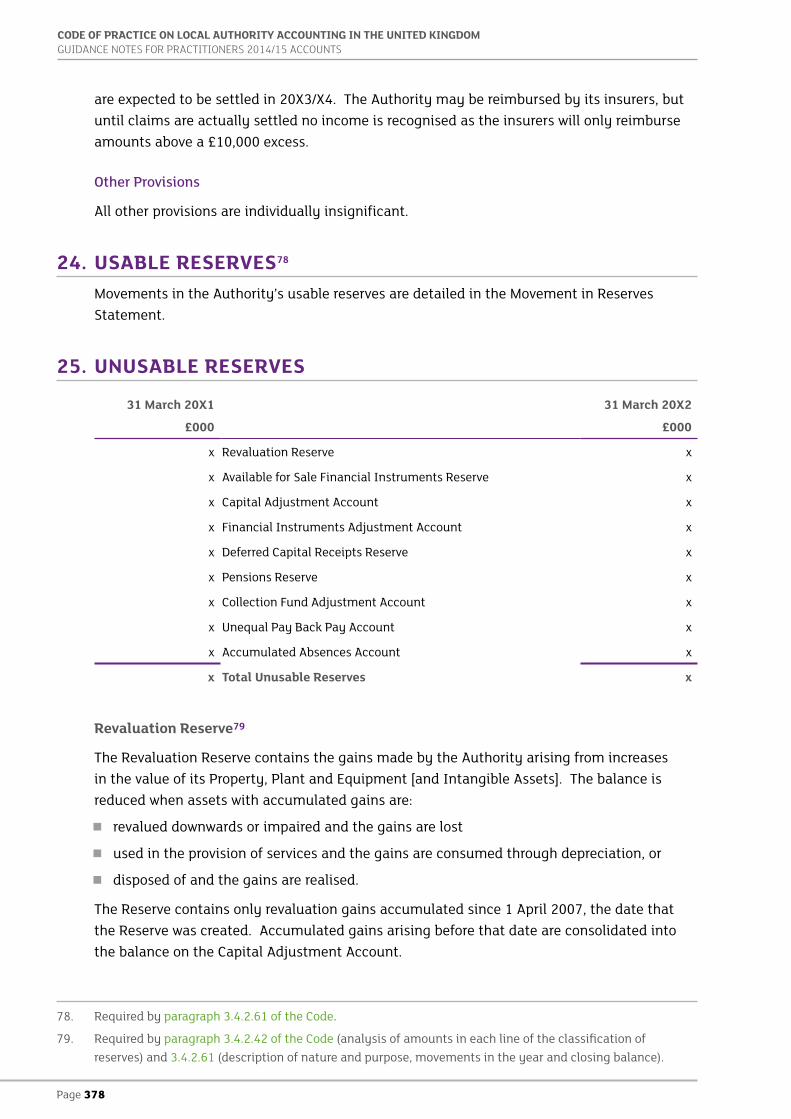

� IFRS 8 Operating Segments

Page 134

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

supported by the interpretations in:

� IPSAS 1 Presentation of Financial Statements

� IPSAS 2 Cash Flow Statements.

A5 Paragraph 3.4.1.4 of the Code confirms that it has adapted the requirements of IAS 1 by specifying the format of the statements, disclosures and terminology required to be applied in local government. Practitioners should not then need to make reference to the underlying standards when planning the format of the Statement of Accounts.

A6 However, the Code’s provisions are intended to prescribe the minimum level of detail that authorities must provide, but do not discourage a greater level of disclosure:

� where more detail is required for a true and fair view, that extra detail must be provided (in which case the underlying standards might be relevant for practitioners)

� where the authority considers it would be helpful to include more than the minimum level of detail, additional disclosures can be made, provided that they are appropriate (as a minimum this would require that they give a true and fair view and do not distort or detract from the true and fair view given by the minimum disclosures) (see also paragraph C8 of Module 1).

Specific Requirements for the Financial StatementsA7 Paragraph 3.4.2.16 of the Code reaffirms the objectives of the financial statements as being to

provide information about the financial position, financial performance and cash flows of an authority that is useful to a wide range of users in making and evaluating decisions about the allocation of resources. The implications of these objectives are discussed in greater detail in paragraphs A9 to A18 of Module 2.

A8 Paragraphs 3.4.2.18 to 3.4.2.36 of the Code then present a series of principles that must be reflected when preparing the financial statements elements of the Statement of Accounts. This part of the Code should be regarded as essential reading by practitioners when planning the overall format of their authority’s Statement of Accounts and the accounting policies to be applied – see the following table.

Page 135

MODULE 3 \ THE FINANCIAL STATEMENTS

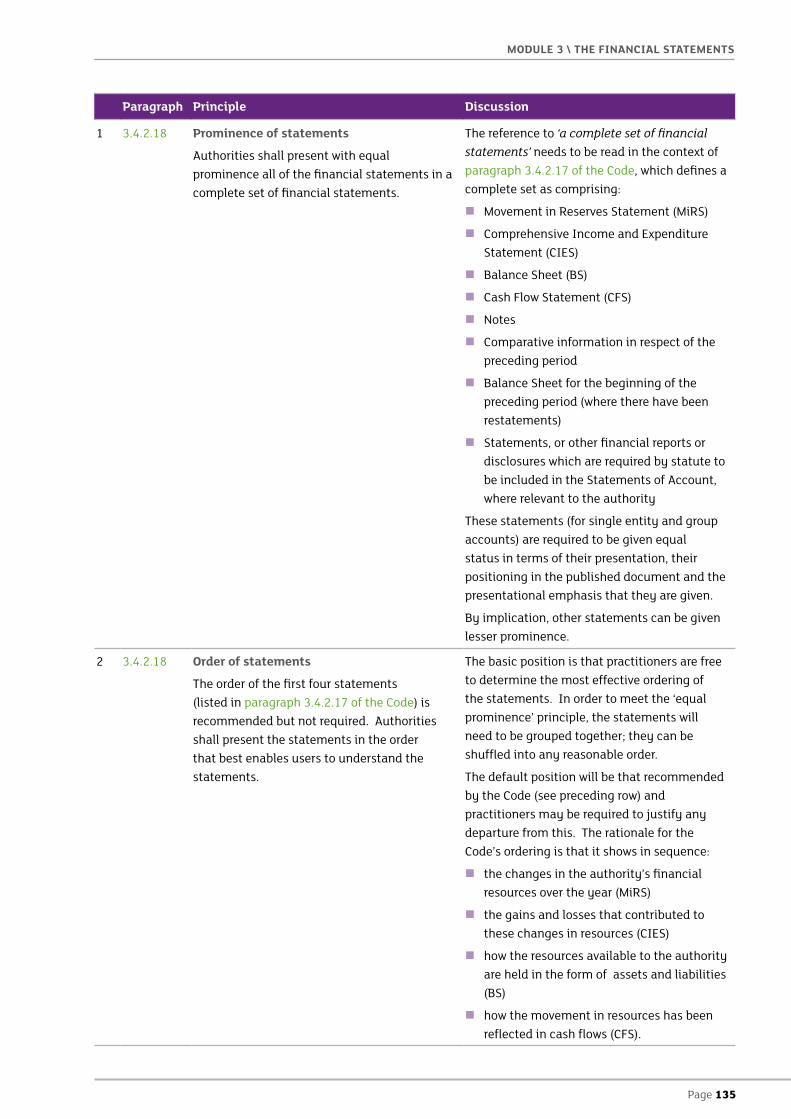

Paragraph Principle Discussion

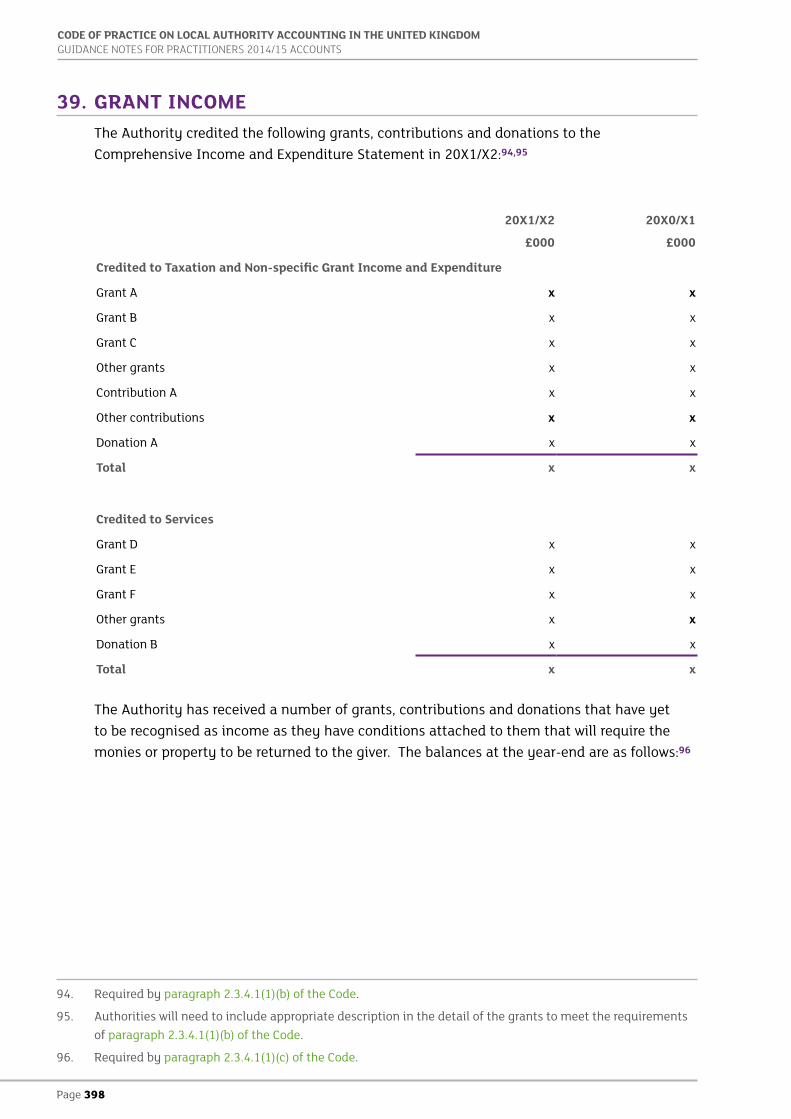

1 3.4.2.18 Prominence of statements

Authorities shall present with equal prominence all of the financial statements in a complete set of financial statements.

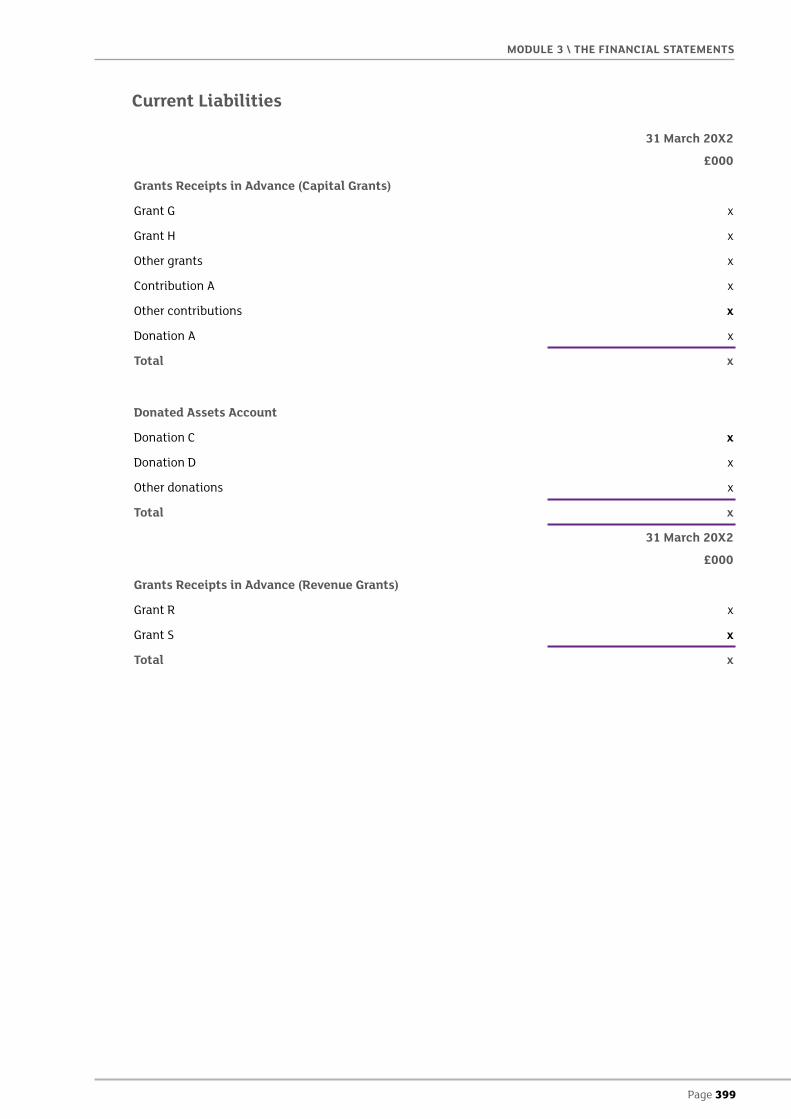

The reference to ‘a complete set of financial statements’ needs to be read in the context of paragraph 3.4.2.17 of the Code, which defines a complete set as comprising:

� Movement in Reserves Statement (MiRS)

� Comprehensive Income and Expenditure Statement (CIES)

� Balance Sheet (BS)

� Cash Flow Statement (CFS)

� Notes

� Comparative information in respect of the preceding period

� Balance Sheet for the beginning of the preceding period (where there have been restatements)

� Statements, or other financial reports or disclosures which are required by statute to be included in the Statements of Account, where relevant to the authority

These statements (for single entity and group accounts) are required to be given equal status in terms of their presentation, their positioning in the published document and the presentational emphasis that they are given.

By implication, other statements can be given lesser prominence.

2 3.4.2.18 Order of statements

The order of the first four statements (listed in paragraph 3.4.2.17 of the Code) is recommended but not required. Authorities shall present the statements in the order that best enables users to understand the statements.

The basic position is that practitioners are free to determine the most effective ordering of the statements. In order to meet the ‘equal prominence’ principle, the statements will need to be grouped together; they can be shuffled into any reasonable order.

The default position will be that recommended by the Code (see preceding row) and practitioners may be required to justify any departure from this. The rationale for the Code’s ordering is that it shows in sequence:

� the changes in the authority’s financial resources over the year (MiRS)

� the gains and losses that contributed to these changes in resources (CIES)

� how the resources available to the authority are held in the form of assets and liabilities (BS)

� how the movement in resources has been reflected in cash flows (CFS).

Page 136

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

Paragraph Principle Discussion

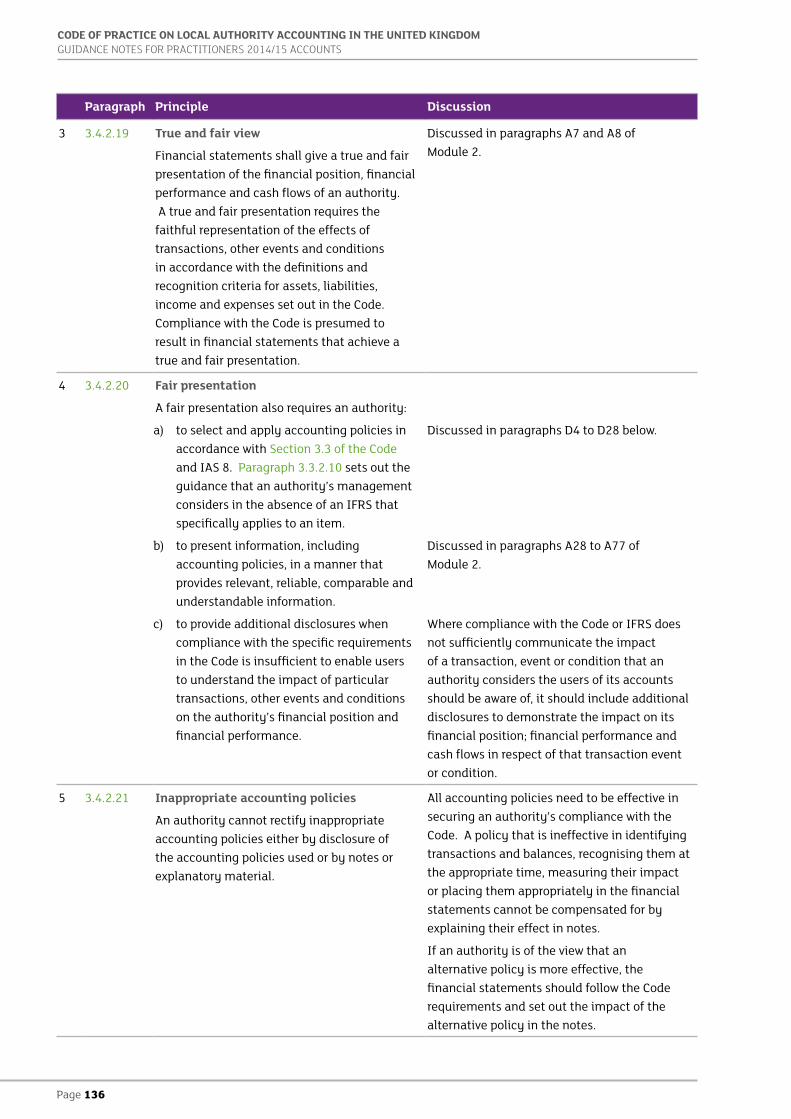

3 3.4.2.19 True and fair view

Financial statements shall give a true and fair presentation of the financial position, financial performance and cash flows of an authority. A true and fair presentation requires the faithful representation of the effects of transactions, other events and conditions in accordance with the definitions and recognition criteria for assets, liabilities, income and expenses set out in the Code. Compliance with the Code is presumed to result in financial statements that achieve a true and fair presentation.

Discussed in paragraphs A7 and A8 of Module 2.

4 3.4.2.20 Fair presentation

A fair presentation also requires an authority:

a) to select and apply accounting policies in accordance with Section 3.3 of the Code and IAS 8. Paragraph 3.3.2.10 sets out the guidance that an authority’s management considers in the absence of an IFRS that specifically applies to an item.

b) to present information, including accounting policies, in a manner that provides relevant, reliable, comparable and understandable information.

c) to provide additional disclosures when compliance with the specific requirements in the Code is insufficient to enable users to understand the impact of particular transactions, other events and conditions on the authority’s financial position and financial performance.

Discussed in paragraphs D4 to D28 below.

Discussed in paragraphs A28 to A77 of Module 2.

Where compliance with the Code or IFRS does not sufficiently communicate the impact of a transaction, event or condition that an authority considers the users of its accounts should be aware of, it should include additional disclosures to demonstrate the impact on its financial position; financial performance and cash flows in respect of that transaction event or condition.

5 3.4.2.21 Inappropriate accounting policies

An authority cannot rectify inappropriate accounting policies either by disclosure of the accounting policies used or by notes or explanatory material.

All accounting policies need to be effective in securing an authority’s compliance with the Code. A policy that is ineffective in identifying transactions and balances, recognising them at the appropriate time, measuring their impact or placing them appropriately in the financial statements cannot be compensated for by explaining their effect in notes.

If an authority is of the view that an alternative policy is more effective, the financial statements should follow the Code requirements and set out the impact of the alternative policy in the notes.

Page 137

MODULE 3 \ THE FINANCIAL STATEMENTS

Paragraph Principle Discussion

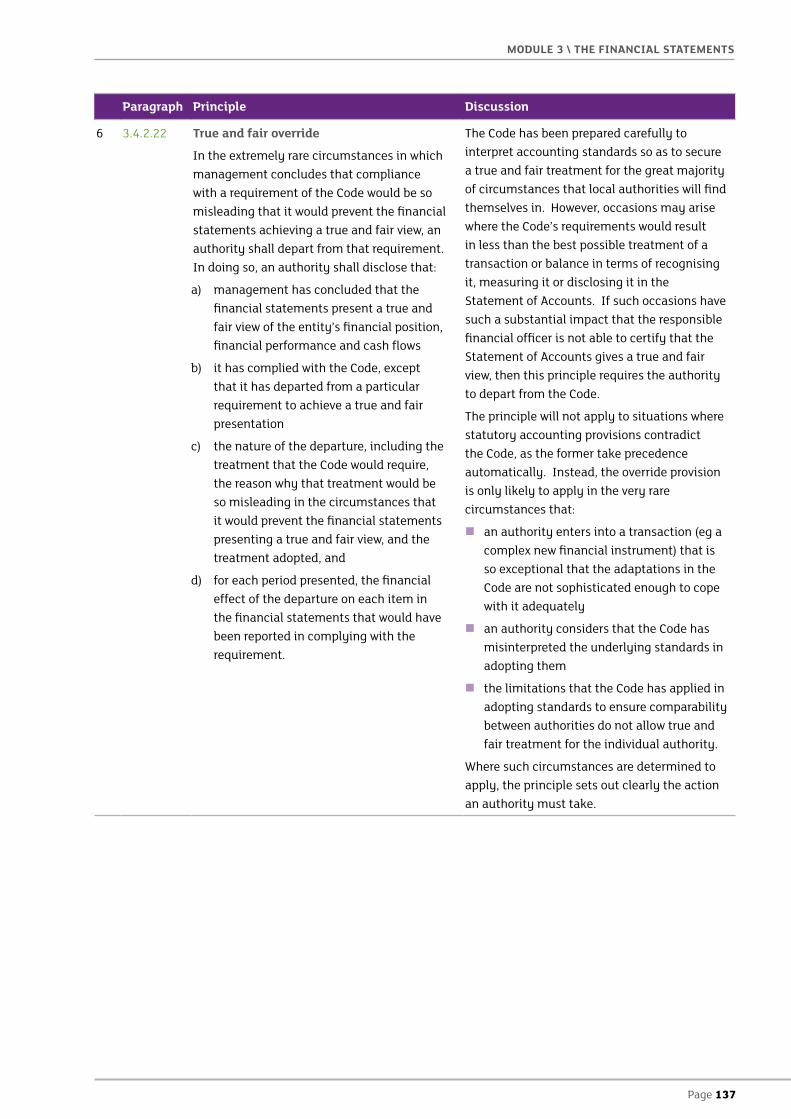

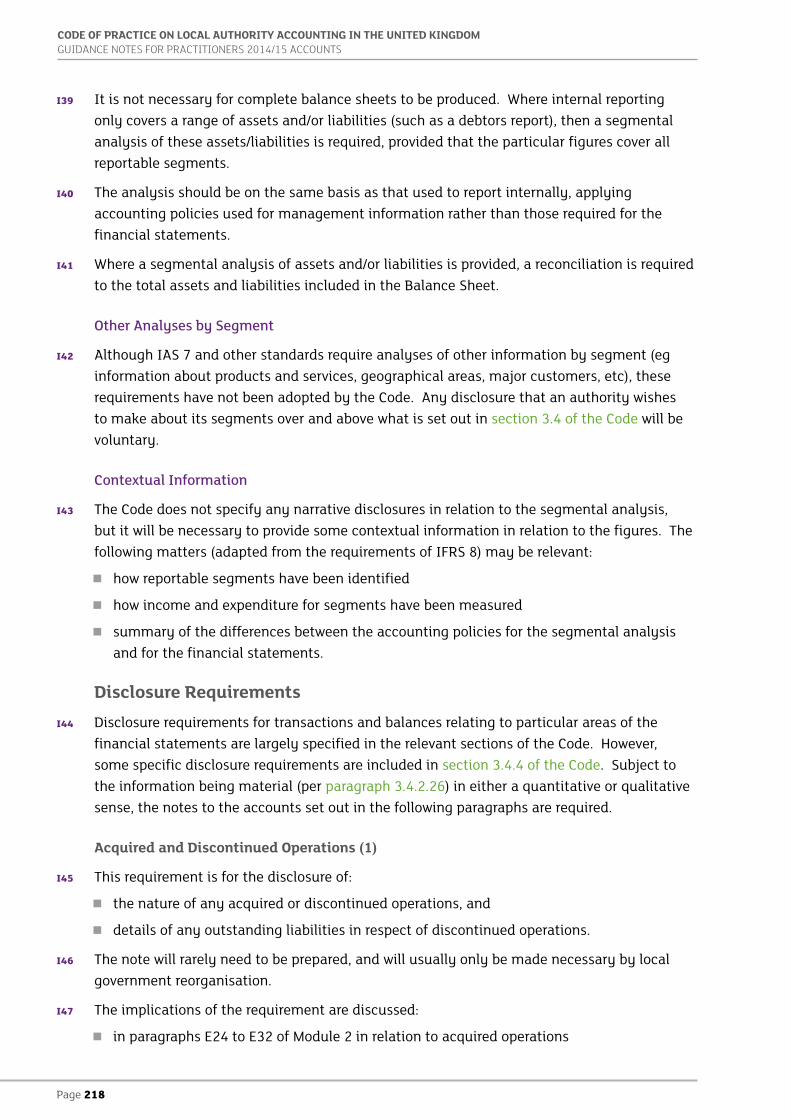

6 3.4.2.22 True and fair override

In the extremely rare circumstances in which management concludes that compliance with a requirement of the Code would be so misleading that it would prevent the financial statements achieving a true and fair view, an authority shall depart from that requirement. In doing so, an authority shall disclose that:

a) management has concluded that the financial statements present a true and fair view of the entity’s financial position, financial performance and cash flows

b) it has complied with the Code, except that it has departed from a particular requirement to achieve a true and fair presentation

c) the nature of the departure, including the treatment that the Code would require, the reason why that treatment would be so misleading in the circumstances that it would prevent the financial statements presenting a true and fair view, and the treatment adopted, and

d) for each period presented, the financial effect of the departure on each item in the financial statements that would have been reported in complying with the requirement.

The Code has been prepared carefully to interpret accounting standards so as to secure a true and fair treatment for the great majority of circumstances that local authorities will find themselves in. However, occasions may arise where the Code’s requirements would result in less than the best possible treatment of a transaction or balance in terms of recognising it, measuring it or disclosing it in the Statement of Accounts. If such occasions have such a substantial impact that the responsible financial officer is not able to certify that the Statement of Accounts gives a true and fair view, then this principle requires the authority to depart from the Code.

The principle will not apply to situations where statutory accounting provisions contradict the Code, as the former take precedence automatically. Instead, the override provision is only likely to apply in the very rare circumstances that:

� an authority enters into a transaction (eg a complex new financial instrument) that is so exceptional that the adaptations in the Code are not sophisticated enough to cope with it adequately

� an authority considers that the Code has misinterpreted the underlying standards in adopting them

� the limitations that the Code has applied in adopting standards to ensure comparability between authorities do not allow true and fair treatment for the individual authority.

Where such circumstances are determined to apply, the principle sets out clearly the action an authority must take.

Page 138

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

Paragraph Principle Discussion

7 3.4.2.23 Going Concern

A local authority’s financial statements shall be prepared on a going concern basis; that is, the accounts should be prepared on the assumption that the functions of the authority will continue in operational existence for the foreseeable future. Transfers of services under combinations of public sector bodies (such as local government reorganisation) do not negate the presumption of going concern.

The Code stipulates that the financial statements are prepared on a going concern basis. They are therefore drawn up under the Code to assume that a local authority’s services will continue to operate for the foreseeable future. This assumption is made because local authorities carry out functions essential to the local community and are themselves revenue-raising bodies (with limits on their revenue-raising powers arising only at the discretion of central government). If an authority were in financial difficulty, the prospects are thus that alternative arrangements might be made by central government either for the continuation of the services it provides or for assistance with the recovery of a deficit over more than one financial year. The Code is clear that transfers of services under combinations of public sector bodies (such as local government reorganisation) do not negate the presumption of going concern. See paragraphs A23 to A27 of Module 2 for further discussion.

8 3.4.2.24 Accruals

A local authority shall prepare its financial statements, except for cash flow information, using the accrual basis of accounting, ie the authority recognises items as assets, liabilities, income and expenses (the elements of financial statements) when they satisfy the definitions and recognition criteria for those elements in the Code.

See paragraphs A19 to A22 of Module 2 for further discussion.

Page 139

MODULE 3 \ THE FINANCIAL STATEMENTS

Paragraph Principle Discussion

9 3.4.2.25 Similar and dissimilar items

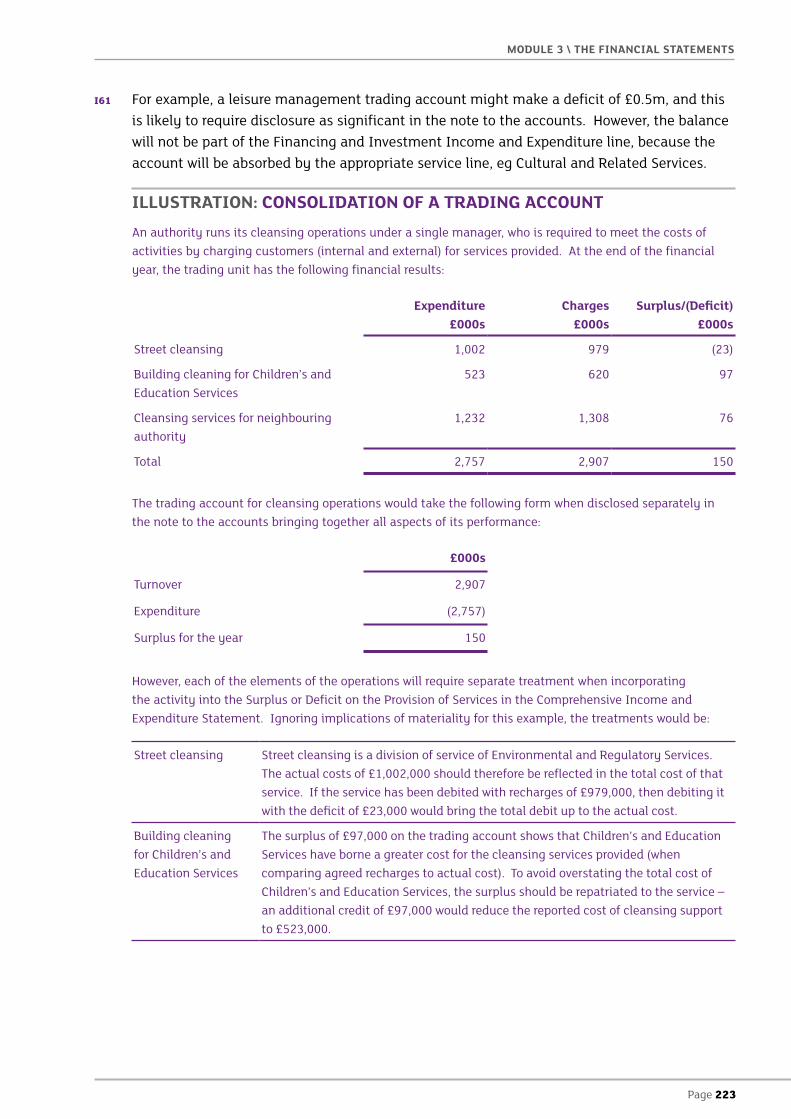

A local authority shall present separately each material class of similar items. A local authority shall present separately items of a dissimilar nature or function unless they are immaterial.

This provision has two main effects:

� where items are similar, they should be grouped together in the financial statements, even if they are then given a more detailed breakdown on the face of one of the statements or in the notes

� where items are dissimilar (particularly where their treatment is not covered by a common accounting policy), they should not be aggregated unless the impact is certain to be immaterial – this principle will apply at the lowest level of disclosure; for example, on the face of the Balance Sheet, Property, Plant and Equipment will aggregate assets measured at historical cost and fair value, but the different categories will need to be separated in a note.

10 3.4.2.26 Immaterial disclosures

A local authority need not provide a specific disclosure required by the Code if the information is not material.

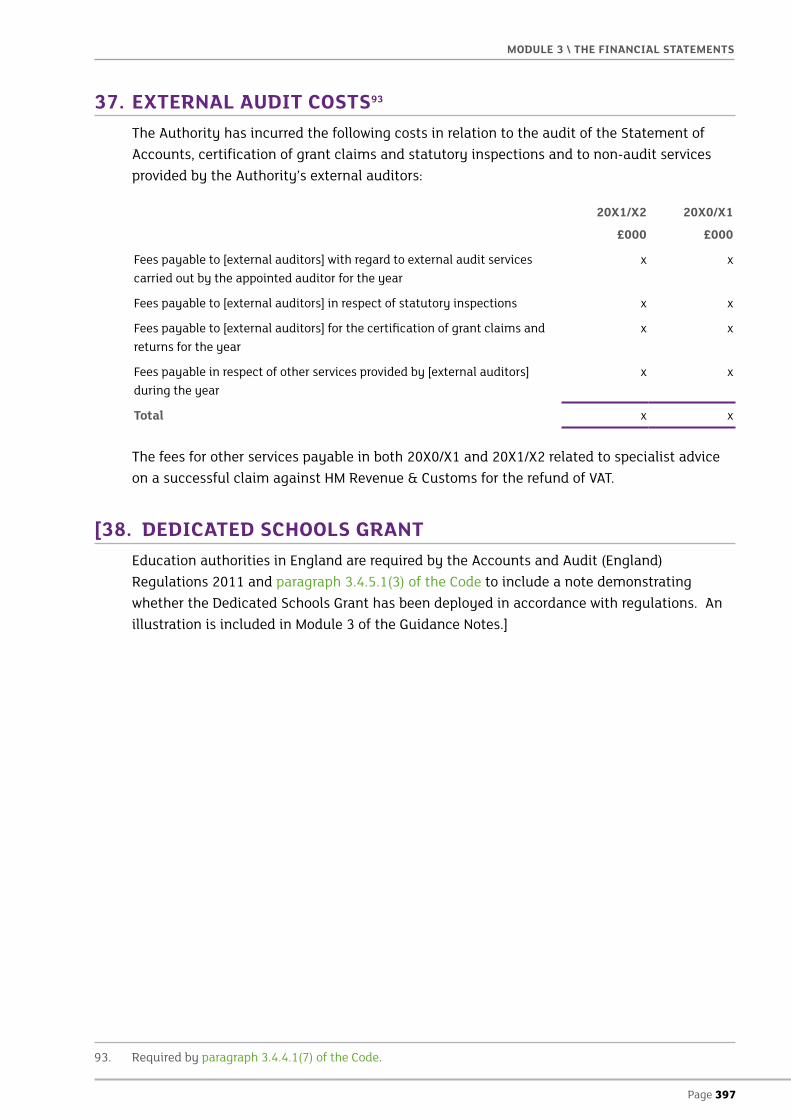

Under this provision authorities are given a comprehensive discretion to disregard Code requirements for disclosures, provided that the information is deemed immaterial. Care needs to be taken to ensure that there would be no readership issues arising from the omission of the information, particularly by considering the qualitative aspects of materiality. For instance, the figures in the note of audit costs are likely to be immaterial in the context of an authority’s overall expenditure, but the purpose of the note is to confirm the independence of the auditor by disclosing the relative amount of fees for non-audit and audit work.

Page 140

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

Paragraph Principle Discussion

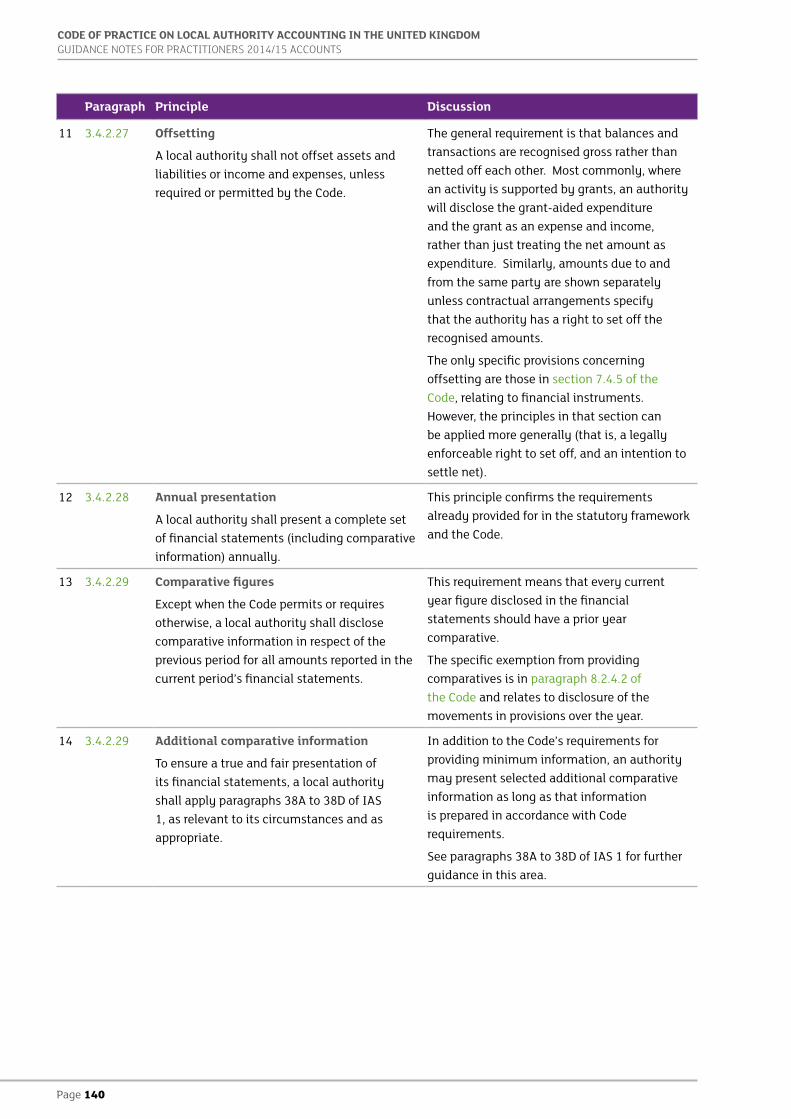

11 3.4.2.27 Offsetting

A local authority shall not offset assets and liabilities or income and expenses, unless required or permitted by the Code.

The general requirement is that balances and transactions are recognised gross rather than netted off each other. Most commonly, where an activity is supported by grants, an authority will disclose the grant-aided expenditure and the grant as an expense and income, rather than just treating the net amount as expenditure. Similarly, amounts due to and from the same party are shown separately unless contractual arrangements specify that the authority has a right to set off the recognised amounts.

The only specific provisions concerning offsetting are those in section 7.4.5 of the Code, relating to financial instruments. However, the principles in that section can be applied more generally (that is, a legally enforceable right to set off, and an intention to settle net).

12 3.4.2.28 Annual presentation

A local authority shall present a complete set of financial statements (including comparative information) annually.

This principle confirms the requirements already provided for in the statutory framework and the Code.

13 3.4.2.29 Comparative figures

Except when the Code permits or requires otherwise, a local authority shall disclose comparative information in respect of the previous period for all amounts reported in the current period’s financial statements.

This requirement means that every current year figure disclosed in the financial statements should have a prior year comparative.

The specific exemption from providing comparatives is in paragraph 8.2.4.2 of the Code and relates to disclosure of the movements in provisions over the year.

14 3.4.2.29 Additional comparative information

To ensure a true and fair presentation of its financial statements, a local authority shall apply paragraphs 38A to 38D of IAS 1, as relevant to its circumstances and as appropriate.

In addition to the Code’s requirements for providing minimum information, an authority may present selected additional comparative information as long as that information is prepared in accordance with Code requirements.

See paragraphs 38A to 38D of IAS 1 for further guidance in this area.

Page 141

MODULE 3 \ THE FINANCIAL STATEMENTS

Paragraph Principle Discussion

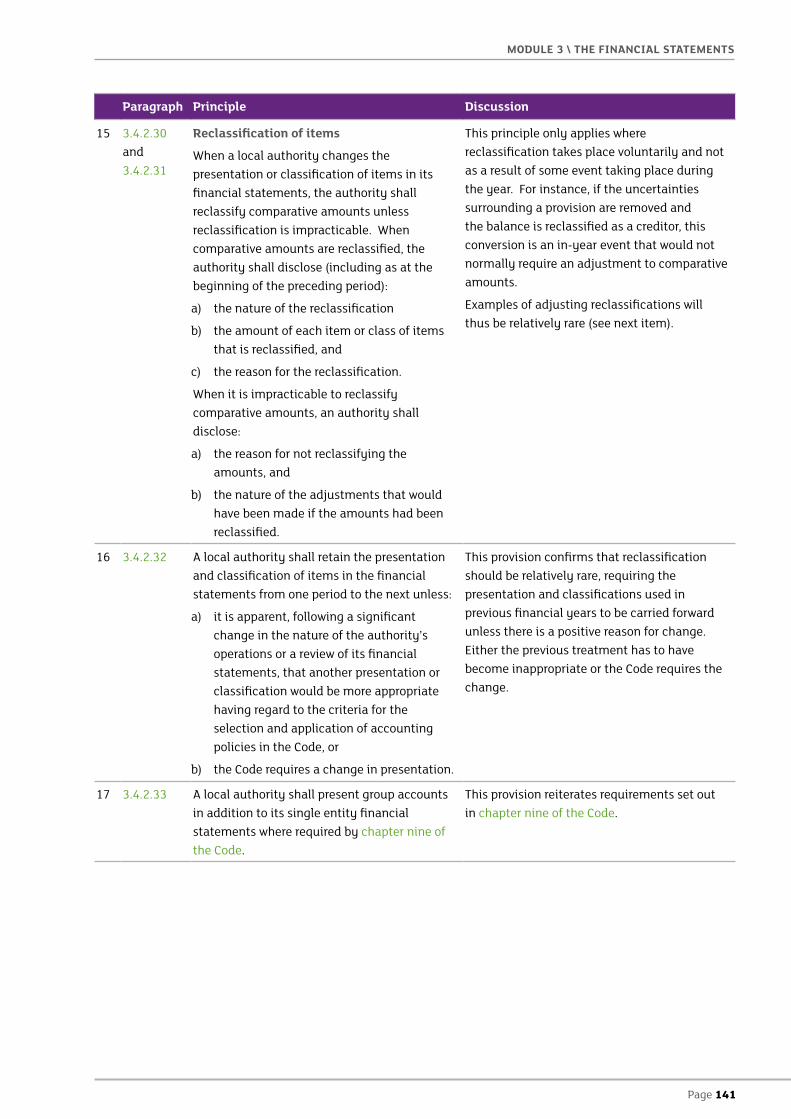

15 3.4.2.30 and 3.4.2.31

Reclassification of items

When a local authority changes the presentation or classification of items in its financial statements, the authority shall reclassify comparative amounts unless reclassification is impracticable. When comparative amounts are reclassified, the authority shall disclose (including as at the beginning of the preceding period):

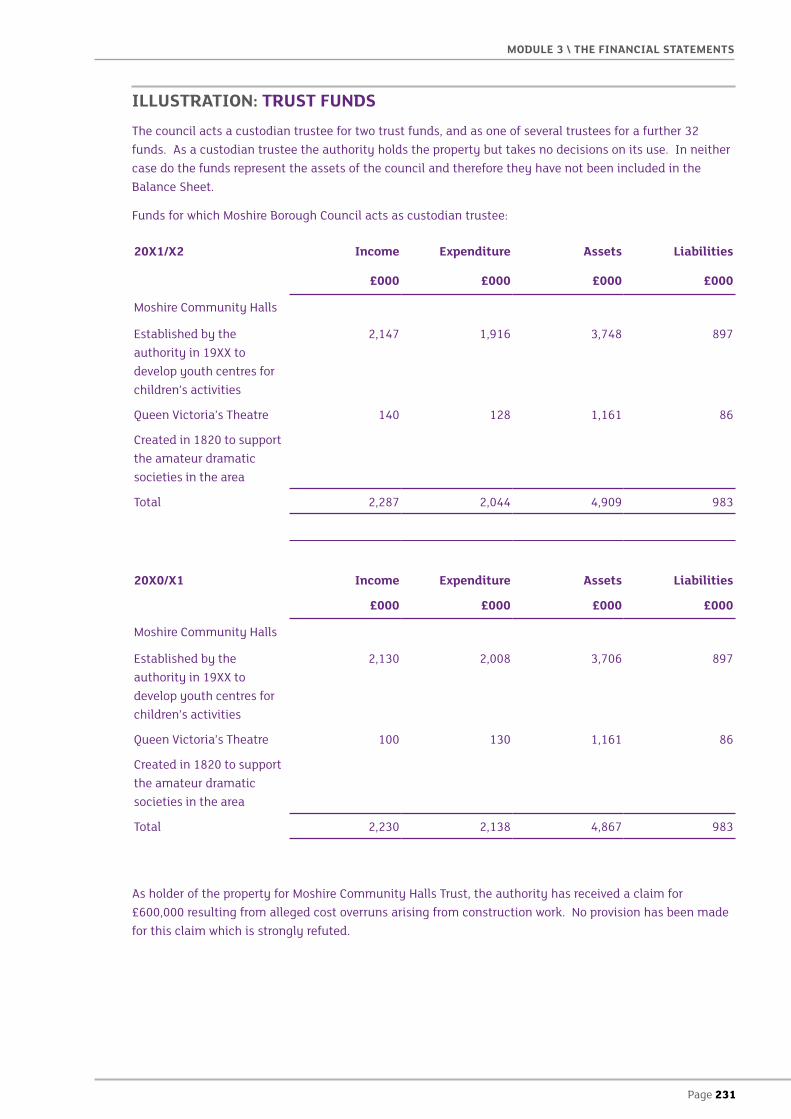

a) the nature of the reclassification

b) the amount of each item or class of items that is reclassified, and

c) the reason for the reclassification.

When it is impracticable to reclassify comparative amounts, an authority shall disclose:

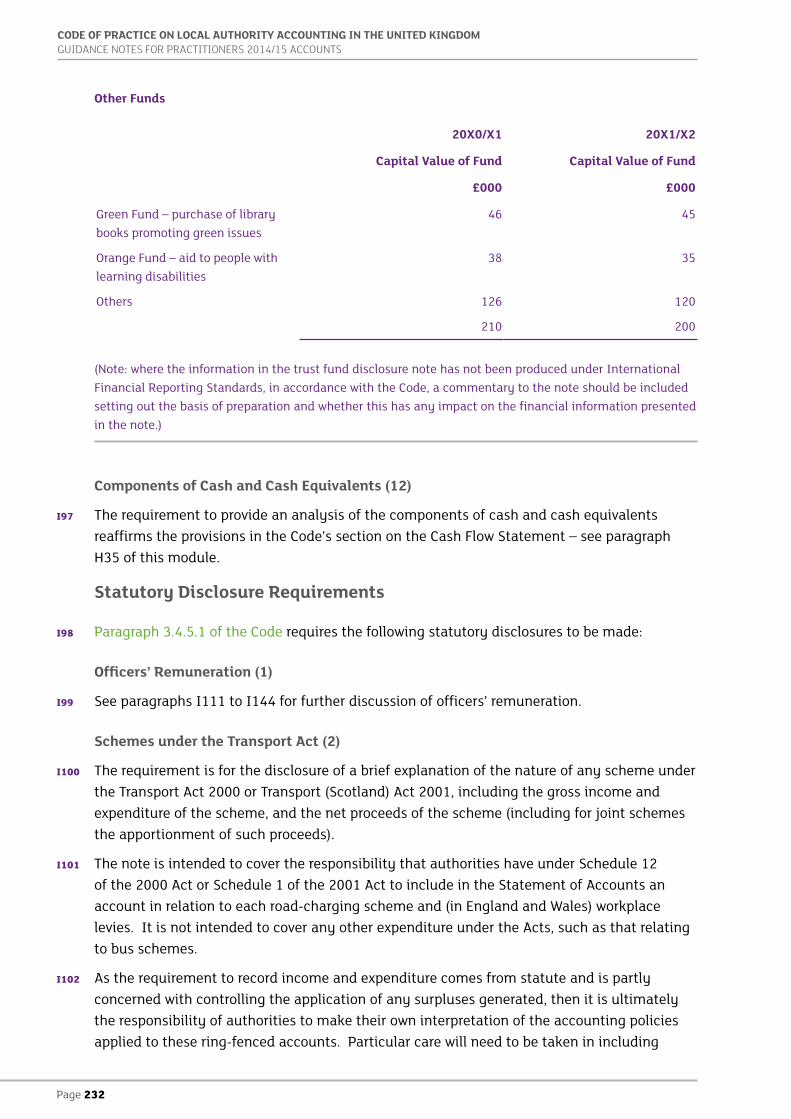

a) the reason for not reclassifying the amounts, and

b) the nature of the adjustments that would have been made if the amounts had been reclassified.

This principle only applies where reclassification takes place voluntarily and not as a result of some event taking place during the year. For instance, if the uncertainties surrounding a provision are removed and the balance is reclassified as a creditor, this conversion is an in-year event that would not normally require an adjustment to comparative amounts.

Examples of adjusting reclassifications will thus be relatively rare (see next item).

16 3.4.2.32 A local authority shall retain the presentation and classification of items in the financial statements from one period to the next unless:

a) it is apparent, following a significant change in the nature of the authority’s operations or a review of its financial statements, that another presentation or classification would be more appropriate having regard to the criteria for the selection and application of accounting policies in the Code, or

b) the Code requires a change in presentation.

This provision confirms that reclassification should be relatively rare, requiring the presentation and classifications used in previous financial years to be carried forward unless there is a positive reason for change. Either the previous treatment has to have become inappropriate or the Code requires the change.

17 3.4.2.33 A local authority shall present group accounts in addition to its single entity financial statements where required by chapter nine of the Code.

This provision reiterates requirements set out in chapter nine of the Code.

Page 142

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

Paragraph Principle Discussion

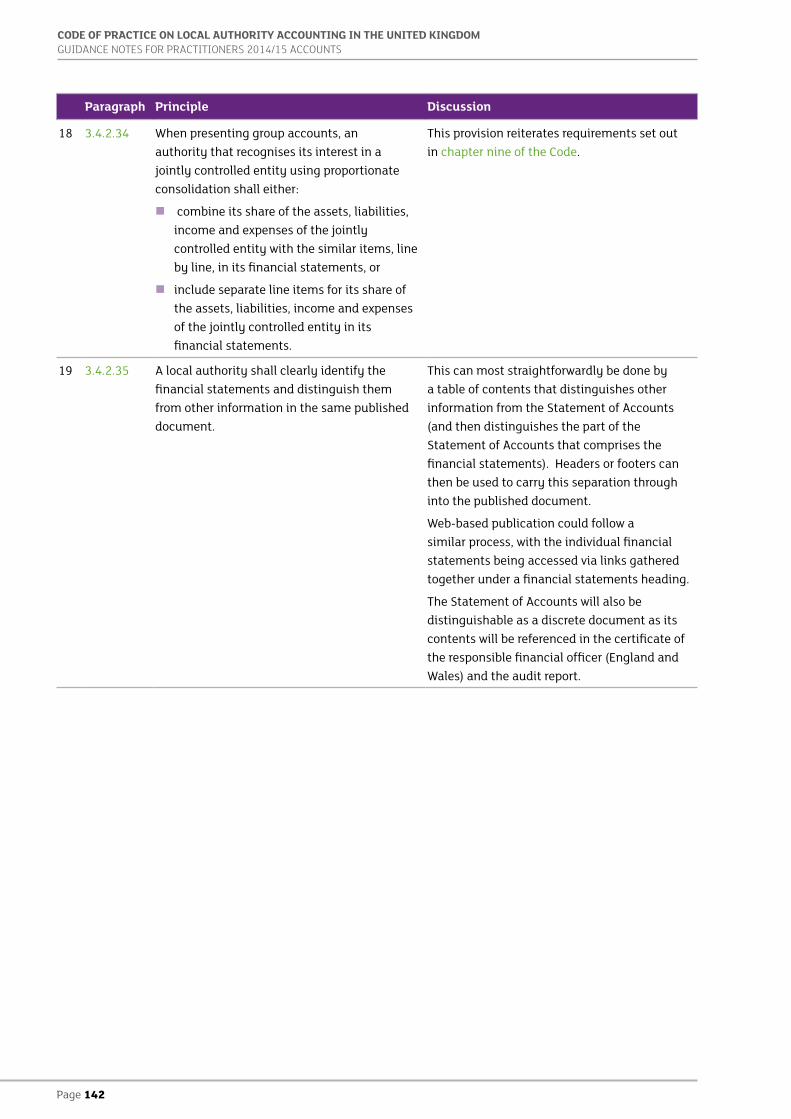

18 3.4.2.34 When presenting group accounts, an authority that recognises its interest in a jointly controlled entity using proportionate consolidation shall either:

� combine its share of the assets, liabilities, income and expenses of the jointly controlled entity with the similar items, line by line, in its financial statements, or

� include separate line items for its share of the assets, liabilities, income and expenses of the jointly controlled entity in its financial statements.

This provision reiterates requirements set out in chapter nine of the Code.

19 3.4.2.35 A local authority shall clearly identify the financial statements and distinguish them from other information in the same published document.

This can most straightforwardly be done by a table of contents that distinguishes other information from the Statement of Accounts (and then distinguishes the part of the Statement of Accounts that comprises the financial statements). Headers or footers can then be used to carry this separation through into the published document.

Web-based publication could follow a similar process, with the individual financial statements being accessed via links gathered together under a financial statements heading.

The Statement of Accounts will also be distinguishable as a discrete document as its contents will be referenced in the certificate of the responsible financial officer (England and Wales) and the audit report.

Page 143

MODULE 3 \ THE FINANCIAL STATEMENTS

Paragraph Principle Discussion

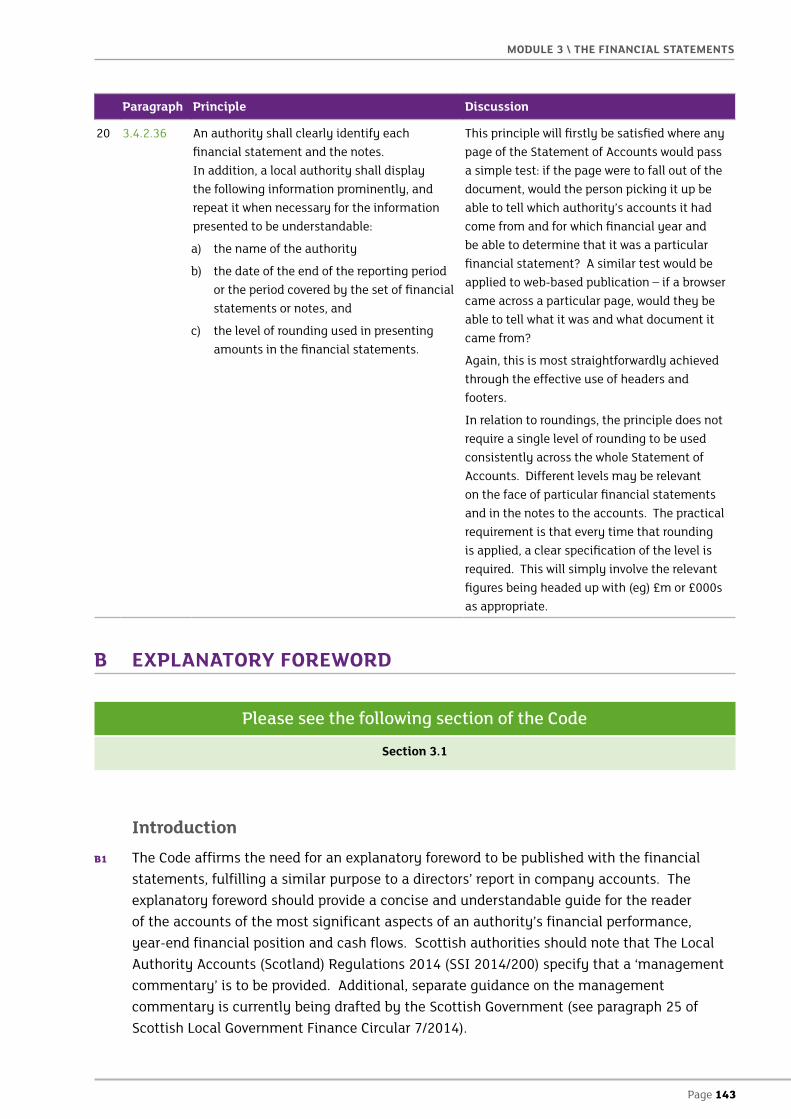

20 3.4.2.36 An authority shall clearly identify each financial statement and the notes. In addition, a local authority shall display the following information prominently, and repeat it when necessary for the information presented to be understandable:

a) the name of the authority

b) the date of the end of the reporting period or the period covered by the set of financial statements or notes, and

c) the level of rounding used in presenting amounts in the financial statements.

This principle will firstly be satisfied where any page of the Statement of Accounts would pass a simple test: if the page were to fall out of the document, would the person picking it up be able to tell which authority’s accounts it had come from and for which financial year and be able to determine that it was a particular financial statement? A similar test would be applied to web-based publication – if a browser came across a particular page, would they be able to tell what it was and what document it came from?

Again, this is most straightforwardly achieved through the effective use of headers and footers.

In relation to roundings, the principle does not require a single level of rounding to be used consistently across the whole Statement of Accounts. Different levels may be relevant on the face of particular financial statements and in the notes to the accounts. The practical requirement is that every time that rounding is applied, a clear specification of the level is required. This will simply involve the relevant figures being headed up with (eg) £m or £000s as appropriate.

B EXPLANATORY FOREWORD

Please see the following section of the Code

Section 3.1

Introduction B1 The Code affirms the need for an explanatory foreword to be published with the financial

statements, fulfilling a similar purpose to a directors’ report in company accounts. The explanatory foreword should provide a concise and understandable guide for the reader of the accounts of the most significant aspects of an authority’s financial performance, year-end financial position and cash flows. Scottish authorities should note that The Local Authority Accounts (Scotland) Regulations 2014 (SSI 2014/200) specify that a ‘management commentary’ is to be provided. Additional, separate guidance on the management commentary is currently being drafted by the Scottish Government (see paragraph 25 of Scottish Local Government Finance Circular 7/2014).

Page 144

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

B2 Paragraph 1.5.3 of the Code requires that the foreword is ‘to’ rather than ‘in’ the Statement of Accounts. This is an important distinction in that it establishes that the foreword is not formally part of the Statement of Accounts and is not then covered directly by the statutory requirements for an audit opinion or (in England and Wales) certification by the responsible financial officer. The foreword then needs to be prepared so that it is consistent with the Statement of Accounts but is not formally bound by true and fair requirements. This means that any figures that are used in the foreword do not have to be based on the Code’s provisions if they would help present the authority’s messages more effectively (whilst remaining consistent with the figures in the Statement of Accounts).

B3 Paragraph 3.1.1.2 of the Code places a limitation on the foreword in that it confirms that its purpose is not to comment on the policies of the authority. This does not mean that the foreword should be free of details of strategic objectives and spending priorities, as it may be impossible to give a proper explanation of the authority’s financial performance and position without some political context. The limitation should instead be read as prohibiting attempts to persuade readers to hold a particular view about the authority’s policies.

B4 Apart from this limitation, the Code is clear that the content and style of the foreword should be a matter of local judgement.

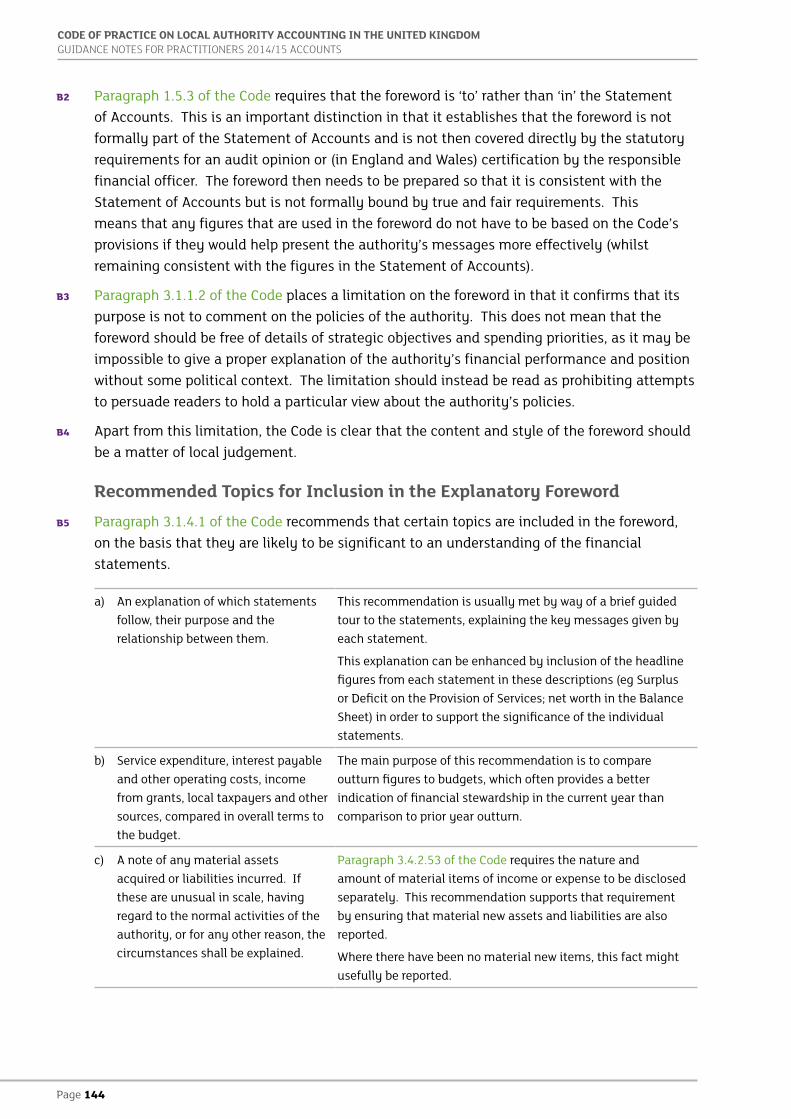

Recommended Topics for Inclusion in the Explanatory ForewordB5 Paragraph 3.1.4.1 of the Code recommends that certain topics are included in the foreword,

on the basis that they are likely to be significant to an understanding of the financial statements.

a) An explanation of which statements follow, their purpose and the relationship between them.

This recommendation is usually met by way of a brief guided tour to the statements, explaining the key messages given by each statement.

This explanation can be enhanced by inclusion of the headline figures from each statement in these descriptions (eg Surplus or Deficit on the Provision of Services; net worth in the Balance Sheet) in order to support the significance of the individual statements.

b) Service expenditure, interest payable and other operating costs, income from grants, local taxpayers and other sources, compared in overall terms to the budget.

The main purpose of this recommendation is to compare outturn figures to budgets, which often provides a better indication of financial stewardship in the current year than comparison to prior year outturn.

c) A note of any material assets acquired or liabilities incurred. If these are unusual in scale, having regard to the normal activities of the authority, or for any other reason, the circumstances shall be explained.

Paragraph 3.4.2.53 of the Code requires the nature and amount of material items of income or expense to be disclosed separately. This recommendation supports that requirement by ensuring that material new assets and liabilities are also reported.

Where there have been no material new items, this fact might usefully be reported.

Page 145

MODULE 3 \ THE FINANCIAL STATEMENTS

d) A note explaining the significance of any pensions liability or asset disclosed.

As the pensions liability is likely to have a highly significant impact on the net worth of an authority (particularly where pension schemes are unfunded), this impact merits particular explanation.

e) An explanation of any material and unusual charge or credit in the accounts. This shall be provided whether the charge is made as part of the cost of services or as an adjustment to the cost of services.

This recommendation complements the requirement of paragraph 3.4.2.53 of the Code for separate disclosure of material items of income and expense in the notes to the accounts. Unusual items included in that note should be highlighted in the foreword and explained in more detail, including those charged or credited to both the Comprehensive Income and Expenditure Statement and the Movement in Reserves Statement.

f) Any significant change in accounting policies. The reason for the change, and the effect on the accounts, shall be explained.

The impact of changes in accounting policies will be detailed in the notes to the financial statements. This recommendation encourages a summary of such changes where they are significant. ‘Significant’ in this context could be read to exclude technical accounting changes that do not have a material practical effect on financial performance or position.

g) Any major change in statutory functions, eg local government reorganisation, which has a significant impact on the accounts. In addition, a comment on planned future developments in service delivery, including a summary of revenue and capital investment plans, distinguishing between expenditure intended to maintain existing levels of service provision and that intended to expand existing services or develop new services and the impact of any reduction in services.

Major changes such as reorganisation and housing stock transfers that have taken place in the year will have had a fundamental impact on the financial statements and will have been given full disclosure. For those changes, this recommendation encourages an up-front explanation of those changes and a summary of the impact.

Future developments will only have been reflected in the financial statements or notes where events have taken place before the accounts are authorised for issue. The explanatory foreword can usefully set out the potential implications of changes in government or authority policy.

h) A note of the authority’s current borrowing facilities and capital borrowing, outlining the purpose and impact of financing transactions entered into during the year and major non-current asset acquisitions and disposals.

For many authorities, the outstanding balance of loans will be an incomprehensibly substantial balance for most readers of the accounts. This recommendation allows an authority to explain how its level of borrowing is prudent and justified by its capital investment programme. Useful context would be provided by reference to the fair value of the authority’s non-current assets and the Capital Financing Requirement.

i) A summary of the authority’s internal and external sources of funds available to meet its capital expenditure plans and other financial commitments including PFI schemes.

This provides an opportunity to give assurance that the authority’s financial position and future prospects support its plans for capital investment.

Page 146

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

j) Details of significant provisions or contingencies and material write-offs. This disclosure should focus on new items and any significant changes to existing items.

As transactions requiring provisions and write-offs to be made can be significant to an authority (eg losses relating to Icelandic banks) but also involve uncertainties, it will be useful to provide a clear consolidated summary and explanation of all such losses.

(‘Write offs’ in this context should be read to include revaluation and impairment losses.)

k) Details of any material events after the reporting date (up to the date the accounts are authorised for issue).

These events will have been reflected in the financial statements, but adjusting events might not have been given the prominence that non-adjusting events have (which require a note). A summary of all material events in the explanatory foreword can therefore be helpful in confirming comprehensively the overall effect.

l) An explanation of the impact of the current economic climate on the authority and the services it provides.

Where the current economic climate has had a direct effect on the authority, this will be reflected in the financial statements (eg in the impairment of assets). This recommendation provides an opportunity to summarise these effects, but also to provide a forward-looking prognosis for the adequacy of the authority’s financial resources.

Issues of particular interest relating to the longer-term effects of the economic downturn might include:

� the extent to which particular spending plans and budgeted income were affected during the year

� the adequacy of balances and reserves to withstand future financial pressures

� how the values of the authority’s assets (and liabilities) have been or might be affected.

B6 The explanatory foreword is also an appropriate place to clarify the relationships between the Statement of Accounts and the other financial information that the authority reports externally. This might be especially relevant for plans that have been published in advance of the availability of outturn figures, where the Statement of Accounts provides an opportunity to provide a more up-to-date context for the plans and the authority’s performance.

B7 As the purpose of the explanatory foreword is to make local authority accounts comprehensible to a wide audience, authorities should use non-technical language in describing what are often complex matters and avoid the use of jargon. Care should be taken not to overwhelm the reader with detail or to obscure the real picture of the authority’s financial standing.

Recommended Practice B8 Entities in the private sector and other public benefit entities are required to produce a

directors’ report (or equivalent statement), one element of which is a business review. This element is the closest parallel to the explanatory foreword that local authorities are required to produce.

B9 Many entities in the private and public sector meet the requirement for a business review by preparing an operating and financial review (OFR). The Accounting Standards Board (ASB)

Page 147

MODULE 3 \ THE FINANCIAL STATEMENTS

issued a Reporting Statement (RS) relating to the OFR in January 2006. It contains seven principles that can provide a useful basis for the production of the explanatory foreword of a local authority. The following table adapts these seven principles for local government:

Purpose Commentary

The explanatory foreword should set out an analysis of the authority through the eyes of management.

Authorities that draft the foreword as a personal report from the member responsible for finance or the director of finance (rather than just put their name at the bottom) have taken a significant step to satisfying this principle.

The intention is that management should use its expert knowledge of the authority’s financial affairs to illuminate the accounts by:

� adding more detail to the significant aspects of the information about the authority’s financial performance and financial position already in the financial statements

� providing an assessment as to whether the authority has performed well during the year in using its revenue and capital resources

� advising on the strategies management will implement to achieve the authority’s corporate objectives, specific performance measures that they might regularly review to achieve those objectives and significant risks that the authority is exposed to.

The explanatory foreword should focus on matters that are relevant to the interests of the principal users of the accounts.

This principle presents difficulties for local authorities, who have a multiplicity of potential users. The foreword cannot be written for a single ideal reader. Some sections will therefore require more detail or merit the use of more technical terminology. However, each section should have a clearly intended readership and be written to meet the assessed needs of that readership.

The explanatory foreword should have a forward-looking orientation, identifying those trends and factors relevant to the users’ assessment of the current and future performance of the authority and the progress towards the achievement of its long-term objectives.

It has traditionally been the case that the foreword is a backward-looking document. There is greater justification for this in the local government than in the private sector, as the annual budgeting process means that individual financial years are more capable of being assessed in isolation. However, issues that should be addressed are those that affected the authority’s development, performance and position during the current year and that are likely to impact on the future development, performance and position.

Issues might include:

� An explanation of resources, principal risks and uncertainties that will impact on the performance or position of the authority. For example, the changing budgetary situation of local authorities is likely to be a resource issue and an area of significant risk and uncertainty for most local authorities in the current economic environment.

� An analysis of trends or factors that management believe will impact on future prospects. Again, the current economic environment, budgetary trends and pensions forecast may be of interest to users of the financial statements.

� Information on future targets (eg key performance information) which management uses to measure achievement of their objectives.

The ASB’s Reporting Statement acknowledges concerns about the disclosure of forward-looking information. Management may wish to indicate that such information should be treated with caution and explain the uncertainties inherent in such information.

Page 148

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

Purpose Commentary

The explanatory foreword should complement as well as supplement the financial statements, in order to enhance the overall corporate disclosure.

The foreword should extend the information in the financial statements to incorporate contextual information that:

� provides additional explanations of amounts recorded in the financial statements

� explains the conditions and events that have shaped the information contained in the financial statements.

Relevant complementary information might come from sources such as the revenue budget, the capital programme and the treasury management policy.

The explanatory foreword should be comprehensive and understandable.

Presentation should be clear and generally avoid unnecessary use of technical terminology. The balance between narrative, tabular and graphical presentation should be carefully judged if it is to be effective.

The explanatory foreword should be balanced and neutral, dealing even-handedly with both good and bad aspects.

Management should maintain a balance between good and bad news, give details of unfavourable events and include information about setbacks as well as positive events.

The explanatory foreword should be comparable over time.

This should mean that management provides consistent measures of performance from year to year and that the content of the foreword is consistent (within the boundaries of ensuring that the information is relevant) from year to year.

Voluntary/Optional Approach to the Production of the Explanatory Foreword

B10 The preceding paragraphs of this section reflect the requirements of the Code since the implementation of IFRS in 2010/11. The Code includes an encouragement for local authorities to prepare the Explanatory Foreword taking into consideration the provisions of paragraphs 5.2.6–5.2.8 of Government’s Financial Reporting Manual (FReM) where these paragraphs disclose information relevant to local authorities.

B11 If authorities opt to take the FReM into consideration this might not necessarily mean that substantial amendment will be needed to the format that an authority has traditionally used.

B12 The FReM disclosures may be used effectively to provide a checklist against which practitioners can analyse the adequacy of their existing format and demonstrate the performance and financial position of the authority.

B13 Paragraphs 5.2.6 to 5.2.8 of the FReM contain a mixture of direct requirements for disclosures, as well as cross-references to requirements set out in the Companies Act 2006 (as amended). In summary, the consolidated requirements are for:

Page 149

MODULE 3 \ THE FINANCIAL STATEMENTS

Requirement Discussion

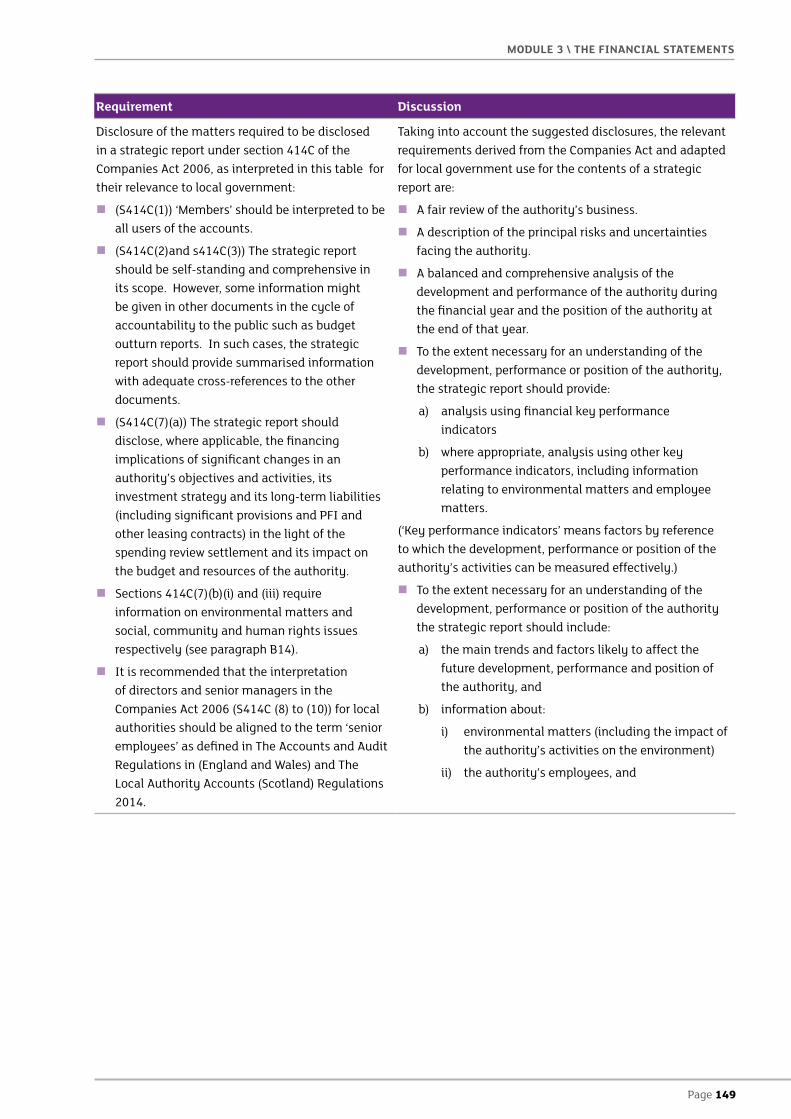

Disclosure of the matters required to be disclosed in a strategic report under section 414C of the Companies Act 2006, as interpreted in this table for their relevance to local government:

� (S414C(1)) ‘Members’ should be interpreted to be all users of the accounts.

� (S414C(2)and s414C(3)) The strategic report should be self-standing and comprehensive in its scope. However, some information might be given in other documents in the cycle of accountability to the public such as budget outturn reports. In such cases, the strategic report should provide summarised information with adequate cross-references to the other documents.

� (S414C(7)(a)) The strategic report should disclose, where applicable, the financing implications of significant changes in an authority’s objectives and activities, its investment strategy and its long-term liabilities (including significant provisions and PFI and other leasing contracts) in the light of the spending review settlement and its impact on the budget and resources of the authority.

� Sections 414C(7)(b)(i) and (iii) require information on environmental matters and social, community and human rights issues respectively (see paragraph B14).

� It is recommended that the interpretation of directors and senior managers in the Companies Act 2006 (S414C (8) to (10)) for local authorities should be aligned to the term ‘senior employees’ as defined in The Accounts and Audit Regulations in (England and Wales) and The Local Authority Accounts (Scotland) Regulations 2014.

Taking into account the suggested disclosures, the relevant requirements derived from the Companies Act and adapted for local government use for the contents of a strategic report are:

� A fair review of the authority’s business.

� A description of the principal risks and uncertainties facing the authority.

� A balanced and comprehensive analysis of the development and performance of the authority during the financial year and the position of the authority at the end of that year.

� To the extent necessary for an understanding of the development, performance or position of the authority, the strategic report should provide:

a) analysis using financial key performance indicators

b) where appropriate, analysis using other key performance indicators, including information relating to environmental matters and employee matters.

(‘Key performance indicators’ means factors by reference to which the development, performance or position of the authority’s activities can be measured effectively.)

� To the extent necessary for an understanding of the development, performance or position of the authority the strategic report should include:

a) the main trends and factors likely to affect the future development, performance and position of the authority, and

b) information about:

i) environmental matters (including the impact of the authority’s activities on the environment)

ii) the authority’s employees, and

Page 150

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

Requirement Discussion

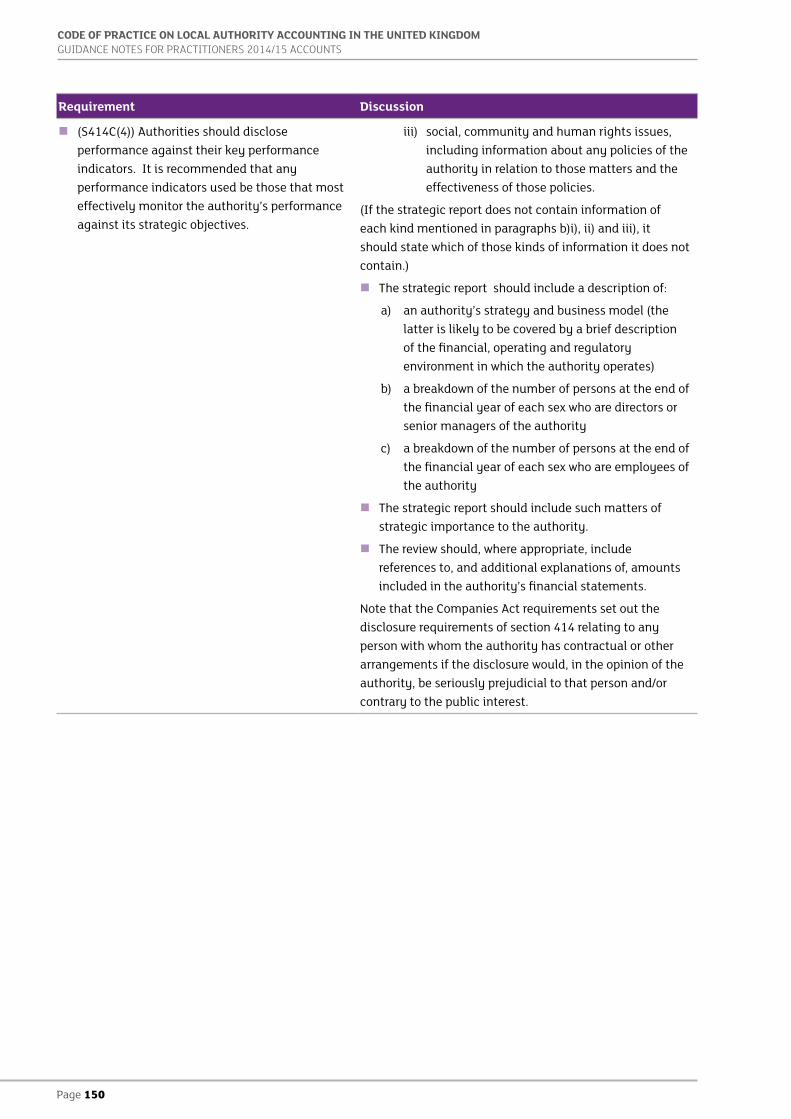

� (S414C(4)) Authorities should disclose performance against their key performance indicators. It is recommended that any performance indicators used be those that most effectively monitor the authority’s performance against its strategic objectives.

iii) social, community and human rights issues, including information about any policies of the authority in relation to those matters and the effectiveness of those policies.

(If the strategic report does not contain information of each kind mentioned in paragraphs b)i), ii) and iii), it should state which of those kinds of information it does not contain.)

� The strategic report should include a description of:

a) an authority’s strategy and business model (the latter is likely to be covered by a brief description of the financial, operating and regulatory environment in which the authority operates)

b) a breakdown of the number of persons at the end of the financial year of each sex who are directors or senior managers of the authority

c) a breakdown of the number of persons at the end of the financial year of each sex who are employees of the authority

� The strategic report should include such matters of strategic importance to the authority.

� The review should, where appropriate, include references to, and additional explanations of, amounts included in the authority’s financial statements.

Note that the Companies Act requirements set out the disclosure requirements of section 414 relating to any person with whom the authority has contractual or other arrangements if the disclosure would, in the opinion of the authority, be seriously prejudicial to that person and/or contrary to the public interest.

Page 151

MODULE 3 \ THE FINANCIAL STATEMENTS

Requirement Discussion

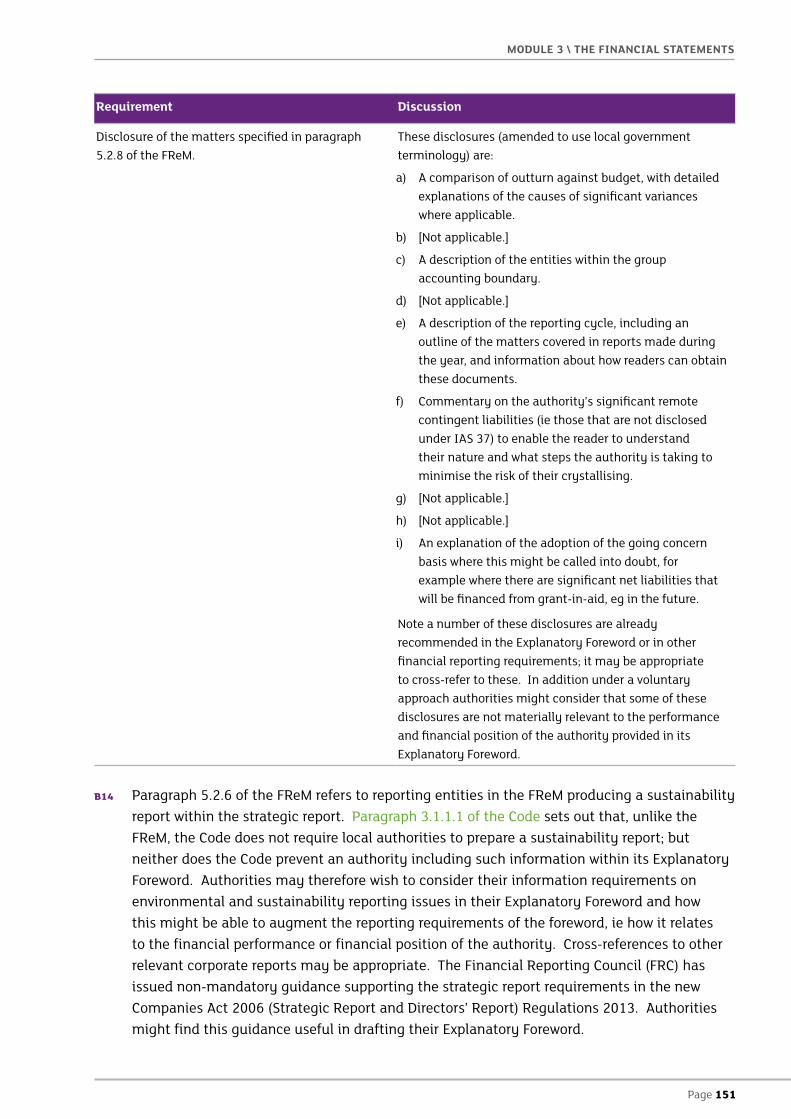

Disclosure of the matters specified in paragraph 5.2.8 of the FReM.

These disclosures (amended to use local government terminology) are:

a) A comparison of outturn against budget, with detailed explanations of the causes of significant variances where applicable.

b) [Not applicable.]

c) A description of the entities within the group accounting boundary.

d) [Not applicable.]

e) A description of the reporting cycle, including an outline of the matters covered in reports made during the year, and information about how readers can obtain these documents.

f) Commentary on the authority’s significant remote contingent liabilities (ie those that are not disclosed under IAS 37) to enable the reader to understand their nature and what steps the authority is taking to minimise the risk of their crystallising.

g) [Not applicable.]

h) [Not applicable.]

i) An explanation of the adoption of the going concern basis where this might be called into doubt, for example where there are significant net liabilities that will be financed from grant-in-aid, eg in the future.

Note a number of these disclosures are already recommended in the Explanatory Foreword or in other financial reporting requirements; it may be appropriate to cross-refer to these. In addition under a voluntary approach authorities might consider that some of these disclosures are not materially relevant to the performance and financial position of the authority provided in its Explanatory Foreword.

B14 Paragraph 5.2.6 of the FReM refers to reporting entities in the FReM producing a sustainability report within the strategic report. Paragraph 3.1.1.1 of the Code sets out that, unlike the FReM, the Code does not require local authorities to prepare a sustainability report; but neither does the Code prevent an authority including such information within its Explanatory Foreword. Authorities may therefore wish to consider their information requirements on environmental and sustainability reporting issues in their Explanatory Foreword and how this might be able to augment the reporting requirements of the foreword, ie how it relates to the financial performance or financial position of the authority. Cross-references to other relevant corporate reports may be appropriate. The Financial Reporting Council (FRC) has issued non-mandatory guidance supporting the strategic report requirements in the new Companies Act 2006 (Strategic Report and Directors’ Report) Regulations 2013. Authorities might find this guidance useful in drafting their Explanatory Foreword.

Page 152

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

C STATEMENT OF RESPONSIBILITIES

Please see the following section of the Code

Paragraphs 3.2.1 to 3.2.4

IntroductionC1 Paragraph 3.2.4.1 of the Code contains a model disclosure of the authority’s and the chief

financial officer’s responsibilities for the Statement of Accounts. Authorities have generally been able to adopt this model without substantial amendment.

C2 The Code requires that the chief financial officer should sign and date the Statement of Accounts under a statement that the accounts give a true and fair view of the financial position of the authority at the accounting date and its income and expenditure for the year then ended.

C3 In England, The Accounts and Audit (England) Regulations 2011 require the Statement of Accounts prepared by 30 June to be certified by the responsible financial officer (RFO). The financial statements are then required to be certified again by the RFO immediately before approval by a committee of the council or otherwise by a resolution of the (local government) body meeting as a whole. Such signatures would traditionally be positioned at the foot of the Balance Sheet, but they could also conveniently be fitted into the Statement of Responsibilities.

C4 In Wales, The Accounts and Audit Regulations 2005 have been amended by The Accounts and Audit (Wales) (Amendment) Regulations 2010 (SI 2010/683 (W.66)). The amended regulations also require the Statement of Accounts prepared by 30 June to be certified by the RFO. The financial statements are then required to be certified again by the RFO immediately before approval by a committee of the council or otherwise by a resolution of the (local government) body meeting as a whole. Again, such signatures would traditionally be positioned at the foot of the Balance Sheet, but they could also conveniently be fitted into the Statement of Responsibilities.

C5 In Scotland, The Local Authority Accounts (Scotland) Regulations 2014 (SSI 2014/200) include a requirement for the accounts to be certified by the proper officer as providing a ‘true and fair view’ of the financial position and transactions of the authority and its group. Finance Circular 7/2014 provides an illustrative example of the Statement of Responsibilities based on the guidance in the Code. The regulations further specify that the unaudited accounts must be submitted to the auditor by 30 June and to the local authority (or an audit or governance committee or equivalent) by 31 August.

C6 In Northern Ireland, The Local Government (Accounts and Audit) Regulations (Northern Ireland) 2006 requires the Statement of Accounts prepared by 30 June to be certified by the chief financial officer (CFO) (see also paragraph B14 of Module 1). Again, such signatures would traditionally be positioned at the foot of the Balance Sheet, but they could also conveniently be fitted into the Statement of Responsibilities.

Page 153

MODULE 3 \ THE FINANCIAL STATEMENTS

D ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS

Please see the following section of the Code

Section 3.3

Introduction D1 Paragraph 3.3.1.1 of the Code requires that authorities follow the requirements of IAS 8

Accounting Policies, Changes in Accounting Estimates and Errors when selecting or changing accounting policies, adopting the accounting treatment and disclosing the changes in accounting policies, changing estimation techniques, and correcting errors. An exception is made where adaptations of IAS 8 to fit the public sector are set out in the Code.

D2 The Code also notes that IPSAS 3 Accounting Policies, Changes in Accounting Estimates and Errors (based on IAS 8) does not add any additional accounting requirements but it may be a useful source of reference for local authorities.

Impact of New Standards

D3 Per paragraph 3.3.1.2 of the Code, IAS 8 requires entities to disclose the expected impact of new standards that have been issued but not yet adopted. The disclosure requirements in relation to new standards are set out in paragraph D53 below.

Selection and Application of Accounting Policies D4 Accounting policies are defined in paragraph 3.3.2.1 of the Code as ‘the specific principles,

bases, conventions, rules and practices applied by an authority in preparing and presenting financial statements’.

D5 Paragraph 3.3.2.9 of the Code requires that where the Code applies to a transaction, other event or condition, an authority should determine the accounting policy or policies to be applied to that item with direct reference to the requirements of the accounting policies stipulated by the Code.

Materiality and Accounting Policies

D6 Accounting policies need not be applied if the effect of applying them would be immaterial. Materiality is defined in paragraph 3.3.2.4 of the Code as it applies to omissions and misstatements:

Omissions or misstatements of items are material if they could, individually or collectively, influence the decisions or assessments of users made on the basis of the financial statements. Materiality depends on the nature or size of the omission or misstatement judged in the surrounding circumstances. The nature or size of the item, or a combination of both, could be the determining factor.

Page 154

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

The definition is consistent with the fundamental qualitative characteristics of financial information discussed in the Code and the IASB’s Conceptual Framework (as a subsidiary concept of relevance) and so may be applied to the application of accounting policies, particularly as the non-application of an accounting policy will often lead to an omission or a misstatement (paragraph 2.1.2.9 of the Code).

D7 In applying the definition of materiality, an authority should refer to the characteristics of the financial statements provided by the Code with reference to the IASB’s Conceptual Framework (see paragraphs A36 to A43 of Module 2). The Code states that users of the financial statements are assumed to have a reasonable knowledge of accounting and of local government and will use reasonable diligence in reading the financial statements. Considerations of materiality will need to reflect this assumed knowledge of the prime users of an authority’s financial statements when judging the economic decisions and assessments of stewardship of its resources that could reasonably be influenced by different bases for disclosure of information.

D8 An authority should start from a presumption that the accounting policies prescribed by the Code should be followed. Departure is permitted only once it can be established that omission, or a different or less a rigorous approach, does not risk a misreading of the authority’s overall financial position, financial performance or cash flows (or any part of it) that might be relevant to the decision-making needs or assessments of the primary users of the financial statements.

D9 Paragraph 8 of IAS 8 also notes that it is inappropriate to make or leave uncorrected immaterial departures from IFRS to achieve a particular presentation, financial position or cash flows. Judgement will need to be made with careful assessment to the economic decisions and assessments of stewardship made by the users of the financial statements. For example, for the authority as a whole, it might be immaterial to revalue plant and equipment. However, the understatement of depreciation that would result for a trading account might allow it to break even when full compliance with the Code would have resulted in a loss being recognised.

Transactions Outside the Scope of the Code

D10 Where the Code does not specifically apply to a transaction, other event or condition, a local authority should use its judgement in developing or applying an accounting policy which results in financial information which is relevant to the decision-making and assessment needs of users. Paragraph 3.3.2.9 of the Code also requires that policies are reliable; ie they:

� represent faithfully the financial position, financial performance and cash flows of the entity – the policy should recognise and measure effectively the income and expense incurred and the assets and liabilities created, increased, reduced or extinguished as a result of a transaction or event

� reflect the economic substance of transactions, other events and conditions and not merely the legal form – the legal form of a transaction does not always represent its economic reality and may need to be overridden; eg an authority can hold the legal title to a property but control none of the future economic benefits or service potential that the property will generate

Page 155

MODULE 3 \ THE FINANCIAL STATEMENTS

� are neutral, ie free from bias – financial statements are not neutral if a particular accounting policy has been selected in a manner designed to influence the making of a decision or assessment in order to achieve a predetermined result or outcome

� are prudent – paragraph 37 of the IASB Framework defines prudence as ‘the inclusion of a degree of caution in the exercise of the judgements needed in making the estimates required under conditions of uncertainty, such that assets or income are not overstated and liabilities or expenses are not understated’, and

� are complete in all material respects.

D11 On occasions where the Code does not specifically apply to a transaction, a local authority will still need to use the Code for its principal source of guidance. It should consider the applicability of the following:

� the Code’s provisions in relation to similar transactions, and related issues

� the definitions, recognition and measurement criteria for assets, liabilities, income and expenses described in chapter two of the Code – see paragraphs A81 to A111 of Module 2.

Note that paragraph 11 of IAS 8 requires that these two provisions be applied in descending order – ie practitioners should consider the Code’s provisions in relation to similar transactions before carrying out a ‘first principles’ analysis based on the definitional criteria.

D12 Local authorities may also consider recent pronouncements by standard setters, and accepted accounting practices within the public sector, but only in so far as these do not conflict with the provisions of the Code. Please also see paragraphs A13 to A16 of Module 1.

Consistency

D13 Paragraph 3.3.2.11 of the Code requires that authorities select and apply their accounting policies consistently for similar transactions, other events and conditions. If the Code specifically requires or permits different accounting policies for categories of similar items, an authority should apply an appropriate policy for each of the categories in question and apply these accounting policies consistently for each category. The Code provides the example of different classes of property, plant and equipment, some of which are carried at fair value and some at historical cost.

Changes in Accounting Policies

D14 Paragraph 3.3.2.12 of the Code requires that a change in accounting policy should only be made if the change:

� is required by the Code, or

� will result in the financial statements providing reliable and more relevant financial information about the effects of transactions, other events or conditions on an authority’s financial position, financial performance and cash flows.

D15 In accordance with the qualitative characteristic of comparability (which depends on consistency and adequate disclosure), an authority should apply the same accounting policy consistently from one period to the next (and within each period), until one of the two conditions for change is satisfied. The users of the financial statements need to be able

Page 156

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

to compare financial statements and information over time in order to be able to evaluate trends in its financial position, financial performance and cash flows (IAS 8, paragraph 15).

D16 It is likely that significant changes in accounting policy other than those specified by the Code will be relatively rare. This is because the Code specifies the accounting policies for a high percentage of the typical transactions, items, events or other conditions that are faced by local authorities (see paragraphs A5 and A6 of Module 2). In addition, some of the options offered by IFRS have been limited by the Code. Examples include the measurement after recognition of property, plant and equipment and options for designation of certain financial instruments.

D17 There are therefore limited opportunities for an authority to choose an accounting policy (as opposed to a basis for estimating figures that will satisfy that policy). Recognition, measurement bases and presentation treatments are specified for the most significant transactions by the Code. However, choices in accounting policies do still exist in the Code, eg in relation to the capitalisation of borrowing costs or where the Code is silent on an unusual transaction.

D18 Paragraph 16 of IAS 8 states that the introduction of an accounting policy to account for transactions or events that are different in substance from those previously occurring (ie where circumstances have changed) is not a change in accounting policy. Likewise, adopting an accounting policy for transactions, other events or conditions that did not occur previously or that were immaterial is not a change in accounting policy and therefore would be applied prospectively.

D19 An example of the situation where a change in circumstances would not meet the Code’s requirements for a change in accounting policy would be where a local authority changes the use of a property. For instance, an authority might move staff out of a building it previously used for administrative purposes and designate the property instead as an investment property. This would mean a slightly different definition of fair value and a different treatment of revaluation gains and losses. However, this is not a change in accounting policy and so no restatement of comparative amounts should be made.

Applying a Change in Accounting Policy

D20 Paragraph 3.3.2.13 of the Code requires that a change in accounting policy is applied retrospectively unless the Code stipulates particular transitional arrangements. Specific transitional provisions are often included in new or revised standards rather than full retrospective application, and the Code will specify transitional arrangements for new standards adopted by the Code where retrospection is impracticable for local government as a whole.

D21 Retrospective application is defined in paragraph 3.3.2.7 of the Code as ‘applying a new accounting policy to transactions, other events and conditions as if that policy had always been applied’. The restated accounts should thus be cleared of the effects of the previous accounting policy, and balances and comparative transactions should be recalculated to apply the policy from the date the income, expense, asset or liability was first recognised.

D22 The Code sets out how a change will need to be implemented in the financial statements:

Page 157

MODULE 3 \ THE FINANCIAL STATEMENTS

� adjusting the opening balance of each affected component of net worth for the earliest period presented, and

� adjusting the other comparative amounts disclosed for each prior period presented

to the extent that it is practicable to determine period-specific and cumulative effects (see paragraph D24).

D23 When an authority applies a change in accounting policy retrospectively or makes a retrospective restatement, or when it reclassifies items, paragraph 3.4.2.17 of the Code (in accordance with paragraphs 40A–40D of IAS 1) requires that it presents an additional Balance Sheet at the beginning of the preceding period (ie a third Balance Sheet) where those adjustments have a material effect on the information in the third Balance Sheet. When an authority is required to present an additional Balance Sheet, it must disclose the information required by paragraphs 3.4.2.30 and 3.4.2.31 of the Code and paragraphs 41–44 of IAS 1 and IAS 8 (see row 14 ‘Reclassification of items’ in the table at paragraph A8 above for further explanation). However, the authority is not required to present the related notes to the third Balance Sheet.

D24 The Code recognises that it is sometimes difficult to achieve comparability of prior periods with the current period. For example, data might not have been collected in the prior periods in a way that allows retrospective application of a new accounting policy. Paragraph 3.3.2.3 of the Code sets out the circumstances where, exceptionally, retrospection can be assessed as impracticable:

Applying a requirement is impracticable when the entity cannot apply it after making every reasonable effort to do so. For a particular prior period, it is impracticable to apply a change in an accounting policy retrospectively or to make a retrospective restatement to correct an error if:

a) the effects of the retrospective application or retrospective restatement are not determinable

b) the retrospective application or retrospective restatement requires assumptions about what management’s intent would have been in that period, or

c) the retrospective application or retrospective restatement requires significant estimates of amounts and it is impossible to distinguish objectively information about those estimates that:

i) provides evidence of circumstances that existed on the date(s) at which those amounts are to be recognised, measured or disclosed, and

ii) would have been available when the financial statements for that prior period were authorised for issue

from other information.

D25 Restating comparative information for prior periods often requires complex and detailed estimation. This, in itself, does not prevent reliable adjustments. When making estimates for prior periods, the basis of estimation should reflect the circumstances that existed at the time. It is self-evident that it becomes increasingly difficult to define those circumstances with the passage of time.

Page 158

CODE OF PRACTICE ON LOCAL AUTHORITY ACCOUNTING IN THE UNITED KINGDOM GUIDANCE NOTES FOR PRACTITIONERS 2014/15 ACCOUNTS

D26 Additionally, the passage of time means that such estimates and circumstances might be influenced by knowledge of events and circumstances that have arisen since the prior period. Retrospective application is not possible in circumstances where it is not possible to determine, from the totality of information currently available, the information that provides evidence of the circumstances on the date the transaction or event occurred and that would have been available when the accounts for that year were authorised for issue.

D27 Paragraph 53 of IAS 8 does not permit the use of hindsight when applying a new accounting policy, either in making assumptions about what management’s intentions would have been in a prior period or in estimating amounts to be recognised, measured or disclosed in a prior period. The prohibition on the use of hindsight is discussed in more detail in paragraph D45.

D28 Paragraphs 23 to 27 of IAS 8 set out the treatment for the two types of impracticability exceptions on retrospective application:

� Period-specific amounts – when it is impracticable to determine the period-specific effect of a change in accounting policy on comparative information for one or more prior periods presented, an authority is instead required to apply the new accounting policy to the carrying amounts of the assets and liabilities as at the beginning of the earliest period for which retrospective application is practicable (which might be the current period). The authority will then need to make a corresponding adjustment to the opening balance of each affected component of net worth for the period.

� Cumulative effect – when it is impracticable to determine the cumulative effects at the beginning of the current period of applying a new accounting policy to all prior periods, an authority is required to adjust the comparative information to apply the new accounting policy from the earliest date practicable.

Changes in Accounting Estimates D29 When preparing their financial statements, authorities will first of all decide their accounting

policies:

� in which period assets, liabilities, gains and losses are to be recognised

� what basis should be used to measure amounts recognised

� where in the various financial statements the amounts should be disclosed and how they should be presented and supported by notes.

Where the basis of measurement for the amount to be recognised is uncertain, then the authority will use an estimation technique.

D30 The use of reasonable estimation is an essential part of the preparation of the financial statements. It does not undermine their reliability. Many items in the financial statements cannot be measured precisely but can only be estimated because of the inherent uncertainties that apply to the provision of local government services, activities and trading organisations. Estimates involve judgements based on the latest available, reliable information. They are applied for example, in determining, the useful lives of property, plant and equipment, provisions, fair values of financial assets and liabilities and actuarial assumptions relating to defined benefit pension schemes.

Page 159

MODULE 3 \ THE FINANCIAL STATEMENTS

D31 The commonly cited illustration of the difference between accounting policies, measurement bases and estimates relates to depreciation:

� the accounting policy in local government is that property, plant and equipment are depreciated by the systematic allocation of their depreciable amounts over their useful lives

� a measurement basis will then be chosen on which to base the systematic allocation – eg historical cost or fair value

� depreciation will then be calculated using estimates of useful life and residual value using a particular methodology (eg straight line).

D32 Accounting estimates need to be distinguished from accounting policies because the effect of a change in an estimate is reflected in the current Comprehensive Income and Expenditure Statement (and sometimes in those of future periods). In contrast, a change in accounting policy will generally require adjustments of previously reported amounts.

D33 An estimate may need to be changed if there is a change in the circumstances on which the estimate was based or the authority has new information or more experience relating to the estimation process.

D34 Paragraph 3.3.2.2 of the Code defines a change in accounting estimate as:

... an adjustment of the carrying amount of an asset or a liability, or the amount of the periodic consumption of an asset, that results from the assessment of the present status of, and expected future benefits and obligations associated with, assets and liabilities. Changes in accounting estimates result from new information or new developments and, accordingly, are not correction of errors.

D35 Paragraph 3.3.2.15 of the Code clarifies that a change in the measurement basis applied to a transaction or balance is not a change in an accounting estimate, but is a change in accounting policy. For example, if the Code specified a move from a measurement basis of historical cost to fair value for a class of assets, this would require a change in accounting policy. However, a change in the method of depreciation would be a change in accounting estimate (confirmed by paragraph 61 of IAS 16). IAS 8 (paragraph 35) notes that where it is difficult to distinguish between a change in accounting policy and a change in accounting estimate, then such a change should be treated as a change in accounting estimate.

D36 Paragraph 3.3.2.16 of the Code requires that (except to the extent discussed in the following paragraph) the effect of a change in accounting estimates should be recognised prospectively (ie from the date of change) in surplus or deficit in:

� the period of the change, if the change affects the period only, or

� the period of the change and future periods, if the change affects both.

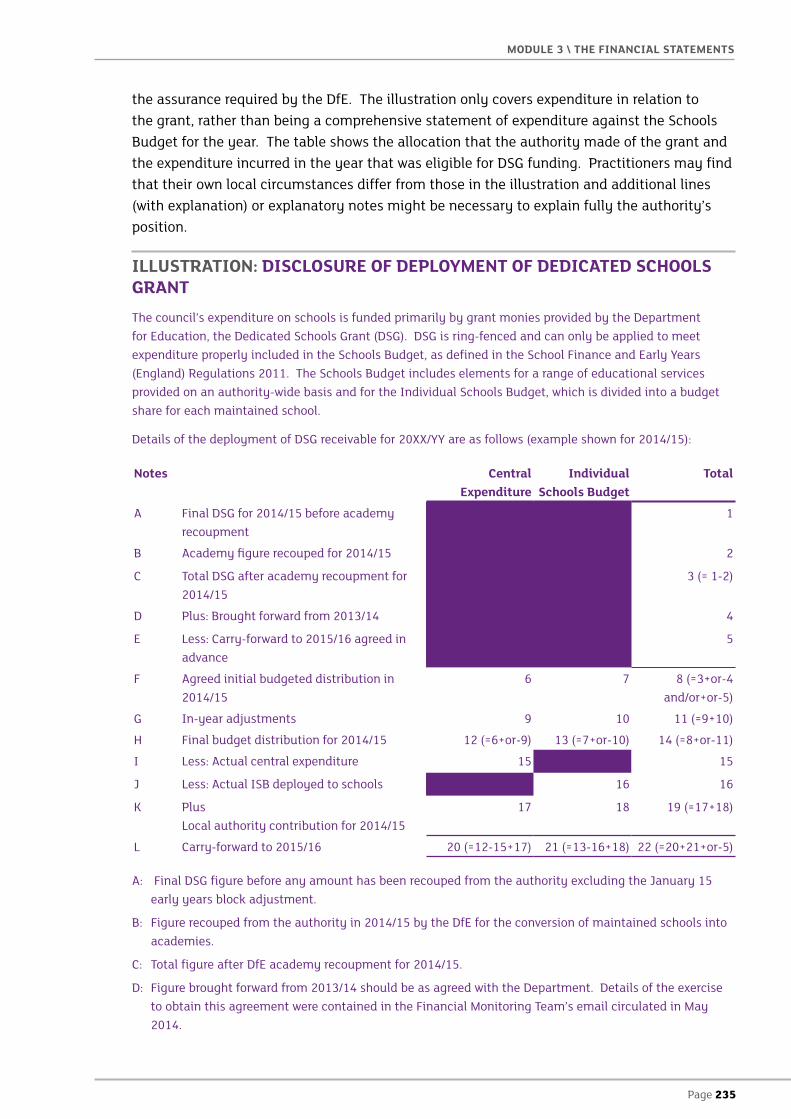

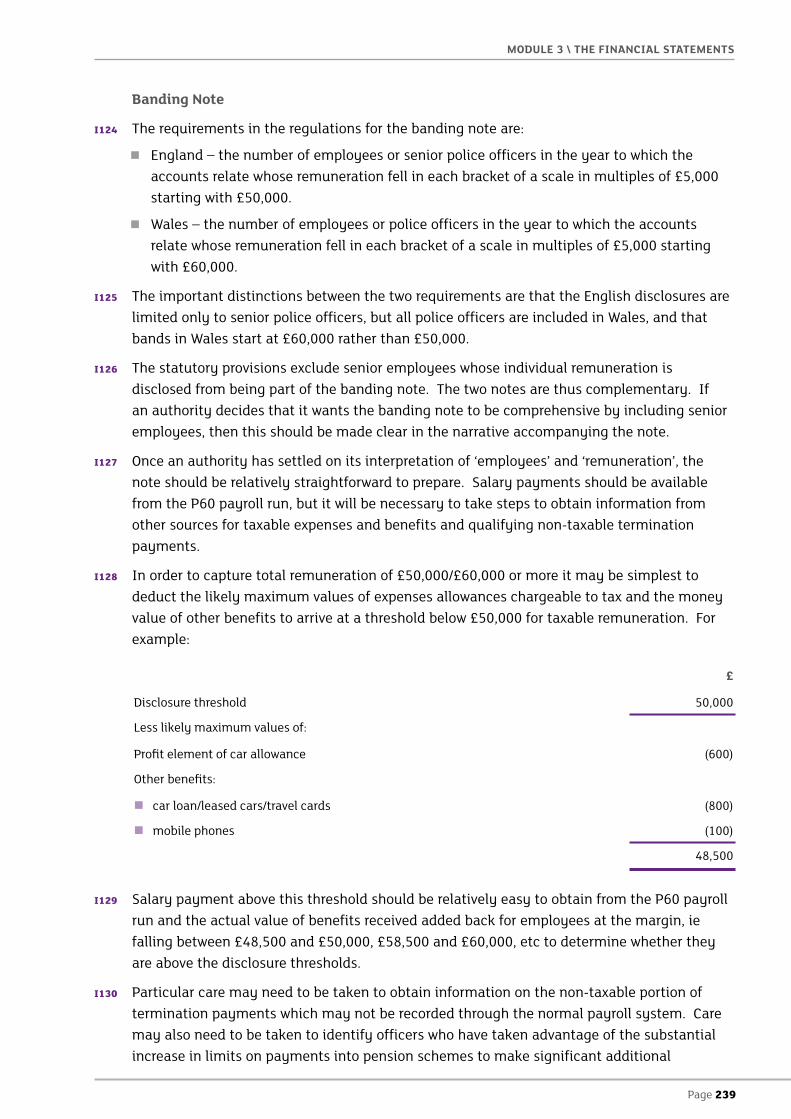

D37 In some circumstances, changes in estimate may impact on assets and liabilities or a component item of net worth. In such circumstances the change is recognised in the carrying amount of the assets and liabilities or item of net worth in the period of change.