modern portfolio management

TRANSCRIPT

MODERN PORTFOLIO MANAGEMENTVEDAPRADHA.R

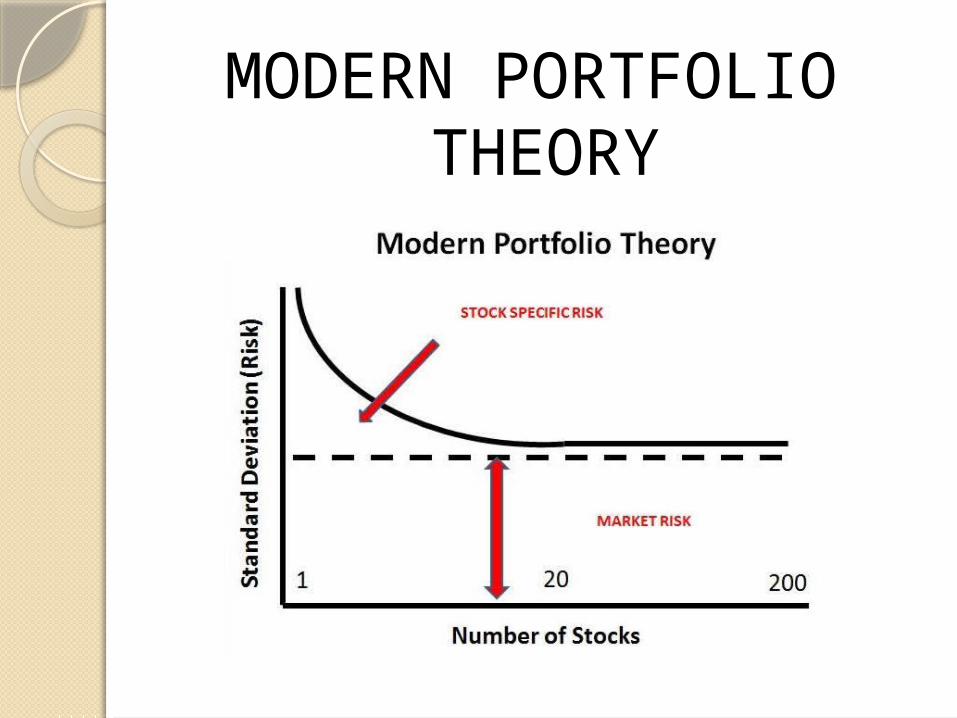

MODERN PORTFOLIO THEORY

MEANING OF INVESTMENT

Modern theory is on the concept of spreading the risk by portfolio diversification

MARKET PORTFOLIOMarket portfolio represents

such a portfolio, in which all the securities traded in the market find exactly the same proportion in which these represent themselves in the overall market capitalisation.

CAPITAL ASSET PRICING MODEL (CAPM)

Capital asset pricing model was developed by William Sharpe to address two important aspects related to risk and return. An investor will be able to select optimal portfolio with the help of analysing the relationship between risk and return.

Relationship between risk and return for an optimal portfolio

Relationship between risk and return for an individual security

USES OF CAPM

Predict the relationship between the risk of an asset and its expected return.

The fair return calculated as per CAPM serves as a standard for comparing it with expected return

It also helps investor to predict the return that can be expected from an asset which is not yet been traded in the market.

CAPM Assumptions: Individuals are risk averse. Individual seek to maximise the expected utility of their

portfolios over a single period investment horizon. Individuals have homogeneous expectations – They have

identical subjective estimates of mean, variances & co-variance among returns.

The market is perfect.No taxes.No transaction or floatation costs.The quantity of risky securities in the market is given. Individuals can borrow and lend freely at a riskless rate of

interest.Securities are completely divisible.The market is competitive.

ELEMENTS OFCAPM:

1 •Security market line (SML)

2 •Capital market line (CPL)

ALPHA & BETA COEFFICIENT

The intercept of the characteristic regression line is alpha, i.e. the distance between the intersection and the horizontal axis. It indicates that the stock return is independent of the market return.

Beta describes the relationship between the stock return and index return.

ARBITRAGE PRICING THEORY

Arbitrage pricing theory was developed by Stephen Ross on the notion that security returns are not based on single factor (index) of the market, instead each security is linked with multiple factors and returns get influenced by these factors.

Macro economic factors which affect security returns are growth rate of industrial production, rate of inflation, spread between long term and short term interest rates.

Securities return differ due o market imperfections, the investors would make arbitrage profits by selling security with low return and buying security with high return.

ASSUMPTIONS

1. Capital markets are perfectly competitive.

2. Investors always prefer more wealth to less wealth with certainty.

3. The stochastic process generating asset returns can be expresses as a linear function of a set of K factors or indices.