mobile in 2013: our take on the top trends & insights

TRANSCRIPT

James Hilton – CEO | [email protected]

The worlds largest specialist mobile marketing agency

Access to M&C Saatchi’s full strategic resources

Over 80 full-time mobile experts

Multi-award winning

Welcome to M&C Saatchi Mobile

Local knowledge & a unique global reach

Strategy Mobile advertising production

Our core mobile offering

agenda Introduction – overview of the market TRENDS 1. Smartphone penetration is slowing in established markets – while emerging markets are on the rise 2. The platform shift 3. Mobile ad spend to skyrocket in 2013 4. The year of the tablet 5. Mobile retail to explode 6. The evolution of the ad network, DSP’s & RTB 7. 4g to accelerate the rich media ad space 8. The rise of social and facebook on mobile 9. Apps vs. mobile web 10. The market is constantly changing

The future of digital

The medium is now 20 years old.

So, how does the market look?

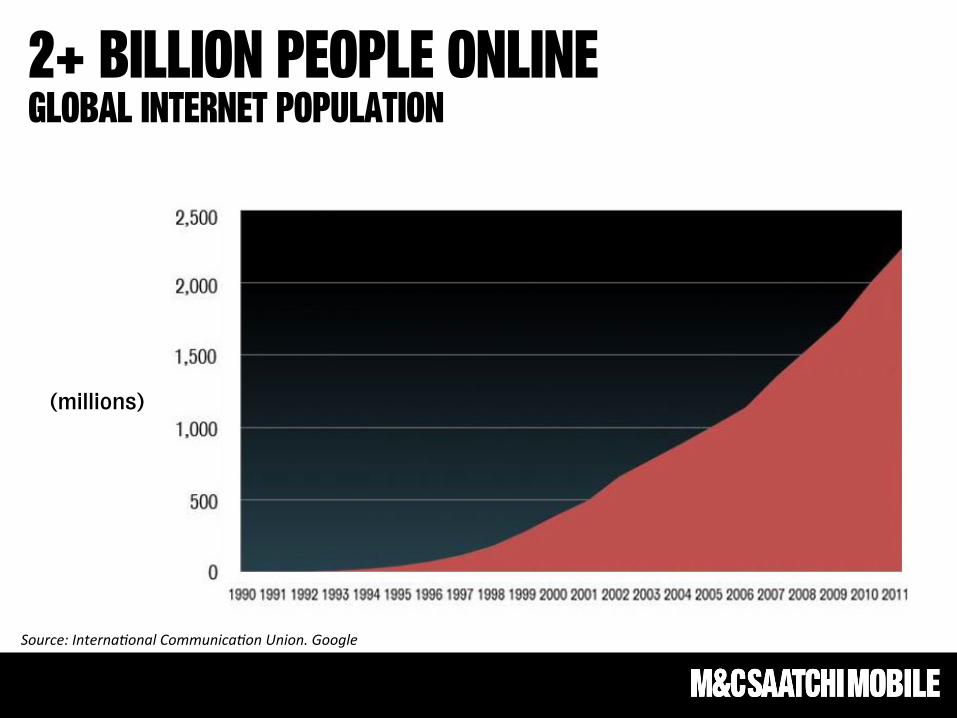

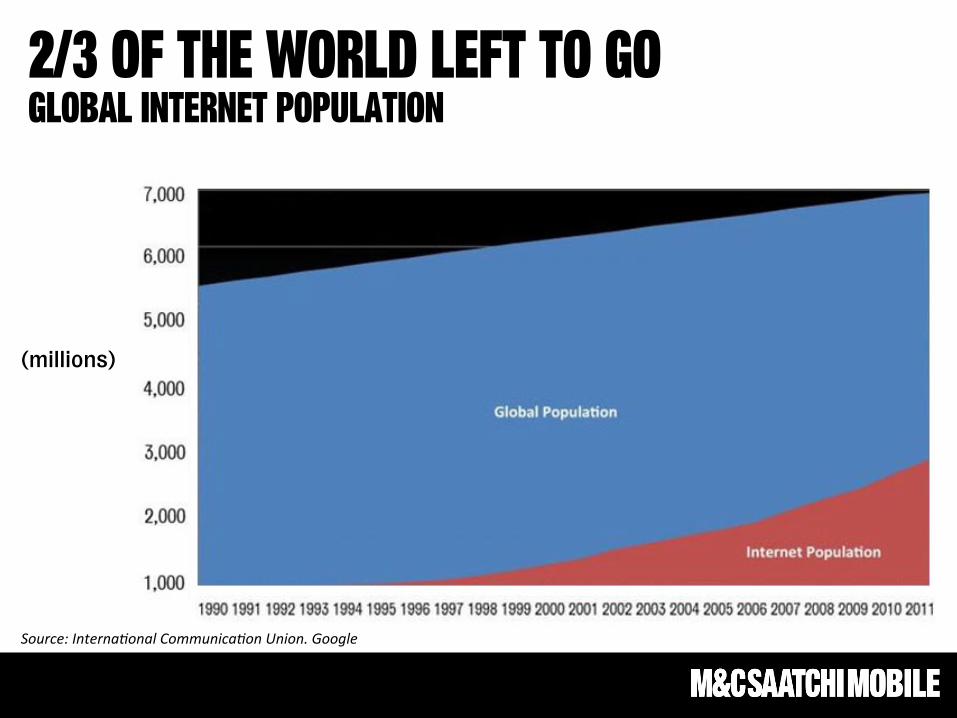

Source: Interna-onal Communica-on Union. Google

2+ billion people online Global internet population

(millions)

Source: Interna-onal Communica-on Union. Google

2/3 of the world left to go Global internet population

(millions)

HOWEVER…

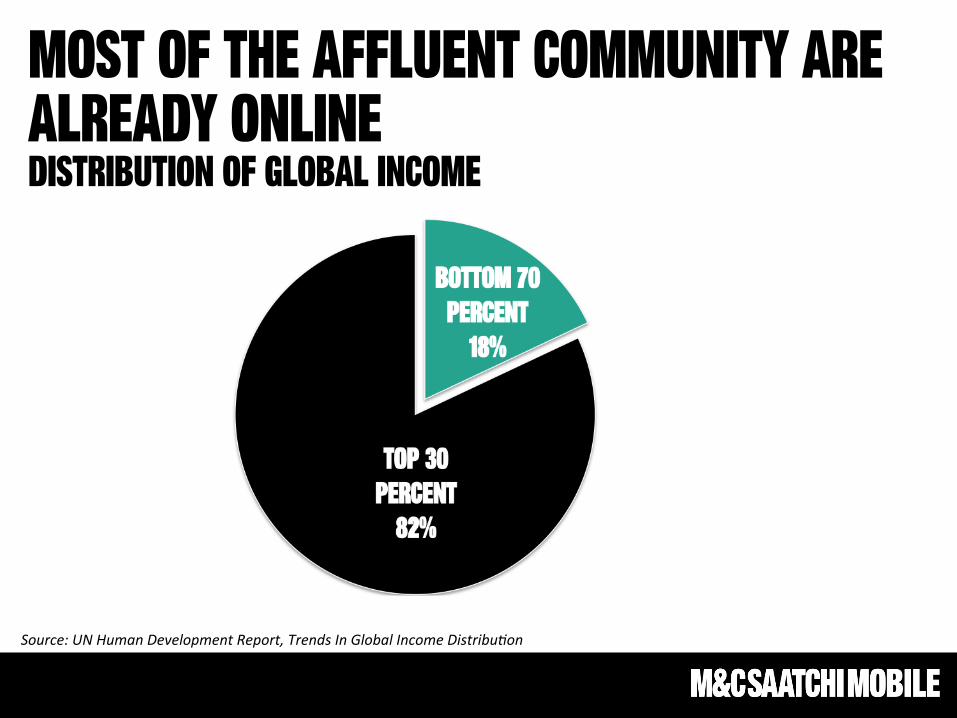

Most of the affluent community are already online Distribution of global income

Source: UN Human Development Report, Trends In Global Income Distribu-on

So the market’s more mature than you think. Meanwhile, something profound happened last year…

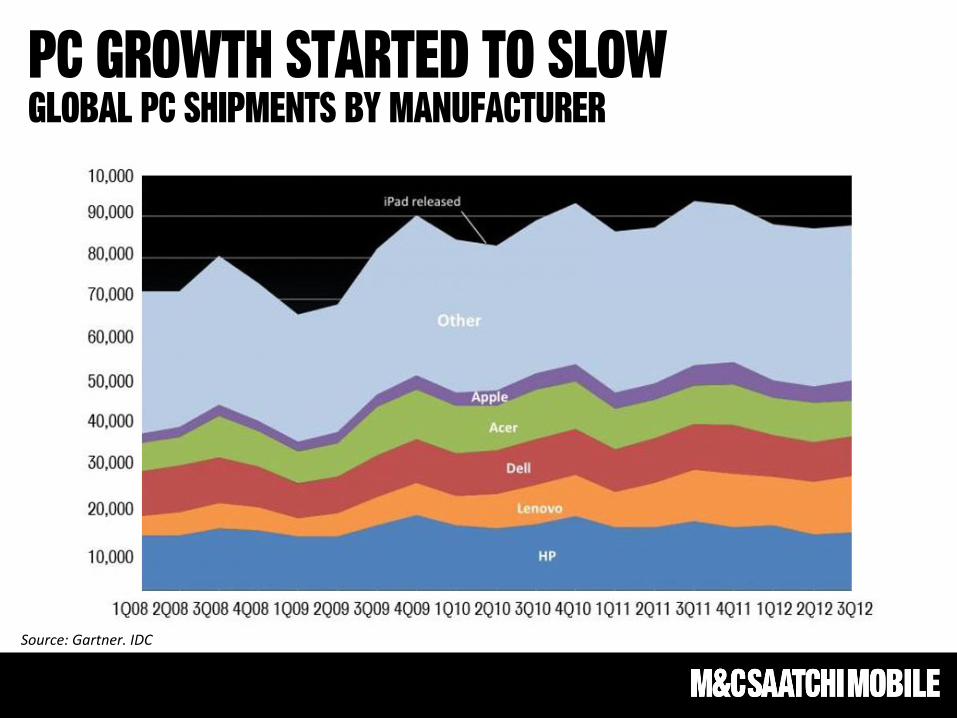

PC growth started to slow Global PC shipments by manufacturer

Source: Gartner. IDC

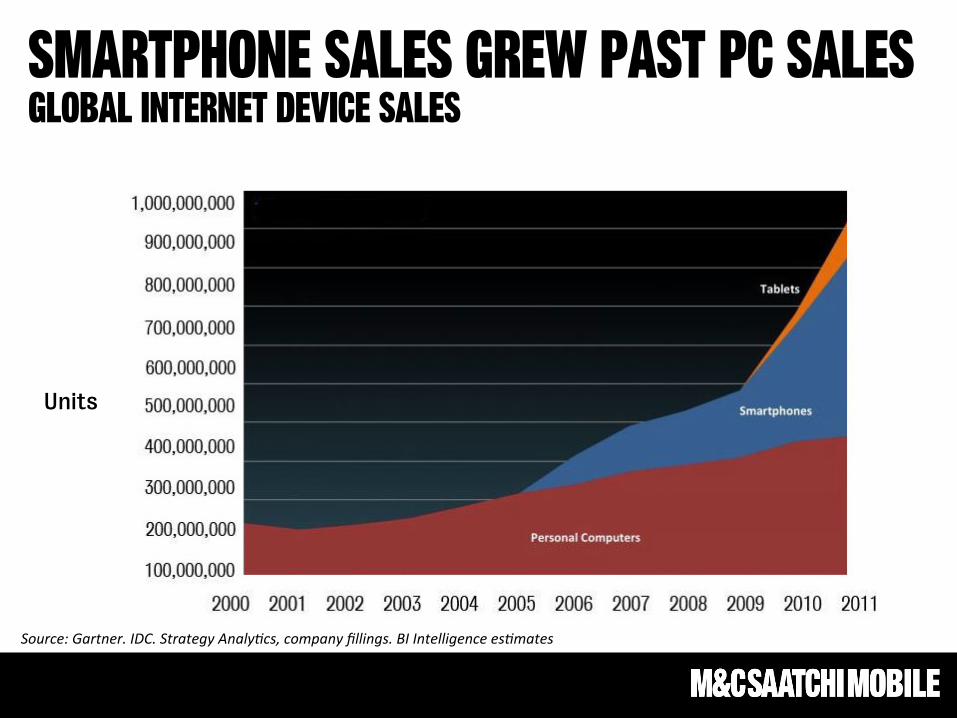

Smartphone sales grew past pc sales Global internet device sales

Units

Source: Gartner. IDC. Strategy Analy-cs, company fillings. BI Intelligence es-mates

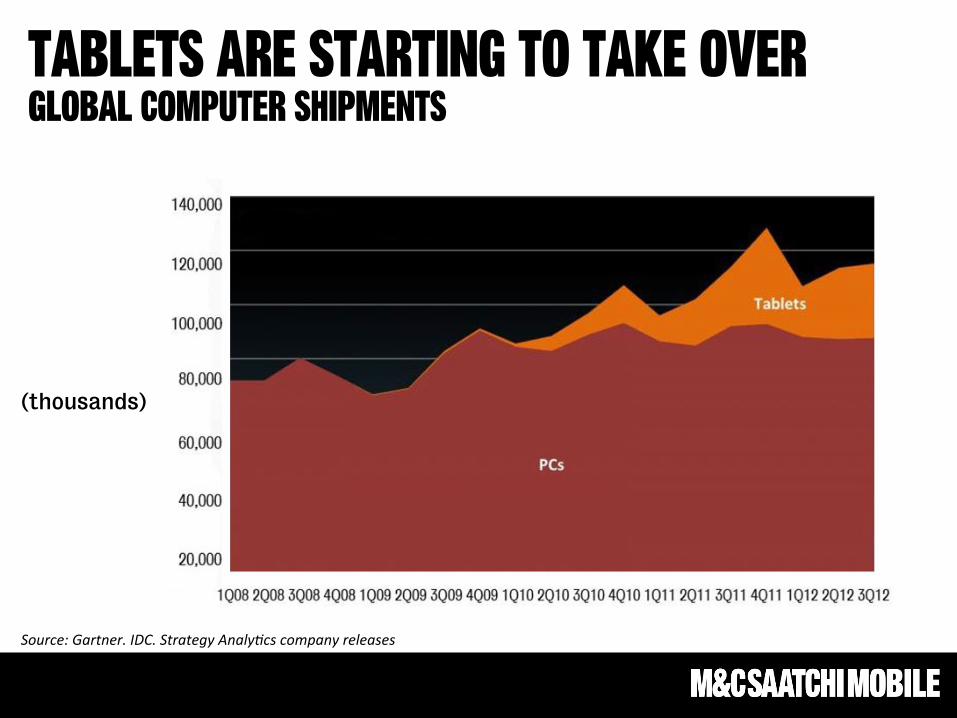

Tablets are starting to take over Global computer shipments

(thousands)

Source: Gartner. IDC. Strategy Analy-cs company releases

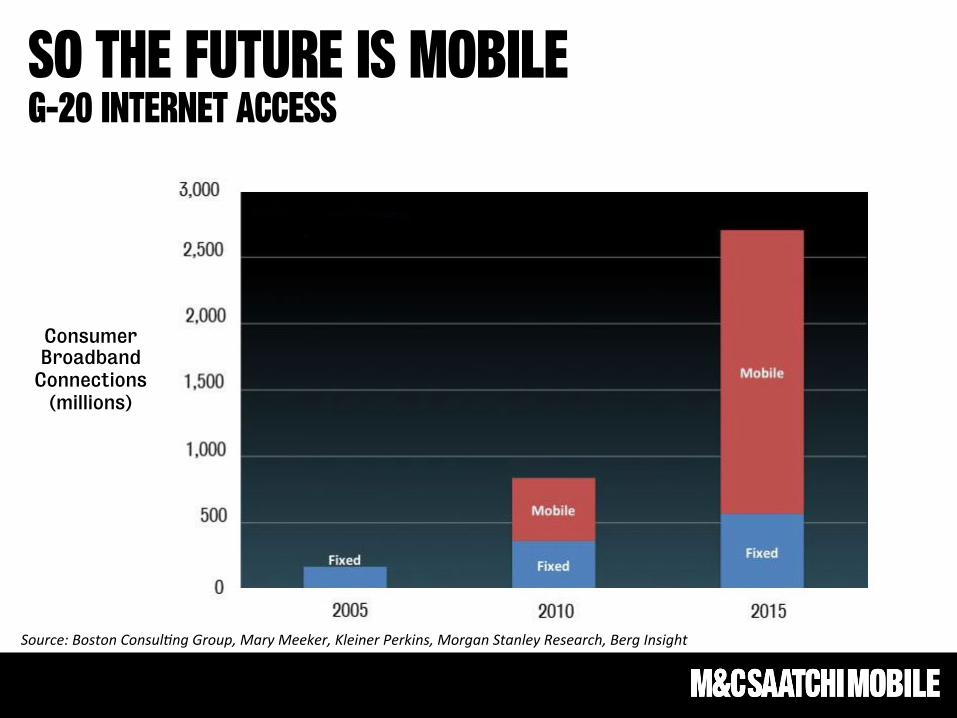

So the future is mobile G-20 internet access

Consumer Broadband

Connections (millions)

Source: Boston Consul-ng Group, Mary Meeker, Kleiner Perkins, Morgan Stanley Research, Berg Insight

Where are we in the mobile revolution? & what are the essentials you need to know?

Trend 1. Smartphone penetration is slowing in established markets while emerging markets are on the rise

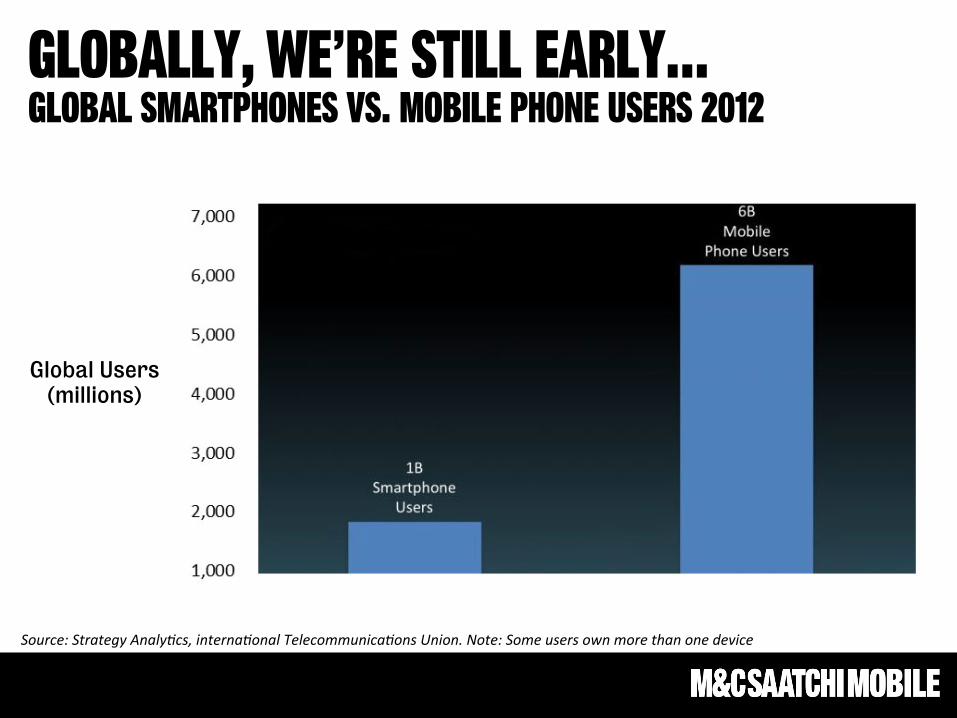

Globally, we’re still early… Global smartphones vs. mobile phone users 2012

Global Users (millions)

Source: Strategy Analy-cs, interna-onal Telecommunica-ons Union. Note: Some users own more than one device

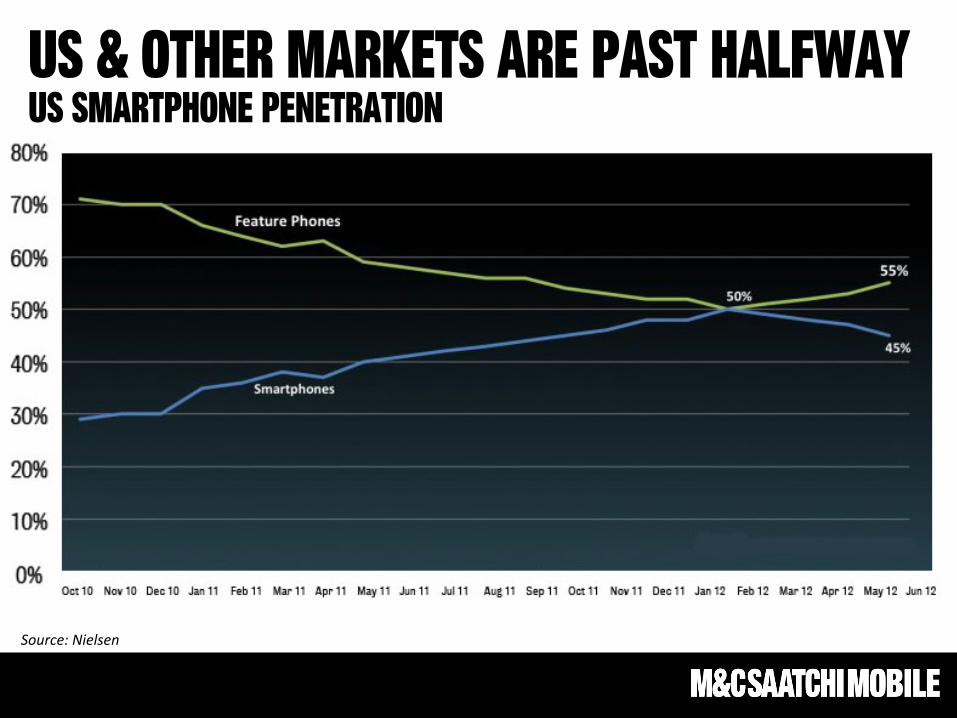

But growth tends to slow after 50% penetration

US & other markets are past halfway US smartphone penetration

Source: Nielsen

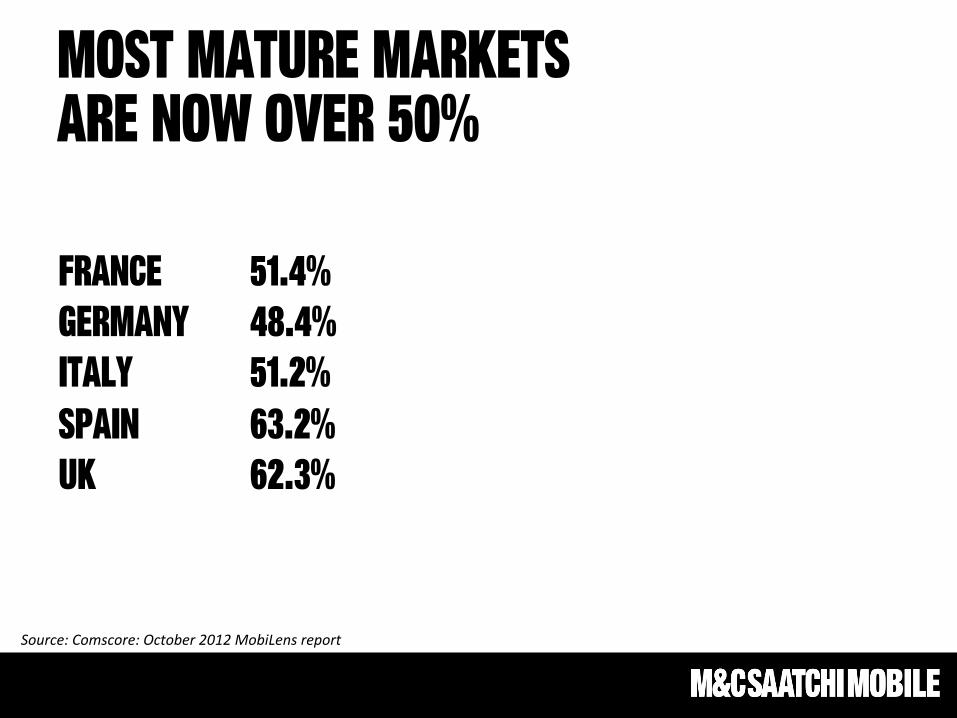

Most mature markets are now over 50%

France 51.4% Germany 48.4% Italy 51.2% Spain 63.2% UK 62.3%

Source: Comscore: October 2012 MobiLens report

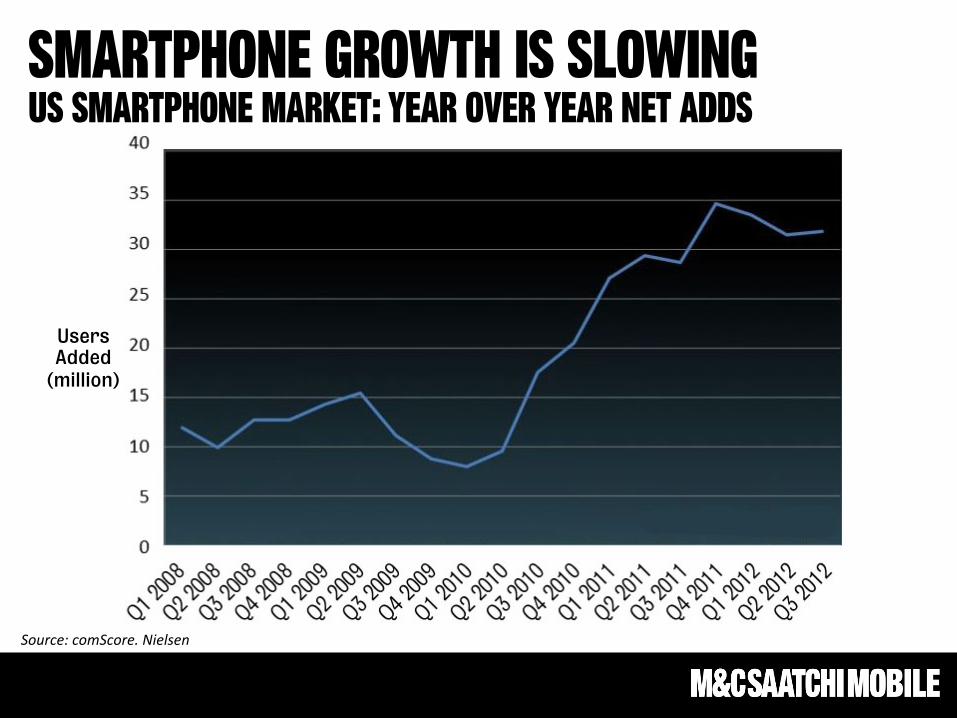

smartphone growth is slowing US smartphone Market: year over year net adds

Users Added

(million)

Source: comScore. Nielsen

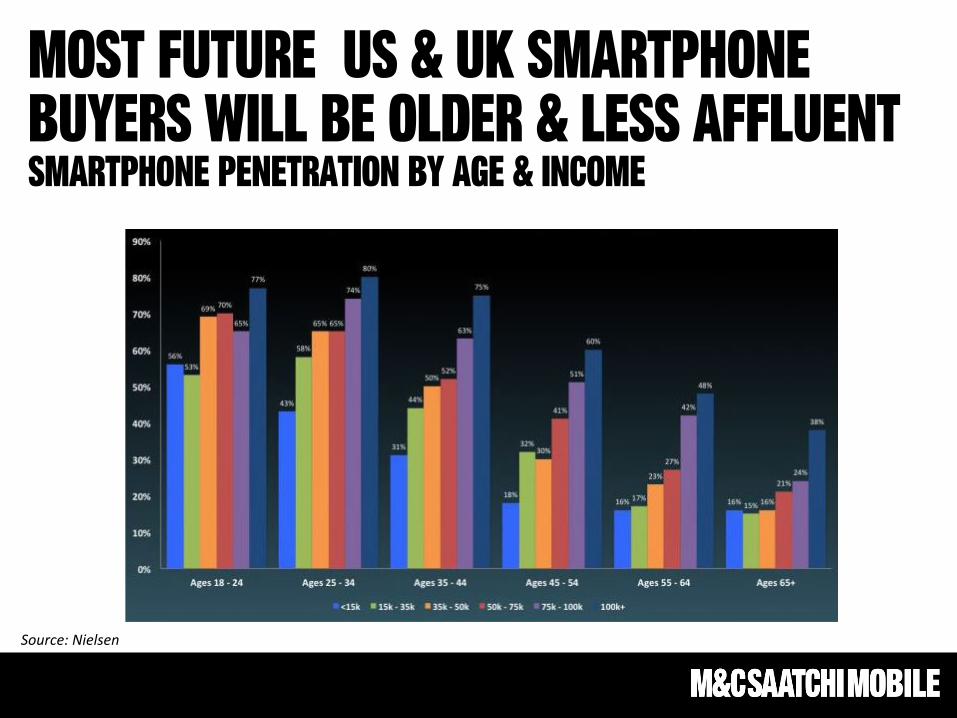

Most future US & UK smartphone buyers will be older & less affluent Smartphone penetration by age & income

Source: Nielsen

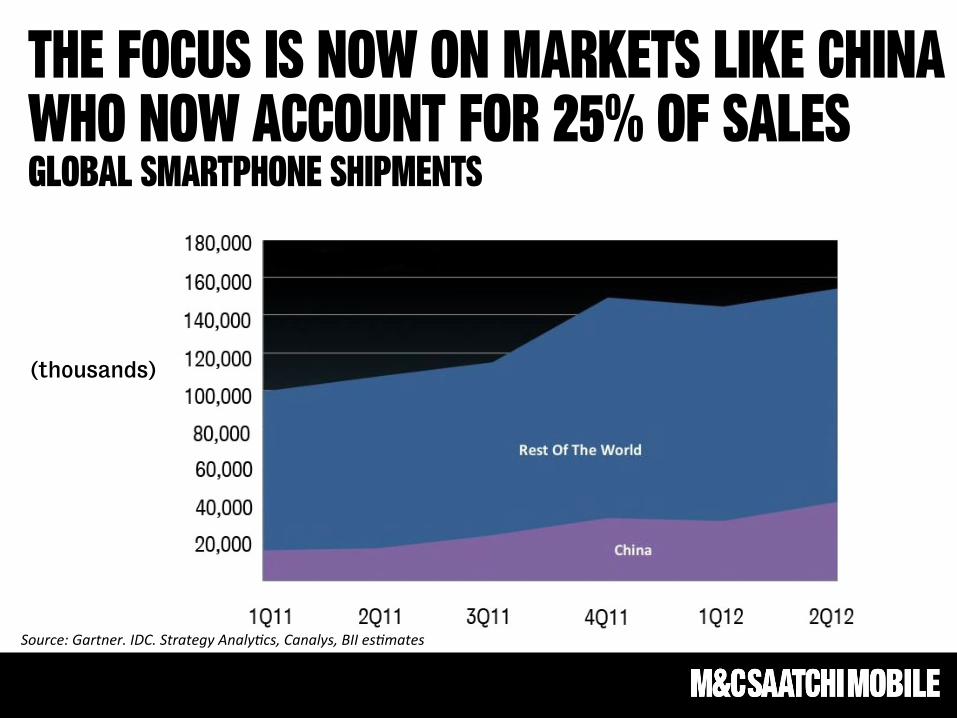

the focus is now on markets like china who now account for 25% of sales Global smartphone shipments

(thousands)

Source: Gartner. IDC. Strategy Analy-cs, Canalys, BII es-mates

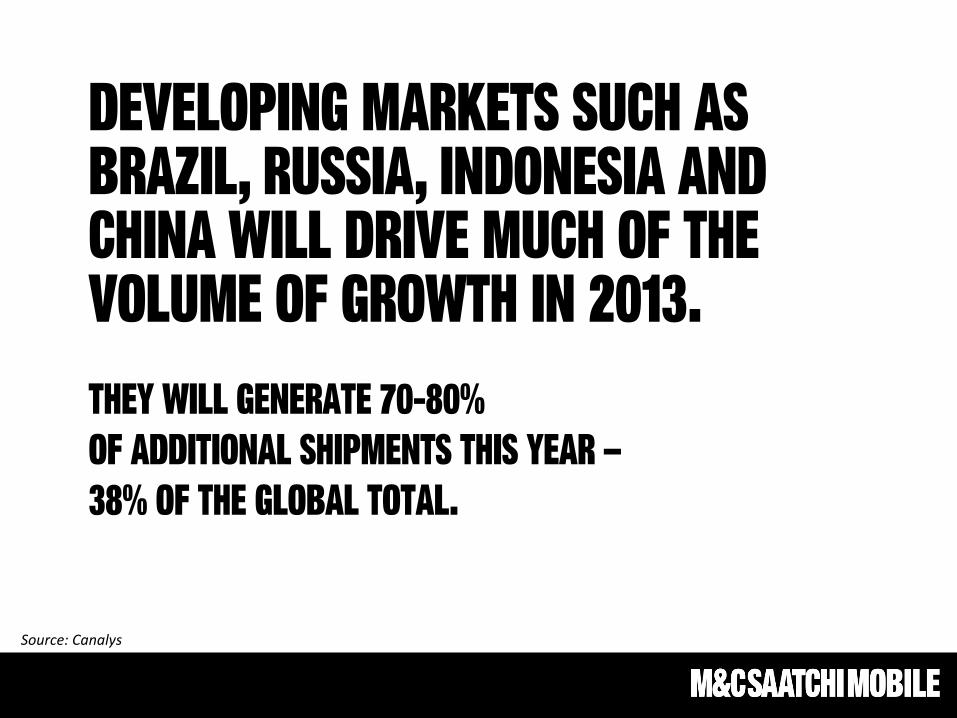

developing markets such as brazil, Russia, Indonesia and China will drive much of the volume of growth in 2013. They will generate 70-80% of additional shipments this year – 38% of the global total.

Source: Canalys

Trend 2. The platform shift

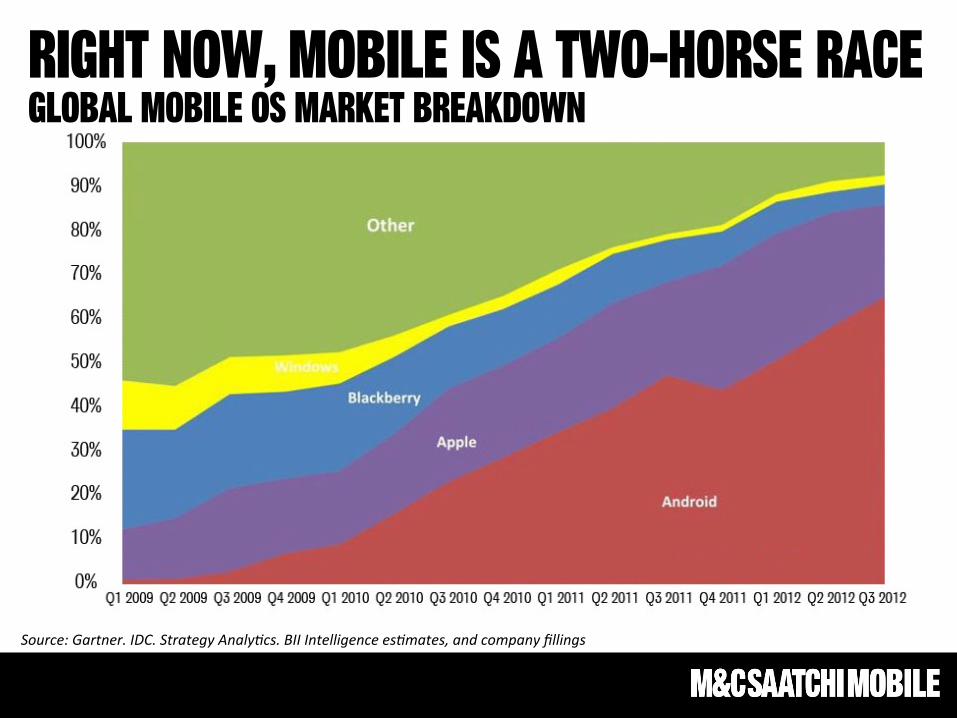

Right now, mobile is a two-horse race Global mobile OS market breakdown

Source: Gartner. IDC. Strategy Analy-cs. BII Intelligence es-mates, and company fillings

Share of Global Unit

Sales

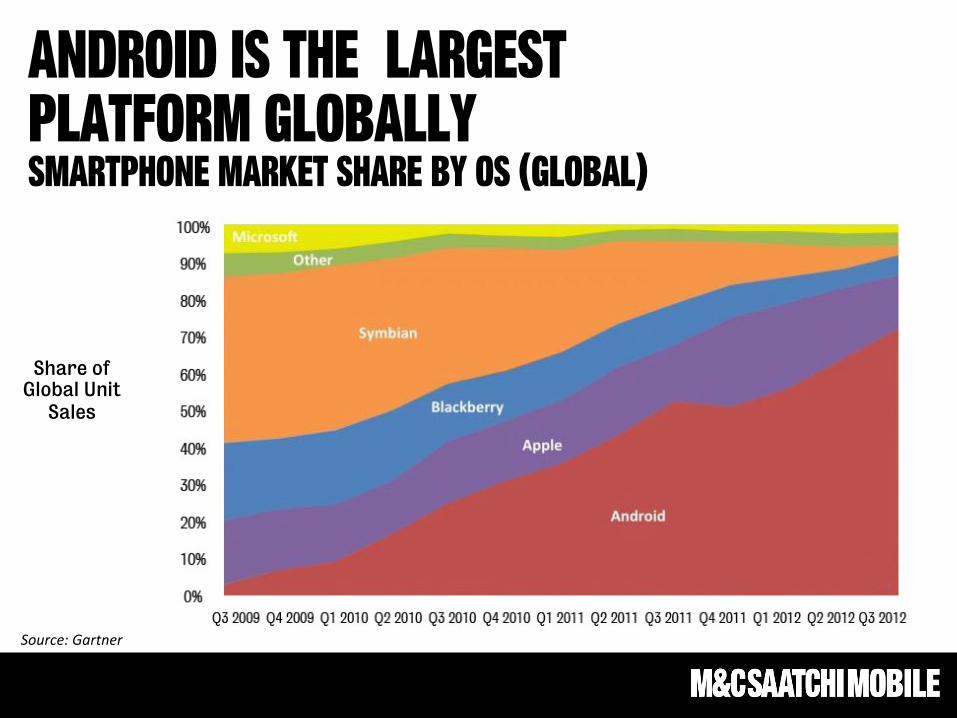

Android is the largest platform globally Smartphone Market Share by OS (global)

Source: Gartner

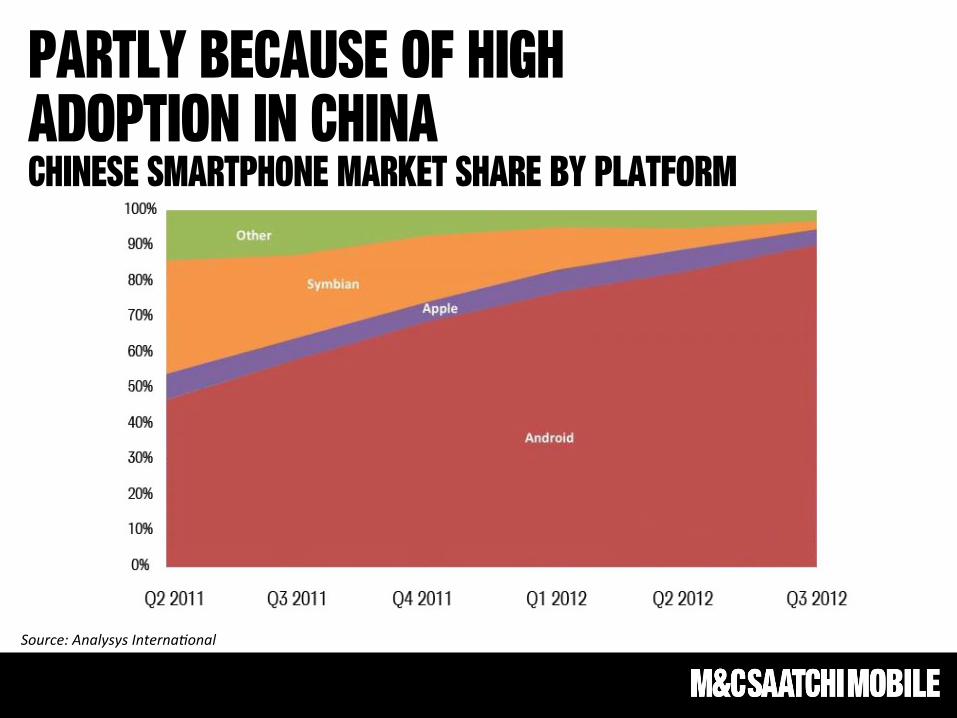

Partly because of high adoption in china Chinese smartphone market share by platform

Source: Analysys Interna-onal

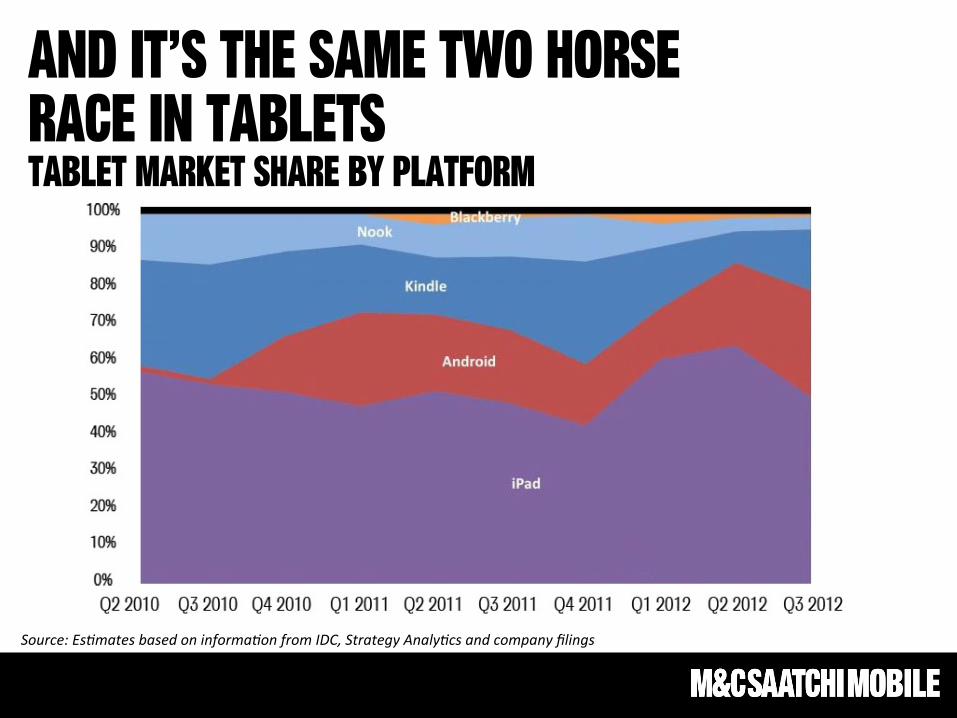

And it’s the same two horse Race in tablets Tablet market share by platform

Source: Es-mates based on informa-on from IDC, Strategy Analy-cs and company filings

(millions)

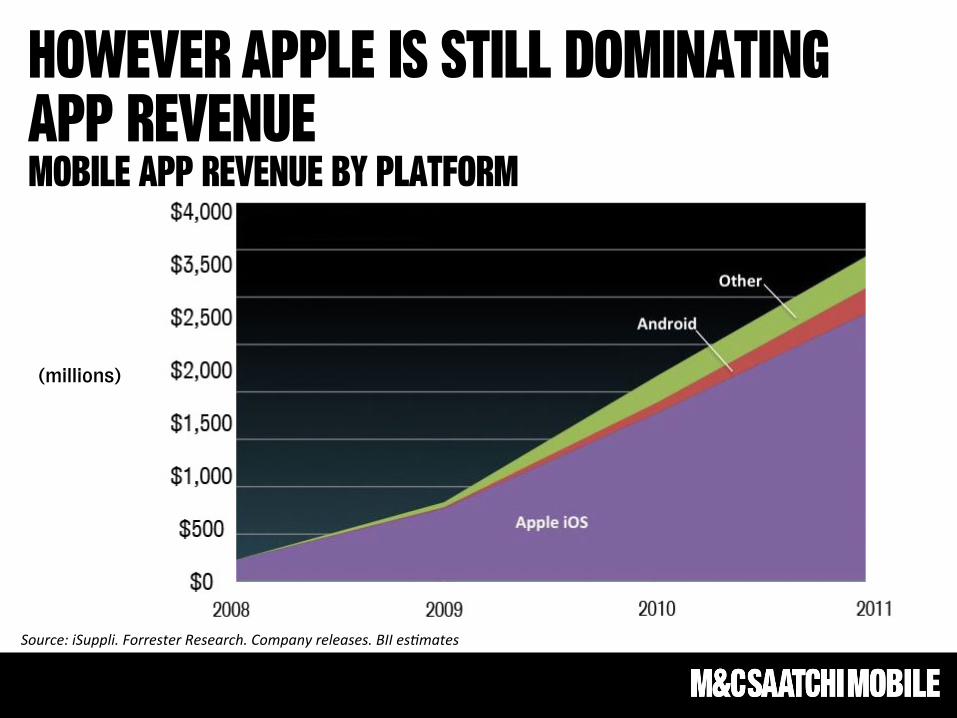

However Apple is still dominating app revenue Mobile app revenue by platform

Source: iSuppli. Forrester Research. Company releases. BII es-mates

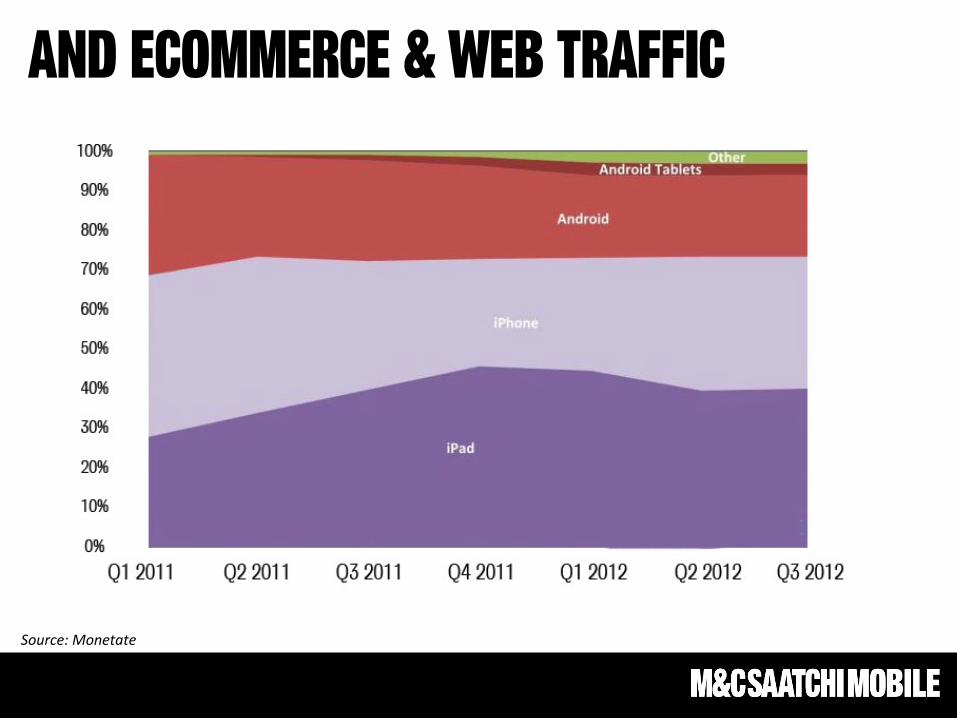

And ecommerce & web traffic

Source: Monetate

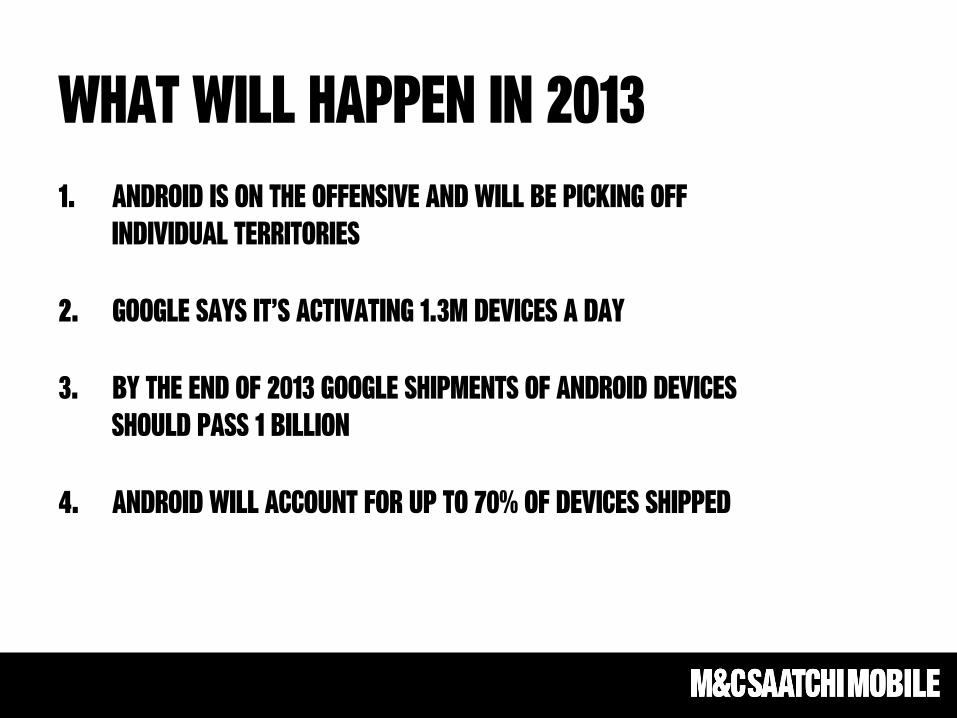

What will happen in 2013 1. Android is on the offensive and will be picking off

individual territories 2. Google says it’s activating 1.3M devices a day

3. By the end of 2013 Google shipments of android devices should pass 1 Billion

4. android will account for up to 70% of devices shipped

Trend 3. Mobile ad spend to Skyrocket in 2013

The global mobile advertising market was worth $6.43B in 2012

it’s forecasted to hit $23B by 2016

Source: Berg Insight

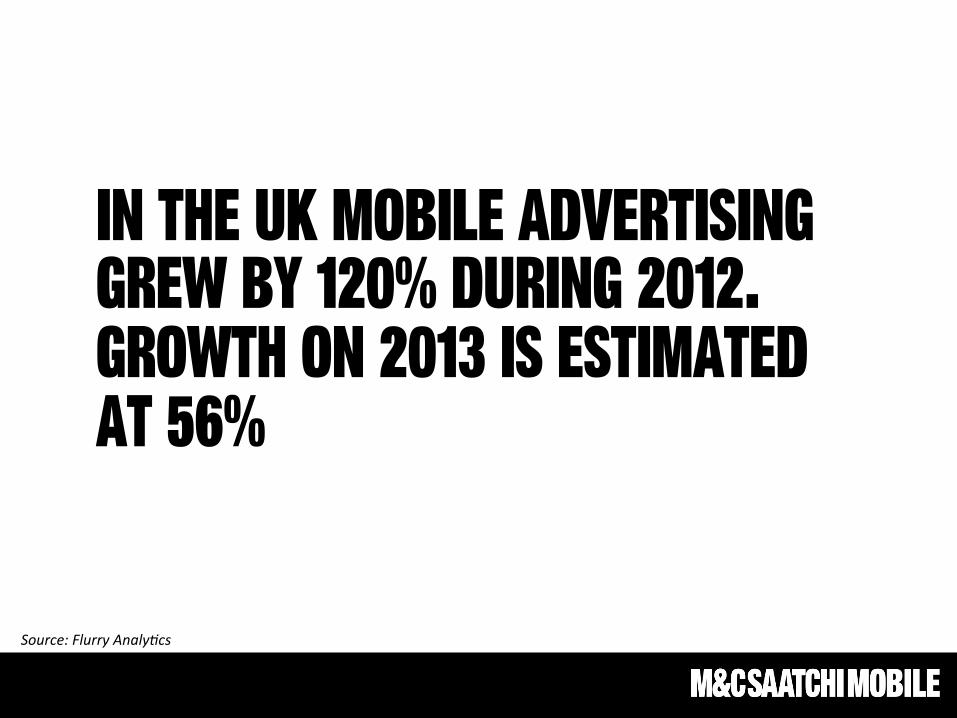

In the UK mobile advertising grew by 120% during 2012. growth on 2013 is estimated at 56%

Source: Flurry Analy-cs

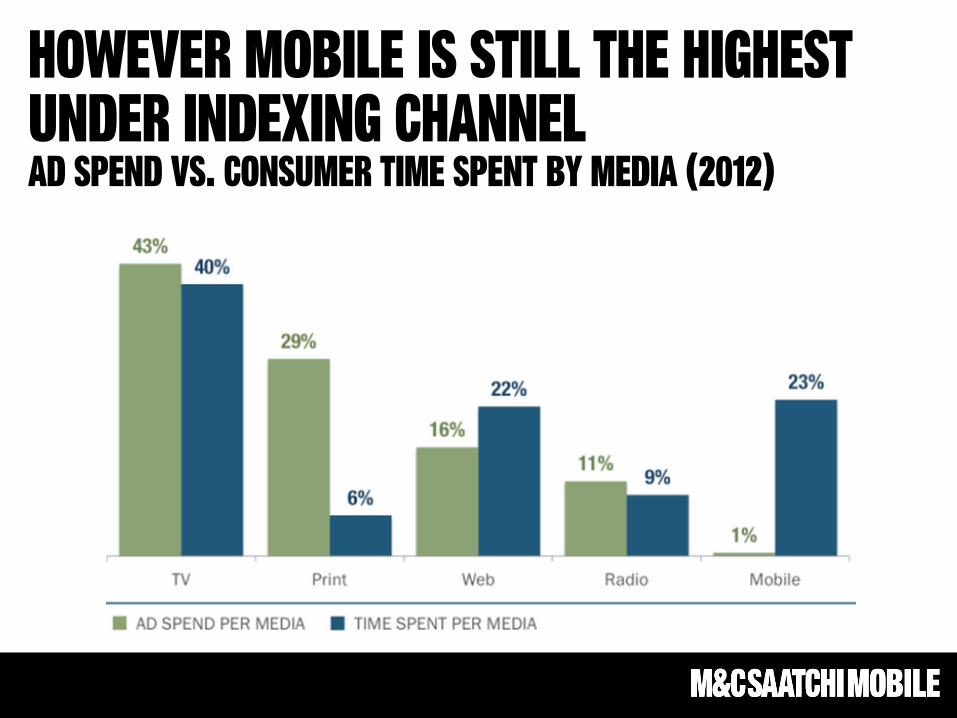

However Mobile Is still the highest under indexing channel Ad spend vs. consumer time spent by media (2012)

What has been holding mobile back & why is it not going to anymore?

The belief that the audience is too fragmented to be reached effectively WE can now directly target consumers more accurately than ever before: age location past location connection handset device content consumed language

The belief that Data And tracking is elusive Sophisticated tracking is now up to 99% accurate

We can track beyond the download – deposits, purchase, usage etc.

DSP’s and RTB changing the landscape

The small screen Constraining Creative sizes

360 imagery

Location services, maps And gps

video

Trend 4. The year of the tablet

ios has dominated the mid to high end tier of the landscape

Android is now gaining market share with multiple tablets

Windows is not yet out of the running

The 7 inch is reaching a new tablet market and becoming a more genuinely mobile device than than it’s larger cousin

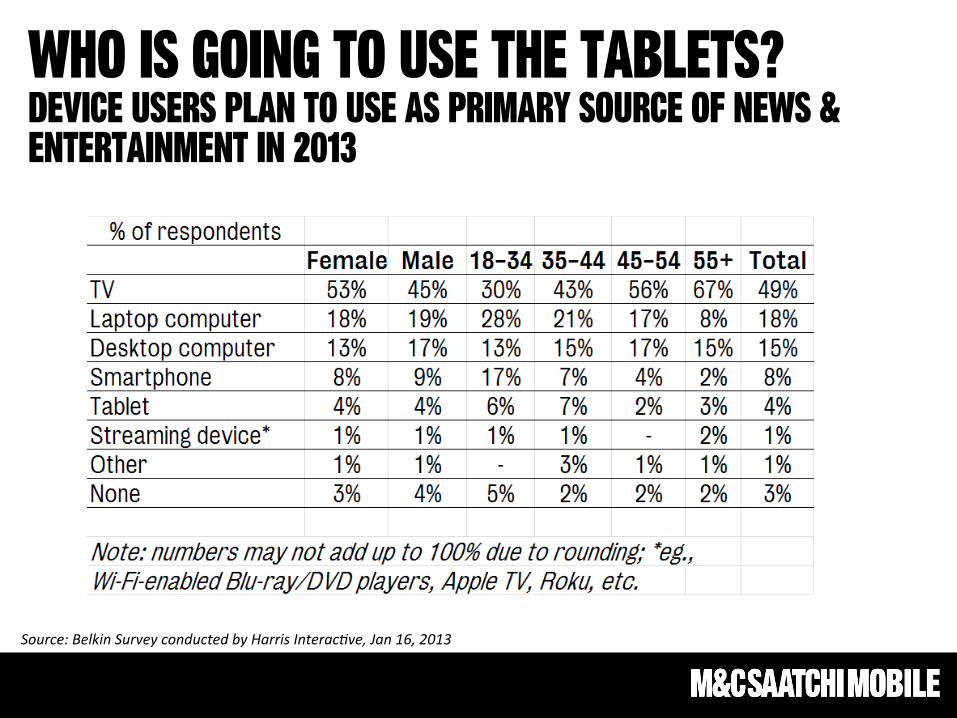

Who is going to use the tablets? Device users plan to use as primary source of news & entertainment in 2013

Source: Belkin Survey conducted by Harris Interac-ve, Jan 16, 2013

Our predictions android will continue to take market share from APPLE Windows to stay a marginal player There will be more smartphone / tablet hybrid releases This year will be the year of the 7 inch

Trend 5. Mobile retail to explode

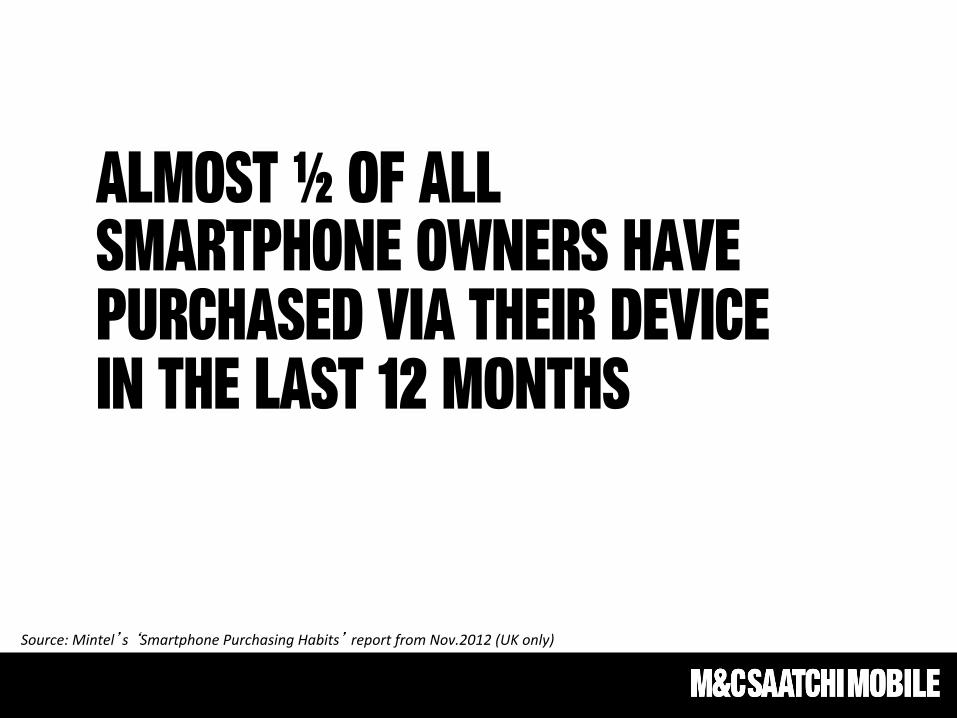

Almost ½ of all smartphone owners have purchased via their device In the last 12 months

Source: Mintel’s ‘Smartphone Purchasing Habits’ report from Nov.2012 (UK only)

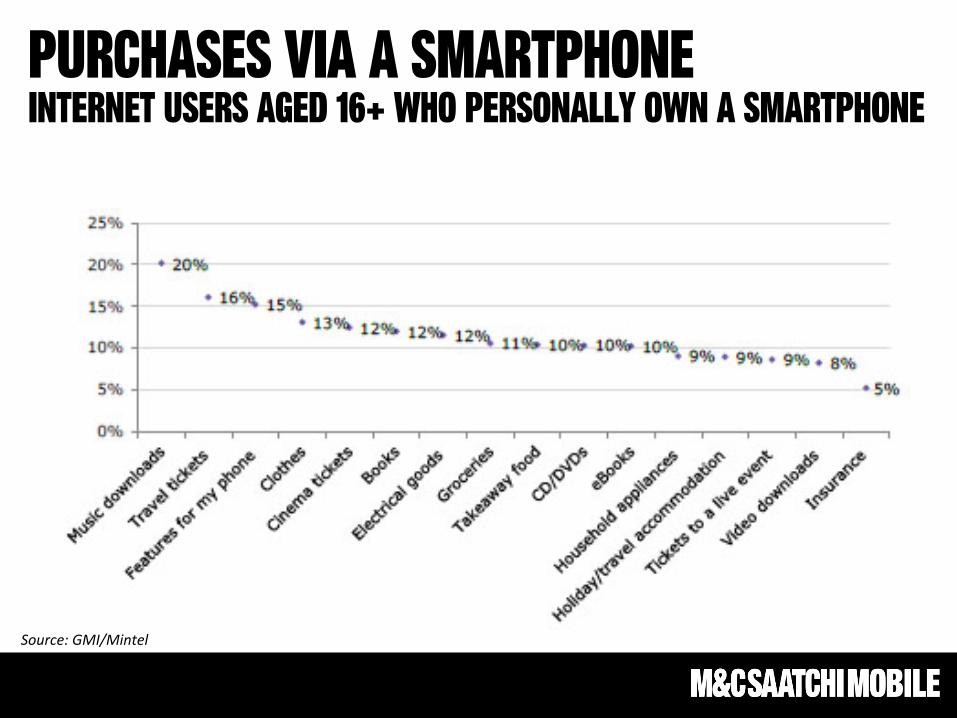

Purchases via a smartphone internet users aged 16+ who personally own a smartphone

Source: GMI/Mintel

47% of consumers use their smartphone to search for local information such as a store they want to visit

Source: Local and the e-‐tailing group, 2012

46% look up a store’s mobile site & 42% check inventory prior to visiting a store

Source: Local and the e-‐tailing group, 2012

Tablet shoppers have a higher propensity to purchase on the device

What you need to consider? Tablet customers are worth more to brands Know your brands mobile touch points – then research, prioritize & start testing Ensure you are mobile optimized Develop a multichannel acquisition strategy on mobile Include mobile search and local in your mobile strategy

Trend 6. The evolution of the ad network, The rise of demand side platforms, & the arrival of Real time bidding

The way brands and agencies buy mobile inventory is changing

We’re taking control of the buying process

ad networks are changing Traditional networks (inMobi, Millenial, Adfonic) are changing their service offering to become more sophisticated …Or being bought by larger telcos (AdMob / google, Quattro / Apple) which ads more precision to their data

How? Bidding directly on inventory via ‘exchanges’ Developing new tools that let buyers target consumers more accurately Developing their own ‘bidder’ or using white labeled DSP’s

Now, a new orthodoxy Is emerging based on

demand side platforms

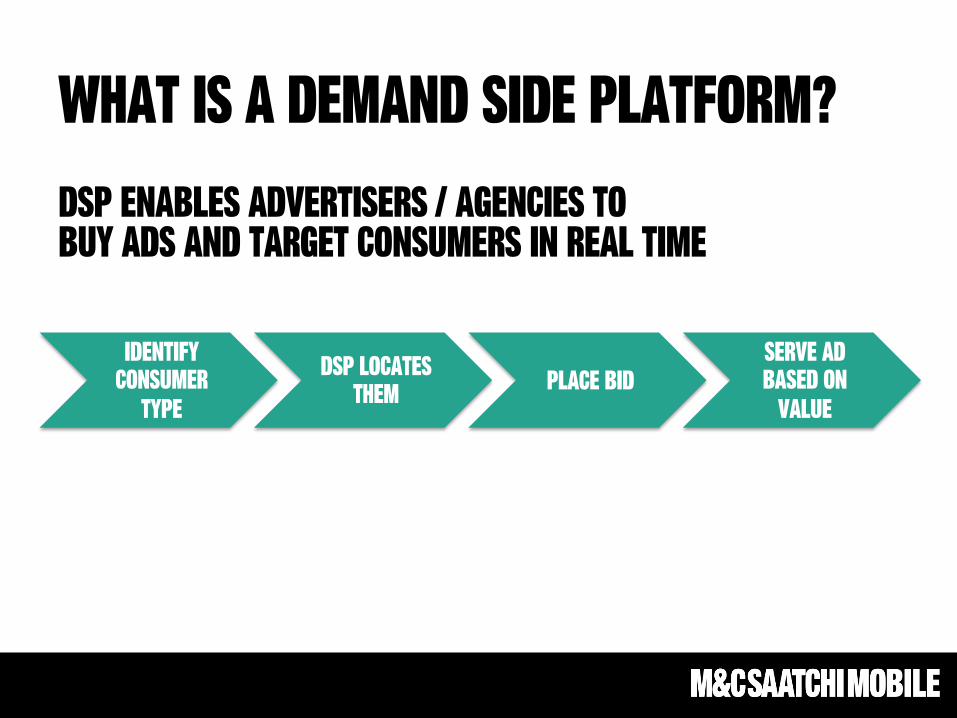

What is a demand side platform? DSP Enables advertisers / agencies to buy ads and target consumers in real time

Identify consumer

type DSP locates

them Place bid Serve ad based on

value

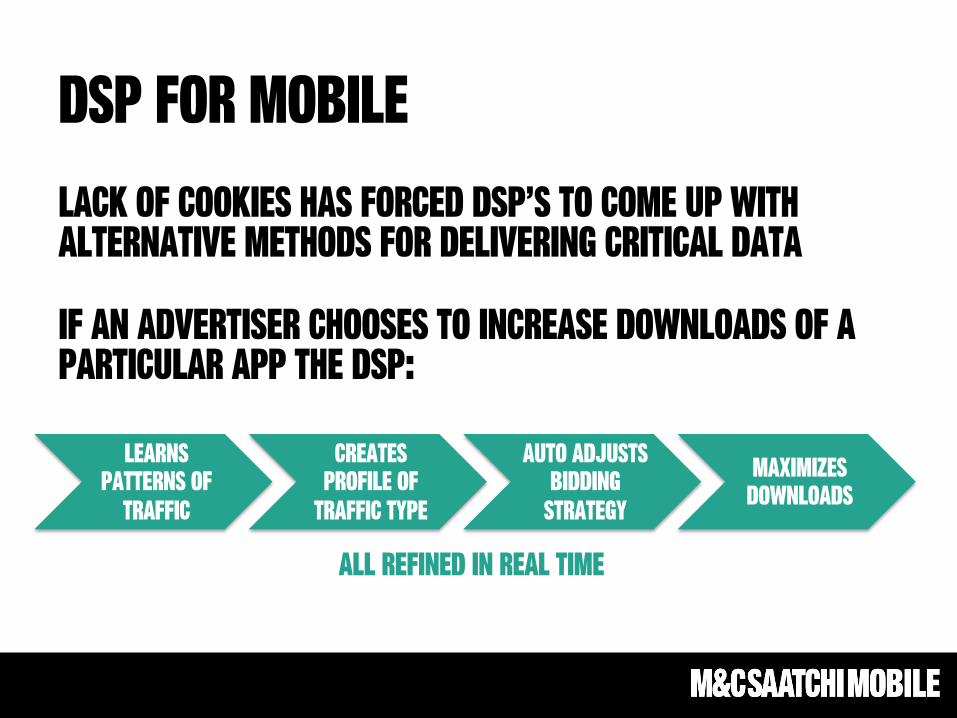

DSP for mobile Lack of cookies has forced DSP’s to come up with alternative methods for delivering critical data If an advertiser chooses to increase downloads of a particular app the DSP:

All refined in real time

Learns patterns of

traffic

Creates profile of

traffic type

Auto adjusts bidding

strategy Maximizes

downloads

The old system of bidding on blind inventory will become outmoded & inefficient

What will real time bidding bring to mobile? A system in which data on the bids, available inventory & the behaviour of consumers is crunched in real time Instantaneous bids for each impression based on data & smart algorithms that change constantly in response to audience changes Transparency

How will this effect marketers? The mobile DSP will transform the efficiency & effectiveness of buying mobile inventory. RTB can improve ad effectiveness by 20-150%* More & more agencies will have their own DSP Only knowledgeable specialists can handle these transactions successfully

*Source: ICD

Trend 7. 4g will accelerate the rich media space, but not that fast

It has been nearly a decade since the first 3g networks were launched

Now we’re seeing that excitement again with LTE or 4g

Everything everywhere launched 4G in the UK in 2012 – tests showed it to be 5 times faster than 3G

By may 2013 vodafone, o2 and 3UK will be able to launch their own 4g services

Who will be using it? The Early adopters due to high Pricing The vast majority will be unwilling to break long contracts to get 4g

How will 4g effect advertising on mobile?

More rich media campaigns Currently most are run across wifi 4G will accelerate consumption – speed and more portable than wifi hotspots WE will see more: • Pre roll video advertising • Ads combining video, audio & interactive elements • Gamification ads • Ads utilizing APS’s

Trend 8. The rise of facebook & social on mobile

Until recently facebook’s problem with mobile has been well documented.

Their audience was migrating to the small screen but ad revenue wasn’t.

In 2012 facebook started the change – declaring itself a mobile first company launched promoted posts that appear in users news feeds and was soon making $500,000 a day Mobile accounted for 23% of Facebook’s $1.33B of advertising revenue in Q4 2012 - $305M mobile ads sold Their mobile app-install ads are now being used by 20% of the 100 top grossing ios apps to attract new users

In 2013 Facebook is rolling out it’s own mobile ad network Giving networks the ability to serve ads placed with FB on 3rd party sites & aps

What you need to know for 2013 Social networks will invest in deeper insight to enhance targeting on mobile Advancements will be predominantly Facebook & Twitter, but sites such as google & pinterest will be monitored for new opportunities Positive results have been seen though advertising on facebook’s app – set to improve with investment in targeting & consumer insight

Trend 9. Apps vs. mobile web

In 2012 many expected the resurgence of mobile web. But is hasn’t panned out that way.

Android app revenues has doubled Q3-Q4

Facebook and others realized HTML5 was not the solution The pendulum is swinging back to apps staying for 2012

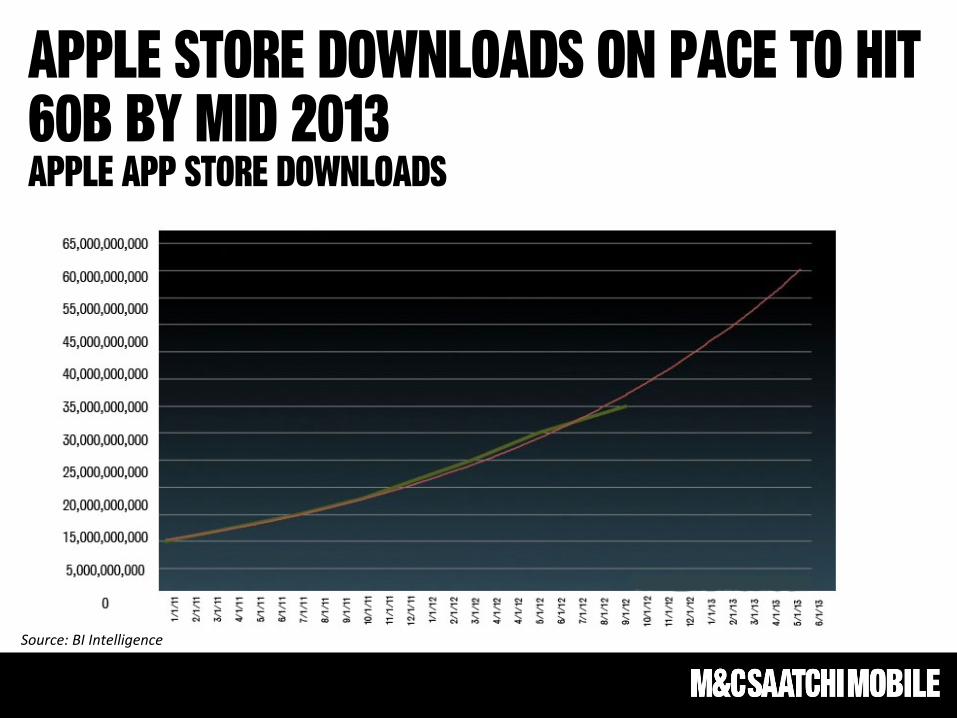

Apple store downloads on pace to hit 60B by mid 2013 Apple app store downloads

Source: BI Intelligence

Minutes Spent Per Month (billions)

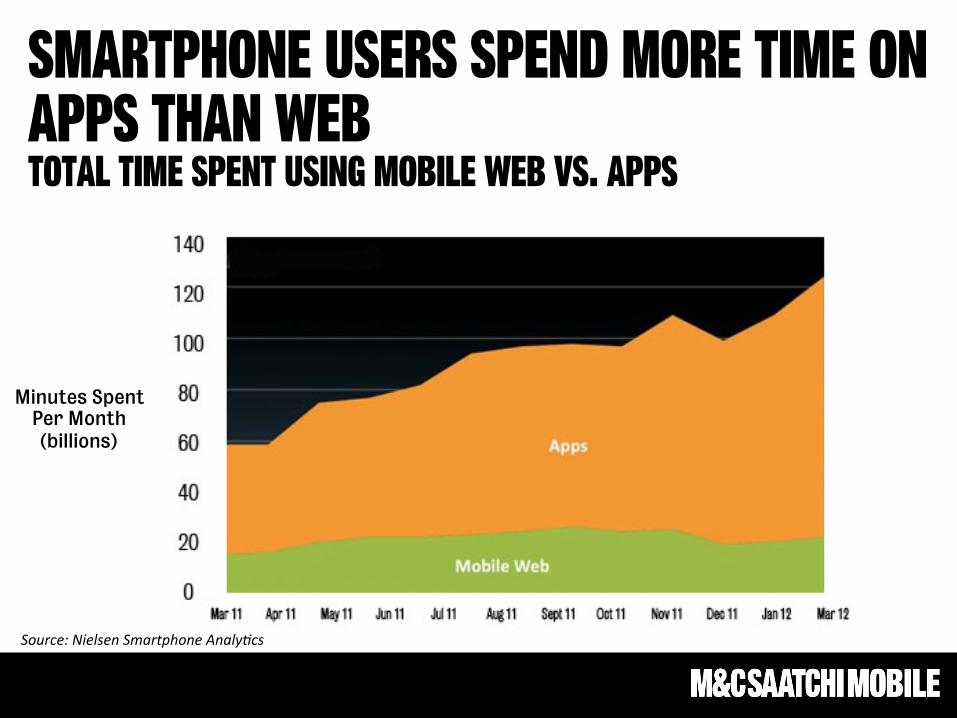

Smartphone users spend more time on apps than web Total time spent using mobile web vs. apps

Source: Nielsen Smartphone Analy-cs

(millions)

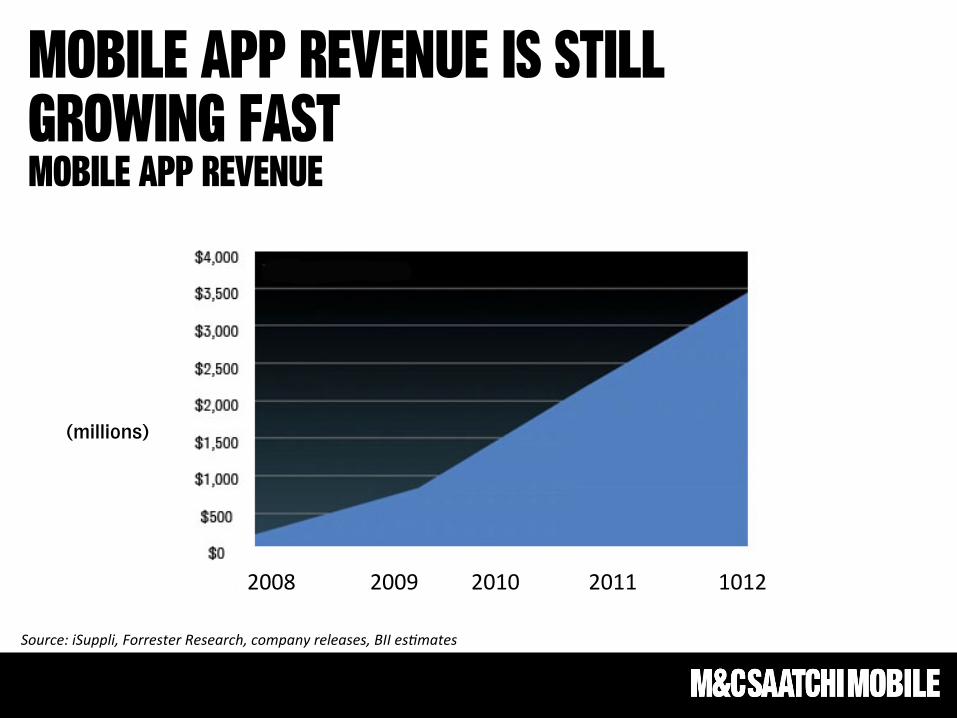

Mobile app revenue is still growing fast Mobile app revenue

2008 2009 2010 2011 1012

Source: iSuppli, Forrester Research, company releases, BII es-mates

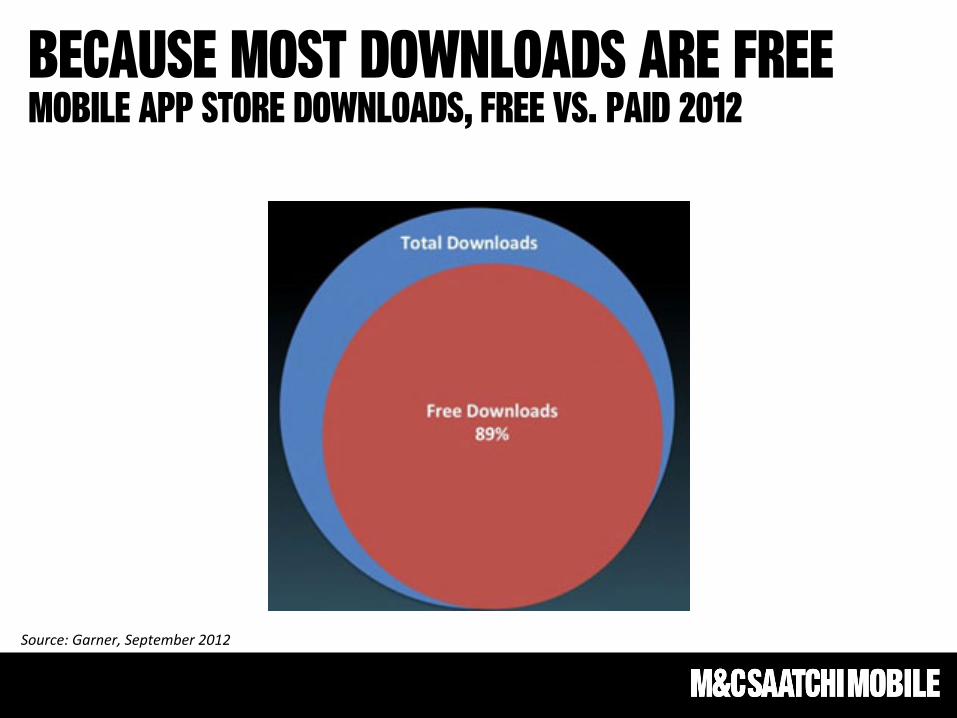

Because Most downloads are free Mobile app store downloads, free vs. paid 2012

Source: Garner, September 2012

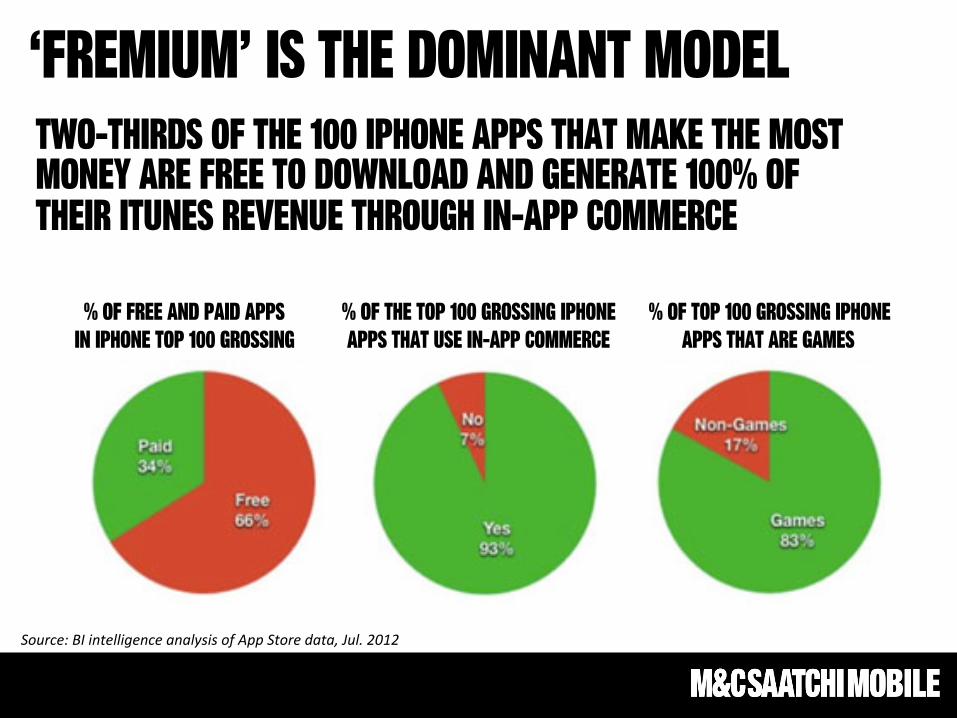

Two-thirds of the 100 iphone apps that make the most money are free to download and generate 100% of their itunes revenue through in-app commerce

% of free and paid apps In iphone top 100 grossing

% of the top 100 grossing iphone Apps that use in-app commerce

% of top 100 grossing iphone Apps that are games

‘Fremium’ is the dominant model

Source: BI intelligence analysis of App Store data, Jul. 2012

Trend 10. The market is constantly changing

Stay informed