microfinance: what have we learned? lessons from randomized experiments dean karlan annie duflo...

TRANSCRIPT

Microfinance: what have we learned?

Lessons from randomized experiments

Dean KarlanAnnie Duflo

April 1st, 2009, Cairo

Introduction

• In the recent years, microfinance has grown tremendously, and attracted a lot of attention

• Yet:– It has also attracted detractors– Many people still are not reached

by financial services– The poor still have access to a very

limited number of financial services

• What is the impact of microfinance on the lives of the poor?

• How can we improve services so that they reach out to more people, and help the poor better?

Outline

• Impact– Consumer credit in South Africa– “Grameen model” microcredit in India – Savings in Kenya

• Improving products• Microfinance and non financial services• Conclusion and further research

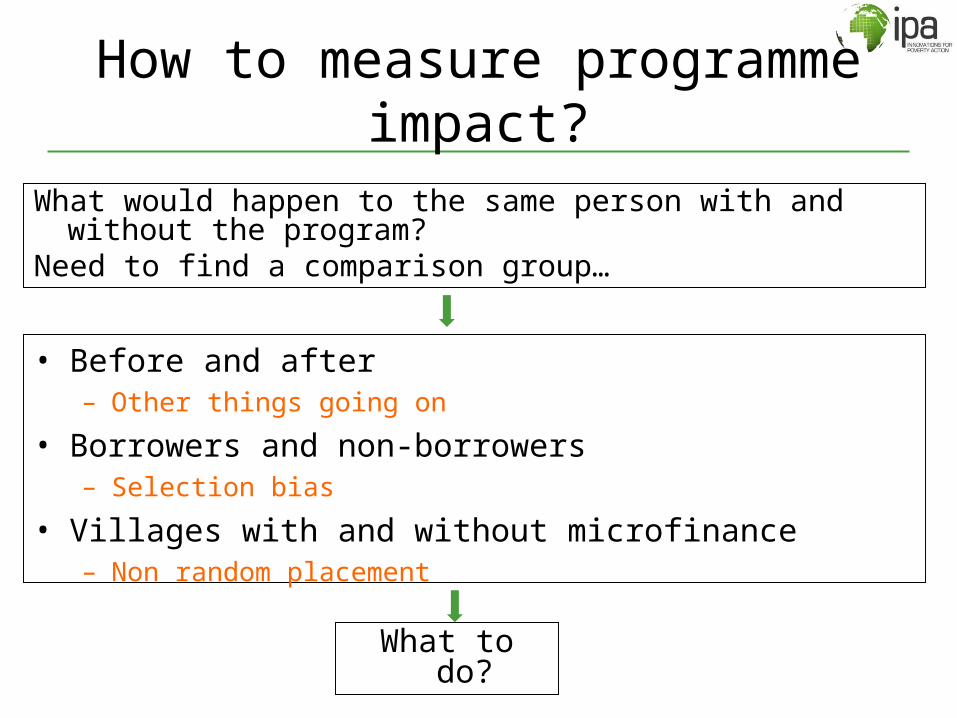

How to measure programme impact?

What would happen to the same person with and without the program?

Need to find a comparison group…

• Before and after– Other things going on

• Borrowers and non-borrowers– Selection bias

• Villages with and without microfinance – Non random placement

What to do?

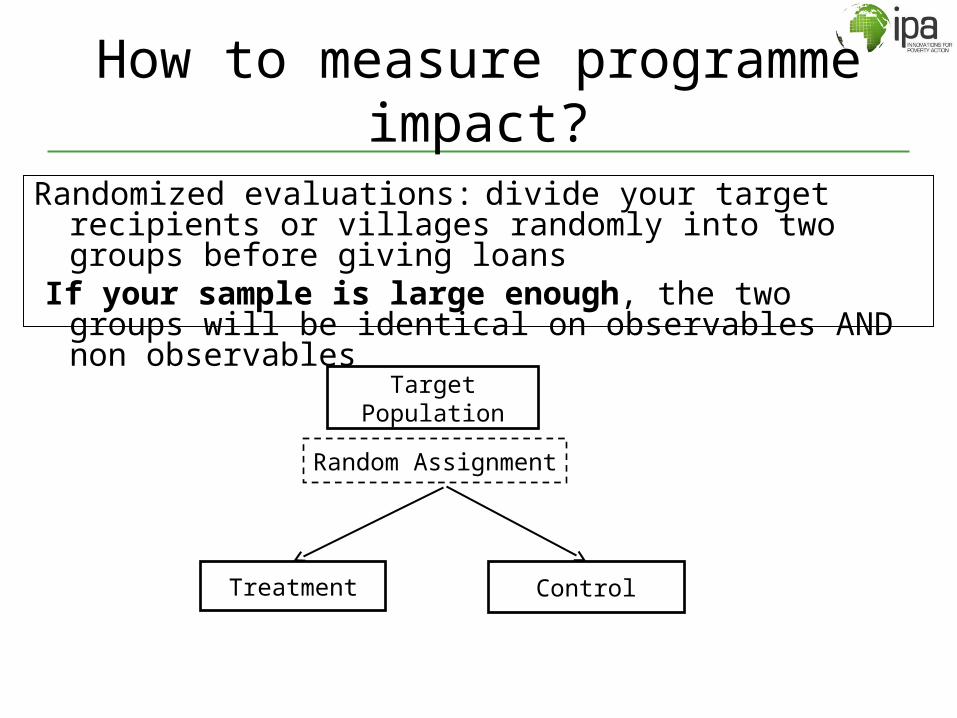

How to measure programme impact?

Randomized evaluations: divide your target recipients or villages randomly into two groups before giving loans

If your sample is large enough, the two groups will be identical on observables AND non observables

Target Population

Treatment Control

Random Assignment

Outline

• Impact– Consumer credit in South Africa– “Grameen model” microcredit in India – Savings in Kenya

• Improving products• Microfinance and non financial services• Conclusion and further research

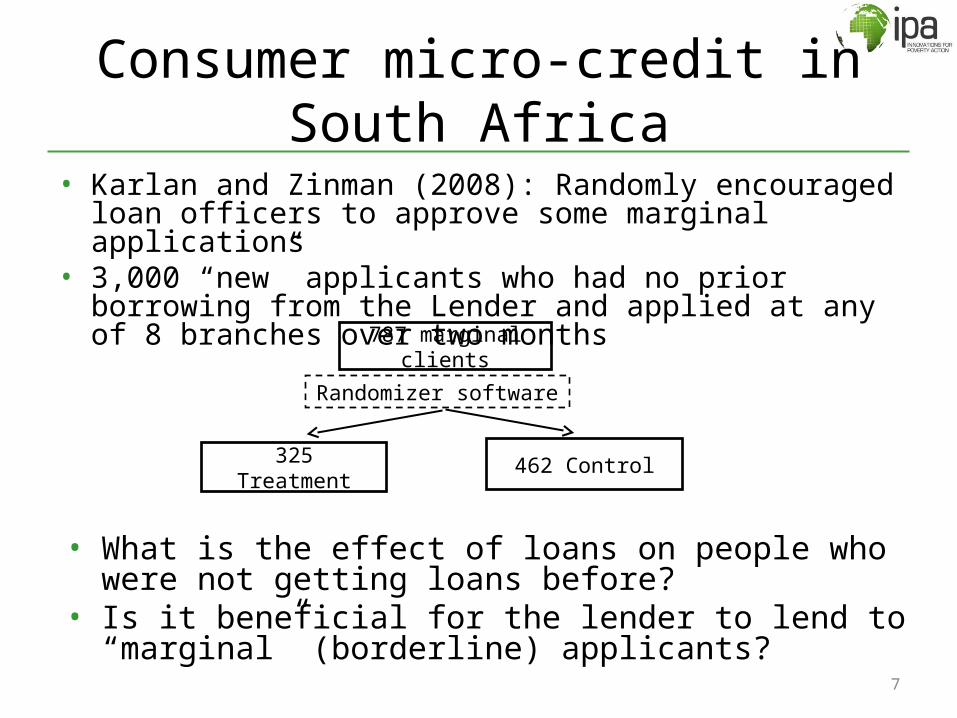

• Karlan and Zinman (2008): Randomly encouraged loan officers to approve some marginal applications

• 3,000 “new” applicants who had no prior borrowing from the Lender and applied at any of 8 branches over two months

7

Consumer micro-credit in South Africa

787 marginal clients

325 Treatment 462 Control

Randomizer software

• What is the effect of loans on people who were not getting loans before?

• Is it beneficial for the lender to lend to “marginal” (borderline) applicants?

Consumer micro-credit in South Africa

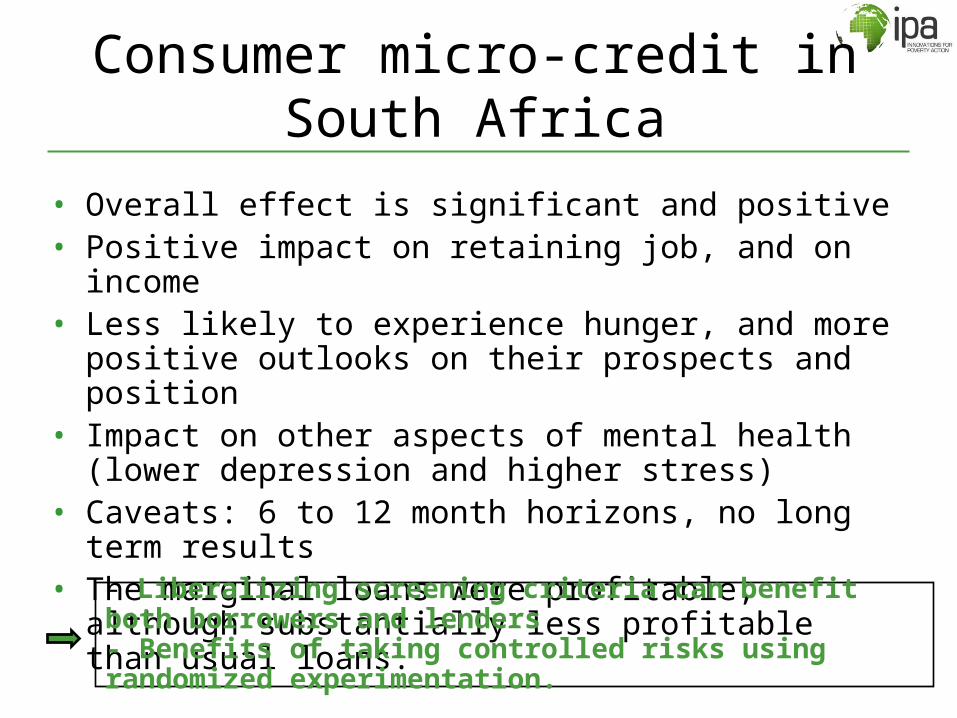

• Overall effect is significant and positive• Positive impact on retaining job, and on income• Less likely to experience hunger, and more positive outlooks on

their prospects and position • Impact on other aspects of mental health (lower depression

and higher stress)• Caveats: 6 to 12 month horizons, no long term results• The marginal loans were profitable, although substantially less

profitable than usual loans.

- Liberalizing screening criteria can benefit both borrowers and lenders - Benefits of taking controlled risks using randomized experimentation.

Outline

• Impact– Consumer credit in South Africa– “Grameen model” microcredit in India – Savings in Kenya

• Improving products• Microfinance and non financial services• Conclusion and further research

Impact of Micro-credit in India

• What is the impact of microcredit: on business creation; durable goods purchase; consumption smoothing, etc.

• Spandana: typical “grameen” model microcredit program• 120 slums in Hyderabad city, randomly divided in two groups

of 60 slums– Spandana introduced micro-credit in one group, the

“treatment group”, and not in the other group, the “control group”.

• Despite the presence of other MFIs, take up of credit and amounts borrowed were higher in treatment slums

Impact of Micro-credit in India

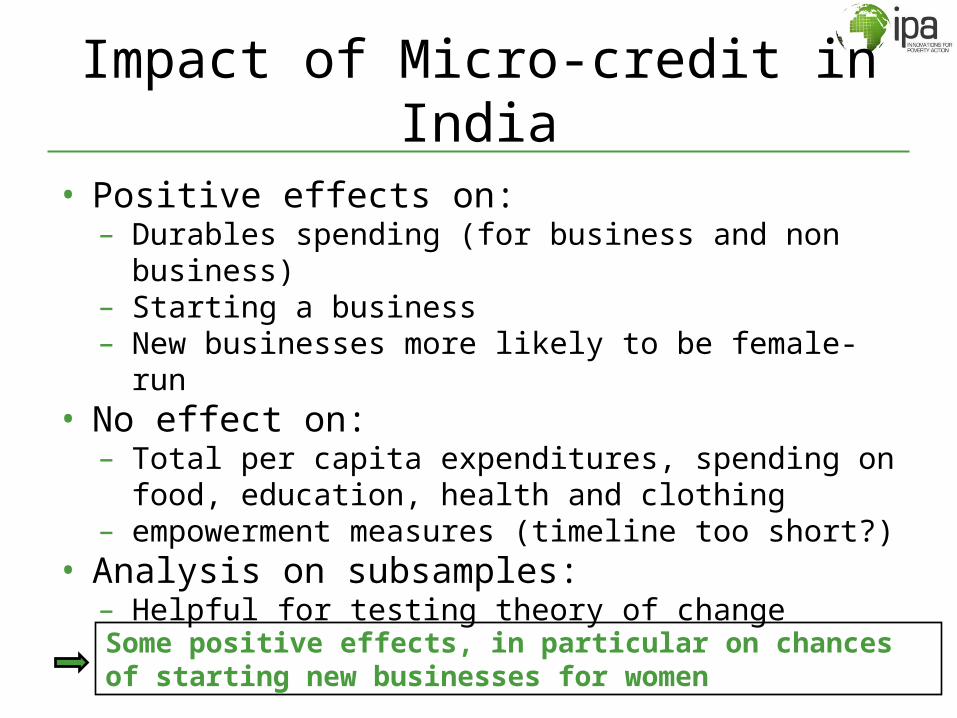

• Positive effects on:– Durables spending (for business and non business)– Starting a business– New businesses more likely to be female-run

• No effect on:– Total per capita expenditures, spending on food,

education, health and clothing– empowerment measures (timeline too short?)

• Analysis on subsamples:– Helpful for testing theory of change

Some positive effects, in particular on chances of starting new businesses for women

Outline

• Impact– Consumer credit in South Africa– “Grameen model” microcredit in India – Savings in Kenya

• Improving products• Microfinance and non financial services• Conclusion and further research

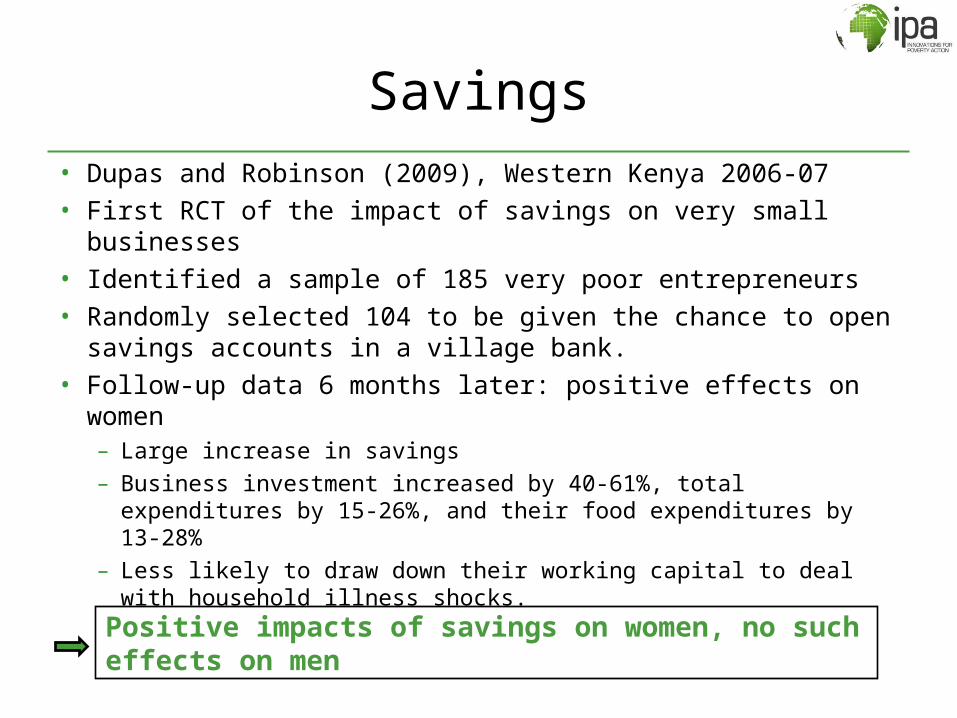

Savings• Dupas and Robinson (2009), Western Kenya 2006-07• First RCT of the impact of savings on very small businesses• Identified a sample of 185 very poor entrepreneurs• Randomly selected 104 to be given the chance to open

savings accounts in a village bank. • Follow-up data 6 months later: positive effects on women

– Large increase in savings– Business investment increased by 40-61%, total expenditures by

15-26%, and their food expenditures by 13-28%– Less likely to draw down their working capital to deal with

household illness shocks.

Positive impacts of savings on women, no such effects on men

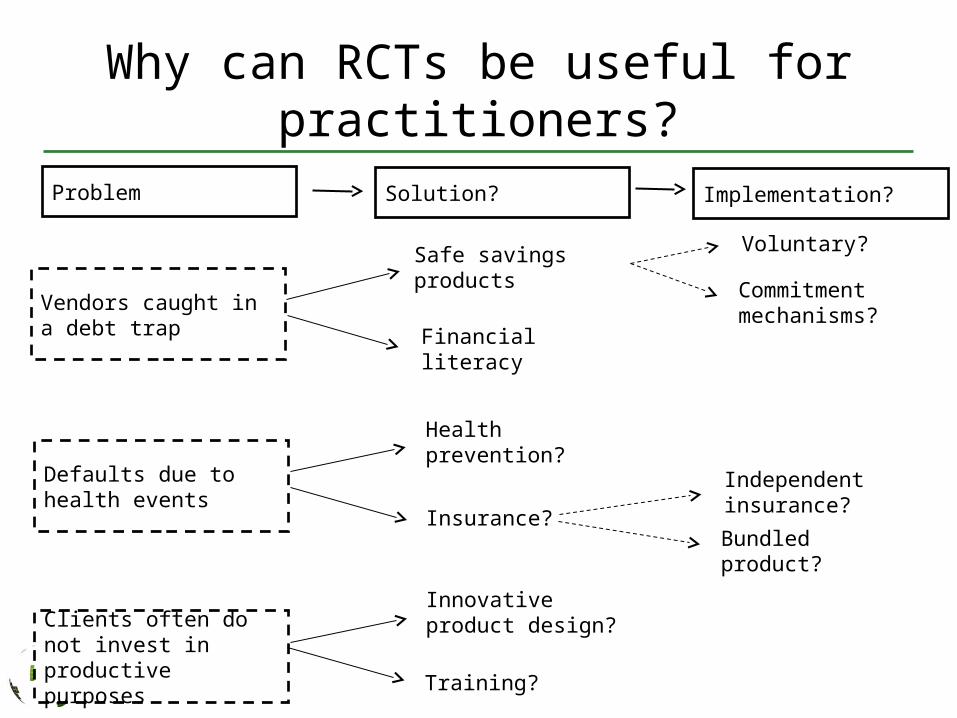

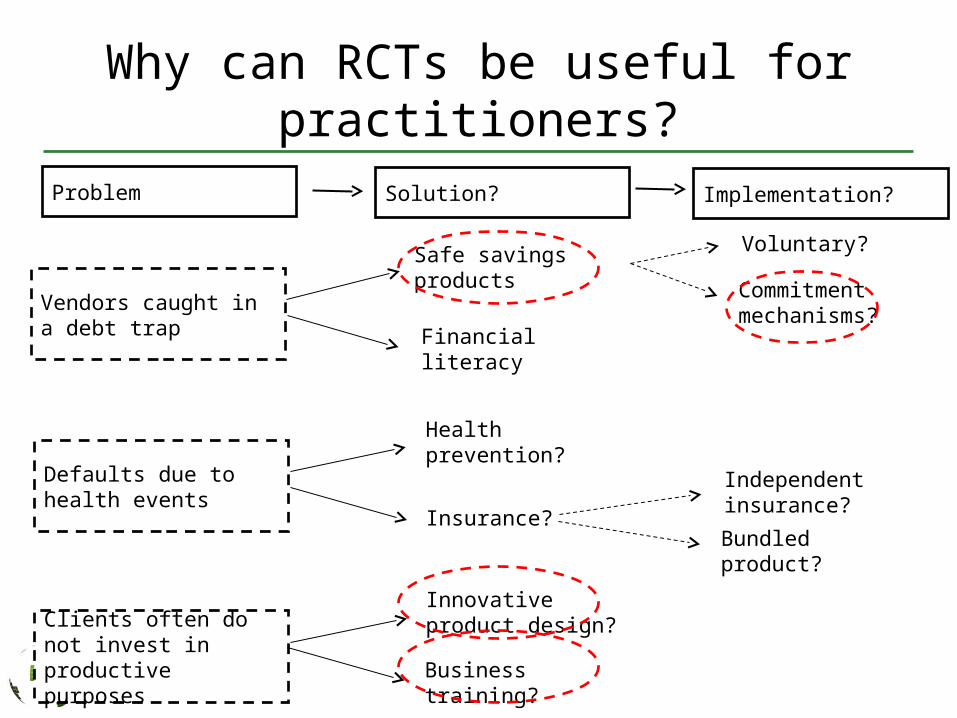

Why can RCTs be useful for practitioners?

Vendors caught in a debt trap

Safe savings products

Financial literacy

Defaults due to health events

Health prevention?

Insurance?

Clients often do not invest in productive purposes

Innovative product design?

Training?

Independent insurance?

Bundled product?

Voluntary?

Commitment mechanisms?

Problem Solution? Implementation?

Outline

• Impact• Improving products– The “Grameen loan”: looking inside the black box– Savings: how to make people save more? – Marketing: how can it affect take-up?

• Microfinance and non financial services• Conclusion and further research

Improving products

• How to improve on existing products, and develop new products in order to: – Improving outreach– Improving use of services– Get the right services to the right people

• RCTs can be used not only to evaluate program impact,

• But also to experiment on product design in such a way that we can understand what works and what does not

Outline

• Impact• Improving products– The “Grameen loan”: looking inside the black box– Savings: how to make people save more? – Marketing: how can it affect take-up?

• Microfinance and non financial services• Conclusion and further research

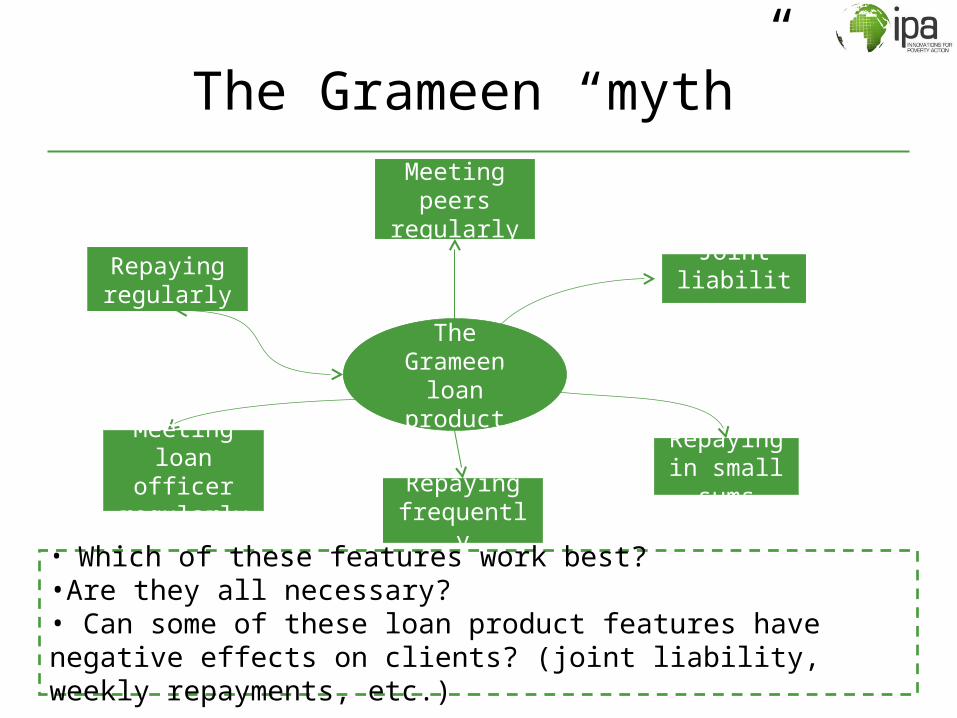

The Grameen “myth”

The Grameen loan product

Joint liability

Repaying in small sums

Repaying regularly

Repaying frequently

Meeting peers

regularly

• Which of these features work best? •Are they all necessary? • Can some of these loan product features have negative effects on clients? (joint liability, weekly repayments, etc.)

Meeting loan officer

regularly

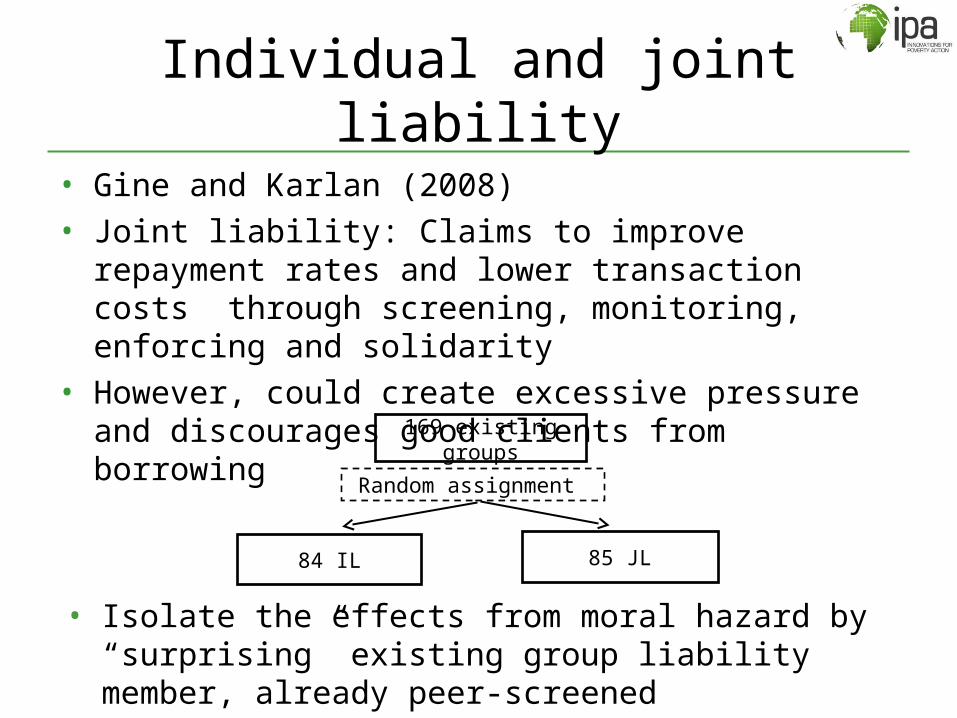

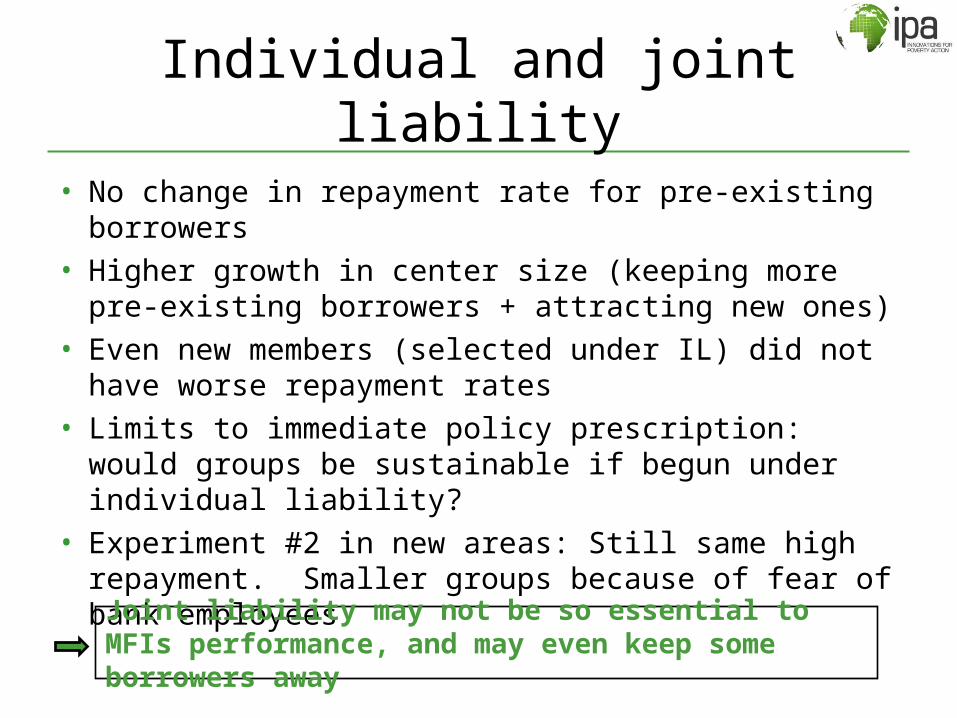

Individual and joint liability

• Gine and Karlan (2008)• Joint liability: Claims to improve repayment rates and lower

transaction costs through screening, monitoring, enforcing and solidarity

• However, could create excessive pressure and discourages good clients from borrowing

169 existing groups

84 IL 85 JL

Random assignment

• Isolate the effects from moral hazard by “surprising” existing group liability member, already peer-screened

Individual and joint liability

• No change in repayment rate for pre-existing borrowers• Higher growth in center size (keeping more pre-existing

borrowers + attracting new ones)• Even new members (selected under IL) did not have

worse repayment rates• Limits to immediate policy prescription: would groups be

sustainable if begun under individual liability?• Experiment #2 in new areas: Still same high repayment.

Smaller groups because of fear of bank employees

Joint liability may not be so essential to MFIs performance, and may even keep some borrowers away

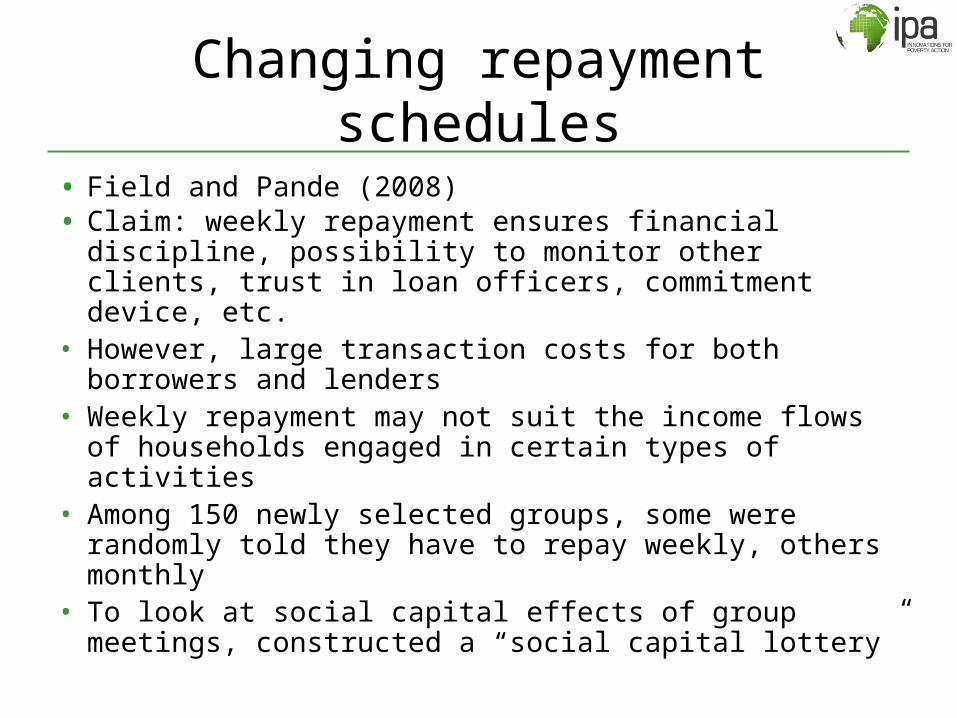

Changing repayment schedules

• Field and Pande (2008)• Claim: weekly repayment ensures financial discipline,

possibility to monitor other clients, trust in loan officers, commitment device, etc.

• However, large transaction costs for both borrowers and lenders

• Weekly repayment may not suit the income flows of households engaged in certain types of activities

• Among 150 newly selected groups, some were randomly told they have to repay weekly, others monthly

• To look at social capital effects of group meetings, constructed a “social capital lottery”

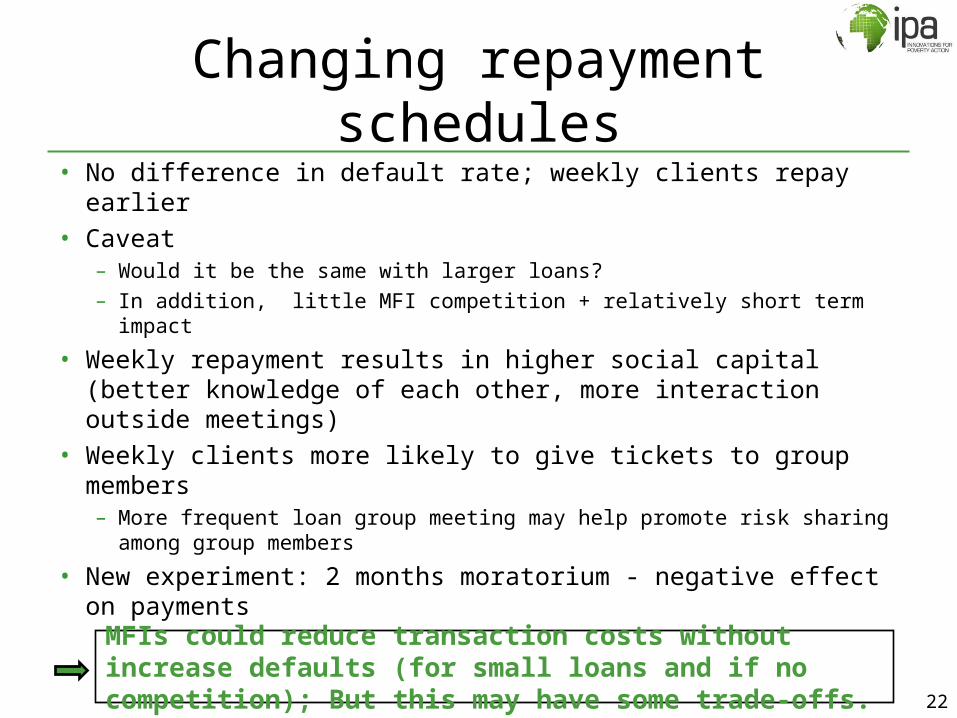

Changing repayment schedules• No difference in default rate; weekly clients repay earlier • Caveat

– Would it be the same with larger loans?– In addition, little MFI competition + relatively short term impact

• Weekly repayment results in higher social capital (better knowledge of each other, more interaction outside meetings)

• Weekly clients more likely to give tickets to group members– More frequent loan group meeting may help promote risk sharing

among group members

• New experiment: 2 months moratorium - negative effect on payments

22

MFIs could reduce transaction costs without increase defaults (for small loans and if no competition); But this may have some trade-offs.

Outline

• Impact• Improving products– The “Grameen loan”: looking inside the black box– Savings: how to make people save more? – Marketing: how can it affect take-up?

• Microfinance and non financial services• Conclusion and further research

Why don’t people save more?

• Poor households have disposable income that they could save• However, they don’t save as much as they could, or want• Sometimes, they borrow at very high interest rates for

businesses that don’t grow – although they could get out of debt by saving more

• Why don’t they save more? • Could be several reasons

– no safe avenues for savings; want to save but tempted; other household members take the money; don’t understand returns to savings..

• If tempted to consume need products that will help people save

• If don’t understand may need financial literacy training

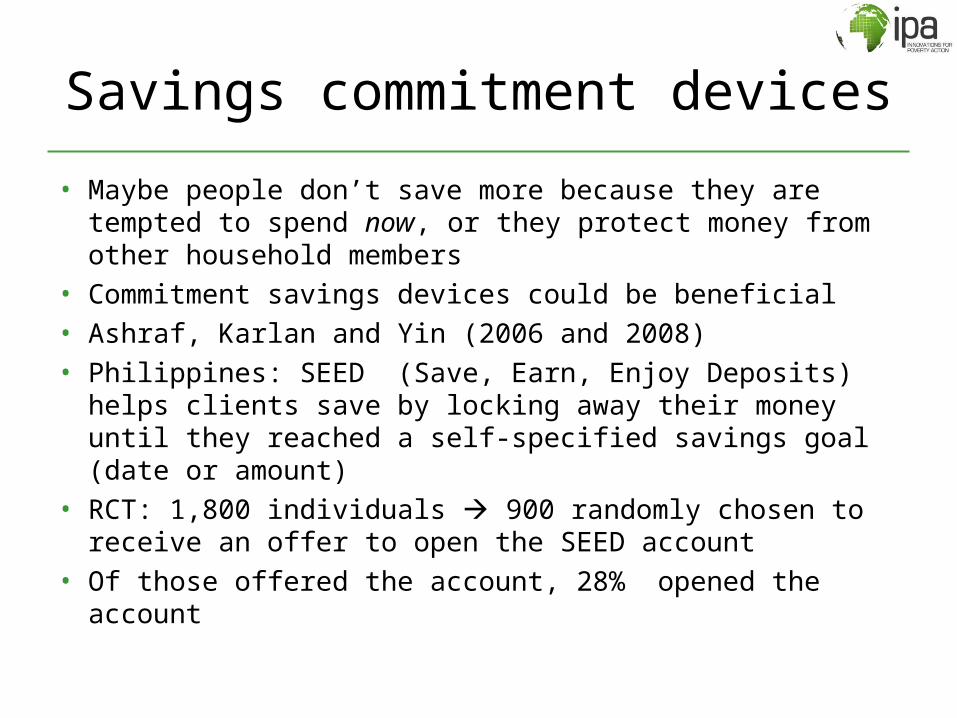

Savings commitment devices

• Maybe people don’t save more because they are tempted to spend now, or they protect money from other household members

• Commitment savings devices could be beneficial• Ashraf, Karlan and Yin (2006 and 2008)• Philippines: SEED (Save, Earn, Enjoy Deposits) helps clients

save by locking away their money until they reached a self-specified savings goal (date or amount)

• RCT: 1,800 individuals 900 randomly chosen to receive an offer to open the SEED account

• Of those offered the account, 28% opened the account

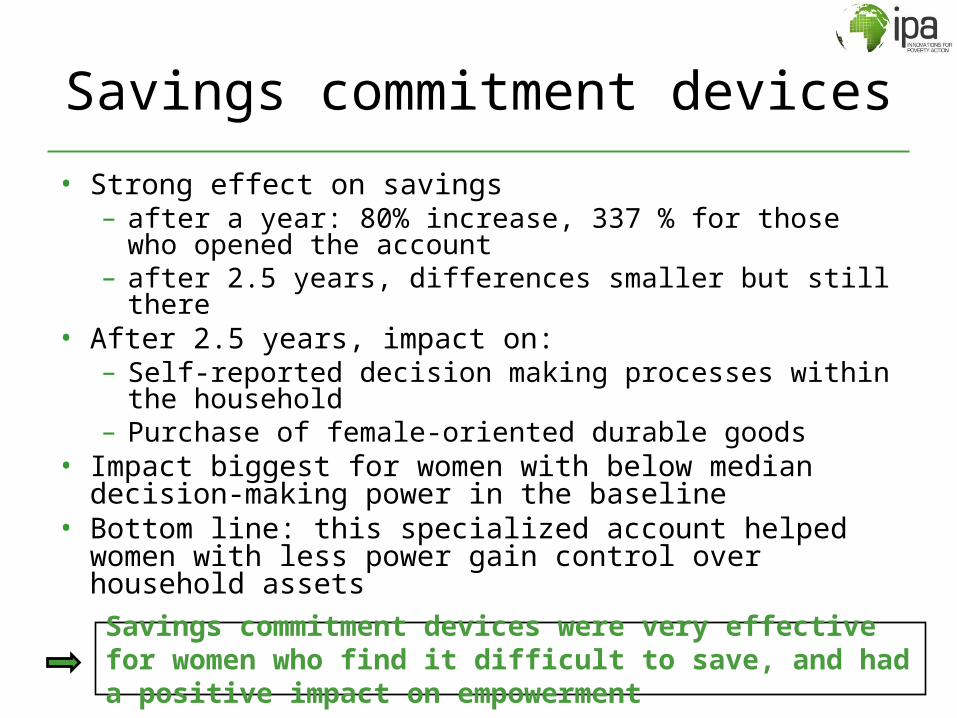

Savings commitment devices

• Strong effect on savings – after a year: 80% increase, 337 % for those who opened the

account– after 2.5 years, differences smaller but still there

• After 2.5 years, impact on:– Self-reported decision making processes within the

household – Purchase of female-oriented durable goods

• Impact biggest for women with below median decision-making power in the baseline

• Bottom line: this specialized account helped women with less power gain control over household assets

Savings commitment devices were very effective for women who find it difficult to save, and had a positive impact on empowerment

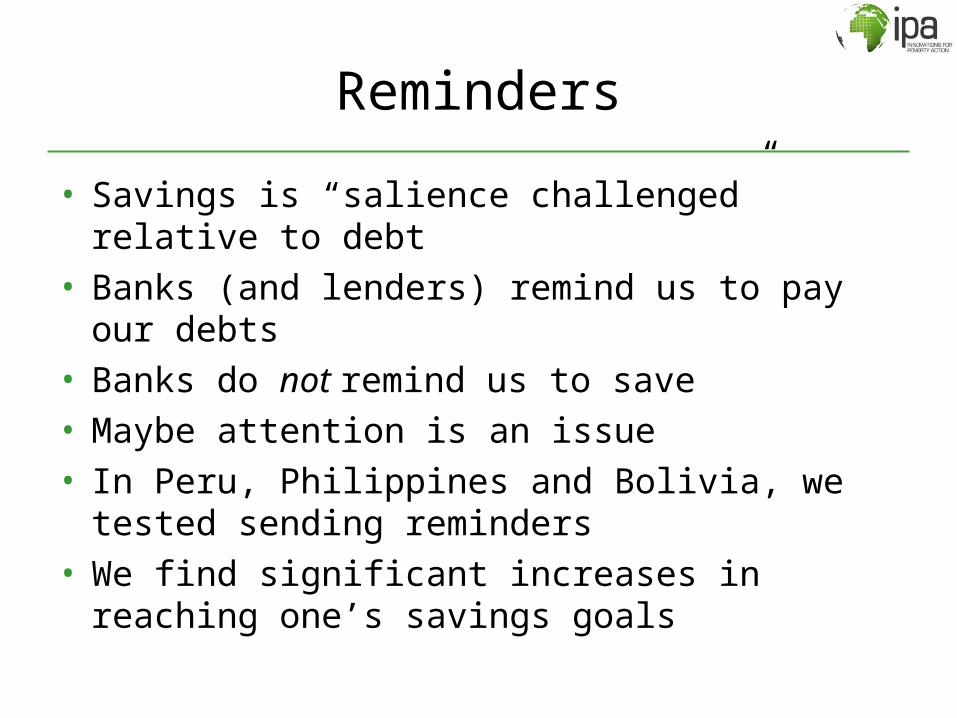

Reminders

• Savings is “salience challenged” relative to debt• Banks (and lenders) remind us to pay our debts• Banks do not remind us to save• Maybe attention is an issue• In Peru, Philippines and Bolivia, we tested sending

reminders• We find significant increases in reaching one’s savings

goals

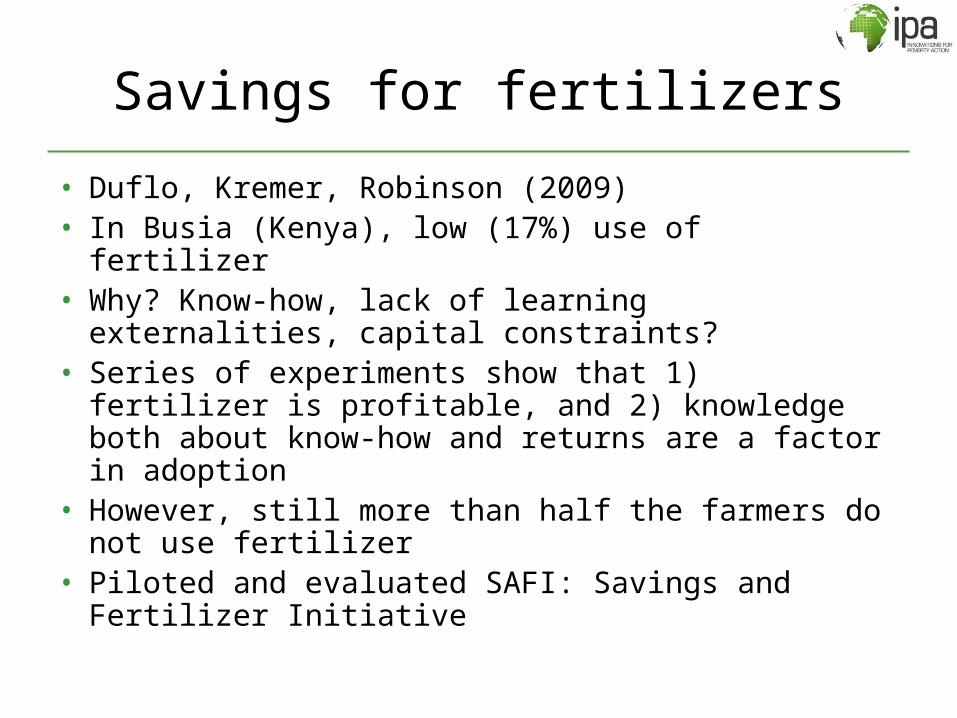

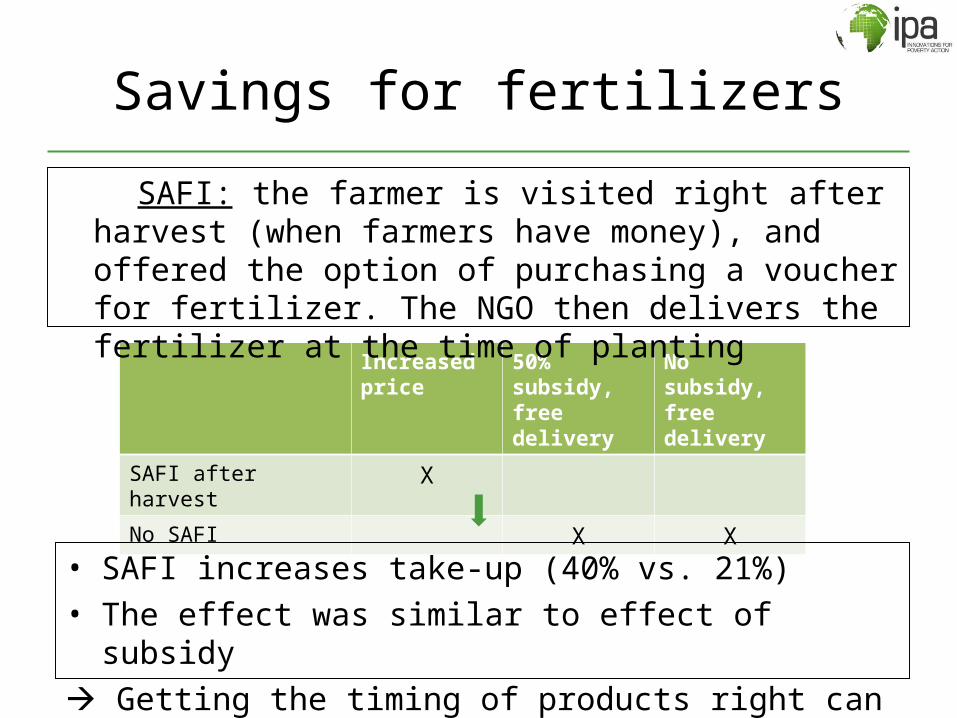

Savings for fertilizers

• Duflo, Kremer, Robinson (2009)• In Busia (Kenya), low (17%) use of fertilizer• Why? Know-how, lack of learning externalities, capital

constraints?• Series of experiments show that 1) fertilizer is profitable,

and 2) knowledge both about know-how and returns are a factor in adoption

• However, still more than half the farmers do not use fertilizer

• Piloted and evaluated SAFI: Savings and Fertilizer Initiative

Savings for fertilizers

Increased price

50% subsidy, free delivery

No subsidy, free delivery

SAFI after harvest XNo SAFI X X

• SAFI increases take-up (40% vs. 21%)• The effect was similar to effect of subsidy Getting the timing of products right can be key

SAFI: the farmer is visited right after harvest (when farmers have money), and offered the option of purchasing a voucher for fertilizer. The NGO then delivers the fertilizer at the time of planting

Outline

• Impact• Improving products– The “Grameen loan”: looking inside the black box– Savings: how to make people save more? – Marketing: how can it affect take-up?

• Microfinance and non financial services• Conclusion and further research

Marketing: South Africa experiment

• Bertrand, Karlan, Mullainathan, Shafir and Zinman (2008-9)

• Experiment with a lender to measure sensitivity to price for borrowers– Randomly vary interest rates offered to people when

sending marketing letters– Also randomly vary various marketing features such as a

woman’s photo on the letter, complicated vs simple explanation of loan contract, etc.

• Photo of a woman: same value to men as dropping the interest rate by 1/3.

Selling weather insurance in India

• Cole, Gine, Tobacman, Topalova, Townsend and Vickery (2008)• Low take-up of weather insurance: Why? • Test effect of price and liquidity constraints • Also test effect of other factors suggested by psychology:

financial education, trust in the selling agent, marketing messages

• Endorsement of the household visit by a local NGO representative increases take up by 10 percentage points amongst households familiar with the NGO

• The act of conducting a household marketing visit also affects take-upMarketing that takes into account psychological and cultural constraints of clients can increase take-up of products

Outline

• Impact• Improving products• Microfinance and non financial services– Business training– Financial literacy

• Conclusion and further research

Business training

• Microfinance’s promise to the poor is that access to credit and banking services will improve their economic opportunities

• Can the poor adequately take advantage of such opportunities given low skills, education levels, social mobility and access to information?

• Returns to business training and financial literacy could be high

• But can one teach basic entrepreneurship skills, or are they fixed personal characteristics?

• Karlan and Valdivia (2008): study with FINCA Peru

Business training in Peru

• Some microcredit groups assigned to receive the “treatment”• 30 to 60 minute entrepreneurship training sessions during their

weekly or monthly banking meeting over one to two years • Improved business knowledge, practices and revenues. • Improved client retention rates for the MFI• Gains outweighed the costs => microfinance “plus” might make

business sense• Larger effects found for those that expressed less interest in

training => demand-driven “market” solutions may not be the best strategy

• More studies needed, also of what are the best ways to implement such trainings, and with non clients as well.

Outline

• Impact• Improving products• Microfinance and non financial services– Business training– Financial literacy

• Conclusion and further research

Financial literacy training

• So far no rigorous study has shown significant impacts of financial literacy training

• India, weather insurance experiment: a short module teaching farmers the concept of insurance and of millimeters increase take-up has no effect– But module was very short

• Verdict still out• Perfect example of where randomized trials can be done

easily to help answer a hot topic in consumer and entrepreneurial finance

• We need more experiments on financial literacy training

Why can RCTs be useful for practitioners?

Vendors caught in a debt trap

Safe savings products

Financial literacy

Defaults due to health events

Health prevention?

Insurance?

Clients often do not invest in productive purposes

Innovative product design?

Business training?

Independent insurance?

Bundled product?

Voluntary?

Commitment mechanisms?

Problem Solution? Implementation?

Outline

• Impact• Improving products• Microfinance and non financial services– Business training– Financial literacy

• Conclusion and further research

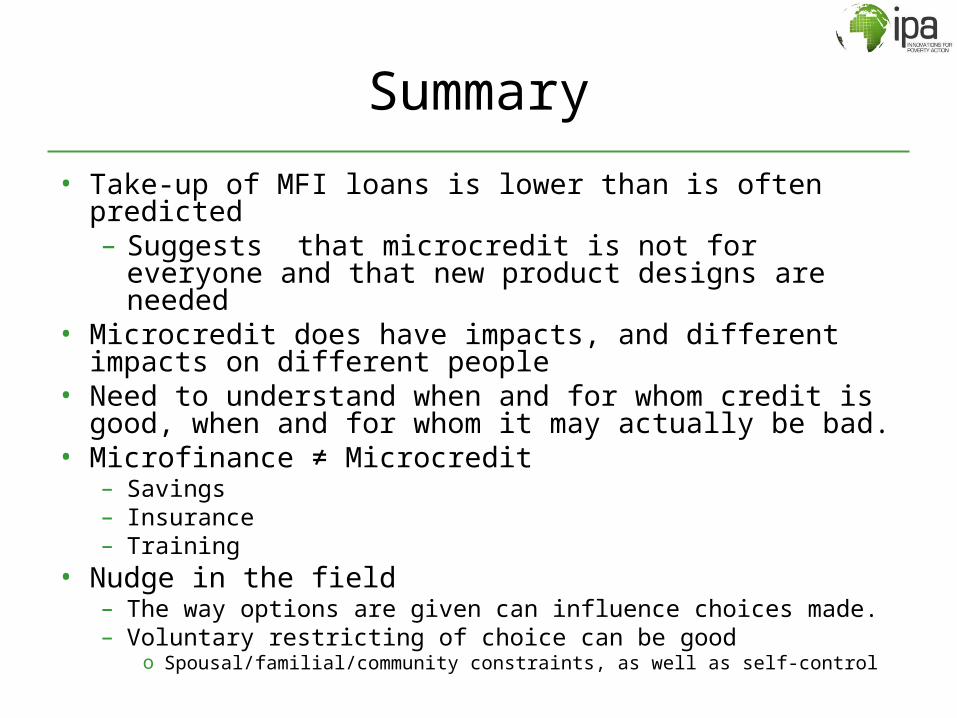

Summary

• Take-up of MFI loans is lower than is often predicted– Suggests that microcredit is not for everyone and that

new product designs are needed• Microcredit does have impacts, and different impacts on

different people• Need to understand when and for whom credit is good, when

and for whom it may actually be bad.• Microfinance ≠ Microcredit

– Savings– Insurance– Training

• Nudge in the field– The way options are given can influence choices made.– Voluntary restricting of choice can be good

o Spousal/familial/community constraints, as well as self-control

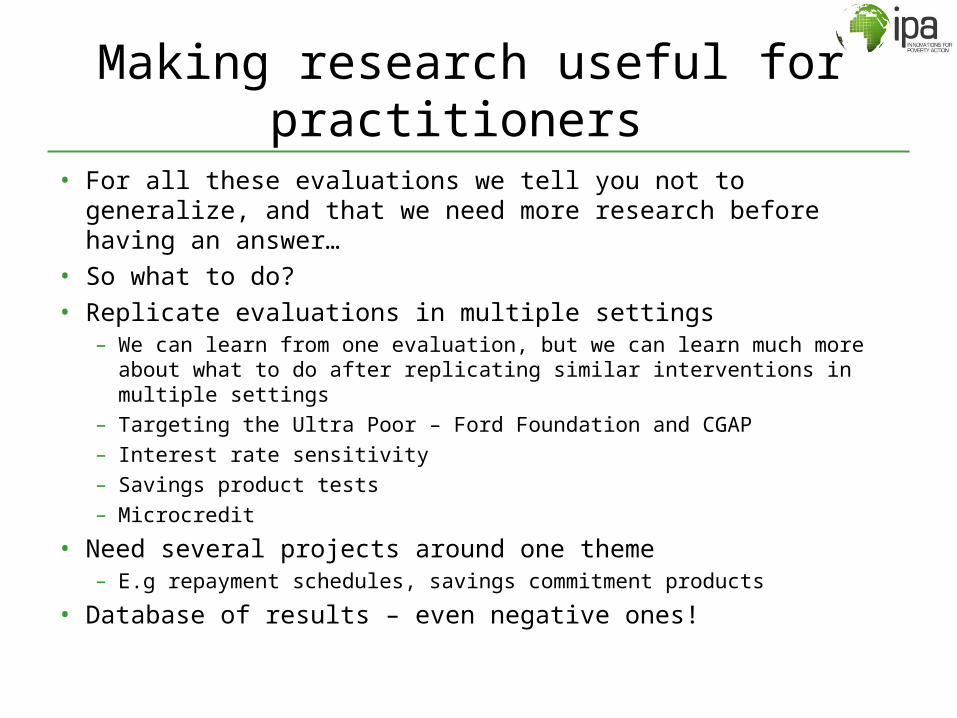

• For all these evaluations we tell you not to generalize, and that we need more research before having an answer…

• So what to do? • Replicate evaluations in multiple settings

– We can learn from one evaluation, but we can learn much more about what to do after replicating similar interventions in multiple settings

– Targeting the Ultra Poor – Ford Foundation and CGAP– Interest rate sensitivity– Savings product tests– Microcredit

• Need several projects around one theme– E.g repayment schedules, savings commitment products

• Database of results – even negative ones!

Making research useful for practitioners

Further research needed

• There are still some important outstanding questions about microfinance

• What services and combination of services work best, and for whom?

• What is the impact of access to an integrated suite of financial services?

• Gender issues: is there differential return to capital for women and for men? Is impact of credit different for both? Do men and women face different constraints to savings?

• How will technology transform access to savings products, and poor households’ financial behavior?