microfinance sector note - equirus...

TRANSCRIPT

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 1 of 63Before reading this report, you must refer to the disclaimer on the last page.

Microfinance aims at catering to economically active, low income, self-employed women who lack access to organized sector credit. We take a contra-view to the market as we believe microfinance has limited growth opportunities with multiple risks of over-leveraging and pricing competition due to fast growth at the cost of due diligence and entry of new players. We believe the sector’s risk reward is unfavorable and we are cautious on companies on the fast track path to grow AUM at all costs. We prefer diversified businesses such as Equitas, but rich valuation leaves room for near term price correction. We initiate on Equitas Holdings and Ujjivan Financial Services with SHORT rating and Sep’17 TP of Rs. 142/share and Rs. 372/share respectively.

Brief background and industry snapshot:

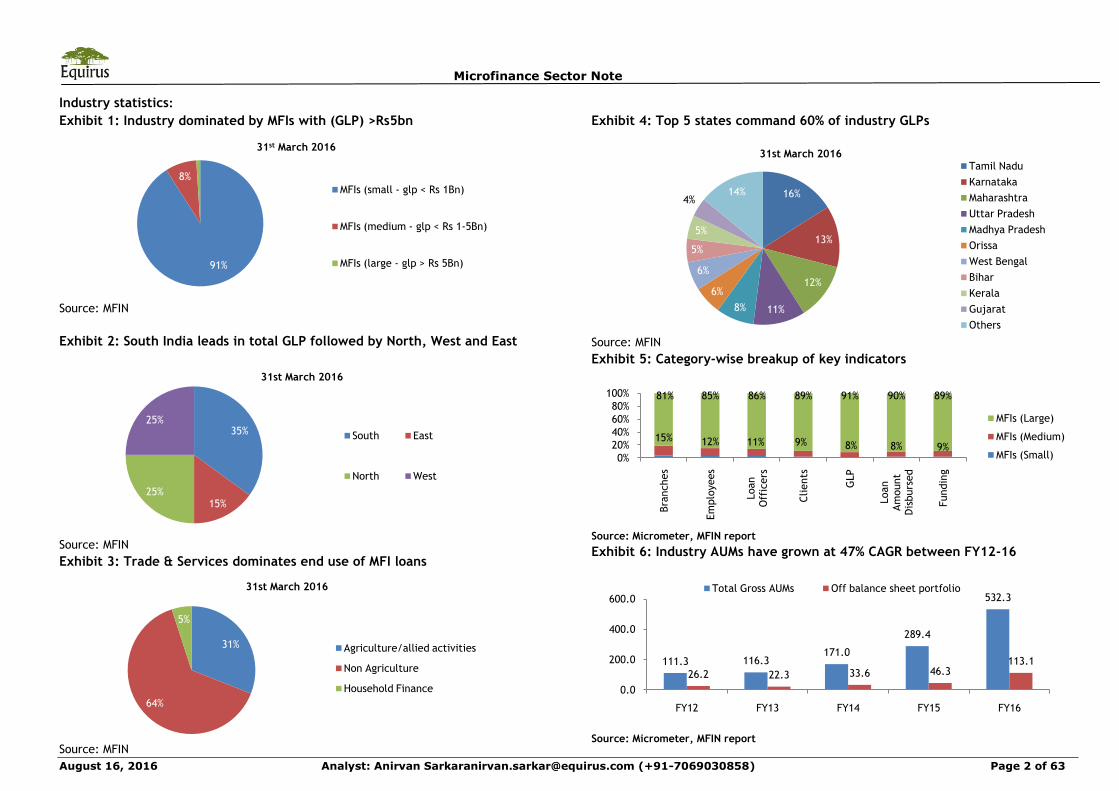

As of FY16, 56 registered NBFC-MFIs have total gross AUM of Rs. 532.3bn (47% CAGR between FY12-16) of which the top 10 MFIs command 72% share. South India leads in GLPs (35%), followed by North and West India (25% each) and East India (15%). Non-agricultural activities account for 64% of portfolio, agriculture and allied activities 31% and household finance 5%.

Transition from SHG to JLG, emergence of SFBs: The microfinance industry has evolved from operating as a mediator for SHG-bank linkages, to for-profit companies providing JLG based loans to economically active self-employed women. In 2015, 8 MFIs received small finance banking (SFB) license from RBI. They are Ujjivan Financial Services, Janalakshmi Financial Services, Equitas Holdings, Disha Microfin, ESAF Microfinance, RGVN Microfinance, Suryoday Microfinance, and Utkarsh Microfinance. SFBs are required to make the bank operational within 18 months of receiving the license and to list the bank separately within 3 years of going operational.

Our thesis:

Limited headroom for microfinance industry growth, fast track growth would require unreal increase in penetration: We take a contra-view to the market as we believe the addressable market for microfinance is much lower than what headline numbers suggest. Notwithstanding India’s large population of economically active poor, microfinance can address limited households (~120mn in FY16) with average ticket size growth of at most 10% yoy. Our calculations (exhibit 16) indicate that industry penetration has to increase from 25% in FY16 to 53% by FY21E to achieve 30% CAGR during this period. This is not possible without expansion in rural areas where economies of scale are difficult.

Risks include bulk defaults from reckless growth: While social collateral protects credit quality, the business bears inherent risks. Previous microfinance crises in India, in Krishna (FY06), Karnataka (FY09) and A.P. (FY10) were preceded by high AUM growth leading to bulk defaults. At present, MFIs are targeting super-normal growth backed by increased investor interest and fund flow. However, we believe super-normal growth at the bottom of the pyramid is bound to be followed by mass defaults and subsequent crises. Also, with

majority of customers being unbanked, the business operates largely on cash basis, with disbursements and collections in cash, leaving significant scope for frauds/thefts.

Fast track growth at the bottom of the pyramid from too many players has a cost!

Possible spread reduction due to supernormal growth will affect margins:Microfinance commands high interest rates due to high risk profile, and creditquality rests on social collateral and limited supply of credit. With too manyparticipants looking to grow quickly, customers will have more choice, andpricing competition can reduce spreads and margins for microfinance business.

Enhanced risk of overleveraging from banks entering microfinance: Whileexisting credit bureaus are regularly updated with borrowing data of customers(regulation stipulates microfinance customers can borrow upto Rs. 60K - recentlyincreased to Rs. 0.1mn - from at most 2 MFIs), the entry of banks inmicrofinance complicates credit data efficiency as bank borrowing data may notbe captured, leading to the risk of overleverage and credit defaults.

Controlled growth appetite and picking quality over quantity willdifferentiate winners and losers: With increased investor interest, MFIs havetargeted super-normal growth to attract funds at the cost of due diligence, atrend that has historically preceded the 3 microfinance crises in India. This willdifferentiate winners from losers in the medium to long term. A classic exampleof slow growth at the bottom of the pyramid is GRUH Finance, whose loan bookstands at Rs. 110bn after 30 years of operations. Newer companies growingultra-fast during favourable market conditions ignore the associated risks ofunsustainable performance, volatility in growth and change in customer creditbehaviour resulting from spurt in credit supply.

Due diligence, control and supervision key to success, larger players score: Microfinance addresses economically active poor forming the top layer of the bottom of the pyramid, not the bottom itself. Our channel checks indicate that credit behaviour has a regional influence. Cherry-picking the right socio-economic group in the right geographies is crucial to maintain asset quality.

Because of limited digitization, retaining strong control and supervision over operations is crucial in microfinance. This is where larger players with strong branch networks have an advantage over smaller players who are forced to operate with a broader radius of operations, reducing control over their domain.

SHORT on Equitas Holdings, SHORT on Ujjivan Financial: We prefer Equitas’s diversified business and their reducing dependence on microfinance but we believe their high valuation would lead to price correction and we are SHORT on the stock. We are cautious on Ujjivan’s portfolio concentration in microfinance and unproven track record of scaling up individual lending business, and we initiate with SHORT rating on the stock.

© 2016 Equirus All rights reserved

Microfinance Sector Note

Fast track growth at the bottom of the pyramid a huge risk, prefer MFIs diversifying businesses,

valuations at unfavorable risk-reward, Initiate with SHORT on Equitas and Ujjivan

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 2 of 63

Industry statistics:

Exhibit 1: Industry dominated by MFIs with (GLP) >Rs5bn

Source: MFIN

Exhibit 2: South India leads in total GLP followed by North, West and East

Source: MFIN

Exhibit 3: Trade & Services dominates end use of MFI loans

Source: MFIN

Exhibit 4: Top 5 states command 60% of industry GLPs

Source: MFIN

Exhibit 5: Category-wise breakup of key indicators

Source: Micrometer, MFIN report

Exhibit 6: Industry AUMs have grown at 47% CAGR between FY12-16

Source: Micrometer, MFIN report

91%

8%

1% 31st March 2016

MFIs (small - glp < Rs 1Bn)

MFIs (medium - glp < Rs 1-5Bn)

MFIs (large - glp > Rs 5Bn)

35%

15%25%

25%

31st March 2016

South East

North West

31%

64%

5%

31st March 2016

Agriculture/allied activities

Non Agriculture

Household Finance

16%

13%

12%

11%8%

6%

6%

5%

5%

4%14%

31st March 2016Tamil Nadu

Karnataka

Maharashtra

Uttar Pradesh

Madhya Pradesh

Orissa

West Bengal

Bihar

Kerala

Gujarat

Others

15% 12% 11% 9% 8% 8% 9%

81% 85% 86% 89% 91% 90% 89%

0%

20%

40%

60%

80%

100%

Bra

nches

Em

plo

yees

Loan

Off

icers

Clients

GLP

Loan

Am

ount

Dis

burs

ed

Fundin

g

MFIs (Large)

MFIs (Medium)

MFIs (Small)

111.3 116.3171.0

289.4

532.3

26.2 22.3 33.6 46.3113.1

0.0

200.0

400.0

600.0

FY12 FY13 FY14 FY15 FY16

Total Gross AUMs Off balance sheet portfolio

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 3 of 63

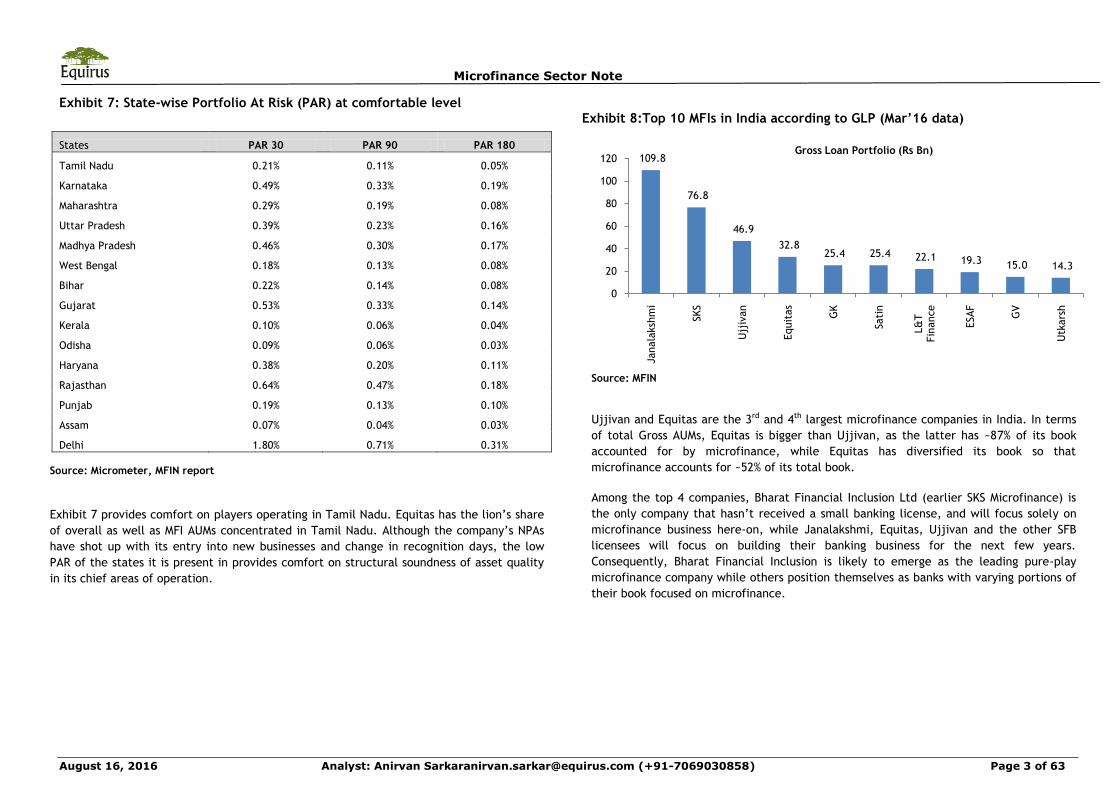

Exhibit 7: State-wise Portfolio At Risk (PAR) at comfortable level

States PAR 30 PAR 90 PAR 180

Tamil Nadu 0.21% 0.11% 0.05%

Karnataka 0.49% 0.33% 0.19%

Maharashtra 0.29% 0.19% 0.08%

Uttar Pradesh 0.39% 0.23% 0.16%

Madhya Pradesh 0.46% 0.30% 0.17%

West Bengal 0.18% 0.13% 0.08%

Bihar 0.22% 0.14% 0.08%

Gujarat 0.53% 0.33% 0.14%

Kerala 0.10% 0.06% 0.04%

Odisha 0.09% 0.06% 0.03%

Haryana 0.38% 0.20% 0.11%

Rajasthan 0.64% 0.47% 0.18%

Punjab 0.19% 0.13% 0.10%

Assam 0.07% 0.04% 0.03%

Delhi 1.80% 0.71% 0.31%

Source: Micrometer, MFIN report

Exhibit 7 provides comfort on players operating in Tamil Nadu. Equitas has the lion’s share

of overall as well as MFI AUMs concentrated in Tamil Nadu. Although the company’s NPAs

have shot up with its entry into new businesses and change in recognition days, the low

PAR of the states it is present in provides comfort on structural soundness of asset quality

in its chief areas of operation.

Exhibit 8:Top 10 MFIs in India according to GLP (Mar’16 data)

Source: MFIN

Ujjivan and Equitas are the 3rd and 4th largest microfinance companies in India. In terms

of total Gross AUMs, Equitas is bigger than Ujjivan, as the latter has ~87% of its book

accounted for by microfinance, while Equitas has diversified its book so that

microfinance accounts for ~52% of its total book.

Among the top 4 companies, Bharat Financial Inclusion Ltd (earlier SKS Microfinance) is

the only company that hasn’t received a small banking license, and will focus solely on

microfinance business here-on, while Janalakshmi, Equitas, Ujjivan and the other SFB

licensees will focus on building their banking business for the next few years.

Consequently, Bharat Financial Inclusion is likely to emerge as the leading pure-play

microfinance company while others position themselves as banks with varying portions of

their book focused on microfinance.

109.8

76.8

46.9

32.8 25.4 25.4 22.1 19.3 15.0 14.3

0

20

40

60

80

100

120

Janala

ksh

mi

SKS

Ujj

ivan

Equit

as

GK

Sati

n

L&

T

Fin

ance

ESAF

GV

Utk

ars

h

Gross Loan Portfolio (Rs Bn)

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 4 of 63

Exhibit 9: Evolution of industry key metrics in the last 4 years

FY12 FY13 FY14 FY15 FY16

Number of clients (mn) 14.8 13.4 16.5 22.6 32.5

Total loans disbursed (mn) NA 12.9 17.6 25.5 34.7

Total loan amount disbursed (Rsbn) NA 158.1 236.8 376.0 618.6

Number of employees ('000) 49.0 42.2 48.1 62.4 85.9

Number of loan officers ('000) 30.2 26.8 30.1 38.9 53.8

Gross AUM 111.8 116.4 171.0 289.4 53.2

Average loan outstanding per client (Rs '000) 7.5 8.7 10.4 12.8 16.4

Average loan disbursed per account NA 12.2 13.4 14.7 17.8

Average clients per branch 2,135 2,161 2,415 2,851 3,358

Average GLP per branch (Rsmn) 16.1 18.8 25 36.5 55.1

Average client per loan officer 491 501 549 582 603

Average GLP per loan officer (Rsmn) 3.7 4.3 5.7 7.4 9.9

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 5 of 63

Exhibit 10: State-wise key indicators for Microfinance industry

States MFI count GLP (Rsbn)

Loan amount

disbursed (Annual,

Rsbn)

Loan disbursed

(Annual, mn)

Average amount

disbursed per

account ('000)

Clients (lakhs) Branches Employees

Tamil Nadu 19 86.87 102.65 5.51 18.63 5.65 1,352 12,665

Karnataka 24 71.65 90 6.253 14.39 3.823 1,198 11,475

Maharashtra 32 63.29 79.42 4.416 17.98 3.711 1,174 10,224

Uttar Pradesh 19 56.45 67.58 3.176 21.28 3.127 988 8,717

Madhya Pradesh 27 40.84 49.73 2.571 19.34 2.805 984 7,494

Odisha 13 31.41 41.68 2.497 16.69 2.135 510 4,525

West Bengal 14 30.75 43.79 2.605 16.81 2.191 643 5,541

Bihar 21 29.21 39.2 2.199 17.83 1.931 629 5,087

Kerala 10 24.34 31.02 1.734 17.89 1.223 350 3,630

Gujarat 19 20.64 22.41 0.977 22.94 1.234 433 3,360

Rajasthan 14 12.59 16.2 0.835 19.40 0.754 217 1,990

Haryana 14 11.65 14.48 0.651 22.24 0.491 169 1,670

Punjab 10 9.88 13.42 0.645 20.81 0.562 128 1,199

Jharkhand 17 8.98 12.53 0.714 17.55 0.566 239 1,850

Chattisgarh 17 8.77 11.23 0.587 19.13 0.586 263 1,826

Assam 10 7.73 9.51 0.466 20.41 0.532 203 1,306

Uttarakhand 11 5.93 4 0.232 17.24 0.331 82 726

Delhi 8 5.82 6.17 0.222 27.79 0.556 41 1,370

Puducherry 10 1.93 2.29 0.114 20.09 0.122 18 176

Andhra Pradesh 5 0.78 2.13 0.129 16.51 0.115 361 2,135

Tripura 5 0.4 0.68 0.04 17.00 0.034 22 152

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 6 of 63

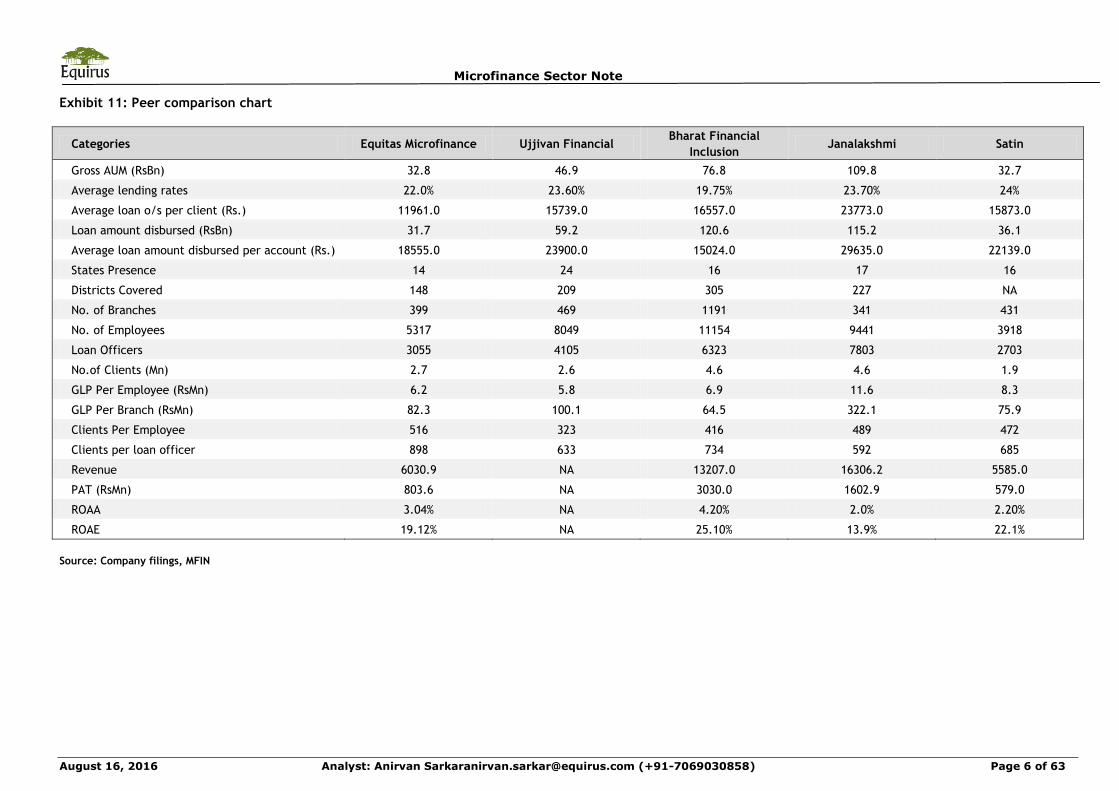

Exhibit 11: Peer comparison chart

Categories Equitas Microfinance Ujjivan FinancialBharat Financial

InclusionJanalakshmi Satin

Gross AUM (RsBn) 32.8 46.9 76.8 109.8 32.7

Average lending rates 22.0% 23.60% 19.75% 23.70% 24%

Average loan o/s per client (Rs.) 11961.0 15739.0 16557.0 23773.0 15873.0

Loan amount disbursed (RsBn) 31.7 59.2 120.6 115.2 36.1

Average loan amount disbursed per account (Rs.) 18555.0 23900.0 15024.0 29635.0 22139.0

States Presence 14 24 16 17 16

Districts Covered 148 209 305 227 NA

No. of Branches 399 469 1191 341 431

No. of Employees 5317 8049 11154 9441 3918

Loan Officers 3055 4105 6323 7803 2703

No.of Clients (Mn) 2.7 2.6 4.6 4.6 1.9

GLP Per Employee (RsMn) 6.2 5.8 6.9 11.6 8.3

GLP Per Branch (RsMn) 82.3 100.1 64.5 322.1 75.9

Clients Per Employee 516 323 416 489 472

Clients per loan officer 898 633 734 592 685

Revenue 6030.9 NA 13207.0 16306.2 5585.0

PAT (RsMn) 803.6 NA 3030.0 1602.9 579.0

ROAA 3.04% NA 4.20% 2.0% 2.20%

ROAE 19.12% NA 25.10% 13.9% 22.1%

Source: Company filings, MFIN

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 7 of 63

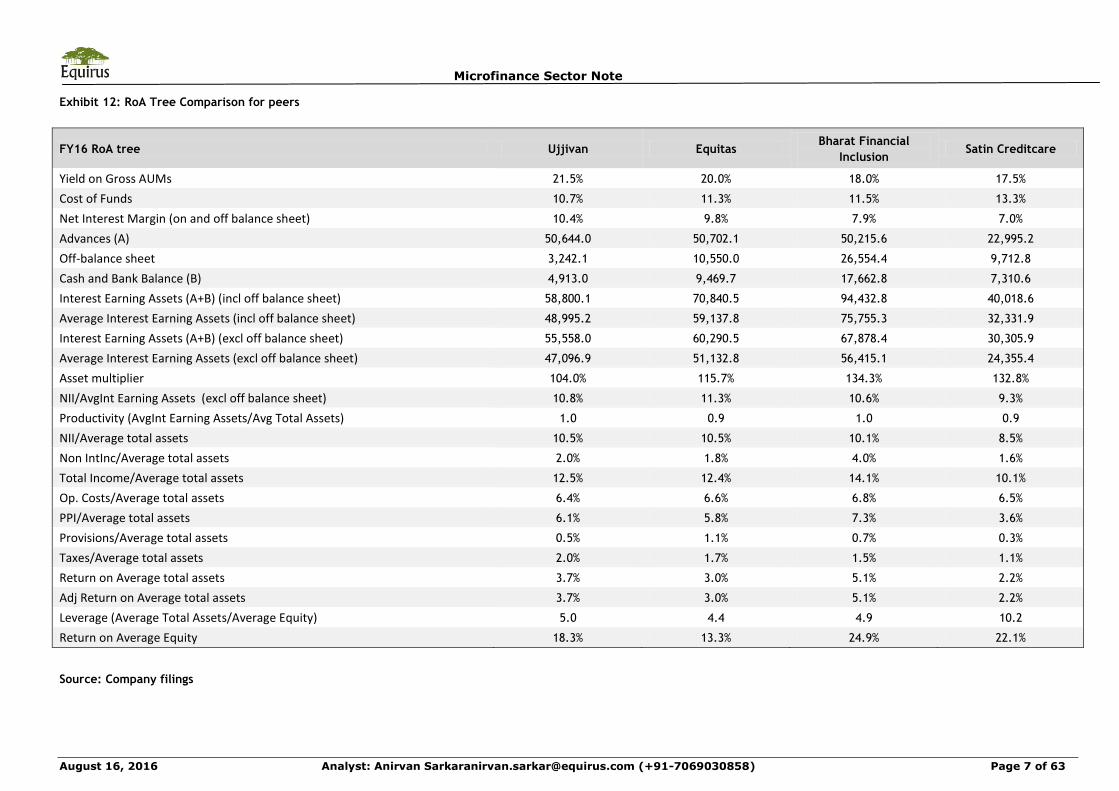

Exhibit 12: RoA Tree Comparison for peers

FY16 RoA tree Ujjivan EquitasBharat Financial

InclusionSatin Creditcare

Yield on Gross AUMs 21.5% 20.0% 18.0% 17.5%

Cost of Funds 10.7% 11.3% 11.5% 13.3%

Net Interest Margin (on and off balance sheet) 10.4% 9.8% 7.9% 7.0%

Advances (A) 50,644.0 50,702.1 50,215.6 22,995.2

Off-balance sheet 3,242.1 10,550.0 26,554.4 9,712.8

Cash and Bank Balance (B) 4,913.0 9,469.7 17,662.8 7,310.6

Interest Earning Assets (A+B) (incl off balance sheet) 58,800.1 70,840.5 94,432.8 40,018.6

Average Interest Earning Assets (incl off balance sheet) 48,995.2 59,137.8 75,755.3 32,331.9

Interest Earning Assets (A+B) (excl off balance sheet) 55,558.0 60,290.5 67,878.4 30,305.9

Average Interest Earning Assets (excl off balance sheet) 47,096.9 51,132.8 56,415.1 24,355.4

Asset multiplier 104.0% 115.7% 134.3% 132.8%

NII/AvgInt Earning Assets (excl off balance sheet) 10.8% 11.3% 10.6% 9.3%

Productivity (AvgInt Earning Assets/Avg Total Assets) 1.0 0.9 1.0 0.9

NII/Average total assets 10.5% 10.5% 10.1% 8.5%

Non IntInc/Average total assets 2.0% 1.8% 4.0% 1.6%

Total Income/Average total assets 12.5% 12.4% 14.1% 10.1%

Op. Costs/Average total assets 6.4% 6.6% 6.8% 6.5%

PPI/Average total assets 6.1% 5.8% 7.3% 3.6%

Provisions/Average total assets 0.5% 1.1% 0.7% 0.3%

Taxes/Average total assets 2.0% 1.7% 1.5% 1.1%

Return on Average total assets 3.7% 3.0% 5.1% 2.2%

Adj Return on Average total assets 3.7% 3.0% 5.1% 2.2%

Leverage (Average Total Assets/Average Equity) 5.0 4.4 4.9 10.2

Return on Average Equity 18.3% 13.3% 24.9% 22.1%

Source: Company filings

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 8 of 63

Ujjivan is the 4th largest microfinance company in India by total gross AUM,

and the 3rd largest by gross microfinance AUM, enjoys better geographical

spread

With a total Gross AUM of Rs. 53.9bn (microfinance AUM of Rs 46.9bn) as of Mar ‘16,

Ujjivan is the 4rd largest NBFC-MFI in India behind Bharat Financial Inclusion Ltd,

Janalakshmi Financial Services and Equitas Holdings. In terms of microfinance portfolio

gross AUM, Ujjivan ranks 3rd, as Equitas holdings has a smaller microfinance portfolio and

a larger individual lending portfolio.

While Equitas and Bharat Financial Inclusion have a larger branch network than Ujjivan,

the latter has a more diversified presence across more states and UTs compared to the

other 2. As of Mar’16, Equitas has 549 branches across 14 states/UTs, BFIL has 1,191

branches across 19 states and 329 districts, and Janalakshmi has 341 branches across 17

states. Compared to them, Ujjivan has 469 branches spread across 24 states and UTs.

While concentration risk is higher for the other companies, it does provide a strong

regional growth opportunity if they target the right areas of growth and execute well.

Bharat Financial Inclusion (BFIL) has higher RoA/RoE than Ujjivan, followed

by Equitas and Satin Creditcare

BFIL enjoys stronger other income profile than Ujjivan, Equitas and Satin, and hence

higher RoA/RoE (5.1%/24.9% for BFIL compared to 3.7%/18.3% for Ujjivan, 3.0%/13.3% for

Equitas and 2.2%/22.1% for Satin). Satin has extremely high leverage for an NBFC-MFI, at

10.2x, compared to 4.9x for each of Ujjivan and BFIL and 4.4x for Equitas. Although

higher expenses in the next few years will bring down the RoA for Ujjivan and Equitas,

they have room for leverage growth as they transform into a bank, so RoE decline will be

protected.

Ujjivan has stronger other income and total income profile and higher cost efficiency

compared to Equitas and Satin and thus enjoys higher RoA/RoE. Satin has one of the

lowest RoAs among NBFC-MFIs (2.2%) in the peer group, owing to high costs (6.5% of avg

assets) and needs to gain cost efficiency in order to ramp up its return ratios.

While both Equitas and Ujjivan have started offering fee income products (insurance), it

will take time to build up and this is not a primary focus area for either of the

companies. Any positive surprise on this would boost returns even higher.

Exhibit 13: Comparison of FY16 RoA/RoE/leverage across companies

Source: Company filings, Equirus Research

0%

5%

10%

15%

20%

25%

30%

Ujjivan Equitas Bharat Financial Inclusion

Satin Creditcare

RoA RoE

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 9 of 63

Exhibit 14: Competitive scorecard for Equitas and Ujjivan

Category Ujjivan Equitas

BusinessMicrofinance will reman core business with 60% of gross AUMs in

microfinance by FY22E

Rapidly diversifying product mix to reduce microfinance to 20% of book by

FY22E

Transition so farIndividual loan book has grown on a low base, no proven track record

of scaling up individual loan book without breaching healthy NPA levels

Proven track record - has increased individual lending to 48% of book in

1QFY17 from 23.5% in FY13

Individual product focus

Lower, within individual loans they are focusing on both housing and

MSE. Lower ticket unsecured loans forms bulk of housing book,

enhancing asset quality risk

Higher, within individual lending focus is on UCV and MSE, with housing at

10% of total individual book and will not be a focus area.

Credit costs outlook

Credit costs will build up due to buildup of individual loan book and

change in recognition days but will remain lower than Equitas in the

near term

Credit costs will build up and will remain higher due to bigger individual

loan book and change in recognition days

Opex outlookOpex will increase with investments in branch infrastructure,

technology and people, will remain lower than Equitas

Opex will increase and will be higher than Ujivan because of more

investment in liability expansion

Deposit scale up

Will be slower than that of Equitas. 280 out of 550 will be bank

branches by FY17E, with no mention of physically separate locations

for liability expansion

Will gain quicker traction in deposit momentum as 412 out of 550 will be

bank branches and each bank branch will have a physically separate

liability premise in a nearby, more visible location

Return ratios RoA will pick up after FY18E and stabilize at ~1.9% RoA wwill pick up after FY18E and stabilize at ~1.8%

Risk reward

Risks are not diversified, any cyclical correction in microfinance will

obliterate the loan book. High valuations assume seamless transition

and do not factor in transition pains or cyclical sector correction

Risks getting rapidly diversified, individual lending growing and

microfinance dependence diminishing rapidly. High valuations assume

seamless transition and do not factor in transition painsSource: Equirus Securities

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 10 of 63

Microfinance: The road ahead

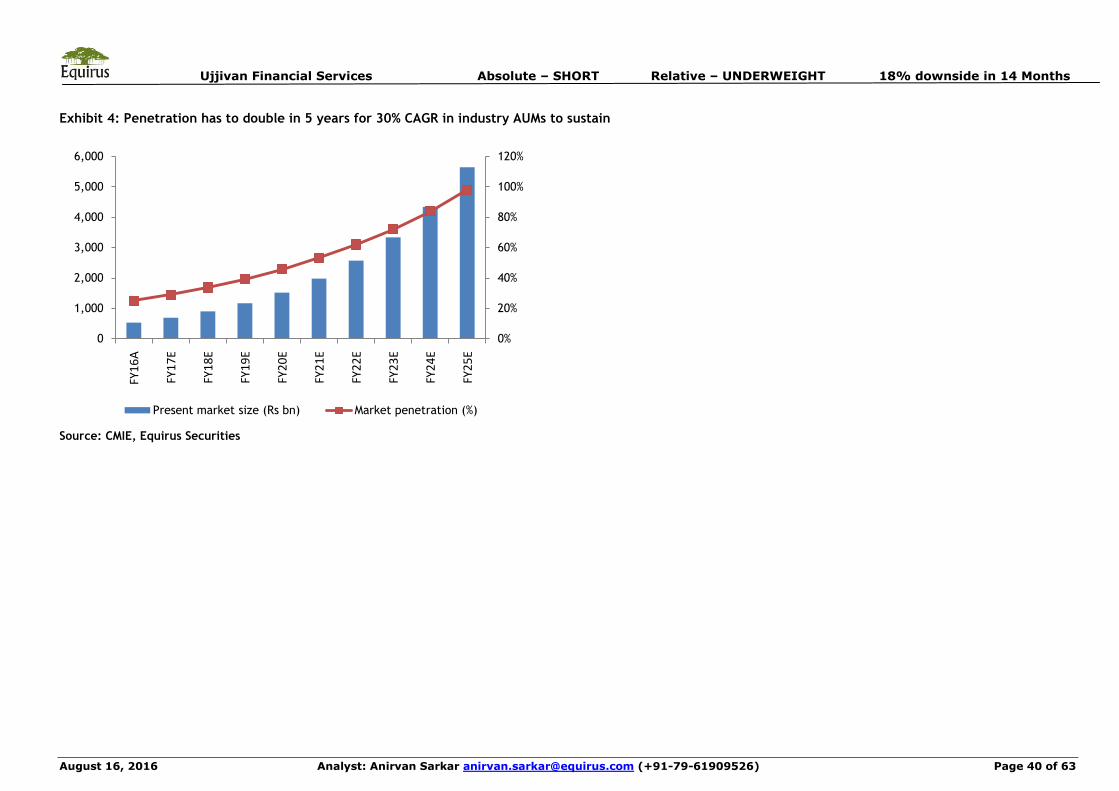

Addressable microfinance market is less than what headline numbers reflect, limiting

growth opportunities for pureplay microfinance companies: While microfinance is a

great business to replace the moneylender and provide access to organized sector

financing for economically weaker sections, the actual market which microfinance can

address in an economically viable manner is quite limited and not reflected by total

rural population. We take a look to analyze the actual addressable market and what

penetration it would take to sustain the present growth rates.

Exhibit 15 shows income distribution in India as of 2015. From the different income

groups shown, the maximum targetable households for microfinance in India are the

middle and low income groups, i.e. a total of 164mn households. Since microfinance

targets economically active women only, not all of these households can be targeted,

which further reduces the targetable market size. We assume ~75% of these households

constitute the target market for microfinance, which comes to ~120mn households.

Exhibit 15: Income distribution in India

Classification Monthly income (Rs '000) No of households (in mn)

Rich 93 2

High income 30 53

Middle income 13 82

Low income 7.5 82

Poor 3.5 56

Total 275

Source: CMIE report

The FY16 average ticket size for microfinance in India was Rs. 17.8K. We estimate that

sustainable healthy ticket size growth can be up to 10% per annum, marginally above GDP

growth rate and inflation. As shown in exhibit 16, for microfinance industry gross AUMs

to grow at 30% CAGR for the next 5 years, industry penetration would have to go up

from 25% in FY16 to 53% in FY21E and 72% in FY23E. This is not feasible for the

industry, as it needs expansion into remote areas where economies of scale cannot be

achieved. This implies that the growth spurt witnessed in the last few years cannot be

sustained. For urban and semi-urban focused companies like Ujjivan, growth would be

an additional challenge as a large part of the targetable market is based in rural India.

Exhibit 16: Increase in penetration with growth in MFI AUMs

FY16 FY17E FY18E FY19E FY20E FY21E FY22E FY23E

Total addressable households (mn)

120 122 124 125 127 129 131 133

Household growth

1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5%

Average ticket (Rs '000)

18 20 22 24 26 29 32 35

Addressable market (Rsbn)

2,137 2,386 2,663 2,974 3,320 3,707 4,139 4,621

Present market (Rsbn)

532 692 900 1,170 1,520 1,977 2,569 3,340

yoy growth 30% 30% 30% 30% 30% 30% 30%

Market penetration

25% 29% 34% 39% 46% 53% 62% 72%

Source: CMIE, MFIN, Equirus Securities

Microfinance crises in the past have been preceded by periods of aggressive growth

causing NPA spikes: India’s past microfinance crises (Karnataka (FY09) and A.P (FY10))

were preceded by periods of aggressive AUM growth, leading to overleveraging and

subsequent building up of uncontrollable NPAs. Post the A.P. crises, MFI AUM growth was

muted till FY13 post which MFI AUMs have grown at a 66% CAGR between FY13-FY16

fueled by equity infusion by PE/VC funds, and with increased investor interest in the

industry as well as banks entering into microfinance lending, this will lead to

overleveraging which will cause asset quality crisis.

Convergence of domains across banks and NBFC-MFIs, emergence of more diversified

businesses and Universal Banks: While SFBs like Ujjivan, Equitas, Satin, ESAF etc are

ramping up their individual lending products in an attempt to diversify their businesses

and position themselves as banks, large private sector banks such as Indusind Bank and

YES Bank have focused on growing their microfinance portfolio (not as a core business) in

view of the attractive RoAs in this segment. This indicates that the financial sector in

India is witnessing a convergence of domains across banks and NBFCs. This especially

holds for retail focused banks and retail NBFCs, housing finance companies, NBFC-MFIs

etc. This, however, increases asset quality risk in microfinance due to possible

overleveraging by customers due to oversupply of credit and information inefficiency.

This also introduces risks to profitability from possible price competition in a crowded

space which offers more choice to customers.

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 11 of 63

Twin impact of corporate lending asset quality disaster with Government’s Financial

Inclusion initiatives will encourage more universal banks: The increased focus of the

government on financial inclusion and bringing small scale industries under organized

sector financing has timed itself with rising NPAs in corporate banking. This leads to 2

things a) more banks shifting focus from corporate to retail and b) more banks/FIs

diversifying their retail lending portfolio to reduce product concentration risk. This will

lead to more banks/FIs re-positioning themselves as Universal Banks to avoid failures due

to stress on any one particular consumer segment.

NBFC-MFI recipients of SFB licenses risk not being able to scale up banking business:

In the light of NBFC-MFIs being granted SFB licenses, it should be noted that we have no

historical precedence of conversion of an NBFC-MFI to a bank. There remains a risk that

they fail to scale up deposits to counter the drop in yields with reduced cost of funds, in

which case returns will drop substantially. While we have been conservative with our

assumptions, we will revisit our thesis post more clarity on their deposit strategy and

visible traction.

Government initiatives expected to benefit Affordable housing and MSME

segments, positive for Ujjivan and Equitas who are expanding their individual

lending portfolio in these segments:

Government initiatives to encourage affordable housing:

The affordable housing industry in India has received a boost from the Credit

Linked Subsidy Scheme (CLSS) under the Pradhan Mantri AwasYojana (PMAY).

Under CLSS, customers from the EWS and LIG categories purchasing homes

having carpet area within 30 sqm (EWS) and 60 sqm (LIG) would be given a

subsidy of Rs. 0.22mn.

PMAY allows 100% tax deduction for builder profits from housing projects for

flats up to 30 sqm. in 4 metro cities and 60 sqm. in other cities during Jun’16 –

Mar’19 and completed within 3 years of approval (Minimum Alternate Tax is still

applicable).

First time home buyers are allowed an additional Rs. 50K of interest deduction

from income tax for loans up to Rs. 3.5mn sanctioned during FY17, provided the

home value is within Rs. 5mn.

Under section 87A of IT Act, the tax rebate limit is raised from Rs. 2,000 to Rs.

5,000 for tax payers with income of up to Rs. 0.5mn. This move will benefit

20mn tax payers in this category.

The house rent rebate has been raised from Rs. 24K to Rs. 60K under section

80GG which will benefit people staying in rented accommodation.

Our channel checks indicate that the implementation of CLSS has been swift, and housing

finance companies as well as banks have seen a surge in demand driven by the scheme.

However, due to supply shortage in urban areas/Tier 1/metro cities, housing finance

providers in Tier 2/3 cities and sub-urban areas would benefit the most from the

increased demand.

Multiple tax incentives for the MSME segment to encourage “Make in India”:

Under section 44AD of Income Tax Act, MSME units having gross receipts of up to

Rs. 20mn (earlier limit was Rs. 10mn) don’t need to maintain detailed books of

accounts and get them audited. This will benefit 3.5mn MSME units.

Under the same Income tax section, the gross receipt limit for professionals has

been raised from the existing level of Rs. 2.5mn to Rs. 5mn to be exempt from

account keeping and audit.

On taxation, income tax rate for an MSME unit whose turnover does not exceed

Rs. 50mn, has been lowered to 29% from 30%.

As part of ‘Make in India Program’, start-up unit profits will be tax exempt for 3

out of 5 years during Apr’16 to Mar’21

Capital gains will not be taxed if invested in regulated / notified funds even if

invested by individuals in notified start-ups.

Suitable changes have been made in customs and excise duty structure on

certain inputs, raw materials, intermediaries and components to reduce costs

and improve competitiveness. These moves are expected to encourage more

capacity expansion and job creation in this segment.

Encouraging data for used and new commercial vehicle financing from top 8

companies a positive for Equitas which is building its portfolio in this

segment:

Data for 8 CV financiers in India from 2008 – 16

Growth: While new CV AUM has grown at a CAGR of 9%, used CV financing has

grown at a CAGR of 22%. In FY16 New CV grew by 14% and used CV grew by 19%.

Over this period UCVs have grown consistently whereas NCV has seen some

volatility.

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 12 of 63

Lending rate: Lending rate for new vehicles in FY15 and 1HFY16 stood at 11.3%

for MHCV and 13.5% for LCVs. For used vehicle lending rate has remained largely

unchanged at 15.4% for used MHCVs and 16.5% for used LCV’s.

LTV: LTV in used CV is 77% for both MHCV and LCV. Average tenure in used

MHCV and LCV segments is 31 months

Improvement in asset quality and recovery/upgradations in the CV segment:

The percentage of repossessed vehicles being released back to customers on

payment of dues has increased to 50-60% compared to 20-30% at peak stress

levels. Time taken to sell the vehicle after repossession has also come down to

15-45 days from 45-90 days earlier.

Delinquency level in used CV segment for 90+ dpd and 180+ dpd are at 6.7% and

2.3% in Mar’16 compared with 7.3% and 2.2% as on Mar’15.

Jharkhand, Bihar, Goa and Puducherry have been impacted by mining related

issues are performing weaker compared to other states. Maharashtra and MP are

also performing weak where financiers have good presence due to drought

situation. Delhi also seems to be performing weak.

Flow Rate analysis carried out in respect to 4,500 contracts that were more than

180 days overdue (as on Sept 30th, 2015) says that in 65% of cases either the

account has been fully resolved (11% of cases) or borrower has paid some

amount despite slipping by more than 6 EMIs in past. In 30% of cases the

contract continues to be in 180 dpd bucket as the overdue amount has not yet

come down; however, borrower is making 1 full EMI payment regularly. In 20% of

cases, the borrower has paid some amount but not paid full EMI amount.

Average loss incurred by financiers at the time of vehicle sale in MHCV segment

has increased by 48% in FY14. However, loss levels have come down to 35% in

1HFY16. Loss level continues to remain high in LCV segment at average loss of

46% in 1HFY16.

Microfinance Sector Note

August 16, 2016 Analyst: Anirvan [email protected] (+91-7069030858) Page 13 of 63

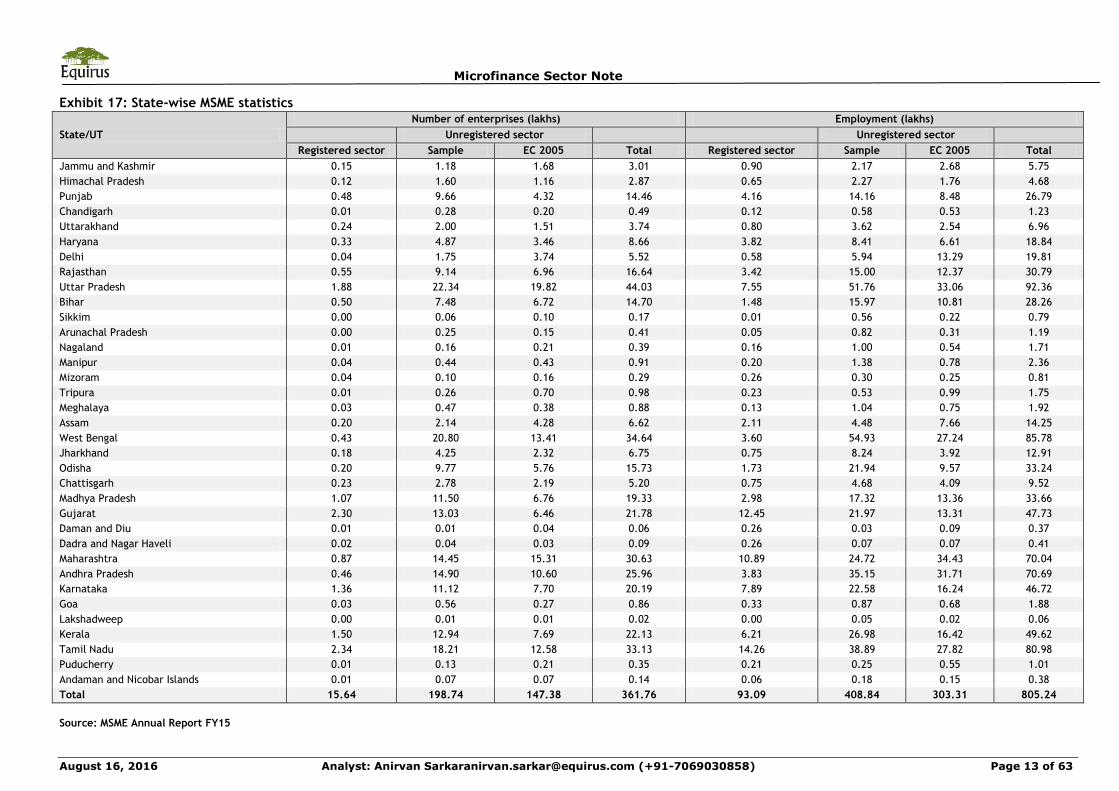

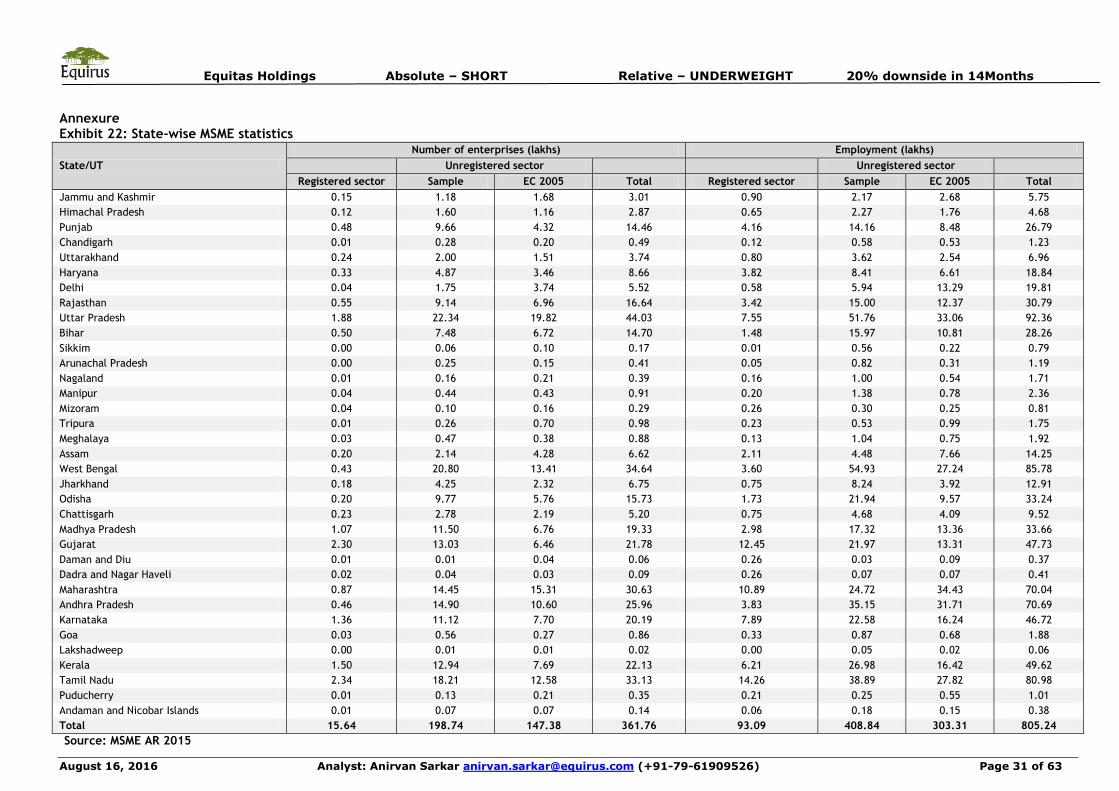

Exhibit 17: State-wise MSME statistics

State/UT

Number of enterprises (lakhs) Employment (lakhs)

Unregistered sector Unregistered sector

Registered sector Sample EC 2005 Total Registered sector Sample EC 2005 Total

Jammu and Kashmir 0.15 1.18 1.68 3.01 0.90 2.17 2.68 5.75

Himachal Pradesh 0.12 1.60 1.16 2.87 0.65 2.27 1.76 4.68

Punjab 0.48 9.66 4.32 14.46 4.16 14.16 8.48 26.79

Chandigarh 0.01 0.28 0.20 0.49 0.12 0.58 0.53 1.23

Uttarakhand 0.24 2.00 1.51 3.74 0.80 3.62 2.54 6.96

Haryana 0.33 4.87 3.46 8.66 3.82 8.41 6.61 18.84

Delhi 0.04 1.75 3.74 5.52 0.58 5.94 13.29 19.81

Rajasthan 0.55 9.14 6.96 16.64 3.42 15.00 12.37 30.79

Uttar Pradesh 1.88 22.34 19.82 44.03 7.55 51.76 33.06 92.36

Bihar 0.50 7.48 6.72 14.70 1.48 15.97 10.81 28.26

Sikkim 0.00 0.06 0.10 0.17 0.01 0.56 0.22 0.79

Arunachal Pradesh 0.00 0.25 0.15 0.41 0.05 0.82 0.31 1.19

Nagaland 0.01 0.16 0.21 0.39 0.16 1.00 0.54 1.71

Manipur 0.04 0.44 0.43 0.91 0.20 1.38 0.78 2.36

Mizoram 0.04 0.10 0.16 0.29 0.26 0.30 0.25 0.81

Tripura 0.01 0.26 0.70 0.98 0.23 0.53 0.99 1.75

Meghalaya 0.03 0.47 0.38 0.88 0.13 1.04 0.75 1.92

Assam 0.20 2.14 4.28 6.62 2.11 4.48 7.66 14.25

West Bengal 0.43 20.80 13.41 34.64 3.60 54.93 27.24 85.78

Jharkhand 0.18 4.25 2.32 6.75 0.75 8.24 3.92 12.91

Odisha 0.20 9.77 5.76 15.73 1.73 21.94 9.57 33.24

Chattisgarh 0.23 2.78 2.19 5.20 0.75 4.68 4.09 9.52

Madhya Pradesh 1.07 11.50 6.76 19.33 2.98 17.32 13.36 33.66

Gujarat 2.30 13.03 6.46 21.78 12.45 21.97 13.31 47.73

Daman and Diu 0.01 0.01 0.04 0.06 0.26 0.03 0.09 0.37

Dadra and Nagar Haveli 0.02 0.04 0.03 0.09 0.26 0.07 0.07 0.41

Maharashtra 0.87 14.45 15.31 30.63 10.89 24.72 34.43 70.04

Andhra Pradesh 0.46 14.90 10.60 25.96 3.83 35.15 31.71 70.69

Karnataka 1.36 11.12 7.70 20.19 7.89 22.58 16.24 46.72

Goa 0.03 0.56 0.27 0.86 0.33 0.87 0.68 1.88

Lakshadweep 0.00 0.01 0.01 0.02 0.00 0.05 0.02 0.06

Kerala 1.50 12.94 7.69 22.13 6.21 26.98 16.42 49.62

Tamil Nadu 2.34 18.21 12.58 33.13 14.26 38.89 27.82 80.98

Puducherry 0.01 0.13 0.21 0.35 0.21 0.25 0.55 1.01

Andaman and Nicobar Islands 0.01 0.07 0.07 0.14 0.06 0.18 0.15 0.38

Total 15.64 198.74 147.38 361.76 93.09 408.84 303.31 805.24

Source: MSME Annual Report FY15

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 14 of 63 Before reading this report, you must refer to the disclaimer on the last page.

Equitas Holdings Absolute : SHORT

Relative : UNDERWEIGHT

Initiating Note Regular Coverage 20% downside in 14 months

Perfectly positioned to leverage quality growth across verticals, rich valuations leave room for near term correction, initiate with SHORT

Financials

© 2016 Equirus All rights reserved

Rating Information

Price (Rs) 176

Target Price (Rs) 142

Target Date 30-Sep-17

Target Set On 16-Aug-16

Implied yrs of growth (ERE) 20

Fair Value (ERE) 141

Fair Value (DDM) NA

Ind Benchmark BANKEX

Model Portfolio Position NA

Stock Information

Market Cap (Rs mn) 59,109.8

Free Float (%) 100%

52 Wk H/L (Rs) 206.25/134.15

Avg Daily Volume (1yr) 63,88,685.1

Avg Daily Value (1yr) 1,061.7

Equity Cap (Rs Mn) 3,353.7

Face Value (Rs) 10.0

Bloomberg Code EQUITAS IN

Ownership Recent 3M 12M %

Promoters 0.00% 0.0% 0.0%

DII 29.3% 0.0% 0.0%

FII 48.1% 0.0% 0.0%

Public 22.6% 0.0% 0.0%

Price % 1M% 3M% 12M%

Absolute -0.5% 17.3% NA

Vs Industry -0.9% 2.8% NA

UJJIVAN 11.5% 74.7% NA

BHARATFIN 2.6% 25.2% 45.3%

Consolidated Quarterly EPS forecast

Rs/Share 1Q 2Q 3Q 4Q

EPS (16A) - - - -

EPS (17E) 1.9 1.6 1.7 1.8

Equitas Holdings is the 4th largest Indian microfinance company with ~8% market share

and microfinance Gross AUM of Rs. 32.8bn as of 4QFY16. We expect them to benefit

from sustainable quality growth in both group and individual lending portfolios to

attain 30% CAGR in total Gross AUM from FY16 to FY22E on the back of regional

presence across flourishing markets in India. However, the stock is trading at 2.7x

FY17E P/ABV and we believe the robust growth prospects, sturdy asset quality and

solid strategy are priced in the CMP, but near-term uncertainties on bank transition

and profitability are not. We believe the stock will correct in the near-term and

initiate coverage with a SHORT rating, arriving at ERoE based Sep’17 TP of Rs. 142

implying 20 years of growth with average RoE of 15.5% and cost of equity of 14.4%.

Branch concentration in the right states will support robust growth in next 5 years:

Equitas has ~83% of its 572 branches in states like TN, Mah, Kar, Raj and MP which

contribute to 88% of Gross AUMs. There is a flourishing market in microfinance,

affordable housing, used CV financing and MSME financing in these states. They are

converting 412 existing branches to bank branches, which will help them scale up

deposit base and maintain return ratios during the transition phase. We expect

Equitas’ Gross/Net AUMs to reach Rs. 300.4bn/284.7bn by FY22E and their deposit

base to reach 40% of total loans and advances, i.e. Rs. 113.9bn by FY22E.

Asset quality will remain sound backed by stringent credit quality monitoring and

controlled ticket size: Equitas’ GNPA/NNPA ratios are 1.61%/1.14% for the total

portfolio. While the microfinance business enjoys low GNPA/NNPA of 0.23%/0.05%, the

UCV/MSE and housing finance portfolios have GNPA/NNPA of 2.94%/2.19% and

5.54%/4.90% respectively. During transition to bank, NPAs are expected to grow due to

reduction of recognition days from 150 to 90. Given low Portfolio At Risk (PAR) for the

industry in Equitas’s states of presence, low ticket size and stringent risk management

practices, asset quality should improve after initial bumps.

Reducing dependence on microfinance a positive, proven track record in scaling up

MSE/UCV financing business ensures transition into more diversified asset base:

While Equitas has steadily reduced dependence on microfinance, their individual loan

book growth will be boosted by multiple government initiatives, such as CLSS under

PMAY, lack of organized players in UCV financing and enhanced MSME tax incentives.

Key Risks relate to slower scale up in deposit base and regulatory pressure in

microfinance: The fixed deposit market is hyper competitive and scale up of deposits

to 40% of total loans could face challenges. Regulatory clampdown remains a risk for

microfinance companies.

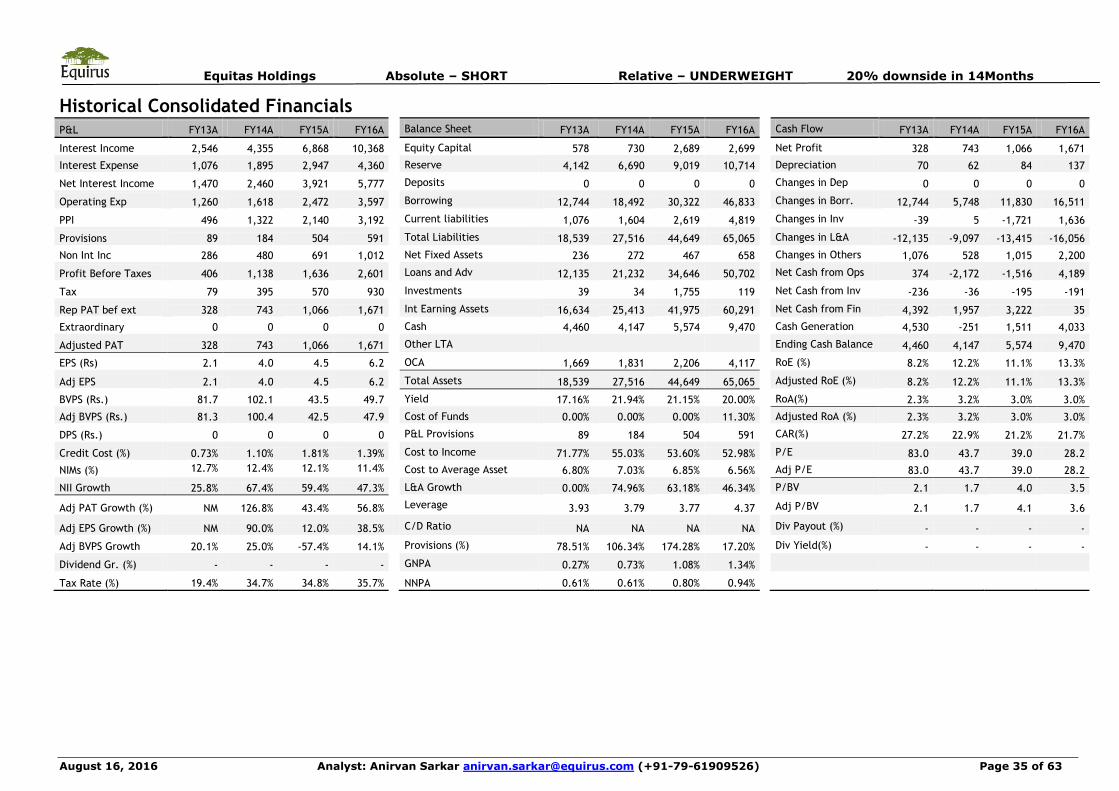

Consolidated Financials

Rs. Mn YE Mar FY16A FY17E FY18E FY19E

Interest Income 10,368 14,013 17,791 21,352

Interest Expense 4,360 5,413 6,949 8,634

Net Interest Inc. 5,777 8,599 10,842 12,718

Other Income 1,012 1,675 2,457 3,101

Operating Exp 3,597 5,753 8,644 9,966

Provisions 591 889 1,657 2,181

PAT 1,671 2,346 1,948 2,387

Loan and Advances 50,702 68,544 84,194 1,07,670

Deposits 0 6,854 12,629 26,917

Net Worth 13,414 22,754 24,703 27,090

NIM 11.40% 9.87% 9.47% 8.93%

Credit Cost 1.39% 1.49% 2.17% 2.27%

Rs Per Share FY16A FY17E FY18E FY19E

EPS 6.2 7.0 5.8 7.1

Adjusted EPS 6.2 7.0 5.8 7.1

Book Value 50 68 74 81

Adjusted BVPS 48 65 68 74

DPS 0 0 0 0

P/B (x) 3.5x 2.6x 2.4x 2.2x

Adj P/B (x) 3.7x 2.7x 2.6x 2.4x

Adj ROE (%) 13.31% 12.97% 8.21% 9.22%

RoA (%) 3.05% 2.71% 1.59% 1.53%

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 15 of 63

Company Snapshot

How we differ from Consensus

- Equirus Consensus % Diff Comment

EPS FY17E 7.0 5.8 22%

We are conservative in our assumptions

on loan growth and provisioning

expenses and hence our estimate for

FY18 PAT is 23% lower than that of the

street

FY18E 5.8 7.5 -23%

NII +

Other

Inc

FY17E 10,275 9,924 4%

FY18E 13,299 13,744 -3%

PAT FY17E 2,346 1,937 21%

FY18E 1,948 2,520 -23%

Our Key Investment arguments: Equitas will experience super-normal growth in the near

to medium term and we like their low dependence on microfinance, low ticket sizes and

robust risk management; High valuations are a concern and we initiate coverage with a

SHORT rating expecting near term correction in the stock price.

Key Assumptions 2016A 2017E 2018E 2019E 2020E

Yields on Advances (%) 20.0% 19.0% 18.3% 17.8% 17.5%

Yield on Investments (%) 12.3% 5.0% 7.2% 7.2% 7.2%

Cost of Funds (%) 11.3% 9.9% 9.9% 9.4% 9.1%

NIMs (%) 11.4% 9.9% 9.5% 8.9% 8.6%

NII Growth (%) 47.3% 48.8% 26.1% 17.3% 29.7%

PPI Growth (%) 49.2% 41.6% 2.9% 25.7% 41.1%

Credit costs (%) 1.4% 1.5% 2.2% 2.3% 2.2%

PAT Growth (%) 56.8% 40.4% -17.0% 22.5% 45.7%

Advances Growth (%) 46.3% 35.2% 22.8% 27.9% 43.2%

Deposit Growth (%) NA NA 84.2% 113.1% 71.8%

Key Risks: Delay in building deposit base, unfavorable political intervention.

Key Triggers: Execution and credit risk monitoring, positive news on scaling up advances

and deposits base

Sensitivity to Key Variables % Change % Impact on EPS

Net Interest Income 10 % 36.7 %

Provisioning Costs 10 % -3.8 %

ERoE Valuations & Assumptions

Rf Ke Term. Growth RoE in Terminal Yr

7.2% 14.4% 5.0% 18.2%

FY16A FY17-21E FY22-26E FY27-36E

NII Growth 47.3% 20.7% - -

NIM (%) 11.3% 10.0% - -

Adj EPS 6.2 9.1 26.8 101.9

Adj RoE (%) 13.3% 11.6% 16.6% 18.0%

-

Years of strong growth 1 5 10 20

Valuation as on date (Rs) 60 55 81 146

Valuation as of Mar’17 65 60 88 159

Our Sep’17 target price of Rs. 142 is based on ERoE valuation assuming 20 years of

growth, implying FY17E P/ABV multiple of 2.2x with an average RoE of 15.5%.

Company Description:

Incorporated in 2005, Equitas Financial Services Ltd (Equitas) is a Tamil Nadu

headquartered microfinance company which has been granted a small banking license by

RBI in 2015. The company offers Microfinance loans, housing loans, Used Commercial

Vehicle (UCV) loans and MSE loans. As on June 30th, 2016, the firm has a distribution

network of 572 branches across 14 states/UTs.

Comparable valuationMkt Cap Rs.

Mn.

Price

Target

Target

Date

EPS P/E BPS P/B RoE Div Yield

Company Reco. CMP FY16A FY17E FY18E FY16A FY17E FY18E FY16A FY17E FY16A FY17E FY18E FY16A FY17E

EQUITAS SHORT 176 59,110 142 Sep '17 6.2 7.0 5.8 28.5 25.2 30.4 47.9 2.7 13.3% 13.0% 8.2% 0.0% 0.5%

UJJIVAN SHORT 451 53,291 372 Sep '17 20.1 20.2 18.1 22.4 22.3 24.9 118.8 2.6 18.9% 13.8% 9.9% 0.1% 0.2%

BHAFIN NA 784 99,884 NA NA 23.9 44.5 50.9 33.0 17.6 15.4 108.6 4.9 24.9% 34.1% 25.9% 0.0% 0.4%

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 16 of 63

Investment Rationale

AUM growth to be helped by strategic concentration in high growth markets in Microfinance, MSE, UCV and affordable housing, conversion into bank branches will help build deposit momentum:

Equitas enjoys a large branch network concentrated in relatively fewer states. As of

Jun’16, the company had 572 branches across 12 states, 1 UT and Delhi. As of 4QFY16,

83% of their branches were concentrated in the top 5 states of TN, Karnataka,

Maharashtra, Rajasthan and M.P. and they contribute to 88% of total gross AUMs (refer

Exhibit 1).

Exhibit 1: Branch concentration coincides with AUM concentration

Source: Company Filings

Equitas has scaled up their individual lending portfolio which stands at ~48% of total gross

AUMs as of 1QFY17 compared to 23.5% in 4QFY13. The company aims to further reduce

microfinance to 30% of their gross AUMs by FY20E.

Within individual lending portfolio, UCV financing (52%) and MSE financing (40%)

contribute to 92% while housing finance constitutes 8% of individual book gross AUMs and

4% of total gross AUMs. Equitas’ primary focus is to grow its UCV and MSE segments to the

bulk of its total gross AUMs while housing finance will remain a smaller part of the total

portfolio. We estimate that by FY22E, the total gross AUMs will consist of 20% in MFI

loans, 75% in UCV and MSE, and 5% in housing finance.

Equitas has received approval from RBI to convert 412 of its branches to bank branches,

which should help deposit building momentum and help them maintain NIM and

profitability. However, scaling up deposits is a gradual process and we estimate that

Equitas will fund 40% of their loan book with deposits by FY22E.

1. Unambitious target for microfinance growth to be easily met due to

impressive Overlap with large Microfinance markets:

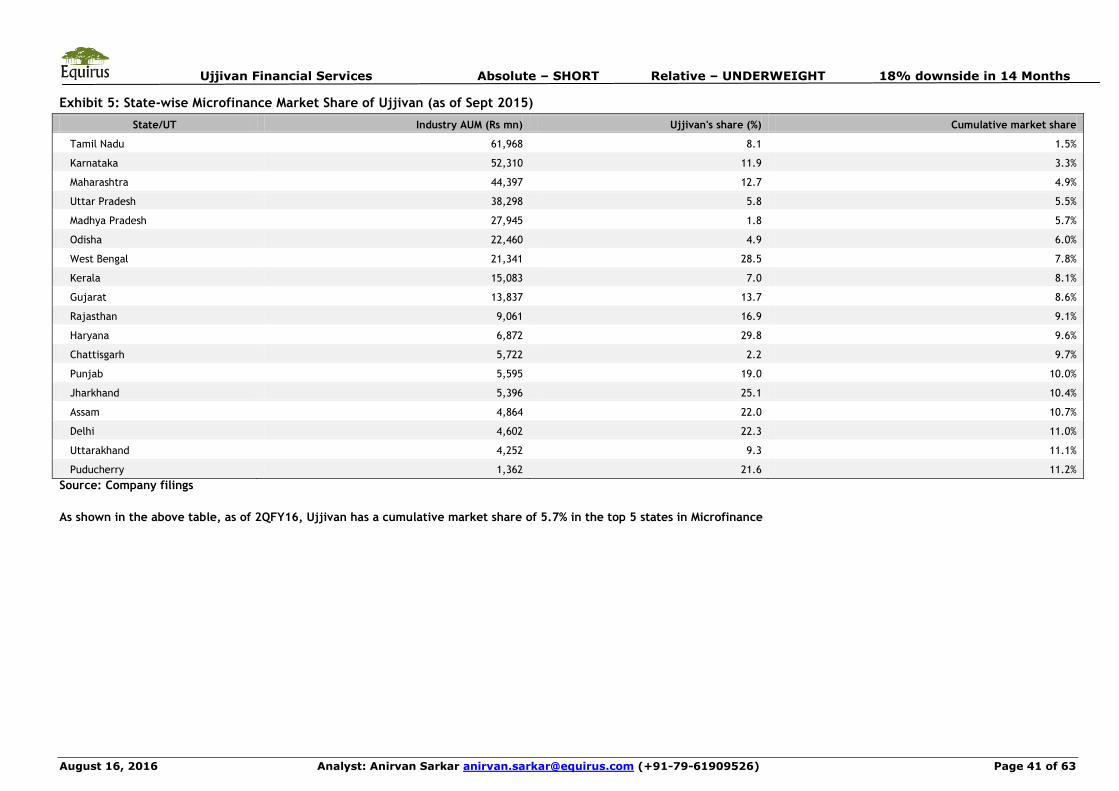

As of 31st March 2016, the top 5 states in India (by Microfinance Gross Loan Portfolio

(GLP)) accounted for 60% of total microfinance GLP in India. From exhibit 2, we see that

Equitas Microfinance has 87% of its MF AUMs concentrated in these 5 states, of which 61%

of is in Tamil Nadu, the largest Microfinance market in India. This strong overlap in focus

areas with the overall industry should help them achieve their targeted growth in their

MF portfolio.

Exhibit 2: Comparison of microfinance AUM distribution across states for Equitas vs. industry

States Percentage of total GLP Percentage of Equitas' GLP

Tamil Nadu 16% 61%

Karnataka 13% 7%

Maharashtra 12% 13%

Uttar Pradesh 11% 0%

Madhya Pradesh 8% 6%

Orissa 6% 0%

West Bengal 6% 0%

Bihar 5% 0%

Kerala 5% 0%

Gujarat 4% 0%

Others 14% 13%Source: Company Filings

We estimate that Equitas’ microfinance gross AUM will grow at 11% CAGR from FY16 –

FY22E to Rs. 60.1bn, in-line with the company’s target of gradually lowering the

microfinance share of the total book by diversifying into UCV, MSE and housing finance.

40.4%

17.3%

8.6%

8.4%

7.8%

6.9%

2.9%7.7%

Tamil Nadu Maharashtra Karnataka

Rajasthan MP Gujarat

Chhattisgarh Others

56.9%

14.8%

7.7%

3.9%

4.7%

4.1%

1.5%

6.4%

Branch concentration AUM concentration

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 17 of 63

Given their strong presence in microfinance hubs in India, this growth is an easily

achievable target.

Exhibit 3: Projected growth in Equitas’ Microfinance Gross AUMs

Source: Company, Equirus Research

2. MSE financing to be boosted by credit growth in the sector, branchand AUM concentration in MSE hubs and multiple tax initiatives byGOI towards “Make in India”

a) Concentrated branch network in MSE hubs in India, proven track record in

scaling up MSE financing provides comfort on ability to grow:

As shown in Exhibit 4, Equitas has 52% of its total MSE AUMs concentrated in the

top 5 states with the largest number of MSMEs. Tamil Nadu, the strongest hub of

Equitas is home to a flourishing MSME sector as the state ranks 3rd in terms of

number of enterprises as well as employment. Tamil Nadu ranks 2nd in terms of

total fixed assets of MSME sector, as shown in Exhibit 22 in annexure, the first

position being held by Gujarat where Equitas has an extensive network as well.

Equitas has already demonstrated its ability to scale up its MSE lending book as

MSE AUMs form 19% of total gross AUMs.

Exhibit 4: Equitas branch network and MSE financing book distribution in top states by number of enterprises

% of total MSME

enterprises

Equitas

branchesEquitas MSE financing AUM %

Uttar Pradesh 12% 0 0%

West Bengal 10% 0 0%

Tamil Nadu 9% 231 33%

Maharashtra 8% 96 19%

Andhra

Pradesh 7% 9 0%

Kerala 6% 0 0%

Gujarat 6% 39 6%

Karnataka 6% 50 11%

Madhya

Pradesh 5% 43 5%

Total 70% 468 74%

Source: MSME AR 2015, company filings

21,440.0

32,830.036,396.9 38,823.3

43,676.250,955.6

56,475.860,090.3

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

FY15A FY16A FY17E FY18E FY19E FY20E FY21E FY22E

Microfinance Gross AUM (Rs mn)

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 18 of 63

b) Multiple tax incentives for the MSME segment to encourage “Make in India”:

Under section 44AD of Income Tax Act, MSMEs having gross receipts of up to Rs.

20mn (earlier limit was Rs. 10mn) don’t need to maintain detailed books of

accounts and get them audited. This will benefit 3.5mn MSMEs.

Under the same Income tax section, the gross receipt limit for professionals has

been raised from the existing level of Rs. 2.5mn to Rs. 5mn to be exempt from

account keeping and audit.

On taxation, income tax rate for MSMEs whose turnover does not exceed Rs.

50mn, has been lowered to 29% from 30%.

As part of ‘Make in India Program’, start-up unit profits will be tax exempt for 3

out of 5 years during Apr’16 to Mar’21.

Capital gains will not be taxed if invested in regulated / notified funds even if

invested by individuals in notified start-ups.

Suitable changes have been made in customs and excise duty structure on

certain inputs, raw materials, intermediaries and components to reduce costs

and improve competitiveness. These moves are expected to encourage more

capacity expansion and job creation in this segment.

These incentives are expected to boost MSME growth in the country and will enhance financing needs, creating more opportunities for Equitas.

c) Bank credit growth points to healthy growth in MSE financing: Bank credit to

MSE segment has grown much more compared to medium and large enterprises

(Exhibit 5), reflecting that number of enterprises in this segment has grown and

hence the market opportunity for financiers is more for the micro and small

enterprises compared to medium.

We expect Equitas to grow its MSE AUMs at a 41% CAGR between FY17 and FY22E to reach

Rs. 98.1bn in gross MSE AUMs by FY22E

Exhibit 5: Growth in Bank credit to MSME sub-segments

Rs million Mar'08 Mar'09 Mar'10 Mar'11 Mar'12 Mar'13 Mar'14 Mar'15

Micro & Small enterprises

1,327 1,690 2,064 2,102 2,367 2,843 3,482 3,800

yoy growth NA 27% 22% 2% 13% 20% 22% 9%

Medium enterprises 1,108 1,222 1,326 1,165 1,248 1,247 1,241 1,245

yoy growth NA 10% 9% -12% 7% 0% -1% 0%

Total 2,435 2,912 3,390 3,267 3,614 4,091 4,723 5,046

Source: RBI

Exhibit 6: Projected growth in Equitas’s MSE gross AUMs

Source: Equirus Research, company filings

17,610.723,246.1

31,171.0

48,077.2

68,861.4

98,127.5

0.0

20,000.0

40,000.0

60,000.0

80,000.0

1,00,000.0

1,20,000.0

FY17E FY18E FY19E FY20E FY21E FY22E

MSE gross AUMs (Rs mn)

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 19 of 63

3. Used commercial vehicles has a huge potential market dominated by

informal financiers, UCV financing at 25% of total gross AUMs

provides comfort on ability to scale up business:

Market dominated by informal financiers provides easy growth for Equitas,

proven track record in UCV financing growth provides comfort on ability to

grow AUMs: The used commercial vehicle (UCV) market in India is dominated by

the unorganized sector which dominates 55% of the market, with the only

organized sector participation coming from Shriram City Union Finance, TATA

OK, Tata Motors Assured and Eicher Sure. This leaves a vast opportunity for the

organized sector. Equitas has grown its UCV financing gross AUMs to Rs. 16.15bn

(25% of total gross AUMs) in 1QFY17. Their extensive presence in Tamil Nadu will

help them since the only significant local competition is from Shriram City Union

Finance, and informal financiers provide an easy way of growing market share.

The entry barrier in this segment is high, with dealer network establishment

being the prime criteria for gaining business traction, so we expect healthy

growth by taking market share from informal financiers.

UCV financing growth has been more consistent compared to new CV

financing: Data from 8 CV financiers from 2008 – 2016 shows that while new CV

AUM has grown at a CAGR of 9%, used CV financing has grown at a CAGR of 22%.

In FY16 New CV grew by 14% and Used CV grew by 19%. Even for the period

under consideration, UCVs have grown consistently whereas NCVs have seen

some volatility.

Moreover their recent initiative, Equitas Technologies Pvt. Ltd. provides freight

facilitation by connecting transport service providers to customers. This should

help them pick up traction in financing transporters and should further help UCV

portfolio growth. We expect Equitas to grow its UCV financing gross AUMs at a

41% CAGR between FY17E and FY22E to Rs. 127.3bn in FY22E

Exhibit 7: Expected Growth in UCV portfolio AUMs

Source: Equirus Research, company filings

22,844.430,154.6

40,434.6

62,365.2

89,326.2

1,27,289.9

0.0

20,000.0

40,000.0

60,000.0

80,000.0

1,00,000.0

1,20,000.0

1,40,000.0

FY17E FY18E FY19E FY20E FY21E FY22E

UCV gross AUMs (Rs mn)

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 20 of 63

4. Credit Linked Subsidy Scheme (CLSS) will drive affordable housinggrowth, extensive network in states with projects in progress willhelp housing book grow:

a) CLSS implementation boosting affordable housing growth, Equitas well-placed

to tap into the growth: Our channel checks indicate that the implementation of

CLSS under PMAY has been swift, and housing finance companies as well as

banks have seen a surge in demand driven by the scheme. While housing is not a

core part of their portfolio and Equitas will continue to focus more on other

products, their housing finance business stands to benefit from this housing

boom.

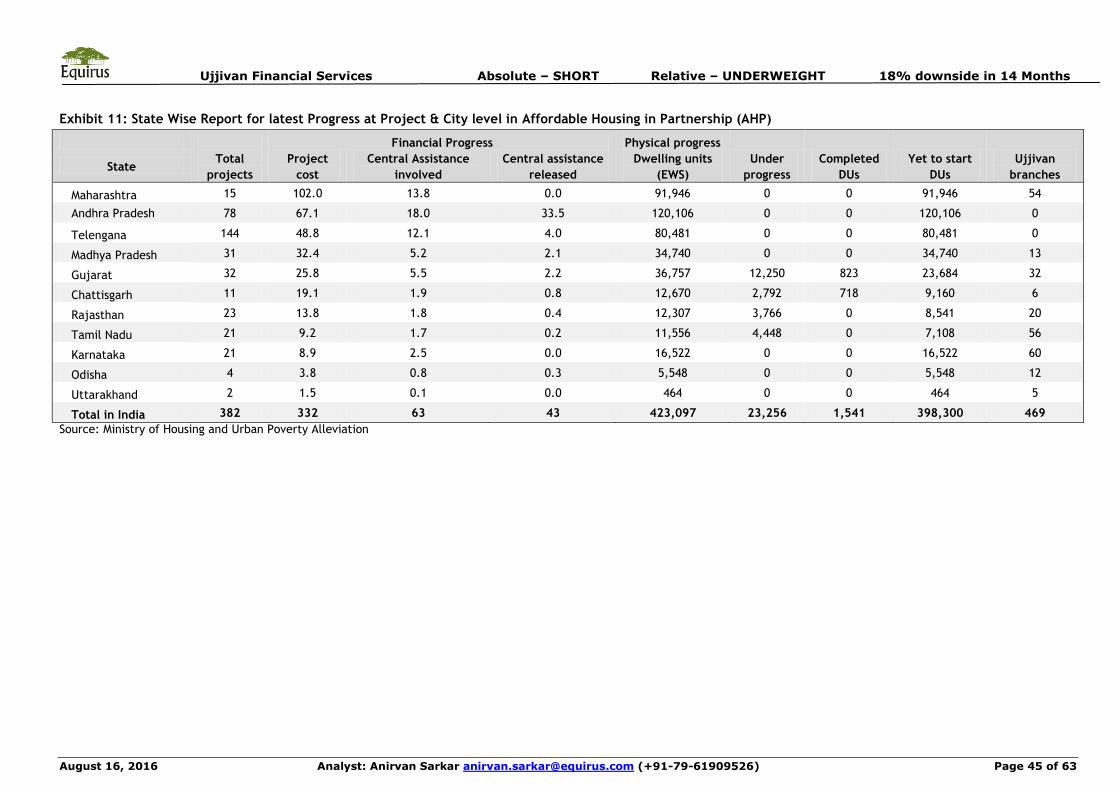

b) Strong presence in states with in-progress affordable housing projectsprovides first mover advantage:

As shown in Exhibits 8 and 9, Equitas enjoys a good branch network in the top 10

states where affordable housing in partnership (AHP) under PMAY has taken off,

as well as the states where projects under Beneficiary Led Construction Scheme

(BLCS) have started. The strategic positioning places them in a sweet spot to

cater to increased housing finance demand in these states. Moreover, they have

15 branches in A.P. and Telengana, states with 35%/47% share in project

cost/number of projects in affordable housing in partnership. Larger MFIs other

than Bharat Financial have very limited or no presence in these 2 states, which

provides them no competition from the new MFI entrants looking to grow in

affordable housing. We estimate they will grow housing finance gross AUMs at a

35% CAGR between FY16-FY22E to Rs. 15bn in FY22E (~5% of total gross AUMs).

Exhibit 8: State-wise progress of affordable housing under AHP (Affordable Housing in Partnership)

Financial Progress Physical progress

StateTotal

projectsProject cost

Central Assistance

involved

Central assistance

released

Dwelling units

(EWS)

Under

progress

Completed

DUs

Yet to start

DUs

Equitas

branches

Maharashtra 15 102.0 13.8 0.0 91,946 0 0 91,946 95

Andhra Pradesh 78 67.1 18.0 3.3 120,106 0 0 120,106 9

Telengana 144 48.8 12.1 4.0 80,481 0 0 80,481 6

Madhya Pradesh 31 32.4 5.2 2.1 34,740 0 0 34,740 43

Gujarat 32 25.8 5.5 2.2 36,757 12,250 823 23,684 38

Chattisgarh 11 19.1 1.9 0.8 12,670 2,792 718 9,160 16

Rajasthan 23 13.8 1.8 0.4 12,307 3,766 0 8,541 46

Tamil Nadu 21 9.2 1.7 0.2 11,556 4,448 0 7,108 222

Karnataka 21 8.9 2.5 0.0 16,522 0 0 16,522 47

Odisha 4 3.8 0.8 0.3 5,548 0 0 5,548 0

Uttarakhand 2 1.5 0.1 0.0 464 0 0 464 1

Total in India 382 332 63 13 423,097 23,256 1,541 398,300 523

Source: Ministry of Housing and Urban Poverty Alleviation

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 21 of 63

Exhibit 9: State-wise progress of affordable housing under BLCS

Financial Progress Physical progress

StateTotal

projectsProject cost

Central Assistance

involved

Central assistance

released

Houses

involved

Under

progress

Completed

Houses

Yet to start

Houses

Equitas

branches

Maharashtra 2 3.3 1.1 0.0 7,399 0.0 0.0 7,399 95

Andhra Pradesh 32 38.7 11.0 0.0 73,041 0.0 0.0 73,041 9

Bihar 85 12.5 4.5 1.8 30,216 0.0 0.0 30,216 0

Madhya Pradesh 12 4.1 1.1 0.4 7,297 0.0 0.0 7,297 43

Mizoram 8 2.1 1.5 0.1 10,286 0.0 0.0 10,286 0

Himachal

Pradesh17 1.0 0.3 0.1 1,914 0.0 0.0 1,914 0

J&K 4 0.2 0.1 0.0 683 0.0 0.0 683 0

Jharkhand 38 7.3 3.0 1.2 20,239 0.0 0.0 20,239 0

Tamil Nadu 185 6.9 4.0 1.2 26,978 9,637 104 17,237 222

Kerala 14 2.6 1.3 0.0 9,299 0.0 0.0 9,299 0

Uttarakhand 19 0.8 0.3 0.1 2,293 0.0 0.0 2,293 1

West Bengal 108 30.3 11.2 0.9 74,880 6,888.0 0.0 67,992 0

Total in India 524 110 40 6 264,525 16,525 104 247,896 370

Source: Ministry of Housing and Urban Poverty Alleviation

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 22 of 63

Exhibit 10: Projected growth in Equitas’s Housing Gross AUMs

Source: Equirus Research, company filings

Exhibit 11: Gross AUM split – Individual lending will grow to 70% of total AUM by FY20E and 80% by FY22E

Source: Equirus Research, company filings

1,800.0 2,460.04,044.1 4,852.9

6,066.1

8,492.6

11,295.2

15,022.6

0

5,000

10,000

15,000

20,000

FY15A FY16A FY17E FY18E FY19E FY20E FY21E FY22E

Housing gross AUM (Rs mn)

45% 40% 36% 30% 25% 20%

28.2% 32.8% 35%36.7% 39.5% 42.4%

21.8% 25.3% 27.0% 28.3% 30.5% 32.7%

5% 2% 2% 5% 5% 5%

0%

20%

40%

60%

80%

100%

FY17E FY18E FY19E FY20E FY21E FY22E

Microfinance UCV MSE Housing

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 23 of 63

Asset quality will remain robust backed by stringent credit

quality monitoring and low microfinance ticket size, continuing

reduction in microfinance exposure and low dependence on

housing adds further comfort:

1. Housing portfolio NPAs are high but bulky exposures are limited, will remain

a miniscule portion of overall loan portfolio: Equitas’ housing finance portfolio

GNPA/NNPA stand at 3.89%/3.16% as of 1QFY17. Although this is a relatively high

number, half of the NPAs are contributed by 10-12 accounts of Rs. 5-10mn each.

Moreover, housing is not a core part of their strategy and hence housing finance

will remain a small part of their portfolio (FY22E ~5% of total gross AUMs).

2. Microfinance portfolio NPAs remain low, ticket sizes are among the lowest in

the industry, steadily reducing exposure to microfinance guards against

cyclical corrections: Within microfinance portfolio Equitas has maintained

excellent credit quality with 0.23%/0.05% GNPA/NNPA ratios in 1QFY17.

Although consolidated NPAs have increased in the last few quarters,

microfinance NPAs have remained steady at healthy levels (exhibit 12). At Rs.

21,974, Equitas has the one of the lowest average ticket size in microfinance

industry, and they don’t intend to increase microfinance ticket size significantly

above this level, which provides comfort on microfinance asset quality.

Moreover, as the company is on track to reduce microfinance exposure to 20% of

gross AUMs by FY22E, any cyclical corrections in the microfinance industry will

guard Equitas against NPAs spiking up.

3. UCV financing NPAs will stay in control, industry data shows encouraging

trends in asset quality improvement:

Data from 8 CV financiers shows that in FY16:

The percentage of repossessed vehicles being released back to customers on

payment of dues has increased to 50-60% compared to 20-30% at peak stress

levels.

Time taken to sell the vehicle after repossession has also come down to 15-45

days from 45-90 days earlier.

Delinquency level in used CV segment for 90+ dpd and 180+ dpd are at 6.7% and

2.3% on Mar’16 compared with 7.3% and 2.2% as on Mar’15.

Flow Rate analysis carried out in respect to 4,500 contracts that were more than

180 days overdue (as on Sept 30th, 2015) says that in 65% of cases either the

account has been fully resolved (11% of cases) or borrower has paid some

amount despite slipping by more than 6 EMIs in past. In 30% of cases the

contract continues to be in 180 dpd bucket as the overdue amount has not yet

come down; however, borrower is making 1 full EMI payment regularly. In 20% of

cases, the borrower has paid some amount but not paid full EMI amount.

Average loss incurred by financiers at the time of vehicle sale in MHCV segment

has increased by 48% in FY14. However, loss levels have come down to 35% in

1HFY16. Loss level continues to remain high in LCV segment at average loss of

46% in 1HFY16.

4. UCV NPA levels have increased largely due to change in recognition days,

underlying asset quality has shown improvement: Equitas’s UCV GNPA/NNPA

are at 4.06%/2.94% in 1QFY17 (exhibit 12). Between 4QFY15 and 1QFY17, NPAs

have increased qoq only in 1QFY16 and 1QFY17, on change in recognition days

from 180 days to 150 days respectively. In the other quarters, both GNPA and

NNPA have steadily declined, reflecting underlying improvement in asset

quality.

5. Strong systems, processes and due diligence guards against asset quality

deterioration even as NPAs build up further, real time updates guard against

cash frauds: Going ahead, Equitas’s NPAs are expected to build up further as

their UCV/MSE book shifts from 150 day recognition to a 120 day policy and then

to a 90 day recognition policy on conversion to a bank. This has already shown

signs of improvement, as the loss given default (LGD) in UCVs have reduced to

42%-43% in FY16 from 55% in FY15. The company provides incentives to loan

officers based on number of customers acquired and not on ticket sizes, which

reduces the propensity to aggressively mis-sell loans without necessary due

diligence. Equitas also very efficient collection mechanism involving individual

customer passbooks and sms updates that provides almost real-time updates,

guarding against cash frauds.

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 24 of 63

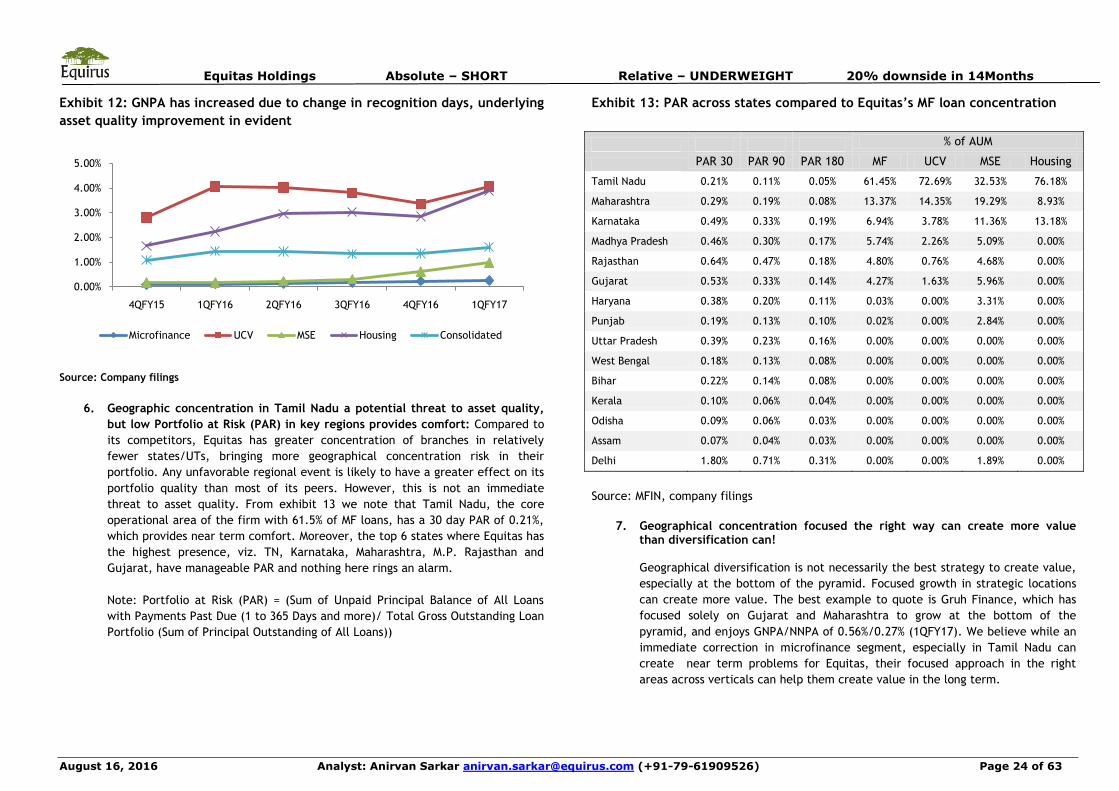

Exhibit 12: GNPA has increased due to change in recognition days, underlying

asset quality improvement in evident

Source: Company filings

6. Geographic concentration in Tamil Nadu a potential threat to asset quality,

but low Portfolio at Risk (PAR) in key regions provides comfort: Compared to

its competitors, Equitas has greater concentration of branches in relatively

fewer states/UTs, bringing more geographical concentration risk in their

portfolio. Any unfavorable regional event is likely to have a greater effect on its

portfolio quality than most of its peers. However, this is not an immediate

threat to asset quality. From exhibit 13 we note that Tamil Nadu, the core

operational area of the firm with 61.5% of MF loans, has a 30 day PAR of 0.21%,

which provides near term comfort. Moreover, the top 6 states where Equitas has

the highest presence, viz. TN, Karnataka, Maharashtra, M.P. Rajasthan and

Gujarat, have manageable PAR and nothing here rings an alarm.

Note: Portfolio at Risk (PAR) = (Sum of Unpaid Principal Balance of All Loans

with Payments Past Due (1 to 365 Days and more)/ Total Gross Outstanding Loan

Portfolio (Sum of Principal Outstanding of All Loans))

Exhibit 13: PAR across states compared to Equitas’s MF loan concentration

% of AUM

PAR 30 PAR 90 PAR 180 MF UCV MSE Housing

Tamil Nadu 0.21% 0.11% 0.05% 61.45% 72.69% 32.53% 76.18%

Maharashtra 0.29% 0.19% 0.08% 13.37% 14.35% 19.29% 8.93%

Karnataka 0.49% 0.33% 0.19% 6.94% 3.78% 11.36% 13.18%

Madhya Pradesh 0.46% 0.30% 0.17% 5.74% 2.26% 5.09% 0.00%

Rajasthan 0.64% 0.47% 0.18% 4.80% 0.76% 4.68% 0.00%

Gujarat 0.53% 0.33% 0.14% 4.27% 1.63% 5.96% 0.00%

Haryana 0.38% 0.20% 0.11% 0.03% 0.00% 3.31% 0.00%

Punjab 0.19% 0.13% 0.10% 0.02% 0.00% 2.84% 0.00%

Uttar Pradesh 0.39% 0.23% 0.16% 0.00% 0.00% 0.00% 0.00%

West Bengal 0.18% 0.13% 0.08% 0.00% 0.00% 0.00% 0.00%

Bihar 0.22% 0.14% 0.08% 0.00% 0.00% 0.00% 0.00%

Kerala 0.10% 0.06% 0.04% 0.00% 0.00% 0.00% 0.00%

Odisha 0.09% 0.06% 0.03% 0.00% 0.00% 0.00% 0.00%

Assam 0.07% 0.04% 0.03% 0.00% 0.00% 0.00% 0.00%

Delhi 1.80% 0.71% 0.31% 0.00% 0.00% 1.89% 0.00%

Source: MFIN, company filings

7. Geographical concentration focused the right way can create more valuethan diversification can!

Geographical diversification is not necessarily the best strategy to create value,

especially at the bottom of the pyramid. Focused growth in strategic locations

can create more value. The best example to quote is Gruh Finance, which has

focused solely on Gujarat and Maharashtra to grow at the bottom of the

pyramid, and enjoys GNPA/NNPA of 0.56%/0.27% (1QFY17). We believe while an

immediate correction in microfinance segment, especially in Tamil Nadu can

create near term problems for Equitas, their focused approach in the right

areas across verticals can help them create value in the long term.

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

4QFY15 1QFY16 2QFY16 3QFY16 4QFY16 1QFY17

Microfinance UCV MSE Housing Consolidated

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 25 of 63

Impact on margins due to transition to SFB will be limited; refinancing opportunities will help better asset liability management

Equitas is one of the 8 microfinance companies which were granted small banking

licenses by RBI in 2015. They aim to be operational by the 1QCY17, and RBI guidelines

mandate them to list the SFB separately within 3 years of commencement of operations.

Once Equitas transforms into a bank, they would be required to comply with SLR/CRR

guidelines by RBI, which are 21.25%/4% post the 9th August 2016 monetary policy

announcement. Their yields are expected to decline owing to lower yields on mandatory

regulatory assets. The company intends to reduce securitization going ahead.

1. Deposit traction will be quick with physical separation between asset and

liability divisions of 412 bank branches: Equitas has received RBI approval for

412 bank branches, which will mean 412 of their 572 branches will be converted

into bank branches, with a separate liability division in a nearby and more

visible location. This strategy will help gain quick traction on gathering deposits.

2. Drop in NIM will be limited even with cautious assumption on deposit

momentum and factoring in drop in yield on AUMs: Equitas’ deposit building

strategy is to garner a part of target deposit base from existing customers, and

raise wholesale deposits to fund the remaining. Post that, they intend to

refinance wholesale deposits with cheaper small ticket retail term deposits and

CASA which will bring the cost of funds further down.

We remain cautious on our assumptions about the pace of building deposits and

assume that 40% of loans and advances can be funded by deposits by FY22E. We

also remain conservative on cost of deposits and assume that cost of deposits

will be ~7.5% in FY22E, to account for the risk that CASA buildup will take time.

While the company has no intent of lowering its lending rates, we still factor in

a 220bps drop in yield on AUMs over the next 3 years to account for

diversification of the portfolio and entry into secured lending, and arrive at

FY18E/FY19E NIMs of 9.5%/8.9% (including off balance sheet) and we estimate

NIMs will drop to 7.9% by FY22E.

3. Moreover, they have significant scope of refinancing from NABARD, SIDBI and

MUDRA, from whom they receive financing at present; however as a bank they

would be provided longer funding tenures which should help asset liability

mismatch problems.

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 26 of 63

Rise in expenses will peak out in FY18; impact on RoA/RoE will

be limited

In FY16 Equitas reported a CI ratio of 53%. CI ratio is expected to increase in the next few

years due to investments in opening branches, hiring manpower, technology expenses

and channel costs. The company plans to convert 412 branches into banking branches

with separate, more visible liability locations for liability expansion by Mar’17.

In view of the elevated costs in the next few years, combined with a reduction in yields

and margins on conversion to a bank as well as elevated credit costs, we expect the

company’s RoA to decline. We estimate RoA will drop to 2.7%/1.6%/1.6% in

FY17E/FY18E/FY19E before picking up in FY20E and stabilizing at ~1.9% levels in FY22E.

However, at present the bank has a leverage of ~4.4x and the bank has room for increase

in leverage, which should limit drop in RoE. We estimate RoE will reach

12.2%/15.6%/18.1% in FY20E/FY21E/FY22E.

Exhibit 14: Costs will peak out in FY18 post which benefits of scale will reflect

Source: Company filings, Equirus estimates

Exhibit 15: RoA will decline going ahead but higher leverage will prop up RoE

Source: Company, Equirus Securities

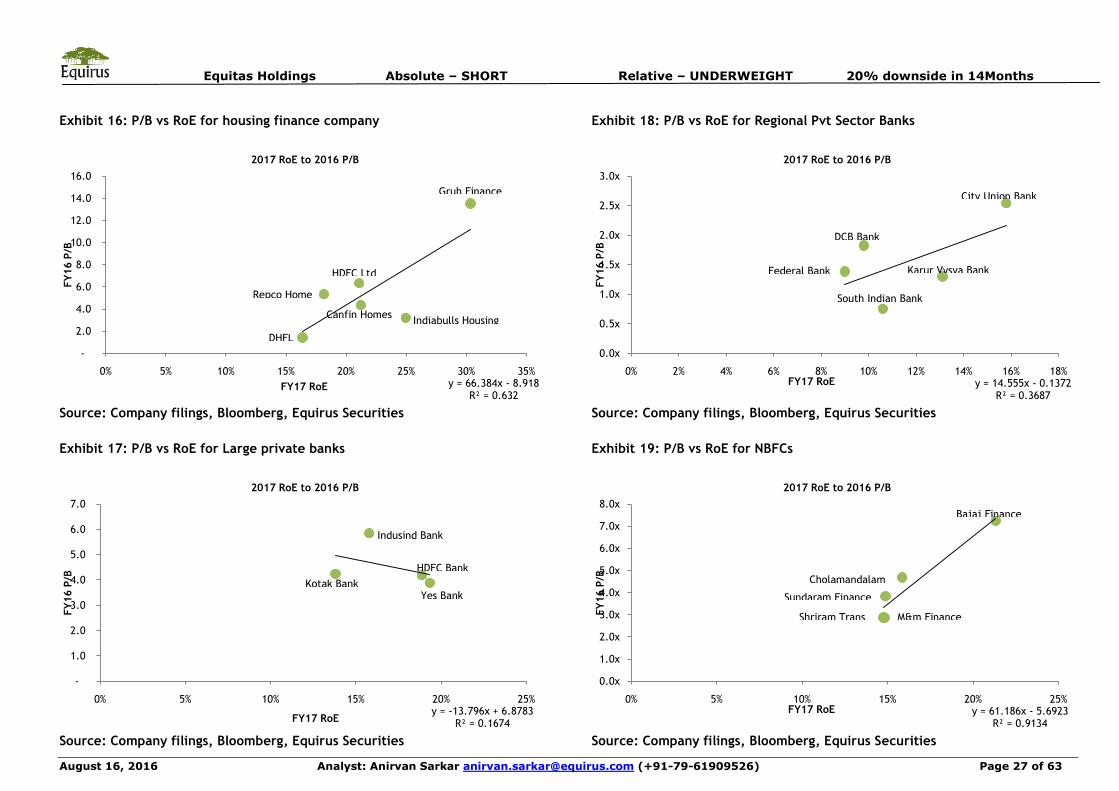

Valuation: At present Equitas is trading at Rs. 176, i.e. at 3.7x FY16A P/ABV. Although

we believe in the strong fundamentals of the company, the present valuation is high and

prices in a seamless bank transition and limited drop in NIM/profitability. The near term

uncertainties of execution and profitability are not factored in the present valuation. In

view of the valuations of new generation private sector banks, old generation private

sector banks, retail NBFCs and microfinance companies (Exhibits 16 through 20), and the

expected drop in profitability in FY17E/FY18E, we believe Equitas needs to prove its

execution on transition in order to be awarded comparable multiples, and should get a

discount to factor transition risks. We arrive at ERoE based Sep’17 TP of Rs. 142 assuming

20 years of growth with average RoE of 15.5% and cost of equity of 14.4%, implying FY17E

P/ABV of 2.2x. 0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

FY15A FY16A FY17E FY18E FY19E FY20E FY21E FY22E

Cost to income

0.0%

5.0%

10.0%

15.0%

20.0%

FY15A FY16A FY17E FY18E FY19E FY20E FY21E FY22E

RoA RoE

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 27 of 63

Exhibit 16: P/B vs RoE for housing finance company

Source: Company filings, Bloomberg, Equirus Securities

Exhibit 17: P/B vs RoE for Large private banks

Source: Company filings, Bloomberg, Equirus Securities

Exhibit 18: P/B vs RoE for Regional Pvt Sector Banks

Source: Company filings, Bloomberg, Equirus Securities

Exhibit 19: P/B vs RoE for NBFCs

Source: Company filings, Bloomberg, Equirus Securities

y = 66.384x - 8.918R² = 0.632

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

0% 5% 10% 15% 20% 25% 30% 35%

FY

16 P

/B

FY17 RoE

2017 RoE to 2016 P/B

y = -13.796x + 6.8783R² = 0.1674

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

0% 5% 10% 15% 20% 25%

FY

16 P

/B

FY17 RoE

2017 RoE to 2016 P/B

y = 14.555x - 0.1372R² = 0.3687

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

FY

16 P

/B

FY17 RoE

2017 RoE to 2016 P/B

y = 61.186x - 5.6923R² = 0.9134

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

0% 5% 10% 15% 20% 25%

FY

16 P

/B

FY17 RoE

2017 RoE to 2016 P/B

Gruh Finance

Indiabulls Housing

DHFL

Repco Home

HDFC Ltd

Canfin Homes

Indusind Bank

Kotak BankYes Bank

HDFC Bank

City Union Bank

Federal Bank

South Indian Bank

Karur Vysya Bank

Bajaj Finance

Sundaram Finance

Cholamandalam

M&m FinanceShriram Trans

DCB Bank

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 28 of 63

Exhibit 20: P/B vs RoE for Microfinance

Source: Company filings, Bloomberg, Equirus Securities

y = 17.975x + 1.0488R² = 0.9229

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

0% 5% 10% 15% 20% 25% 30% 35% 40%

FY

16 P

/B

FY17 RoE

2017 RoE to 2016 P/B

Equitas

SKS Microfinance

Ujjivan

City Union Bank

Equitas Holdings Absolute – SHORT Relative – UNDERWEIGHT 20% downside in 14Months

August 16, 2016 Analyst: Anirvan Sarkar [email protected] (+91-79-61909526) Page 29 of 63

Exhibit 21: ROE-ROA Tree Analysis

FY16A FY17E FY18E FY19E

Yield on Gross AUMs 20.0% 19.0% 18.3% 17.8%

Yield on Investments NA 7.5% 7.5% 7.5%

Cost of Funds 11.3% 9.9% 9.9% 9.4%

Net Interest Margin (incl off balance sheet) 11.4% 9.9% 9.5% 8.9%

Advances (A) 50,702 68,544 84,194 1,07,670

Investments (B) 119 13,234 16,706 22,172

Cash In Hand & Balance with RBI & balances with banks [C]

9,470 9,342 11,793 15,651

Securitization (D) 10,572 12,338 12,864 13,653

Interest Earning Assets (on and off balance sheet) (E = A+B+C+D)

70,863 1,03,458 1,25,557 1,59,145

Average Interest Earning Assets (on and off balance sheet) (F)