microfinance and technology building operational solutions for microfinance and sme projects may 24,...

Post on 20-Dec-2015

214 views

TRANSCRIPT

Microfinance and Technology

Building Operational Solutions for Microfinance and SME ProjectsMay 24, 2010

CGAP Technology Program

14 projects in 10 countries, 13 policy diagnostics• Research, policy, advisory and grant funding• Learning and knowledge sharing• Co-funded by the Bill & Melinda Gates Foundation, CGAP and

the UK Department for International Development• Find us online at http://www.cgap.org/technology

What we do

• Demonstrate innovation and scale in branchless banking projects resulting from CGAP’s technical assistance and/or grant funding.

• Improve broad industry knowledge and practice in the areas of customers, agents, business models and regulatory frameworks.

• Harness existing government payments and remittance flows to provide banking services to large numbers of unbanked people.

• Help policymakers develop regulations that support effective use of mobile technologies for financial inclusion.

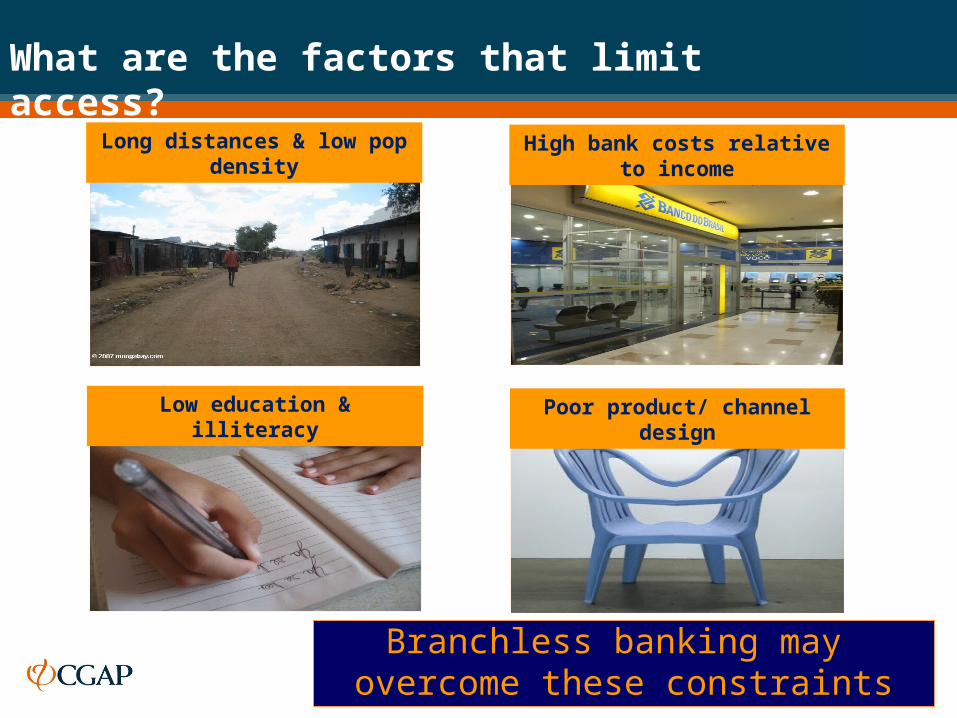

Branchless banking may overcome these constraints

What are the factors that limit access?

Long distances & low pop density High bank costs relative to income

Low education & illiteracy Poor product/ channel design

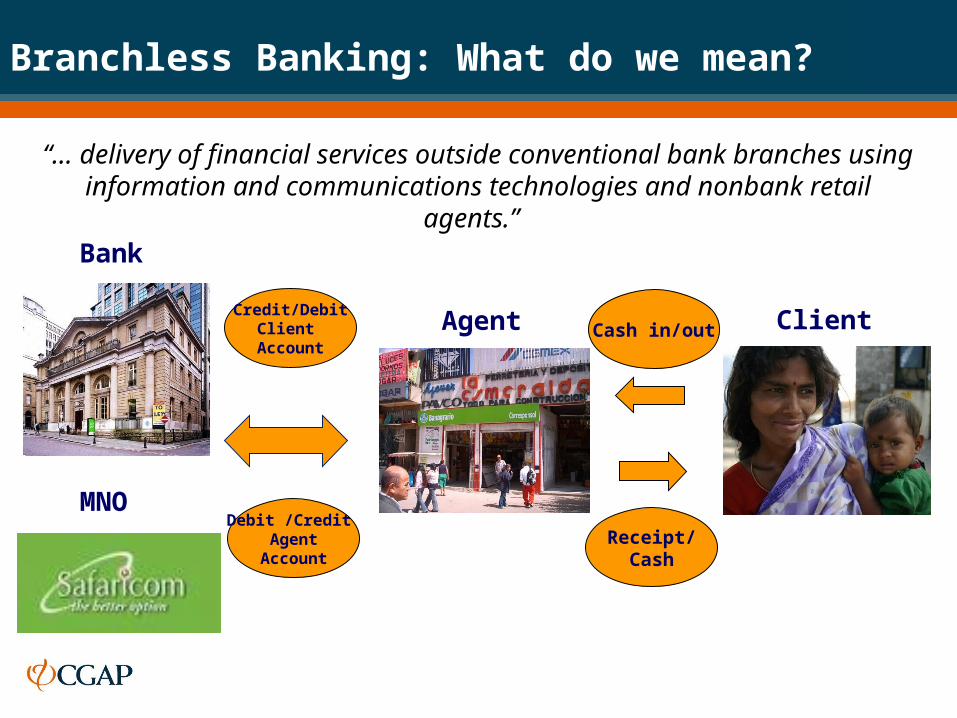

Cash in/out

Receipt/Cash

Bank

Agent ClientCredit/DebitClient

Account

Debit /Credit Agent

Account

Branchless Banking: What do we mean?

“… delivery of financial services outside conventional bank branches using information and communications technologies and nonbank retail agents.”

MNO

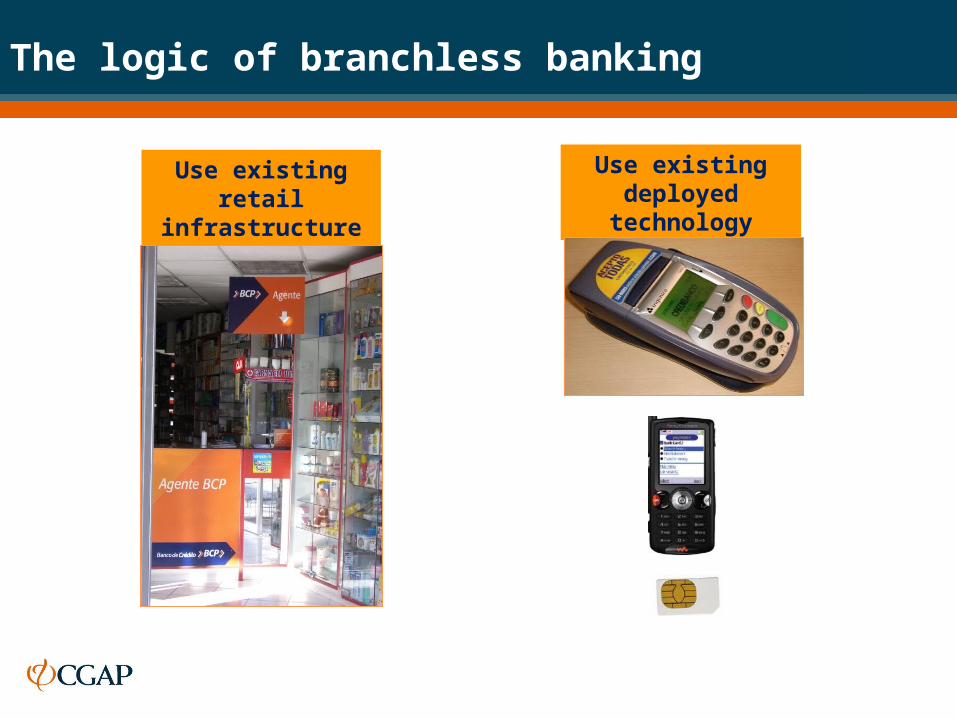

The logic of branchless banking

Use existing retail infrastructure

Use existing deployed technology

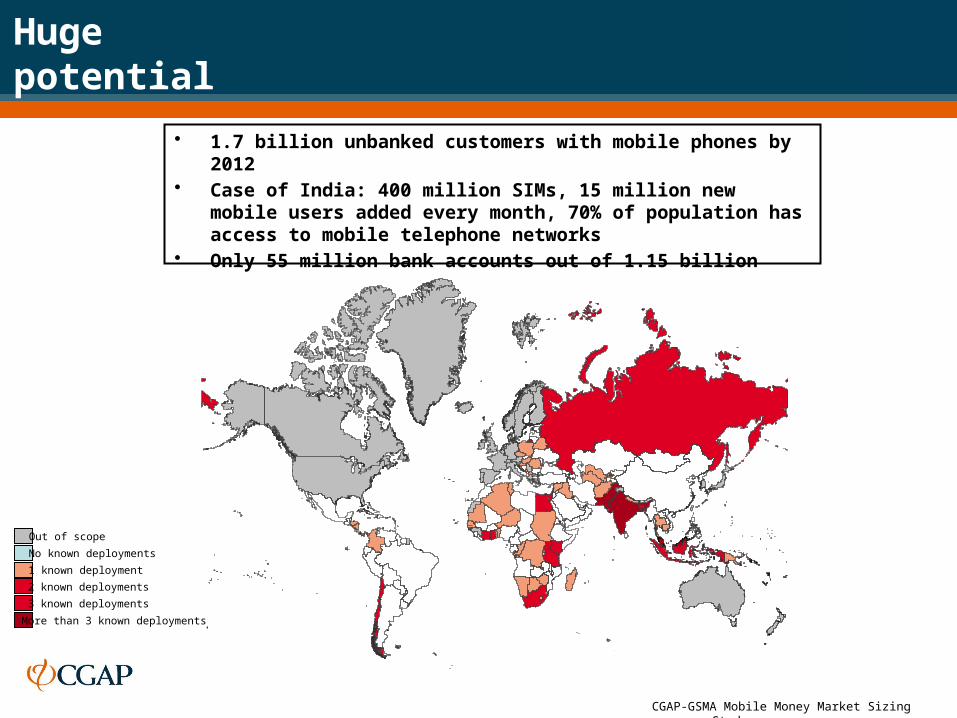

Huge potential

• 1.7 billion unbanked customers with mobile phones by 2012 • Case of India: 400 million SIMs, 15 million new mobile users added

every month, 70% of population has access to mobile telephone networks

• Only 55 million bank accounts out of 1.15 billion population

CGAP-GSMA Mobile Money Market Sizing Study

Out of scope

No known deployments

1 known deployment

2 known deployments

3 known deployments

More than 3 known deployments

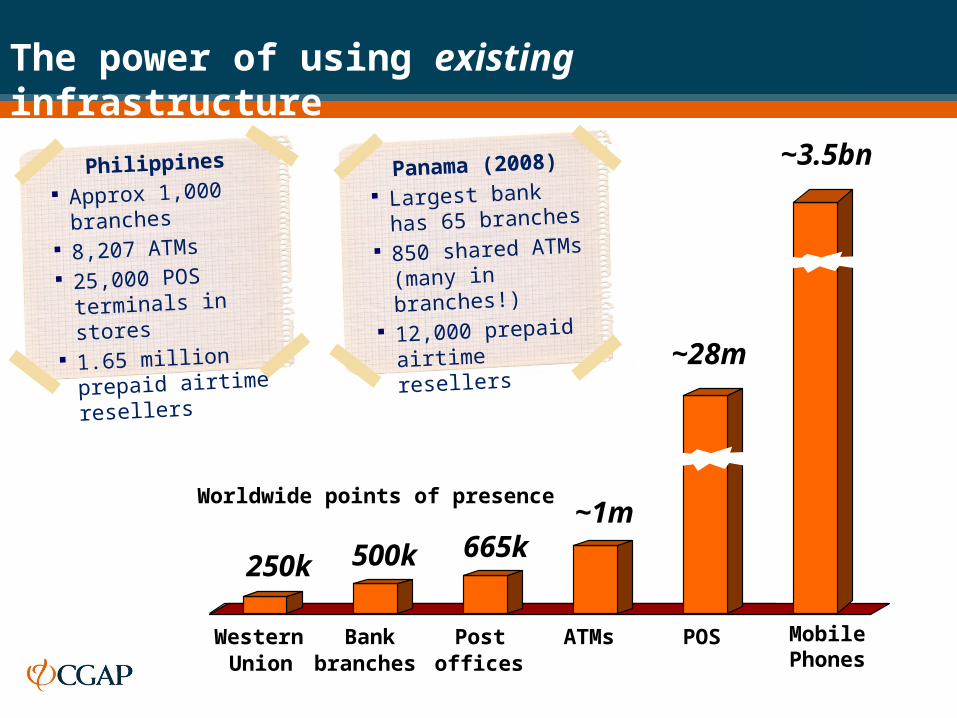

~28m

~3.5bn

~1m665k500k250k

WesternUnion

Bankbranches

Postoffices

ATMs POS Mobile Phones

Worldwide points of presence

The power of using existing infrastructure

Philippines

Approx 1,000 branches

8,207 ATMs 25,000 POS terminals

in stores 1.65 million prepaid

airtime resellers

Panama (2008)

Largest bank has 65

branches 850 shared ATMs

(many in branches!)

12,000 prepaid airtime resellers

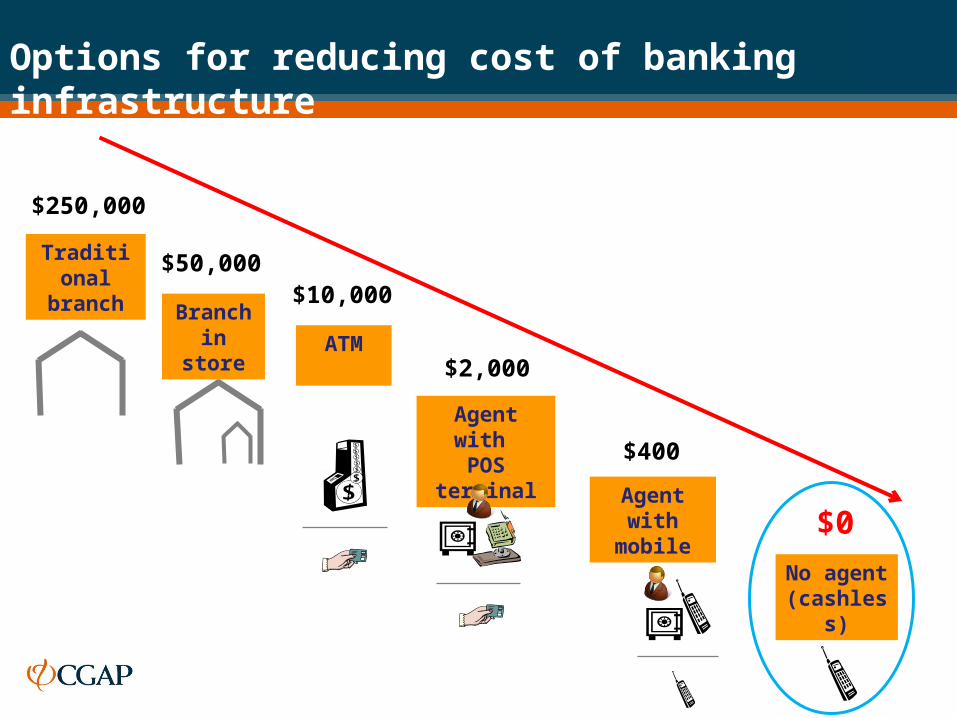

Branchin store

$50,000

ATM

$10,000

No agent (cashless)

$0

Agent with POS terminal

$2,000

Agent with mobile

$400

Options for reducing cost of banking infrastructure

Traditional branch

$250,000

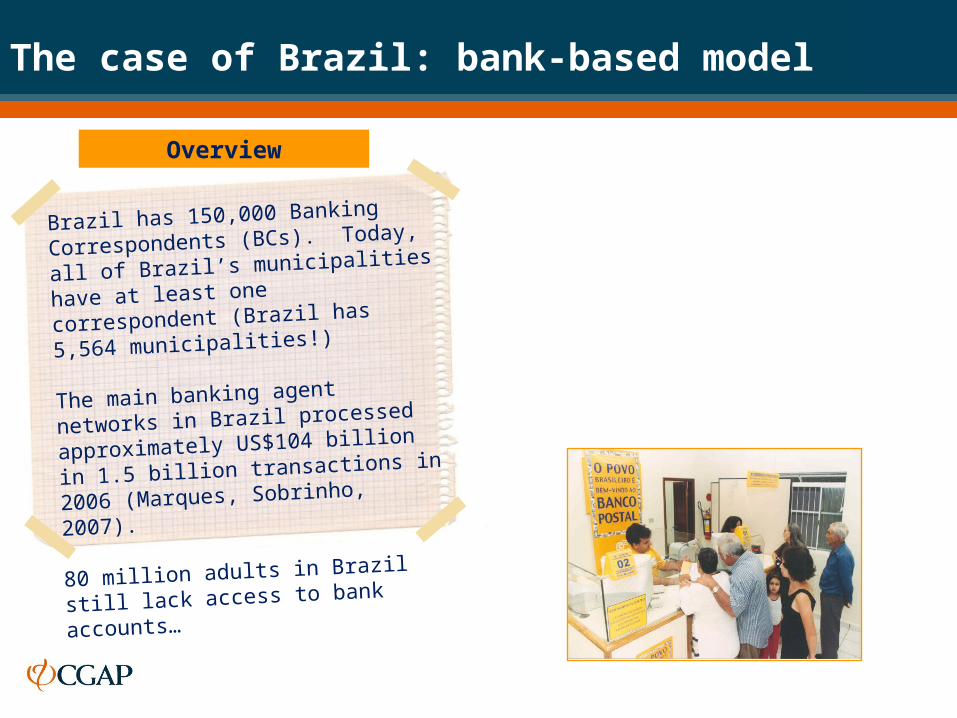

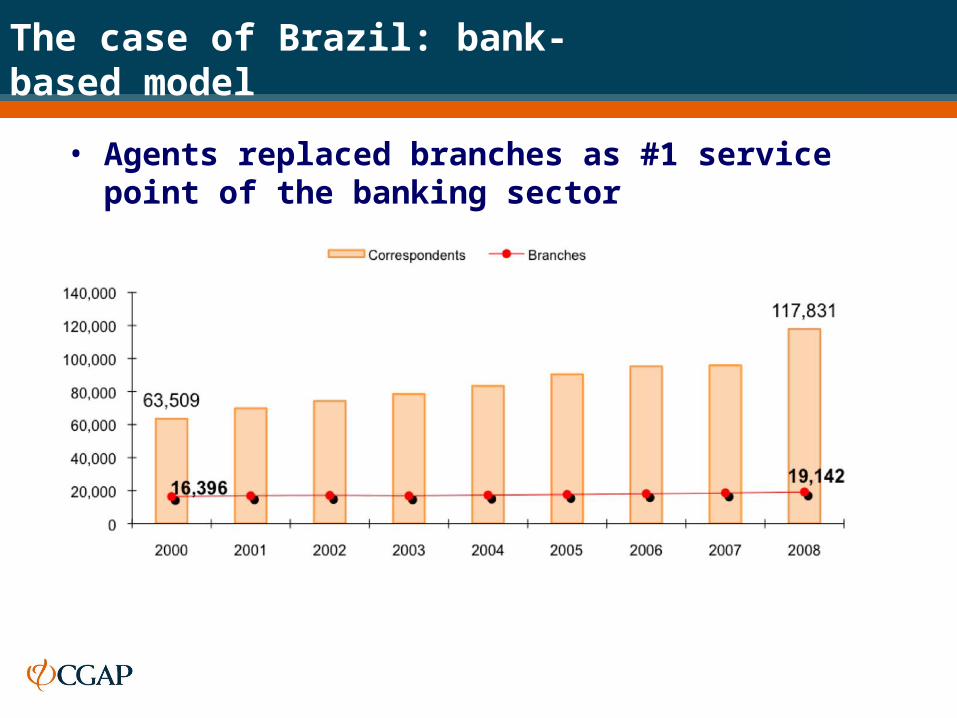

The case of Brazil: bank-based model

Brazil has 150,000 Banking Correspondents

(BCs). Today, all of Brazil’s municipalities

have at least one correspondent (Brazil has

5,564 municipalities!)

The main banking agent networks in Brazil

processed approximately US$104 billion in

1.5 billion transactions in 2006 (Marques,

Sobrinho, 2007).

80 million adults in Brazil still lack access to

bank accounts…

Overview

The case of Brazil: bank-based model

• Agents replaced branches as #1 service point of the banking sector

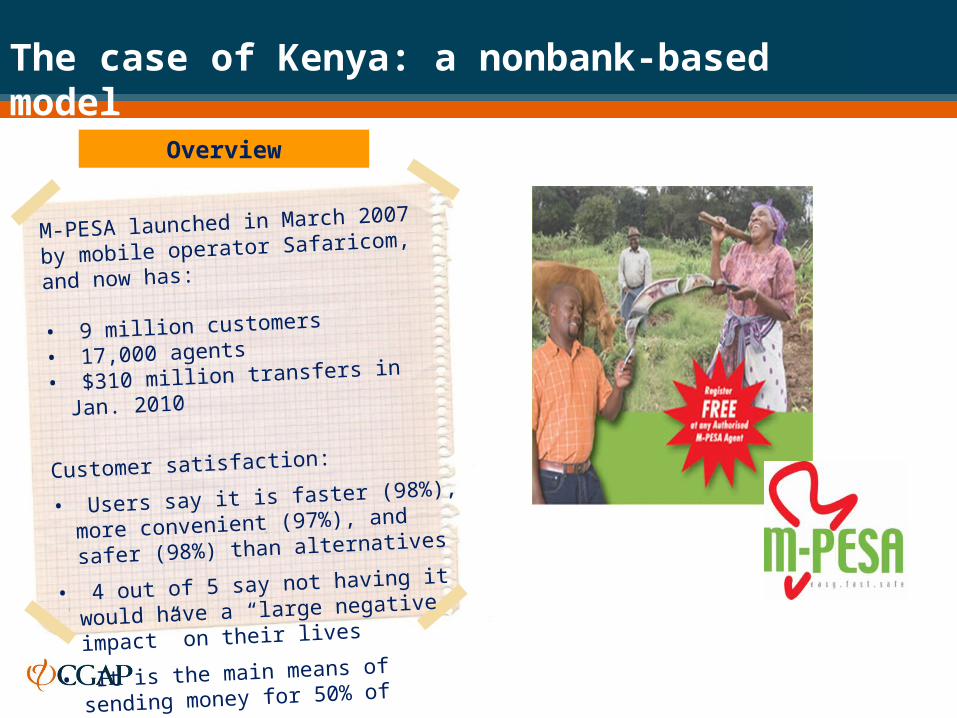

The case of Kenya: a nonbank-based model

M-PESA launched in March 2007

by mobile operator Safaricom, and now has:

• 9 million customers

• 17,000 agents• $310 million transfers in Jan. 2010

Customer satisfaction:

• Users say it is faster (98%), more convenient

(97%), and safer (98%) than alternatives

• 4 out of 5 say not having it would have a

“large negative impact” on their lives

• It is the main means of sending money for

50% of Kenyans

Overview

Regulating agents: Who is permitted to act as an agent?

• Philippines: just about any retailer

• Brazil: retailers, post

offices, lotteries (as

long as being a correspondent is not

their primary business)

• India: cooperatives,

NGOs, post offices

Regulating Agents: Approval needed to work as an agent

• India: none required

• Bolivia: only notification to

Central Bank

• Brazil: no approval, just

need to fill an online form

with the Central Bank

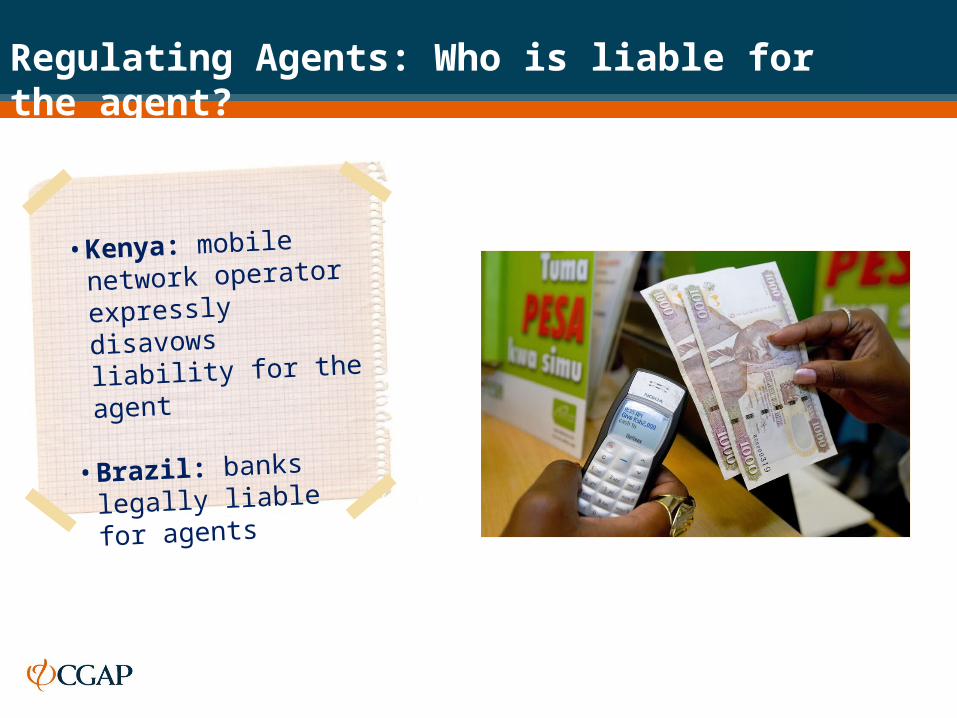

Regulating Agents: Who is liable for the agent?

• Kenya: mobile network

operator expressly

disavows liability for the

agent

• Brazil: banks legally liable

for agents

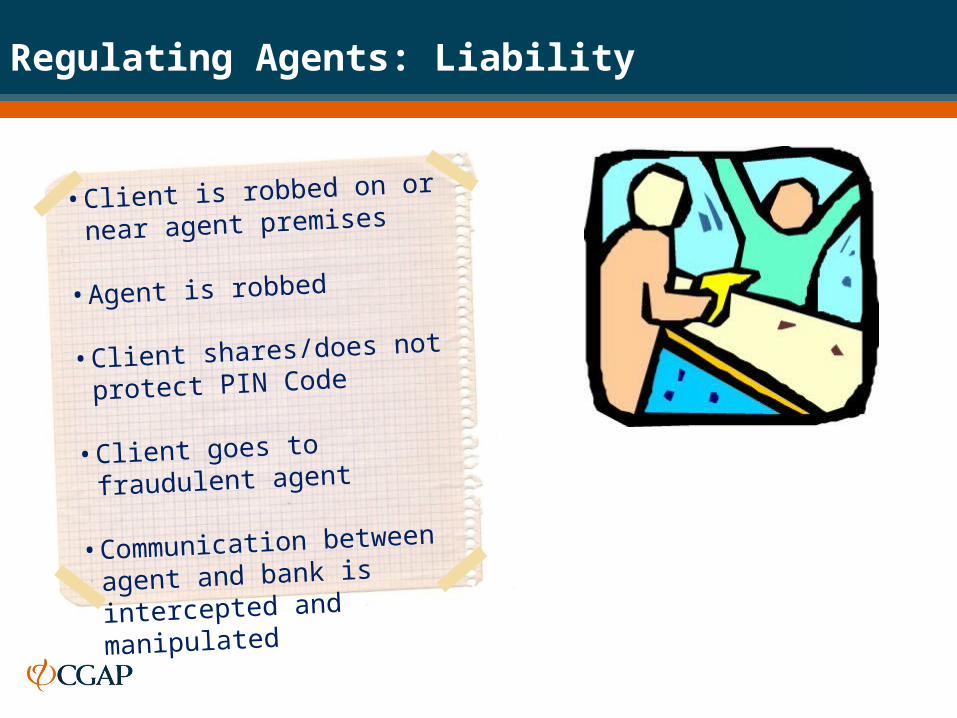

Regulating Agents: Liability

• Client is robbed on or near agent

premises

• Agent is robbed

• Client shares/does not protect PIN

Code

• Client goes to fraudulent agent

• Communication between agent

and bank is intercepted and

manipulated

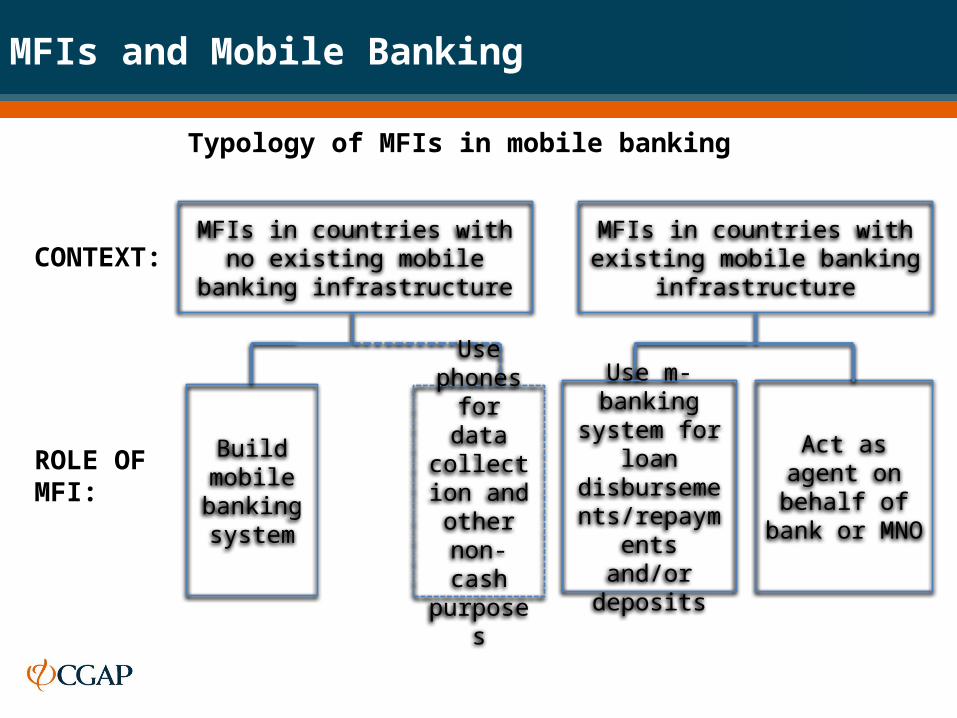

Typology of MFIs in mobile banking

CONTEXT:

ROLE OF MFI:

MFIs in countries with existing mobile banking infrastructure

MFIs in countries with no existing mobile banking infrastructure

Act as agent on behalf of bank

or MNO

Use m-banking system for loan disbursements/

repayments and/or deposits

Buildmobile banking system

Use phones for

data collection and other non-cash purposes

MFIs and Mobile Banking

Advancing financial access for the world’s poor

www.cgap.org

www.microfinancegateway.org