microfinance and risk management: a client perspective · microfinance and risk management: a...

TRANSCRIPT

As the microfinance industry matures,service providers are increasingly con-cerned with developing new and betterproducts. This focus on new product de-velopment is a response to growing com-petition in the microfinance market, thesearch for more defined market niches,and some anxiety about dropout rates.

To design successful products, the firststep entails understanding the financialneeds of clients (and potential clients) andhow financial services fit into their moneymanagement strategies. Understandingclients requires an awareness of the eco-nomic goals of poor households, howpeople manage resources and activities,and how they deal with risk in their day-to-day lives. Such a framework can be auseful starting point to better understandfinancial service preferences of poorhouseholds.

Recent research commissioned as a contri-bution for the forthcoming World Develop-ment Report 2000/1(WDR)1 on povertyhighlights the importance of focusing onrisk and vulnerability as a way of under-standing the possibilities and limitationsof the interface between poverty and micro-finance. The research focused on selectednon-income dimensions of poverty, spe-cifically how people use microfinance ser-vices to build physical, financial, humanand social assets, mitigate risk, and reducevulnerability.

The study addressed four main questions:● Whom do microfinance programs

reach?

Microfinance and Risk Management:A Client Perspective

The Focus Series isCGAP’s primary vehiclefor dissemination togovernments,donors,and private andfinancial institutionson best practices inmicroenterprise finance.

Please contact FOCUS,CGAP Secretariat withcomments, contributions,and to receive other notesin the series:

1818 H Street NW,Washington DC 20433

Tel: 202. 473 9594

Fax: 202. 522 3744

e-mail:[email protected]

WWW:http://www.cgap.org

Focus No. 17

C G A PC G A PC G A PC G A PC G A P T H E C O N S U L T A T I V E G R O U P T O A S S I S T T H E P O O R E S T [ A M I C R O F I N A N C E P R O G R A M ]

M a y 2 0 0 0

● What is the nature of risks facingclients?

● What strategies do clients useto deal with risks they face?

● What is the role of microfinanceservices in this process?

The field studies involved seven micro-finance institutions (MFIs) in four coun-tries including Bolivia, Bangladesh,Uganda and the Philippines. Using lowcost methods, the researchers gathereda mix of primary qualitative and quanti-tative data on clients and non-clients.In total, the study drew on data fromfield interviews with some 1,500 micro-finance clients in the four countries.The field findings were supplementedwith secondary information and findingsfrom other recent impact studies.

Findings from the WDR research

W h o m d o p r o g r a m s r e a c h ?

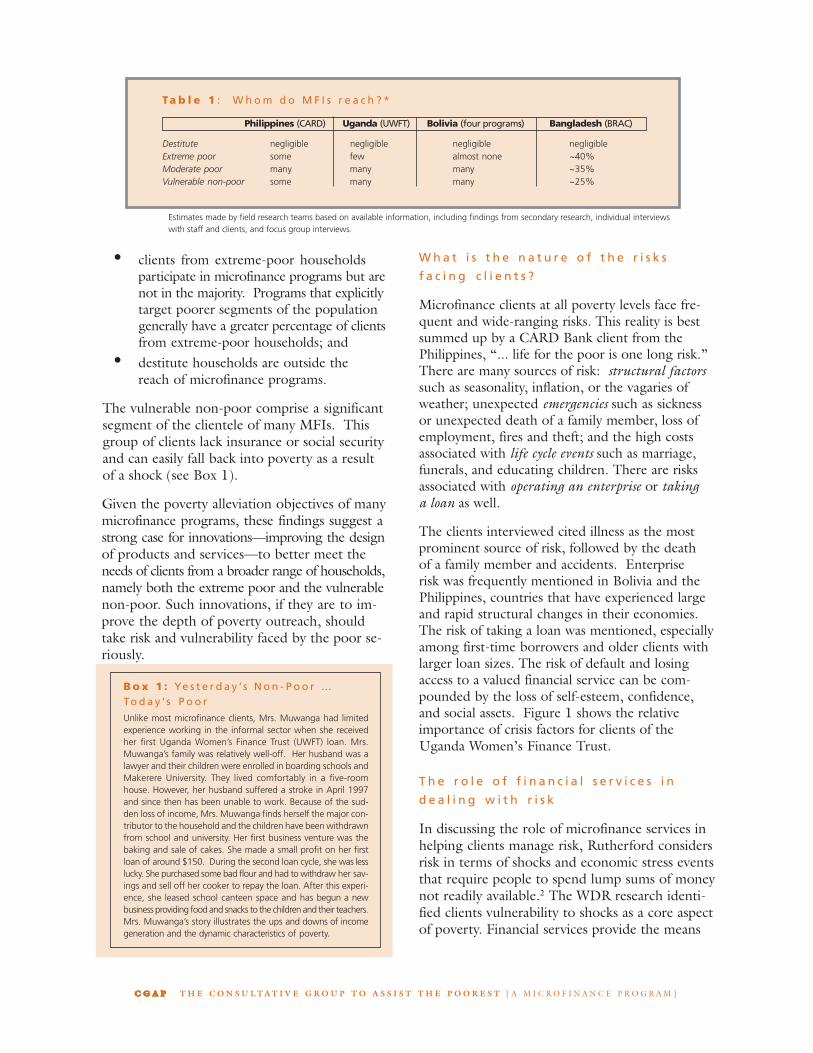

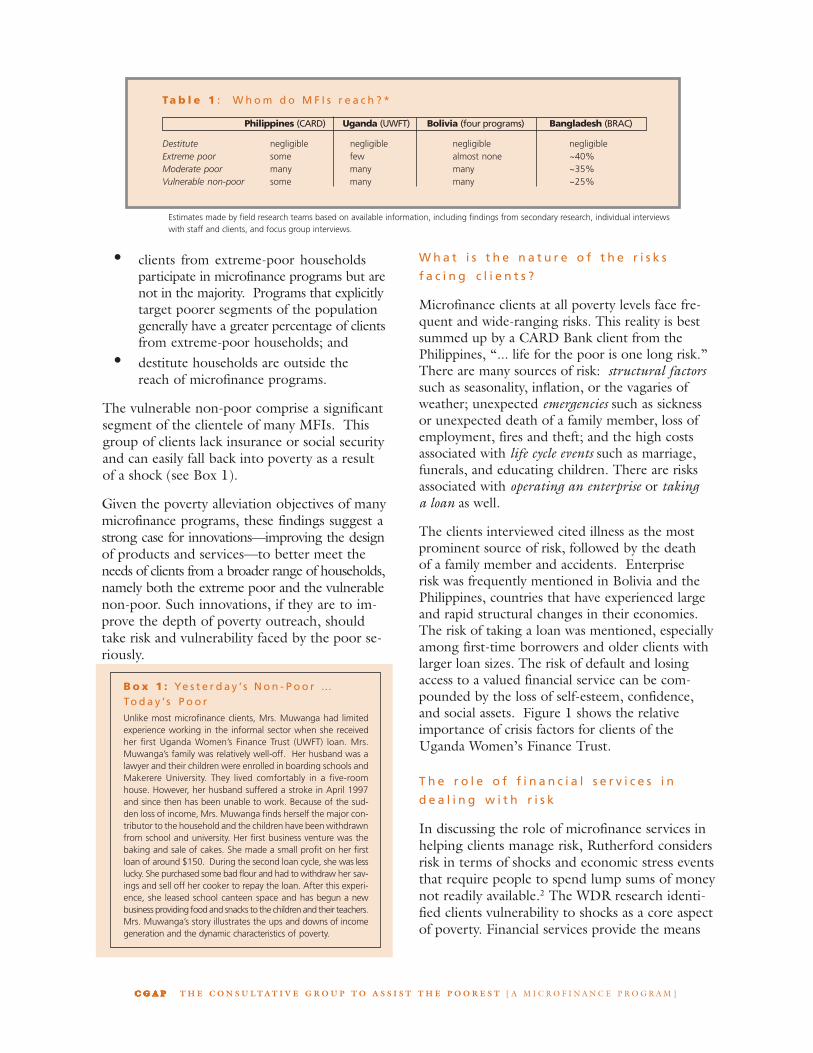

Wealth ranking by household povertylevel shows that microfinance clients inthe study programs are heterogeneous.Clients defined themselves relative topoverty categories that included destitute,extreme poor, moderate poor (roughlyjust below the poverty line), and vulner-able non-poor (just above the povertyline). As shown in Table 1, the WDRresearch, complemented with the findingsfrom other impact studies, suggests that:

● most clients come from moderatepoor and vulnerable non-poorhouseholds;

As the microfinance industry matures,service providers are increasingly con-cerned with developing new and betterproducts. This focus on new product de-velopment is a response to growing com-petition in the microfinance market, thesearch for more defined market niches,and some anxiety about dropout rates.

To design successful products, the firststep entails understanding the financialneeds of clients (and potential clients) andhow financial services fit into their moneymanagement strategies. Understandingclients requires an awareness of the eco-nomic goals of poor households, howpeople manage resources and activities,and how they deal with risk in their day-to-day lives. Such a framework can be auseful starting point to better understandfinancial service preferences of poorhouseholds.

Recent research commissioned as a contri-bution for the forthcoming World Develop-ment Report 2000/1(WDR)1 on povertyhighlights the importance of focusing onrisk and vulnerability as a way of under-standing the possibilities and limitationsof the interface between poverty and micro-finance. The research focused on selectednon-income dimensions of poverty, spe-cifically how people use microfinance ser-vices to build physical, financial, humanand social assets, mitigate risk, and reducevulnerability.

The study addressed four main questions:● Whom do microfinance programs

reach?

Microfinance and Risk Management:

A Client Perspective

The Focus Series isCGAP’s primary vehiclefor dissemination togovernments,donors,and private andfinancial institutionson best practices inmicroenterprise finance.

Please contact FOCUS,CGAP Secretariat withcomments, contributions,and to receive other notesin the series:

1818 H Street NW,Washington DC 20433

Tel: 202. 473 9594

Fax: 202. 522 3744

e-mail:[email protected]

WWW:http://www.cgap.org

Focus No. 17

C G A PC G A PC G A PC G A PC G A P T H E C O N S U L T A T I V E G R O U P T O A S S I S T T H E P O O R E S T [ A M I C R O F I N A N C E P R O G R A M ]

M a y 2 0 0 0

● What is the nature of risks facingclients?

● What strategies do clients useto deal with risks they face?

● What is the role of microfinanceservices in this process?

The field studies involved seven micro-finance institutions (MFIs) in four coun-tries including Bolivia, Bangladesh,Uganda and the Philippines. Using lowcost methods, the researchers gathereda mix of primary qualitative and quanti-tative data on clients and non-clients.In total, the study drew on data fromfield interviews with some 1,500 micro-finance clients in the four countries.The field findings were supplementedwith secondary information and findingsfrom other recent impact studies.

Findings from the WDR research

W h o m d o p r o g r a m s r e a c h ?

Wealth ranking by household povertylevel shows that microfinance clients inthe study programs are heterogeneous.Clients defined themselves relative topoverty categories that included destitute,extreme poor, moderate poor (roughlyjust below the poverty line), and vulner-able non-poor (just above the povertyline). As shown in Table 1, the WDRresearch, complemented with the findingsfrom other impact studies, suggests that:

● most clients come from moderatepoor and vulnerable non-poorhouseholds;

C G A PC G A PC G A PC G A PC G A P T H E C O N S U L T A T I V E G R O U P T O A S S I S T T H E P O O R E S T [ A M I C R O F I N A N C E P R O G R A M ]

● clients from extreme-poor householdsparticipate in microfinance programs but arenot in the majority. Programs that explicitlytarget poorer segments of the populationgenerally have a greater percentage of clientsfrom extreme-poor households; and

● destitute households are outside thereach of microfinance programs.

The vulnerable non-poor comprise a significantsegment of the clientele of many MFIs. Thisgroup of clients lack insurance or social securityand can easily fall back into poverty as a resultof a shock (see Box 1).

W h a t i s t h e n a t u r e o f t h e r i s k s

f a c i n g c l i e n t s ?

Microfinance clients at all poverty levels face fre-quent and wide-ranging risks. This reality is bestsummed up by a CARD Bank client from thePhilippines, “... life for the poor is one long risk.”There are many sources of risk: structural factorssuch as seasonality, inflation, or the vagaries ofweather; unexpected emergencies such as sicknessor unexpected death of a family member, loss ofemployment, fires and theft; and the high costsassociated with life cycle events such as marriage,funerals, and educating children. There are risksassociated with operating an enterprise or takinga loan as well.

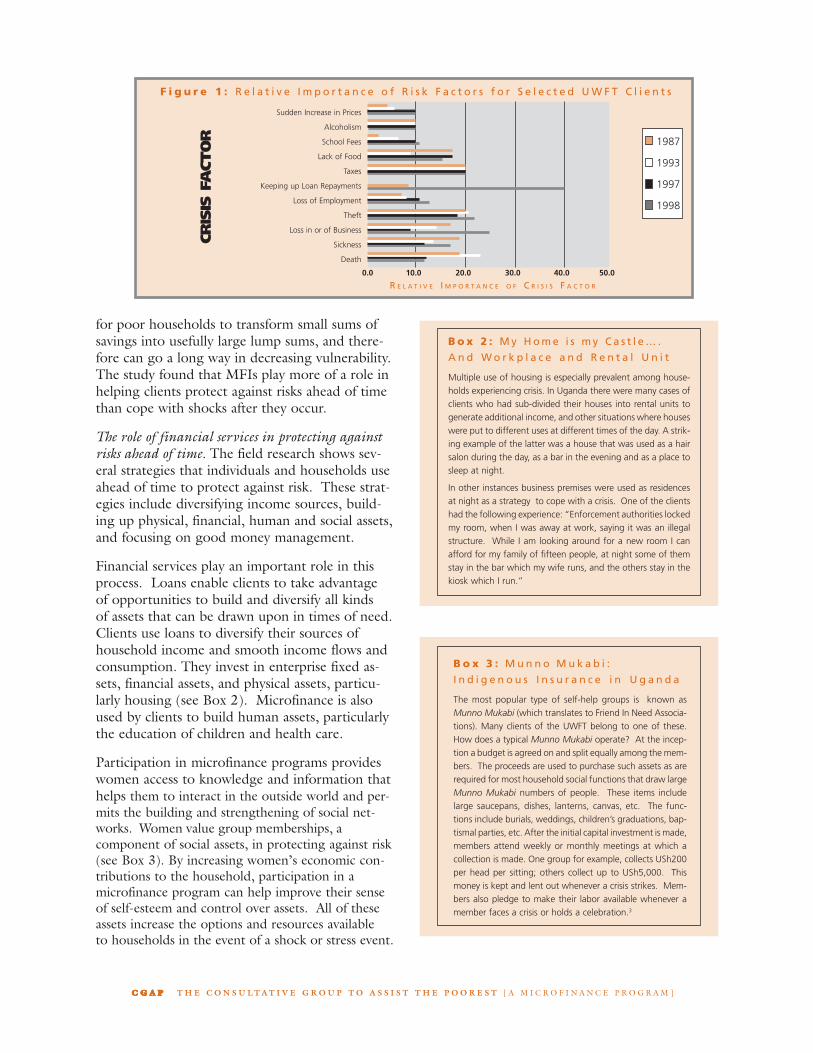

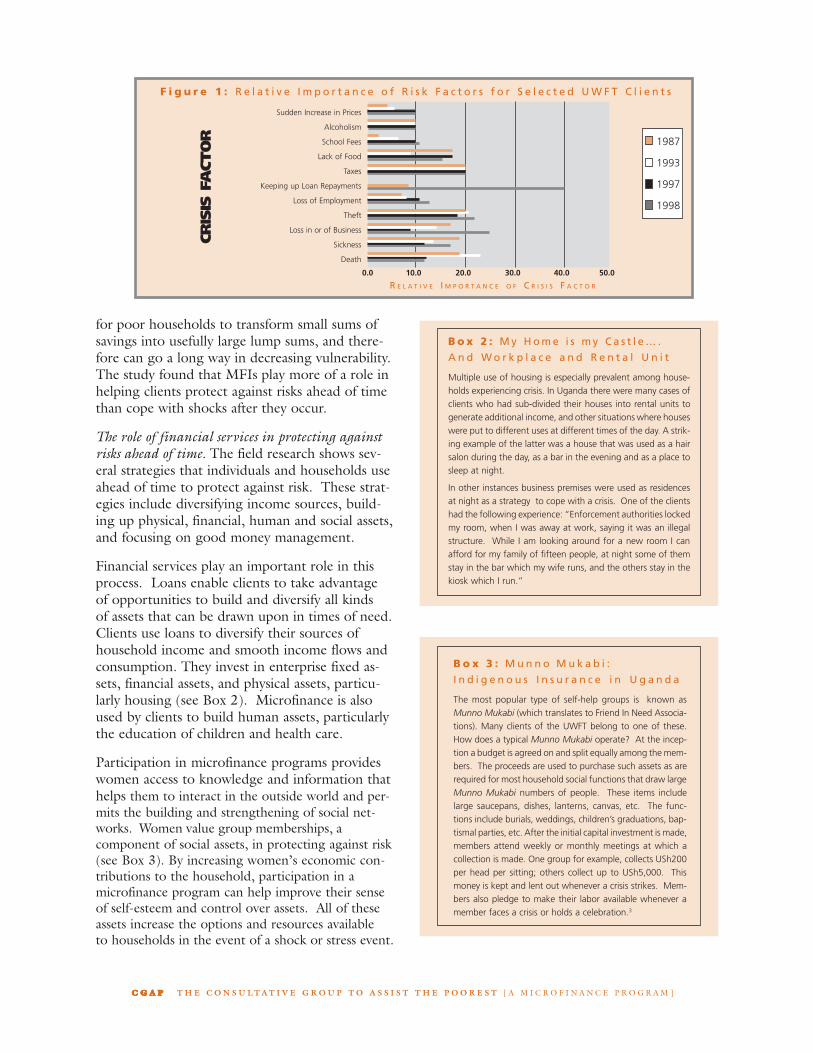

The clients interviewed cited illness as the mostprominent source of risk, followed by the deathof a family member and accidents. Enterpriserisk was frequently mentioned in Bolivia and thePhilippines, countries that have experienced largeand rapid structural changes in their economies.The risk of taking a loan was mentioned, especiallyamong first-time borrowers and older clients withlarger loan sizes. The risk of default and losingaccess to a valued financial service can be com-pounded by the loss of self-esteem, confidence,and social assets. Figure 1 shows the relativeimportance of crisis factors for clients of theUganda Women’s Finance Trust.

T h e r o l e o f f i n a n c i a l s e r v i c e s i n

d e a l i n g w i t h r i s k

In discussing the role of microfinance services inhelping clients manage risk, Rutherford considersrisk in terms of shocks and economic stress eventsthat require people to spend lump sums of moneynot readily available.2 The WDR research identi-fied clients vulnerability to shocks as a core aspectof poverty. Financial services provide the means

Ta b l e 1 : W h o m d o M F I s r e a c h ? *

Philippines (CARD) Uganda (UWFT) Bolivia (four programs) Bangladesh (BRAC)

Destitute negligible negligible negligible negligibleExtreme poor some few almost none ~40%Moderate poor many many many ~35%Vulnerable non-poor some many many ~25%

Estimates made by field research teams based on available information, including findings from secondary research, individual interviewswith staff and clients, and focus group interviews.

B o x 1 : Ye s t e r d a y ’ s N o n - P o o r …To d a y ’s P o o r

Unlike most microfinance clients, Mrs. Muwanga had limitedexperience working in the informal sector when she receivedher first Uganda Women’s Finance Trust (UWFT) loan. Mrs.Muwanga’s family was relatively well-off. Her husband was alawyer and their children were enrolled in boarding schools andMakerere University. They lived comfortably in a five-roomhouse. However, her husband suffered a stroke in April 1997and since then has been unable to work. Because of the sud-den loss of income, Mrs. Muwanga finds herself the major con-tributor to the household and the children have been withdrawnfrom school and university. Her first business venture was thebaking and sale of cakes. She made a small profit on her firstloan of around $150. During the second loan cycle, she was lesslucky. She purchased some bad flour and had to withdraw her sav-ings and sell off her cooker to repay the loan. After this experi-ence, she leased school canteen space and has begun a newbusiness providing food and snacks to the children and their teachers.Mrs. Muwanga’s story illustrates the ups and downs of incomegeneration and the dynamic characteristics of poverty.

Given the poverty alleviation objectives of manymicrofinance programs, these findings suggest astrong case for innovations—improving the designof products and services—to better meet theneeds of clients from a broader range of households,namely both the extreme poor and the vulnerablenon-poor. Such innovations, if they are to im-prove the depth of poverty outreach, shouldtake risk and vulnerability faced by the poor se-riously.

C G A PC G A PC G A PC G A PC G A P T H E C O N S U L T A T I V E G R O U P T O A S S I S T T H E P O O R E S T [ A M I C R O F I N A N C E P R O G R A M ]

for poor households to transform small sums ofsavings into usefully large lump sums, and there-fore can go a long way in decreasing vulnerability.The study found that MFIs play more of a role inhelping clients protect against risks ahead of timethan cope with shocks after they occur.

The role of financial services in protecting againstrisks ahead of time. The field research shows sev-eral strategies that individuals and households useahead of time to protect against risk. These strat-egies include diversifying income sources, build-ing up physical, financial, human and social assets,and focusing on good money management.

Financial services play an important role in thisprocess. Loans enable clients to take advantageof opportunities to build and diversify all kindsof assets that can be drawn upon in times of need.Clients use loans to diversify their sources ofhousehold income and smooth income flows andconsumption. They invest in enterprise fixed as-sets, financial assets, and physical assets, particu-larly housing (see Box 2). Microfinance is alsoused by clients to build human assets, particularlythe education of children and health care.

Participation in microfinance programs provideswomen access to knowledge and information thathelps them to interact in the outside world and per-mits the building and strengthening of social net-works. Women value group memberships, acomponent of social assets, in protecting against risk(see Box 3). By increasing women’s economic con-tributions to the household, participation in amicrofinance program can help improve their senseof self-esteem and control over assets. All of theseassets increase the options and resources availableto households in the event of a shock or stress event.

Sudden Increase in Prices

Alcoholism

School Fees

Lack of Food

Taxes

Keeping up Loan Repayments

Loss of Employment

Theft

Loss in or of Business

Sickness

Death

1987

1993

1997

1998

F i g u r e 1 : R e l a t i v e I m p o r t a n c e o f R i s k F a c t o r s f o r S e l e c t e d U W F T C l i e n t s

R E L A T I V E I M P O R T A N C E O F C R I S I S F A C T O R

0.0 10.0 20.0 30.0 40.0 50.0

B o x 3 : M u n n o M u k a b i :

I n d i g e n o u s I n s u r a n c e i n U g a n d a

The most popular type of self-help groups is known asMunno Mukabi (which translates to Friend In Need Associa-tions). Many clients of the UWFT belong to one of these.How does a typical Munno Mukabi operate? At the incep-tion a budget is agreed on and split equally among the mem-bers. The proceeds are used to purchase such assets as arerequired for most household social functions that draw largeMunno Mukabi numbers of people. These items includelarge saucepans, dishes, lanterns, canvas, etc. The func-tions include burials, weddings, children’s graduations, bap-tismal parties, etc. After the initial capital investment is made,members attend weekly or monthly meetings at which acollection is made. One group for example, collects USh200per head per sitting; others collect up to USh5,000. Thismoney is kept and lent out whenever a crisis strikes. Mem-bers also pledge to make their labor available whenever amember faces a crisis or holds a celebration.3

B o x 2 : M y H o m e i s m y C a s t l e … .

A n d W o r k p l a c e a n d R e n t a l U n i t

Multiple use of housing is especially prevalent among house-holds experiencing crisis. In Uganda there were many cases ofclients who had sub-divided their houses into rental units togenerate additional income, and other situations where houseswere put to different uses at different times of the day. A strik-ing example of the latter was a house that was used as a hairsalon during the day, as a bar in the evening and as a place tosleep at night.

In other instances business premises were used as residencesat night as a strategy to cope with a crisis. One of the clientshad the following experience: “Enforcement authorities lockedmy room, when I was away at work, saying it was an illegalstructure. While I am looking around for a new room I canafford for my family of fifteen people, at night some of themstay in the bar which my wife runs, and the others stay in thekiosk which I run.”

CRIS

IS F

ACT

OR

C G A PC G A PC G A PC G A PC G A P T H E C O N S U L T A T I V E G R O U P T O A S S I S T T H E P O O R E S T [ A M I C R O F I N A N C E P R O G R A M ]

Source: Adapted from Sebstad, Jennefer and Monique Cohen (March, 2000),“Synthesis Report on Microfinance, Risk Management and Poverty.” The report isbased on field studies by Ronald T. Chua, Paul Mosley, Graham A.N. Wright, andHassan Zaman. Paper submitted to USAID by AIMS. Washington, D.C.: Manage-ment Systems International. The note was prepared by Imran Matin and BrigitHelms of the CGAP Secretariat. Publication Manager: Tiphaine Crenn.

Maintaining access to MFI program credit, in itself,is a protectional risk management strategy for manyclients (see Box 4). They go to great lengths to en-sure repayment, particularly when confronted with acrisis or shock, often by mobilizing informal sourcesof finance to ensure repayment. Repayment meansaccess to a new loan to start back on the road to re-covery, to restock a microenterprise, to rebuild ahouse, to pay school fees.

The role of financial services in coping with shocks oreconomic stress events afterwards. Once a shock orstress event occurs, people use various coping strate-gies: they modify consumption, raise income bymobilizing labor or selling assets, they draw on in-formal and formal savings, and draw down claimson informal group-based insurance mechanisms.

The WDR field studies suggest that clients generallyuse low to medium stress strategies in coping withloss – modified consumption, labor mobilization andinformal borrowing from friends and relatives. Theyseek to conserve productive assets and thus maintainincome-earning potential when possible. Acrosscountries, clients were reluctant to withdraw childrenfrom school, cash in savings, or sell productive assets.

In general, clients tend to use informal sources ofcredit more often than MFI credit to cope with lossesfollowing a shock. When they were used, MFI ser-vices were only accessed when other sources were

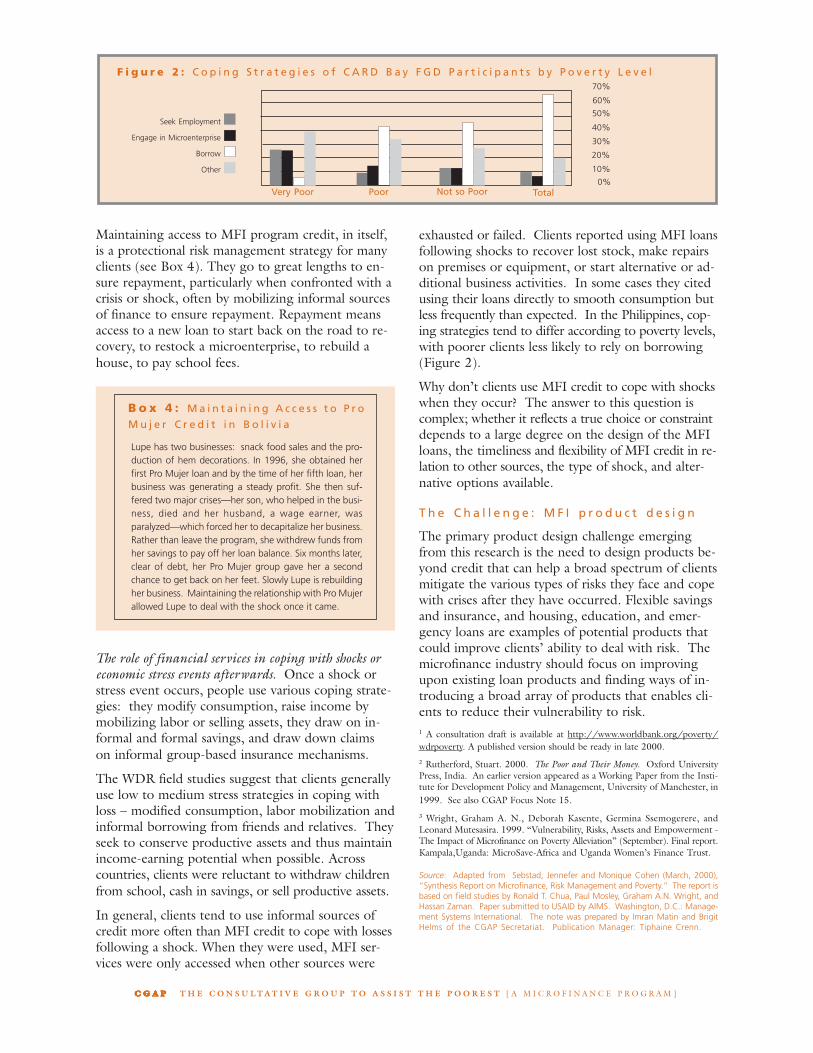

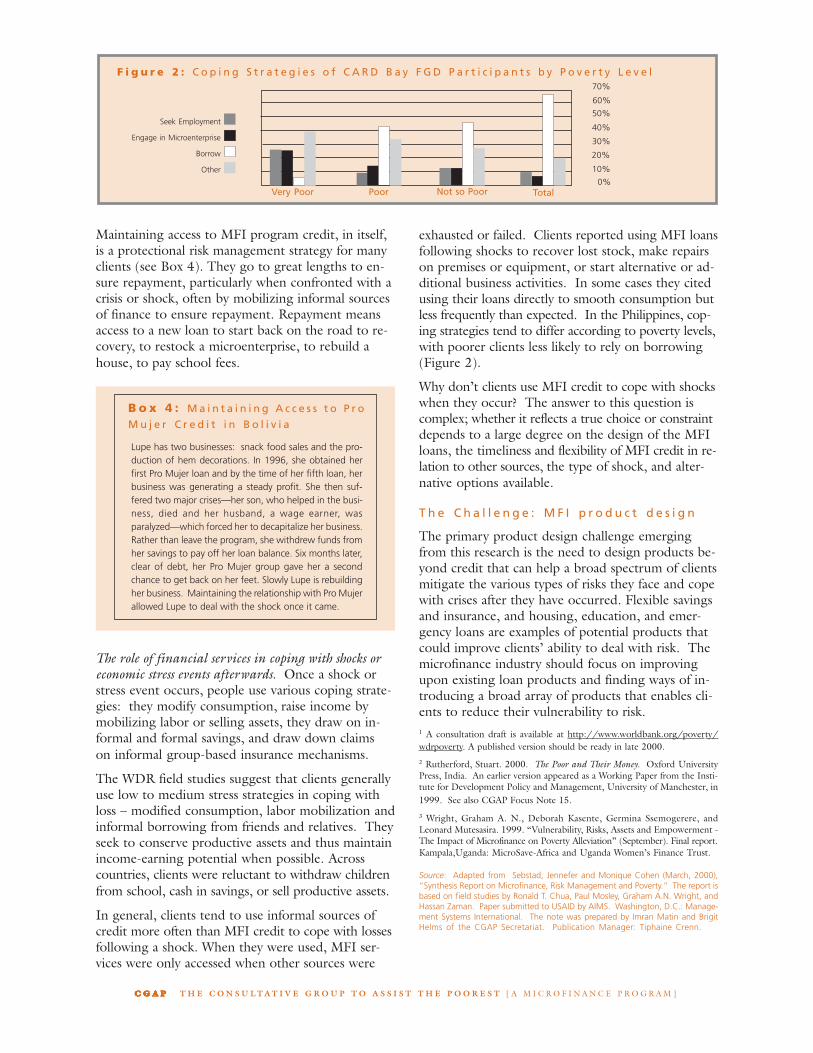

exhausted or failed. Clients reported using MFI loansfollowing shocks to recover lost stock, make repairson premises or equipment, or start alternative or ad-ditional business activities. In some cases they citedusing their loans directly to smooth consumption butless frequently than expected. In the Philippines, cop-ing strategies tend to differ according to poverty levels,with poorer clients less likely to rely on borrowing(Figure 2).

Why don’t clients use MFI credit to cope with shockswhen they occur? The answer to this question iscomplex; whether it reflects a true choice or constraintdepends to a large degree on the design of the MFIloans, the timeliness and flexibility of MFI credit in re-lation to other sources, the type of shock, and alter-native options available.

T h e C h a l l e n g e : M F I p r o d u c t d e s i g n

The primary product design challenge emergingfrom this research is the need to design products be-yond credit that can help a broad spectrum of clientsmitigate the various types of risks they face and copewith crises after they have occurred. Flexible savingsand insurance, and housing, education, and emer-gency loans are examples of potential products thatcould improve clients’ ability to deal with risk. Themicrofinance industry should focus on improvingupon existing loan products and finding ways of in-troducing a broad array of products that enables cli-ents to reduce their vulnerability to risk.1 A consultation draft is available at http://www.worldbank.org/poverty/wdrpoverty. A published version should be ready in late 2000.2 Rutherford, Stuart. 2000. The Poor and Their Money. Oxford UniversityPress, India. An earlier version appeared as a Working Paper from the Insti-tute for Development Policy and Management, University of Manchester, in1999. See also CGAP Focus Note 15.

3 Wright, Graham A. N., Deborah Kasente, Germina Ssemogerere, andLeonard Mutesasira. 1999. “Vulnerability, Risks, Assets and Empowerment -The Impact of Microfinance on Poverty Alleviation” (September). Final report.Kampala,Uganda: MicroSave-Africa and Uganda Women’s Finance Trust.

F i g u r e 2 : C o p i n g S t r a t e g i e s o f C A R D B a y F G D P a r t i c i p a n t s b y P o v e r t y L e v e l

Seek Employment

Engage in Microenterprise

Borrow

Other

B o x 4 : M a i n t a i n i n g A c c e s s t o P r o

M u j e r C r e d i t i n B o l i v i a

Lupe has two businesses: snack food sales and the pro-duction of hem decorations. In 1996, she obtained herfirst Pro Mujer loan and by the time of her fifth loan, herbusiness was generating a steady profit. She then suf-fered two major crises—her son, who helped in the busi-ness, died and her husband, a wage earner, wasparalyzed—which forced her to decapitalize her business.Rather than leave the program, she withdrew funds fromher savings to pay off her loan balance. Six months later,clear of debt, her Pro Mujer group gave her a secondchance to get back on her feet. Slowly Lupe is rebuildingher business. Maintaining the relationship with Pro Mujerallowed Lupe to deal with the shock once it came.

Very Poor Poor Not so Poor Total

70%

60%

50%

40%

30%

20%

10%

0%

C G A PC G A PC G A PC G A PC G A P T H E C O N S U L T A T I V E G R O U P T O A S S I S T T H E P O O R E S T [ A M I C R O F I N A N C E P R O G R A M ]

● clients from extreme-poor householdsparticipate in microfinance programs but arenot in the majority. Programs that explicitlytarget poorer segments of the populationgenerally have a greater percentage of clientsfrom extreme-poor households; and

● destitute households are outside thereach of microfinance programs.

The vulnerable non-poor comprise a significantsegment of the clientele of many MFIs. Thisgroup of clients lack insurance or social securityand can easily fall back into poverty as a resultof a shock (see Box 1).

W h a t i s t h e n a t u r e o f t h e r i s k s

f a c i n g c l i e n t s ?

Microfinance clients at all poverty levels face fre-quent and wide-ranging risks. This reality is bestsummed up by a CARD Bank client from thePhilippines, “... life for the poor is one long risk.”There are many sources of risk: structural factorssuch as seasonality, inflation, or the vagaries ofweather; unexpected emergencies such as sicknessor unexpected death of a family member, loss ofemployment, fires and theft; and the high costsassociated with life cycle events such as marriage,funerals, and educating children. There are risksassociated with operating an enterprise or takinga loan as well.

The clients interviewed cited illness as the mostprominent source of risk, followed by the deathof a family member and accidents. Enterpriserisk was frequently mentioned in Bolivia and thePhilippines, countries that have experienced largeand rapid structural changes in their economies.The risk of taking a loan was mentioned, especiallyamong first-time borrowers and older clients withlarger loan sizes. The risk of default and losingaccess to a valued financial service can be com-pounded by the loss of self-esteem, confidence,and social assets. Figure 1 shows the relativeimportance of crisis factors for clients of theUganda Women’s Finance Trust.

T h e r o l e o f f i n a n c i a l s e r v i c e s i n

d e a l i n g w i t h r i s k

In discussing the role of microfinance services inhelping clients manage risk, Rutherford considersrisk in terms of shocks and economic stress eventsthat require people to spend lump sums of moneynot readily available.2 The WDR research identi-fied clients vulnerability to shocks as a core aspectof poverty. Financial services provide the means

Ta b l e 1 : W h o m d o M F I s r e a c h ? *

Philippines (CARD) Uganda (UWFT) Bolivia (four programs) Bangladesh (BRAC)

Destitute negligible negligible negligible negligibleExtreme poor some few almost none ~40%Moderate poor many many many ~35%Vulnerable non-poor some many many ~25%

Estimates made by field research teams based on available information, including findings from secondary research, individual interviewswith staff and clients, and focus group interviews.

B o x 1 : Ye s t e r d a y ’ s N o n - P o o r …To d a y ’s P o o r

Unlike most microfinance clients, Mrs. Muwanga had limitedexperience working in the informal sector when she receivedher first Uganda Women’s Finance Trust (UWFT) loan. Mrs.Muwanga’s family was relatively well-off. Her husband was alawyer and their children were enrolled in boarding schools andMakerere University. They lived comfortably in a five-roomhouse. However, her husband suffered a stroke in April 1997and since then has been unable to work. Because of the sud-den loss of income, Mrs. Muwanga finds herself the major con-tributor to the household and the children have been withdrawnfrom school and university. Her first business venture was thebaking and sale of cakes. She made a small profit on her firstloan of around $150. During the second loan cycle, she was lesslucky. She purchased some bad flour and had to withdraw her sav-ings and sell off her cooker to repay the loan. After this experi-ence, she leased school canteen space and has begun a newbusiness providing food and snacks to the children and their teachers.Mrs. Muwanga’s story illustrates the ups and downs of incomegeneration and the dynamic characteristics of poverty.

Given the poverty alleviation objectives of manymicrofinance programs, these findings suggest astrong case for innovations—improving the designof products and services—to better meet theneeds of clients from a broader range of households,namely both the extreme poor and the vulnerablenon-poor. Such innovations, if they are to im-prove the depth of poverty outreach, shouldtake risk and vulnerability faced by the poor se-riously.

C G A PC G A PC G A PC G A PC G A P T H E C O N S U L T A T I V E G R O U P T O A S S I S T T H E P O O R E S T [ A M I C R O F I N A N C E P R O G R A M ]

for poor households to transform small sums ofsavings into usefully large lump sums, and there-fore can go a long way in decreasing vulnerability.The study found that MFIs play more of a role inhelping clients protect against risks ahead of timethan cope with shocks after they occur.

The role of financial services in protecting againstrisks ahead of time. The field research shows sev-eral strategies that individuals and households useahead of time to protect against risk. These strat-egies include diversifying income sources, build-ing up physical, financial, human and social assets,and focusing on good money management.

Financial services play an important role in thisprocess. Loans enable clients to take advantageof opportunities to build and diversify all kindsof assets that can be drawn upon in times of need.Clients use loans to diversify their sources ofhousehold income and smooth income flows andconsumption. They invest in enterprise fixed as-sets, financial assets, and physical assets, particu-larly housing (see Box 2). Microfinance is alsoused by clients to build human assets, particularlythe education of children and health care.

Participation in microfinance programs provideswomen access to knowledge and information thathelps them to interact in the outside world and per-mits the building and strengthening of social net-works. Women value group memberships, acomponent of social assets, in protecting against risk(see Box 3). By increasing women’s economic con-tributions to the household, participation in amicrofinance program can help improve their senseof self-esteem and control over assets. All of theseassets increase the options and resources availableto households in the event of a shock or stress event.

Sudden Increase in Prices

Alcoholism

School Fees

Lack of Food

Taxes

Keeping up Loan Repayments

Loss of Employment

Theft

Loss in or of Business

Sickness

Death

1987

1993

1997

1998

F i g u r e 1 : R e l a t i v e I m p o r t a n c e o f R i s k F a c t o r s f o r S e l e c t e d U W F T C l i e n t s

R E L A T I V E I M P O R T A N C E O F C R I S I S F A C T O R

0.0 10.0 20.0 30.0 40.0 50.0

B o x 3 : M u n n o M u k a b i :

I n d i g e n o u s I n s u r a n c e i n U g a n d a

The most popular type of self-help groups is known asMunno Mukabi (which translates to Friend In Need Associa-tions). Many clients of the UWFT belong to one of these.How does a typical Munno Mukabi operate? At the incep-tion a budget is agreed on and split equally among the mem-bers. The proceeds are used to purchase such assets as arerequired for most household social functions that draw largeMunno Mukabi numbers of people. These items includelarge saucepans, dishes, lanterns, canvas, etc. The func-tions include burials, weddings, children’s graduations, bap-tismal parties, etc. After the initial capital investment is made,members attend weekly or monthly meetings at which acollection is made. One group for example, collects USh200per head per sitting; others collect up to USh5,000. Thismoney is kept and lent out whenever a crisis strikes. Mem-bers also pledge to make their labor available whenever amember faces a crisis or holds a celebration.3

B o x 2 : M y H o m e i s m y C a s t l e … .

A n d W o r k p l a c e a n d R e n t a l U n i t

Multiple use of housing is especially prevalent among house-holds experiencing crisis. In Uganda there were many cases ofclients who had sub-divided their houses into rental units togenerate additional income, and other situations where houseswere put to different uses at different times of the day. A strik-ing example of the latter was a house that was used as a hairsalon during the day, as a bar in the evening and as a place tosleep at night.

In other instances business premises were used as residencesat night as a strategy to cope with a crisis. One of the clientshad the following experience: “Enforcement authorities lockedmy room, when I was away at work, saying it was an illegalstructure. While I am looking around for a new room I canafford for my family of fifteen people, at night some of themstay in the bar which my wife runs, and the others stay in thekiosk which I run.”

CRIS

IS F

ACT

OR

C G A PC G A PC G A PC G A PC G A P T H E C O N S U L T A T I V E G R O U P T O A S S I S T T H E P O O R E S T [ A M I C R O F I N A N C E P R O G R A M ]

Source: Adapted from Sebstad, Jennefer and Monique Cohen (March, 2000),“Synthesis Report on Microfinance, Risk Management and Poverty.” The report isbased on field studies by Ronald T. Chua, Paul Mosley, Graham A.N. Wright, andHassan Zaman. Paper submitted to USAID by AIMS. Washington, D.C.: Manage-ment Systems International. The note was prepared by Imran Matin and BrigitHelms of the CGAP Secretariat. Publication Manager: Tiphaine Crenn.

Maintaining access to MFI program credit, in itself,is a protectional risk management strategy for manyclients (see Box 4). They go to great lengths to en-sure repayment, particularly when confronted with acrisis or shock, often by mobilizing informal sourcesof finance to ensure repayment. Repayment meansaccess to a new loan to start back on the road to re-covery, to restock a microenterprise, to rebuild ahouse, to pay school fees.

The role of financial services in coping with shocks oreconomic stress events afterwards. Once a shock orstress event occurs, people use various coping strate-gies: they modify consumption, raise income bymobilizing labor or selling assets, they draw on in-formal and formal savings, and draw down claimson informal group-based insurance mechanisms.

The WDR field studies suggest that clients generallyuse low to medium stress strategies in coping withloss – modified consumption, labor mobilization andinformal borrowing from friends and relatives. Theyseek to conserve productive assets and thus maintainincome-earning potential when possible. Acrosscountries, clients were reluctant to withdraw childrenfrom school, cash in savings, or sell productive assets.

In general, clients tend to use informal sources ofcredit more often than MFI credit to cope with lossesfollowing a shock. When they were used, MFI ser-vices were only accessed when other sources were

exhausted or failed. Clients reported using MFI loansfollowing shocks to recover lost stock, make repairson premises or equipment, or start alternative or ad-ditional business activities. In some cases they citedusing their loans directly to smooth consumption butless frequently than expected. In the Philippines, cop-ing strategies tend to differ according to poverty levels,with poorer clients less likely to rely on borrowing(Figure 2).

Why don’t clients use MFI credit to cope with shockswhen they occur? The answer to this question iscomplex; whether it reflects a true choice or constraintdepends to a large degree on the design of the MFIloans, the timeliness and flexibility of MFI credit in re-lation to other sources, the type of shock, and alter-native options available.

T h e C h a l l e n g e : M F I p r o d u c t d e s i g n

The primary product design challenge emergingfrom this research is the need to design products be-yond credit that can help a broad spectrum of clientsmitigate the various types of risks they face and copewith crises after they have occurred. Flexible savingsand insurance, and housing, education, and emer-gency loans are examples of potential products thatcould improve clients’ ability to deal with risk. Themicrofinance industry should focus on improvingupon existing loan products and finding ways of in-troducing a broad array of products that enables cli-ents to reduce their vulnerability to risk.1 A consultation draft is available at http://www.worldbank.org/poverty/wdrpoverty. A published version should be ready in late 2000.2 Rutherford, Stuart. 2000. The Poor and Their Money. Oxford UniversityPress, India. An earlier version appeared as a Working Paper from the Insti-tute for Development Policy and Management, University of Manchester, in1999. See also CGAP Focus Note 15.

3 Wright, Graham A. N., Deborah Kasente, Germina Ssemogerere, andLeonard Mutesasira. 1999. “Vulnerability, Risks, Assets and Empowerment -The Impact of Microfinance on Poverty Alleviation” (September). Final report.Kampala,Uganda: MicroSave-Africa and Uganda Women’s Finance Trust.

F i g u r e 2 : C o p i n g S t r a t e g i e s o f C A R D B a y F G D P a r t i c i p a n t s b y P o v e r t y L e v e l

Seek Employment

Engage in Microenterprise

Borrow

Other

B o x 4 : M a i n t a i n i n g A c c e s s t o P r o

M u j e r C r e d i t i n B o l i v i a

Lupe has two businesses: snack food sales and the pro-duction of hem decorations. In 1996, she obtained herfirst Pro Mujer loan and by the time of her fifth loan, herbusiness was generating a steady profit. She then suf-fered two major crises—her son, who helped in the busi-ness, died and her husband, a wage earner, wasparalyzed—which forced her to decapitalize her business.Rather than leave the program, she withdrew funds fromher savings to pay off her loan balance. Six months later,clear of debt, her Pro Mujer group gave her a secondchance to get back on her feet. Slowly Lupe is rebuildingher business. Maintaining the relationship with Pro Mujerallowed Lupe to deal with the shock once it came.

Very Poor Poor Not so Poor Total

70%

60%

50%

40%

30%

20%

10%

0%