micro business and individual unit managerial improvement loan (marukei loan) for small businesses...

TRANSCRIPT

Micro Business and Individual Unit

Managerial Improvement Loan (MARUKEI Loan)

for Small Businesses

JAPAN FINANCE CORPORATIONMicro Business and Individual Unit (JFC-Micro)

1

Taro MORITAInternational Cooperation Office

ADFIAP International CEO Forum VII November 18, 2010, Siem Riep, Cambodia

Micro Business and Individual Unit

Content

2

1. Introduction of JFC-Micro

2. “MARUKEI Loan” Program

Appendix

1. Collaboration with Business Supporters 2. JFC-Micro’s International Cooperation

Micro Business and Individual Unit

3

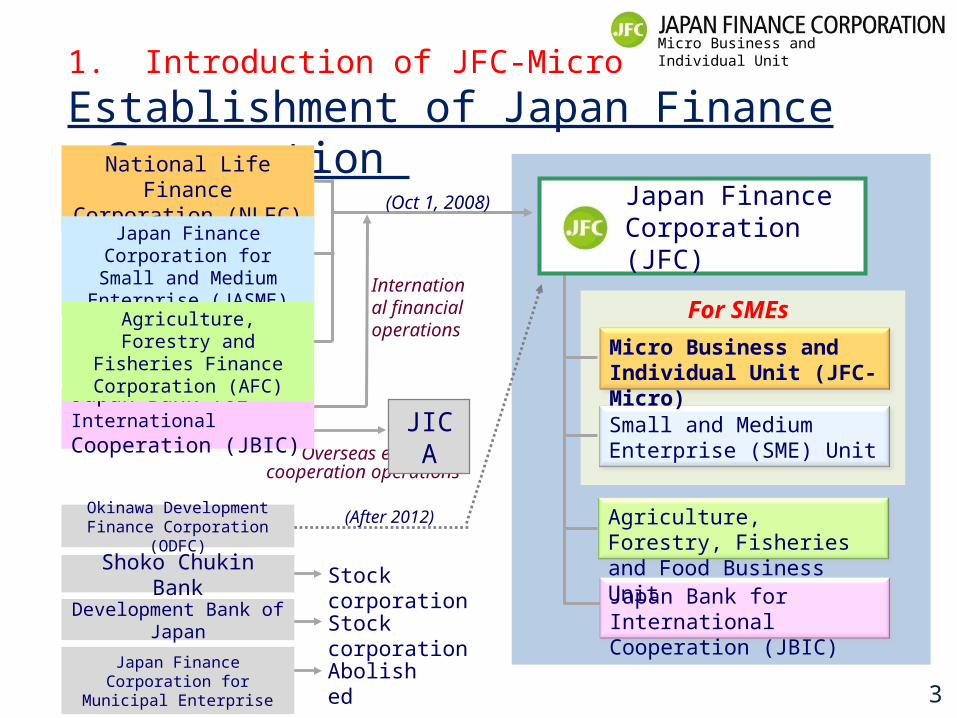

1. Introduction of JFC-Micro

Establishment of Japan Finance Corporation

International financial operations

Overseas economic cooperation operations

JICA

National Life Finance Corporation (NLFC)

Japan Bank for International Cooperation (JBIC)

Japan Bank for International Cooperation (JBIC)

Stock corporation

Stock corporation

Abolished

Shoko Chukin Bank

Development Bank of Japan

Japan Finance Corporation for Municipal Enterprise

Japan Finance Corporation for Small and Medium Enterprise

(JASME)

(After 2012)Okinawa Development Finance Corporation (ODFC)

(Oct 1, 2008) Japan Finance Corporation (JFC)

Small and Medium Enterprise (SME) Unit

Micro Business and Individual Unit (JFC-Micro)

For SMEsAgriculture, Forestry and Fisheries Finance Corporation

(AFC)

Agriculture, Forestry, Fisheries and Food Business Unit

Micro Business and Individual Unit

4

1. Introduction of JFC-Micro

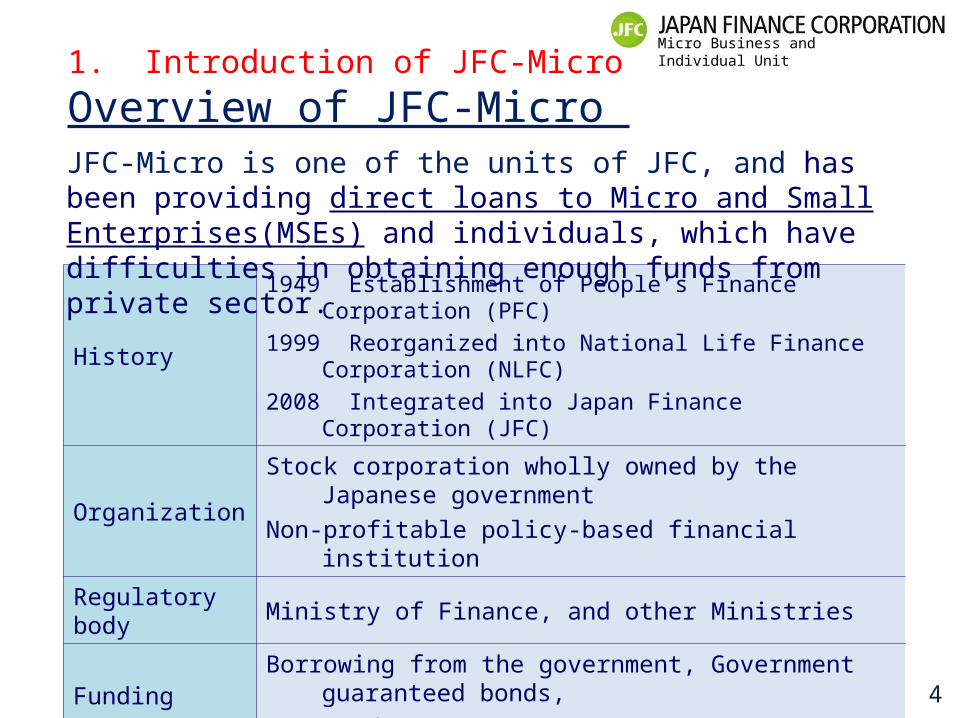

Overview of JFC-Micro

History1949 Establishment of People’s Finance Corporation (PFC)

1999 Reorganized into National Life Finance Corporation (NLFC)

2008 Integrated into Japan Finance Corporation (JFC)

OrganizationStock corporation wholly owned by the Japanese government

Non-profitable policy-based financial institution

Regulatory body Ministry of Finance, and other Ministries

FundingBorrowing from the government, Government guaranteed bonds,

JFC Bonds

Size Branch offices: 152 Employees: approx. 4,700

Loans Outstanding

Business Loans to MSEs 6,531 billion yen (=80 billion USD)

Other Loans 961 billion yen

JFC-Micro is one of the units of JFC, and has been providing direct loans to Micro and Small Enterprises(MSEs) and individuals, which have difficulties in obtaining enough funds from private sector.

Micro Business and Individual Unit

5

1. Introduction of JFC-Micro

Characteristics of JFC-Micro Loan

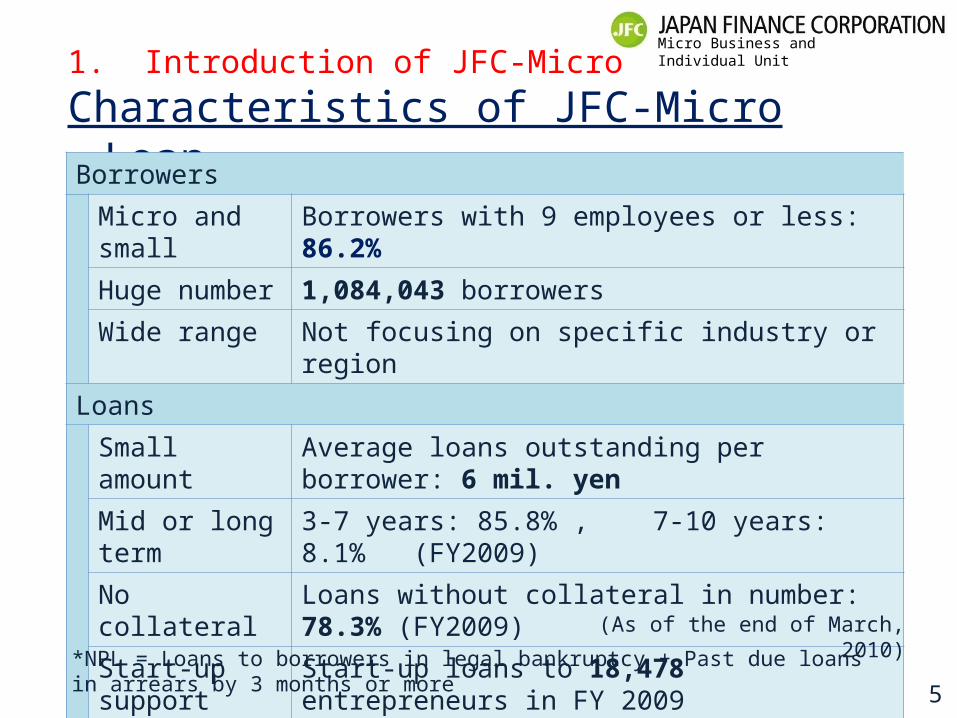

Borrowers

Micro and small Borrowers with 9 employees or less: 86.2%

Huge number 1,084,043 borrowers

Wide range Not focusing on specific industry or region

Loans

Small amount Average loans outstanding per borrower: 6 mil. yen

Mid or long term 3-7 years: 85.8% , 7-10 years: 8.1% (FY2009)

No collateral Loans without collateral in number: 78.3% (FY2009)

Start-up support Start-up loans to 18,478 entrepreneurs in FY 2009

Risk management loan

9.1% (NPL* ratio: 2.7% + Restructured loan ratio 6.4%)

*NPL = Loans to borrowers in legal bankruptcy + Past due loans in arrears by 3 months or more

(As of the end of March, 2010)

Micro Business and Individual Unit

6

1. Introduction of JFC-Micro

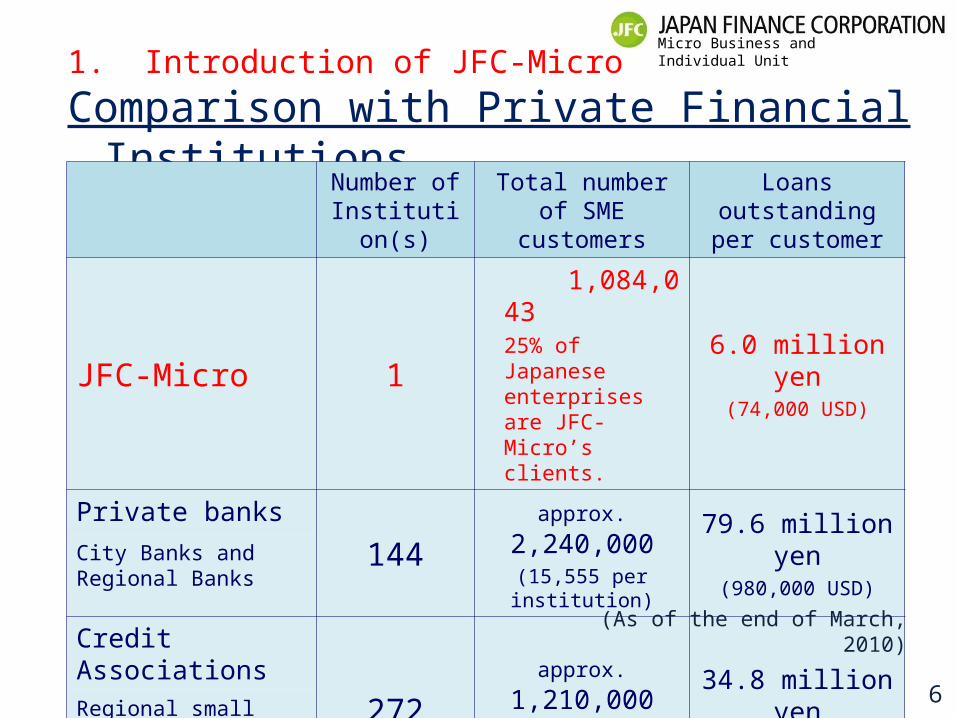

Comparison with Private Financial Institutions

Number of Institution(s)

Total number of SME customers

Loans outstanding per customer

JFC-Micro 1 1,084,04325% of Japanese enterprises are JFC-Micro’s clients.

6.0 million yen(74,000 USD)

Private banks144 approx. 2,240,000

(15,555 per institution)

79.6 million yen(980,000 USD)City Banks and Regional

Banks

Credit Associations272 approx. 1,210,000

(4,448 per institution)

34.8 million yen(430,000 USD)Regional small financial

institutions for SME

(As of the end of March, 2010)

Micro Business and Individual Unit

7

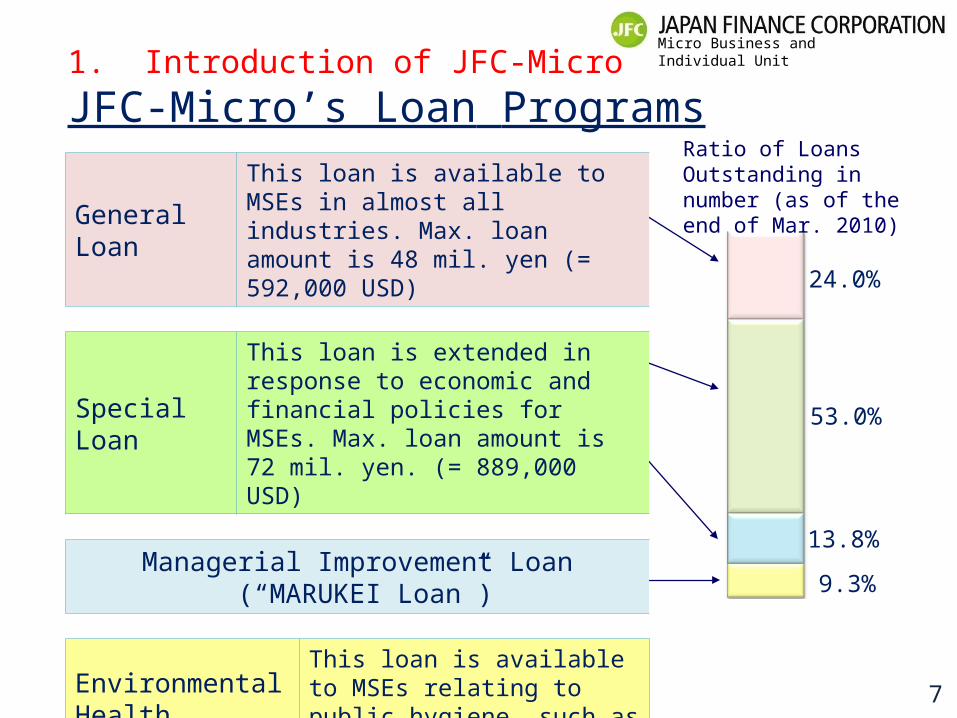

53.0%

24.0%

9.3%

13.8%

Ratio of Loans Outstanding in number (as of the end of Mar. 2010)

1. Introduction of JFC-Micro

JFC-Micro’s Loan Programs

General LoanThis loan is available to MSEs in almost all industries. Max. loan amount is 48 mil. yen (= 592,000 USD)

Special Loan

This loan is extended in response to economic and financial policies for MSEs. Max. loan amount is 72 mil. yen. (= 889,000 USD)

Managerial Improvement Loan (“MARUKEI Loan”)

Environmental Health Business Loan (EHB Loans)

This loan is available to MSEs relating to public hygiene, such as restaurants, barber shops, beauty parlors, laundries, hotels, etc.

Micro Business and Individual Unit

8

2. “MARUKEI Loan” Program

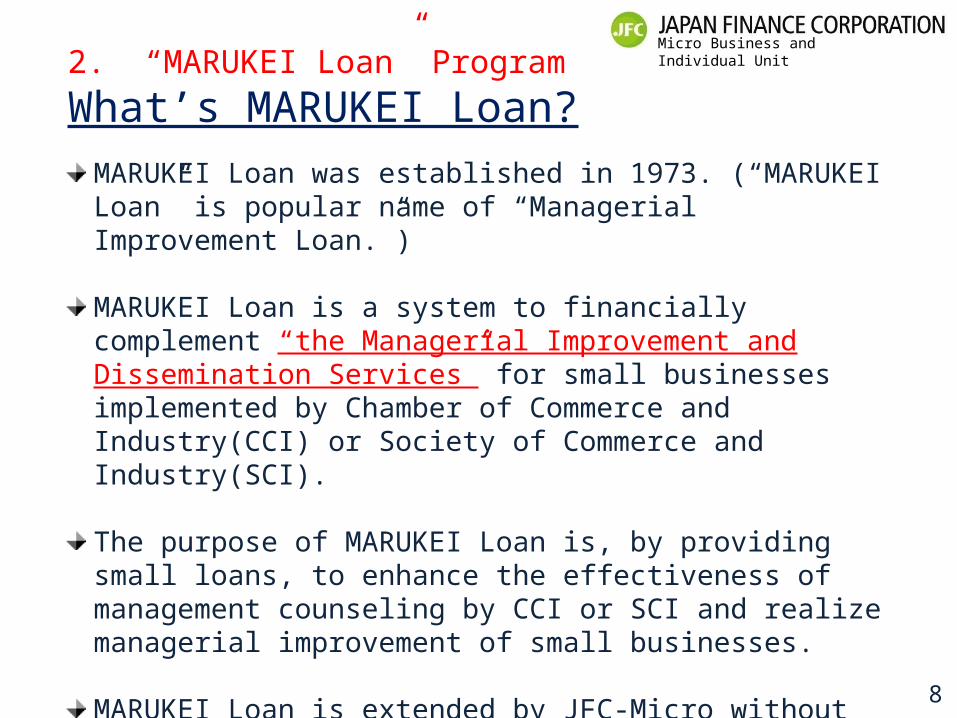

What’s MARUKEI Loan?

MARUKEI Loan was established in 1973. (“MARUKEI Loan” is popular name of “Managerial Improvement Loan.”)

MARUKEI Loan is a system to financially complement “the Managerial Improvement and Dissemination Services” for small businesses implemented by Chamber of Commerce and Industry(CCI) or Society of Commerce and Industry(SCI).

The purpose of MARUKEI Loan is, by providing small loans, to enhance the effectiveness of management counseling by CCI or SCI and realize managerial improvement of small businesses.

MARUKEI Loan is extended by JFC-Micro without taking any collateral or a guarantor on the basis of recommendation from CCI or SCI.

Micro Business and Individual Unit

9

2. “MARUKEI Loan” Program

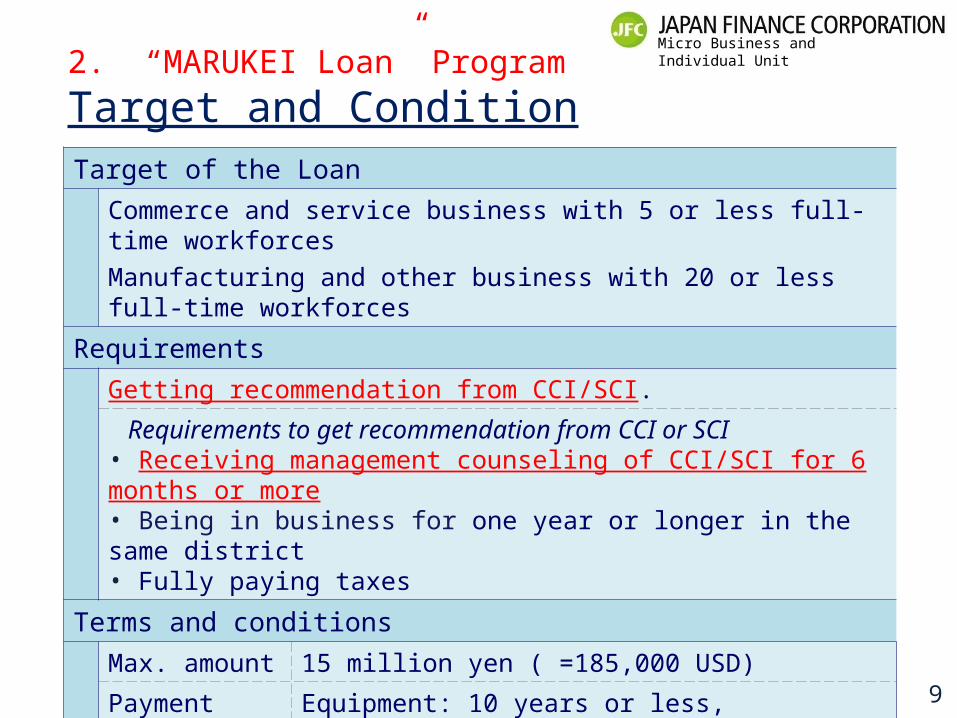

Target and ConditionTarget of the Loan

Commerce and service business with 5 or less full-time workforces

Manufacturing and other business with 20 or less full-time workforces

Requirements

Getting recommendation from CCI/SCI.

Requirements to get recommendation from CCI or SCI• Receiving management counseling of CCI/SCI for 6 months or more• Being in business for one year or longer in the same district• Fully paying taxes

Terms and conditions

Max. amount 15 million yen ( =185,000 USD)

Payment period Equipment: 10 years or less, Working: 7 years or less

Collateral Collateral or a guarantor is not necessary.

Interest rate 0.3% lower than JFC-Micro basic rate

Micro Business and Individual Unit

10

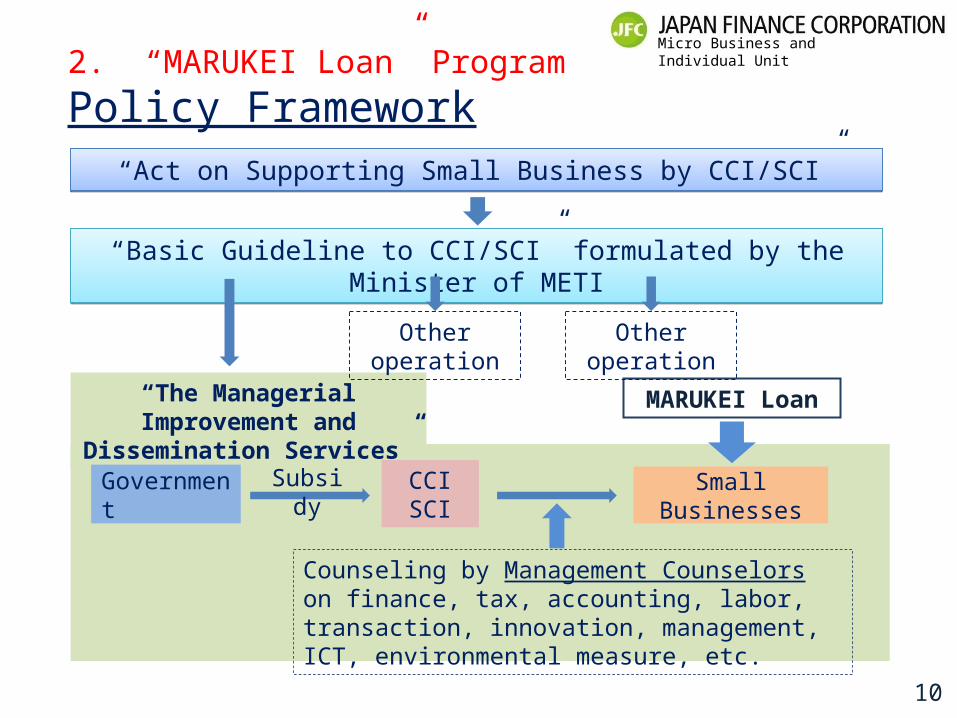

2. “MARUKEI Loan” Program

Policy Framework

“Act on Supporting Small Business by CCI/SCI”“Act on Supporting Small Business by CCI/SCI”

“Basic Guideline to CCI/SCI” formulated by the Minister of METI“Basic Guideline to CCI/SCI” formulated by the Minister of METI

“The Managerial Improvement and Dissemination Services”

Other operation

CCISCI Small BusinessesGovernment

Counseling by Management Counselors on finance, tax, accounting, labor, transaction, innovation, management, ICT, environmental measure, etc.

MARUKEI Loan

Subsidy

Other operation

Micro Business and Individual Unit

11

2. “MARUKEI Loan” Program

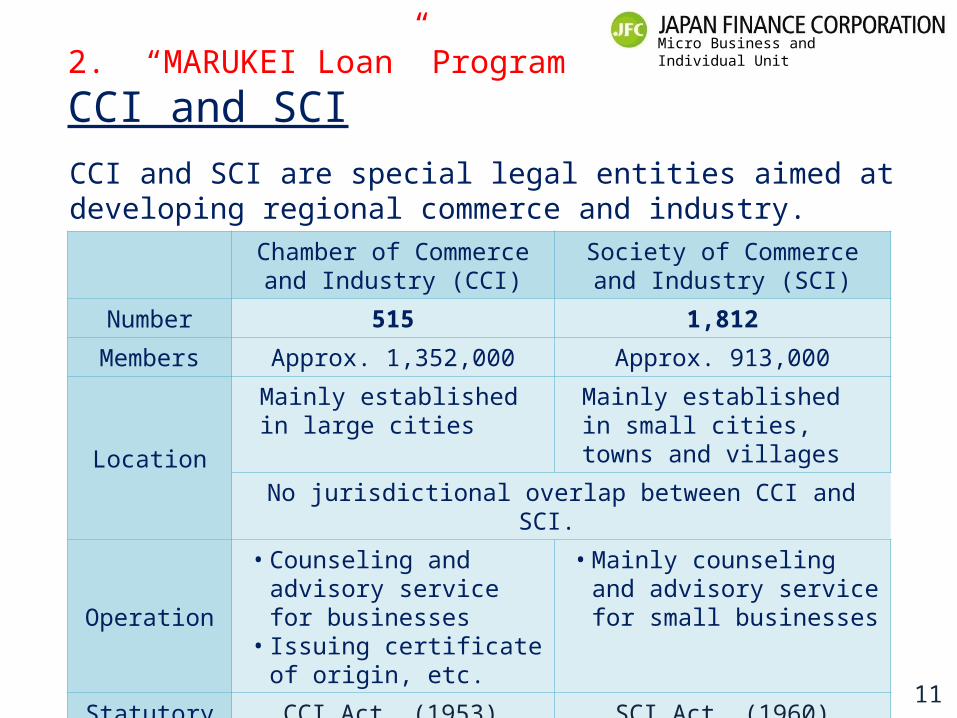

CCI and SCI

CCI and SCI are special legal entities aimed at developing regional commerce and industry.

Chamber of Commerce and Industry (CCI)

Society of Commerce and Industry (SCI)

Number 515 1,812

Members Approx. 1,352,000 Approx. 913,000

Location

Mainly established in large cities

Mainly established in small cities, towns and villages

No jurisdictional overlap between CCI and SCI.

Operation

• Counseling and advisory service for businesses

• Issuing certificate of origin, etc.

• Mainly counseling and advisory service for small businesses

Statutory Law CCI Act (1953) SCI Act (1960)

Micro Business and Individual Unit

12

2. “MARUKEI Loan” Program

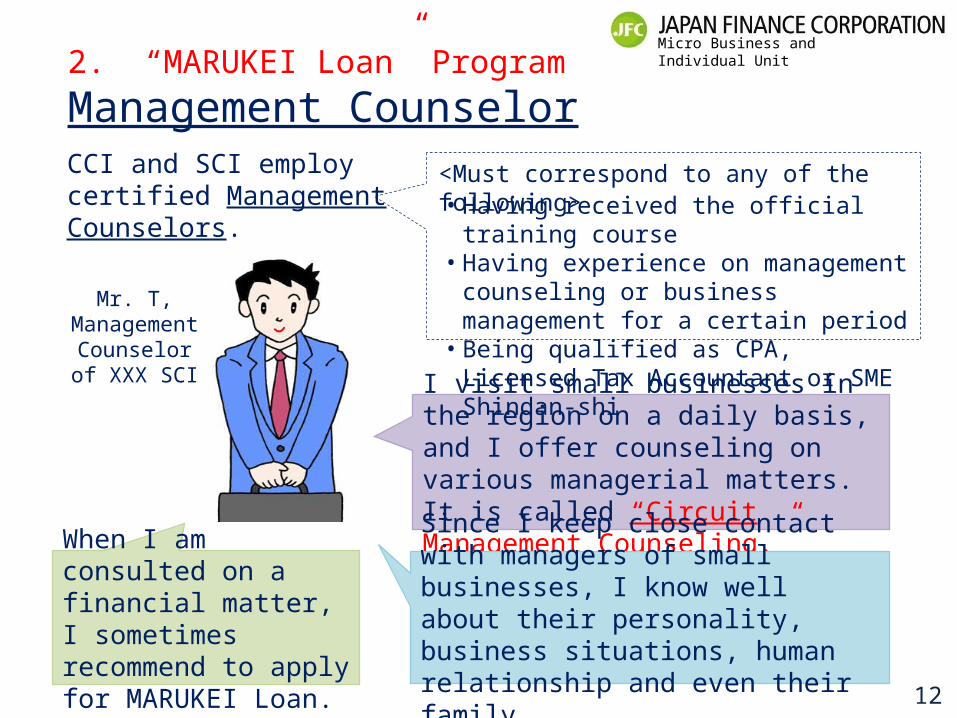

Management CounselorCCI and SCI employ certified Management Counselors.

I visit small businesses in the region on a daily basis, and I offer counseling on various managerial matters. It is called “Circuit Management Counseling.”

Since I keep close contact with managers of small businesses, I know well about their personality, business situations, human relationship and even their family.

When I am consulted on a financial matter, I sometimes recommend to apply for MARUKEI Loan.

• Having received the official training course• Having experience on management counseling

or business management for a certain period• Being qualified as CPA, Licensed Tax

Accountant or SME Shindan-shi

<Must correspond to any of the following>

Mr. T, Management

Counselorof XXX SCI

Micro Business and Individual Unit

13

2. “MARUKEI Loan” Program

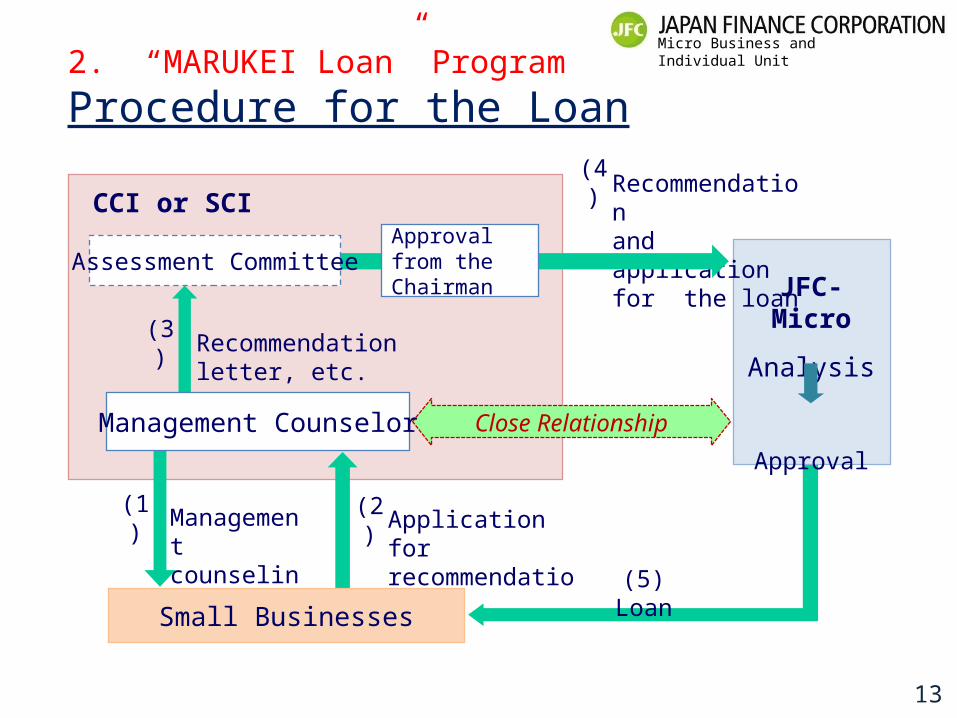

Procedure for the Loan

JFC-Micro

Analysis

Approval

Managementcounseling

(1) Application for recommendation

(2)

Recommendationand application for the loan

(4)

Recommendation letter, etc.(3)

CCI or SCI

(5) LoanSmall Businesses

Approval from the Chairman

Close Relationship

Assessment Committee

Management Counselor

Micro Business and Individual Unit

14

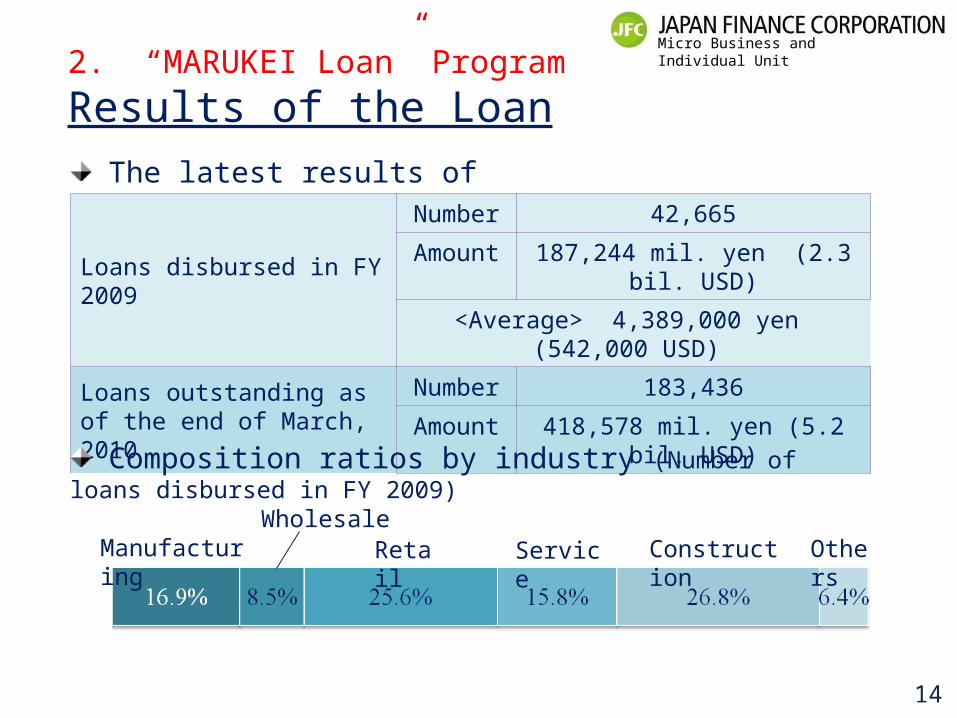

2. “MARUKEI Loan” Program

Results of the Loan

The latest results of the loan

Loans disbursed in FY 2009

Number 42,665

Amount 187,244 mil. yen (2.3 bil. USD)

<Average> 4,389,000 yen (542,000 USD)

Loans outstanding as of the end of March, 2010

Number 183,436

Amount 418,578 mil. yen (5.2 bil. USD)

Composition ratios by industry (Number of loans disbursed in FY 2009)

ManufacturingWholesale

Retail Service Construction Others

Micro Business and Individual Unit

15

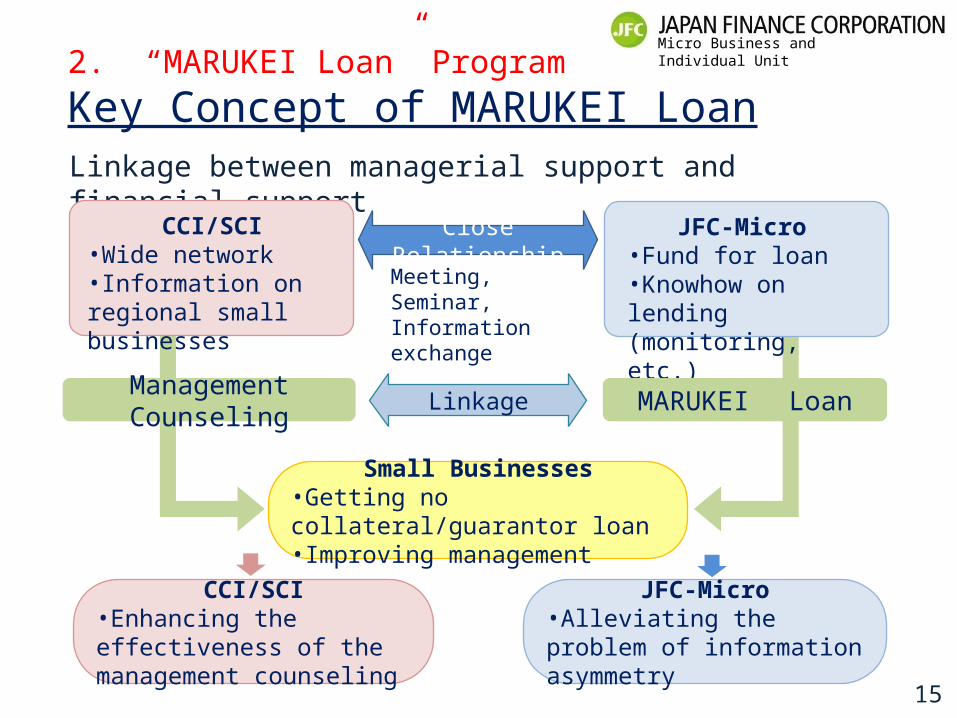

2. “MARUKEI Loan” Program

Key Concept of MARUKEI LoanLinkage between managerial support and financial support

CCI/SCI•Wide network•Information on regional small businesses

JFC-Micro•Fund for loan•Knowhow on lending (monitoring, etc.)

Close Relationship

MARUKEI Loan

CCI/SCI•Enhancing the effectiveness of the management counseling

Small Businesses•Getting no collateral/guarantor loan•Improving management

JFC-Micro•Alleviating the problem of information asymmetry

Management Counseling Linkage

Meeting, Seminar, Information exchange

Micro Business and Individual Unit

16

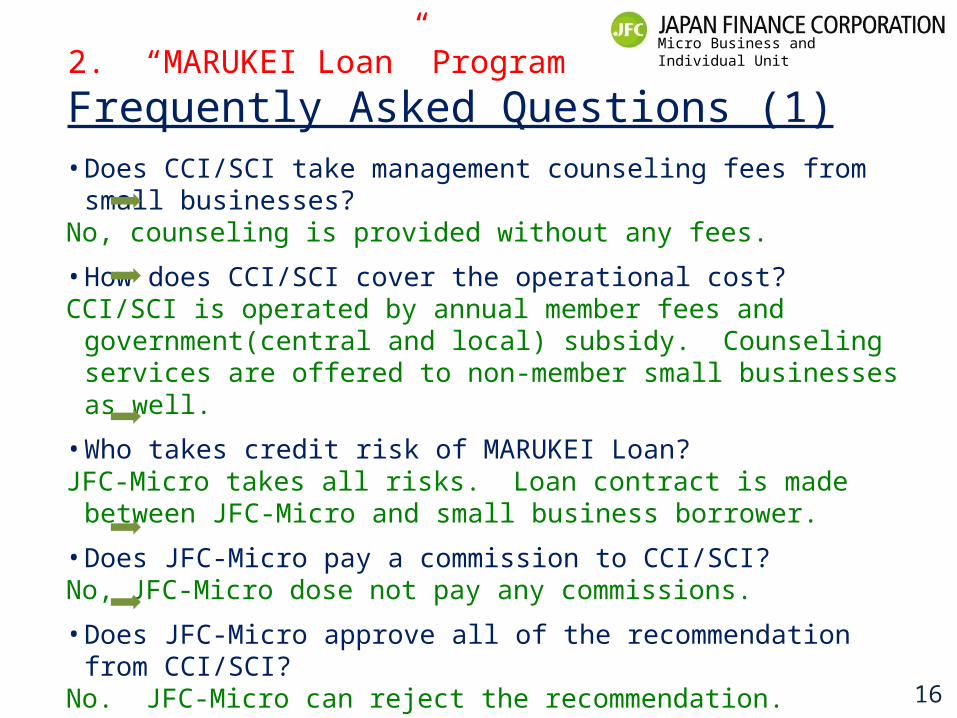

2. “MARUKEI Loan” Program

Frequently Asked Questions (1) • Does CCI/SCI take management counseling fees from small businesses?No, counseling is provided without any fees.

• How does CCI/SCI cover the operational cost?CCI/SCI is operated by annual member fees and government(central and

local) subsidy. Counseling services are offered to non-member small businesses as well.

• Who takes credit risk of MARUKEI Loan?JFC-Micro takes all risks. Loan contract is made between JFC-Micro and

small business borrower.

• Does JFC-Micro pay a commission to CCI/SCI?No, JFC-Micro dose not pay any commissions.

• Does JFC-Micro approve all of the recommendation from CCI/SCI?No. JFC-Micro can reject the recommendation. However, in reality, most of

them are approved.

Micro Business and Individual Unit

17

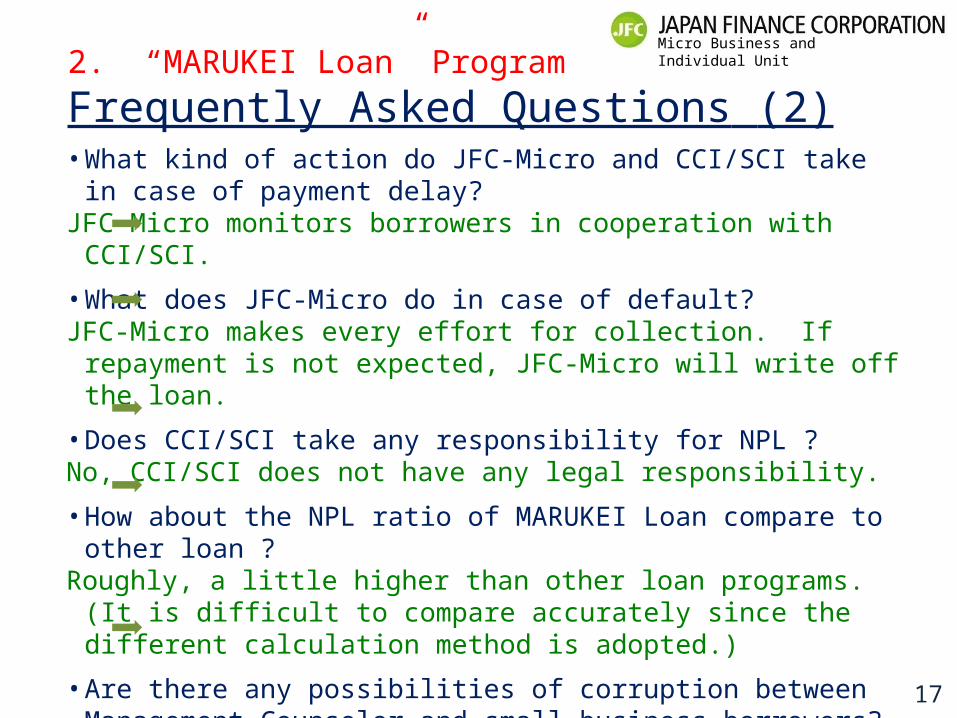

2. “MARUKEI Loan” Program

Frequently Asked Questions (2) • What kind of action do JFC-Micro and CCI/SCI take in case of payment

delay?JFC-Micro monitors borrowers in cooperation with CCI/SCI.

• What does JFC-Micro do in case of default? JFC-Micro makes every effort for collection. If repayment is not expected,

JFC-Micro will write off the loan.

• Does CCI/SCI take any responsibility for NPL ?No, CCI/SCI does not have any legal responsibility.

• How about the NPL ratio of MARUKEI Loan compare to other loan ?Roughly, a little higher than other loan programs. (It is difficult to compare

accurately since the different calculation method is adopted.)

• Are there any possibilities of corruption between Management Counselor and small business borrowers?

To avoid such situation, JFC-Micro keeps close relationship with CCI/SCI and checks carefully each recommendation before approval.

Micro Business and Individual Unit

18

Appendix 1

Collaboration with Business Supporters

Licensed Tax Accountant

Management counseling

Technical support for entrepreneurs

Financial and managerial advice

MARUKEI Loan

Business Supporters JFC-Micro

Business Startup Loan

CCI

SCI

Close Relationship

General Loan

Special Loan

+

+

+

SME

SMRJ, Local Government

University, College

NPO

SMRJ: “Organization for Small and Medium Enterprises and Regional Innovation, Japan”

Environmental Health Trade Association

Managerial advice on EHB

EHB Loans+

Micro Business and Individual Unit

19

Appendix 2

JFC-Micro’s International Cooperation

JFC-Micro has accumulated unique knowhows on Micro and Small Enterprise finance , such as credit analysis techniques, over the past 60 years. Recently, not a few foreign countries requested JFC-Micro to transfer its experience, knowledge and techniques. In order to meet these demands, JFC-Micro established International Cooperation Office in 2001.

Participating in ODA technical assistance projects by MOF, JICA, etc. in the field of SME/MSE finance

Dispatching experts to international conferences and seminars related to SME/MSE finance or microfinance.

Accepting foreign study groups and dispatching staff to seminars held in Japan to give lectures.

Micro Business and Individual Unit

20

Thank you for your attention!

<E-mail> [email protected]

<Website> http://www.k.jfc.go.jp/pfce/indexe.html

Contact Us.

International Cooperation Office,

Japan Finance Corporation,

Micro Business and Individual Unit

(JFC-Micro)