mhm executive education series webinar … · mhm executive education series: financial instruments...

TRANSCRIPT

9/20/2012

1

MHM Executive Education Series:Financial Instruments & Fair Value

Presented by:

Mike Loritz, Keith Peterka, Hal Hunt

September 20, 2012

Age

1

2

Discuss basic accounting requirements for the reporting of financial instruments at fair value

Discuss examples of valuation concepts and fundamentals for specific financial instrumentse

nda

3

4

Discuss common valuation issues for EmployeeStock Ownership Plans (ESOP)

Review common disclosure concepts andrequirements

Accounting Requirements

3

Accounting Requirements –

Financial Instruments and Fair Value

9/20/2012

2

Financial Instruments & Fair Value

Entities must apply “fair value” measurements in both recurring and non-recurring circumstances:

– Valuation of debt and equity securities with readily determinable fair values (certain industries report all securities at fair value)fair value)

– Year-end disclosure of financial instruments carried at other than fair value (debt, loans, etc.)

– Assets/liabilities acquired (assumed) in a business combination– Asset impairment testing– Valuation of derivatives and hedged items– Measurement of asset retirement obligations and financial

guarantees– Assets held for sale– Many others…

Adoption Timeline – Fair Value Measurements

FAS No. 107 & 115Investments valued at fair value

FAS No. 157 (adopt 2008)- Apply new fair value definition

ASU 2010 – 06 (adopt 2010)- Disaggregate hierarchy disclosures by “nature

and risk” class for all assets and liabilities- Disclose transfers between Level 1 and Level 2- Other new disclosures

pp y- Hierarchy disclosures (level)

FSP FAS No. 157-4 (adopt 2009)Disaggregate hierarchy disclosures by

“nature and risk” category for equity and debt securities

ASU 2009-12 “NAV” (adopt 2009)- Use of NAV as a practical expedient for alt invest.- Additional disclosures and hierarchy guidance

ASU 2010-06 (adopt 2011)Expanded disclosure of Level 3 activity

ASU 2011-04 (adopt 2012)- Description of valuation processes for Level 3- Unobservable inputs table (quantitative) for L3- Public entities to disclose all L1 and L2

transfers- Public entities to provide narrative description

of sensitivity of FV to changes in unobservable inputs (qualitative) for L3

Financial Instruments & Fair Value

9/20/2012

3

Financial Instruments & Fair Value

Investment Securities

ASC 320 – Debt and Equity Securities applies to:– Investments in equity securities that have readily

determinable fair values• The fair value of an equity security is readily determinable if sales

prices or bid-and-asked quotations are currently available on a securities exchange registered with the U.S. Securities and Exchange Commission (SEC) or in the over-the-counter market, provided that those prices or quotations for the over-the-counter market are publicly reported by the National Association of Securities Dealers Automated Quotations systems or by Pink Sheets LLC. Restricted stock meets that definition if the restriction terminates within one year

– All investments in debt securities

Financial Instruments & Fair Value

Investment Securities

ASC 320 – Debt and Equity Securities• Debt and equity securities within the scope of ASC

320 must be classified as either:320 must be classified as either:a. Trading b. Available-for-salec. Held-to-maturity*

*Although not reported at fair value, HTM securities are subject to fair value disclosures under ASC 825 as well as non-recurring OTTI measurement when appropriate.

Financial Instruments & Fair Value

Investment SecuritiesTherefore, the following securities not within the scope ofASC 320 are not required to be recorded at fair value on arecurring basis: Cost method equity securities

• Includes equity securities that do not meet the definition of“readily determinable fair value”

Equity securities that are accounted for under theequity method (ASC 323)

Investments in consolidated subsidiaries

* Derivative instruments are recorded at fair value, however, are not within the scope of ASC 320.

9/20/2012

4

Financial Instruments & Fair Value

Investment Securities - Impairment• An investment is impaired if its fair value is less than

cost. An analysis must be performed to determine if the impairment is considered other-than-temporary (OTTI).

• Analysis performed on an individual security basis– Equity Securities – Qualitative assessment– Debt Securities – An entity shall compare the present

value of cash flows expected to be collected from the security with the amortized cost basis of the security. If the present value of cash flows expected to be collected is less than the amortized cost basis of the security, an other-than-temporary impairment shall be considered to have occurred.

Financial Instruments & Fair Value

Investment Securities - ImpairmentRecognition• If sale of Equity Securities – entire difference between

cost and fair value (impairment) is recorded in earnings• Debt Securities

– Probable – Same as equity securities (difference between cost basis and fair value is recorded to earnings)

– If sale is not probable – The amount of the impairment related to credit loss is recorded through earnings and the amount related to other factors is recorded in AOCI.

Financial Instruments & Fair Value

Derivative Financial Instruments• ASC 815 “Derivatives and Hedging” provides guidance for the

recognition and measurement of derivative financial instruments.

• All derivatives are recorded on the balance sheet at fair value

• Specialized accounting may apply if a transaction qualifies for hedge accounting and the proper election is made• The special accounting applies to the hedged item (fair value)

and offsetting entry (cash flow)• Derivative is always recorded at fair value

9/20/2012

5

Financial Instruments & Fair Value

Fair Value OptionASC 825-10-15 provides for an entity to elect to account for certain financial instruments at fair value (recurring basis);• A recognized financial asset and financial liability

• A firm commitment that would otherwise not be recognized at• A firm commitment that would otherwise not be recognized at inception and that involves only financial instruments

• A written loan commitment

• The rights and obligations under certain insurance contracts

• The rights and obligations under certain warranties

• A host financial instrument resulting from the separation of an embedded nonfinancial derivative from a nonfinancial hybrid instrument under paragraph 815-15-25-1

Financial Instruments & Fair Value

Accounting Standards Codification (ASC) 820, Fair Value Measurements and Disclosures provides guidance with respect to:

• Defines fair value

• Sets out a framework for measuring fair value, which refers to certain valuation concepts and practices

• Requires certain disclosures about fair value measurements

ASC 820 does not provide guidance with respect to the recognition or classification of financial

instruments.

Financial Instruments & Fair Value

FASB ASC 820 includes disclosure requirements which are identified as measurement on a recurring basis or nonrecurring basis. • Disclosure requirements include the valuation techniques and

inputs used to develop fair value measurements for • assets and liabilities that are measured at fair value on a

recurring basis in periods subsequent to initial recognition and

• non-recurring measurements recorded during the period.

• The level within the fair value hierarchy in which the fair value measurement in its entirety falls

9/20/2012

6

Financial Instruments & Fair Value

FASB ASC 825-10-50 provides additional guidance with respect to fair value disclosures for (1) all public companies, (2) all nonpublic companies with total assets greater than $100 million, and (3) any company that holds or uses derivative financial instrumentsinstruments. • Requires fair value disclosure of all financial instruments on the

company’s balance sheet as well as the methods and significant assumptions used to determine fair value.

• The disclosure requirements apply regardless of the recognition and measurement of the financial instruments in the financial statements.

• ASU 2011-04 now requires disclosure of the classification within the fair value hierarchy as well.

Financial Instruments & Fair Value

Fundamentals of Fair Value per ASC 820:1. Must use market participant view in measuring fair

value (not entity specific view)

2 Fair value represents an exit price in the entity’s2. Fair value represents an exit price in the entity s principal or most advantageous market– The price that would be received for selling an asset

– The price that would be paid to transfer a liability

3. Provides for a hierarchy that requires the use of observable market inputs when available– Entity specific inputs are allowed when observable market data

is not available, however, it must be from a market participant’s view!

Financial Instruments & Fair Value

Common issues related to fair value of financial instruments:

– Bid/ask prices – middle range allowed

– Transactions costs – should not be includeda sac o s cos s s ou d o be c uded

– Blockage discounts – should not be included

– Inclusion of an entity’s own credit risk - required

– Net Asset Value (NAV) – may not be fair value

– Control premiums – may be applied to Level 2 or 3 securities

– Restricted Securities – restriction must be included

9/20/2012

7

Financial Instruments & Fair Value

• In exchange traded markets, exit prices should be based on closing market prices• May need policy election if equity securities traded on a

continuous or foreign market

• In broker/dealer markets, bid/ask prices are more readily available than closing prices:• Fair value represents the price within the bid/ask spread that

would be received to acquire the asset or transfer the liability.

• Mid-market pricing or other pricing conventions can be used as a practical expedient for fair value measurements.

• Offsetting positions should be consistent between the long and short positions.

Financial Instruments & Fair Value

Most Advantageous Market – Level One SecuritiesCompany A owns 1,000 shares of XYZ Corp common stock. XYZstock trades on the NYSE and the Tokyo Stock Exchange routinely inboth markets. Company A believes they could sell the entire block ofshares at a $ 25 per share discount Information as of December 31shares at a $.25 per share discount. Information as of December 31,2011 is as follows:

Closing Costs Net Proceeds

NYSE $5.00 $.50 $4.50

TSE $5.45 $1.00 $4.45

What is the fair value of the shares held by Company A?

What if the transaction costs in NYSE were the

same as TSE?

Financial Instruments & Fair Value

Valuation techniques:When fair value is directly observable (exchange traded), the quoted market price must be used for measuring fair value, generally without any adjustments.

P ibl ti f i ti k t- Possible exceptions for inactive markets

• ASC 820-10-35-24A describes three commonly accepted valuation techniques:

– Market approach

– Income approach

– Cost approach

9/20/2012

8

Financial Instruments & Fair Value

Market Approach • Level 1 securities• The fair value of a

private equity security may be estimated based on observable EBITDA multiples, market caps, etc. for similar companies

Income Approach• Interest rate swap

discounted cash flows

• Option Black Scholes, Monte Carlo model (or other option models

• Private company equities - DCF

Cost ApproachGenerally not

applicable to financial instruments (start up

phase company equities possibly)

Valuation ConceptsValuation Concepts

Fair Value – Financial Instruments

LoansLoans receivable that are not debt securities will bereported on the balance sheet using one of three models:

• Held for sale Lower of cost or fair value*• Held-for-sale - Lower of cost or fair value

• Loans held for investment - Amortized cost less an allowance for credit losses.*

• Fair value for loans for which the option under ASC 825-10 has been elected.

*However, fair value disclosures may still be required under ASC 325

9/20/2012

9

Fair Value – Financial Instruments

Loans – Fair Value Measurements• Fair value is generally determined based on the loans

expected future cash flows discounted at market rates.– Impairments are measured using the loan’s effective rate

• Mortgage loans held for sale may use a market approach.(as market observable data may be available)

• Credit impaired loans – the credit impairment may beincorporated into the estimated cash flows or the discountrate.

• Collateral dependent - A company must measure impairmentbased on the fair value of the collateral once the creditordetermines foreclosure is probable.

Fair Value – Financial Instruments

Investment Securities (as defined by ASC 320)

• EQUITY - Publically traded equity securities andpublically traded debt are level 1 securities and shoulduse the closing price on the applicable exchange.g p pp g

• DEBT - Most debt securities (including most USTreasuries) are valued using a pricing model and arelevel 2 securities.– Proprietary models used by pricing services.

– Use inputs such as credit risk and interest rates.

– To be level 1, the bond must be traded and have a marketobservable price.

Fair Value – Financial Instruments

Investment Securities (as defined by ASC 320)

• MUTUAL FUND – a mutual fund is not an exchangetraded instrument

– Classification may depend on the level of activityClassification may depend on the level of activity.Most open-end funds sell shares to the public everybusiness day which are priced at net asset value(NAV).

– Closed-end funds and some open-ended funds thatare infrequently traded may be level 2 measurements(or considered a NAV practical expedient).

9/20/2012

10

Fair Value – Financial Instruments

Alternative Investments

May report the investment in these funds at the net asset value (NAV) in certain instances.

–Entities that apply the investment guide and meet certain criteriaEntities that apply the investment guide and meet certain criteria (ASC 946-10-15-2)

–Entities that report a NAV or it equivalent (real estate fund)

Definition

Investments in private investment funds; including investments in hedge funds, private equity funds, venture capital funds, commodity funds, real estate funds, offshore

fund vehicle, and fund-of-funds, as well as bank common/collective trust funds.

Fair Value – Financial Instruments

Alternative Investments

Required disclosures if the NAV is used include alldisclosures required by ASC 820 plus several specificdisclosures regarding each major investment categoryg g j g yreported at the NAV.

– Liquidation restrictions, including estimated period oftime

–Unfunded commitments

–Redemption rights and other restrictions

–Potential sale at amount other than NAV

Fair Value – Financial Instruments

Private Company Equity Securities

• If quoted prices in active markets or arm’s lengthtransactions have occurred for the entity’s equitysecurities, use that information first.,

• If not, then management should select the valuationmethod(s) that are appropriate for their industry, lifecycle, etc.– A single valuation method may be appropriate

– Or, it may be more appropriate to use multiple valuationmethodologies (typically market and income approach)

9/20/2012

11

Fair Value – Financial Instruments

Private Company Securities

• Valuation should consider the relative applicability of the valuation techniques used given:– Nature of the industryNature of the industry

– Current market conditions

– Quality, reliability and verifiability of the data used in each model

– Comparability of public entity or transaction data used

– Additional considerations unique to the entity

• Consideration should be given to significant differences in valuation methodologies (why are they different?)

Fair Value – Financial InstrumentsPrivate Company Securities

• Market Approach – Market value of equity (MVE) to net income or book value

– Enterprise value to EBIT

E t i l t EBITDA– Enterprise value to EBITDA

– Enterprise value to revenue

– Enterprise value to debt free cash flows

– Enterprise value to book value of assets

• Income Approach– Discounted cash flows

– Probability weighted cash flows

Typically, a combination of these methods is appropriate.

Fair Value – Financial Instruments

Interest rate swaps are not traded on an exchange, thus the income approach is t i ll d t

Settlement Value (received from the counterparty) vs Fair Value

typically used to measure fair value

• Settlement value does not consider counterparty (CVA) or company specific creditworthiness (DVA), thus does not represent fair value

• Many times the amount reported by the counterparty includes accrued interest receivable/payable

Interest Rate Swaps

9/20/2012

12

Fair Value – Financial Instruments

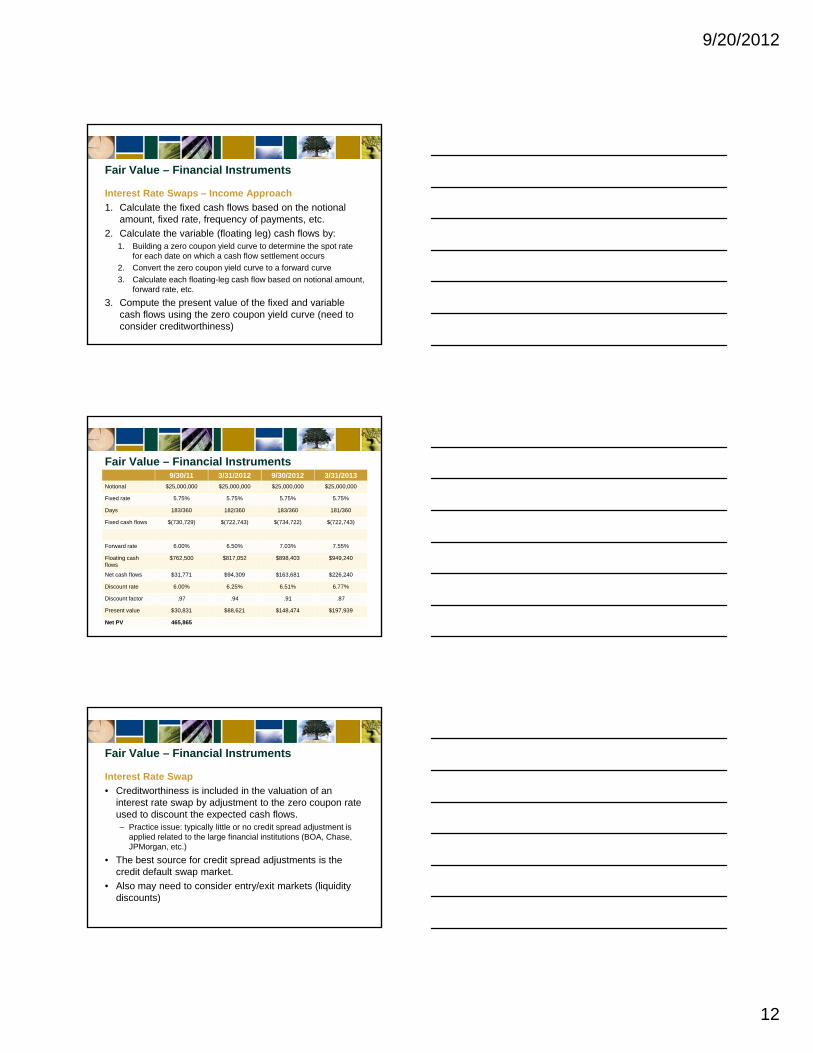

Interest Rate Swaps – Income Approach

1. Calculate the fixed cash flows based on the notional amount, fixed rate, frequency of payments, etc.

2 Calculate the variable (floating leg) cash flows by:2. Calculate the variable (floating leg) cash flows by:1. Building a zero coupon yield curve to determine the spot rate

for each date on which a cash flow settlement occurs

2. Convert the zero coupon yield curve to a forward curve

3. Calculate each floating-leg cash flow based on notional amount, forward rate, etc.

3. Compute the present value of the fixed and variable cash flows using the zero coupon yield curve (need to consider creditworthiness)

Fair Value – Financial Instruments9/30/11 3/31/2012 9/30/2012 3/31/2013

Notional $25,000,000 $25,000,000 $25,000,000 $25,000,000

Fixed rate 5.75% 5.75% 5.75% 5.75%

Days 183/360 182/360 183/360 181/360

Fixed cash flows $(730,729) $(722,743) $(734,722) $(722,743)

Forward rate 6.00% 6.50% 7.03% 7.55%

Floating cash flows

$762,500 $817,052 $898,403 $949,240

Net cash flows $31,771 $94,309 $163,681 $226,240

Discount rate 6.00% 6.25% 6.51% 6.77%

Discount factor .97 .94 .91 .87

Present value $30,831 $88,621 $148,474 $197,939

Net PV 465,865

Fair Value – Financial Instruments

Interest Rate Swap

• Creditworthiness is included in the valuation of an interest rate swap by adjustment to the zero coupon rate used to discount the expected cash flows.p– Practice issue: typically little or no credit spread adjustment is

applied related to the large financial institutions (BOA, Chase, JPMorgan, etc.)

• The best source for credit spread adjustments is the credit default swap market.

• Also may need to consider entry/exit markets (liquidity discounts)

9/20/2012

13

Fair Value – Financial Instruments

Option Contract

• An option provides one party with the option, however, not the obligation, to buy or sell something in the future.

• Some options are publically or exchange tradedSome options are publically or exchange traded, however, most are not.

• Options issued as share based compensation typically are not the same as traded options.

• Options are typically valued using the income approach (if market observable data is not available).– Black-Scholes Merton

– Monte-Carlo

Fair Value – Financial Instruments

Option Contract

Inputs to a basic option pricing model:1. Underlying price (stock price)

2 St ik ( i ) i2. Strike (exercise) price

3. Term (time to expiration)

4. Risk-free interest rate

5. Expected dividends

6. Volatility

Fair Value – Financial Instruments

Option ContractThe Black Scholes model acts in a manner to predict theexpected intrinsic value of the instrument on the date the optionwill be exercised (an expected forward stock price is determined).

–Growth is assumed at the risk-free rate.

–Holding costs (dividends, borrowings, etc.) are deducted.

–Use of implied volatility to project a range of stock prices at the exercise date.

–Differences between estimated stock prices and the strike price are weighted to determine the expected intrinsic value.

–The expected intrinsic value is discounted using the risk free interest rate.

9/20/2012

14

Fair Value – Financial Instruments

Stock Price $5.00 $6.00 $5.00 $5.00

Exercise price $5.00 $5.00 $5.00 $5.00

Current date 1/1/2011 1/1/2011 1/1/2011 1/1/2011

Expiration d t

1/1/2016 1/1/2016 1/1/2021 1/1/2016date

Volatility 25% 25% 25% 60%

Risk free rate 3.00% 3.00% 3.00% 3.00%

Dividend yield 1.00% 1.00% 1.00% 1.00%

Fair Value $.7865 $1.3076 $.8926 $2.0337

Fair Value – Financial Instruments

Cash Equivalents

Many reporting entities classify certain short-term debt andequity securities, such as treasury bills, commercial paperand money market funds, as part of cash equivalents.y , p q

– These securities represent financial instruments andare still subject to the fair value disclosurerequirements of ASC 820.

– Given the short maturity, in most cases there will be nosignificant difference between the carrying value andfair value.

Fair Value – Financial Instruments

Certificates of Deposit

• Certificates of deposit are financial instrumentssubject to fair value disclosures.– A bank CD typically does not meet the definition of aA bank CD typically does not meet the definition of a

security (as defined in ASC 320), thus is not subject to theclassification guidance in ASC 320.

– Additionally, a CD typically would not be considered asecurity for purposes of applying the Not-for-Profitmeasurement guidance. However, if the NFP holdsany negotiable CDs, you would likely need toevaluate further.

9/20/2012

15

Fair Value – Financial Instruments

Fair Value – Liabilities

Absent a quoted price for a liability, exit price should be determined from the perspective of a market participantdetermined from the perspective of a market participant that holds the identical liability as an asset, even when

the asset is not traded (level 3 measurement).

Fair Value – Financial Instruments

Fair Value – Liabilities

The fair value of a company’s debt is typically determined using an income approach (DCF) which is driven by two main inputs:p

1. Interest rates

2. The Company’s own creditworthiness– A decrease in an entity’s creditworthiness can be

included in two different ways:

» Adjusting the discount rate

» Adjusting the estimated cash flows (payments)

The carrying amount of variable rate debt is typically not equal to fair value!

Employee Stock Ownership Plans

45

Employee Stock Ownership Plans

9/20/2012

16

ESOP & Valuation Issues

What is an ESOP?• An ESOP is a qualified, defined contribution employee benefit plan

that invests primarily in the stock of the employer company.

• ESOPs are “tax-qualified” in return for meeting certain rules designed to protect the interests of plan participants anddesigned to protect the interests of plan participants and beneficiaries.

• ESOP sponsors (and selling shareholders in certain situations) also receive various tax benefits.

• A valuation of ESOP shares by an independent third party is required by the Department of Labor (DOL) and the Internal Revenue Service (IRS) to insure that the value is determined by a party who does not have a personal or financial interest in the valuation result.

ESOP & Valuation Issues

What is the standard of value in ESOP valuations?• The IRS standard is "Fair Market Value".

• Fair Market Value has a great deal of case law behind it.

• The definition of Fair Market Value is most clearly defined by the IRS in Revenue Ruling 59 60IRS in Revenue Ruling 59-60.

• The DOL substantially embraces all of the aspects of Fair Market Value as defined in Revenue Ruling 59-60, but the ERISA legislation imposes additional considerations.

• ERISA mandates that all qualified plans have a trustee, and the trustee has to act in the best interests of the plan participants.

• ERISA imposes fiduciary responsibilities on all of the trustees. Fiduciary responsibilities are often at the center of ESOP based valuation litigation.

ESOP & Valuation Issues

What is “Fair Market Value”?

• Fair Market Value is the price for which property would sell under the existing market conditions for such property as established in arms-length negotiations b t k l d bl d i d d t tibetween knowledgeable and independent parties.

• The “Market” implied in definitions of Fair Market Valueencompasses all potential buyers and sellers of the property involved.

9/20/2012

17

ESOP & Valuation Issues

How is “Fair Market Value” determined?• The Fair Market Value of business interests that is generating

earnings is determined to a large degree on the basis of what a knowledgeable buyer would be willing to pay for the earnings stream considering available rates of return on relatively risk-free g yinvestments and the risks associated with the investment being appraised.

• The present value of future earnings using a risk adjusted market rate is one of the most common approaches, referred to in business valuations as Discounted Future Earnings (DFE).

• Reference to the results of mathematical formulas is not the sole determinant of Fair Market Value.

• Court cases continue to support the usage of both Discounts for Lack of Control and Discounts for Lack of Marketability under the Fair Market Value standard.

ESOP & Valuation Issues

Would the valuation methodology employed by the ESOP fiduciary (i.e. Fair Market Value) vary from that of Topic 820 (i.e. Fair Value)?• May be consistent when public companies are the ESOP plan

sponsors:sponsors:

• Topic 820 stipulates that “fair value” must be determined based upon observable inputs (e.g. quoted market prices) where available.

• The tax code stipulates that only ESOP’s holding shares traded on an exchange that is registered under Section 6 of the Securities Exchange Act of 1934 may rely upon quoted prices as the measurement of value. All other securities must be subject to valuation based upon an independent appraisal.

ESOP & Valuation Issues

Would the valuation methodology employed by the ESOP fiduciary (i.e. Fair Market Value) vary from that of Topic 820 (i.e. Fair Value)?• However, the two rules may be in conflict when:

Th iti t d d th O th t B ll ti B d– The securities are traded on the Over-the-counter Bulletin Board (“OTCBB”). The OTCBB may constitute an active market for certain securities, but in Notice 2011-19, the IRS emphasized that such securities must still be valued based upon an independent appraisal for purposes of those Code sections which rely on fair value of ESOP securities.

– The fiduciary uses the market to set the ESOP price, but it is the average of the 20 trading days prior to year-end, rather than the year-end price. Topic 820 would require the year-end price.

9/20/2012

18

ESOP & Valuation Issues

May be inconsistent when private companies are the ESOP plan sponsors:

• Topic 820 stipulates certain constraints with respect to the measurement of fair value with which the fiduciary

tmay not agree.

• For example, premiums or discounts based upon the size of a holding are not recognized under GAAP.

• The fiduciary might, however, conclude that such premiums or discounts should be recognized for purposes of the Employee Retirement Income Security Act and the Internal Revenue Code (IRC).

ESOP & Valuation Issues

What are we to do when inconsistencies arise?

• Every situation is unique and requires careful analysis.

• Where such circumstances arise, it is important that our terminology clearly distinguishes what amount that is the ESOP fiduciary’s determination of value, as opposed to the Topic 820 measurement of fair value.

• Next course of action would involve the ESOP trustee, the valuation firm, ERISA counsel and others.

Disclosures

54

Disclosures

9/20/2012

19

Financial Instruments & Fair Value

Disclosures

The following disclosures are required by ASC 820:• The fair value measurement at the end of the reporting period

• The level within the fair value hierarchy (Level 1 2 or 3) (1)• The level within the fair value hierarchy (Level 1, 2, or 3) (1)

• The amounts of any transfers between Level 1 and Level 2 ofthe fair value hierarchy (recurring only)*

• A description of the valuation technique(s) and the inputsused in the fair value measurement for Level 2 and 3instruments. (1)

• A reconciliation from the opening balances to the closingbalances for Level 3 instruments as well as realized andunrealized gains/losses.

Financial Instruments & Fair Value

Disclosures

• A description of the valuation processes used todetermine fair value of Level 3 instruments

• A narrative description of the sensitivity of the Level 3A narrative description of the sensitivity of the Level 3fair value measurements to changes in unobservableinputs*

• Disclosure not required by non-public entities

(1) Denotes disclosure required for financial instruments in which fair value is disclosed in accordance with ASC 825 only (public companies only – not applicable to non-public entities)

Financial Instruments & Fair Value

Disclosures

• ASC 820 encourages companies to combine the requireddisclosures under ASC 820 and ASC 825, if applicable,however, such combined presentation is not required., p q

• The guidance in ASC 820 requires the fair valuedisclosures (quantitative and qualitative) to bedisaggregated by class of assets and liabilities rather thanby major category.

–As a result, fair value measurements will typically requiregreater disaggregation than the related line item(s) in thebalance sheet.

9/20/2012

20

Fair Value – Financial Instruments

Some typical classifications within the hierarchy:Investment Level

Traded equities Level 1

US T-Bills Level 1/2

US Treasuries Level 2

Municipal securities Level 2

US Agency securities Level 2

Private (hedge) funds Level 2/3

Private company equities Level 3

Private company debt Level 3

Funds - Net Asset Value (NAV) Level 2/3

Certificates of deposit Level 2

Mutual Funds Level 1/2

Speaker BiographyMichael Loritz, CPA

Shareholder, Mayer Hoffman McCann P.C.

913.234.1226

Mike has 15 years of public accounting experience with financial and service basedcompanies, including the engineering and construction industry. He is a member of theMHM's Professional Standards Group, providing accounting knowledge leadership in theareas of derivative financial instruments, share-based compensation, fair value, leasing,revenue recognition and others.

Mike's experience includes over 14 years with a Big Four firm where he was responsiblefor client service for large and small SEC filers and non-public entities, audit/accountingtechnical expertise and training instruction and delivery.

Speaker BiographyKeith Peterka, CPA

Shareholder

Mayer Hoffman McCann P.C.

610.862.2744

With more than 19 years of experience in public accounting, Keith performs national firmresponsibilities for IFRS, fair value accounting and auditing, revenue recognition andbusiness combinations. He has also developed national training programs for accountingpronouncements and complex accounting topics.

Keith is a subject matter expert for IFRS, SEC reporting and fair value accounting inMHM’s Professional Standards Group. He also is a member on the IFRS Foundation'sSmall & Medium-sized Entities (SMEs) Implementation Group.

9/20/2012

21

Speaker BiographyHal Hunt, CPA

Shareholder

Mayer Hoffman McCann P.C.

913.234.1012

Hal leads MHM’s Employee Benefit Plan Audit Practice. With over 25 years of diverseexperience with employee benefit plan accounting, auditing and compliance issues, he isalso a member of the firm’s Professional Standards Group as subject matter expert onEBP plan audits, as well as Business Combinations and Leasing.

As the National Practice Leader for EBP Audits, Hal is responsible for providing internaltraining on the subject, along with providing technical support to engagement teams,serving as engagement quality reviewer and developing resource tools for our EBP auditprofessionals.

Q ti ?Questions?