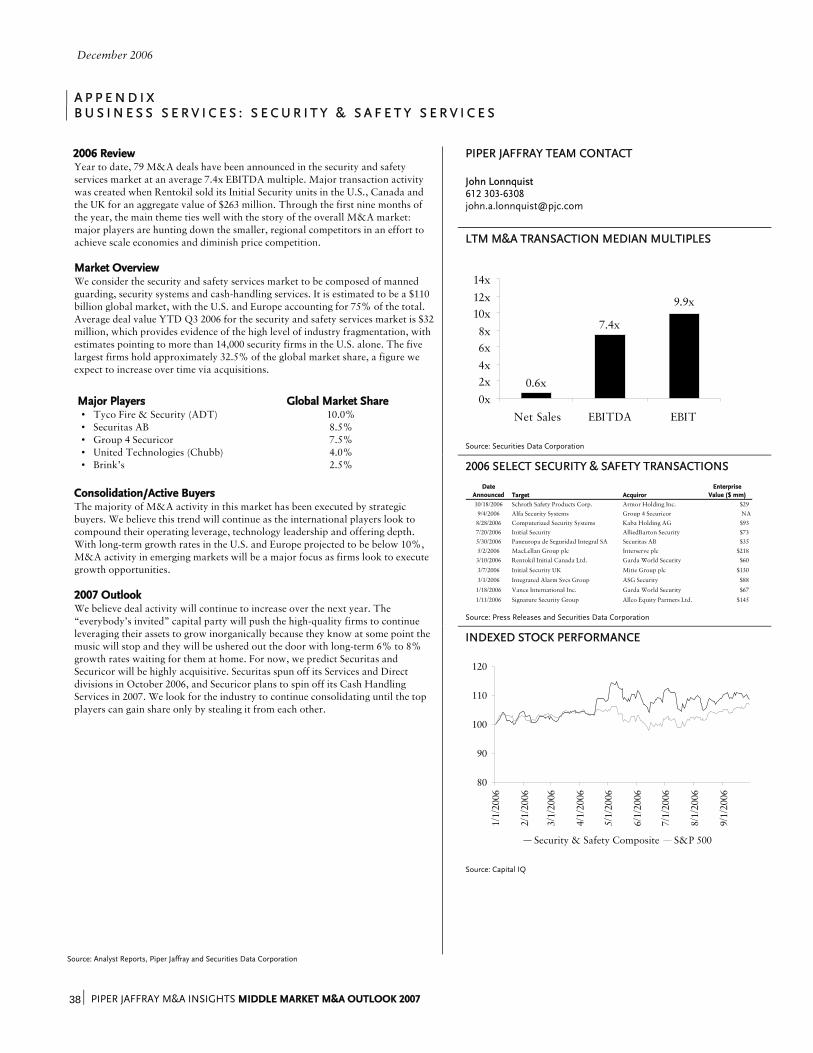

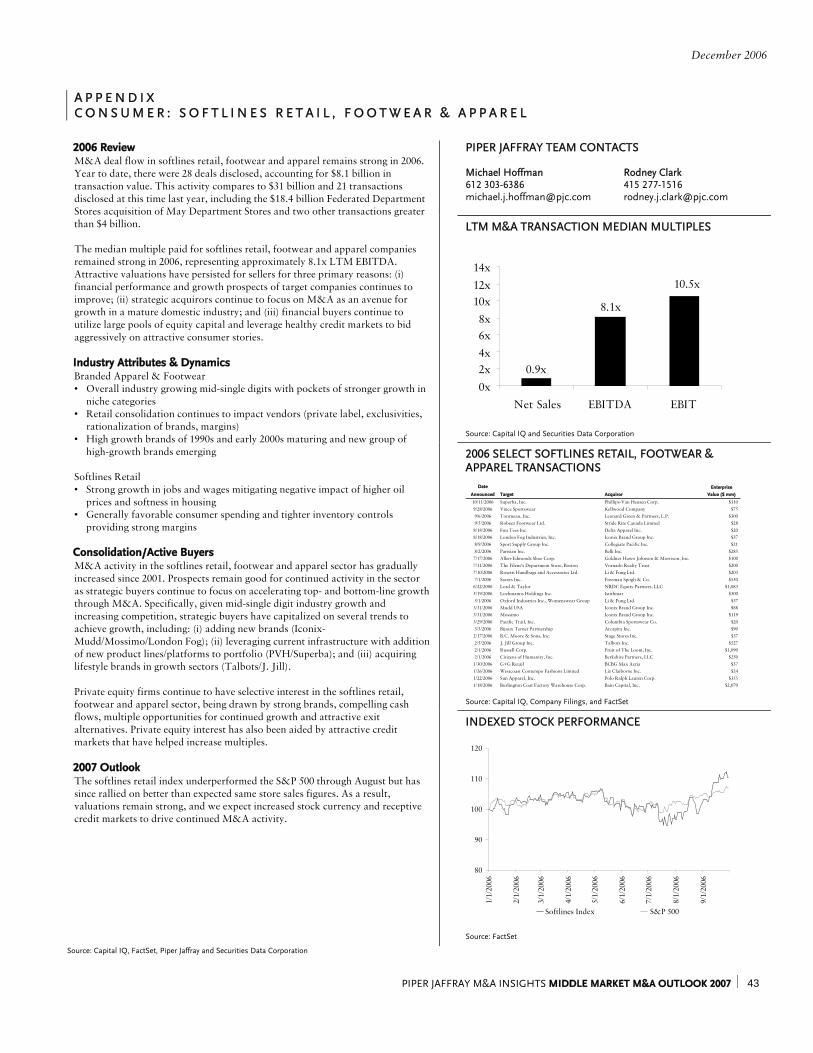

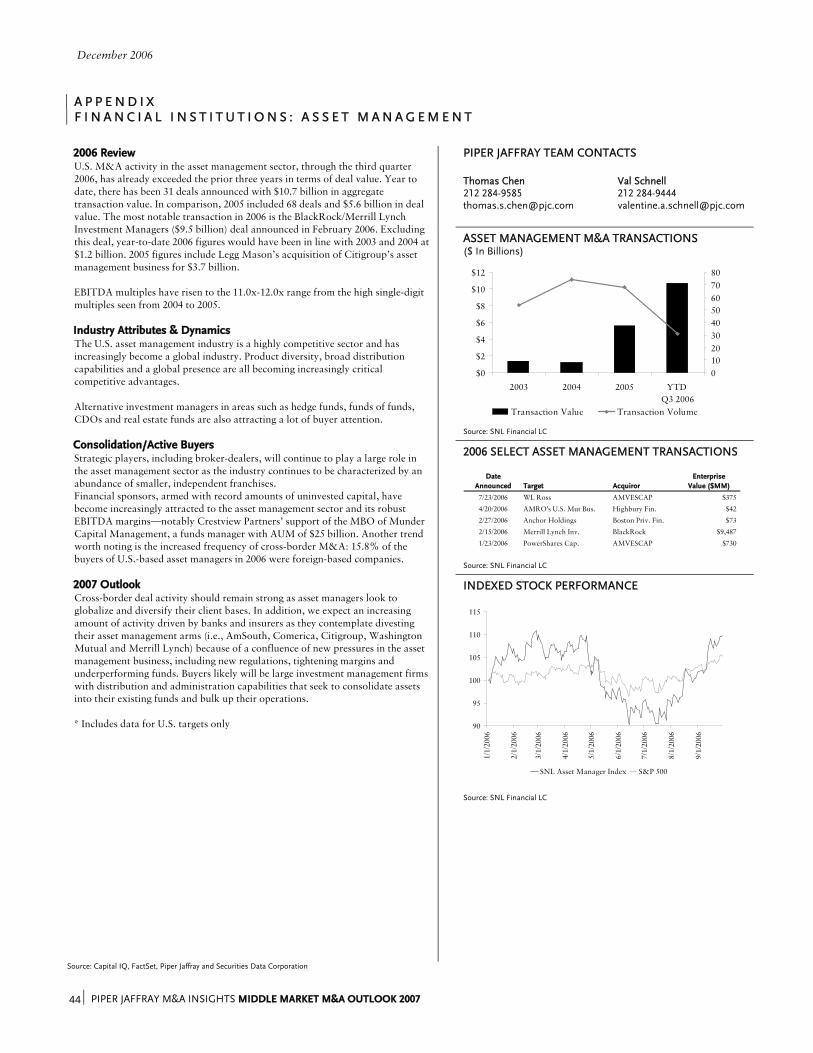

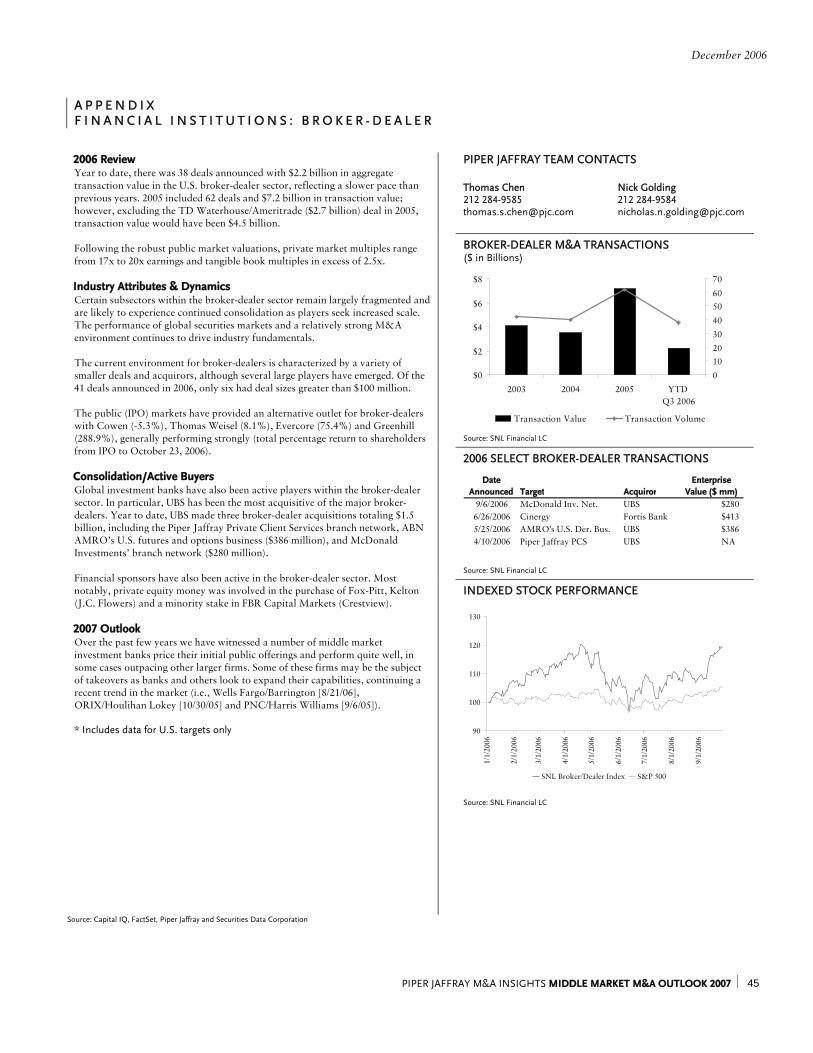

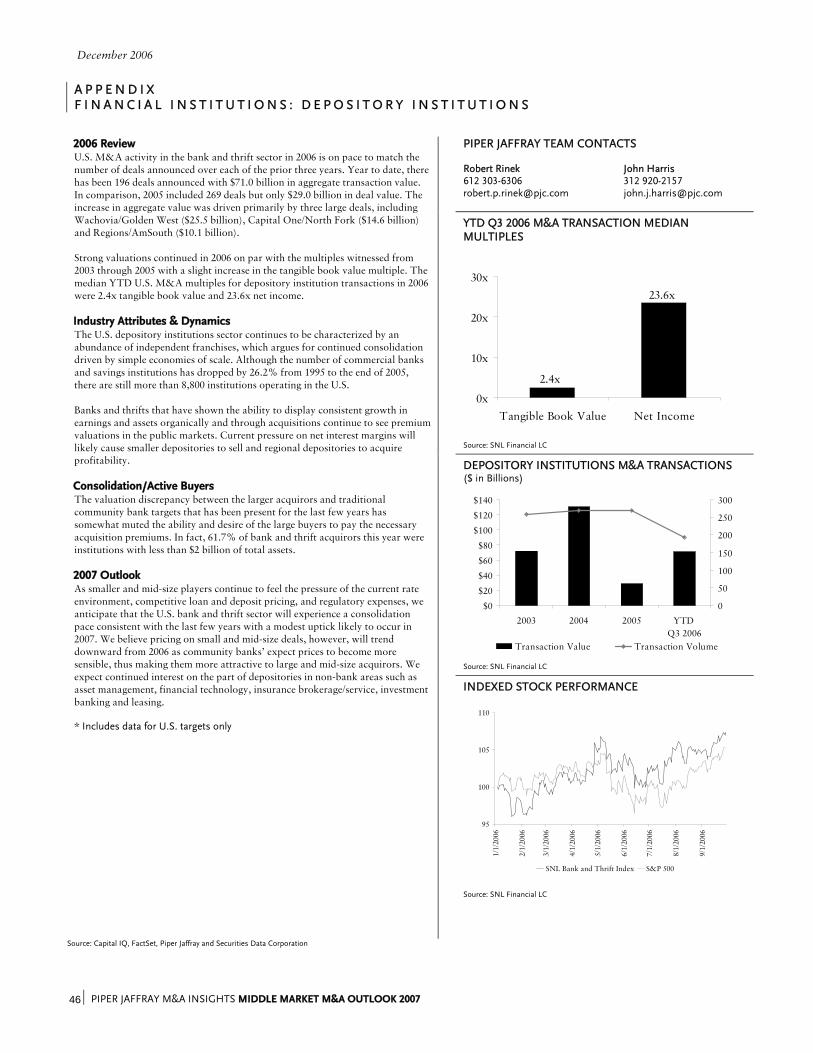

mergers & acquisitions insights - piper jaffray · mergers & acquisitions insights middle...

TRANSCRIPT

M E R G E R S & A C Q U I S I T I O N S

MERGERS & ACQUISITIONS INSIGHTS

M I D D L E M A R K E T M & A O U T L O O K 2 0 0 7

D E C E M B E R 2 0 0 6

Jon W. Kreidler, CFA Adam B. Kroll612 303-6328 312 [email protected] [email protected]

Cooper R. Caillier Joseph C. McConnell312 920-3252 612 [email protected] [email protected]

head of middle market m&a:

Jeff A. Rosenkranz312 [email protected]

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 1

T A B L E O F C O N T E N T S

Executive Summary.................................................................................... 3 Part I: M&A Activity – “A Macro Look”

Introduction ...................................................................................... 4 Worldwide M&A Activity ................................................................ 4 Domestic M&A Activity ................................................................... 5 Middle Market M&A Activity ........................................................... 7 European M&A Activity....................................................................10 Emerging Market M&A Activity .......................................................12

Part II: Capital Markets Introduction ......................................................................................15 Debt Markets.....................................................................................15 Initial Public Offering Activity ...........................................................18

Part III: Private Equity/Leveraged Buyouts

Introduction ......................................................................................22 LBO Volume......................................................................................23 Portfolio Company Hold Periods .......................................................25 Private Equity Fundraising .................................................................26 Uninvested Equity Capital..................................................................28 Competitive Environment ..................................................................29

Part IV: Strategic Buyers Introduction ......................................................................................30 Capital Structure................................................................................31 Cash Levels........................................................................................32

Part V: Conclusion .....................................................................................34 Appendix: 2006 Piper Jaffray M&A Sector Analysis

Alternative Energy - Biofuels ...........................................................................................36 Business Services - Employer Services ............................................................................37 - Security & Safety Services ................................................................38 Consumer - Consumer Products..........................................................................39 - Food Processing & Distribution .......................................................40 - Hardlines & Specialty Retail ............................................................41 - Restaurants......................................................................................42 - Softlines Retail, Footwear & Apparel...............................................43

December 2006

2 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

Financial Institutions - Asset Management...........................................................................44 - Broker-Dealer ..................................................................................45 - Depository Institutions ....................................................................46 - Insurance .........................................................................................47 - Specialty Finance .............................................................................48 - Technology & Services ....................................................................49

Health Care - Biopharmaceuticals..........................................................................50 - Health Care Services ........................................................................51 - Info-Driven Health Care ..................................................................52 - Life Sciences Tools & Diagnostics....................................................53 - Medical Technology ........................................................................54

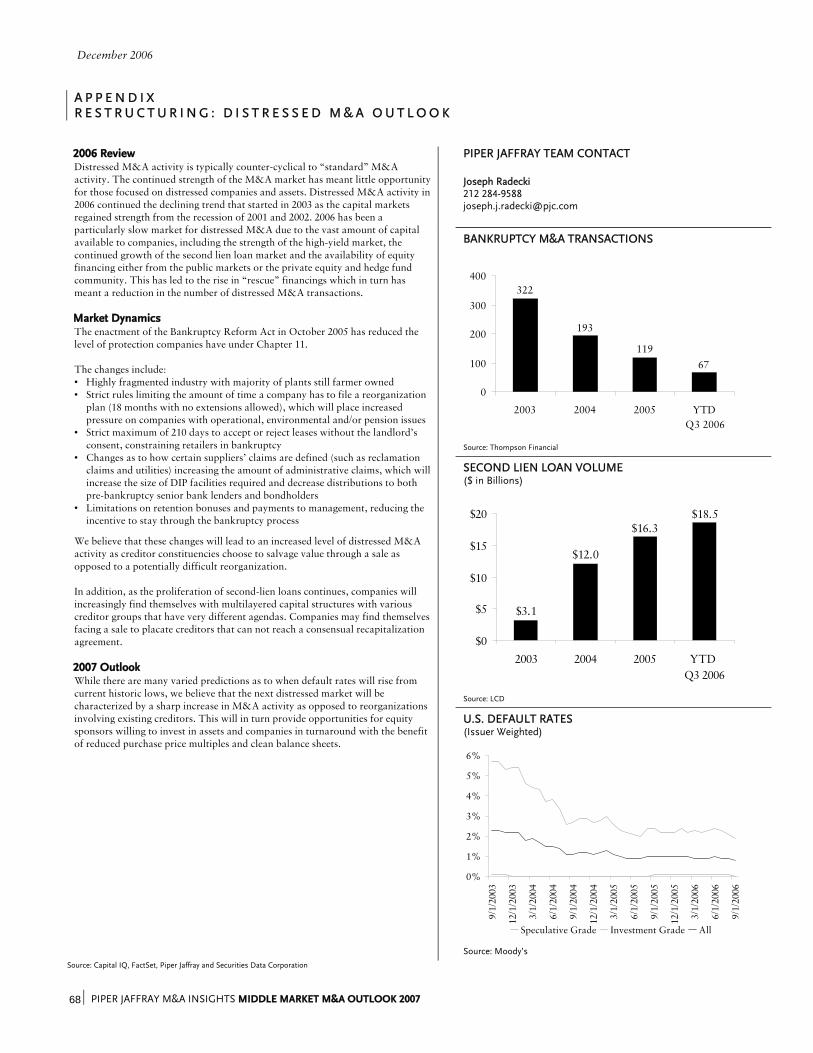

Industrial Growth - Aerospace & Defense.......................................................................55 - Automotive Aftermarket..................................................................56 - Building Products.............................................................................57 - Flow & Process Control...................................................................58 - Industrial Distribution .....................................................................59 - Packaging ........................................................................................60 - Specialty Chemicals .........................................................................61 - Specialty Vehicles.............................................................................62 Technology - Communications Equipment............................................................63 - Hardware & Semiconductors...........................................................64 - Internet............................................................................................65 - IT Services .......................................................................................66 - Software ..........................................................................................67 Restructuring - Distressed M&A Outlook................................................................68

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 3

E X E C U T I V E S U M M A R Y

In our Middle Market M&A Outlook 2006, we predicted that the rapid pace of mergers and acquisitions (“M&A”) activity experienced in 2005, both in terms of the number of announced deals and their respective aggregate value, would continue through 2006. As anticipated, domestic M&A activity has increased year-to-date (as of the end of the third quarter) over last year with 10% more announced transactions and a 13% increase in deal value. The underlying drivers had a lot of steam behind them, as 2005 ended with record levels of uninvested private equity capital and the general economic indicators were also pointing toward continued growth. The economy was like a freight train rolling down the tracks at 100 miles per hour, so there were few people willing to predict it would be able to slow down any time soon. Of course that will not stop us from taking credit for hitting the bulls eye with our prediction. Continuing on a three-year trend, average deal size is expected to increase again in 2006. This trend has been driven by not only an improving M&A environment, but also the growing size of mega-funds in the private equity world. The mega-funds, the largest of which is expected to exceed $20 billion by the end of 2006, are now large enough to swallow the proverbial whale. We also have a great deal of confidence in our outlook for 2007, so let’s see if we can do it again. The current momentum will be driven through at least the first half of 2007 by:

• Strategic acquirors continuing to seek growth opportunities through acquisitions as they focus on “buy” versus “build” strategies, primarily due to improved company performance, strong balance sheets and increased shareholder demands for growth;

• Financial buyers remaining aggressive due to significant uninvested capital and a healthy fundraising environment;

• Credit markets remaining liquid and lending at aggressive multiples; and

• Positive economic growth (domestic and international) along with inflation remaining in check and stability in the interest rate and commodity markets.

The second half of 2007, however, might reflect a typical season for the Chicago Cubs—early success leading to a lot of hope and hype through June … well, you know the rest. There are certainly risks surrounding the longevity of the bull run. The risks have been looming for the last 18 months—natural disasters, terrorist activity, consumer spending declines, pressure on the U.S. dollar, volatile and rising commodity prices, and political uncertainty relating to global conflicts. The core drivers of the M&A market, particularly those in the middle market, are intact for now and provide a strong base for continued momentum into 2007. Like the Cubs, the economy has a new general manager, Federal Reserve Bank Chairman, Ben Bernanke, and we are all hoping he is the guy to keep us in the game through October, and beyond. An informative and in-depth review and preview of the M&A market is included herein. Further, please see the appendix for select industry analyses of Piper Jaffray focus sectors. We hope you enjoy our insights, and we welcome your questions and comments.

December 2006

4 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

P A R T I : M & A A C T I V I T Y — “ A M A C R O L O O K ”

Introduction

The frenetic pace of M&A activity which has taken place over the past two years continued unabated during the first three quarters of 2006. Overall, 2006 M&A activity played out across a wide swath of industries and deal sizes as both buyers and sellers benefited from an abundance of available capital, strong business fundamentals and a supportive global economy. The surprise, however, has been the market’s tremendous resilience, despite the peaks in oil and other commodities, and the large move in short-term interest rates. The astounding magnitude of recent private equity fundraising is a clear indication the pace of mega-deals will not slow anytime soon. The small and middle market however, remain the driving force behind deal volume. These firms have a significantly higher beta than their mid- and large-cap brethren because they tend to be far less diversified. Moreover, small- to mid-size firms do not have access to the capital markets and as a result, are far more dependent on bank debt to support M&A activity. Therefore, the most likely factor to cause a weakening in M&A volume would be a credit tightening triggered by a macroeconomic slowdown. Nonetheless, a substantial overhang of uninvested private equity capital and healthy cash levels among the strategics will provide significant food to keep all the investment bankers and their clients fed for a while. While we expect the pace of M&A activity to continue well into 2007, the day of reckoning is coming. During the boom of the late 1990s we all bought a few tech stocks at 100 times 2010 revenue and forgot the old adage—pigs get fed and hogs get slaughtered. The market often forgets, but the tech bubble is not too far in the rear view mirror. This time investors have gotten smarter with their capital.

Worldwide M&A Activity M&A activity worldwide, through the first three quarters of 2006, totaled more than

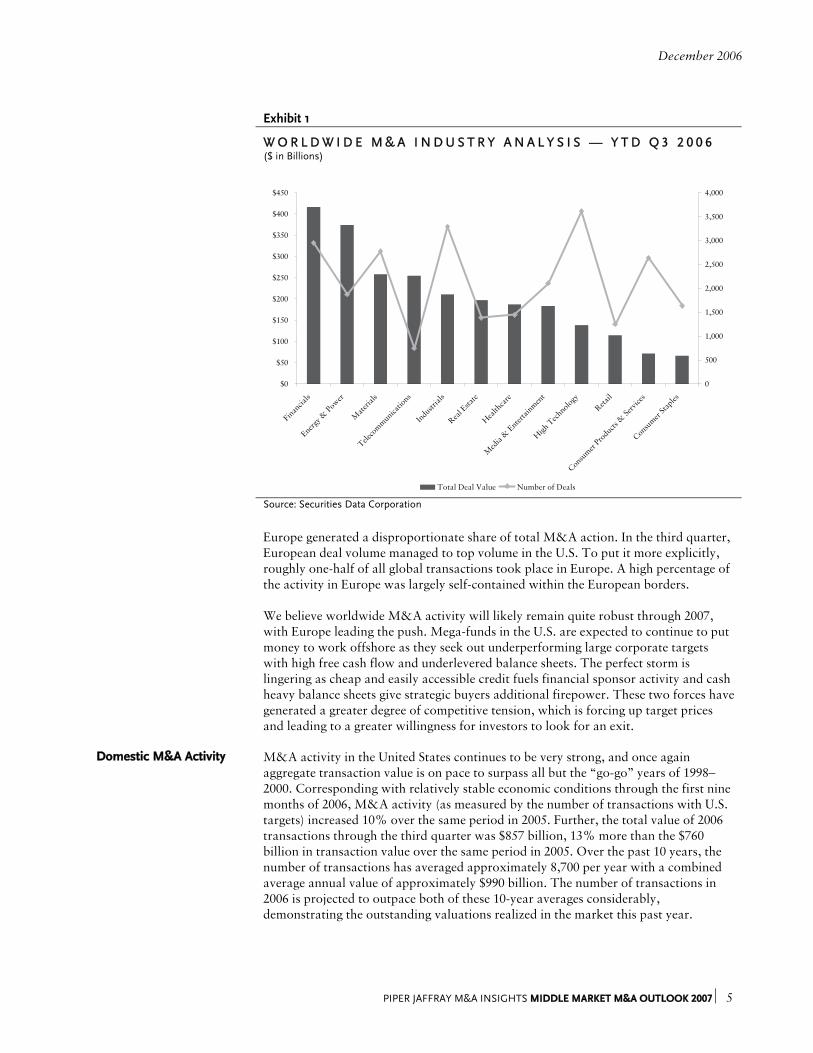

$2.4 trillion. Not surprisingly, the financial sector led the charge with $416 billion in total announced deal values, thus accounting for more than 16% of total value, which represents a 22% increase over the comparable 2005 period. Two strategic mega-deals (one in Europe and one in the U.S.) which certainly contributed to this involved Banca Intesa Spa and its pending $37.6 billion merger with San Paolo IMI Spa and the announced Wachovia marriage to Gold West Financial for $25.0 billion. To put these deals in perspective, the former was the fifth largest global deal announced during the first three quarters, while the latter fell into the number ten spot. The energy and power sector came in a formidable second place with more than $374 billion in total deal value led by the second largest announced global deal as EON AG attempts to takeover Endesa for a reported $57 billion. The material sector rounded out the top three; however, it easily took the most improved player award as the sector saw total deal value jump 104% and volume increase 8.3% over 2005 levels. From a volume perspective, the high-tech sector took the prize with 3,167 announced deals, the second consecutive year that the sector was the leader from an activity standpoint. Not since the bubble days of the late 1990s has technology M&A activity been so robust.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 5

Exhibit 1

W O R L D W I D E M & A I N D U S T R Y A N A L Y S I S — Y T D Q 3 2 0 0 6 ($ in Billions)

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

Financia

ls

Energy &

Power

Mate

rials

Teleco

mmunicatio

ns

Industr

ials

Real E

state

Health

care

Med

ia &

Entertai

nment

High T

echnology

Retail

Consumer

Products

& Se

rvice

s

Consumer

Staples

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Total Deal Value Number of Deals Source: Securities Data Corporation Europe generated a disproportionate share of total M&A action. In the third quarter,

European deal volume managed to top volume in the U.S. To put it more explicitly, roughly one-half of all global transactions took place in Europe. A high percentage of the activity in Europe was largely self-contained within the European borders. We believe worldwide M&A activity will likely remain quite robust through 2007, with Europe leading the push. Mega-funds in the U.S. are expected to continue to put money to work offshore as they seek out underperforming large corporate targets with high free cash flow and underlevered balance sheets. The perfect storm is lingering as cheap and easily accessible credit fuels financial sponsor activity and cash heavy balance sheets give strategic buyers additional firepower. These two forces have generated a greater degree of competitive tension, which is forcing up target prices and leading to a greater willingness for investors to look for an exit.

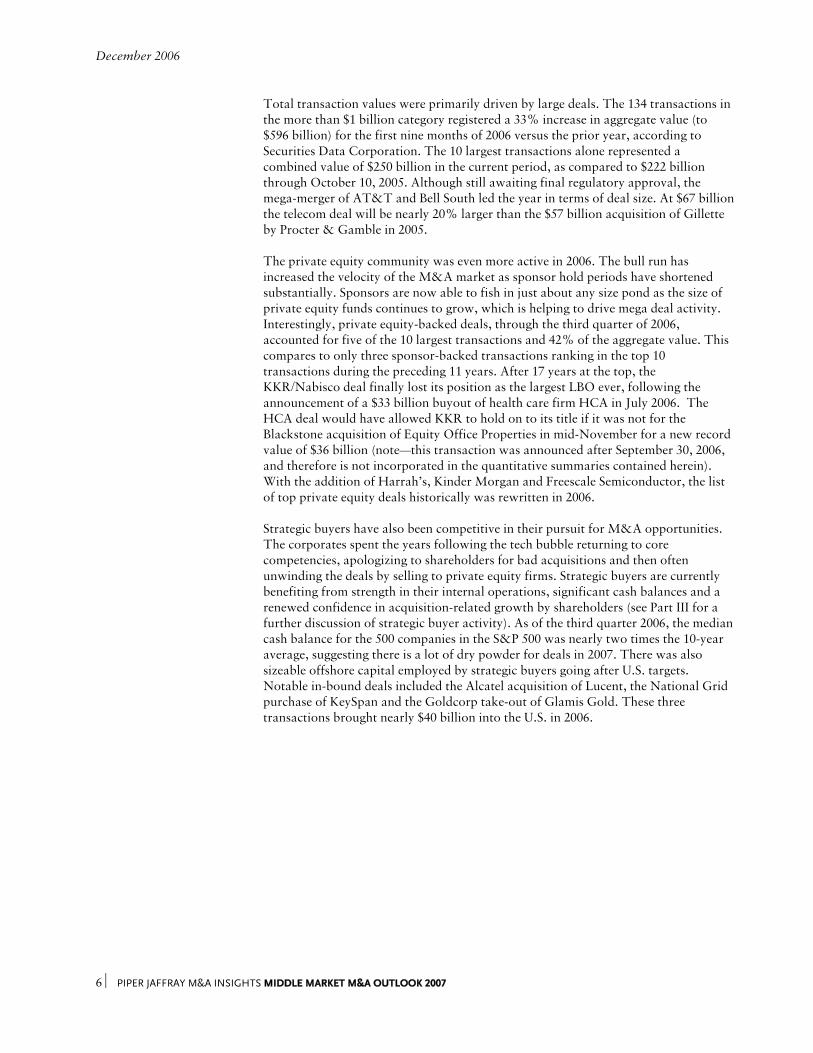

Domestic M&A Activity M&A activity in the United States continues to be very strong, and once again

aggregate transaction value is on pace to surpass all but the “go-go” years of 1998–2000. Corresponding with relatively stable economic conditions through the first nine months of 2006, M&A activity (as measured by the number of transactions with U.S. targets) increased 10% over the same period in 2005. Further, the total value of 2006 transactions through the third quarter was $857 billion, 13% more than the $760 billion in transaction value over the same period in 2005. Over the past 10 years, the number of transactions has averaged approximately 8,700 per year with a combined average annual value of approximately $990 billion. The number of transactions in 2006 is projected to outpace both of these 10-year averages considerably, demonstrating the outstanding valuations realized in the market this past year.

December 2006

6 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

Total transaction values were primarily driven by large deals. The 134 transactions in the more than $1 billion category registered a 33% increase in aggregate value (to $596 billion) for the first nine months of 2006 versus the prior year, according to Securities Data Corporation. The 10 largest transactions alone represented a combined value of $250 billion in the current period, as compared to $222 billion through October 10, 2005. Although still awaiting final regulatory approval, the mega-merger of AT&T and Bell South led the year in terms of deal size. At $67 billion the telecom deal will be nearly 20% larger than the $57 billion acquisition of Gillette by Procter & Gamble in 2005. The private equity community was even more active in 2006. The bull run has increased the velocity of the M&A market as sponsor hold periods have shortened substantially. Sponsors are now able to fish in just about any size pond as the size of private equity funds continues to grow, which is helping to drive mega deal activity. Interestingly, private equity-backed deals, through the third quarter of 2006, accounted for five of the 10 largest transactions and 42% of the aggregate value. This compares to only three sponsor-backed transactions ranking in the top 10 transactions during the preceding 11 years. After 17 years at the top, the KKR/Nabisco deal finally lost its position as the largest LBO ever, following the announcement of a $33 billion buyout of health care firm HCA in July 2006. The HCA deal would have allowed KKR to hold on to its title if it was not for the Blackstone acquisition of Equity Office Properties in mid-November for a new record value of $36 billion (note—this transaction was announced after September 30, 2006, and therefore is not incorporated in the quantitative summaries contained herein). With the addition of Harrah’s, Kinder Morgan and Freescale Semiconductor, the list of top private equity deals historically was rewritten in 2006. Strategic buyers have also been competitive in their pursuit for M&A opportunities. The corporates spent the years following the tech bubble returning to core competencies, apologizing to shareholders for bad acquisitions and then often unwinding the deals by selling to private equity firms. Strategic buyers are currently benefiting from strength in their internal operations, significant cash balances and a renewed confidence in acquisition-related growth by shareholders (see Part III for a further discussion of strategic buyer activity). As of the third quarter 2006, the median cash balance for the 500 companies in the S&P 500 was nearly two times the 10-year average, suggesting there is a lot of dry powder for deals in 2007. There was also sizeable offshore capital employed by strategic buyers going after U.S. targets. Notable in-bound deals included the Alcatel acquisition of Lucent, the National Grid purchase of KeySpan and the Goldcorp take-out of Glamis Gold. These three transactions brought nearly $40 billion into the U.S. in 2006.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 7

Exhibit 2

U . S . M & A A C T I V I T Y ($ in Billions)

$0

$400

$800

$1,200

$1,600

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3

2005

YTD Q3

2006

0

3,000

6,000

9,000

12,000

15,000

Total Reported Deal Values Number of Deals Source: Securities Data Corporation

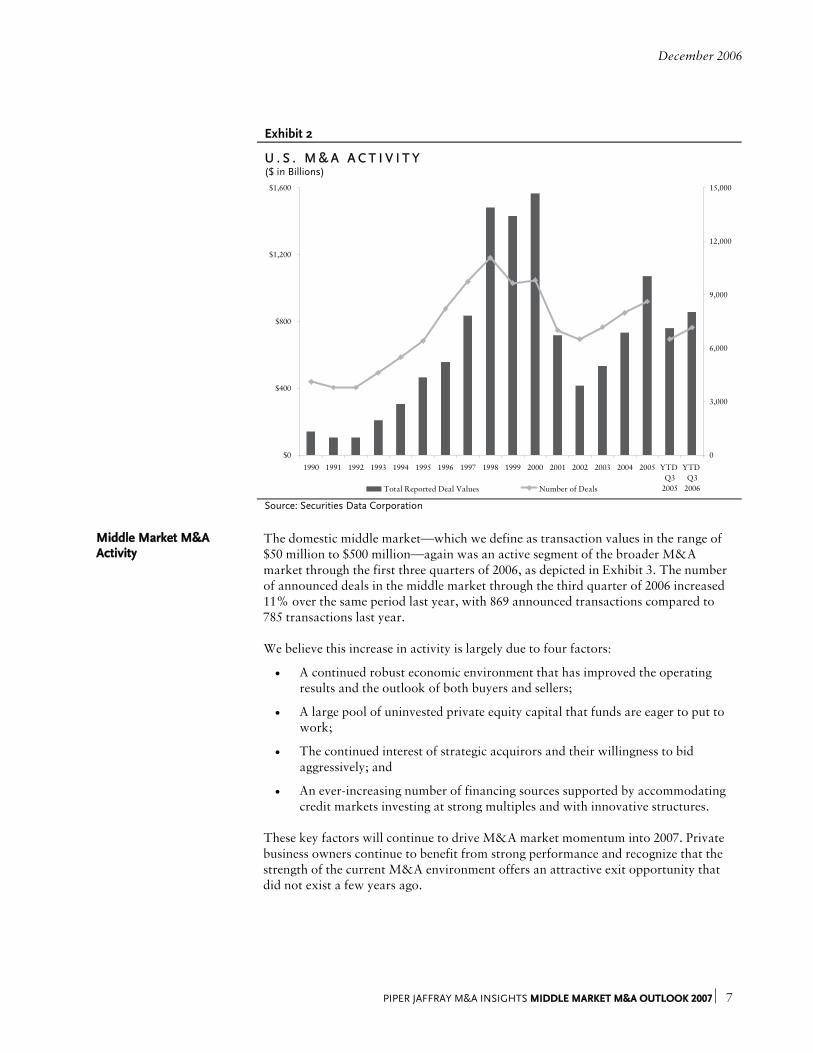

Middle Market M&A Activity

The domestic middle market—which we define as transaction values in the range of $50 million to $500 million—again was an active segment of the broader M&A market through the first three quarters of 2006, as depicted in Exhibit 3. The number of announced deals in the middle market through the third quarter of 2006 increased 11% over the same period last year, with 869 announced transactions compared to 785 transactions last year. We believe this increase in activity is largely due to four factors:

• A continued robust economic environment that has improved the operating results and the outlook of both buyers and sellers;

• A large pool of uninvested private equity capital that funds are eager to put to work;

• The continued interest of strategic acquirors and their willingness to bid aggressively; and

• An ever-increasing number of financing sources supported by accommodating credit markets investing at strong multiples and with innovative structures.

These key factors will continue to drive M&A market momentum into 2007. Private business owners continue to benefit from strong performance and recognize that the strength of the current M&A environment offers an attractive exit opportunity that did not exist a few years ago.

December 2006

8 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

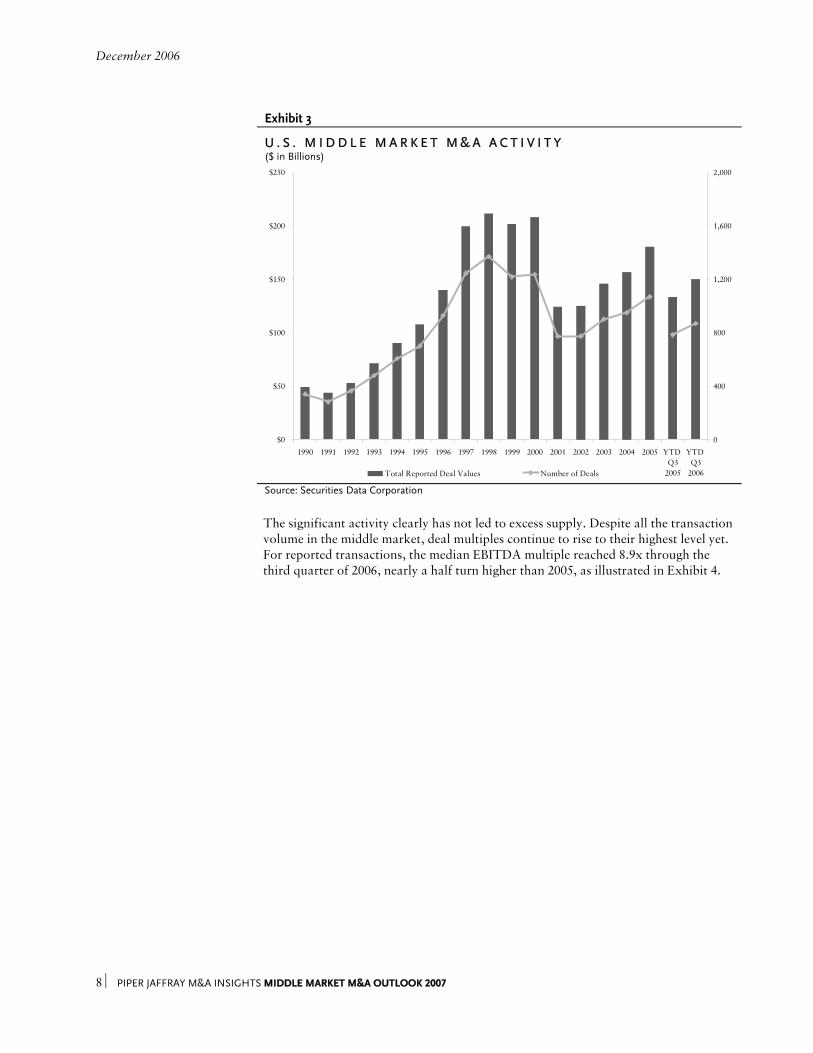

Exhibit 3

U . S . M I D D L E M A R K E T M & A A C T I V I T Y ($ in Billions)

$0

$50

$100

$150

$200

$250

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3

2005

YTD Q3

2006

0

400

800

1,200

1,600

2,000

Total Reported Deal Values Number of Deals Source: Securities Data Corporation

The significant activity clearly has not led to excess supply. Despite all the transaction

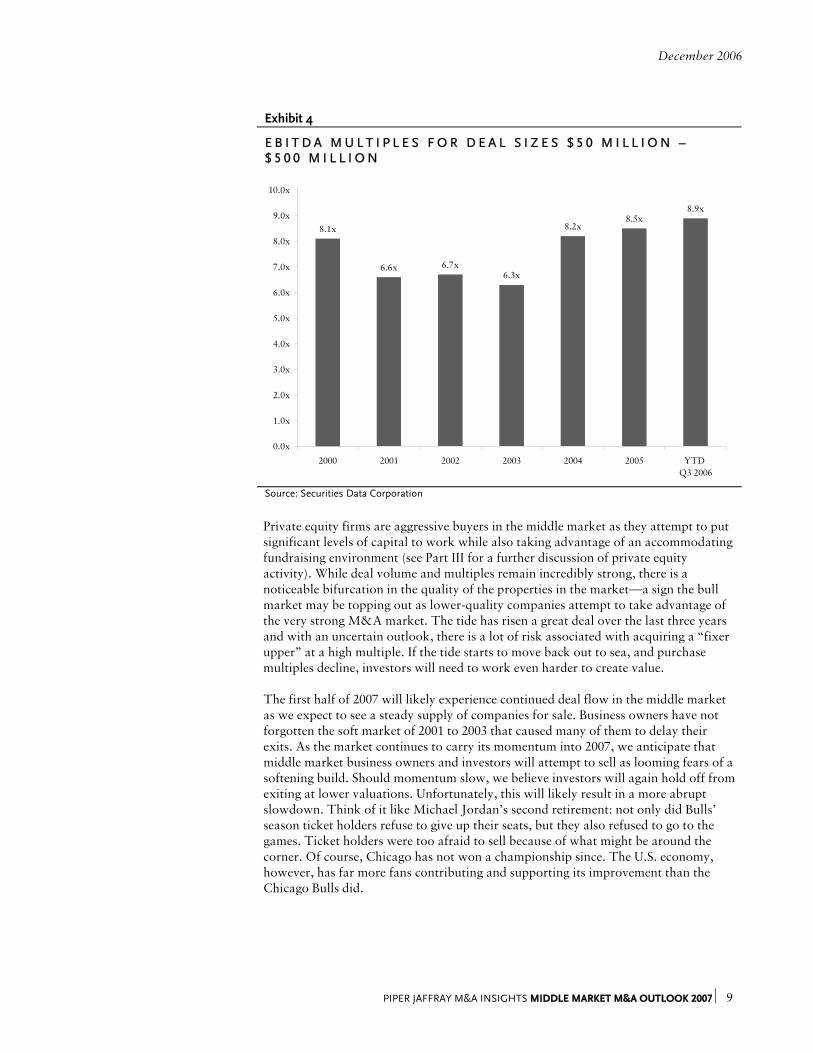

volume in the middle market, deal multiples continue to rise to their highest level yet. For reported transactions, the median EBITDA multiple reached 8.9x through the third quarter of 2006, nearly a half turn higher than 2005, as illustrated in Exhibit 4.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 9

Exhibit 4

E B I T D A M U L T I P L E S F O R D E A L S I Z E S $ 5 0 M I L L I O N – $ 5 0 0 M I L L I O N

8.1x

6.6x 6.7x6.3x

8.2x8.5x

8.9x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

9.0x

10.0x

2000 2001 2002 2003 2004 2005 YTD Q3 2006

Source: Securities Data Corporation

Private equity firms are aggressive buyers in the middle market as they attempt to put

significant levels of capital to work while also taking advantage of an accommodating fundraising environment (see Part III for a further discussion of private equity activity). While deal volume and multiples remain incredibly strong, there is a noticeable bifurcation in the quality of the properties in the market—a sign the bull market may be topping out as lower-quality companies attempt to take advantage of the very strong M&A market. The tide has risen a great deal over the last three years and with an uncertain outlook, there is a lot of risk associated with acquiring a “fixer upper” at a high multiple. If the tide starts to move back out to sea, and purchase multiples decline, investors will need to work even harder to create value. The first half of 2007 will likely experience continued deal flow in the middle market as we expect to see a steady supply of companies for sale. Business owners have not forgotten the soft market of 2001 to 2003 that caused many of them to delay their exits. As the market continues to carry its momentum into 2007, we anticipate that middle market business owners and investors will attempt to sell as looming fears of a softening build. Should momentum slow, we believe investors will again hold off from exiting at lower valuations. Unfortunately, this will likely result in a more abrupt slowdown. Think of it like Michael Jordan’s second retirement: not only did Bulls’ season ticket holders refuse to give up their seats, but they also refused to go to the games. Ticket holders were too afraid to sell because of what might be around the corner. Of course, Chicago has not won a championship since. The U.S. economy, however, has far more fans contributing and supporting its improvement than the Chicago Bulls did.

December 2006

10 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

European M&A Activity M&A activity in Europe (defined as acquisitions of European-based companies) has

been almost as active as the U.S., with over 4,700 transactions through the first nine months of 2006, an increase of 25% over the prior year period. Deal values for the period were up a staggering 48%, reaching $876 billion, according to Bloomberg data. The most active industries for M&A activity have been financials, energy and industrials, which collectively account for nearly 50% of total European M&A activity. There have been a number of key catalysts to the growth in both intra-European and cross-border M&A activity:

• Solid earnings and cash reserves by European companies;

• Significant access to credit;

• Attractive growth rates in the central and eastern European emerging markets;

• Privatization of entities within the former Soviet bloc; and

• An increasingly receptive political environment. The high end of the M&A market in Europe had its own share of mega-deals, with the intended $57 billion E.On acquisition of Endesa as the largest followed by the long battled Mittal/Arcelor deal at $43.6 billion. The third-largest European deal is the pending $40.9 billion bid by Suez for Gaz de France. Private equity-backed buyouts also claimed their share of the headlines with marquee deals. Among the most publicized were BAA’s $28 billion deal backed by private equity firms, Caisse de Depot et Placement du Quebec and GIC Special Investments with strategic investor Grupo Ferrovial, and the $9 billion acquisition of Dutch media concern VNU led by KKR, Blackstone and Carlyle. The M&A momentum in Europe is likely to continue as slow domestic growth in some European countries has prompted many companies to look outside their own borders for expansion opportunities. The disparate European governments have become far more friendly to cross-border M&A over the last several years. ABN AMRO’s year-long trek to close its acquisition of Banca Antonveneta SpA serves as a clear example that markets within Europe are truly “open” and industries once protected by strong nationalism no longer have a big brother protecting them from bullies from other neighborhoods. As corporate consolidation across European borders has intensified, a race has begun among competing companies to acquire prime targets. Furthermore, the private equity community has continued to gain momentum and is establishing itself as a driving force of M&A activity in Europe. With the expansion of the EU and economic growth in Central and Eastern Europe, an increasing number of European corporate and private equity investors are directing their funds toward investments in developing European countries. Countries such as Russia, Poland and Serbia offer European investors the opportunity to acquire recently privatized companies—particularly in the industrial and building sectors—for very attractive multiples, although the largest wave of privatization is in the rearview mirror. With strong corporate balance sheets, large pools of uninvested American and European private equity capital and attractive acquisition targets in Europe, there is little question that both the means and the opportunities exist for expansion in this important market.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 11

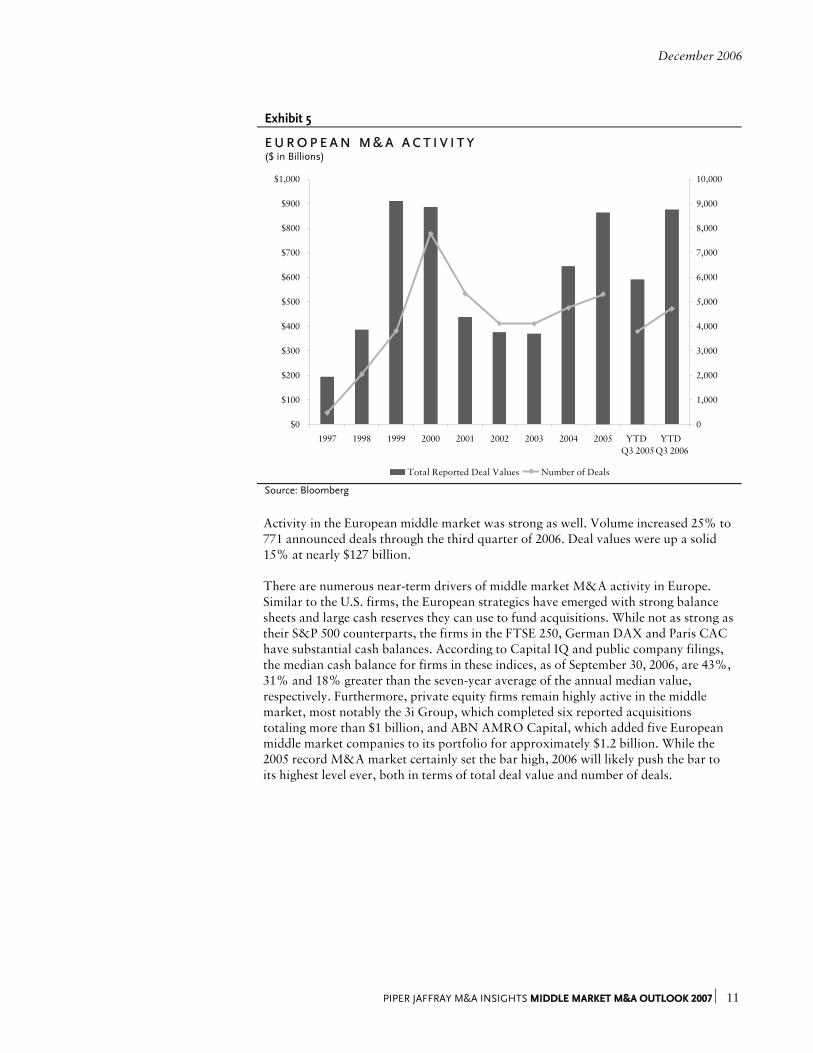

Exhibit 5

E U R O P E A N M & A A C T I V I T Y ($ in Billions)

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3 2005

YTD Q3 2006

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Total Reported Deal Values Number of Deals

Source: Bloomberg Activity in the European middle market was strong as well. Volume increased 25% to

771 announced deals through the third quarter of 2006. Deal values were up a solid 15% at nearly $127 billion. There are numerous near-term drivers of middle market M&A activity in Europe. Similar to the U.S. firms, the European strategics have emerged with strong balance sheets and large cash reserves they can use to fund acquisitions. While not as strong as their S&P 500 counterparts, the firms in the FTSE 250, German DAX and Paris CAC have substantial cash balances. According to Capital IQ and public company filings, the median cash balance for firms in these indices, as of September 30, 2006, are 43%, 31% and 18% greater than the seven-year average of the annual median value, respectively. Furthermore, private equity firms remain highly active in the middle market, most notably the 3i Group, which completed six reported acquisitions totaling more than $1 billion, and ABN AMRO Capital, which added five European middle market companies to its portfolio for approximately $1.2 billion. While the 2005 record M&A market certainly set the bar high, 2006 will likely push the bar to its highest level ever, both in terms of total deal value and number of deals.

December 2006

12 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

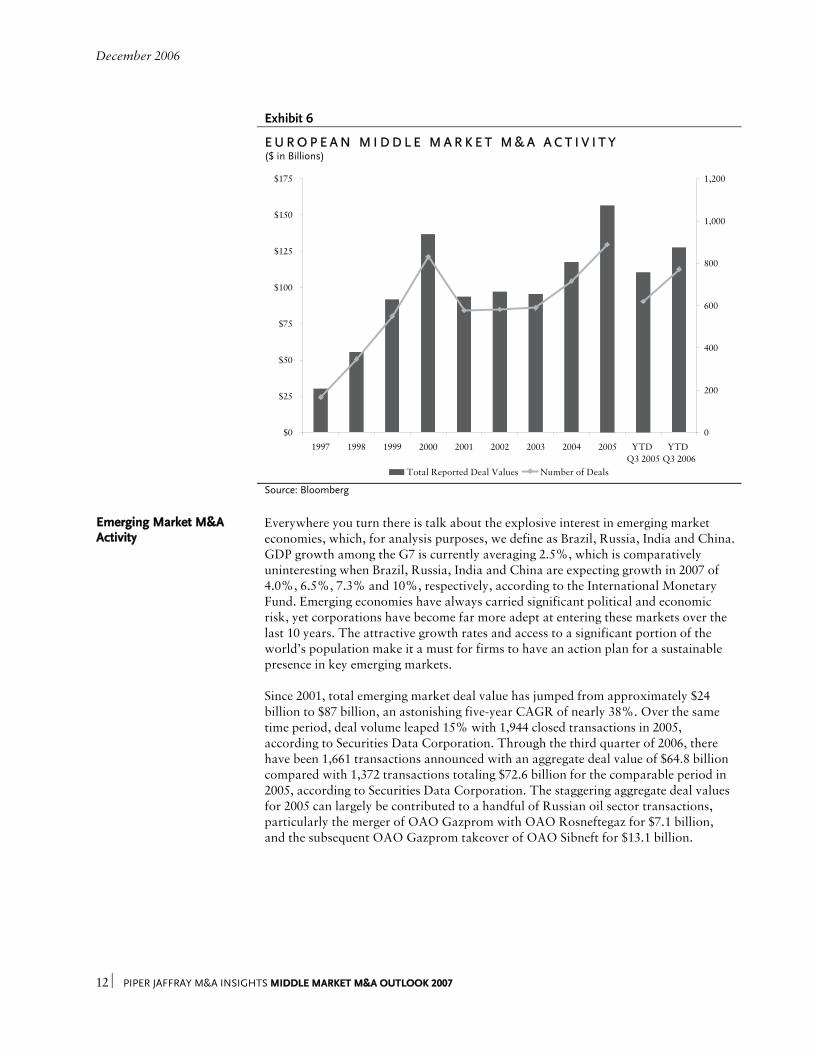

Exhibit 6

E U R O P E A N M I D D L E M A R K E T M & A A C T I V I T Y ($ in Billions)

$0

$25

$50

$75

$100

$125

$150

$175

1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3 2005

YTD Q3 2006

0

200

400

600

800

1,000

1,200

Total Reported Deal Values Number of Deals

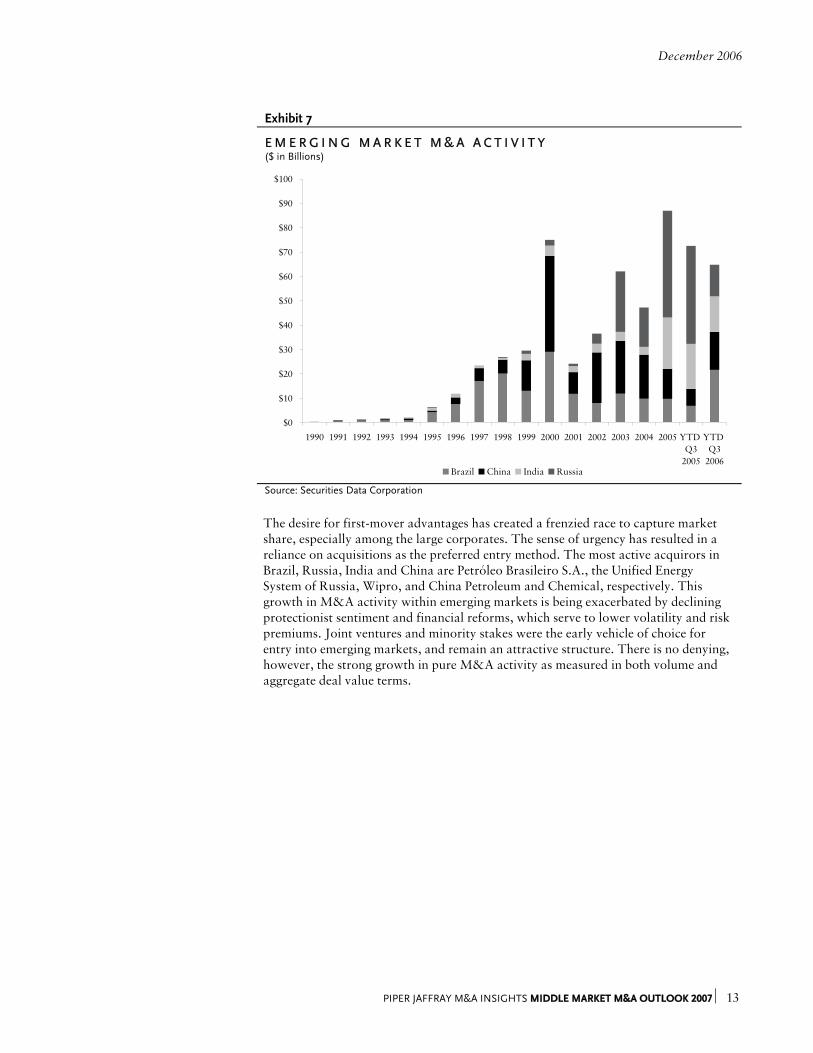

Source: Bloomberg Emerging Market M&A Activity

Everywhere you turn there is talk about the explosive interest in emerging market economies, which, for analysis purposes, we define as Brazil, Russia, India and China. GDP growth among the G7 is currently averaging 2.5%, which is comparatively uninteresting when Brazil, Russia, India and China are expecting growth in 2007 of 4.0%, 6.5%, 7.3% and 10%, respectively, according to the International Monetary Fund. Emerging economies have always carried significant political and economic risk, yet corporations have become far more adept at entering these markets over the last 10 years. The attractive growth rates and access to a significant portion of the world’s population make it a must for firms to have an action plan for a sustainable presence in key emerging markets. Since 2001, total emerging market deal value has jumped from approximately $24 billion to $87 billion, an astonishing five-year CAGR of nearly 38%. Over the same time period, deal volume leaped 15% with 1,944 closed transactions in 2005, according to Securities Data Corporation. Through the third quarter of 2006, there have been 1,661 transactions announced with an aggregate deal value of $64.8 billion compared with 1,372 transactions totaling $72.6 billion for the comparable period in 2005, according to Securities Data Corporation. The staggering aggregate deal values for 2005 can largely be contributed to a handful of Russian oil sector transactions, particularly the merger of OAO Gazprom with OAO Rosneftegaz for $7.1 billion, and the subsequent OAO Gazprom takeover of OAO Sibneft for $13.1 billion.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 13

Exhibit 7

E M E R G I N G M A R K E T M & A A C T I V I T Y ($ in Billions)

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3

2005

YTD Q3

2006Brazil China India Russia

Source: Securities Data Corporation

The desire for first-mover advantages has created a frenzied race to capture market

share, especially among the large corporates. The sense of urgency has resulted in a reliance on acquisitions as the preferred entry method. The most active acquirors in Brazil, Russia, India and China are Petróleo Brasileiro S.A., the Unified Energy System of Russia, Wipro, and China Petroleum and Chemical, respectively. This growth in M&A activity within emerging markets is being exacerbated by declining protectionist sentiment and financial reforms, which serve to lower volatility and risk premiums. Joint ventures and minority stakes were the early vehicle of choice for entry into emerging markets, and remain an attractive structure. There is no denying, however, the strong growth in pure M&A activity as measured in both volume and aggregate deal value terms.

December 2006

14 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

Exhibit 8

E M E R G I N G M A R K E T E B I T D A M U L T I P L E S

5.7x6.1x

7.0x 7.2x

8.7x

9.6x

10.8x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

2000 2001 2002 2003 2004 2005 YTD Q3 2006

Source: Bloomberg and Securities Data Corporation

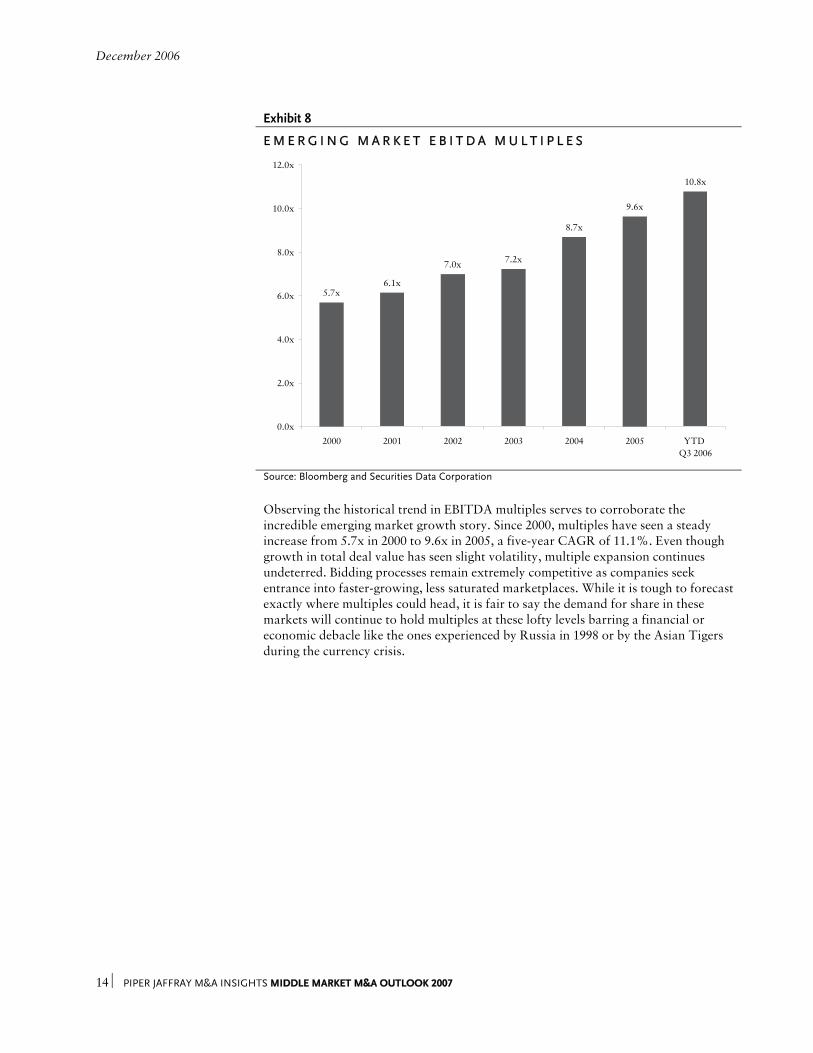

Observing the historical trend in EBITDA multiples serves to corroborate the

incredible emerging market growth story. Since 2000, multiples have seen a steady increase from 5.7x in 2000 to 9.6x in 2005, a five-year CAGR of 11.1%. Even though growth in total deal value has seen slight volatility, multiple expansion continues undeterred. Bidding processes remain extremely competitive as companies seek entrance into faster-growing, less saturated marketplaces. While it is tough to forecast exactly where multiples could head, it is fair to say the demand for share in these markets will continue to hold multiples at these lofty levels barring a financial or economic debacle like the ones experienced by Russia in 1998 or by the Asian Tigers during the currency crisis.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 15

P A R T I I : C A P I T A L M A R K E T S

Introduction

The debt and equity capital markets have a significant impact on M&A activity. The debt markets have remained aggressive and have provided ready capital to support corporate and private equity investor buyouts. Conversely, the equity capital markets offer an alternative exit strategy to a negotiated sale for investors, which takes supply out of the M&A market in the short run. In the long run, however, corporate buyers with ready access to the equity markets can use their stock as currency to foster an increase in M&A. IPO activity in 2006 has continued at a healthy clip from 2005, although it’s down slightly from 2005, and there is a strong backlog of issuances that indicates the early part of 2007 will be active.

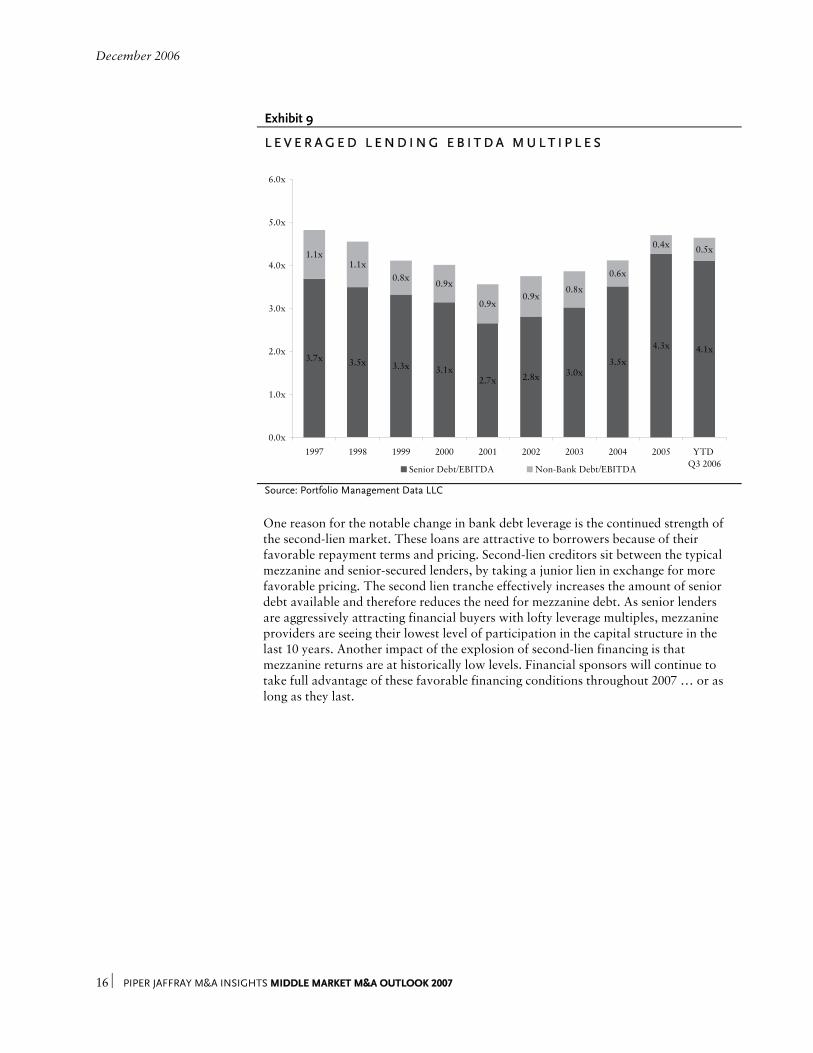

Debt Markets The debt markets have remained strong in 2006 after particularly active years in 2004 and 2005. Sustained improvement in corporate performance has made both bank and high-yield debt available at favorable terms. A significant number of alternative, nonregulated financing sources (aka, hedge funds) have provided a considerable supply of debt capital to the marketplace. This supply has fostered a very competitive and aggressive environment for lenders and provided the much-needed fuel for the buyout fire. Due to the overall strength of the financing environment, we believe that private equity firms will remain competitive and strategic buyers will continue to make acquisitions well into 2007. While total debt multiples were down slightly from the previous year, average senior debt multiples employed in transactions remained at historically high levels, holding above four times EBITDA, while average mezzanine debt multiples strengthened slightly. Another driver in the debt markets over recent years has been the emergence of alternative providers of debt capital, including hedge funds and private investors. Over the last four years there has been a significant increase in collateralized debt/loan obligation funds (“CDOs” or “CLOs”) that have created a liquid market for otherwise illiquid bank loans. The onset of these investment vehicles and the resulting liquidity and trading activity have enabled hedge funds and other alternative sources of capital to invest in middle market firms. These alternative lenders are not faced with the same regulatory oversight of commercial banks and, as a result, they can take on significantly more risk and even view the debt through the eyes of a future equity holder if things go south. The hawkish Federal Reserve policy has led to an attractive coupon of more than 8% on a typical senior secured leveraged loan, which is amplified by the impact of the yield curve compression on corporate bond pricing. Moreover, the fact that middle market leveraged loans are not registered securities and therefore do not come under the purview of Sarbanes-Oxley and SEC reporting requirements, makes the asset class attractive to issuers. The additional influx of willing lenders will continue to support the favorable environment.

December 2006

16 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

Exhibit 9

L E V E R A G E D L E N D I N G E B I T D A M U L T I P L E S

3.7x 3.5x 3.3x 3.1x2.7x 2.8x 3.0x

3.5x

4.3x 4.1x

1.1x1.1x

0.8x0.9x

0.9x0.9x

0.8x

0.6x

0.4x 0.5x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3 2006Senior Debt/EBITDA Non-Bank Debt/EBITDA

Source: Portfolio Management Data LLC

One reason for the notable change in bank debt leverage is the continued strength of

the second-lien market. These loans are attractive to borrowers because of their favorable repayment terms and pricing. Second-lien creditors sit between the typical mezzanine and senior-secured lenders, by taking a junior lien in exchange for more favorable pricing. The second lien tranche effectively increases the amount of senior debt available and therefore reduces the need for mezzanine debt. As senior lenders are aggressively attracting financial buyers with lofty leverage multiples, mezzanine providers are seeing their lowest level of participation in the capital structure in the last 10 years. Another impact of the explosion of second-lien financing is that mezzanine returns are at historically low levels. Financial sponsors will continue to take full advantage of these favorable financing conditions throughout 2007 … or as long as they last.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 17

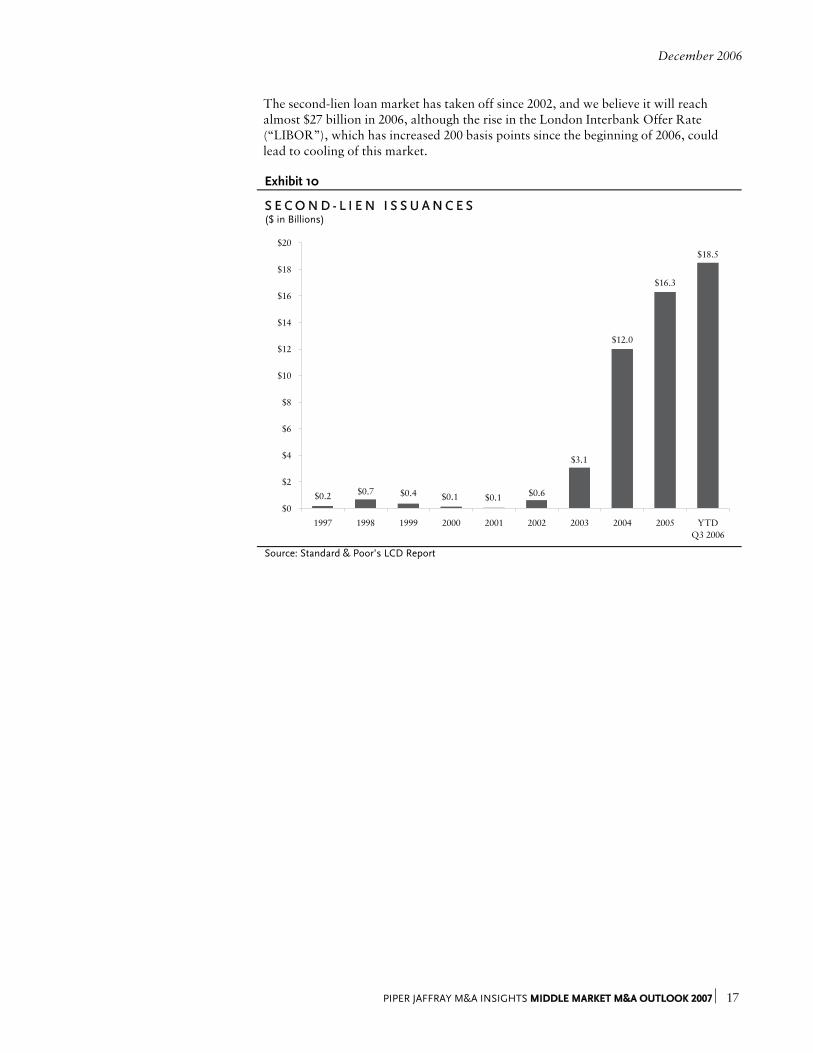

The second-lien loan market has taken off since 2002, and we believe it will reach almost $27 billion in 2006, although the rise in the London Interbank Offer Rate (“LIBOR”), which has increased 200 basis points since the beginning of 2006, could lead to cooling of this market.

Exhibit 10

S E C O N D - L I E N I S S U A N C E S ($ in Billions)

$3.1

$0.2 $0.7 $0.4 $0.1 $0.1 $0.6

$12.0

$16.3

$18.5

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

1997 1998 1999 2000 2001 2002 2003 2004 2005 YTDQ3 2006

Source: Standard & Poor’s LCD Report

December 2006

18 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

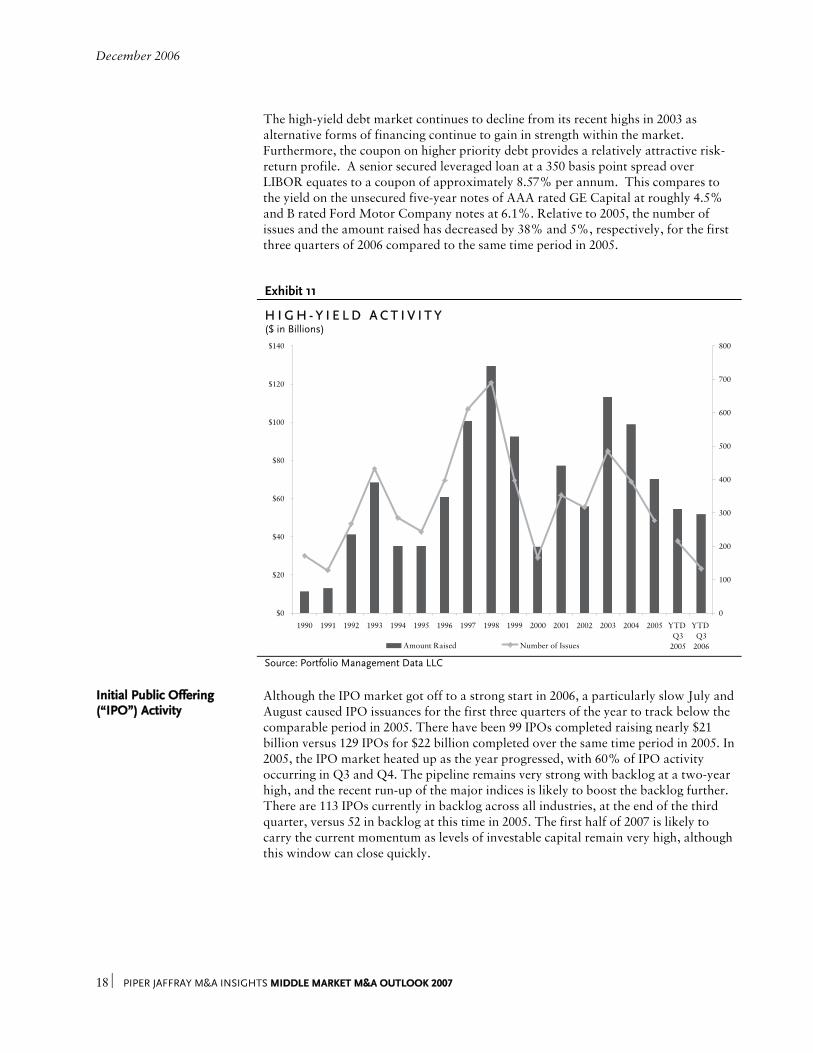

The high-yield debt market continues to decline from its recent highs in 2003 as

alternative forms of financing continue to gain in strength within the market. Furthermore, the coupon on higher priority debt provides a relatively attractive risk-return profile. A senior secured leveraged loan at a 350 basis point spread over LIBOR equates to a coupon of approximately 8.57% per annum. This compares to the yield on the unsecured five-year notes of AAA rated GE Capital at roughly 4.5% and B rated Ford Motor Company notes at 6.1%. Relative to 2005, the number of issues and the amount raised has decreased by 38% and 5%, respectively, for the first three quarters of 2006 compared to the same time period in 2005.

Exhibit 11

H I G H - Y I E L D A C T I V I T Y ($ in Billions)

$0

$20

$40

$60

$80

$100

$120

$140

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3

2005

YTD Q3

2006

0

100

200

300

400

500

600

700

800

Amount Raised Number of Issues

Source: Portfolio Management Data LLC Initial Public Offering (“IPO”) Activity

Although the IPO market got off to a strong start in 2006, a particularly slow July and August caused IPO issuances for the first three quarters of the year to track below the comparable period in 2005. There have been 99 IPOs completed raising nearly $21 billion versus 129 IPOs for $22 billion completed over the same time period in 2005. In 2005, the IPO market heated up as the year progressed, with 60% of IPO activity occurring in Q3 and Q4. The pipeline remains very strong with backlog at a two-year high, and the recent run-up of the major indices is likely to boost the backlog further. There are 113 IPOs currently in backlog across all industries, at the end of the third quarter, versus 52 in backlog at this time in 2005. The first half of 2007 is likely to carry the current momentum as levels of investable capital remain very high, although this window can close quickly.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 19

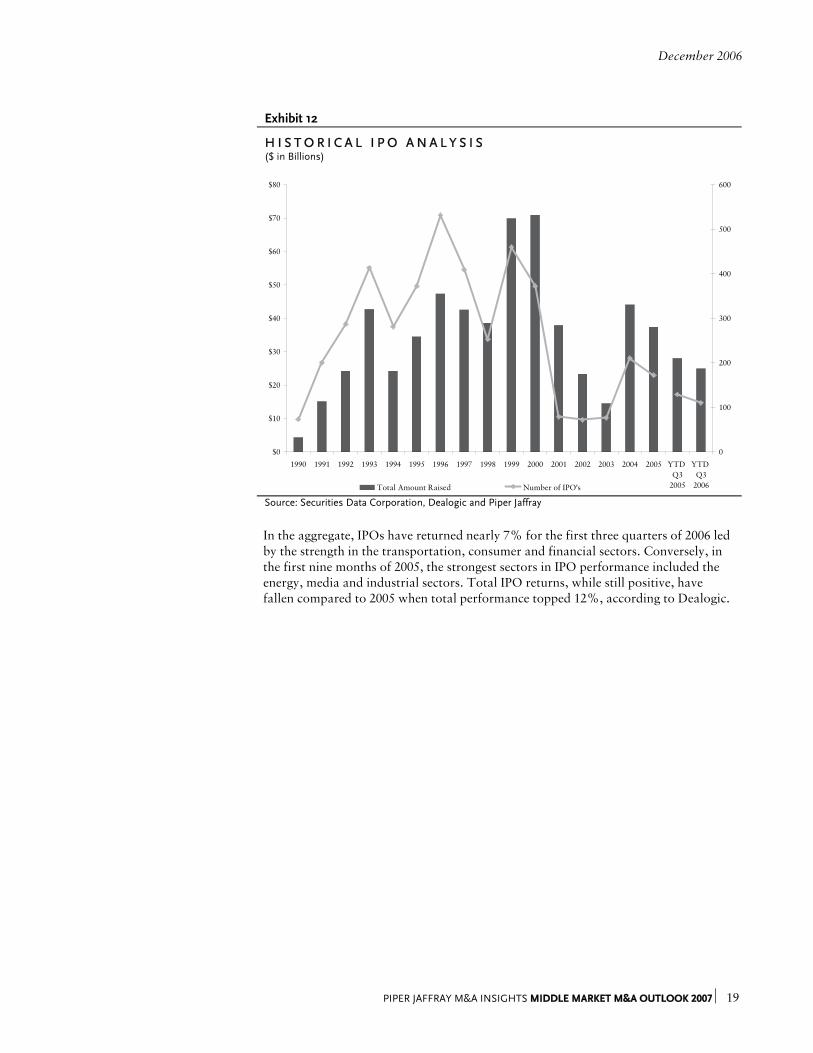

Exhibit 12

H I S T O R I C A L I P O A N A L Y S I S ($ in Billions)

$0

$10

$20

$30

$40

$50

$60

$70

$80

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3

2005

YTD Q3

2006

0

100

200

300

400

500

600

Total Amount Raised Number of IPO's Source: Securities Data Corporation, Dealogic and Piper Jaffray

In the aggregate, IPOs have returned nearly 7% for the first three quarters of 2006 led

by the strength in the transportation, consumer and financial sectors. Conversely, in the first nine months of 2005, the strongest sectors in IPO performance included the energy, media and industrial sectors. Total IPO returns, while still positive, have fallen compared to 2005 when total performance topped 12%, according to Dealogic.

December 2006

20 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

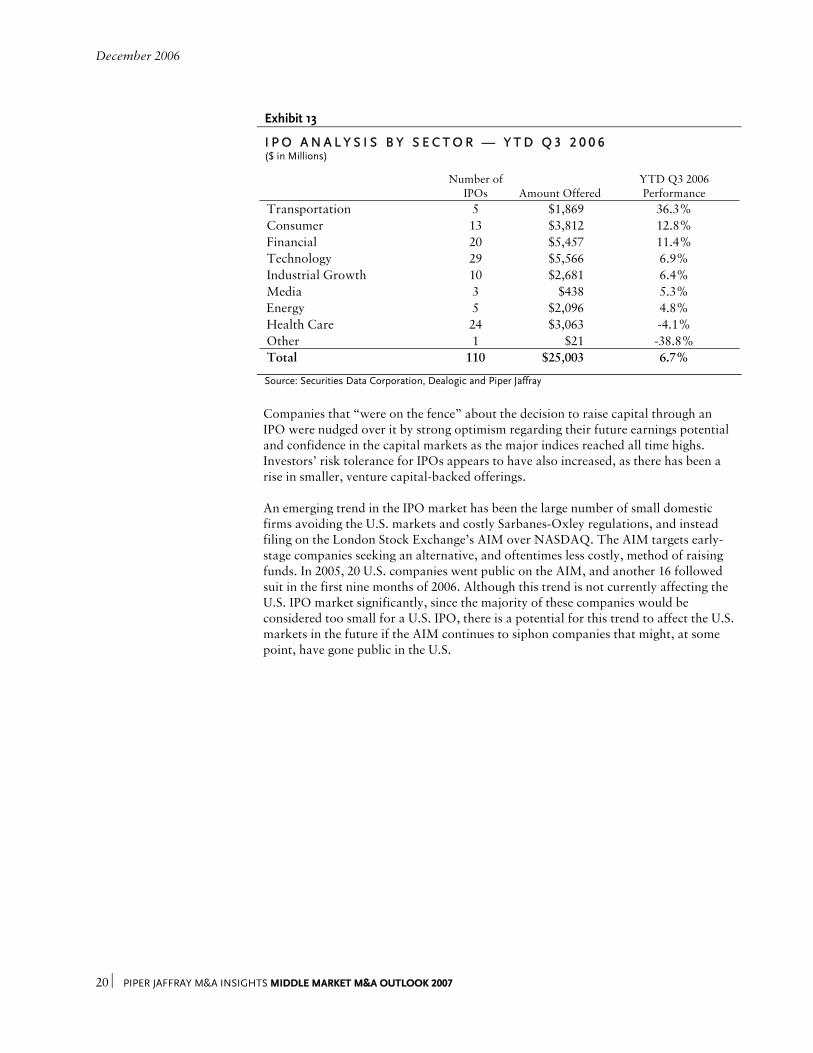

Exhibit 13

I P O A N A L Y S I S B Y S E C T O R — Y T D Q 3 2 0 0 6 ($ in Millions)

Number of

IPOs Amount Offered YTD Q3 2006 Performance

Transportation 5 $1,869 36.3% Consumer 13 $3,812 12.8% Financial 20 $5,457 11.4% Technology 29 $5,566 6.9% Industrial Growth 10 $2,681 6.4% Media 3 $438 5.3% Energy 5 $2,096 4.8% Health Care 24 $3,063 -4.1% Other 1 $21 -38.8% Total 110 $25,003 6.7%

Source: Securities Data Corporation, Dealogic and Piper Jaffray

Companies that “were on the fence” about the decision to raise capital through an IPO were nudged over it by strong optimism regarding their future earnings potential and confidence in the capital markets as the major indices reached all time highs. Investors’ risk tolerance for IPOs appears to have also increased, as there has been a rise in smaller, venture capital-backed offerings. An emerging trend in the IPO market has been the large number of small domestic firms avoiding the U.S. markets and costly Sarbanes-Oxley regulations, and instead filing on the London Stock Exchange’s AIM over NASDAQ. The AIM targets early-stage companies seeking an alternative, and oftentimes less costly, method of raising funds. In 2005, 20 U.S. companies went public on the AIM, and another 16 followed suit in the first nine months of 2006. Although this trend is not currently affecting the U.S. IPO market significantly, since the majority of these companies would be considered too small for a U.S. IPO, there is a potential for this trend to affect the U.S. markets in the future if the AIM continues to siphon companies that might, at some point, have gone public in the U.S.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 21

Exhibit 14

S P O N S O R - B A C K E D I P O A N A L Y S I S ($ in Billions)

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3 2005

YTD Q3 2006

0

50

100

150

200

250

300

350

400

450

500

Total Capital Raised Number of IPOs

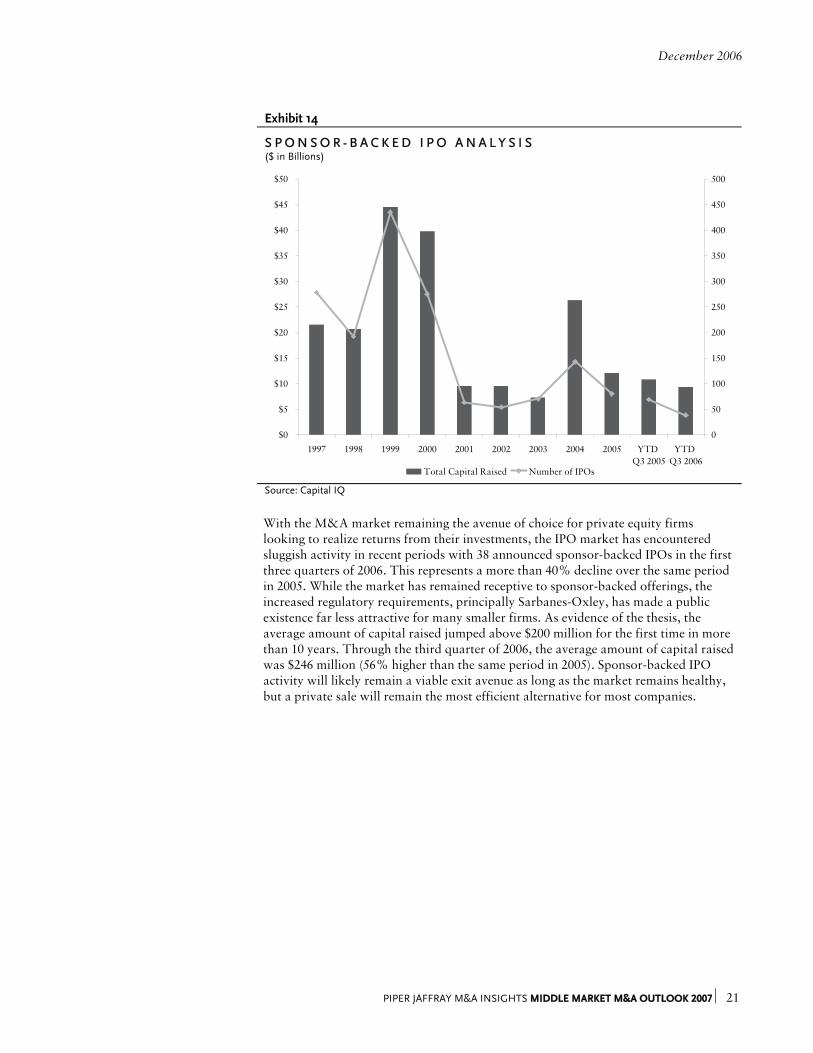

Source: Capital IQ With the M&A market remaining the avenue of choice for private equity firms

looking to realize returns from their investments, the IPO market has encountered sluggish activity in recent periods with 38 announced sponsor-backed IPOs in the first three quarters of 2006. This represents a more than 40% decline over the same period in 2005. While the market has remained receptive to sponsor-backed offerings, the increased regulatory requirements, principally Sarbanes-Oxley, has made a public existence far less attractive for many smaller firms. As evidence of the thesis, the average amount of capital raised jumped above $200 million for the first time in more than 10 years. Through the third quarter of 2006, the average amount of capital raised was $246 million (56% higher than the same period in 2005). Sponsor-backed IPO activity will likely remain a viable exit avenue as long as the market remains healthy, but a private sale will remain the most efficient alternative for most companies.

December 2006

22 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

P A R T I I I : P R I V A T E E Q U I T Y / L E V E R A G E D B U Y O U T S

Introduction

2006 is following up the record-setting levels of 2004 and 2005 with another stellar performance. To date, 2006 has been highlighted by one giant take-private after another, with deal sizes that have not been seen since the 1980s. Announcements of $15 billion and $20 billion transactions have become commonplace over the past year, with such behemoths as office building owner Equity Office Properties Trust ($36 billion), hospital operator HCA Inc. ($33 billion), casino operator Harrah’s ($26 billion) and pipeline operator Kinder Morgan ($22 billion), all having been announced in the past year. The new mega-funds (greater than $10 billion) are opening up entirely new sectors of the M&A market, putting deals in play that previously had not been considered. Private equity also continues to play an increasingly important role in cross-border investments, with global flows of foreign direct investment expected to exceed $1 trillion for the first time since 2000. Investments in the Asia-Pacific region continue to grow and gain prominence in the private equity community with China and India increasing their clout and capabilities constantly. The overall growth in deal volume and size has played out across a wide swath of industries, deal sizes and geographies as both buyers and sellers benefited from an abundance of available capital, strong business fundamentals and performances, and a supportive macroeconomic environment. Valuations are healthy, and attractive properties remain widely available in the market. Although all signs continue to point toward further strength, there may be a few clouds on the horizon. In our view, there appears to be a bifurcation of deals coming to the market recently, with many more companies in the market with stories to tell. Financial buyers are pursuing the “A” properties with increasing vigor, investing more time, resources and dollars in the early stages of processes to increase their chances of success. Conversely, “B” properties are finding a much less responsive audience. While these deals are still getting done, private equity interest is more restrained and the processes are more difficult. Shorter hold periods for investments may be an indication that sponsors believe that the market is going to turn and are trying to get liquid. A slight hiccup in the economy or another unforeseen catastrophe, whether man-made or natural, could depress the market rather quickly. Although we expect that the current strength of M&A activity will continue into 2007, it is hard for us to believe that there is room for significant improvement for the whole year versus a robust 2006. A slowdown in the M&A market is somewhere on the horizon; how quickly it approaches, though, is still up for debate.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 23

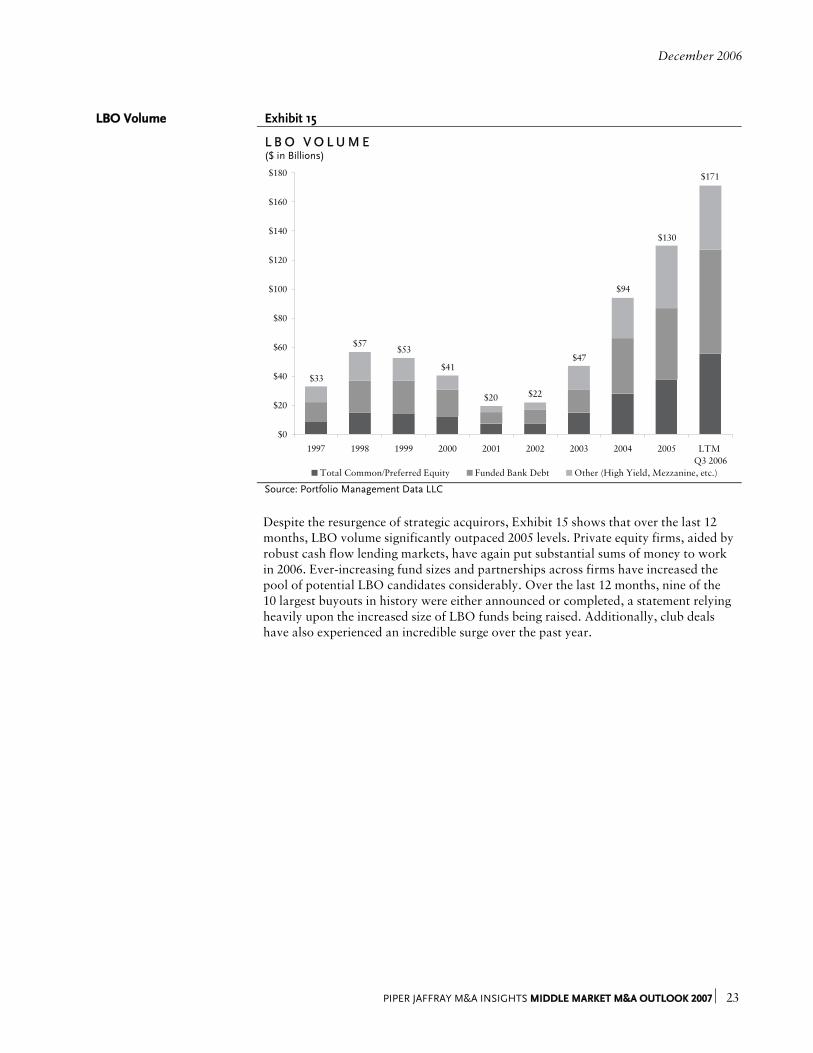

LBO Volume Exhibit 15

L B O V O L U M E ($ in Billions)

$33

$57$53

$41

$20 $22

$47

$94

$130

$171

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

1997 1998 1999 2000 2001 2002 2003 2004 2005 LTM Q3 2006

Total Common/Preferred Equity Funded Bank Debt Other (High Yield, Mezzanine, etc.) Source: Portfolio Management Data LLC

Despite the resurgence of strategic acquirors, Exhibit 15 shows that over the last 12

months, LBO volume significantly outpaced 2005 levels. Private equity firms, aided by robust cash flow lending markets, have again put substantial sums of money to work in 2006. Ever-increasing fund sizes and partnerships across firms have increased the pool of potential LBO candidates considerably. Over the last 12 months, nine of the 10 largest buyouts in history were either announced or completed, a statement relying heavily upon the increased size of LBO funds being raised. Additionally, club deals have also experienced an incredible surge over the past year.

December 2006

24 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

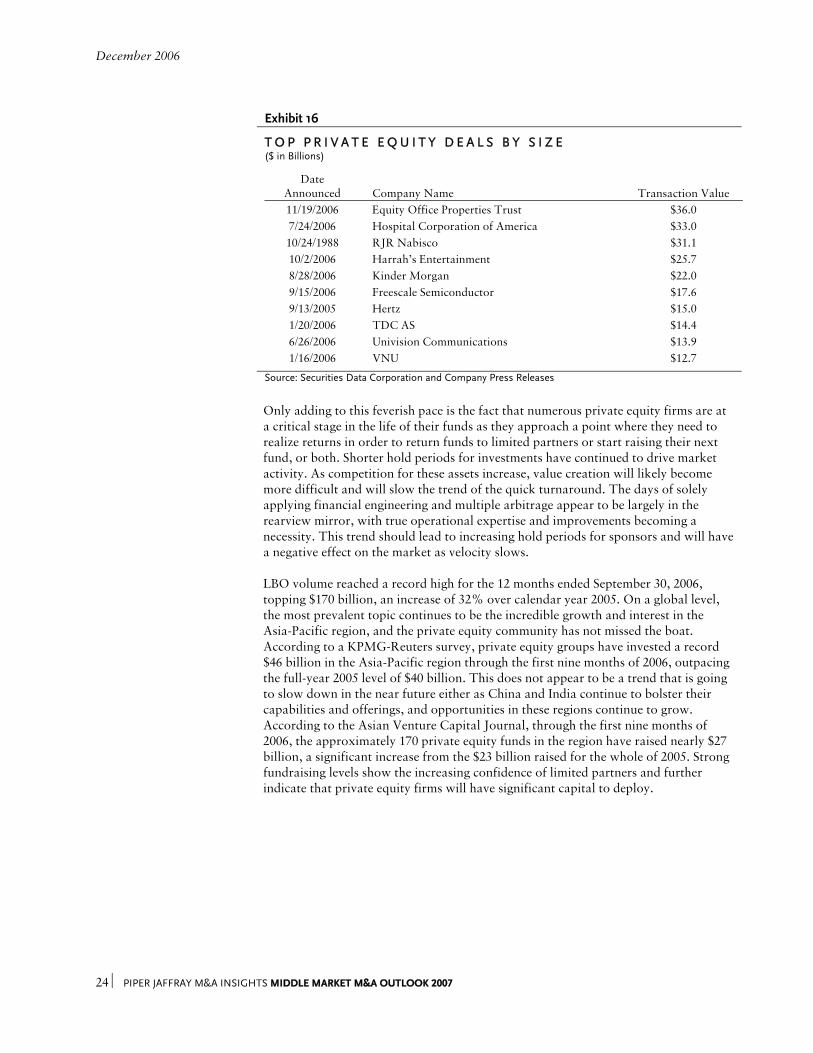

Exhibit 16

T O P P R I V A T E E Q U I T Y D E A L S B Y S I Z E ($ in Billions)

Date

Announced Company Name Transaction Value 11/19/2006 Equity Office Properties Trust $36.0 7/24/2006 Hospital Corporation of America $33.0 10/24/1988 RJR Nabisco $31.1 10/2/2006 Harrah’s Entertainment $25.7 8/28/2006 Kinder Morgan $22.0 9/15/2006 Freescale Semiconductor $17.6 9/13/2005 Hertz $15.0 1/20/2006 TDC AS $14.4 6/26/2006 Univision Communications $13.9 1/16/2006 VNU $12.7

Source: Securities Data Corporation and Company Press Releases Only adding to this feverish pace is the fact that numerous private equity firms are at

a critical stage in the life of their funds as they approach a point where they need to realize returns in order to return funds to limited partners or start raising their next fund, or both. Shorter hold periods for investments have continued to drive market activity. As competition for these assets increase, value creation will likely become more difficult and will slow the trend of the quick turnaround. The days of solely applying financial engineering and multiple arbitrage appear to be largely in the rearview mirror, with true operational expertise and improvements becoming a necessity. This trend should lead to increasing hold periods for sponsors and will have a negative effect on the market as velocity slows. LBO volume reached a record high for the 12 months ended September 30, 2006, topping $170 billion, an increase of 32% over calendar year 2005. On a global level, the most prevalent topic continues to be the incredible growth and interest in the Asia-Pacific region, and the private equity community has not missed the boat. According to a KPMG-Reuters survey, private equity groups have invested a record $46 billion in the Asia-Pacific region through the first nine months of 2006, outpacing the full-year 2005 level of $40 billion. This does not appear to be a trend that is going to slow down in the near future either as China and India continue to bolster their capabilities and offerings, and opportunities in these regions continue to grow. According to the Asian Venture Capital Journal, through the first nine months of 2006, the approximately 170 private equity funds in the region have raised nearly $27 billion, a significant increase from the $23 billion raised for the whole of 2005. Strong fundraising levels show the increasing confidence of limited partners and further indicate that private equity firms will have significant capital to deploy.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 25

Portfolio Company Hold Exhibit 17 Periods

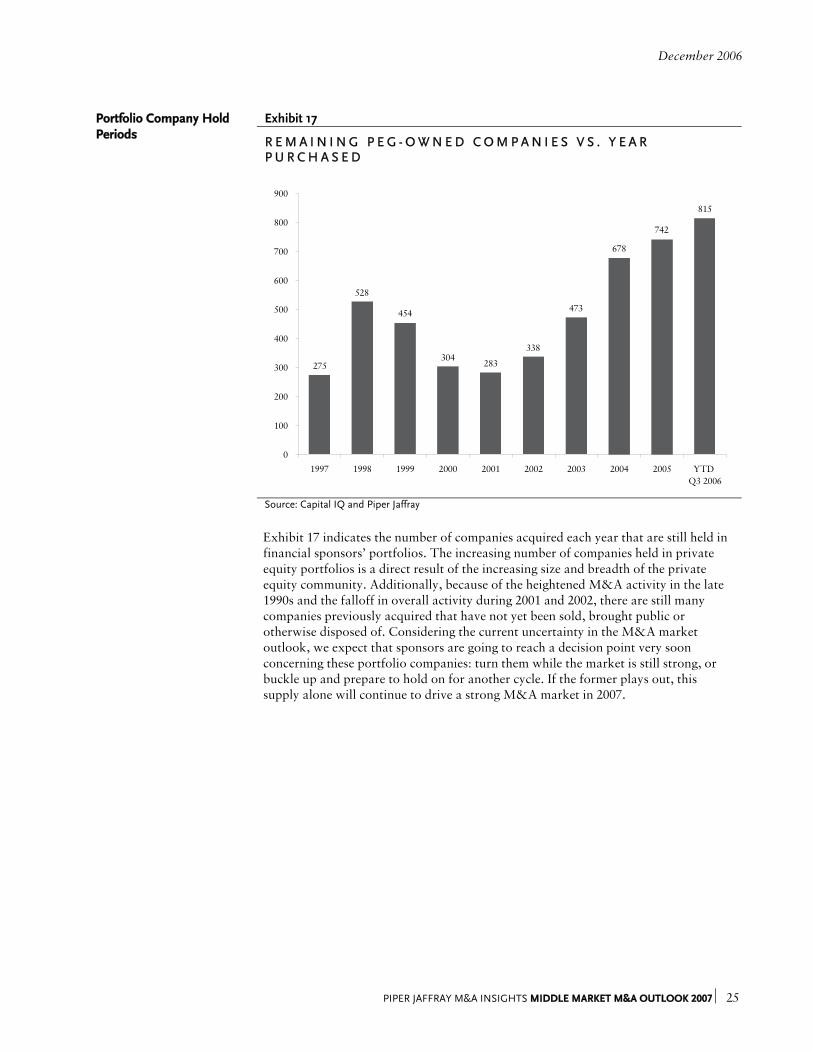

R E M A I N I N G P E G - O W N E D C O M P A N I E S V S . Y E A R P U R C H A S E D

275

473

815

742

678

338

283304

454

528

0

100

200

300

400

500

600

700

800

900

1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3 2006

Source: Capital IQ and Piper Jaffray

Exhibit 17 indicates the number of companies acquired each year that are still held in

financial sponsors’ portfolios. The increasing number of companies held in private equity portfolios is a direct result of the increasing size and breadth of the private equity community. Additionally, because of the heightened M&A activity in the late 1990s and the falloff in overall activity during 2001 and 2002, there are still many companies previously acquired that have not yet been sold, brought public or otherwise disposed of. Considering the current uncertainty in the M&A market outlook, we expect that sponsors are going to reach a decision point very soon concerning these portfolio companies: turn them while the market is still strong, or buckle up and prepare to hold on for another cycle. If the former plays out, this supply alone will continue to drive a strong M&A market in 2007.

December 2006

26 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

Private Equity Fundraising Exhibit 18

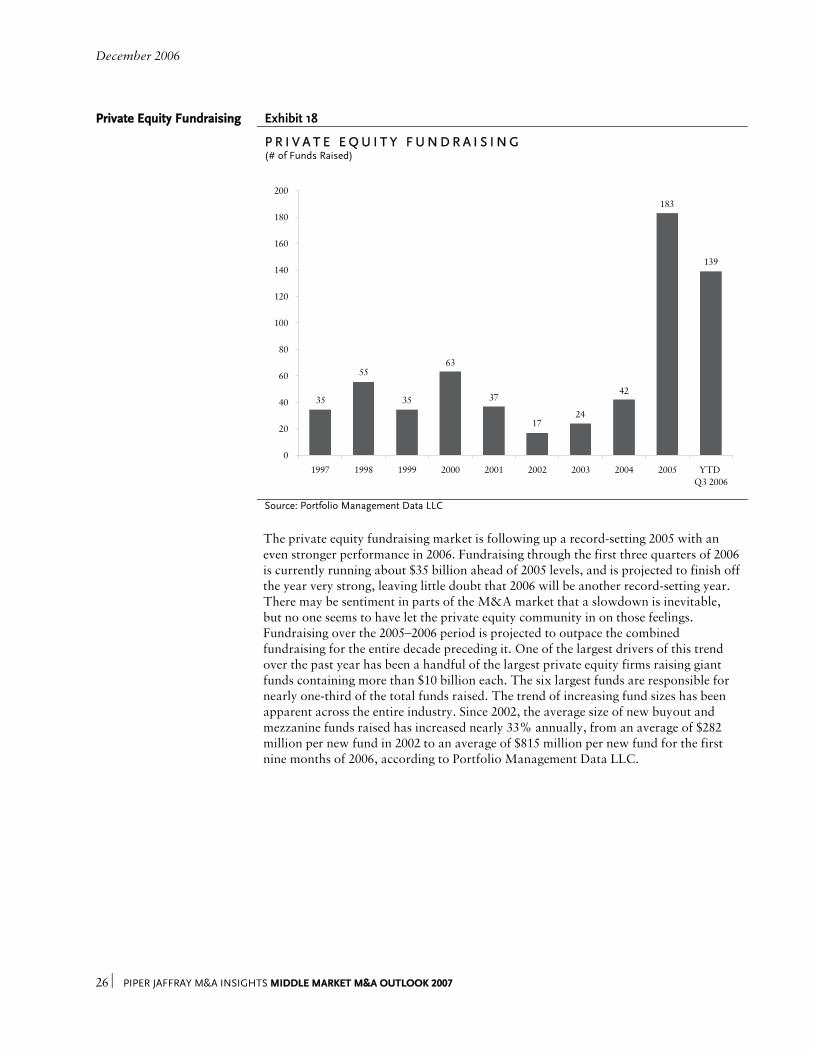

P R I V A T E E Q U I T Y F U N D R A I S I N G (# of Funds Raised)

139

183

42

17

37

63

35

55

3524

0

20

40

60

80

100

120

140

160

180

200

1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3 2006

Source: Portfolio Management Data LLC

The private equity fundraising market is following up a record-setting 2005 with an

even stronger performance in 2006. Fundraising through the first three quarters of 2006 is currently running about $35 billion ahead of 2005 levels, and is projected to finish off the year very strong, leaving little doubt that 2006 will be another record-setting year. There may be sentiment in parts of the M&A market that a slowdown is inevitable, but no one seems to have let the private equity community in on those feelings. Fundraising over the 2005–2006 period is projected to outpace the combined fundraising for the entire decade preceding it. One of the largest drivers of this trend over the past year has been a handful of the largest private equity firms raising giant funds containing more than $10 billion each. The six largest funds are responsible for nearly one-third of the total funds raised. The trend of increasing fund sizes has been apparent across the entire industry. Since 2002, the average size of new buyout and mezzanine funds raised has increased nearly 33% annually, from an average of $282 million per new fund in 2002 to an average of $815 million per new fund for the first nine months of 2006, according to Portfolio Management Data LLC.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 27

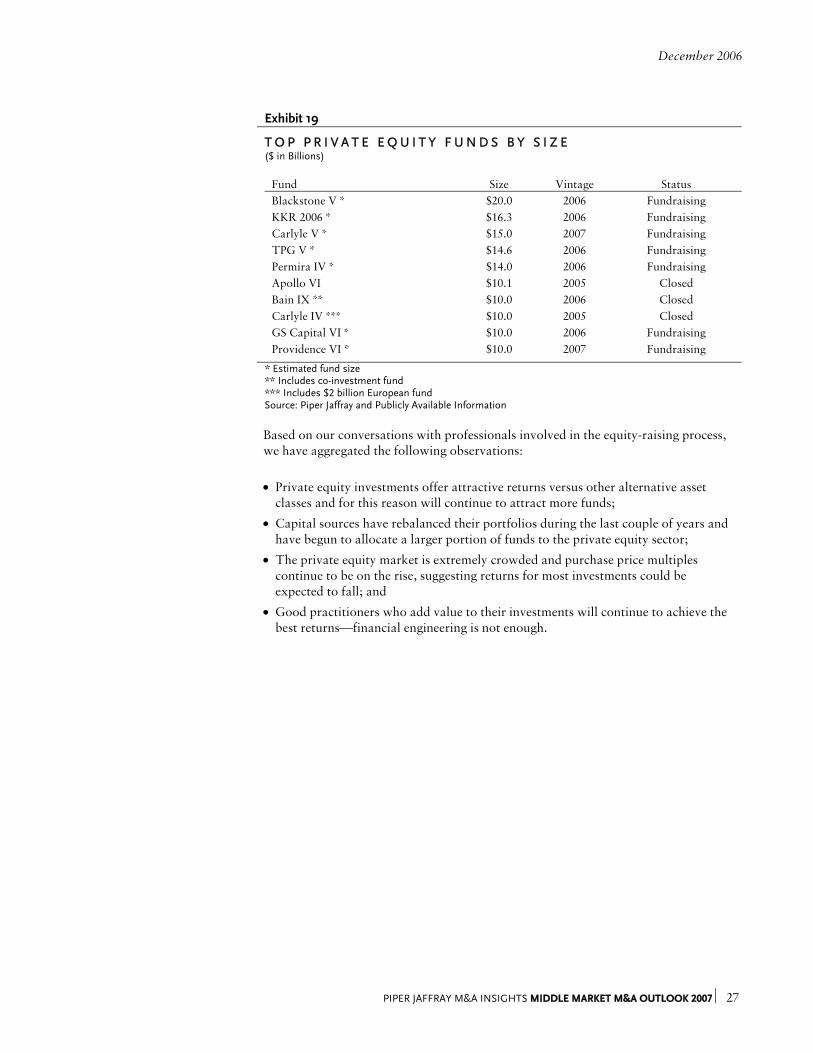

Exhibit 19

T O P P R I V A T E E Q U I T Y F U N D S B Y S I Z E ($ in Billions)

Fund Size Vintage Status Blackstone V * $20.0 2006 Fundraising KKR 2006 * $16.3 2006 Fundraising Carlyle V * $15.0 2007 Fundraising TPG V * $14.6 2006 Fundraising Permira IV * $14.0 2006 Fundraising Apollo VI $10.1 2005 Closed Bain IX ** $10.0 2006 Closed Carlyle IV *** $10.0 2005 Closed GS Capital VI * $10.0 2006 Fundraising Providence VI * $10.0 2007 Fundraising

* Estimated fund size

** Includes co-investment fund *** Includes $2 billion European fund Source: Piper Jaffray and Publicly Available Information

Based on our conversations with professionals involved in the equity-raising process,

we have aggregated the following observations:

• Private equity investments offer attractive returns versus other alternative asset classes and for this reason will continue to attract more funds;

• Capital sources have rebalanced their portfolios during the last couple of years and have begun to allocate a larger portion of funds to the private equity sector;

• The private equity market is extremely crowded and purchase price multiples continue to be on the rise, suggesting returns for most investments could be expected to fall; and

• Good practitioners who add value to their investments will continue to achieve the best returns—financial engineering is not enough.

December 2006

28 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

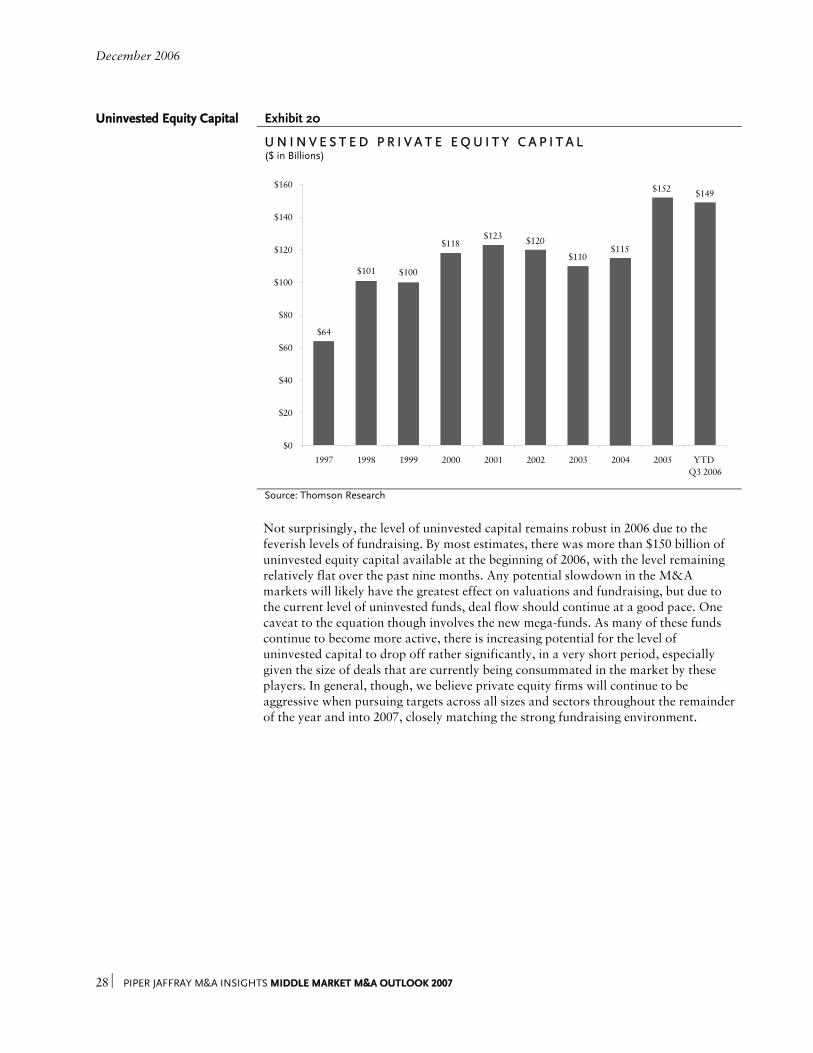

Uninvested Equity Capital Exhibit 20

U N I N V E S T E D P R I V A T E E Q U I T Y C A P I T A L ($ in Billions)

$149$152

$115$120$123

$118

$100$101

$64

$110

$0

$20

$40

$60

$80

$100

$120

$140

$160

1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3 2006

Source: Thomson Research

Not surprisingly, the level of uninvested capital remains robust in 2006 due to the

feverish levels of fundraising. By most estimates, there was more than $150 billion of uninvested equity capital available at the beginning of 2006, with the level remaining relatively flat over the past nine months. Any potential slowdown in the M&A markets will likely have the greatest effect on valuations and fundraising, but due to the current level of uninvested funds, deal flow should continue at a good pace. One caveat to the equation though involves the new mega-funds. As many of these funds continue to become more active, there is increasing potential for the level of uninvested capital to drop off rather significantly, in a very short period, especially given the size of deals that are currently being consummated in the market by these players. In general, though, we believe private equity firms will continue to be aggressive when pursuing targets across all sizes and sectors throughout the remainder of the year and into 2007, closely matching the strong fundraising environment.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 29

Competitive Environment As the middle market has become more competitive, financial acquirors have been

forced to differentiate themselves from the pack with both prospective targets and potential limited partners. Increasingly, private equity firms are earnestly seeking an “angle” that will allow them to bid aggressively and distinguish themselves in a competitive process. In particular, sponsors are often attempting to demonstrate the following attributes:

• Demonstrated industry expertise (e.g., ability to drive operational improvements, pursue growth through add-on acquisitions);

• Unique firm attributes such as an executive network or in-house operational expertise;

• Ability to move quickly and provide certainty to close;

• Commitment and dedication to the deal by investing significant time, resources and dollars up front; and

• Good chemistry with management teams. Overall, we expect the private equity community to remain extremely active through 2007. Private equity firms are expected to continue to be active sellers of portfolio companies to take advantage of the current high valuations. More cyclical companies with improved financial performance and investments have performed particularly well. Likewise, more capital almost certainly will be put to work against a backdrop of a strong economy and robust financing markets.

December 2006

30 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

P A R T I V : S T R A T E G I C B U Y E R S

Introduction

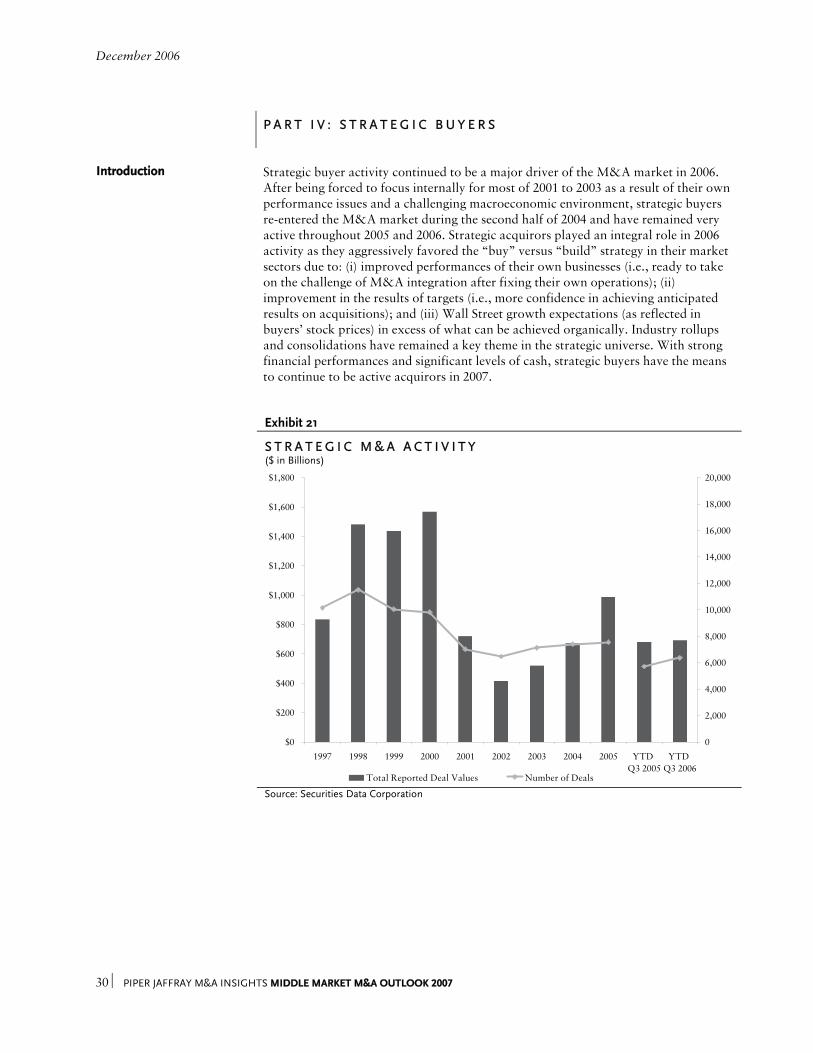

Strategic buyer activity continued to be a major driver of the M&A market in 2006. After being forced to focus internally for most of 2001 to 2003 as a result of their own performance issues and a challenging macroeconomic environment, strategic buyers re-entered the M&A market during the second half of 2004 and have remained very active throughout 2005 and 2006. Strategic acquirors played an integral role in 2006 activity as they aggressively favored the “buy” versus “build” strategy in their market sectors due to: (i) improved performances of their own businesses (i.e., ready to take on the challenge of M&A integration after fixing their own operations); (ii) improvement in the results of targets (i.e., more confidence in achieving anticipated results on acquisitions); and (iii) Wall Street growth expectations (as reflected in buyers’ stock prices) in excess of what can be achieved organically. Industry rollups and consolidations have remained a key theme in the strategic universe. With strong financial performances and significant levels of cash, strategic buyers have the means to continue to be active acquirors in 2007.

Exhibit 21

S T R A T E G I C M & A A C T I V I T Y ($ in Billions)

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

1997 1998 1999 2000 2001 2002 2003 2004 2005 YTD Q3 2005

YTD Q3 2006

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

Total Reported Deal Values Number of Deals Source: Securities Data Corporation

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 31

While the total number of deals has remained fairly consistent over the past five years,

the average deal size has been increasing rather consistently since 2002. This has not been the case over the first nine months of 2006, with average deal sizes taking a slight dip compared to the prior year, although remaining strong. Total strategic deal value (where strategic acquirors purchased U.S.-based companies) increased 2% for the first three quarters of 2006 versus the same period last year, while the total number of deals increased nearly 11%. When compared to the overall U.S. M&A market, as mentioned in the first section of this report, strategic M&A activity lagged total deal values (a 2% increase compared to a 13% increase) but was relatively inline with the percentage increase in the number of transactions (an 11% increase compared to a 10% increase) for the first three quarters over the same period last year. Total value of the strategic M&A market continues to be driven by a host of mega-mergers as illustrated in Exhibit 22.

Exhibit 22

L A R G E S T S T R A T E G I C T R A N S A C T I O N S B Y V A L U E ($ in Billions)

Date

Announced Target Acquiror Transaction

Value 3/24/2006 BellSouth Corp. AT&T Inc. $66.7 11/19/2006 Phelps Dodge Corp. Freeport McMoRan $25.8 5/07/2006 Golden West Financial Corp. Wachovia Corp. $25.0 6/22/2006 Kerr-McGee Corp. Anadarko Petroleum Corp. $19.0 6/26/2006 Pfizer Consumer Healthcare Johnson & Johnson Inc. $16.6 3/12/2006 North Fork Bancorp Capital One Financial $14.8 4/02/2006 Lucent Technologies Inc. Alcatel SA $17.0 5/07/2006 Fisher Scientific Inc. Thermo Electron Corp. $11.9 2/25/2006 KeySpan Corp. National Grid plc $11.8 5/24/2006 AmSouth Bancorp Regions Financial Corp. $10.1

Source: Securities Data Corporation and Company Press Releases Capital Structure

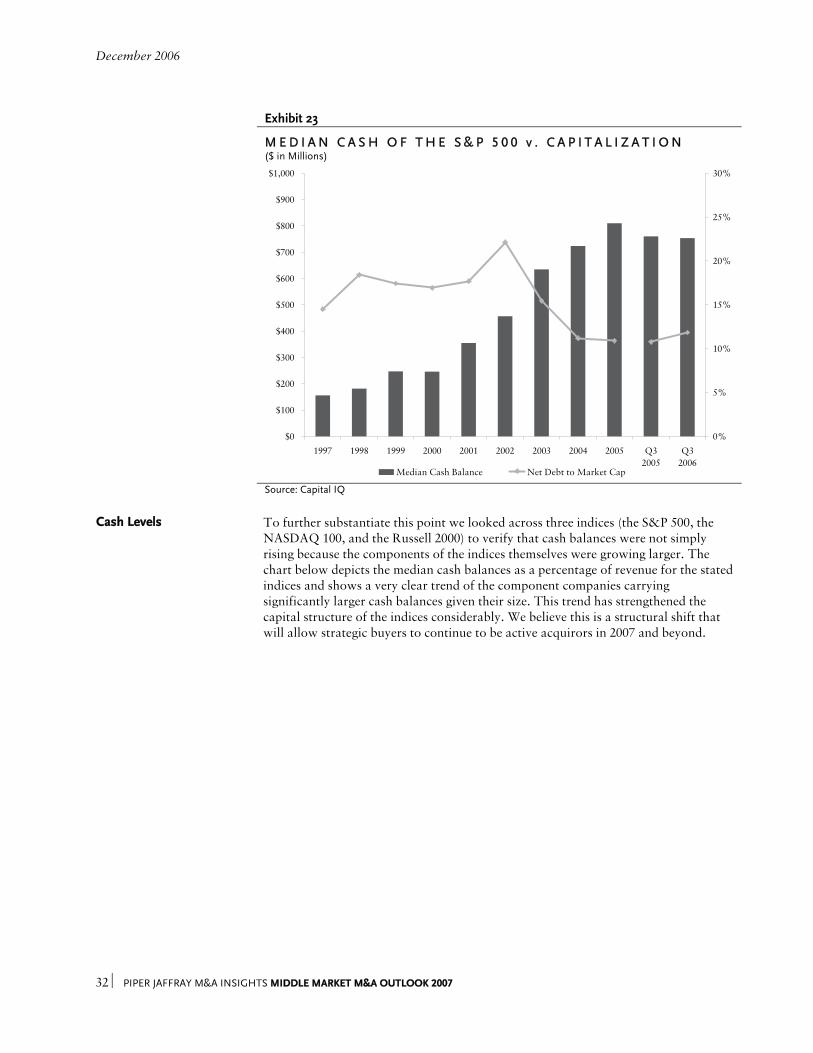

Because of the strong operational and financial results of the strategic buyer universe and the U.S. economy in general over the past few years, U.S. companies have been able to delever their balance sheets, while at the same time build considerable cash reserves. After experiencing a very challenging environment through the bubble burst over the turn of the century, and numerous natural and man-made events since then, many of these companies have decided to play it safer by building their own insurance policies into their capital structure through increased cash holdings and a reduction in net debt. An added bonus of this safety net is that it makes these strategic buyers much more flexible and better prepared to take on potential M&A opportunities that they may have otherwise passed on. The median cash balance for the S&P 500 as of the third quarter 2006, was $727 million, a decline of 4% versus the September 30, 2005, figure of $761 million, but nearly twice the average level from the previous decade of $382 million. The median net debt to market capitalization ratio has also fallen dramatically over the past four years, from a peak of nearly 30% in 2002 to a new level hovering around 11% to 12% since 2004, with the September 2006 level coming in at 12%.

December 2006

32 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

Exhibit 23

M E D I A N C A S H O F T H E S & P 5 0 0 v . C A P I T A L I Z A T I O N ($ in Millions)

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 Q32005

Q32006

0%

5%

10%

15%

20%

25%

30%

Median Cash Balance Net Debt to Market Cap

Source: Capital IQ

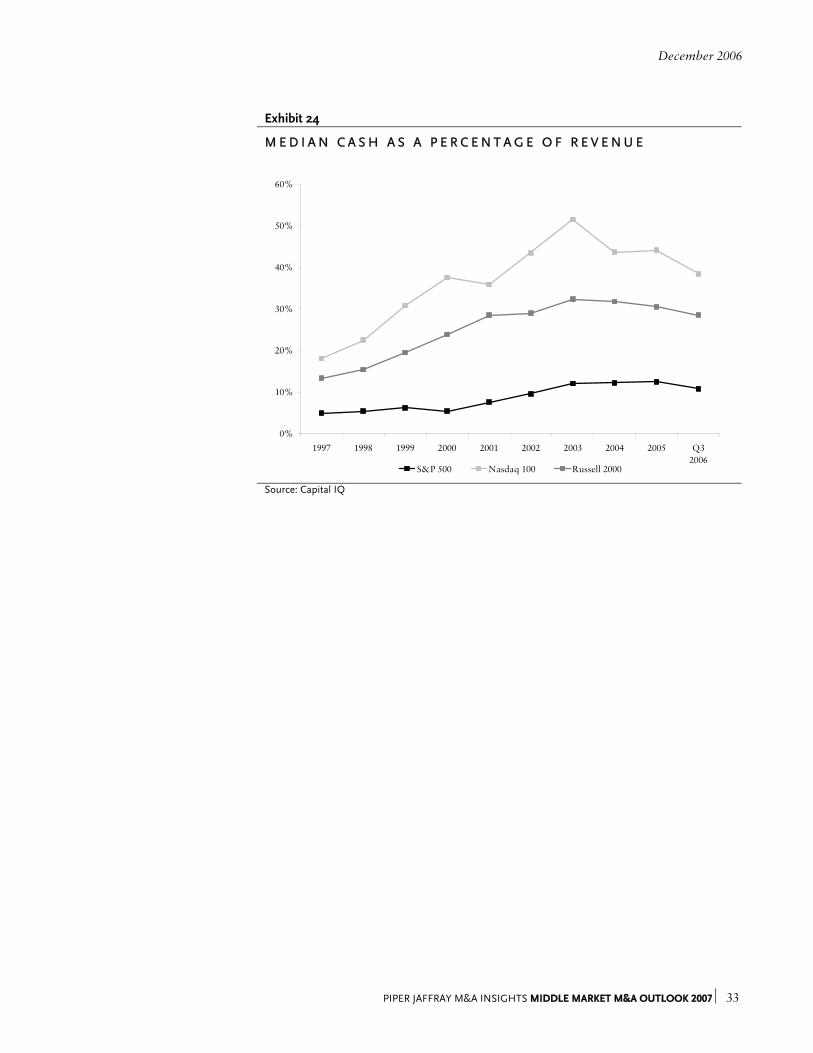

Cash Levels

To further substantiate this point we looked across three indices (the S&P 500, the NASDAQ 100, and the Russell 2000) to verify that cash balances were not simply rising because the components of the indices themselves were growing larger. The chart below depicts the median cash balances as a percentage of revenue for the stated indices and shows a very clear trend of the component companies carrying significantly larger cash balances given their size. This trend has strengthened the capital structure of the indices considerably. We believe this is a structural shift that will allow strategic buyers to continue to be active acquirors in 2007 and beyond.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 33

Exhibit 24

M E D I A N C A S H A S A P E R C E N T A G E O F R E V E N U E

0%

10%

20%

30%

40%

50%

60%

1997 1998 1999 2000 2001 2002 2003 2004 2005 Q32006

S&P 500 Nasdaq 100 Russell 2000

Source: Capital IQ

December 2006

34 ⏐ PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007

P A R T V : C O N C L U S I O N

Last year, we wrote that we believed 2006 was poised for continued strength and growth in the M&A market but that it was unlikely that 2006 would significantly outperform 2005. It appears that we may have been overly conservative in our outlook of the M&A market. 2006 turned out to be another record year in terms of M&A activity. M&A activity has increased year-to-date (as of the end of the third quarter) over last year with 10% more announced transactions and a 13% increase in deal value. Our outlook for 2007 definitely would be classified as more conservative. We are now three years into an active M&A market and signs are beginning to point toward fatigue. Many quality properties have successfully come to market and while many “A” properties remain in the pipeline, many lesser-grade companies remain also. The bifurcation between the two classes has started to become more apparent, with the top-quality companies demanding as much attention as ever before, and their more complex and storied counterparts receiving more scrutiny. Capital is cheap, fundraising remains strong and uninvested capital persists at record highs, but there seems to be an increasing feeling that the music is going to end soon. We are not ruling out a prolonged set or an encore or two, but eventually the lights are going to be turned on and the show must end. While risks surround the longevity of the bullish economy, most of these risks are not new. Natural disasters, terrorist activity, pressure on the U.S. dollar, volatile and rising commodity prices and political uncertainty relating to the global conflicts have existed throughout the bull run in the M&A market. There are still many strong signs in the M&A market that point toward continued strength. Additionally, we believe that the growth in the M&A market over the past three years has been built on stronger fundamentals than past periods and that a potential slowdown will be much more muted than those experienced over the past decade. There are many fundamental differences between the current M&A market and those of the past:

• Liquidity in the debt markets—In 2000, the debt markets dried up. We believe that is less likely to occur now because of an influx of autonomous, unregulated, market-funded lenders that have come online since 2000 and created greater overall diversity in the debt markets;

• Large capital pools—There is a record level of uninvested capital in the private equity world that needs to be deployed, and with the ever-increasing size of funds, the scope of potential targets has increased as financial buyers are able to take on much larger acquisitions than any time in the past;

• Broader, more diversified market potential—International markets have opened up considerably over recent years, with substantial opportunities continuing to present themselves and become more viable in emerging markets such as Brazil, China, India and Russia;

• Fundamental buy/sell cycle of private equity firms—The growth of private equity firms and their need to buy and sell into and out of their portfolios will reduce cyclicality more now than in 2000 as they are a bigger portion of the overall M&A market; and

• Healthier strategic acquirors—Strategic acquirors now have large amounts of cash on their balance sheets and have significantly delevered over the past few years.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 35

Although there are some clouds on the horizon, we do not believe it is time to pull out the umbrellas just yet. While we don’t believe that M&A activity in 2007 will be able to top the impressive results of 2006 and the potential for a slowdown in the market is as high as it has been since this cycle began, we continue to be optimistic for another solid year in terms of activity, as the market is currently much healthier, more robust and potentially more resilient than it has ever been in the past, and is well-positioned to meet any eventual problems head-on.

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 36 ⏐

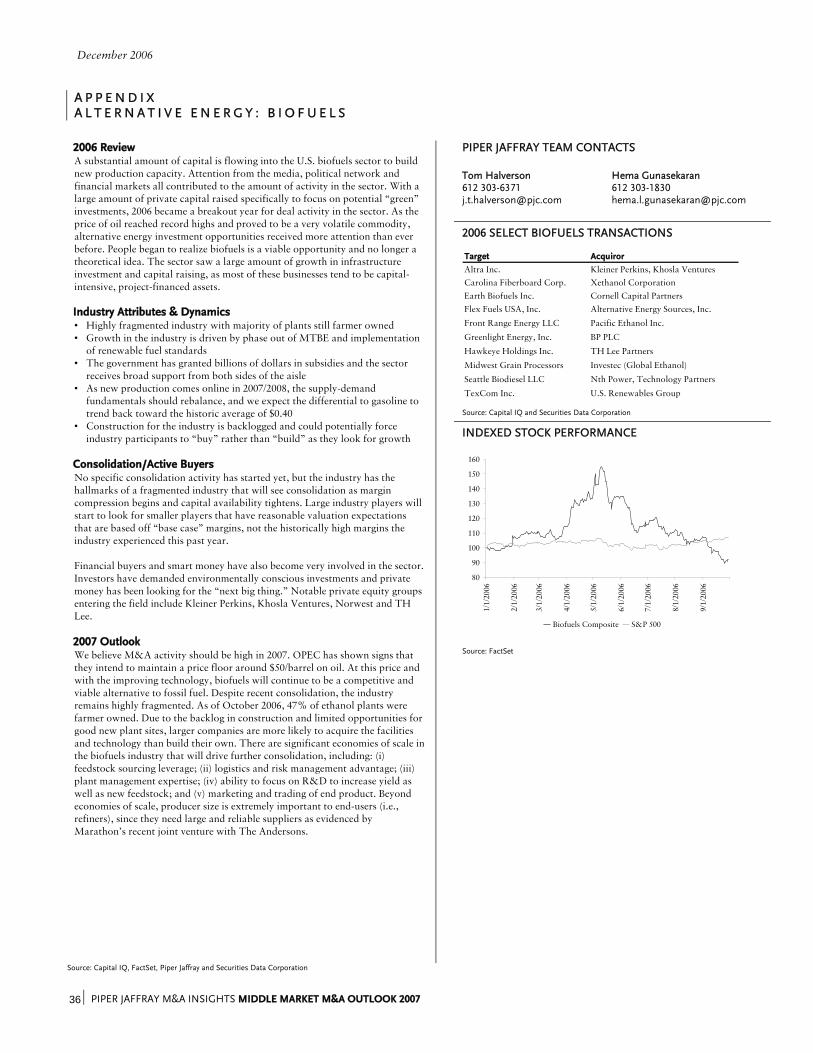

A P P E N D I X A L T E R N A T I V E E N E R G Y : B I O F U E L S

PIPER JAFFRAY TEAM CONTACTS Tom Halverson Hema Gunasekaran 612 303-6371 612 303-1830 [email protected] [email protected]

2006 SELECT BIOFUELS TRANSACTIONS

Target Acquiror

Altra Inc. Kleiner Perkins, Khosla VenturesCarolina Fiberboard Corp. Xethanol CorporationEarth Biofuels Inc. Cornell Capital PartnersFlex Fuels USA, Inc. Alternative Energy Sources, Inc.

Front Range Energy LLC Pacific Ethanol Inc.

Greenlight Energy, Inc. BP PLC

Hawkeye Holdings Inc. TH Lee Partners

Midwest Grain Processors Investec (Global Ethanol)

Seattle Biodiesel LLC Nth Power, Technology Partners

TexCom Inc. U.S. Renewables Group

Source: Capital IQ and Securities Data Corporation

2006 Review A substantial amount of capital is flowing into the U.S. biofuels sector to build new production capacity. Attention from the media, political network and financial markets all contributed to the amount of activity in the sector. With a large amount of private capital raised specifically to focus on potential “green” investments, 2006 became a breakout year for deal activity in the sector. As the price of oil reached record highs and proved to be a very volatile commodity, alternative energy investment opportunities received more attention than ever before. People began to realize biofuels is a viable opportunity and no longer a theoretical idea. The sector saw a large amount of growth in infrastructure investment and capital raising, as most of these businesses tend to be capital-intensive, project-financed assets. Industry Attributes & Dynamics • Highly fragmented industry with majority of plants still farmer owned • Growth in the industry is driven by phase out of MTBE and implementation

of renewable fuel standards • The government has granted billions of dollars in subsidies and the sector

receives broad support from both sides of the aisle • As new production comes online in 2007/2008, the supply-demand

fundamentals should rebalance, and we expect the differential to gasoline to trend back toward the historic average of $0.40

• Construction for the industry is backlogged and could potentially force industry participants to “buy” rather than “build” as they look for growth

Consolidation/Active Buyers No specific consolidation activity has started yet, but the industry has the hallmarks of a fragmented industry that will see consolidation as margin compression begins and capital availability tightens. Large industry players will start to look for smaller players that have reasonable valuation expectations that are based off “base case” margins, not the historically high margins the industry experienced this past year. Financial buyers and smart money have also become very involved in the sector. Investors have demanded environmentally conscious investments and private money has been looking for the “next big thing.” Notable private equity groups entering the field include Kleiner Perkins, Khosla Ventures, Norwest and TH Lee. 2007 Outlook We believe M&A activity should be high in 2007. OPEC has shown signs that they intend to maintain a price floor around $50/barrel on oil. At this price and with the improving technology, biofuels will continue to be a competitive and viable alternative to fossil fuel. Despite recent consolidation, the industry remains highly fragmented. As of October 2006, 47% of ethanol plants were farmer owned. Due to the backlog in construction and limited opportunities for good new plant sites, larger companies are more likely to acquire the facilities and technology than build their own. There are significant economies of scale in the biofuels industry that will drive further consolidation, including: (i) feedstock sourcing leverage; (ii) logistics and risk management advantage; (iii) plant management expertise; (iv) ability to focus on R&D to increase yield as well as new feedstock; and (v) marketing and trading of end product. Beyond economies of scale, producer size is extremely important to end-users (i.e., refiners), since they need large and reliable suppliers as evidenced by Marathon’s recent joint venture with The Andersons.

INDEXED STOCK PERFORMANCE

80

90

100

110

120

130

140

150

160

1/1/

2006

2/1/

2006

3/1/

2006

4/1/

2006

5/1/

2006

6/1/

2006

7/1/

2006

8/1/

2006

9/1/

2006

Biofuels Composite S&P 500

Source: FactSet

Source: Capital IQ, FactSet, Piper Jaffray and Securities Data Corporation

December 2006

PIPER JAFFRAY M&A INSIGHTS MIDDLE MARKET M&A OUTLOOK 2007 ⏐ 37

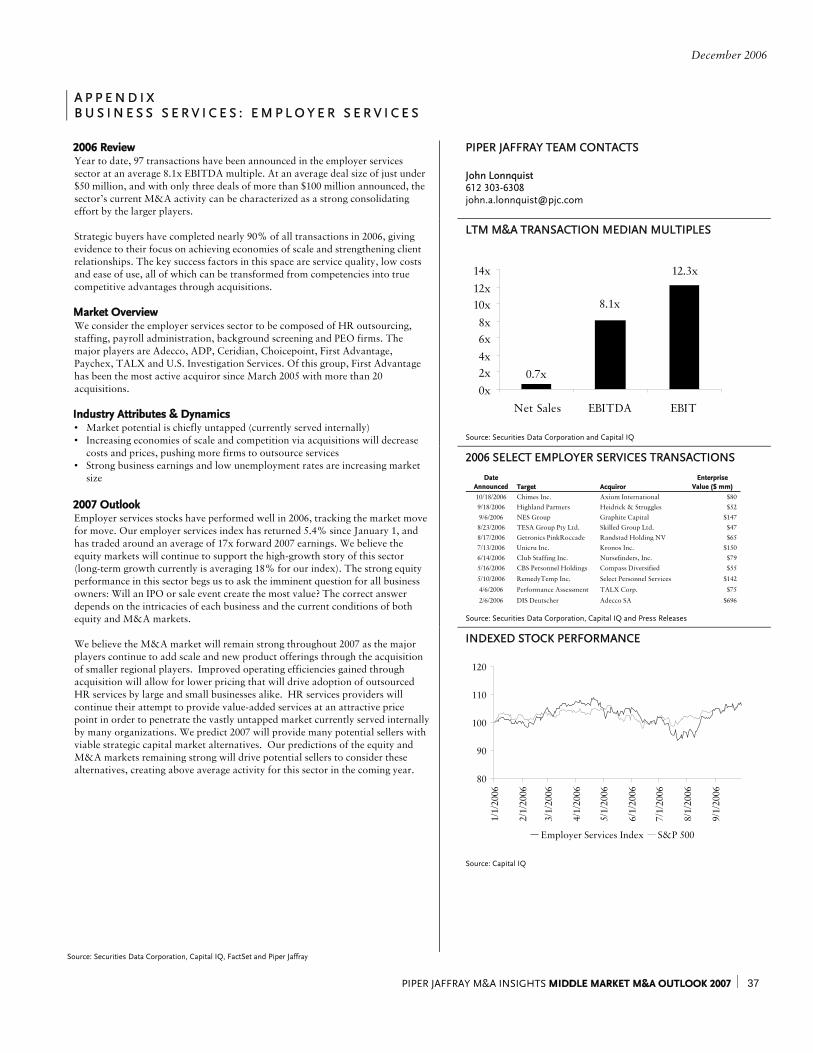

A P P E N D I X B U S I N E S S S E R V I C E S : E M P L O Y E R S E R V I C E S

PIPER JAFFRAY TEAM CONTACTS John Lonnquist 612 303-6308 [email protected]

LTM M&A TRANSACTION MEDIAN MULTIPLES

0.7x

8.1x

12.3x

0x2x4x6x8x

10x12x14x

Net Sales EBITDA EBIT

Source: Securities Data Corporation and Capital IQ

2006 SELECT EMPLOYER SERVICES TRANSACTIONS

DateAnnounced Target Acquiror

EnterpriseValue ($ mm)

10/18/2006 Chimes Inc. Axium International $809/18/2006 Highland Partners Heidrick & Struggles $529/6/2006 NES Group Graphite Capital $1478/23/2006 TESA Group Pty Ltd. Skilled Group Ltd. $478/17/2006 Getronics PinkRoccade Randstad Holding NV $657/13/2006 Unicru Inc. Kronos Inc. $1506/14/2006 Club Staffing Inc. Nursefinders, Inc. $795/16/2006 CBS Personnel Holdings Compass Diversified $55

5/10/2006 RemedyTemp Inc. Select Personnel Services $142

4/6/2006 Performance Assessment TALX Corp. $75

2/6/2006 DIS Deutscher Adecco SA $696

Source: Securities Data Corporation, Capital IQ and Press Releases

2006 Review Year to date, 97 transactions have been announced in the employer services sector at an average 8.1x EBITDA multiple. At an average deal size of just under $50 million, and with only three deals of more than $100 million announced, the sector’s current M&A activity can be characterized as a strong consolidating effort by the larger players. Strategic buyers have completed nearly 90% of all transactions in 2006, giving evidence to their focus on achieving economies of scale and strengthening client relationships. The key success factors in this space are service quality, low costs and ease of use, all of which can be transformed from competencies into true competitive advantages through acquisitions. Market Overview We consider the employer services sector to be composed of HR outsourcing, staffing, payroll administration, background screening and PEO firms. The major players are Adecco, ADP, Ceridian, Choicepoint, First Advantage, Paychex, TALX and U.S. Investigation Services. Of this group, First Advantage has been the most active acquiror since March 2005 with more than 20 acquisitions. Industry Attributes & Dynamics • Market potential is chiefly untapped (currently served internally) • Increasing economies of scale and competition via acquisitions will decrease

costs and prices, pushing more firms to outsource services • Strong business earnings and low unemployment rates are increasing market