member booklet - prudential staff pension scheme · prudentialstaff pension scheme –member...

TRANSCRIPT

Your Pension. Your Future.

Member Booklet

Defined Benefit Section

2

Contents

Introduction 2

The DB Section of the Scheme at a glance 3

Your benefits at Normal Retirement Date 4

Death before retirement 6

Death after retirement 7

Leaving the DB Section of the Scheme 8

Additional Voluntary Contributions 9

Temporary absence 10

Looking after your interests 10

Tax status 12

Changes in personal circumstances 12

The State and you 13

Definitions 14

Appendix 1-Reductions to your Annual Allowance 17

Introduction The Defined Benefit (DB) Section of thePrudential Staff Pension Scheme (theScheme) is an important and valuablebenefit the Company provides for itsemployees. In addition to helping youprovide for your financial well-being inretirement, it also provides security for youand your family.

This booklet is a summary of what membership of the DBSection of the Scheme has to offer. It outlines the main benefitsand explains the basic principles of how it works. While theTrustee has tried to ensure the accuracy of this booklet, it is nota legal document. All your benefits are payable in accordancewith the Trust Deed and Rules, the legal document governingthe Scheme. In the event of any discrepancy between anyinformation provided to you and the Trust Deed and Rules, theTrust Deed and Rules will prevail.

If you wish to see a copy of the Trust Deed and Rules or haveany queries then please contact:

Pensions ManagerPrudential Staff Pension Scheme3 Sheldon SquarePaddingtonLondonW2 6PR

If you have any questions or you would like more informationabout any aspect of this booklet or the benefits payable underthe DB Section of the Scheme, please contact your dedicatedAdministration Team:

Email:

Call:

Write to:

01245 673515 (UK callers)(44) 1245 673515 (Overseas callers)

Prudential Staff Pension SchemePS Administration LimitedPriory PlaceNew London RoadChelmsford CM2 0PP

Finally, there are a number of defined terms used throughout this booklet and their meanings are given on pages 14 to 16.

Prudential Staff Pension Scheme – Member Booklet

HOW IT WORKSMembership of the DB Section of the Scheme is non-contributory and the Company pays the cost of providing yourbenefits. The Scheme assets are kept strictly separate from theCompany’s assets and are invested with the object of growingin value over the years. When members retire, die or leave theDB Section of the Scheme, the Scheme assets are used toprovide the appropriate benefits.

BENEFITSThe DB Section of the Scheme provides the following benefits:

Retirement

Benefits are provided on retirement (pages 4 to 5).

n A pension which accrues at 1/60th a year and is basedon your Final Pensionable Earnings and PensionableService;

n An optional lump sum (paid tax-free under currentlegislation).

Death

Benefits may be provided whether you die before or afterretirement (pages 6 and 7).

n A lump sum death benefit to one or more of yourBeneficiaries which can include your Spouse, Civil Partner/same sex spouse and children;

n A pension for your Spouse, Civil Partner/same sexspouse or Dependant(s);

n A pension for your Eligible Child(ren) (up to a maximum of 3).

Leaving

Benefits are provided if you leave the Company beforeretirement (pages 8 to 9). The benefits you may receivedepends on how long you have been a member of the DBSection of the Scheme but may include:

n A deferred pension;

n A transfer value.

3

The DB Section of the Scheme at a glanceANNUAL ALLOWANCEThis is the limit on the amount of pension savings that you canbuild up that may qualify for tax relief in any tax year. Theperiod over which this is measured for the Annual Allowance isknown as the Pension Input Period (PIP). For the DB Section ofthe Scheme, the PIP is the same as the tax year (i.e it runs from6 April to 5 April).

From 2016/17 the Annual Allowance will be £40,000. You cancarry forward unused allowance from up to three previousyears.

Please note that if you are a high earner (i.e. broadly the totalvalue of your total taxable income plus any pension savings youmake exceeds £150,000) or you have chosen to take benefitsfrom a registered pension scheme as a taxed lump sum or youtake income drawdown or a short-term annuity (or an annuitycapable of reducing), your Annual Allowance may be reduced. Please refer to the Scheme websitewww.prudentialstaffpensionscheme.co.uk or Appendix 1 ofthis booklet for more information.

LIFETIME ALLOWANCEThe Lifetime Allowance is a limit on the value of all yourpension savings you build up during your working life from theScheme and any other registered pension scheme. The limit iscurrently set at £1 million for the 2016/17 tax year.

You may be subject to a tax charge if the value of all yourpension benefits (across all arrangements you belong to)exceed the Lifetime Allowance. Please refer to the Schemewebsite www.prudentialstaffpensionscheme.co.uk.

Further information on the Annual Allowance and LifetimeAllowance can also be found at www.hmrc.gov.uk andwww.pensionsadvisoryservice.org.uk.

ELIGIBILITYYou will have been informed if you are a member of the DBSection of the Scheme. Membership of the DB Section of theScheme was closed to new entrants on and from 1 August 2003.

PAYING FOR THE DB SECTION OF THE SCHEMEn Membership of the DB Section of the Scheme is non-contributory. The Company is responsible for paying thewhole amount required to provide the benefits promised bythe DB Section of the Scheme and its administration costs.

n Although you do not need to contribute to the DB Sectionof the Scheme, you can choose to increase the benefits youwill receive by paying Additional Voluntary Contributions(AVCs). See page 9 for further details.

n There is currently no charge by the Scheme for exercisingany of your benefits if you leave the DB Section of theScheme before your Normal Retirement Date for example, ifyou take flexible retirement or transfer your benefits toanother arrangement.

Membership of the DB Section of the Scheme is non-contributory and theCompany pays the cost of providing your benefits. The Scheme assets are keptstrictly separate from the Company’s assets and are invested with the object ofgrowing in value over the years.

“”

LIMITS TO HOW MUCH YOU CAN SAVEThere are limits on the amount of pension savings you canmake. These limits cover both how much you can save eachyear (the Annual Allowance) and how much you can save intotal (the Lifetime Allowance).

Your benefits at Normal Retirement DateThe DB Section of the Scheme provides you with a pension and the option of a tax-free lump sum based on anaccrual rate of 1/60ths, your Final Pensionable Earnings and Pensionable Service at your Normal RetirementDate, normally your 60th Birthday. You will be entitled to receive your Scheme pension from your NormalRetirement Date and the pension will be paid monthly for the rest of your life.

Prudential Staff Pension Scheme – Member Booklet

4

The formula used to work out your Scheme pension is:

Complete months of Pensionable Service count as a proportionof a year.

Example:

The example below shows the pension payable to a memberretiring at Normal Retirement Date with Final PensionableEarnings of £20,000 and Pensionable Service of 15 years.

15/60 x £20,000 = £5,000 a year

If you joined the DB Section of the Scheme before April 1986please contact your dedicated Administration Team for detailsof how your pension is calculated.

Benefits provided by the DB Section of the Scheme are subjectto HM Revenue & Customs limits.

GUARANTEED MINIMUM PENSION (GMP)From 6 April 1978 until 5 April 2016 (inclusive), the DB Sectionof the Scheme was contracted out of the State Second PensionScheme (S2P), formally known as the State Earnings RelatedPension Scheme (SERPS). If you were an active member of theDB Section of Scheme during this period you will have built upa Guaranteed Minimum Pension (GMP) for the period youwere contracted out of the S2P before 6 April 1997 which willbe included in the pension detailed above. The value will beroughly equal to the pension you would have received if youhad stayed in the S2P. Please refer to the Scheme websitewww.prudentialstaffpensionscheme.co.uk or the definitionssection at the back of this booklet for further information onGMPs.

PART-TIME SERVICESpecial rules apply if you have part-time Service while aScheme member. Further details and an example calculationare provided on page 12 but, in general, the formula above isused to calculate your benefits, with your actual FinalPensionable Earnings increased to your full-time equivalent andyour Pensionable Service decreased to take into account yourreduced hours worked.

PENSION INCREASESOnce your pension is in payment it will be increased each yearas follows:

n Benefits earned for Pensionable Service on or after 6 April 2005 - increased in line with the rise in theConsumer Prices Index (CPI) for the year in question, up toa maximum of 2.5%. Increases normally take effect from

1 April each year and are based on the CPI increasemeasured as at the previous 30 September. In addition theCompany may choose to award discretionary increases.

n Benefits earned for Pensionable Service between 6 April 1997 and 5 April 2005 - increased by the rise inthe CPI for the year in question, up to a maximum of 5%.Increases normally take effect from 1 April each year and arebased on the CPI increase measured as at the previous 30 September. In addition the Company may choose toaward discretionary increases.

n Benefits earned for Pensionable Service before 6 April 1997 - will only attract increases on the GMP partof your pension. Your GMP earned prior to 6 April 1988 mayreceive increases from the State if you reached StatePension Age before 6 April 2016 (in which case these will bepaid with your State Pension). The GMP element earnedfrom 6 April 1988, which are paid by the Scheme, will beincreased by CPI up to a maximum of 3% per annum. Anypension in excess of the GMP may be increased at theCompany’s discretion.

PAYMENT OF YOUR PENSIONYour pension from the DB Section of the Scheme will be paidmonthly, in advance, on the first working day of each month.The first installment will be paid directly into your chosen bankaccount and may be more than one month’s pension.

Remember, pensions are treated as earned income, and are taxedin the same way as your current earnings under the PAYE system.

YOUR TAX-FREE LUMP SUMYou may exchange (or “commute”) up to 25% of the value ofyour benefits for a one-off lump sum. Under current legislation,the lump sum is normally paid tax-free.

Taking a tax-free lump sum will lead to a reduction in yourannual pension calculated by applying a rate specified by theScheme Actuary. The actual amount of cash you can receive foreach £1 of pension given up will depend on the rates in force atthe time.

Your tax-free lump sum may be restricted to ensure the pensionyou receive is not less than any GMP you have built up withinthe DB Section of the Scheme.

EXTRA PENSION FOR DEPENDANTSUnder the Scheme’s Trust Deed and Rules your Spouse or CivilPartner/same sex spouse is automatically entitled to a pensionon your death. Before you retire you may also choose to ask theTrustee to give up part of your pension to provide additionalbenefits (payable on your death) for your Spouse, CivilPartner/same sex spouse or a Dependant(s).

1/60 x Final Pensionable Earnings xPensionable Service

5

FLEXIBLE RETIREMENTThe Company is aware that situations and needs change andwants to support all employees. Therefore you no longer needto stop working before taking your Scheme pension under theflexible retirement option. Certain conditions apply, namely:

n You are aged at least 55;

n You have completed at least 2 years' Qualifying Service;

n You have agreement from the Company;

n You sign a new contract of employment which may notinclude any special terms that previously applied.

You have the same options available to you under flexibleretirement as you do if you were retiring at your NormalRetirement Date.

You may continue to build up pension benefits after takingflexible retirement but these will be as a member of the DefinedContribution (DC) Section of the Scheme. The basis upon whichfuture pension benefits are earned differs greatly between theDB and DC Sections of the Scheme. In the DC Section of theScheme the Company will pay 6% of Pensionable Pay known asEmployer Credits. These are held in a Personal Account on yourbehalf and invested to purchase units in your chosen fund(s)and the final value of these units will be used to providebenefits. Membership of the DC Section of the Scheme is non-contributory but you may make personal contributions. If youdecide to make personal contributions then the Company willpay Matching Employer Credits up to a further 6% ofPensionable Pay.

In the event of your death in Service you will be treated as havingdied after retirement (see page 7). In addition, a lump sum may bepayable from the DC Section of the Scheme.

For more information about what benefits will be payable onyour death if you become an active member of the DC Sectionof the Scheme, please refer to the Member Booklet for the DCSection of the Scheme which is available on the websitewww.prudentialstaffps.co.uk.

For more information about flexible retirement please contactyour dedicated Administration Team. It is also recommendedthat you seek independent financial advice if you need help onmaking this very important decision. If you do not have afinancial adviser details of those near to you can be found atwww.unbiased.co.uk.

LATE RETIREMENTIf you stay in Service with the Company after your NormalRetirement Date you can continue to build up pension benefitsuntil you complete 40 years' Pensionable Service. If you continueworking after completing 40 years' Pensionable Service, yourbenefits are increased by a factor decided by the Trustee ascalculated by the Scheme Actuary to make up for their latepayment. Should you die while employed after your NormalRetirement Date, benefits will be paid to your Spouse, CivilPartner/same sex spouse, Dependant(s) or children as describedfor death in Eligible Service but by reference only to completedPensionable Service.

THE STATE SPREADING OPTIONIf you take your pension from the Scheme before reaching yourState Pension Age, your retirement income will not include anyBasic State Pension. This is because the Basic State Pension isonly payable from State Pension Age.

However in certain circumstances the DB Section of theScheme gives you the option of electing to receive totalretirement income which is broadly the same both before andafter State Pension Age. This is called the “State SpreadingOption” and works as follows:

n You surrender, for the remainder of your lifetime, part ofyour DB Section pension in exchange for a temporaryincrease from your date of retirement until you reach StatePension Age.

n At State Pension Age, this temporary increase will stop andyour Basic State Pension will start to be paid. Details of thisoption will be provided shortly before retirement or onrequest from your dedicated Administration Team.

EARLY RETIREMENT FROM SERVICE – ON REQUESTYou may normally retire before your Normal Retirement Date ifyou meet all of the following conditions:

n You are age 55 or more;

n You have completed at least 2 years' Qualifying Service;

n The Company gives its approval.

Your pension will be reduced by factors decided by the Trusteeas calculated by the Scheme Actuary to take account of the factyou are being paid early and for a longer period of time.

If you have Pensionable Service between 6 April1978 and5 April 1997 the pension you receive from the DB Section ofthe Scheme must be at least equal to your GMP. If your earlyretirement pension is not at least equal to your GMP at GMPPension Age your early retirement options may need tobe restricted.

EARLY RETIREMENT THROUGH ILL-HEALTHIf you have to leave Service with the Company at any age dueto ill-health, you may be granted an immediate early retirementpension. Two categories of ill-health pension are available – thelevel which applies will depend on the view of the Company’smedical adviser as to the extent of your ill-health.

Total Incapacity Pension (meaning you cannot undertakeany paid employment)

The calculation of the pension under this category will be basedon your potential Pensionable Service to your Normal RetirementDate and your Final Pensionable Earnings at the date you retire.

Serious Incapacity Pension (meaning you cannotundertake your current job or similar)

The calculation of the pension under this category will be basedon your completed Pensionable Service at the time of retirement.

Your Service must have stopped for a Serious IncapacityPension to be payable, though the amount payable will not bereduced to take account of early payment.

If you are in receipt of a pension due to ill-health, the Trusteemay review and (if appropriate to do so) reduce, increase orsuspend that pension.

Prudential Staff Pension Scheme – Member Booklet

6

Death before retirementIf you die in Eligible Service while earning pension benefits under the DB Section of theScheme the following benefits will be payable.

LUMP SUMA lump sum equal to 4 times your Final Pensionable Earnings at thedate of your death, together with a refund of the value of any AVCsyou may have paid.

SPOUSE'S/CIVIL PARTNER/SAME SEXSPOUSE'S PENSIONYour Spouse or Civil Partner/same sex spouse will receive a pension,payable for life, equal to 54% of the pension you would havereceived at your Normal Retirement Date, but based on your FinalPensionable Earnings at the date of your death. Please note, thepension your Civil Partner/same sex spouse will receive will onlyrelate to your Pensionable Service on or after 5 December 2005. Inthe event of the death of your Spouse or Civil Partner/same sexspouse, the pension will continue to be paid in respect of any EligibleChild(ren) (up to a maximum of 3).

If you have Pensionable Service between 6 April 1978 and 5 April 1997 your Spouse or Civil Partner/same sex spouse’spension may include a Spouse GMP. For more information pleaserefer to the Glossary.

DEPENDANT’S PENSIONIf you die without leaving a Spouse or Civil Partner/same sexspouse, a pension will be payable to one or more of yourDependant(s), in such proportions as the Trustee decides. Theamount of pension will be equal to that which would have been paidto a Spouse or Civil Partner/same sex spouse. In addition, the lumpsum payable can be used to provide any Dependant's annuity.

If the Dependant’s pension is paid to an Eligible Child whosubsequently dies, the Dependant’s pension will continue to be paidto other Eligible Child(ren). However if the Dependant’s pension ispaid to a person who is not an Eligible Child who subsequently dies,the Dependant’s pension will stop.

ELIGIBLE CHILD'S PENSIONIn addition, if you die leaving an Eligible Child(ren), a pension willbe paid in respect of each Eligible Child (up to a maximum of 3).The amount payable is 1/6th of the pension you would havereceived at your Normal Retirement Date but based on your FinalPensionable Earnings at the date of your death. The pension willbe payable in respect of your Eligible Child(ren) while they areunder age 18. If they remain in full-time education or vocationaltraining, the pension may continue at the Trustee’s discretion butnot normally beyond the age of 23.

PAYMENTPensions payable on your death will be payable from the dayafter your death. The first installment will be paid in proportionto one month’s pension depending on the date of your death.After this it will be paid monthly in advance on the first workingday of the month.

OPTING OUTIf you have opted out of Pensionable Service and die while inEligible Service then only the lump sum of 4 times your FinalPensionable Earnings will become payable. Any Spouse, CivilPartner/same sex spouse or Eligible Child(ren) pensionspayable will be the same as a death of a member with adeferred benefit (see page 8).

If you do decide to opt out of the DB Section of the Scheme,then under Automatic Enrolment legislation the Company willbe obliged to re-enrol you into the DC Section of the Schemeapproximately every 3 years or may do so earlier should yourcircumstances change. You do have the right to opt out of theDC Section of the Scheme as part of the Automatic Enrolmentprocess.

7

Death after retirementIf you die after retirement, the followingbenefits will be payable.

5 YEAR GUARANTEE – LUMP SUMThe DB Section of the Scheme guarantees that your pension ispaid for a minimum of 5 years. In the event of your death within5 years of your retirement, a lump sum equal to the unpaidbalance of 5 years’ of your pension will be payable to one ormore of your Beneficiaries. The lump sum will normally be paidfree of tax. This amount does not take into account any futurepension increases.

Note: If you had taken the State Spreading Option (see page 5)when you retired, this 5 year period will be reduced.

SPOUSE'S/CIVIL PARTNER/SAME SEXSPOUSE'S PENSIONYour Spouse or Civil Partner/same sex spouse will receive apension equal to 50% of the full pension you were entitled to atretirement (i.e. before exchanging any pension for a tax-freelump sum and excluding any pension from AVC funds and theState Spreading Option if elected but including any increasesgranted since that time). Please note, the pension your CivilPartner/same sex spouse will receive will only relate to yourPensionable Service on or after 5 December 2005.

In the event of your Spouse’s or Civil Partner/same sexspouse's death, the pension will continue to be paid in respectof any Eligible Child(ren) (up to a maximum of 3).

If you have Pensionable Service between 6 April 1978 and 5 April 1997 your Spouse or Civil Partner/same sex spouse’spension may include a Spouse GMP. For more information pleaserefer to the Glossary.

DEPENDANT’S PENSIONIf you die without leaving a Spouse or Civil Partner/same sexspouse, a pension may be payable to one or more of yourDependant(s), in such proportions as the Trustee decides. Theamount of the pension will be equal to that which would havebeen paid to a Spouse or Civil Partner/same sex spouse.

If the Dependant’s pension is paid to an Eligible Child whosubsequently dies, the Dependant’s pension will continue to bepaid to other Eligible Child(ren). However if the Dependant’spension is paid to a person who is not an Eligible Child whosubsequently dies, the Dependant’s pension will stop.

ELIGIBLE CHILD’S PENSIONIn addition, if you die leaving Eligible Child(ren) (up to amaximum of 3) they will receive a pension from the DB Sectionof the Scheme. The amount payable is equal to 1/6th of thepension at the date of your death, including any increases sinceyour retirement and ignoring any options you made atretirement. The pension will be payable in respect of yourEligible Child(ren) while they are under age 18. If they remainin full-time education or vocational training, the pension maycontinue at the Trustee’s discretion but not normally beyondthe age of 23.

PAYMENTPensions payable on your death will be payable from the dayafter your death. The first installment will be in proportion toone month’s pension depending on the date of your death.After this it will be paid monthly in advance on the first workingday of the month.

The DB Section of theScheme guarantees that yourpension is paid for a minimumof 5 years.

“”

Prudential Staff Pension Scheme – Member Booklet

8

Example:

The example shows the pension payable to a member whojoined at the age of 22 and leaves after completing 10 years’Pensionable Service with Final Pensionable Earnings of £15,000.

10/60 x £15,000 = £2,500 a year

Note: You will receive additional credit for any transfer value youhave been allowed to transfer into the DB Section of the Schemefrom a previous arrangement.

Your deferred pension will be revalued until you take it, toreduce the impact of inflation.

PAYMENT OF YOUR DEFERRED PENSIONYour deferred pension will normally become payable at yourNormal Retirement Date. However, with the Trustee’s consent,it may be paid early:

n From age 55; or

n On the grounds of ill-health subject to appropriate medicalevidence.

You will have the same options of taking part of your pension asa tax-free lump sum and providing extra pension for aDependant(s) (see page 4).

Once payment starts, your pension will be increased in thesame way as described in the section ‘Your benefits at NormalRetirement Date’ (see page 4).

If you wish to defer the commencement of your pension to alater date, you will need the permission of the Trustee.

DEATH BEFORE RETIREMENTIf you die before your deferred pension becomes payable, thefollowing benefits will be payable.

Spouse's/Civil Partner/same sex spouse’s pension

Your Spouse or Civil Partner/same sex spouse will receive apension of 50% of your deferred pension, including anyincreases granted from your date of leaving up to the date ofyour death. In the event of your Spouse's or Civil Partner/samesex spouse's death, the pension will continue to be paid inrespect of any Eligible Child(ren) (up to a maximum of 3).

Dependant’s pension

If you die without leaving a Spouse or Civil Partner/same sexspouse, a pension may be payable to one or more of yourDependant(s) in such proportions as the Trustee decides. Theamount of the pension will be equal to that which would havebeen paid to a Spouse or Civil Partner/same sex spouse.

If the Dependant’s pension is paid to an Eligible Child whosubsequently dies, the Dependant’s pension will continue to bepaid to other Eligible Child(ren). However if the Dependant’s

pension is paid to a person who is not an Eligible Child who subsequently dies, the Dependant’s pension will stop.

Eligible Child’s pension

In addition, if you die leaving Eligible Child(ren) (up to a maximum of 3), pensions will be paid to each Eligible Child equal to 1/6th of your pension. The pension will be payable to your Eligible Child(ren) while they are under age 18. If they remain in full time education or vocational training, the pension may continue at the Trustee’s discretion but not normally beyond the age of 23.

Lump sum

A lump sum equal to 5 times your deferred pension had it come into payment on the date of your death (less any actuarial discounting) together with any AVCs you have paid (plus any bonuses) will also be payable to your estate.

Payment

Any pensions payable on your death will be payable from the day after your death. The first installment will be paid in proportion to one month’s pension depending on the date of your death. After this it will be paid monthly in advance on the first working day of the month.

DEATH AFTER RETIREMENTIf you die after you have retired, benefits will be paid in the same way as described on page 7.

EXPRESSION OF WISH FORMThe Trustee decides who should receive any benefits payable on your death, but consideration will be given to anyone that you have nominated as a Beneficiary in an Expression of Wish Form. It is very important that you complete and maintain an Expression of Wish Form to keep the Trustee informed of any changes in your circumstances, for example if you marry, divorce or have children. You can download an Expression of Wish Form from the website www.prudentialstaffps.co.uk or by contacting your dedicated Administration Team on 01245 673515 or [email protected].

TRANSFER OF BENEFITSProvided that the receiving arrangement is a registered pension scheme or a Recognised Overseas Pension Scheme (ROPS) if you are transferring overseas, then you do generally have the option to take a transfer value from the DB Section of the Scheme before your Normal Retirement Date. You can also transfer your benefits into the DC Section of the Scheme. If you paid AVCs under the DB Section of the Scheme then these would need to be transferred as well.

Leaving the DB Section of the SchemeIf you leave, or opt out of, the DB Section of the Scheme without transferring your benefits toanother registered pension scheme, your pension will remain in the DB Section of theScheme until you reach your Normal Retirement Date and you will be treated as a deferredmember. Your pension is calculated in the same way as at retirement but using yourPensionable Service and Final Pensionable Earnings at your date of leaving.

9

The transfer value will take the form of a capital sum, known asthe cash equivalent transfer value, representing the value of thepension you earned under the DB Section of the Scheme up tothe date you left. It includes the value of any AVCs you havepaid under the DB Section of the Scheme.

You may ask for an estimate of the cash equivalent transfer valueavailable to you. Normally within 3 months of your request, theTrustee will give you a written statement of entitlement. This willshow your cash equivalent transfer value which is guaranteedfor 3 months from the date on which it has been calculated (theguarantee date). The statement will be given to you normallywithin 10 working days of the guarantee date.

If you want to transfer your benefits from the DB Section of theScheme to a defined contribution arrangement to access thenew pension flexibilities (such as a UFPLS) and your totalbenefits in the DB Section of the Scheme exceed £30,000, youmust obtain independent financial advice before being allowedto do so (although the Trustee always recommends that youseek independent financial advice when making a decisionabout your retirement).

If you want to transfer the cash equivalent transfer valuequoted to another registered scheme or buy-out policy, youmust apply in writing to the Trustee within 3 months from theguarantee date shown on the statement of entitlement.

The Trustee is not legally required to provide you with anotherstatement within 12 months of the date of the last request.

If the estimate of the cash equivalent transfer value is neededbecause of a divorce settlement, you should tell the Trustee thiswhen asking for the estimate as the Trustee may need furtherinformation from you. Please note there is no 3 monthsguarantee attached to these quotations.

Calculation of the cash equivalent transfer value

The cash equivalent transfer value is the amount the Trusteedetermines, having taken advice from the Scheme Actuary, tobe sufficient at the date of calculation to provide your deferredbenefits at your Normal Retirement Date, allowing for anyguaranteed and statutory increases to be applied between thedate you leave Pensionable Service and your NormalRetirement Date. The Trustee has a policy of including anallowance for any discretionary increases made in thecalculation of cash equivalent transfer values. Further details will be provided by your dedicated Administration Team upon request.

OPTING OUT WHILE REMAINING EMPLOYED BYTHE COMPANYIf you wish to opt out of the DB Section of the Scheme thenyou will need to contact your dedicated Administration Team oryour local HR Department.

You will still be covered for a lump sum equal to 4 times yourFinal Pensionable Earnings at the date of your death if you diewhile employed by the Company, plus any contributions youhave paid. This is payable tax-free under current legislation upto the Lifetime Allowance.

n You will not generally be permitted to rejoin the DB Sectionof the Scheme once you have opted out. You do have theoption of joining the DC Section of the Scheme. UnderAutomatic Enrolment legislation the Company will be obligedto enrol you into the DC Section of the Scheme once youhave opted out of the DB Section of the Scheme (and to

re-enrol you into the DC Section of the Schemeapproximately every 3 years or earlier should yourcircumstances change).

You do have the right to opt out of the DC Section of theScheme as part of the Automatic Enrolment process.

n If you are considering opting out of the DB Section of theScheme, you are advised to seek independent financialadvice. If you do not have a financial adviser details of thosenear to you can be found at www.unbiased.co.uk.

Additional VoluntaryContributions (AVCs)The DB Section of the Scheme is non-contributory andthe Company pays the cost of providing your benefits.However, you can choose to pay AVCs to increase yourfuture benefits.

AVCs are a flexible way of making your own contributionsnow to increase your benefits in the future. You can payregular monthly contributions or a one-off lump sum. What'smore, under current legislation, your AVCs are tax-free, asthey are deducted from your salary before tax is calculated.So, if you pay tax at 20%, a contribution of £100 will only costyou £80. The payroll system automatically provides this taxrelief. You can normally pay AVCs tax efficiently of up to100% of your salary up to the Annual Allowance.

If you participate in Pensions Plus, your Salary is reducedby the amount of your AVCs meaning that the AVCs arenot subject to tax or National Insurance.

Please note if you joined the DB Section of the Schemeon or after 1 June 1989, you can only pay up to 15% ofyour Salary to the in-house AVC arrangement (which isactually integrated within the DB Section of the Schemeand is not a separate commercial product). Any amountsabove this limit (up to 100% of salary) must instead bemade into the commercial arrangement with a range offund options selected by the Trustee. For moreinformation on AVCs please refer to “A guide to theDefined Benefit Section's Additional VoluntaryContributions arrangements” which can be found on theScheme website www.prudentialstaffps.co.uk.

Note:

If you wish to provide additional pension for your Spouse,Civil Partner/same sex spouse or a Dependant(s), youmay choose to give up part of your AVCs, instead of yourScheme pension, when you retire.

You can start, increase, reduce or stop your AVCs at anytime by downloading and completing the relevant formfrom the website or by contacting your dedicatedAdministration Team.

Prudential Staff Pension Scheme – Member Booklet

10

Temporary absenceMost absences from work are for arelatively short time and yourmembership of the DB Section of the Scheme in these circumstancesremains unchanged.

If you are away for a longer period andyou stop receiving contractual pay orstatutory sick pay, your membership may be continued with Company andTrustee consent.

MATERNITY LEAVE AND MATERNITYABSENCEIf you are away from work to have a baby, yourmembership and benefits under the DB Section of theScheme will continue for all your maternity leave in linewith the Company’s Maternity Policy.

Your membership, Pensionable Service and benefits willcontinue on the same basis which would have applied toyou had you been working normally. The Company willcontinue to make its normal contributions on your behalf.

Your benefits will continue to build up based on the full salaryyou would have received had you not been on maternityleave. If you do not return to work, your Pensionable Servicewill generally stop 18 weeks after the later of the date yourmaternity leave or statutory maternity pay ceases.

For further information please contact your local HR teamor your dedicated Administration Team.

PATERNITY LEAVEYour membership, Pensionable Service and benefits willcontinue as if you were working normally.

ADOPTION/PARENTAL/OTHER LEAVEThere may be circumstances in which you need to take timeoff work for other reasons, for example adoption leave,parental leave or for an emergency involving your family.Please contact your HR team for further information.

Looking after yourinterestsTRUSTEEPrudential Staff Pensions Limited, a trust corporation, is theTrustee of the Scheme and is responsible for ensuring that theScheme is administered in accordance with the Trust Deed and Rules.

The Trustee holds, manages and invests assets for the benefitof members and their Beneficiaries. Trust structures are usedfor pension arrangements such as the Scheme and this meansits assets are held separately from those of the Company.

The Trustee is appointed by the Company and its TrusteeDirectors are selected under the agreed arrangements and inline with prevailing legislation.

Information on the Trustee is provided each year in our in-house publication Pension Overview copies of which are storedin the Documents section of the websitewww.prudentialstaffps.co.uk.

KEEPING YOU IN THE PICTUREKnowing where you stand with your pension is very important.As a member of the DB Section of the Scheme, you will be sentinformation designed to keep you informed about your benefitsand the DB Section of the Scheme in general. In addition to thisbooklet and the information made available on the Scheme’swebsite www.prudentialstaffps.co.uk, all active members willalso be able to view online a personalised Annual BenefitStatement of their benefits each year.

Copies of the latest formal Scheme Report and Accounts andother Scheme documentation are available on the website. Acopy of the Scheme Report and Accounts can be providedupon request from your dedicated Administration Team.

Your benefits will continue tobuild up based on the fullsalary you would havereceived had you not beenon maternity leave.

“”

11

STAYING IN TOUCHKeeping in touch while you are with the Company is one thing, but it’s easy to lose touch if you move on.

If you leave the Company with a deferred pension, the Trustee will keep a record of your last known address so that you can be contacted about your benefits or any issues affecting the DB Section of the Scheme. To help the Trustee do this, it is important that you keep the Trustee informed of any change of address or your circumstances once you have left. If for any reason you lose track of the details of your pension under the DB Section of the Scheme, you can trace it through The Pension Tracing Service, which maintains a register of pension schemes.

If you want to contact The Pension Tracing Service the address is:

The Pension Service 9, Mail Handling Site A, Wolverhampton, WV98 1LU

Tel: 0345 6002 537Website: www.gov.uk/find-pension-contact-details

HELP AT HANDThe Trustee will do all that it can to ensure that the DB Section of the Scheme is administered to the highest standard, but we appreciate that there may be times when you are unhappy about a certain situation or you have a concern that you need to raise.

Most queries and problems stem from a misunderstanding of information and normally can be quickly and informally sorted out without the need to use any formal procedures. You should first of all refer any query to your dedicated Administration Team on 01245 673515.

If you are still unhappy about the matter, you may then wish to consider making a formal complaint through the Internal Dispute Resolution Procedure.

INTERNAL DISPUTE RESOLUTION PROCEDUREIf you have not been able to resolve any complaint about the DB Section of the Scheme informally, there is a 2-stage formal procedure you may use. Full details can be obtained from the Pensions Manager at the address shown below.

Stage 1 - You should put your case in writing to the Pensions Manager, Prudential Staff Pension Scheme, 3 Sheldon Square, Paddington, London, W2 6PR – who will fully consider your complaint and will normally give you a decision within 2 months of receipt of your complaint.

Stage 2 - If you are not satisfied with the Stage 1 decision, you can appeal to the Trustee to consider your complaint. You will normally receive a decision from the Trustee within 2 months of receipt of your complaint.

Special application forms are available to make a complaint or appeal. If you wish, you may use a representative to act on your behalf.

The Internal Dispute Resolution Procedure applies to matters concerning the DB Section of the Scheme that affect members and others who may have an interest under the DB Section of the Scheme. It does not apply to disputes between employees and the Company, nor does it apply to disputes where Court proceedings have started or that are being investigated by the Pensions Ombudsman.

OUTSIDE HELPIn addition to the Scheme’s own arrangements, the followingexternal bodies may also be able to provide assistance:

The Pension Service

The Pension Service website provides information on Statebenefits.

Tel: 0800 731 7898Website: www.gov.uk/contact-pension-service

You can apply online at www.gov.uk/check-state-pension fora forecast of the benefits you could receive from the State, orcall 0800 731 7898, or +44 (0)191 218 7777 if calling fromoverseas, to go through the application by phone.

The Pensions Advisory Service (TPAS)

TPAS is an independent voluntary body that provides free helpand advice to members and other beneficiaries of occupationaland personal pension schemes. TPAS is available at any time toassist members and other beneficiaries with any pension querythey may have or any difficulty they have failed to resolve withthe trustees or administrators of a scheme. If you want tocontact TPAS the address is:

11 Belgrave Road, London, SW1V 1RB

Tel: 0300 123 1047Website: www.pensionsadvisoryservice.org.uk

The Pensions Ombudsman

The Pensions Ombudsman may investigate and decide uponany complaint or dispute of fact or law or complaints aboutmaladministration in relation to how an occupational pensionscheme is run. The Pensions Ombudsman may be contacted at: 11 Belgrave Road, London, SW1V 1RB

Tel: 020 7630 2200 Website: www.pensions-ombudsman.org.uk

Please note that the Pensions Ombudsman normally insists the matter is first dealt with through a scheme's own internaldispute resolution procedures and raised with TPAS.

The Pensions Regulator

The Pensions Regulator is a regulatory body which has a rangeof powers to help safeguard pension rights of pension schemesand is able to intervene where trustees, employers orprofessional advisers have failed in their duties. The PensionsRegulator may be contacted at:

Napier House, Trafalgar Place, Brighton, BN1 4DW

Tel: 0345 600 0707Website: www.thepensionsregulator.gov.uk

Prudential Staff Pension Scheme – Member Booklet

12

PART-TIME SERVICE Where part-time Service is involved, for the purpose ofcalculating your pension and tax-free lump sum, your part-timesalary is converted to its full-time equivalent and yourPensionable Service decreased to take into account yourreduced hours worked.

So, your Final Pensionable Earnings are increased to calculatethe earnings that would be paid if you worked full-time. Forexample: if you earn £12,000 for working half of the ‘normal’full time hours, you would earn twice that (ie. £24,000) if youwere full-time. The precise formula used is:

Final Pensionable Earnings for hours worked x(full-time hours/your part-time hours)

Your Pensionable Service is decreased to calculate its full-timeequivalent. Again, the precise formula is:

Pensionable Service x (your part-time hours/full-time hours)

Once these adjustments have been made, your pension iscalculated in the normal way.

If you change your hours, each period of Service is converted toits full-time equivalent, as are your Final Pensionable Earnings.

MARITAL STATUSIt helps the Trustee pay benefits promptly if it is kept informedof any change in your marital status or other familycircumstances.

DIVORCE OR DISSOLUTION OF A CIVILPARTNERSHIPThe Trustee must comply with any order made by a Courtfollowing a divorce or dissolution of a Civil Partnership.

GIVING UP YOUR BENEFITSYou are not generally allowed to give up, transfer to someoneelse or cash in your benefits accrued under the DB Section ofthe Scheme except as described in this booklet.

The DB Section of the Scheme isarranged so that the Trustee hasdiscretion to decide who receivesthe lump sum payments made onyour death.

“”

Tax statusThe Scheme is a registered scheme for HMRevenue & Customs’ purposes. As aregistered scheme, it enjoys a number oftax advantages. Contributions and benefitsfrom the DB Section of the Scheme will besubject to the Annual Allowance andLifetime Allowance.

INCOME TAXYour pension will be subject to PAYE income tax.

INHERITANCE TAXUnder present legislation, any lump sum benefits paid under the DB Section of the Scheme if you die in Eligible Service or in retirement will not normally be subject to inheritance tax. The DB Section of the Scheme is arranged so that the Trustee has discretion to decide who receives the lump sum payments made on your death.

As noted above, whilst the Trustee decides who should receive any benefits payable on your death, consideration will be given to anyone that you have nominated as a Beneficiary in an Expression of Wish Form. It is very important that you complete and maintain an Expression of Wish Form to keep the Trustee informed of any changes in your circumstances, for example if you marry, divorce or have children. You can download an Expression of Wish Form from the websitewww.prudentialstaffps.co.uk or by contacting your dedicated Administration Team on 01245 673515 [email protected].

You should note that, if you leave the DB Section of the Scheme and die before your deferred pension becomes payable, any lump sum will be paid to your estate and, as such, may be subject to inheritance tax.

Changes in personal circumstances

13

The State and youThe State Pension is a regular income you may receive from the Government when you reachState Pension Age.

From April 2016 the Government has introduced a new single-tier flat-rate pension. As a member of the DB Section of theScheme prior to April 2016 you were contracted out of theState Earnings Related Pension Scheme (SERPS), for serviceprior to April 2002 and the Second State Pension (S2P) forservice after April 2002 but before April 2016. Therefore youmay not receive the full level of the new State Pension. Furtherinformation on the new State Pension can be found atwww.gov.uk/new-state-pension.

CESSATION OF CONTRACTING OUTContracting out for all defined benefit occupational pensionschemes, including the DB Section of the Scheme, ceased witheffect from 6 April 2016. The DB Section of the Scheme wascontracted out for the period 6 April 1978 to 5 April 2016(inclusive).

As a member of the DB Section ofthe Scheme prior to April 2016 youwere contracted out. Therefore youmay not receive the full level of thenew State Pension.

“”

Prudential Staff Pension Scheme – Member Booklet

14

This booklet uses certain words that may require further explanation. The definitions below should help you understand any technical termsthat may not be familiar to you.

Annual Allowance This is the limit on the amount of pension savings that you can build up that may qualify for tax relief in any tax year. The period over which this is measured for the Annual Allowance is known as the Pension Input Period (PIP). For the DB Section of the Scheme, the PIP is the same as the tax year (i.e. it runs from 6 April to 5 April).

From 2016/17 the Annual Allowance will be £40,000, but you may carry forward unused allowances from up to three previous years.

Please note, if you are a high earner (i.e. broadly the total value of your total taxable income plus any pension savings you make exceeds £150,000 or you have chosen to take benefits from a registered pension scheme as a taxed lump sum or you take income drawdown or a short term annuity (or an annuity capable of reducing) your Annual Allowance may be reduced. Please refer to Appendix 1 or the Scheme website www.prudentialstaffpensionscheme.co.uk for more information.

Additional Voluntary These are any personal contributions that you choose to pay and are usually payable monthly although one-off paymentsContributions are allowed. Under current legislation, any AVCs you pay will attract tax relief, as they are deducted from your salary(AVCs) before tax is calculated. If, for example, you pay tax at 20%, an AVC of £100 will only cost you £80. Civil Partner This is the person you have entered into a registered civil partnership with under the Civil Partnership Act 2004.

Company Company means The Prudential Assurance Company Limited or any associated company/employer that offers you membership of the Scheme through your contract of employment.

Consumer Price The official index used by the Government as its measure of inflation. The Government previously used the Index (CPI) Retail Prices Index as its official index for measuring inflation.

DB Section This is the Defined Benefit (DB) Section of the Prudential Staff Pension Scheme (the Scheme).

DC Section This is the Defined Contribution (DC) Section of the Prudential Staff Pension Scheme (the Scheme).

Deferred Pension This refers to the benefits retained within the Scheme when you leave before your Normal Retirement Date. The value of those benefits will be revalued to try to reduce the impact of inflation. The deferred pension will normally become payable from your Normal Retirement Date but can be paid earlier or later in certain circumstances. You may choose to transfer all of your benefits under the DB Section of the Scheme to another registered pension scheme instead of taking a deferred pension from the Scheme. Your deferred pension is sometimes referred to as your preserved pension.

Dependant Your Spouse/Civil Partner/same sex spouse or any other person who, in the opinion of the Trustee, is financially dependant upon you at the date you take your pension or die.

Eligible Children In most cases, this means your own or adopted child under age 18 or later if still in full-time education/ vocational training and the Trustee so decides (though not normally beyond age 23).

Eligible Service In general, this means the permanent Service you complete with the Company.

In summary, for the purposes of the DB Section of the Scheme, this means the highest of:

1.Your basic salary earned in the 12 months immediately before leaving Service, ignoring any additions such asbonuses or overtime;

2.Your highest annual salary in any one tax year in the last 5 years before leaving Service; or

3. Your average annual salary over the best 3 consecutive tax years in the last 10 years before you leave Service.

The earliest tax year which will count in points 2 and 3 above is that commencing 6 April 2000.

If you participate in the Company’s Pension Plus arrangement, for these purposes, you are treated as if you do not participate in that arrangement.

There are occasions when your Final Pensionable Earnings may be calculated differently. If you have any questions about this definition, please contact your dedicated Administration Team in the first instance.

Flexible Retirement You no longer need to stop working for the Company before taking your pension benefits. Subject to certain conditions, you can choose to take your pension from the DB Section of the Scheme and continue working for the Company under the flexible retirement option.

Guaranteed If you were an active member of the DB Section of the Scheme between 6 April 1978 and 5 April 2016 Minimum Pension (inclusive), you will have accrued a GMP within the Scheme. This is the minimum pension the Scheme can pay to you as a result of you contracting out of either the State Earnings Related Pension Scheme (SERPS) or the Second State Pension (S2P).

n Contracting out – In return for you and the Company paying a reduced level of National Insurance contributions,you stopped building up your second tier State Pension entitlement. The Scheme committed to pay this amountto you as part of your overall Scheme entitlement.

Definitions

Final PensionableEarnings

15

n State Earnings Related Pension Scheme (SERPS) – From 6 April 1978 to 5 April 2002 this was the second tierof State Pension. In addition to your Basic State Pension the State would pay an additional pension based on yourearnings.

n Second State Pension (S2P) – In 2002 the Government replaced SERPS with S2P. The principles were broadly the same in that S2P was a second tier of State Pension provision.

With effect from 5 April 2016, the Government abolished the two-tier State Pension provision in favour of a single-tier flat-rate State Pension. Please see State Pension below for further information.

GMP Pension Age GMP Pension Age is currently 60 for women and 65 for men.

Lifetime Allowance The Lifetime Allowance is a limit on the value of all your pension savings you build up during your working life from the Scheme and any other registered pension scheme. This limit is currently set at £1 million for the 2016/17 tax year.

You may be subject to a tax charge if the value of all your pension benefits (across all arrangements you belong to) exceed the Lifetime Allowance. Further information on the Lifetime Allowance can be found on the Scheme website www.prudentialstaffpensionscheme.co.uk or visit www.pensionsadvisoryservice.org.uk and www.hmrc.gov.uk.

Normal Retirement The date at which you are expected to retire which for the DB Section of the Scheme is normally age 60. This Date is sometimes referred to as your Normal Pensionable Date.

Pensionable Pay For the purposes of the DC Section of the Scheme, this means your basic salary.

If you participate in the Company’s Pension Plus arrangement, for these purposes, you are treated as if you do not participate in that arrangement.

Pensions Plus The Company operates a salary exchange arrangement called Pensions Plus, for more information please see the document Your Guide to Pensions Plus available from your local HR team.

Pensionable Service In general, this means the permanent Service (in years and complete months) you complete with the Company as an active member of the DB Section of the Scheme.

Qualifying Service This is the period of time you are an active member of the DB Section of the Scheme.

Service This is the period of time you are an employee of the Company.

Spouse This is the person to whom you are legally married.

Spouse GMP 50% of the member’s GMP at date of death (if applicable).

State Pension This is the pension you may receive from the State when you reach your State Pension Age. The type of State Pension you receive will depend on when you reach State Pension Age.

Those reaching State Pension Age on or after 6 April 2016

The State Pension you receive will be a single-tier flat-rate pension. The full State Pension is currently £155.65per week (2016/17 tax year). You may receive more or less than the full amount depending on what NationalInsurance (NI) contributions you have paid. Normally you will have needed to pay NI contributions for at least10 qualifying years to receive any State Pension.

Further information can be found at www.gov.uk/new-state-pension.

Those who reached State Pension Age before 6 April 2016

The State Pension you receive will be made of 2 elements:

n The Basic State Pension – This element of the State Pension was paid to everyone who meet one or more of the following criteria:

n You were working and NI contributions were paid by you or on your behalf;

n You were a parent or carer and claiming certain benefits or credits;

n You got certain benefits, eg for unemployment or sickness;

n You were paying voluntary NI contributions.

You needed 30 years’ worth of contributions to get the full Basic State Pension. These were your ‘qualifying years’. If you had fewer than 30 years, your Basic State Pension would be less unless you topped this up by paying voluntary NI contributions.

n The Second State Pension (S2P) or State Earning Related Pension Scheme (SERPS) – This secondelement of the State Pension was based on your earnings. From 6 April 1978 to 5 April 2016, you could optout of S2P (or SERPS) by being a member of a contracted out pension scheme, such as the DB Section ofthe Scheme. You and your employer would pay a reduced rate of NI and an amount broadly equivalent tothe amount you would have received had you stayed in the S2P (or SERPS) would be paid to you by yourcontracted out pension scheme.

Prudential Staff Pension Scheme – Member Booklet

16

Small Print

Company means The Prudential Assurance Company Limited or any associated company/employer that offersyou membership of the Scheme through your contract of employment.

All benefits are payable in accordance with the Trust Deed and Rules, the legal document governing theScheme. In the event of any discrepancy between any information provided to you and the Trust Deed andRules, the Trust Deed and Rules will prevail.

Data protection

In order to administer the DB Section of the Scheme, it is necessary for information about you and yourDependants to be held and processed by the Trustee or other parties who act on behalf of the Trustee. TheTrustee, the Scheme Actuary and the actuarial advisers are each data controllers under the Data ProtectionAct 1998. This information is kept secure and only disclosed in limited circumstances, for example,information may be disclosed to companies within the Prudential Group, Trustee advisers and otherorganisations in connection with the operation of the DB Section of the Scheme. Information may also bedisclosed to any future potential employers and their advisers and, only if the Trustee, the Scheme Actuaryor the actuarial advisers are legally obliged to do so, to Government or regulatory organisations.

You will receive confirmation of your State Pension entitlement when you reach your State Pension Age.

Please visit www.gov.uk/browse/working/state-pension for further information on State Pension provision, including information on how to get a State Pension statement.

State Pension Age The age at which the Basic State Pension becomes payable.

For men born before 6 December 1953, the current State Pension Age is 65. For women born after 5 April 1950 but before 6 December 1953, the current State Pension Age will be between 60 and 65. From November 2018 the State Pension Age for both men and women will start to increase to eventually reach 68.

Trustee Prudential Staff Pensions Limited, a trust corporation, is the Trustee of the Scheme and is responsible for ensuring that the Scheme is administered in accordance with the Trust Deed and Rules. The Trustee holds, manages and invests assets for the benefit of members and their Beneficiaries. Trust structures are used for pension arrangements such as the Scheme and this means its assets are held separately from those of the Company.

Uncrystallised Funds A way of taking some or all of your money purchase pension savings (without designating funds as available for drawdownPension Lump Sum or buying an annuity) as a cash lump sum.(UFPLS)

17

Published by the Trustee of the Prudential Staff Pension Scheme, Laurence Pountney Hill, London EC4R 0HH.

Designed & produced by Concert Consulting UK Ltd 2016. CC/14-11-16 V8.3

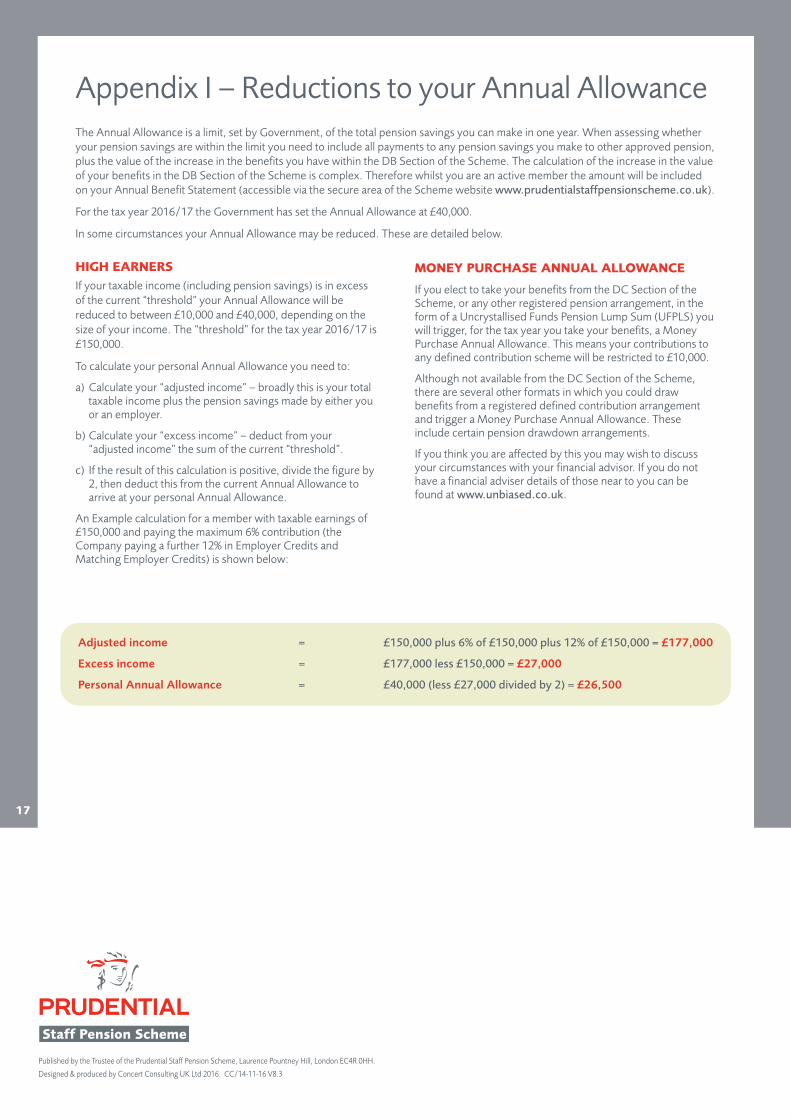

Appendix I – Reductions to your Annual AllowanceThe Annual Allowance is a limit, set by Government, of the total pension savings you can make in one year. When assessing whetheryour pension savings are within the limit you need to include all payments to any pension savings you make to other approved pension,plus the value of the increase in the benefits you have within the DB Section of the Scheme. The calculation of the increase in the valueof your benefits in the DB Section of the Scheme is complex. Therefore whilst you are an active member the amount will be includedon your Annual Benefit Statement (accessible via the secure area of the Scheme website www.prudentialstaffpensionscheme.co.uk).

For the tax year 2016/17 the Government has set the Annual Allowance at £40,000.

In some circumstances your Annual Allowance may be reduced. These are detailed below.

MONEY PURCHASE ANNUAL ALLOWANCE

If you elect to take your benefits from the DC Section of theScheme, or any other registered pension arrangement, in theform of a Uncrystallised Funds Pension Lump Sum (UFPLS) youwill trigger, for the tax year you take your benefits, a MoneyPurchase Annual Allowance. This means your contributions toany defined contribution scheme will be restricted to £10,000.

Although not available from the DC Section of the Scheme,there are several other formats in which you could drawbenefits from a registered defined contribution arrangementand trigger a Money Purchase Annual Allowance. Theseinclude certain pension drawdown arrangements.

If you think you are affected by this you may wish to discussyour circumstances with your financial advisor. If you do nothave a financial adviser details of those near to you can befound at www.unbiased.co.uk.

HIGH EARNERSIf your taxable income (including pension savings) is in excessof the current “threshold” your Annual Allowance will bereduced to between £10,000 and £40,000, depending on thesize of your income. The “threshold” for the tax year 2016/17 is£150,000.

To calculate your personal Annual Allowance you need to:

a) Calculate your “adjusted income” – broadly this is your totaltaxable income plus the pension savings made by either youor an employer.

b) Calculate your “excess income” – deduct from your“adjusted income” the sum of the current “threshold”.

c) If the result of this calculation is positive, divide the figure by 2, then deduct this from the current Annual Allowance to arrive at your personal Annual Allowance.

An Example calculation for a member with taxable earnings of£150,000 and paying the maximum 6% contribution (theCompany paying a further 12% in Employer Credits andMatching Employer Credits) is shown below:

Adjusted income = £150,000 plus 6% of £150,000 plus 12% of £150,000 = £177,000

Excess income = £177,000 less £150,000 = £27,000

Personal Annual Allowance = £40,000 (less £27,000 divided by 2) = £26,500