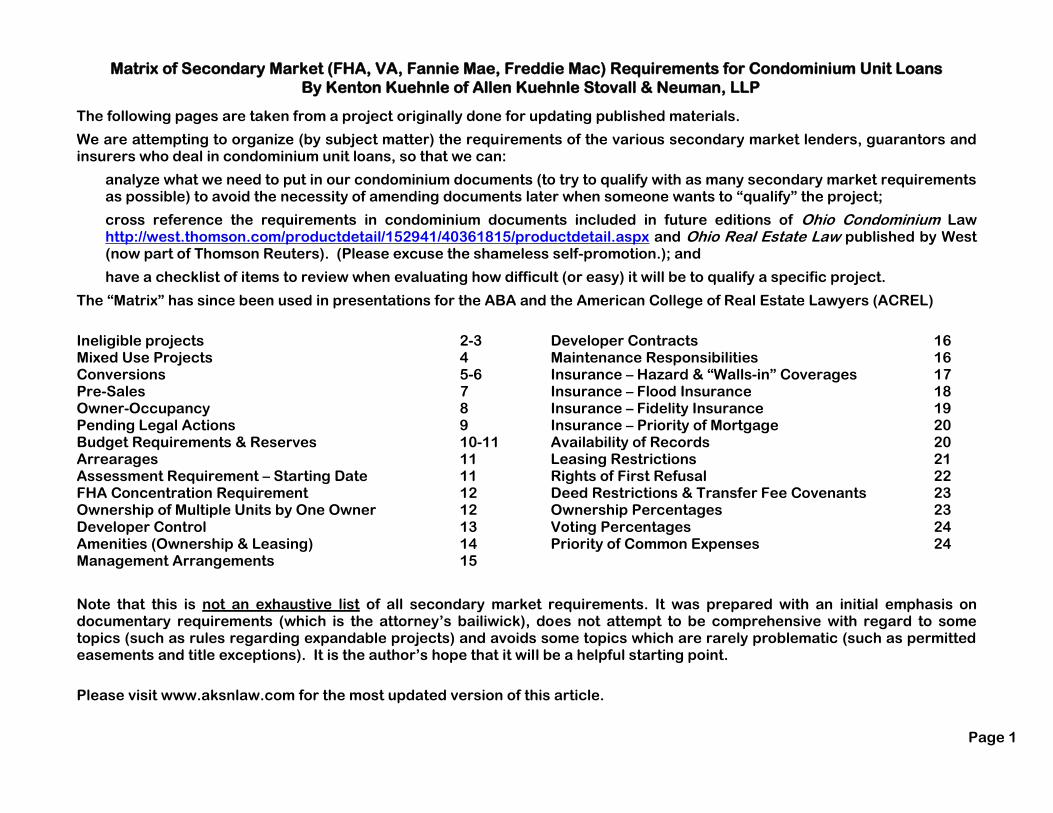

matrix of secondary market (fha, va, fannie mae, freddie ... · page 1 matrix of secondary market...

TRANSCRIPT

Page 1

Matrix of Secondary Market (FHA, VA, Fannie Mae, Freddie Mac) Requirements for Condominium Unit Loans

By Kenton Kuehnle of Allen Kuehnle Stovall & Neuman, LLP

The following pages are taken from a project originally done for updating published materials.

We are attempting to organize (by subject matter) the requirements of the various secondary market lenders, guarantors and insurers who deal in condominium unit loans, so that we can:

analyze what we need to put in our condominium documents (to try to qualify with as many secondary market requirements as possible) to avoid the necessity of amending documents later when someone wants to “qualify” the project;

cross reference the requirements in condominium documents included in future editions of Ohio Condominium Law http://west.thomson.com/productdetail/152941/40361815/productdetail.aspx and Ohio Real Estate Law published by West (now part of Thomson Reuters). (Please excuse the shameless self-promotion.); and

have a checklist of items to review when evaluating how difficult (or easy) it will be to qualify a specific project.

The “Matrix” has since been used in presentations for the ABA and the American College of Real Estate Lawyers (ACREL)

Ineligible projects 2-3 Mixed Use Projects 4 Conversions 5-6 Pre-Sales 7 Owner-Occupancy 8 Pending Legal Actions 9 Budget Requirements & Reserves 10-11 Arrearages 11 Assessment Requirement – Starting Date 11 FHA Concentration Requirement 12 Ownership of Multiple Units by One Owner 12 Developer Control 13 Amenities (Ownership & Leasing) 14 Management Arrangements 15

Developer Contracts 16 Maintenance Responsibilities 16 Insurance – Hazard & “Walls-in” Coverages 17 Insurance – Flood Insurance 18 Insurance – Fidelity Insurance 19 Insurance – Priority of Mortgage 20 Availability of Records 20 Leasing Restrictions 21 Rights of First Refusal 22 Deed Restrictions & Transfer Fee Covenants 23 Ownership Percentages 23 Voting Percentages 24 Priority of Common Expenses 24

Note that this is not an exhaustive list of all secondary market requirements. It was prepared with an initial emphasis on documentary requirements (which is the attorney’s bailiwick), does not attempt to be comprehensive with regard to some topics (such as rules regarding expandable projects) and avoids some topics which are rarely problematic (such as permitted easements and title exceptions). It is the author’s hope that it will be a helpful starting point.

Please visit www.aksnlaw.com for the most updated version of this article.

Page 2

Ineligible Projects

FHA FHA Condominium Project Approval & Processing Guide 1.4 (June 30, 2011)

Mandatory rental pools or other arrangements which restrict owner’s ability to occupy the unit;

25% of total space is used for nonresidential purposes

Condominium Hotels or “Condotels” (examples – has registration services, has word “hotel” or “motel” in title

Located in Coastal Barriers of Atlantic, Gulf of Mexico or Great Lakes

Timeshares or segmented ownerships

Multi-dwelling Units;

Assisted Living Facilities

Projects where developer retains ownership of common areas or amenities after control turned over

FNMA Fannie Mae Single Family/2011 Selling Guide B4-2.1-02 (12/01/2010).

Hotel or motel, or that restrict owner’s ability to occupy their own unit, or which have mandatory rental pool agreements, or which give management control over occupancy (see regs for further descriptions)

Projects with non-incidental business operations owned by association (e.g., spa, restaurant, health club)

Investment securities (filed with SEC or where promoted as investment opportunities)

Tenancy-in-common or similar arrangements; Timeshares or other segmented ownership projects

New project (not fully completed or less than 90% conveyed to purchasers) with a unit less than 400 sq. ft. Fannie Mae Single Family/2011 Selling Guide B4-2.2-04 (12/01/2010).

Sales where Interested Party Contributions are in excess of Fannie Mae’s eligibility policies for individual mortgage loans, including, but not limited to:

Builder/developer contributions; sales concessions; and HOA or principal and interest payment abatements and/or contributions not disclosed on HUD-1.

For rules on HOA credits in excess of 12 months which are paid outside of closing and not disclosed on the HUD-1, see Fannie Mae Single Family/2011 Selling Guide B3-4.1-03 (06/30/2010).

Projects where more than 20% of the total space is used for non-residential purposes

Page 3

Ineligible Projects (continued)

FNMA (Continued) Fannie Mae Single Family/2011 Selling Guide B4-2.1-02 (12/01/2010).

Projects where a single entity (individual, investor group, etc.) owns more than 10% of total units.

Multi-dwelling unit projects or co-ops (see regs for variations on the theme)

Projects that represent legal, but non-conforming, use of land if zoning regulations prohibit rebuilding the improvements to current density in the event of partial or full destruction

See “Pending Legal Actions” section for additional description of actions which would make project ineligible

Freddie Freddie Mac Single Family Seller/Servicer’s Guide 42.3 (08/16/10)

(a) project which is (or has potential to be) subject to state or federal securities regulation

(b) Hotel or resort

(c) project with multi-dwelling units

(d) project with more than 20% of square footage used for non-residential use

(e) common interest [tic] (f) fragmented ownership; or (g) timeshare

(i) legal non-conforming use (attached projects)

(j) litigation (or ADR) involving safety, structural soundness, habitability

(k) projects sold with excessive “interested party contributions” (See Freddie Mac Single Family Seller/Servicer’s Guide 25.3 (08/16/11)

(l) where single entity owns more than 10% of units

(m) project comprised of owners who own their units and renters who rent or lease from the developer or a third party. (doesn’t apply to conversions where tenants entitled to rent by law)

(n) continuing care facilities (see regs. for further description)

(o) project that Fannie Mae has rejected

Page 4

Mixed Use

FHA FHA Condominium Project Approval & Processing Guide 2.1.3 (June 30, 2011)

No more than 25% of total floor area non-residential/commercial (special rules for “live/work” projects)

Exceptions can be granted to existing projects > 1 year old, where control turned over, but no more than 35%

VA Commercial areas are acceptable, but will be considered in value. 38 CFR §36.4360a(g)

If mixed use, voting rights among members must be fully described, including provisions allowing for representation or protection of minority interests. VA Lenders Handbook, 16-B, Exhibit A,(A)4(a) (7/1/2000).

FNMA No more than 20% commercial. Fannie Mae Single Family/2011 Selling Guide B4-2.2-04 (12/01/2010).

Freddie project is ineligible if more than 20% of total square footage is non-residential [42.3(d) (08/16/10) and 42.11(h) (10/09/09) Freddie Mac Single-Family Seller/Servicer’s Guide.

Can’t have multiple classes of unit owners and with a commercial entity as manager over the entire project. 42.7(d), (04/01/11).

Can’t have a hotel, and may not have fragmented ownership or interest. 42.7(d),2 (04/01/11).

Docs must explicitly address retail and commercial uses. 42.7(d),5 (04/01/11).

Commercial owners pay all costs related to commercial space. For example, renovation of retail space or retail lobby (unless whole building where majority of residential and majority of commercial owners agree). 42.7(d), 6 (04/01/11).

Commercial owners can’t override residential on issues involving residential units. 42.7(d),9

Docs must identify CE reserved for residential owners, including parking. 42.7(d),10 (04/01/11).

Commercial owners carry appropriate commercial insurance paid for by them. 42.7(d),8 (04/01/11).

Operating reserves of at least 3 months. 42.7(d),12 (04/01/11).

Docs explicitly address how assessments divided b/w residential & commercial units. 42.7(d),11 (04/01/11).

Project management must not manage a rental program for residential units. 42.7(d),13 (04/01/11).

If common entrance, a majority of commercial & a majority of residential votes are needed for upgrade. 42.7(d),7 (04/01/11).

Page 5

Conversions

FHA FHA Condominium Project Approval & Processing Guide 1.5.1 (June 30, 2011) has detailed rules for newly converted projects for which applications for approval are submitted through HUD “HARP” process (no DELRAP, where Direct Endorsement Lender approves project) with 2 years from date of conversion.

For All Newly Converted Projects:

Only where conversion complete, not based on conversions or phases that are anticipated in the future

Work completed as evidenced by engineering or architectural inspection w/i 12 months of completion

Reserve study & engineer’s report: commenting favorably on structural integrity, remaining useful life

Review of current year budget, current balance sheet, actual income & expense statement must determine that budget and operating results are sufficient and:

Includes allocations/line items sufficient to maintain & preserve all amenities and features unique to project

Provide funding and replacement reserves for capital expenditures & deferred maintenance of 10% of budget

Provides funding for insurance coverage and deductibles

Funds to cover total cost of any items identified in reserve study or engineers report that need to be replaced within 5 years from date of study must be deposited in HOA’s reserve account

Detailed description of work proposed or already completed in order for units to be ready for sale

Developer must provide comprehensive sale and marketing strategy

Additional for NON-GUT (painting, new carpet, replacement of cabinets, fixtures, doors or windows) Conversions

51% conveyed or under contract to owner-occupant principal residents (contract & loan commitments)

Developer may own up to 49% of units at time of project approval

No other owner may own more than 10%

Additional for GUT (down to shell; new HVAC or Electrical components; any structural modification) Conversions

100% complete (except preference items) before any unit mortgage is endorsed. (May escrow for weather related delays for common area items only)

Building permit (or equivalent) is required and Temporary or Permanent Certificate of Occupancy (or equivalent)

Page 6

Conversions (continued)

VA In a conversion where the declarant is in control or still marking units not previously occupied, declarant must provide a statement by a registered professional engineer and/or architect, with an estimate of the remaining useful life of all components (10 years is required on all structural and mechanical components, or declarant must fund 1/10th the cost for each year less than 10). Not required for resale units when declarant is not in control and/or selling units (but it is, apparently, required where declarant is either in control or selling units.) 38 CFR 36.4360a(b)(7)(i)(C) (07/01/93)

In declarant controlled project, a statement by local authorities of the adequacy of off-site utilities (eg, sanitary or water) is required. If local authority declines, one may be obtained from a licensed professional engineer. 38 CFR 36.4360a(b)(7)(ii) (07/01/93)

FNMA For “gut” conversions (where property is renovated down to its shell, including new HVAC and electrical) created in last 3 years, engineer’s report (or functional equivalent) that was originally obtained for conversion must comment favorably on structural integrity and condition and remaining useful life of major components (heating & cooling systems, plumbing, electrical, elevators, boilers, roof, etc.). Fannie Mae Single Family/2011 Selling Guide B4-2.2-04 (12/01/2010).

For newly created, non-gut conversion, must be processed through FNMA’s Project Eligibility Review Service (“PERS”) The engineer’s report mentioned above, along with an independent reserve study, must be provided along with detailed descriptions of work proposed or already completed for units to be ready for sale. Fannie Mae Single Family/2011 Selling Guide B4-2.2-08 (12/01/2010). See also “Budget Requirements/Reserves” below.

Freddie Freddie Mac Single-Family Seller/Servicer’s Guide 42.2(i) (03/11/10) requires that for newly converted projects, the appraiser or other licensed professional must state that the project is structurally sound, and the condition and remaining useful life of the major components are sufficient for residential use.

All rehabilitation work is completed.

If a partial rehabilitation, lender must verify that all repairs affecting soundness and habitability are complete and replacement reserves have been allocated for all capital improvements, and the underwriter has determined that the reserves are sufficient to fund the improvements.

42.6(C) of the Guide (03/11/10) repeats the requirement that for conversions, there must be an initially funded reserve consistent with the remaining useful life of the individual common elements.

Page 7

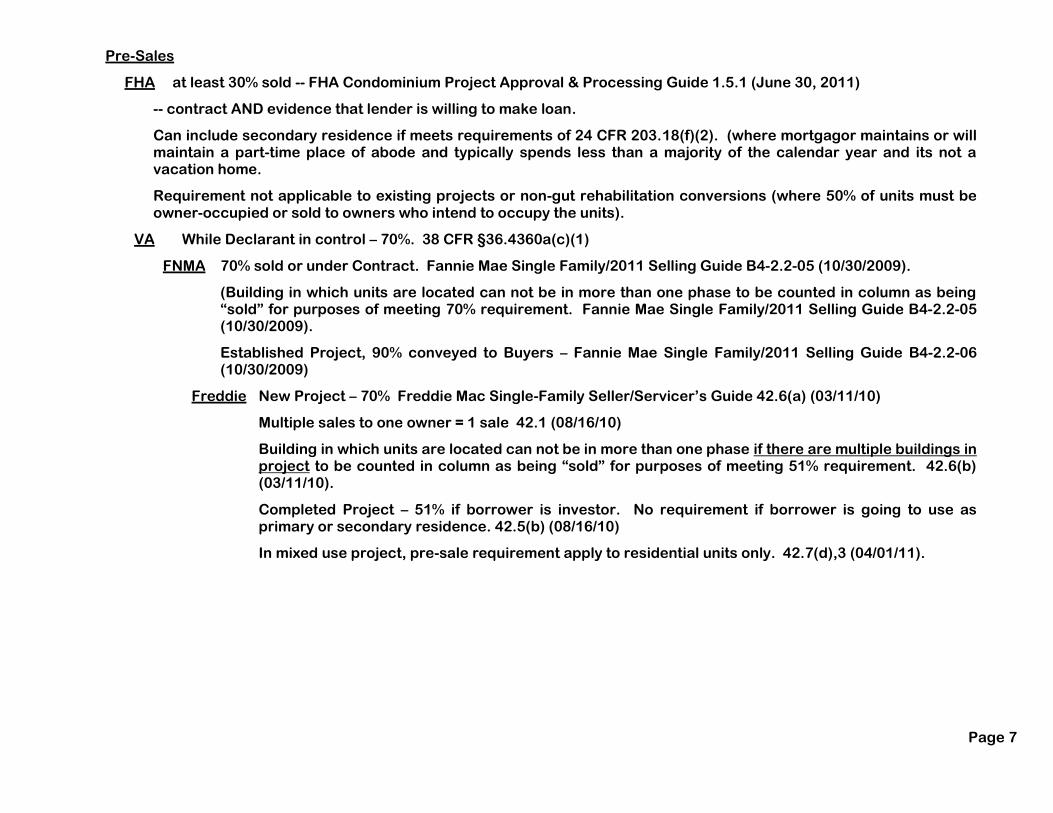

Pre-Sales

FHA at least 30% sold -- FHA Condominium Project Approval & Processing Guide 1.5.1 (June 30, 2011)

-- contract AND evidence that lender is willing to make loan.

Can include secondary residence if meets requirements of 24 CFR 203.18(f)(2). (where mortgagor maintains or will maintain a part-time place of abode and typically spends less than a majority of the calendar year and its not a vacation home.

Requirement not applicable to existing projects or non-gut rehabilitation conversions (where 50% of units must be owner-occupied or sold to owners who intend to occupy the units).

VA While Declarant in control – 70%. 38 CFR §36.4360a(c)(1)

FNMA 70% sold or under Contract. Fannie Mae Single Family/2011 Selling Guide B4-2.2-05 (10/30/2009).

(Building in which units are located can not be in more than one phase to be counted in column as being “sold” for purposes of meeting 70% requirement. Fannie Mae Single Family/2011 Selling Guide B4-2.2-05 (10/30/2009).

Established Project, 90% conveyed to Buyers – Fannie Mae Single Family/2011 Selling Guide B4-2.2-06 (10/30/2009)

Freddie New Project – 70% Freddie Mac Single-Family Seller/Servicer’s Guide 42.6(a) (03/11/10)

Multiple sales to one owner = 1 sale 42.1 (08/16/10)

Building in which units are located can not be in more than one phase if there are multiple buildings in project to be counted in column as being “sold” for purposes of meeting 51% requirement. 42.6(b) (03/11/10).

Completed Project – 51% if borrower is investor. No requirement if borrower is going to use as primary or secondary residence. 42.5(b) (08/16/10)

In mixed use project, pre-sale requirement apply to residential units only. 42.7(d),3 (04/01/11).

Page 8

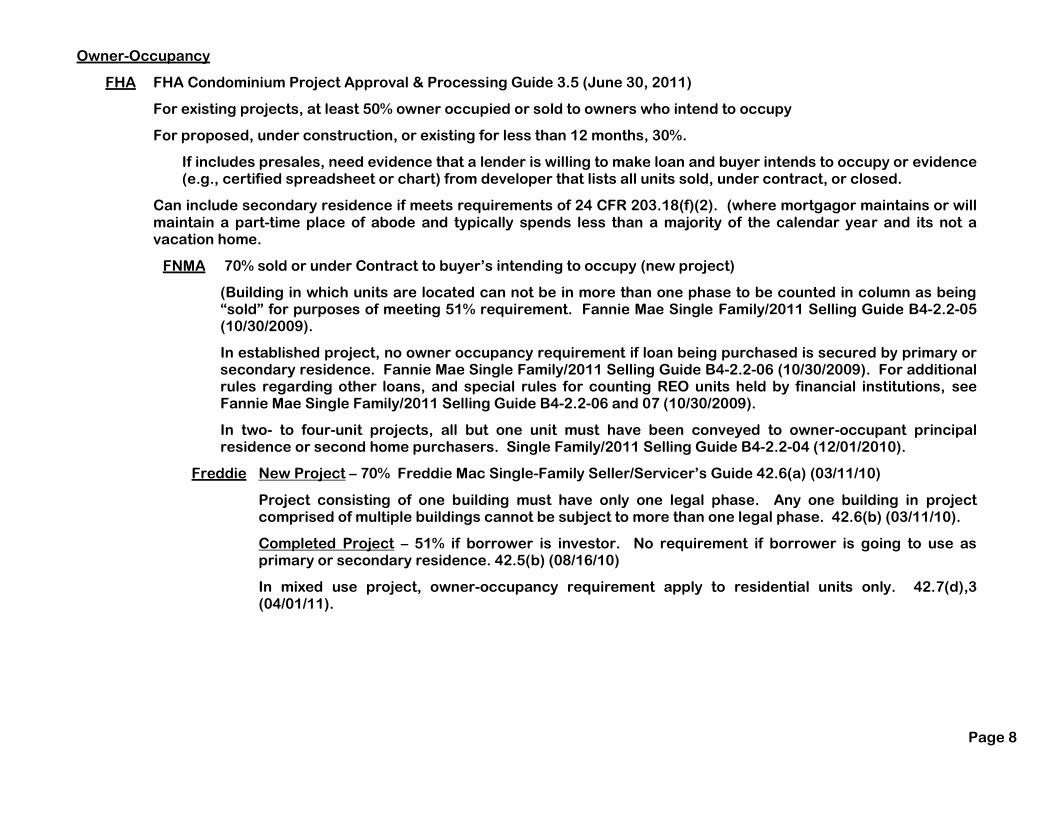

Owner-Occupancy

FHA FHA Condominium Project Approval & Processing Guide 3.5 (June 30, 2011)

For existing projects, at least 50% owner occupied or sold to owners who intend to occupy

For proposed, under construction, or existing for less than 12 months, 30%.

If includes presales, need evidence that a lender is willing to make loan and buyer intends to occupy or evidence (e.g., certified spreadsheet or chart) from developer that lists all units sold, under contract, or closed.

Can include secondary residence if meets requirements of 24 CFR 203.18(f)(2). (where mortgagor maintains or will maintain a part-time place of abode and typically spends less than a majority of the calendar year and its not a vacation home.

FNMA 70% sold or under Contract to buyer’s intending to occupy (new project)

(Building in which units are located can not be in more than one phase to be counted in column as being “sold” for purposes of meeting 51% requirement. Fannie Mae Single Family/2011 Selling Guide B4-2.2-05 (10/30/2009).

In established project, no owner occupancy requirement if loan being purchased is secured by primary or secondary residence. Fannie Mae Single Family/2011 Selling Guide B4-2.2-06 (10/30/2009). For additional rules regarding other loans, and special rules for counting REO units held by financial institutions, see Fannie Mae Single Family/2011 Selling Guide B4-2.2-06 and 07 (10/30/2009).

In two- to four-unit projects, all but one unit must have been conveyed to owner-occupant principal residence or second home purchasers. Single Family/2011 Selling Guide B4-2.2-04 (12/01/2010).

Freddie New Project – 70% Freddie Mac Single-Family Seller/Servicer’s Guide 42.6(a) (03/11/10)

Project consisting of one building must have only one legal phase. Any one building in project comprised of multiple buildings cannot be subject to more than one legal phase. 42.6(b) (03/11/10).

Completed Project – 51% if borrower is investor. No requirement if borrower is going to use as primary or secondary residence. 42.5(b) (08/16/10)

In mixed use project, owner-occupancy requirement apply to residential units only. 42.7(d),3 (04/01/11).

Page 9

Pending Legal Actions

FHA Pending legal actions must be disclosed (except for routine foreclosures commenced by unit lenders) FHA Condominium Project Approval & Processing Guide 2.1.8 (June 30, 2011) Attorney letter must address:

reasons;

anticipated settlement/judgment date;

whether insurance coverage is sufficient to pay without affecting financial solvency of project;

whether it could affect ability of owners to transfer title to units; and

whether it could impact owner’s rights

VA If developer controls, one of items to be submitted, even for existing unit resales, is a “litigation statement” VA Lenders Handbook, 16-A-03(18) (7/14/2003).

FNMA Fannie Mae Single Family/2011 Selling Guide B4-2.1-02 (12/01/2010) lists “ineligible projects”:

-Any project for which HOA is named as a party to pending litigation

-Developer is named as a party to litigation and project is not yet turned over

Related to safety, structural soundness, habitability or functional use of the project

Minor matters not considered:

Non-monetary dispute involving neighbor disputes or rights of quiet enjoyment;

Where claimed amount is known, covered by insurance, and insurance company is defending; or

HOA is plaintiff in foreclosure or action for assessments.

Freddie Freddie Mac Single-Family Seller/Servicer’s Guide 42.3(j) (08/16/10) includes, in its list of “ineligible projects”:

-Where Developer (where project not turned over to home owners) or HOA;

-Is a party to current litigation, arbitration, mediation or other ADR; AND

-Dispute involves safety, structural soundness or habitability of the project.

Page 10

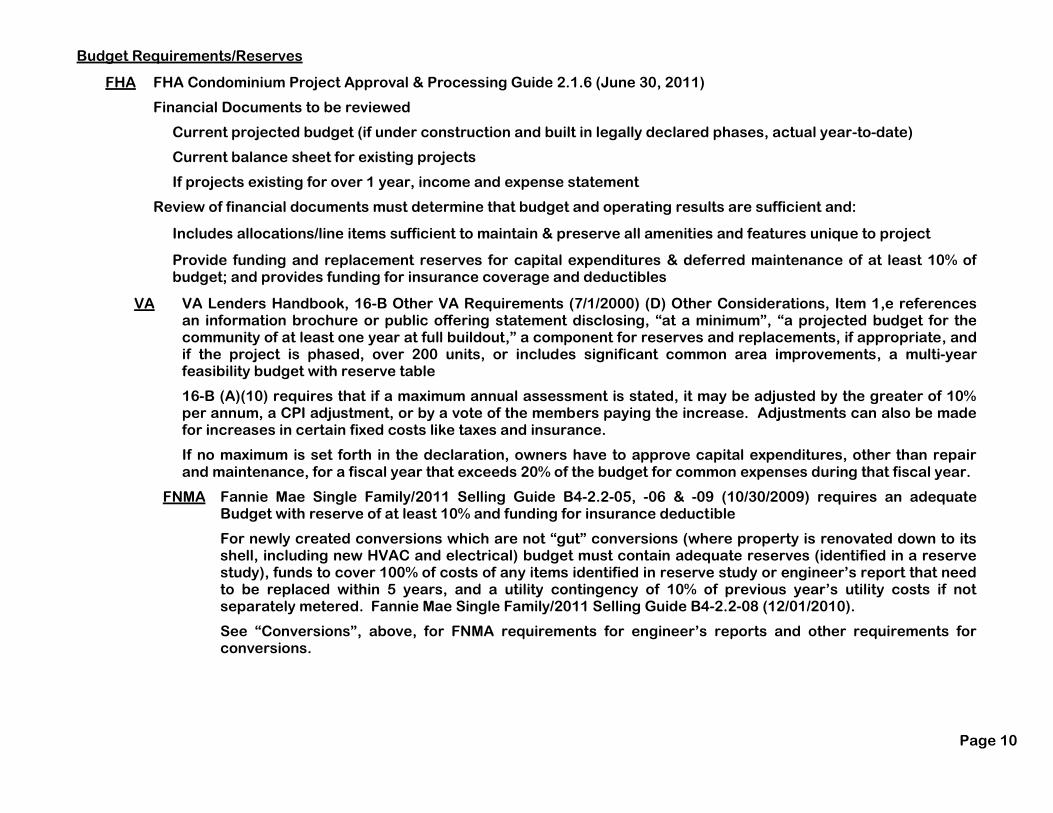

Budget Requirements/Reserves

FHA FHA Condominium Project Approval & Processing Guide 2.1.6 (June 30, 2011)

Financial Documents to be reviewed

Current projected budget (if under construction and built in legally declared phases, actual year-to-date)

Current balance sheet for existing projects

If projects existing for over 1 year, income and expense statement

Review of financial documents must determine that budget and operating results are sufficient and:

Includes allocations/line items sufficient to maintain & preserve all amenities and features unique to project

Provide funding and replacement reserves for capital expenditures & deferred maintenance of at least 10% of budget; and provides funding for insurance coverage and deductibles

VA VA Lenders Handbook, 16-B Other VA Requirements (7/1/2000) (D) Other Considerations, Item 1,e references an information brochure or public offering statement disclosing, “at a minimum”, “a projected budget for the community of at least one year at full buildout,” a component for reserves and replacements, if appropriate, and if the project is phased, over 200 units, or includes significant common area improvements, a multi-year feasibility budget with reserve table

16-B (A)(10) requires that if a maximum annual assessment is stated, it may be adjusted by the greater of 10% per annum, a CPI adjustment, or by a vote of the members paying the increase. Adjustments can also be made for increases in certain fixed costs like taxes and insurance.

If no maximum is set forth in the declaration, owners have to approve capital expenditures, other than repair and maintenance, for a fiscal year that exceeds 20% of the budget for common expenses during that fiscal year.

FNMA Fannie Mae Single Family/2011 Selling Guide B4-2.2-05, -06 & -09 (10/30/2009) requires an adequate Budget with reserve of at least 10% and funding for insurance deductible

For newly created conversions which are not “gut” conversions (where property is renovated down to its shell, including new HVAC and electrical) budget must contain adequate reserves (identified in a reserve study), funds to cover 100% of costs of any items identified in reserve study or engineer’s report that need to be replaced within 5 years, and a utility contingency of 10% of previous year’s utility costs if not separately metered. Fannie Mae Single Family/2011 Selling Guide B4-2.2-08 (12/01/2010).

See “Conversions”, above, for FNMA requirements for engineer’s reports and other requirements for conversions.

Page 11

Budget Requirements/Reserves (Continued)

Freddie Freddie Mac Single-Family Seller/Servicer’s Guide 42.5(c) (08/16/10) and 42.6(c) (03/11/10) requires appropriate allocations for line items pertinent to type and status of project.

At least 10% of “operating budget” [for established project 42.5(c) (08/16/10)] for replacement reserves for capital expenditures and deferred maintenance based on remaining useful life and adequate funding for insurance deductible. [For new projects, 10% of “budget” 42.6(c) (03/11/10)]

For conversions, there must be an initially funded reserve consistent with the remaining useful life of the individual common elements Seller/Servicer’s Guide 42.6(c) (03/11/10).

For mixed use projects, operating reserve must equal 3-months of operating expenses 42.7(d),12 (04/01/11).

Arrearages

FHA No more than 15% for more than 30 days, including bank-owned units. FHA Condominium Project Approval & Processing Guide (June 30, 2011)

Jurisdictional Homeownership Center can consider exception and go to 20% if:

Current fund balance and operating results evidence excess available funds in amount of outstanding arrearage

Financial statements and reserve account balance reveals HOA has sufficiently accounted for bad debt and arrearages

Current reserve study supports sufficiency of current assessments to meet component replacement needs, and

HOA provides evidence of actions to collect

FNMA No more than 15% for more than 30 days. Fannie Mae Single Family/2011 Selling Guide B4-2.2-04 (12/01/2010) and B4-2.2-06 (10/30/2009)

Freddie No more than 15% for more than 30 days. Freddie Mac Single-Family Seller/Servicer’s Guide 42.6(d) [new projects] (03/11/10) and 42.5(d) [established projects] (08/16/10)

Assessment Requirements – Starting Date

Freddie For a new project, the assessments must begin on a specific date. Whether or not all units have been sold. Freddie Mac Single-Family Seller/Servicer’s Guide 42.6(c) (03/11/10)

Page 12

FHA Concentration Requirement

FHA FHA will not insure any more than 50% of the units in a project. FHA Condominium Project Approval & Processing Guide 3.6 (June 30, 2011). Jurisdictional Homeowners Center can grant exemption.

FHA concentration can be increased to 100% if all requirements for project approval are met and:

100% complete all construction completed for 1 year, as evidenced by final or temporary CO for last unit

100% sold and no entity owns more than 10% (except for eligible governmental or nonprofit programs)

Control turned over

Budget provides funding replacement reserves for capital expenditures & deferred maintenance of at least 10%

Owner-Occupancy ration at least 50%

Gut-rehabilitation (as well as proposed and under-construction projects) not eligivle

Ownership of multiple Units by one owner

FHA FHA Condominium Project Approval & Processing Guide 2.1.4 (June 30, 2011)

One investor/entity may not own more than 10% of the Units (not counting unit investor occupies)

Developer’s unoccupied units are not counted, but includes units she rents

Eligible non-profit government housing program not subject to 10% limitation. 24 CFR 203.41

FNMA No single entity – the same individual, investor group, partnership or corporation other than the developer during the initial marketing period, may own more than 10% of the total units in the project. Fannie Mae Single Family/2011 Selling Guide B4-2.2-05 (10/30/2009).

If less than 10 units, no more than one can be owned by one party.

Freddie No single entity owns more than 10% of units (or, if less than 10 units, no one owns more than one unit). Freddie Mac Single-Family Seller/Servicer’s Guide 42.3(l) (06/16/10)

Page 13

Developer Control

FHA Later of (1) 120 days after 75% units conveyed; (2) 3 years after 1st conveyance; OR (3) requirement of state or local condominium law. FHA Condominium Project Approval & Processing Guide 1.9 (June 30, 2011)

VA Earlier of 120 days after 75% units conveyed OR 3-5 years (5-7 if phased) after first conveyance 38 CFR 4359 (a)(1)

BUT VA Lender’s Handbook, Exhibit A “Other VA Requirements” Item (A),4,(b) states the second item as “7 years from the date of recording the declaration or, if a phased project, 5 years after recordation of the most recently recorded annexation document.”

Relinquishing control includes not having right to veto any action of members or board 38 CFR 4359(a)(1)

Declarant is prohibited from retaining the right to veto actions of the Association (except to the extent that declarant’s development rights are affected). Item (D),2,(c) of VA Lender’s Handbook, Exhibit A “Other VA Requirements”.

FNMA “The developer or sponsor should provide for and promote the unit owners’ early participation in the management of the project.” Fannie Mae Single Family/2011 Selling Guide B4-2.2-05 (10/30/2009). No specific time frames referenced.

For established projects, control has been turned over to the owners. Fannie Mae Single Family/2011 Selling Guide B4-2.2-06 (10/30/2009).

Freddie Additional Condominium Warranties include that “the developer has transferred or will transfer control of the HOA to the home owners within a reasonable period of time. Freddie Mac Single-Family Seller/Servicer’s Guide 42.11(a) (10/09/09). No specific time frames referenced.

does not apply to Detached Condominium Project where mortgaged unit is primary or secondary home of unit owner. Seller/Servicer’s Guide 42.11,2

Page 14

Amenities (ownership and leasing)

FHA Lease of recreational or parking areas or facilities unacceptable unless HOA has right of termination, without penalty, on up to 90-day notice. FHA Condominium Project Approval & Processing Guide 1.8.10 (June 30, 2011)

VA VA Lenders Handbook, 16-B, Exhibit A,(D)2 (7/1/2000) references rights reserved by the declarant, its affiliates, “or other party,” which are not acceptable unless reviewed by VA, includes

Lease of the common area to the association or accepting leases from the association except in connection with development related offices such as marketing, sales or construction office for the project

Accepting franchises or licenses from the association for the provision of central television antennae service, cable television or like services.

If parking is not provided within each unit, documents must:

Assign specific spaces to each unit

Assign a specific area to a specific group of units, or

Make other provision assuring parking in compliance with local requirements

OR declarant is to provide other evidence of compliance with local ordinances VA Lenders Handbook, 16-B, Exhibit A,(A)16 (7/1/2000).

FNMA Unit owners in the project must have the sole ownership interest in, “and rights to the use of” (-06) [“and have rights to the use of,” (-05)] the project’s facilities, common elements, and limited common elements. The developer may not retain any ownership interest in any of the facilities. The amenities and facilities – including parking and recreational facilities – may not be subject to a lease between owners or the association & another party. Fannie Mae Single Family/2011 Selling Guide B4-2.2-05 & -06 (10/30/2009).

Freddie When control is turned over, the owners must be the sole owners of all buildings, roads, parking and amenities, and developer must not retain any ownership interest in the common elements. The common elements, including amenities such as parking and recreational facilities, must not be subject to a lease between the unit owners, the association and any other party. Freddie Mac Single-Family Seller/Servicer’s Guide 42.2(g) (03/11/10)

Page 15

Management Arrangements

FHA Any management contract, employment contract, or any contract to which Declarant or an affiliate is a party is unacceptable unless HOA has right of termination, without penalty, on up to 90-day notice. FHA Condominium Project Approval & Processing Guide 1.8.10 (June 30, 2011)

VA 38 CFR 4358(a), in a section titled “examples of reserved rights of declarant, sponsor or affiliate of declarant which are usually unacceptable” includes binding the association to any management contract unless it is terminable without penalty on no more than 90-days notice.

38 CFR 4360a(f) (07/01/93), in a section titled “appraisal requirements”, provides that the “management agreement must be terminable for cause upon 30-days notice, and run for a reasonable period of from 1 to 3 years and be renewable with consent of the association and the management. (Management contracts negotiated by the declarant should not exceed 2 years.)”

VA Lenders Handbook, 16-B, Exhibit A,(D)2(c) (7/1/2000) prohibits the declarant, its affiliates, the sponsor “or other party” from retaining the right to enter into management agreements which extend beyond the declarant control period unless those contracts are: (i) limited to 2 years or (ii) permit the owner-controlled board to terminate the contract.

The declaration should provide that the majority of eligible mortgagees can demand professional management. VA Lenders Handbook, 16-B, Exhibit A,(A)17,h (7/1/2000)

FNMA Fannie Mae prefers that the project be professionally managed. Management contract must be for a “reasonable term” and must “include equitable provisions for termination” Fannie Mae Single Family/2011 Selling Guide B4-2.2-05 (10/30/2009). The management contracts termination provision must not require a penalty payment or advance notice of more than 90 days. B4-2.2-06 (10/30/2009)

Freddie Management contract must be for a “reasonable term” and must “include equitable provisions for termination” (must not require the payment of a penalty or advance notice of more than 90 days). Freddie Mac Single-Family Seller/Servicer’s Guide 42.11(i) (10/09/09)

Page 16

Developer Contracts (other than Management Contracts) (see also “Amenities”)

FHA Any management contract, employment contract, lease of recreational or parking areas or facilities, or any contract or lease (including franchises and licenses) to which Declarant or an affiliate is a party is unacceptable unless HOA has right of termination, without penalty, on up to 90-day notice. FHA Condominium Project Approval & Processing Guide 1.8.10 (June 30, 2011)

VA In 38 CFR 36.4358, the section titled “examples of reserved rights of declarant, sponsor, or affiliate of declarant which are usually unacceptable” includes binding the association to any contract or lease to which the declarant is a party unless it is terminable without penalty on no more than 90-days notice.

38 CFR 36.4358 spells out reserved rights which are usually acceptable include, provided they are for a reasonable period of time and are subject to a concomitant obligation to restore include:

(1) easements provided for in declaration, over common elements (not units) for completing improvements, but only if access otherwise not reasonably available;

(2) easements over common elements (not units) for making repairs; and

(3) rights to maintain facilities (identified in declaration) reasonably necessary to market units, including sales and management offices, model units, parking areas and advertising signs.

Maintenance Responsibilities

VA Responsibility for maintenance and repair of all portions of the condominium property shall be set forth clearly. §38 CFR 36.4357(d)(1)

If association maintains areas it does not own (such as within a public right of way for landscaping or signage or storm water management), [does this include areas within units? After all, technically, the association doesn’t own anything.] attorney must provide a description and rationale. VA Lenders Handbook, 16-B, Exhibit A,(A)8 (7/1/2000).

Page 17

Insurance – Hazard Ins. - What’s Covered (Must Association Policy include “Walls-in” coverage?

FHA Does not require Association to carry “walls-in” coverage, but requires borrow to obtain a walls-in policy (HO-6) if master policy does not include interior coverage, including replacement of interior improvements and betterments. FHA Condominium Project Approval & Processing Guide 2.1.9 (June 30, 2011)

FNMA The Lender must review the entire condominium project insurance policy to ensure that the association maintain a master or blanket policy. In addition to all general and limited common elements that are normally included in coverage, the master policy “also must cover fixtures, equipment, and replacement of improvements and betterment coverage to cover any improvements that the borrower may have made.”

“If the master or blanket policy does not cover the unit’s interior, then the borrower must obtain a “walls-in” policy, commonly known as an HO-6 policy” in no less than 20% of the unit’s appraised value. “The standard requirement for a 5% deductible applies.” Fannie Mae Single Family/2011 Selling Guide B7-3-05 (10/30/2009).

For detached projects FNMA [see Fannie Mae Single Family/2011 Selling Guide B4-2.2-03 (06/28/2011)] requires property to be covered by either:

the type of hazard and flood insurance coverage required for single family detached structures, if the condo unit consists of the entire structure as well as the site and air space, OR

the project’s master hazard and flood insurance policies if the condo unit consists of only the air space for the unit and the improvements and site are considered to be common areas or limited common areas

May not have a blanket policy (or self insurance arrangement) that covers multiple unaffiliated condo associations or projects. Fannie Mae Single Family/2011 Selling Guide B7-3-05 (10/30/2009).

Freddie Building and structures, fixtures, machinery equipment and supplies maintained for the service of the condominium project. Freddie Mac Single-Family Seller/Servicer’s Guide 58.2(c) (10/06/06)

fixtures, improvements, alterations and equipment within the individual units, regardless of ownership, unless the unit owners are required by the governing documents to insure those items. Ibid

If units are in a detached project, Freddie will accept insurance that meets the requirements for 1 to 4 unit properties. Freddie Mac Single-Family Seller/Servicer’s Guide 58.2(c) (10/06/06)

Page 18

Flood Insurance

FHA The Association, not the borrower, is to maintain flood insurance under the National Flood Insurance Program (“NFIP”) on buildings located in a Special Flood Hazard Area (“SHFA”) for replacement cost, up to $250,000 per unit. Mortgagee is responsible for determining if any part of project is in a 100-year flood plain. FHA Condominium Project Approval & Processing Guide 2.1.10 (June 30, 2011). Mortgagee may acquire this information from a third party only to the extent that the third party guarantees the accuracy of the information [(National Flood Insurance Act of 1968 §1365(d)]

VA If in special flood hazard area, flood insurance for lesser of loan amount or maximum available. 38 CFR 36.4326

FNMA If “any part of the improvements are within a Special Flood Hazard Area (“SFHA”) & if flood insurance is available under National Flood Insurance Program (“NFIP”), (if not available, your out) “association must obtain a Residential Condominium Building Association Policy for each building that is located in an SFHA.” The amount of coverage has 3 components: (1) building coverage of 100% of insurable value including machinery and equipment; (2) contents coverage of 100% of insurable value of contents owned by association; and (3) coverage for each unit of lesser of $250,000 or replacement cost. Max deductible $25,000. Fannie Mae Single Family/2011 Selling Guide B7-3-08 (12/30/2009).

If the association does not purchase the complying policy, unit owner is required to get one for his unit, for the “lower” of: (a) 100% replacement cost of the insurable value; (b) maximum available from NFIP (“which is currently $250,000 per dwelling”); or (c) unpaid principal balance of mortgage. Max deductible $5,000.

Freddie Freddie Mac Single-Family Seller/Servicer’s Guide 58.3 (08/20/09) If any portion of building is in a special flood hazard area designated as Zone “A” or “V” and community participates in NFIP (if they don’t, your out) then you must have either:

A building coverage of lower of replacement cost or $250,000 x number of residential units in building

plus contents coverage of lower of value of contents owned by association or max available for content’s coverage from NFIP

with maximum deductibles allowed by NFIP

OR B Unit Owner Coverage at the lowest of: (a) 100% replacement cost of the insurable improvements; (b) maximum available from NFIP; or (c) unpaid principal balance of mortgage

with maximum deductibles allowed by NFIP

Page 19

Fidelity Insurance

FHA FHA Condominium Project Approval & Processing Guide 2.1.9 (June 30, 2011) require that if condo is over 20 Units, bond required for officers, directors, employees and all other persons handling or responsible for funds. No less than 3 months of assessments plus reserve funds.

Management co needs to have bond for its officers, employees and agents handling or responsible for funds of, or administered on behalf of, HOA.

(1) Name association as an oblige; (2) Maximum of funds, including reserves, in custody of HOA or management agent; (3) Not less than 3 months of assessments plus reserve funds unless state law requires a maximum amount

VA Recommends, but does not require, association to purchase bond (3 months + reserves) 38 CFR 36.4359(e)(2).

FNMA Over 20 Units, blanket fidelity ins. required for any one who either handles or is responsible for funds. Management co needs to have bond if it handles funds. Amount of maximum funds in custody of HOA or its management agent at any time. Fannie Mae Single Family/2011 Selling Guide B7-4-02 (10/30/2009).

Lesser amount (3 months of assessments) permitted if condo documents require one of the following:

Separate bank accounts for working and reserve accounts with statements sent directly to assn.

Management company maintains separate accounts for all associations it represents and does not have authority to draw checks or transfer funds from association’s reserve account, OR

Two board members must sign checks on reserve account.

Notice required 10 days before cancellation to association AND to each servicer who services a Fannie Mae held or serviced loan. Fannie Mae Single Family/2011 Selling Guide B7-4-02 (10/30/2009).

Freddie Over 20 Units, bond required for loss from dishonest or fraudulent acts committed by directors, managers, trustees, employees or volunteers who manage funds. Management co needs to have bond if it handles funds. Amount of maximum funds handled, with minimum of 3 months of assessments plus reserves. Freddie Mac Single-Family Seller/Servicer’s Guide 58.5 (03/01/08)

Lesser amount (3 months of assessments) permitted if condo documents require one of the following:

Separate bank accounts for working and reserve accounts with statements sent directly to assn.

Management company maintains separate accounts for all associations in represents and does not have authority to draw checks or transfer funds from association’s reserve account, OR

Two board members must sign checks on reserve account.

Page 20

Insurance - Priority of Mortgagee to collection of insurance proceeds

FNMA No provision of condo docs can give the unit owner or any other party (association?) priority over any rights of the first mortgage holder (under its mortgage) in the case of payment to the unit owner of insurance proceeds or condemnation awards for losses to or a taking of condo units and/or common elements. Fannie Mae Single Family/2011 Selling Guide B4-2.2-13 (10/30/2009).

Availability of Records

VA Association is required to make records available (at least available for inspection upon request, during normal business hours and under other reasonable circumstances) to owners, lenders, holders & insurers and guarantors of first mortgages: Declaration, By-laws, Rules & other books, records and financial statements. 38 CFR 4357(c)(3)

VA Lenders Handbook, 16-B, Exhibit A “Other VA Requirements, (A),17 (7/1/2000) requires that the declaration contain a provision guaranteeing mortgagees and agencies the right to inspect association documents and records on the same terms as members, and, granting the majority of eligible holders of first mortgages the right to demand an audit of the association’s financial records.

Likewise, the handbook, at 16-B, Exhibit A, (B),8 requires that the bylaws contain provisions requiring the association to keep records (i) of its governing documents (i.e., association documents, rules and regulations and design standards); (ii) its actions (board resolutions, meeting minutes, etc.); and (iii) its financial condition (receipts and expenditures affecting finances, operations and administration of the association, budget, financial statements, etc.)

The association is not required to keep such records longer than 3 years, unless otherwise required by applicable law.

Documents, books and records kept on behalf of the association are to be available for examination and copying by a member or such members authorized agent during normal business hours and upon reasonable notice and for a reasonable charge except for privileged or confidential information.

Page 21

Leasing Restrictions

FHA Housing and Economic Recovery Act of 2008 authorized FHA to insure loans under National Housing Act section 203. FHA has determined that the requirements in FHA regulations at 24 CFR part 203 applies to mortgage loans for the purchase of condominium units. (See “Waiver of Federal Housing Administration Regulations at 24 CFR 203.41 (a)(3)” issued March 18, 2011).

Units cannot be subject to legal restrictions on conveyance 24 CFR 203.41(b), which includes leases 24 CFR 203(a)(3), but FHA permits restrictions:

establishment of a maximum number of rental units (not to exceed % which would exceed FHA owner-occupied requirements)

prohibitions against leases for less than 30 days or in excess of maximum allowable term (e.g. 6 months or 12 months)

requirements that leases be in writing and subject to declaration and by-laws

right of association to request names of all tenants and family members who will occupy the unit

Association may not require that tenant be approved by association, including but not limited to meeting creditworthy standards. FHA Condominium Project Approval & Processing Guide 1.8.9 (June 30, 2011)

VA Under 38 CFR 36.4358(c)(6), There shall be no prohibition or restriction on a unit owner’s right to lease his unit except in the following two circumstances:

Minimum initial term of up to 1 year; OR

Age restrictions or restrictions imposed by state and local housing authorities

According to VA Lenders Handbook, 16-B, Exhibit A,(D)3 (7/1/2000), the following restrictions on alienation are not permitted:

b. Right of prior approval of either a prospective purchaser or tenant;

c. Leasing restrictions which amount to unreasonable restrictions on use and occupancy of a unit; or

d. Any minimum lease term in excess of 1 year.

Freddie Freddie Mac Single-Family Seller/Servicer’s Guide 42.11(b) (10/09/09) requires that amendments of a material adverse nature be agreed to by mortgagees representing at least 51% of unit votes. Examples of actions which require mortgagee consent include: “Imposition of any restriction on the leasing or rental of units.”

Page 22

Rights of First Refusal

FHA FHA Condominium Project Approval & Processing Guide 2.1.2 (June 30, 2011) permits a right of first refusal unless it violates discriminatory conduct prohibitions under the Fair Housing Act regulations. 24 CFR 100.

VA For declarations recorded on or after 12/1/1976, no right of first refusal or right to prior approval of a purchaser is permitted.

For declarations recorded prior to 12/1/76, a right of first refusal or a right to provide a substitute buyer is permitted so long as the price is not lower than the owner is willing sell, the terms are just as favorable, the association has 30 days to respond, and the notice and election is required to be by certified or registered mail. 38 CFR 36.4350(b)(5)(ii)

Permitted exceptions include restrictions that are part of a government program:

(A) to assist low or moderate income purchasers (and other conditions); or

(B) a program to protect older people 38 CFR 36.4350(b)(5)(vi)

FNMA Fannie Mae Single Family/2011 Selling Guide B4-2.2-05 (10/30/2009) provides:

Right of First Refusal or first option to purchase can not be exercised:

in any way that could be interpreted as unlawful or discriminatory OR

would impair the marketability of units

Rights of first refusal won’t impact foreclosure, deed-in-lieu of foreclosure, or lease or sale of a unit acquired by a mortgagee or assignee. Selling Guide B4-2.2-13 (10/30/2009)

Freddie Freddie Mac Single-Family Seller/Servicer’s Guide provides

Right of First Refusal or first option to purchase can not be exercised:

in any way that could be interpreted as unlawful or discriminatory OR

would impair the marketability of units 42.11(k) (10/09/09).

Rights of first refusal won’t impact foreclosure, deed-in-lieu of foreclosure, or lease or sale of a unit acquired by a mortgagee or assignee. 42.2(e) (03/11/10)

Page 23

Deed Restrictions and Transfer Fee Covenants

FHA Housing and Economic Recovery Act of 2008 authorized FHA to insure loans under National Housing Act section 203. FHA has determined that the requirements in FHA regulations at 24 CFR part 203 applies to mortgage loans for the purchase of condominium units. (See “Waiver of Federal Housing Administration Regulations at 24 CFR 203.41 (a)(3)” issued March 18, 2011).

Units cannot be subject to legal restrictions which would cause a conveyance 24 CFR 203.41(b), which includes leases 24 CFR 203(a)(3), by the borrower to:

Be void, or voidable, by a third party

Be the basis of contractual liability of the borrower

Terminate, or subject to termination, the borrower’s interest in the property

Be subject to consent of a third party

Be grounds for accelerating or increasing the interest rate on an insured mortgage

Be subject to limits on the amount of sales proceeds a borrower can retain

With regard to this last point, the Community Association Institute believes that this language from FHA Condominium Project Approval & Processing Guide 1.8.8 (June 30, 2011) means that FHA will not fund loans in condominium projects with deed-based transfer fees.

FNMA The Federal Housing Finance Agency has proposed the following Rule for Fannie Mae and Freddie Mac. & They should not purchase or invest in any mortgage encumbered by private transfer fee covenants which Freddie require a transfer fee payment to a third party (examples: developer or its trustee, a homeowner

association, affordable housing group or another community or non-profit group) upon the resale of the property. The revised proposal would exempt fees paid to homeowners’ associations where the fees are used for the “direct benefit” (maintenance, improvements and amenities benefitting) the encumbered properties or adjacent properties. Federal Register February 8, 2011, Volume 76, Number 26 at page 6702. The proposal would apply to covenants created after the publication date of the proposed rule.

Ownership Percentages

VA acceptable methods of allocating interests include

Equal / Square Footage / Fair Market Value / Other method that is “equitable and reasonable” 38 CFR 36.4357(b)

Page 24

Voting Percentages

VA 38 CFR 36.4358(c)(2) acceptable methods of allocating votes:

Equal/Following % interests/Square Footage/Fair Market Value/Other method that is “equitable and reasonable”

Declarant’s voting rights may not be “weighted beyond 3 to 1 in the Declarant’s favor (based on the total number of units planned.)” VA Lenders Handbook, 16-B, Exhibit A,(A)4(b) (7/1/2000). [this provision does not appear to negate the developer’s right to appoint directors during the period of developer control. 16-B Exhibit A, (A)5.]

Freddie Can’t have multiple classes of unit owners and with a commercial entity as manager over the entire project. Freddie Mac Single-Family Seller/Servicer’s Guide 42.7(d),1 (04/01/11).

Commercial owners can’t override residential on issues involving residential units. Freddie Mac Single-Family Seller/Servicer’s Guide 42.7(d),9 (04/01/11).

Priority of Common Expenses

VA Units which will be subject to a VA-guaranteed loan will not be subject to delinquent assessments in excess of 6 months in any case in which the association has not brought enforcement action against the current owner. VA Lenders Handbook, 16-B, Exhibit A,(A)12 (7/1/2000).

FNMA Fannie Mae Single Family/2011 Selling Guide B4-2.1-06 (04/01/2009) allows up to 6 months of regular common expense assessments to have priority over Fannie Mae’s mortgage lien. Fannie Mae will not be liable for any fees or charges related to the collection of the six months of unpaid assessments that accrued before acquisition of title to the unit. Will not purchase a loan in a jurisdiction that allows for more than six months of regular common expense assessments to have priority over Fannie Mae’s lien.

Fannie Mae Single Family/2011 Selling Guide B4-2.2-13, Condo Project Review and Legal Document Requirements (10/30/2009) adds “If the condominium association’s lien priority includes costs of collecting unpaid dues, the lender will be liable for any fees or costs related to the collection of the unpaid dues.

Freddie Any first mortgagee that obtains title pursuant to remedies in the mortgage or through foreclosure will not be liable for more than 6 months of regularly budgeted assessments or charges accrued before acquisition of title. If the Association’s lien priority includes costs of collecting unpaid assessments, the Seller will be liable for any fees or costs related to the collection of the unpaid assessments. Freddie Mac Single-Family Seller/Servicer’s Guide 42.11(e) (10/09/09).

BUYING DIRTY PROPERTY SAFELY -- EPA Clarifies the "No Affiliation" Requirement for Purposes of Qualifying for

Protection as a Bona Fide Prospective Purchaser or Contiguous Property Owner Under the Brownfields Amendments

By Jane K. Warren1 and Shawn S. Smith2

On September 21, 2011, the United States Environmental Protection Agency (EPA) issued a memorandum titled "Enforcement Discretion Guidance Regarding the Affiliation Language of CERCLA’s Bona Fide Prospective Purchaser and Contiguous Property Owner Liability Protections." This guidance document attempts to clarify when EPA will (or will not) exercise its enforcement discretion in determining that a purchaser of contaminated property is not "affiliated with" another potentially responsible party (PRP) under the Comprehensive Environmental Response, Compensation, and Liability Act, 42 U.S.C. §9601 et seq. (CERCLA). The "no affiliation" requirement is a potentially significant hurdle for purchasers attempting to qualify for CERCLA liability protection under the Bona Fide Potential Purchaser (BFPP) and Contiguous Property Owner (CPO) provisions of the 2002 Brownfields Amendments. The BFPP provision, which provides protection from CERCLA liability for a party who knowingly purchases contaminated property after January 11, 2002, requires that the party satisfy a number of requirements, including that the party not be "affiliated with" a PRP of the contaminated property. Specifically, a purchaser cannot be:

(i) potentially liable, or affiliated with any other person that is potentially liable, for response costs at a facility through (I) any direct or indirect familial relationship; or (II) any contractual, corporate, or financial relationship (other than a

contractual, corporate, or financial relationship that is created by the instruments by which title to the facility is conveyed or financed or by a contract for the sale of goods or services); or

(ii) the result of a reorganization of a business entity that was potentially

liable. The CPO provision, which offers similar protection from CERCLA liability, provides, in part:

A person that owns real property that is contiguous to or otherwise similarly situated with respect to, and that is or may be contaminated by a release or threatened release of a hazardous substance from, real property that is not owned by that person shall not be considered to be an owner or operator of a vessel or facility . . . solely by reason of the contamination if . . . .

1

2

(ii) the person is not --

(I) potentially liable, or affiliated with any other person that is potentially liable, for response costs at a facility through any direct or indirect familial relationship or any contractual, corporate, or financial relationship (other than a contractual, corporate, or financial relationship that is created by a contract for the sale of goods or services); or

(II) the result of a reorganization of a business entity that was

potentially liable . . . . In the new guidance document, the EPA emphasized that relationships between a purchaser and PRP "not created to avoid CERCLA liability" would generally not constitute a prohibited "affiliation" and, therefore, would not prevent the purchaser from qualifying as a BFPP or CPO. In particular, the EPA identified four permissible affiliations:

1. relationships between a purchaser and a PRP at other properties; 2. relationships between a purchaser and a PRP that arose after the

purchase and sale of the property; 3. contractual relationships created at the time that title to the property is

transferred; and 4. relationships created between a tenant and an owner.

To illustrate, the EPA provided a series of hypothetical real estate transactions and analyzed whether it would exercise its enforcement discretion and treat the purchaser as a BFPP or CPO. Though the EPA, by issuing this guidance, sought to clarify the "no affiliation" requirement, the EPA nevertheless reiterated that it will apply this guidance on a case-by-case basis and "may deviate from this guidance as necessary or appropriate based on the facts of each case." Thus, while indemnification or insurance agreements between buyers and sellers may not automatically constitute an impermissible "affiliation," EPA reserves the right to look behind the documents.

1 Jane Kimball Warren is an environmental partner in the firm's Hartford office. Her 26 years of environmental experience have made her keenly aware of the need for sophisticated, practical business lawyers who are knowledgeable about the complex issues and opportunities in the highly regulated fields of environmental and land use law. She brings a multidisciplinary viewpoint to her work, and utilizes other attorneys within the practice group, as well as corporate, litigation or other practitioners as needed to provide clients with comprehensive, full-service resources. She appreciates the often-varied interests of lending institutions, developers, manufacturers, corporations, regulators and others. Her approach is to be sensitive to how these industries' dynamics affect her clients' decision-making processes. Contact Jane at [email protected].

3

2 Shawn Smith is an associate in the firm’s Hartford office. He has experience in the area of environmental law representing large utilities, lending institutions, electric suppliers and a municipality on due diligence, permitting, regulatory compliance and enforcement matters. Contact Shawn at [email protected].

The PEB Report on Mortgage Notes Dale A. Whitmani

As every real estate attorney knows, the nation’s courts have been clogged with mortgage foreclosure litigation for the past several years. In many cases, the litigated issues revolve around the interaction of the Uniform Commercial Code and state foreclosure law. Since relatively few foreclosure lawyers (much less judges) are UCC experts, the outcomes of the reported cases often reflect some degree of uncertainty or confusion. To help improve this situation, the Permanent Editorial Board for the Uniform Commercial Code (“the PEB”) released, on November 14, 2011, a report entitled “Application of the Uniform Commercial Code to Selected Issues Relating to Mortgage Notes.” This action is entirely within the PEB’s traditions; one of its charges is to issue commentaries “and other articulations as appropriate to reflect the correct interpretation of the” Code. (Its principal task is to recommend amendments and changes in the Code itself from time to time.) In this brief article, I will describe the approach taken by the PEB and make some observations about its Report in light of current controversies surrounding the secondary mortgage market and mortgage securitization. For the most part, I have omitted citations, since the Report itself is fully documented. What law governs? The Report deals with both Article 3 and Article 9 of the Code, but these two articles do not apply to all mortgage notes with equal force. Article 9, which deals with the way sales and security transfers of notes occur, plainly applies to all mortgage notes, whether they are negotiable or not. (Article 9 uses the term “instrument,” which is defined as a document of a “type that in ordinary business is transferred by delivery with any necessary endorsement or assignment.” This definition covers all promissory notes.) Article 3, on the other hand, by its terms applies only to negotiable notes. It says nothing at all about nonnegotiable notes, which are left to the common law of contracts. As it turns out, this situation is highly problematic, since it can be extremely difficult to determine with certainty whether a note is negotiable or not. The definition of negotiability is complex and technical, and for many mortgage notes, arguments can plausibly be made either way. The courts often seem to assume that mortgage notes are negotiable and are covered by Article 3, but only rarely do they actually analyze the note language to determine whether negotiability exists. For example, I have not found a single reported judicial opinion anywhere in the nation that fully and competently analyzes the negotiability of the standard Fannie Mae/Freddie Mac 1-to-4-family residential note. Hence, it is often unclear which body of law governs mortgage notes – Article 3 or the common law. This is, in a sense, a weakness of the PEB Report. It spells out very

1

clearly the way Article 3 operates on negotiable notes, but it provides no help in determining whether Article 3 applies, or exactly what rules will govern if Article 3 does not. This is, in my view, a fundamental structural problem with the present law that must be dealt with if we are ever to have clarity. But the PEB did not consider clarifying this to be its responsibility. Ownership vs. entitlement to enforcement. The PEB report does an excellent job of explaining the distinction made in Article 3 between owning a note and being entitled to enforce it. These two concepts are quite distinct in Article 3, and confusing them has produced a good deal of nonsense in briefs and judicial opinions. Entitlement to enforce a note means that one can sue on it or (if applicable foreclosure requirements are met) foreclose the mortgage that secures it. The maker of the note (the mortgagor) is the party most concerned with who is entitled to enforce the note; the concept is designed to protect the maker against having to pay twice or defend against multiple claims on the note. If the maker pays in full the person entitled to enforce the note, it is discharged and the mortgage that secures it is extinguished. On the other hand, ownership of the note means that one is entitled to its economic value. The owner and the person entitled to enforce the note are not necessarily the same, and it is entirely possible that someone other than the owner can sue on the note or foreclose the mortgage that secures it. This distinction may seem arbitrary, but it is actually highly useful. Because in foreclosure the foremost issue is whether the foreclosing party has the right to enforce the note, the Report clearly explains how one can become entitled to enforce. In brief, there are three ways: 1. Becoming a holder. This will occur if the note has been delivered to and is in the possession of the person enforcing it, with an appropriate endorsement (either in blank – which makes the note a “bearer note,” or specially – an endorsement that specifically identifies the person to whom the note is delivered). These actions will constitute the person who takes the note a “holder,” entitling him or her to enforce the note. (Incidentally, don’t get sidetracked worrying about whether the “holder” is “in due course.” In the vast majority of mortgage foreclosures it doesn’t matter, since the maker/mortgagor does not raise and does not have any defenses to the action.) 2. Becoming a nonholder who has the rights of a holder. This will occur if the note has been delivered to and is in the possession of the person enforcing it, but without an endorsement. In the absence of an endorsement, the person taking delivery can’t be a holder, but he or she can still get the right of enforcement if the delivery was made for the purpose of transferring that right. See, e.g., Leyva v. National Default Servicing Corp., 255 P.3d 127 (Nev.2011), applying this principle and requiring the servicer to provide specific, affirmative proof that the note was delivered for the purpose of transferring the right of enforcement.

2

3. Providing a “lost note affidavit.” Under Sec. 3-309, a person who doesn’t qualify to enforce the note under (1) or (2) above because of a lack of possession may still enforce it by providing a “lost note affidavit.” However, the requirements for the affidavit are quite strict: the note must have been destroyed, its whereabouts not discoverable, or it must be in the wrongful possession of an unknown person or one who cannot be served. Because in so many current foreclosure cases the secondary market investor or securitized trust does not have possession of the note, the lost note affidavit procedure is extremely important. Prior to the 2002 amendments to 3-309, some courts took the view that the party attempting to enforce the note had to aver that it lost the note itself; a loss of the note by its predecessor (for example, the originator of the note) would not count. See, e.g., Dennis Joslin Co. v. Robinson Broadcasting Corp, 977 F. Supp. 491(D.D.C. 1997). The situation is well explained in Timothy R. Zinnecker, Extending Enforcement Rights to Assignees of Lost, Destroyed, or Stolen Negotiable Instruments under U.C.C. Article 3: A Proposal for Reform, 50 U. Kan. L. Rev. 111 (2001). This narrow interpretation of 3-309 was corrected by the 2002 amendments to Article 3, which now allow a person to enforce the note if he or she “has directly or indirectly acquired ownership of the instrument from a person who was entitled to enforce the instrument when loss of possession occurred.” But the 2002 amendments have been adopted in only ten states, so in much of the nation a secondary market investor may still be in serious trouble if the note was lost or destroyed by its predecessor. This was exactly the result in State Street Bank v. Lord, 851 So.2d 790 (Fla.App.2003). To return to the first two methods of becoming “entitled to enforce” described above: while they require that the enforcing party possess the note, they do not literally insist that the note be produced in court. Conceivably, the foreclosing party could prove that it had possession of the note by other means, such as oral testimony or affidavits. But one can see why many courts in judicial foreclosure states have demanded that the note itself be produced; if you have the note, why not show it to the judge? See, e.g., 5 Star Management, Inc. v. Rogers, 940 F.Supp. 512 (E.D.N.Y.1996); In re Wilhelm, 407 B.R. 392 (Bankr. D. Idaho 2009), pointing out that having a mortgage assignment from MERS is no substitute for getting delivery of the note. Nonjudicial foreclosure. In most states where nonjudicial foreclosure is available, the security instrument usually used is a deed of trust, and the trustee is authorized by the documents and by statute to give the appropriate notices and conduct the foreclosure sale when instructed to do so by the “beneficiary” – that is, the person entitled to enforce the note. But there are many uncertainties in the application of the principles discussed above to trustees’ sales. It seems fairly clear that the beneficiary need not show the note or the lost note affidavit to the trustee in order to commence the foreclosure process; the trustee, after all, is not a judge, and in general is entitled to accept the representations of the beneficiary as to the state of the mortgage loan; see, e.g., Kachlon v. Markowitz, 85 Cal. Rptr. 3d 532 (Cal.App. 2008).

3

Hence, in a nonjudicial foreclosure there is usually no forum in which the rights of the person purporting to have the right of enforcement of the note can be adjudicated. Unless the mortgagor brings an action to enjoin the foreclosure, or a suit after foreclosure for damages or to set aside the sale (all of which are expensive actions, fraught with uncertainty), no one will insist on the putative beneficiary’s proving that it has the right of enforcement. Even if a lost note affidavit is theoretically necessary (because the note was negotiable and the party foreclosing does not possess it), no one will demand that it be produced. Moreover, consider the provision of 3-309 which provides that, in a “lost note” case, the maker of the note is entitled to “adequate protection” (typically in the form of a bond) against the possibility that someone else will later attempt to enforce the note. In a nonjudicial foreclosure this provision will likely go entirely ignored or unenforced, since there is no one to make the foreclosing party provide the protection. To put it mildly, this situation is unsatisfactory and needs work. Of course, if a nonjudicial foreclosure is completed, but the party who instructed the trustee to foreclose was not authorized to do so, the sale might be subject to attack later in an action to set it aside or for damages. Under many nonjudicial foreclosure states, however, it is not easy to tell precisely who has authority to commence the foreclosure process, particularly if the loan has been sold on the secondary market. Indeed, it sometimes seems as of the drafters were unaware that secondary market existed. The UCC’s requirements may be relevant to this question, but they obviously cannot provide a complete answer, and resort must be taken to the foreclosure statute and the accompanying case law. Note and mortgage assignments. The PEB Report points out that of sales of notes (as distinct from transfers of the right of enforcement) are covered by UCC Article 9. Somewhat confusingly, Article 9 employs the terminology of security or collateral assignments to apply to outright sales of notes as well; thus the transferor is termed the “debtor,” the transferee is the “secured party,” and the rights transferred constitute a “security interest” even when an outright sale occurs. Once one gets over this semantic hurdle, however, Article 9’s requirements are simple: ownership of the note can be transferred either by delivering possession of the note itself or by signing a “security agreement” (which in this case is simply a written assignment or agreement of sale). It isn’t necessary to do both of these things; either alone is sufficient, and no Article 9 filing is needed for perfection of the transfer. (Observe, however, that while a signed agreement will transfer ownership, it won’t transfer the right of enforcement under Article 3, as we have already seen.) The PEB Report makes two additional and important points about complying with Article 9. First, if a written agreement is used, the description of the note or notes being transferred need not be very specific. Indeed, even a broad phrase such as “all of the transferor’s notes,” or all of the notes that fit a certain definition, will suffice. This suggests that conveyance clauses using general descriptions of groups of notes, such as are often found in Pooling and Servicing Agreements in mortgage securitizations,

4

may well be effective to transfer ownership even if no detailed schedule of the notes is attached. But this, of course, can be a close factual question. Second, the PEB Report points out that under Sec. 9-203(g), a sale of a note complying with Article 9 will automatically transfer or assign the mortgage that secures it. From Article 9’s viewpoint, no separate assignment of the mortgage is needed. This would seems to follow even if the mortgage is technically held by a nominee such as MERS; beneficial ownership of the mortgage will still follow the note without the need for any further documentation. Moreover, any discussion about whether the note and mortgage have been severed or separated from one another is completely off-base. They literally can’t be severed if the note transfer complies with Article 9. This is, of course, entirely consistent with traditional mortgage law, which has always held to the same principle: the mortgage follows the note. See, e.g., Restatement (Third) of Property (Mortgages) Sec. 5.4. The power to foreclose. Article 9 makes the transfer of ownership of notes, and the mortgages that secure them, easy. However, as the PEB Report points out, having ownership of a mortgage under Article 9 does not necessarily mean that the owner can foreclose it. The reason is obvious when one considers the real property recording system. Neither of the two ways of transferring note ownership under Article 9 – delivery of the note or signing a written agreement or assignment of the note – will create any record of the corresponding mortgage transfer in the recording system. Hence, in a number of states (although probably a minority), foreclosure statutes provide that no valid foreclosure of the mortgage can occur unless the foreclosing party has a chain of mortgage assignments from the originating lender to the foreclosing party. Such states include (in a non-exhaustive list) Alabama, Connecticut, Florida, Idaho, Kansas, Massachusetts, Minnesota, Michigan, Oregon, South Dakota, and Wyoming. Most of the statutes require the chain to be recorded, but some do not. This sort of statutory requirement was the basis for the much-discussed Massachusetts opinion in U.S. Bank v. Ibanez, 941 N.E.2d 40 (Mass.2011). Another recent example is In re McCoy, 446 B.R. 453 (Bankr.D.Or.2011). While the PEB Report does not address the issue, it seems unlikely that state courts would accept the implicit mortgage assignment growing out of Sec. 9-203(g) as satisfying these statutory requirements. What is wanted is a “real” mortgage assignment that is or can be recorded in the real estate records. Note that there is typically no requirement in the statutes that the mortgage assignment be given or recorded simultaneously with the transfer of ownership of the note, or even that the two chains of ownership follow the same route. For example, it seems entirely possible that ownership a pool of securitized notes could be transferred under 9-203(g) by a Pooling and Servicing Agreement, followed months or years later by written assignments of the mortgages directly from the originator or MERS to the securitized trustee. What if the originator is unwilling to give such assignments, or has been dissolved or cannot be found? Article 9 provides at least a partial solution. If the original

5

6

transfer of the notes was by a written agreement (which, you will recall, is termed a “security agreement” in Article 9), the secondary market purchaser is authorized by 9-607(b) to record the “security agreement” in the real estate records, along with an affidavit stating that a default on the underlying mortgage note has occurred. It would seem that state courts should be willing to accept this sort of recording in lieu of an actual chain of mortgage assignments, since it obviously serves the same policy objective of providing a recorded explanation of the foreclosing party’s authority. However, I’m aware of no cases considering the question.

Rather strangely, the introductory language of 9-607(b) states that it can be used “if necessary to enable a secured party to exercise under subsection (a)(3) the right of a debtor to enforce a mortgage nonjudicially.” There seems to be no good reason why the procedure should not be equally available to facilitate a judicial foreclosure if the state’s rules require a recorded chain of mortgage assignments for that purpose.

Conclusion. In sum, the PEB Report is a clear, concise, and accurate summary

of the way Articles 3 and 9 interact with mortgage law. It tells us: 1. How one becomes entitled to enforce a negotiable note. 2. How one becomes the owner of a note (negotiable or not). 3. One way that a person can become the owner of the mortgage that secures a

note. 4. One way that a person who becomes such an owner can memorialize that

ownership in the real estate records, even if obtaining a mortgage assignment is not possible.

The interaction between the UCC and foreclosure law remains in some ways

imperfect, and there are still thorny questions that remain unanswered, but the Report is likely to be of very substantial assistance to courts and lawyers as they work their way through the current backlog of foreclosures.

i Dale Whitman is an Emeritus Professor of Law at the University of Missouri-Columbia and the author of numerous books and articles on real estate finance and property law. He was co-reporter, with Grant Nelson, of the Restatement (Third) of Property (Mortgages) and reporter for the Uniform Nonjudicial Foreclosure Act.