market design options of kazakhstan and …activity completion report market design options of...

TRANSCRIPT

ACTIVITY COMPLETION REPORT

MARKET DESIGN OPTIONS OF KAZAKHSTAN AND ITS ROLE IN THE CENTRAL ASIA REGIONAL ELECTRICITY MARKET

(89.KZ, 107.KZ,108.KZ&117.UZ)

INOGATE Technical Secretariat and Integrated Programme in support of the Baku Initiative and the Eastern Partnership energy objectives

Contract No 2011/278827

A project within the INOGATE Programme

Implemented by:

Ramboll Denmark A/S (lead partner) EIR Development Partners Ltd.

The British Standards Institution LDK Consultants S.A. MVV decon GmbH ICF International

Statistics Denmark Energy Institute Hrvoje Požar

Document title Activity Completion Report “Market Design Options of Kazakhstan and its Role in the Central Asia Regional Electricity Market” (89.KZ, 107.KZ,108.KZ&117.UZ)

Document status Final

Name Date

Prepared by Emmanuelle Rault, Konstantinos Perrakis, Nikos Tourlis, Nikos Patsos and Mariyash Zhakupova

04/04/2016

Checked by

Nikos Tsakalidis Adrian Twomey

06/04/2016

Approved by

Peter Larsen 23/05/2016

This publication has been produced with the assistance of the European Union. The contents of this publication are the sole responsibility of the authors and can in no way be taken to reflect the views of the European Union.

3

Acronyms

APX UK APX Power UK (formerly named UKPX) AREM Agency for the Regulation of Natural Monopolies, mainly

regulating tariffs AS Ancillary Services ASECA Automated system of electricity control and accounting ATS Trade system administrator AZ K The Agency for Competition Protection which monitors

operation of competitive markets CAPS Central Asian Power System CCA Competition capacity auctions CCGT Combined Cycle Gas Turbine CCS Carbon Capture and Storage CDA Capacity Delivery Agency CDC Energia Central Dispatch Centre (of Central Asia) CHP/DH Combined Heat and Power/ District Heating CHPP Combined Heat and Power Plant CIGRE Council on Large Electric Systems CIS Commonwealth of Independent States COGEN Cogeneration Association of Europe CONE Cost Of New Entry CPM Capacity Payments CRE Energy Regulatory Commission of France DC Direct Current DECC Department of Energy and Climate Change (UK) DG Directorate General (of the European Commission) DG-TREN Directorate General for Transport and Energy DPM long-term capacity supply agreements (in their Russian

abbreviation) DR Demand Response DSR Demand Side Response E.ON European holding company based in Düsseldorf, North Rhine-

Westphalia, Germany EC European Commission EDF Electricite de France EEX European Energy Exchange AG, Germany's energy exchange ENTSO European Network of Transmission System Operators EOM Energy Only Market EPA Environmental Protection Agency EPC European price coupling EPEX SPOT SE European Power Exchange is an exchange for power spot

trading in Germany, France, Austria, Switzerland and Luxembourg

ERGEG European Regulators Group for Electricity and Gas

4

EU European Union EU IEM European Union Internal Electricity Market EUR Euro EWEA European Wind Energy Association EXAA Energy Exchange Austria FERC Federal Energy Regulatory Commission (of the US) GW Giga Watt HHI Herfindahl-Hirschman Index HPP Hydro Power Plant IAEE International Association of Energy Economics IEM Internal Electricity Market IEM Energy management system INOGATE Technical Secretariat & Integrated Programme in support of the

Baku Initiative and the Eastern Partnership energy objectives” project, funded by EC/Europeaid

IPE International Petroleum Exchange, now ICE Futures (since 2005) ISO Independent System Operator ISO-NE ISO New England (US) IT Information Technology ITO Independent Transmission operator ITS INOGATE Technical Secretariat JSC Joint Stock Company KARNM Kazakhstan’s Agency for Regulation of Natural Monopolies KEA Kazakhstan Electricity Association KEGOC the Transmission System Operator -, which includes the

National Dispatch Center and serves as the system operator of the National Electric Power System

KOREM The Kazakhstan Wholesale Energy and Capacity Market Operator, which operates centralized trading platform for the short-, mid-and long-terms trading

KREM An alternative acronym for KARNM (see above) KZ The Republic of Kazakhstan LLC Limited Liability Company LMP Locational Marginal Pricing LPX Leipzig Power Exchange GmbH LSE Load serving entities (decentralised) LSE Load Serving Entities LTA Long term agreements MCP Market Clearing Price MINT Ministry of Industry and New Technologies (re-organised to

Ministry of Energy) MIP Mixed Integer Program MOPR Minimum Offer Price Rule MRC Multi Regional Coupling MISO Midcontinent ISO (US) MW Mega Watt MWh Mega Watt Hour

5

NOME Law Nouvelle Organisation du Marché de l'Electricité Law NordPool The single financial energy market for Norway, Denmark,

Sweden, Finland, Estonia, Latvia, Lithuania, Germany and the UK.

NREL National Renewable Energy Laboratory (US) NWE North west Europe NYISO New York ISO OHPL Overhead Power transmission lines OTC Over The Counter (trading) OU Ownership Unbundling PDC Power distribution company PEGAS Pan-European Gas Cooperation PJM PJM is a regional transmission organization (RTO) that

coordinates the movement of wholesale electricity in all or parts of 13 states and the District of Columbia.

POLPX Polish Power Exchange PowerEX Marketer of wholesale energy products and services in western

Canada and the western US, and a growing niche player in other markets across North America

Powernext SA Powernext S.A. designs and operates spot and futures exchanges for the trading of power, gas, and emissions contracts in the European energy sector.

PV Solar Solar Photovoltaics PXs Power Exchange(s) RAO UES Unified Energy System of Russia ( an electric power holding

company before its restructuring) RCC RES Renewable Energy Sources RM Regulated market RSE Regional State Enterprises RTE Transmission System Operator of France RTO Regional Transmission Operator SEM Single Electricity Market SO System Operator ST Steam Turbine TM Target Model TTF Dutch gas trading exchange TYNDP Ten Year Network Development Plan UES Kazakhstan’s Unified Energy System UES CA Unified Energy System Of Central Asia UK United Kingdom UKPX United Kingdom Power Exchange UNDP United Nations Development Programme US United States USA United States of America USSR Union of Soviet Socialist Republics UZ Republic of Uzbekistan

6

VAT Value Added Tax VG Variable Generation VOLL Value-Of-Lost-Load VPP Virtual power plants

7

1 Contents 1 PART 1 – EUROPEAN COMMISSION .............................................................................................. 12

1.1 Background ........................................................................................................................... 12

1.2 Essence of the Activity .......................................................................................................... 12

1.3 Key Findings .......................................................................................................................... 14

1.4 Ownership and Benefits of the Activity ............................................................................... 15

1.5 Recommendations ................................................................................................................ 15

1.6 Challenges Faced ................................................................................................................... 17

1.7 Impact Matrix ....................................................................................................................... 17

2 PART 2 - BENEFICIARIES ................................................................................................................. 19

2.1 Executive Summary ............................................................................................................... 19

2.2 Background ............................................................................................................................ 26

2.2.1 Objectives of the study, key findings and recommendations ....................................... 26

2.2.2 Methodology and outputs ............................................................................................. 27

2.2.3 Limitations and further work......................................................................................... 27

2.2.4 Structure of the report .................................................................................................. 28

2.3 ELECTRICITY MARKETS .......................................................................................................... 29

2.3.1 Concepts in the new market structure .......................................................................... 29

2.3.1.1 The rationale of preserving networks as natural monopoly ..................................... 29

2.3.1.2 Unbundling ................................................................................................................ 30

2.3.1.3 Trading in wholesale electricity markets ................................................................. 31

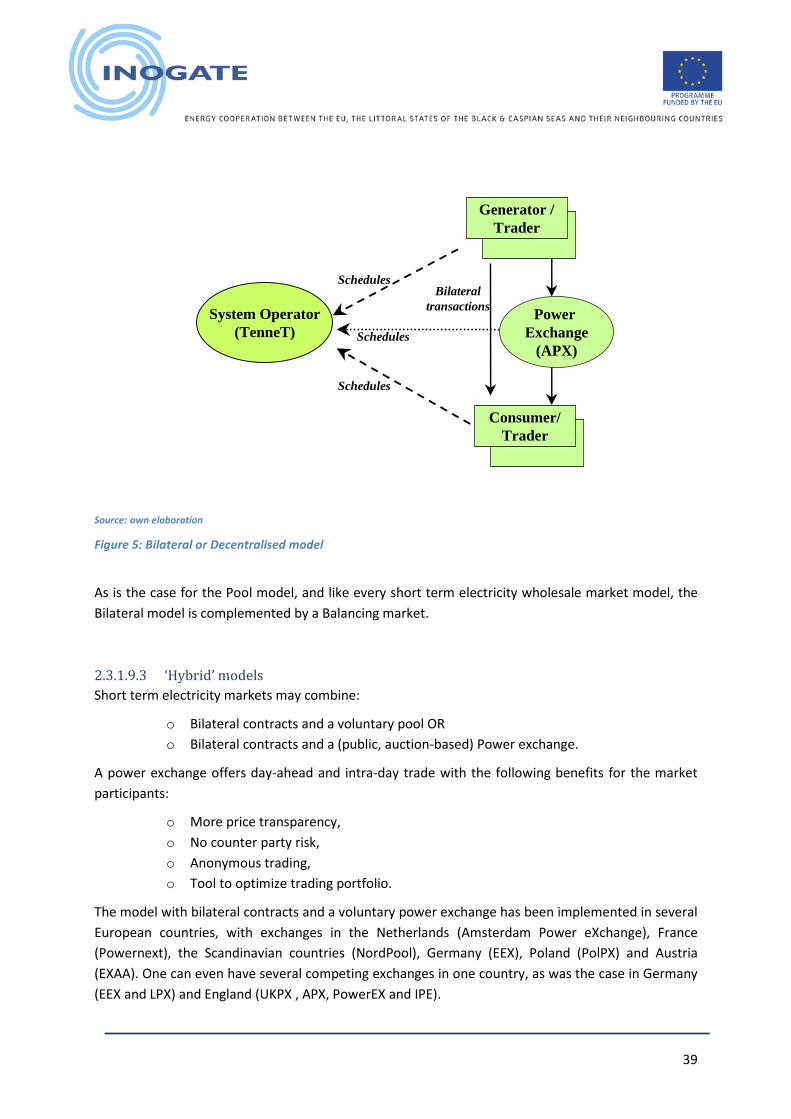

2.3.1.4 Bilateral contracts ..................................................................................................... 31

2.3.1.5 Power Pools or Electricity pools ................................................................................ 32

2.3.1.6 Power exchanges ....................................................................................................... 33

2.3.1.7 Balancing markets ..................................................................................................... 36

2.3.1.8 Coordination of electricity markets ........................................................................... 36

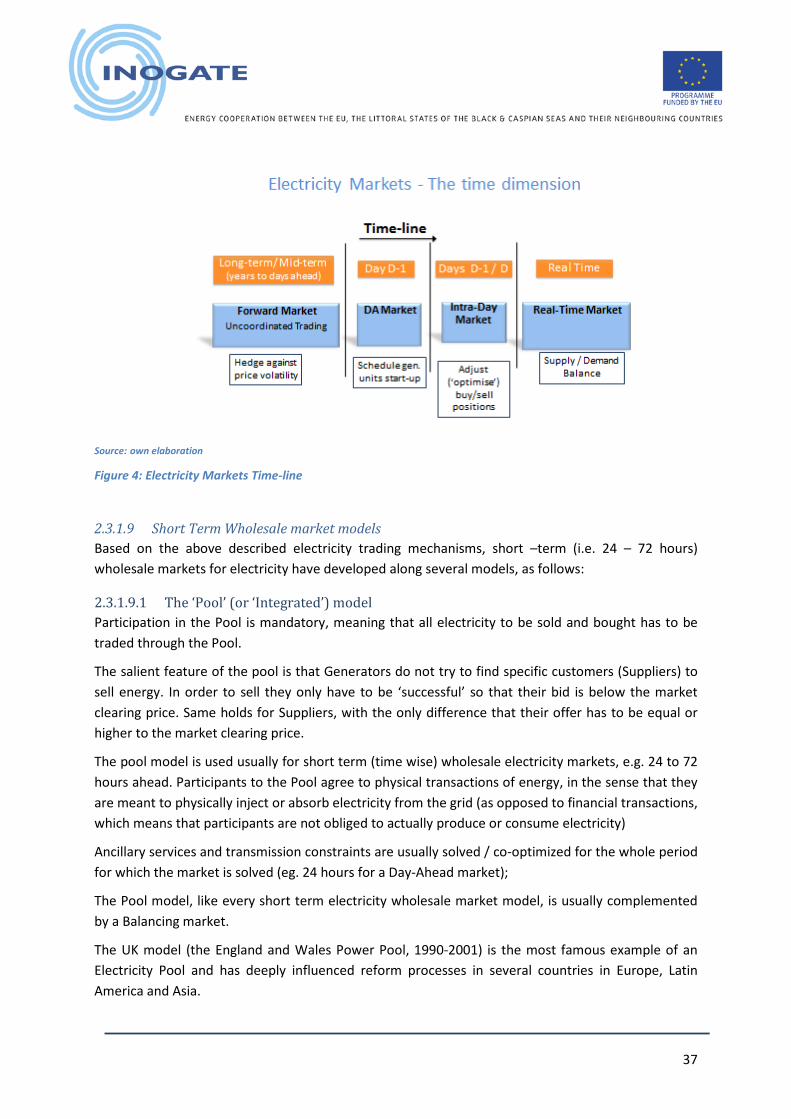

2.3.1.9 Short Term Wholesale market models ...................................................................... 37

2.3.1.10 Determination of the wholesale price of electricity ............................................. 40

2.3.2 Electricity markets liberalisation in the EU ................................................................... 40

2.3.2.1 Drivers of liberalisation and its evolution in the EU .................................................. 40

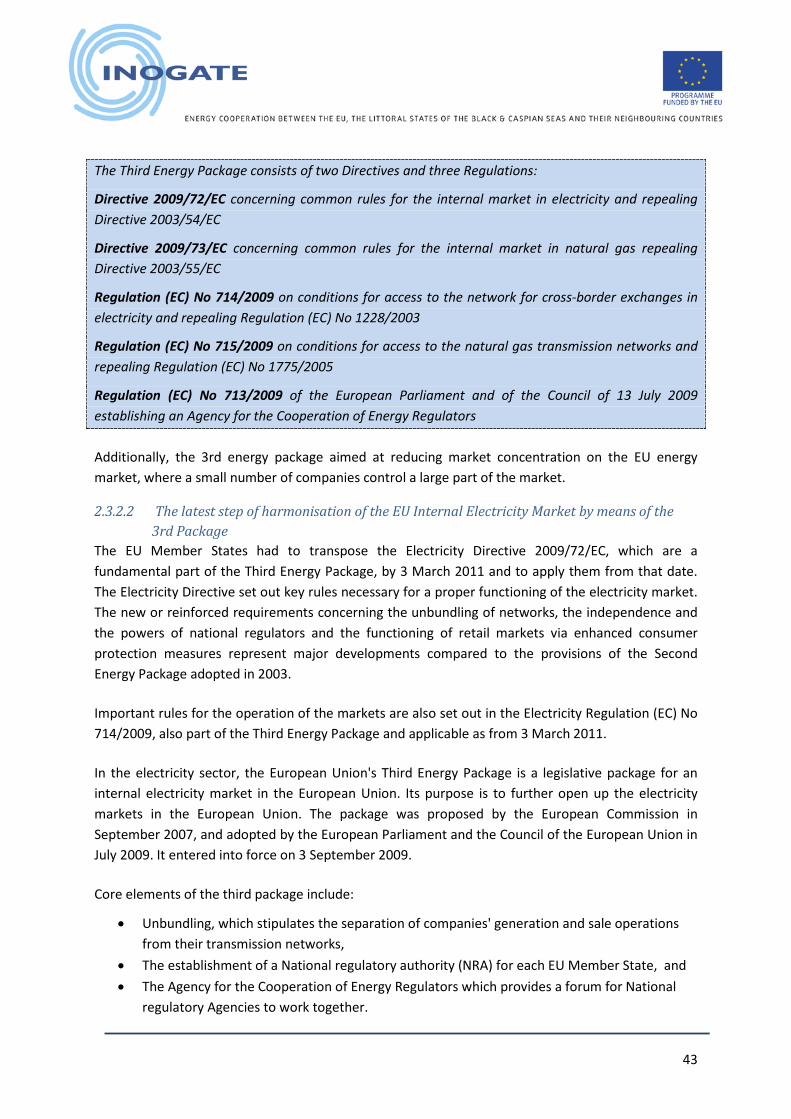

2.3.2.2 The latest step of harmonisation of the EU Internal Electricity Market by means of the 3rd Package ......................................................................................................................... 43

8

2.3.2.3 Unbundling in the notion of the EU legislation ......................................................... 44

2.3.2.4 National Regulatory Authorities ................................................................................ 45

2.3.2.5 Agency for Cooperation of Energy Regulators .......................................................... 46

2.3.2.6 Cross-border cooperation ......................................................................................... 46

2.3.3 Integration of national markets – the EU Internal Energy Market ............................... 50

2.3.3.1 Regulation 1228/2003 and Directive 2003/54 .......................................................... 50

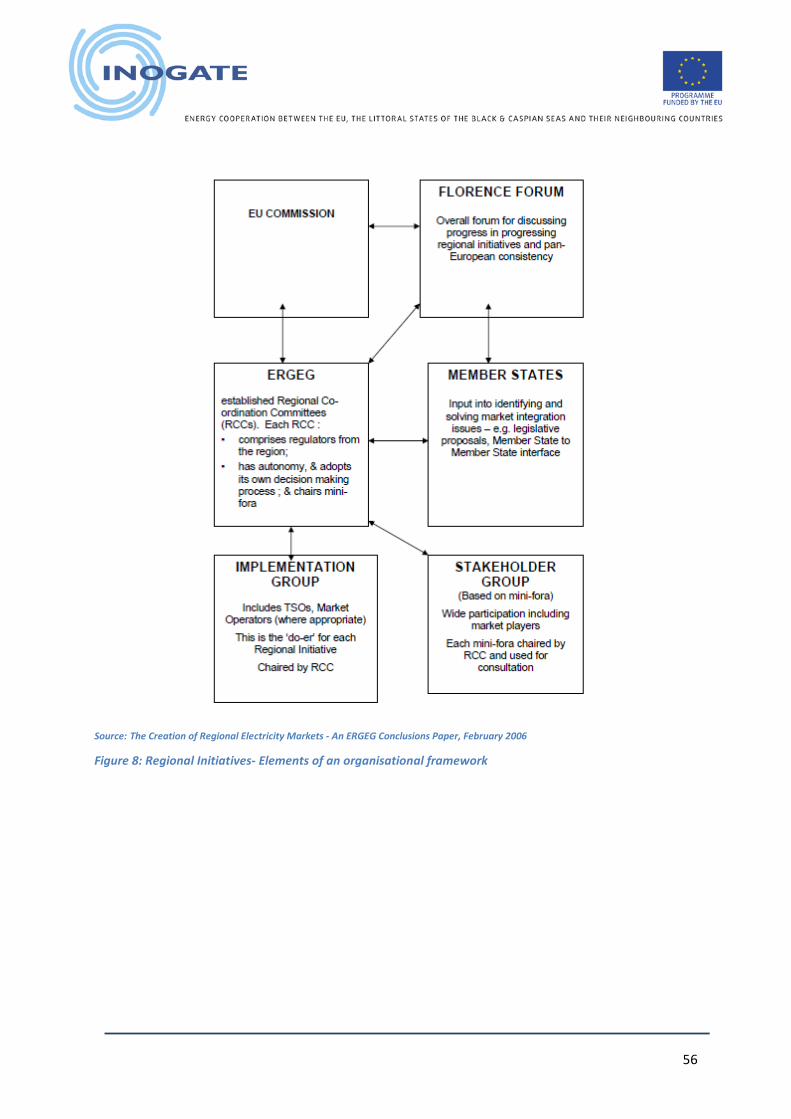

2.3.3.2 Regional Initiatives within the EU ............................................................................. 51

2.3.3.3 The 3rd Energy Package (2009) ................................................................................. 57

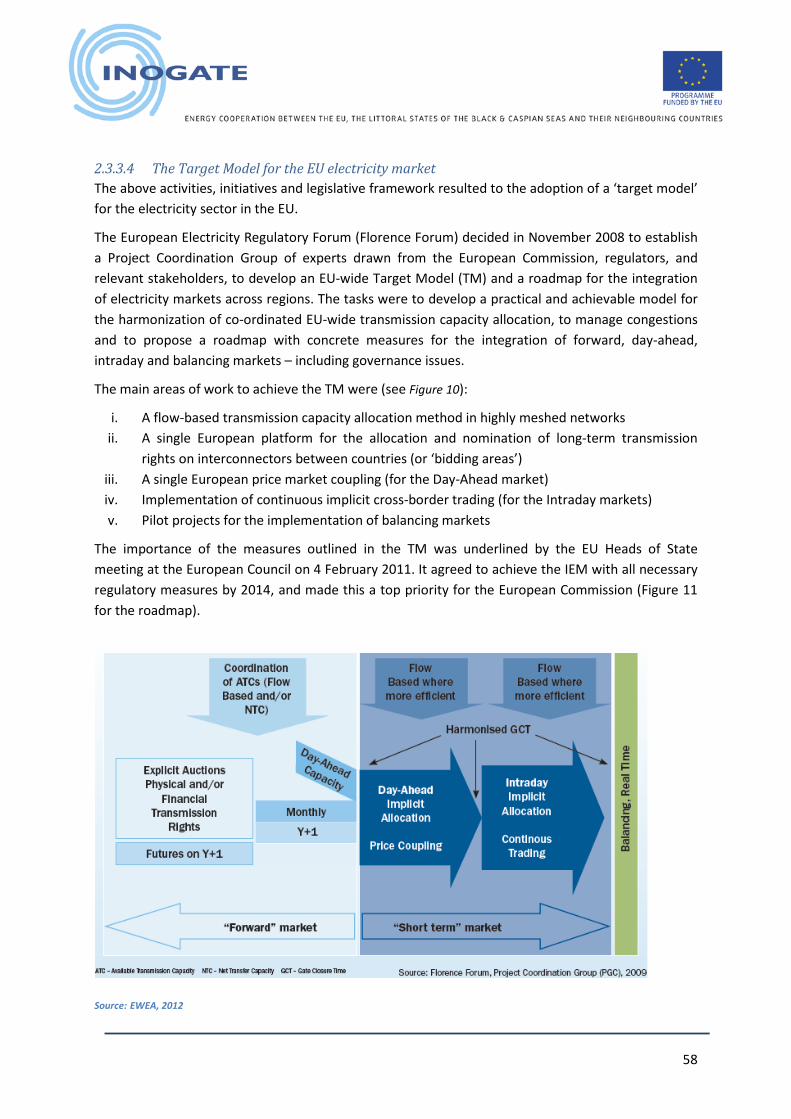

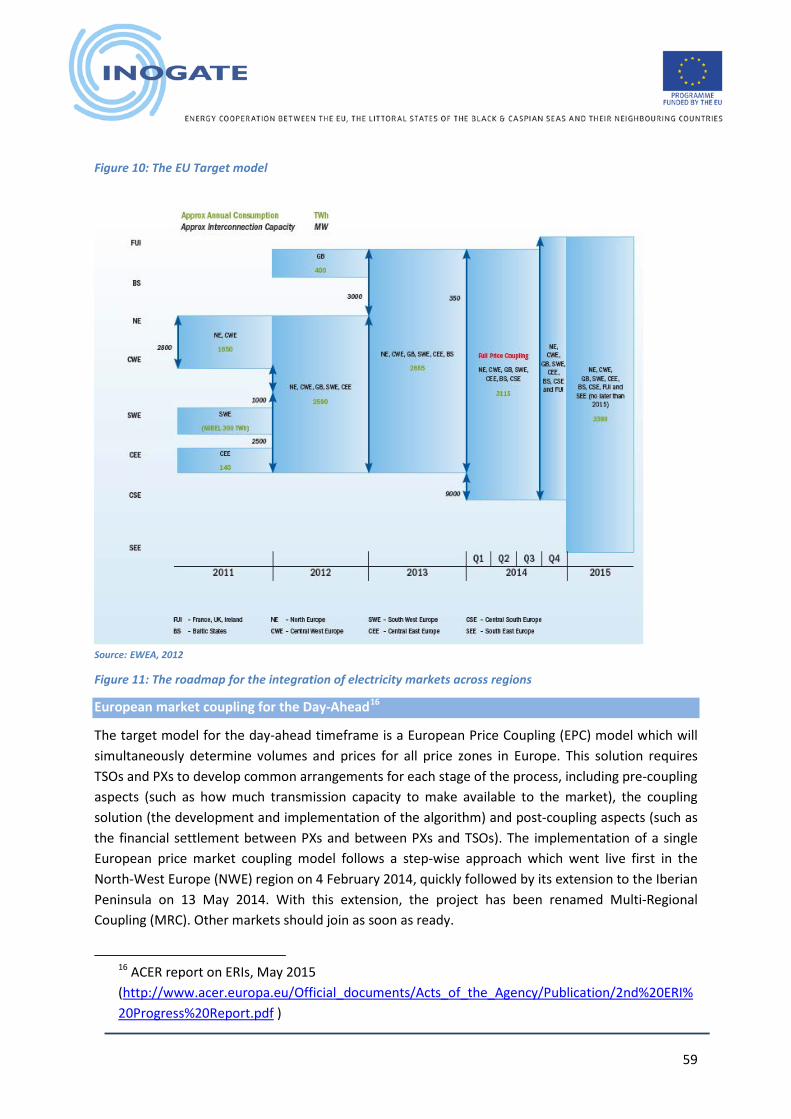

2.3.3.4 The Target Model for the EU electricity market ....................................................... 58

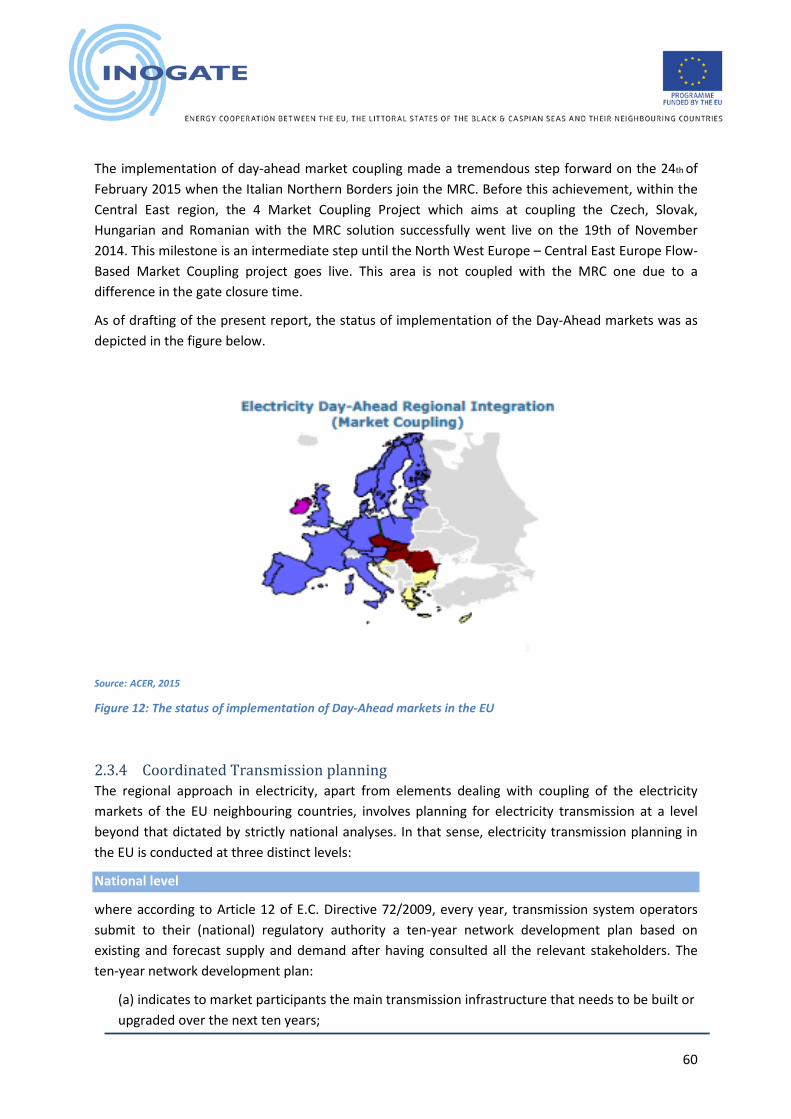

2.3.4 Coordinated Transmission planning .............................................................................. 60

2.4 THE ELECTRICITY MARKETS IN KAZAKHSTAN ........................................................................ 63

2.4.1 Electricity sector overview ............................................................................................ 63

2.4.1.1 The legal framework governing the electricity sector in Kazakhstan ....................... 63

2.4.1.2 Public authorities’ functions and powers in the area of electricity market operation and energy development .......................................................................................................... 63

2.4.1.3 Recent developments as regards the legal framework governing the electricity sector 64

2.4.1.4 Competition law and regulatory specificities in Kazakhstan ..................................... 64

2.4.2 The Kazakhstan’s Wholesale Electricity Market ............................................................ 64

2.4.3 Key challenges of the power sector in Kazakhstan ....................................................... 66

2.4.4 Gap analysis on the legal basis governing the Kazakh and EU electricity markets ....... 67

2.4.4.1 Key provisions of the EU Electricity Market .............................................................. 69

2.4.4.2 Gap Analysis .............................................................................................................. 72

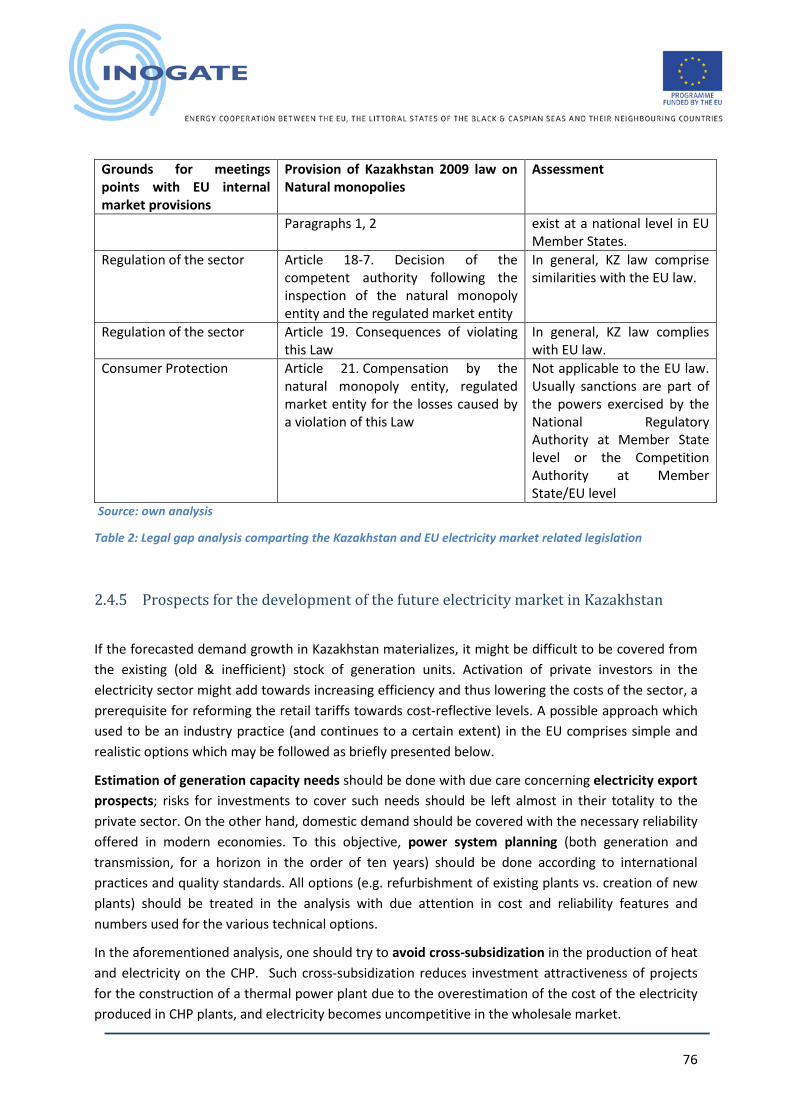

2.4.5 Prospects for the development of the future electricity market in Kazakhstan ........... 76

2.5 ELECTRICITY SECTOR INVESTMENTS UNDER A LIBERALISED MARKET REGIME .................... 78

2.5.1 Background .................................................................................................................... 78

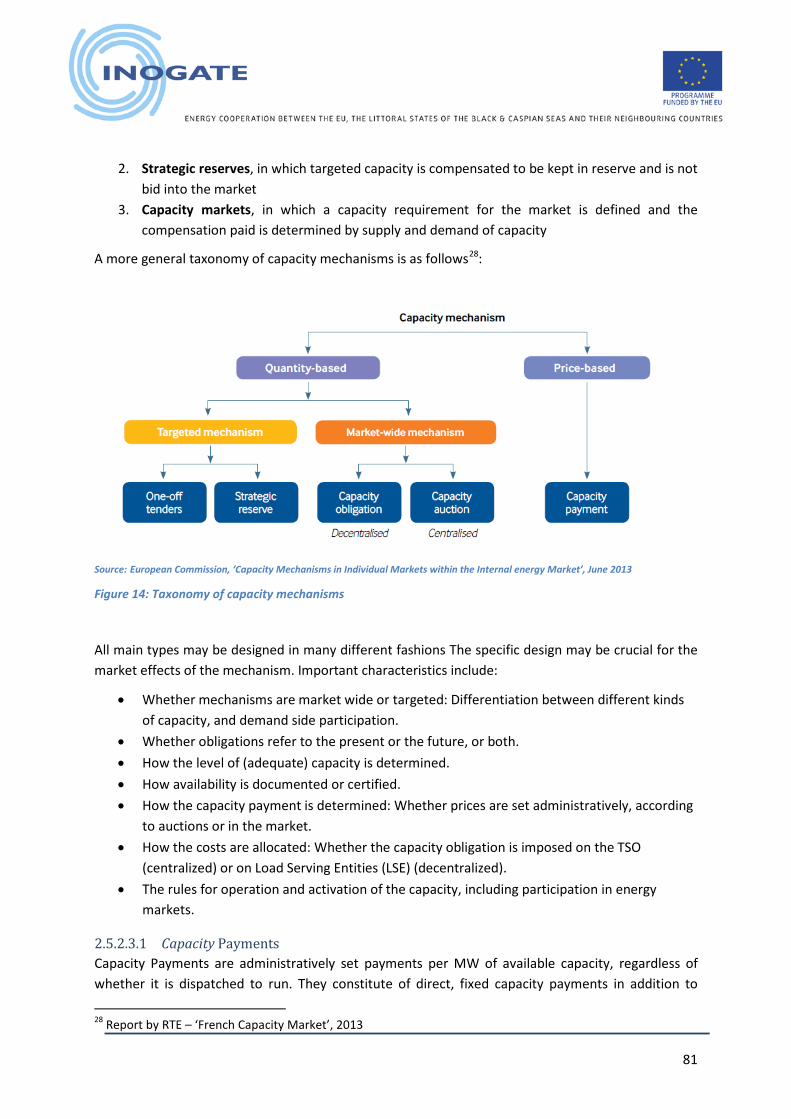

2.5.2 Investments in generation & Capacity support schemes .............................................. 79

2.5.2.1 New generation capacity in liberalized markets ....................................................... 79

2.5.2.2 Energy-only markets versus markets with capacity mechanisms ............................. 79

2.5.2.3 Capacity support schemes ......................................................................................... 80

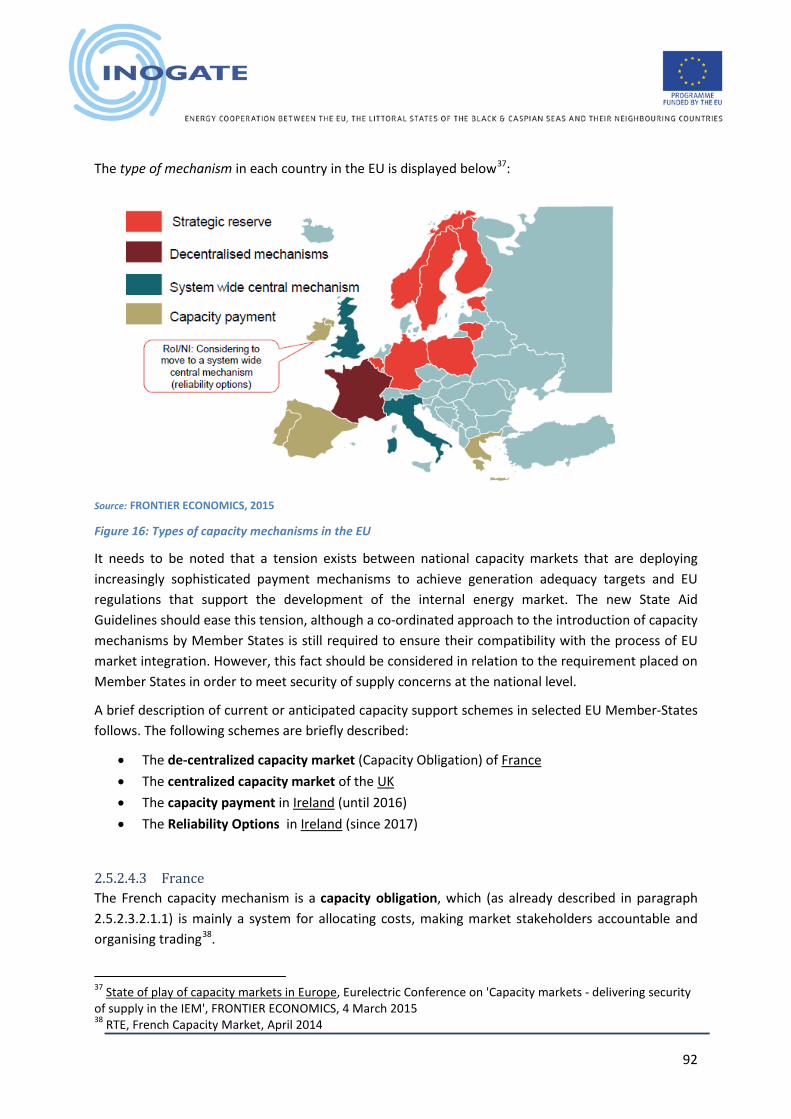

2.5.2.4 The EU experience ..................................................................................................... 87

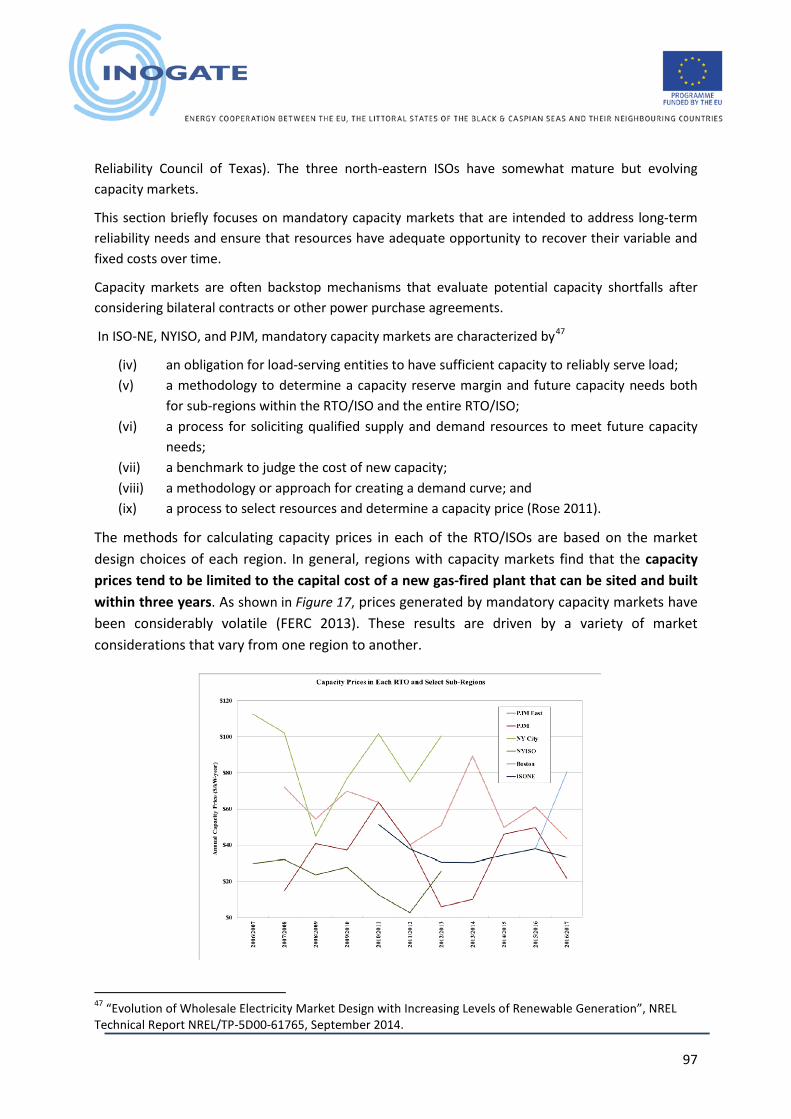

2.5.2.5 Experience in the USA ............................................................................................... 96

9

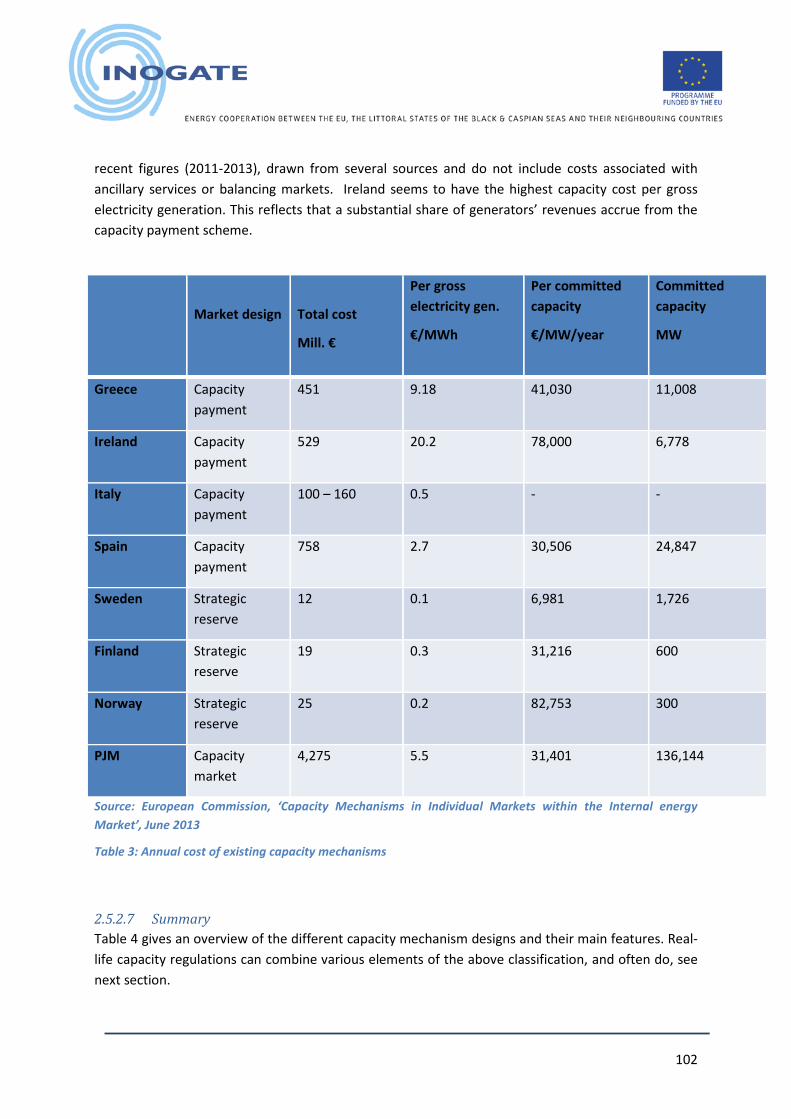

2.5.2.6 Annual cost of existing capacity mechanisms ......................................................... 101

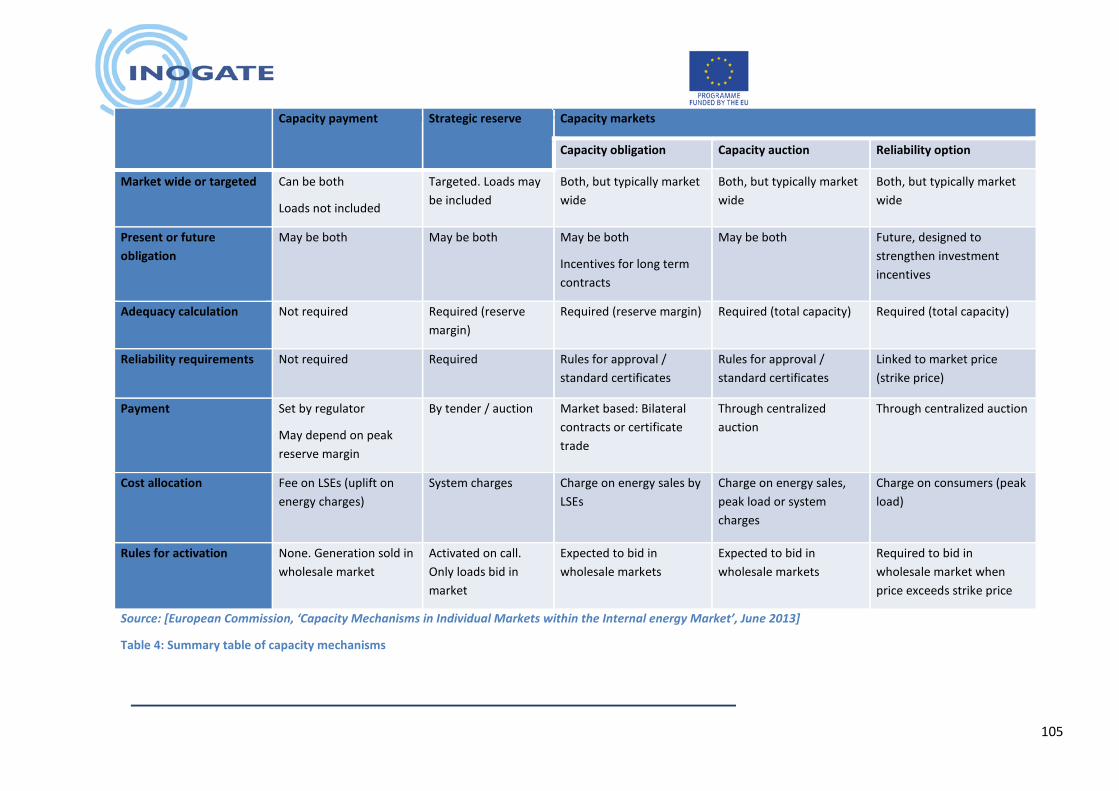

2.5.2.7 Summary.................................................................................................................. 102

2.5.3 Renewable Generation and Capacity Markets ............................................................ 106

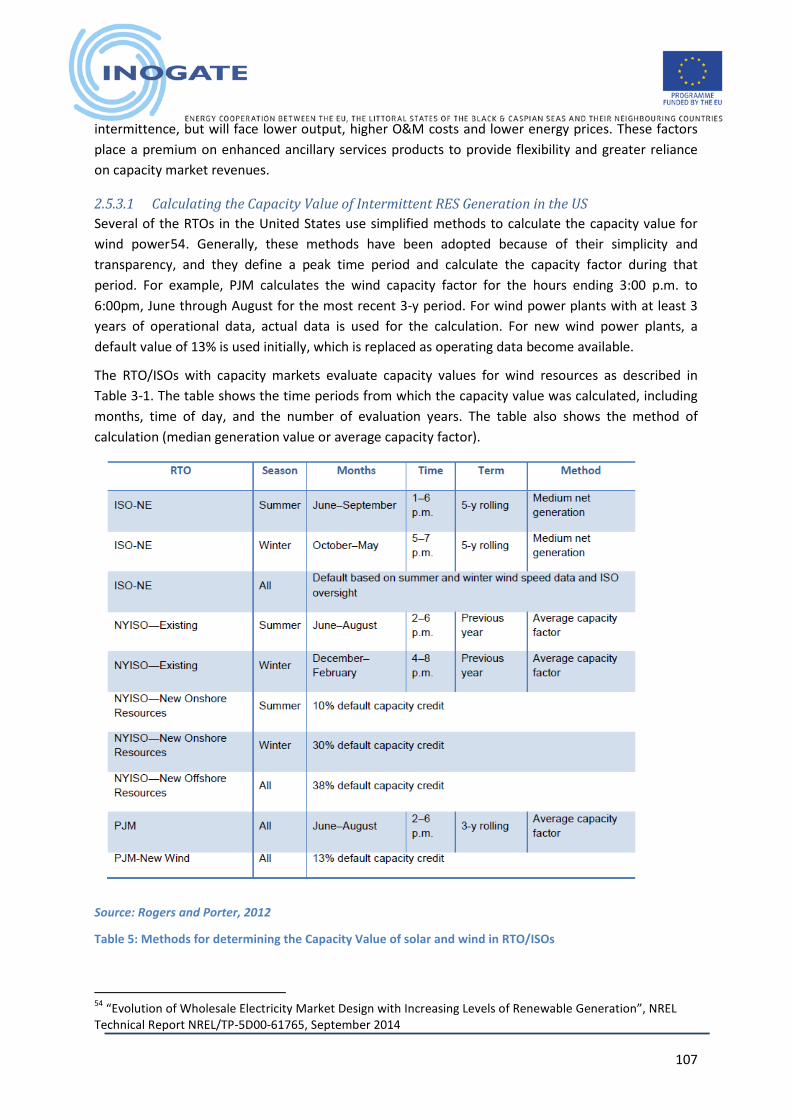

2.5.3.1 Calculating the Capacity Value of Intermittent RES Generation in the US ............. 107

2.5.3.2 The capacity-based RES support scheme in Russia ................................................. 108

2.6 Key Findings ......................................................................................................................... 113

2.7 Ownership and Benefits of the Activity ............................................................................... 114

2.8 SPECIFIC ISSUES AND RECOMMENDATIONS PERTINENT TO THE FUTURE DEVELOPMENT OF THE ELECTRICITY SECTOR IN KAZAKHSTAN ..................................................................................... 114

2.8.1 Technical, market and organizational aspects ............................................................ 114

2.8.1.1 Mandatory vs. non-mandatory participation in PX ................................................. 114

2.8.1.2 Interaction of capacity and energy markets: .......................................................... 115

2.8.1.3 CHP in participation in capacity markets................................................................. 115

2.8.1.4 CHP technologies able to participate in capacity mechanisms ............................... 119

2.8.1.5 Governance in the capacity market ........................................................................ 120

2.8.2 Legal aspects................................................................................................................ 121

2.8.2.1 The role and legal status of Power Exchanges in the EU ........................................ 121

2.8.2.2 Recommendations with regards to the implementation of a capacity market in Kazakhstan ............................................................................................................................... 126

2.9 REGIONAL MARKET OF CENTRAL ASIA ................................................................................ 133

2.10 Challenges Faced ................................................................................................................. 136

2.11 Impact .................................................................................................................................. 136

2.12 APPENDICES ......................................................................................................................... 137

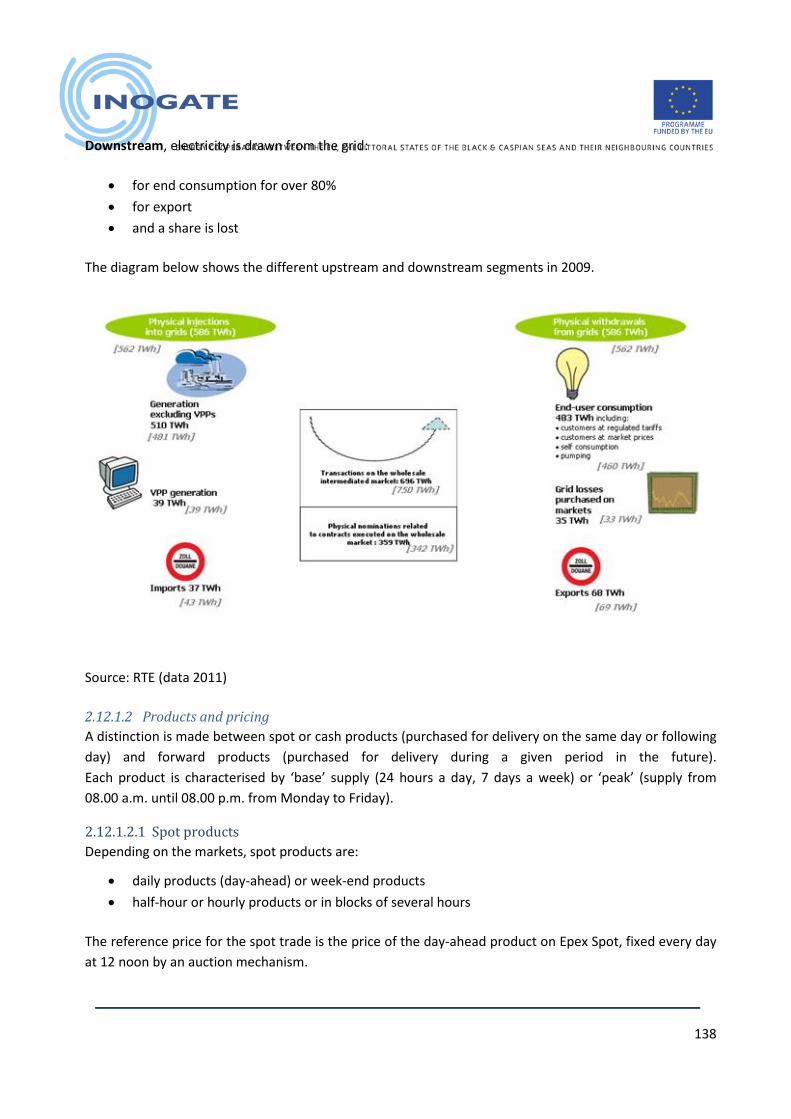

2.12.1 APPENDIX 1: EU Best Practices: Example of the French Wholesale Market / trading activities 137

2.12.1.1 Definition ............................................................................................................. 137

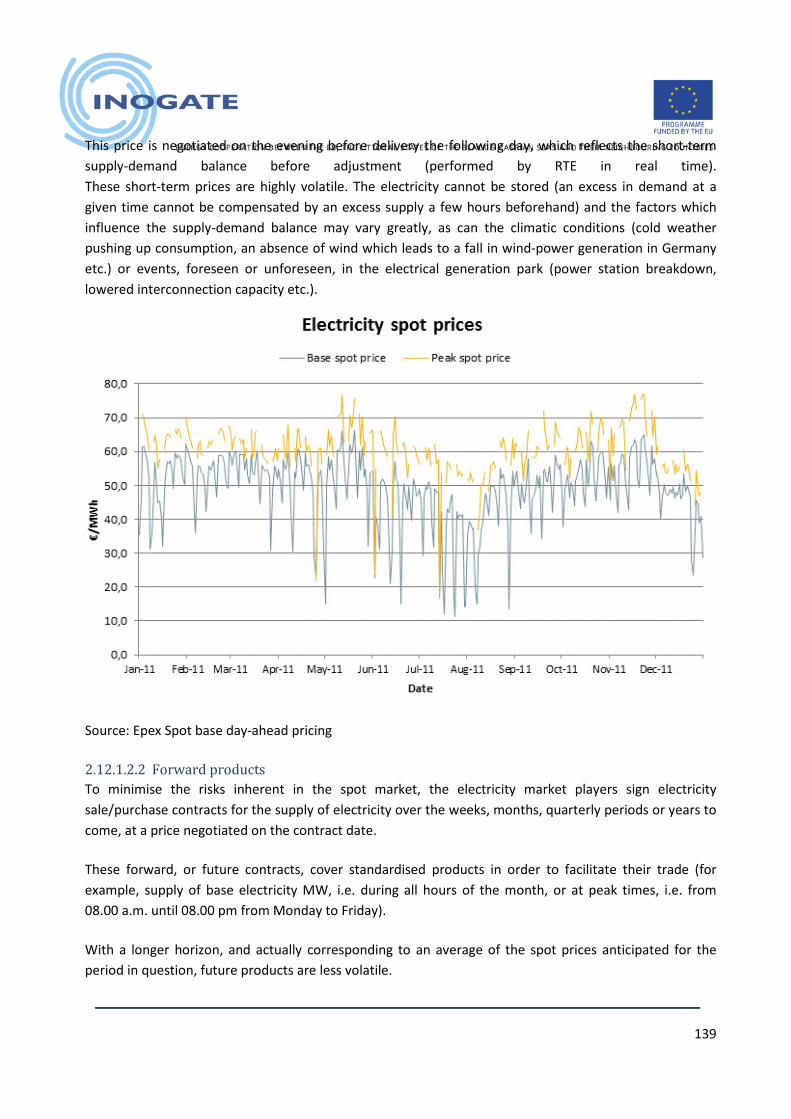

2.12.1.2 Products and pricing ............................................................................................ 138

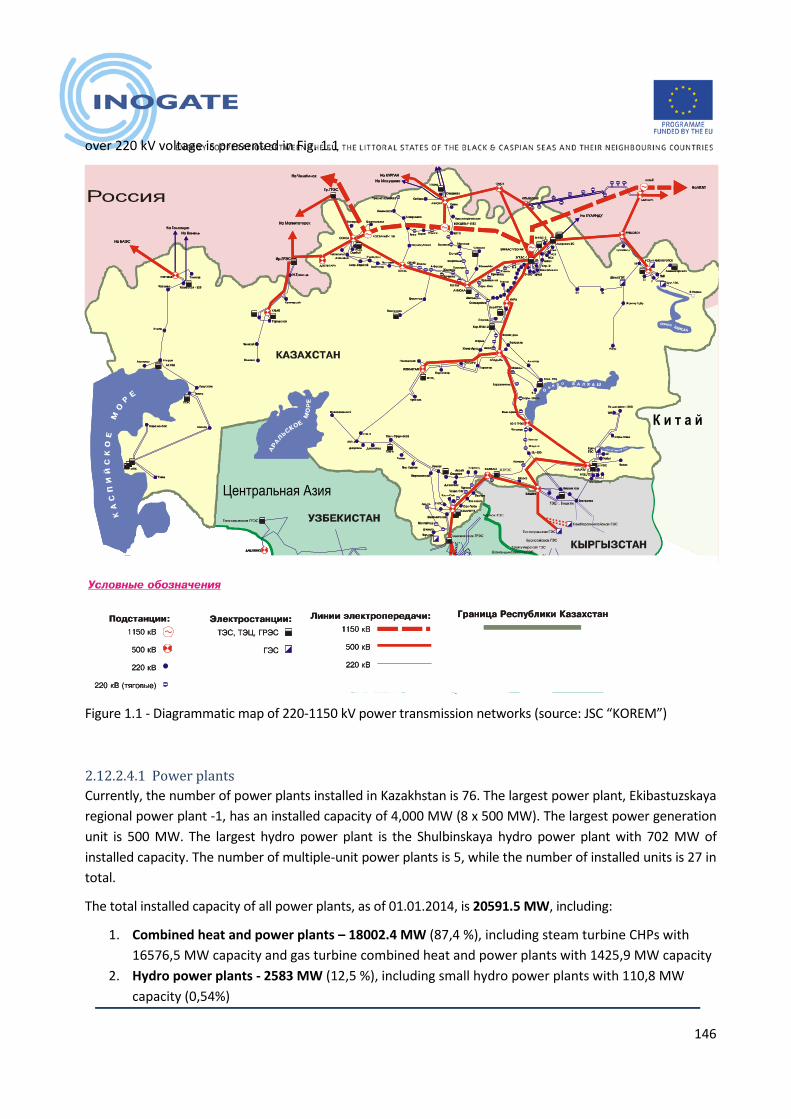

2.12.2 APPENDIX 2: Kazakhstan Electricity Sector Profile ...................................................... 142

2.12.2.1 Brief characteristics of the Republic of Kazakhstan ............................................ 142

2.12.2.2 State authorities vested with functions and powers in the area of functioning and development of the energy sector .......................................................................................... 142

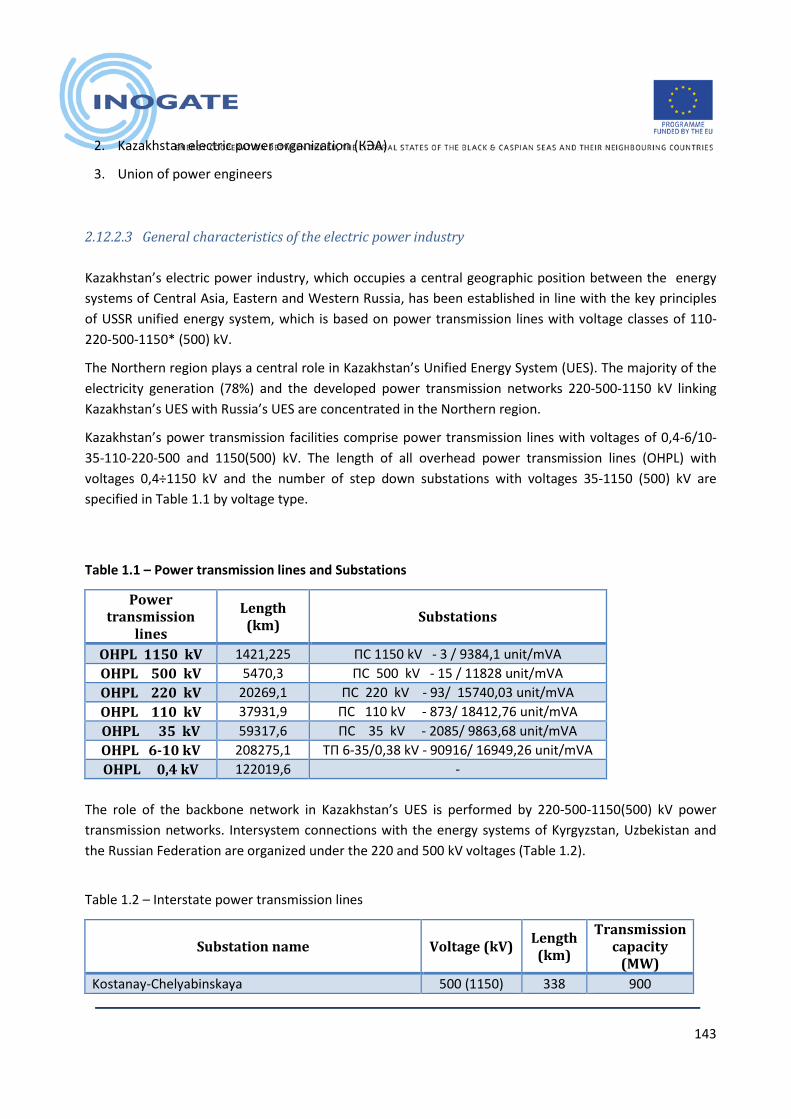

2.12.2.3 General characteristics of the electric power industry ....................................... 143

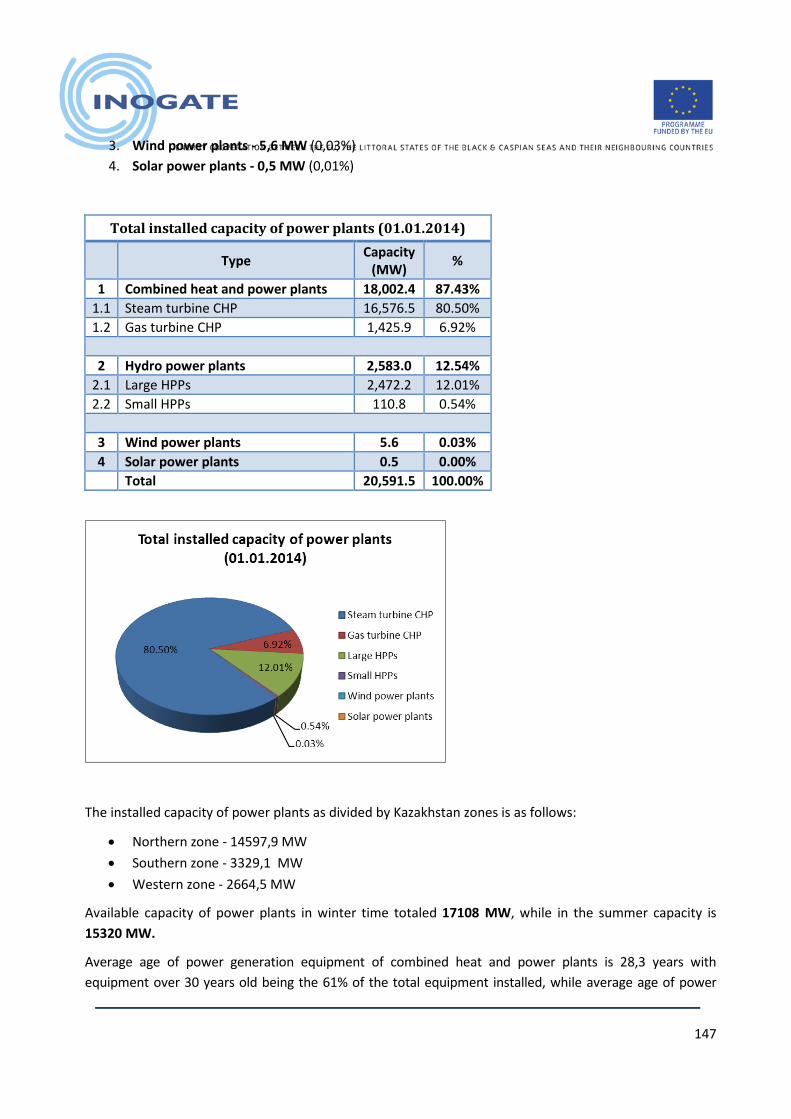

2.12.2.4 Current status of Kazakhstan electric power industry ........................................ 145

10

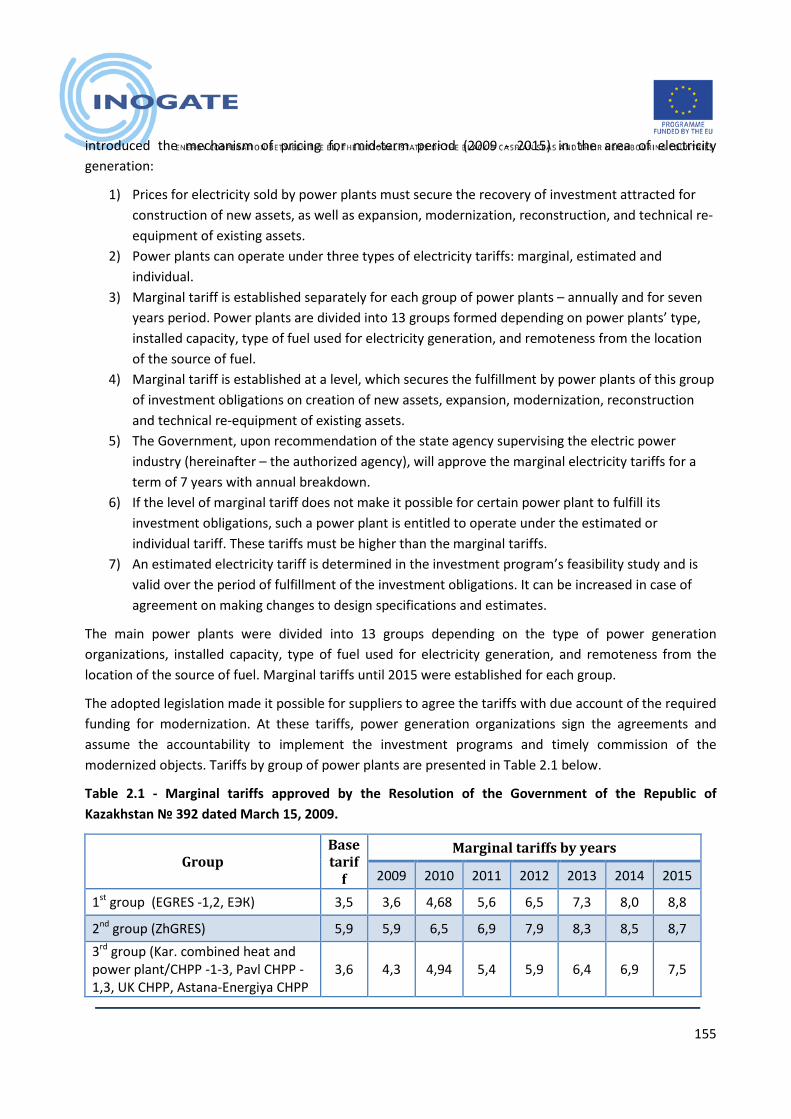

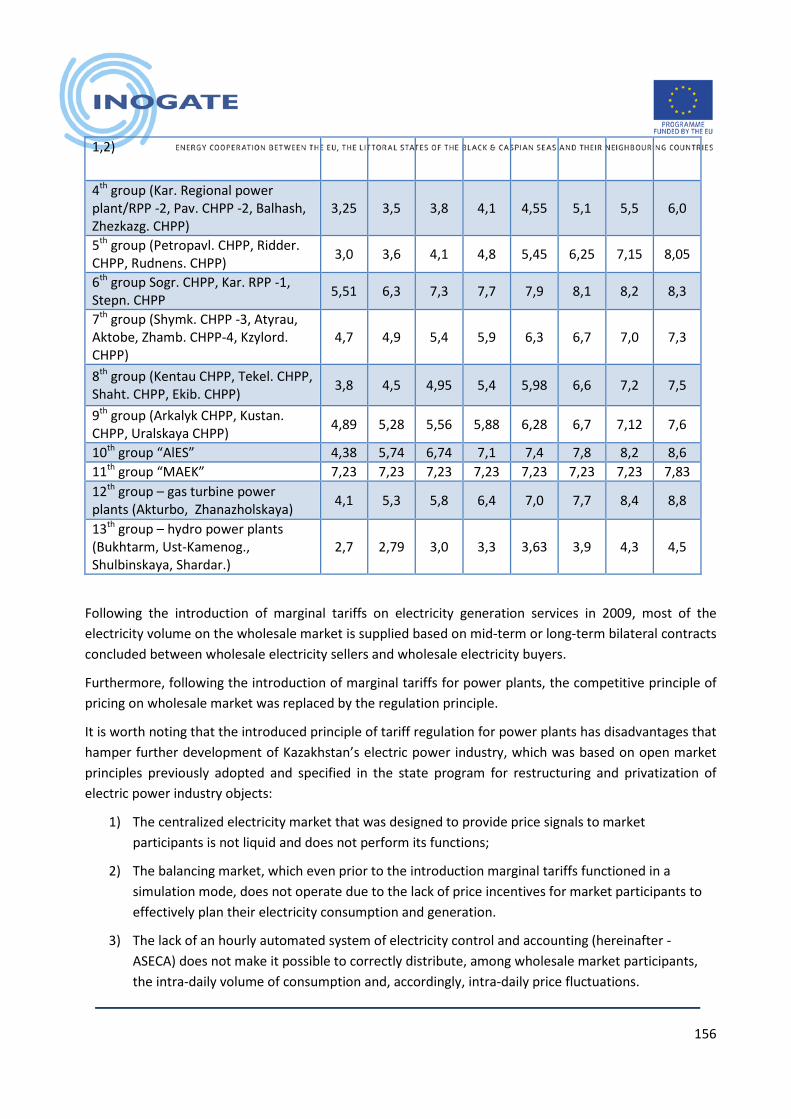

2.12.2.5 Existing Market Model and Tariff setting Principles ........................................... 151

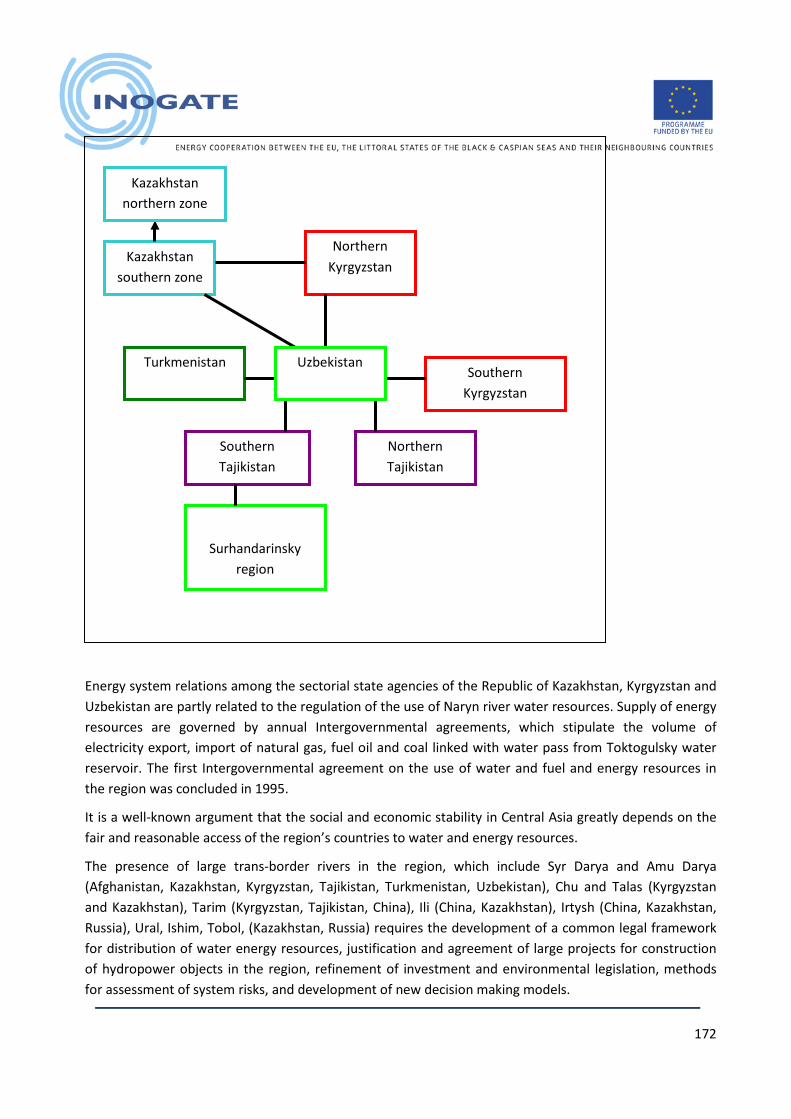

2.16.2.2 Brief description of parallel operation with energy systems of neighboring countries (Russia, Kyrgyzstan, Uzbekistan) ............................................................................. 171

3 BIBLIOGRAPHY ............................................................................................................................ 178

11

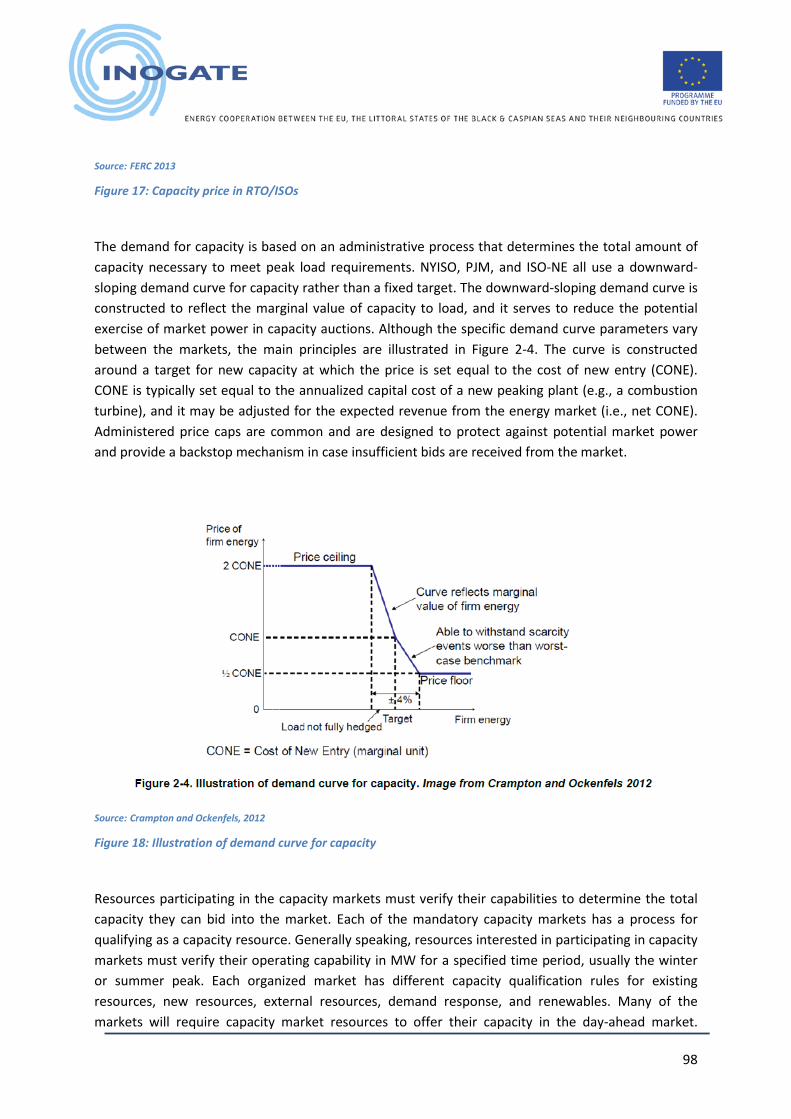

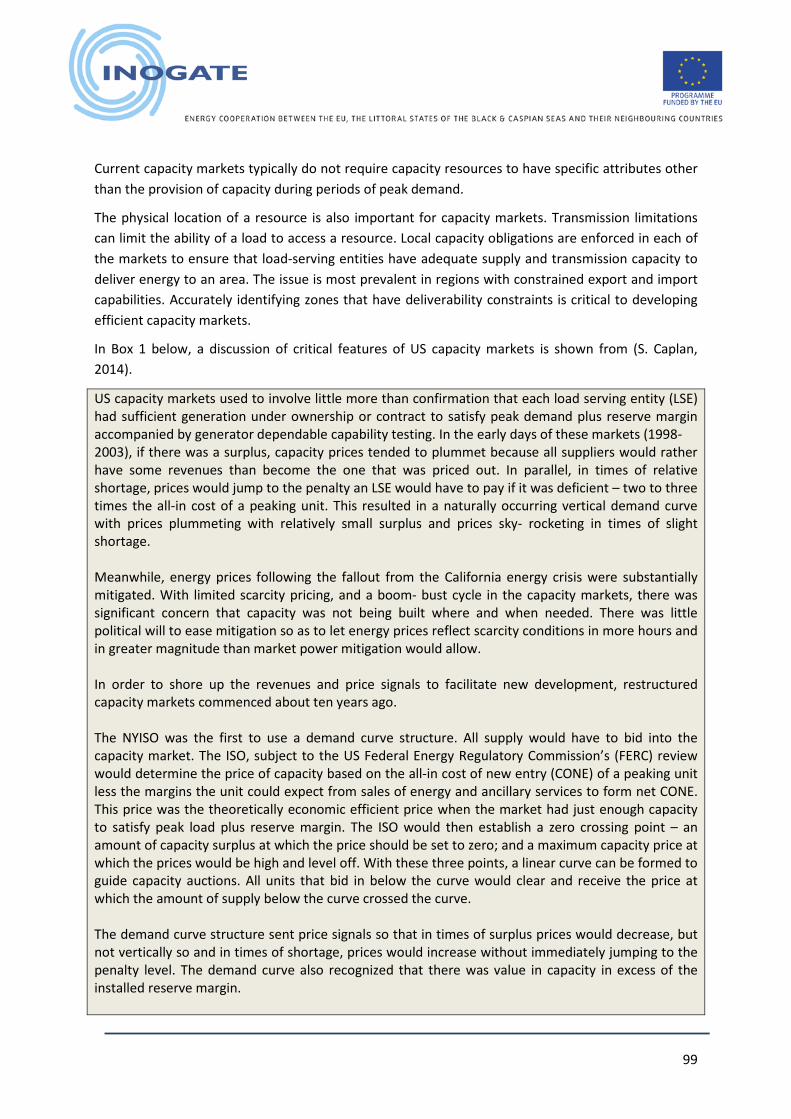

List of Figures: Figure 1: Price discovery - either at the intersection of demand and supply, two-sided pool (left) or supply .................................................................................................................................................... 32 Figure 2: Basic structure of an auction ................................................................................................. 35 Figure 3: Simple bid matching .............................................................................................................. 35 Figure 4: Electricity Markets Time-line .................................................................................................. 37 Figure 5: Bilateral or Decentralised model ............................................................................................ 39 Figure 6: Pool model and bilateral trade model .................................................................................... 40 Figure 7: The electricity market liberalisation time-line of the EU Directives ....................................... 42 Figure 8: Regional Initiatives- Elements of an organisational framework ............................................ 56 Figure 9: The final 7+1 regions in which “Regional Initiatives” were established ................................. 57 Figure 10: The EU Target model ............................................................................................................ 59 Figure 11: The roadmap for the integration of electricity markets across regions ............................... 59 Figure 12: The status of implementation of Day-Ahead markets in the EU .......................................... 60 Figure 13: The 6 Regions for which regional investment plans are prepared in the EU ........................ 62 Figure 14: Taxonomy of capacity mechanisms ..................................................................................... 81 Figure 15: Development stage and type of capacity mechanism in the EU .......................................... 91 Figure 16: Types of capacity mechanisms in the EU .............................................................................. 92 Figure 17: Capacity price in RTO/ISOs ................................................................................................... 98 Figure 18: Illustration of demand curve for capacity ............................................................................ 98 Figure 19: Installed cogeneration capacities in Europe in terms of fuel input .................................... 116 Figure 20: Generalised process diagram of an advanced type of CHP with fuel and operational flexibility .............................................................................................................................................. 118 Figure 21: Back-pressure versus extraction Steam Turbine types ....................................................... 120

List of Tables: Table 1: Questions and Answers on the third legislative package for an internal EU electricity market ............................................................................................................................................................... 49 Table 2: Legal gap analysis comparting the Kazakhstan and EU electricity market related legislation 76 Table 3: Annual cost of existing capacity mechanisms ....................................................................... 102 Table 4: Summary table of capacity mechanisms ............................................................................... 105 Table 5: Methods for determining the Capacity Value of solar and wind in RTO/ISOs ...................... 107

12

1 PART 1 – EUROPEAN COMMISSION

1.1 Background

Assignment Title: “Market Design Options of Kazakhstan and its Role in the Central Asia Regional Electricity Market”

Country and Dates: Kazakhstan, November 2014 –August 2015 Beneficiary Organisation(s): Ministry of Energy of the Republic of Kazakhstan, KOREM, CDC

Energia (International organisation based in Uzbekistan) Beneficiary Organisation’s key contact persons – name and e-mail address

Mr. Taltat Abilgazy, [email protected] Mr. Erjan Madiev, [email protected] Mr. Khamidilla Shamsiev, [email protected]

Deliverables Produced A report addressing the issues of internal market design for the electricity sector of Kazakhstan as well as a roadmap for the further development of electricity cooperation in Central Asia

Expert Team Members Nikos Tourlis, Task Leader, Energy Markets Expert Konstantinos Perrakis, Electricity (EU) Expert Emmanuelle Rault, Energy Law Expert Nikos Patsos, Energy Analyst Mariyash Zhakupova Local Electricity Expert

1.2 Essence of the Activity

The present report comprises the final deliverable of an assignment carried out under the Ad-Hoc Expert Facility (AHEF) of “INOGATE Technical Secretariat & Integrated Programme in support of the Baku Initiative and the Eastern Partnership energy objectives” project, funded by EC/Europeaid. Five applications for provision of Technical Assistance have been combined in this technical assistance assignment as they all shared common characteristics and comprised merits for addressing them collectively. The applications included:

• 89.KZ Study and analysis of experience in in development of power exchange trade in the countries of the Western Europe submitted by JSC "Kazakhstan Operator of Electricity Market" (JSC KOREM)

• 107.KZ Study and analysis of the existing models of electricity market in the countries of Europe, CIS and USA submitted by Ministry of Energy of the Republic of Kazakhstan

• 108.KZ Study and analysis of tariff setting in the area of electricity (production, transmission, supply) in the countries of Europe, CIS and USA

• 117.UZ Study and analysis of the existing models of electricity market in the countries of Europe, CIS and USA submitted by the International non-governmental organisations Central Dispatch Centre Energy

as they are filed under Component B: Electricity & Gas in the AHEF Registry. The assignment has been implemented over the period of November 2014 –August 2015.

13

1.2.1 Objectives of the study, key findings and recommendations According to the ToR the assignment had to work with the Ministry Energy on the strategic aspect of electricity sector development and future operation and KOREM on the tactical one of improving the market by analysing specific aspects and compare with the EU practices. It also involved the Ministry of Economy, KEGOC and the industry associations. In addition to the above the assignment also addressed with the cooperation of CDC Energia the regional dimension taking Kazakhstan as a reference and starting point.

The specific objectives of the task included:

For MINT:

• To get acquainted with the EU experience in regards of development and integration of electricity markets;

• To understand the distinction between competitive and regulated segments of the electricity sector and the manner that electricity composite prices/tariffs evolve in relation to these;

• To receive information on the mechanisms of achieving investments in a liberalised market environment, on who is responsible for planning and on how these investments are recovered;

For KOREM:

• To understand the distinction energy (i.e. forward, spot, balancing) and capacity markets; • To introduce the EU experience with regard to wholesale electricity market models and the

so-called Target Model; • To receive information on the nature and content of trading and settlement arrangements

that should exist in order to govern the relationships of the market participants;

For All Beneficiaries:

• To get acquainted with the EU experience with regard to cross border arrangements in the EU;

• To discuss whether these principles would be in whole or in part useful for developing a regional market in Central Asia.

14

1.3 Key Findings

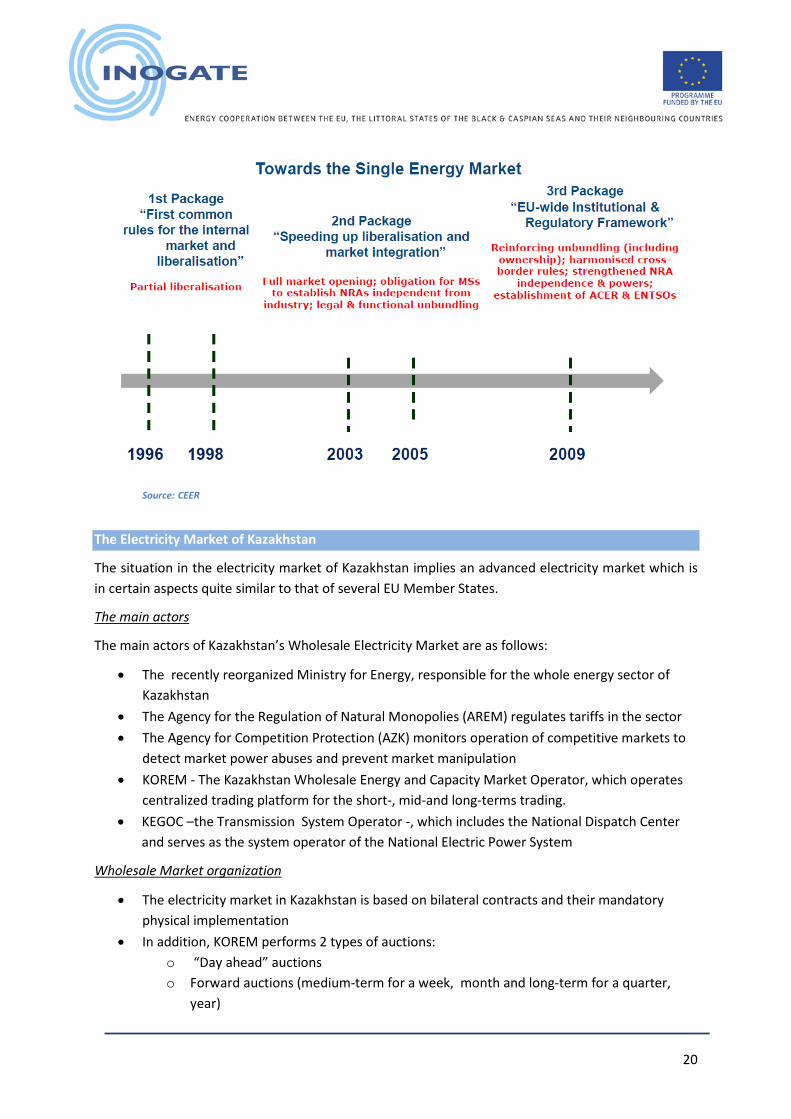

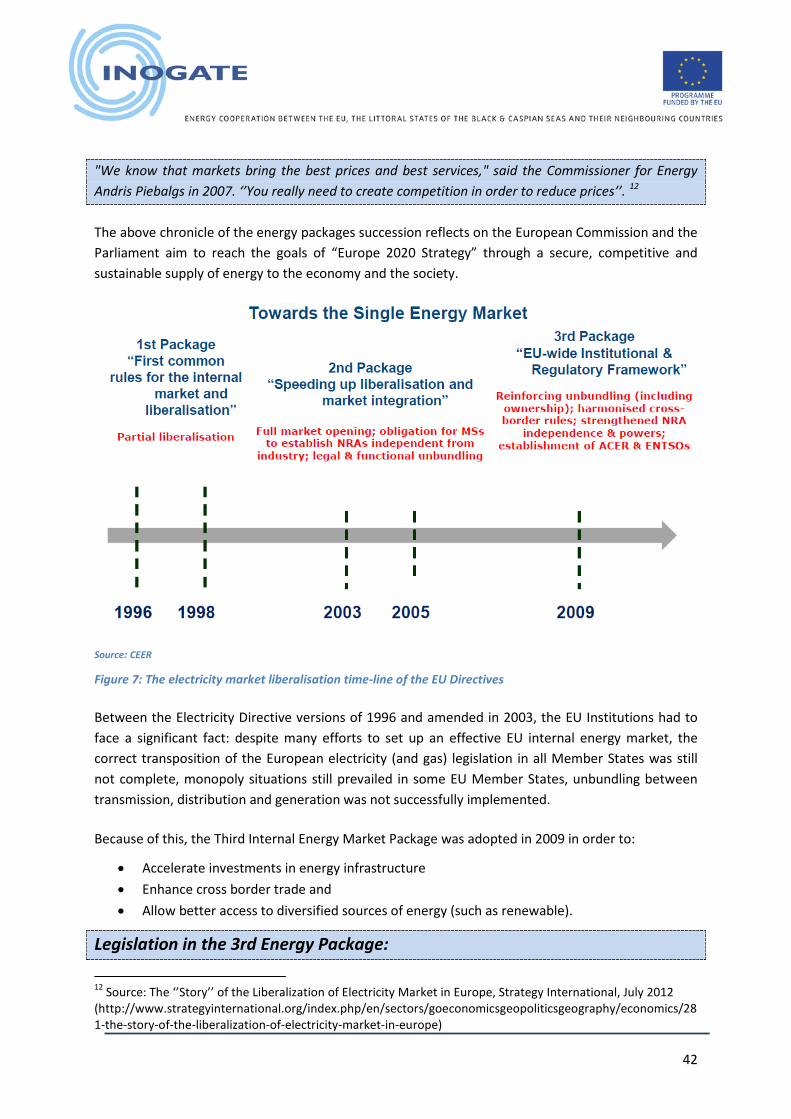

The EU Member States had to transpose the Electricity Directive 2009/72/EC, which are a fundamental part of the Third Energy Package, by 3 March 2011 and to apply them from that date. The Electricity Directive set out key rules necessary for a proper functioning of the electricity market. The new or reinforced requirements concerning the unbundling of networks, the independence and the powers of national regulators and the functioning of retail markets via enhanced consumer protection measures represent major developments compared to the provisions of the Second Energy Package adopted in 2003. Important rules for the operation of the markets are also set out in the Electricity Regulation (EC) No 714/2009, also part of the Third Energy Package and applicable as from 3 March 2011.

Unbundling within energy markets refers to the unbundling of vertically integrated structures. The unbundling of generation, transmission, distribution and retail sales has an important role within the electricity market with regard to the implementation of competition. The inclination towards the unbundling of the transmission and distribution operations, which are referred to as network operations and which, as already mentioned, carry natural monopoly characteristics, from generation and retail sales activities, is based on the concern that the dominant undertaking may limit in various ways the access of other undertakings that it is competing with in generation and retail sales areas.

The above activities, initiatives and legislative framework resulted to the adoption of a ‘target model’ for the electricity sector in the EU.

The European Electricity Regulatory Forum (Florence Forum) decided in November 2008 to establish a Project Coordination Group of experts drawn from the European Commission, regulators, and relevant stakeholders, to develop an EU-wide Target Model (TM) and a roadmap for the integration of electricity markets across regions. The tasks were to develop a practical and achievable model for the harmonization of co-ordinated EU-wide transmission capacity allocation, to manage congestions and to propose a roadmap with concrete measures for the integration of forward, day-ahead, intraday and balancing markets – including governance issues.

In energy-only market designs, the (only) traded commodity is electricity (MWh/h). In such markets, the supplying companies get revenues only by selling electricity, either in organized wholesale markets and/or through bilateral contracts with customers. The companies recover capital and fixed costs of power generation because the selling prices or the wholesale market prices turn out to be higher than the variable costs (mostly fuel costs) of power generation, either continuously or periodically, but in a sufficient number of hours. Generation capacity adequacy is supposed to be derived from the resulting market dynamics. Moreover, scarcity pricing ensures revenues to cover capital cost of peak (and other) generation capacity.

By contrast, market designs with explicit capacity mechanisms recognize two market commodities, namely electricity (the output) and generation capacity (the means). Introducing capacity mechanisms imply that generators receive payments for the mere availability of capacity in addition to revenues obtained from the energy market. One might say that in a market with an explicit capacity mechanism the energy market is still the main instrument for short term optimization of

15

resources, while the capacity mechanisms is the main instrument for long term development of generation capacity.

1.4 Ownership and Benefits of the Activity

Despite the fact that the “missing money problem” has not yet hit the Kazakh wholesale electricity market, the Ministry of Energy considers establishing capacity support mechanisms. On the other hand the Market Operator of Kazakhstan evaluates different market design features with a view to propose amendments/improvements to the current market design in Kazakhstan. These include the mandatory vs voluntary participation of market actors to the Power Exchange, the impact of participation of the CHP generation to the capacity support mechanism as well as generally the enhancement of the role of the PX in the wholesale electricity market. On top of these issues which concern only Kazakhstan as the most advanced and important (in terms of its size) electricity market in the Central Asian region, INOGATE has always been looking to enhance and support the central role of Kazakhstan on the creation of a regional Central Asia electricity market. These interlinked objectives have led to the combination of the originally distinct applications for technical assistance. The results can be viewed as a knowledge base enhancement which may under appropriate circumstances and with the support of other international development partners working in Kazakhstan translate into reforms and eventually the creation of a regional electricity market.

1.5 Recommendations

Capacity Mechanisms and the lessons learnt for Kazakhstan

Capacity mechanisms are set up in order to remedy to the risk of insufficient electricity generation, it is normally opened to both existing and new generation plants.

The ultimate goal of the introduction of capacity market mechanisms is to ensure the security of supply and benefit the end users has regards both the security of supply and cost -reflective tariffs.

The introduction of capacity market mechanisms must be assessed according to two main objectives:

• Foster and incentivise investment in power generation and • Ensure a better control of the electricity demand, especially during peak hours

These objectives being met, any country setting up a capacity market should be able to secure its supply. However, the introduction of capacity market mechanisms has inevitably an effect on the balance of power market and on its competition/openness level.

Therefore, one should take into account a number of risks and challenges affecting the deployment of a sustainable and opened electricity market:

• The introduction of a capacity market can have the consequence to strengthening the market position of dominant operators and exclude the possibility of entrance of new players on the market. The energy and competition regulatory framework need to be given sufficient

16

monitoring and sanction powers in order to ensure fair competition and avoid market dominance behaviour.

• Any dominant or strong market player should be particularly monitored by the regulator in order to avoid further market dominance (as for example, by holding certificates in order to create an unbalance of the certificate markets and ensure higher certificates trading prices)

• The evaluation of the capacity needs should take into account opportunities connected to the interconnection system and the import of electricity. These will affect positively the security of supply and the volume of electricity import should be taken into account

• Protection of equality of treatment among operators is key in order to avoid predatory behaviour from dominant market players

• The cost of capacity market certificates should be included in the calculation of regulated tariffs

• The possibility to launch tender for new capacity needs to be assessed vs. investment in new generation capacity which would have occurred in a traditional market

The Central Asia Regional Electricity market – A roadmap

In the centrally planned era the regional electricity flow in the Central Asia Region used to be part of a wider economic planning context. Electricity, water, cotton, fuels and other commodities where exchanged year-round in an area which used to be part of a single state. With the collapse of the Soviet Union the re-scheduled deliveries were hard to be matched as commodities and were now produced by different counties under different conditions. The history is more or less known and what is important to be highlighted is that the electricity flows in the region have gradually and steadily been decreasing in an area where the hydro-thermal cooperation would be beneficial - as it used to be in the past but nowadays even more due to the technological advancements.

Kazakhstan beyond any doubt comprises an important player in the future market –primarily due to its market size and level of advancement – but it is rather unlikely that it could catalytically lead the process in which the rest of the partners are not convinced to follow.

As far as the Roadmap for the development of the Regional Central Electricity Market is concerned, in the views of the ITS team this can for the time being define general directions but for the detailed milestones to be accurately defined would require all prerequisites to be in place. Instead of a full-defined Roadmap the one proposed below describes the necessary prerequisites for a process to be set up in order to guide the development. Perhaps the discussions at international level would be able to support and facilitate a process such as the one briefly described below:

17

1.6 Challenges Faced

One of the biggest challenges faced in the present assignment had to do with the considerable gap of the EU and Kazakh legislation with respect to the organisation and operation of the energy sector generally. While the organisation of the electricity market of Kazakhstan is in many ways similar to several EU countries the primary legislation is way too generic in comparison to the 3rd Energy Package. Some of the reported issues in the electricity market have also direct relevance to competition legislation and we assume that this might not only lead to unique considerations in the electricity sector but might probably affect the Kazakh economy as a whole.

Another challenge had to do with the infrequent exchange of experiences between Kazakhstan and the EU. Kazakhstan being a member of the Euro-Asian Economic Union is determined to integrate its electricity market with the other members of the union and this does not entail compliance to the EU Acquis. It is therefore rather difficult to identify and propose solutions of the reform of certain segments of the electricity markets in an isolated manner.

Last but not least, the development of cross border electricity infrastructure in Central Asia has both shifted the centre of gravity to countries that fall beyond the regional group of five Central Asian ex-soviet union countries while it currently has little in common with the regulatory framework adopted in Europe for the development of key energy infrastructure.

1.7 Impact Matrix

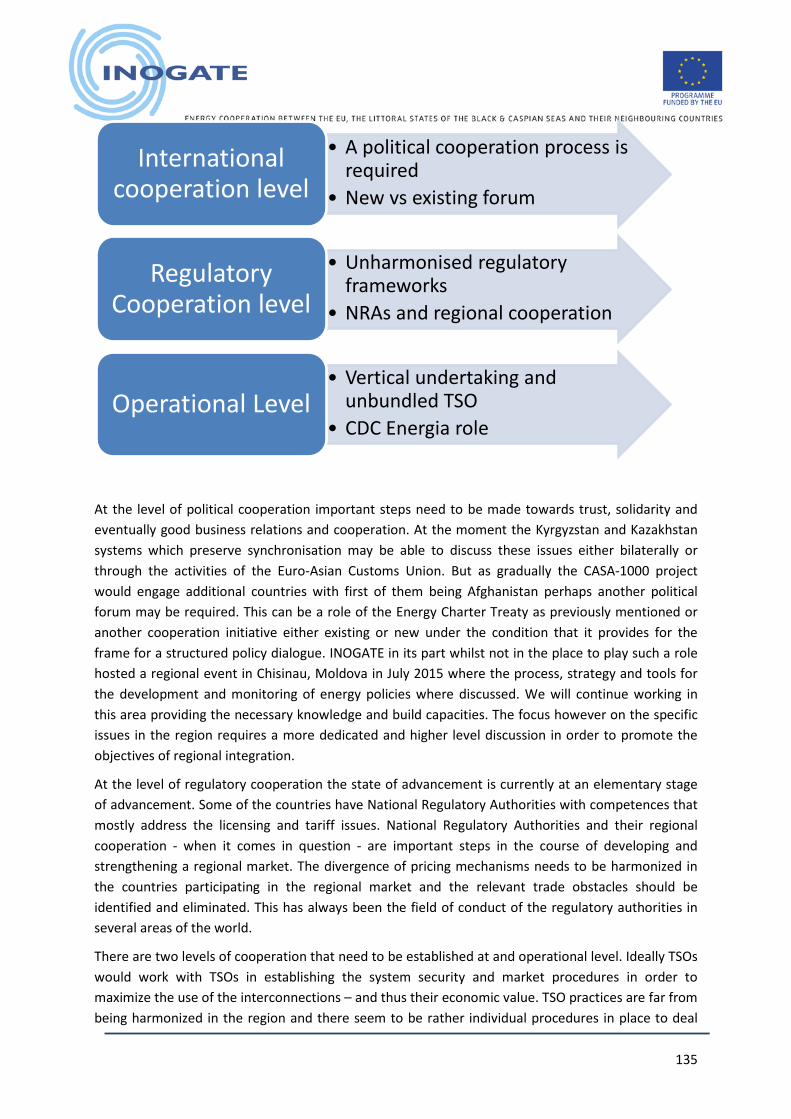

The main role of this assignment was to raise awareness of key decision makers in the Kazakh electricity market. It is understood that several lessons learnt as well as the terminology, taxonomy

• A political cooperation process is required

• New vs existing forum

International cooperation level

• Unharmonised regulatory frameworks

• NRAs and regional cooperation

Regulatory Cooperation level

• Vertical undertaking and unbundled TSO

• CDC Energia role Operational Level

18

and principles of the EU electricity markets might serve as an important background and basis for further thinking on questions that might appear to be in their essence similar to those discussed in this report. We hope that reform process in the electricity sector of Kazakhstan will continue with the support of other international development partners and this will also include the objectives of the creation of a regional electricity market. Looking at this work from a different perspective we hope that part of this analysis will be useful to any party that is interested in the Kazakh electricity market irrespectively of the viewpoint (EU or non-EU reader).

19

2 PART 2 - BENEFICIARIES

2.1 Executive Summary

Liberalisation of the Electricity Markets and the EU

The recent economic appreciation of the network industries in general and within them the electricity supply industry continues to recognise the merits of monopoly but only with regards to the networks i.e. proposing that inefficiencies of the monopoly are less than the avoided cost of spontaneous network investment and that allocative efficiencies may be achieved by introducing competition to the generation and supply segments. The high cost of electricity networks (both at transmission and distribution level) can make it efficient to have a single supplier of network services in a particular geographic area, leading to a natural monopoly industry structure. In addition, the electricity networks are regulated to manage the risk of monopoly pricing, where a business can charge higher prices or provide poorer services compared with the situation in a competitive market. Thus, even in the liberalized electricity sector, network tariffs are not determined by market forces: because each network is a monopoly and so market forces cannot be relied upon to provide efficient prices.

The EU Member States had to transpose the Electricity Directive 2009/72/EC, which are a fundamental part of the Third Energy Package, by 3 March 2011 and to apply them from that date. The Electricity Directive set out key rules necessary for a proper functioning of the electricity market. The new or reinforced requirements concerning the unbundling of networks, the independence and the powers of national regulators and the functioning of retail markets via enhanced consumer protection measures represent major developments compared to the provisions of the Second Energy Package adopted in 2003. Important rules for the operation of the markets are also set out in the Electricity Regulation (EC) No 714/2009, also part of the Third Energy Package and applicable as from 3 March 2011.

20

Source: CEER

The Electricity Market of Kazakhstan

The situation in the electricity market of Kazakhstan implies an advanced electricity market which is in certain aspects quite similar to that of several EU Member States.

The main actors

The main actors of Kazakhstan’s Wholesale Electricity Market are as follows:

• The recently reorganized Ministry for Energy, responsible for the whole energy sector of Kazakhstan

• The Agency for the Regulation of Natural Monopolies (AREM) regulates tariffs in the sector • The Agency for Competition Protection (AZK) monitors operation of competitive markets to

detect market power abuses and prevent market manipulation • KOREM - The Kazakhstan Wholesale Energy and Capacity Market Operator, which operates

centralized trading platform for the short-, mid-and long-terms trading. • KEGOC –the Transmission System Operator -, which includes the National Dispatch Center

and serves as the system operator of the National Electric Power System

Wholesale Market organization

• The electricity market in Kazakhstan is based on bilateral contracts and their mandatory physical implementation

• In addition, KOREM performs 2 types of auctions: o “Day ahead” auctions o Forward auctions (medium-term for a week, month and long-term for a quarter,

year)

21

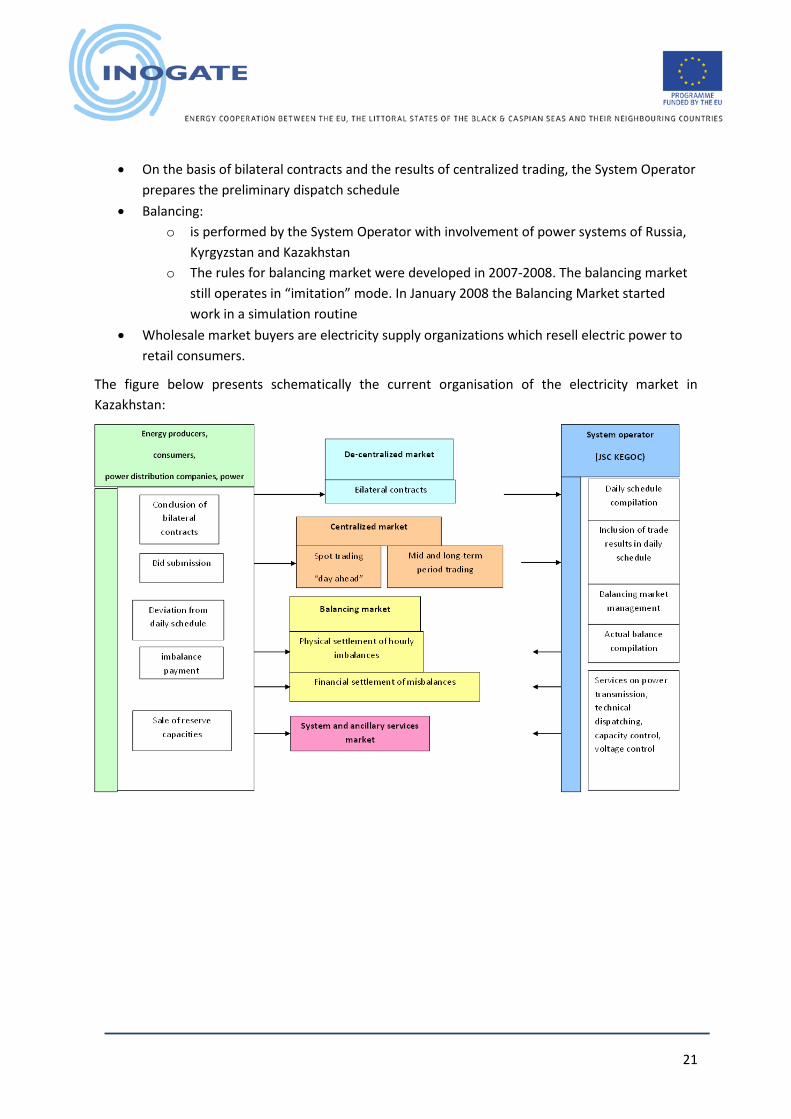

• On the basis of bilateral contracts and the results of centralized trading, the System Operator prepares the preliminary dispatch schedule

• Balancing: o is performed by the System Operator with involvement of power systems of Russia,

Kyrgyzstan and Kazakhstan o The rules for balancing market were developed in 2007-2008. The balancing market

still operates in “imitation” mode. In January 2008 the Balancing Market started work in a simulation routine

• Wholesale market buyers are electricity supply organizations which resell electric power to retail consumers.

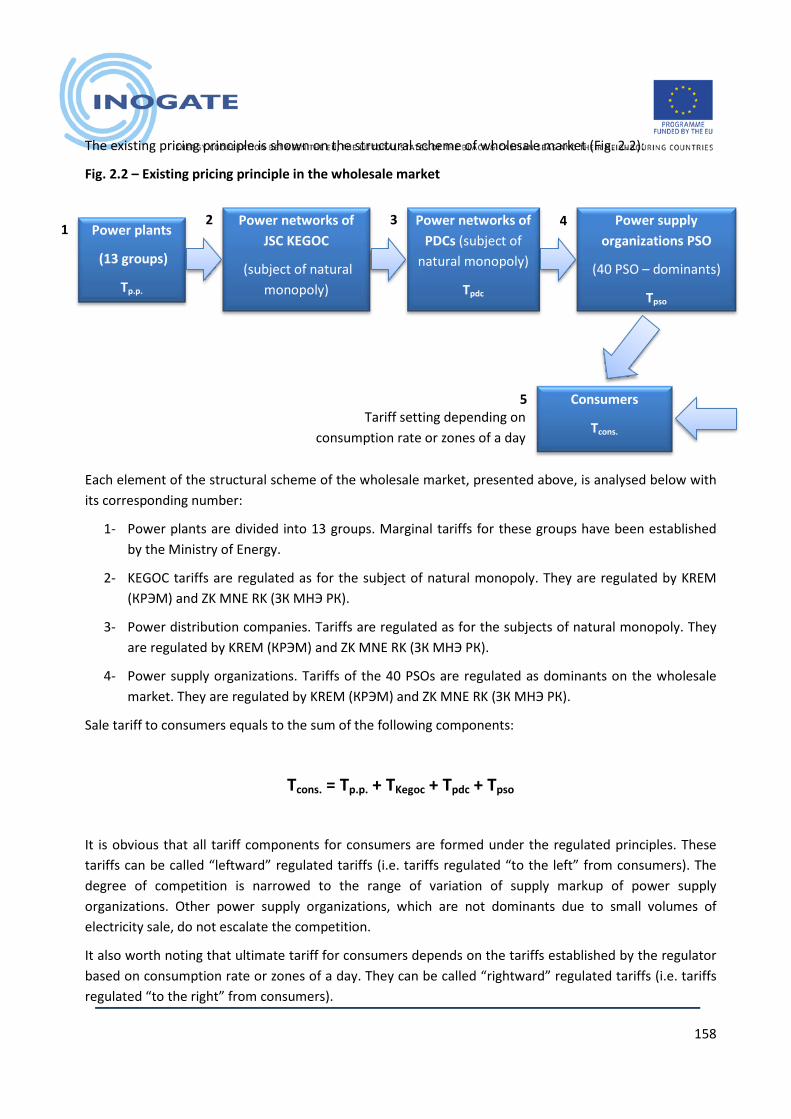

The figure below presents schematically the current organisation of the electricity market in Kazakhstan:

22

Challenges in regards to the future development of the electricity sector in Kazakhstan and key recommendations

During our review of the electricity sector of Kazakhstan we have identified a number of deviations from the current EU status quo; the electricity demand is increasing at a constant pace in Kazakhstan, centralised planning is not adequately consulted with the relevant stakeholders (or at least the ITS team has not been able to find this documented), electricity tariffs transparency and their effect on competition is rather different compared to the practices of most EU Member States. Last but not least, the role, responsibilities and authorities of National Energy Regulatory Authorities are spread among several governmental authorities. In this context the section below presents some high level recommendations which in the ITS team of experts’ opinion need to be discussed at national level.

Estimation of generation capacity needs should be done with due care concerning electricity export prospects; risks for investments to cover such needs should be left almost in their totality to the private sector. On the other hand, domestic demand should be covered with the necessary reliability offered in modern economies. To this objective, power system planning (both generation and transmission, for a horizon in the order of ten years) should be done according to international practices and quality standards. All options (e.g. refurbishment of existing plants vs. creation of new plants) should be treated in the analysis with due attention in cost and reliability features and numbers used for the various technical options.

In the aforementioned analysis, one should try to avoid cross-subsidization in the production of heat and electricity on the CHP. Such cross-subsidization reduces investment attractiveness of projects for the construction of a thermal power plant due to the overestimation of the cost of the electricity produced in CHP plants, and electricity becomes uncompetitive in the wholesale market.

Tariffs and revenue collection should ensure the viability of the system. Subsidisation of specific categories of consumers (low income, remote areas, etc.) should be explicitly calculated and included either in the tariffs or through appropriate financial subsistence (provided either to the electricity sector -generators, network companies- or outside of the electricity market). In both the latter options, the expenses should be covered from the public budget and foreseen on an annual basis or equivalently each regulatory period.

Unbundling of accounts (e.g. for energy, for reserves, for transmission, for distribution, for system operation, etc.) should be also a priority, given that such unbundling will help identify inefficiencies in a much easier and transparent way.

Benchmarking of the costs of the various categories in the electricity market should be performed often (e.g. on a 2 years basis) according to international standards and with participation of accredited accounting firms.

New capacity should be procured according to auctions, in quantities as they are calculated based on the aforementioned long-term plan. PPAs are considered to be an appropriate approach at the current state of the market.

A comprehensive and efficient market monitoring system should be established. Market monitoring reports should be produced on a 3-month and yearly basis.

23

In addition, assigning the monitoring and regulation function of the electricity (and heat) sector in one body might add to efficiency in the operation of the sector. More specifically, the integration of responsibilities that now belong to AREM (Agency for the Regulation of Natural Monopolies, mainly regulating tariffs) and AZ K (The Agency for Competition Protection which monitors operation of competitive markets) will improve the capabilities of the singe institution to detect market power abuses and prevent market manipulation. Such a regulatory body would, for example approve the power system development plans (both generation and transmission) which should be in turn developed by KEGOC in collaboration with the regional transmission companies.

Capacity Mechanisms and the lessons learnt for Kazakhstan

Capacity mechanisms are set up in order to remedy to the risk of insufficient electricity generation, it is normally opened to both existing and new generation plants.

The ultimate goal of the introduction of capacity market mechanisms is to ensure the security of supply and benefit the end users has regards to both the security of supply and cost -reflective tariffs.

The introduction of capacity market mechanisms must be assessed according to two main objectives:

• Foster and incentivise investment in power generation and • Ensure a better control of the electricity demand, especially during peak hours

These objectives being met, any country setting up a capacity market should be able to secure its supply. However, the introduction of capacity market mechanisms has inevitably an effect on the balance of power market and on its competition/openness level.

Therefore, one should take into account a number of risks and challenges affecting the deployment of a sustainable and opened electricity market:

• The introduction of a capacity market can have the consequence to strengthening the market position of dominant operators and exclude the possibility of entrance of new players on the market. The energy and competition regulatory framework need to be given sufficient monitoring and sanction powers in order to ensure fair competition and avoid market dominance behaviour.

• Any dominant or strong market player should be particularly monitored by the regulator in order to avoid further market dominance (as for example, by holding certificates in order to create an unbalance of the certificate markets and ensure higher certificates trading prices)

• The evaluation of the capacity needs should take into account opportunities connected to the interconnection system and the import of electricity. These will affects positively the security of supply and the volume of electricity import should be taken into account

• Protection of equality of treatment among operators is key in order to avoid predatory behaviour from dominant market players

• The cost of capacity market certificates should be included in the calculation of regulated tariffs

24

• The possibility to launch tender for new capacity needs to be assessed vs. investment in new generation capacity which would have occurred in a traditional market

The Central Asia Regional Electricity market – A roadmap

In the centrally planned era the regional electricity flow in the Central Asia Region used to be part of a wider economic planning context. Electricity, water, cotton, fuels and other commodities where exchanged year-round in an area which used to be part of a single state. With the collapse of the Soviet Union the re-scheduled deliveries were hard to be matched as commodities where now produced by different counties under different conditions. The history is more or less known and what is important to be highlighted is that the electricity flows in the region have gradually and steadily been decreasing in an area where the hydro-thermal cooperation would be beneficial - as it used to be in the past but nowadays even more due to the technological advancements.

Kazakhstan beyond any doubt comprises an important player in the future market –primarily due to its market size and level of advancement – but it is rather unlikely that it could catalytically lead the process in which the rest of the partners are not convinced to follow.

As far as the Roadmap for the development of the Regional Central Electricity Market is concerned, in the views of the ITS team this can for the time being define general directions but the detailed milestones to be accurately defined they would require all prerequisites to be in place. Instead of a full-defined Roadmap the one proposed below describes the necessary prerequisites for a process to be set up in order to guide development. Perhaps the discussions at international level would be able to support and facilitate a process such as the one briefly described below:

25

• A political cooperation process is required

• New vs existing forum

International cooperation level

• Unharmonised regulatory frameworks

• NRAs and regional cooperation

Regulatory Cooperation level

• Vertical undertaking and unbundled TSO

• CDC Energia role Operational Level

26

2.2 Background

The present report comprises the final deliverable of an assignment carried out under the Ad-Hoc Expert Facility (AHEF) of “INOGATE Technical Secretariat & Integrated Programme in support of the Baku Initiative and the Eastern Partnership energy objectives” project, funded by EC/Europeaid. Five applications for provision of Technical Assistance have been combined in this technical assistance assignment as they all shared common characteristics and comprised merits for addressing them collectively. The applications included:

• 89.KZ Study and analysis of experience in in development of power exchange trade in the countries of the Western Europe submitted by JSC "Kazakhstan Operator of Electricity Market" (JSC KOREM)

• 107.KZ Study and analysis of the existing models of electricity market in the countries of Europe, CIS and USA submitted by Ministry of Energy of the Republic of Kazakhstan

• 108.KZ Study and analysis of tariff setting in the area of electricity (production, transmission, supply) in the countries of Europe, CIS and USA

• 117.UZ Study and analysis of the existing models of electricity market in the countries of Europe, CIS and USA submitted by the International non-governmental organisations Central Dispatch Centre Energy

as they are filed under Component B: Electricity & Gas in the AHEF Registry. The assignment has been implemented over the period of November 2014 –August 2015.

2.2.1 Objectives of the study, key findings and recommendations According to the ToR the assignment had to work with the Ministry Energy on the strategic aspect of electricity sector development and future operation and KOREM on the tactical one of improving the market by analysing specific aspects and compare with the EU practices. It also involved the Ministry of Economy, KEGOC and the industry associations. In addition to the above the assignment also addressed with the cooperation of CDC Energia the regional dimension taking Kazakhstan as a reference and starting point.

The specific objectives of the task included:

For MINT:

• To get acquainted with the EU experience in regards of development and integration of electricity markets;

• To understand the distinction between competitive and regulated segments of the electricity sector and the manner that electricity composite prices/tariffs evolve in relation to these;

• To receive information on the mechanisms of achieving investments in a liberalised market environment, on who is responsible for planning and on how these investments are recovered;

For KOREM:

• To understand the distinction energy (i.e. forward, spot, balancing) and capacity markets;

27

• To introduce the EU experience with regard to wholesale electricity market models and the so-called Target Model;

• To receive information on the nature and content of trading and settlement arrangements that should exist in order to govern the relationships of the market participants;

For All Beneficiaries:

• To get acquainted with the EU experience with regard to cross border arrangements in the EU;

• To discuss whether these principles would be in all or in part useful for developing a regional market in Central Asia.

2.2.2 Methodology and outputs The approach involved a mixed field work and homework effort that involved two missions to Astana. The assessment commenced with homework on the electricity sector profile of Kazakhstan with a view that the team establishes the basic background knowledge on the sector. The first mission to Astana was carried out in December 2014. The purpose of the mission was to discuss the guiding ideas over which the analysis would deploy and also to get feedback on specific issues that were of an immediate and specific interest to the beneficiaries (mostly KOREM). There has been analysis on the specific issues and also on the remainder of the subjects mentioned in the ToR during the period between January and April 2015. In April 2015 the second mission has been carried with the purpose of providing answers to the detailed requests of KOREM and also to hold a workshop in the Ministry of Energy in which both national market design but also regional Central Asia electricity market developments were to be discussed. This second mission included also the participation of CDC Energy which INOGATE and several international institutions recognise as a specialist organisation in the regional electricity market of Central Asia.

Kazakhstan is a major electricity market in the region and has so far achieved considerable reforms in comparison to the neighbouring markets in Central Asia. In that sense INOGATE has developed this study as a background work for the Ministry of Energy in order to communicate the developments in relation to the integration of the European electricity market. We believe that certain aspects of this work might reveal a point of reference for the Ministry of Energy in the process of developing and modernise the electricity sector in Kazakhstan. The conditions for the development of a regional electricity market in Central Asia at the moment do not allow for a detailed discussion on the market design specifics. The development of infrastructure which is currently underway and supported by several IFIs as well as the need for political and regulatory cooperation need to be dealt with as a matter of priority. INOGATE follows closely the development in this respect and will be available to discuss future engagement should certain precedents such as the political and regulatory cooperation are established.

2.2.3 Limitations and further work The aim of the study was to develop the necessary background for the beneficiaries in order to contribute in their turn in the national dialogue for the future development of the Kazakh electricity market. One of the key limitations identified during this assignment is that European legislation

28

especially after the adoption of the 3rd Energy Package has become quite detailed and specific particularly in the areas of generation authorisation, Regulated Third Party Access and Unbundling of the Transmission System Operators. While these legal and regulatory provisions have gradually emerged as a mechanism for the integration the national European markets into the Internal Electricity Market their validity and transferability is becoming increasingly challenging in countries outside the EU. Kazakhstan, on the other hand, as a member of the Euro-Asia Economic Union will have to work towards the legal and regulatory integration with Russia and Kyrgyzstan. There are a few areas which mostly relate to merely technical and operational aspects in the electricity markets that have only briefly mentioned in this study and could form part of the future cooperation between Kazakhstan and INOGATE in the future.

2.2.4 Structure of the report The report comprises two major parts each one comprising a distinct geography namely; the European Union and the Republic of Kazakhstan. Particularly, the electricity market models and EU legislation as well as the so far experience with capacity mechanism comprise the major part of this report. The review of the electricity sector of Kazakhstan and the legal gap analysis as well as the review of the status and recommendations on the Central Asia Electricity Markets comprise the remainder of this report. More specifically:

Chapter 2.3 discusses electricity markets the models that have emerged and their legal implementation in the EU.

Chapter 2.4 attempts an review of the key areas related to the electricity market in Kazakhstan and includes a high level legal gap analysis.

Chapter 2.5 provides an overview of introduction of new generation capacities in liberalised markets.

Chapter 2.6 discusses specific and immediate legal, technical and regulatory issues that are currently on stake in the discussion for the future development of the Kazakh electricity market.

Chapter 2.7 is devoted to the review of the progress of the development of the Central Asia Electricity Market and provides recommendations for structuring the dialogue on broader cooperation.

Two appendices comprise an integral part of this report with each of them corresponding to:

Appendix 1: The French Electricity Market

Appendix 2: Kazakhstan Electricity Sector Profile

29

2.3 ELECTRICITY MARKETS

2.3.1 Concepts in the new market structure This section discusses briefly the motivation and economic rationale under which several energy policy makers (including Kazakh as it is evident by the Law on Natural Monopolies) to restructure their national electricity supply industries and introduce competition in certain segments while keeping (primarily) the networks as natural monopolies. This section in addition to the description of the resulting organization of the sector extends to the impact of these reforms on price discovery mechanisms and the prevailing wholesale electricity market models.

2.3.1.1 The rationale of preserving networks as natural monopoly Electricity in general has the typical characteristics of a good to be supplied by a natural monopoly. At least this was the prevailing economic perspective of the industry from its emergence during the Thomas Edison and Nicola Tesla era until recently. There are several arguments justifying that with most of them being founded on the premises of economies of scale, and security of operations. First, the generation of electricity involves significant economies of scale. In order to produce electricity, a plant needs to be erected to generate the first kilowatt-hour. After the initial investment, however, additional megawatts can be produced in the same generation plant without incurring new fixed costs. Consequently, production on a larger scale can be done at decreasing average cost. Secondly, transmission and distribution are quintessential natural monopolies1. The building of networks entails high, largely sunk fixed costs so that it would be economically wasteful to have multiple network resources covering the same area. Third, complementarities between generation and transmission lead to substantial economies of scope. This explains the rationale for the structural integration of the electricity industry. A striking attribute of a transmission grid is “its ability to synchronize dispersed generating units into a stable network”2. Production from facilities with higher marginal cost can be substituted by production from facilities with lower marginal cost in real time, thereby increasing efficiency. Moreover, in order to ensure electricity supply, there needs to be a continuous balancing of generation and consumption. If one single element of the system (e.g. a generation unit or a transmission line) does not work properly, it can endanger the stability of the entire electricity grid3. These special characteristics of electricity make it very complicated to replace the existing vertical and horizontal integration with decentralized market mechanisms4.

The recent economic appreciation of the network industries in general and within them the electricity supply industry continues to recognise the merits of monopoly but only with regards to the networks i.e. proposing that inefficiencies of the monopoly are less than the avoided cost of

1 Kessides (2004). p. 133. Reforming Infrastructure: Privatization, Regulation and Competition. Herndon, VA, USA: World Bank 2 According to Joskow, cited in: Kessidis (2004). p. 133, Reforming Infrastructure: Privatization, Regulation and Competition. Herndon, VA, USA: World Bank 3 Kessides (2004). p. 133. Reforming Infrastructure: Privatization, Regulation and Competition. Herndon, VA, USA: World Bank 4 Joskow (2003). p. 5. Electricity Sector Restructuring and Competition: Lessons Learned. Latin American Economic Review.

30

spontaneous network investment and that allocative efficiencies may be achieved by introducing competition to the generation and supply segments. The high cost of electricity networks (both at transmission and distribution level) can make it efficient to have a single supplier of network services in a particular geographic area, leading to a natural monopoly industry structure. In addition, the electricity networks are regulated to manage the risk of monopoly pricing, where a business can charge higher prices or provide poorer services compared with the situation in a competitive market. Thus, even in the liberalized electricity sector, network tariffs are not determined by market forces: because each network is a monopoly and so market forces cannot be relied upon to provide efficient prices.

2.3.1.2 Unbundling Keeping certain parts of the industry as a natural monopoly while allowing third parties to get access to the networks and eventually compete on a level playing field led to the introduction of the notion of unbundling.

The Notion of Unbundling

Unbundling within energy markets refers to the unbundling of vertically integrated structures. The unbundling of generation, transmission, distribution and retail sales has an important role within the electricity market with regard to the implementation of competition. The inclination towards the unbundling of the transmission and distribution operations, which are referred to as network operations and which, as already mentioned, carry natural monopoly characteristics, from generation and retail sales activities, is based on the concern that the dominant undertaking may limit in various ways the access of other undertakings that it is competing with in generation and retail sales areas. The mechanism referred to as vertical unbundling aims to provide the access of all players to distribution and transmission systems without discrimination and the prevention of cross subsidization between undertakings conducting generation, transmission, distribution and supply activities.

Unbundling within the electricity market may be realized as:

• unbundling of accounts, which provides for the independent accounting for separate operations

• legal unbundling, which provides for the organization of different activities under different legal entities. However, this does not prevent such different activities from being owned by the investment group.

• functional unbundling: accounting separation, plus (1) relying on the same information about its transmission system as the other market players when buying and selling power, and (2) separating employees involved in transmission from those involved in power sales.

• operational unbundling: operation of, and decisions about, investment in the transmission grid are the responsibility of an entity that is independent of the owner(s) of generation; however, ownership of the transmission grid remains with the owner(s) of generation.

• ownership unbundling, to the contrary of legal unbundling, requires the unbundled assets and activities to not be owned by the same investment group.

31

Thus, within the electricity sector, it is essential that unbundling be realized within vertically integrated undertakings in order to support the entry of new players to the market and to prevent discrimination between undertakings within the market.

2.3.1.3 Trading in wholesale electricity markets Trading in liberalized wholesale electricity markets5&6 can be characterized according to the features of the underlying contracts, i.e. whether the underlying contract is for ‘physical’ delivery or just a pure financial contract:

• Contracts for physical delivery tend to be formed closer to the delivery time, and are formed between appropriate market participants, in this case between generators and suppliers or end –users.

• Financial contracts tend to be formed well in advance of the delivery time; in such contracts it is not necessary that the parties can actually be engaged in transactions of physical delivery of electricity, i.e. traders not owing / representing any generation capacity or not consumption installation may engage in such contracts.

Concerning the type of market, wholesale electricity trading can be performed via:

• Bilateral Over-the-Counter (OTC) contracts with free formats; such contracts may be established over a variety of products and for various time horizons (from long-term, i.e. 3 years ahead, up to one-day ahead).

• Organized markets (Pools or Power Exchanges/PXs); organised markets can be implemented in different horizons:

o Long-term / forward markets (for physical or financial delivery of energy), with different standardized formats of contracts; usually implemented through a PX;

o Day-Ahead organized markets (physical delivery of energy); usually implemented through a Pool or a PX;

o Intraday markets (physical delivery of energy); usually implemented through a PX;

2.3.1.4 Bilateral contracts As for many commodities, a way to trade electricity is a market mechanism based on (physical or financial) bilateral contracts. This means that sellers and buyers freely enter into bilateral contracts for power supply. Sellers will normally be generators and buyers can be traders, electricity suppliers, distribution companies and eligible consumers. However, generators could also become a buyer (e.g. in case they have a shortage of generation). Likewise, consumers can become sellers. Brokers can act as an intermediate between buyers and sellers dealing in standard contracts. These types of transactions are referred to as Over the Counter (OTC).

As mentioned above, such contracts may be established over a variety of products and for various time horizons (from long-term, i.e. 3 years ahead, up to one-day ahead). In addition, they may involve ‘physical’ delivery of electricity or be just pure financial contracts.

5 http://www.oscogen.ethz.ch/reports/oscogen_d5_1b_010702.pdf 6 http://ocw.mit.edu/courses/engineering-systems-division/esd-934-engineering-economics-and-regulation-of-the-electric-power-sector-spring-2010/lecture-notes/MITESD_934S10_lec_11.pdf

32

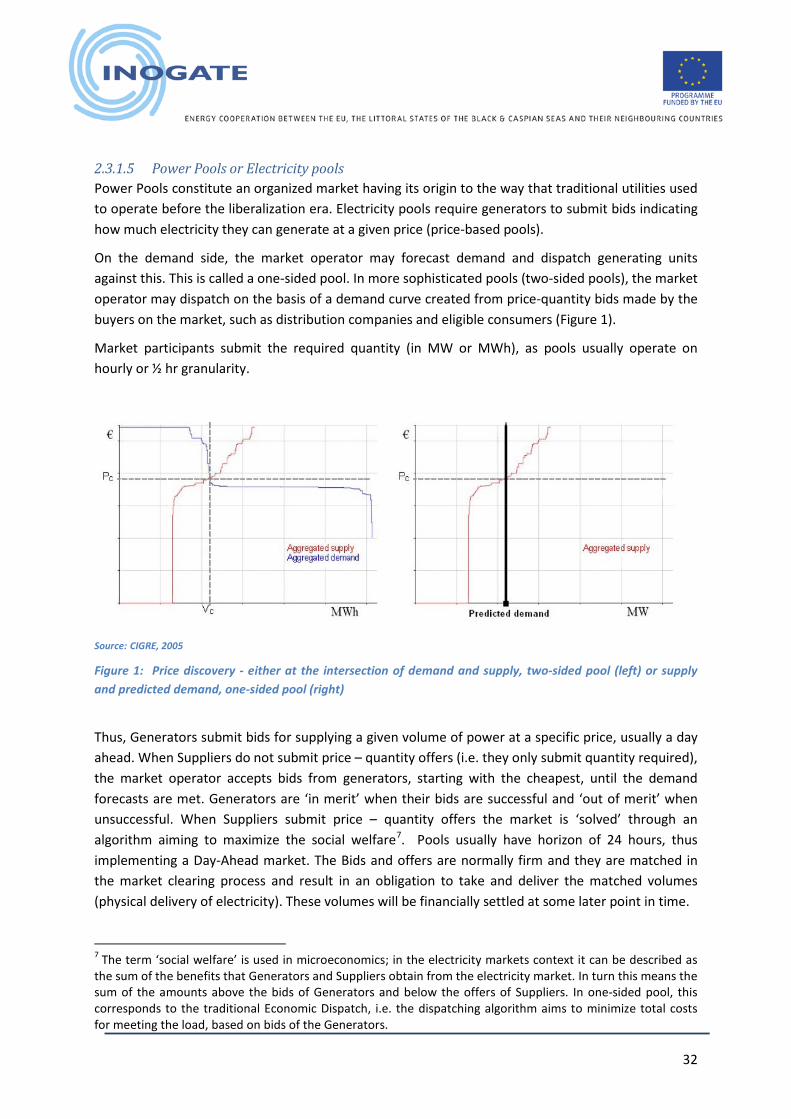

2.3.1.5 Power Pools or Electricity pools Power Pools constitute an organized market having its origin to the way that traditional utilities used to operate before the liberalization era. Electricity pools require generators to submit bids indicating how much electricity they can generate at a given price (price-based pools).

On the demand side, the market operator may forecast demand and dispatch generating units against this. This is called a one-sided pool. In more sophisticated pools (two-sided pools), the market operator may dispatch on the basis of a demand curve created from price-quantity bids made by the buyers on the market, such as distribution companies and eligible consumers (Figure 1).

Market participants submit the required quantity (in MW or MWh), as pools usually operate on hourly or ½ hr granularity.

Source: CIGRE, 2005

Figure 1: Price discovery - either at the intersection of demand and supply, two-sided pool (left) or supply and predicted demand, one-sided pool (right)

Thus, Generators submit bids for supplying a given volume of power at a specific price, usually a day ahead. When Suppliers do not submit price – quantity offers (i.e. they only submit quantity required), the market operator accepts bids from generators, starting with the cheapest, until the demand forecasts are met. Generators are ‘in merit’ when their bids are successful and ‘out of merit’ when unsuccessful. When Suppliers submit price – quantity offers the market is ‘solved’ through an algorithm aiming to maximize the social welfare7. Pools usually have horizon of 24 hours, thus implementing a Day-Ahead market. The Bids and offers are normally firm and they are matched in the market clearing process and result in an obligation to take and deliver the matched volumes (physical delivery of electricity). These volumes will be financially settled at some later point in time.

7 The term ‘social welfare’ is used in microeconomics; in the electricity markets context it can be described as the sum of the benefits that Generators and Suppliers obtain from the electricity market. In turn this means the sum of the amounts above the bids of Generators and below the offers of Suppliers. In one-sided pool, this corresponds to the traditional Economic Dispatch, i.e. the dispatching algorithm aims to minimize total costs for meeting the load, based on bids of the Generators.

33

Based on the set of generator costs received and on customer demand for electricity, the System Marginal Price (SMP) for each (hourly or half-hour) trading period is determined by the Market Operator, using a stack of the cheapest generator cost bids necessary to meet the demand. More efficient generators are generally run to meet demand in the trading period. The marginal generator needed to meet the demand sets the SMP for that trading period. The other generators who have submitted bids lower than this price are deemed to be in merit and will also be scheduled to run. The SMP for each trading period is paid to all generators that are needed to meet demand. All generators who have submitted a bid which is under the SMP earn a profit, known as inframarginal rent, on the difference between their bid offer and the SMP. In some pool implementations the market is solved and SMP is calculated for each trading period independently from other trading periods. In some other implementations, all 24 hours of the Day-ahead horizon are solved simultaneously (co-optimized), thus taking into account intertemporal constraints such as start-up/shut down times of generating units, ramping rates of generating units etc.

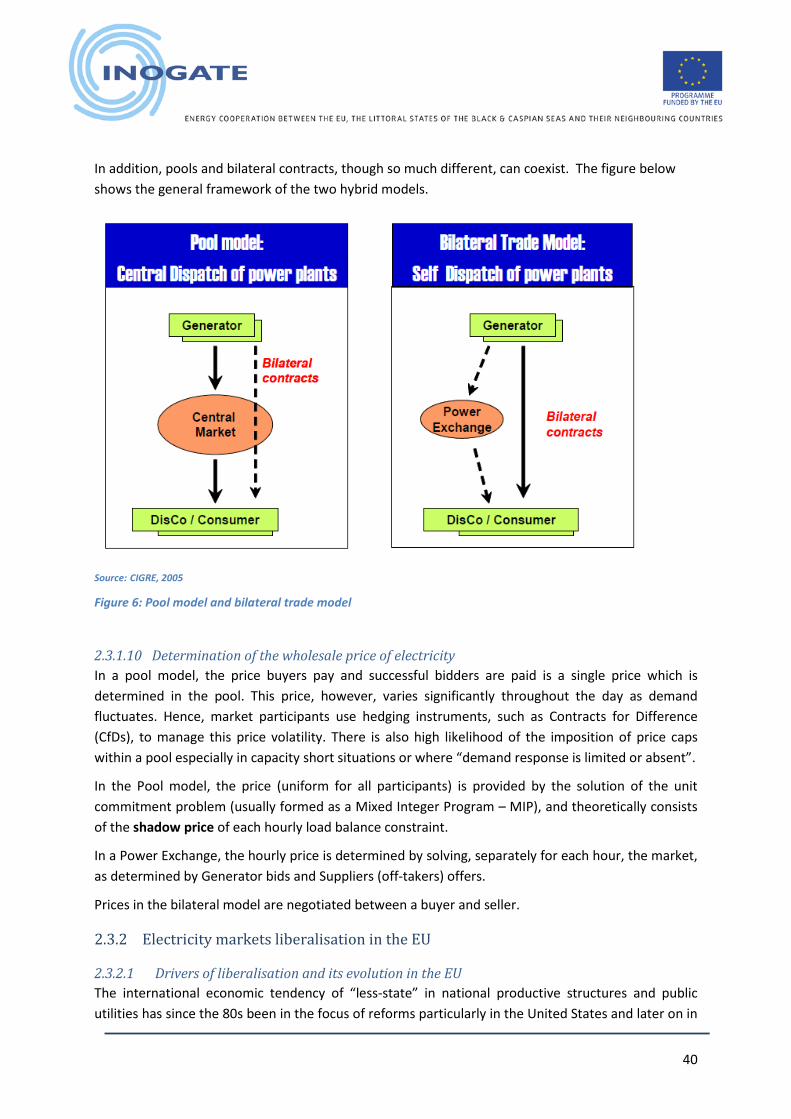

A pool can be a compulsory pool or a voluntary pool. A compulsory (or gross pool) requires all generators, except the smallest ones, to sell their output to the pool at the pool’s price. In a voluntary (or net pool), generators can agree bilateral trades with buyers for the delivery of electricity, but must inform the system operator who takes it into account when scheduling (see below Section 2.3.1.9.3 on ‘Hybrid Model’.)

During the matching process the network can be treated as a “copper plate” resulting in a single energy price in the whole control area. The cheapest generation gets priority regardless of network constraints. In a second stage the feasibility of the achieved solution is examined. If there is congestion, some out-of-merit generators are dispatched to replace in-merit generators. This is the so-called “constrained-on/off” generation. The cost of this action constitutes the uplift charge and is added to the ‘equilibrium’ price (Pc):

P energy = Pc + P congestion

Alternatively the matching can be on the basis of a security constrained dispatch taking into account both generation marginal price and the physical aspects of the transmission system. This is common in a pool model.

2.3.1.6 Power exchanges Power exchanges in the liberalised electricity market context signify an important mechanism to implement wholesale electricity markets. Over the last years and in the face of the ongoing liberalisation of the electricity sector in Europe and many other parts of the world, a number of electricity exchanges have been put into operation.

The main goal of exchange-based markets lies in the facilitation of the trading standardized products and the promotion of market information, competition, and liquidity. Power exchanges (ideally) also provide other benefits, such as a neutral marketplace, a neutral price reference, easy access, low transaction costs, a safe counterpart, and clearing and settlement service. Besides, exchange-based

34

spot market prices are an important reference both for over-the-counter (bilateral) trading, and for the trading of forward, future and option contracts.

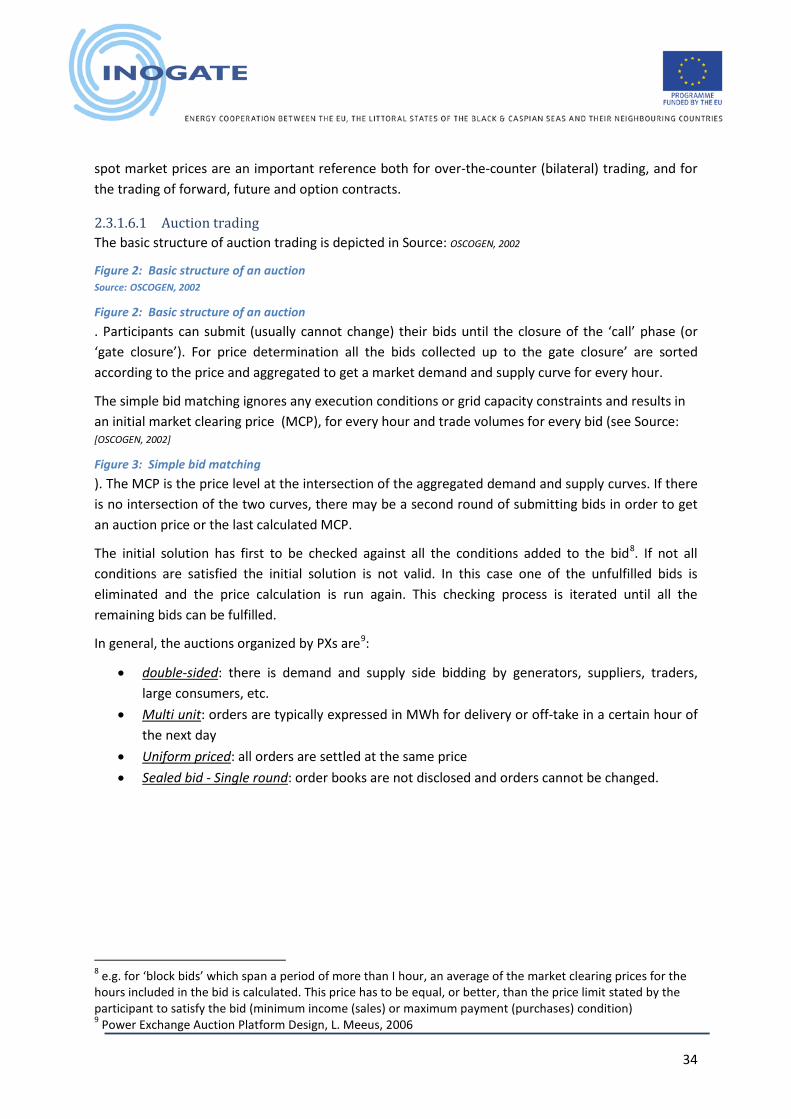

2.3.1.6.1 Auction trading The basic structure of auction trading is depicted in Source: OSCOGEN, 2002

Figure 2: Basic structure of an auction Source: OSCOGEN, 2002

Figure 2: Basic structure of an auction . Participants can submit (usually cannot change) their bids until the closure of the ‘call’ phase (or ‘gate closure’). For price determination all the bids collected up to the gate closure’ are sorted according to the price and aggregated to get a market demand and supply curve for every hour.

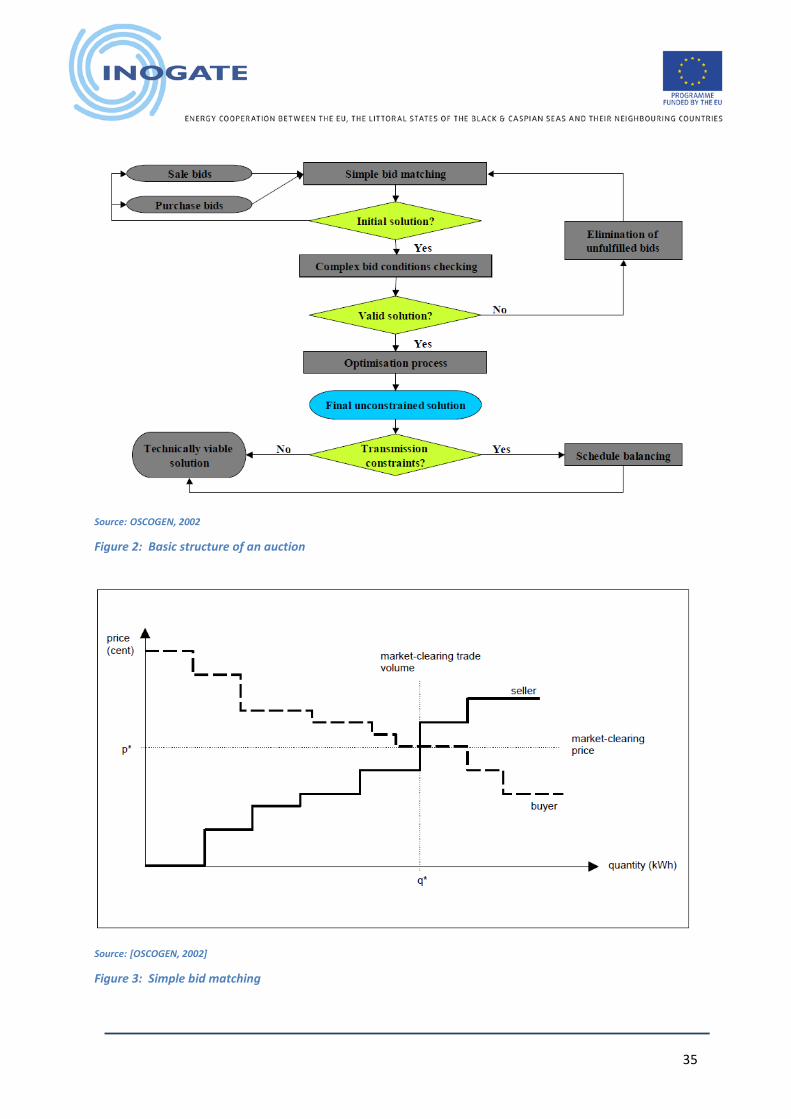

The simple bid matching ignores any execution conditions or grid capacity constraints and results in an initial market clearing price (MCP), for every hour and trade volumes for every bid (see Source: [OSCOGEN, 2002]

Figure 3: Simple bid matching ). The MCP is the price level at the intersection of the aggregated demand and supply curves. If there is no intersection of the two curves, there may be a second round of submitting bids in order to get an auction price or the last calculated MCP.

The initial solution has first to be checked against all the conditions added to the bid8. If not all conditions are satisfied the initial solution is not valid. In this case one of the unfulfilled bids is eliminated and the price calculation is run again. This checking process is iterated until all the remaining bids can be fulfilled.

In general, the auctions organized by PXs are9:

• double-sided: there is demand and supply side bidding by generators, suppliers, traders, large consumers, etc.

• Multi unit: orders are typically expressed in MWh for delivery or off-take in a certain hour of the next day

• Uniform priced: all orders are settled at the same price • Sealed bid - Single round: order books are not disclosed and orders cannot be changed.

8 e.g. for ‘block bids’ which span a period of more than I hour, an average of the market clearing prices for the hours included in the bid is calculated. This price has to be equal, or better, than the price limit stated by the participant to satisfy the bid (minimum income (sales) or maximum payment (purchases) condition) 9 Power Exchange Auction Platform Design, L. Meeus, 2006

35

Source: OSCOGEN, 2002

Figure 2: Basic structure of an auction

Source: [OSCOGEN, 2002]

Figure 3: Simple bid matching

36

2.3.1.6.2 Continuous trading Some exchanges provide an alternative trading form to the auction system called continuous trading. This form is used to either trade only block contracts (Borzen, EEX) or individual hours and block contracts (UKPX, APX UK). Continuous trading differs from auctions in the following points. Firstly, participants have access to the order book. Secondly, each incoming bid is immediately checked and matched if possible according to price/time priority. Finally, the transaction price is not the same for all transactions as it is determined according to only the concerned bids.