market and research group (marg) pvt. ltd. new delhipdf.usaid.gov/pdf_docs/pnabz412.pdf · ·...

TRANSCRIPT

Study Design:Household Savings lVIobiIization for Housing Finance

Companies

Market and Research Group (MARG) Pvt. Ltd.New Delhi

March 1994

Prepared forIndo-US Housing Finance Expansion Program

Abt Associates Inc.Management Support Services Contractor

B2/13 (2nd Floor)Vasant Vihar

New Delhi 110 057

USAID Pn~ied No. 386-0526-00-C-2295-00

fl

•

HOUSEHOLD SAVINGS MOBILIZATIONFOR HOUSING FINANCE COMPANIES

THE STUDY DESIGN

March, J.994

Prepared for Abt Associates Inc. U.S.A.

By MARG, Marketing and ResearchGroup Pvt. Ltd., New Delhi

MARG/AS/AM/9058

,,' '.

1.

II.

III.

IV.

V.

CON TEN T S

INTRODUCTION

METHODOLOGY

FINDINGS

THE PROPOSED STUDY DESIGN

APPENDIX

Page No.

1

2

5

15

I

I INTRODUCTION

with the onset of liberalisation, administered funds areon the decline. With the exception of a few, all HousingFinance Companies (HFCs) are dependent to a great extenton administered funds and / or assured credit.

There is hence a need for them to a0apt to these newmarket conditions and adapt themselves to mobiliseresources from the household sector.

It is to help the HFCs obtain an understanding of thehousehold savings preferences and inputs for schemedesign and marketing techniques that Abt Associates, themanagement support services contractor to the Indo-USAIDHousing Finance Expansion Program would like tocommission a research.

This document presents the design for such a study.

1

II

II.1

METHODOLOGY

Prior to actually designing the study, MARG and theClient agreed that some exploratory research would beuseful. This research would facilitate a betterunderstanding of the market and hence would providevaluable inputs for all aspects of the study whether interms of coverage, content, or target respondent.

This exploratory research included i

1) A review of some secondary data

2) Depth interviews

3) Focus group discussions.

Review of Secondary Data

This stage involved the study of

Our own syndicated research, i.e. Investrack

Published information of the National Housing Bank

Balance sheets and Deposit scheme brochures ofvarious Hou~ing Finance Companies

II.2

Miscellaneous reports, memoranda andrelated to the issue of Housing Financefunding

Depth Interviews

monograhsCompanies'

Qualified executives of MARG conducted detailedinterviews with representatives of various HousingFinance Companies to obtain their views on the obstaclesand opportunities for household deposit mobilisation.

All interviewsinterview guide.

were conducted with(See Appendix)

2

the help of an

The persons interviewed by us were

1. Mr.A.V. Goel, Senior ManagerCan Fin Homes Ltd.Hotel Kohinoor Park, III FloorVeer Sarvakar Road,Opp. Siddi Vinayaka TemplePrabhadevi,Bombay - 400 025

2. Mr. K. NenjundeshwarCan Fin Homes Ltd.32, Race Course RoadBangalore 560 001

3. Mr. S. Krishnamurthy,General Manager-Northern RegionHDFC, HDFC HouseB-6/3, Safdarjung EnclaveDDA Commercial ComplexNew Delhi 110 029

4. Mr. Nasser MunjeeExecutive DirectorHDFC, Ramon House169, Backbay ReclamationBombay 400 020

5. Mr. P. Nageswara Rao, PresidentVysya Bank Housing Finance Ltd.72, St. Marks RoadBangalore 560 001

6. Mr. A.K. DamManaging DirectorSBI Home Finance Ltd.Nagaland House11,Shakespeare SaraniCalcutta 700 071

7. Mr. R. K. Wadhawan,Chairman & Managing DirectorDewan Housing Finance Ltd.'Madhava' Opp.Sales Tax OfficeBandra Kurla ComplexBombay 400 051

8. Mr. Nitin PalanyManaging DirectorGRUH, l\mbica HouseNear CU Shah CollegeAshram RoadAhmedabad 380014

3

II.3

9. Mr. Paul DiamondChief ExecutiveLIC Housing Finance Ltd.Bombay Life Building, 2nd FloorVeer Nariman RoadBombay 400 023

10. Mr. T. C G110salChief ExecutivePeerless Abasan5, Loudon StreetCalcutta

11. Mr. Alok PrasadDy. General ManagerThe National Housing BankHindustan Times BuildingK. G. MargNew Delhi.

Focus Group Discussions

These discussions aimed at exploring the views of thetwo sets of investors i.e. the small investor and thelarge one. Accordingly, four groups were held, one ofeach type in Bombay and Hyderabad.

Bombay and Hyderabad were identified as the centres asBombay represents a mature market and Hyderabad agrowing one. The group characteristics were as follows.

Group Type I

Group Type II

Sex MaleAge 30-55 yearsMarital Status : MarriedMonthly Personal Income Rs.2500+1993 Investment Amount: Rs 10,000

Sex MaleAge 30-55 yearsMarital Status : MarriedMonthly Personal Income: RS.6000+1993 Investment Amount": Rs.50,000+

The groups were moderated by trained executives ofQUEST, MARG's in-house qualitative research division.Discussions centred around a pre-designed discussionguide (See Appendix) .

The information collected at all stages was thenanalysed by MARG to understand the market, with all it'simplications and to design an appropriate survey.

4

III FINDINGS

The findings of the exploratory research can be groupedinto various categories.

III.1

III.2

The Market Characteristics

Feedback of the Housing Finance Companies on

a) Importance of household savingsoption.

as a funding

III.3

b) Market definition

c) Constraints of deposit mobilisation

d) The strategies for deposit mobilisation

e) Their research needs

Focus group discussion conclusions on

a) Current Investment Preferences.

b) Investor motivations

c) Investor Knowledge Levels

d) Investor perceptions of

Company deposits

Housing Finance Companies

Deposit schemes of Housing Finance Companies

5

III.1 Market Characteristics

A studyprovidesInvestor.

of our own syndicated research,some interesting information on

INVESTRACKthe- Indian

INVESTRACK defined the investor as the financialdecision maker in-households with a minimum declaredmonthly household income of RS.4000. Investrack useddeclared household income as the screening criteria.The survey interviewed 4000+ respondents across 16 ofthe class I towns.

This research provides some useful information on themarket i

* The Indian Investor may be segmented intoclusters (See Appendix)

5

*

*

*

Investors keep 60% of their portfolio in fixedincome securities and the balance in growth schemes

Company Deposits (the closest surrogate to HousingFinance Companies' deposits) enjoy a penetrationof about 16% (All India)

This penetration seems positively related towealth and age. It is also relatively more commonamong

salaried individualstowns with a population of 5 M+Maharashtrians and South Indians

However Investrack does not provide any information onindividuals with incomes of less than RS.4000 per month.It also concentrates on the top 16 towns and does notcover. small towns or rural areas. Moreover, Investrackcovered fixed/company deposits at a generic level andnot those specifically held with HFCs.

6

III.2 Discussions with the representatives ofHousing Finance Companies ranged on amatters. Broadly speaking these could befollows

the variousvariety of

grouped as

III.2.a Importance of household savings as a funding option.

All surveyed Housing Finance Company's did not underminethe importance of household savings in their resourcemix and were firm in their resolve to tap into them.

What did vary across companies was the present level ofdeposit mobilisation activity and the time frames foractive mobilisation.

III.2.b Market Definition

All Housing Finance Companies officials believed that

There existed a market for the fixed depositproduct

This market was however a marginally declining one

The market was inversely related to the stockmarkets' performance

The market lay among the middle and lower middleclass of people

In terms of town class,largest in large metros,have a sizeable market

while collections aresmaller urban centres

thetoo

The Fixed Deposit as an investment option 18

favoured by the retired or older investor

Officials also believed that a rural market fordeposits may exist but the cost factor ofcollection would need to be considered. Atpresent, all surveyed Housing Finance Companieswith the exception of GRUB and Vysya bank, wereinclined to market their schemes in areas wherethey have on administrative presence.

7

III.2.c Constraints

Housing Finance Company officiqls listedobstacles in their efforts at successfulmobilisation.

variousdeposit

Officials believed that a ~Level playing field' amongall participants in the financial market was essential,if they were to complete meaningfully for a share of thehousehold resources. They would like to be on par withbanks, co-operative societies, finance companies etc.

The constraints discussed were

Tax deducted at source or the law that obligescompanies to deduct tax at source on interest Idividend payments of RS.2500 and above. This wasstated as the single most irritant in the HFC'sability to attract and service customers

Acceptance of Cash deposits of amounts greater thanRs.20,OOO. To prevent conversion of undeclaredfunds into deposits, companies are not permitted toaccept cash pa~nents for deposits larger thanRs.20,OOOI-. However HFC officials believe thatthis acts against genuine investors in rural /semi-urabn areas where cash is held purely becausethe banking system / habit to not as strong as inurban India.

Term of deposit.Housing Financeshould not bedeposits coulddismissed fearstheir resourcesview was however

Companies believed thatspecified and that shorterbe an attractive option.

about their inability towith their disbursements.

not shared by the NHB

termtermThey

matchThis

Advertisement of FinancialsHousing Finance Companies felt that an importanthurdle in creating awareness among the public wasthe statute which required them to publish a ~full

advertisement' stating their financials, pastperformance etc. These advertisements are lengthyand costly and hence the frequency is not as muchas desired. Consequently the required level ofpublic awareness may not be created.

Deposit InsuranceOfficials were divided on whether or not DepositInsurance by the NBS could facilitate greaterdeposits. At present bank deposits are insured tothe maximum extent of Rs.30,OOO per acccount.

8

III.2.d Strategies for Fixed Deposits

Housing Finance Companies' representative interviewedbelieved that they could attract depositors by

* Attractively designed schemes

* Excellent customer service

* A motivated and exhaustive agent network

* Concentrating on the areas where they have apresence

III.2.e Research Needs

Officials of the various Housing Finance Companies wereasked about the possible uses of the proposed research.

Their answers fell into three main categories

1) To validate their constraints among the investingpublic so that their stand could be effectivelypresented to policy makers

2) To provide an analysis ofinvestor in terms of

his agehis occupationinvested amountlife cycle stagelocation

the fixed deposit

111.3

3) To provide inputs to develop customer friendlyschemes

Group discussions among the investor classes in the twocities revealed various dimensions of the investmentbehaviour.

These may be studied as follows

III.3.a Current Investment Preferences

Investors are primarily motivated by 3 conflictingdesires at the time of portfolio allocation i.e.

* Tax savings / risk cover

* principal security

* High returns

9

Most individuals aim to satisfy their tax requirementsfirst. These are often referred to as "compulsorysavings". Also included here is the need to provide arisk cover. Hence, LIC, NSC, PPF are the schemes optedfor first.

Then an individuals looks at other schemes which offerbetter returns but at the same time he is assured thathis capital/principal is safe. At this stage he isthus willing to look at variable interest rate optionswith secured principal. Liquidity too is an importantconsideration at this stage. Mutual Funds, Debentures,Gold, Bank Deposits are the schemes considered here.

Then if an individual still has a surplus he is willingto 'gamble', 'speculate', take an 'informed decision''calculated risk' and invest in primary, or secondaryshares.

This tendency was cornman across three groups i.e the twoBombay groups and the larger investor group ofHyderabad. The small investor in Hyderabad thoughtquite differently. He looked for liquidity, safety,risk cover for his family. The desire for the sharemarket is very limited.

This group finds it difficult tolooks for regular, forced savings.common in this group.

III.3.b Investor motivations

save andChits and

thereforeLIC are

As earlier research such as 'INVESTRACK'investors both large and small look for

safetytax benefitsreturn and liquidity

has proved,

Among investor classes the smaller investor ofsmaller town i.e Hyderabad is less, confident,risk averse than his counterpart in Bombay.

themore

Another motivation, not yet proved, but seems to existis to be "considered a smart/savvy investor". Investorsseem to want "a part of the action" and be perceivedas knowledgeable. This suggests that there may be apsychological need to be considered knowledgeable onwhich instruments could be positioned.

10

The investors of Hyderabad both large and small seeinvestments as a way of building tangible assets whetherit is a house, gold or teak plantations or for thespecific purpose of looking after their wives orchildren.

Investors of Bombay on the' other hand invest to earn "anextra income" or "to keep up with the times".

There was also a feeling of uncertainly due toliberalisation and its possible fallout, in terms ofretrenchement, 'voluntary retirement and hence a needwas expressed to "make money quickly". This was theview of Bombay's smaller investor.

III.3.c Investor Knowledge Levels

Knowledge levels seem to be directly related . toInvestment amounts with the 'large investment' classdisplaying a detailed understanding of the market.

Large investors of both cities were aware of the conceptof proportional allotment of shares and its implicationson Mutual Funds.

Similarly they were aware of the possibility of fallinginterest rates, inflation calculations and risks ininvestments e.g. Bank.of Karad, Nirlon episodes.

Smaller investors are less informed more so in the caseof Hyderabad.

Bombay's smaller investor was aware of DepositInsurance and is clearly more confident than hisHyderabad counterpart. Overall the three groups (exceptthe small investor of Hyderabad) were confident,believed in themselves and wanted to be seen asinformed, knowledgeable players.

III.3.d Investor Perceptions

i) Perception of Fixed Deposits

Investors are aware of scheme features andoperations. There are however no strong feeling onfixed / company deposits. They are seen as justanother option available to the investor. It seemsto offer no single 'Unique Selling Proposition.This feeling was common across all groups.

11

To paraphrase, there was no motivation to investin a fixed deposit / company deposit.

When probed, advantages of the fixed deposit wereperceived to be the interest rate, regular income,shorter term and the promise of better customerservice vis-a-vis nationalised banks.

Disadvantages were that there were otherinstruments which were more attractive i.edebentures in terms of return and service. Alsothe security of the company deposit was questioned.Nirlon etc. were stated as examples where investorslost heavily. There is also a fear than companiesmay not be all that prompt in principal andinterest repayments.

ii) Perceptions of Housing Finance Companies.

Across all groups there was an awareness of anentity called a Housing Finance Company. Theawareness was the weakest in the smaller investorgroup in Hyderabad.

Respondents were also well informed about thefunctions and objectives of the Housing FinanceCompanies.

Housing Finance Companies had varying connotationsamong investors ie., some saw them asintermediaries dispensing funds sanctioned by thegovernment.

Some sawobligation

them as fulfilling a social

Some saw thembuilders / II

as being in collusionoperating a racket ll

with

Among all the Housing Finance Companies awarenessof HDFC, LIC, SBI & Can Fin Homes was higher.

For the other companies which had a strong parent,the parent body was known but not its HousingFinance SUbsidiary.

Among the small private companies Dewan Housing wasfairly well known - beinq spontaneously mentionedin 3 groups. It however had some negativesattached to it. (It was seen by some to promoteits own constructions and collude with builders.)

12

The name of GRUH too was somewhat familiar to theparticipants due to the fact that it was listed.Quite clearly listing of a company's share improvedit's awareness.

The smaller investors of Hyderabad were somewhatsuspicious of lIFCs seeing them as "'fly by night'operators .... eg. Tapovan etc.

Overall HDFC had a very positive image - as a soundcompany with excellent customer service.

LIC was a close second SBT & Can Fin Homes too werewell regarded.

iii) Perceptions of deposit schemes of HFCs.

Investors across all groups were aware of Depositschemes of HDFC. One individual had invested in"Easy way" of HDFC.

However they were not very familiardetails. They felt it was a "'recent'and was yet to catch on.

with schemedevelopment

There was marginal awareness of schemes of SBI andCan Fin. Homes.

On being shown an outline of the Deposit features,(See Appendix) no excitement was generated amongparticipants.

Standard reactions were .

"There is nothing new' .....

"~t is a universal offering .... "

However the features that interested respondentsthe most was the possibility of a loan. This wasmost marked in Bombay, keeping their overalldesire to participate in the share market.

On their willingness to invest in these schemes,respondents were unenthusistic. Factors which couldpositively influence them were

* Promoter name ie. HDFC

* Link to Housing Loan

l~

* Interest rate rebate or concessional rates ofinterest on housing loans subsequentlyavailed and a loan sanction preference

* Some promotion by agents / brokers or sharingof commissions.

Reservations to investing were

* Lack of knowledge of the company / promoter'sperformance

* Lack of any major positive

The only group to show some willingness to investin HFC deposits was the small investor inHyderabad.

Single respondents in both the high investment'groups mentioned that an HFC's deposit would besafer. than a manufacturing company since it hasmore fixed assets i.e. houses.

Overall the view was that only if the person waslooking for a housing loan sometime in the futurewould he consider investing in an HFC deposit or toparaphrase there was no ~stand-alone' motivation toinvest with a Housing Finance Company.

14

positively

buying abe more

in fixed

IV.

IV.1

THE PROPOSED STUDY DESIGN

The Research Objective

On the basis of the findings of the exploratoryresearch various hypotheses have been shortlisted. Theobjective of the research is to validate thesehypotheses ;

a) Market Related Hypotheses

There is a class of people who believe in fixeddeposits and with continue to regard them as aviable investment option. These are likely to be ;

middle and lower middle classsalaried or retiredmarriedand residing in both large and small towns.

In large towns the incidence of fixed deposits maybe lower due to a more knowledgeable and exposedinvestor class but the collections are vast due tothe sheer volume of investors. The small towns onthe other hand, have a higher incidence of fixeddeposits due to a relatively less knowledgeable /exposed investor class but lower collections.

b) Marketing Related Hypotheses

The image of HFCs is not always a positive oneThe level of safety associated with a companyis an important influencer to investing in itA good agent network can contribute to depositmobilization.The goodwill enjoyed by an HFC issignificantly more in the areas where it has aphysical presenceThe intention to invest in a company isinfluenced by the familiarity of the companynameInvestors desirous of building /house some time in the future willinclined to invest their savingsdeposits of HFCsQuality customer service canreinforce investment decisionsInvestors are attracted by innovative schemesCertain [caturcn of the lIFC deposit. act as abarrier to investment.

15

/

IV.2 The Survey Contents

To ensure complete validation of the hypotheses thesurvey would cover the following information areas

* Market Related Hypotheses

Incidence of investmentsAllocation of portfolioIncidence of investments in fixed depositsMethod of investment decision makingFuture investment intentions including housepurchase intentionAttitude to investment

* Marketing Related Hypotheses

Awareness / familiarity levels of various HFCsand their competitors i.e. Banks, UTIComparison of HFCs and their competitors onvarious dimensions i.e. stability,trustworthiness, credibility, managementexpertise etc.Service expectations of investors i.e.

instant deposit receiptsprompt payment of interest/principalspeedy redressal of queries, polite staffetc.

Role of agents in the mobilization process.

Investor preferences for scheme features

cumulative vs income schemesmonthly vs quarterly paymentsubscription amountsone time investment vs continuousperiodic investmentoverdraft preferencesterm preferencesadditional benefits i.e. housing loanlinkages, interest rebate, prefentialtreatment for loan sanotionsharing of commissionhome collections vs visits to companypassbook / checking facilitespassbook/checking facilities

16

'I. ,

Barriers to investing in fixed deposits ofHFCs. The extent to which deposits could beincreased if

the tax deducted at source condition wasrelaxeddeposit insurance was providedcredit ratings were publishedcash deposits were acceptedshorter term deposits were offerednomination facilities were providedcommissions were flexible

In addition the survey would obtain demographicinformation i.e. age, income, education,occupation, lifecycle stage and mother tongue.

17

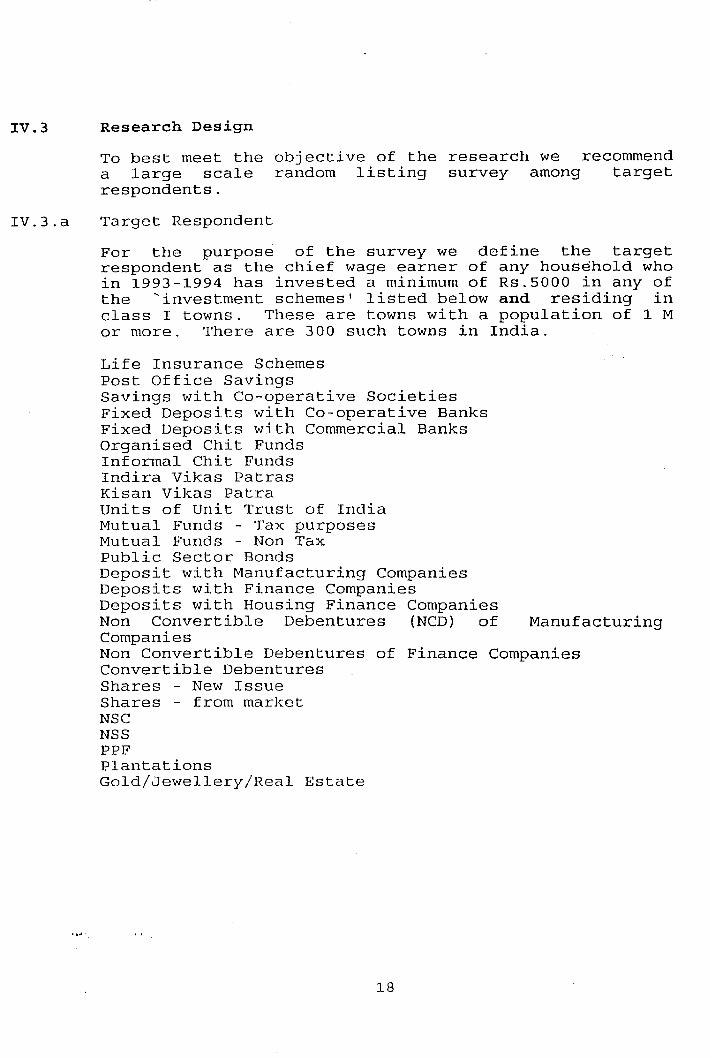

IV.3

IV.3.a

Research Design

To best meet the objective of the research we recommenda large scale random listing survey among targetrespondents.

Target Respondent

For the purpose of the survey we define the targetrespondent as the chief wage earner of any hous~hold whoin 1993-1994 has invested a minimum of RS.5000 in any ofthe 'investment schemes' listed below and residing inclass I towns. These are towns with a population of 1 Mor more. There are 300 such towns in India.

Life Insurance SchemesPost Office SavingsSavings with Co-operative SocietiesFixed Deposits with Co-operative BanksFixed Deposits with Commercial BanksOrganised Chit FundsInformal Chit FundsIndira Vikas PatrasKisan Vikas PatraUnits of Unit Trust of IndiaMutual Funds - Tax purposesMutual Funds - Non TaxPublic Sector BondsDeposit with Manufacturing CompaniesDeposits with Finance CompaniesDeposits with Housing Finance CompaniesNon Convertible Debentures (NCD) of ManufacturingCompaniesNon Convertible Debentures of Finance CompaniesConvertible DebenturesShares - New IssueShares - from marketNSCNSSPPFPlantationsGold/Jewellery/Real Estate

18

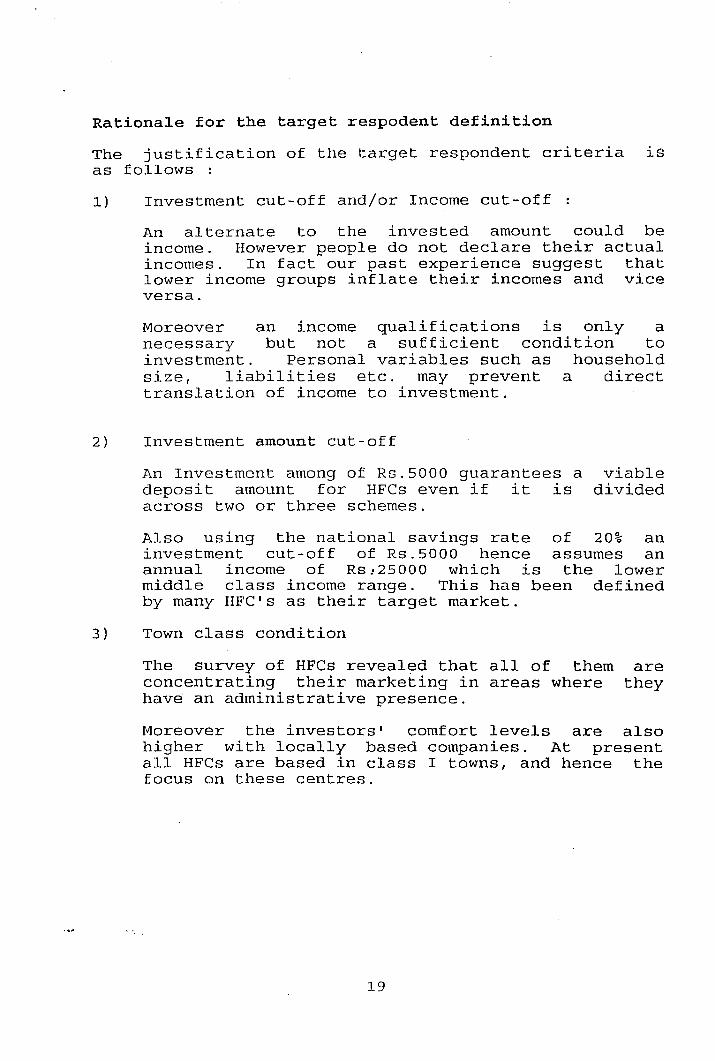

Rationale for the target respodent definition

The justification of the target respondent criteria isas follows :

1) Investment cut-off and/or Income cut-off

An alternate to the invested amount could beincome. However people do not declare their actualincomes. In fact our past experience suggest thatlower income groups inflate their incomes and viceversa.

Moreover an income qualifications is only anecessary but not a sufficient condition toinvestment. Personal variables such as householdsize, liabilities etc. may prevent a directtranslation of income to investment.

2) Investment amount cut-off

An Investment among of RS.5000 guarantees adeposit amount for HFCs even if it isacross two or three schemes.

viabledivided

Also using the national savings rate of 20% aninvestment cut-off of RS.5000 hence assumes anannual income of Rs!25000 which is the lowermiddle class income range. This has been definedby many HFC's as their target market.

3) Town class condition

The survey of HFCs revealed that all of themconcentrating their marketing in areas wherehave an administrative presence.

arethey

Moreover the investors' comfort levels are alsohigher with locally based companies. At presentall HFCs are based in class I towns, and hence thefocus on these centres.

19

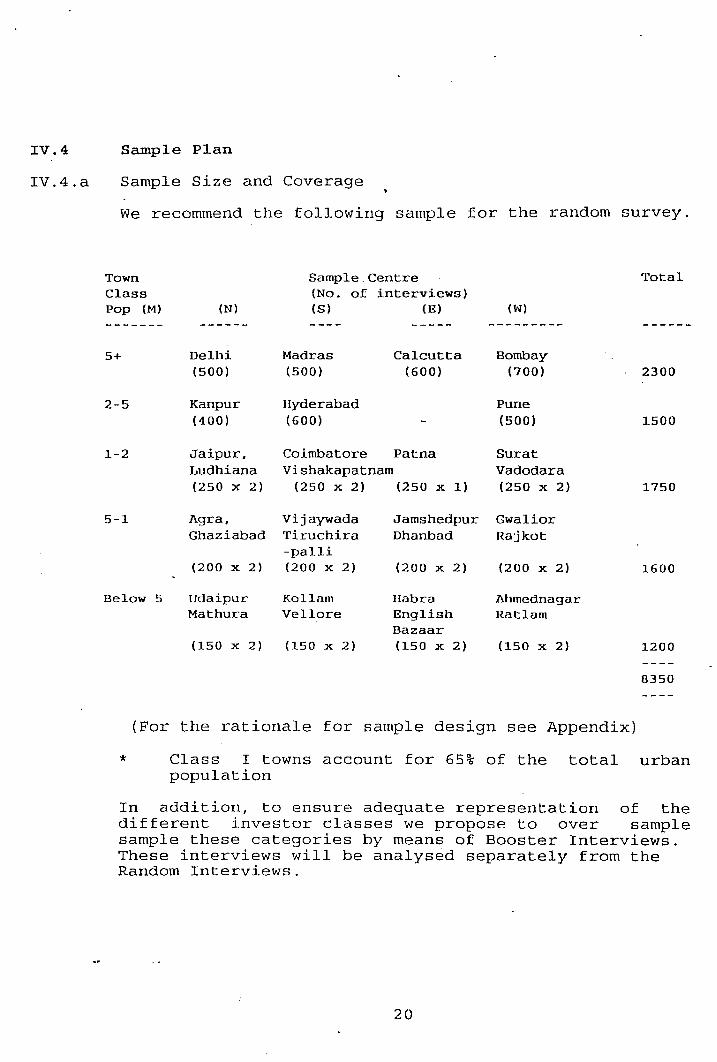

IV.4

IV.4.a

Sample Plan

Sample Size and Coverage

We recommend the following sample for the random survey.

Town Sample. CentreClass (No. of interviews)Pop (M) (N) (S) (E) (W)

------- ------ ---------

5+ Delhi Madras Calcutta Bombay(500) (500) (600) (700)

2-5 Kanpur Hyderabad Pune(400) (600) (500)

1-2 Jaipur, Coimbatore Patna SuratLudhiana Vishakapatnam Vadodara(250 x 2) (250 x 2) (250 x 1) (250 x 2)

5-1 Agra, Vijaywada Jamshedpur GwaliorGhaziabad Tiruchira Dhanbad Rajkot

-palli(200 x 2) (200 x 2) (200 x 2) (200 x 2)

Below 5 Udaipur Kallam Habra AhmcdnagarMathura Vellore English Ratlam

Bazaar(150 x 2) (150 x 2) (150 x 2) (150 x 2)

Total

2300

1500

1750

1600

1200

0350

(For the rationale for sample design see Appendix)

* Class I towns account for 65% of the total urbanpopulation

In addition, to ensure adequate representation of thedifferent investor classes we propose to over samplesample these categories by means of Booster Interviews.These interviews will be analysed separately from theRandom Interviews.

20

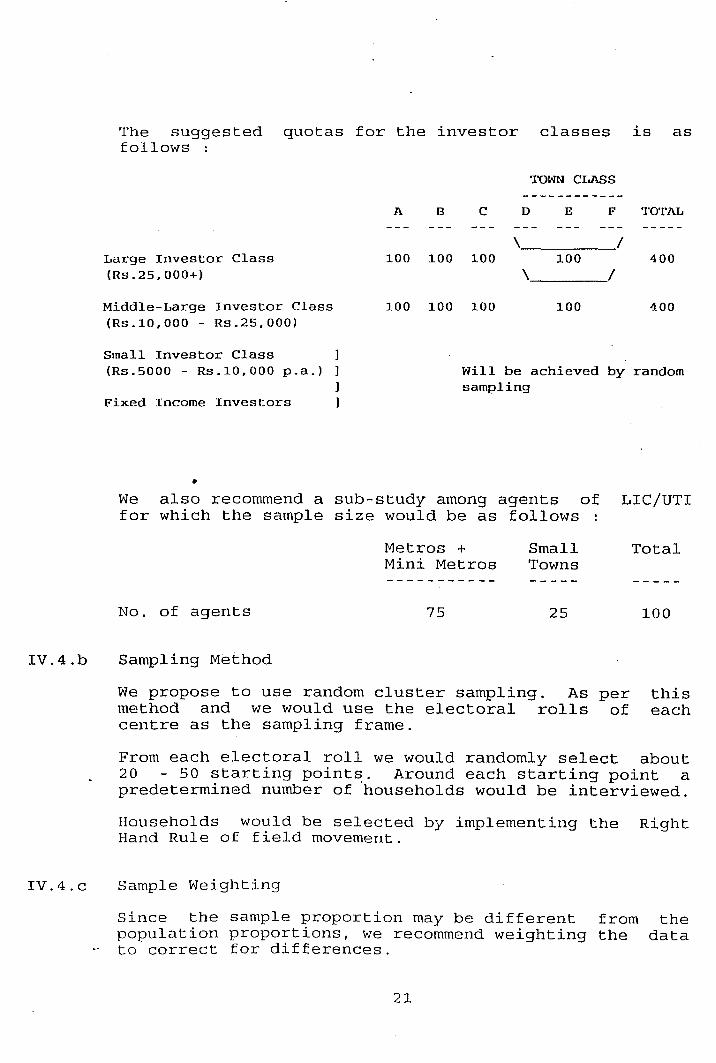

The suggested quotas for the investor classes is asfollows :

TOWN CLASS

A B C D E F TOTAL

Large Investor Class(Rs.25,000+)

Middle-Large Investor Class(RS.l0,000 - Rs.25,000)

100 100 100

100 100 100

\_---_/100

\_--_/

100

400

400

Small Investor Class(Rs.5000 - Rs.l0,000 p.a.)

Fixed Income Investors

•

Will be achieved by randomsampling

We also recommend a sub-study among agents of LIe/UTIfor which the sample size would be as follows

IV.4.b

No. of agents

Sampling Method

Metros +Mini Metros

75

SmallTowns

25

Total

100

We propose to use random cluster sampling. As permethod and we would use the electoral rolls ofcentre as the sampling frame.

thiseach

IV.4.c

From each electoral roll we would randomly select about20 - 50 starting point~. Around each starting point apredetermined number of households would be interviewed.

Households would be selected by implementing the RightHand Rule of field movement.

Sample Weighting

Since the sample proportion may be different frompopulation proportions, we recommend weighting theto correct for differences.

21

thedata

IV.4.d Analysis

The survey would facilitate the analysis of responsesby ;

Town classRegionInvestor typeInvestor classInvestor class x Town class

However it would not facilitate an analyses by

Town class x RegionInvestor class x Region

Recommended analysis techniques are multi dimensionalscaling, St. James's mode~ and Conjoint Analysis.

22

v.

Segment

APPENDIX

INVESTOR SEGMENTATION

Needs Profile

1. Wealthy InformedPlayers 18%

2. Lazy Investor19%

Promoterreputation

Tax benefits

Knowledge

High return/Capitalappreciation

Hassle freeinvestment

Tax benefits

High return/Capitalappreciation

High Income/Wealth

Age 35-50

High/Mediumrisk

High stockmarketparticipation

South IndianTelugu/Malayali

Financialsector

High income

Medium/LowWealth

Young

Medium risk

Low stockmarketparticipation

. East-Bengali

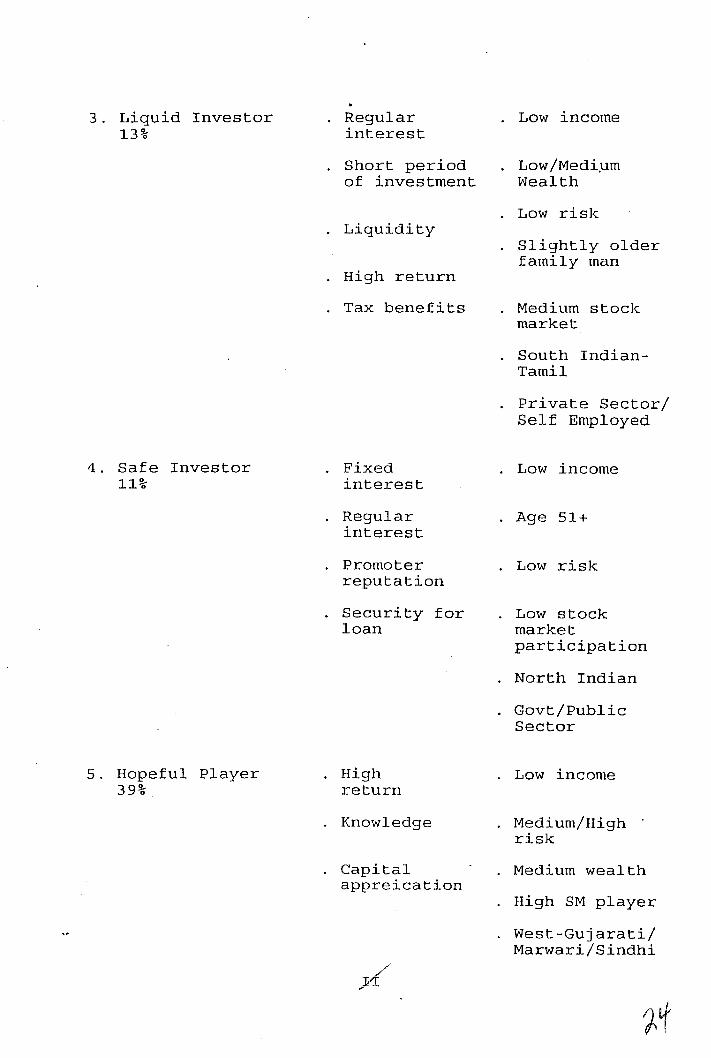

3. Liquid Investor13%

4. Safe Investor11%

5. Hopeful Player39%

Regularinterest

Short periodof investment

Liquidity

High return

Tax benefits

Fixedinterest

Regularinterest

Promoterreputation

Security forloan

Highreturn

Knowledge

Capitalappreication

· Low income

Low /Medi.umWealth

Low risk

Slightly olderfamily man

Medium stockmarket

South IndianTamil

Private Sector/Self Employed

· Low income

· Age 51+

· Low risk

Low stockmarketparticipation

North Indian

Govt/PublicSector

. Low income

Medium/High .risk

Medium wealth

High SM player

West-Gujarati/Marwari/Sindhi

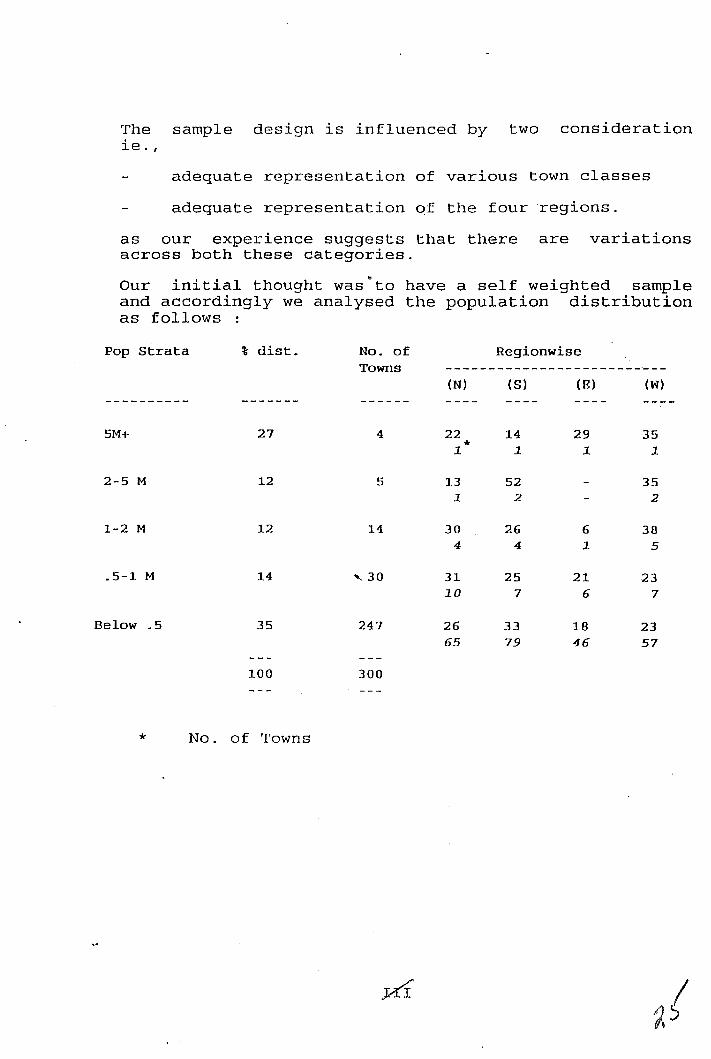

The sample design is influenced by two considerationie. ,

adequate representation of various town classes

adequate representation qf the four regions.

as our experience suggests that there are variationsacross both these categories.

Our initial thought was~to have a self weighted sampleand accordingly we analysed the population distributionas follows

Pop Strata

5M+

2-5 M

1-2 M

.5-1 M

Below .5

%' dist.

27

12

12

14

35

100

No. of RegionwiseTowns -----------------------'---

(N) (8) ( E) (W)------

4 22 14 29 35*l. l. l. 1.

5 13 52 351. 2 2

14 30 26 6 384 4 1. 5

" 30 31 25 21 231.0 7 6 7

247 26 33 18 2365 79 46 57

300

* No. of Towns

However using the same distribution for the sample hadsome drawbacks

i) A large proportion of the interviews would have tobe conducted in the small towns with populationsof less than 5 lakhs. There are move than 200such towns in which HFCs have only a marginalpresence and which is not their immediate targetmarket.

Thus devoting this large proportion of the sampleto this segment would imply either,

inadequate interviews of the middle town.classes ie., with populations of 5 lakhs20 lakhs.

an enlarged sample size with correspondingtime & cost implications.

ii) Inadequate representation in some cells.

This again implied either enhancingsize with time & cost implicationscertain town classes x region cells.

the sampleor ignoring

To overcome these problems the sample design broadlyreflects the population distribution wherever feasibleand where it does not we will weight the dataappropriately.

The towns identified in each cell were selected withthe help of random number tables.