mandalay resources corporation january 2015 investor presentation

TRANSCRIPT

JAN2015

DELIVERING

VALUE AND GROWTH

This presentation contains "forward-looking statements" within the meaning of applicable securities laws, including statements relating to life of

mine production plans, exploration plans and the growth and strategy of Mandalay. Actual results and developments may differ materially from

those contemplated by these statements depending on, among other things: exploration results or production results not meeting management’s

expectations; capital, production and operating cost results not meeting current plans; and changes in commodity prices and general market and

economic conditions. The factors identified above are not intended to represent a complete list of the factors that could affect Mandalay. A

description of additional risks that could result in actual results and developments differing from those contemplated by forward looking

statements in this news release can be found under the heading “Risk Factors” in Mandalay’s annual information form dated March 28, 2014 and

in its final prospectus dated September 2, 2014, copies of which are available under Mandalay's profile at www.sedar.com. Although Mandalay

has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-

looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can be

no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those

anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

Quality Control and AssuranceQuality control and assurance programs are implemented in line with the standards of National Instrument 43-101.

The exploration program at Costerfield is supervised by Chris Gregory (Member, Australian Institute of Geoscientists accredited Chartered

Professional (Mining)), General Manager of Australasian Business Development for Mandalay and a Qualified Person as defined under National

Instrument 43-101. Mr. Gregory regularly visits Costerfield, supervises the collection and interpretation of scientific and technical information

contained in this presentation.

The exploration programs on the Cerro Bayo and La Quebrada projects are supervised by Ronald Luethe (Member: American Institute of

Professional Geologists and an Idaho Registered Professional Geologist), General Manager of Mandalay Chile Ltda. and a Qualified Person as

defined under National Instrument 43-101. Mr. Luethe visits the Cerro Bayo and La Quebrada projects often, supervises the collection and

interpretation of scientific and technical information contained in this presentation.

Dr. Mark Sander (Member: AusIMM), President of Mandalay, has visited the Costerfield, Cerro Bayo, and La Quebrada projects several times

during 2010, 2011, 2012 and 2013 and has supervised the preparation of this presentation. He has also visited the Challacollo project in 2013

and 2014.

All currency references in US$ unless otherwise indicated

Forward-looking Statements

2

15,854 63,351

107,941 126,908

253,796

520,175 633,000

771,500

0

200,000

400,000

600,000

800,000

1,000,000

0

50,000

100,000

150,000

200,000

2010 2011 2012 2013 2014 2015

Oz A

u E

q. Y

ear-

En

d

Re

se

rves

Oz A

u E

q. A

nn

ual

Pro

du

cti

on

2009

• Costerfield, Australia

• Gold & Antimony

2010• Cerro Bayo, Chile

• Silver & Gold

2013

• Challacollo, Chile

• Silver & Gold

2014

• Björkdal, Sweden

• Gold

$3.2 $11.1$20.6

$92.2

$171.8 $166.9

$1.7

$32.0

$79.9$67.7

0

50

100

150

200

2010 2011 2012 2013 2014 (9M)

US

$ M

M

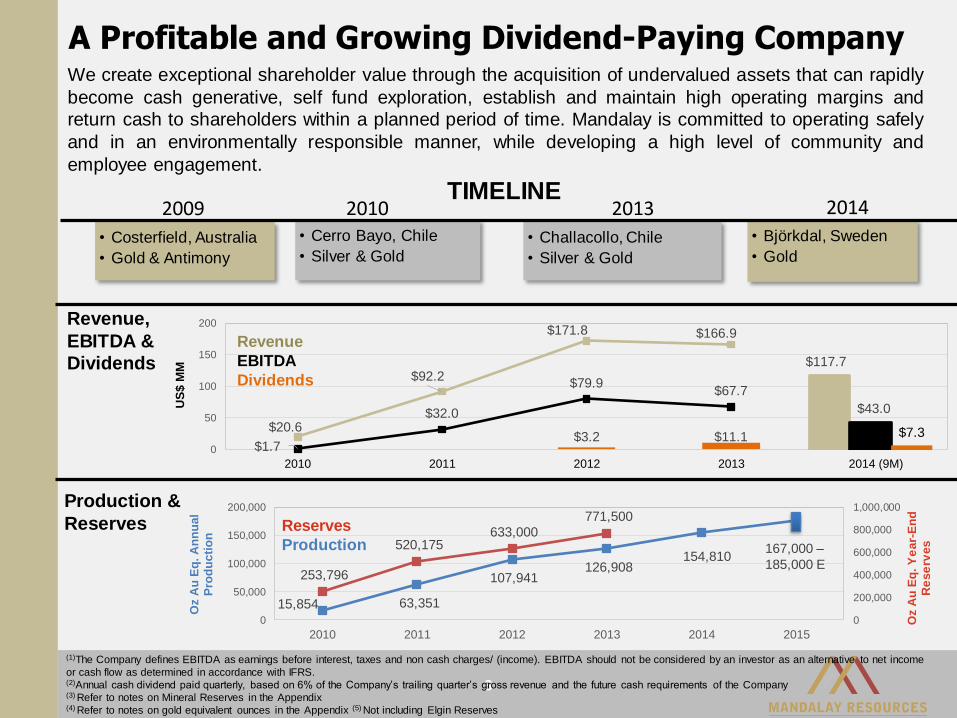

A Profitable and Growing Dividend-Paying Company

3

We create exceptional shareholder value through the acquisition of undervalued assets that can rapidly

become cash generative, self fund exploration, establish and maintain high operating margins and

return cash to shareholders within a planned period of time. Mandalay is committed to operating safely

and in an environmentally responsible manner, while developing a high level of community and

employee engagement.

(1)The Company defines EBITDA as earnings before interest, taxes and non cash charges/ (income). EBITDA should not be considered by an investor as an alternative to net income

or cash flow as determined in accordance with IFRS.(2)Annual cash dividend paid quarterly, based on 6% of the Company’s trailing quarter’s gross revenue and the future cash requirements of the Company(3) Refer to notes on Mineral Reserves in the Appendix(4) Refer to notes on gold equivalent ounces in the Appendix (5) Not including Elgin Reserves

TIMELINE

Production &

Reserves

Revenue,

EBITDA &

Dividends

Revenue

EBITDA

Dividends

$117.7

$43.0

$7.3

Reserves

Production154,810

167,000 –

185,000 E

4

50%

100%

150%

200%

250%

300%

Q3

200

9

Q4

200

9

Q1

201

0

Q2

201

0

Q3

201

0

Q4

201

0

Q1

201

1

Q2

201

1

Q3

201

1

Q4

201

1

Q1

201

2

Q2

201

2

Q3

201

2

Q4

201

2

Q1

201

3

Q2

201

3

Q3

201

3

Q4

201

3

Q1

201

4

Q2

201

4

Q3

201

4

15-N

ov-

14

CU

M %

VA

LUE

CH

AN

GE

SIN

CE

Q3,

200

9

MANDALAY Cumulative Returns 15% Annual Compounded Rate of Return

Gold Silver

MND LAG MND OUTPERFORM

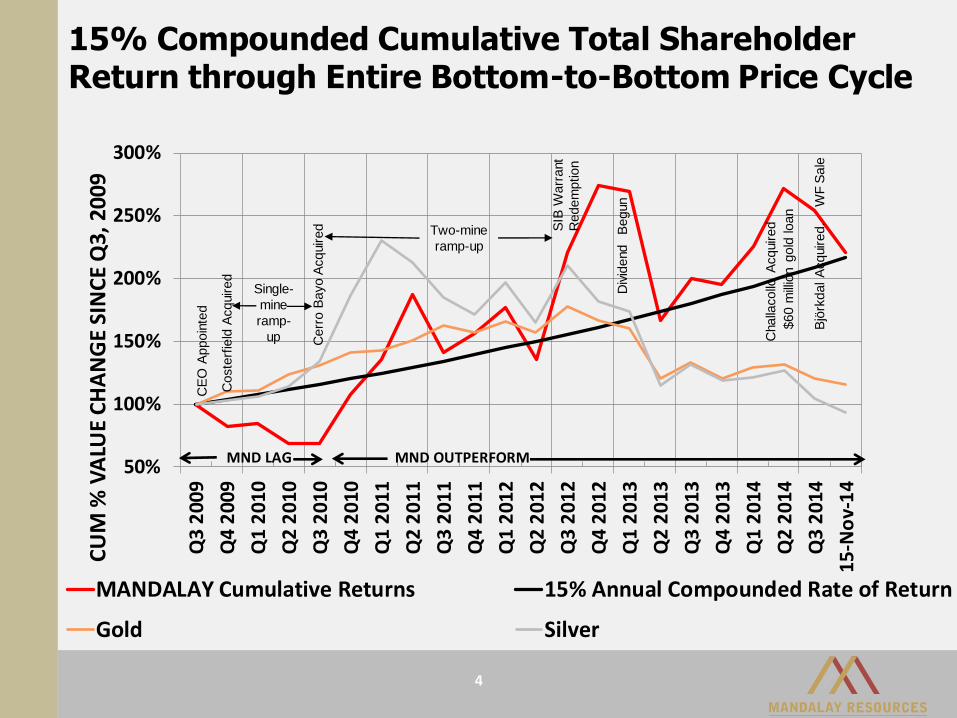

15% Compounded Cumulative Total Shareholder Return through Entire Bottom-to-Bottom Price Cycle

CE

O A

ppoin

ted

Single-

mine

ramp-

up Cerr

o B

ayo

Acquired Two-mine

ramp-up

SIB

Warr

ant

Redem

ption

Div

idend

Begun

Challa

collo

Acquired

$60 m

illio

n g

old

loan

Bjö

rkdal A

cquired.

W

FS

ale

Coste

rfie

ld A

cquired

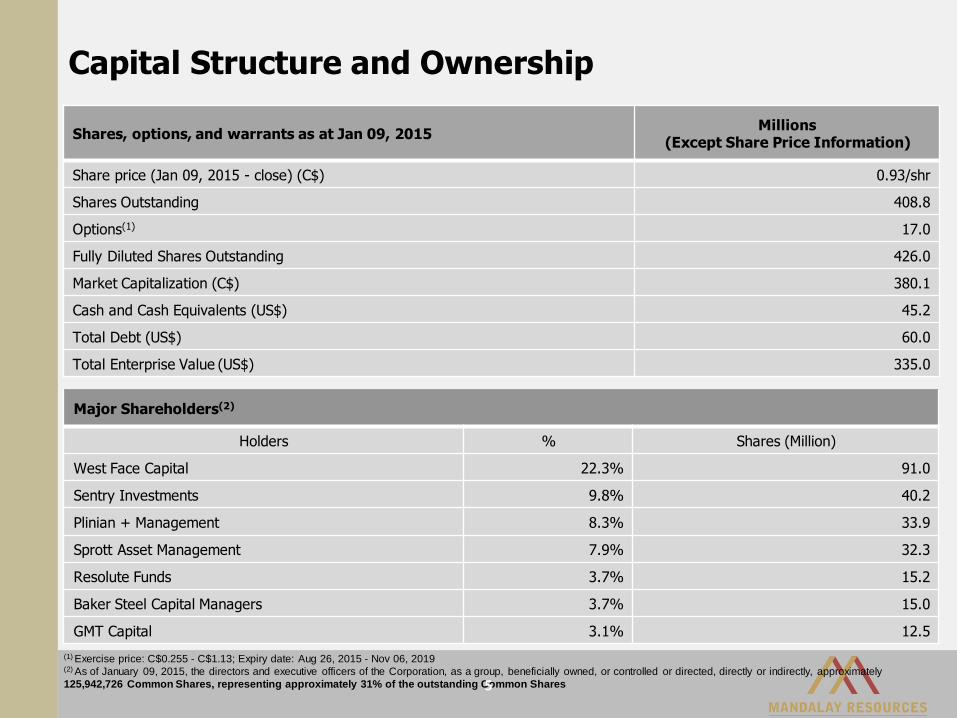

(1) Exercise price: C$0.255 - C$1.13; Expiry date: Aug 26, 2015 - Nov 06, 2019(2) As of January 09, 2015, the directors and executive officers of the Corporation, as a group, beneficially owned, or controlled or directed, directly or indirectly, approximately

125,942,726 Common Shares, representing approximately 31% of the outstanding Common Shares

Capital Structure and Ownership

5

Major Shareholders(2)

Holders % Shares (Million)

West Face Capital 22.3% 91.0

Sentry Investments 9.8% 40.2

Plinian + Management 8.3% 33.9

Sprott Asset Management 7.9% 32.3

Resolute Funds 3.7% 15.2

Baker Steel Capital Managers 3.7% 15.0

GMT Capital 3.1% 12.5

Shares, options, and warrants as at Jan 09, 2015Millions

(Except Share Price Information)

Share price (Jan 09, 2015 - close) (C$) 0.93/shr

Shares Outstanding 408.8

Options(1) 17.0

Fully Diluted Shares Outstanding 426.0

Market Capitalization (C$) 380.1

Cash and Cash Equivalents (US$) 45.2

Total Debt (US$) 60.0

Total Enterprise Value (US$) 335.0

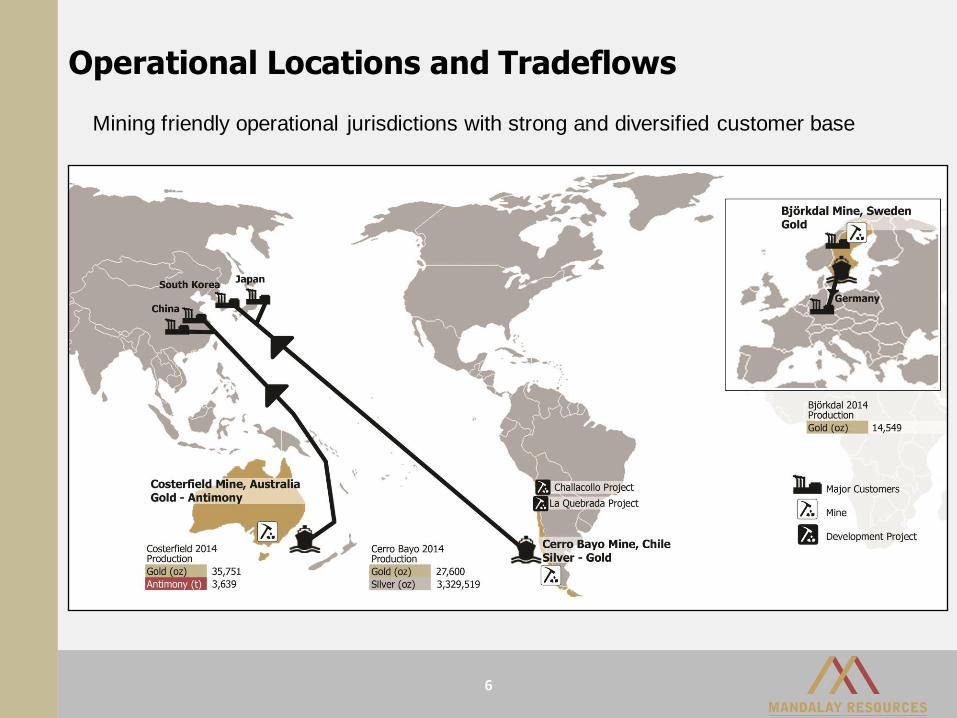

Operational Locations and Tradeflows

6

Mining friendly operational jurisdictions with strong and diversified customer base

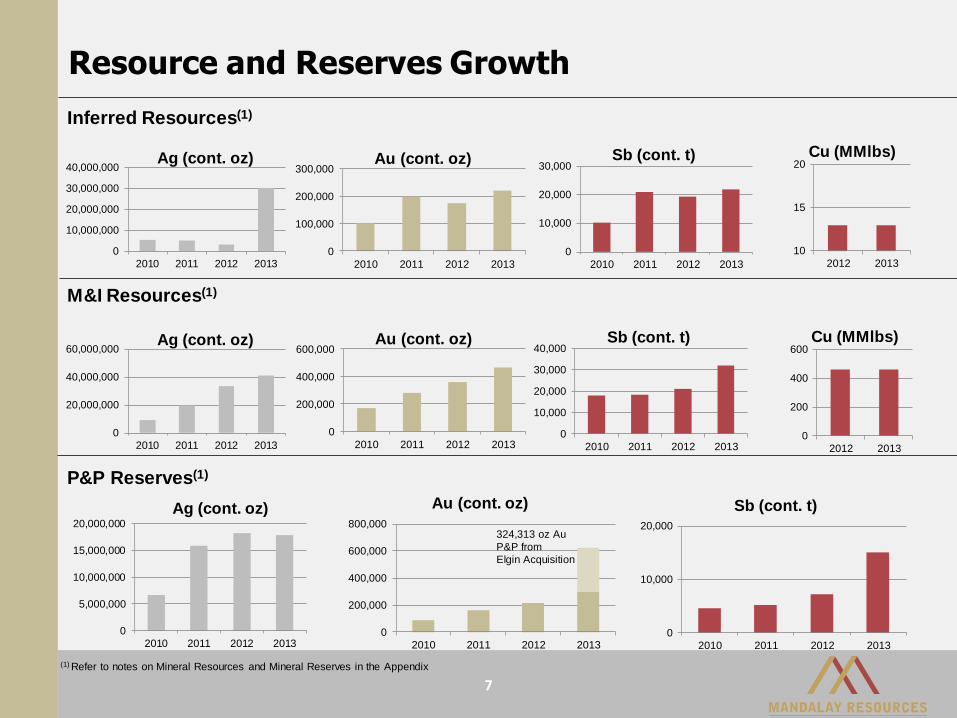

Resource and Reserves Growth

M&I Resources(1)

P&P Reserves(1)

0

20,000,000

40,000,000

60,000,000

2010 2011 2012 2013

Ag (cont. oz)

0

200,000

400,000

600,000

2010 2011 2012 2013

Au (cont. oz)

0

10,000

20,000

30,000

40,000

2010 2011 2012 2013

Sb (cont. t)

(1) Refer to notes on Mineral Resources and Mineral Reserves in the Appendix

0

200

400

600

2012 2013

Cu (MMlbs)

0

5,000,000

10,000,000

15,000,000

20,000,000

2010 2011 2012 2013

Ag (cont. oz)

0

200,000

400,000

600,000

800,000

2010 2011 2012 2013

Au (cont. oz)

0

10,000

20,000

2010 2011 2012 2013

Sb (cont. t)

324,313 oz Au

P&P from

Elgin Acquisition

Inferred Resources(1)

0

10,000,000

20,000,000

30,000,000

40,000,000

2010 2011 2012 2013

Ag (cont. oz)

0

100,000

200,000

300,000

2010 2011 2012 2013

Au (cont. oz)

0

10,000

20,000

30,000

2010 2011 2012 2013

Sb (cont. t)

10

15

20

2012 2013

Cu (MMlbs)

7

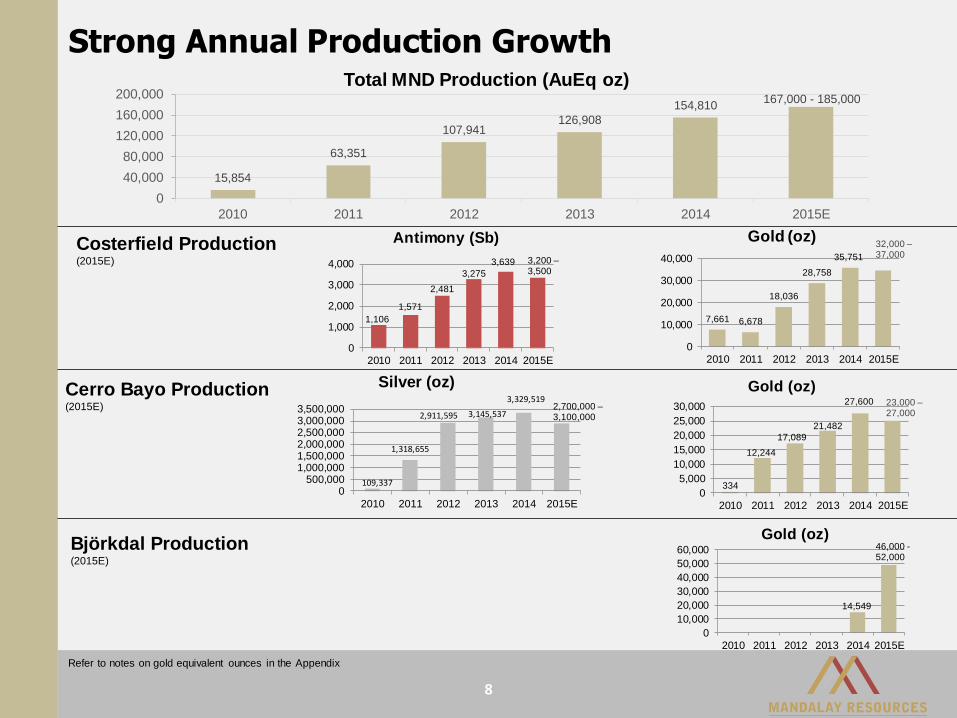

Strong Annual Production Growth

8

109,337

1,318,655

2,911,595 3,145,537

3,329,519

0500,000

1,000,0001,500,0002,000,0002,500,0003,000,0003,500,000

2010 2011 2012 2013 2014 2015E

Silver (oz)

334

12,244

17,089

21,482

27,600

0

5,000

10,000

15,000

20,000

25,000

30,000

2010 2011 2012 2013 2014 2015E

Gold (oz)

7,661 6,678

18,036

28,758

35,751

0

10,000

20,000

30,000

40,000

2010 2011 2012 2013 2014 2015E

Gold (oz)Costerfield Production(2015E)

Cerro Bayo Production(2015E)

1,106

1,571

2,481

3,275

3,639

0

1,000

2,000

3,000

4,000

2010 2011 2012 2013 2014 2015E

Antimony (Sb)

Björkdal Production(2015E)

14,549

0

10,000

20,000

30,000

40,000

50,000

60,000

2010 2011 2012 2013 2014 2015E

Gold (oz)

15,854

63,351

107,941126,908

154,810

0

40,000

80,000

120,000

160,000

200,000

2010 2011 2012 2013 2014 2015E

Total MND Production (AuEq oz)

Refer to notes on gold equivalent ounces in the Appendix

167,000 - 185,000

32,000 –37,000

23,000 –27,000

46,000 -52,000

3,200 –3,500

2,700,000 –3,100,000

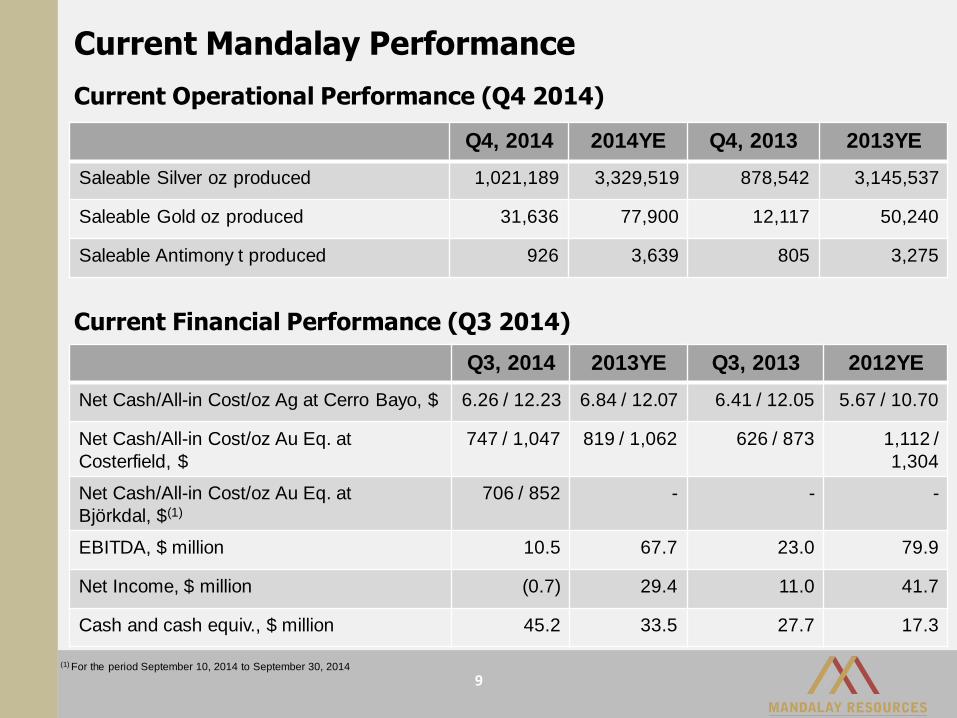

Current Financial Performance (Q3 2014)

9

Current Operational Performance (Q4 2014)

Q4, 2014 2014YE Q4, 2013 2013YE

Saleable Silver oz produced 1,021,189 3,329,519 878,542 3,145,537

Saleable Gold oz produced 31,636 77,900 12,117 50,240

Saleable Antimony t produced 926 3,639 805 3,275

Q3, 2014 2013YE Q3, 2013 2012YE

Net Cash/All-in Cost/oz Ag at Cerro Bayo, $ 6.26 / 12.23 6.84 / 12.07 6.41 / 12.05 5.67 / 10.70

Net Cash/All-in Cost/oz Au Eq. at

Costerfield, $

747 / 1,047 819 / 1,062 626 / 873 1,112 /

1,304

Net Cash/All-in Cost/oz Au Eq. at

Björkdal, $(1)

706 / 852 - - -

EBITDA, $ million 10.5 67.7 23.0 79.9

Net Income, $ million (0.7) 29.4 11.0 41.7

Cash and cash equiv., $ million 45.2 33.5 27.7 17.3

Current Mandalay Performance

(1) For the period September 10, 2014 to September 30, 2014

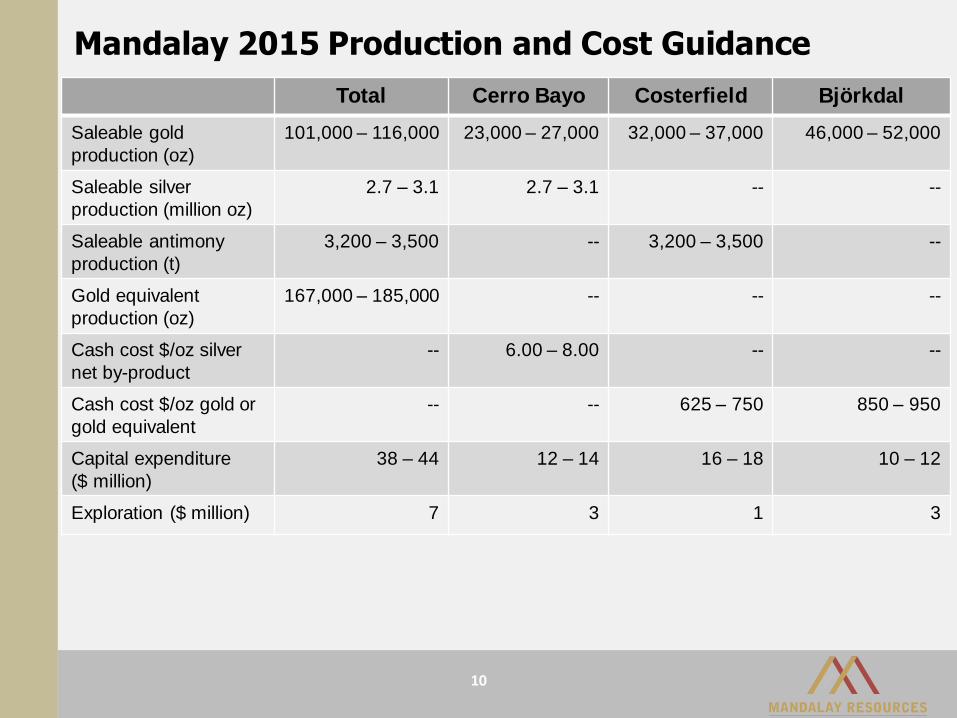

10

Total Cerro Bayo Costerfield Björkdal

Saleable gold

production (oz)

101,000 – 116,000 23,000 – 27,000 32,000 – 37,000 46,000 – 52,000

Saleable silver

production (million oz)

2.7 – 3.1 2.7 – 3.1 -- --

Saleable antimony

production (t)

3,200 – 3,500 -- 3,200 – 3,500 --

Gold equivalent

production (oz)

167,000 – 185,000 -- -- --

Cash cost $/oz silver

net by-product

-- 6.00 – 8.00 -- --

Cash cost $/oz gold or

gold equivalent

-- -- 625 – 750 850 – 950

Capital expenditure

($ million)

38 – 44 12 – 14 16 – 18 10 – 12

Exploration ($ million) 7 3 1 3

Mandalay 2015 Production and Cost Guidance

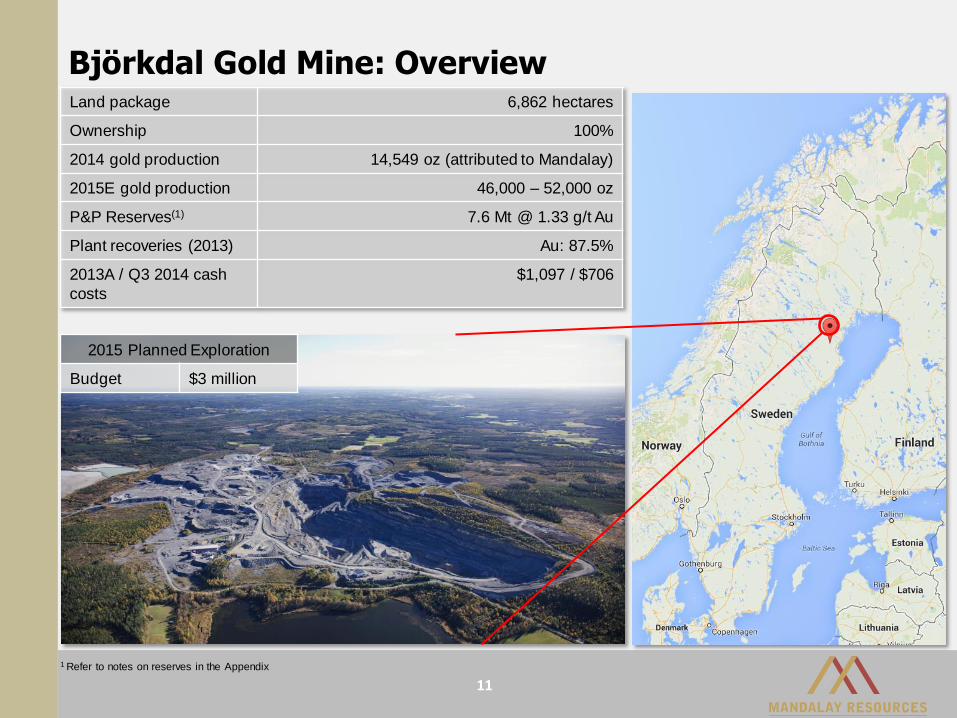

Björkdal Gold Mine: Overview

11

Land package 6,862 hectares

Ownership 100%

2014 gold production 14,549 oz (attributed to Mandalay)

2015E gold production 46,000 – 52,000 oz

P&P Reserves(1) 7.6 Mt @ 1.33 g/t Au

Plant recoveries (2013) Au: 87.5%

2013A / Q3 2014 cash

costs

$1,097 / $706

1 Refer to notes on reserves in the Appendix

2015 Planned Exploration

Budget $3 million

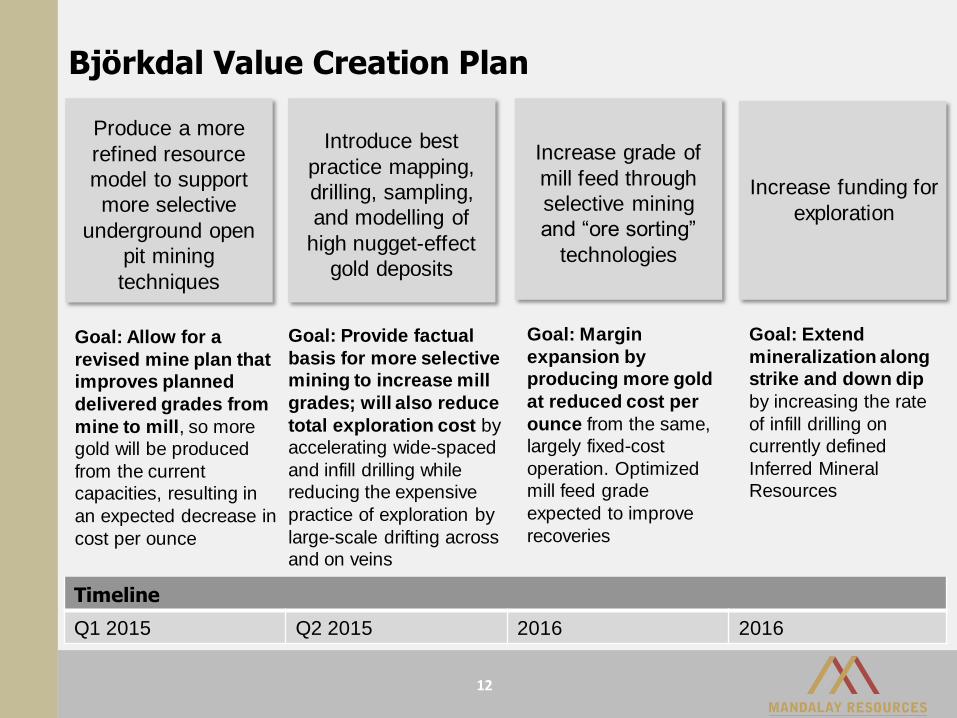

Björkdal Value Creation Plan

12

Goal: Allow for a

revised mine plan that

improves planned

delivered grades from

mine to mill, so more

gold will be produced

from the current

capacities, resulting in

an expected decrease in

cost per ounce

Produce a more

refined resource

model to support

more selective

underground open

pit mining

techniques

Goal: Margin

expansion by

producing more gold

at reduced cost per

ounce from the same,

largely fixed-cost

operation. Optimized

mill feed grade

expected to improve

recoveries

Increase grade of

mill feed through

selective mining

and “ore sorting”

technologies

Goal: Extend

mineralization along

strike and down dip

by increasing the rate

of infill drilling on

currently defined

Inferred Mineral

Resources

Increase funding for

exploration

Introduce best

practice mapping,

drilling, sampling,

and modelling of

high nugget-effect

gold deposits

Goal: Provide factual

basis for more selective

mining to increase mill

grades; will also reduce

total exploration cost by

accelerating wide-spaced

and infill drilling while

reducing the expensive

practice of exploration by

large-scale drifting across

and on veins

Timeline

Q1 2015 Q2 2015 2016 2016

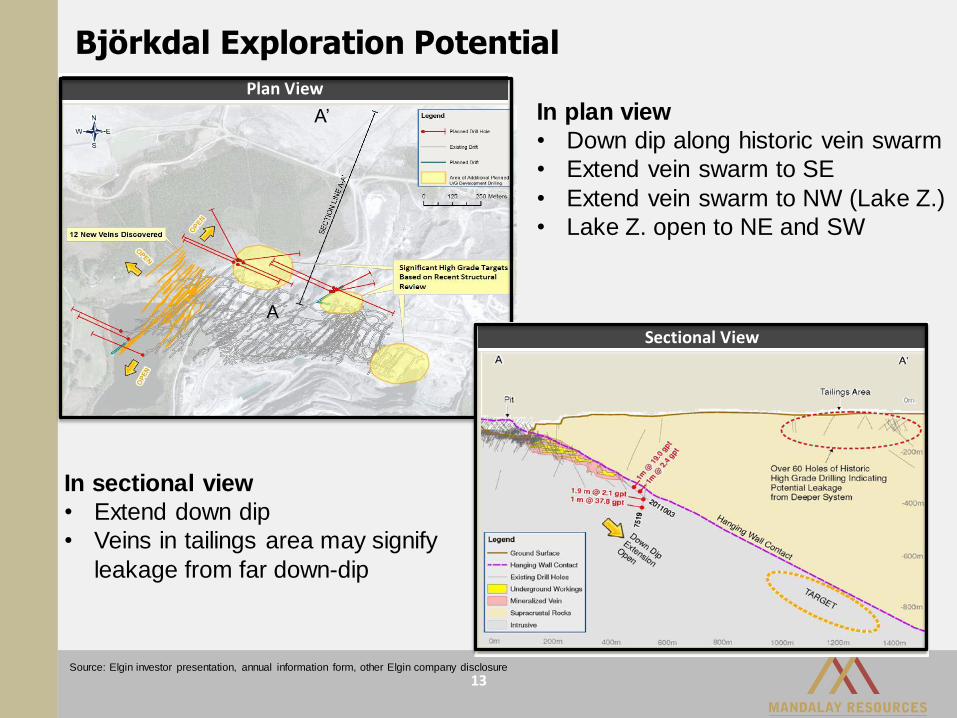

13

Plan View

Björkdal Exploration Potential

Source: Elgin investor presentation, annual information form, other Elgin company disclosure

A

A’

Sectional View

In plan view

• Down dip along historic vein swarm

• Extend vein swarm to SE

• Extend vein swarm to NW (Lake Z.)

• Lake Z. open to NE and SW

In sectional view

• Extend down dip

• Veins in tailings area may signify

leakage from far down-dip

Cerro Bayo Silver-Gold Mine

14

Land package 23,106 hectares

Ownership 100%

2014 silver production 3,329,519 oz

2014 gold production 27,600 oz

2015E silver production 2.7 – 3.1 Moz

2015E gold production 23,000 – 27,000 oz

P&P Reserves 2.5 Mt @ 224 g/t Ag; 2.2 g/t Au

Plant recoveries (Q3 2014) Ag: 92.66%, Au: 89.93%

2013A Cash costs/oz Ag

net Au credits / Q3 2014

$6.84 / $6.26

2015 Planned Exploration

Budget $3 million

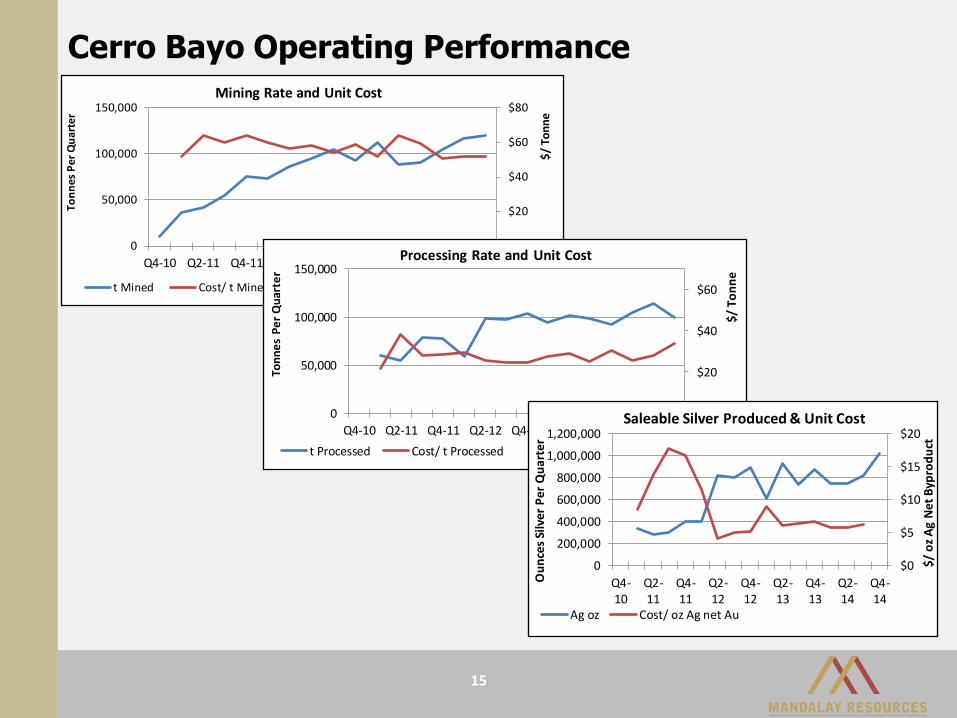

Cerro Bayo Operating Performance

15

$0

$20

$40

$60

$80

0

50,000

100,000

150,000

Q4-10 Q2-11 Q4-11 Q2-12 Q4-12 Q2-2013

Q4-2013

Q2-2014

$/

Ton

ne

Ton

nes

Per

Qu

arte

r

Mining Rate and Unit Cost

t Mined Cost/ t Mined

$0

$20

$40

$60

0

50,000

100,000

150,000

Q4-10 Q2-11 Q4-11 Q2-12 Q4-12 Q2-13 Q4-13 Q2-14

$/ T

on

ne

Ton

ne

s P

er

Qu

arte

r

Processing Rate and Unit Cost

t Processed Cost/ t Processed

$0

$5

$10

$15

$20

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Q4-10

Q2-11

Q4-11

Q2-12

Q4-12

Q2-13

Q4-13

Q2-14

Q4-14

$/ o

z A

g N

et B

ypro

du

ct

Ou

nce

s Si

lver

Per

Qu

arte

r

Saleable Silver Produced & Unit Cost

Ag oz Cost/ oz Ag net Au

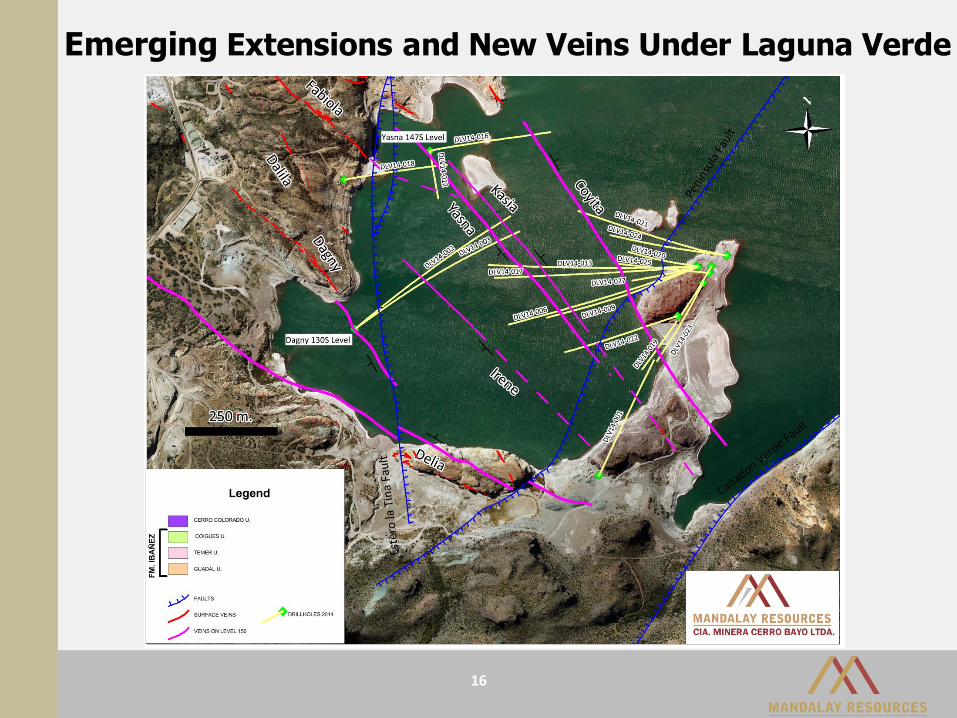

LAGUNA VERDE

Emerging Extensions and New Veins Under Laguna Verde

16

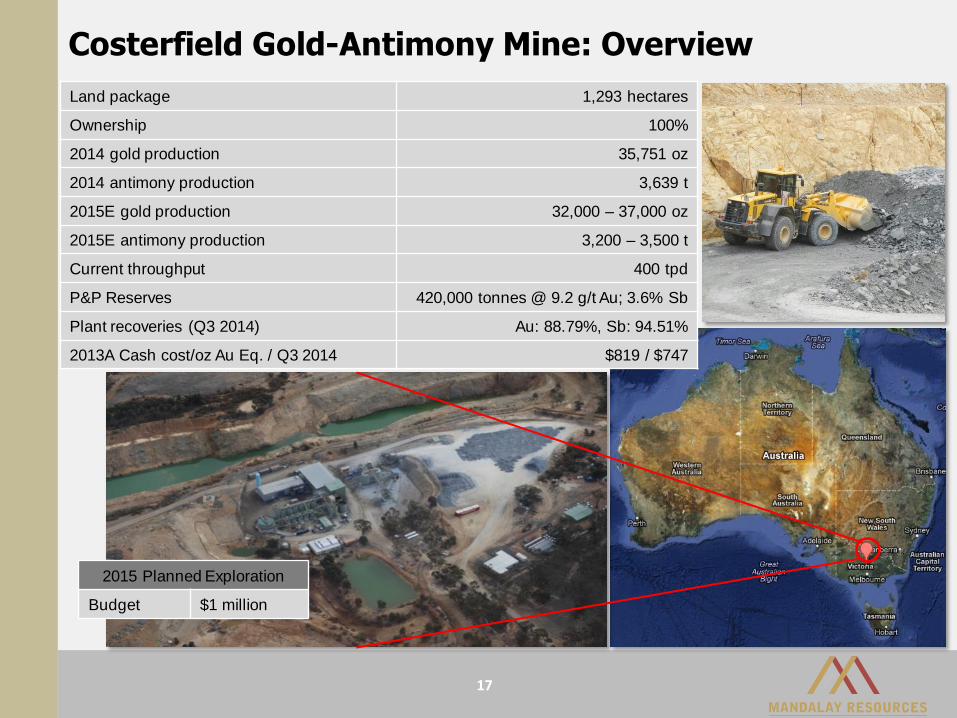

Costerfield Gold-Antimony Mine: Overview

17

2015 Planned Exploration

Budget $1 million

Land package 1,293 hectares

Ownership 100%

2014 gold production 35,751 oz

2014 antimony production 3,639 t

2015E gold production 32,000 – 37,000 oz

2015E antimony production 3,200 – 3,500 t

Current throughput 400 tpd

P&P Reserves 420,000 tonnes @ 9.2 g/t Au; 3.6% Sb

Plant recoveries (Q3 2014) Au: 88.79%, Sb: 94.51%

2013A Cash cost/oz Au Eq. / Q3 2014 $819 / $747

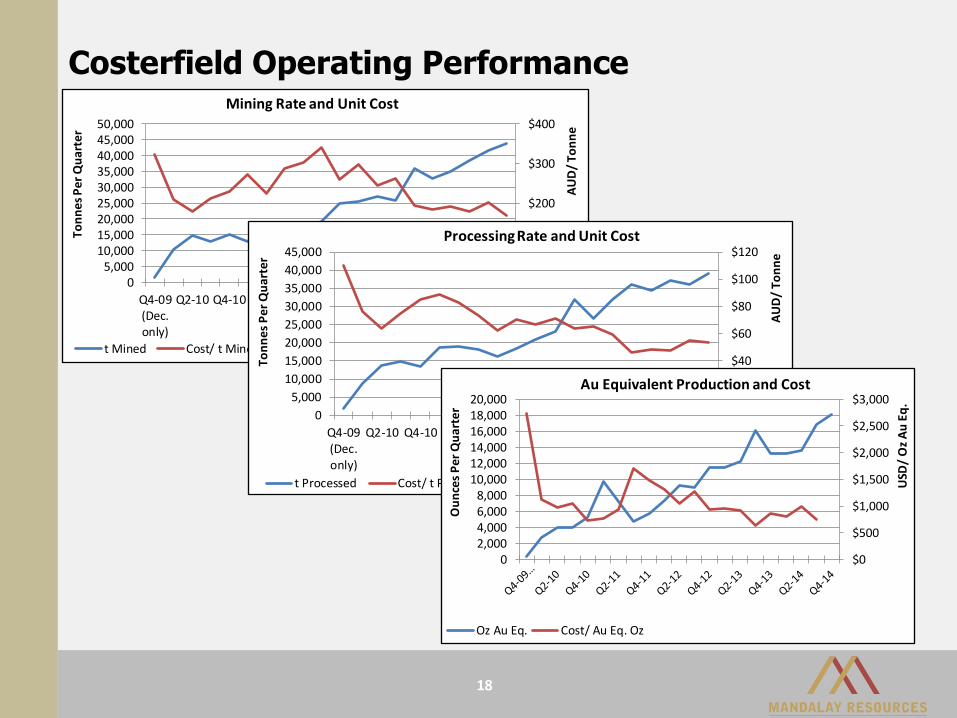

Costerfield Operating Performance

18

$0

$100

$200

$300

$400

05,000

10,00015,00020,00025,00030,00035,00040,00045,00050,000

Q4-09(Dec.only)

Q2-10 Q4-10 Q2-11 Q4-11 Q2-12 Q4-12 Q2-13 Q4-13 Q2-14

AU

D/

Ton

ne

Ton

nes

Per

Qu

arte

r

Mining Rate and Unit Cost

t Mined Cost/ t Mined

$0

$20

$40

$60

$80

$100

$120

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Q4-09(Dec.only)

Q2-10 Q4-10 Q2-11 Q4-11 Q2-12 Q4-12 Q2-13 Q4-13 Q2-14

AU

D/

Ton

ne

Ton

ne

s P

er

Qu

art

er

Processing Rate and Unit Cost

t Processed Cost/ t Processed

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

USD

/ O

z A

u E

q.

Ou

nce

s P

er Q

uar

ter

Au Equivalent Production and Cost

Oz Au Eq. Cost/ Au Eq. Oz

Challacollo Silver-Gold Project: Overview

19

Land package 20,378 hectares

Ownership 100%

Location 130 km SE of Iquique, Chile

Mineralization Epithermal, oxidized Ag-Au

Elevation approx. 1,500 metres ASL

Resource Indicated: 1 mt @ 242 g/t Ag;

Inferred: 4 mt @193 g/t Ag

20

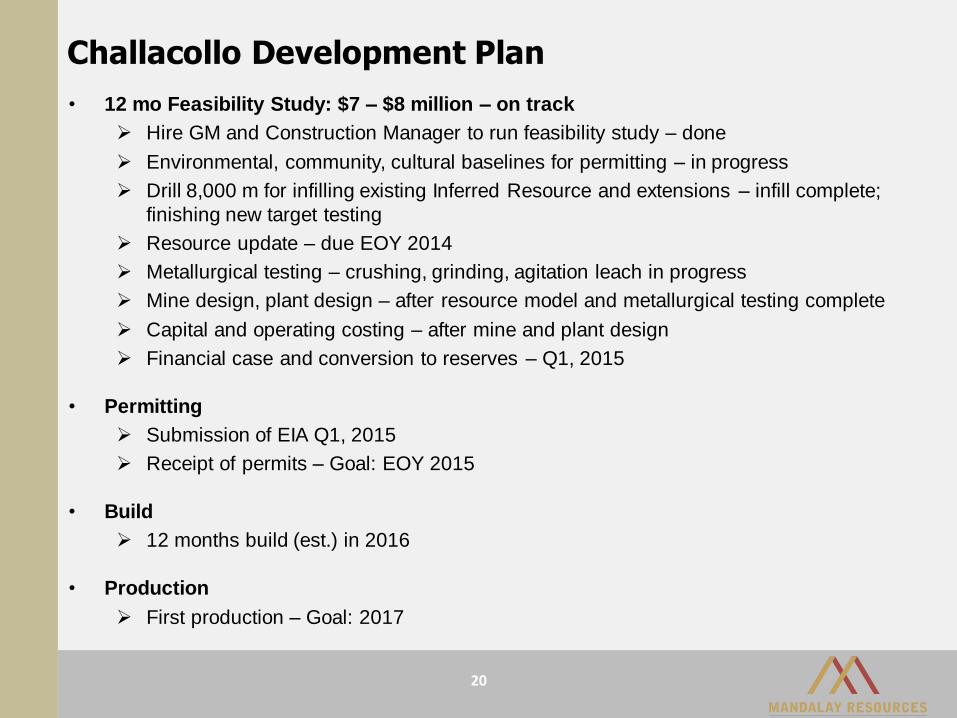

• 12 mo Feasibility Study: $7 – $8 million – on track

Hire GM and Construction Manager to run feasibility study – done

Environmental, community, cultural baselines for permitting – in progress

Drill 8,000 m for infilling existing Inferred Resource and extensions – infill complete;

finishing new target testing

Resource update – due EOY 2014

Metallurgical testing – crushing, grinding, agitation leach in progress

Mine design, plant design – after resource model and metallurgical testing complete

Capital and operating costing – after mine and plant design

Financial case and conversion to reserves – Q1, 2015

• Permitting

Submission of EIA Q1, 2015

Receipt of permits – Goal: EOY 2015

• Build

12 months build (est.) in 2016

• Production

First production – Goal: 2017

Challacollo Development Plan

21

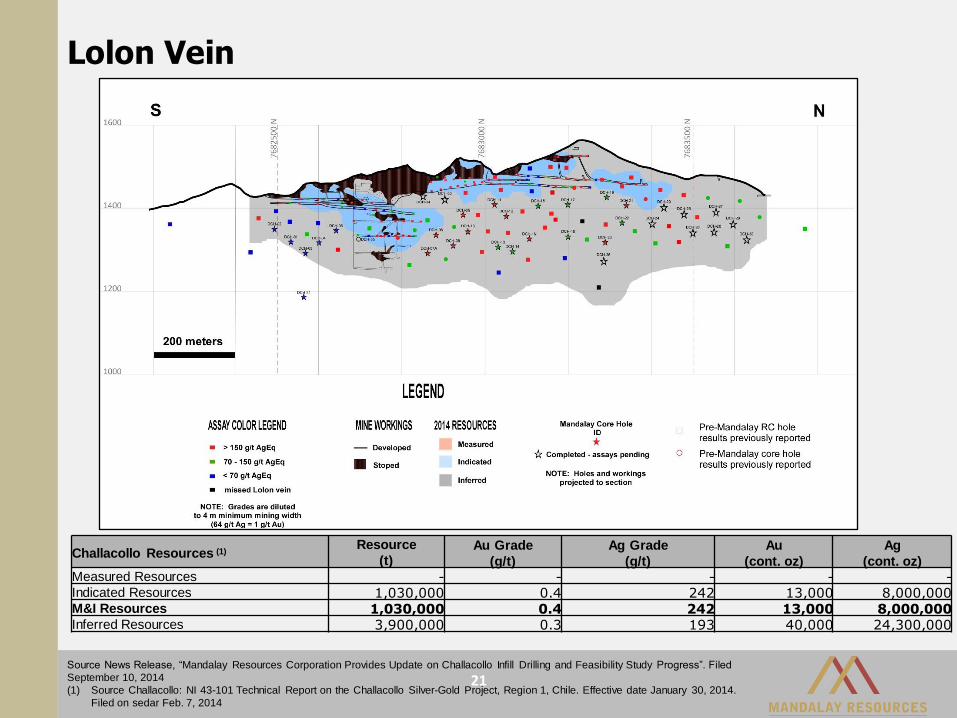

Lolon Vein

Challacollo Resources (1)Resource

(t)Au Grade

(g/t)

Ag Grade

(g/t)

Au

(cont. oz)

Ag

(cont. oz)Measured Resources - - - - -Indicated Resources 1,030,000 0.4 242 13,000 8,000,000 M&I Resources 1,030,000 0.4 242 13,000 8,000,000 Inferred Resources 3,900,000 0.3 193 40,000 24,300,000

Source News Release, “Mandalay Resources Corporation Provides Update on Challacollo Infill Drilling and Feasibility Study Progress”. Filed

September 10, 2014

(1) Source Challacollo: NI 43-101 Technical Report on the Challacollo Silver-Gold Project, Region 1, Chile. Effective date January 30, 2014.

Filed on sedar Feb. 7, 2014

MND (221% value change) outperformed through the entire 2009-2014 bottom-to-bottom price cycle:

• Entire set of Currencies (85-111%)

• Entire set of Precious Metals (92-115%)

• Entire set of Base Metals (88-117%)

• Entire Big Diversified category(49-131%)

• Entire Prospect Generator category (48-196%)

• Entire Royalty/Streaming category (71-209%)

• Entire Gold Mutual Fund category (53-69%)

• Entire Resource Mutual Fund category (113-191%)

• Entire Mega Gold category (35-54%)

• All but 1 Big Gold company (13-251%)

• All but 2 Mid Tier Gold companies (17-2700%)

• Entire set of Junior Gold companies (28-160%)

• All but 2 Gold Development companies (13-776%)

• All but 1 Big Silver company (21-314%)

• Entire Mid Tier Silver category (31-104%)

• Entire set of Junior silver producers (32-110%)

• Entire set of Silver Developers (6-132%)

• Entire set of Big Copper companies (101-213%)

• Entire set of Mid-Tier Base Metals companies (17-198%)

• Entire set of Base Metals developers (16-62%)

• Entire PGM space (5-196%)

22

• Mandalay vs.:

• 125 alternative investments

• In 21 different strategy

categories

• Over the 21 quarters from

Q3-2009 to Nov. 15, 2014

(period that Plinian has led

Mandalay)

• Value metric is:

• Common shareholder equity

value assuming market

purchase of shares,

excluding warrants and

special dividends but

including ordinary dividends

and stock splits

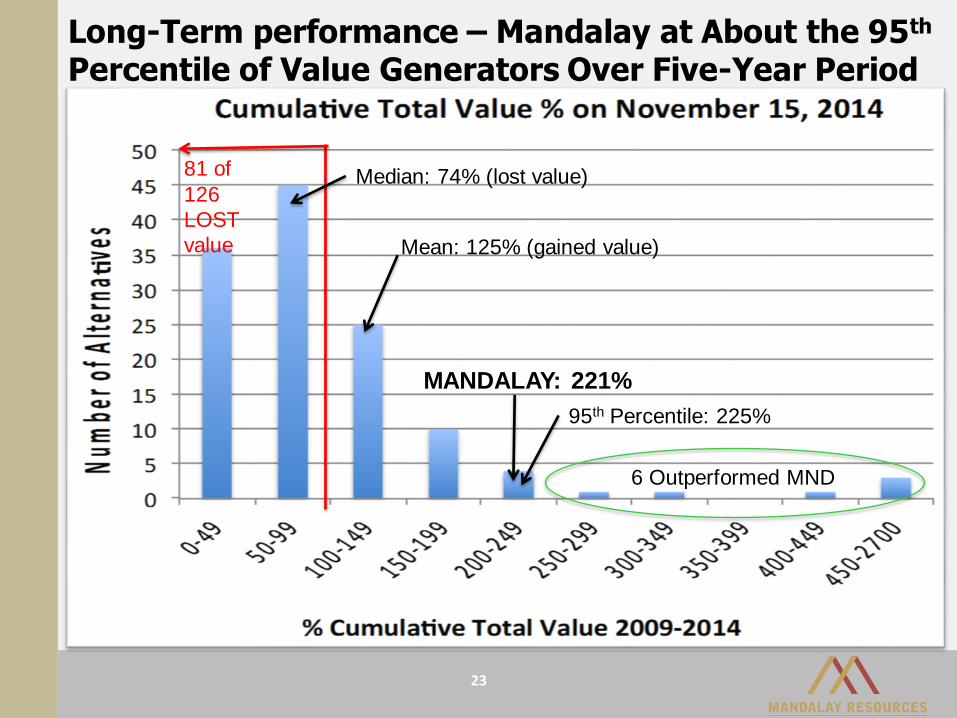

Long-Term performance – Mandalay at About the 95th

Percentile of Value Generators Over Five-Year Period

23

81 of

126

LOST

value Mean: 125% (gained value)

Median: 74% (lost value)

95th Percentile: 225%

MANDALAY: 221%

6 Outperformed MND

24

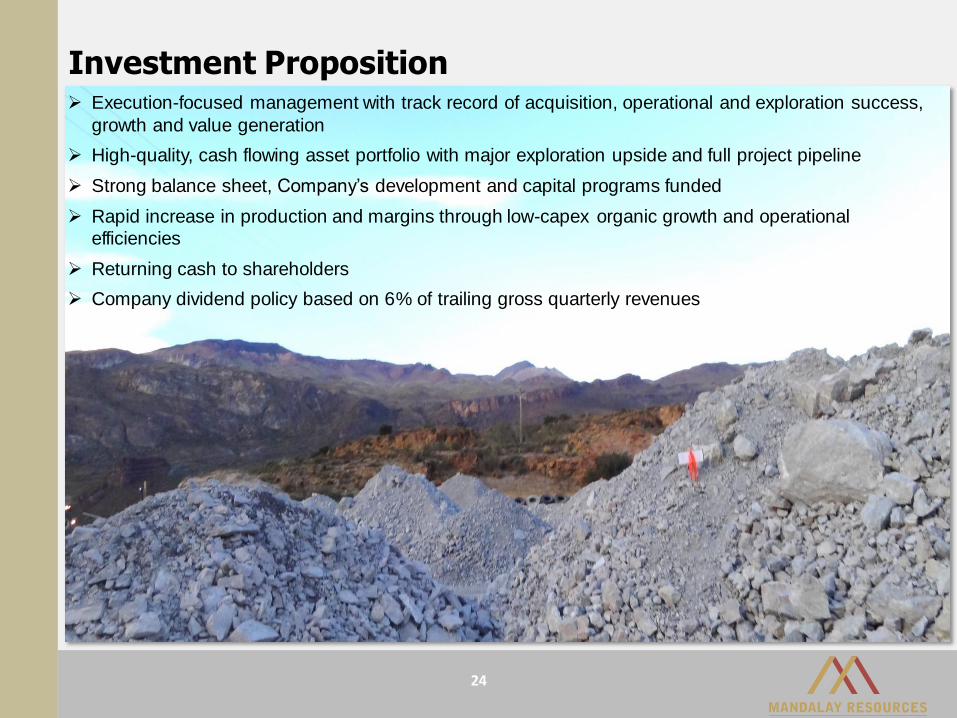

Investment Proposition Execution-focused management with track record of acquisition, operational and exploration success,

growth and value generation

High-quality, cash flowing asset portfolio with major exploration upside and full project pipeline

Strong balance sheet, Company’s development and capital programs funded

Rapid increase in production and margins through low-capex organic growth and operational

efficiencies

Returning cash to shareholders

Company dividend policy based on 6% of trailing gross quarterly revenues

JAN2015

DELIVERING

VALUE AND GROWTH

For more information, please contact:

Greg DiTomaso

Director, Investor Relations

Tel: 647.260.1566

Email: [email protected]

Company Website: www.mandalayresources.com

Twitter: @MandalayAuAg

26

Management and Board of Directors

Senior Management

Board of Directors

Brad Mills, CEO and

Executive Director

Former CEO Lonmin

plc, over 30 years of

experience in Copper,

Gold, PGMs

Mark Sander, President

28 years of experience in

exploration, strategy and

operating improvements

Sanjay Swarup, CFO

and Executive Director

Former Lonmin plc, over

20 years of industry

experience

Belinda Labatte,

Head of Stakeholder

Engagement & Corporate

Affairs

Over 10 years of experience

in capital markets

Braam Jonker,

Chairman

Peter R. Jones,

Independent Director

Tony Griffin,

Independent Director

Robert Doyle,

Independent Director

Dominic Duffy, COO

Mining Engineer with

extensive technical and

operational management

experience

Numbers may differ slightly from source documents due to rounding

27

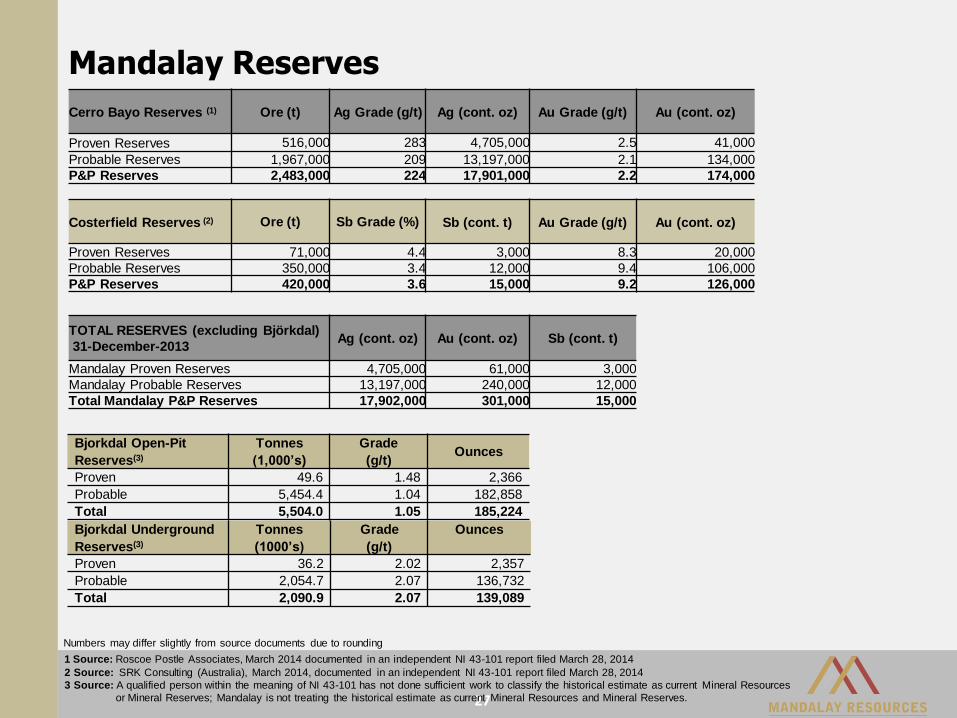

Mandalay Reserves

Cerro Bayo Reserves (1) Ore (t) Ag Grade (g/t) Ag (cont. oz) Au Grade (g/t) Au (cont. oz)

Proven Reserves 516,000 283 4,705,000 2.5 41,000

Probable Reserves 1,967,000 209 13,197,000 2.1 134,000

P&P Reserves 2,483,000 224 17,901,000 2.2 174,000

Costerfield Reserves (2) Ore (t) Sb Grade (%) Sb (cont. t) Au Grade (g/t) Au (cont. oz)

Proven Reserves 71,000 4.4 3,000 8.3 20,000

Probable Reserves 350,000 3.4 12,000 9.4 106,000

P&P Reserves 420,000 3.6 15,000 9.2 126,000

TOTAL RESERVES (excluding Björkdal)

31-December-2013Ag (cont. oz) Au (cont. oz) Sb (cont. t)

Mandalay Proven Reserves 4,705,000 61,000 3,000

Mandalay Probable Reserves 13,197,000 240,000 12,000

Total Mandalay P&P Reserves 17,902,000 301,000 15,000

1 Source: Roscoe Postle Associates, March 2014 documented in an independent NI 43-101 report filed March 28, 2014

2 Source: SRK Consulting (Australia), March 2014, documented in an independent NI 43-101 report filed March 28, 2014

3 Source: A qualified person within the meaning of NI 43-101 has not done sufficient work to classify the historical estimate as current Mineral Resources

or Mineral Reserves; Mandalay is not treating the historical estimate as current Mineral Resources and Mineral Reserves.

Bjorkdal Open-Pit

Reserves(3)

Tonnes

(1,000’s)

Grade

(g/t)Ounces

Proven 49.6 1.48 2,366

Probable 5,454.4 1.04 182,858

Total 5,504.0 1.05 185,224

Bjorkdal Underground

Reserves(3)

Tonnes

(1000’s)

Grade

(g/t)

Ounces

Proven 36.2 2.02 2,357

Probable 2,054.7 2.07 136,732

Total 2,090.9 2.07 139,089

28

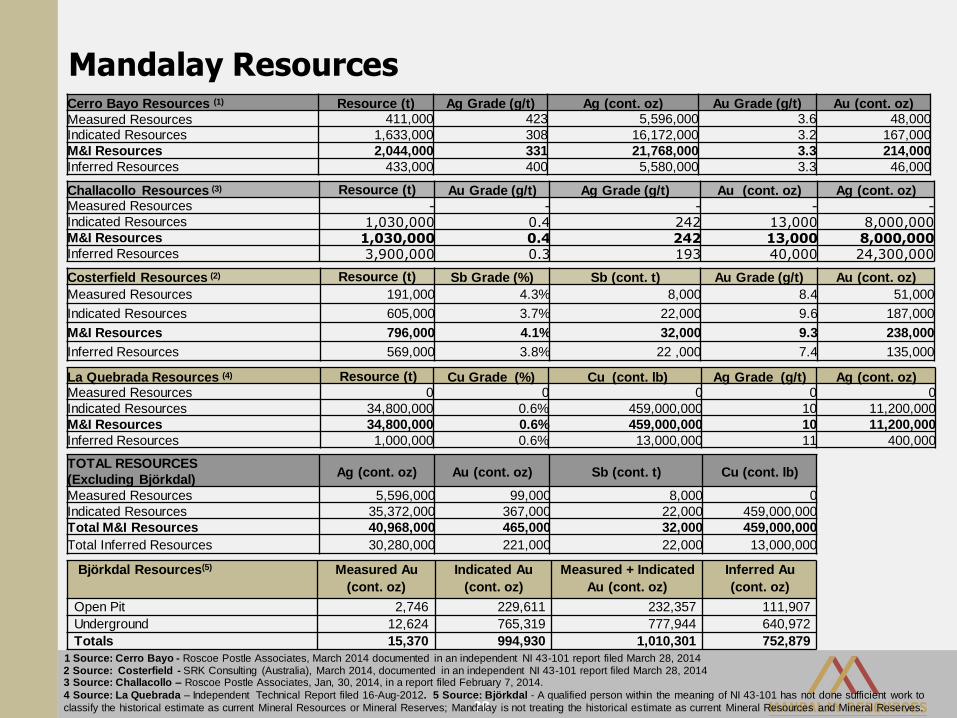

Mandalay ResourcesCerro Bayo Resources (1) Resource (t) Ag Grade (g/t) Ag (cont. oz) Au Grade (g/t) Au (cont. oz)

Measured Resources 411,000 423 5,596,000 3.6 48,000

Indicated Resources 1,633,000 308 16,172,000 3.2 167,000

M&I Resources 2,044,000 331 21,768,000 3.3 214,000

Inferred Resources 433,000 400 5,580,000 3.3 46,000

Costerfield Resources (2) Resource (t) Sb Grade (%) Sb (cont. t) Au Grade (g/t) Au (cont. oz)

Measured Resources 191,000 4.3% 8,000 8.4 51,000

Indicated Resources 605,000 3.7% 22,000 9.6 187,000

M&I Resources 796,000 4.1% 32,000 9.3 238,000

Inferred Resources 569,000 3.8% 22 ,000 7.4 135,000

TOTAL RESOURCES

(Excluding Björkdal)Ag (cont. oz) Au (cont. oz) Sb (cont. t) Cu (cont. lb)

Measured Resources 5,596,000 99,000 8,000 0

Indicated Resources 35,372,000 367,000 22,000 459,000,000

Total M&I Resources 40,968,000 465,000 32,000 459,000,000

Total Inferred Resources 30,280,000 221,000 22,000 13,000,000

1 Source: Cerro Bayo - Roscoe Postle Associates, March 2014 documented in an independent NI 43-101 report filed March 28, 20142 Source: Costerfield - SRK Consulting (Australia), March 2014, documented in an independent NI 43-101 report filed March 28, 2014

La Quebrada Resources (4) Resource (t) Cu Grade (%) Cu (cont. lb) Ag Grade (g/t) Ag (cont. oz)Measured Resources 0 0 0 0 0

Indicated Resources 34,800,000 0.6% 459,000,000 10 11,200,000

M&I Resources 34,800,000 0.6% 459,000,000 10 11,200,000

Inferred Resources 1,000,000 0.6% 13,000,000 11 400,000

Challacollo Resources (3) Resource (t) Au Grade (g/t) Ag Grade (g/t) Au (cont. oz) Ag (cont. oz)Measured Resources - - - - -Indicated Resources 1,030,000 0.4 242 13,000 8,000,000 M&I Resources 1,030,000 0.4 242 13,000 8,000,000 Inferred Resources 3,900,000 0.3 193 40,000 24,300,000

3 Source: Challacollo – Roscoe Postle Associates, Jan, 30, 2014, in a report filed February 7, 2014.

4 Source: La Quebrada – Independent Technical Report filed 16-Aug-2012. 5 Source: Björkdal - A qualified person within the meaning of NI 43-101 has not done sufficient work to

classify the historical estimate as current Mineral Resources or Mineral Reserves; Mandalay is not treating the historical estimate as current Mineral Resources and Mineral Reserves.

Björkdal Resources(5) Measured Au

(cont. oz)

Indicated Au

(cont. oz)

Measured + Indicated

Au (cont. oz)

Inferred Au

(cont. oz)

Open Pit 2,746 229,611 232,357 111,907

Underground 12,624 765,319 777,944 640,972

Totals 15,370 994,930 1,010,301 752,879