managing working capital globally - c.ymcdn.comc.ymcdn.com/sites/ · 2 corporate panelist biography...

TRANSCRIPT

Managing Working Capital Globally Trends in today’s markets

Robin Veariel, Working Capital Advisor, Bank of America Merrill Lynch John Engeman, Director of Treasury, David Yurman May 28, 2015

2

Corporate Panelist Biography

John Engeman, is the Director of Treasury for David Yurman, responsible for global treasury and

insurance. Prior to joining the company in 2014, he was the Vice President, Assistant Treasurer of Kate Spade & Company (formerly Liz Claiborne) and the Treasurer of the Kate Spade Foundation. His primary responsibilities included managing global treasury operations, focusing on cash and risk management, investments, debt and liquidity management. Prior to joining Kate Spade, he was the Treasurer of Agfa Corporation.

John is a Certified Treasury Professional, Certified Management Accountant, Certified Financial Manager and Distinguished Toastmaster. He is a member of the National Association of Corporate Treasurers, Association for Financial Professionals, Institute of Management Accountants and Toastmasters International. He has a BBA in finance from the University of Notre Dame and his MBA from Hofstra University.

3

Agenda

•Working Capital basics

•Best Practices in Liquidity Management

•Global Working Capital Trends

•Global Liquidity Trends

•Global Payment Trends

•Global Trade Trends

•Summary

4

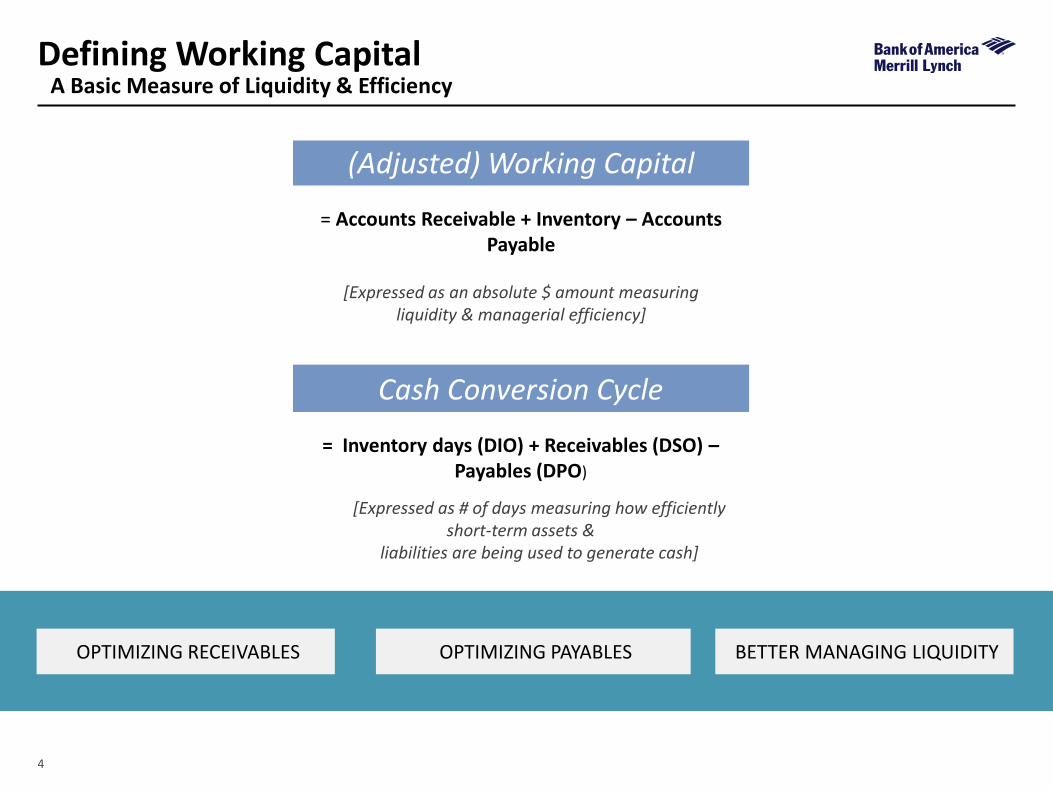

Cash Conversion Cycle

= Inventory days (DIO) + Receivables (DSO) – Payables (DPO)

[Expressed as # of days measuring how efficiently short-term assets &

liabilities are being used to generate cash]

(Adjusted) Working Capital

= Accounts Receivable + Inventory – Accounts Payable

[Expressed as an absolute $ amount measuring liquidity & managerial efficiency]

Defining Working Capital A Basic Measure of Liquidity & Efficiency

OPTIMIZING PAYABLES OPTIMIZING RECEIVABLES BETTER MANAGING LIQUIDITY

5

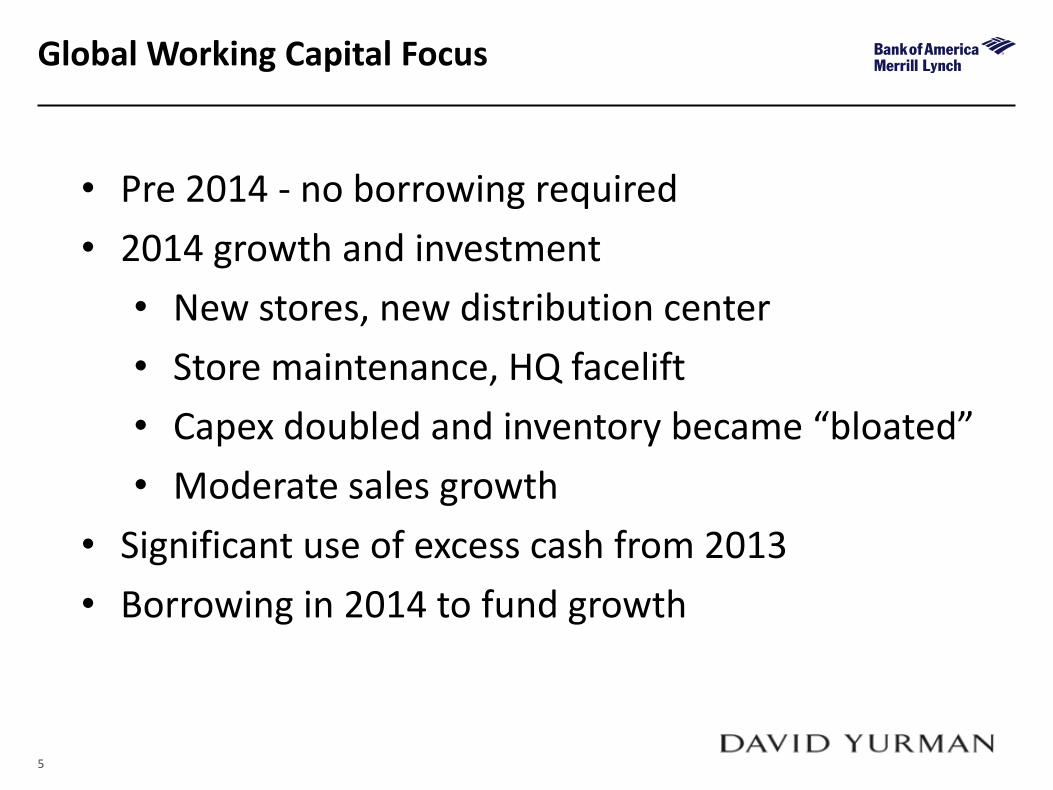

Global Working Capital Focus

• Pre 2014 - no borrowing required

• 2014 growth and investment

• New stores, new distribution center

• Store maintenance, HQ facelift

• Capex doubled and inventory became “bloated”

• Moderate sales growth

• Significant use of excess cash from 2013

• Borrowing in 2014 to fund growth

6

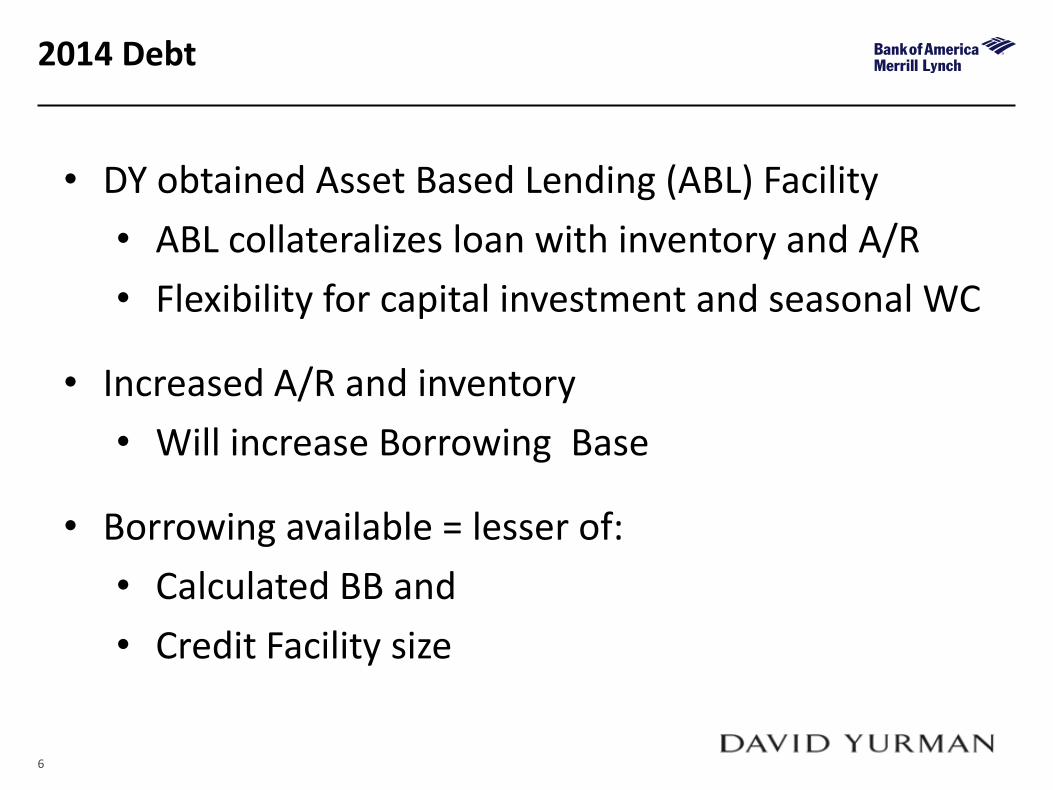

2014 Debt

• DY obtained Asset Based Lending (ABL) Facility

• ABL collateralizes loan with inventory and A/R

• Flexibility for capital investment and seasonal WC

• Increased A/R and inventory

• Will increase Borrowing Base

• Borrowing available = lesser of:

• Calculated BB and

• Credit Facility size

7

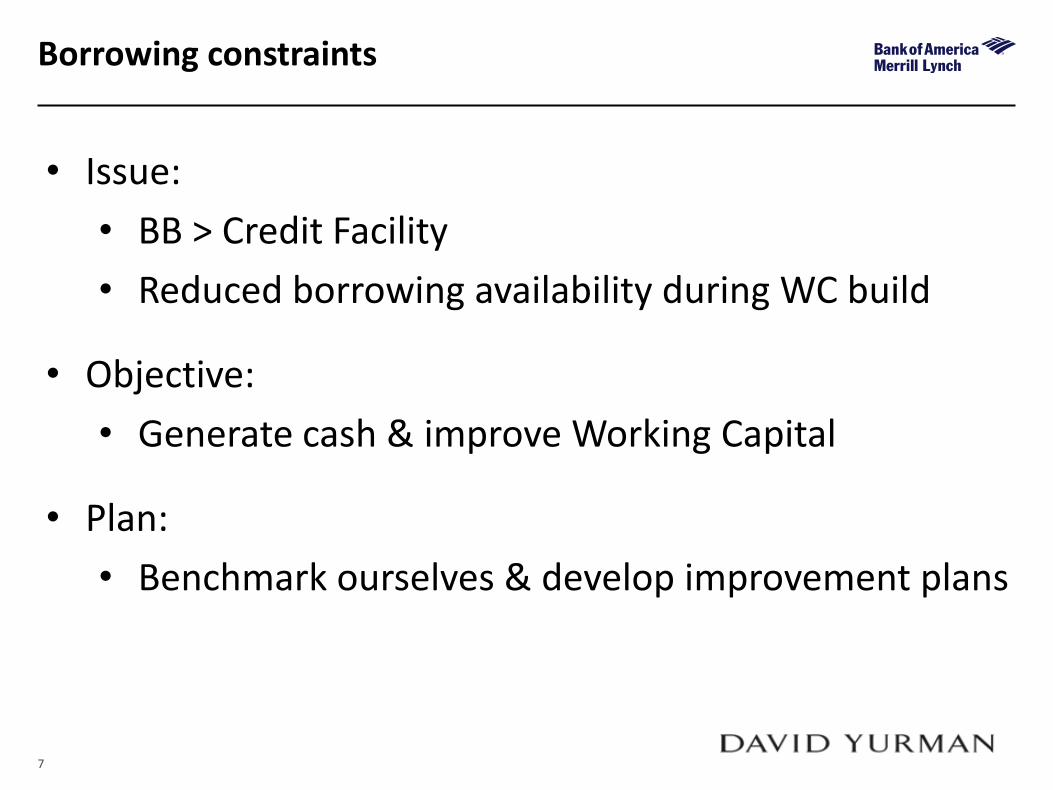

Borrowing constraints

• Issue:

• BB > Credit Facility

• Reduced borrowing availability during WC build

• Objective:

• Generate cash & improve Working Capital

• Plan:

• Benchmark ourselves & develop improvement plans

8

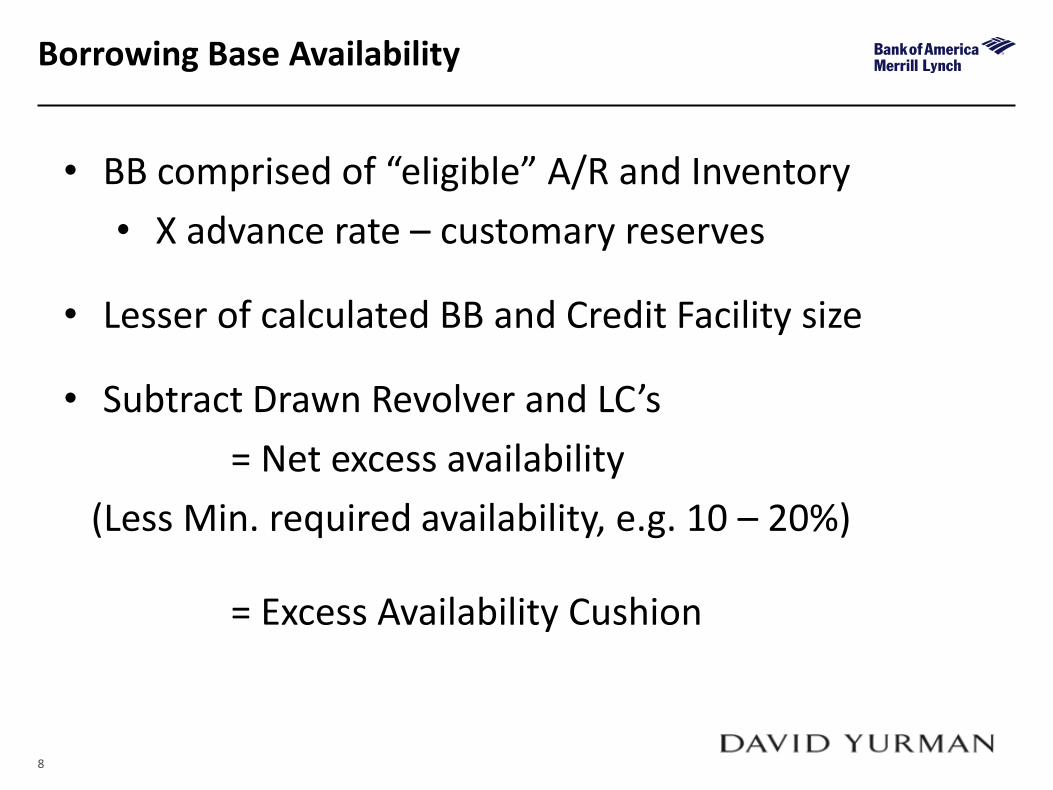

Borrowing Base Availability

• BB comprised of “eligible” A/R and Inventory

• X advance rate – customary reserves

• Lesser of calculated BB and Credit Facility size

• Subtract Drawn Revolver and LC’s

= Net excess availability

(Less Min. required availability, e.g. 10 – 20%)

= Excess Availability Cushion

9

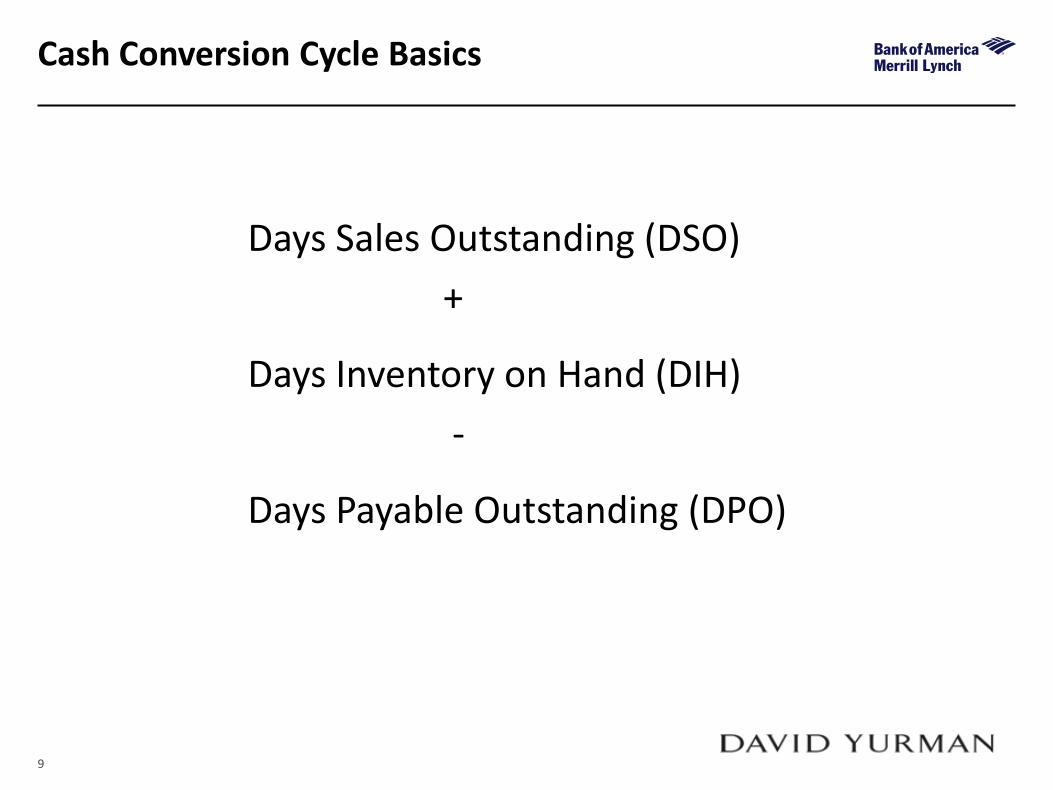

Cash Conversion Cycle Basics

Days Sales Outstanding (DSO)

+

Days Inventory on Hand (DIH)

-

Days Payable Outstanding (DPO)

10

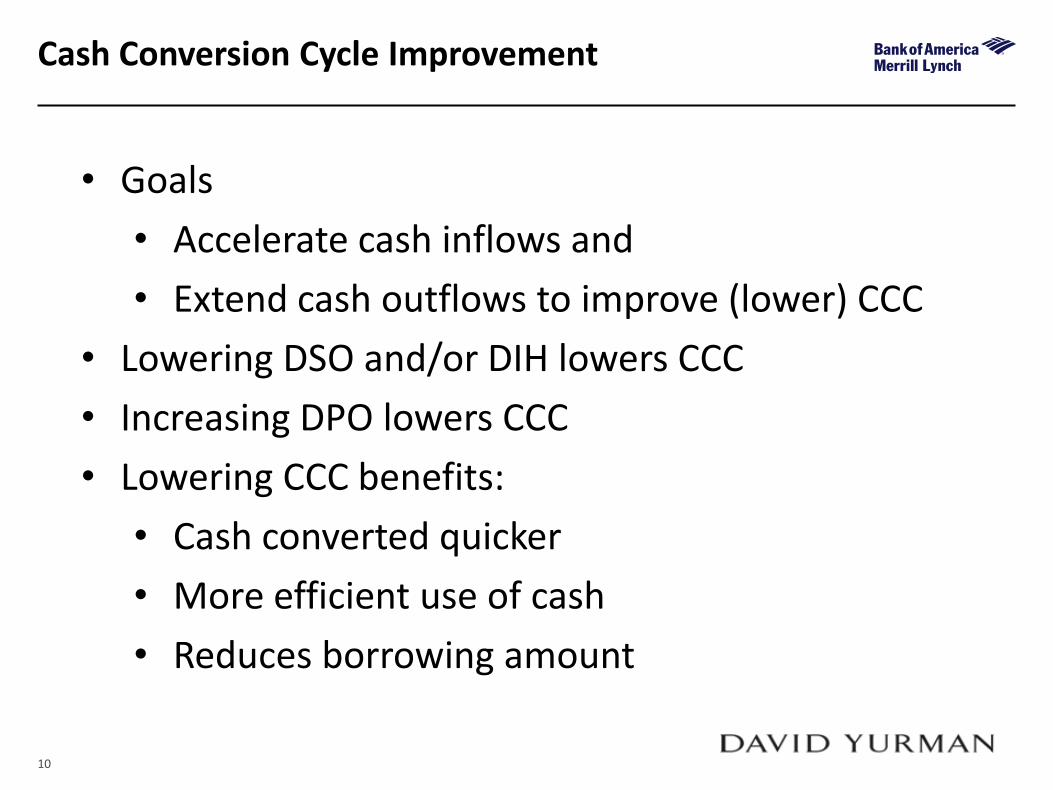

Cash Conversion Cycle Improvement

• Goals

• Accelerate cash inflows and

• Extend cash outflows to improve (lower) CCC

• Lowering DSO and/or DIH lowers CCC

• Increasing DPO lowers CCC

• Lowering CCC benefits:

• Cash converted quicker

• More efficient use of cash

• Reduces borrowing amount

11

Meeting Liquidity Objectives Best Practices

BEST PRACTICES OBJECTIVES

12

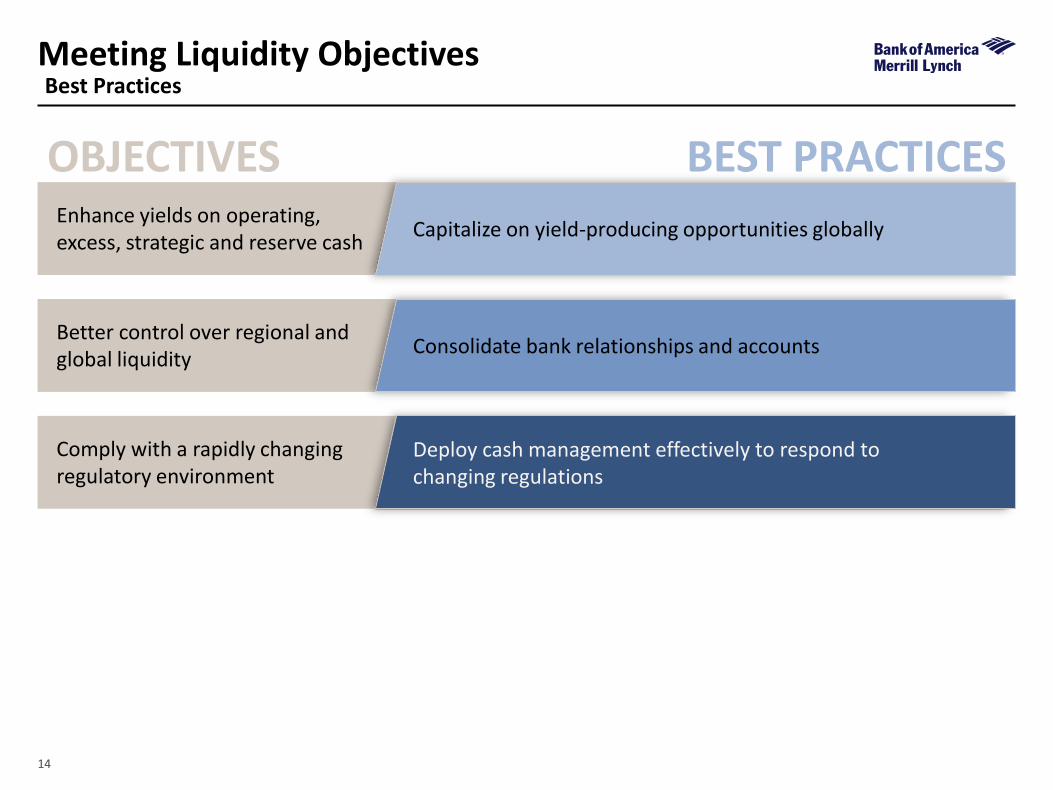

Meeting Liquidity Objectives Best Practices

BEST PRACTICES Enhance yields on operating, excess, strategic and reserve cash

OBJECTIVES

Capitalize on yield-producing opportunities globally

13

Meeting Liquidity Objectives Best Practices

BEST PRACTICES Enhance yields on operating, excess, strategic and reserve cash

Better control over regional and global liquidity

OBJECTIVES

Capitalize on yield-producing opportunities globally

Consolidate bank relationships and accounts

14

Meeting Liquidity Objectives Best Practices

BEST PRACTICES Enhance yields on operating, excess, strategic and reserve cash

Better control over regional and global liquidity

Comply with a rapidly changing regulatory environment

OBJECTIVES

Capitalize on yield-producing opportunities globally

Consolidate bank relationships and accounts

Deploy cash management effectively to respond to changing regulations

15

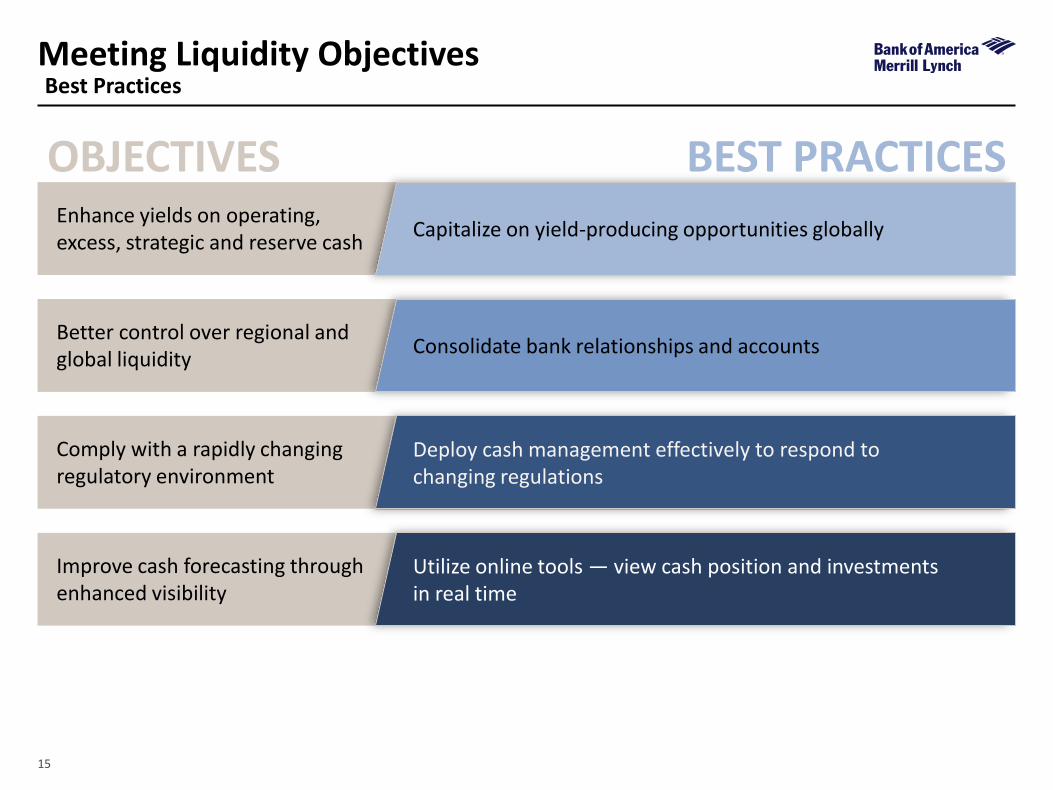

Meeting Liquidity Objectives Best Practices

BEST PRACTICES Enhance yields on operating, excess, strategic and reserve cash

Better control over regional and global liquidity

Comply with a rapidly changing regulatory environment

OBJECTIVES

Improve cash forecasting through enhanced visibility

Capitalize on yield-producing opportunities globally

Consolidate bank relationships and accounts

Deploy cash management effectively to respond to changing regulations

Utilize online tools — view cash position and investments in real time

16

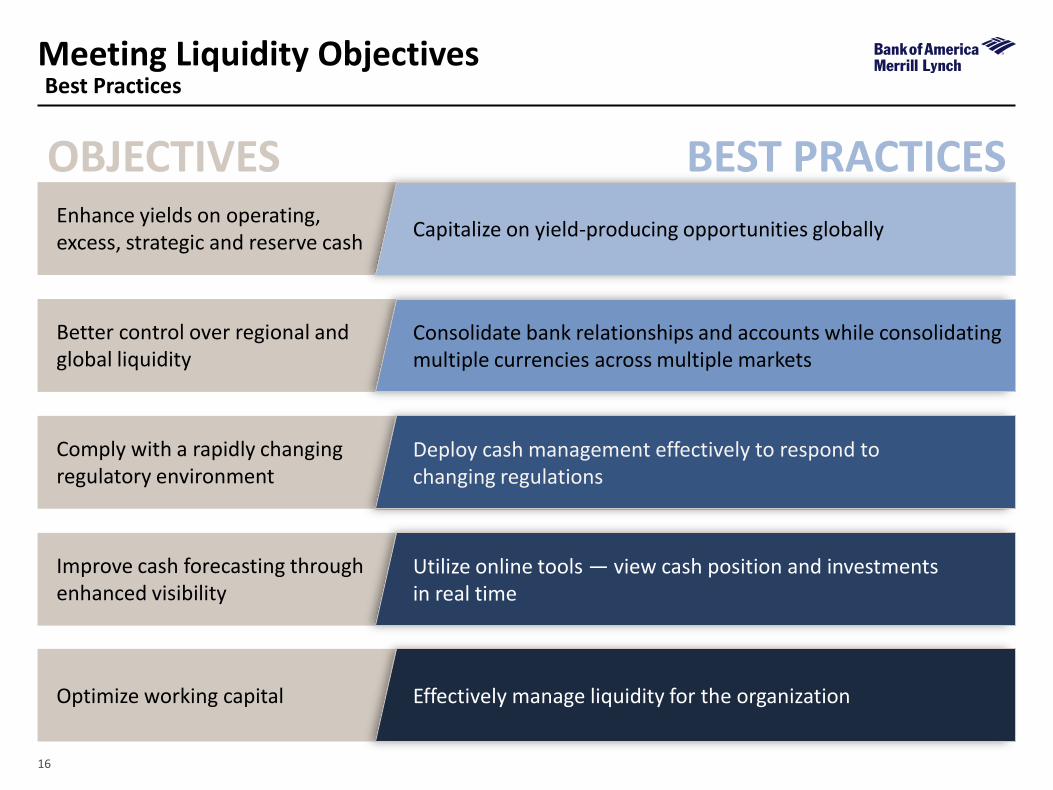

Meeting Liquidity Objectives Best Practices

BEST PRACTICES Enhance yields on operating, excess, strategic and reserve cash

Better control over regional and global liquidity

Comply with a rapidly changing regulatory environment

OBJECTIVES

Improve cash forecasting through enhanced visibility

Capitalize on yield-producing opportunities globally

Consolidate bank relationships and accounts while consolidating multiple currencies across multiple markets

Deploy cash management effectively to respond to changing regulations

Utilize online tools — view cash position and investments in real time

Optimize working capital Effectively manage liquidity for the organization

Global Working Capital Trends

global working capital performance has improved by 2% year over year (1)

(1) Source: PwC Annual Global Working Capital Survey, Cash for Growth (July 2014)

18

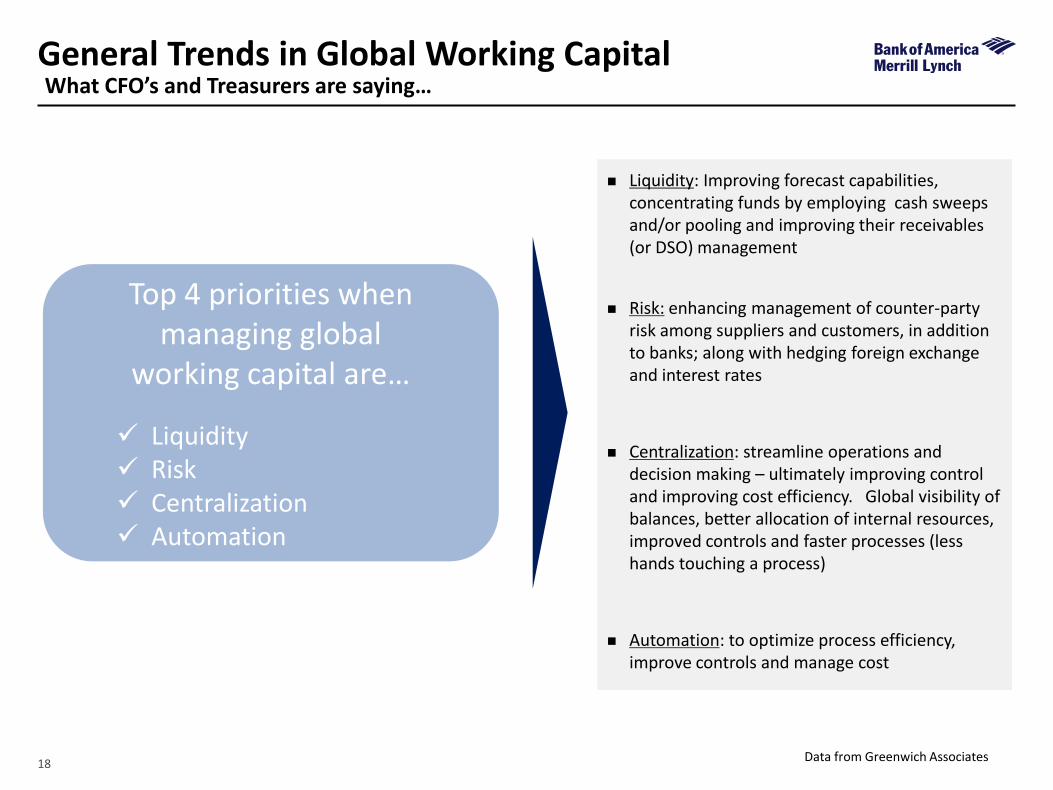

General Trends in Global Working Capital What CFO’s and Treasurers are saying…

Liquidity: Improving forecast capabilities, concentrating funds by employing cash sweeps and/or pooling and improving their receivables (or DSO) management

Risk: enhancing management of counter-party risk among suppliers and customers, in addition to banks; along with hedging foreign exchange and interest rates

Centralization: streamline operations and decision making – ultimately improving control and improving cost efficiency. Global visibility of balances, better allocation of internal resources, improved controls and faster processes (less hands touching a process)

Automation: to optimize process efficiency, improve controls and manage cost

Top 4 priorities when managing global

working capital are…

Liquidity Risk Centralization Automation

Data from Greenwich Associates

19

Global Working Capital Performance Factors Behind Performance Variations

20

Global Working Capital Performance Factors Behind Performance Variations

Payment practices Payment terms and behaviors, payment usage,

legal frameworks and cash collection effectiveness

21

Focus on cash & effectiveness of WC management Intensity of management focus on cash

& WC management processes

Global Working Capital Performance Factors Behind Performance Variations

Payment practices Payment terms and behaviors, payment usage,

legal frameworks and cash collection effectiveness

22

Logistics & distribution infrastructure Supply chain costs,

services levels and risks

Focus on cash & effectiveness of WC management Intensity of management focus on cash

& WC management processes

Global Working Capital Performance Factors Behind Performance Variations

Payment practices Payment terms and behaviors, payment usage,

legal frameworks and cash collection effectiveness

23 23

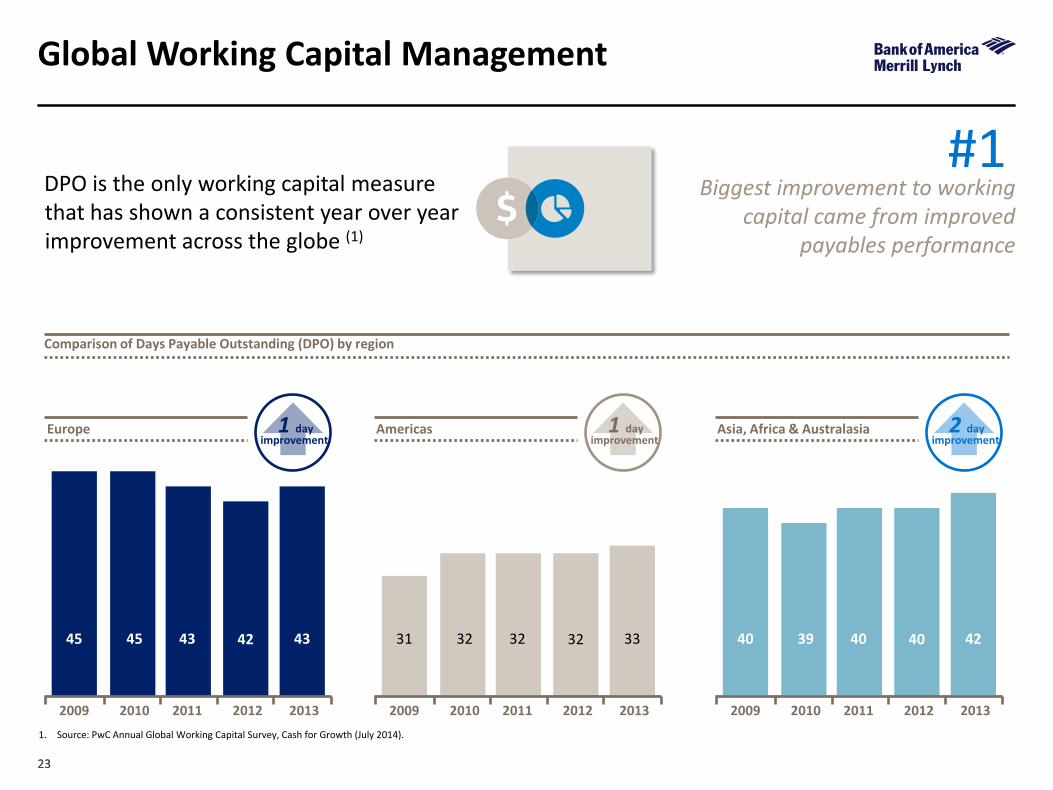

Global Working Capital Management

DPO is the only working capital measure that has shown a consistent year over year improvement across the globe (1)

Biggest improvement to working capital came from improved

payables performance

1. Source: PwC Annual Global Working Capital Survey, Cash for Growth (July 2014).

45 45 43 43 42

2009 2010 2011 2012 2013

Europe improvement

1 day

Comparison of Days Payable Outstanding (DPO) by region

31 32 32 33 32

2009 2010 2011 2012 2013

Americas improvement

1 day

40 39 40 42 40

2009 2010 2011 2012 2013

Asia, Africa & Australasia improvement

2 day

#1

24 24

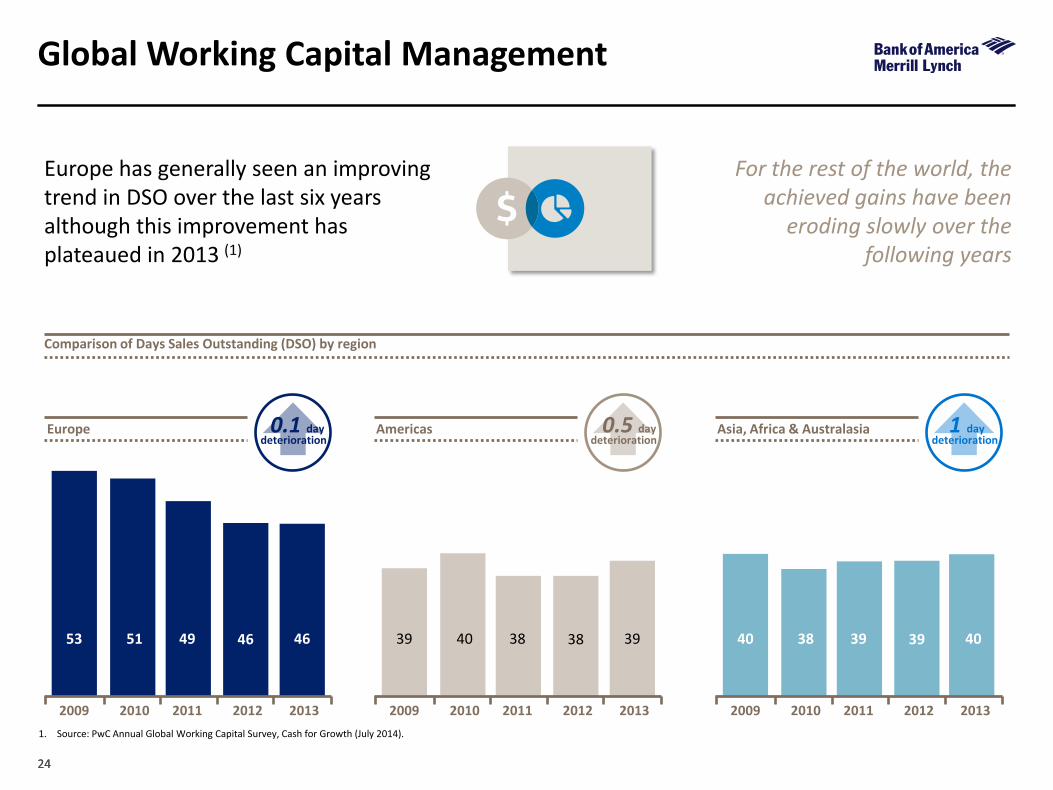

Global Working Capital Management

Europe has generally seen an improving trend in DSO over the last six years although this improvement has plateaued in 2013 (1)

For the rest of the world, the achieved gains have been

eroding slowly over the following years

1. Source: PwC Annual Global Working Capital Survey, Cash for Growth (July 2014).

53 51 49 46 46

2009 2010 2011 2012 2013

Europe deterioration

0.1 day

Comparison of Days Sales Outstanding (DSO) by region

39 40 38 39 38

2009 2010 2011 2012 2013

Americas deterioration

0.5 day

40 38 39 40 39

2009 2010 2011 2012 2013

Asia, Africa & Australasia deterioration

1 day

25 25

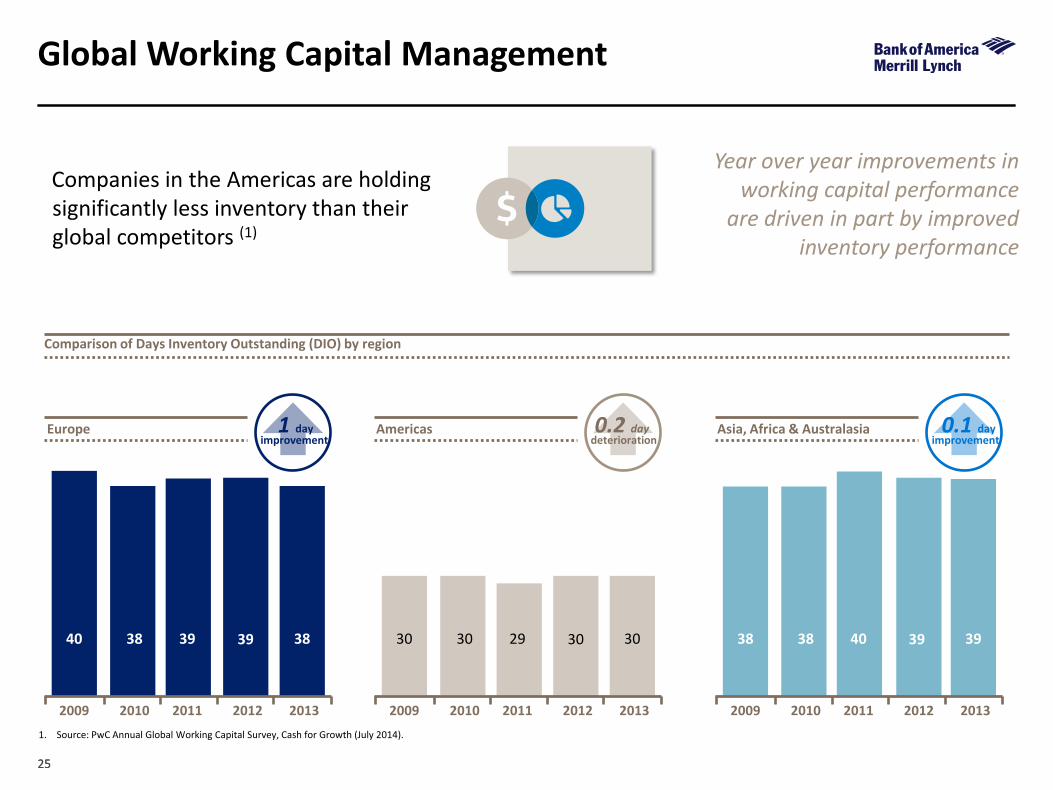

Global Working Capital Management

Companies in the Americas are holding significantly less inventory than their global competitors (1)

Year over year improvements in working capital performance

are driven in part by improved inventory performance

1. Source: PwC Annual Global Working Capital Survey, Cash for Growth (July 2014).

40 38 39 38 39

2009 2010 2011 2012 2013

Europe improvement

1 day

Comparison of Days Inventory Outstanding (DIO) by region

30 30 29 30 30

2009 2010 2011 2012 2013

Americas deterioration 0.2 day

38 38 40 39 39

2009 2010 2011 2012 2013

Asia, Africa & Australasia improvement 0.1 day

Global Liquidity Trends

27 27

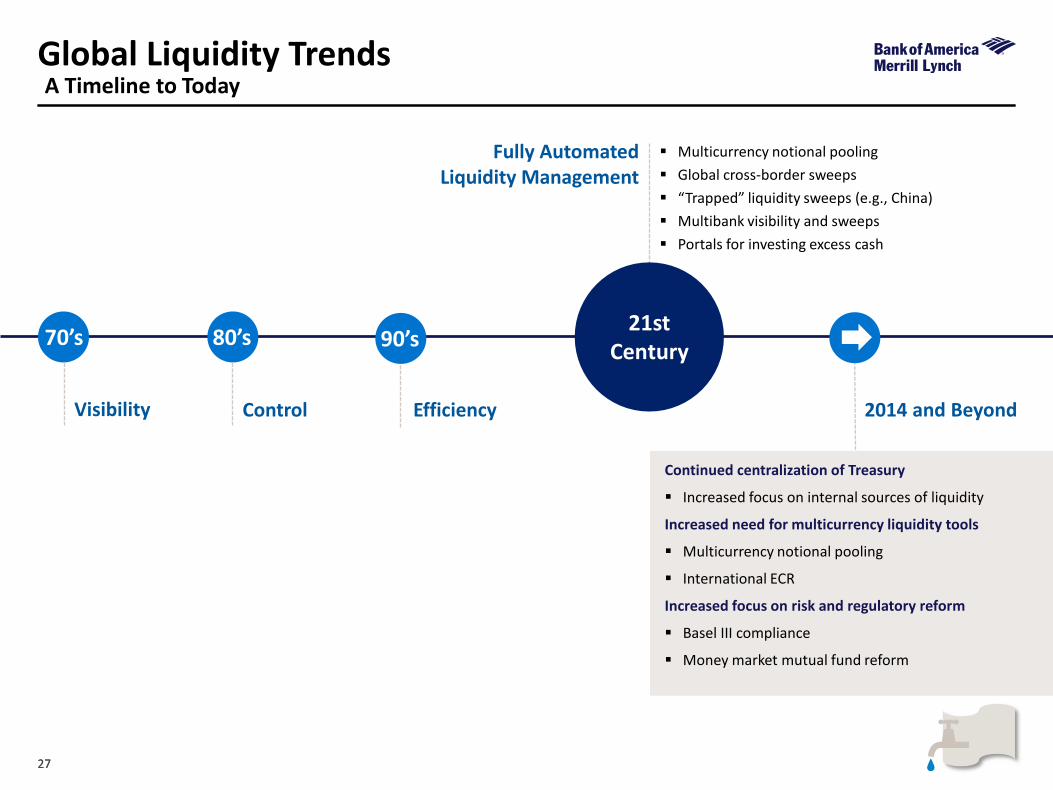

Global Liquidity Trends A Timeline to Today

70’s

Visibility

80’s

Control

90’s

Efficiency

21st Century

Fully Automated Liquidity Management

Continued centralization of Treasury

Increased focus on internal sources of liquidity

Increased need for multicurrency liquidity tools

Multicurrency notional pooling

International ECR

Increased focus on risk and regulatory reform

Basel III compliance

Money market mutual fund reform

Multicurrency notional pooling

Global cross-border sweeps

“Trapped” liquidity sweeps (e.g., China)

Multibank visibility and sweeps

Portals for investing excess cash

2014 and Beyond

28 28

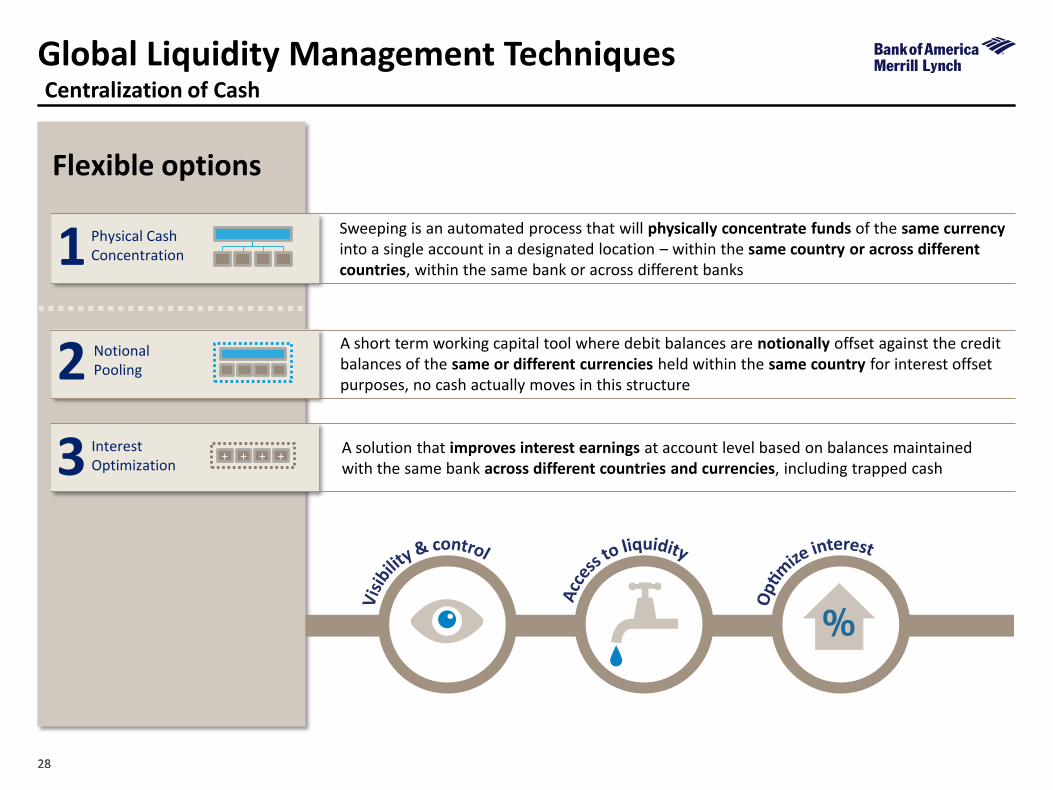

Global Liquidity Management Techniques Centralization of Cash

Sweeping is an automated process that will physically concentrate funds of the same currency into a single account in a designated location – within the same country or across different countries, within the same bank or across different banks

A solution that improves interest earnings at account level based on balances maintained with the same bank across different countries and currencies, including trapped cash

A short term working capital tool where debit balances are notionally offset against the credit balances of the same or different currencies held within the same country for interest offset purposes, no cash actually moves in this structure

Flexible options

3 Interest Optimization

+ + + +

2 Notional Pooling

1 Physical Cash Concentration

29 29

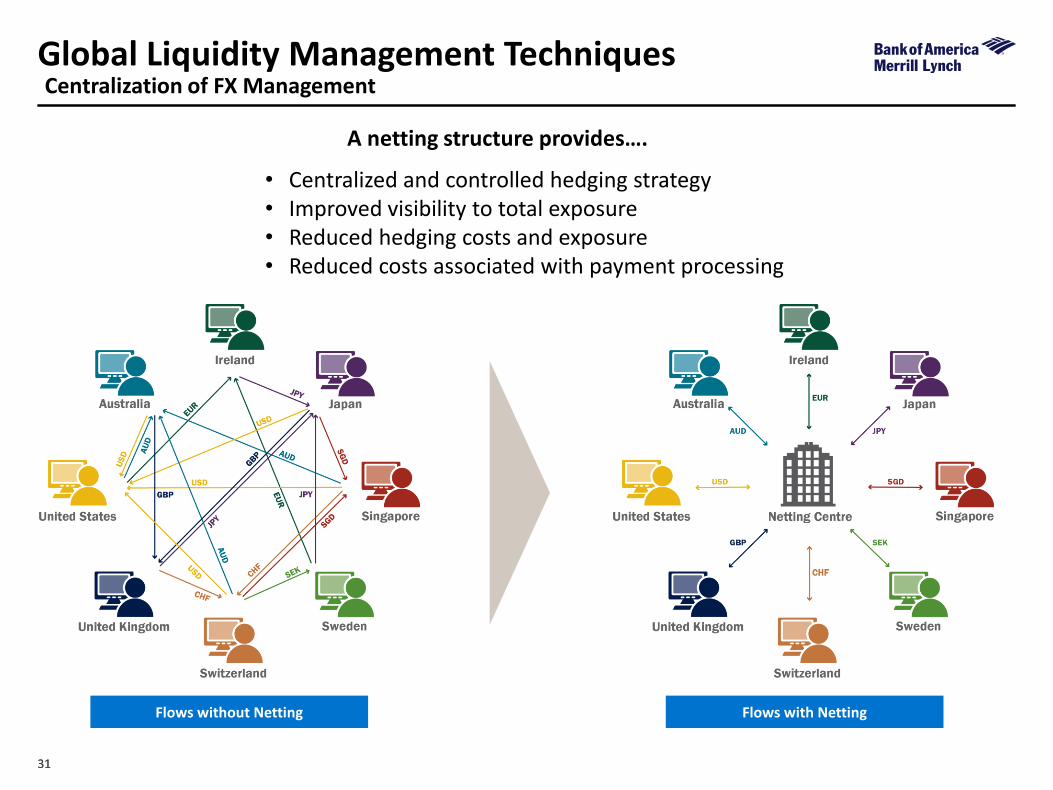

Global Liquidity Management Techniques

A netting structure provides….

• Centralized and controlled hedging strategy • Improved visibility to total exposure • Reduced hedging costs and exposure • Reduced costs associated with payment processing

Centralization of FX Management

30 30

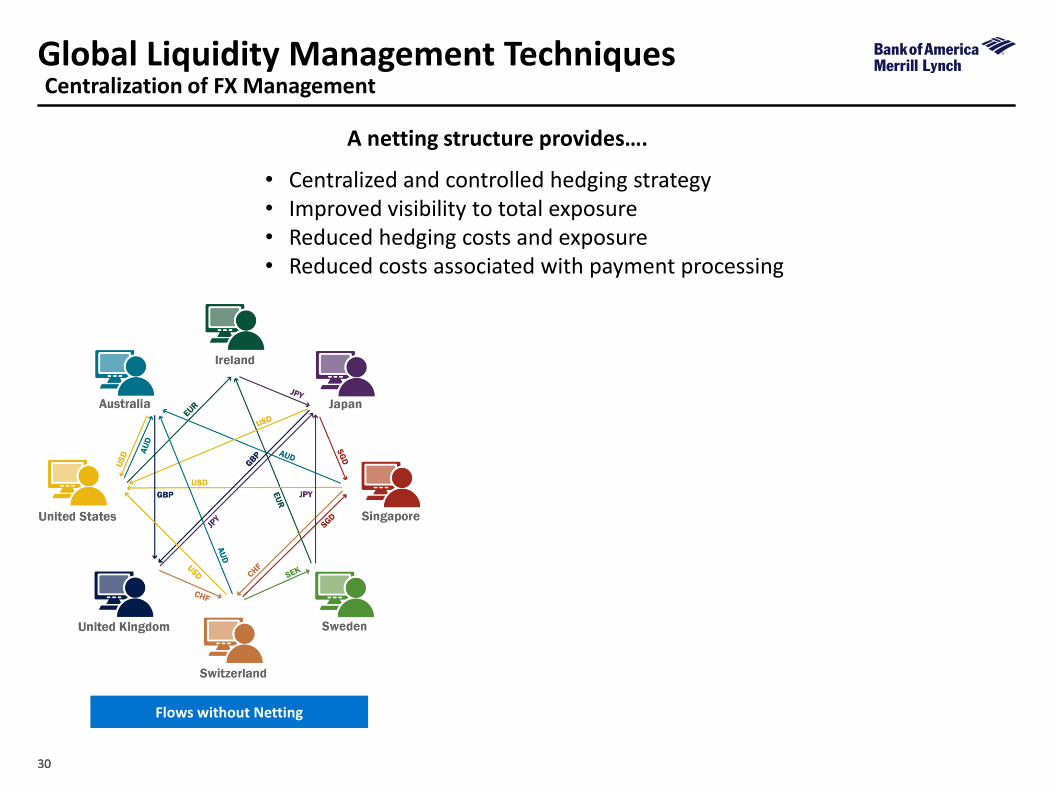

Global Liquidity Management Techniques Centralization of FX Management

A netting structure provides….

• Centralized and controlled hedging strategy • Improved visibility to total exposure • Reduced hedging costs and exposure • Reduced costs associated with payment processing

Flows without Netting

31 31

Global Liquidity Management Techniques Centralization of FX Management

A netting structure provides….

• Centralized and controlled hedging strategy • Improved visibility to total exposure • Reduced hedging costs and exposure • Reduced costs associated with payment processing

Flows without Netting Flows with Netting

32 32

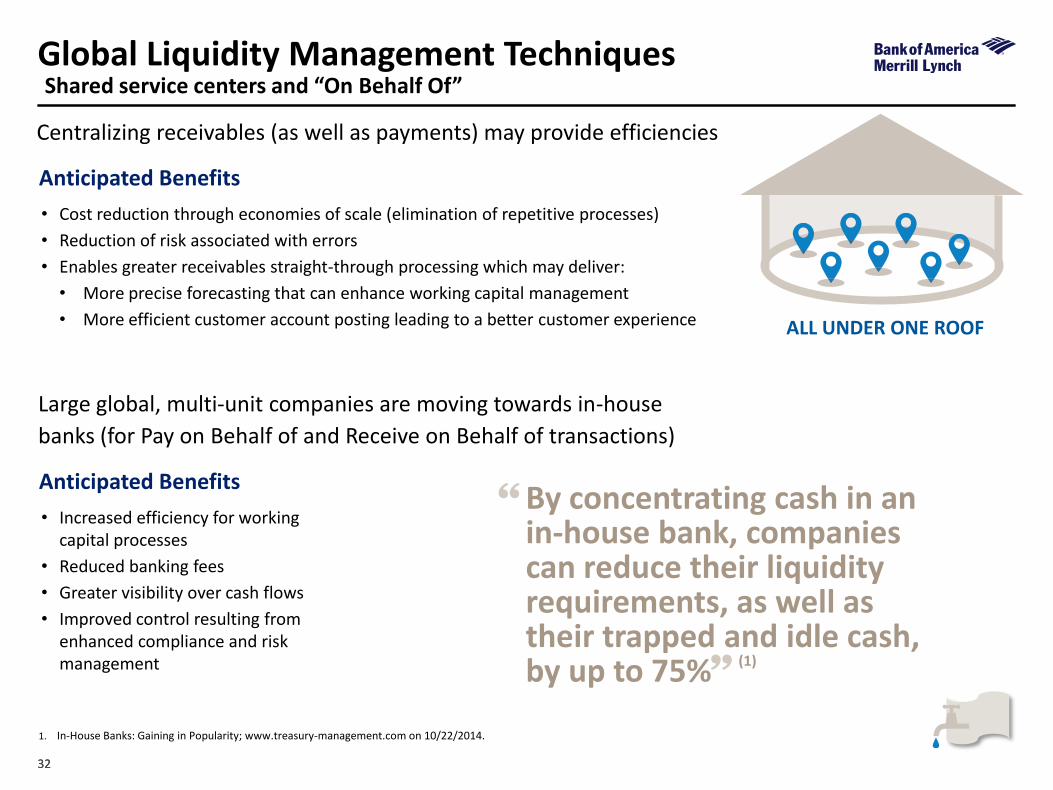

Global Liquidity Management Techniques Shared service centers and “On Behalf Of”

Centralizing receivables (as well as payments) may provide efficiencies

• Cost reduction through economies of scale (elimination of repetitive processes)

• Reduction of risk associated with errors

• Enables greater receivables straight-through processing which may deliver:

• More precise forecasting that can enhance working capital management

• More efficient customer account posting leading to a better customer experience

Anticipated Benefits

Large global, multi-unit companies are moving towards in-house

banks (for Pay on Behalf of and Receive on Behalf of transactions)

• Increased efficiency for working capital processes

• Reduced banking fees

• Greater visibility over cash flows

• Improved control resulting from enhanced compliance and risk management

Anticipated Benefits By concentrating cash in an in-house bank, companies can reduce their liquidity requirements, as well as their trapped and idle cash, by up to 75%

“

” 1. In-House Banks: Gaining in Popularity; www.treasury-management.com on 10/22/2014.

ALL UNDER ONE ROOF

(1)

33 33

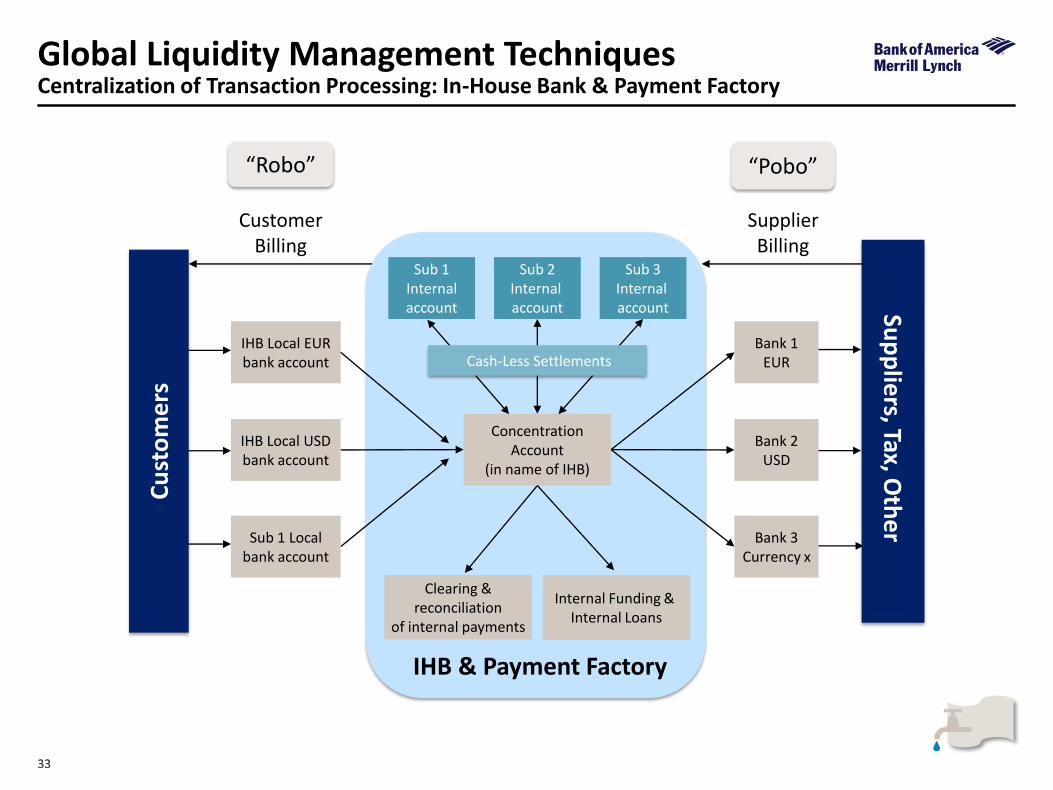

Global Liquidity Management Techniques Centralization of Transaction Processing: In-House Bank & Payment Factory

IHB Local EUR bank account

IHB Local USD bank account

Sub 1 Local bank account

Bank 1 EUR

Bank 2 USD

Bank 3 Currency x

Cu

sto

me

rs

Sup

plie

rs, Tax, Oth

er

IHB & Payment Factory

Sub 1 Internal account

Sub 2 Internal account

Sub 3 Internal account

Concentration

Account (in name of IHB)

Customer Billing

Supplier Billing

“Pobo” “Robo”

Clearing & reconciliation

of internal payments

Internal Funding &

Internal Loans

Cash-Less Settlements

Global Payment Trends

35 35

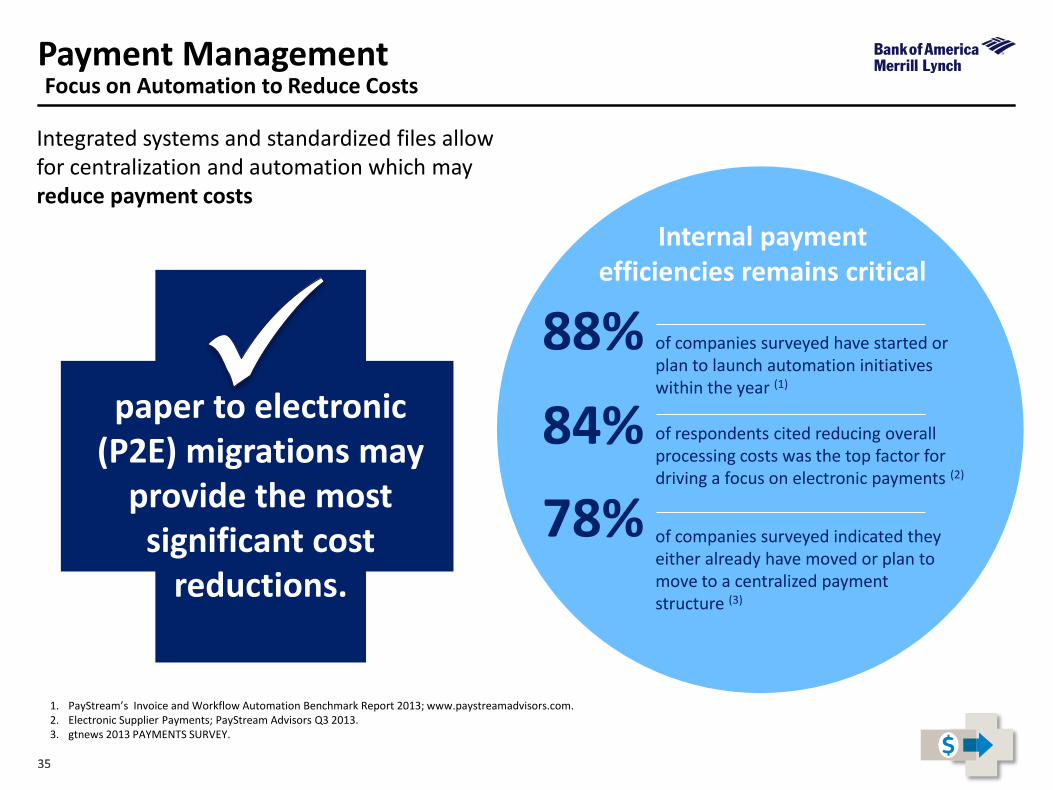

Payment Management

1. PayStream’s Invoice and Workflow Automation Benchmark Report 2013; www.paystreamadvisors.com. 2. Electronic Supplier Payments; PayStream Advisors Q3 2013. 3. gtnews 2013 PAYMENTS SURVEY.

Internal payment efficiencies remains critical

of companies surveyed indicated they either already have moved or plan to move to a centralized payment structure (3)

88%

of respondents cited reducing overall processing costs was the top factor for driving a focus on electronic payments (2)

84%

78%

of companies surveyed have started or plan to launch automation initiatives within the year (1)

Integrated systems and standardized files allow for centralization and automation which may reduce payment costs

paper to electronic

(P2E) migrations may provide the most

significant cost reductions.

Focus on Automation to Reduce Costs

36

Global Working Capital Improvement

• Convert paper payments to Electronic Payments • Benefits:

• Cost Savings • Reduced Fraud • Process Efficiencies • Improved Cash Conversion Cycle (“CCC”)

37

Working Capital Initiatives

• Optimize conversion by maximizing volumes to Card Payment • Value provided by additional “float” added • Vendor gets paid on due date; DYE preserves cash by

paying card statement at end of statement grace period (30 day cycle + 25-day grace period) vs paying by check (clears in 1-5 days)

• Those vendors that won’t take card: target for ACH payments

• Program goal = convert as many check payments as possible to electronic payment

• Estimate 40-50% of payments will convert to electronic payment

• Any vendors not taking electronic payment, outsource check processing to bank at reduced processing cost

38

There Is More!

BIGGER $AVINGS

• Card payments earn REBATES

• Greater volume increases rebate

• Rebate grid = X% to Y% of Card volume

• $20 Million in payments, e.g. $200K+ Rebate

• $30 Million in payments, e.g. $300K+ Rebate

• Goal is to convert vendor payments from check payment to Card (thru an ePayables solution)

39

Optimizing Payment Methods – the Outcome

• Global working capital improved

• Debt maintained or reduced

• Days payable outstanding (DPO) increased

• Cash Conversion Cycle improved (lowered)

• CFO………………………….. HAPPY

40 40

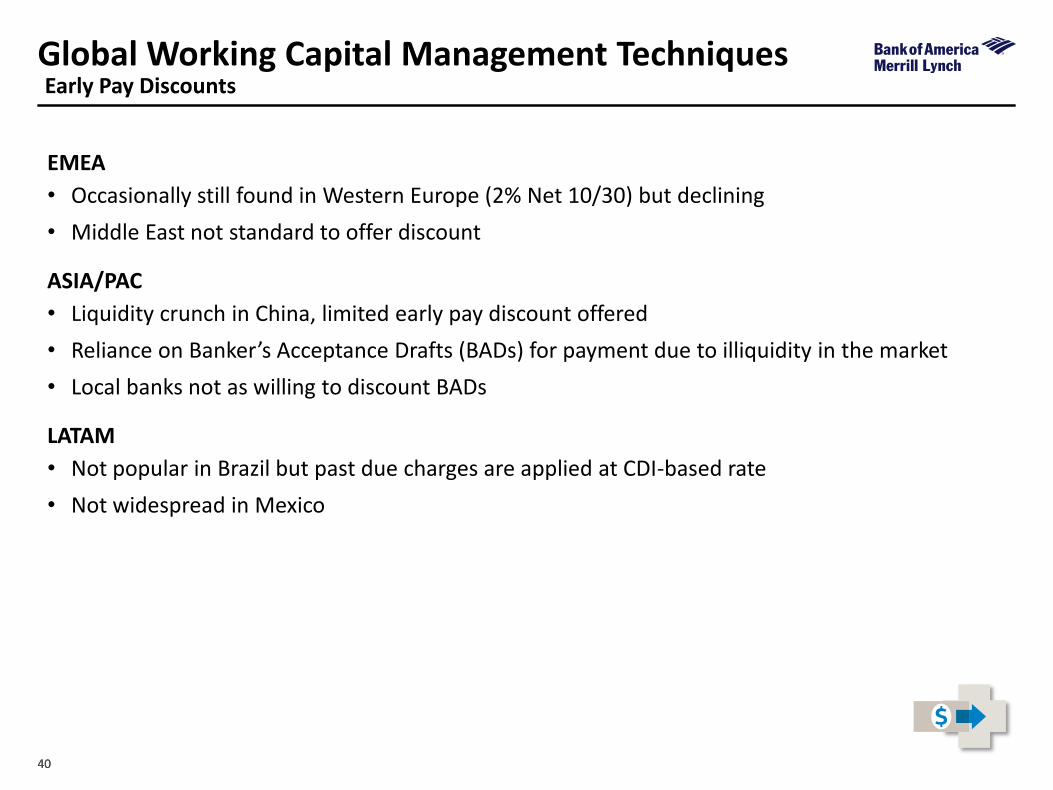

Global Working Capital Management Techniques Early Pay Discounts

EMEA

• Occasionally still found in Western Europe (2% Net 10/30) but declining

• Middle East not standard to offer discount

ASIA/PAC

• Liquidity crunch in China, limited early pay discount offered

• Reliance on Banker’s Acceptance Drafts (BADs) for payment due to illiquidity in the market

• Local banks not as willing to discount BADs

LATAM

• Not popular in Brazil but past due charges are applied at CDI-based rate

• Not widespread in Mexico

Global Trade Trends

42 42

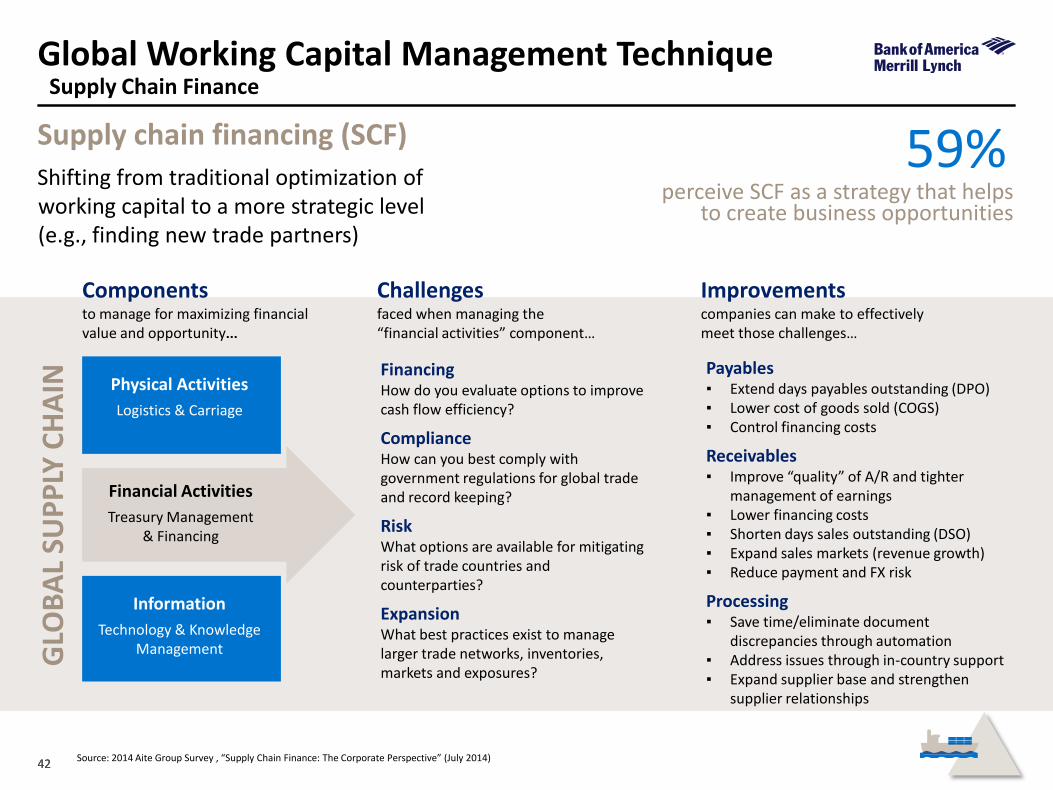

Global Working Capital Management Technique

Supply chain financing (SCF)

Shifting from traditional optimization of working capital to a more strategic level (e.g., finding new trade partners)

59% perceive SCF as a strategy that helps

to create business opportunities

Components to manage for maximizing financial value and opportunity…

GLO

BA

L SU

PP

LY C

HA

IN

Physical Activities

Logistics & Carriage

Challenges faced when managing the “financial activities” component…

Financing How do you evaluate options to improve cash flow efficiency?

Compliance How can you best comply with government regulations for global trade and record keeping?

Risk What options are available for mitigating risk of trade countries and counterparties?

Expansion What best practices exist to manage larger trade networks, inventories, markets and exposures?

Improvements companies can make to effectively meet those challenges…

Payables ▪ Extend days payables outstanding (DPO) ▪ Lower cost of goods sold (COGS) ▪ Control financing costs

Receivables ▪ Improve “quality” of A/R and tighter

management of earnings ▪ Lower financing costs ▪ Shorten days sales outstanding (DSO) ▪ Expand sales markets (revenue growth) ▪ Reduce payment and FX risk

Processing ▪ Save time/eliminate document

discrepancies through automation ▪ Address issues through in-country support ▪ Expand supplier base and strengthen

supplier relationships

Financial Activities

Treasury Management & Financing

Information

Technology & Knowledge Management

Source: 2014 Aite Group Survey , “Supply Chain Finance: The Corporate Perspective” (July 2014)

Supply Chain Finance

43 43

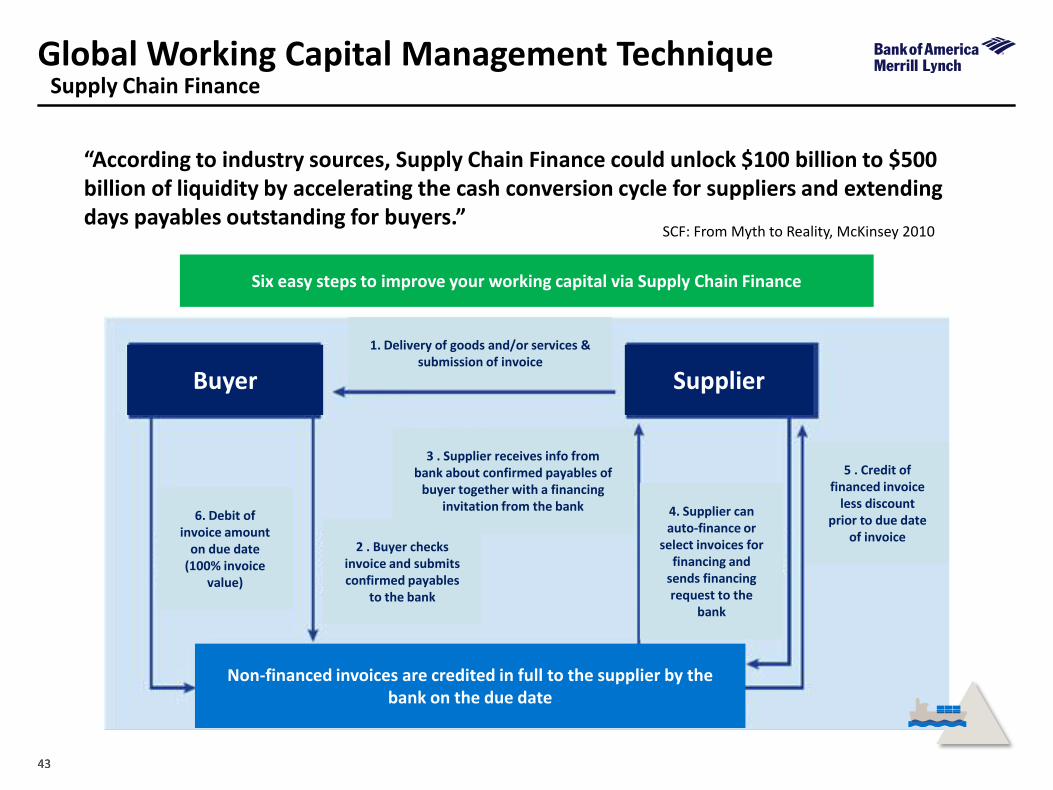

Global Working Capital Management Technique Supply Chain Finance

“According to industry sources, Supply Chain Finance could unlock $100 billion to $500 billion of liquidity by accelerating the cash conversion cycle for suppliers and extending days payables outstanding for buyers.”

SCF: From Myth to Reality, McKinsey 2010

Six easy steps to improve your working capital via Supply Chain Finance

Non-financed invoices are credited in full to the supplier by the bank on the due date

1. Delivery of goods and/or services & submission of invoice

2 . Buyer checks invoice and submits confirmed payables

to the bank

3 . Supplier receives info from bank about confirmed payables of

buyer together with a financing invitation from the bank 4. Supplier can

auto-finance or select invoices for

financing and sends financing request to the

bank

5 . Credit of financed invoice

less discount prior to due date

of invoice

6. Debit of invoice amount

on due date (100% invoice

value)

Buyer Supplier

44 44

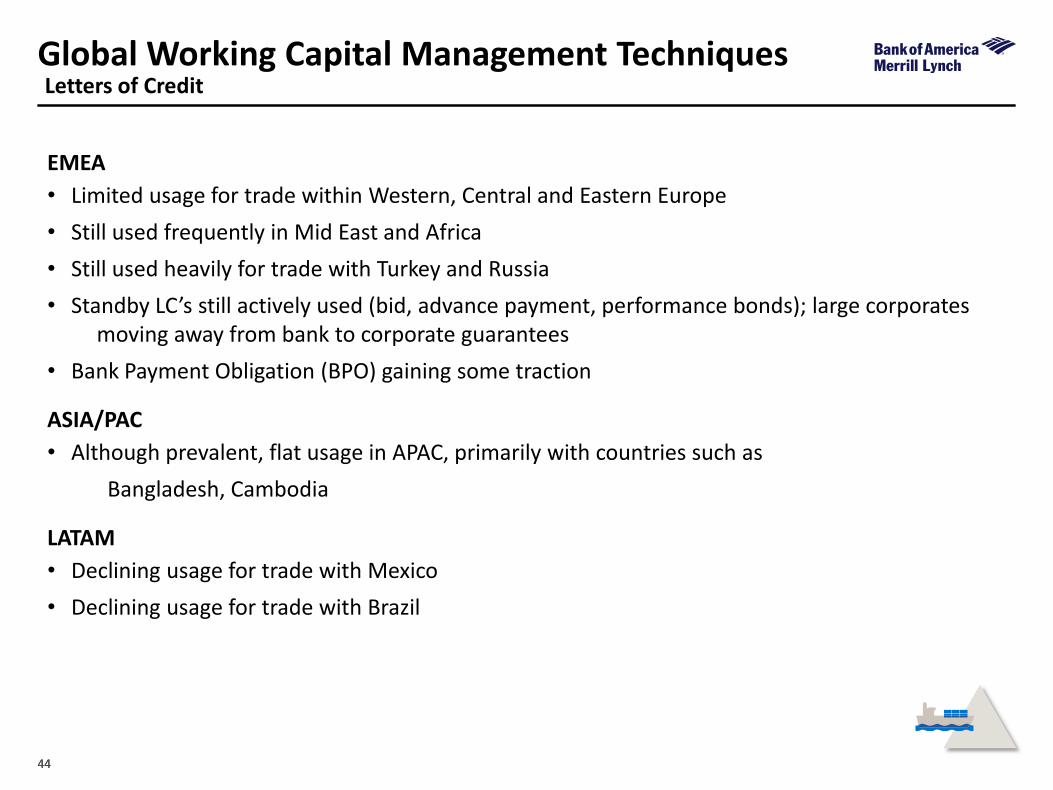

Global Working Capital Management Techniques Letters of Credit

EMEA

• Limited usage for trade within Western, Central and Eastern Europe

• Still used frequently in Mid East and Africa

• Still used heavily for trade with Turkey and Russia

• Standby LC’s still actively used (bid, advance payment, performance bonds); large corporates moving away from bank to corporate guarantees

• Bank Payment Obligation (BPO) gaining some traction

ASIA/PAC

• Although prevalent, flat usage in APAC, primarily with countries such as

Bangladesh, Cambodia

LATAM

• Declining usage for trade with Mexico

• Declining usage for trade with Brazil

Summary

46 46

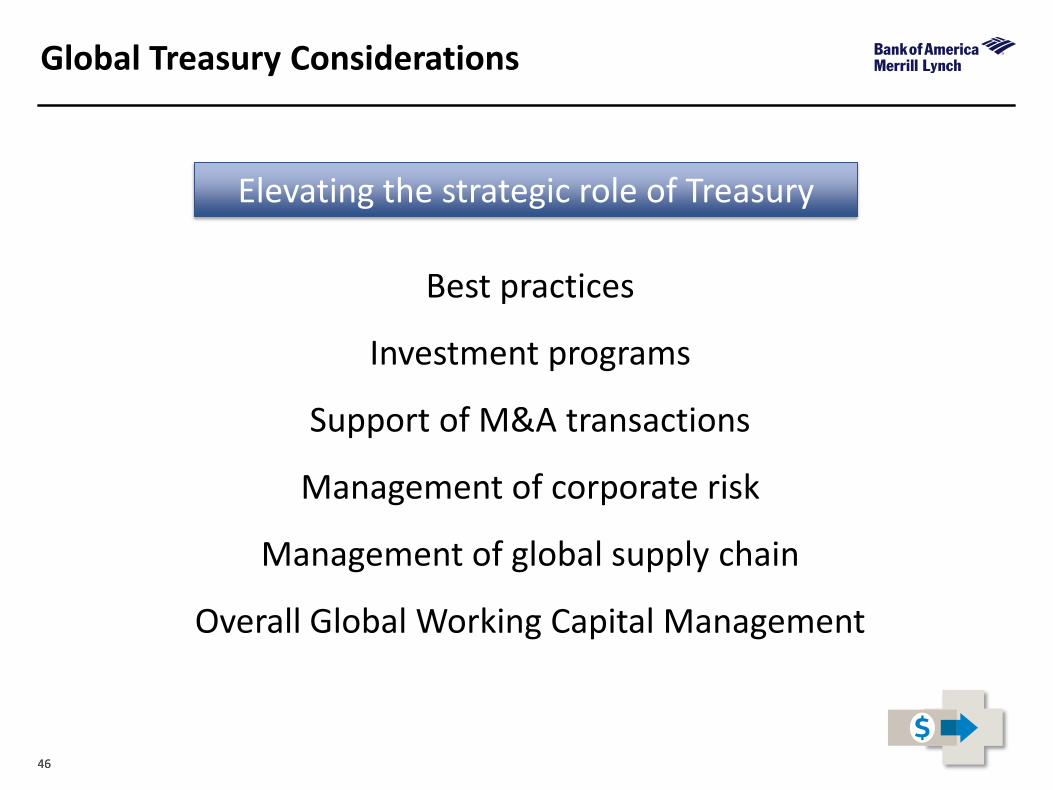

Global Treasury Considerations

Best practices

Investment programs

Support of M&A transactions

Management of corporate risk

Management of global supply chain

Overall Global Working Capital Management

Elevating the strategic role of Treasury

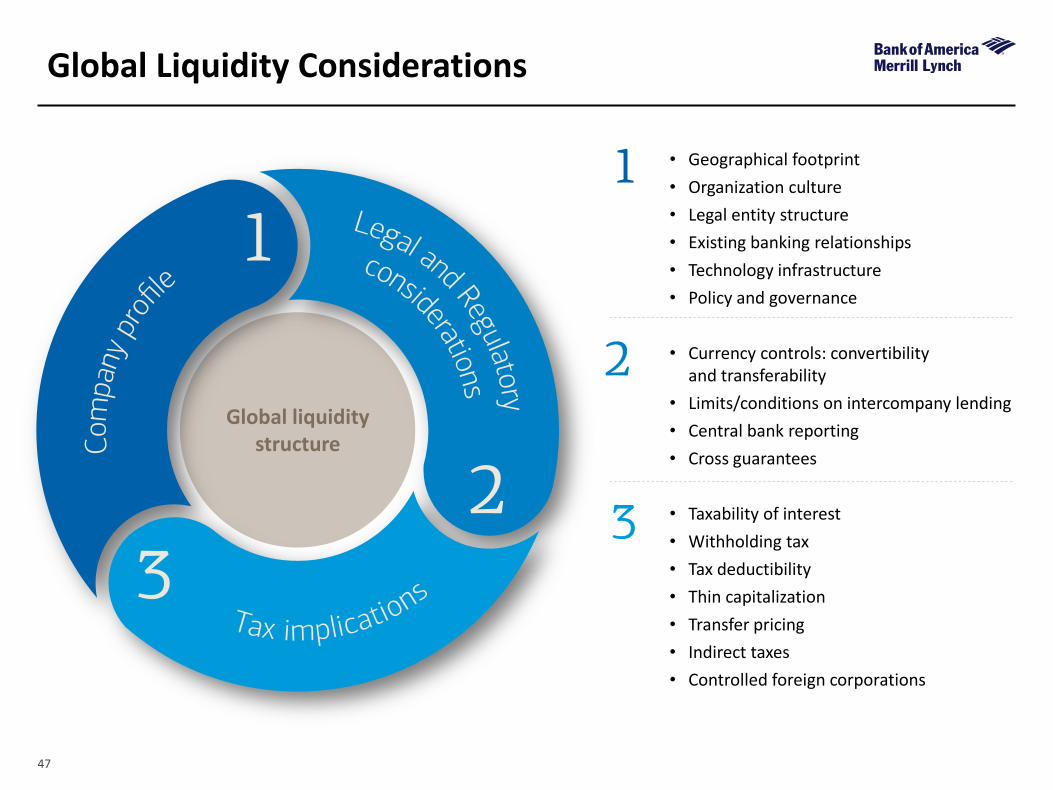

47

• Geographical footprint

• Organization culture

• Legal entity structure

• Existing banking relationships

• Technology infrastructure

• Policy and governance

• Currency controls: convertibility and transferability

• Limits/conditions on intercompany lending

• Central bank reporting

• Cross guarantees

• Taxability of interest

• Withholding tax

• Tax deductibility

• Thin capitalization

• Transfer pricing

• Indirect taxes

• Controlled foreign corporations

Global Liquidity Considerations

Global liquidity structure

48 48

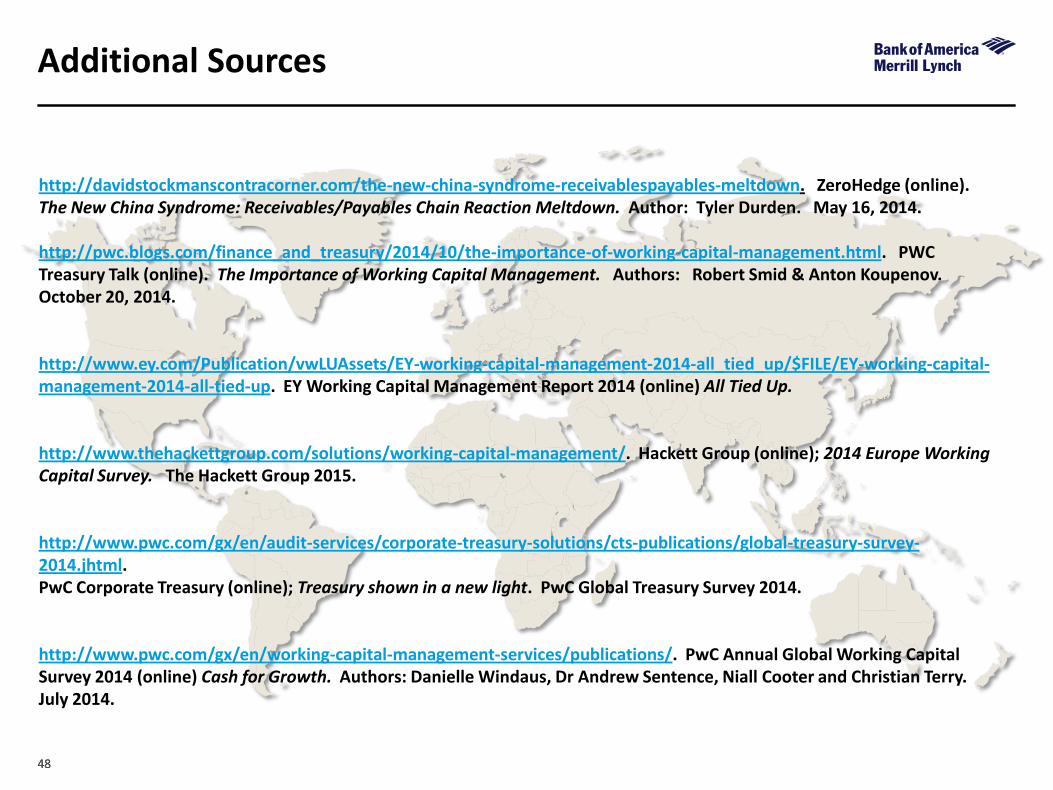

Additional Sources

http://davidstockmanscontracorner.com/the-new-china-syndrome-receivablespayables-meltdown. ZeroHedge (online). The New China Syndrome: Receivables/Payables Chain Reaction Meltdown. Author: Tyler Durden. May 16, 2014. http://pwc.blogs.com/finance_and_treasury/2014/10/the-importance-of-working-capital-management.html. PWC Treasury Talk (online). The Importance of Working Capital Management. Authors: Robert Smid & Anton Koupenov. October 20, 2014. http://www.ey.com/Publication/vwLUAssets/EY-working-capital-management-2014-all_tied_up/$FILE/EY-working-capital-management-2014-all-tied-up. EY Working Capital Management Report 2014 (online) All Tied Up. http://www.thehackettgroup.com/solutions/working-capital-management/. Hackett Group (online); 2014 Europe Working Capital Survey. The Hackett Group 2015. http://www.pwc.com/gx/en/audit-services/corporate-treasury-solutions/cts-publications/global-treasury-survey-2014.jhtml. PwC Corporate Treasury (online); Treasury shown in a new light. PwC Global Treasury Survey 2014. http://www.pwc.com/gx/en/working-capital-management-services/publications/. PwC Annual Global Working Capital Survey 2014 (online) Cash for Growth. Authors: Danielle Windaus, Dr Andrew Sentence, Niall Cooter and Christian Terry. July 2014.

49

Notice to Recipient

John Engeman is not affiliated with Bank of America Corporation and are solely responsible for the information they present at this event.

“Bank of America Merrill Lynch” is the marketing name for the global banking and global markets businesses of Bank of America Corporation. Lending, derivatives, and other commercial banking activities are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., member FDIC. Securities, capital markets, strategic advisory, and other investment banking activities are performed globally by investment banking affiliates of Bank of America Corporation (“Investment Banking Affiliates”), including, in the United States, Merrill Lynch, Pierce, Fenner & Smith Incorporated and Merrill Lynch Professional Clearing Corp., both of which are registered broker-dealers and members of SIPC, and, in other jurisdictions, locally registered entities. Merrill Lynch, Pierce, Fenner & Smith Incorporated and Merrill Lynch Professional Clearing Corp. are registered as futures commission merchants with the CFTC and are members of the NFA.

This document is intended for information purposes only and does not constitute a binding commitment to enter into any type of transaction or business relationship as a consequence of any information contained herein.

These materials have been prepared by one or more subsidiaries of Bank of America Corporation solely for the client or potential client to whom such materials are directly addressed and delivered (the “Company”) in connection with an actual or potential business relationship and may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with us. We assume no obligation to update or otherwise revise these materials, which speak as of the date of this presentation (or another date, if so noted) and are subject to change without notice. Under no circumstances may a copy of this presentation be shown, copied, transmitted or otherwise given to any person other than your authorized representatives. Products and services that may be referenced in the accompanying materials may be provided through one or more affiliates of Bank of America, N.A.

We are required to obtain, verify and record certain information that identifies our clients, which information includes the name and address of the client and other information that will allow us to identify the client in accordance with the USA Patriot Act (Title III of Pub. L. 107-56, as amended (signed into law October 26, 2001)) and such other laws, rules and regulations.

We do not provide legal, compliance, tax or accounting advice. Accordingly, any statements contained herein as to tax matters were neither written nor intended by us to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer.

For more information, including terms and conditions that apply to the service(s), please contact your Bank of America Merrill Lynch representative.

Investment Banking Affiliates are not banks. The securities and financial instruments sold, offered or recommended by Investment Banking Affiliates, including without limitation money market mutual funds, are not bank deposits, are not guaranteed by, and are not otherwise obligations of, any bank, thrift or other subsidiary of Bank of America Corporation (unless explicitly stated otherwise), and are not insured by the Federal Deposit Insurance Corporation (“FDIC”) or any other governmental agency (unless explicitly stated otherwise).

This document is intended for information purposes only and does not constitute investment advice or a recommendation or an offer or solicitation, and is not the basis for any contract to purchase or sell any security or other instrument, or for Investment Banking Affiliates or banking affiliates to enter into or arrange any type of transaction as a consequent of any information contained herein.

With respect to investments in money market mutual funds, you should carefully consider a fund’s investment objectives, risks, charges, and expenses before investing. Although money market mutual funds seek to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in money market mutual funds. The value of investments and the income derived from them may go down as well as up and you may not get back your original investment. The level of yield may be subject to fluctuation and is not guaranteed. Changes in rates of exchange between currencies may cause the value of investments to decrease or increase.

We have adopted policies and guidelines designed to preserve the independence of our research analysts. These policies prohibit employees from offering research coverage, a favorable research rating or a specific price target or offering to change a research rating or price target as consideration for or an inducement to obtain business or other compensation.

Copyright 2015 Bank of America Corporation. Bank of America N.A., Member FDIC, Equal Housing Lender.