managerial accounting 15th ed chapter 6a

TRANSCRIPT

PowerPoint Authors:Susan Coomer Galbreath, Ph.D., CPACharles W. Caldwell, D.B.A., CMAJon A. Booker, Ph.D., CPA, CIACynthia J. Rooney, Ph.D., CPA

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Super-variable Costing

Appendix 6A

6A-2

Learning Objective 6

(Appendix 6A)

Prepare an income statement using super-

variable costing and reconcile this approach with variable costing.

6A-3

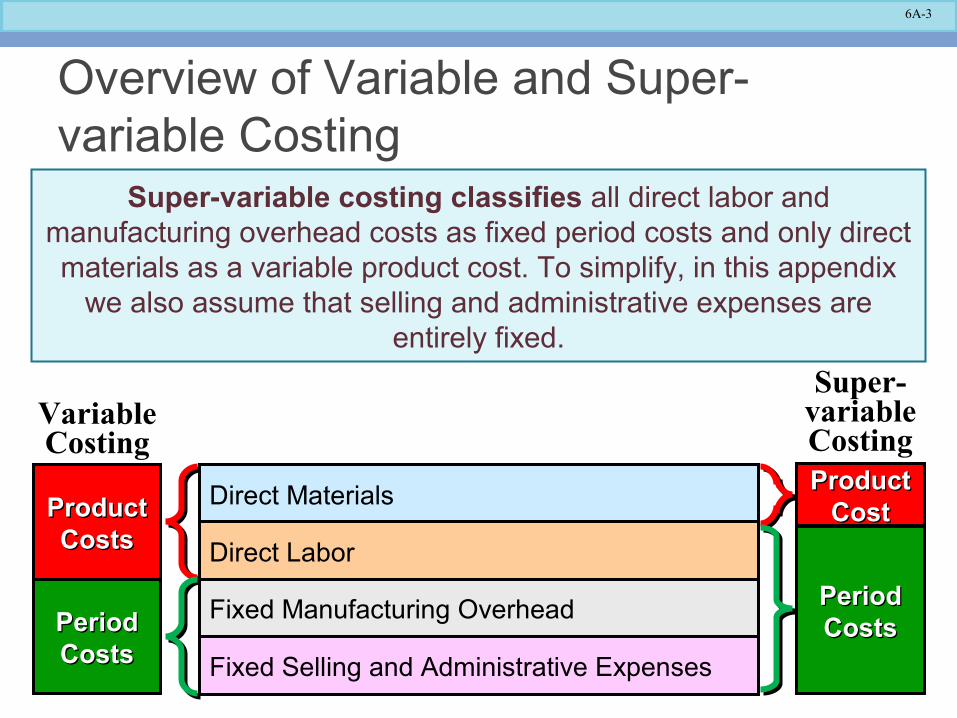

Overview of Variable and Super-variable Costing

Direct Materials

Direct Labor

Fixed Manufacturing Overhead

Fixed Selling and Administrative Expenses

VariableCosting

Super-variableCosting

ProductProductCostsCosts

PeriodPeriodCostsCosts

ProductProductCostCost

PeriodPeriodCostsCosts

Super-variable costing classifies all direct labor and manufacturing overhead costs as fixed period costs and only direct materials as a variable product cost. To simplify, in this appendix

we also assume that selling and administrative expenses are entirely fixed.

6A-4

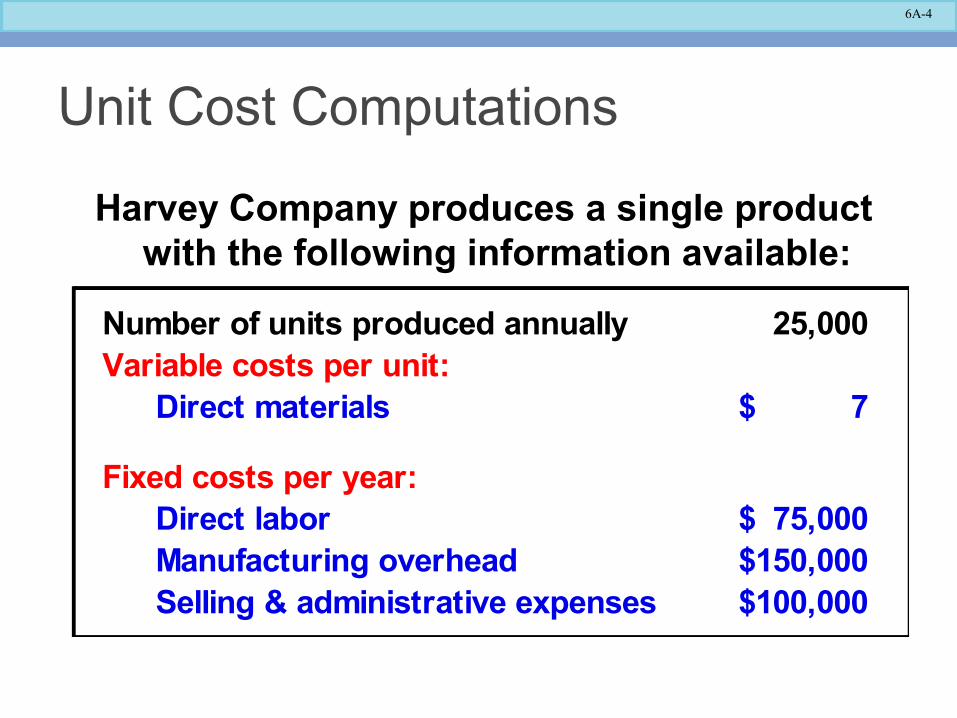

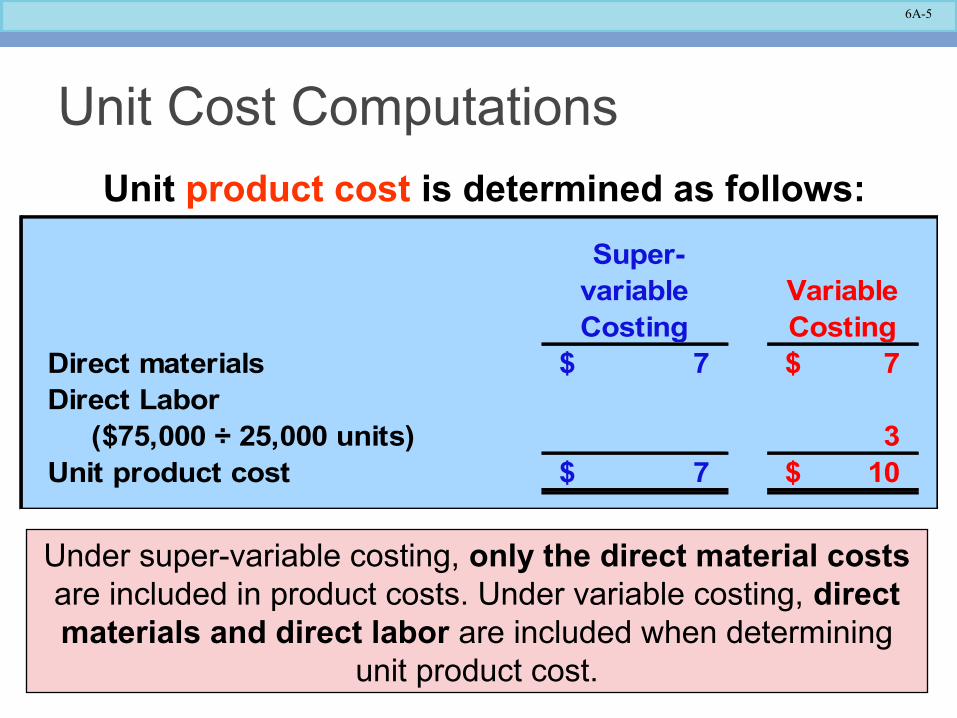

Unit Cost Computations

Harvey Company produces a single product with the following information available:

Number of units produced annually 25,000 Variable costs per unit:

Direct materials 7$

Fixed costs per year:Direct labor 75,000$ Manufacturing overhead 150,000$ Selling & administrative expenses 100,000$

6A-5

Unit product cost is determined as follows:

Super-variable Costing

Variable Costing

Direct materials 7$ 7$ Direct Labor ($75,000 ÷ 25,000 units) 3 Unit product cost 7$ 10$

Unit Cost Computations

Under super-variable costing, only the direct material costs are included in product costs. Under variable costing, direct materials and direct labor are included when determining

unit product cost.

6A-6

Let’s assume the following additional information for Harvey Company.▫ 20,000 units were sold during the year at a price

of $30 each.▫ There is no beginning inventory.

Now, let’s compute net operatingincome using both super-variableand variable costing.

Variable and Super-variable Costing Income Statements

6A-7

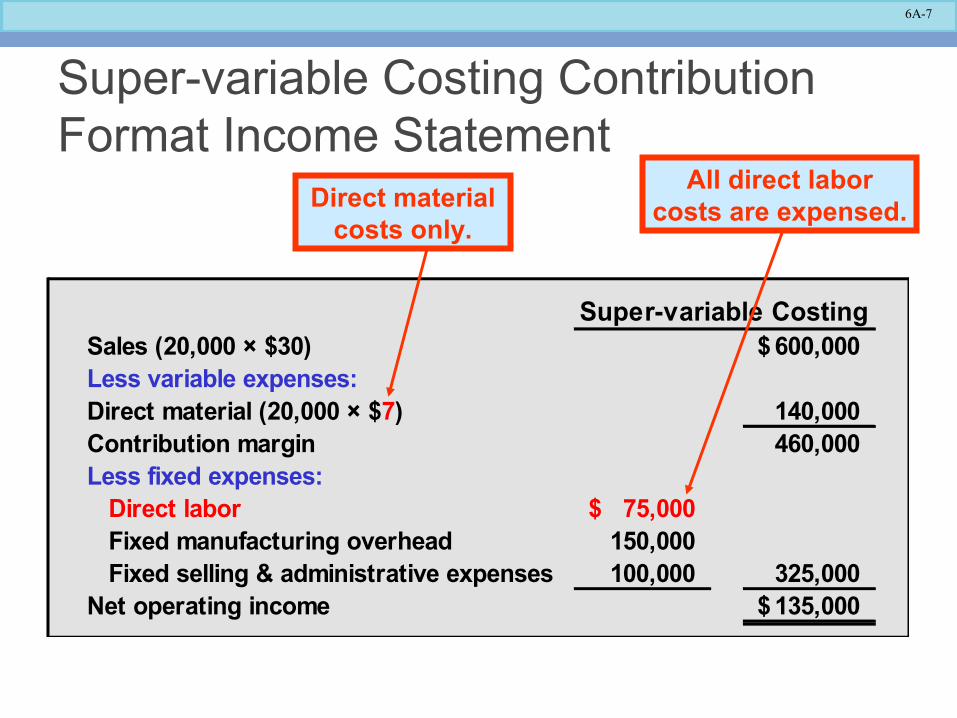

Super-variable Costing Contribution Format Income Statement

Super-variable CostingSales (20,000 × $30) 600,000$ Less variable expenses:Direct material (20,000 × $7) 140,000 Contribution margin 460,000 Less fixed expenses: Direct labor 75,000$ Fixed manufacturing overhead 150,000 Fixed selling & administrative expenses 100,000 325,000 Net operating income 135,000$

Direct material costs only.

All direct laborcosts are expensed.

6A-8

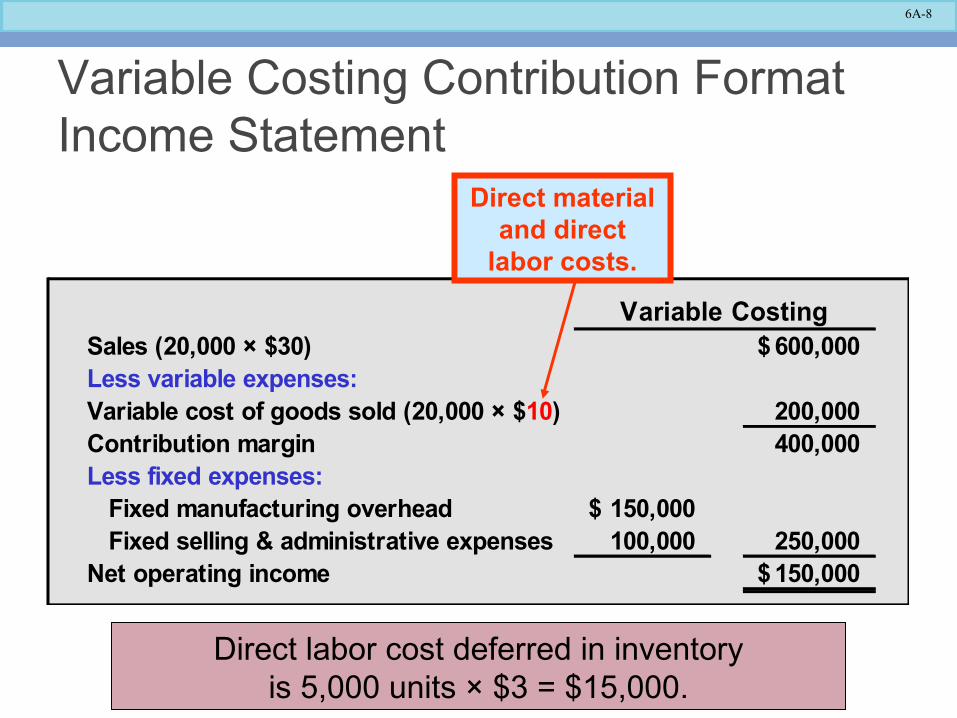

Variable CostingSales (20,000 × $30) 600,000$ Less variable expenses:Variable cost of goods sold (20,000 × $10) 200,000 Contribution margin 400,000 Less fixed expenses: Fixed manufacturing overhead 150,000$ Fixed selling & administrative expenses 100,000 250,000 Net operating income 150,000$

Direct material and direct

labor costs.

Direct labor cost deferred in inventoryis 5,000 units × $3 = $15,000.

Variable Costing Contribution Format Income Statement

6A-9

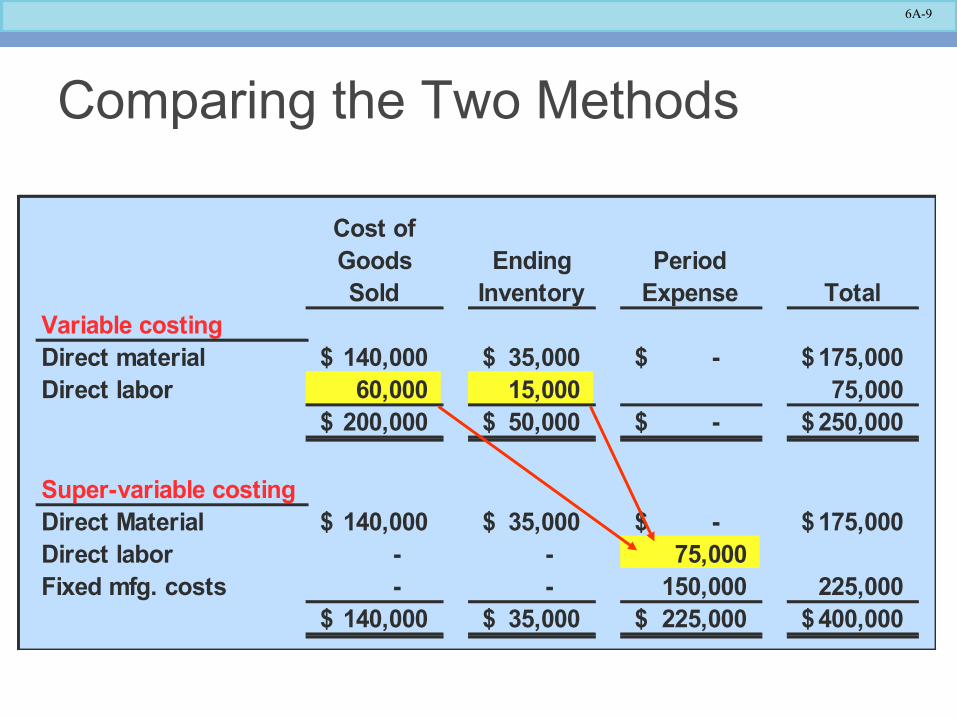

Cost of Goods Sold

Ending Inventory

Period Expense Total

Variable costingDirect material 140,000$ 35,000$ -$ 175,000$ Direct labor 60,000 15,000 75,000

200,000$ 50,000$ -$ 250,000$

Super-variable costingDirect Material 140,000$ 35,000$ -$ 175,000$ Direct labor - - 75,000 Fixed mfg. costs - - 150,000 225,000

140,000$ 35,000$ 225,000$ 400,000$

Comparing the Two Methods

6A-10

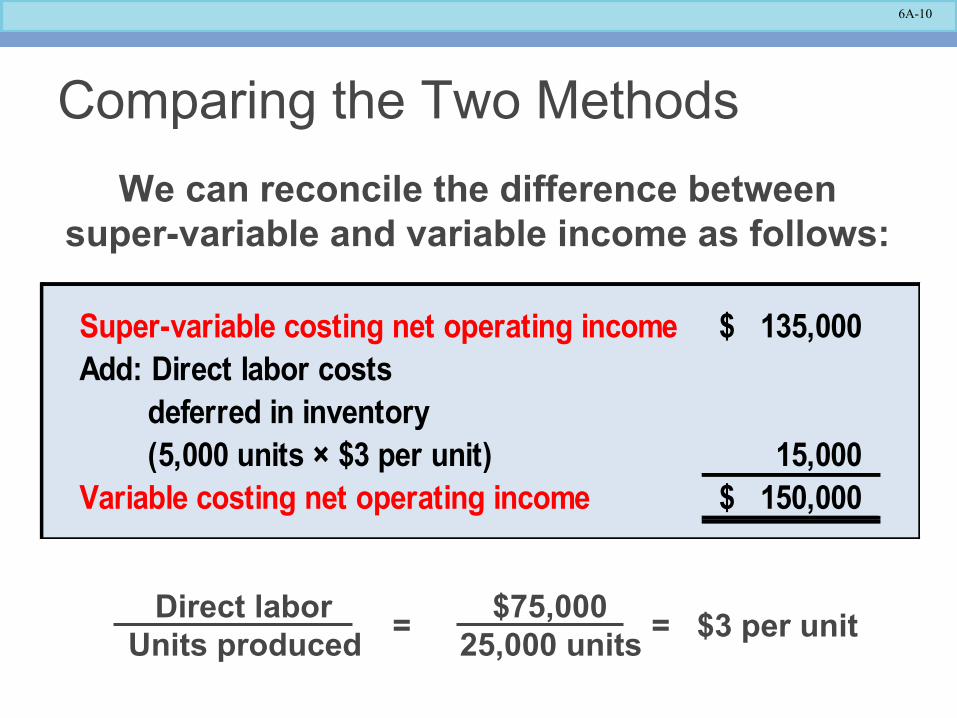

Direct labor $75,000 Units produced 25,000 units

= = $3 per unit

We can reconcile the difference betweensuper-variable and variable income as follows:

Super-variable costing net operating income 135,000$ Add: Direct labor costs deferred in inventory (5,000 units × $3 per unit) 15,000 Variable costing net operating income 150,000$

Comparing the Two Methods

6A-11

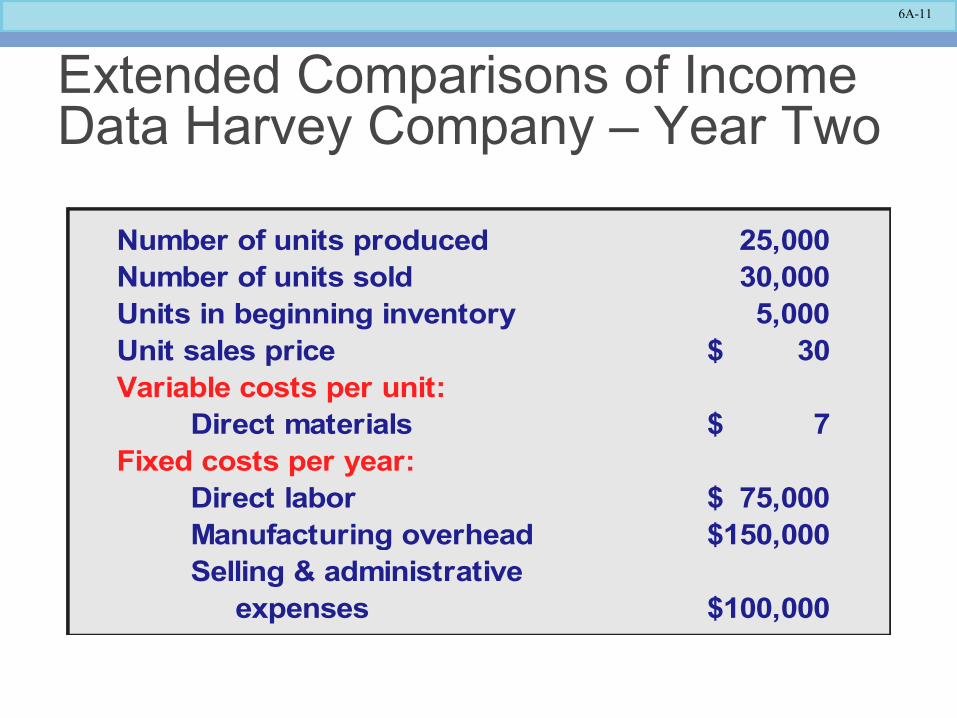

Extended Comparisons of Income Data Harvey Company – Year Two

Number of units produced 25,000 Number of units sold 30,000 Units in beginning inventory 5,000 Unit sales price 30$ Variable costs per unit:

Direct materials 7$ Fixed costs per year:

Direct labor 75,000$ Manufacturing overhead 150,000$ Selling & administrative expenses 100,000$

6A-12

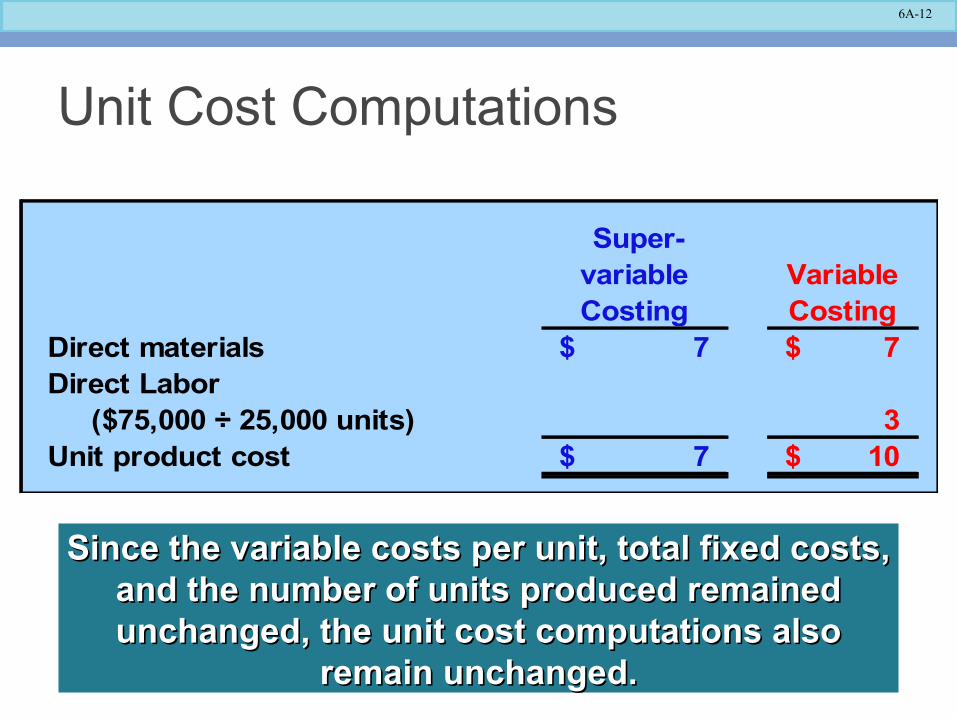

Since the variable costs per unit, total fixed costs, Since the variable costs per unit, total fixed costs, and the number of units produced remained and the number of units produced remained unchanged, the unit cost computations also unchanged, the unit cost computations also

remain unchanged.remain unchanged.

Super-variable Costing

Variable Costing

Direct materials 7$ 7$ Direct Labor ($75,000 ÷ 25,000 units) 3 Unit product cost 7$ 10$

Unit Cost Computations

6A-13

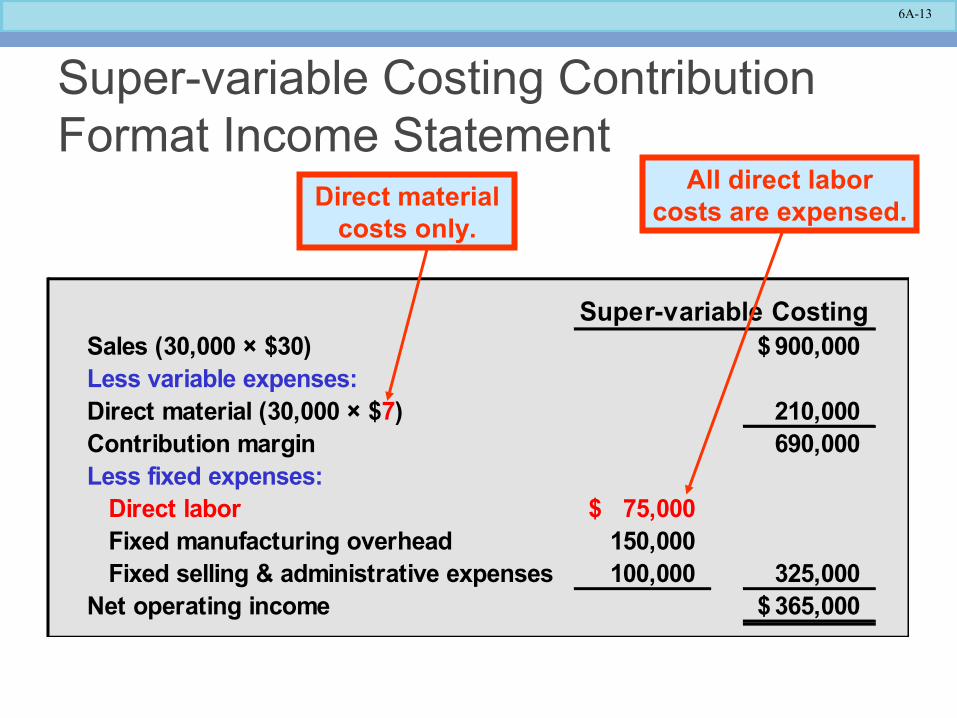

Super-variable CostingSales (30,000 × $30) 900,000$ Less variable expenses:Direct material (30,000 × $7) 210,000 Contribution margin 690,000 Less fixed expenses: Direct labor 75,000$ Fixed manufacturing overhead 150,000 Fixed selling & administrative expenses 100,000 325,000 Net operating income 365,000$

Direct material costs only.

All direct laborcosts are expensed.

Super-variable Costing Contribution Format Income Statement

6A-14

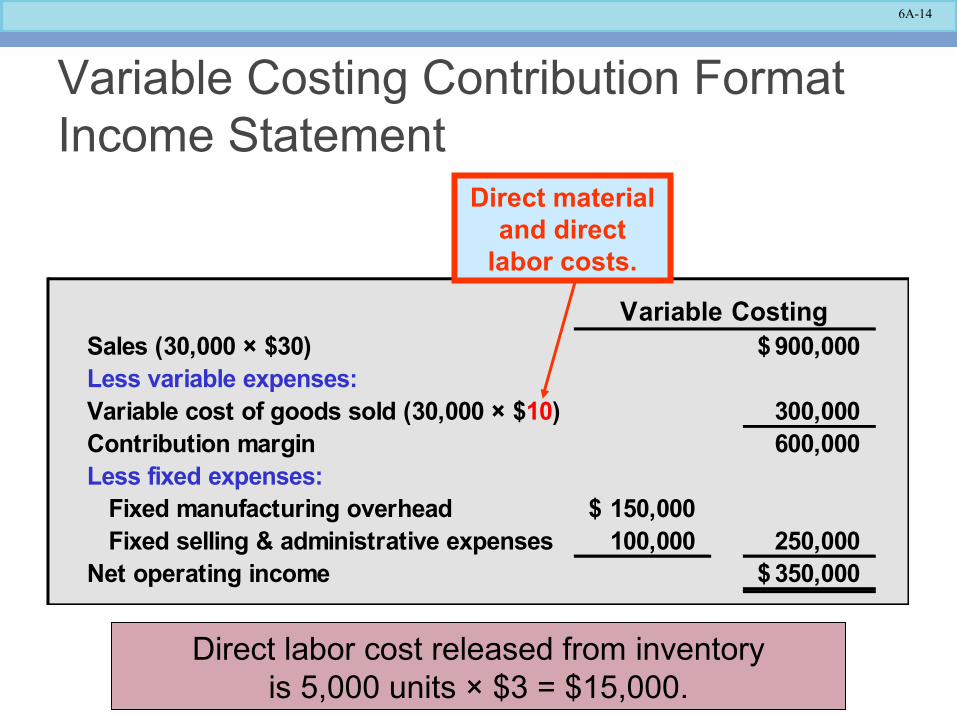

Variable Costing Contribution Format Income Statement

Variable CostingSales (30,000 × $30) 900,000$ Less variable expenses:Variable cost of goods sold (30,000 × $10) 300,000 Contribution margin 600,000 Less fixed expenses: Fixed manufacturing overhead 150,000$ Fixed selling & administrative expenses 100,000 250,000 Net operating income 350,000$

Direct material and direct

labor costs.

Direct labor cost released from inventoryis 5,000 units × $3 = $15,000.

6A-15

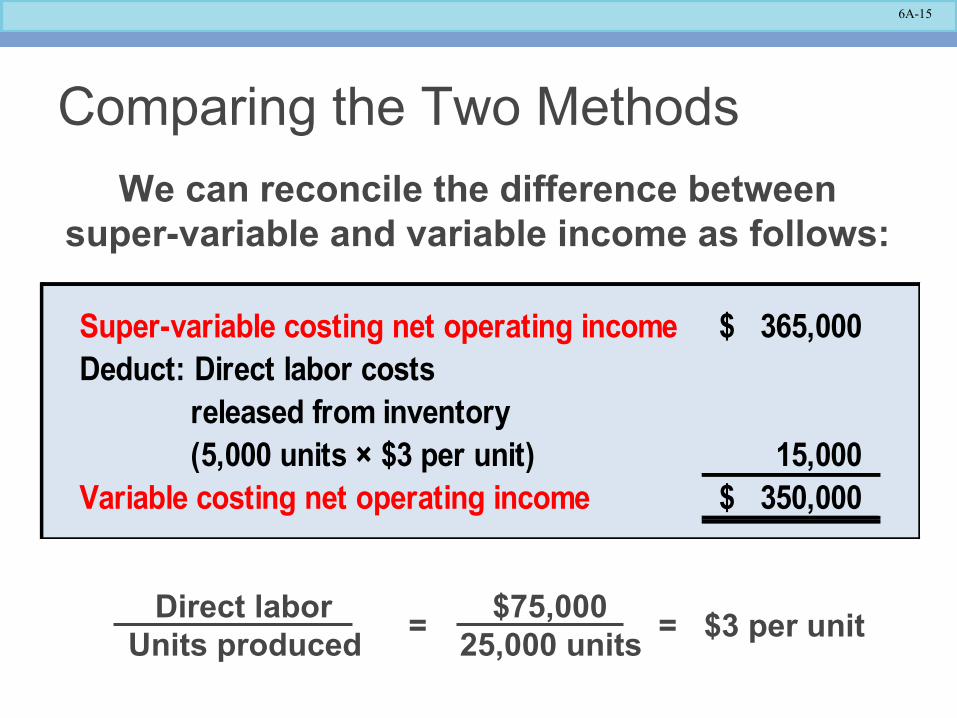

Comparing the Two Methods

Direct labor $75,000 Units produced 25,000 units

= = $3 per unit

We can reconcile the difference betweensuper-variable and variable income as follows:

Super-variable costing net operating income 365,000$ Deduct: Direct labor costs released from inventory (5,000 units × $3 per unit) 15,000 Variable costing net operating income 350,000$

6A-16

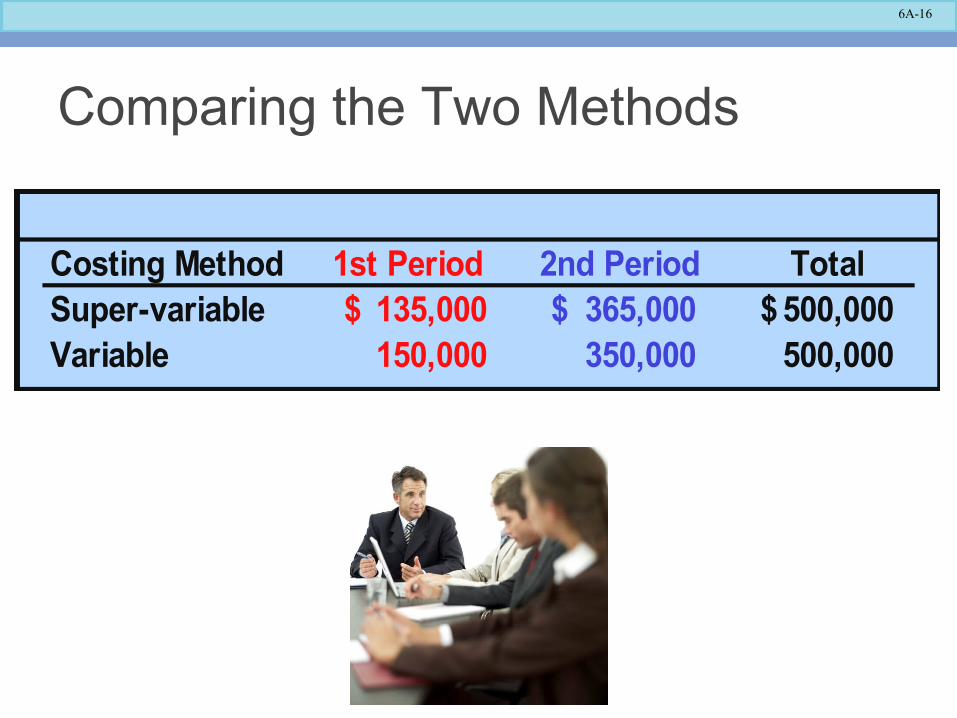

Costing Method 1st Period 2nd Period TotalSuper-variable 135,000$ 365,000$ 500,000$ Variable 150,000 350,000 500,000

Comparing the Two Methods

6A-17

End of Appendix 6A