management commentary / welltec · accounting year: january 1, 2013 ... is one of maximizing...

TRANSCRIPT

1 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

ANNUAL REPORT

Our

late

st t

ool a

dditi

on, t

he a

war

d-w

inni

ng W

ell C

utter®

Gam

e-ch

angi

ng s

olut

ions

for o

ur c

lient

s in

trans

form

ing th

e industry

Safe

r and

mor

e su

stain

able

with higher

recovery

2013Welltec International ApS

Central Business Registration No: 30 69 50 03

2 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

Company Welltec International ApS

Gydevang 25

3450 Allerød

Denmark

Phone: +45 48 14 35 14

Fax: +45 48 14 35 18

Website: www.welltec.com

E-mail: [email protected]

Central Business Registration No: 30 69 50 03

Registered in: Allerød

Accounting year: January 1, 2013 – December 31, 2013

Executive Board Jørgen Hallundbæk, Chief Executive Officer

Board of Directors Søren Jørgensen, Chairman

Jørgen Hallundbæk

Johannes K. J. Sikkens

Scott C. Collins

Company auditors Deloitte Statsautoriseret Revisionspartnerselskab

COMPANY DETAILS

our VALUES

DISRUPTIVE INNOVATIONISRU – We move with courage thto challenge conventional thinkinggto c

CLIENT DEDICATIONN – We do what it takes to completelyomaddress our clients’ challengeso

LEADERSHIP – We pride ourselves on taking actions that keep hrus in the forefronth

PROFESSIONALISM – We deliver what we promiseee

PERFORMANCE – We drive results through the dskills and committment of our people

3 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

CONTENTS

Company Details 2

Company Profile 4

CEO Letter 5

Consolidated Key Figures 6

Management Commentary 7

Financial Review 7

Outlook 12

Strategy 15

Competitive Strengths 17

Risks 19

Corporate Governance 21

Corporate Social Responsibility 22

Statement by Management on the Annual Report 28

Independent Auditor’s Reports 29

Financial Statements 30

Consolidated Group 30

Parent Company 71

Group Chart 85

4 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

COMPANY PROFILE

Welltec® is a leading provider of robotic intervention services

and completion solutions to the oil and gas industry. Our pi-

oneering technology enables operators to optimize the man-

agement and development of their assets throughout their

life-cycle. We address the factors that maximize value creation,

continuously innovating to reduce well construction time,

speed up access to the hydrocarbons and reduce the capital ex-

penditure compared to more conventional methods. The effect

is one of maximizing hydrocarbon production and increasing

total recovery while minimizing operating downtime.

Our lightweight technology also reduces the risk to personnel

and increases many safety aspects of the industry by enabling

smaller work crews and minimizing heavy lifting. Furthermore,

our technology allows operators to avoid the use of rigs, sig-

nificantly reducing the industry’s carbon footprint. Our ability

to operate in extended reach and horizontal wells allows op-

erators to drill multiple wells from the same topside location,

thereby further reducing the environmental footprint.

This is Welltec’s philosophy; to challenge existing conventions

and think laterally in order to develop products and services

which increase oil and gas recovery while improving the sus-

tainable, economic, environmental, and safety aspects of our

industry. In practice we develop, test and manufacture state-

of-the-art technology to enhance the production and recov-

ery rates for our clients, thereby improving their profitability

through a longer term revenue stream, while at the same time

improving upon health, safety and environmental attributes.

Our game-changing solutions allow our customers, some of

the world’s largest national and independent oil companies,

to optimize production through ground-breaking flexible well

completion solutions (WCS) and innovative well intervention

services (WIS). Our disruptive innovation challenges the con-

ventions, maximizing production, increasing oil recovery and

improving well-integrity and safety, with faster and less intru-

sive solutions in environments that are becoming increasingly

complex, remote and hostile.

In an industry characterized by maturing fields and increasing

depletion, the premium attached to technology which aids in

reversing these trends is continuing to gain momentum. Our

value proposition is compelling; our technology enables clients

to unlock more production from their assets and to address res-

ervoir complexities and uncertainties with a greater number of

options, which are cleaner, safer and more sustainable.

WE EMPLOY OVER 1,000 PEOPLE WORLD WIDE

– WITH 47 BASES IN 31 COUNTRIES

,

5 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

CEO LETTER

During the past year we decided to change our organizational

structure and implemented a more decentralized set-up that

balances global coordinated management with fast, local de-

cision-making to provide flexibility and strengthen our regional

capabilities.

While this transformation seems logical, the transition has not

been without challenges and a continued effort is needed in

2014. Regional differences, steep learning curves and organi-

zational alignment challenges have all prolonged the adapta-

tion process, and we did not deliver on our high expectations.

However, I remain confident that our efforts in 2014 will pave

the way for continued growth.

We have remained true to our vision of transforming the oil in-

dustry into one that is safer and more sustainable while achiev-

ing a higher recovery.

Our safety records were already well above industry standards

yet in 2013 we have taken this even higher with unprecedent-

ed safety improvements. Being a truly safe company to work

with is not only part of our vision; it is a critical element in posi-

tioning for winning major contracts worldwide.

The industry focus is shifting towards higher recovery and more

sustainable ways of extracting hydrocarbons, but we still have a

major task in driving the adoption of our enabling technology.

All three elements of our vision: safer, sustainable, higher re-

covery, are leading to lower lifting costs and therefore provide

significant value creation and improved margins for our clients.

The conventional wisdom is still, however, that these elements

increase costs, which may be true with the old technologies,

but the application of our technology achieves the best of both

worlds.

Operationally, we have managed to improve on our unparal-

leled levels of service quality. Our technology works, our opera-

tional processes work and our execution works. This provides a

reliable solution in the face of uncertain well conditions. Push-

ing the boundaries isn’t easy and when we look behind the

stats it becomes clear that we don’t improve because we ‘play-

it-safe’; we improve because we constructively learn from our

experiences.

We have a solid base on which to progress. Our clients have

firmly embraced our latest award-winning innovation, the Well

Cutter®, which eliminates the need to use explosives and the

risks and costs involved. Our largest clients’ satisfaction with

their early adoption of our Flex-Well® Completion Concept

proves that Welltec® has an expanding role to play in that mar-

ket too.

We have established the strategic framework to take Welltec®

to the next level in its corporate development. Our vision is

prevailing and our mission is to continue to drive the industry

adoption. The key is how successfully we can implement real

shifts in behaviors both from an internal and an external per-

spective. I believe that a united, refocused organization with a

stronger regional presence, continued technological leadership

and unparalleled service quality, will provide the foundation for

further success in the years to come

Jørgen Hallundbæk, CEO

nued technological leadership

will provide the foundatttiooioioooioiooioioooiooiooooooiooioioooiooiooooioiooioiooooooooooiooooooooooooooiooooooooioooooooooioooooioooooooiooooooooooon nnnnnnnnnnnnnnnnnnnn for

ome

Jørgen Hallundbæk, CEO

6 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

CONSOLIDATED KEY FIGURES Welltec International ApS – group

2013Restated

2012 2011 2010 2009

STATEMENT OF COMPREHENSIVE INCOME (USD in millions)

Revenue 321 295 229 164 135

Earnings before interest, tax depreciation and amortization (EBITDA)* 135 140 111 87 78

Operating profit (EBIT) before special items 72 86 57 48 39

Operating profit (EBIT) 68 86 57 46 37

Net financials (26) (38) (24) (16) (22)

Profit before tax 42 48 33 30 16

Net profit for the year 21 24 17 18 8

CASH FLOWS (USD in millions)

Cash flows from operating activities 100 95 84 74 74

Cash flows from investment activities (86) (79) (61) (46) (36)

Cash flows from financing activities (18) 12 (26) (29) (32)

Total cash flows (4) 29 (3) (1) 5

BALANCE (USD in millions)

Trade receivables 83 85 50 36 39

Equity 279 246 315 300 293

Total assets 712 692 596 577 602

Investments in intangible assets** 34 31 28 26 21

Investments in tangible assets** 55 51 36 22 17

Investments in financial assets 0 0 0 0 0

KEY RATIOS (%)

EBITDA-margin 42.1 47.3 48.5 52.7 57.8

EBIT-margin before special items 22.5 29.2 24.9 29.1 28.9

ROIC excl. goodwill 29.2 36.7 33.7 25.9 22.0

Return on equity 7.9 8.6 5.5 6.1 2.8

Number of employees, average 1,055 916 730 590 527

*EBITDA is defined as profits/loss before income taxes, financial expenses, financial income, special items and total depreciation and amortization. Depreciation for these purposes includes

depreciation attributable to development and manufacturing which is capitalized because it is considered a part of the costs that are directly attributable to the manufacturing of our products.

Furthermore, EBITDA has been adjusted for issued warrants (non-cash).

**Investments in intangible and tangible assets are defined as addition of fixed assets including additions from financial leasing and additions through business combinations.

The key figures are prepared in accordance with the Danish Society of Financial Analysts’ “Recommendations & Financial Ratios 2010”.

Change in presentation and functional currency

In the third quarter, Management decided to change the reporting currency of its consolidated financial statements to USD in order, to best represent the core business performance and its un-

derlying exposures. This is both from an operational and a capital structure perspective. In addition this accommodates requests from investors and serves to make the consolidated financial state-

ments more comparable within Welltec’s peer group. At the same, Management reconsidered the group’s functional currency and assessed the USD to be the functional currency for the Danish

operation and operations in some other countries. Management identified the issuance of USD bonds in the beginning of 2012 as the main event triggering the change in functional currency from

DKK to USD, and consequently the change in functional currency is deemed to have taken place at that date.

7 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

alternatives. In Europe and Russia CIS, geographic expansion in

the Caspian region has counterbalanced lower activity in the

North Sea and on land Russia earlier in the year. In the Middle

East we have expanded operations in Qatar, Oman and Yemen,

where we set a new record for the 218 Well Tractor® with the

longest distance covered in one descent. The tool string, con-

veying a Production Logging Tool (PLT), was tractored for an im-

pressive 14 kilometers in difficult borehole conditions to depths

and inclinations that conventional methods cannot achieve.

In the Americas, revenues of USD 112 million represented

growth of 5%. In the US new client activity on land and in-

creased subsea activity in the Gulf of Mexico has primarily con-

tributed to the growth. This included two world firsts using

Riserless Light Well Interventions (RLWI). The first to retrieve

Crown Plugs and the second for the clean out of asphaltene.

Welltec’s RLWI capabilities open up the possibility of intervening

Revenue

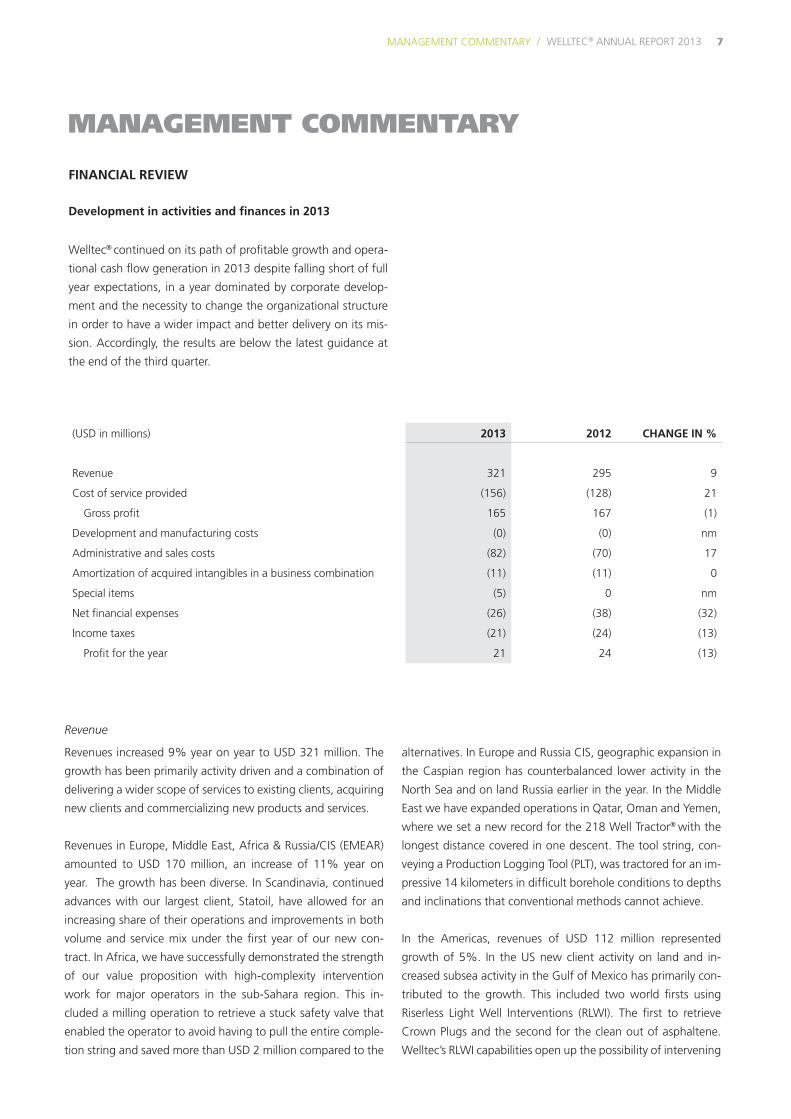

Revenues increased 9% year on year to USD 321 million. The

growth has been primarily activity driven and a combination of

delivering a wider scope of services to existing clients, acquiring

new clients and commercializing new products and services.

Revenues in Europe, Middle East, Africa & Russia/CIS (EMEAR)

amounted to USD 170 million, an increase of 11% year on

year. The growth has been diverse. In Scandinavia, continued

advances with our largest client, Statoil, have allowed for an

increasing share of their operations and improvements in both

volume and service mix under the first year of our new con-

tract. In Africa, we have successfully demonstrated the strength

of our value proposition with high-complexity intervention

work for major operators in the sub-Sahara region. This in-

cluded a milling operation to retrieve a stuck safety valve that

enabled the operator to avoid having to pull the entire comple-

tion string and saved more than USD 2 million compared to the

(USD in millions) 2013 2012 CHANGE IN %

Revenue 321 295 9

Cost of service provided (156) (128) 21

Gross profit 165 167 (1)

Development and manufacturing costs (0) (0) nm

Administrative and sales costs (82) (70) 17

Amortization of acquired intangibles in a business combination (11) (11) 0

Special items (5) 0 nm

Net financial expenses (26) (38) (32)

Income taxes (21) (24) (13)

Profit for the year 21 24 (13)

MANAGEMENT COMMENTARY

FINANCIAL REVIEW

Development in activities and finances in 2013

Welltec® continued on its path of profitable growth and opera-

tional cash flow generation in 2013 despite falling short of full

year expectations, in a year dominated by corporate develop-

ment and the necessity to change the organizational structure

in order to have a wider impact and better delivery on its mis-

sion. Accordingly, the results are below the latest guidance at

the end of the third quarter.

8 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

in subsea wells and actively managing fields that are not eco-

nomically viable with conventional methods. Successes on the

East Coast of Canada have increased our share of operations

with major operators and offset the adverse effects of some

extreme weather conditions in the third quarter. Across Latin

America, Welltec® has grown in all of the markets it operates

in, leveraging on an expanded tool fleet to widen the scope of

services with the region’s national oil companies, particularly in

Mexico and Brazil.

In Asia Pacific, revenues grew 10% to USD 40 million. A high-

light for the region was the completion of seven years with no

lost time incidents (LTI’s), demonstrating utmost dedication to

safety. Financially, India was the main driver following land-

mark direct contract awards with major operators and delivery

of high value mechanical services, such as opening sliding side

doors (SSDs) on wireline, using the Well Stroker® in place of coil

tubing due to its superior depth control, power and precision.

Cost of service provided

The cost of service provision was USD 156 million, an increase

of 21% compared to last year. This was higher relative to the

revenue growth and explained in terms of both the growth and

change in activity mix, geographically and in the type of ser-

vices performed.

The increase in cost of service provision was primarily attribut-

able to increased field staff costs of USD 11 million, with aver-

age operational headcount increasing 20% to support higher

levels of activity. The number of jobs performed increased by

19% over the same period, partly reflecting an increased in-

vestment in operational capacity at the start of the year to sup-

port growth, and partly on account of qualitative changes in

the sales mix.

The service mix is diverse and dynamic, reflecting an ever-

changing-mix of operations across the globe, onshore and off-

shore, in established and emerging markets, and for new and

existing clients. Other direct operational costs have increased

27%, with proportionally higher levels of leasing, freight and

direct material costs, largely reflecting the growth from new

clients and emerging countries that require greater operational

investments. A characteristic of our growth cycle and indeed

strategy is the broadening of the client base within our core

tractor conveyance offerings and leveraging to provide a more

value-adding scope of services. The reduction in gross margin

can partly be explained by this development, with an increased

share of conveyance activity in the full year.

Administrative and sales costs

Administrative and sales costs were USD 82 million, an increase

of 17% compared to last year. The increase was a combination

of the increased scale of operations, through higher premises,

IT and administrative costs, a 16% growth in average head-

count and increased consultancy fees relating to HR strategy

and executive level projects.

Earnings before interest, tax, depreciation, amortization and

special items (EBITDA)

EBITDA reduced by 3% to USD 135 million, representing an

EBITDA margin of 42% against 47% in 2012. This develop-

ment was the combination the change in service mix, with in-

creased conveyance activity, and reduced gross margins with

the expansion of activity.

Operating profit before special items (EBIT)

EBIT decreased by 16% to USD 72 million. The EBIT margin was

23% against 29% in 2012, reflecting the reduction in earnings

and the relative development in depreciations and amortizations.

9 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

Special items

Special items of USD 5 million relate the adjustment to head-

count in the second quarter as part of the decentralization

initiative and non-recurring consultancy fees.

Net financial expenses

Net financial expenses were USD 26 million, a decrease of 32%

compared to last year. Interest expenses were 2% higher, re-

flecting the first, full year following the bond offering. This was

countered by gains on the fair value adjustment of derivative

financial instruments and a net reduction in unrealized currency

losses.

Income taxes

Income taxes were USD 21 million, a decrease of 13% year

on year, reflecting the reduced level of operating profit, partly

offset by an increase in the effective tax rate. This increase was

due to the revision of tax provisions on issues addressed during

the year and the adverse effects arising from the non-deduct-

ibility of the higher interest expense and non-deductibility of

withholding taxes.

Profit for the year

Profit was USD 21 million, a decrease of 13% on 2012. This

development was due to the reduction in EBIT and increase in

special items, partly offset by the reduction in net financial ex-

penses and income taxes.

Free cash flows

Welltec® continued to generate strong cash flows from opera-

tions and improved the level of days’ sales outstanding (DSO)

across the year through improved processes and strict working

capital discipline. The cash generated was used to service inter-

est payments, repurchase shares and reinvested in D&E proj-

ects, patents and additional tractors and tools as part of the

cycle of continued growth delivery. Additionally, capital expen-

ditures increased in support of the well completions business,

including the acquisition of Alslev Rustfri Montage and lease-

hold improvements on the new production facility in Esbjerg.

CAPEX % of Revenue

3748

64

8289

28% 29% 28% 28% 28%

2009 2010 2011 2012 2013

CF from operations % of Revenue

74 7484

95 100

55%45%

37% 32% 31%

2009 2010 2011 2012 2013

REVENUE (USD in millions) EBITDA (USD in millions)

CAPEX (USD in millions)CASH FLOW FROM OPERATIONS (USD in millions)

Revenue YOY Growth

135164

229295 321

4%

21%40%

29%

9%

2009 2010 2011 2012 2013

EBITDA Margin

78 87111

140 135

58%53%

49% 47%42%

2009 2010 2011 2012 2013

Branches

Welltec International ApS group has several branches with sales activities in foreign countries. Please see group chart on page 85.

10 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

Significant events in 2013

Adjustment to headcount

As part of the initiative to decentralize while ensuring the

right mix of competencies and capabilities, Welltec® reduced

the number of employees at its Danish headquarters by 27 in

April 2013. This mainly related to indirect capacity costs and re-

aligned the business on the underlying growth trajectory.

Capital increase

During the third quarter, Welltec® completed a private place-

ment with PFA, Denmark’s largest pension fund. Gross pro-

ceeds amounted to USD 46 million, securing PFA a minority

interest, and have been designated to strengthen Welltec’s

capital structure and further develop the business.

BID PRICE (USD)

96

98

100

102

104

106

108

110

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

BID YIELD (%)

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

Bond performance

The Senior Secured Notes have continued to trade above par,

with meaningful demand in the secondary trading. The im-

plied funding cost has been reduced from 8.5% upon issuance

to 6.4% at year end.

,

11 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

Development in activities and finances in Q4

The fourth quarter demonstrated sequential growth but was

slightly lower than last year due to the activity mix and adverse

currency developments.

A plateau in the growth rate was recognized earlier in the year

and dedicated efforts to address the underlying challenges

have continued, including several strategic initiatives that have

been set in motion to transition the organization to the next

phase of corporate development and accelerate growth.

Revenues increased sequentially to USD 84 million; represent-

ing a 2% reduction on the fourth quarter last year which was

boosted by the client-sponsored development of our Coil Tub-

ing Well Tractor® and a relatively large sale of our well comple-

tion products.

Adjusting for currency developments, however, underlying

revenues showed continued growth with further operational

successes with our Well Cutter®, RCB Well Cleaner® and Well

Stroker®.

Another operational highlight was the delivery of additional

Well Annular Barriers, WAB® to both existing and new clients,

with multiple qualifications made for more sales and product

releases in 2014. This followed the announcement of an agree-

ment to lease a new dedicated and purpose-built production

facility in Esbjerg, and represents the next step in our expansion

in the Well Completions market. This also contributed to the

increase in CAPEX in the period.

CAPEX % of Revenue

23 26 21 1626

26%35%

25%21%

30%

2012 Q4 2013 Q1 2013 Q2 2013 Q3 2013 Q4

CAPEX (USD in millions)

CF from operations % of Revenue

3329

17 1936

39% 38%

20%25%

42%

2012 Q4 2013 Q1 2013 Q2 2013 Q3 2013 Q4

CASH FLOW FROM OPERATIONS (USD in millions)

Revenue YOY Growth

86 75 84 78 84

39% 16% 23%

2% (2%)

2012 Q4 2013 Q1 2013 Q2 2013 Q3 2013 Q4

REVENUE (USD in millions) EBITDA (USD in millions)

EBITDA Margin

3927

3933 36

46%

36%

47% 42% 43%

2012 Q4 2013 Q1 2013 Q2 2013 Q3 2013 Q4

Quarterly numbers in above graphs are unaudited.

12 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

OUTLOOK

While macro-economic factors continue to impact the opera-

tions of our clients, the total potential market that Welltec® can

address far exceeds any boundaries imposed by the capacity of

our organization or short term trends in the industry.

Strong market fundamentals underlie the increasing demand

for our services. With the shale gas revolution and increasing

depletion of maturing oilfields, operating environments are be-

coming increasingly unconventional, remote and hostile. The

strategic focus of the oil and gas industry is shifting towards

the development and optimization of assets with a step change

in complexity and development risk. This is Welltec’s sphere of

expertise.

Our technology offers advantages in all types of wells. As the

absolute leader within robotic well intervention technology,

Welltec® remains in a prime position to benefit from these mar-

ket drivers. However, the industry adoption of robotic technol-

ogy to displace tried-and-tested conventional methods rep-

resents a significant barrier to growth in a conservative and

risk-averse industry. The ability to drive this transformation is a

primary element of the organizational changes implemented in

the second half of 2013.

We expect a decentralized organization with a stronger region-

al presence and a unified approach to gain further traction over

the course of the coming year. Organic growth will result from

increased activity and uptake of all our services, leveraging on

the many contract awards and extensions secured in 2013

as well as building on the operational successes in our wide

portfolio of offerings. This will be predominantly within well

intervention. Continued momentum in our well completions

business will provide an increased contribution, although the

associated lead times will naturally limit this development in the

coming year.

Innovation remains an integral part of our competitive advan-

tage. The release pipeline for 2014 includes the launch of our

next generation tractor, the Well Tractor CR® (compact rig-

up), which will be the shortest, fastest tractor in the market.

This provides value in applications globally with limited rig-up

heights such as small platforms and provides synergies with our

efforts to provide applications supporting RLWI initiatives. Also

planned is the launch of the first of Welltec’s diagnostic tools,

the Welltec® Hardware Scanner, which adds value for our cus-

tomers through its capabilities to provide real-time measure-

ments for correlation as well as hardware position.

Management expects continued growth in revenue in 2014

and an improvement in EBITDA. Revenue is expected to be

around USD 340 million (6% growth) with an EBITDA of USD

140 million, equating to an EBITDA margin around 42% on the

basis of a similar service-mix as delivered in 2013.

Forward-looking statements provide current expectations or

forecasts for events, such as product launches, and financial

performance. Such statements are subject to risks, uncertain-

ties and inaccurate assumptions. Actual results may differ from

expected results. Factors that may affect future results include

fluctuations in exchange rates, oil and gas prices, changes in in-

terest rates, production problems, unexpected contract breach-

es or terminations, market-driven price decreases, introduction

of a competing product, Welltec’s ability to successfully market

both new and existing products, exposure to lawsuits and un-

expected growth in costs and expenses.

13 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

ouurrrr VVVVVVVAAAALLLLLLUES

DISRUPTIVE INNOOVVVVAAATAATAA IOOOOONNNN – We move wwiith ccooouuuraagto challennnngggeege cooooonno ventional thhinkinnggggto challennnngggeeg cooooonnventional thhinkingnggg

CLIENT DEDICATIOOONNNNN ––– WeWee ddddo o what it taakkekekeeesss toto ccompletely addrrreeeessssss s ouuur clclieieentnts’ chaallllennne gggegess

LEADERSHIP – We pppprririiriddede oouururseseelvlvlvlvlvvveeeseseses on taakikikkikikikikikingngggngngngngnggg aaaaaaaactctctctctctccc ioioioioi nsn that keep usus iinnnnnnn ttthththe forefront

PROFESSIOOONONNNAAAAAALISSSSM – We deliver wwwwhahahat t wewe pprooromimimimimisesesese

PERFORRRRRMMMMAMAMANNNCE – WeWeWeWeWeWeeWee dddddddddddddddrirrrr ve resullltstsstt tthrough tthehe skskskkkilililillllllsl aaaandndndndnn cccoommmmmmimittmmmmemeeeeeeeem ntnnnnnn of ouuurr r ppeoplee

ge

oououourrrr MMMMMMMIISSSSIIOONNissss tttoooo o dddedevelop and deliver

GAGAAMMMME-CHANGINGGAGAAGGAMMME-C solutions

enable our clients towwwhwhwhicich e

E THE MANAGEMENT OOOOOPTIMIZE

D DEVELOPMENTAND

of their assets.o

VISION, MISSION AND VALUES

our VVVVISIONNNNis too TTRRRRANSFORMMMM the

upupststrereaammmmm oil and gggaas indus-

try suchh,,, ttthht at it beeccoomes SAFER

and mooooorrrere SUSTAAAIAINABLE while

aaaachievinnngg higher

RECCCOOVERY.

14 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

15 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

STRATEGYWelltec® has a simple, coherent strategic concept and

framework.

Our Vision

Welltec’s unique perspective is to transform the upstream oil

and gas industry such that it becomes safer and more sustain-

able while achieving higher recovery.

Our Mission

Our mission, therefore, is to develop and deliver game-chang-

ing solutions, which allow our clients to optimize the manage-

ment and development of their assets.

Our Values

We hold and adhere to a constant set of values that resonate in

our everyday work:

Disruptive Innovation

We move with courage to challenge conventional thinking

Client Dedication

We do what it takes to completely address our clients’

challenges

Leadership

We pride ourselves on taking actions that keep us in the

forefront

Professionalism

We deliver what we promise

Performance

We drive results through the skills and commitment of our

people

Together, our mission and values create a core guiding philoso-

phy that embodies what Welltec® stands for. This is the corner-

stone of our success and provides the constant unifying ele-

ment as we strive to realize of transforming the oil and gas

industry.

Welltec® is strategically focused on driving the company’s

growth through continued development on four strategic

themes: Growth, Strength, Position and Profitability.

Growth

We believe that challenging conventional solutions will con-

tinue to allow us to deliver disruptive technology that adds

significant value for our clients. Coupled with improved service

delivery and responsiveness to our client’s needs, we will de-

liver growth in several key regions:

• Scandinavia: Welltec® will continue to leverage on the

long-standing relationships with our largest clients, which

provide both the impetus and pathway for introducing

new solution concepts to them as well as their peers in the

Norwegian Sea.

• Americas: Our value proposition allows for continued

growth in the highly competitive onshore markets. The cur-

rent footprint in the conveyance market for unconventional

oil and gas plays in North America provides the platform for

further client penetration with higher-value services such as

milling, cleaning and mechanical services that continue to

be served by conventional technologies. Increased penetra-

tion in the Gulf of Mexico and in offshore Latin America

constitute a potential for significant growth in the majority

of offerings.

• Europe, Russia and CIS (ERC): Welltec® will seek to

MANAGEMENT EXPECTS CONTINUED GROWTH IN REVENUESAND MAINTAINED EBITDA MARGINS IN 2014

GROWTHOour VISION

is to TRANSFORM the up-

stream oil and gas industry such,

that it becomes SAFER and more

SUSTAINABLE while achieving

higher RECOVERY.YY

16 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

accelerate the uptake of its services in some of the emerg-

ing territories, such as the Caspian where international

access and production continues to increase. In Continen-

tal Europe and the more established markets, Welltec® will

increase its market share through growth in more complex

services, such as riserless well intervention services (RLWI) in

the North Sea.

• Africa: Continued business development with the region’s

dominant international oil companies will provide the main

driver of growth, leveraging on key direct contract awards

• Middle East: Welltec® remains committed to pursuing con-

tinued collaborations and contracts in Saudi Arabia as well

as further opportunities throughout the region. Many of

the national oil companies continue to express sustained in-

terest in our products, particularly in UAE, Qatar and Oman.

• Asia Pacific: Welltec® plans to capitalize on the considerable

market growth potential, both through increased penetra-

tion of existing clients in Malaysia and India, and further

penetration of new clients the south of the region, adding

new business in Indonesia and Australia.

Strength

We plan to continuously strengthen our business and opera-

tional models to provide better services in a way that endorses

long term relationships with our customers. Working more

closely with our customers over longer periods of time ensures

not only a more stable revenue stream but also allows Welltec®

to develop faster and more accurate solutions to meet our

customers’ challenges; thereby perpetuating the value cycle.

We have begun several projects which support this initiative,

including:

• Expansion of our service offerings and product ranges to

broaden our portfolio and reduce dependency upon any

single service or solution;

• Establishing more direct, contractual ties with our custom-

ers as well as longer duration agreements which secure

more planned, dedicated work;

• Streamlining our organizational structure to reflect our

value chain, and thereby matching a global, company-wide

integration of services where roles, responsibilities and

interactions between different parts of the organization are

being clarified to improve performance;

• Recruiting and retaining engineering and management

talent;

• Introducing scalable structures and procedures across our

organization that support our growth, primarily through le-

veraging our already established IT-driven infrastructure and

ensuring that knowledge is built into the structure of the

organization rather than depending on specific individuals;

• Patenting our technology and protecting our intellectual

property and proprietary know-how.

Position

Welltec® is focused on providing unique solutions and avoiding

those markets where services are effectively commoditized. We

intend to attract and satisfy more reference customers through

a focus on global account management, increasing the skill

sets of our current account managers, maintaining our focus

on direct customer relationships and by accelerating the rate of

technology replacement to our offerings across all geographies.

We pursue and maintain strategic partnerships with other ser-

vice providers, such as selected wireline providers, vessel provid-

ers and technology companies, where our combined offerings

BROADEN OUR PORTFOLIO AND REDUCE DEPENDENCY UPON ANY SINGLE SERVICE OR SOLUTION

STRENGTH &POSITION

17 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

can be presented to clients as a complete solution. Welltec® can

therefore leverage on both direct client relationships to act as

lead contractor as well as serve as subcontractor to strategic

partners.

Furthermore we actively engage in developing new solution

concepts that addresses our customer’s largest challenges, such

as RLWI for subsea wells, plug and abandonment of wells and

open-hole intervention services in horizontals that require inte-

grated, specialized solutions and equipment. These solutions

provide significant value to our customers as they enable them

to redefine the manner in which they operate and establish

new industry standards. We believe the value creation this de-

livers for our clients will be rewarded through an increase in our

own business. Overall, Welltec’s goal is to maintain its position

as a top provider of the current offerings while simultaneously

providing unique, new solutions in other segments. Our pipe-

line of new service and product initiatives are aimed at develop-

ing a diversified and growing business in terms of revenues and

margins in 2014 and beyond.

Strong market fundamentals support the increasing demand

for well intervention services. The market remains advanta-

geous and our clients continue to embrace our technology and

the services and solutions we provide. While increased activity

in our segments by large service companies may create short

term challenges, it also brings a welcomed boost in driving the

industry’s adoption of our technology and in doing so signifi-

cantly increases the addressable market. It also represents a sig-

nificant endorsement of the robotic well intervention technol-

ogy we have pioneered.

Profitability

Optimizing on costs is an integral part of creating value for our

clients and we are proactively looking for more effective and ef-

ficient ways to deliver without impairing the exceptionally high

standards of our operations. Cost-consciousness in conjunction

with providing solutions which serve to optimize production se-

cures high margins and ensures financial strength for continued

expansion.

The financial goals for growth and profitability enable continual

investments in line with the company’s strategies to strengthen

Welltec’s position and ultimately deliver its mission.

COMPETITIVE STRENGTHS

Global presence

Over the last decade, operational and capital expenditure by oil

and gas companies has increased. Welltec® expects this trend

to continue given the ongoing efforts to improve production

from existing fields and search for new reserves. Forecast spend

for the major oil and gas companies is up and this trend will

favor companies such as Welltec® that have advanced and dif-

ferentiated technological offerings covering all phases of the

well lifecycle.

From a global perspective, oil fields are maturing and new dis-

coveries are not keeping pace with declines or demand consid-

eration. This combination of increasingly mature fields, reduced

quantity and size of new discoveries and increasing global

WE PURSUE STRATEGIC

PARTNERSHIPS WITH OTHER

SERVICE PROVIDERS, SUCH

AS SELECTED WIRELINE PRO-

VIDERS, VESSEL PROVIDERS AND

TECHNOLOGY COMPANIES, WHERE OUR

COMBINED OFFERINGS CAN BE PRESENTED TO

CUSTOMERS AS A COMPLETE SOLUTION.

our MISSIONis to develop and deliver GAME-

CHANGING solutions which

enable our clients to OPTIMIZE THE

MANAGEMENT AND DEVELOPMENT

of their assets.

18 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

demand represents a huge challenge for all. Welltec’s expec-

tations are that our value proposition of developing methods

for increased reservoir optimization will resonate with our cus-

tomer’s around the world as they seek to increase the life span

of existing fields.

New discoveries are increasingly being made in areas present-

ing significant operational complexity for exploration and de-

velopment. Almost half of all newly discovered oil reserves

since 2000 have been made in offshore deep-water or ultra

deep-water. An increasing portion of new supply is also com-

ing from unconventional reserves (such as shale gas or shale oil)

adding further complexity in the form of more horizontal well

designs. The shift in discoveries and resource types have also

increased the technical risk of projects and the requirements

of the equipment and services necessary to handle these more

challenging operating conditions, which have also driven the

need to use advanced technologies in well intervention. It is

our experience that oil and gas companies are becoming more

likely to work with suppliers of high-quality services as they de-

liver a higher long-term value. With the increased complexity

and costs of new discoveries, well interventions have become

an attractive economic proposition compared to exploring for

new reserves. Welltec’s technology, which has a proven record

of successful operations in these environments, will continue to

be in demand.

TECHNOLOGY

Superior offering

The increased focus on enhancing oil and gas recovery rates

and improving well profitability has led to an increasing indus-

try acceptance of Welltec’s robotic technology.

Well intervention services increases well profitability through

increased recovery rates and cash flow from production. Given

the challenges of sustaining oil and gas production to meet de-

mand we expect the well intervention market will grow signifi-

cant in the coming years. Due to its superior performance, we

expect robotic technology to grow even faster than the market

for conventional intervention technologies, and gradually even

replacing older methods. Robotic intervention technology is su-

perior to these conventional methods because it is:

• safer given its smaller footprint and lower number of per-

sonnel involved, leading to significant health and safety

advantages for our customers;

• less intrusive because it requires a smaller set up space and

a more limited amount of equipment to be inserted into

the well, typically resulting in less damage to the well;

• an order of magnitude faster than conventional methods

due to deployment and rig up times; and

• more cost efficient, both in terms of lower direct in-

tervention costs and lower future costs for subsequent

interventions.

19 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

Market Leader

We pioneered the well intervention services market with our

robotic technology. Our technological leadership has been rec-

ognized by both customers and industry associations, and we

have been awarded a number of industry awards annually. We

have also accumulated a long list of “firsts” for our intervention

solutions within the industry and hold the majority of World

Records for the operations we perform, including deepest well

intervention, highest deviation well intervention, deepest wa-

ter depth intervention using RLWI, most footage tractored on

one trip to the well site, et al.

To maintain our leading position and further grow our business

we continue to focus on technological innovation. We often

work in conjunction with our clients on developing new ap-

plications and tools in order to solve specific needs of our cus-

tomers. This enables us to develop a deep understanding of

our customers’ business requirements and the challenges they

face while strengthening our relationships with them. We de-

vote considerable time and resources to development and engi-

neering, and are working on several projects to deliver the next

generation of tools and solutions.

Hand-in-hand with our dedicated efforts on technology inno-

vations, we vigorously protect our intellectual property. In 2013

alone, 144 patents were issued and we now have in the region

of 2,500 forecasted patents based on patent families at various

stages of registration or application. Welltec® operates a com-

prehensive program to protect critical intellectual property and

proprietary know-how, comprising the following internal pro-

tective barriers (the list is not exhaustive):

• Physical restrictions on access to and restrictions on record-

ing and photographic activities on Welltec® facilities;

• Application of various encrypting measures and the use of

either specially adapted or internally developed software

• Limited access to view, print and distribute technology blue-

prints and other sensitive documentation, with none, or

distorted, drawing specs on externally distributed drawings;

• Extensive IT-system log on access and security measures,

combined with limited off-site access and remote deletion

of sensitive information on lost IT-hardware;

• Extended use and tracking of non-disclosure agreements,

disclaimers and confidentiality agreements;

• Rigorous patenting of certain technology advances in rel-

evant countries and associated patent prosecution.

These measures are in place to avoid unintended dissemina-

tion of our trade secrets, know-how and sensitive information

in general.

We believe that our leading position will be maintained and

our business will grow as a consequence of our commitment

to quality in execution and customer service. In the oil and gas

service industry, technical reliability and overall service qual-

ity are paramount factors in customers’ purchasing decisions.

Through continuous evolution and improvement of work pro-

cesses, Welltec® offers superior service quality, as reflected in

the achievement of a 96% ratio of runs to misruns, which is

the generally accepted industry measure of service quality.

RISKS

Risks Related to Our Business

Business and industry related risks

While we believe our business to be relatively unaffected by

macro-economic factors, it is ultimately affected by the level of

expenditures of companies engaged in the production, explo-

ration and development of oil and gas.

Cyclical market

The oil and gas industry is cyclical and while demand for

Welltec’s services is primarily dependent on customer’s operat-

ing expenditures, demand for Welltec’s services also depends

somewhat on the capital expenditures of customers. A de-

crease in operating expenditures may have adverse effects on

Welltec’s revenue and profits in the shorter term, while a de-

crease in the capital expenditures may have adverse effects on

Welltec’s revenue and profits in the longer term.

Customers

Welltec’s clients are typically not required to make minimum

purchases under sales contracts and customers can typically

terminate contracts without cause and on short notice. Not-

withstanding our broad customer base, Welltec® have one cus-

tomer that accounted for more than 16% of our revenue, and

loss of the trading relationship with this customer would have

an adverse effect on our revenue and profits. As such, visibility

with respect to future revenues is limited and there can be no

assurance that a trading relationship with important customers

will continue.

20 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

Competitors

Welltec® competes with large multinational companies that can

offer integrated services which Welltec® cannot offer. Further,

Welltec are, to some extent, dependent on equipment provided

by our competitors and such competitors could restrict us from

accessing wells using their equipment. In general, competition

can result in pricing pressures, lower sales and reduced mar-

gins that could have an adverse effect on Welltec’s revenue and

profits.

Operational risks

Service quality

Welltec’s ability to provide a high quality product and service

provision is of importance in respect of securing repeat sales

with new and existing clients. Our service quality can be nega-

tively affected by an inability to attract, train and retain highly

skilled and qualified personnel to develop, manufacture and

operate our equipment, with an adverse effect on Welltec’s

revenue.

Supply chain

Welltec® may experience constraints, anomalies or interruptions

in our supply chain, restricting Welltec’s ability to provide the

service or product in alignment with the expectations of the

customers. Such constraints may be due to supply chain bottle-

necks, delays or disruptions in clearing goods from customs or

events restricting Welltec’s ability to procure, develop or manu-

facture new equipment or spare parts or maintain the existing

fleet, and such could negatively affect our results of operations.

Catastrophic events

Welltec’s business operations could be subject to various cat-

astrophic events, including blow outs, explosions, damage to

or loss of third party property, injury to personnel, reputational

damage and oil and hazardous substance spills into the envi-

ronment, both on and off shore. Such events could, if the im-

pact of such event is not covered by Welltec’s insurance or are

not subjected to Welltec’s contractual indemnification protec-

tion, have an adverse effect on Welltec’s revenue and profits.

Financial risks

Financial exposure

Due to Welltec’s foreign activities and credit facilities in foreign

currencies, its profit/loss, cash flows and equity are affected by

changes in exchange rates and interest rates for a number of

currencies.

Foreign exchange fluctuations

The reporting currency of the group is US Dollars and the func-

tional currency for most of the group’s subsidiaries is that of

the country in which the subsidiary is domiciled. The functional

currency of the Danish operation and operations in some other

countries is US dollars. This reflects the revenue and principal

source of financing. A significant proportion of the group’s rev-

enues, expenses and other liabilities are denominated in curren-

cies other than the US Dollar, in particular Norwegian Kroner,

Danish Kroner and Canadian Dollar. Fluctuations in the value of

other currencies as compared with the US Dollar could result in

translation losses or gains.

21 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

Taxes

Welltec® files income tax returns in multiple jurisdictions.

Welltec’s effective tax rate could be adversely affected by sev-

eral factors, including changes in the income taxed by or al-

located to the various jurisdictions with differing statutory tax

rates; changing tax laws, regulations and interpretations of

such tax laws in multiple jurisdictions; and the resolution of is-

sues arising from tax audits or examinations together with any

related interest or penalties. The determination of local tax li-

ability is always subject to review or examination by authori-

ties in operating jurisdictions. If a tax authority in any jurisdic-

tion reviews filed tax returns and based on filing proposes an

adjustment, including adjustments of transfer prices and terms

applied, such an adjustment could have a negative impact on

Welltec’s net profit.

Liquidity risk

Welltec’s ability to make payments on and to refinance our in-

debtedness and to fund planned capital expenditures and oth-

er strategic investments will depend on our ability to generate

cash in the future. This, to a certain extent, is subject to gen-

eral economic, financial, competitive, legislative, regulatory and

other factors that are beyond our control. Welltec® expects to

continue making capital investments in order to develop and

purchase additional equipment to expand our services, increase

our capacity and replace existing equipment. Such capital in-

vestments require cash that could otherwise be applied to oth-

er business needs. However, if Welltec® does not incur these

expenditures while our competitors make substantial invest-

ments, our market share may decline and our business may be

adversely affected.

Legal risks

Regulatory

Welltec® conducts business in multiple jurisdictions in a highly

regulated industry. As such, Welltec® is directly or indirectly,

subject to a variety of federal, provincial, state and local laws,

regulations and guidelines, in all such jurisdictions, including

laws and regulations relating to health and safety, the conduct

of operations including business ethics and trade compliance,

taxation, the protection of the environment and the manufac-

ture, management, transportation and disposal of certain ma-

terials used in operations. Accordingly, Welltec® could become

subject to liabilities relating to the violation of such regulations

in multiple jurisdictions, with an adverse effect on the profits.

Technology

Welltec® is a technology company, constantly challenging the

operational boundaries in the industry. However, third parties

may assert that our products, services, solutions and other in-

tellectual property may infringe, on their proprietary rights. Any

such potential future claims, regardless of merit, could result in

multi-jurisdictional litigation, which could result in substantial

expenses, causes significant delays and materially disrupt the

conduct of business and have an adverse effect on our financial

condition and results of operations.

CORPORATE GOVERNANCE

Welltec® aims to establish, maintain and operate a corporate

governance system that is compliant with best practice, rec-

ognized governance principles sufficient to satisfy the require-

ments of a public Danish company.

22 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

CORPORATE SOCIAL RESPONSIBILITY

The following statement of Corporate Social Responsibility

(CSR) pursuant to the Danish Financial Statements Act Section

99a is part of the Management’s Commentary in the Annual

Report 2013.

Corporate Social Responsibility Policy

Welltec® focuses its CSR efforts on areas and issues directly af-

fecting our business. We have outlined our responsibility in po-

lices developed to comply with the objectives of CSR and ap-

proved by the Board of Directors. These principles are reviewed

on a regular basis and updated against relevant codes of cor-

porate governance and international standards, including the

UN’s Universal Declaration of Human Rights, the ILO’s Declara-

tion on Fundamental Principles and Rights at Work, the OECD’s

Guidelines for Multinational Enterprises, the Rio Declaration

on Environment and Development, the UN Convention against

Corruption, as well as applicable legislation governing the in-

terest of our stakeholders.

In 2013 the Board has adopted a new code of conduct to sup-

port the CSR initiatives. The areas currently covered by CSR pol-

icies are: (i) Business Ethics, (ii) Anti-Corruption, (iii) Health and

Safety, (iv) Environment, (v) Employment, (vi) Customers, and

(vii) Community.

The responsibility of monitoring overall CSR compliance has

been delegated to the heads of Legal, Human Resources, QHSE

(Quality, Health, Safety, and Environment) and Commercial De-

partments. Key performance indicators are regularly monitored

and appropriate audits are performed and followed up.

The policies have been incorporated into our code of conduct

and continue to be communicated to all employees. It is acces-

sible on both our website and intranet. Moreover, a concert-

ed effort is made to ensure that these are deep rooted in our

thinking and our way of doing business.

Business Ethics

Policy

At Welltec® ‘we say what we do and we do what we say’.

This principle is the back bone of Welltec’s Code of Conduct

and promotes certainty in relation to all our stakeholders that

predictability and reliability are the norm when dealing with

Welltec®. It is our policy to comply with all governmental laws,

rules and regulations applicable to our business and we strive

to follow the course of action leading to the highest degree of

integrity in situations where the law may be permissive.

Implementation

Integrity and ethical conduct is a fundamental part of manage-

ment procedures and Welltec´s Code of Conduct and is an un-

derlying driver in all we do. The methods we employ to attain

results are as important as the results themselves.

Welltec® employees are expected to perform their work with

honesty, truthfulness and integrity, and conduct their business

affairs fairly. All employees are responsible for the immediate

and accurate reporting to higher management of work-relat-

ed information of importance to the governing guidelines. We

strongly encourage dialogue to make each other aware of situ-

ations that give rise to ethical questions and to articulate ac-

ceptable ways of handling those situations.

Key results in 2013 and future plans

Welltec® has performed appropriate internal investigations into

possible non-ethical behavior by employees following internal

controls or whistle-blowing. We have in continuation of the

investigative findings applied consequences towards the em-

ployees when relevant and further strengthened internal com-

munication in respect of compliance programs.

To improve our efforts to facilitate sound business ethics, we

applied in August 2012 for permission from the Danish author-

ities to establish a formalized whistle-blower program, which

we expected to launch in 2013. In January 2014 the Danish

authorities have issued permission to establish a formalized

whistle-blower program.

Anti-Corruption

Policy

Our conviction to uphold ethical standards in all our corporate

activities is a common mind-set of all our employees and we

strive to do business with customers and suppliers of sound

business character and reputation. We have strict guidelines

covering facilitation payments, bribery, entertainment and

gifts, and our screening processes provide full transparency to

mitigate the risk of corruption.

23 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

Implementation

Welltec® maintains a general Partner Screening Program appli-

cable for agents, representatives and joint venture partners in

territories where transparency and corruption are imminent is-

sues. This comprises a questionnaire combined with a review

process under which a potential partner is vetted for undue

relationships and channels of influence.

Furthermore, Welltec® operates a zero-tolerance policy towards

corruptive behavior of employees and representatives. Any indi-

cation implying corruption will immediately trigger an internal

investigation led by the Legal Department and supplemented

by the HR Department.

Key results in 2013 and future plans

One screening was performed in 2013 and the partnership is

still being considered.

We have strengthened our screening abilities by the application

of external screening partners and their databases.

We expect to initiate a new Anti-Bribery and Corruption pro-

gram and supplement the implementation with an employee

training program. We will continue to improve the screening

procedures, review processes and further incorporate addi-

tional FCPA (Foreign Corrupt Practices Act) based initiatives.

Furthermore, we continue to monitor the initiatives and guide-

lines issued by OECD (Organization for Economic Cooperation

and Development) and Transparency International to identify

policies and procedures that could improve our anti-corruption

measures.

Health, Safety and Environment (HSE)

Policy

Our paramount concern is the health and safety of our employ-

ees, customers and everyone else that comes into contact with

our activities. This concern reaches far beyond such measures

required under applicable law. Health and safety underpins all

our operations and we continuously monitor HSE performance

and work to identify improvement initiatives. All our employees

are aware that the safety of people and protection of the envi-

ronment is an absolute priority.

Implementation

HSE is an integral part of decision-making, processes and train-

ing. Comprehensive incident reporting systems are in place to

review and address:

• Any injury or near miss in relation to our activities. Perfor-

mance statistics are kept and analyzed to ensure adoption of

best practices protecting the health and safety of individuals.

• Any unintentional discharge into the environment of dam-

aging substances or near misses in relation to one of our

operations. These are carefully analyzed to ensure adoption

of best practices in order to protect the environment to the

benefit of us all.

Weekly corporate management meetings are opened with a re-

view on any health and safety issues which may have occurred.

All locations have an HSE Officer employed to lead the HSE ef-

fort, ensure compliance with Welltec’s policies and local legisla-

tion and conduct monthly meetings where all employees are

required to attend.

All new hires attend an HSE introduction program and we oper-

ate a Safety Card Observation Program (SCOP) to report on and

encourage safe working practices.

As part of Welltec’s commitment to manage climate change

SCOP CARD

DESCRIPTION OF OBSERVATION

DISCUSSION AND AGREED ACTION

FOLLOW-UP / REMARKS

Observer’s Name

Date (Month/year)

Country

Client

Job ID

Place

Unsafe observation Safe Near miss (CA only)

What (code )

Why (code )

Yes No

Follow-up required

All new hires

attend an HSE

introduction

program and we

operate a Safety

Card Observa-

tion Program

(SCOP) to report

on and encour-

age safe working

practices.

24 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

impacts, Welltec’s facilities are audited by the relevant Munici-

pality, Nature and Environment Auditor. At any local operation,

we ensure that respect for the environment is applied such

that sustainability and recycling is promoted and secured to

the greatest extent reasonably possible, while at the same time

closely monitoring consumption of chemicals, waste, electric-

ity, heat and water.

The corporate QHSE function performs internal HSE audits at

the headquarters and local bases worldwide in order to assess

the effectiveness of the internal QHSE Management System of

Welltec. The audits are the prime instrument for reviewing the

business interfaces internally between HQ and bases, and ex-

ternally with customers, and create specific action points for

the cycle of continuous improvement.

Key results in 2013 and future plans

Only five small environmental accidents occurred, where the

spill is less than 1kg, and four of them were fully recovered.

Respect for and preservation of the environment is a key ele-

ment of our business proposition.

Despite the growth in activity, Welltec® experienced no change

in the total number of Medical Treatments (MTO) and Restrict-

ed Work Case Frequency (RWC/RWCF), and only an incre-

mental increase in Lost Time Incidents (LTI), while Vehicle Ac-

cident Frequency (VA/VAF). This followed an increased focus on

strengthening the vehicle safety culture through training and

the implementation of processes designed to share knowledge

and analyze trends and root causes. There were no Fatalities

(FTL) in 2013 or previously

A worldwide survey of Safety Culture assessing the physical and

psychological work climate did not indicate any major issues,

and subsequent action plans have been drawn up to oversee

improvements in the physical workplace within each sector.

Quality is and has always been deeply ingrained in all processes

at Welltec®. Welltec® is ISO 9001 certified by Det Norske Veritas

(DNV) with periodic re-certification audits every 3 years.

Furthermore, oil operators, service partners and authorities

perform external audits to assess Welltec’s ability to effectively

manage the hazards associated with the services provided. In

2013, Welltec® Denmark was audited by DNV and local bas-

es were audited by Petrobras, BHP, BP, Chevron, and Statoil,

among others. None of these audits resulted in significant

remarks.

2009 2010 2011 2012 20130

2

4

6

8

10

MTO LTI RWC FTL

NUMBERS OF INCIDENTS

INCIDENTS FREQUENCY

2009 2010 2011 2012* 2013*0

1

2

3

4

5

Inci

dent

s pe

r 20

0,00

0 w

orki

ng

hour

s

MTOF LTIF RWCF TRCF

VEHICLE ACCIDENTS

0

5

10

15

20

25

2009 2010 2011 2012* 2013*0.0

0.2

0.4

0.6

0.8

1.0

VA p

r. 2

00.0

00 k

m

VA VAF

Employment

Policy

Welltec® believes that its employees, both as individuals and as

part of a team, are the most important assets of the business.

Hence, and with due consideration to the often challenging

working conditions in the field, applies measures which ‘go

beyond the norm’ to safeguard and maximize the health and

safety aspects of the employees performing their duties.

Welltec® recognizes a shared responsibility on behalf of all em-

ployees to exercise the human rights principles of mutual re-

spect and dignity in all working relationships and consequently

enforces a policy of zero tolerance with regard to harassment

or discrimination.

*All incidents from 2012-2013 have been re-evaluated to align with industry standards

25 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

In 2013, as a natural extension of previous practice, the board

of directors adopted a Diversity and Equal Opportunity Employ-

ment Policy. The policy formalizes our commitment to always

choosing the best person for the job regardless of that person’s

race, color, religion, disability, gender, sexual orientation, age or

nationality. Furthermore, Welltec® will actively work to increase

the share of females in management positions, for example, by

putting the needed extra effort into identifying relevant female

candidates when recruiting.

Implementation

Welltec® actively recruits employees from many sources, includ-

ing first-tier academic institutions as well as leading companies

in the industry, depending on the requirements of a given posi-

tion. A variety of objective profiling tools are used to help as-

sess the candidates. Furthermore, we actively encourage mobil-

ity and career progression within Welltec®.

Welltec® operates an extensive in-house training program cov-

ering core operational aspects as well as sales skills and pro-

grams aimed at legal compliance. Participation is registered

and tracked in the HR system, enabling on-going identification

of training needs and supporting work-force planning.

For long-term ill employees, we work closely and actively with

local authorities and community centres in order to define indi-

vidual solutions, including definition of flex jobs (permanently

reduced work time), temporarily reduced work time, redefini-

tion of work area, etc.

Our workforce

The employee population is very diverse with respect to na-

tionalities, reflecting the truly global nature of the company. As

such there are around 50 nationalities employed in Welltec®.

As is common in the oil industry, the share of females is low in

Welltec®. Women make up 12% of the total employee popu-

lation and 8% of management level employees. There are no

women on the Board of Directors.

Key results in 2013 and future plans

During the year, more than 200 employees have received in-

ternal training in the areas of Field Engineer courses, special

equipment courses, Project Management courses, sales train-

ing etc.

2013 has seen the launch of several new initiatives on the HR

front. A standardized on boarding program has been launched

for all staff worldwide. A single HR system has been imple-

mented globally. As intended, this enables greater consistency

in data, workforce transparency and supports the continued

implementation of uniform and streamlined processes. Further,

Employee Self Service was launched in late 2013.

All five employees that have been long-term ill during 2013

have benefitted from the individual solutions Welltec® provides.

12 % vs. 88 % of all employees

50NATIONALITIES

EMPLOYED

26 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013

Welltec® will continue to improve in the area of employment.

Plans for 2014 include implementing a standardized approach

to performance management worldwide and increasing trans-

parency to employee competencies beyond those captured

today.

In 2013 Welltec® saw one incident in violation of the Diversity

and Equal Employment Opportunity Policy. The matter was in-

vestigated and appropriate disciplinary actions and reinforce-

ment of policy were applied.

Also during 2013 Welltec® initiated the Welltec Fellowship

which enables the retention of senior employees at or beyond

age of retirement, which have recognized industry experience

for internal and external training, coaching and marketing in

Welltec´s interests.

Welltec® will also continue to evaluate ways to increase the

share of females in management and expect to report on the

results of this following 2014. Furthermore, the board of direc-

tors has set the goal of having at least one female member of

the board of directors by April 1, 2017.

Customers

Policy

Welltec® views customers as business partners and pursues an

open and transparent relationship characterized by frequent

dialogue and a focus on serving their best interests.

It is our policy to provide solutions that excel in quality, con-

form to industry best practice and adhere to responsible

standards of performance, including taking due care and

consideration to protection of the environment and the health

and safety of all people involved.

We operate an open door policy in situations where a custom-

er or regulatory body wishes to investigate a non-successful

operation or an issue of regulatory non-compliance. All non-

optimal or non-compliant findings from the internal Welltec®

investigation are openly disclosed to achieve maximum trans-

parency and optimal lessons learned.

0

1,000

2,000

3,000

4,000

5,000

6,000

2011 2012 2013

Run Count Misrun - Welltec

SERVICE QUALITY

SERVICE QUALITY

90%

92%

94%

96%

98%

100%

2011 2012 2013

27 MANAGEMENT COMMENTARY / WELLTEC® ANNUAL REPORT 2013

Implementation

In such situations, a failure investigation is initiated to ensure:

• that investigations requested by the clients are performed;

• that conformed and controlled methods are followed when

handling misruns, covering from job planning, equipment,

procedures, communication to human factors;

• lessons learned are properly communicated throughout the

organization in order to minimize the risk of re-occurrence;

• A failure report is prepared on a timely manner for the cli-

ent, prior to officially closing the investigation.

Key results in 2013 and future plans

The overall numbers of customer-requested quality investiga-

tions increased in 2013, with Welltec’s corporate QHSE depart-

ment increasingly involved to ensure the highest standards are

applied to match heightened expectations from customers as

the scope and complexity of services increase.

A global training program, as part of the Welltec® Academy,

serves to increase expertise in the use of our operational plan-

ning software to ensure continuous improvement of service

quality on jobs performed. The program underlines the con-

stant focus on maintaining the very highest levels of service

quality and is reflected in the continued service quality delivery

above 95% as compared to a 39% increase in run count with

the growth in activity.

Service Quality (SQ) is derived from the total number of con-

ducted runs as compared to misruns, and defined as:

SQ = (total number of runs – total number of misruns) / total

number of runs.

Welltec® will continue its efforts to minimize the risk of non-

successful operations by communicating lessons learned

throughout the organization and with the customer or regula-

tory body.

The dedication to meeting client objectives and focus on driv-

ing dialogue continues to lead to an increase in the number of

regular customer meetings, with a 25% rise in 2013.

Community

Policy

At Welltec®, we inherently share a responsibility that reaches

beyond our immediate business and has an impact on the in-

terests of all our stakeholders. These encompass not only our

shareholders but also our customers, employees, suppliers,

the local communities in which we operate, as well as the sur-

rounding environment and the human beings occupying it.

Improving the environment in and around our operations is

an integral part of our business. We operate from a significant

number of properties in a variety of countries, and we have re-

sponsibility to our employees, to the people living and working

nearby as well as the environment. It is our policy therefore to

engage with the local community as both a neighbor and resi-

dent and support efforts to improve the local area, for example

by addressing antisocial behavior, crime and vandalism as well

as promoting road safety.

Implementation and future plans

We will actively promote engagement between our staff and

the community, supporting local community-based projects

and charities, including fund-raising and initiatives for the de-

velopment and education of young people in the areas where

we operate.

28 / MANAGEMENT COMMENTARYWELLTEC® ANNUAL REPORT 2013