#malg14 keynote address - zach lewy, arrow global - slideset

TRANSCRIPT

Confidentiality notice: This document is confidential and contains proprietary information and intellectual property of Arrow Global Limited. None of the information contained herein may be reproduced or disclosed under any circumstances without the express written permission of Arrow Global Limited.

“TICKING THE BOX ON PROBLEM DEBT – SO JOB DONE THEN?”

Zach Lewy, Founder and Executive Director, Arrow Global 19 November 2014

Proprietary and C

onfidential 2

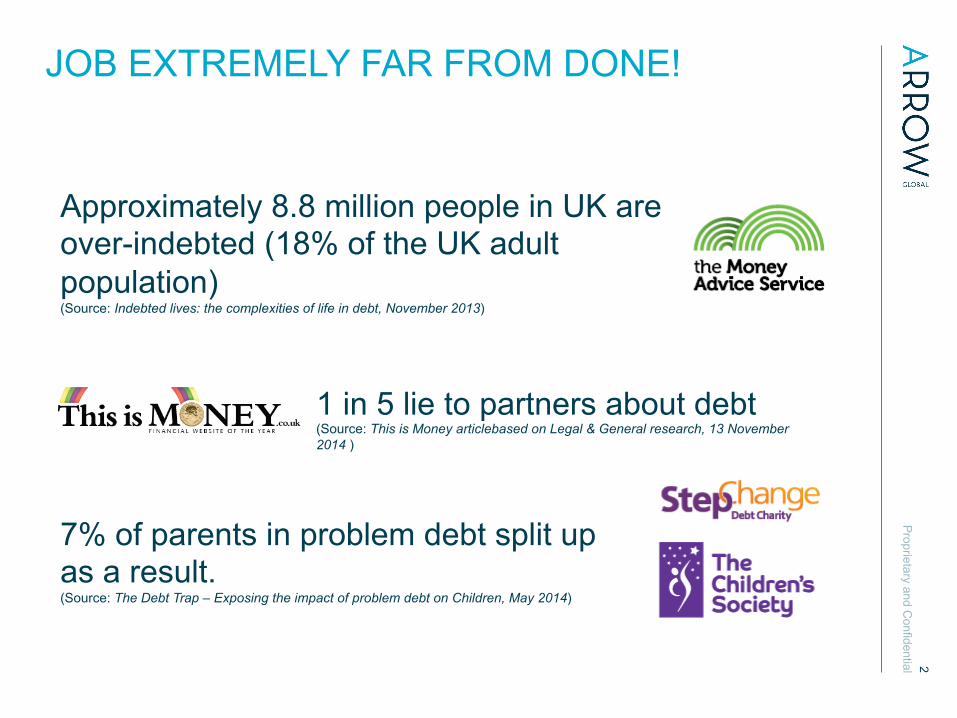

JOB EXTREMELY FAR FROM DONE!

Approximately 8.8 million people in UK are over-indebted (18% of the UK adult population) (Source: Indebted lives: the complexities of life in debt, November 2013)

1 in 5 lie to partners about debt (Source: This is Money articlebased on Legal & General research, 13 November 2014 )

7% of parents in problem debt split up as a result. (Source: The Debt Trap – Exposing the impact of problem debt on Children, May 2014)

Proprietary and C

onfidential

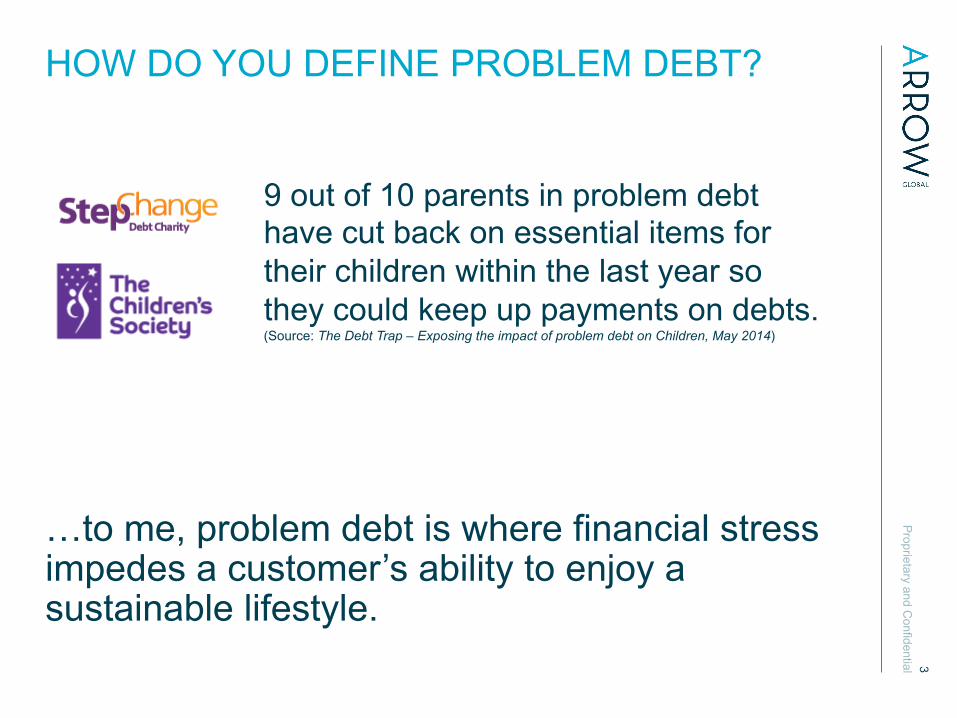

…to me, problem debt is where financial stress impedes a customer’s ability to enjoy a sustainable lifestyle.

3

HOW DO YOU DEFINE PROBLEM DEBT?

9 out of 10 parents in problem debt have cut back on essential items for their children within the last year so they could keep up payments on debts. (Source: The Debt Trap – Exposing the impact of problem debt on Children, May 2014)

Proprietary and C

onfidential 4

UNDERSTANDING THE PROBLEM

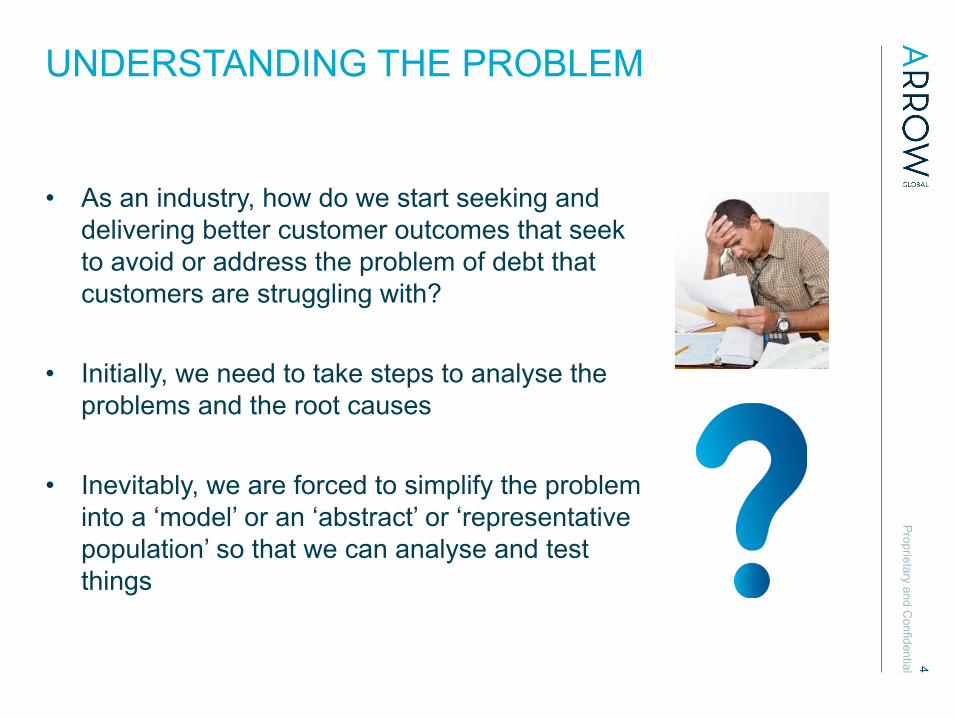

• As an industry, how do we start seeking and delivering better customer outcomes that seek to avoid or address the problem of debt that customers are struggling with?

• Initially, we need to take steps to analyse the problems and the root causes

• Inevitably, we are forced to simplify the problem into a ‘model’ or an ‘abstract’ or ‘representative population’ so that we can analyse and test things

Proprietary and C

onfidential 5

ENSURING THE BEST CUSTOMER OUTCOME

vs. Actuarial Optimisation

Behavioural Economic

• Do the paradigms we use to understand customers have significant flaws?

• The rational actor hypothesis defined as being actuarially optimal is very risky

• In the ‘real world’ customer behaviours and motivations deviate materially from actuarial optimal positions

• Situational factors also bias customer choice far away from the actuarial optimal

• Actuarial optimisation is convenient to model but can lead to inferior customer outcomes if misapplied to different real world conditions

Proprietary and C

onfidential 6

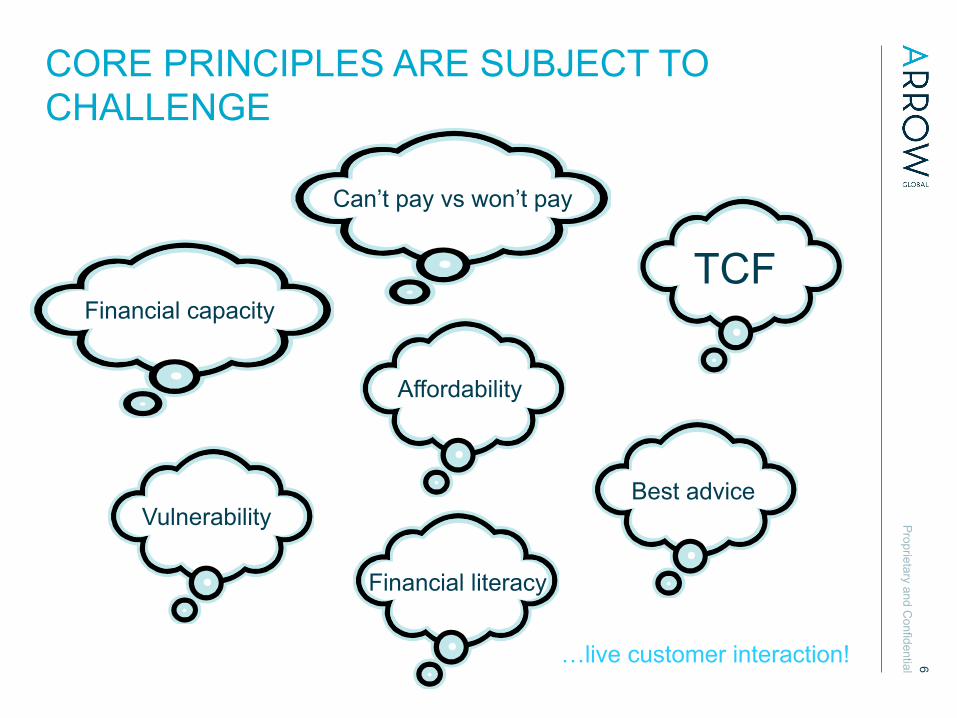

CORE PRINCIPLES ARE SUBJECT TO CHALLENGE

Financial literacy

Financial capacity

Can’t pay vs won’t pay

Affordability

TCF

Best advice Vulnerability

…live customer interaction!

Proprietary and C

onfidential 7

AN EXAMPLE

‘Shawn’

Late with bills

Bounced cheque

Overdraft charges

Collection calls Avoiding paying fair share with friends

Guilty purchase

Skimping on daughter’s birthday gift

Proprietary and C

onfidential 8

CIRCUMSTANCES ARE ENOUGH TO ADVERSELY AFFECT CAPACITY

• Imagine Shawn’s car has some trouble, which requires a £300 service

• Shawn’s auto insurance will cover half the cost • Shawn needs to decide whether to go ahead and get his car

fixed, or take a chance and hope that it lasts for a while longer

Proprietary and C

onfidential

• Imagine that your car has some trouble, which requires an expensive £3,000 service

• Your auto insurance will cover half the cost. You need to decide whether to go ahead and get the car fixed, or take a chance and hope that it lasts for a while longer

• Customer solves problem by terminating insurance that he benefited from. This improves his affordability and liquidity in the short term but reduces shock buffers to many future challenges including problem debts • If this were not the actuarially correct answer, who bears

responsibility and obligation for such circumstances? • This problem is compounded if customers suffer reduced

capacities due to problem debt conditions 9

CIRCUMSTANCES ARE ENOUGH TO ADVERSELY AFFECT CAPACITY

Proprietary and C

onfidential 10

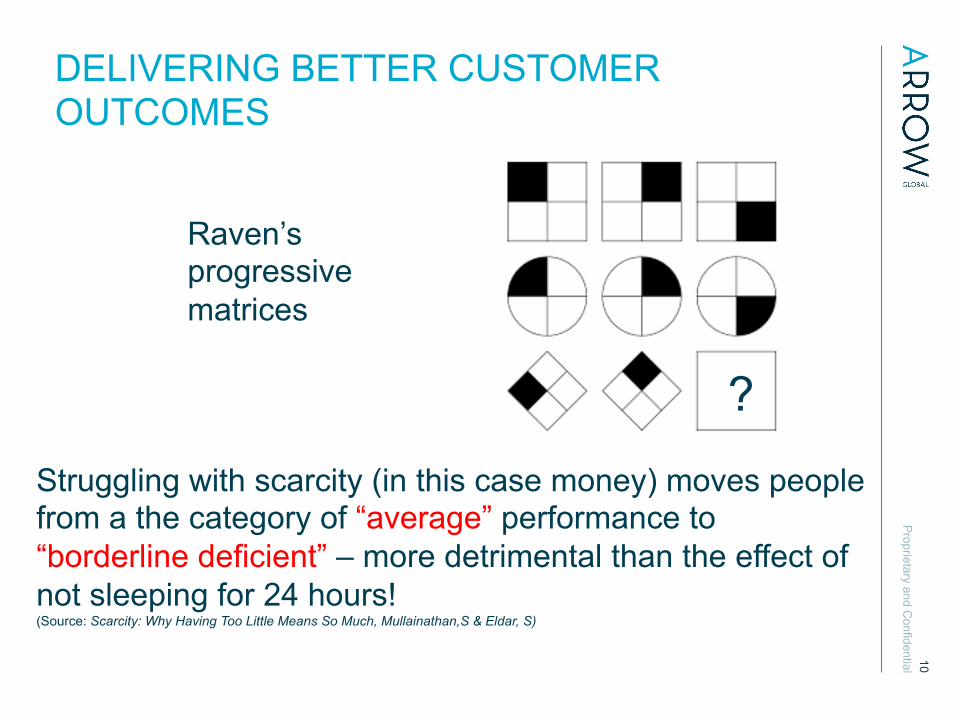

DELIVERING BETTER CUSTOMER OUTCOMES

?

Raven’s progressive matrices

Struggling with scarcity (in this case money) moves people from a the category of “average” performance to “borderline deficient” – more detrimental than the effect of not sleeping for 24 hours! (Source: Scarcity: Why Having Too Little Means So Much, Mullainathan,S & Eldar, S)

Proprietary and C

onfidential 11

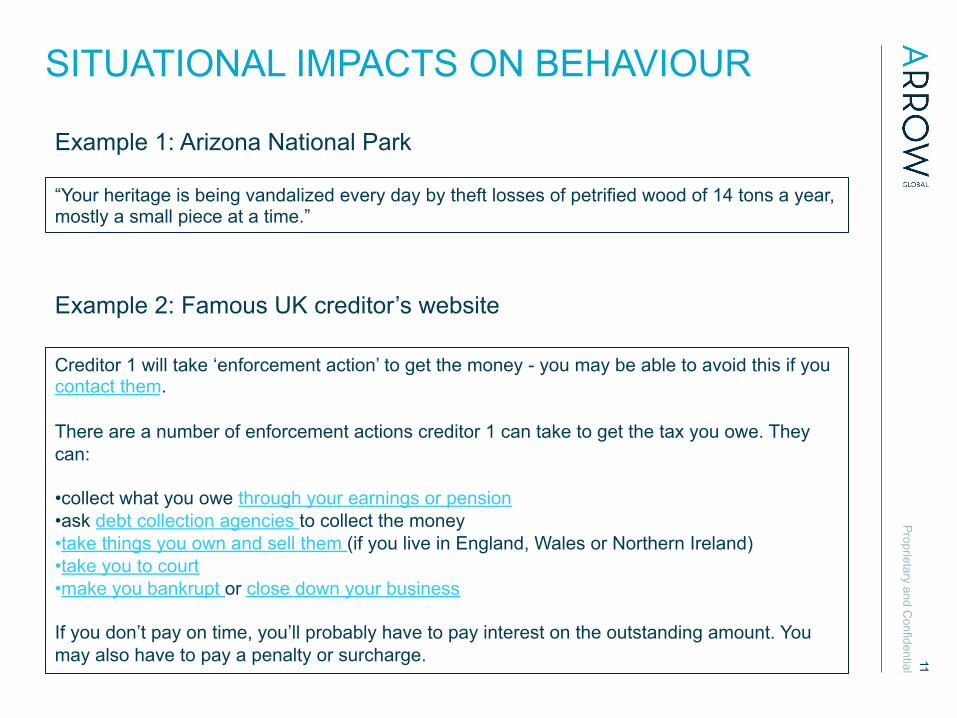

SITUATIONAL IMPACTS ON BEHAVIOUR

“Your heritage is being vandalized every day by theft losses of petrified wood of 14 tons a year, mostly a small piece at a time.”

Example 1: Arizona National Park

Example 2: Famous UK creditor’s website

Creditor 1 will take ‘enforcement action’ to get the money - you may be able to avoid this if you contact them. There are a number of enforcement actions creditor 1 can take to get the tax you owe. They can: • collect what you owe through your earnings or pension • ask debt collection agencies to collect the money • take things you own and sell them (if you live in England, Wales or Northern Ireland) • take you to court • make you bankrupt or close down your business

If you don’t pay on time, you’ll probably have to pay interest on the outstanding amount. You may also have to pay a penalty or surcharge.

Proprietary and C

onfidential 12

RELEVANT ALTERNATIVE APPROACH EXAMPLES

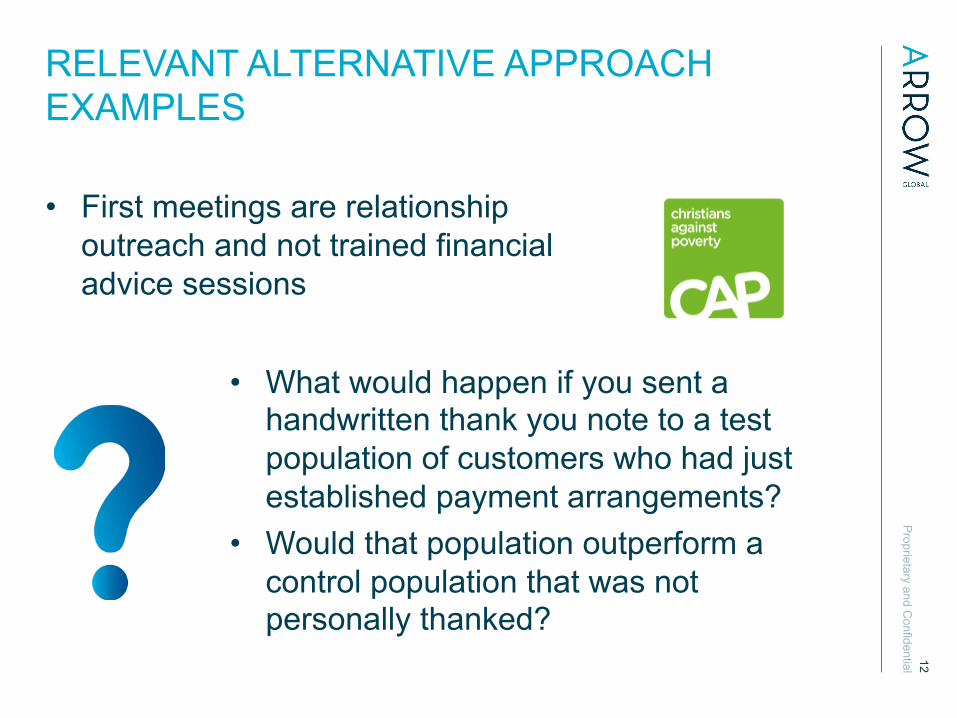

• First meetings are relationship outreach and not trained financial advice sessions

• What would happen if you sent a handwritten thank you note to a test population of customers who had just established payment arrangements?

• Would that population outperform a control population that was not personally thanked?

Proprietary and C

onfidential 13

DO WE APPROACH KEY ISSUES IN THE RIGHT WAY? • Is an I&E the right place to start? Do we need to start on a more

personal relationship level? • What is the interplay between customer confidence and positive

customer outcomes – particularly in the long term? • What is the impact on creditor business models from customers

who ‘fully’ recover versus those who ‘limp along’? How does that improvement impact compare to the path dependent negative cycles that certain creditor and advisor behaviour creates?

• How many customers don’t seek financial advice because the market makes it emotionally hard to access?

• How many unhelpful social behaviours do we create or perpetuate by applying the incorrect can’t pay / won’t pay paradigm

• How do we best help problem debt customers?

Proprietary and C

onfidential 14

WHOSE PROBLEM IS IT?

Problem debt costs society £8.3 billion. (Source: StepChange )

Pay growth outstrips inflation for first time in five years (Source: Telegraph article based on data from Office for National Statistics, 12 November 2014)

Families in the red ‘pose threat the UK recovery’ as household debt more than quadruples since 1990 (Source: This is Money article based on information from financial research firm Verum, 14 August 2014)