madness of crowds: market-place dynamics - …€¦ · félix yamasato looks at how bunker players...

TRANSCRIPT

INDEPENDENT INTELLIGENCE FOR THE GLOBAL BUNKER INDUSTRYwww.bunkerspot.com Volume 9 Number 3 June / July 2012

Inside:• Credit Management• Bunker Blending• Barge Market• Mediterranean Focus• News and Events

MADNESS OF CROWDS:Market-place dynamics

bunkerspot June / July 2012 www.bunkerspot.com 3

Contents

FEATURES

COMMERCIAL ISSUESChris Thorpe looks at how crowd-mentality can confuse the markets 24Félix Yamasato looks at how bunker players can avoid financial pitfalls by taking a closer look at customers’ cash flows 26

BARGE MARKETSJon Thielemann of Marcon International gives a broker’s view of the tank barge market 28

BUNKER BLENDINGJon Moreau of Cameron Jiskoot argues that in-line blending can be the key to successful bunkering 30

FUEL ADDITIVESRalph E. Lewis of Power Research Inc. argues that improving ships’ engine efficiency and cutting emissions makes sound business sense 32

EXHAUST EMISSIONS MONITORINGAlbert Leyson of Drew Marine looks at new developments in the field of exhaust emission monitoring 38

SHIP SUPPLY SERVICESRobert Steen Kledal of Wrist Ship Supply looks at how a progressive approach to ship supplying can boost operational efficiencies 42

REGIONAL FOCUS: MEDITERRANEANNikos Marmatsouris of GAC looks at the changing dynamics of the Mediterranean shipping market 44

REGIONAL FOCUS: AFRICAHammama Sait of Total Marine Fuels outlines the company’s strategy for growing its business in Africa 47

ENERGY SECURITY‘Market sentiment’ over the situation in Iraq always appears to be one of the key factors influencing oil, and therefore bunker, prices. John Drake looks at the practicalities of doing business in Iraq 48

DATA RECOVERYPaul Johnston from Seadebt explains how a long-standing bunker claim was pursued across several jurisdictions 51

MARINE LUBRICANTSAs OW Bunker launches its new global Marine Lubricants Unit, Stathis Grafakos discusses how a combined bunker and lubricant supply service can help shipowners and operators maximise operational efficiencies and reduce supply chain costs 52

MARITIME BOOKSLlewellyn Bankes-Hughes looks at three of the latest maritime books published by Petrospot 54

EVENTSEvents and training course diary 56

NETWORKINGBunker people on the move 58

HEAD OFFICEPetrospot Limited · Petrospot House Somerville Court ·Trinity Way ·Adderbury Oxfordshire OX17 3SN · England +44 1295 81 44 55 +44 1295 81 44 66 [email protected] www.cargosecurityinternational.com

DIRECTOR - PUBLISHING / EDITORIan Taylor +44 7876 70 45 41 [email protected]

MANAGING DIRECTOR / PUBLISHERLlewellyn Bankes-Hughes +44 7768 57 44 30 [email protected]

ASSOCIATE EDITORLesley Bankes-Hughes +44 7815 57 86 43 [email protected]

ADVERTISING SALES MANAGERSteve Simpson +44 7800 75 52 78 [email protected]

MAGAZINE LAYOUT & PRODUCTIONCheryl Marshall +44 7725 58 67 01 [email protected]

PUBLISHING ASSISTANTBradley Fowler [email protected]

DIRECTOR - EVENTSLuci Llewellyn-Jones +44 7775 92 42 24 [email protected]

EVENTS MANAGERStacey Smith [email protected]

EVENTS COORDINATOREsther Ramos [email protected]

EVENTS & MARKETING ASSISTANTHannah Whitty [email protected]

MARKETING MANAGERMelody Aguero [email protected]

SALES MANAGERLouise McKee +44 7951 70 31 03 [email protected]

EVENTS & SALES Osei Mitchell +44 7789 20 20 10 [email protected] Leader +44 7771 54 03 82 [email protected] Matthew Conisbee +44 7500 68 88 70 [email protected] Ocampo [email protected]

ACCOUNTSHelen Wilkins [email protected]

NORTH AMERICA REPRESENTATIVEJackie Hoo Bryant (Miami, United States) +1 305 456 1838 +1 786 302 7667 [email protected]

AFRICA REPRESENTATIVEMaria Tierney (Cape Town, South Africa) +27 22 448 1726 +27 72 804 9569 [email protected]

NEWS Bunker Overview 4Europe 8Americas 14Asia Pacific 18Africa and Mideast 22

Bunkerspot is an integrated news and intelligence service for the international bunker industry. The bi-monthly magazine and 24/7 electronic news service, www.bunkerspot.com, both provide highly-specific information on all aspects of the marine fuels industry. Bunkerspot Magazine (published in February, April, June, August, October and December) annual subscription rate, including unlimited

access to the website www.bunkerspot.com, is UK£250/€280/US$400. ISSN 1741-6981. Copyright Petrospot Limited © 2012. All rights reserved. Published by Petrospot Limited, a dynamic independent publishing, training and events organisation, focused on providing information resources for the transportation, energy and maritime industries. Disclaimer: Bunkerspot is an editorially independent magazine and electronic news information service. The information contained in the magazine and website is presented in good faith. Opinions expressed are not necessarily those of Petrospot Limited, which does not guarantee the accuracy of the information contained in Bunkerspot. Nor does Petrospot accept responsibility for errors or omissions or their consequences. No part of Bunkerspot may be reproduced, stored in a retrieval system or transmitted in any form or by any means electronic, mechanical, photographic, recorded or otherwise, without the prior written permission of the publisher. Visit www.petrospot.com

June / July 2012 bunkerspotwww.bunkerspot.com4

Bunker Overview

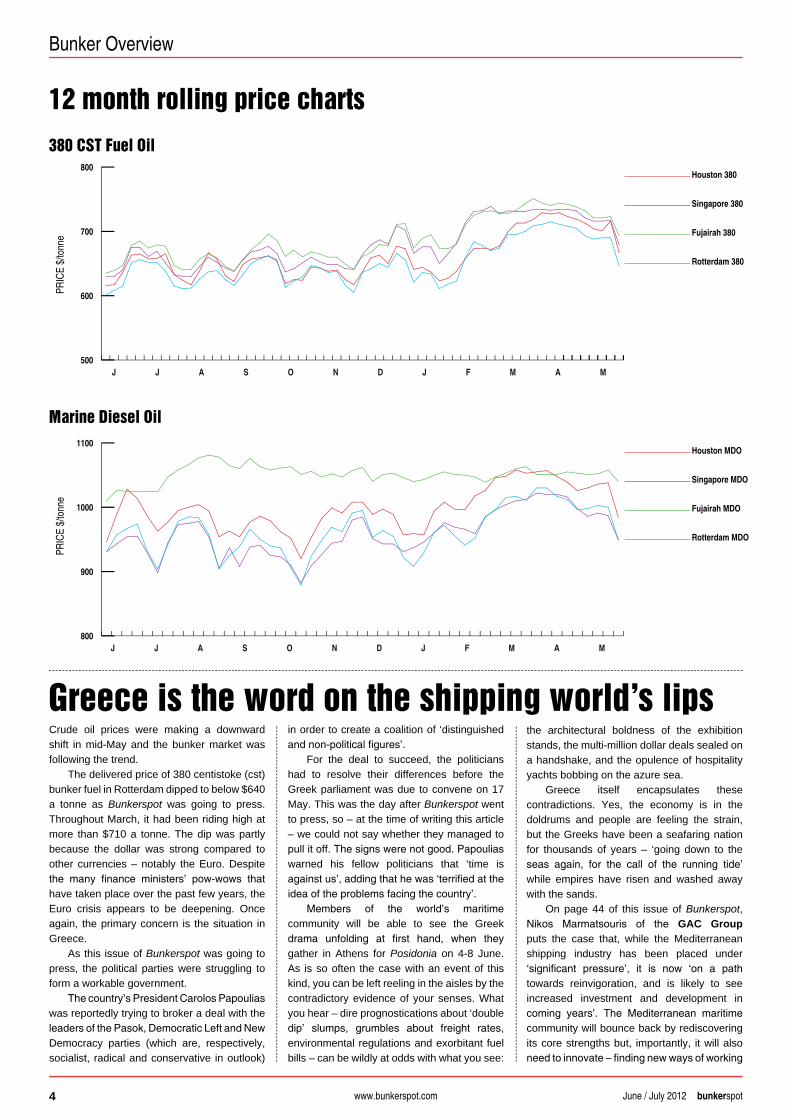

Greece is the word on the shipping world’s lipsCrude oil prices were making a downward shift in mid-May and the bunker market was following the trend.

The delivered price of 380 centistoke (cst) bunker fuel in Rotterdam dipped to below $640 a tonne as Bunkerspot was going to press. Throughout March, it had been riding high at more than $710 a tonne. The dip was partly because the dollar was strong compared to other currencies – notably the Euro. Despite the many finance ministers’ pow-wows that have taken place over the past few years, the Euro crisis appears to be deepening. Once again, the primary concern is the situation in Greece.

As this issue of Bunkerspot was going to press, the political parties were struggling to form a workable government.

The country’s President Carolos Papoulias was reportedly trying to broker a deal with the leaders of the Pasok, Democratic Left and New Democracy parties (which are, respectively, socialist, radical and conservative in outlook)

12 month rolling price charts

in order to create a coalition of ‘distinguished and non-political figures’.

For the deal to succeed, the politicians had to resolve their differences before the Greek parliament was due to convene on 17 May. This was the day after Bunkerspot went to press, so – at the time of writing this article – we could not say whether they managed to pull it off. The signs were not good. Papoulias warned his fellow politicians that ‘time is against us’, adding that he was ‘terrified at the idea of the problems facing the country’.

Members of the world’s maritime community will be able to see the Greek drama unfolding at first hand, when they gather in Athens for Posidonia on 4-8 June. As is so often the case with an event of this kind, you can be left reeling in the aisles by the contradictory evidence of your senses. What you hear – dire prognostications about ‘double dip’ slumps, grumbles about freight rates, environmental regulations and exorbitant fuel bills – can be wildly at odds with what you see:

the architectural boldness of the exhibition stands, the multi-million dollar deals sealed on a handshake, and the opulence of hospitality yachts bobbing on the azure sea.

Greece itself encapsulates these contradictions. Yes, the economy is in the doldrums and people are feeling the strain, but the Greeks have been a seafaring nation for thousands of years – ‘going down to the seas again, for the call of the running tide’ while empires have risen and washed away with the sands.

On page 44 of this issue of Bunkerspot, Nikos Marmatsouris of the GAC Group puts the case that, while the Mediterranean shipping industry has been placed under ‘significant pressure’, it is now ‘on a path towards reinvigoration, and is likely to see increased investment and development in coming years’. The Mediterranean maritime community will bounce back by rediscovering its core strengths but, importantly, it will also need to innovate – finding new ways of working

Marine Diesel Oil

PRIC

E $/

tonn

e

380 CST Fuel Oil

PRIC

E $/

tonn

e

800

900

1000

1100Houston MDO

Singapore MDO

Fujairah MDO

Rotterdam MDO

J J A S O N D J F M A M

500

600

700

800Houston 380

Singapore 380

Fujairah 380

Rotterdam 380

J J A S O N D J F M A M

800

900

1000

1100Houston MDO

Singapore MDO

Fujairah MDO

Rotterdam MDO

J J A S O N D J F M A M

500

600

700

800Houston 380

Singapore 380

Fujairah 380

Rotterdam 380

J J A S O N D J F M A M

June / July 2012 bunkerspotwww.bunkerspot.com6

Bunker Overview

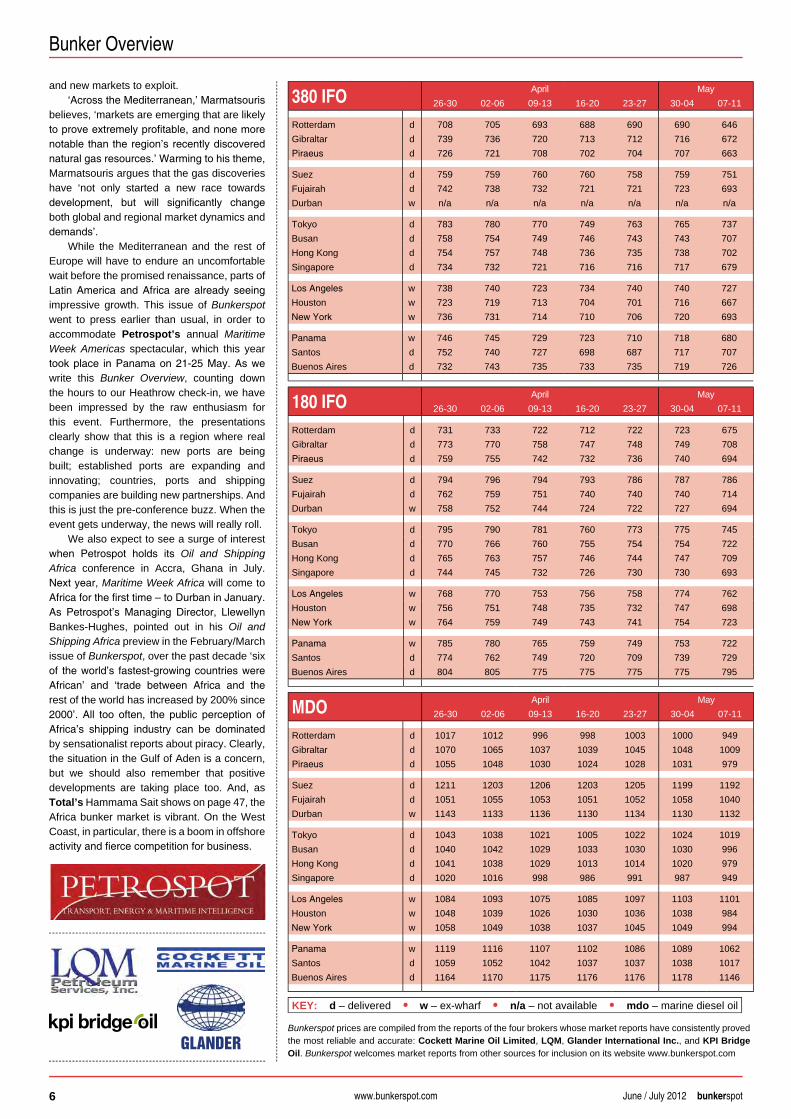

380 IFO April May26-30 02-06 09-13 16-20 23-27 30-04 07-11

Rotterdam d 708 705 693 688 690 690 646Gibraltar d 739 736 720 713 712 716 672Piraeus d 726 721 708 702 704 707 663

Suez d 759 759 760 760 758 759 751Fujairah d 742 738 732 721 721 723 693Durban w n/a n/a n/a n/a n/a n/a n/a

Tokyo d 783 780 770 749 763 765 737Busan d 758 754 749 746 743 743 707Hong Kong d 754 757 748 736 735 738 702Singapore d 734 732 721 716 716 717 679

Los Angeles w 738 740 723 734 740 740 727Houston w 723 719 713 704 701 716 667New York w 736 731 714 710 706 720 693

Panama w 746 745 729 723 710 718 680Santos d 752 740 727 698 687 717 707Buenos Aires d 732 743 735 733 735 719 726

180 IFO April May26-30 02-06 09-13 16-20 23-27 30-04 07-11

Rotterdam d 731 733 722 712 722 723 675Gibraltar d 773 770 758 747 748 749 708Piraeus d 759 755 742 732 736 740 694

Suez d 794 796 794 793 786 787 786Fujairah d 762 759 751 740 740 740 714Durban w 758 752 744 724 722 727 694

Tokyo d 795 790 781 760 773 775 745Busan d 770 766 760 755 754 754 722Hong Kong d 765 763 757 746 744 747 709Singapore d 744 745 732 726 730 730 693

Los Angeles w 768 770 753 756 758 774 762Houston w 756 751 748 735 732 747 698New York w 764 759 749 743 741 754 723

Panama w 785 780 765 759 749 753 722Santos d 774 762 749 720 709 739 729Buenos Aires d 804 805 775 775 775 775 795

MDO April May26-30 02-06 09-13 16-20 23-27 30-04 07-11

Rotterdam d 1017 1012 996 998 1003 1000 949Gibraltar d 1070 1065 1037 1039 1045 1048 1009Piraeus d 1055 1048 1030 1024 1028 1031 979

Suez d 1211 1203 1206 1203 1205 1199 1192Fujairah d 1051 1055 1053 1051 1052 1058 1040Durban w 1143 1133 1136 1130 1134 1130 1132

Tokyo d 1043 1038 1021 1005 1022 1024 1019Busan d 1040 1042 1029 1033 1030 1030 996Hong Kong d 1041 1038 1029 1013 1014 1020 979Singapore d 1020 1016 998 986 991 987 949

Los Angeles w 1084 1093 1075 1085 1097 1103 1101Houston w 1048 1039 1026 1030 1036 1038 984New York w 1058 1049 1038 1037 1045 1049 994

Panama w 1119 1116 1107 1102 1086 1089 1062Santos d 1059 1052 1042 1037 1037 1038 1017Buenos Aires d 1164 1170 1175 1176 1176 1178 1146

KEY: d – delivered • w – ex-wharf • n/a – not available • mdo – marine diesel oil

GLANDER

and new markets to exploit. ‘Across the Mediterranean,’ Marmatsouris

believes, ‘markets are emerging that are likely to prove extremely profitable, and none more notable than the region’s recently discovered natural gas resources.’ Warming to his theme, Marmatsouris argues that the gas discoveries have ‘not only started a new race towards development, but will significantly change both global and regional market dynamics and demands’.

While the Mediterranean and the rest of Europe will have to endure an uncomfortable wait before the promised renaissance, parts of Latin America and Africa are already seeing impressive growth. This issue of Bunkerspot went to press earlier than usual, in order to accommodate Petrospot’s annual Maritime Week Americas spectacular, which this year took place in Panama on 21-25 May. As we write this Bunker Overview, counting down the hours to our Heathrow check-in, we have been impressed by the raw enthusiasm for this event. Furthermore, the presentations clearly show that this is a region where real change is underway: new ports are being built; established ports are expanding and innovating; countries, ports and shipping companies are building new partnerships. And this is just the pre-conference buzz. When the event gets underway, the news will really roll.

We also expect to see a surge of interest when Petrospot holds its Oil and Shipping Africa conference in Accra, Ghana in July. Next year, Maritime Week Africa will come to Africa for the first time – to Durban in January. As Petrospot’s Managing Director, Llewellyn Bankes-Hughes, pointed out in his Oil and Shipping Africa preview in the February/March issue of Bunkerspot, over the past decade ‘six of the world’s fastest-growing countries were African’ and ‘trade between Africa and the rest of the world has increased by 200% since 2000’. All too often, the public perception of Africa’s shipping industry can be dominated by sensationalist reports about piracy. Clearly, the situation in the Gulf of Aden is a concern, but we should also remember that positive developments are taking place too. And, as Total’s Hammama Sait shows on page 47, the Africa bunker market is vibrant. On the West Coast, in particular, there is a boom in offshore activity and fierce competition for business.

Bunkerspot prices are compiled from the reports of the four brokers whose market reports have consistently proved the most reliable and accurate: Cockett Marine Oil Limited, LQM, Glander International Inc., and KPI Bridge Oil. Bunkerspot welcomes market reports from other sources for inclusion on its website www.bunkerspot.com

June / July 2012 bunkerspotwww.bunkerspot.com24

‘An insurance company will cover hurricane or

accidental fire damage, but will not sell a policy that pays if the price of crude

goes over $200 per barrel’

‘Almost certainly, the madness of crowds will take the price of oil and refined fuels to levels beyond reason again and again’

If you have not already entered the world of e-books, I recommend doing so for one simple reason:

classics can be downloaded for free. And your first download may be the 1841 classic Extraordinary Popular Delusions and the Madness of Crowds authored by Charles Mackay. His examples have been used time and again to explain economic history to students and investors alike. But his book is particularly useful in the study of commodities with respect to investor behaviour. The most famous case is arguably the great Tulip Mania of 1624 when tulip bulb prices traded higher than the price of gold. Fast forward to the 21st century and we find fresh cases filling the textbooks comparing manias ranging from the internet to real estate. When approaching oil as a commodity, fuel experts should beware the madness of crowds and how their behaviour may have significant impact on market prices.

When asked where we think oil prices are going, the simple – albeit frustrated – response for an industry expert is ‘I have no idea’. In a statistical game of large numbers, the best guess is 50-50 either higher or lower. This is not to say that overheated markets ought to cool off. But from day to day, hour by hour, the chances of a move higher or lower are 50-50. Nobody likes this reality but statisticians are happy to point out the game is all in the numbers and not the market pundits’ latest prognostications. The market is filled with information that inf luences expectations of the next move. And of course there are a number of reasons why market prices can appear irrational yet explainable. It is also fair and logical to dissect theories and make predictions as long as it done with the mind that popular opinion skews the outcome again and again. When human behaviour is tested in the markets, we often notice that logic takes second seat to gut-feeling. This is the main reason why insurance companies refuse to offer policies that cover markets that can be affected by human decision. For example, an insurance company will cover hurricane or accidental fire damage, but will not sell a policy that pays if the price of crude goes over $200 per barrel. They simply have no way to judge market behaviour, but they can believe their statistical models that predict hurricanes and the average occurrence of a fire.

Commercial Issues

Chris Thorpe looks at how crowd-mentality can

confuse the markets

Long term parkingIn an opposite fashion, modern investment portfolio theory uses the statistical argument to include more commodities in their strategy as they aim to increase returns through diversified risk. Research suggests that commodities as an asset class enable portfolio managers to achieve more diversification and lower volatility of investment returns on a risk adjusted basis. As investment portfolio managers continue to embrace this research, the amount of passive money in commodities will continue to increase. From an investment trend perspective, commodities have become a proxy bet on the growth of China and other emerging markets which are highly dependent on fuel for economic output. When investors and portfolio managers attempt to diversify they look no farther than investment products such as the Standard & Poors (S&P) GCSI (formerly the Goldman Sachs Commodity Index) that has a composition of approximately 70% in energies. These are not hedge funds that take positions on both the long and short side of the market. Their investment strategy is buy and hold – whether demand is weak or supply is abundant may be irrelevant. This kind of money is parked by pension funds and endowments, individuals and trusts. They simply have no interest in fundamentals. On a recent visit to a pension fund in Canada, we learned that they had committed a tidy $8 billion to commodities, primarily using passive index tools. $8 billion to buy and hold until redemptions call for liquidation.

Speculators are mad?Investor and fund interest in commodities is labelled ‘speculative interest’ due to the fact that these market participants are awaiting the greater fool to buy at a higher price and enable a profitable exit. It is true that most speculative interest is driven by investment funds. Unfortunately, the assumption that

Oil and the madness of crowds

Chris Thorpe is Executive Director, Global Energy Derivatives, with INTL FCStone Inc.

Contact: Chris Thorpe INTL FCStone Inc. Tel: +1 212 774 5963 Web: www.hcenergy.com

bunkerspot June / July 2012 www.bunkerspot.com 25

‘Beware the madness of consumers when you see someone try to control the price of crude by buying a

refinery’

to logistical constraints and product mix handicaps, others are extremely profitable because they sit next to discounted crude oil and have the optimal product mix that favours distillates. Buying a refinery does not reduce the price of crude oil but it does guarantee owning supply of products you do not want. For example, Delta would like to improve its supply of low cost jet fuel. Depending on configuration and technology, refineries must also produce gasoline and bunker fuel which may or may not have the same economic market incentives. Environmental constraints only make matters worse as consumers are restricted to a narrowing range of product substitutes, thereby affecting demand and prices on a regional basis. The refining business is in many ways just as challenging as the marine freight industry right now. High priced crude oil has squeezed profit margins for refining and transportation industries alike, forcing some players to react in curious ways. Beware the madness of consumers when you see someone try to control the price of crude by buying a refinery.

Predicting the price of crude oil is impossible at the best of times using fundamental analysis – and the challenge is magnified by the inf luence of crowds. However, understanding the relationships between different grades, refinery issues and product logistics can be useful for planning and hedging. We cannot underestimate the complexities of refined products and the ongoing changes in global market. And as long as investor capital is patiently and persistently buying energy commodities, no certain end is in sight for high oil prices until oil producers aggressively sell their future production. But this is an unlikely scenario given the current positioning of Iran toward Israel and the ensuing trade embargo. Almost certainly, the madness of crowds will take the price of oil and refined fuels to levels beyond reason again and again. Preparing a sound hedging plan should encompass a sound respect for the next mania. Without a plan, reactive behaviour is the norm and madness is often the result.

‘We cannot underestimate the complexities of refined products and the ongoing changes in global market. And as long as investor capital is patiently and

persistently buying energy commodities, no certain

end is in for high oil prices until oil producers

aggressively sell their future production’

Oil and the madness of crowds Commercial Issues

speculators are always bullish is also wrong. For example, crude oil futures have had record high volumes in the speculative interest category whilst natural gas futures have been well below normal. Since the market is supplied by producers of these fuels, they are the natural sellers in the market. When suppliers are bullish, they refuse to commit to sell more and the price rises despite the actual supply outlook. Since the madness of crowds applies to both buyers and sellers, the argument of where the price ought to be is continuously in f lux and arguably unknowable.

The price of oil in itself has become increasingly difficult to understand. The differences between grades and delivery points clouds where the actual fair price should be. Index funds, for example, have begun to shift their allocation from the West Texas Intermediate (WTI) – the Midwest American benchmark – to Brent – the North Sea European benchmark – which currently trades at a significant premium. Whilst the WTI futures contract has been the global price discovery mechanism since the 1980s, other indices have gained momentum as the crowd mentality shifts. For example, the majority of physical crude oil now moves from Saudi Arabia to Asia. So it would be a fair assumption to imply that Saudi grades are significant. But it is not surprising that WTI and Brent have held the incumbency as key benchmarks. Since the Saudi government will not allow a futures contract based on their common grade of crude oil, the market continues to depend on alternatives. Recent attempts by the New York Mercantile Exchange (NYMEX) to foster a Dubai-based exchange with an Omani grade crude specification have had mixed results.

And it just gets more complex from there. Among the refineries of the world, there are various grades of crude oil that are converted to refined products that may or may not be in demand locally. Each refinery has its own limitations of how much gasoline, distillates and fuel oil it can produce. In fact, the oldest refineries in the US are geared to produce too much gasoline, which is now being exported in record volumes to other countries on a regular basis. The refinery conundrum has led to some drastic closures and sale efforts recently - teasing some unlikely buyers. Delta Air Lines, for one, purchased a near scrap value ConocoPhillips refinery in Trainer, Pennsylvania, as Bunkerspot went to press. At least at the surface, this is evidence that the big consumers are truly confused about hedging and market pricing. Perhaps this is a result of group madness at Delta. While certain refiners are not profitable due

June / July 2012 bunkerspotwww.bunkerspot.com26

f low base’ or CFB.Also remember that assets are cash

outf lows, while liabilities are cash inf lows. If you are a client of Lloyd’s List Intelligence (LLI) and have received or read one of the reports issued by the New York off ice, you probably knew this already, but let’s state this clearly: working capital surpluses are really net cash outf lows unless they are entirely covered by cash in the bank.

Although using these tools is still looking at the past, it allows you to set a base from which to forecast what may have been going on since the latest f inancials you received from your customer. But how can you do this? One way I have found to get closer to the answer is to look at cash f low margins and how they may have been affected by the changes in rates since the CB and CFB were determined.

For instance, you are looking a dry bulk operator specialising on Supramaxes with a f leet of 10 units and the latest f inancial statements are for calendar year 2009. At that point, there was a cash balance of $5 million (your CB) and based on your calculations (using above tips) net cash f low for 2007 stood at $20 million (your CFB) on revenue of $166.54 million. The net cash f low margin was 6%.

Since 2007, Supramaxes have seen the following performance:

● 2008: declined by 13.60% ● 2009: declined by 58.86% ● 2010: rose by 77.59% ● 2011: declined by 37.19% ● So far in 2012: decline by 30.77%.

Based on this data, you can calculate what the maximum net cash f low margin would have been and whether or not you feel comfortable extending credit. Table 1 displays the changes in margin. The wider the margin, the higher the comfort level in extending credit – so as the margin contracts markedly use this tool as the f irst screen from which to do further research

How do you keep your bunker business away from trouble at a time when most of the

shipping industry is facing low rates and high bunker prices for such an extended period of time? The obvious answer is: do not extend credit to companies with weak liquidity, right? Well, credit managers at bunker suppliers or traders and container leasing companies around the world seem to agree that ‘not getting paid by one of our good paying customers’ would be a nightmare especially if this ‘good paying’ customer happens to be a major buyer.

This is, of course, mostly related to those customers for whom you do not have f inancial statements, and if even if you do, they are not provided promptly (e.g. six months to a year from closing).

Let’s start by establishing what constitutes liquidity. At its most basic level, liquidity is comprised of cash at hand plus any available credit facilities. In other words, what is in your wallet plus anything available on your credit cards. At the company level, the latter does not include credit available to purchase fuel, but rather credit facilities that allow you to access cash to pay suppliers, like revolving bank credit lines. Another layer of liquidity is net cash f low or, at the personal level, what is left from your paycheck after you pay all your bills and taxes (not much, right?).

Most companies in the shipping industry do not produce f inancial statements and if they do, you’ll have a cash balance from a particular date. This f igure is your ‘cash base’ or CB.

Since cash f low statements are rarely available, even when the other two f inancial statements are provided, let’s learn to build an operating cash f low statement when all we have are profit and loss statements and balance sheets. Remember that these statements are based on traditional accounting methods and do not necessarily ref lect cash inf lows and outf lows.

Start with net income (or net losses) and begin to add non-cash items like depreciation and amortisation, deferred income taxes and write-offs. Other items to consider are minority interests and undistributed equity earnings. After that, you need to account for changes in working capital since ‘booked’ revenue or sales are not necessarily received in the period (e.g. accounts receivable), just like all expenses are only paid when they are due (e.g. accounts payable). This becomes your ‘cash

Félix Yamasato looks at how bunker players can avoid financial pitfalls by

taking a closer look at customers’ cash flows

Commercial Issues

Go with the flow

Félix Yamasato is Regional Manager, Americas Analyst Team with Lloyd’s List Intelligence.

Contact: Félix K. Yamasato Lloyd’s List Intelligence Tel: +1 646 957 8971 Mob: +1 203 667 1082 Email: [email protected] Web: www.lloydslistintelligence.com

‘If the revenue from a single uninsured client

represents more than your cash or equity reserves or even your available bank credit, you are a high risk

to your counterparties’

bunkerspot June / July 2012 www.bunkerspot.com 27

is either gained or lost due to rate changes is mostly channelled into higher or lower profits due to fixed expenses that were already covered in the last period for you which you had figures.

● it may also be that only a portion of the fleet is sensitive to market rates. Here there is another layer of complexity since long-term contracts at fixed rates will require you to know the level of counterparty risk associated

and weed out any potential failures before they actually happen.

This is just a simplistic way to see the potential changes in profits, so you need to keep in mind the following:

● capital structure of the company – meaning that if there is heavy debt servicing coming up or expiring, margins could contract or expand

● it may also be that every single dollar that

Commercial Issues

with the latter contracts (e.g. Eagle Bulk fixtures to Korean Line).

Remember that margins are very useful in helping you compare between the different classes (ship size) and sub-sectors of the shipping industry.

Concentration of risk is almost as important as counterparty risk assessments, meaning that if the revenue from a single uninsured client represents more than your cash or equity reserves or even your available bank credit, you are a high risk to your counterparties.

Do I need to tell you about what has happened to a bunker trader that decided to cater to a failing business and now has left debts with bunker suppliers as a result of a single ‘bad customer’?

The global credit manager at one of the largest physical bunker suppliers explicitly cited his fear that small bunker traders can be brought down by concentration risk.

Changes in Supramax Rates

Maximum Cash Flow Margin Change Expected Cash Flow

2007 110.70% 6.00% $20,000,000

2008 -13.60% 5.18% ($2,720,000) $17,280,000

2009 -15.86% 4.36% ($2,740,608) $14,539,392

2010 77.59% 7.75% $11,281,114.25 $25,820,506.25

2011 -37.19% 4.87% ($9,602,646.28) $16,217,859.98

2012 -30.77% 3.37% ($4,990,235.52) $11,227,624.46

Table 1

SPOT BUNKER MARKETMABUX MARINE DIRECTORY

OIL FUTURES ONLINE

Register now - Two weeks free trial

Mabux Marine Directory features Suppliers, Traders and Brokers Worldwide

Real-Time & DelayedICE: Gas Oil, Brent Crude OilNYMEX: Light Crude Oil (WTI), Heating Oil

Our Spot Bunker Market Offers more than 350 ports and counting, with indications daily updated

Notice:

SPOT BUNKER MARKETMABUX MARINE DIRECTORY

OIL FUTURES ONLINE

Register now - Two weeks free trial

Mabux Marine Directory features Suppliers, Traders and Brokers Worldwide

Real-Time & DelayedICE: Gas Oil, Brent Crude OilNYMEX: Light Crude Oil (WTI), Heating Oil

Our Spot Bunker Market Offers more than 350 ports and counting, with indications daily updated

Notice:

Notice:

1. Rotterdam shows the usual Market once a day indications.

2. Rotterdam is connected to the ICE’s price variations as published on our website.

Your ONE-STOP Website for Your Bunker Dealswww.mabux.com

June / July 2012 bunkerspotwww.bunkerspot.com28

and a shallow operating draft is not required – especially after receiving a quote on one 135,000 barrel full ABS ocean, double-hull barge which was higher than one might pay for a vintage very large crude carrier (VLCC) today.

That is not to say that double-hull barges are not selling. In 2010, Marcon sold 17 double-hull, inland tank barges to Ingram Barge Company. American Commercial Lines recently purchased eight 20,000 barrel tank barges from SeaRiver Maritime, a subsidiary of ExxonMobil.

Single-hull phase-outDouble-hull barges coming on the market at any price cannot offset the past availability of single-hull barges. This year the number of second-hand tank barges listed by Marcon has dropped a significant 40%, confirming that the single-hull phase-out is close to accomplishing its goal.

The US domestic market, as far as supply and demand in equipment, finally seems to be getting back to balance after the fast and furious shedding of single-hull barges and mass construction of replacement double-hull units after OPA 90 came into law.

Unlike the commoditised international tanker markets that are in the midst of a cyclical correction after an overbuilding, the domestic market is much less volatile and susceptible to dramatic effects of geopolitical events and shifts in ton-mile economics.

The Jones Act-protected fleet is largely based on long-term upstream and downstream supply and demand in the United States and is driven primarily by specific regional commitments.

While we did see a short period of oversupply of tank barges at the end of the last decade as newbuildings were overlapping retirements, this did not have a lasting effect on the industry.

Over the last five years, the overall domestic tank barge fleet has grown from just over 4,000 barges with an average age of 30 years in 2007 to over 4,500 in March 2012.

While the actual US Coast Guard (USCG) data reports today’s average age as 22 years, it realistically is much less. Included in the current data are a number of older barges still officially designed as tank barges, but retired from petroleum trade to other services, plus there are several fleets of large 100,000 to 200,000 barrel ocean barges that were refitted with double hulls at great cost which still show an original build date.

In any case, the data reflects a younger and larger fleet able to service the continuing demand for petroleum and chemical products and, hopefully, a more stable market.

The graduated phase-out of single-hull tankers and barges in the United States – implemented

through the Oil Pollution Act of 1990 (OPA 90) in response to the Exxon Valdez oil spill in 1989 – is almost complete two years before the 2015 deadline.

By 2005, only about 50% of US coastal barges were double hull and construction proceeded at a fast pace.

Most single-hull petroleum barges and tankers were retired prior to their designated retirement dates and sold outside the United States for further trading, scrapped or converted to alternate usages. OPA 90 caused the US flag tank barge sale and purchase (S&P) market to be flooded with 20-30 year old tank barges, especially during the mid-2000 years.

Barges suitable either for conversion or future trading overseas were generally sold at levels above scrap, ranging from a low of about $3 to $15 a barrel and barges were fast leaving the US registry.

Buyers for this type of single-hull equipment today, especially units over 100,000 barrels, are finding the cupboard bare. Marcon International expects to close the sale of one 149,000 barrel single-hull petroleum barge shortly, but we will see relatively few of these size and type units back on the market for sale in the future.

Large barges, especially older units without double bottoms, were the first to be regulated out of trade and the first to be sold or scrapped.

Even smaller barges that are good conversion candidates to deck and other service are now becoming scarce with around two more years to go until their official retirement dates.

As the supply of these barges further declines, the prices for better quality units may strengthen until the day that the last of these are sold.

During the 1990s and 2000s, it was very rare to see a full double-hull barge meeting all OPA 90 requirements on the market. Some double-hull barges, though, are starting to appear in the normal course of events – especially with some sellers interested in seeing some under-utilised equipment going foreign and out of competition.

Buyers looking for storage barges or units for future trading who are used to yesteryear’s pricing of large, ocean single-hull barges, however, are in for a shock.

Good 100,000 to 250,000 barrel ocean-classed, double-hull barges can be developed, but prices may be close to the unit’s replacement cost.

We have recently suggested to a number of buyers to consider older tankers where US flag

Barge Markets

Jon Thielemann of Marcon International

gives a broker’s view of the tank barge market

Jon Thielemann is a broker with Marcon International Inc.Since 1981, Marcon International has closely followed the tug, barge and offshore petroleum markets with over 1,250 vessels and barges sold or chartered worldwide. Sales include 140 tank barges totalling in excess of 7.3 million barrels capacity. Of the over 14,000 vessels and barges Marcon currently tracks, more than 660 are tank barges with around 70 inland, coastal and ocean barges officially for sale.

Contact:Jon ThielemannMarcon International Inc.Tel: +1 360 678 8880Fax: +1 360 678 8890Email: [email protected]: www.marcon.com

Doubling up

June / July 2012 bunkerspotwww.bunkerspot.com30

‘The uptake of in-line blending is due, in part, to the measurement and

control technology – previously available only to refineries or very large

facilities – which now can cost-effectively be deployed in small tank

farms/bunker facilities, or even on barges’

as larger physical bunker suppliers. However, like any technology, it is vital to ensure that the solution selected can be implemented successfully.

This is one of the drivers behind the International Bunker Industry Association’s (IBIA) recently published Guide to In-line Blending. The guide is intended to provide impartial guidance to those considering the use of in-line blending as part of their bunker delivery strategy. An evaluation framework, such as the one featured in the guide, provides bunker suppliers with a much needed tool to help them select a fit-for-purpose in-line blending solution that delivers the highest ROI for their business. It also will help them decide the most suitable technology for blending, whether it is in-line or a more traditional solution.

Business goalsAll capital investment should be evaluated on the ROI it delivers. This also is true with blenders. It is important to recognise that different types of blending systems have widely varying capital expenditure and operational expenditure (CAPEX/OPEX) costs and savings, in addition to any incremental operational flexibility one may provide. Therefore, it is important to define both the products to be blended and the blending quality/accuracy required to meet an ROI model. All too often, companies invest in blending technology without a precise definition of the performance required to meet their business goals.

Type of in-line blender Selection of the most appropriate type of blending is vital. In-line blenders now include online measurement and control of parameters

Most bunker fuel is blended at some point in the process from refinery to point of delivery.

This process traditionally has been carried out either within the refinery, often with an in-line blender and a range of components to achieve the required bunker fuel, or in tank farms using simpler, traditional tank blending methods and fewer components.

Bunker prices are now even higher than they were in 2008, which is placing pressure on bunker suppliers’ margins. This, in conjunction with more stringent fuel specifications such as the International Organization for Standardization’s (ISO) revised ISO 8217:2010, and the sulphur requirements of Emission Control Areas (ECAs), are making the savings and improvement in quality delivered by in-line blending increasingly attractive to the industry.

The uptake of in-line blending is due, in part, to the measurement and control technology – previously available only to refineries or very large facilities – which now can cost-effectively be deployed in small tank farms/bunker facilities, or even on barges, and can deliver a return on investment (ROI) in less than six months. Recent case studies have shown that when compared with traditional blending techniques, savings of more than $20 a tonne can be delivered by a well-designed and installed in-line blending system.

In our daily lives we have been surrounded by products such as gasoline, aviation fuel, medicine, healthcare and beauty products and food and drink that are blended on demand to extremely high specifications using a range of technologies, including in-line blending. Why then has the bunker industry waited until now to start adopting in-line blending? This is due, in part, to a reluctance to move away from established traditional practice. However, the more likely explanation is that it is due to a historic lack of expertise within the industry as to how to correctly specify and deploy these systems. This often has resulted in deployment of the wrong technology for the wrong application, giving some in-line blending applications a bad reputation.

New technologyOver the last 10 years, a wide range of technology-based solutions, previously available only to larger corporations (e.g. from manufacturing resource planning to telephony systems), has become accessible to all businesses. This also is true in the bunker market where high accuracy, easy-to-use in-line blending solutions now are available to small and medium-sized companies as well

Jon Moreau of Cameron Jiskoot

argues that in-line blending can be the key to successful bunkering

Bunker Blending

Jon Moreau is Director, Business Development for Jiskoot Quality Systems.

Contact:Jon MoreauCameron JiskootTel: +44 1892 518000Email: [email protected]: www.c-a-m.com/jiskoot

In-line solutions

bunkerspot June / July 2012 www.bunkerspot.com 31

‘Compared with traditional blending techniques,

savings of more than $20 a tonne can be delivered by a well-designed and

installed in-line blending system’

elements. It is risky to select components without understanding how they will interact with one another, the control system and the dynamics of the site environment. This can result in savings during CAPEX, but never the optimal OPEX, and can therefore fail to deliver the best possible ROI.

SummaryA correctly designed, installed and configured advanced-control in-line blender can add significant value to terminal operations. But if poorly designed and executed, it can result in sub-specification blends, increased costs due to reblending, potential revenue losses and plant downtime. With advanced-control in-line blending, new levels of bunkering efficiency, competiveness and profitability can be achieved.

The IBIA guideline provides potential users of in-line blending with a framework on how to work closely with a blending systems manufacturer from an early stage of a project. This will ensure they are involved in the complete scope of blending operations and can increase the value they bring. It also can provide a perspective on the real ROI that can be delivered and how a system should be configured within a facility. It is clear that significant payback and ROI can be achieved if the correct technology is selected.

More facilities likely will consider deploying advanced-control in-line blending systems as the number of facilities that have deployed and benefited from the savings of these systems increases. What is evident is that in-line blending will play a more prominent role in meeting the needs of physical bunker suppliers to deliver a range of bunkers from a wide and ever-changing range of feedstock. In the future, those suppliers who embrace the use of the latest technology to produce bunker fuel that meets specification at the lowest cost and with the highest flexibility will dominate the market.

interdependence on the other facets of the facility and the effects of issues such as pressure loss on loading rates all need consideration.

Blender configurationOne of the keys to the successful design of any in-line blending system is the selection of the correct components, their integration within the package and the performance guarantee of the total blending system. Of vital importance to the success, and hence profitability, of an in-line blender is how well the individual components perform and how well they operate once integrated in the blender with the control system. Selection of appropriate blender components is the first stage of ensuring the quality of the final blended product.

Some of the primary design considerations for key components are:

● flow meters – turndown, suitability for crude and susceptibility to hydraulic noise

● control valves – optimal control, stability and response time without adverse pressure drop

● mixing system – pressure drop, degree of mixing and rangeability

● control system – real-time three-term PID control, proven (i.e. not site-specific)

● analyser system – location, noise, response time and flow weighting at standard conditions.

Incorrect selection or implementation of any of these components will result in fundamental system errors that likely are impossible to resolve. Once selection is made, it is important to verify that the selected components are proven and can function optimally for the full range of blends. A common error when designing blending systems is a lack of attention to the critical

Bunker Blending

such as viscosity, density and sometimes sulphur. Accurate flow measurement and control enables blends to be optimised to these parameters with high precision at reference conditions, even if there are variations in the feedstock. This is particularly suitable for bunker applications where the quality of the components being blended varies during the blend process.

Also available are in-line blenders that now can cost-effectively and dynamically calculate multiple quality parameters in real time throughout a blend (based on a quality certificate). Calculated quality parameters of this nature allow the blend to still be optimised for an analyser-measured quality parameter, such as viscosity, while having the ability to dynamically limit the process to ensure that the blend cannot exceed a defined quality parameter (such as sulphur, for example). This is particularly suitable for applications where the cost of a second or third expensive analyzer is not justified.

It is worth noting that, unlike a tank blending system, an in-line blending system can be designed with a high-shear mixing system that will give a performance similar to a laboratory system. This enables it to more readily achieve blends that might have been tested using a high-shear mixer in the laboratory. It also is worth noting that in-line blending, and in fact all other types of blending, cannot blend incompatible products or produce a blend with an impossible blend ratio.

Location of blenderThe location of a blending installation might at first seem trivial. However, an in-line blender is the heart of a successful operation and, therefore, its interaction with and

June / July 2012 bunkerspotwww.bunkerspot.com32

‘The real cost of oil has hardly changed over the years when compared to traditional stores of value – gold and silver… but this is no consolation to vessel owners who must buy bunker fuel in

dollars – not gold or silver coinage’

Bunker prices remain high, charter rates low, and the world economy seems perpetually moribund. Yet

vessel owners might find some solace in the words of the late American insurance executive W. Clement Stone, when he said: ‘Got a problem? Congratulations!’

Growing up in dire poverty, Stone became one of America’s first self-made billionaires. He understood that crisis begets innovation, and innovation begets success. In recent years, many innovations have been introduced in the commercial shipping industry promising a better tomorrow. Some of these advances are now reality – helping vessel owners survive and even prosper. Shipowners may be getting leaner, but they are also getting smarter, implementing innovative strategies for optimum vessel efficiency and profitability.

Many owners have already developed vessel by vessel efficiency improvement plans outlined in the Ship Energy Efficiency Management Programme (SEEMP) guidelines issued in 2009 by the Marine Environment Protection Committee (MEPC) of the International Maritime Organization (IMO). Last July MEPC voted to make the SEEMP programme mandatory in January 2013.

In this article we will take a brief look at the SEEMP recommendations, why economic challenges make these recommendations imperative, and the remarkable efforts by engine makers and shipowners to optimise vessel efficiency with innovative technology. We will also evaluate the effect of fuel quality on propulsion system efficiency, and review an inexpensive but highly effective technology now saving millions of dollars annually for savvy vessel owners.

The goal of the MEPC action is reduction of carbon dioxide (CO2) from marine propulsion systems, by some estimates the source of anywhere from 4% to 6% of so-called ‘greenhouse’ emissions worldwide. With greater fuel efficiency, CO2 reductions follow, the thinking goes.

Whether or not the greenhouse theory of ‘global warming’ holds up over time is anyone’s guess. Yet there is no guesswork in understanding that improving vessel propulsion efficiency in order to reduce costs is simply good business, benefiting the owner, the charterer, and consumers who buy goods transported by sea.

Ralph E. Lewis of Power Research Inc. argues that

improving ships’ engine efficiency and cutting

emissions makes sound business sense

Fuel expense remains the dominant cost for both cruise and container ships, passenger ferries and all vessels trading on the spot market. Charterers bearing the fuel cost burden are also well aware of efficiency benefits - major criteria in the vessel selection process.

While emissions reduction remains a laudable goal, vessel owners in 2012 are far more focused on two daunting and overriding concerns, challenges that threaten their very survival in the turmoil of today’s marketplace. These challenges are high fuel costs and low charter rates.

High fuel costs Economic principles in free markets dictate that with reduced demand, fuel prices should decline. But these rules do not always apply in the petroleum industry. Marine fuel sales in Singapore recently dropped to a two-year low, yet prices remain high. Politicians find easy targets to blame – oil companies, speculators, ‘peak oil’, Organization of Petroleum Exporting Countries (OPEC) and so on. Yet the underlying cause is quite simple – US dollar inflation.

Enter the Federal Reserve System, the central bank of the United States. Independent of Presidential and Congressional authority – the Fed is essentially a private corporation with limited Federal oversight. The Fed is also the primary lender to the United States government: it now holds more than 61% of US government debt – more than China, Japan,

Fuel Additives

‘Whether or not the greenhouse theory of “global warming” holds up over time is anyone’s guess. Yet

there is no guesswork in understanding that

improving vessel propulsion efficiency in order to reduce costs is simply good business’

Business efficiency

Ralph E. Lewis is the Vice President, Technical of Power Research Inc.

Contact:Power Research Inc.Tel: +1 713 490 1100Email: [email protected]: www.priproduct.com

June / July 2012 bunkerspotwww.bunkerspot.com34

Not all is gloomy. Solutions are at hand, many of them included in the MEPC efficiency guidelines.

MEPC efficiency guidelines The basic concepts for efficient vessel operation have been well understood, if not always implemented, for decades. Many of these are reflected in the MEPC guidance memo (MEPC.1 Circ.683) for SEEMP development, including improved voyage planning, speed optimisation, more efficient trim, ballast and propeller design, weather routeing, improved hull maintenance, waste heat recovery and better cargo handling practices – all commonsense measures.

In addressing propulsion system efficiency, the MEPC memo notes that ‘the new breed of electronic controlled engines can provide fuel efficiency gains’, also suggesting that other methods to improve efficiency ‘might include fuel additives, adjustment of cylinder oil consumption, valve improvements, torque analysis and automated engine analysis systems’.

The guidelines almost appear understated in view of the major advances which have been made by engine makers over the past decade. Both MAN Diesel and Wärtsilä have invested in large bore, two-stroke test bed engines upon which these two dominant players have developed groundbreaking technologies to enhance engine durability and efficiency. In recent years, they have clearly established that with increases in peak firing pressure (pmax), specific fuel oil consumption (SFOC) is reduced.

Reduced fuel consumption Peak firing pressure is simply the highest pressure attainable in a cylinder during combustion – the optimum efficiency attainable. Achieving this across all load ranges has been a major focus of MAN Diesel in the development of the company’s ME series electronic engines.

A first step is a concept known as ‘auto tuning’. Firing pressure from each cylinder is monitored by a sensor, the data sent to an onboard processor with software that interprets

the results and formulates an appropriate response which makes operational adjustments to achieve greater engine balance and improved thermal efficiency.

The system depends on the capability of varying both fuel injection timing and compression ratio. On conventional engines, this process is somewhat complicated by the fact that the camshaft design determines valve timing. So in the ME series engine, the camshaft functionality is eliminated – replaced by computer-controlled actuators that determine the precise timing of fuel injection and valve opening and closing.

This system permits continued engine balancing at any operational profile, providing optimum pmax pressures while reducing SFOC. MAN Diesel studies verify that pmax improvements of 5-to-10 bar mean a corresponding reduction in SFOC of 1%-2%, a 0.25 decrease in SFOC for every bar pressure increase.

Wärtsilä first experimented in the early 1990s with electronically controlled fuel injection systems. Today, the RT-Flex series of engines use a common rail system that permits complete control of fuel injection timing, rate of fuel flow, fuel pressure and timing of valve operation. An option for the company’s electronic two-stroke engine, the RT-Flex series, is an intelligent combustion monitoring (ICM) system which continuously evaluates firing pressure data from all cylinders in order to properly time fuel injection and valve operation and provide ongoing engine balancing to optimise reduced fuel consumption. The good news is that ICM system can be retrofitted to any older mechanical two-stroke engine.

The ICM system incorporates technology originally developed by ABB as the Cylmate system, pioneered in the early 2000s. In two-stroke engine testing conducted in February 2007 to verify the relationship between pmax and SFOC, ABB incorporated a highly accurate, KRAL fuel mass flow meter. The test verified that with a 10 bar increase in pmax, SFOC was reduced 2.2% – a relationship later mirrored in test data reported by MAN Diesel.

Engine design improvements have made major advancements in recent years, but one joker in the deck yet remains to defy all mechanical engineering efforts to optimise combustion.

Reducing fuel consumption In 2011, Det Norske Veritas (DNV) and Viswa Lab reported a significant increase in bunker fuel quality complaints among operators, some attributable to increased use of cutter stock to dilute heavy fuels to 1.0% sulphur in meeting the Emission Control

‘Peak firing pressure is simply the highest pressure

attainable in a cylinder during combustion –

the optimum efficiency attainable’

and everybody else combined. Acquiring such massive debt is an easy process for the Fed. It simply creates the money out of thin air – a process known as ‘debt monetisation’.

This sleight of hand was facilitated when President Nixon decoupled the US dollar from the gold standard in 1971. Since that time, the value of the dollar – the world reserve currency used for international oil trading – has declined by more than 83%, thanks to continued Fed increases in the money supply. In fact, the real cost of oil has hardly changed over the years when compared to traditional stores of value – gold and silver.

In 1960, for example, two silver 10 cent pieces (dimes), having a combined composition of 0.18 ounces of silver, could purchase one gallon of gasoline. Today, the same 0.18 ounces of silver, now worth about $5.40 in 2012 dollars – will also buy a gallon of gasoline, with change left over for a soft drink, at least in the United States.

In real terms, oil is still cheap, but this no consolation to vessel owners who must buy bunker fuel in dollars – not gold or silver coinage. Excessive fiat currency creation, likely to continue and even accelerate in years to come, will remain an ongoing challenge for vessel operators, forcing technological adaptation.

Low charter rates As investor Warren Buffet presciently cautioned in 2007: ‘When the tide goes out, we find out who’s been swimming without a bathing suit.’ That year, spurred on with cheap credit and high charter rates, shipowners were on a ship building spree.

This ‘irrational exuberance’ (apologies to former Fed Chairman Alan Greenspan) occurred only months before the 2008 economic debacle, resulting in a huge wave of vessel deliveries in the midst of global recession. Charter rates plummeted, and only recently have begun to tick up. In this case, the supply and demand model is working. Some vessel owners have by necessity ceased trade. A few stragglers are struggling to survive, laying up vessels while reducing administrative staff and even crew size. Yet many are boldly moving forward with innovation and improved business practices.

In 2010, total vessel deliveries reached a record high. Deliveries in 2011 were approximately 85% of those the year before, and 2012 deliveries will likely be the same as 2011. Since 2008, the global tanker fleet has grown by an estimated 40%. On the dry bulk side, vessel deliveries are expected to peak this year, but deliveries scheduled through 2013 will likely keep rates depressed through year’s end, cautions Moody’s Investor Service.

Fuel Additives

June / July 2012 bunkerspotwww.bunkerspot.com36

was as much as 7.5 bars – operating loads now common for vessels at eco-speeds, and loads typical of auxiliary engines. Translated, the results meant a range of SFOC reduction of 1.3% to 1.9% percent, hardly insignificant numbers.

Since then, Power Research Inc. has acquired pmax and SFOC data from a variety of vessels to measure the extent of fuel cost savings with PRI-RS and PRI-27. The results consistently correspond with the MAN Diesel PRI test bed data. For example, a container vessel operating on a fixed schedule consuming 380 centistoke (cst) fuel oil has been continually monitoring PRI-27 performance on a two-stroke MAN Diesel 7S70 MC-C. With the PRI-27 thermal

stability additive, pmax has increased an average of 3.89 bar, providing an SFOC reduction of almost 1%. Translated into dollars – annual vessel fuel costs have been reduced by $147,000. Coupled with recovery in lost fuel value from reduced sludge precipitation with PRI-27, the total saving has been $174,000 annually for the vessel. In another example, a cruise ship operating with six Wärtsilä 46/50DF engines is showing an across the board increase in pmax with PRI-RS. When compared to identical load ranges operating on untreated fuel, pmax increase with PRI-RS is averaging 3.72 bar – resulting in a 0.93% reduction in SFOC. Based on present fuel prices and consumption rates, the vessel is saving $312,000 in annual fuel costs. Sludge data from the vessel also confirms a 30% reduction in sludge with PRI-RS, recovering

sufficient fuel value to more than cover the overall investment in the chemistry. Spread over a 20-vessel fleet, annual savings with PRI-RS totals $6.24 million.

Similar results have been verified for PRI’s thermal stability treatment for distillate fuels, PRI-D. In 2005, PRI-D was evaluated at Southwest Research Institute (SWRI) in San Antonio, Texas under the US Environmental Protection Agency (EPA) Heavy Duty Diesel Transient Test cycle. Like the test conducted two years later at MAN Diesel, CO, THC and PM were reduced on the Cummins L-10 engine. Brake specific fuel consumption (BSFC) declined by 1%, and brake specific horsepower increased by 1%. SWRI testing of PRI-D on a larger Cummins KTA 19M3 engine also verified power increase and BSFC reduction across three load ranges.

‘These 1%-2% savings may not sound like much at first, but when calculated over time and over an entire fleet, a company can literally save millions of dollars,’ says Blake Davidson, PRI chief financial officer. ‘On the heavy fuel side, PRI-RS and PRI-27 are also formulated with highly effective sludge dispersants, yet another way to recover lost fuel value. And with low sulphur gasoil, PRI-D contains the most advanced lubricity chemistry available to safely protect fuel pumps from excessive wear and premature failure.’

Cost savingsAdditional efficiencies and cost savings accrue. With PRI thermal stability chemistry, the contamination rate of auxiliary engine lube oil has been reduced as much as 30% on many vessels – saving owners considerable expense in lube oil replacement costs. Deposit prevention on auxiliary engines with PRI is permitting engineers to extend overhaul intervals to engine maker schedules. Time between exhaust boiler and purifier cleaning cleanings is increased, and vessels once fined in ports by aggressive smoke police are now getting the all clear.

Area (ECA) mandate. Among other problems, vessel owners reported increased incidences of poor ignition quality and excessive fuel sludge precipitation. Many of them are now resolving these troubling issues with a series of chemical fuel treatments developed by Power Research Inc. Vessel owners quickly discovered that the company’s PRI-RS and PRI-27 heavy fuel oil chemical treatments actually boost pmax while reducing SFOC – a benefit now confirmed in stringent, laboratory engine testing. Additionally, both lab and shipboard data confirm the capabilities of these chemistries to reduce fuel sludge precipitation in a range of 30%-45% – recovering lost fuel value. The results are consistent and clear, and the financial savings have been impressive.

PRI-RS and PRI-27 are formulated with deposit modifier type chemistries specifically designed to elevate the thermal stability of blended heavy fuel oils. The approach is rooted in the reality of petroleum fuel behaviour which dictates that the more thermally stable the fuel – the more completely it combusts. While the concept of thermal stability is a relatively new one regarding marine fuels, petroleum chemists associated with aviation fuels have long recognised the criticality of fuel thermal stability for combustion in aero-derivative gas turbine engines, the focus of decades of research. Prevention of damaging, power robbing deposits with optimal combustion is a primary safety goal for aircraft turbine engine makers, so critical that strict standards have long been mandated to ensure maximum thermal stability in aviation fuels.

While many marine fuel additive makers have developed a wide range of detergents, dispersants and iron-laced catalysts in efforts to ‘clean up after the elephant’, PRI researchers continue to focus instead on chemistries that optimise thermal stability, a ‘proactive’ approach that completely negates the need for harsher and less effective measures. The work is yielding impressive results.

In April 2007, just two months after ABB was establishing the relationship between pmax and SFOC in Sweden, the value of the PRI research was verified in testing conducted by MAN Diesel in Denmark on a 5L21/31 engine under the strict MARPOL Annex VI test protocol. At all load ranges, application of PRI-RS to the fuel resulted in reduction of carbon monoxide (CO), total unburned hydrocarbons (THC) and particulate matter (PM) – all markers of improved combustion efficiency.

The PRI-RS effect on pmax in the MAN Diesel test was also pronounced. At all load ranges combined, pmax shot up an impressive 5.2 bars. At reduced load ranges, the increase

Fuel Additives

‘With PRI thermal stability chemistry, the contamination rate of

auxiliary engine lube oil has been reduced as

much as 30% on many vessels – saving owners considerable expense in

lube oil replacement costs’

June / July 2012 bunkerspotwww.bunkerspot.com38

‘Market-based measures will undoubtedly continue to evolve as exhaust emission monitoring tools like the CEMS become a

standard part of the new build specification’

January 2013. The EEDI is calculated as the sum of the CO2 exhaust emissions from the main and auxiliary engines minus any CO2 emission reduction technologies employed (e.g. wind power) and divided by the amount of transport work for particular vessel types. Specifically, the CO2 exhaust emission is calculated using a conversion factor based on the carbon content of the type of fuel used. The essence of EEDI is that it mandates new vessels to improve CO2 efficiency through ship design as future EEDI reduction schemes would eventually be planned, adopted and subsequently phased in.

The second measure, the Ship Energy Efficiency Management Plan (SEEMP), however, is applicable to all ships, including those that are already in operation. The SEEMP establishes a quantifiable mechanism to improve the energy efficiency of a ship’s operation with the adoption of one or more measures that can be quantifiably monitored and evaluated. Verified at the first intermediate MARPOL Annex VI International Energy Efficiency Certificate (IEEC) survey or renewal survey on or after 1 January 2013, the SEEMP is applicable to all vessels of 400 gross tonnes (GT) and above operating in international waters. Although the SEEMP covers nearly every possible improvement measure such as improved combustion, optimised hull and propeller maintenance through more frequent scheduling, this article focuses on performance monitoring and in particular on exhaust emissions monitoring.

Exhaust emission reduction measures such as fuel-water emulsions for reducing

At a recent green ship event, discussions focused on proposing a revision to the International

Convention for the Safety of Life at Sea (SOLAS) 1974, as amended, where it stipulates that no fuel oil with a f lashpoint of less than 60°C is permissible for use as marine fuel oil. The proposal is centered on decreasing the minimum f lash point requirement for marine distillate grade fuel oils from 60°C to 52°C, which is the f lash point specification for non-marine or on-road diesel fuel in the United States as well as in other countries. Lowering the f lash point requirement would potentially open up a wider supply basis for the marine fuel market.

The proposal obviously was related to the upcoming medium and long-term International Maritime Organization (IMO) MARPOL Annex VI legislation calling for more stringent maximum sulphur limits for distillate fuel oils. The availability of low sulphur fuels continues to be a significant industry concern. Refiners are reluctant to make the necessary investments to ensure low sulphur distillate demands will be met.

As marine regulatory bodies continue to review land-based emission control solutions that have been successfully implemented, it is conceivable that a vessel delivered in 2013 would eventually be subject to new restrictions not yet envisaged by the shipping industry, its customers, or its regulators. These future constraints may bear a resemblance to those set by non-marine industries, especially if the fuel used in marine and non-marine engines are sourced from a shared supply pool. It would only be a matter of time before the environmental mechanisms used ashore to monitor emissions would be migrated to the marine sector. Until then and for the near term, there are two new market-based measures from IMO that are geared to help the maritime industry improve its environmental footprint.

Applicable to new ships as defined by the IMO’s Marine Environment Protection Committee’s MEPC.1/Circ.681, the Energy Efficiency Design Index (EEDI) becomes the mandatory technical measure of a ship’s carbon dioxide (CO2) efficiency on 1

Albert Leyson of Drew Marine looks at new developments in the

field of exhaust emission monitoring

Exhaust Emissions Monitoring

‘While most in-situ CEMS are incapable of handling

calibration gases for routine or regulatory

checks, Drew Marine’s in-situ CEMS unit is offered

with up to two cylinders suitable for up to five

calibrations per cylinder’

Albert Leyson is the Marketing Manager with Drew Marine USA Inc.Drew Marine will be exhibiting at this year’s Posidonia (4-8 June, Athens): Hall #2, Booth 2.213.

Contact:Albert LeysonDrew Marine USA Inc.Tel: +1 973 526 57Fax: +1 973 887 1426Email: [email protected]: www.drew-marine.com

Measured approach

June / July 2012 bunkerspotwww.bunkerspot.com40

‘To measure or not to measure is no longer

the question, but rather we need to ask which technological means

should be used to measure exhaust gas emissions reliably and accurately’

remains important to consider not just CO2 in market-based measures, but the total emissions that have an impact to the environment (see Figure 2).

The need to demonstrate environmental responsibility is of paramount importance in today’s marine industry. If maritime regulators continue to consider and implement established, land-based mechanisms, such as using on-road diesel fuel and emissions trading, to meet the industry’s goals, then the need to reliably and accurately measure exhaust emissions in order to prove compliance may inevitably be required.

To measure or not to measure is no longer the question, but rather we need to ask which technological means should be used to measure exhaust gas emissions reliably and accurately.

nitrogen oxide (NOx) and sea water scrubbers for reducing sulphur oxide (SOx) are just two of the technologies being evaluated by ship operators faced with impending regulations looming on the horizon for both types of emissions. With an implementation date of 1 January 2015, which is less than three years away, the fuel used in Emission Control Area (ECA) zones will be limited to 0.1% sulphur maximum. The following year on 1 January 2016, IMO Tier III standards for NOx will be set 80% lower than Tier I limits for vessels operating in designated NOx ECA zones.

In consideration of the four key elements of the SEEMP – planning, implementation, evaluation, and monitoring – it is essential that the installation of any exhaust emission reduction technology includes the means to prove that the equipment performs as designed, the emissions are easily quantifiable, and the benefits to the environment are clearly ascertained. For existing vessels in operation on which emission reduction measures are being considered as part of their SEEMP goals for next year, the installation of exhaust emission monitoring equipment would be beneficial as a baseline reference, in establishing realistic targets based on their equipment provider’s performance claims and the ongoing monitoring of exhaust emissions – system performance.

In-situ monitoringThe most effective method for measuring exhaust emissions is through in-situ monitoring using a continuous emissions monitoring system (CEMS). This widely accepted land-based technology is extensively used to monitor exhaust gas emissions in sensitive areas as well as part of critical industrial process and control applications. In contrast to extractive monitoring systems, that often require complex sample lines needing to be traced with steam or electrical heating elements to bring the exhaust gas to the analyser, an in-situ CEMS provides simple continuous measurement capability by bringing the measurement analyser adjacent to the exhaust stack.

While most in-situ CEMS are incapable of handling calibration gases for routine or regulatory checks, Drew Marine’s in-situ CEMS unit is offered with up to two cylinders suitable for up to five calibrations per cylinder. The concentration of each calibration gas is typically based on 80% Full-Scale Def lection (FSD) of the measurement range of the CEMS unit. When additional gas is required, cylinders can be easily exchanged by Drew Marine in all major locations.

In the coming years, shippers and charterers will demand operators improve their emission quality. Initiatives by local governments and ports are expected to increase in number and most will utilise EEDI and/or SEEMP, as they were established by the IMO, as a means to monitor the actions taken to improve emission quality. Singapore, for example, offers incentives to partake in its Maritime Singapore Green Initiative. The initiative includes a Green Ship Programme that encourages ocean-going ships to go 10% below the target IMO EEDI baseline. All ships verified will receive 20% rebate on annual tonnage fees and 50% rebate on initial registration fees.

Another example is Canada’s Green Marine Environmental Program. This initiative has identified seven major environmental issues affecting the marine industry, including NOx and SOx emissions. The programme evaluates the progress of participants through performance indicators on a scale of one to five, where at level three, the exhaust emissions are no longer calculated or defined by industry best practices but are quantified in order to understand their true environmental impact. Furthermore, participating members’ exhaust emission reduction measures are subject to external verification by a third-party every two years and the results published online.

These market-based measures will undoubtedly continue to evolve as exhaust emission monitoring tools like the CEMS become a standard part of the new build specification, as they are for modern industrial facilities today. By the same token, existing conversion factors might be replaced with actual fuel carbon content obtained from analytical testing in order to improve the overall estimation of CO2 as regulatory bodies begin to scrutinise actual emissions versus rated or designed emissions (see Figure 1).

Over the next few years, assuming of course that the SOLAS f lash point issue has been resolved, the marine industry shall have access to a supply of low sulphur distillate from non-marine sources. One can argue that switching to low sulphur fuel automatically leads to lower SOx; however, this does not negate the need to measure exhaust emissions in order to demonstrate compliance when switching over from high sulphur to low sulphur fuel whilst operating in ECA zones. In addition, even though vessels operating on liquefied natural gas (LNG) emit 85% less NOx emissions, they still emit CH4 as methane slip emissions if after treatment is not employed.Therefore, it

Exhaust Emissions Monitoring

Fig. 1 Derivation of CF or Fuel to CO2 Conversion Factor Based on Fuel Carbon Content For Use in EEDI (MEPC.1/Circ.681)

Type of Fuel Reference Carbon Content

CF (t-CO2/t-Fuel)

Diesel/Gas Oil ISO 8217 Grades DMX through DMC 0.875 3.206000Light Fuel Oil (LFO) ISO 8217 Grades RMA through RMD 0.86 3.151040Heavy Fuel Oil (HFO) ISO 8217 Grades RME through RMK 0.85 3.114400Liquified Petroleum Gas (LPG) Propane 0.819 3.000000

Butane 0.827 3.030000Liquified Natural Gas (LNG) – 0.75 2.750000

Fig. 2 Excerpt of Table 2.14 of Climate Change 2007 from the Intergovernmental Panel on Climate Change (IPCC)

Industrial Designation or Common Name

Chemical Formula

Global Warming Potential for Given Time Horizon

20-yr 100-yr 500-yrCarbon dioxide CO2 1 1 1Methane CH4 72 25 7.6Nitrous oxide N2O 289 298 153Carbon monoxide CO – 1.9 –

Fig. 1 Derivation of CF or Fuel to CO2 Conversion Factor Based on Fuel Carbon Content For Use in EEDI (MEPC.1/Circ.681)

Type of Fuel Reference Carbon Content

CF (t-CO2/t-Fuel)

Diesel/Gas Oil ISO 8217 Grades DMX through DMC 0.875 3.206000Light Fuel Oil (LFO) ISO 8217 Grades RMA through RMD 0.86 3.151040Heavy Fuel Oil (HFO) ISO 8217 Grades RME through RMK 0.85 3.114400Liquified Petroleum Gas (LPG) Propane 0.819 3.000000

Butane 0.827 3.030000Liquified Natural Gas (LNG) – 0.75 2.750000

Fig. 2 Excerpt of Table 2.14 of Climate Change 2007 from the Intergovernmental Panel on Climate Change (IPCC)

Industrial Designation or Common Name

Chemical Formula

Global Warming Potential for Given Time Horizon

20-yr 100-yr 500-yrCarbon dioxide CO2 1 1 1Methane CH4 72 25 7.6Nitrous oxide N2O 289 298 153Carbon monoxide CO – 1.9 –

Figure 1: Derivation of CF or fuel to CO2 conversion factor based on fuel carbon content for use in EEDI (MEPC.1/Circ.681)

Figure 2: Excerpt of Table 2.14 of Climate Change 2007 from the Intergovernmental Panel on Climate Change (IPCC)

Liquefied Petroleum Gas (LPG)

Liquefied Natural Gas (LNG)

June / July 2012 bunkerspotwww.bunkerspot.com42

Robert Steen Kledal is the Managing Director of Wrist Ship Supply.Prior to joining Wrist Ship Supply in 2010, Kledal was a Senior Vice President with Maersk Line.