long term investment: investment regulation, financial...

TRANSCRIPT

___________________________________________________________________________

2017/FDM1/008 Session: 3

Long Term Investment: Investment Regulation, Financial Instruments, Risk Mitigation and Risk

Sharing Mechanisms

Purpose: Information Submitted by: Organisation for Economic Co-operation and

Development

Finance and Central Bank Deputies’ MeetingNha Trang, Viet Nam23-24 February 2017

1

LONG TERM INVESTMENT: INVESTMENT REGULATION, FINANCIAL

INSTRUMENTS, RISK MITIGATION AND RISK SHARING MECHANISMS

APEC FINANCE AND CENTRAL BANK DEPUTIES’ MEETING, 23-24 February 2017, Nha Trang, Viet Nam

André Laboul, Special Financial Advisor and Senior Counsellor, OECD

1. Attracting private sector capital through PPPs to deliver crucial infrastructure;

2. Mobilizing long-term financing for infrastructure, particularly through enhancing member-economies’ capacity for project preparation and developing capital markets and flexible financial instruments that would attract institutional investors;

3. Demonstrating the importance of and activating long-term vehicles to support long-term investment; and

4. Promoting inclusive infrastructure in urban development and for regional connectivity.

APEC Cebu Action Plan – Pillar IV

2

2

I. ADRESSING OBSTACLES RELATED TO THE ROLE OF INSTITUTIONAL INVESTORS (witha focus on regulation)

II. PROMOTING THE DIVERSIFICATION OF FINANCING INSTRUMENTS

III. ADDRESSING RISKS AND THE MEANS TO MITIGATE THEM

3

I. ADRESSING OBSTACLES RELATED TO THE ROLE OF INSTITUTIONAL INVESTORS(with a focus on regulation)

4

3

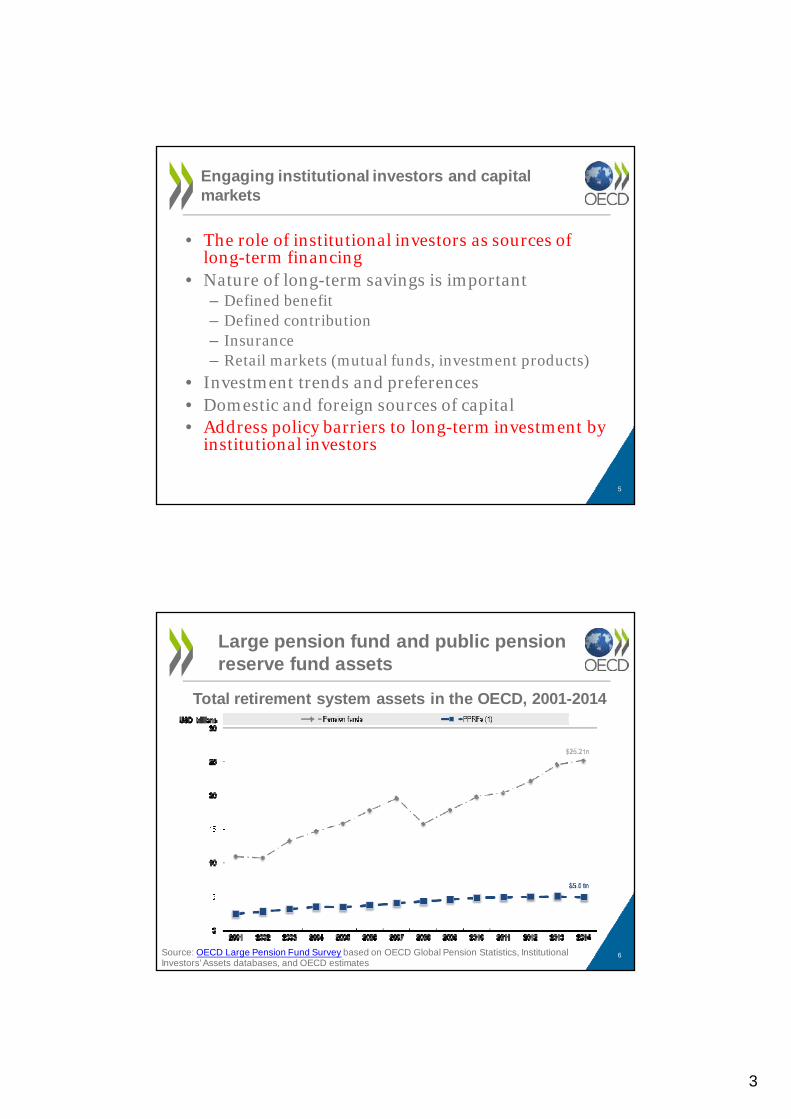

• The role of institutional investors as sources of long-term financing

• Nature of long-term savings is important– Defined benefit– Defined contribution– Insurance– Retail markets (mutual funds, investment products)

• Investment trends and preferences• Domestic and foreign sources of capital• Address policy barriers to long-term investment by

institutional investors

Engaging institutional investors and capital markets

5

Large pension fund and public pension reserve fund assets

Source: OECD Large Pension Fund Survey based on OECD Global Pension Statistics, Institutional Investors’ Assets databases, and OECD estimates

Total retirement system assets in the OECD, 2001-2014

6

4

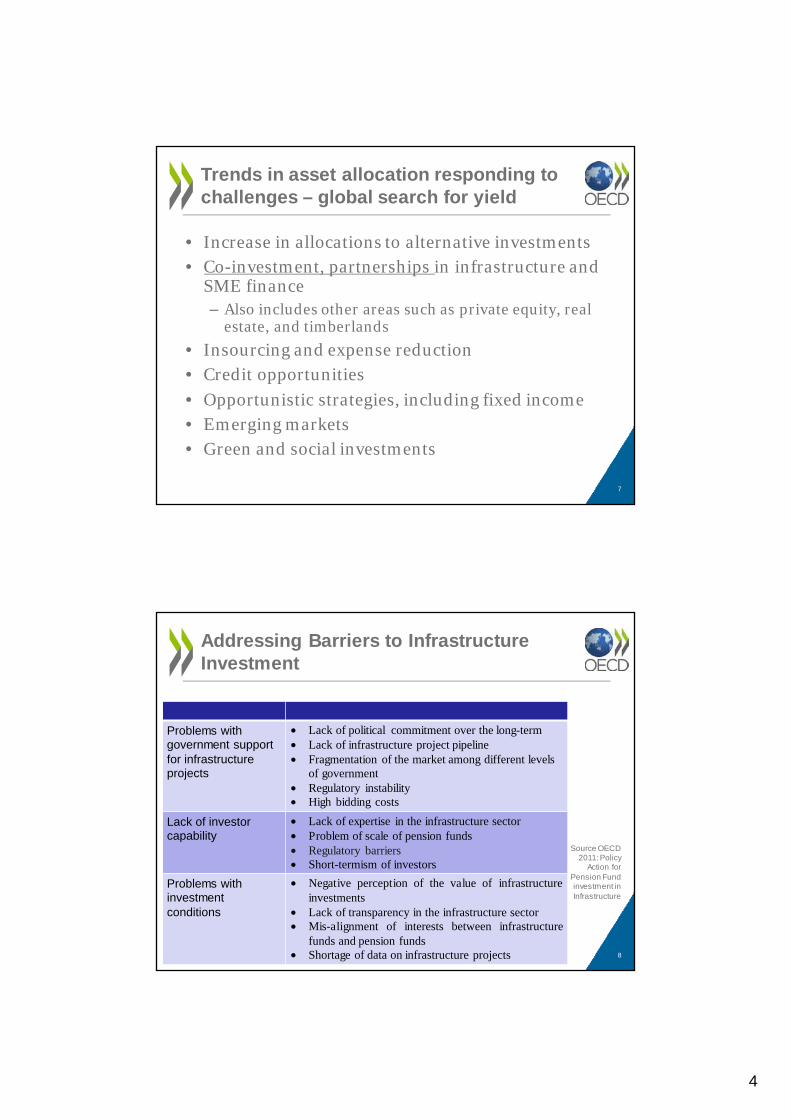

• Increase in allocations to alternative investments• Co-investment, partnerships in infrastructure and

SME finance– Also includes other areas such as private equity, real

estate, and timberlands

• Insourcing and expense reduction• Credit opportunities• Opportunistic strategies, including fixed income• Emerging markets• Green and social investments

Trends in asset allocation responding to challenges – global search for yield

7

Addressing Barriers to Infrastructure Investment

Source OECD 2011: Policy

Action for Pension Fund investment in Infrastructure

Problems with government support for infrastructure projects

• Lack of political commitment over the long-term• Lack of infrastructure project pipeline• Fragmentation of the market among different levels

of government• Regulatory instability• High bidding costs

Lack of investor capability

• Lack of expertise in the infrastructure sector• Problem of scale of pension funds• Regulatory barriers• Short-termism of investors

Problems with investment conditions

• Negative perception of the value of infrastructureinvestments

• Lack of transparency in the infrastructure sector• Mis-alignment of interests between infrastructure

funds and pension funds• Shortage of data on infrastructure projects 8

5

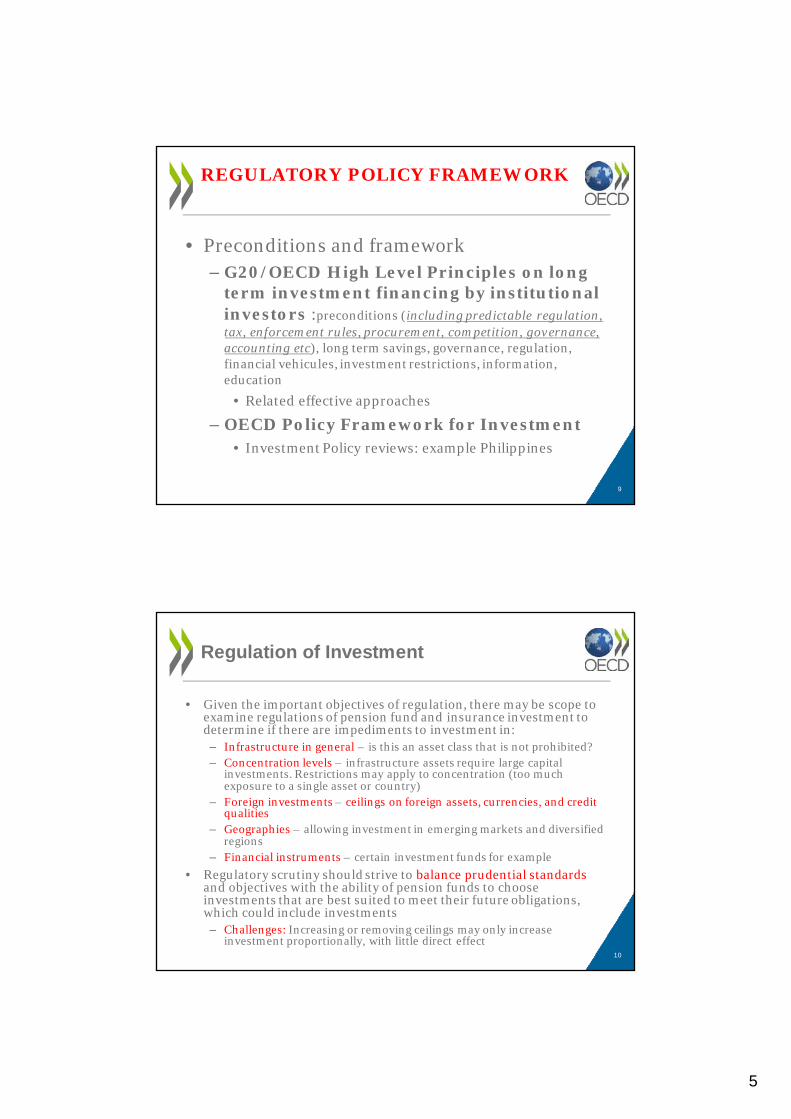

REGULATORY POLICY FRAMEWORK

• Preconditions and framework– G20/OECD High Level Principles on long

term investment financing by institutionalinvestors :preconditions (including predictable regulation, tax, enforcement rules, procurement, competition, governance, accounting etc), long term savings, governance, regulation, financial vehicules, investment restrictions, information, education

• Related effective approaches

– OECD Policy Framework for Investment• Investment Policy reviews: example Philippines

9

Regulation of Investment

• Given the important objectives of regulation, there may be scope to examine regulations of pension fund and insurance investment to determine if there are impediments to investment in:– Infrastructure in general – is this an asset class that is not prohibited?– Concentration levels – infrastructure assets require large capital

investments. Restrictions may apply to concentration (too much exposure to a single asset or country)

– Foreign investments – ceilings on foreign assets, currencies, and credit qualities

– Geographies – allowing investment in emerging markets and diversified regions

– Financial instruments – certain investment funds for example

• Regulatory scrutiny should strive to balance prudential standards and objectives with the ability of pension funds to choose investments that are best suited to meet their future obligations, which could include investments – Challenges: Increasing or removing ceilings may only increase

investment proportionally, with little direct effect10

6

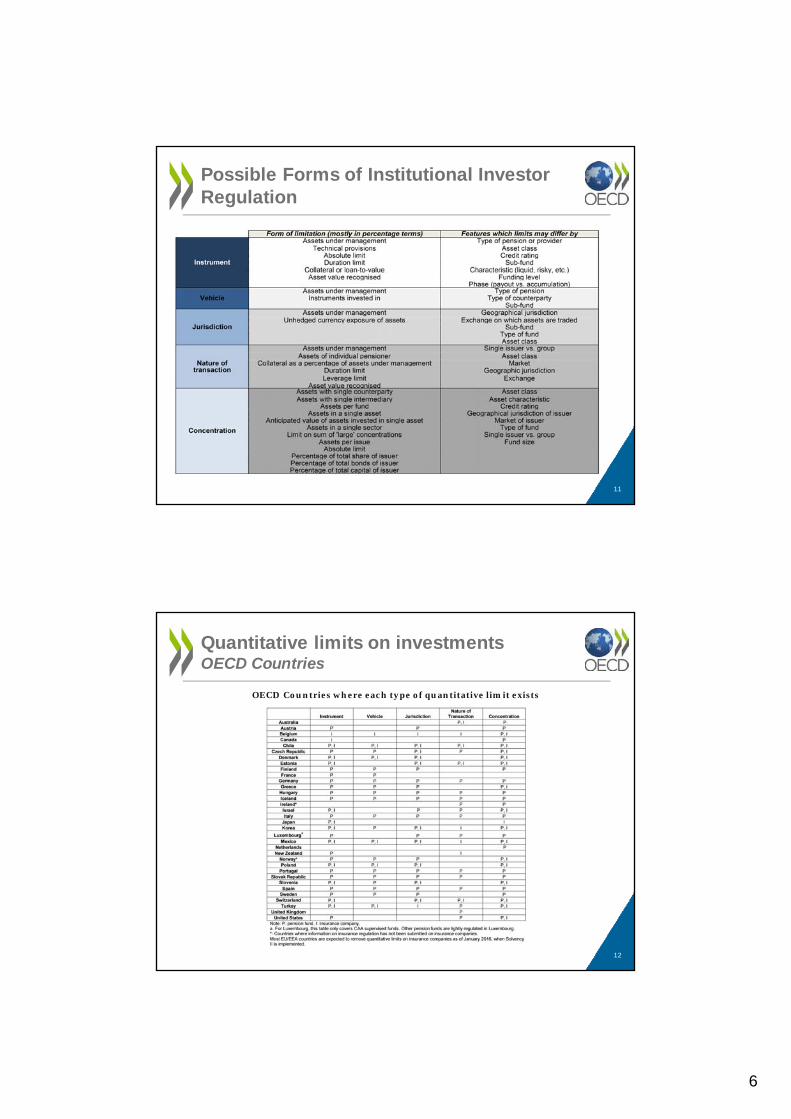

Possible Forms of Institutional Investor Regulation

11

Quantitative limits on investmentsOECD Countries

12

OECD Countries where each type of quantitative limit exists

7

13

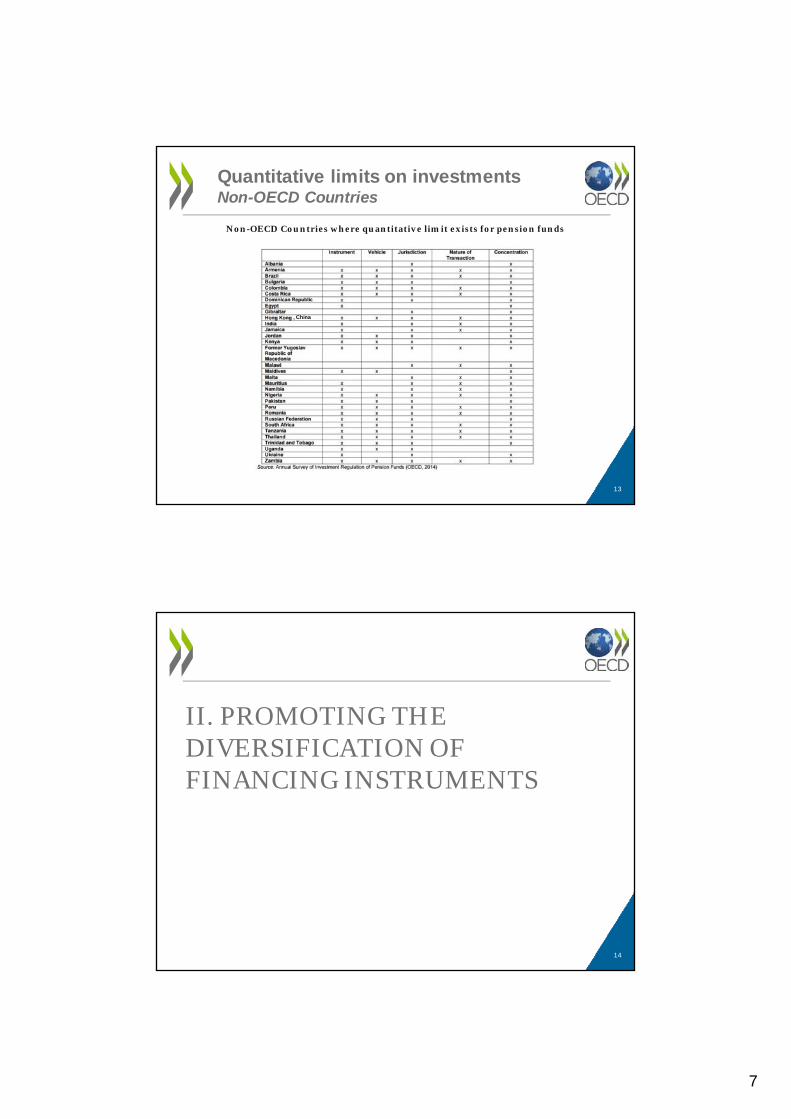

Non-OECD Countries where quantitative limit exists for pension funds

Quantitative limits on investmentsNon-OECD Countries

, China

II. PROMOTING THE DIVERSIFICATION OF FINANCING INSTRUMENTS

14

8

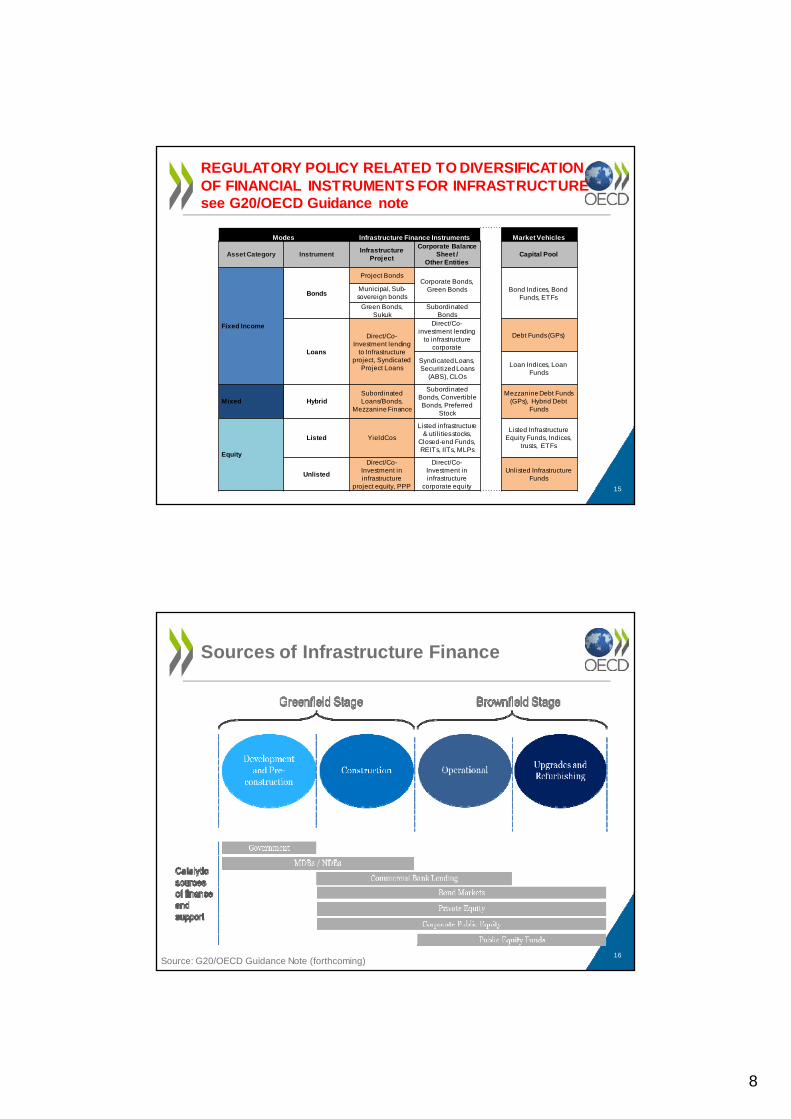

REGULATORY POLICY RELATED TO DIVERSIFICATION OF FINANCIAL INSTRUMENTS FOR INFRASTRUCTURE see G20/OECD Guidance note

15

Modes Infrastructure Finance Instruments Market Vehicles

Asset Category InstrumentInfrastructure

Project

Corporate Balance Sheet /

Other EntitiesCapital Pool

Fixed Income

Bonds

Project BondsCorporate Bonds,

Green Bonds Bond Indices, Bond Funds, ETFs

Municipal, Sub-sovereign bonds

Green Bonds, Sukuk

Subordinated Bonds

Loans

Direct/Co-Investment lending

to Infrastructure project, Syndicated

Project Loans

Direct/Co-investment lending

to infrastructure corporate

Debt Funds (GPs)

Syndicated Loans, Securitized Loans

(ABS), CLOs

Loan Indices, Loan Funds

Mixed HybridSubordinated Loans/Bonds,

Mezzanine Finance

Subordinated Bonds, Convertible Bonds, Preferred

Stock

Mezzanine Debt Funds (GPs), Hybrid Debt

Funds

Equity

Listed YieldCos

Listed infrastructure & util ities stocks,

Closed-end Funds, REITs, IITs, MLPs

Listed Infrastructure Equity Funds, Indices,

trusts, ETFs

Unlisted

Direct/Co-Investment in infrastructure

project equity, PPP

Direct/Co-Investment in infrastructure

corporate equity

Unlisted Infrastructure Funds

Sources of Infrastructure Finance

Source: G20/OECD Guidance Note (forthcoming)16

9

LINKS BETWEEN REGULATORY REFORMS

17

Infrastructure Finance Instruments

• PPPs can be useful instruments for projects where revenues are not certain or adequately provided through user fees

– Widely used across APEC member economies with examples in transportation, power, and telecommunication

• Examples: power plants in Thailand, Build-Operate-Transfer structures in Vietnam, high speed rail in Malaysia

– Some asset types such as airports, seaports, or renewable energy assets may be economically viable on a stand-alone basis

– Other models such as direct or indirect ownership through corporate structures or fund structures can be used

• Renewable energy finance, in this way, has been supported by long-term power purchase agreements

• Infrastructure finance could benefit from the use of flexible financing instruments

– Equity funds, investment platforms, listed equity trusts, could invest directly, or through SPVs and PPPs

• Certain APEC member economies would benefit from deepening domestic equity markets. Singapore, Malaysia, Thailand, Indonesia, and the Philippines have made progress

– The fund and investment platform model can also combine co-investment with commercial banks, insurance companies, and corporates, leveraging in-house expertise and skillsets while also mobilising a larger amount of capital

18

10

• Optimisation of capital structure• Efficient risk allocation to the party that is best able to manage risk• Commercial banks acting as co-investors; the formation of

syndicates– Banks as Mandated Lead Arrangers, crowding in institutional investors

• Promote the development of project infrastructure bonds to mobilise further financing by institutional investors– Deepen local corporate bond markets

• Government partnership in setting up funds• MDBs and credit enhancement, risk mitigation• MDBs and governments as co-investors• Blended finance

Linking Traditional Infrastructure Finance with Diversified Instruments and Techniques

19

PREAMBLE

Establish a strong legal and institutional framework that supports an efficient microeconomicenvironment, transparency, well-functioning capital markets and ensures regulatory certaintyand stability.

Promote the development of local currency capital markets (including equity, bonds andderivative markets), and their integration with their international counterparts.

Establish a national infrastructure roadmap and long term government strategy, develop arobust and transparent pipeline of investable infrastructure projects, and enhanceinfrastructure connectivity.

EXTRACT FROM G20/OECD GUIDANCE NOTE

20

11

I. DIVERSIFYING INSTRUMENTS AND OPTIMISING RISK ALLOCATION

• Promote cooperative, targeted and transparent risk allocation mechanisms amongst the various financialstakeholders active on the infrastructure spectrum, including MDBs and NDBs, banks, companies,institutional investors and governments, positioning the different actors depending on their risk profilesand institutional objectives and favouring joint actions, securitisation and balance sheet optimisation.

• Promote governmental support to innovative financial approaches, such as asset recycling, land valuecapture, special assessment districts, and tax increment financing.

• Encourage diverse channels of debt financing for infrastructure projects, in particular through non-bankchannels, including syndication of bank loans through capital markets, the development of a robustproject finance market, revival or innovative use of local currency infrastructure project bonds and of sub-sovereign bonds, securitisation and the formation of lending consortia. Promote the development ofalternative instruments for de-risked stagesof projects or hybrid investment vehicles.

• Encourage the formation of transparent and robust secondary market for infrastructure, and thedevelopment of specific products to improve access to capital market financing for infrastructure,including new vehicles to foster investor’s participation (equity or debt, public and private) ininfrastructure projects and recycling of capital through securitisation.

• Review the financing needs and instruments of small-scale infrastructure projects, which may be differentfrom large-scale infrastructure. Promote project pooling, social and development impact investmentinstruments, and building networks of investors with local authorities and partners.

EXTRACT FROM G20/OECD GUIDANCE NOTE

21

• II. EQUITY INSTRUMENTS FOR THE FINANCING OF INFRASTRUCTURE

• Facilitate the establishment of robust unlisted infrastructure equity markets. Review the ability of equityfunds to access infrastructure assets in the local market, including the suitability of greenfield assets forexisting business models, and also the local laws that govern such vehicles.

• Review the availability of qualifying assets for diverse listed equity instruments, including existing equitybusiness models such as Real Estate Investment Trusts (REITs), Master Limited Partnerships (MLPs), trustsand open- and closed-end funds.

• Encourage the formation of investment platforms and partnerships where government, NDBs and MDBscan leverage private sector investment.

• Review risk mitigation and incentives that especially encourage equity investment.

• Promote synergies between MDBs and NDBs and the broader equity market base, including through co-financing facilities, insurance pools, wider range of currency hedging tools, and asset securitisation.

• Review the efficiency of tax policies for infrastructure finance, noting the tax treatment of debt and equityin the capital structure.

EXTRACT FROM G20/OECD GUIDANCE NOTE

22

12

• III. ENGAGING INSTITUTIONAL INVESTORS AND CAPITAL MARKETS

• Foster collaborative mechanisms between investors and the creation of pooling of capital especially forsmaller investors and between investors and other stakeholders such as banks and MBDs and NDBs.

• Consider risk mitigation instruments and incentives specifically focused on investors in general, includingguarantees, coverage of political and regulatory risks, credit enhancements, and more diversifiedinsurance offerings, while ensuring their efficacy as well as taking due account of the impact on publicfinances.

• Review financial regulations that may potentially pose unintentional barriers to infrastructure investmentby institutional investors, taking into account prudential, investor protection, and overarching financialstability objectives.

• Bundling assets to reach relevant scale, appealing for institutional investors, including consortia of smallscale PPP projects.

EXTRACT FROM G20/OECD GUIDANCE NOTE

23

• IV. ADDRESSING THE INFORMATION GAP AND DEVELOPING INFRASTRUCTURE AS ANASSET CLASS

• Promote international infrastructure data collection, including with the consideration of atemplate for a preferred set of information to be collected (macro and micro level) andquantitative data on historical cash flows and performance at the project level andqualitative data covering project characteristics and sustainability issues.

• Promote standardisation and harmonisation of project documentation and of approaches toinfrastructure valuation and analysis.

• Consider a definition of sustainable and quality infrastructure investment to facilitate datacollection on sustainability and resilience factors in infrastructure investment.

• Support initiatives to create infrastructure benchmarks which will in turn help to describeinfrastructure as an asset class. Benchmarks should describe the investment characteristicsand properties of infrastructure debt and equity instruments, helping investors completetheir strategic asset allocation and liability benchmarking processes.

EXTRACT FROM G20/OECD GUIDANCE NOTE

24

13

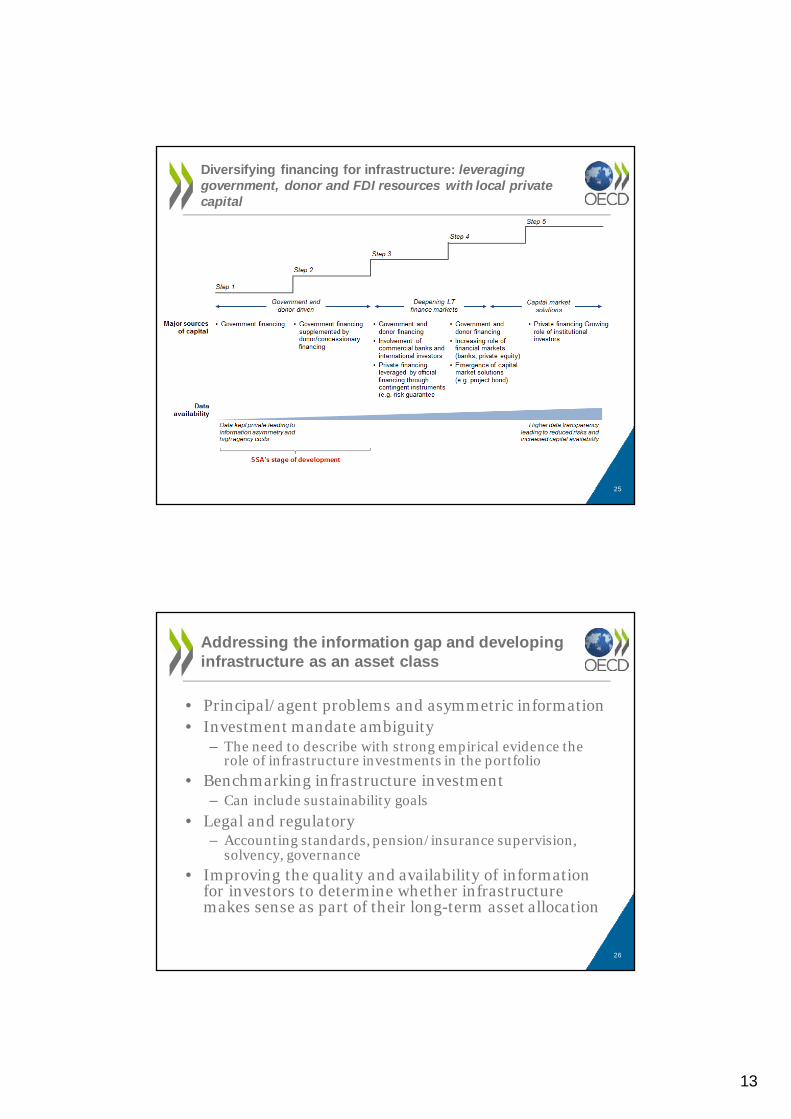

Diversifying financing for infrastructure: leveraging government, donor and FDI resources with local private capital

25

• Principal/agent problems and asymmetric information• Investment mandate ambiguity

– The need to describe with strong empirical evidence the role of infrastructure investments in the portfolio

• Benchmarking infrastructure investment– Can include sustainability goals

• Legal and regulatory– Accounting standards, pension/insurance supervision,

solvency, governance• Improving the quality and availability of information

for investors to determine whether infrastructure makes sense as part of their long-term asset allocation

Addressing the information gap and developing infrastructure as an asset class

26

14

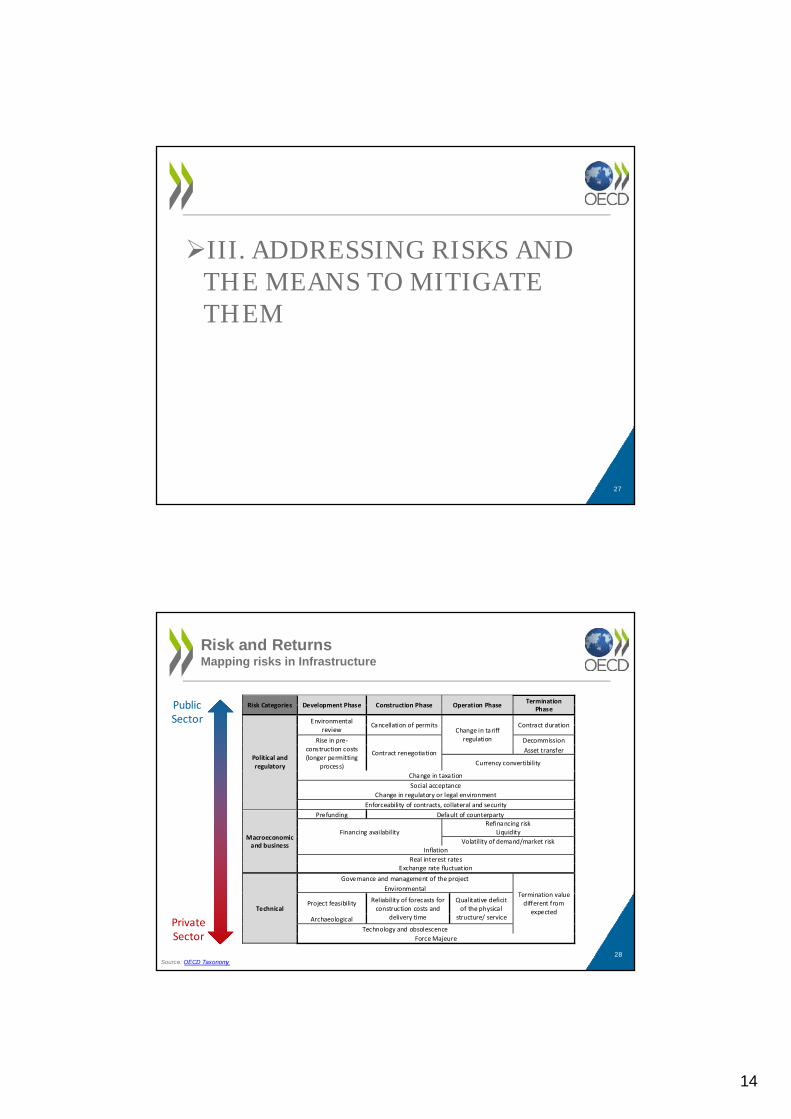

III. ADDRESSING RISKS AND THE MEANS TO MITIGATE THEM

27

Risk and ReturnsMapping risks in Infrastructure

28

Risk Categories Development Phase Construction Phase Operation Phase Termination Phase

Political and regulatory

Environmental review

Cancellation of permits Change in tariff

regulation

Contract duration

Rise in pre-construction costs (longer permitting

process)

Contract renegotiation

Decommission Asset transfer

Currency convertibility

Change in taxation Social acceptance

Change in regulatory or legal environment Enforceability of contracts, collateral and security

Macroeconomic and business

Prefunding Default of counterparty

Financing availability Refinancing risk

Liquidity Volatility of demand/market risk

Inflation Real interest rates

Exchange rate fluctuation

Technical

Governance and management of the project

Termination value different from

expected

Environmental

Project feasibility Reliability of forecasts for construction costs and

delivery time

Qualitative deficit of the physical

structure/ service Archaeological Technology and obsolescence

Force Majeure

Public Sector

Private Sector

Source: OECD Taxonomy

15

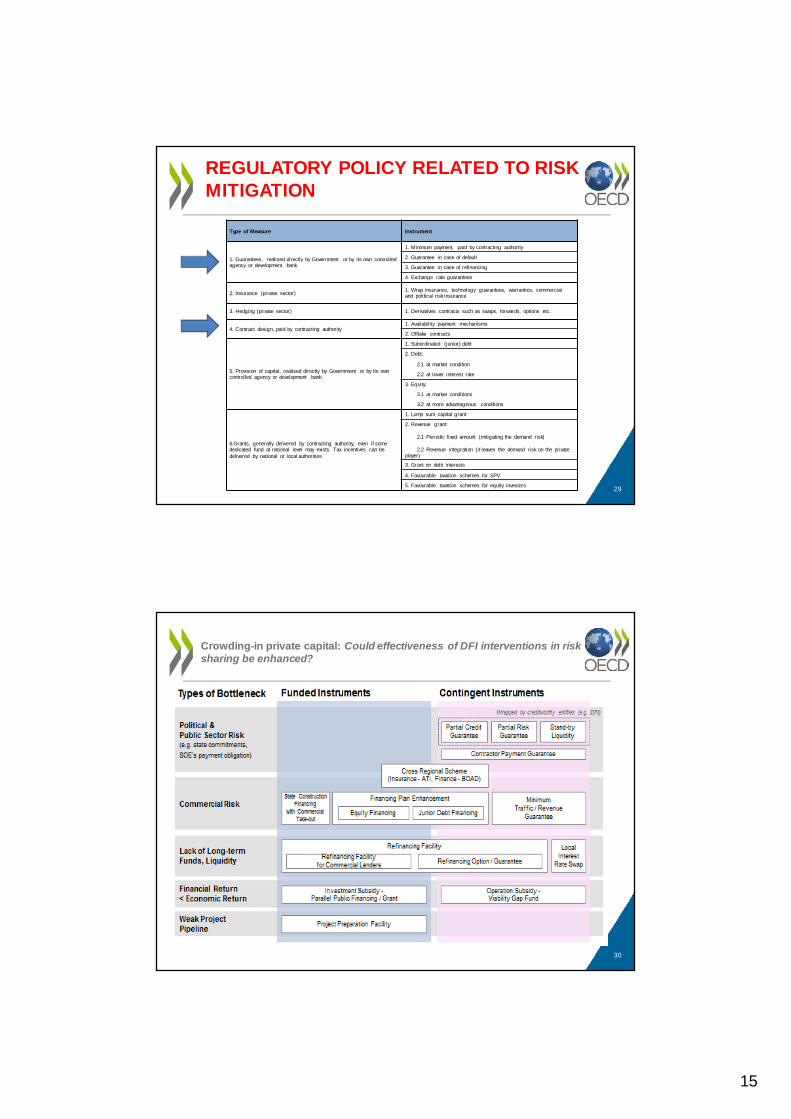

REGULATORY POLICY RELATED TO RISK MITIGATION

29

Type of Measure Instrument

1. Guarantees, realised directly by Government or by its own controlled agency or development bank

1. Minimum payment, paid by contracting authority

2. Guarantee in case of default

3. Guarantee in case of refinancing

4. Exchange rate guarantees

2. Insurance (private sector)1. Wrap insurance, technology guarantees, warranties, commercial and political risk insurance

3. Hedging (private sector) 1. Derivatives contracts such as swaps, forwards, options etc.

4. Contract design, paid by contracting authority1. Availability payment mechanisms

2. Offtake contracts

5. Provision of capital, realised directly by Government or by its own controlled agency or development bank

1. Subordinated (junior) debt

2. Debt:

2.1 at market condition

2.2 at lower interest rate

3. Equity:

3.1 at market conditions

3.2 at more advantageous conditions

6.Grants, generally delivered by contracting authority, even if some dedicated fund at national level may exists. Tax incentives can be delivered by national or local authorities

1. Lump sum capital grant

2. Revenue grant:

2.1 Periodic fixed amount (mitigating the demand risk)

2.2 Revenue integration (it leaves the demand risk on the private player)

3. Grant on debt interests

4. Favourable taxation schemes for SPV

5. Favourable taxation schemes for equity investors

Crowding-in private capital: Could effectiveness of DFI interventions in risk sharing be enhanced?

30

16

Risk Mitigation Instruments in ASEAN Member States

31

• Insurance, guarantees, credit enhancement are particularly important for access to debt financing and to mitigate political and regulatory risks

– Allows for longer tenors and lower cost of financing

– Covering political risks and contract risks• Example; Indonesia Infrastructure Guarantee Fund; bond guarantees in Malaysia

– Multilateral development banks as Lead Arrangers, providing credit enhancement– Supply of private sector insurance coverage varies across ASEAN

– Significant gaps remain in coverage in some countries, particularly for breach of contract and adverse regulatory changes

• Commercial risks related to construction, exchange rate, demand and counterparty risks constrain equity and debt financing

– Contractual arrangements can be an effective strategy for transferring and mitigating commercial risks

– In Malaysia, project companies increasingly bear traffic risk on toll roads, Indonesia and Philippines increasingly seeking to shift demand risk to project companies

– Joint ventures or alliances with local companies can also help to mitigate commercial risks

• Availability of foreign exchange risk mitigation instruments• Currency hedging or currency guarantees

Leveraging the role of MDBsby catalyzing private resources / more ‘bang for the buck’

• Leveraging MDBs’ balance sheets while maintaining their AAA rating

• Making portfolios of MDB assets available to private investors

– MDBs finance initial project development and sell project (brownfield) debt

• Reorientation of MDB asset-exposures

– moving from loans to risk-sharing;

– credit enhancement for project loans and bonds;

– guarantees for take-off agreements,

– targeted loan guarantees (for the construction phase)32