life insurance fraud-project

DESCRIPTION

life insurance fraud projectTRANSCRIPT

UNIVERSITY OF MUMBAI

PROJECT ON

“STUDY OF FRAUDS IN INSURANCE SECTOR”

BACHELOR OF COMMERCE

(BANKING & INSURANCE)

SEMESTER VI

(2013-2014)

SUBMITTED BY

LAXSHMI K. PASI

ROLL NO. -10741

PROJECT GUIDE

Prof. NANDINI JAGANNARAYAN

HINDI VIDYA PRACHAR SAMITI’S

RAMNIRANJAN JHUNJHUNWALA COLLEGE,

GHATKOPAR (WEST), MUMBAI-400 086.

1

“A FRAUDS IN INSURANCE SECTOR”

BACHELOR OF COMMERCE

(BANKING & INSURANCE)

SEMESTER VI

(2011-2012)

SUBMITTED

IN THE PARTIAL FULFILLMENT OF THE REQUIREMENTS

FOR THE AWARD OF DEGREE OF BACHELOR OF

COMMERCE- BANKING & INSURANCE

BY

VRUSHALI B. GHORPADE.

ROLL NO: - 9

HINDI VIDYA PRACHAR SAMITI’S

RAMNIRANJAN JHUNJHUNWALA COLLEGE

GHATKOPAR (WEST), MUMBAI-400086.

2

CERTIFICATE

THIS IS TO CERTIFY THAT Miss VRUSHALI B. GHORPADE OF B.COM.

BANKING & INSURANCE SEMESTER VI (2011-12) HAS SUCCESSFULLY

COMPLETED THE PROJECT ON “A FRAUDS IN INSURANCE SECTOR”

UNDER THE GUIDANCE OF Prof. NANDINI JAGANNARAYAN .

PRINCIPAL

(DR. USHA MUKUNDAN)

PROJECT GUIDE/ INTERNAL EXAMINER

(Prof. NANDINI JAGANNARAYAN)

EXTERNAL EXAMINER

DECLARATION

3

I, Miss VRUSHALI B. GHORPADE THE STUDENT OF B.COM. BANKING

& INSURANCE SEMESTER VI (2011-12) HEREBY DECLARES THAT I

HAVE COMPLETED THE PROJECT ON “A FRAUDS IN INSURANCE

SECTOR”

THE INFORMATION SUBMITTED IS TRUE AND ORIGINAL TO THE BEST

OF MY KNOWLEDGE.

SIGNATURE OF STUDENT

NAME OF THE STUDENT

VRUSHALI B. GHORPADE

ROLL NO. 9

ACKNOWLEDGEMENT

4

I would like to express my sincere gratitude to the almighty that has showered her

blessing on me without which this project would have not been possible.

I would also like to express my heartfelt gratitude to our principal Dr .USHA

MUKUNDAN, who has given me opportunity to conduct this study.

My guide Mrs. NANDINI JAGANNARAYAN also deserves sincere thanks that

has given me her guidance throughout the project and made it a success.

I would also like to thank our madam Mrs. LAKSHMI CHANDRASHEKRAN

who have cleared some of my doubts.

My parents have been a backbone to me in completing this project and my friends

who extended their constant support during my study also deserve heartfelt thanks.

INDEX

5

SR NO. CHAPTERS PAGE NO.

1 EXECUTIVE SUMMERY 8

2 SCOPE OF THE STUDY

3 INDIAN INSURANCE SECTOR 12

4 INSURANCE FRAUD 19

5 TYPES OF INSURANCE FRAUD 22

6 LIFE INSURANCE 29

7 FRAUD IN INSURANCE ON RISE

(SURVEY 2010-2011)

34

8 RISE IN THE NUMBER OF FRAUD CASES

IN LAST ONE YEAR

37

9 CLAIMS / SURRENDER RELATED FRAUD A

CONCERN FOR INSURERS

39

11 REAL EYES….. REALISE….. REAL LIES 43

12 AREAS THAT NEED MORE STRINGENT ANTI-

FRAUD REGULATION

44

13 TYPES OF FRAUD AFFECTING INSURANCE

COMPANIES

46

SR NO. CHAPTERS PAGE NO.

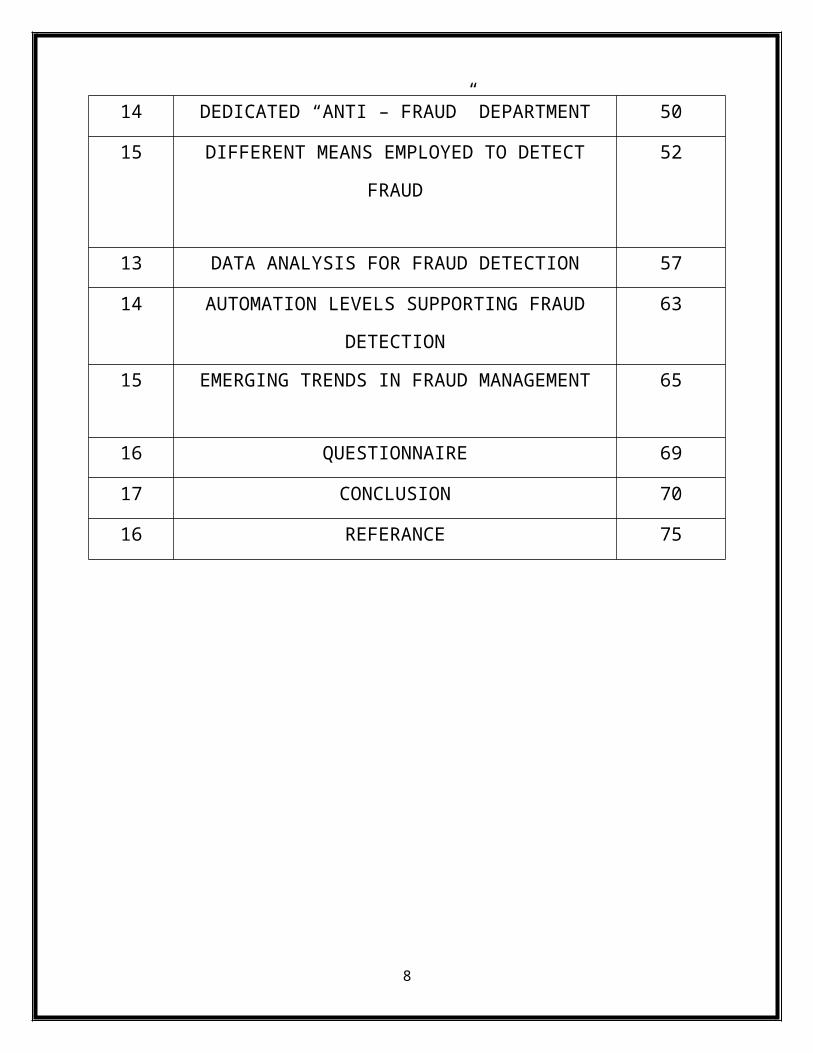

14 DEDICATED “ANTI – FRAUD” DEPARTMENT 50

6

15 DIFFERENT MEANS EMPLOYED TO DETECT

FRAUD

52

13 DATA ANALYSIS FOR FRAUD DETECTION 57

14 AUTOMATION LEVELS SUPPORTING FRAUD

DETECTION

63

15 EMERGING TRENDS IN FRAUD MANAGEMENT 65

16 QUESTIONNAIRE 69

17 CONCLUSION 70

16 REFERANCE 75

7

EXECUTIVE SUMMERY

India, one of the fastest growing economies in the world, has risen in the demand

for insurance products. Over the last 10 years, the insurance industry has grown at

a Capital Annual Compounded Growth rate (CAGR) of around 20%. However,

with the exponential growth in the industry, there has also been an increased

incidence of frauds in the country. Insurance fraud encompasses a wide range of

illicit practices and illegal acts involving intentional deception or

misrepresentation.

The industry has witnessed an increase in the number of fraud cases in the last one

year. Organizations are waking up to the fact that frauds are driving up the

overall costs of insurance and premiums for policy holders, which may there

often their viability and also have a bearing on their profitability.

Hence, companies need a more vigorous fraud management framework. Although

this survey focuses on retail insurance, frauds related to commercial insurance

claims and third-party claims are also on the rise. The sophistication of fraudsters

in the area of commercial insurance claims and third-part claims makes it all the

more difficult for organizations to detect and control fraud in time. Fraud impacts

organizations in several areas including financially, operationally and

physiologically.

8

OBJECTIVE OF THE STUDY

To study about frauds in insurance To examine the frauds taking place in insurance sector To study the profile of “life insurance corporation of India” and the frauds

taking place

SCOPE OF THE STUDY

Fraud impacts organizations in several areas including financially, operationally

and physiologically while the monitory loss can be staggering. Its loss of

reputation on an organization can be staggering. Its loss of reputation, goodwill

and customer relations can be devastating. As fraud can be perpetrated by any

employee within an organization or by those outside it, it is important for

companies to have an effective fraud management program in place to safeguard

their assets and reputation.

IMPORTANCE OF THE STUDY

Insurance premiums have increased due to false or exaggerated personal injury fraud claims, covering life, home, and motor and business accident policies. In some case claimants would suffer a genuine accident, but then exaggerating the injuries or the time of recovery amounts to an insurance fraud.

9

Functions of insurance fraud surveillance specialist:

As an investigator or surveillance specialist the insurance fraud surveillance officer should validate these claims.

It is foremost duty of insurance fraud surveillance to see that genuine claimants do not suffer at the same time ensuring that cheats are found out and punished.

As surveillance specialist who regularly conduct observations on claimants a true account of the claimants day to day activities are reported and at no time should it be advantageous or disadvantageous to the client or the subject.

Also during an investigation he should not create any circumstances which may encourage or enforce any person’s subject of an enquiry to engage in any activity which may be harmful to their interests and at all times he should perform his duties in a lawful and ethical manner.

It is imperative that he takes help of at least one more investigator when conducting mobile surveillance.

When operations are conducted with the purpose of assessing the capabilities of the subject it is vital that these are carried out in a discreet manner and by taking cognizance of the relevant legislation.

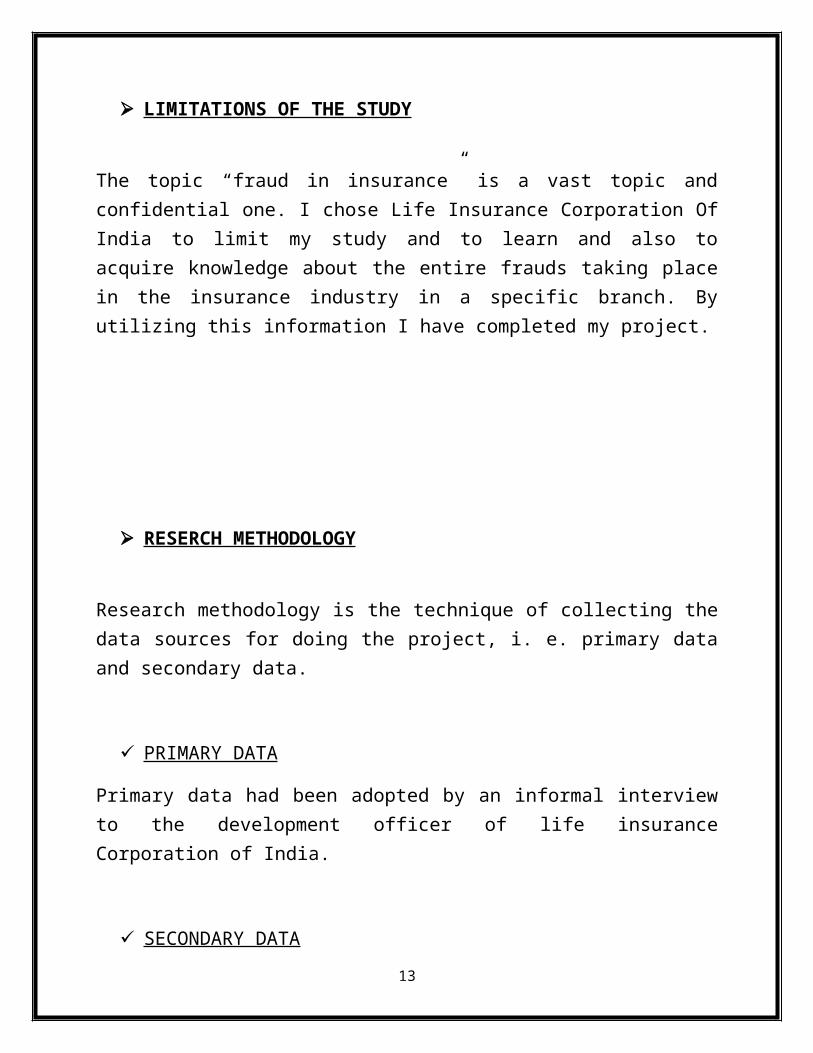

LIMITATIONS OF THE STUDY

The topic “fraud in insurance” is a vast topic and confidential one. I chose Life Insurance Corporation Of India to limit my study and to learn and also to acquire knowledge about the entire frauds taking place in the insurance industry in a specific branch. By utilizing this information I have completed my project.

10

RESERCH METHODOLOGY

Research methodology is the technique of collecting the data sources for doing the project, i. e. primary data and secondary data.

PRIMARY DATA

Primary data had been adopted by an informal interview to the development officer of life insurance Corporation of India.

SECONDARY DATA

Secondary data are adopted by collecting the information’s from different management books, websites of insurance sector and especially the LIC websites, journals and magazines and current news from newspapers, the names of secondary data has been specified in the Bibliography.

11

CHAPTER 1 - INDIAN INSURANCE SECTOR

INTRODUCTION

The Insurance sector in India governed by Insurance Act, 1938, the Life Insurance

Corporation Act, 1956 and General Insurance Business (Nationalisation) Act,

1972, Insurance Regulatory and Development Authority (IRDA) Act, 1999 and

other related Acts. With such a large population and the untapped market area of

this population Insurance happens to be a very big opportunity in India. Today it

stands as a business growing at the rate of 15-20 per cent annually. Together with

banking services, it adds about 7 per cent to the country’s GDP .In spite of all this

growth the statistics of the penetration of the insurance in the country is very poor.

Nearly 80% of Indian populations are without Life insurance cover and the Health

insurance. This is an indicator that growth potential for the insurance sector is

immense in India. It was due to this immense growth that the regulations were

introduced in the insurance sector.

Since then the insurance industry has gone through many sea changes .The

competition LIC started facing from these companies were threatening to the

existence of LIC .since the liberalization of the industry the insurance industry has

never looked back and today stand as the one of the most competitive and

exploring industry in India. The entry of the private players and the increased use

of the new distribution are in the limelight today. The use of new distribution

techniques and the IT tools has increased the scope of the industry in the longer

run.

12

SOME AREAS OF FUTURE GROWTH

LIFE INSURANCE

The traditional life insurance business for the LIC has been a little more than a

savings policy. Term life (where the insurance company pays a predetermined

amount if the policyholder dies within a given time but it pays nothing if the

policyholder does not die) has accounted for less than 2% of the insurance

premium of the LIC (Mitra and Kayak, 2001). For the new life insurance

companies, term life policies would be the main line of business.

HEALTH INSURANCE

Health insurance expenditure in India is roughly 6% of GDP, much higher than

most other countries with the same level of economic development. Of that, 4.7%

is private and the rest is public. What is even more striking is that 4.5% are out of

pocket expenditure (Berman, 1996). There has been an almost total failure of the

public health care system in India. This creates an opportunity for the new

insurance companies. Thus, private insurance companies will be able to sell health

insurance to a vast number of families who would like to have health care cover

but do not have it.

PENSION

The pension system in India is in its infancy. There are generally three forms of

plans: provident funds, gratuities and pension funds. Most of the pension schemes

are confined to government employees (and some large companies). The vast

majority of workers are in the informal sector. As a result, most workers do not

13

have any retirement benefits to fall back on after retirement. Total assets of all the

pension plans in India amount to less than (USD) 40 billion.

Therefore, there is a huge scope for the development of pension funds in India. The

finance minister of India has repeatedly asserted that a Latin American style

reform of the privatized pension system in India would be welcome (Roy, 1997).

Given all the pros and cons, it is not clear whether such a wholesale privatization

would really benefit India or not (Sinha, 2000).

14

PRESENT SCENARIO OF INSURANCE INDUSTRY

India with about 200 million middle class household shows a huge untapped

potential for players in the insurance industry. The insurance sector in India

has come to a position of very high potential and competitiveness in the

market. Indians, have always seen life insurance as a tax saving device, are

now suddenly turning to the private sector that are providing them new

products and variety for their choice.

Consumers remain the most important Centre of the insurance sector. After

the entry of the foreign players the industry is seeing a lot of competition

and thus improvement of the customer service in the industry.

Computerization of operations and updating of technology has become

imperative in the current scenario. Foreign players are bringing in

international best practices in service through use of latest technologies

The insurance agents still remain the main source through which insurance

products are sold. The concept is very well established in the country like

India but still the increasing use of other sources is imperative. At present

the distribution channels that are available in the market are listed below.

Direct selling

Corporate agents

Group selling

Brokers and cooperative societies

Bancassurance

15

Customers have tremendous choice from a large variety of products from

pure term (risk) insurance to unit-linked investment products. Customers are

offered unbundled products with a variety of benefits as riders from which

they can choose. More customers are buying products and services based on

their true needs and not just traditional money back policies, which is not

considered very appropriate for long-term protection and savings. There is

lots of saving and investment plans in the market. However, there are still

some key new products yet to be introduced - e.g. health products.

The rural consumer is now exhibiting an increasing propensity for insurance

products. A research conducted exhibited that the rural consumers are

willing to rule out anything between Rs 3,500 and Rs 2,900 as premium

each year. In the insurance the awareness level for life insurance is the

highest in rural India, but the consumers are also aware about motor,

accidents and cattle insurance. In a study conducted by MART the results

showed that nearly one third said that they had purchased some kind of

insurance with the maximum penetration skewed in favor of life insurance.

The study also pointed out the private companies have huge task to play in

creating awareness and credibility among the rural populace. The perceived

benefits of buying a life policy range from security of income bulk return in

future, daughter's marriage, children's education and good return on savings,

in that order, the study adds.

16

REPORT HIGHTLIGHT

Gains of liberalization in Indian insurance sector. Indian insurance market segmentation by products. Size of the market and market share of life insurers, in INR (crore). Market share of non – life insurers. Forecast of life insurance growth up to 2012. Forecast of non-life insurance growth up to 2012. Market revenue of both public and private insurers. Policies and measures taken by IRDA to develop the insurance market. Research and development activities. Regulation of insurance and reinsurance companies. Major challenges that Indian insurance sector is facing. Profiles of the major players.

CHAPTER 2 - INSURANCE FRAUDS

17

Fraud occurs when someone knowingly lies to obtain some benefit or advantage to

which they are not otherwise entitled or someone knowingly denies some benefit

that is due and to which someone is entitled. Depending on the specific issues

involved, an alleged wrongful act may be handled as an administrative action by

the Department or the Fraud Division may handle it as a criminal matter.

Insurance fraud is any act committed with the intent to fraudulently obtain

payment from an insurer. Insurance fraud has existed ever since the beginning of

insurance as a commercial enterprise. Fraudulent claims account for a significant

portion of all claims received by insurers, and cost billions of dollars annually.

Types of insurance fraud are very diverse, and occur in all areas of insurance.

Insurance crimes also range in severity, from slightly exaggerating claims to

deliberately causing accidents or damage. Fraudulent activities also affect the lives

of innocent people, both directly through accidental or purposeful injury or

damage, and indirectly as these crimes cause insurance premiums to be higher.

Insurance fraud poses a very significant problem, and governments and other

organizations are making efforts to deter such activities.

CAUSES

The “chief motive in all insurance crimes is financial profit.” Insurance contracts

provide both the insured and the insurer with opportunities for exploitation. One

18

reason that this opportunity arises is in the case of over-insurance, when the

amount insured is greater than the actual value of the property insured. This

condition can be very difficult to avoid, especially since an insurance provider

might sometimes encourage it in order to obtain greater profits. This allows

fraudsters to make profits by destroying their property because the payment they

receive from their insurers is of greater value than the property they destroy.

Insurance companies are also susceptible to fraud because false insurance claims

can be made to appear like ordinary claims. This allows fraudsters to file claims for

damages that never occurred, and so obtain payment with little or no initial cost.

The most common form of insurance fraud is inflating of loss.

TYPES OF INSURANCE FRAUD

Insurance fraud can be classified as either hard fraud or soft fraud.

1) HARD FRAUD

Hard fraud includes someone staging a car accident, injury, arson, loss, break-in, or

someone writing false bills to Medicare to illegally receive money from their

insurance companies. This type of fraud often receives more media attention and

it’s easier to detect. Hard fraud often involves criminal activity and the intention of

squeezing millions of dollars out of insurance companies. But, the average person

can also be found guilty of hard fraud.

2) SOFT FRAUD

Soft fraud, which is far more common than hard fraud, is sometimes also referred

to as opportunistic fraud. This type of fraud consists of policyholders exaggerating

otherwise legitimate claims. Worker’s compensation claims is the most frequent

and expensive type of soft fraud. It costs insurance companies millions of dollars a

year. As a result, insurance premiums are rising. Yet, approximately up to one-

19

third of consumers don’t see anything wrong with employees receiving worker’s

compensation benefits even if they are healthy enough to go back to work.

For example, when involved in a collision an insured person might claim more

damage than was really done to his or her car. Soft fraud can also occur when,

while obtaining a new insurance policy, an individual misreports previous or

existing conditions in order to obtain a lower premium on their insurance policy.

TYPES OF LIFE INSURANCE FRAUD

Whether we are a policyholder or a shareholder in an insurance company,

insurance fraud affects us. The field of insurance is wide and fraud exists in every

area. Therefore, there is a need to study the most important types of insurance –

life insurance and major types of life insurance fraud and how they affect bottom

line.

Insurance fraud comes in two main categories

1. seller fraud

Seller fraud occurs when the seller of a policy hijacks the usual

process, in a way that maximizes his or her profit.

TYPES OF SELLER FRAUD

There are many variations of seller fraud, but they all center around four basic

types. These are:

1. GHOST COMPANIES

In the ghost company scenario, policies are issued and premiums accepted from

policyholders, but the company underwriting the policy isn't legitimate and

often doesn't exist. These outright frauds are a type of boiler room operation,

where a team of high-pressure scam artists dial likely victims to sell them false

policies. Unfortunately, the fraud isn't usually discovered until someone tries to

20

file a claim on the policy their family member thought was in effect, in the

event of his or her death.

2. PREMIUM THEFT

The premium theft scenario is when the insurance rep accepts premiums, but

doesn't submit them to the company underwriting the policy, thus invalidating

the policy. In this case, the agent essentially pockets the money. Premium theft

has become less of an issue as more companies have moved towards direct

deposit models, but it is still possible in some cases.

3. CHURNING

Churning refers to a situation where the insurance rep advises the customer to

cancel, renew and open new policies in a way that is beneficial to him or her,

instead of beneficial to the client. This type of insurance fraud often targets

seniors and is driven by the agent's desire for larger commissions. Churning

keeps a portfolio constantly in flux, with the primary purpose of lining the

advisor's pockets.

4. OVER OR UNDER COVERAGE

Similar to churning, under or over coverage occurs when an insurance rep

convinces customers to buy coverage they don't need, or sells a lesser policy

and represents it as a complete policy. In either case, the rep is trying to

maximize commissions and ensure the sale, rather than focusing on meeting the

client's needs.

2. Buyer fraud.

Buyer fraud occurs when the buyer bends the process to obtain more

coverage, or claim more cash, than he or she is rightly entitled to.

TYPES OF BUYER FRAUD

21

Buyer fraud also comes in a number of different flavors, but they all center on a

theme of dishonesty. Basic types of buyer fraud include:

1. POST-DATED LIFE INSURANCE

Post-dated life insurance refers to a policy that has been arranged after the death

of the person being insured, but appears to have been issued before death. This

type of fraud is usually carried out with the help of an insurance agent. It is also

one of the easier types of fraud for insurance companies to detect, because

record keeping has become more stringent.

2. FALSE MEDICAL HISTORY

Falsifying medical history is one of the most common types of insurance fraud.

By omitting details such as a smoking habit or a pre-existing condition, the

buyer hopes to get the insurance policy for cheaper than he or she would have

otherwise been able.

3. MURDER FOR PROCEEDS

There are two versions of the murder for proceeds fraud. In the first, the insured

doesn't know they are insured and are understandably surprised to be murdered.

In the second, the policy is legitimate and was taken out in better times,

however, financial hardships lead the perpetrator to decide that killing his or her

spouse/family member/business partner, for the money, is the best way out of

the problem.

4. LACK OF INSURABLE INTEREST

As with murder for proceeds, insuring people you shouldn't be insuring, in

hopes that they will die, constitutes fraud. Insurance is founded on the idea of

protecting people from financial loss, so using it to gamble on lives for a

financial gain is a perversion of the system. This includes vertical settlements,

22

which combine non-insurable interest with falsified policies taken out on the

terminally ill.

5. SUICIDAL ACCIDENT

Just as financial hardship can lead otherwise rational people towards murder,

the same factors can lead people to commit suicide in a way so it looks

accidental. This constitutes fraud in that it is an intentional act for the purpose

of collecting the insurance proceeds, and would not have occurred if those

proceeds did not exist. This can be a very difficult one to detect, as the medical

examiner has final say in accidental death. Even if it is clearly a suicide, the

claim centers on the state of mind, rational or not, at the time of suicide.

6. FAKING DEATH OR DISABILITY

Many life insurance policies have riders for disability, creating the temptation

to fake one to get the payout. However, some people take it a step further and

fake their own deaths. In both cases, the fraudster has to deal with the

possibility of being discovered through an investigation.

This is just one of the case that life insurance come across involving forgery of

death certificate, medical reports, etc. with the attempt to avail of claim from the

company. According to survey by India forensic research, a MUMBAI based

research agency, life insurance frauds are the most prevalent after the motor and

health insurance.

Life insurance is a long term contract between a policyholder and an insurer, which

assures the policyholder’s family / dependents’ a certain amount of money in the

case of the death of the policyholder.

HINTS FOR LIFE INSURANCE FRAUD

It is important to remember that the hints listed below are merely possible “red flags” that they may be some evidence consistent with an insurance fraud schemes.

23

Any one or two of these by themselves may not raise your suspicion; however when you have several of these hints person or a pattern begins to emerge, you should investigate further or forward your suspicion to the insurance fraud prevention decision.

The policy’s effective date is close to the date of death. The deceased is not well known by relatives and lived alone. Policies tend to be for small coverage which is many times available in mass

offerings, i.e. in magazines, mal- in and television and advertisement. The agents “loss ratios” appear unusually skewed, considering the size of the

market and types of people insured. Policies requiring physical examinations are almost never used in these

schemes. Numerous life insurance policies were purchased on the victim. Different carries were used in securing coverage for no apparent reason. The coverage amount is not commensurate with the social position of the

deceased; e.g. a loss income clerical worker has a life insurance estate of millions.

An unusually large number of death certificates ewer obtained by the beneficiary.

SOME OF THE COMMON FRAUDULENT ACTIVITIES ARE:-

1. AGE PROOF :-

All insurance policies have an eligible age at which the policy can be taken. To

accommodate oneself into the product or enjoy a minimum premium, age proofs

are modified to show a reduced age.

2. ADDRESS PROOF :-

Many issuers accept bank projects have a valid address proof. But these are often

victim of manipulation to show a reduced age.

3. MEDICAL TESTS :-

Some cases require medical tests to issue the policy. However, to substantiate not

disclosed or miss presented medical conditions, a different person may be sent at

24

the time of the tests. While this may help to get the policy, it would create

discrepancy at the time of claims, even leading to reputation.

4. FABRICATING DATE OF DEATH :-

The benefit of keeping your policy in force by paying regular premiums cannot be

understated. Not doing so, results in the policy to lapse and becoming illegible to

avail the death benefit on the policy. However cases have been seen where the date

of death as on the death certificate has been fraudulently change to a death before

the actual death when the policy was in force, so as to register claim.

5. FORGERY OF DEATH CERTIFICATE :-

To avail the death certificate, a false death benefited, a small death certificate is

created on the name of living person.

6. MANIPULATING REASON OF DEATH :-

If a history of an aliment which has been diagnosed before or at the time of filling

the proposal is deducted, the claim can be repudiated. To safeguard oneself from

this situation, the reasons of death are modified so as to fabricate a genuine claim.

Some of the frauds pertaining to age proofs, address proofs can be detected at the

underwriting stage, while others may be detected during the policy term or at the

time processing the claim. If detected at the underwriting stage, the proposal form

is rejected and policy is not issued. If detected midterm, the policy can be

cancelled.There are various factors which trigger suspicion and hence an

investigation on fraudulent claims. The income / occupation details furnished at

issuance stage and actual fraud at investigation stage, pattern of issuance coverage

availed i .e. at what age did customer started buying and within what span of time

how much coverage was bought, time of death, medical case sheets, comments on

postmortem report and co-relating the various sources of information often help to

smell a wrong doing.

25

Frauds in life insurance occurs mainly due to:-

Fabrication of documents to save on premiums.

Avail covers which are not allowed for a particular age group.

Obtain the death benefit through the unfair means.

Some extreme cases have also found to involve murder by kin for monetary

benefit.

THE COST OF INSURANCE FRAUD

Just as there are two main types of life insurance fraud, there are also two

consequences. When people engage in buyer fraud, it raises the cost of insurance.

The reason for this is very simple; insurance companies are really good at

modeling, so they tweak their models to account for buyer fraud and then spread

that cost across all their policyholders. In a very real way, every person who tries

to stick it to the insurance company ultimately makes your policy cost more.

In contrast, seller fraud can potentially hurt just the select few that experience it. It

is, in every essence of the word, bad luck. However, on the whole, every time the

insurance company you invest in treats someone badly, it loses business to a

company with a better reputation and controls on the agents. As an investor, you

will be tempted to move your capital to the better performing company, thus

punishing seller fraud in a roundabout way. The internet has also helped reduce

seller fraud, as many shady outfits and practices become exposed sooner in the

game. Insurance is a business that is built on risk analysis and probabilities. Every

instance of insurance fraud puts pressure on the business, whether seller or buyer

fraud. For this reason, many companies build generous contingency funds to

protect them against fraud, as well as other unforeseen events. While this is good

from the investor's perspective, it does unfortunately lead to your personal life

insurance premiums being higher than they otherwise would have been, in a more

honest world.

26

27

CHAPTER 5 - FRAUD IN INSURANCE ON RISE

India is one of the fastest growing economies among BRIC countries, and so is the

case with the country’s insurance sector. LIFE INSURANCE CORPORATION

OF INDIA has conducted the Insurance Fraud Survey to assess the fraud scenario,

the potential risk exposure, the economic impact and the industry practices to

counter fraud risk.

The significant role fraud plays in negatively affecting the insurance sector is often

under-reported or discounted. It is a general consensus in the market that fraud

cases have significantly increased in the last one year. Claims / surrender related

fraud is the biggest concern for insurance companies, and the majority of

respondents feel that more anti-fraud regulations are the need of the hour. Fraud

risk in insurance is a complex matter, which affects both the parties — insurers as

well as policyholders. Frauds increase the cost of insurance, resulting in insurers

losing to their competitors, and at the same time, policyholders paying higher

premiums.

There have been increased incidences of fraud over the last one year.

Fraud risk exposure from claims or surrender is a major concern area for

industry players. They have emphasized the need for increased anti-fraud

regulations in the area of claims management.

Frauds are driving up overall costs for insurers and premiums for

policyholders.

28

There is a need for a more rebuts data analytics tools to effectively

detect red flags.

It’s imperative to screen all the key vendors.

Fraud risk poses a very big challenge for the insurance sector. Business leaders are

aware of the need to address this risk, but the lack of a comprehensive and

integrated approach to fraud risk management continues to be a concern. The

increasing number of frauds and the growing degree of risk necessitates that

insurance companies regularly review their policies, build in checks and use new

and advanced technology to avoid such issues. However, no system can be

foolproof, but a proactive and dynamic approach can make a company ready to

counter fraudsters and gain an edge over its competitors. As India’s insurance

industry matures, fraud risk management is going to be a major concern for

insurers and business leaders. Insurers will need to continuously reassess their

processes and policies to manage and mitigate the risk of fraud. Fraud risk in the

insurance value chain can emanate from internal and external factors.

The risk of employee’s misusing confidential information and colluding with

fraudsters is on the rise and insurers will need to put in place internal checks and

balances to minimize such issues.

External fraud risk can arise at various stages, e.g., registration of clients,

underwriting, reinsurance and the claims process. The severity of fraud can range

from a slight exaggeration to deliberately causing loss of insured assets. The

essential components of fraud are the intent to deceive and the desire to induce an

organization to pay more than it otherwise would.

Fraud detection and management should be a proactive process, which

includes identification of suspicious claims that have a high possibility of

being fraudulent, through a computerized statistical analysis. Approximately

29

8% of life high value policies to monitor and investigate fraud risk, which

mitigates such risks to a large extent. Insurers need to put in place fraud

investigation teams (with the right credentials) that work in tandem with law

enforcement agencies to weed out fraudulent claims. It is also important for

the industry to build a shared or centralized database to share information

related to frauds.

THE THREE BROAD CATEGORIES OF FRAUD ARE:-

POLICY HOLDER AND CLAIMS FRAUD: fraud against insurer by

policyholder and / or other parties in the purchase and / or execution of an

insurance product.

INTERMEDIARY FRAUD: - frauds by intermediaries against insurer

and / or policyholders.

INTERNAL FRAUD: - fraud against insurer by employee on his / her own

volition or in collusion with parties that are internal or external to insurer.

The CBI registered a case against the Divisional Manager of the company

for allegedly collecting money from customers and issuing cover notes to

them, but neither the money nor the cover note was deposited with the

Insurance Company.

A former employee of one of the biggest private life insurance companies

allegedly cheated the company’s customers by issuing fake receipts

Insurance companies have five key areas of risk exposure. These are related to –

Claims or surrender

Premiums

Applications

Employee-related fraud

Vendor-related third party fraud

30

In the business of general insurance, a large number of frauds occur in health

insurance, and these pertain to overstating of claims or involve the manipulation of

the documents of non-existing hospitals, pharmacies, etc., or to cover up

nondisclosure of facts at the proposal stage. It has been observed that there are a

higher number of fraudulent cases in the case of hospitalization benefits and

personal accident policies. According to an Indian association, “Out of the total

outgoings in health insurance, nearly 25% are fraudulent claims.”

CHAPTER 9 - REAL EYES...REALIZE...REAL LIES…

Short History of Antifraud Efforts

31

Fraud in insurance has undoubtedly existed the industry’s beginnings in the seventeenth century, but it received little attention until the 1980s because l aw enforcement agenc ies had o ther p r io r i t i es and were reluctant to provide the training needed to investigate and prosecute cases of insurance fraud. And, given the fine line between investigating suspicious claims and harassing legitimate claimants, some insurers were afraid that a concerted effort to eradicate fraud might be perceived as an t i - c o n s u m e r m o v e . I n a d d i t i o n t h e n e e d t o c o m p l y w i t h t h e t i m e requirements for Paying claims imposed by fair claim practice regulations i n m a n y s t a t e s m a d e i t d i f f i c u l t t o a d e q u a t e l y i n v e s t i g a t e s u s p i c i o u s claims. But by the mid-1980s the rising price of insurance, particularly auto and h e a l t h i n s u r a n c e t o g e t h e r w i t h t h e g r o w t h i n f r a u d c o m m i t t e d b y organ ized c r imina l s , p rompted many insure r s to r eexamine the i s sue .

Gradually, insurers began to see the benefit of strengthening antifraud laws and more stringent enforcement as a means of controlling escalating cos t s — a pro-consumer move — and they found ready a l l i es among those who been adversely affected by fraud. These included consumers, who were paying for fraud through their insurance premiums; the people used by organized fraud groups to file false claims, often the poor, who s o m e t i m e s f o u n d t h e m s e l v e s o n t h e w r o n g s i d e o f t h e l a w ; a n d chiropractors and other medical professionals who were concerned that t h e i r r e p u t a t i o n a s a g r o u p w a s b e i n g t a r n i s h e d b y o r g a n i z e d f r a u d ringleaders who had recruited their members to make fraudulent claims for treatment.

32

CHAPTER 8 - AREAS THAT NEED MORE STRINGENT ANTI- FRAUD

REGULATION

Fraud risk arising from claims or surrender being the key concern for most

insurance companies calls for more stringent regulations. If claims-related frauds

can be detected in time, it can help insurers save significantly cost. The survey

indicates that almost one out of every two respondents feel that more strict anti-

fraud regulations are needed for effective and transparent claims or surrender

management.

It is estimated that India’s health insurance sector is losing around INR10 billion

on false claims every year. Apart from depleting the financial resources of

insurance company’s fraudulent claims or surrender also affect policy holders

33

Adversely, since the latter have to pay higher premiums for insurance products.

The respondents emphasized on the urgency of preventing fraudulent claims or

surrender to plug revenue losses.

As claims or surrender is prone to fraud or value inflation handling of claims or

surrender affects the long-term Sustainability of a company’s profits. To manage

fraud, companies can adopt a hybrid approach to detection, using a Combination of

profiling rules to filter fraudulent transactions with advanced analytics software.

Some measures taken by general insurance companies to check fraud in the

reimbursement of medical policies is denial of the claims of policy holders if they

fail to submit their papers after their discharge from hospitals within the stipulated

timeframe. Insurance companies have so far taken a lenient approach on this

aspect.

CHAPTER 9 - FRAUD AFFECTING INSURANCE COMPANIES

34

Nearly 31% of the respondent indicates that insurance companies are most affected

by miss-selling due to premeditated fabrication and / or fraudulent miss

presentation of material information, as compared to the different types of frauds

that affect insurance companies adversely. Insurance continues to be miss-sold

with senior citizens being the softest targets as they do not understand new

products. Recent media news highlights the prevalence of this kind of fraud, “A

74-yearold man was fraudulently sold four insurance policies and two pension

plans by a clutch of bank executives, who obtained his personal details on the

pretext of opening a bank account.” Measures such as mystery shopping can

provide some relief by identifying and eliminating miss-selling.

The Insurance Regulatory and Development Authority (IRDA) have put in place a

significant role to bring about transparency in the selling process by stipulating that

“…. All insurance companies (life and general) have to resolve complaints from

policy holders within 14 days and any failure to do so will attract penalty. Any

failure on the part of insurers to follow this procedure and time frame will attract

penalties by the IRDA.”

Collusion between parties and fake documentation are the other critical types

of fraud that affect insurance companies.

The former mainly occurs in collusion with patients, who are undergoing a

particular treatment and are made to sign for more expensive procedures by

hospitals. In some cases, hospitals claim money for patients who have not actually

been admitted to these hospitals. Such patients are paid a small amount by such

hospitals, which claim large amounts from insurance companies. In other cases,

manipulation of documents is common in the segment. India Forensic Research

indicates that medical bills are the most commonly forged documents

35

In its quest to restrict unfair practices, IRDA has formulated the Insurance

Regulatory and Development Authority (Protection of Policyholders’ Interests)

Regulations, 2002. To counter the increase in the number and complexity of

frauds, IRDA has announced draft regulations for open market consultation, to

reduce “unfair practices” and the “information gap” in domestic insurance.

Some of the proposed regulations:-

An amendment of IRDA’s regulations to protect policyholders’ interests and

issuance of key feature

documents for insurance products

Guidelines on distance marketing and sale process verification of insurance

products.

Standardization of terms and conditions on unit-linked insurance products

IRDA’s acquisition of a database for the distribution of insurance products

In its bid to check financial fraud, IRDA has made it mandatory for all insurers to

obtain a recent photograph of new customers.

CHAPTER 10 - DEDICATED “ANTI – FRAUD” DEPARTMENT

36

Fraud can be perpetrated in many ways. Therefore, an insurer should adopt a

holistic approach to adequately identify, measure, control and monitor fraud risk.

For an insurance organization, its fraud management strategy should form part of

its business strategy and be consistent with its overall mission and objectives.

Detection of insurance fraud should be in two steps:-

The first is to proactively identify suspicious claims or surrender that has a

high possibility of being fraudulent. This can be done by conducting data

analysis using various forensic tools or by putting in place an effective fraud

risk assessment framework. Additionally, insurance companies can provide

their stakeholders with a fraud reporting mechanism.

Regardless of the mode of implementing step one, the next step should be to

investigate these fraud claims or surrender and conduct further analysis

According to India’s Ministry of Labor and Employment’s advisory note, which

was sent to insurance companies, “It is in the interest of insurance companies to

spend time and effort on an effective monitoring mechanism to ensure that claim

ratios are realistic, manageable and correct?” In a data-driven industry such as

insurance, companies will not only need to compete in terms of their product

offerings, but will also be required to leverage business intelligence-enabled

analytics to attain a competitive edge?

CHAPTER 12 - DATA ANALYSIS FOR FRAUD DETECTION

37

Data analysis technology enables auditors and fraud examiners to analyze an

organization’s business data to gain insight into how well internal controls are

operating and to identify transactions that indicate fraudulent activity or the

heightened risk of fraud. Data analysis can be applied to just about anywhere in an

organization where electronic transactions are recorded and stored. Data analysis

also provides an effective way to be more proactive in the fight against fraud.

Whistleblower hotlines provide the means for people to report suspected fraudulent

behavior but hotlines alone are not enough.

To effectively test for fraud, all relevant transactions must be tested across all

applicable business systems and applications. Analyzing business transactions at

the source level helps auditors provide better insight and a more complete view as

to the likelihood of fraud occurring. It helps focus investigative action to those

transactions that are suspicious or illustrate control weaknesses that could be

exploited by fraudsters. Follow-on tests should be performed to further that

auditor’s understanding of the data and to search for symptoms of fraud in the data.

There is a spectrum of analysis that can be deployed to detect fraud. It ranges from

point-in-time analysis conducted in an ad hoc context for one-off fraud

investigation or exploration, through to repetitive analysis of business processes

where fraudulent activity is likely to more likely to occur. Ultimately, where the

risk of fraud is high and the likelihood is as well, organizations can employ an

“always on” or continuous approach to fraud detection – especially in those areas

where preventative controls are not possible or effective.

ANALYTICAL TECHNIQUES FOR FRAUD DETECTION

To get started requires an understanding of:

The areas in which fraud can occur

What fraudulent activity would look like in the data

38

What data sources are required to test for indicators of fraud

The following techniques are effective in detecting fraud. Auditors should ensure

they use these, where appropriate. They include the following:

Calculation of statistical parameters- (e.g., averages, standard deviations,

high/low values) – to identify outliers that could indicate fraud.

Classification – to find patterns amongst data elements.

Stratification of numbers - to identify unusual (i.e., excessively high or

low) entries.

Digital analysis using Bedford’s Law -to identify unexpected occurrences

of digits in naturally occurring data sets.

Joining different diverse sources -to identify matching values (such as

names, addresses, and account numbers) where they shouldn’t exist.

Duplicate testing -to identify duplicate transactions such as payments,

claims, or expense report items.

Gap testing-to identifies missing values in sequential data where there

should be none.

Summing of numeric values-to identify control totals that may have been

falsified.

Validating entry dates-to identify suspicious or inappropriate times for

postings or data entry.

FRAUD DETECTION PROGRAMME STRATEGY

Instead of relying on reactive measures like whistleblowers, organizations can and

should take a more hands-on approach to fraud detection. A fraud detection and

prevention program should include a range of approaches – from point-in-time to

recurring and, ultimately, continually for those areas where the risk of fraud

39

warrants. Based on key risk indicators, point-in-time testing will help identify

transactions to be investigated. If that testing reveals indicators of fraud, recurring

testing or continuous analysis should be considered.

LIFE INSURANCE

Determine patterns of overpayment of premiums.

Review transaction payments comprising more than one type of payment

instrument.

Report multiple accounts to collect funds or payment to beneficiaries.

Report purchase of multiple products in a short period of time.

Review beneficiaries with multiple policies.

Isolate transactions for follow-up where employees that are beneficiaries.

Determine agents/brokers with statistically high numbers of claim payouts.

Calculate benefit payments paid for lapsed policies.

Find policy loans that are greater than face value.

Report unauthorized policy changes.

Identify missing, duplicate, void or out of sequence check numbers.

CHAPTER 14- EMERGING TRENDS IN FRAUD MANAGEMENT

Insurance fraud management has gained significant momentum within the past

twenty years. Growing competition, decreasing margins and increasing innovation

40

will all put pressure on insurers to strengthen this capability. To date, employees

are seen as the essential success factor for efficient fraud management and the most

important method for identifying potential insurance fraud. Experience and expert

knowledge should be complemented with training and tailored general checklists

to fuel success.

The fraud management processes within these insurance companies are supported

by bespoke software. Use of packaged software tends to be concentrated in the

business divisions focused on motor, property and casualty insurance where IT

helps to support a range of small damage claims. There is a persistent need for

automated detection systems and workflows to improve fraud detection in these

businesses as employees can be supported through automated, systematic

examination procedures. Reliable packaged software solutions have already been

implemented successfully.

Although more than half of the respondents expect to see an increase in the use of

automated fraud detection and understands the technical possibilities of software

tools to support fraud detection and fraud enquiry. A more modern and efficient

approach to claims processing has a wide range of potential benefits it opens up the

door to cost savings; it makes faster triage possible and allows employees to

concentrate on carrying out loss or benefit cases or even conducting the enquiry.

FOUR DIMENSIONS OF FRAUD MANAGEMENT

Bearing Point offers efficient and integrated fraud management solutions, that:-

41

Create clear responsibilities in the enterprise

Allocate cases to the right employees

Optimize processes in the organization

Show automation options which orientate themselves at the individual

needs of our customers

Fraud management strategy within insurance companies needs to take into

consideration four dimensions.

1. THE ORGANIZATION

The organization dimension contains the organizational structure and integration of

fraud management within the overall company. Roles and responsibilities within

fraud management must be defined clearly to enable the processes within fraud

42

investigation. It is important to learn from experience and develop strategies and

measures for fraud prevention. Therefore input from the organization as well as

responsibilities for this process need to be defined.

2. EMPLOYEES

Employees face many challenges regarding fraud. Initially, they need to detect

fraud, and in a suspicious case they need to investigate the claim fully and

document reasons for rejecting a claim that would stand up in court if a law suit

was brought against the company. The employee’s observations and experiences

play a decisive role. The employee dimension is about abilities and competencies –

managing existing skills through increased training as well as driving recruiting

strategy.

3. THE PROCESSES

The processes dimension allows companies to define efficient processes that

support the detection and investigation of fraud in a standardized and systematic

manner. Existing processes can be re-defined to optimize their impact: reducing

time and costs while also releasing resources to focus on other value added tasks.

Clearly defined processes create security for your employees and enhance

prospects of success for a new fraud management strategy.

4. INNOVATIVE TECHNOLOGIES

Innovative technologies are now being applied to the problem of fraud detection

and investigation. Selecting the right tools to support your optimized processes can

allow you to pinpoint the right cases to investigate and reduce claim payments

43

overall. In parallel, unsuspicious claims can be paid faster. By shortening the time

it takes to carry out investigations the company can alleviate the pressure of a

premature decision.

CHAPTER 15 – QUESTIONNAIRE

44

Explain about the kinds of frauds in insurance sector?

How do you detect them?

What measures have you taken to protect them?

What is the maximum value of loss that you have face because of frauds? How do you make it good?

CHAPTER 16 – CONCLUSION

45

Insurance, a very well-known concept today and many people could relate to in

more than one ways. This is the influence of the changing times that have changed

the concept of insurance in the minds of the young and the old. People have

changed their attitude towards their insurance and new look from being

an entry of luxury to an investment and necessity. The number of people

taking insurance has increased considerably in the past few decades due

to the entry of private players in the market.

One knows that every coin has two sides. Similarly, insurance also has two faces. One of which is investments and getting regular returns from financial institutions for oneself and for loved ones. The other, awfully,

46

is of which people deceive insurance companies for their undue advantage and cause intimidation to many others.

Though, there have been many laws and agencies all over the world to impede such criminal activity, it is not a full proof solution to all insurance frauds.

In a world today where every person seeks their right to information and demands the same, it is very difficult to scam them. One must know all the loop-holes of their business to scheme someone. Lack of knowledge and not knowing ones basic rights on behalf of prey could land them in scrambled scam bisque.

There have been many institutions and agencies formed all over the world to de tec t f raud and pena l i ze the one consc ien t ious fo r such mishaps . There i s d iv is ion of insurance f raud , INTERNATIONAL ASSOCIATION OF INSURANCE FRAUD AGENCIES ( IAIFA) , e tc . th rough the endur ing and consc ious endeavor o f these ins t i tu t ions insurance f raud t empo has dec l ined by an enormous amount . Several have studied preceding and enduring market conditions to identify with the diverse frauds that take place and the reasons behind committing these frauds.

One cannot diminish frauds, schemes, swindles, scams but can positively b e a l e r t o f t h e m s o a s n o t b e a v i c t i m o f i t t h e m s e l v e s . T u m b l i n g fraudulent situations is a unremitting and collective effort of countless. One must be sensitive and offer their helping as much as they can. One can either grumble about how things are all going wide of the mark o r s w a l l o w t h e c o n s e q u e n c e s . O r p u t t h e i r f o o t d o w n a n d m a k e a n a t t empt to change the immora l to the r igh t . The wrong wi l l change and everyone will see the bright light of truth and right

47

with the revolution of knowledge, awareness, and an attitude for change amongst the humanity.

INSURANCE FRAUD : THE CRIME YOU PAY FOR

Watch out- insurance crooks are picking your pocket in order to line theirs. These thieves are committing insurance fraud, one of America’s largest criminal industries. Insurance fraud is a crime, and one way or another, honest consumers and businesses pay the price.

Insurance fraud occurs every day and in every state. People of all races, incomes and ages are victimized.

THE FUTURE- STILL DANGEROUS

Despite the encouraging progress, insurance fraud will remain a vast and dangerous criminal enterprise. Here are several fraud trends consumers should know about:

The internet will hatch new insurance swindles as computer- survey consumers buy from online insurance companies that may be virtually untraceable. Young people raised on the internet will be the vanguard of this crime wave.

The global economy is igniting huge insurance money – laundering schemes, often involving fake insurers that bilk people out of millions. Tracking them across international borders will pose a big problem.

The large population bulge og aging boomers needing more medical attention will keep health fraud near the forefront of the largest and costliest fraud crimes.

48

Insurance fraud against immigrants will remain a serious problem as diverse ethnic continue migrating. Many fraud crimes will be committed by fraud rings or organized mafias of immigrants themselves.

The elderly will remain one of the largest targets of insurance swindles. Investment schemes are among the newest approaches: thousands of seniors are investing in bogus verticals – life insurance policies that don’t exist or were obtained illegally. Many seniors also are investing in fake promissory notes sold by insurance agents and guaranteed by non- existent insurance companies.

EVERYONE’S SOLUTION

Everyone pays for a insurance fraud, and so everyone must join in stamping out these swindles. Consumers, lawmakers, insurance, companies, doctors, lawyers and many more must be part of the answer. Insurance fraud will disappear only when criminals realize fraud is a fast highway to jail, not an easy road to riches.

PROTECT YOURSELF: STAY ALERT

You can protect yourself against insurance scams: stay alert, ask questions, and go slow or back out if an insurance transaction seems suspicious.

Never sign blank insurance claim forms Demand detailed bills for repair and medical services. Check closely for

accuracy. Make sure “free services” aren’t actually hidden in insurance bill. Be wary of buying insurance from door-to-door or telephone sales people. Be suspicious if the price of insurance seems too low to be true. Contact your state insurance department to make sure the agent and

company are licensed.

49

Keep your insurance identification number secret; insurance crooks can steal it and involve you inn scams.

Contacts you’re STATE INSURANCE DEPARTMENT and the NATIONAL INSURANCE CRIME BUREAU if you think you’re being scammed or someone asks you it take part in a fraud.

CHAPTER 17 – REFERANCE

50

Primary data had been adopted by an informal interview to agent of life insurance.

Secondary data are adopted by collecting the information’s from different management books websites of insurance sector and especially the LIC websites Journals and magazines and news from newspapers.

51