liability, recognition_measurement.pdf

TRANSCRIPT

1

Accounting for Liabilities in IFRS: Recognition, Measurement and Conservatism

Richard Barker, Senior Lecturer, Judge Business School, Cambridge University

Anne McGeachin, Senior Lecturer, University of Aberdeen Business School

This version: April 2012

The authors are grateful for comments from seminar participants at Aberdeen, Cambridge, Edinburgh, ICAS, Oxford and the ASB’s Academic Panel, and for workshop funding from ICAEW and EFRAG.

2

Accounting for Liabilities in IFRS: Recognition, Measurement and Conservatism

Abstract

An important application for financial accounting theory is in accounting standards, for

which clarity of conceptual foundation can be viewed as essential in addressing the practical

complexities of determining financial position and financial performance. Viewed from this

perspective, the recognition and measurement of liabilities in IFRS is inadequately theorised:

there is an absence of coherent and consistently-applied theory in both the conceptual

framework for financial reporting and in accounting standards themselves. Moreover, this

absence does not result simply from a failure to apply theory that is well-established in the

literature. Instead, potentially relevant contributions from the literature are few in number,

largely disconnected from one another, and at best only indirectly focused on the challenge

at hand. In this paper, we focus on measurement theory, which enables insights into the

considerable inconsistencies and difficulties that exist in IFRS with respect to accounting for

liabilities. Our analysis contributes to accounting theory with respect to recognition,

measurement and conservatism, with policy implications resulting from the application of

that theory in accounting standards.

Keywords

Liabilities; Recognition; Measurement Theory; Conservatism; Conceptual Framework;

IFRS.

3

Accounting for Liabilities in IFRS: Recognition, Measurement and Conservatism

1. Introduction

The purpose of this paper is to contribute to accounting theory and financial reporting

practice concerning the recognition and measurement of liabilities. Our research is motivated

by the observation that IFRS is inadequately theoretically grounded in this area. Without

formal explanation or justification, IFRS standards and proposals contain multiple different

methods of recognising and measuring liabilities, with inconsistencies among these methods

and with no two standards or proposals adopting the same method. The conceptual challenge

in accounting for liabilities has been considerable and longstanding, with liabilities projects

such as leases, revenue recognition, pension obligations, provisions and insurance contracts

having had a prominent and sustained presence on the IASB’s agenda.

We seek to understand what is going on here. Does inconsistency in IFRS imply flawed

application by the IASB of established theory, or is it evidence of inadequately developed

theory? We do not find answers to either of these questions in the literature. Indeed,

potentially relevant contributions from the literature are few in number, largely disconnected

from one another, and at best only indirectly focused on the challenge at hand.

The paper is structured as follows. In the next section, we set out our research method. The

paper is predominantly theoretical, in that we seek to analyse and develop recognition and

measurement theory and to identify normative implications. There is also a specific sense in

which our method can be interpreted as empirical. While not a conventional empirical test of

theory against (quantitative) data, our method can be viewed analogously as a test of abstract

theory against the qualitative, textual embodiment of that theory in accounting standards. By

this method, we seek to reject the hypothesis, which we argue to be implicitly adopted in

4

IFRS, that measurement theory is generally applicable to the recognition and measurement of

liabilities.

Consistent with this approach, we set out in Section 3 an analysis of measurement theory,

drawn from the literature. Our specific interpretation of this theory starts with the claim that

the process of measurement requires the existence of a currently observable measurement

attribute. As the future cannot be observed directly, it is not possible to measure directly

attributes that are expected to exist in the future. In particular, future cash flows are not

currently measurable. What can be measured, at least in principle, is a currently-held

expectation of a future cash flow. A market price, for example, is a currently observable

measurement attribute, but of current expectations about future cash flows, not of the future

cash flows themselves. In cases where there is no market price, and noting that expectations

are inherently subjective, an important question, both for theory and for associated practice, is

whether it is appropriate to base the balance sheet valuation of liabilities upon expectations.

If not, many liabilities would not be recognised because they do not have currently

observable measurement attributes.

In Sections 4 and 5, we introduce, respectively, the IASB’s conceptual framework (IASB,

2010; hereafter ‘Framework’)1 and IFRS accounting standards themselves (including

proposed revisions to standards). The IASB’s theoretical approach in these statements can be

broadly characterised as one of presuming measurability for all liabilities. We argue that the

boundaries of applicability of measurement theory - the distinction between the ‘measurable’

and the ‘immeasurable’ noted above - provide insight into the limitations of this approach.2

In particular, there exist categories of liabilities which, for good informational reasons, are

recognised in IFRS, yet for which measurement theory provides no support. In this context,

there is therefore flawed application by the IASB of the established theory upon which it

5

implicitly justifies its decisions. In turn, this also implies either inadequately developed

theory in IFRS that would support those decisions, or that the decisions are not justifiable.

In Section 6, we turn to this need for additional theory. We first argue that, for reasons that

have not been recognised in the literature, there are challenges of recognition and

measurement that are unique to liabilities, as opposed to assets. Combining this insight with

our analysis of measurement theory, we argue the need for a normative theory of

conservatism in IFRS, as a necessary complement to measurement theory under conditions of

uncertainty. We conclude the paper in Section 7, identifying potential avenues for further

research, as well as policy implications for IFRS.

The specific contributions of our paper, which all concern the application of accounting

theory in IFRS, can be grouped under the following four headings: recognition, measurement,

liability measurement and conservatism.

Concerning recognition, we identify a conceptual inconsistency in the recognition criteria

contained within the IASB’s Framework. Specifically, ‘probable outflow’ and ‘reliable

measurement’ are both treated by the Framework as necessary conditions for recognition, as

opposed to the absence of both being necessary conditions for non-recognition. We propose

a revision to IFRS, in the form of a recognition algorithm for the Framework, in which

reliable measurement and probable outflow are each sufficient but not necessary conditions

for the recognition of a liability. In this context, the criterion of reliable measurement is

consistent with the application of measurement theory, while the criterion of probable

outflow arises specifically where measurability is not achievable, and where an alternative

justification is therefore needed.

Concerning measurement, we identify inconsistency between the theory of measurement and

the IASB’s interpretation of measurement, as set out in its 2010 revisions to the Framework,

and in accounting standards themselves. In the revised Framework, the IASB’s conceptual

6

commitment to ‘measurement’ is in the form of the faithful representation of economic

phenomena, which is defined in terms of completeness, neutrality and freedom from error.

Yet, when viewed from the perspective of measurement theory, such a commitment is

logically undermined by the relegation of verifiability in the Framework. This relegation

serves to rule out measurability as a necessary condition for faithful representation. The

implication is that faithful representation has diminished meaning, such that it cannot be

described as a measurement process, even though it is treated as such in accounting

standards.

Concerning liability measurement, we identify and tabulate an extraordinary degree of

conceptual and practical inconsistency in IFRS. Our analysis of measurement theory

provides several insights into the underlying sources of this inconsistency. We identify

flawed logic in the IASB’s attempt to define settlement amount as a measurement objective.

Specifically, by focusing on the amount an entity would rationally pay at the end of a

reporting period to be relieved of a present obligation, the IASB gives the appearance of

transforming unobservable future cash flows into a current, measurable attribute. Yet in the

absence of an active market, as is common, this appearance is without substance. Related to

this, we identify that expected cash flows, selection of discount rates and risk adjustments

(including own credit risk), each of which have frustrated progress in IFRS, have been

misunderstood as problems of measurement, rather than being inevitable consequences of

there being no observable measure. We suggest that these conceptual insights can be used to

explain cases where the IASB has struggled, for example in its failed attempt to amend IAS

37, where its proposal to remove the probable outflow recognition threshold was premised on

an incorrect presumption of measurability.

Finally, our paper makes a contribution to the theory of conservatism, and to the application

of that theory in IFRS. We identify that the IASB’s recent decision to exclude conservatism

7

from the Framework is grounded in a misunderstanding of measurement theory. Specifically,

conservatism has been misrepresented by the IASB as a process of biased measurement, yet it

is better understood as a response to an absence of measurability. Extending the analysis of

conservatism in the literature, we note that while the application of conservatism to assets is

consistent with measurement theory (ie assets that have no observable measure are not

recognised), the application to liabilities is in conflict, because it implies a need for lower

standards of verifiability, not higher (ie liabilities with no observable measure still need to be

recognised). A consequence is that the conceptual difficulties caused by an absence of

measurability are greater for liabilities than for assets, which accords with the greater relative

inconsistency and ongoing challenge experienced by the IASB in the measurement of

liabilities. We identify a need to develop a normative theory of conservatism, which

addresses the conflict with measurability, and which can be embedded into the Framework.

Overall, our contributions are to accounting theory, and to the application of that theory in

IFRS. Specifically, we use the lens of measurement theory to identify and explain conceptual

inconsistencies in IFRS, and we draw implications for developing the (inter-related) concepts

of recognition, measurement and conservatism in the Framework, and for the application of

these concepts in accounting standards. Our research method, which embodies this emphasis

on theory, is set out in the next section of the paper.

2. Research Method: Analysis, Application and Development of Theory

In our research method, we have followed the approach to theory-building of Van de Ven

(2007), who defines theory as ‘a pattern of conceptual organisation that explains phenomena

by rendering them intelligible.’ Van de Ven describes the process of theory-building as

comprising three elements, which are logically sequential but which in practice work together

8

in an iterative cycle: an abductive process of conceiving or creating a theory; a deductive

process of constructing or elaborating a theory; and an inductive process of justifying or

evaluating a theory.

The phenomena that we seek to explain, in Van de Ven’s sense, are the conceptual

inconsistencies in IFRS with respect to the recognition and measurement of liabilities. Our

meaning of ‘IFRS’ in this context is all accounting standards, exposure drafts (EDs) and

discussion papers (DPs) issued (or revised) by the IASB concerning the recognition and

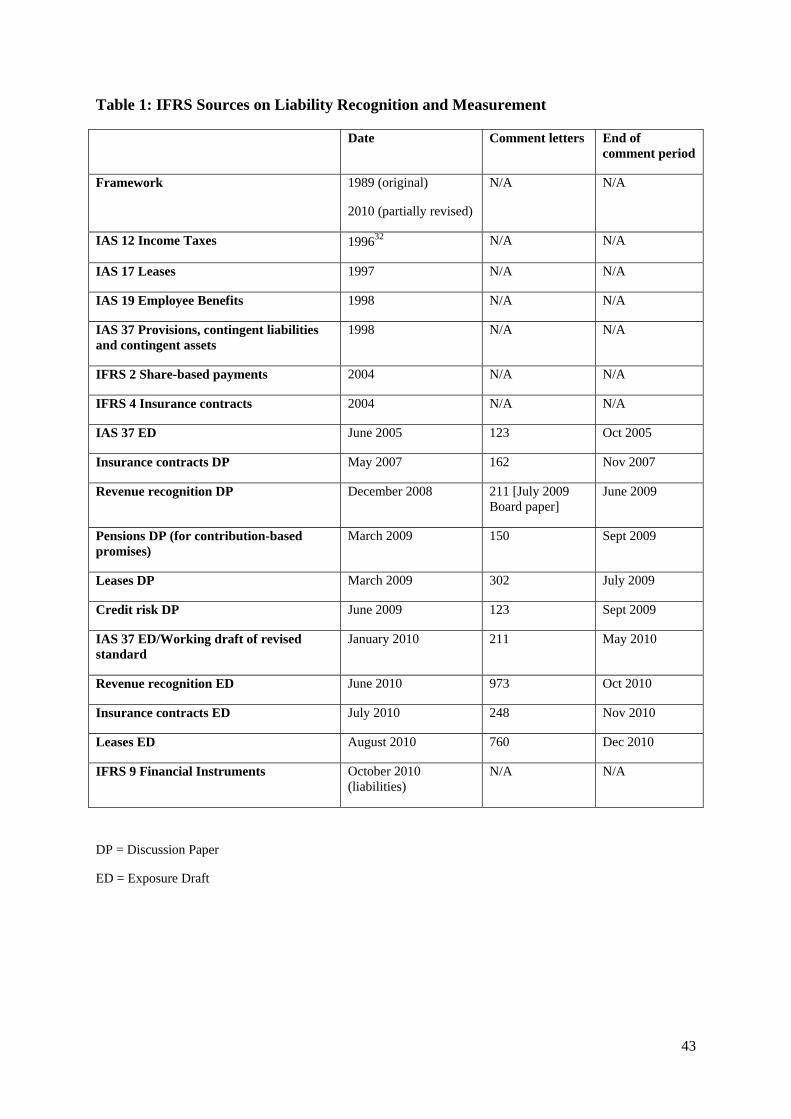

measurement of liabilities. These data are summarised in Table 1.3 Taken together, they are

rich in information. They contain not only the formal requirements of IFRS, but also the

IASB’s formal explanations for these requirements. Through the issues raised by each

document, and the changes made from one document to the next, these documents also help

to reveal areas of tension and challenge, together with the reasons why these challenging

situations are perceived to exist, and the extent to which they are either similar or different in

nature across accounting standards.

While our focus is IFRS, our analysis is equally applicable to US GAAP (Benson et al.,

2007). The FASB’s conceptual framework provided the foundation and logical structure for

the IASB’s Framework (Storey and Storey, 1998; Riahi-Belkaoui, 2004). The 2010 revisions

to both frameworks were carried out jointly by both IASB and FASB, and adopted

simultaneously by both. The IASB and the FASB have been working together since 2002 to

achieve convergence of IFRS and US GAAP, with a common set of high quality global

standards being a priority for both organisations (the ‘Norwalk Agreement’, FASB, 2006).

** Insert Table 1 here **

In the abductive process of our theory-building, our challenge was to identify a ‘candidate

theory’ – a theoretical lens through which we might hope to render intelligible the

9

inconsistencies that we observed, by means of drawing out a systematic, underlying theme.

This was not a simple process. It was also risky, because there could be no guarantee that we

would find a theory that would serve our purpose, especially as the observed inconsistencies

were many, varied and hitherto poorly understood. The process involved considerable

iteration, over several months, between different aspects of IFRS and various lines of thought

in the literature, as we sought to understand the theoretical nature of the underlying

inconsistencies in IFRS. We also drew upon the public-record comment letters sent to the

IASB in response to the DPs and EPs, as these provided further insight into the practical

challenges faced by the IASB and, thereby, possible indications of where to locate flawed or

under-developed applications of theory (these sources are summarised in Table 1).

Our iterative process took different forms at different times, as our thinking and

understanding evolved. In each case, we focused on one element of inconsistency in IFRS

and sought theory that might help to explain it. One focus was on alternative measurement

attributes in different areas of IFRS, and on seeking to understand these alternatives in the

light of the (partially) corresponding literature, for example Edwards and Bell (1961), Horton

et al. (2011), Macve (2010) and Whittington (2010). Another focus was conservatism, which

features explicitly in the IASB’s 2010 revisions to the Framework (and in stakeholders’

responses to these revisions), as well as (mostly implicitly) in accounting standards

themselves, and again in partially corresponding analysis and evidence in the literature, such

as Basu (1997) and Watts (2003a, 2006). Further focuses included the underlying definition

of liabilities (contrasting the Framework with, for example, the discussion in Beaver, 1991,

Botosan et al., 2005 and Murray, 2010), as well as the distinctive recognition and

measurement aspects of liabilities in comparison with assets (as discussed, for example, in

Baxter, 1975, Lennard, 2002 and Nobes, 2003). This process of ‘searching for theory’

eventually led us to narrow our attention to the theory of measurement, which appeared to

10

offer the greatest traction on our research question. Accordingly, we set out in Section 3 an

analysis of measurement theory that serves as the theoretical foundation for our paper.

Our next step in theory-building was to elaborate on our interpretation of measurement

theory, through a simple, deductive process of setting out its logical structure. Specifically,

for any given liability, X, we can set out two premises and a conclusion, as follows. Our first

premise is that X is a liability, our second premise is that all liabilities are measurable, and

our (inexorable) conclusion is that X is measurable. In other words, and as will be illustrated

and argued in Sections 4 and 5, if the working assumption in IFRS is that measurement

theory is applicable to all liabilities, then if X meets the definition of a liability, it is

necessarily assumed to be measurable.

In the final, inductive process of evaluating theory, we set out to test the second of our two

premises, and so the validity of the (deductively-stated) theory. In other words, we seek to

demonstrate that while our second premise is assumed to be true in IFRS, it can be shown to

be false, and that therefore our deductively-stated conclusion can be shown to be false also.

Such a test could in principle be conducted empirically or rhetorically, and our approach

could be understood in either way: it is rhetorical in that we evaluate the internal logical

validity of measurement theory, as adopted in IFRS; it is empirical in that we test the

hypothesis that measurement theory is generally applicable against the (qualitative) data of

the application of that theory in the requirements of IFRS, with the aim of falsifying our

hypothesis (King et al, 1994). Viewed empirically, our approach must be interpreted

carefully. We do not, in a conventional sense, apply theory to data. Instead, we test whether

a concrete application of theory in IFRS is consistent with an abstract, general statement of

that theory.

11

This approach enabled us to better understand the theoretical structure of IFRS, and the

inherent inconsistencies and limitations therein. Our analysis led us to conclude, as will be

argued in Sections 4 and 5, that the application of measurement theory in IFRS is flawed, and

that conceptual inconsistencies result with respect to recognition criteria, the definition of

measurement, and the application of measurement attributes. In turn, this implied the need

for additional theory in IFRS, to be applied in cases where measurability is not achievable. In

this regard, measurement theory suggested a natural path to follow. We argue in Section 6

that the limited applicability of measurement theory is manifest for liabilities to a greater

degree than for assets, and that conservatism in accounting is the primary reason for this. Yet

the IASB’s application of measurement theory has led it to reject conservatism as being

nothing more than biased measurement, instead of adopting theory to rationalise the presence

of conservatism. Moreover, we identify that this need for conservatism in IFRS is different

from that identified in the literature (Watts, 2003a, 2006), because when the theory of

conservatism is applied to liabilities, as opposed to assets, it is not consistent with the theory

of measurement, but instead in conflict.

Overall, therefore, the research method in our paper focuses on the application of two

theories in accounting: measurement and conservatism. We argue that application of the

former is flawed in IFRS because the theory is not applicable to all liabilities, while the need

for the latter is incorrectly rejected in the Framework, even though it is applied in practice in

the requirements of IFRS.

The paper now proceeds as follows. Drawing upon the academic literature, Section 3 sets out

the interpretation of measurement theory that is adopted in the paper. As described above,

Sections 4 and 5 then test this theory against the qualitative data in, respectively, the

Framework, and the requirements or proposals issued by the IASB. In Section 6, we then set

12

out the implications of our analysis for conservatism in accounting. Section 7 concludes the

paper.

3. Measurement Theory

There is no universally accepted definition of measurement. A standard reference is Stevens

(1946), who defines measurement as any process of ‘the assignment of numerals to objects or

events according to rules.’ This definition has been criticised for being too loose, because it

allows more or less any assignment of numbers to categories to be defined as measurement,

even if the underlying method of assignment is inherently arbitrary (Lord, 1953). On this

basis, any number reported in a financial statement is by definition a measure, based as it is

upon the application of a rule, in the form of an accounting standard. If the concept of

measurement is to have any analytical traction, something more is required.

Deeper insight comes from considering the process of measurement, which can be broken

down into three stages: definition of the attribute to be measured, determination of the

quantum (or measurement scale) and application of a measurement instrument to the item in

question (Vehmanen, 2007). It is only the third of these stages that is empirical. While the

measurement attribute and the measurement scale can be determined in principle, the

application of a measurement instrument can only be done in practice, and it requires the

existence of a currently observable measurement attribute. This is an essential point.

Measurement is straightforward in certain cases, such as cash, or assets and liabilities with

observable market values in active markets, or where there exist certain contractual

commitments at the balance sheet date.4 Consider, however, if the desired measurement

attribute for a liability is the cost of performance, which can be defined as the (entity-

specific) present value of economic benefits expected to be consumed in settlement of the

13

liability. In this case, the attribute to be measured is the cost of performance, and the

quantum is money, yet a fundamental problem arises, which is that a measurement instrument

cannot be applied. This is because future cash flows are not currently observable. The cost

of performance therefore cannot, in the sense described here, be measured: the future does

not currently exist, and so future cash flows are immeasurable (Chambers, 1998; Rosenfield,

2003).

The concept of measurement error is likewise inapplicable to the (non-existent) future. While

there is likely to be estimation error in practice for the measurement of any currently

observable item, the item is nevertheless in principle measurable (Morgenstern, 1950). This

measurement is also in principle verifiable and it can therefore be considered to be objective

(McKernan, 2007). In contrast, forecast error is not measurement error; it is instead the

difference between a current forecast and a future realisation that does not yet exist. And to

the extent that any given forecast is a matter of individual opinion about something that is

unobservable, it is subjective and cannot be verified.5 Moreover, while measurement can be

viewed, in the simplest case, as relating to a single, measurable amount, forecasts can be

conceptualised as a probability distribution, making the perceived economic value of the

asset or liability equal to expected value. The values determined by measurement and by

forecasting are therefore different in nature.

It is essential here not to confuse the data in a forecasting model, with which a cost of

performance can be determined, and future data themselves, which do not currently exist

(Winston, 1988). It is possible to use a model to determine the expected value of future cash

flows, and while the future cash flows themselves do not exist, the currently-held

expectations do, and so they are in principle measurable. Sterling (1970) cautions that these

expected values, based upon forecasts, are ‘not a measurement of wealth unless one defines

wealth as a state of mind,’ and an important question is therefore whether (and if so in what

14

way) it is appropriate to base the balance sheet valuation of liabilities upon measures of

expectations.6

It is in this context that the market mechanism comes into play as a measurement instrument,

because market prices provide observable and verifiable evidence of currently-held

expectations. In effect, the market transforms subjective expectations about the future into

currently observable amounts. In contrast, certain other types of expectation, such as those

underpinning management’s forecast of the cost of performance, are not directly observable

in practice, meaning that they cannot be measured, and that they are subjective and non-

verifiable (Nagel, 1986).7

A further consideration is that measurement can be of different types. Stevens (1946) noted

the existence of ‘different kinds of scales and different kinds of measurement, not all of equal

power and usefulness.’ He proposed a classification of these scales into four types: nominal,

ordinal, interval and ratio. Chambers (1964, 1965) noted that the secondary metrics common

in accounting, such as net assets, leverage and return on equity, are conceptually valid only if

there is ratio measurement, which is the most demanding category in Stevens’ typology.

Moreover, for this purpose, there must be only a single measurement attribute used for all

assets and liabilities, because core properties of additivity and ratio measurement would

otherwise not hold (Chambers, 1998; Barth, 2006).

This strict measurement perspective can be contrasted with an informational perspective

(Christensen, 2010a). While not tightly defined, an informational perspective views

accounting information as part of a broader information set, providing one source of input to

users’ economic decision-making. Consistent with this perspective, and given the inherent

practical difficulties of a strict measurement perspective under conditions of imperfect and

incomplete markets (Beaver and Demski, 1974; Beaver, 1989), it is inappropriate to rule out

15

of consideration value attributes that are not strictly measurable, nor to automatically

disallow mixed measurement. In particular, an informational perspective would suggest

reporting information relevant to the sustainable economic performance of the entity, as

opposed to a stricter statement of financial position at the balance sheet date, especially when

that statement does not capture the economic choice that is likely to be undertaken by the

entity (Macve, 2010; Whittington, 2010). An informational perspective would in principle

allow the recognition of assets and liabilities that are not strictly measurable, for example

because recognition of such items is necessary for the timely recognition of unrealised gains

and losses, an important part of accruals accounting (Ball and Shivakumar 2005).8 Assets or

liabilities exist even if their values cannot be measured, and information pertaining to them

may be useful even though it is inevitably subjective.

The next sections of the paper explore the application of measurement theory in IFRS, based

upon testing the hypothesis that measurement theory is generally applicable to the recognition

and measurement of liabilities. We present our analysis in two parts, which are the

theoretical foundations of liability recognition and measurement in the Framework (Section

4) and theory and practice in accounting standards themselves (Section 5).

4. Recognition and Measurement in the Conceptual Framework

It is striking, and perhaps revealing with respect to theoretical foundations, that the IASB’s

Framework provides remarkably little guidance on recognition and measurement, even

though it is clear on the importance of both factors for effective financial reporting. To the

extent that the Framework does reveal the IASB’s position, the communication is often

implicit. This is in spite of the Framework having been (partially) revised as recently as

2010, with these revisions addressing specifically the Objectives (Chapter 1) and Qualitative

16

Characteristics (Chapter 3) of information in the financial statements, and thereby re-

evaluating the nature and purpose of measurement (IASB, 2010).

A liability is defined in the Framework as ‘a present obligation of the entity arising from past

events, the settlement of which is expected to result in an outflow from the entity of resources

embodying economic benefits’ (para 4.4). Yet the Framework also has two recognition

thresholds that serve to constrain the practical applicability of this definition: ‘a liability is

recognised in the balance sheet when it is probable that an outflow of resources embodying

economic benefits will result from the settlement of a present obligation and the amount at

which settlement will take place can be measured reliably’ (para 4.46, italics added).9

Measurement theory, as set out in Section 3, cannot explain the IASB’s adoption of these

recognition thresholds. This is illustrated in Table 2, where the Framework’s criteria lead to

liability recognition only in the illustrative example of a simple bank loan, and where there is

non-recognition for each of the other three examples, because either or both of the

recognition thresholds are not crossed.

** Insert Table 2 here **

It is possible, as in the illustrated example of a liability that is a derivative financial

instrument, to have a currently observable market price, and so reliable measurement, yet for

it to be probable that there will not be an outflow of resources. In this case, adoption of

measurement theory would render the probable outflow criterion irrelevant: if the liability can

be measured, it should be on the balance sheet. The same conclusion, that the probable

outflow criterion is irrelevant, holds also for the items in Table 2 that are not reliably

measurable. This is because, whether or not there is a probable outflow, consistency with

measurement theory requires that the liability is not recognised.

17

This irrelevance for the probable outflow criterion under measurement theory does not,

however, imply that the criterion is irrelevant for financial reporting. This is because there

may be a case for recognising liabilities that cannot be measured, while also a case for

excluding from recognition liabilities where the outflow of resources is unlikely to happen –

as, for example, in the distinction between a provision and a contingent liability, and

elsewhere in IFRS (Murray, 2010).10 The Framework’s requirements are imprecise in this

respect, in that ‘probable’ is not defined.11 Yet measurement theory suggests that this

imprecision is unavoidable. The concept of ‘probable’ is explicitly concerned with

unobservable future cash flows, and therefore with inherent subjectivity and the absence of

strict measurability at the balance sheet date: if a tighter definition could be achieved, it

would not be needed. The point is that the probability threshold is relevant only when there

is not reliable measurement, so making the threshold necessarily vague.

An implication of this analysis is that the Framework incorrectly requires both reliable

measurement and probable outflow as necessary conditions for recognition, instead of

requiring the absence of both as necessary conditions for non-recognition. This is addressed

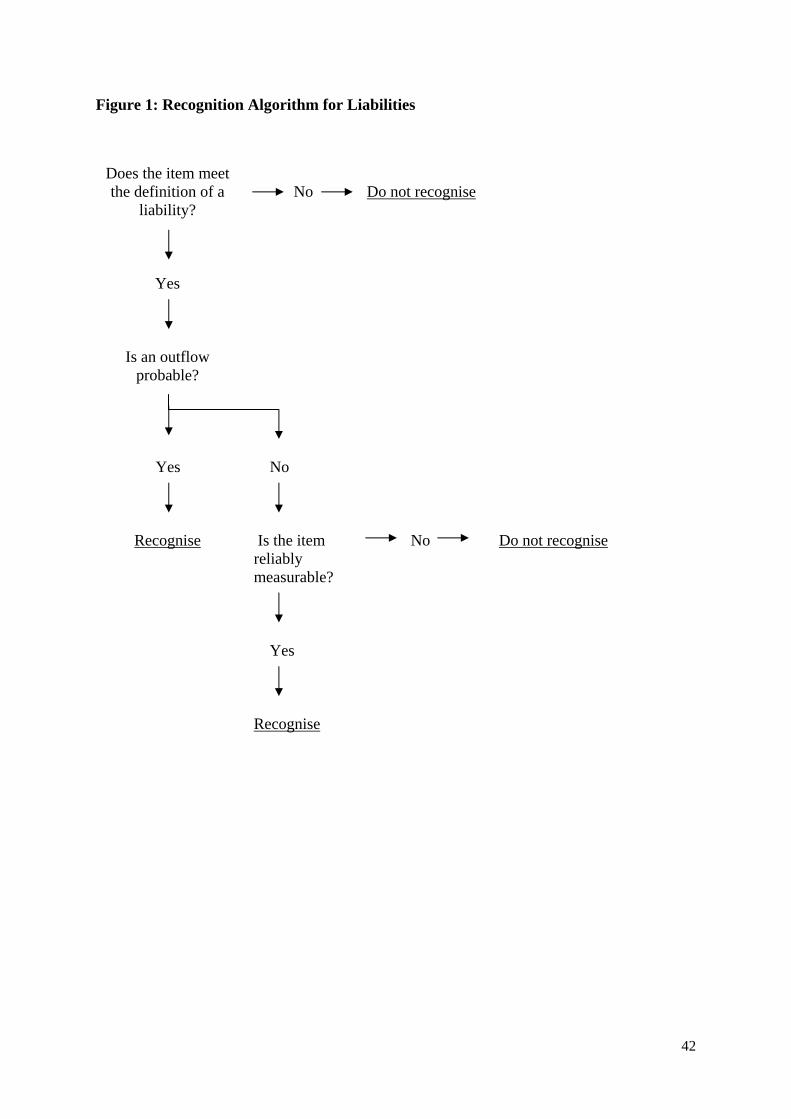

in Figure 1, which is proposed as an alternative to the current recognition thresholds in the

Framework.

** Insert Figure 1 here **

Consistent with the Framework, a prerequisite for recognition in Figure 1 is meeting the

definition of a liability. The first filter thereafter is whether there is a probable outflow, and

if there is then the liability is recognised. Critically, this filter is only necessary when the

recognised liability is a subjective forecast of future cash flows, as in the case of a provision.

If, in contrast, the market mechanism has transformed uncertain future cash flows into

quantified risk and thereby created an observable measure, then the probable outflow

18

threshold is not needed. The second filter is reliable measurability, with the effect that all

reliably measurable liabilities are recognised. If Figure 1 is applied, three of the four

categories in Table 2 now lead to recognition, as opposed to only one under the Framework.

All probable outflows are recognised (not just those that are reliably measurable) and all

reliably measurable liabilities are recognised (not just those with a probable outflow).

Contingent liabilities that cannot be measured reliably and do not have a probable outflow

continue to remain unrecognised, and the imprecise nature of ‘probable’ outflows remains as

a pragmatic recognition threshold for immeasurable liabilities. The imprecision is an

unavoidable corollary of immeasurability: while recognition is desirable, precision is in

principle unobtainable.

This approach presumes the desirability of recognising probable outflows that are not

observable and therefore not reliably measurable, which is inconsistent with measurement

theory. Yet this outcome is unavoidable if, under an informational perspective, forecasts are

regarded as providing useful information and are thereby worth recognising in financial

statements.

If liabilities are to be recognised in cases where the desired measurement attribute is not

observable, then the Framework could accommodate this in one of two ways. The first is that

adopted by the IASB in 2010, which is to adopt a notion of measurement that is broad enough

to encompass both amounts that are observable and amounts that are not. We will argue in

the remainder of this section that such an approach is inadequate, because it does not allow

analytically coherent distinctions to be made. The second approach is to apply measurement

theory only when it is valid to do so, meaning that an alternative conceptual basis is required

to support the recognition of immeasurable liabilities; we will return to this second approach

in Section 6.

19

In its 2010 revision to the Framework, the IASB effectively broadened its definition of

reliable measurement, allowing it to encompass subjective forecasts (O’Brien, 2009).

Specifically, the IASB replaced ‘reliability’ with ‘faithful representation’, the components of

which are completeness (representation is not partial), neutrality (there is no intended bias)

and freedom from error (the item portrayed is the economic phenomenon in question); para

QC12. As the following extract makes clear, faithful representation is considered to be

applicable even when observable measurement is not possible.

Faithful representation does not mean accurate in all respects ... For example, an

estimate of an unobservable price or value cannot be determined to be accurate or

inaccurate. However, a representation of that estimate can be faithful if the amount is

described clearly and accurately as being an estimate, the nature and limitations of

the estimating process are explained, and no errors have been made in selecting and

applying an appropriate process for developing the estimate. (para QC15)

This is faithful representation of the process of determining an estimate, rather than faithful

representation of the balance sheet item itself. As the analysis of measurement theory in

Section 3 makes clear, an unobservable price or value cannot in principle be verified, no

matter what process is applied in its determination. Indeed, while the Discussion Paper that

preceded the revised Framework had included the notion of verifiability, it was later dropped,

as explained in BC3.36: “some respondents (to the DP) pointed out that including

verifiability as an aspect of faithful representation could result in excluding information that

is not readily verifiable ... (which) would make the financial reports much less useful. The

Board agreed and repositioned verifiability as an enhancing qualitative characteristic, very

desirable but not necessarily required.”

Yet verifiability is the essence of objectivity, because it is the basis on which independent

observers can reach the same measurement (Sterling, 1970; Nagel, 1986). In relegating the

20

requirement for verifiability, the applicability of the IASB’s concept of faithful representation

is broadened, while its meaning is weakened. Viewed in terms of Table 2, the approach fails

to make the distinction between items that are reliably measurable and those that are not, but

instead creates a concept that embraces both categories.12 If the concept of faithful

representation is, in this way, allowed to embrace both objective, verifiable measurement and

subjective forecasts, then it cannot in principle be tightly defined.13 This is, in effect, an

informational perspective, not a measurement perspective.14 Yet, and as will now argued in

Section 5, the IASB has not in practice interpreted it as such. In developing accounting

standards, the IASB has used the rhetoric of measurement theory, allowing its own definition

of faithful representation to be misinterpreted as a definition of measurement,

notwithstanding that the Framework in substance adopts an informational perspective.

5. Recognition and Measurement in Accounting Standards

In this section, we explore the application of measurement theory in accounting standards

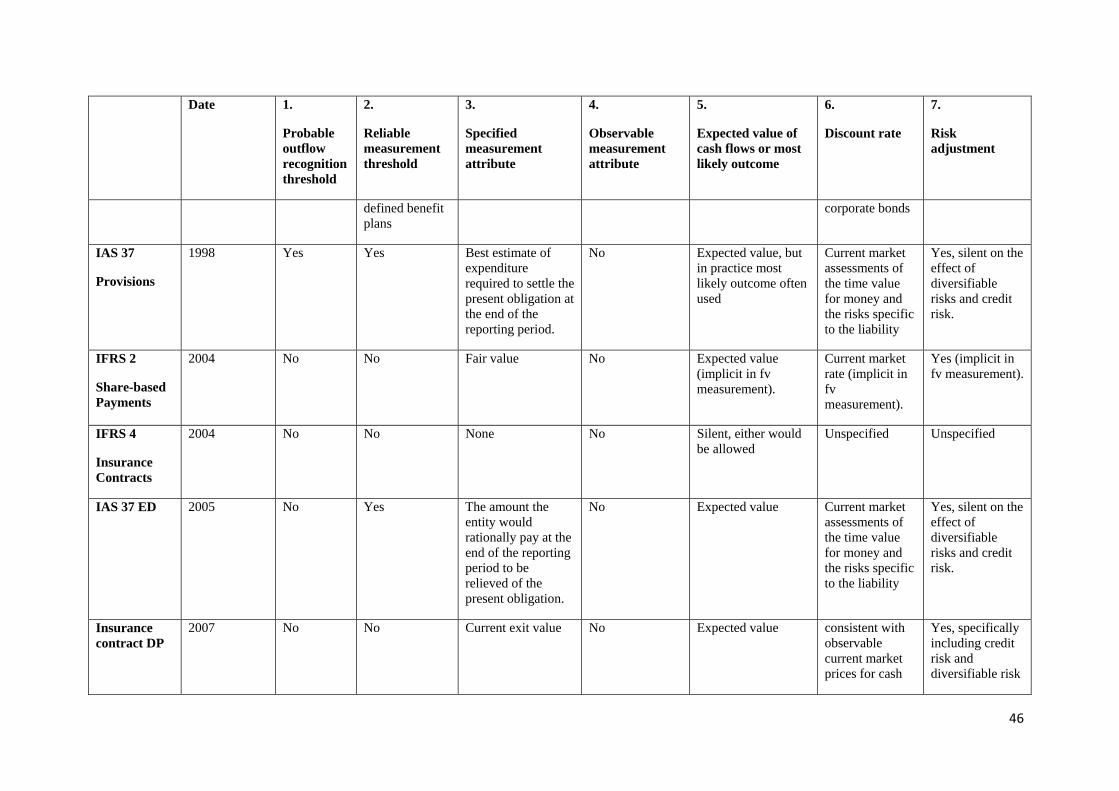

themselves (including proposals for new standards). Table 3 summarises the requirements of

all of the IASB pronouncements that comprise the source data for our paper. It can be seen

that these pronouncements contain multiple different methods of determining the carrying

amounts of liabilities, with inconsistencies among these methods and with no two standards

or proposals adopting the same method. In this section, we analyse this remarkably

inconsistent state of affairs. Our discussion follows the structure of Table 3, first addressing

recognition (the probable outflow recognition and reliable measurement thresholds), followed

by measurement. The analysis of measurement considers first the measurement attribute,

followed by the existence of observable measures and then, in cases where the measurement

21

attribute is unobservable, the approach taken by the IASB to the determination of cash flows,

discount rate and risk adjustment.

** Insert Table 3 here **

The first issue we consider is that of a probable outflow recognition threshold. While

included in the Framework, such a threshold is present in only one other IASB

pronouncement, in IAS 37 (column 1 in Table 3). Moreover, the EDs of amendments to IAS

37 (2005 and 2010) proposed removing the threshold, which, if enacted, would result in the

Framework being the sole outlier.15 In this context, the IASB has stated ‘The IASB regards

aligning IAS 37 with other IFRSs - so that all liabilities are recognised - as more important

than preserving consistency with all aspects of the existing 20-year-old Framework’ (IASB,

2010).

The IASB’s position is consistent with adopting the hypothesis that all liabilities can be

measured, and hence should be recognised. Under this view, a probability recognition

threshold is just an arbitrary and conceptually indefensible barrier. This is illustrated in the

IASB’s explanation that applying such a threshold would result in ‘the flawed conclusion that

a performance obligation arising from a guarantee, a warranty or an insurance contract should

not be recognised until it is probable that a claim will arise’ (IASB, 2006). Here, consistent

with the application of measurement theory, the IASB is rightly saying that a probability

threshold is not needed when there is an observable measurement (an entry value in these

cases). However, the IASB is also claiming that a probability threshold would be

inconsistent with a measurement based on the probability-weighted average of expected cash

flows (IASB, 2006), a claim that fails to recognise that, in the sense described in Section 3,

there can be no strict measurement based on estimates of expected future cash flows, and that

it is precisely in such cases that a probability threshold potentially has a role to play.

22

Moreover, by attempting to align IAS 37 in this way with all other IFRSs and so breaking

from consistency with the Framework’s probable outflow recognition threshold, the IASB is

asserting the general applicability of measurement theory, even for liabilities that are not

strictly measurable and for which alternative theoretical justification is needed.

As with the probability threshold, a reliable measurement threshold is rare in standards on

liabilities, in spite of its presence in the Framework (column 2 in Table 3). The criterion that

a liability must be capable of reliable measurement is explicit only in IAS 37 and in specific

parts of IAS 19.16 IAS 37 notes that ‘the use of estimates is an essential part of the

preparation of financial statements,’ yet it then claims that this ‘does not undermine their

reliability’ notwithstanding that provisions are, ‘by nature ... more uncertain than most other

items in the statement of financial position.’ This is again consistent with the Framework,

but not with measurement theory. IAS 37 concludes that, ‘except in extremely rare cases, an

entity will be able to determine a range of possible outcomes and can therefore make an

estimate of the obligation that is sufficiently reliable to use in recognising a provision.’ IAS

37 therefore comes close to acknowledging the problem of the immeasurable, but in the end

asserts the conceptually inconsistent notion of reliability. Elsewhere in IFRS, the criterion of

reliable measurement is simply assumed to be met, and so measurement theory is assumed to

be generally applicable.

This assumption of measurability, and with it the validity of the IASB’s application of

measurement theory, does not stand up to scrutiny. This can be seen by first considering

whether each DP, ED or IFRS states clearly its desired measurement attribute. As was

discussed in Section 3, the identification of the measurement attribute is fundamental to the

concept of measurement, and therefore to the general applicability of measurement theory in

IFRS. Yet, remarkably, there is not always a specified measurement attribute in IFRS.

Moreover, and even more remarkably, whenever an attribute is stated, it is in each case

23

different from any attribute stated elsewhere (column 3 of Table 3). Further, none of these

attributes is described in the same terms as any of those described in the Framework, albeit in

the 1989 text (i.e. historical cost, current cost, settlement value and present value). All of this

suggests an extraordinary lack of conceptual clarity.

Although the stated objectives in the IFRSs, EDs and DPs are all different in some way, they

can be categorised broadly into three groups: fair value, cost (subsequently amortised cost),

and the amount the entity would rationally pay at the end of the reporting period to be

relieved of the present obligation (or similar wording). The first category, fair value, is an

observable measure if there are active markets. However, the IASB also requires fair value

in situations where there are no active markets, at which point it ceases to be an observable

measurement attribute (IFRS 13, 2011). The second category, cost, is an observable measure

on initial recognition, but amortised cost in subsequent periods need not be (Thomas, 1974).

The third category, the amount the entity would rationally pay at the end of the reporting

period to be relieved of the present obligation, is the definition that the IASB has developed

for liabilities for which it wishes to recognise a cost of performance. The measurement

attribute in IAS 37, for example, is the best estimate of expenditure that an entity would

rationally pay to settle an obligation. In the 2005 ED of amendments to IAS 37, and repeated

and reinforced in the 2010 ED, the measurement attribute was clarified as being the amount

the entity would rationally pay at the end of the reporting period to be relieved of the present

obligation (Rees, 2006). This can be interpreted as an attempt to transform the cost of

performance from an estimate of future cash flows into a current attribute, and it can

therefore be seen as going some way towards the appearance of an observable measure. Yet

what we have here is a hypothetical market attribute. Conceptually, it exists at the balance

sheet, but while in principle it is observable, in practice it is not. Indeed, if it were, then there

24

would have been no need for the 2005 and 2010 EDs, because there would have been no need

to assert and defend an (invalid) application of measurement theory.

One aspect of liability measurement that is not discussed in the Framework, but that has a

strong influence in the IASB’s standards and proposals, is whether the amount initially

recognised should be linked to an amount observed (or observable) in a transaction (column 4

in Table 3). There is a fundamental difference between those liabilities where initial

recognition is at an amount identified in an exchange transaction (which is measurable), as

opposed to cases where determination of an amount to be recognised relies on estimates of

future cash flows (which is immeasurable).

Liabilities for which an initial measure can be identified in an exchange transaction are

covered by IFRS 9, the insurance contracts ED and the revenue recognition ED. In all these

cases, the initial measurement of the liability is linked to the amount identified in the

exchange transaction. This is consistent with measurement theory, because these proposals

could be characterised as stating a preference for an observable measure over a forecast of

future cash flows.

Using an observable transaction price, when one exists, does not, however, solve the problem

of what to do when one does not exist, nor if it is thought desirable to remeasure the liability

subsequent to initial recognition. In these cases, and in the absence of active markets, there is

no observable measure, yet the evidence in IFRS is that the IASB continues to presume

measurability. This leads to conceptual confusion, as the IASB employs the language of

measurement in specifying how the amount it wishes to be recognised should be determined.

To illustrate, if the cost of performance could be observed, there would be no need to

consider what expected cash flows should be included in its measurement. Because it cannot

be observed, the IASB has specified that the probability-weighted average of all possible cash

25

flows (expected value) should be used (column 5 of Table 3), arguing that this is necessary to

meet the measurement objective of an amount that the entity would pay to transfer or settle

the liability at the reporting date (for example, 2005 and 2010 EDs of amendments to IAS

37). The IASB’s position is that expected value is necessary to arrive at a meaningful

measure, whereas under a valid application of measurement theory, the question would never

arise: there is not an observable measurement attribute and therefore measurement is not

possible.

As with cash flows, if cost of performance could be observed, there would be no need to

consider what discount rate to use. In current practice, IFRSs, EDs and DPs are uniform in

their requirements and proposals that all carrying amounts that are based on estimates of

future cash flows should be discounted, whenever the impact of discounting is material

(except for IAS 12).17 There are differences, however, on which discount rate to use to reflect

the time value of money (column 6 of Table 3). There is one (almost) universal feature,

which is that all the discount rates being considered by the IASB are current rates. The only

exception to this is the rate proposed in the leases ED.18 However, even having established an

almost common approach to including the time value of money, further questions arise as to

how this should be done. For example the insurance contracts DP and ED raise the issue of

the liquidity characteristics of the liability and propose that the discount rate should reflect

the liquidity characteristics of the item being measured. All other IFRS, EDs and DPs are

silent on this issue.

A related challenge concerns adjustments for risk. There are differences in IFRS on whether

to include a risk-adjustment for the uncertainties surrounding the cash flows and, if a risk-

adjustment is included, what the objective of the risk-adjustment is, how to treat diversifiable

risk, and how to treat credit risk (column 7 of Table 3). These challenges have proved

intractable for the IASB. As with the cash flows and discount rate, however, the question of

26

the effect of risk would not need to be considered if cost of performance were an observable

measure. It is the absence of measurability that, ironically, has led the IASB to consider the

effect of risk in trying to ‘measure’ the cost of performance. For example, the IAS 37 and

insurance contracts projects both use the language of measurement to require/propose an

adjustment for risk, but only after significant debate and disagreement within the IASB over

the objective and the impact of diversifiable risk (IAS 37 2010 ED, Insurance Contracts ED).

The inclusion of own credit risk in the carrying amount of a liability has also proved

irresolvable. IAS 37 is silent on the matter, while the insurance contracts ED includes own

credit risk only in the residual margin that calibrates the liability measurement to the

transaction price.19 In 2010, the IASB decided to abandon its standalone project on own

credit risk.

The general point being illustrated here is that the practical challenges faced by the IASB in

determining expected cash flows, discount rates and risk adjustments are not issues of

measurement, even though the IASB characterises them as such. Instead, they must be

conceptualised in a different way. Those aspects of financial reporting practice that are

inadequately theorised from a measurement perspective require adoption of an alternative

theory, which is at present notable for its absence in IFRS. In the next section, we therefore

turn to this need for new theory. We first make the observation that the need is greater for

liabilities than for assets, and that this asymmetry has been overlooked in the literature. As

will be seen, this conclusion follows directly from a consideration of two related factors. The

first is that, while measurement attributes are in principle equally applicable to liabilities and

to assets, they are in practice less likely to be observable for liabilities, making measurement

inherently less achievable. The second is that the practice of conservatism in accounting

leads to the recognition of immeasurable liabilities, but not immeasurable assets. Taken

27

together, these factors lead to greater inconsistency for liabilities than for assets in the

application of measurement theory in IFRS.

6. Conservatism and the Distinctive Nature of Liabilities

We first note that the literature contains many theoretical papers and other contributions,

published over several decades, relating primarily to the measurement of assets (for example,

Edwards and Bell, 1961; Sterling, 1970). Relatively little has been published specifically

addressing liabilities.20 There are perhaps two reasons for this. First, when addressing value

attributes, it is natural and intuitive to think first of assets, or else to subsume liabilities within

net assets. Second, if a liability is conceptualised as the opposite of an asset, then an analysis

of assets can simply be viewed in the mirror for the purpose of analysing liabilities.

As will be argued in this section, however, liabilities are not simply the opposite of assets.

Moreover, the challenges of measurement are greater for liabilities than for assets, and the

need for alternative theory to underpin practice is therefore greater also.

In a straightforward case such as a fixed-rate bank loan, the asset (liability) in a bank’s

(borrower’s) accounts, is a right to receive (obligation to transfer) economic benefits: the

liability mirrors the asset, and the accounting for each counterparty is in principle identical. 21

In general, and as set out in Table 4, for any measurement attribute of an asset, there is an

analogue for a liability (see also Baxter, 1975; Nobes, 2001; Lennard, 2002; Macve, 2010;

Horton et al., 2011). For a bank loan, the measurement attribute might be an exit value, given

by the present value of contractual payments (cost of performance), the amount for which the

loan could be exchanged in the capital market (fair value), or the amount that the creditor is

contractually entitled to pay, at the balance sheet date, in full settlement of the outstanding

28

balance (cost of release).22 Alternatively, it could be either an entry cost, being the amount

that the entity would expect to receive if it chose to replace an existing loan (current

equivalent proceeds), or else a hybrid of the above (settlement amount or relief value).

** Insert Table 4 here **

While there is theoretical consistency between liabilities and assets, there are differences

resulting from data limitations that are likely to exist in practice. For many liabilities, for

example, a cost of transfer may not exist. This might arise where inflows occur in advance of

performance, for example arising from revenue contracts with customers (Samuelson, 1993).

The difference here from the earlier case of a bank loan is that, while there is an inflow of

economic benefits, the liability is in the form of a performance obligation (an expected

outflow of goods or services), rather than a contractual future cash outflow.23 Such

obligations typically have unique, entity-specific attributes, and there may be no readily

available way of transferring the liability, and hence no cost of transfer. For other liabilities,

there is no cost of release. This is often the case of with provisions, which typically have

either no underlying contract (e.g. lawsuits) or else a contract with effectively no current exit

option (e.g. pension obligations in most jurisdictions).24 Moreover, provisions can in general

be viewed as liabilities for which the debit entry on initial recognition is not an asset with an

observable value, such as cash.25 Hence there is no observable entry value. Indeed, in a case

such as a lawsuit, there is arguably no entry value at all, because there is no inflow of

resource; so the only basis for determining a carrying amount is exit value.

In principle, these observations concerning the data limitations for liabilities could also be

said to hold for some assets. This is illustrated in Table 5, which summarises the four

possible cases concerning the availability of entry and/or exit prices.

** Insert Table 5 here **

29

For many fixed assets, there is likely to be an observable entry value without an observable

exit value, where value is derived in use, while the example of an asset generated by (some)

share-based compensation illustrates the case of an exit value that is observable with an entry

value that is not observable. In general, for both assets and liabilities, where only the entry

value or exit value is observable, a typical, implicit assumption is that of an exchange of

equal value, where the (unknown) value of the asset or liability can be set equal to the

(known) value of the corresponding side of the double entry.26 In practice, however, entry

values are more likely to be observable for assets, because their acquisition is usually

associated with the sacrifice of monetary resource.27 This makes both entry valuation and

indirect exit valuation relatively difficult to attain for liabilities than for assets. In contrast,

the recognition of, for example, a provision is not triggered by a transaction stated in

monetary terms. Accordingly, while measurability may be no different in principle between

assets and liabilities, it is likely to be more problematic in practice for liabilities.28

The final case in Table 5, where neither entry nor exit value is observable, is possible for

certain intangible assets, such as internally-generated brands. Yet such cases are extremely

rare in practice for assets, but not so for liabilities. This is a particularly important

observation for this paper because carrying amounts in these cases are not measurable but are

instead estimates based only on forecasts. Consistency with measurement theory would

therefore require non-recognition. Accordingly, the IFRS requirement for greater recognition

in practice, in these cases, of liabilities rather than assets, stands in need of both explanation

and conceptual justification.29

We have so far identified a practical reason why such recognition is more likely to be

required for liabilities than for assets, but there is also an important theoretical reason, a

difference in nature, which leads to the recognition of immeasurable liabilities, but not of

immeasurable assets. This difference arises from conservatism, the effects of which can be

30

illustrated by contrasting IAS 37 with IAS 38. In the latter, it is acknowledged that for

internally-generated goodwill and some internally-generated intangible assets, it is not

possible to determine reliably their cost (ie entry value, para 49) or future economic benefits

(ie exit value, para 51). Such assets are thereby not recognised. Yet, without explanation, the

exact opposite conclusion is reached in IAS 37, where measurability is presumed for

provisions: ‘except in extremely rare cases, an entity will be able to determine a range of

possible outcomes and can therefore make an estimate of the obligation that is sufficiently

reliable to use in recognising a provision.’ (para 25) The difference here is not in

measurability but in a desired recognition outcome, and the reason for this difference is that

the practical effect of conservatism is that liabilities are not simply the opposite of assets.

Conservatism can be defined as the differential verifiability required for the recognition of

gains and losses, whereby expected losses are recognised with less verification than expected

gains (Basu, 1997; Watts, 2003a). To some extent, conservatism has been viewed in the

academic literature as evidence of tradition and convention, rather than as a practice that can

be justified conceptually (Sterling, 1970). In contrast, a more recent strand in the literature

has provided theoretical support for conservatism. In particular, a contracting explanation

(Watts, 2003a) identifies a need for conservatism as a means of addressing the moral hazard

that arises when management and investors have asymmetric information and asymmetric

payoffs. Central to this explanation is the role of verifiability, because it is optimal for

contractual metrics to have a high standard of verifiability for an entity’s net assets.

Mackintosh (2006) describes this school of thought as ‘firm in its conclusion that accounting

needs to report figures that are verifiable or “hard”.’ Empirical evidence supports both the

existence of conservatism and the contracting explanation (Basu, 1997; Watts, 2003b; Ryan,

2006; LaFond and Watts, 2008; LaFond and Roychowdhury, 2008; Giner et al, 2011).

31

On this account, the demand for conservatism creates a demand for verifiability, to mitigate

the effects of asymmetric information and payoffs (Gassen and Schwedler, 2010). Hence, in

commenting on a Preliminary Views document for a revised Framework, the Financial

Accounting Standards Committee of the American Accounting Association proposed a

‘conservative bias, wherein revenue is not reported as such unless it is clear (certain or very

highly probable) that is been) earned ... (and) expenses are reported currently (not deferred in

the form of assets’ (Benston et al., 2007). At first sight, this is consistent with the application

of measurement theory in IFRS. This is certainly true for assets, and therefore for both of the

illustrative examples employed by Benston et al. The theory of conservatism in the literature

leads to the conclusion that if an asset cannot be measured reliably, it should not be

recognised. Watts (2006), for example, calls for standard-setters to both ‘require

verifiability’ and ‘allow conservatism.’ In turn, and following the analysis in Section 4, this

implies that a probable inflow recognition threshold is not needed for assets, thereby

simplifying the algorithm in Figure 1 to the questions of definition (does an asset exist?) and

measurement (can the asset be measured reliably?).

While conservatism thereby rules out recognising asset values that are based upon forecasts,

the same need not apply to liabilities. Rather, conservatism would encourage their

recognition. Referring back to Table 5, if, in practice, entry values and exit values are

unavailable, the principle of conservatism is conventionally applied. In the case of a lawsuit,

for example, a liability of uncertain amount is typically recognised in the accounts of the

defendant (under IAS 37), while, even with no difference at all in either the amount under

consideration or the associated uncertainty, an asset is typically not recognised in the

accounts of the plaintiff (under IAS 38). Consistent with this reasoning, it was argued in

Section 4, using Table 2, that the Framework’s recognition criteria for liabilities would be

conceptually more coherent if there was recognition when an outflow of resources is probable

32

(as well as for all measurable liabilities, see Figure 1). These are applications of

conservatism, of differential verifiability, whereby immeasurable liabilities are recognised,

but not immeasurable assets. In the case of liabilities therefore, and in contrast with assets,

the theories of conservatism and of measurement are not aligned. Instead, they are in

conflict, and the association between conservatism and reduced information asymmetry duly

loses some of its force. Standard setters cannot, in this context, both require verifiability and

allow conservatism.

In practice in IFRS, conservatism is applied in accounting standards themselves while being

simultaneously denied conceptually in the Framework. The IASB has explicitly rejected the

concept of conservatism, through its use in the Framework of the language of measurement,

by which anything that is deemed to be representationally faithful is treated conceptually as a

measure. In evaluating conservatism as a candidate for ‘an aspect of faithful representation,’

the Framework (BC3.27) argues that its inclusion in this regard would be ‘inconsistent with

neutrality.’ Yet the Framework defines neutral information as ‘without bias’ (para QC 14),

which has little practical meaning when applied to unverifiable subjective estimates. In

explicitly ruling out conservatism in this way, the Framework argues from a position that is

tenable only when there is reliable measurement, and yet the theory of conservatism outlined

above applies only when there is not reliable measurement.30 The Framework therefore

dismisses conservatism on inappropriate grounds, misinterpreting it as a deliberate process of

biased measurement, rather than (in the context of liabilities) as a justification, based upon

asymmetry of information and payoffs, for recognising probable outflows in the absence of

observable measurement.31 In effect, the choice between requiring verifiability and allowing

conservatism is resolved in the wrong way: measurability is assumed rather than

immeasurability being acknowledged, and conservatism is rejected rather than required.

33

Conservatism is also not used to support IASB proposals for requirements in standards, even

when it would be a natural argument to use. For example, in terms of conservatism, not

having a probability recognition threshold for liabilities is more conservative than having

one. But the IASB does not use conservatism as a justification for the proposed removal of

the threshold from IAS 37. All its arguments are based on the flawed application of

measurement theory discussed above, which leads to the conclusion that all liabilities can be

measured and therefore should be recognised.

Conservatism also could be employed by the IASB in the analysis of credit risk. The IASB is

aiming for a measurement attribute of the amount that an entity would pay to transfer or settle

the liability at the reporting date. This would include the effect of its creditworthiness.

However, conservatism would argue against recognition of a liability at the smaller amount

caused by including the effect of credit risk, and so against recognition of a gain when an

entity’s creditworthiness decreases. Although the IASB has acknowledged the ‘counter-

intuitive’ nature of the inclusion of credit risk, it does not advance conservatism as the reason

for this counter-intuition, preferring instead to depart from its stated measurement attribute

for pragmatic reasons, without any theoretical justification (IASB, 2009, para 48).

It is only in the insurance and revenue recognition projects that conservatism is

acknowledged as a desirable concept, albeit not by name. The basis for conclusions to the

insurance contract DP argued that the observed price for the transaction with the

policyholder, although useful as a reasonableness check on the initial measurement of the

insurance liability, should not override an unbiased estimate of the amount another party

would require to take over the insurer’s contractual rights and obligations. The justification

for the IASB’s change from this approach in the insurance ED was the desire to avoid day

one gains, consistent with the revenue recognition project, and consistent also with

conservatism.

34

In summary, while conservatism does not find theoretical endorsement in IFRS, it is

nevertheless prevalent in accounting standards themselves, and it is therefore in practice

consistent with the theory outlined above from the literature. A simple need, therefore, is to

embed a theory of conservatism from the literature into IFRS. Where the literature falls short

in this regard, however, is that it is insufficiently normative. Empirical evidence points to the

existence of conservatism in practice, and underlying theory explains this practice in terms of

economic benefits. This is a positive approach, describing and attempting to explain

behaviours that have evolved in practice. Yet standard setting is a normative activity. It

exists as a market intervention, as a mechanism of policy with the explicit aim of creating

outcomes that the market itself would not be expected to generate. Viewed in this light, the

conflict between the theories of conservatism and of measurement leaves open the important

question of how this conflict might be resolved. There is therefore an implication for future

research, as will be discussed in the final section of the paper.

7. Conclusions

We set out to understand why IFRS contains multiple and inconsistent recognition and

measurement requirements for liabilities. We apply measurement theory to extant and

proposed IFRS, identifying where the theory can be said to hold and where it cannot. We

argue that, while measurement attributes for liabilities are conceptually analogous to those for

assets, measurement is relatively problematic for liabilities in practice, primarily because

conservatism encourages the recognition of liabilities that have no observable measure.

However, the IASB does not acknowledge either the limitations of measurability or the

existence of conservatism. This leads the IASB to seek all its answers within the context of

measurement, thereby missing the opportunity to adopt insights resulting from a theory of

35

conservatism. In contrast, conservatism has become increasingly important in the literature,

in particular in positive empirical studies. The literature does not, however, offer a

sufficiently normative theory of conservatism, and it therefore falls short from the perspective

of adoption by the IASB in the Framework and in accounting standards. Our paper therefore

has implications for both revisions to IFRS and for further research.

The implications for revising IFRS are as follows. First, measurement should be defined

more tightly in the Framework, in line with the analysis in Sections 3 and 4. This tightening

would make verifiability a necessary requirement for reliable measurement, in contrast with

the present state where verifiability is ‘desirable but not necessarily required.’ The tightening

would also clarify that the notion of faithful representation relates uniquely to observable

amounts, and cannot in principle relate, as in the present Framework, to the faithful

description of the process of forecasting an unobservable amount. Second, the recognition

thresholds in the Framework should be re-defined in line with Figure 1 and the associated

analysis in Section 4. Accordingly, all measurable amounts would be recognised, with the

probable outflow recognition threshold being reserved for immeasurable amounts. Third, the

probable outflow recognition threshold should be justified conceptually in the Framework.

Such justification cannot in principle be based upon measurement theory, for the reasons

argued in Section 4. Instead, and as argued in Section 6, a theory of conservatism is required

in IFRS, for which the literature provides a foundation. Fourth, and in line with the analysis

in Section 5, individual accounting standards should make a clear distinction between

amounts that are measures and those that are forecasts, noting that only the latter give rise to

the subjective issues of probability distributions of expected cash flows, discount rates and

risk adjustments.

Beyond these proposed changes to IFRS, there is also scope for further improvement, yet for

this to be possible there is a need for a normative theory of conservatism. Meeting this need

36

is an implication of the paper for further research. The potential for research in this area can

be illustrated with two examples.

The first example concerns the degree of differential verifiability that IFRS should require for

the recognition of gains and losses, and the extent to which this should vary in different

applications. For practical purposes, accounting standards need to specify not just whether

conservatism should be applied, but also to what degree. This requires understanding the

informational value of conservatism in different settings, for example where asymmetries of

incentives and information are likely to arise and why. One possible line of enquiry, which

addresses the underlying behavioural aspects of conservatism, is suggested by decision

theory. The concept of Choquet expected utility concerns decisions that are made in the

absence of a known distribution, where a decision-maker’s utility is a function of his or her

degree of ambiguity aversion, which in turn determines the desired level of conservatism

(Gilboa and Schmeidler, 1989). In this setting, which can be modelled analytically and/or

tested experimentally, the level of ambiguity can be determined endogenously by the game-

theoretic actions of other players, and so it enables analysis not just of information

asymmetry but also of incentive asymmetry.

The second example concerns financial statement presentation, in particular whether amounts

recognised conservatively should be presented differently from amounts that can be

interpreted as unbiased measures. On this question, a normative approach would seek to

develop financial statement presentation in a way that is currently not required. In this

context, an implication of the IASB’s presumption of measurability is the effective denial of

the role of forecast error in balance sheet valuation, because errors are presumed to arise from

measurement alone (Christensen, 2010b). Viewed from this perspective, the probable

outflow recognition criterion appears unacceptably imprecise and arbitrary. Indeed, it is not

needed if all liabilities are viewed as measurable. Yet if the concept of forecast error is

37

acknowledged, amounts recognised on the basis of an estimated probable outflow provide

useful information, albeit of a different nature than measurable amounts. Management’s

willingness and ability to forecast future outcomes provide information both ex ante, at the

time of the forecast, and ex post, in comparing the outcome that was forecasted with that

which ultimately arose. Acknowledgement of the role of forecasting error, and of a

distinction in financial statement presentation between measures and forecasts, and between

ex ante forecasts and ex post forecast revisions, would enhance the informational usefulness

of the financial statements (Barker, 2004; Glover et al, 2005; Gassen and Schwedler, 2010).

In conclusion, our paper is motivated by extant and important conceptual inconsistencies in

IFRS, for which the literature offers limited directly relevant analysis. We seek to apply

measurement theory in order to explain these conceptual inconsistencies, which leads to three

conclusions: first is the need to revise the treatment of recognition and measurement in IFRS,

in order to make it consistent with measurement theory; second is the need to introduce a

theory of conservatism in IFRS, in order to justify financial reporting practice that cannot be

explained by measurement theory; and third is the need to develop a normative theory of

conservatism in the literature, in order to enable and justify a greater impact on policy and

practice.

38

References

Ball, R., and L. Shivakumar (2005). The role of accruals in asymmetrically timely gain and loss recognition. Journal of Accounting Research 44, pp. 207-242.

Barker, R. (2004). Reporting Financial Performance. Accounting Horizons, 18(2), pp. 157-172.

Barth, M. (2006). Including Estimates of the Future in Today’s Financial Statements, Accounting Horizons, 20(3), pp.271-285.

Basu, S. (1997). The conservatism principle and the asymmetric timeliness of earnings. Journal of Accounting and Economics, 24, pp. 3-37.

Baxter, W.T. (1975). Accounting Values and Inflation. London: McGraw-Hill.