knowledge capital and venture capital investments: new evidence from european panel data

TRANSCRIPT

Knowledge Capital and VentureCapital Investments:New Evidence from EuropeanPanel Data

Andrea SchertlerUniversity of Kiel, Chair of Finance

Abstract. Countries with a high amount of knowledge capital are likely to havehigher volumes of venture capital (VC) investments because more researchers comeup with innovative business ideas that require venture capital finance. Using paneldata techniques, the paper finds evidence that VC investments depend strongly onthe countries’ knowledge capital measured by the number of patents, or the numberof R&D researchers, or gross domestic expenditures on R&D. In addition, the paperanalyzes whether government-financed knowledge capital fulfills a special rolefor VC investments. It finds only weak evidence that VC investments depend, with adelay of several years, on government-financed knowledge capital.

JEL classification: G24, G32.

Keywords: VC investments; knowledge capital; Western Europe; panel data.

1. INTRODUCTION

The impact of venture capital finance on knowledge creation has beendiscussed in many recent papers (see, e.g., Engel, 2003; Kortum and Lerner,2000; Mull, 1990). According to these papers, venture capital (VC) invest-ments flow into young high-technology firms that create new knowledge inthe form of patents and highly qualified employees. Thus, VC investmentscan cause knowledge creation. This is, however, not the only possible causalrelationship between venture capital finance and knowledge capital.

There are arguments for a reverse causality between venture capital financeand knowledge capital on a countrywide basis. Government-financed andbusiness-financed knowledge capital may affect VC investments positivelybecause highly qualified employees or patent owners are likely to start upfirms and require venture capital finance for their start-ups. Venture capital

German Economic Review 8(1): 64–88

r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007, 9600 Garsington Road, Oxford OX4 2DQ, UKand 350 Main Street, Malden, MA 02148, USA.

finance is interesting for those particular start-ups whose profitability can beincreased by venture capitalists’ supporting services and whose risks requiremonitoring mechanisms not embodied in standard credit and equity finance.Thus, demand for venture capital comes only from particular firms, such asyoung, innovative, high-technology firms. Compared with business-financedknowledge capital, government-financed knowledge capital may play aspecial role because government-financed basic research may lower theresearch costs of potential entrepreneurs. As a result, business-financed aswell as government-financed knowledge capital is likely to be an importantprecondition for a vibrant venture capital industry.

The key question that I study in this paper is whether countries with highknowledge capital show higher volumes of VC investments than countrieswith low knowledge capital. To answer this question, I use a panel dataset of15 European countries over the years 1991–2001. This panel dataset allowstesting whether previous years’ knowledge capital has a significant impact onthe volume of today’s VC investments. I find evidence that my measures oftotal knowledge capital, which is the sum of government-financed andbusiness-financed knowledge capital, have strong explanatory power for VCinvestments. This result is robust with regard to various measures ofknowledge capital, such as the number of patent applications, the numberof R&D researchers or gross expenditures on R&D. In addition, I find weakevidence that my measures of government-financed knowledge capital affectVC investments positively with a delay of several years.

This reverse causality, i.e. the impact of previous years’ government- andbusiness-financed knowledge capital on VC investments, has not beenaddressed in depth in the recent literature. Using a country panel dataset,Da Rin et al. (2005) have not found a significant link between governmentR&D expenditures and the ratio of VC investments in either high-technologyindustries or firms’ early stage of development to total VC investments. Forfirms listed on the Neuer Markt, Audretsch and Lehmann (2004) have notfound a significant link between the number of patents a firm holds andventure capital backing. By contrast, using a US state-level panel dataset,Gompers and Lerner (1999) have found evidence that the volume and thenumber of VC investments depend positively on the logarithm of previousyears’ real industrial R&D expenditures per capita, and, in addition, thevolume of investments depends positively on the logarithm of previous years’real academic R&D expenditures per capita.

This paper also relates to the papers by Jeng and Wells (2000) and Leleuxand Surlemont (2003), who have analyzed determinants of VC investments.1

Jeng and Wells (2000) have found evidence that the market value of initialpublic offerings has a significantly positive impact, while labor market

1. In addition, there is a growing body of literature that analyzes the impact of VC investmentson labor market performance (see, e.g., Belke et al., 2005; Fehn and Fuchs, 2004; Wasmer andWeil, 2000).

Knowledge Capital and Venture Capital Investments

r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007 65

rigidities have a significantly negative impact on VC investments. Leleuxand Surlemont (2003) have analyzed whether funds offered by publicauthorities seed the industry or whether they crowd out private funds. Theirresults support neither the seeding nor the crowding-out hypothesis. Jengand Wells (2000) and Leleux and Surlemont (2003) have, however, not takeninto account the impact of the countries’ knowledge capital on VCinvestments.

The remainder of the paper is organized as follows. In Section 2, I discussthe theoretical background for the empirical analysis. In Section 3, I describethe panel dataset, offer descriptive statistics on VC investments andknowledge capital for European countries and introduce control variablesused in the empirical analysis. In Section 4, I present estimation results on therole of total knowledge capital and government-financed knowledge capitalfor VC investments. In Section 5, I summarize the main findings of theempirical analysis.

2. THEORETICAL BACKGROUND

This paper tests two hypotheses related to the influence of knowledge capitalon the size of VC investments. My first hypothesis deals with the totalknowledge capital available in a country, which is financed by the privatesector and by governments. My second hypothesis deals with the part ofknowledge capital available in a country that is only government-financed.

Countries with a high amount of total knowledge capital are likely togenerate more business start-ups in high-technology industries thancountries with a low amount of knowledge capital. This is because thefounder of a high-technology start-up must be highly skilled and because thefounders need employees who are highly skilled, as well. Financial sources ofhigh-technology start-ups are limited. Family members and friends, impor-tant financial sources for start-ups, cannot fulfill the high capital needs ofhigh-technology start-ups. Banks cannot fulfill the high capital needs becausestart-ups in high-technology industries are likely to have low amounts ofcollateral necessary to obtain bank credits. Start-ups in high-technologyindustries have low amounts of collateral because they invest in intangibleassets more often. As Holmstrom and Tirole (1997) argue, monitoring is apartial substitute for collateral in order to mitigate incentive problems.Monitoring of start-ups in high-technology industries, however, must be ofhigh quality because start-ups in high-technology industries do not havetrack records. It may also require specific high-technology skills not commonto bank managers. In summary, the financial means of family members andfriends are limited and banks do not have the control mechanisms at theirdisposal that are necessary to mitigate adverse selection and moral hazardproblems of start-ups in high-technology industries.

A. Schertler

66 r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007

At this point, the specific role of venture capital finance, which results in apositive correlation between venture capital finance and the profitability offirms (see, e.g., Brav and Gompers, 1997; Engel, 2002; Engel and Keilbach,2002; Hellmann and Puri, 2000; Megginson and Weiss, 1991), comes intoplay. Venture capitalists are active, informed financial intermediaries. Theydo not only offer capital in the form of equity, but they actively selectpromising firms out of a large number of firms seeking finance. Using aSilicon Valley sample of firms, Hellmann and Puri (2000) have documentedthat innovator firms are more likely to be venture-capital-backed thanimitator firms. The number of innovator firms in a country is, ceteris paribus,higher in countries with high knowledge capital. This evidence and theevidence presented by Engel (2003) for Germany highlight the importance ofthe active selection process in venture capital finance.

Besides the active selection, venture capitalists are actively involved inmonitoring and supporting firms they have chosen to finance (Sahlman,1990). In the United States, lead venture capitalists, who support firms whenseveral venture capitalists invest money, spend on an average two hours perweek in firms when these firms are in their early stage of development(Gorman and Sahlman, 1989). These services are important because foundersof start-ups in high-technology industries are well qualified in their field ofexpertise, but they are likely lacking skills for the commercialization ofproduction. Thus, there is a double moral hazard problem between foundersand venture capitalists as firms’ success does not depend only on the effort ofthe entrepreneur, but also on the effort of the venture capitalist inmonitoring and supporting the firms (see, e.g., Casamatta, 2003; Lulfesmann,2000; Repullo and Suarez, 2004; Schmidt, 2003).

In summary, my first hypothesis is that the countries’ total knowledgecapital, which is the sum of business- and government-financed knowledgecapital, affects the size of VC investments positively.

My second hypothesis deals with the part of knowledge capital that hasbeen financed by governments. According to the theoretical model byKeuschnigg (2003), government-financed knowledge capital, such as basicresearch, is likely to play a special role in the size of VC invest-ments. Keuschnigg (2003) argues that the probability of researchers comingup with innovative business ideas increases with governments’ basic research.In his model, governments are interested in investing in basic researchbecause basic research is a public good. More specifically, governments’basic research in areas that lead to commercial applications reduces privatestart-up efforts, as it lowers the research costs of potential entrepreneurs.Thus, countries with a high amount of government-financed knowledgecapital are likely to generate more business ideas in high-technologyindustries than countries with a low amount of government-financedknowledge capital.

Therefore, my second hypothesis is that government-financed knowledgecapital affects the size of VC investments positively.

Knowledge Capital and Venture Capital Investments

r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007 67

3. DATA

3.1. Venture capital and knowledge capital

VC investments for 15 Western European countries are available from theEuropean Venture Capital Association (EVCA) on an annual basis. As EVCA’stotal investments, which are often called private equity investments, alsocomprise management buy-out and buy-in activities, VC investments mustbe approximated. For this, I use investments in firms’ early stage (seed andstart-up stages) in which the initial business concept is formed, prototypes ofnew products are developed and an initial marketing campaign is launched.Compared with other stages of development, such as the expansion stage, theearly stage is a very risky one. In addition to investments in the early stage, Iuse investments in firms’ early and expansion stages. In the expansion stage,firms require large amounts of external funding because the cash flow oftendoes not yet generate enough liquidity for the internal financing of the firms’growth. Because European countries differ in size, I scale investment volumesby gross domestic product (GDP). Table 1 gives a description of the variablesand data sources.

Apart from using investment volumes, I follow Gompers and Lerner (1999)and use the investment numbers scaled by population. Using the investmentnumbers is of particular interest, as high investment volumes, which mayindicate a well-developed venture capital industry, can be the result of a fewlarge investments, so that only a few firms are venture-capital-backed. Thus,the size of the venture capital industries may be overestimated when usingsolely investment volumes.

I check the robustness of the relationship between total knowledge capitaland VC investments by using VC investments in firms operating in theinformation and communications (IT) industry and VC investments in firmsoperating in the biotechnology and medical (BIO) industry. This allows me touse an industry-specific measure of knowledge capital, such as patentapplications in the IT industry and in the BIO industry.

Table 2 presents the mean values and standard deviations of investments inthe early stage, the early and expansion stages and all stages. It showssubstantial differences in investments in the early stage across Europeancountries averaged over the years 1991–2001. Investments in the early stagein Belgium, Finland and the Netherlands were higher than 0.03 per cent ofGDP. In contrast, investments in the early stage in Austria were as low as0.006 per cent of GDP.

Differences in investments in the early stage, in the early and expansionstages and in all private equity stages across countries were also substantial. Inthe United Kingdom, for example, investments in all stages accounted forabout 0.41 per cent of GDP. However, investments in the early stageaccounted for only 0.02 per cent of GDP, and investments in the early andexpansion stages for about 0.1 per cent of GDP. In the United Kingdom,

A. Schertler

68 r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007

Ta

ble

1D

ata

def

init

ion

san

dso

urc

es

Vari

ab

les

Des

crip

tio

nSo

urc

e

VC

inves

tmen

tsEarl

y-st

age

inve

stm

ents

:G

over

nm

ent-

an

dp

rivate

sect

or-

fun

ded

VC

inves

tmen

tsin

the

earl

yst

age

of

firm

s’d

evel

op

men

t(v

olu

mes

inp

erce

nt

of

GD

P,n

um

ber

sin

per

cen

to

fp

op

ula

tio

n)

Earl

y-and

expansi

on-s

tage

inve

stm

ents

:G

over

nm

ent-

an

dp

rivate

sect

or-

fun

ded

VC

inves

tmen

tsin

the

earl

yan

dex

pan

sio

nst

age

of

firm

s’d

evel

op

men

t(v

olu

mes

inp

erce

nt

of

GD

P,n

um

ber

sin

per

cen

to

fp

op

ula

tio

n)

ITin

vest

men

ts:

VC

inves

tmen

tsin

firm

so

per

ati

ng

inth

ein

form

ati

on

an

dco

mm

un

icati

on

sin

du

stry

(vo

lum

esin

per

cen

to

fG

DP,

nu

mb

ers

inp

erce

nt

of

po

pu

lati

on

)B

IOin

vest

men

ts:

VC

inves

tmen

tsin

firm

so

per

ati

ng

inth

eb

iote

chn

olo

gy

an

dm

edic

al

ind

ust

ry(v

olu

mes

inp

erce

nt

of

GD

P,n

um

ber

sin

per

cen

to

fp

op

ula

tio

n)

EV

CA

(vari

ou

sis

sues

)

Kn

ow

led

ge

cap

ital

Num

ber

ofpate

nt

appli

cati

ons

(per

cen

to

fp

op

ula

tio

n).

Th

ese

ries

nu

mb

erfo

rap

pli

cati

on

sb

yth

eEu

rop

ean

Pate

nt

Off

ice

(EPO

)is

65a.

Th

ese

ries

nu

mb

erfo

rap

pli

cati

on

sb

yth

eU

SPate

nt

Off

ice

is65b

.T

he

seri

esn

um

ber

of

the

nu

mb

ero

fp

ate

nt

ap

pli

cati

on

sto

the

EPO

inth

eIC

Tse

cto

r(p

rio

rity

yea

r)is

67.

Th

ese

ries

nu

mb

erfo

rth

en

um

ber

of

pate

nt

ap

pli

cati

on

sto

the

EPO

inth

eb

iote

chn

olo

gy

sect

or

(pri

ori

tyyea

r)is

68

Num

ber

ofR

&D

rese

arc

her

s(p

erce

nt

of

po

pu

lati

on

).C

alc

ula

ted

fro

mgo

ver

nm

ent-

fin

an

ced

R&

Dre

searc

her

s,an

db

usi

nes

sen

terp

rise

rese

arc

her

s.T

he

seri

esn

um

ber

of

go

ver

nm

ent-

fin

an

ced

R&

Dre

searc

her

sis

56.

Th

ese

ries

nu

mb

ero

fb

usi

nes

sen

terp

rise

rese

arc

her

sis

27

Main

scie

nce

an

dte

chn

olo

gy

stati

stic

s(O

EC

D,

2003)

Knowledge Capital and Venture Capital Investments

r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007 69

GER

D:

Gro

ssd

om

esti

cex

pen

dit

ure

so

nR

&D

as

ap

erce

nta

ge

of

GD

P.C

alc

ula

ted

fro

mth

ego

ver

nm

ent-

fin

an

ced

an

dth

eb

usi

nes

s-fi

nan

ced

GER

D.

Th

ese

ries

nu

mb

ero

fgo

ver

nm

ent-

fin

an

ced

GER

Dis

12.

Th

ese

ries

nu

mb

ero

fb

usi

nes

s-fi

nan

ced

GER

Dis

11

Gro

wth

inn

ewfu

nd

sra

ised

Gro

wth

rate

of

new

fun

ds

rais

edfo

rp

rivate

inves

tmen

tsEV

CA

(vari

ou

sis

sues

)

Go

ver

nm

ent

VC

fun

din

gN

ewfu

nd

sp

rovid

edb

ygo

ver

nm

ents

as

ap

erce

nta

ge

of

tota

ln

ewfu

nd

sra

ised

for

pri

vate

equ

ity

inves

tmen

tsEV

CA

(vari

ou

sis

sues

)

Pen

sio

nfu

nd

sN

ewfu

nd

sp

rovid

edb

yp

ensi

on

fun

ds

as

ap

erce

nta

ge

of

tota

ln

ewfu

nd

sra

ised

for

pri

vate

equ

ity

inves

tmen

tsEV

CA

(vari

ou

sis

sues

)

Em

plo

ym

ent

pro

tect

ion

ind

exM

easu

res

the

lab

or

mark

etri

gid

ity

thro

ugh

stri

ctn

ess

of

pro

tect

ion

again

std

ism

issa

lso

fre

gu

lar

an

dte

mp

ora

ryem

plo

ym

ent.

Tw

ovalu

esare

avail

ab

leo

ver

the

ob

serv

ati

on

per

iod

:o

ne

des

crib

esth

est

rict

nes

sin

the

late

1980s,

wh

ile

the

oth

erd

escr

ibes

the

stri

ctn

ess

inth

ela

te1990s.

Th

evalu

eo

fth

ela

te1980s

isu

sed

for

the

yea

rs1991–9

3,

wh

ile

the

valu

eo

fth

ela

te1990s

isu

sed

for

the

yea

rs1994–2

001

OEC

D(1

999,

Tab

le2.5

)

Cap

ital

gain

sta

xra

teW

orl

dw

ide

corp

ora

teta

xgu

ide

(vari

ou

sis

sues

)Len

din

gra

teIF

SC

D-R

OM

(IM

F,2003)

Gro

wth

rate

of

GD

PO

EC

DSt

ati

stic

al

Com

pen

diu

m(2

004)

Sto

ckm

ark

etre

turn

sA

nn

ual

retu

rns

on

sto

ckm

ark

ets

for

fast

-gro

win

gfi

rms

calc

ula

ted

fro

md

ail

ysh

are

ind

ices

Data

stre

am

Not

e:T

he

foll

ow

ing

cou

ntr

ies

are

incl

ud

edin

the

regre

ssio

nan

aly

sis:

Au

stri

a,

Bel

giu

m,

Den

mar

k,

Fin

lan

d,

Fra

nce

,G

erm

an

y,Ir

elan

d,

Italy

,N

eth

erla

nd

s,N

orw

ay,

Po

rtu

gal,

Spain

,Sw

eden

,Sw

itze

rlan

dan

dth

eU

nit

edK

ingd

om

.

A. Schertler

70 r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007

Ta

ble

2V

Cin

ves

tmen

tsin

Eu

rop

e

Earl

y-s

tage

inves

tmen

ts

Earl

y-

an

dex

pan

sio

n-s

tage

inves

tmen

tsIT

inves

tmen

tsB

IOin

ves

tmen

tsPri

vate

equ

ity

inves

tmen

ts

Vo

lum

eN

um

ber

Vo

lum

eN

um

ber

Vo

lum

eN

um

ber

Vo

lum

eN

um

ber

Vo

lum

eN

um

ber

Au

stri

aM

ean

0.5

80

0.0

38

1.6

76

0.0

67

0.7

04

0.0

30

0.1

62

0.0

10

2.1

00

0.0

70

Stan

dard

dev

iati

on

0.9

54

0.0

48

2.5

54

0.0

84

1.2

26

0.0

45

0.2

46

0.0

14

2.9

35

0.0

88

Bel

giu

mM

ean

3.2

82

0.0

96

9.5

03

0.2

06

4.3

77

0.0

92

1.1

81

0.0

21

11.1

30

0.2

27

Stan

dard

dev

iati

on

3.6

95

0.0

89

7.2

90

0.1

35

4.7

18

0.0

92

1.0

88

0.0

14

8.0

28

0.1

39

Den

mark

Mea

n1.3

66

0.0

71

3.9

14

0.1

47

1.7

81

0.0

60

1.1

94

0.0

43

5.1

11

0.1

67

Stan

dard

dev

iati

on

2.4

71

0.0

88

4.9

73

0.1

42

2.7

35

0.0

80

2.0

97

0.0

62

6.2

75

0.1

68

Fin

lan

dM

ean

3.4

13

0.2

22

7.1

96

0.3

56

3.3

89

0.1

43

1.5

32

0.0

76

10.2

81

0.4

06

Stan

dard

dev

iati

on

3.9

06

0.2

06

6.0

78

0.2

52

3.7

04

0.1

38

1.7

29

0.0

64

9.6

09

0.2

82

Fra

nce

Mea

n1.8

67

0.0

73

7.0

64

0.2

28

3.6

94

0.0

95

0.9

68

0.0

31

14.0

39

0.3

15

Stan

dard

dev

iati

on

2.4

96

0.0

66

5.3

90

0.0

83

4.8

64

0.0

61

0.6

13

0.0

07

9.3

10

0.0

91

Ger

man

yM

ean

2.2

35

0.0

72

6.7

43

0.1

47

2.2

96

0.0

47

1.2

06

0.0

21

9.2

60

0.1

59

Stan

dard

dev

iati

on

2.7

47

0.0

59

5.5

63

0.0

96

2.7

90

0.0

44

1.5

10

0.0

23

7.5

36

0.0

99

Irel

an

dM

ean

2.2

80

0.0

92

7.4

19

0.2

33

4.5

14

0.1

35

0.4

20

0.0

12

8.7

71

0.2

57

Stan

dard

dev

iati

on

3.1

85

0.1

00

4.9

58

0.1

52

5.6

04

0.1

45

0.3

54

0.0

08

5.1

11

0.1

61

Italy M

ean

1.2

16

0.0

20

4.6

23

0.0

40

1.3

87

0.0

11

0.0

79

0.0

02

9.2

41

0.0

51

Stan

dard

dev

iati

on

1.2

94

0.0

16

3.3

83

0.0

25

3.0

91

0.0

17

0.2

14

0.0

01

7.3

53

0.0

26

Knowledge Capital and Venture Capital Investments

r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007 71

Net

her

lan

ds

Mea

n3.7

45

0.0

94

14.8

05

0.2

61

5.8

94

0.1

06

1.2

52

0.0

27

23.9

40

0.3

35

Stan

dard

dev

iati

on

3.0

97

0.0

49

9.1

02

0.0

91

5.0

73

0.0

64

0.7

15

0.0

11

15.4

49

0.1

25

No

rway

Mea

n1.4

46

0.0

99

8.5

03

0.3

30

4.3

44

0.1

48

0.5

07

0.0

39

9.8

46

0.3

63

Stan

dard

dev

iati

on

1.7

28

0.0

80

4.3

02

0.1

43

4.3

15

0.1

03

0.6

07

0.0

27

5.2

81

0.1

44

Po

rtu

gal

Mea

n1.0

53

0.0

27

6.1

37

0.0

95

1.3

59

0.0

15

0.4

15

0.0

03

8.4

31

0.1

11

Stan

dard

dev

iati

on

0.6

44

0.0

17

2.4

00

0.0

30

1.8

64

0.0

13

1.0

71

0.0

02

3.3

61

0.0

33

Spain

Mea

n1.0

15

0.0

21

5.6

08

0.0

61

1.2

23

0.0

11

0.4

50

0.0

03

7.5

90

0.0

66

Stan

dard

dev

iati

on

0.9

09

0.0

10

3.9

87

0.0

17

1.6

62

0.0

11

0.7

64

0.0

01

6.0

24

0.0

18

Swed

enM

ean

2.8

13

0.1

42

9.3

20

0.2

55

4.7

75

0.1

25

2.4

78

0.0

52

26.7

08

0.2

94

Stan

dard

dev

iati

on

4.3

67

0.2

08

11.6

06

0.3

09

6.4

88

0.1

65

3.3

60

0.0

70

32.7

87

0.3

34

Swit

zerl

an

dM

ean

1.5

16

0.0

51

4.0

38

0.1

19

1.8

02

0.0

59

0.7

13

0.0

18

7.2

24

0.1

46

Stan

dard

dev

iati

on

2.4

67

0.0

63

4.2

11

0.1

07

1.9

42

0.0

63

0.8

49

0.0

20

7.1

81

0.1

15

Un

ited

Kin

gd

om

Mea

n2.1

53

0.0

46

12.8

84

0.2

10

7.2

79

0.0

81

3.4

28

0.0

38

41.4

58

0.3

38

Stan

dard

dev

iati

on

3.1

28

0.0

41

9.6

19

0.0

47

6.0

37

0.0

47

3.3

48

0.0

11

23.7

06

0.0

40

Not

e:T

his

tab

lere

po

rts

des

crip

tive

stati

stic

sfo

rEu

rop

ean

cou

ntr

ies

(1991–2

001).

Vo

lum

esare

as

ap

erce

nta

ge

ofG

DP,

mu

ltip

lied

by

100.N

um

ber

sare

as

ap

erce

nta

ge

of

po

pu

lati

on

,m

ult

ipli

edb

y100.

IT(B

IO)

inves

tmen

tsare

inves

tmen

tsin

ven

ture

-cap

ital

-back

edfi

rms

op

erati

ng

inth

ein

form

ati

on

an

dco

mm

un

icati

on

s(b

iote

chn

olo

gy

an

dm

edic

al)

ind

ust

ry.

A. Schertler

72 r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007

private equity was most often used to finance management buy-out deals. InFinland, by contrast, investments in all stages accounted for about 0.1 percent of GDP, while investments in the early stage accounted for 0.03 per cent,and investments in the early and expansion stages accounted for 0.07 percent of GDP. Thus, compared with the situation in the United Kingdom,private equity was substantially less often used to finance management buy-out deals.

Table 2 also informs on the importance of private equity investments inthe IT and BIO industries. According to industry investment volumes andnumbers, IT firms received more than three times as much private equity asBIO firms.

For the countries’ total knowledge capital, I use either the number ofpatent applications to the European or the US Patent Office scaled bypopulation, or the number of R&D researchers scaled by population, or thegross domestic expenditures on R&D scaled by GDP (GERD). For thecountries’ government-financed knowledge capital, I use either the govern-ment-financed number of R&D researchers scaled by population, or thegovernment-financed GERD scaled by GDP. Table 3 offers the mean valuesand standard deviations for the variables measuring knowledge capital. Itindicates that the countries also differ with respect to the knowledge capitalavailable in the countries.

Before I analyze whether the countries’ knowledge capital helps inexplaining VC investments, I discuss in the following the variables for whichI control in the empirical analysis.

3.2. Control variables

Recent theoretical and empirical literature has argued that VC investmentsdepend on the volume of new funds raised for private equity and venturecapital deals, new funds provided by governments and pension funds,developments in stock markets for fast-growing firms, labor market regula-tions and taxation of capital gains. In particular, a boost in new funds raisedmay lead to higher investments in later stages and to lower investments inthe early stage (Gompers, 1998). This is because firms in the early stagecannot employ as much capital as firms in later stages, and becausemonitoring capacities of venture capitalists cannot be increased in the shortrun (Keuschnigg, 2003). In order to control for changes in the conditions ofnew funds raised, I use the growth rate in new funds raised for private equityinvestments.

New funds provided by governments may have a positive impact on thesize of the venture capital industry in the case of positive externalities(Gebhardt and Schmidt, 2002; Lerner, 2002a), while they may have a negativeimpact in the case of adverse incentives on deal selection (EuropeanCommission, 2000; Keuschnigg and Nielsen, 2001; Murray and Marriot,1998). I take the role of governments into account by using the share of new

Knowledge Capital and Venture Capital Investments

r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007 73

Ta

ble

3K

no

wle

dge

cap

ital

inEu

rop

e Pate

nts

R&

Dre

searc

her

sG

ER

D

US

off

ice

Eu

rop

ean

off

ice

ITB

IOTo

tal

Go

ver

nm

ent-

fin

an

ced

To

tal

Go

ver

nm

ent-

fin

an

ced

Au

stri

aM

ean

0.0

061

0.0

105

0.0

016

0.0

004

0.3

023

0.0

106

1.4

509

0.7

191

Stan

dard

dev

iati

on

0.0

011

0.0

026

0.0

007

0.0

001

0.0

631

0.0

012

0.0

474

0.0

373

Bel

giu

mM

ean

0.0

064

0.0

093

0.0

019

0.0

007

0.3

965

0.0

125

1.6

441

0.4

386

Stan

dard

dev

iati

on

0.0

009

0.0

023

0.0

007

0.0

003

0.0

736

0.0

040

0.1

147

0.0

373

Den

mark

Mea

n0.0

080

0.0

114

0.0

021

0.0

014

0.5

053

0.0

648

1.7

273

0.6

782

Stan

dard

dev

iati

on

0.0

017

0.0

036

0.0

013

0.0

004

0.0

914

0.0

076

0.2

427

0.0

243

Fin

lan

dM

ean

0.0

139

0.0

176

0.0

086

0.0

005

0.6

398

0.0

762

2.5

132

0.8

541

Stan

dard

dev

iati

on

0.0

035

0.0

067

0.0

049

0.0

001

0.2

269

0.0

098

0.5

070

0.0

384

Fra

nce

Mea

n0.0

064

0.0

100

0.0

027

0.0

004

0.4

083

0.0

439

2.0

655

0.9

327

Stan

dard

dev

iati

on

0.0

007

0.0

016

0.0

007

0.0

001

0.0

226

0.0

027

0.0

776

0.1

171

Ger

man

yM

ean

0.0

123

0.0

195

0.0

042

0.0

005

0.5

338

0.0

453

2.3

073

0.8

336

Stan

dard

dev

iati

on

0.0

022

0.0

050

0.0

017

0.0

003

0.0

297

0.0

016

0.1

030

0.0

406

Irel

an

dM

ean

0.0

034

0.0

036

0.0

012

0.0

002

0.2

820

0.0

096

1.0

720

0.2

850

Stan

dard

dev

iati

on

0.0

014

0.0

016

0.0

008

0.0

001

0.0

779

0.0

036

0.1

266

0.0

272

Italy M

ean

0.0

028

0.0

051

0.0

008

0.0

001

0.1

570

0.0

236

1.0

400

0.5

550

Stan

dard

dev

iati

on

0.0

004

0.0

012

0.0

002

0.0

000

0.0

049

0.0

007

0.0

921

0.0

378

A. Schertler

74 r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007

Net

her

lan

ds

Mea

n0.0

079

0.0

144

0.0

059

0.0

007

0.3

509

0.0

476

1.7

482

0.8

136

Stan

dard

dev

iati

on

0.0

011

0.0

050

0.0

033

0.0

003

0.0

633

0.0

042

0.0

792

0.1

044

No

rway

Mea

n0.0

052

0.0

061

0.0

014

0.0

003

0.4

775

0.0

674

1.5

432

0.7

414

Stan

dard

dev

iati

on

0.0

011

0.0

017

0.0

006

0.0

001

0.0

622

0.0

027

0.0

455

0.0

672

Po

rtu

gal

Mea

n0.0

001

0.0

002

0.0

000

0.0

000

0.0

389

0.0

278

0.5

743

0.4

243

Stan

dard

dev

iati

on

0.0

000

0.0

001

0.0

000

0.0

000

0.0

139

0.0

067

0.1

179

0.0

739

Spain

Mea

n0.0

006

0.0

013

0.0

002

0.0

000

0.1

164

0.0

245

0.7

809

0.3

836

Stan

dard

dev

iati

on

0.0

001

0.0

005

0.0

001

0.0

000

0.0

257

0.0

050

0.0

413

0.0

378

Swed

enM

ean

0.0

160

0.0

188

0.0

058

0.0

006

0.6

948

0.0

266

3.2

314

0.9

441

Stan

dard

dev

iati

on

0.0

038

0.0

053

0.0

027

0.0

002

0.1

046

0.0

030

0.3

759

0.0

519

Swit

zerl

an

dM

ean

0.0

186

0.0

288

0.0

056

0.0

009

0.6

685

0.0

073

2.4

700

0.6

922

Stan

dard

dev

iati

on

0.0

013

0.0

056

0.0

021

0.0

003

0.0

363

0.0

012

0.0

517

0.0

510

Un

ited

Kin

gd

om

Mea

n0.0

062

0.0

075

0.0

023

0.0

005

0.4

021

0.0

238

1.5

527

0.6

050

Stan

dard

dev

iati

on

0.0

008

0.0

015

0.0

008

0.0

002

0.0

153

0.0

027

0.1

357

0.0

673

Not

e:T

his

tab

lere

po

rts

des

crip

tive

stati

stic

sfo

rEu

rop

ean

cou

ntr

ies

(1991–2

001).

ITd

eno

tes

the

info

rmati

on

an

dco

mm

un

icati

on

sin

du

stry

.B

IOd

eno

tes

the

bio

tech

no

logy

an

dm

edic

al

ind

ust

ry.Pate

nts

an

dR

&D

rese

arch

ers

are

scale

db

yp

op

ula

tio

n.G

ER

Dis

the

gro

ssex

pen

dit

ure

so

nR

&D

as

ap

erce

nta

ge

of

GD

P.

Ta

ble

3C

on

tin

ued

Pate

nts

R&

Dre

searc

her

sG

ER

D

US

Off

ice

Eu

rop

ean

off

ice

ITB

IOTo

tal

Go

ver

nm

ent-

fin

an

ced

To

tal

Go

ver

nm

ent-

fin

an

ced

Knowledge Capital and Venture Capital Investments

r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007 75

funds provided by governments divided by total new funds for private equityinvestments.

I control for the role of pension funds whose change in regulation has hada significant effect on the development of the venture capital industry in theUnited States (Gompers and Lerner, 1999; Lerner, 2002b). I use new fundsprovided by pension funds relative to total new funds. This variable reflectstwo important aspects of pension funding. It reflects that the assets managedby pension funds in European countries differ in size (see OECD InstitutionalInvestor Database, 2003). Moreover, it reflects regulations concerning thepercentage of pension funds’ portfolios that can be invested in high-risk assetclasses. For example, in Spain, pension funds can invest up to 10 per cent oftheir portfolios in unquoted firms (Tejada, 2003a), while in Portugal, pensionfunds can invest 15 per cent of their portfolios in unquoted firms (Tejada,2003b).

Developments in stock markets for fast-growing firms are likely to affectthe size of VC investments positively (Bascha and Walz, 2001; Black andGilson, 1998; Gompers, 1996). In order to capture developments in stockmarkets for fast-growing firms, I create a variable for annual stock marketreturns calculated from daily return indices of Europe’s stock markets for fast-growing firms. For Germany, I use the share index of the Neuer Marktfounded in 1997. For France, I use the share index of the Nouveau Marchefounded in 1996. For Spain, I use the share index of the Nuevo Mercadofounded in 2000. For the United Kingdom, I use the share index of theAlternative Investment Market founded in 1995. For all other countries, I usethe share index of the EASDAQ founded in 1996.

In addition to stock market returns, I use a dummy variable that equals onein 1999 and 2000 and zero otherwise. This dummy variable captures theextraordinary development in stock markets for fast-growing firms at the endof the 1990s that might result from periodically overoptimistic investors andfrom firms using the opportunity to go public in times of higher stock prices(Ritter, 1991).

Moreover, I control for labor market regulations emphasized, for example,by Da Rin et al. (2005) by taking into account differences in employmentprotection, for the price for alternative finance by using lending rates, and forthe capital gains taxes emphasized, for example, by Gompers and Lerner(1999) and Poterba (1989).

4. EMPIRICAL ANALYSIS

4.1. Specification of the regression equation

In order to test whether the various measures of total knowledge capitalhave a significant impact on VC investments, I start from the followingspecification:

A. Schertler

76 r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007

VCit ¼ Kit�2aþ eit ; t ¼ 1; . . . ;T ; i ¼ 1; . . . ; N ð1Þ

where Kit�2 denotes the variable that measures knowledge capital in yeart�2, a denotes a coefficient to be estimated and eit denotes the error vector.

As the degree of integration affects the empirical specification that I canuse, I perform the panel unit root tests developed by Levin et al. (2002), whichassumes identical coefficients across countries, and the test developed by Imet al. (2003), which allows for heterogeneous coefficients across countries.Generally, I cannot reject the hypothesis of non-stationarity for variousmeasures of VC investments scaled either by GDP or population, as well as myvarious measures of knowledge capital.2 Therefore, I specify the followingmodel based on first differences that are stationary:

DVCit ¼ DKit�2aþ Deit ; t ¼ 1; . . . ;T ; i ¼ 1; . . . ; N ð2Þ

where Dait ¼ ait � ait�1 denotes the first difference of the variable a.Then I add my control variables, which are stationary:3

DVCit ¼ Xitbþ DKit�2aþ Deit ; t ¼ 1; . . . ; T ; i ¼ 1; . . . ; N ð3Þ

where Xit denotes the matrix of my control variables and b denotes acoefficient vector to be estimated.

My estimation strategy is as follows: I estimate (3) as a cluster model byusing OLS and a country-specific correction of the standard errors(Wooldridge, 2002). The cluster model is robust to misspecifications in theform of heteroskedasticity and correlation within the observations of acountry.

4.2. Total knowledge capital

In this section, I test my first hypothesis, which says that VC investments arelikely to be higher in those countries that are well endowed with knowledgecapital. The estimation results are presented in Table 4.

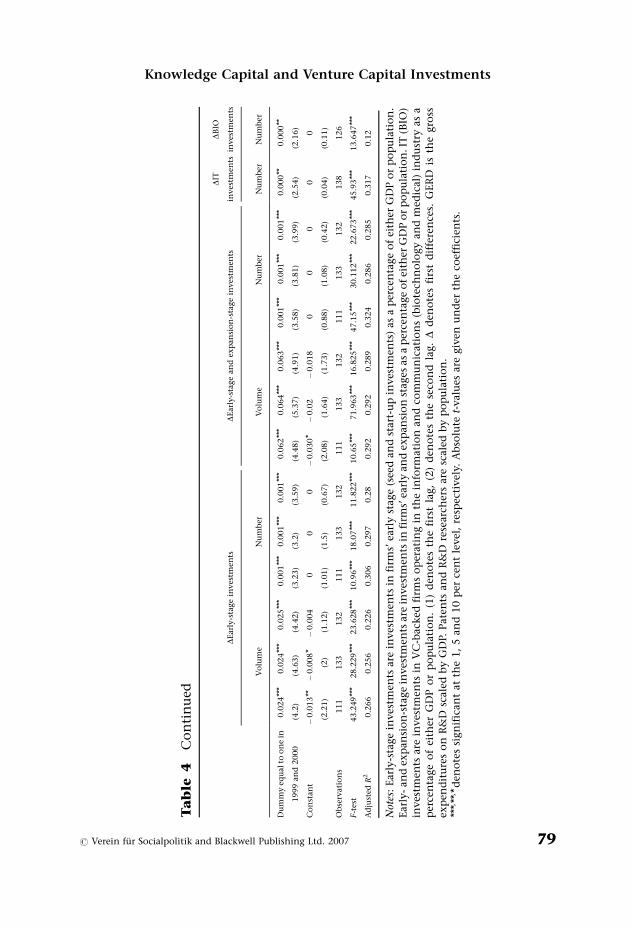

I find strong evidence in favor of my first hypothesis. The number ofpatents has a positive and significant impact on the volume and the numberof investments in the early stage, and in the early and expansion stages. Thenumber of R&D researchers has a significantly positive impact on the volumeand number of investments in the early stage, and on the number ofinvestments in the early and expansion stages. In addition, GERD has apositive and significant effect on the number of investments in the early stageand in the early and expansion stages.

The signs and significances of the coefficients of my variables capturingknowledge capital are robust with respect to alternative model specifications.

2. The results of panel unit root tests are available from the author on request.3. First differencing the control variables does not change the results with respect to the effects

of knowledge capital on VC investments.

Knowledge Capital and Venture Capital Investments

r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007 77

Ta

ble

4To

tal

kn

ow

led

ge

cap

ital

DEarl

y-s

tage

inves

tmen

tsD

Earl

y-s

tage

an

dex

pan

sio

n-s

tage

inves

tmen

ts

DIT

inves

tmen

ts

DB

IO

inves

tmen

ts

Vo

lum

eN

um

ber

Vo

lum

eN

um

ber

Nu

mb

erN

um

ber

DPate

nts

US

off

ice

(2)

9.8

73**

*0.3

68**

13.6

17**

0.5

35**

(3.3

4)

(2.7

5)

(2.5

5)

(2.8

4)

DR

&D

rese

arc

her

(2)

0.1

79**

*0.0

08**

0.0

81

0.0

08**

(3.2

5)

(2.9

1)

(0.5

6)

(2.9

1)

DG

ER

D(2

)0.0

24

0.0

02**

�0.0

37

0.0

03**

(1.2

5)

(2.1

6)

(1.0

2)

(2.3

2)

DIn

du

stry

pate

nts

(2)

0.2

65**

*0.6

05**

(3.8

1)

(2.1

7)

Gro

wth

rate

of

new

fun

ds

rais

ed(1

)

�0.0

77

�0.0

36

�0.0

39

�0.0

01

0�

0.0

01

�0.1

85*�

0.1

04

�0.0

86

�0.0

02

00

00.0

01

(1.6

7)

(1.3

)(1

.23)

(0.5

3)

(0.1

5)

(0.7

2)

(2.0

1)

(1.0

5)

(0.8

7)

(0.4

3)

(0.2

1)

(0.2

)(0

.1)

(0.9

8)

New

fun

ds

of

go

ver

nm

ents

(1)

�0.0

17

0.0

01

�0.0

03

00.0

00**

0�

0.0

42

�0.0

01

�0.0

06

00.0

01*

00

0.0

00*

(1.6

6)

(0.1

9)

(0.4

1)

(0.5

3)

(2.2

5)

(1.2

7)

(1.5

3)

(0.0

6)

(0.4

1)

(0.1

5)

(1.8

9)

(0.9

5)

(0.6

)(1

.83)

New

fun

ds

of

pen

sio

n

fun

ds

(1)

0.0

06

0.0

15

0.0

17

00.0

01**

0.0

01*

0.0

45

0.0

54

0.0

61

00.0

01

0.0

01

00

(0.2

9)

(1.0

6)

(1.2

5)

(0.6

)(2

.19)

(2.0

4)

(1.0

5)

(1.3

)(1

.5)

(0.2

9)

(1.1

9)

(1.1

2)

(1.7

1)

(0.1

9)

Em

plo

ym

ent

pro

tect

ion

ind

ex

�0.0

01

�0.0

01

00

00

0.0

01

0.0

02

0.0

03

00

00

0

(0.5

4)

(0.4

3)

(0.3

3)

(0.2

2)

(0.1

2)

(0)

(0.1

9)

(0.5

8)

(0.8

6)

(0.9

9)

(0.2

7)

(0.4

3)

(0.0

1)

(0.5

8)

Cap

ital

gain

sta

xra

te0

00

00

00

00

00

00

0

(1.1

3)

(0.3

7)

(0.5

3)

(1.5

9)

(1.5

2)

(1.1

9)

(0.4

6)

(1.4

3)

(1.0

4)

(0.5

)(0

.53)

(0.5

4)

(0.9

4)

(0.2

5)

Len

din

gra

te0.1

33

0.0

63

0.0

35

00.0

01

00.1

82

0.0

2�

0.0

08

0�

0.0

01

�0.0

02

00

(1.5

1)

(1.5

)(0

.87)

(0.0

1)

(0.6

1)

(0.2

2)

(0.7

7)

(0.1

4)

(0.0

7)

(0.1

2)

(0.7

5)

(1.2

4)

(0.2

3)

(0.1

1)

Gro

wth

rate

of

GD

P0.0

75**

0.0

15

0.0

15

0.0

03**

*0.0

01

0.0

01

0.0

6�

0.0

12

�0.0

03

0.0

03**

0.0

01

0.0

01

0.0

01

0

(2.7

8)

(1.0

2)

(0.9

8)

(3.2

2)

(1.2

3)

(0.7

5)

(1.2

5)

(0.4

3)

(0.0

8)

(2.5

6)

(1.1

7)

(0.9

)(0

.93)

(0.1

6)

Sto

ckm

ark

etre

turn

s0.0

28*

0.0

41**

0.0

42**

0.0

01

0.0

01**

0.0

01**

*0.0

63**

0.0

79**

*0.0

79**

*0.0

01

0.0

01**

0.0

02**

0.0

01*

0

(2.0

8)

(2.9

5)

(2.9

3)

(1.6

7)

(2.9

3)

(3.0

9)

(2.7

4)

(3.3

3)

(3.3

1)

(1.4

6)

(2.2

)(2

.3)

(2.0

3)

(0.4

1)

A. Schertler

78 r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007

Du

mm

yeq

ualto

on

ein

1999

an

d2000

0.0

24**

*0.0

24**

*0.0

25**

*0.0

01**

*0.0

01**

*0.0

01**

*0.0

62**

*0.0

64**

*0.0

63**

*0.0

01**

*0.0

01**

*0.0

01**

*0.0

00**

0.0

00**

(4.2

)(4

.63)

(4.4

2)

(3.2

3)

(3.2

)(3

.59)

(4.4

8)

(5.3

7)

(4.9

1)

(3.5

8)

(3.8

1)

(3.9

9)

(2.5

4)

(2.1

6)

Co

nst

an

t�

0.0

13**�

0.0

08*�

0.0

04

00

0�

0.0

30*�

0.0

2�

0.0

18

00

00

0

(2.2

1)

(2)

(1.1

2)

(1.0

1)

(1.5

)(0

.67)

(2.0

8)

(1.6

4)

(1.7

3)

(0.8

8)

(1.0

8)

(0.4

2)

(0.0

4)

(0.1

1)

Ob

serv

ati

on

s111

133

132

111

133

132

111

133

132

111

133

132

138

126

F-t

est

43.2

49**

*28.2

29**

*23.6

28

***

10.9

6**

*18.0

7**

*11.8

22

***

10.6

5**

*71.9

63

***

16.8

25**

*47.1

5**

*30.1

12

***

22.6

73**

*45.9

3**

*13.6

47**

*

Ad

just

edR

20.2

66

0.2

56

0.2

26

0.3

06

0.2

97

0.2

80.2

92

0.2

92

0.2

89

0.3

24

0.2

86

0.2

85

0.3

17

0.1

2

Not

es:

Ear

ly-s

tage

inves

tmen

tsare

inves

tmen

tsin

firm

s’ea

rly

stage

(see

dan

dst

art

-up

inves

tmen

ts)

as

ap

erce

nta

ge

of

eith

erG

DP

or

po

pu

lati

on

.Earl

y-an

dex

pan

sio

n-s

tage

inves

tmen

tsare

inves

tmen

tsin

firm

s’ea

rly

an

dex

pan

sio

nst

ages

as

ap

erce

nta

ge

ofei

ther

GD

Po

rp

op

ula

tio

n.IT

(BIO

)in

ves

tmen

tsare

inves

tmen

tsin

VC

-back

edfi

rms

op

erat

ing

inth

ein

form

ati

on

an

dco

mm

un

icat

ion

s(b

iote

chn

olo

gy

an

dm

edic

al)

ind

ust

ryas

ap

erce

nta

ge

of

eith

erG

DP

or

po

pu

lati

on

.(1

)d

eno

tes

the

firs

tla

g,

(2)

den

ote

sth

ese

con

dla

g.D

den

ote

sfi

rst

dif

fere

nce

s.G

ER

Dis

the

gro

ssex

pen

dit

ure

so

nR

&D

scale

db

yG

DP.

Pate

nts

an

dR

&D

rese

arch

ers

are

scale

dby

po

pu

lati

on

.**

*,**

, *d

eno

tes

sign

ific

an

tat

the

1,

5an

d10

per

cen

tle

vel

,re

spec

tivel

y.A

bso

lute

t-val

ues

are

giv

enu

nd

erth

eco

effi

cien

ts.

Ta

ble

4C

on

tin

ued

DEarl

y-s

tage

inves

tmen

tsD

Earl

y-s

tage

an

dex

pan

sio

n-s

tage

inves

tmen

ts

DIT

inves

tmen

ts

DB

IO

inves

tmen

ts

Vo

lum

eN

um

ber

Vo

lum

eN

um

ber

Nu

mb

erN

um

ber

Knowledge Capital and Venture Capital Investments

r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007 79

As a first robustness check, I estimate whether private equity investments inselected industries depend on the number of patent applications in theseindustries. The results of this exercise are also reported in Table 4. Theestimation results show that an increase in the number of patents in the ITindustry leads to an increase in the number of private equity investments inIT firms. Moreover, an increase in the number of patents in the BIO industryleads to an increase in the number of private equity investments in BIO firms.Thus, using a closer specification of knowledge capital for particularindustries leads to the same conclusion as the broader specification ofknowledge capital: the countries’ total knowledge capital explains the size ofVC investments.

As a second robustness check, I estimate my model for two sub-samples.In a first sub-sample, I exclude the United Kingdom, because the Britisheconomy is more market-based than the other European economiesconsidered here (Beck and Levine, 2002). In a second sub-sample, I excludelarge countries, i.e. France, Germany and the United Kingdom. The sizeof an economy may have implications for the knowledge capital coefficients,as large economies may be more efficient in realizing economies of scale.Venture capitalists operating in large economies may realize economies ofscale more often, as they may have more opportunities to syndicate theirinvestments and to concentrate their investment activity on particulartechnologies and stages of firms’ development. By focusing their invest-ment activity on particular stages and technologies, venture capitalists mayaccumulate more specific experience necessary for the successful selectionand monitoring of high-technology firms. Economies of scale may bereflected in lower coefficients of the variables capturing knowledge capital.Moreover, in the second half of the 1990s, the large countries in my samplehave developed comparatively liquid stock market segments for fast-growingfirms, while the small countries have failed to develop liquidity in thesemarkets (Bottazzi and Da Rin, 2002; Tejada, 2003a).

The robustness check reveals that neither excluding the UnitedKingdom nor the three largest countries from the sample changes myestimation results for VC investments substantially.4 When excluding theUnited Kingdom, I observe smaller coefficients of the variables capturingknowledge capital. The t-values are also lower. However, changes in the sizeand significance do not change the conclusion of my empirical analysis.When excluding the three largest countries, I observe in some specificationsan increase in the size of the coefficients and their significance. For example,GERD helps in explaining investments in the early stage when large countriesare excluded from the sample. Overall, however, there is a high degree ofsimilarity between the estimation results of the sub-samples and the fullsample.

4. The results of the robustness checks are available from the author on request.

A. Schertler

80 r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007

What about the signs and significance of the coefficients of my controlvariables? A boost in new funds raised has the expected negative andsignificant impact on the volume of investments in the early and expansionstages only in one specification. It does not affect investments in the earlystage.

New funds provided by governments have the expected positive andsignificant effect on the number of investments in the early stage in one outof three model specifications presented in Table 4 but they do not affect theinvestments volume in the early stage. In a related paper, Leleux andSurlemont (2003) have analyzed the impact of public authorities’ funding ofVC investments. They have found a positive and significant effect ofgovernment funding on the volume of VC investments. Thus, contrary tothe results by Leleux and Surlemont (2003), I do not find a significantrelationship between government funding and volumes of VC investments.The difference in the results may be caused by different model specifications:Leleux and Surlemont (2003) have used volumes of VC investments, while Iuse first differences because of their non-stationary behavior.

Funds provided by pension funds help in explaining the number ofinvestments in the early stage. New funds provided by pension funds have apositive and significant impact on the number of investments in the earlystage but not on investments in the early and expansion stages. This is in linewith the evidence presented in Schertler (2005): new funds provided bypension funds, as compared with funds provided by corporate investors, aremore often used for financing early-stage deals than later stage deals. Recentliterature has analyzed the role of pension funds by including the wealth ofpension funds in the regression analysis instead of the share of new fundsprovided by pension funds. Jeng and Wells (2000) have found evidence thatthe wealth of private pension funds is a significant determinant of venturecapital fundraising over time but not across countries. Schertler (2004) hasnot found a significant relationship between assets of pension funds and VCinvestments. As I mentioned before, assets of pension funds can be a poormeasure of pension funds activity in venture capital industries because thepension funds are allowed to invest different amounts of their assets inunquoted firms.

The stock market returns of fast-growing firms have a positive andsignificant impact on the volume and the number of investments in theearly stage, in the early and expansion stages and in IT. The higher the returnsare, the higher the increase in VC investments. This result is in line withprevious results. Using US data, Gompers and Lerner (1999) have documen-ted that the previous year’s equity market return has a positive effect on theinvestment number but not on the investment volume. Using a panel datasetsimilar to the one used here, Da Rin et al. (2005) have found that the ratio ofinvestments in the early stage to total private equity investments dependspositively on a dummy variable equal to one if a stock market for fast-growingfirms is available in a particular country.

Knowledge Capital and Venture Capital Investments

r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007 81

The growth rate of GDP helps in explaining the volume and the number ofinvestments in the early stage only when I use the number of patentapplications. Gompers and Lerner (1999) and Romain and van Pottelsberghe(2004) have documented a procyclical behavior of VC investments. Gompersand Lerner (1999) find that the growth of gross state products leads to anincrease in VC investments. In the paper by Romain and van Pottelsberghe(2004), which is based on a sample similar to the one used here, the growthrate of GDP is positive and significant in all model specifications, while I finda significantly positive impact only in some specifications. This may bebecause I use a first-difference approach, while Romain and van Pottelsberghe(2004) use VC investments in levels.

Other control variables included, i.e. the lending rate, the employmentprotection index and the capital gains tax rate, do not explain the variousmeasures of VC investments, except the dummy variable, which is equal toone for the years 1999 and 2000. The dummy variable has a positive andhighly significant coefficient. However, excluding this dummy variable doesnot substantially change the signs and significance of the other variables.5

4.3. Government-financed knowledge capital

In this section, I test my second hypothesis, which says that VC investmentsare likely to be higher in those countries that have high amounts ofgovernment-financed knowledge capital. In a first step, I follow Gompers andLerner (1999) and include both business-financed and government-financedknowledge capital, which is either GERD or R&D researchers. In a secondstep, I include only the government-financed knowledge capital. Theestimation results are presented in Table 5.

I find only weak evidence in favor of my second hypothesis. If I jointlyinclude business-financed and government-financed knowledge capital[columns (1)–(6) in Table 5], business-financed knowledge capital has apositive impact in most specifications, while government-financed knowl-edge capital has no significant impact on VC investments. More specifically,government-financed GERD and government-financed R&D researchers turnout to be insignificant for the investments in the early stage and in the earlyand expansion stages. Business-financed GERD affects the number ofinvestment in the early stage and in the early and expansion stagessignificantly positively, but it does not affect the volume of investments. Incontrast to this result, Romain and van Pottelsberghe (2004) have reportedpositive effects of business R&D expenditures on the volume of investmentsin the early stage. Their positive coefficients are likely to be the result of theunderlying positive trend in their data.

5. I also use year dummies for 1999 and 2000. The coefficients on these two dummies are mostoften statistically significant and are of a similar magnitude. I also use other year dummycombinations. This offers, however, no additional insights.

A. Schertler

82 r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007

Ta

ble

5G

over

nm

ent-

fin

an

ced

kn

ow

led

ge

cap

ital

DEarl

y-s

tage

inves

tmen

ts

DEarl

y-

an

dex

pan

sio

n-s

tage

inves

tmen

tsD

Earl

y-s

tage

inves

tmen

tsD

Earl

y-

an

dex

pan

sio

n-s

tage

inves

tmen

ts

Nu

mb

erV

olu

me

Nu

mb

erV

olu

me

Nu

mb

erN

um

ber

DIn

du

stry

-fin

an

ced

GER

D(2

)0.0

03**

0.0

04**

(2.2

3)

(2.6

5)

DG

over

nm

ent-

fin

an

ced

GER

D(2

)

0.0

01

�0.0

01

(0.7

3)

(0.6

7)

DB

usi

nes

s-fi

nan

ced

R&

D

rese

arc

her

s(2

)

0.0

22**

*0.3

17**

0.0

19**�

0.0

94

(4.9

4)

(2.3

2)

(2.7

5)

(0.2

1)

DG

over

nm

ent-

fin

an

ced

R&

D

rese

arc

her

s(2

)

�0.0

43*

0.7

45

�0.0

43

1.7

32

�0.0

05

�0.0

1

(1.8

3)

(1.1

2)

(1.3

3)

(1.4

2)

(0.3

5)

(0.5

5)

DG

over

nm

ent-

fin

an

ced

R&

D

rese

arc

her

s(3

)

0.0

29

0.0

32

(0.9

1)

(0.8

8)

DG

over

nm

ent-

fin

an

ced

R&

D

rese

arc

her

s(4

)

0.0

32**

0.0

36

(2.2

7)

(1.5

8)

DG

over

nm

ent-

fin

an

ced

R&

D

rese

arc

her

s(5

)

0.0

42**

0.0

62**

(2.5

)(2

.42)

Gro

wth

rate

of

new

fun

ds

rais

ed(1

)

�0.0

01

0�

0.0

32

00.0

01

�0.0

98

00

00

0.0

01

0.0

01

0.0

01

0

(0.7

)(0

.04)

(1.1

4)

(0.1

6)

(0.2

6)

(0.9

3)

(0.2

9)

(0.2

)(0

.23)

(0.0

1)

(0.4

)(0

.34)

(0.3

5)

(0.1

5)

New

fun

ds

of

go

ver

nm

ents

(1)

00.0

00*�

0.0

02

00

�0.0

02

00

00.0

00*

0.0

01

00

0.0

01

(1.3

5)

(2.0

5)

(0.3

2)

(1.1

1)

(1.6

)(0

.16)

(1.7

6)

(1.7

1)

(1.5

4)

(1.9

)(1

.5)

(1.4

7)

(1.3

5)

(1.6

2)

New

fun

ds

of

pen

sio

nfu

nd

s

(1)

0.0

00*

00.0

11

00

0.0

52

0.0

01

0.0

01

0.0

01*

0.0

01

0.0

01

0.0

01

0.0

01

0.0

01

(1.8

5)

(1.6

9)

(0.8

3)

(0.9

)(0

.95)

(1.1

7)

(1.6

)(1

.75)

(1.7

8)

(1.6

5)

(0.9

8)

(1.0

7)

(1.1

)(1

.1)

Em

plo

ym

ent

pro

tect

ion

ind

ex

00

�0.0

01

00

0.0

01

00

00

00

00

(0.3

5)

(0.2

5)

(0.5

7)

(0.0

8)

(0.3

7)

(0.4

)(0

.18)

(0.3

)(0

.36)

(0.6

1)

(0.1

)(0

.02)

(0.0

3)

(0.3

)

Cap

ital

gain

sta

xra

te0

00

00

00

�0.0

00*

0�

0.0

00**

00

00

(1.1

5)

(0.0

9)

(0.1

4)

(0.5

6)

(0.5

)(1

.02)

(1.1

9)

(1.9

6)

(1.7

2)

(2.1

6)

(0.3

6)

(0.7

9)

(0.6

3)

(0.8

5)

Len

din

gra

te0

0.0

01

0.0

4�

0.0

01

�0.0

01

�0.0

13

�0.0

01

�0.0

01

�0.0

01

�0.0

01

�0.0

02

�0.0

02

�0.0

03

�0.0

03

(0.3

5)

(0.6

2)

(1.0

6)

(0.4

2)

(0.7

7)

(0.0

9)

(0.3

5)

(0.4

1)

(0.4

9)

(0.3

7)

(0.9

9)

(1.0

6)

(1.0

8)

(1.1

1)

Knowledge Capital and Venture Capital Investments

r Verein fur Socialpolitik and Blackwell Publishing Ltd. 2007 83

Gro

wth

rate

of

GD

P0.0

01

0.0

01

0.0

23

0.0

02*

0.0

01

�0.0

04

0.0

01*

0.0

01*

0.0

01

0.0

01*

0.0

01

0.0

02

0.0

02

0.0

02

(1.3

)(1

.56)

(1.5

5)

(1.8

2)

(1.2

9)

(0.1

3)

(1.7

9)

(2.0

1)

(1.7

4)

(2.0

8)

(1.4

)(1

.7)

(1.4

6)

(1.5

5)

Sto

ckm

ark

etre

turn

0.0

01**

*0.0

01**

0.0

42**

0.0

02**

0.0

01*

0.0

80**

*0.0

01**

0.0

01**

0.0

01**

0.0

01**

0.0

01*

0.0

01*

0.0

01*

0.0

01*

(3.1

9)

(2.7

6)

(2.9

3)

(2.3

8)

(2.1

1)

(3.3

4)

(2.4

1)

(2.6

2)

(2.3

3)

(2.3

9)

(2)

(2.0

8)

(1.9

3)

(1.9

8)

Du

mm

yeq

ual

too

ne

in1999

an

d2000

0.0

01**

*0.0

01**

*0.0

24**

*0.0

01**

*0.0

01**

*0.0

64**

*0.0

01**

*0.0

01**

*0.0

01**

*0.0

01**

*0.0

01**

*0.0

01**

*0.0

01**

*0.0

01**

*

(3.5

4)

(3.2

8)

(4.5

2)

(3.9

4)

(3.8

6)

(5.5

1)

(3.7

9)

(4.1

2)

(3.7

1)

(3.8

3)

(4.2

4)

(4.4

2)

(4.2