is there such a thing as having too much cash? · is there such a thing as having too much cash?...

TRANSCRIPT

OCTOBER 2012 1ADVANCING INSIGHTS ADVANCING COMMERCE.

Global Insights

IS THERE SUCH A THING AS HAVING TOO MUCH CASH?

In many places the persistence of cash is symptomatic of a large informal economy. Such economies can only run on cash, and this preference for cash feeds, and is in turn fed by, bad behavior such as corruption and bribery. This bad behavior can be a substantial drag on the overall economy, suggesting that governments benefit by moving their citizenry away from cash. In recent years several countries, notably Korea, Mexico, and Argentina, have done just this, taking regulatory measures to persuade both buyers and sellers to reduce their use of cash.

In this article we will look at the links between cash, bad behavior, and negative economic consequences, and conclude by discussing some of the solutions governments around the world have implemented to solve the problem of too much cash.

Anyone who has ever negotiated a purchase knows why it might be preferable to pay for it with cash. Sellers often ask to be paid in cash because it constitutes an immediate transfer of funds that can be put to use right away. Because of this, sellers are often willing to lower their prices for buyers willing to pay cash. Cash also eliminates the risks associated with partial payments or credit, and it offers anonymity to both buyer and seller.

The considerations above make a strong case, then, for using cash when buying stolen goods or when seeking to avoid giving the tax man his due, but for most of the purchases we make every day, considerations like financing and anonymity are rarely top of mind. For the vast majority of payments we make, how we choose to pay depends mainly on habit and convenience. Cash is almost always an option for payment (except when buying online), but its convenience often depends on how much of it you have in your wallet. Other factors, such as card rewards or purchase insurances offered on credit cards, mean that cash is very often the least beneficial payment instrument for the purchaser. Online shopping and online banking have fundamentally changed the way we buy things, suggesting that deeply ingrained purchasing habits can change. So why does so much cash usage persist?

BY HUGH THOMAS AND KEVIN MELLYN

An Examination of the Links Between Cash Usage and Bad Behavior

ADVISORS’ PRELIMINARY ESTIMATES OF GLOBAL CASH USAGE SUGGEST THAT 8.3 TRILLION DOLLARS ($US) OF CONSUMER PURCHASES ANNUALLY ARE MADE OUTSIDE THE FORMAL ECONOMY, USING CASH. THIS INCLUDES AN ESTIMATED $US 6.8 TRILLION OF UNDERGROUND ECONOMY PURCHASES AND APPROXIMATELY $US 1.5 TRILLION IN ILLEGAL PURCHASES.

$8.3*

TRILLION

* Transparency International 2010, havocscope.com 2010, MasterCard Advisors’ analysis.

Global Insights

2ADVANCING INSIGHTS ADVANCING COMMERCE.

Developed Markets with Low Cash Usage*

Developed Markets with High Cash Usage*

Developing Markets with High Cash Usage*

Markets in Transition*

Canada Sweden Germany Japan Brazil India Australia Kenya Turkey

France U.K. Italy U.S.A. China Russia Korea South Africa

HEAVY CASH USAGE IS NOT RESTRICTED TO DEVELOPING MARKETS

Countries around the world fall into four broad categories of cash usage patterns. Places such as Canada and the U.K. are examples of developed markets with low cash usage, while Germany and the U.S. are examples of developed markets with high cash usage. Places such as Australia, Turkey, and Korea are considered markets in transition, where regulatory measures impacting payment choice have been initiated. The final category, which includes the majority of the world’s countries and population, fall into the category of developing markets with high cash usage.

FIGURE 1: GLOBAL CASH USAGE CATEGORIES

*Example markets. Source: MasterCard Advisors’ Analysis

Global Insights

3ADVANCING INSIGHTS ADVANCING COMMERCE.

FIGURE 2: ESTIMATED PERCENTAGE OF CONSUMER PAYMENTS (BY VALUE) MADE WITH CASH

Sources: World Bank Database 2011 and MasterCard Advisors’ analysis; figures exclude black and gray market spend.

100%80%60%

MARKETS IN TRANSITION / HIGH CASH

40%20%0%

ARG

MEX

100%80%60%

MARKETS IN TRANSITION / LOW CASH

40%20%0%

AUS

KOR

100%80%60%

DEVELOPING MARKETS / LOWER CASH

40%20%0%

BRA

CHI

CHN

PERU

THL

100%80%60%

DEVELOPING MARKETS / HIGHEST CASH

40%20%0%

BUL

IND

INDO

ROM

RUS

100%80%60%

DEVELOPED MARKETS / LOW CASH

40%20%0%

BEL

CAN

DEN

FIN

FRA

IRE

NED

NOR

SLV

SWE

SWI

TAI

UK

100%80%60%

DEVELOPED MARKETS / HIGH CASH

40%20%0%

AUT

CZH

GER

GRE

HUN

ITA

JPN

POL

PORT

SING

SLVK

SPA

US

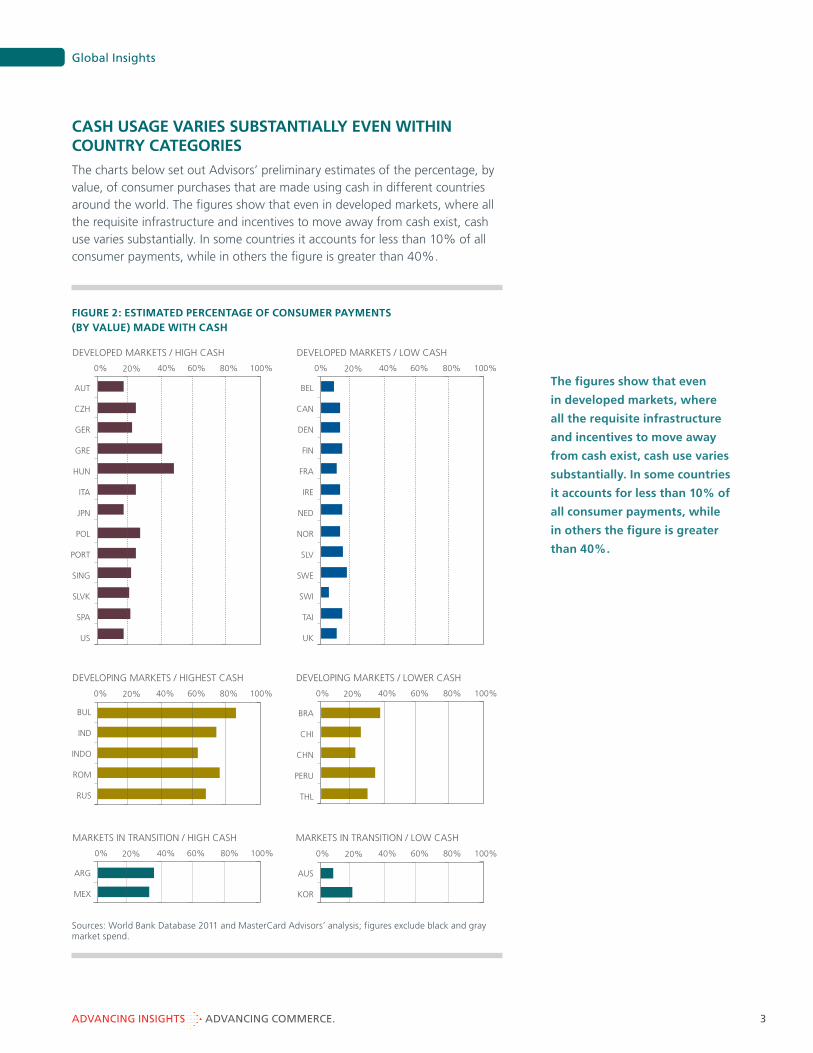

CASH USAGE VARIES SUBSTANTIALLY EVEN WITHIN COUNTRY CATEGORIES

The charts below set out Advisors’ preliminary estimates of the percentage, by value, of consumer purchases that are made using cash in different countries around the world. The figures show that even in developed markets, where all the requisite infrastructure and incentives to move away from cash exist, cash use varies substantially. In some countries it accounts for less than 10% of all consumer payments, while in others the figure is greater than 40%.

The figures show that even

in developed markets, where

all the requisite infrastructure

and incentives to move away

from cash exist, cash use varies

substantially. In some countries

it accounts for less than 10% of

all consumer payments, while

in others the figure is greater

than 40%.

Global Insights

4ADVANCING INSIGHTS ADVANCING COMMERCE.

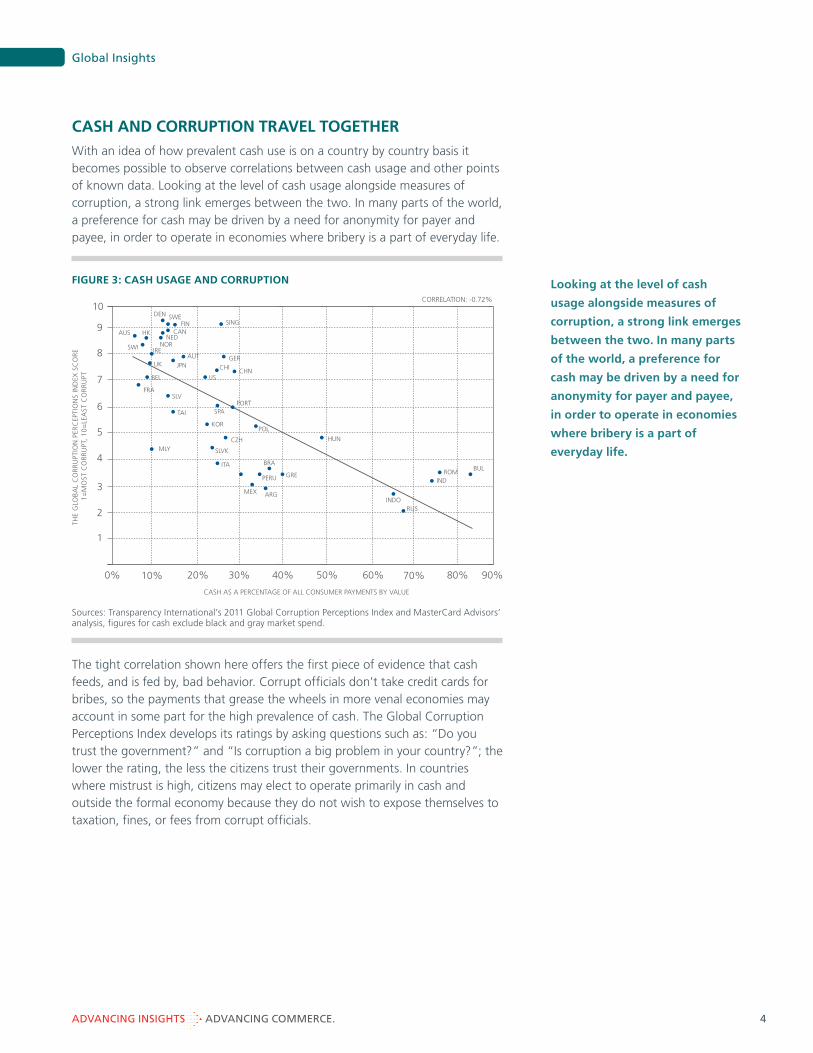

CASH AND CORRUPTION TRAVEL TOGETHER

With an idea of how prevalent cash use is on a country by country basis it becomes possible to observe correlations between cash usage and other points of known data. Looking at the level of cash usage alongside measures of corruption, a strong link emerges between the two. In many parts of the world, a preference for cash may be driven by a need for anonymity for payer and payee, in order to operate in economies where bribery is a part of everyday life.

FIGURE 3: CASH USAGE AND CORRUPTION

Sources: Transparency International’s 2011 Global Corruption Perceptions Index and MasterCard Advisors’ analysis, figures for cash exclude black and gray market spend.

The tight correlation shown here offers the first piece of evidence that cash feeds, and is fed by, bad behavior. Corrupt officials don’t take credit cards for bribes, so the payments that grease the wheels in more venal economies may account in some part for the high prevalence of cash. The Global Corruption Perceptions Index develops its ratings by asking questions such as: “Do you trust the government?” and “Is corruption a big problem in your country?”; the lower the rating, the less the citizens trust their governments. In countries where mistrust is high, citizens may elect to operate primarily in cash and outside the formal economy because they do not wish to expose themselves to taxation, fines, or fees from corrupt officials.

Looking at the level of cash

usage alongside measures of

corruption, a strong link emerges

between the two. In many parts

of the world, a preference for

cash may be driven by a need for

anonymity for payer and payee,

in order to operate in economies

where bribery is a part of

everyday life.

50%40%30%

CASH AS A PERCENTAGE OF ALL CONSUMER PAYMENTS BY VALUE

THE

GLO

BA

L C

OR

RU

PTIO

N P

ERC

EPTI

ON

S IN

DEX

SC

OR

E 1

=M

OST

CO

RR

UPT

, 1

0=

LEA

ST C

OR

RU

PT

CORRELATION: -0.72%

20%10%0% 90%80%70%60%

10

9

8

7

6

5

4

3

2

1

DEN

HKAUS

SWI

FRA

BEL

UK

IRE

NEDCAN

FINSWE

NOR

JPN

AUT

SING

GER

CHI

USCHN

MLY

TAI

SLV

SPAPORT

KOR

CZH

SLVK

ITA

POL

MEX

PERU

ARG

BRA

GRE

HUN

INDORUS

INDROM

BUL

Global Insights

5ADVANCING INSIGHTS ADVANCING COMMERCE.

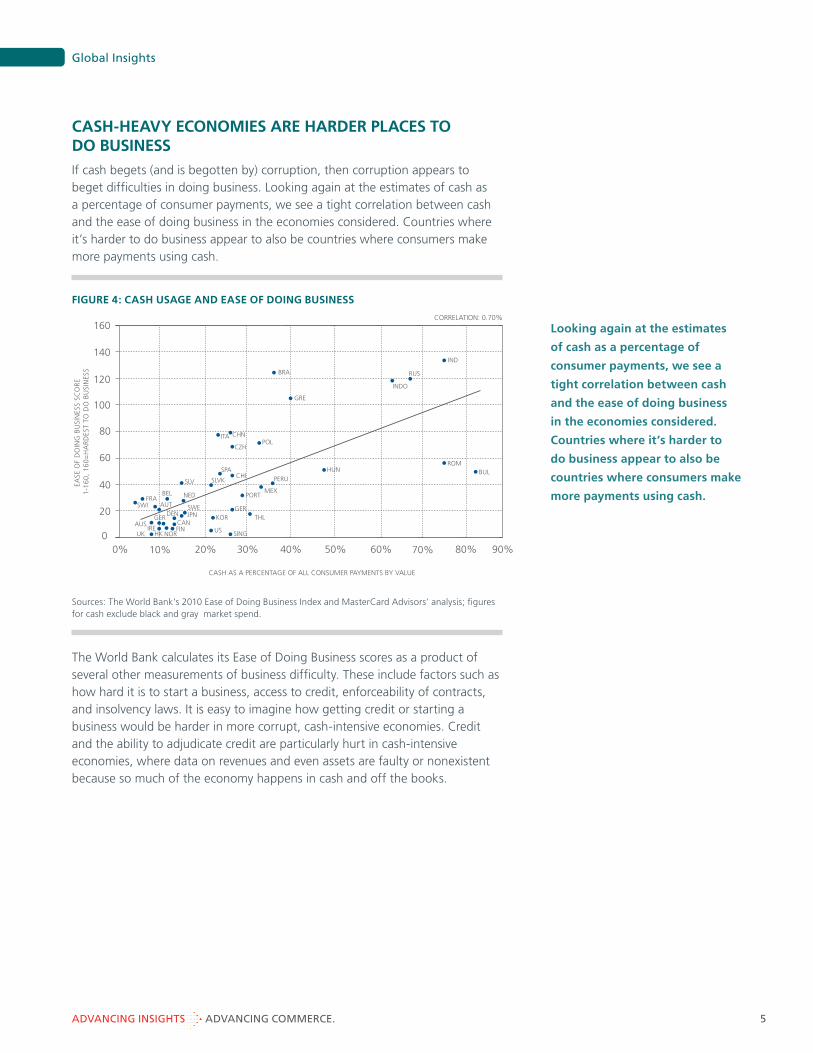

CASH-HEAVY ECONOMIES ARE HARDER PLACES TO DO BUSINESS

If cash begets (and is begotten by) corruption, then corruption appears to beget difficulties in doing business. Looking again at the estimates of cash as a percentage of consumer payments, we see a tight correlation between cash and the ease of doing business in the economies considered. Countries where it’s harder to do business appear to also be countries where consumers make more payments using cash.

FIGURE 4: CASH USAGE AND EASE OF DOING BUSINESS

Sources: The World Bank’s 2010 Ease of Doing Business Index and MasterCard Advisors’ analysis; figures for cash exclude black and gray market spend.

The World Bank calculates its Ease of Doing Business scores as a product of several other measurements of business difficulty. These include factors such as how hard it is to start a business, access to credit, enforceability of contracts, and insolvency laws. It is easy to imagine how getting credit or starting a business would be harder in more corrupt, cash-intensive economies. Credit and the ability to adjudicate credit are particularly hurt in cash-intensive economies, where data on revenues and even assets are faulty or nonexistent because so much of the economy happens in cash and off the books.

Looking again at the estimates

of cash as a percentage of

consumer payments, we see a

tight correlation between cash

and the ease of doing business

in the economies considered.

Countries where it’s harder to

do business appear to also be

countries where consumers make

more payments using cash.

50%40%30%

CORRELATION: 0.70%

20%10%0% 90%80%70%60%

BULROM

IND

RUS

INDO

BRA

GRE

HUN

PERU

MEXPORT

THLGER

KOR

SINGUS

SWEJPN

CANFIN

NORHKUK

GERAUS

DEN

IRE

NED

AUT

SLV

BELFRA

SWI

SLVK

SPACHI

ITA CHN

CZHPOL

160

140

120

100

80

60

40

20

0

CASH AS A PERCENTAGE OF ALL CONSUMER PAYMENTS BY VALUE

EASE

OF

DO

ING

BU

SIN

ESS

SCO

RE

1-1

60

, 1

60

=H

AR

DES

T TO

DO

BU

SIN

ESS

Global Insights

6ADVANCING INSIGHTS ADVANCING COMMERCE.

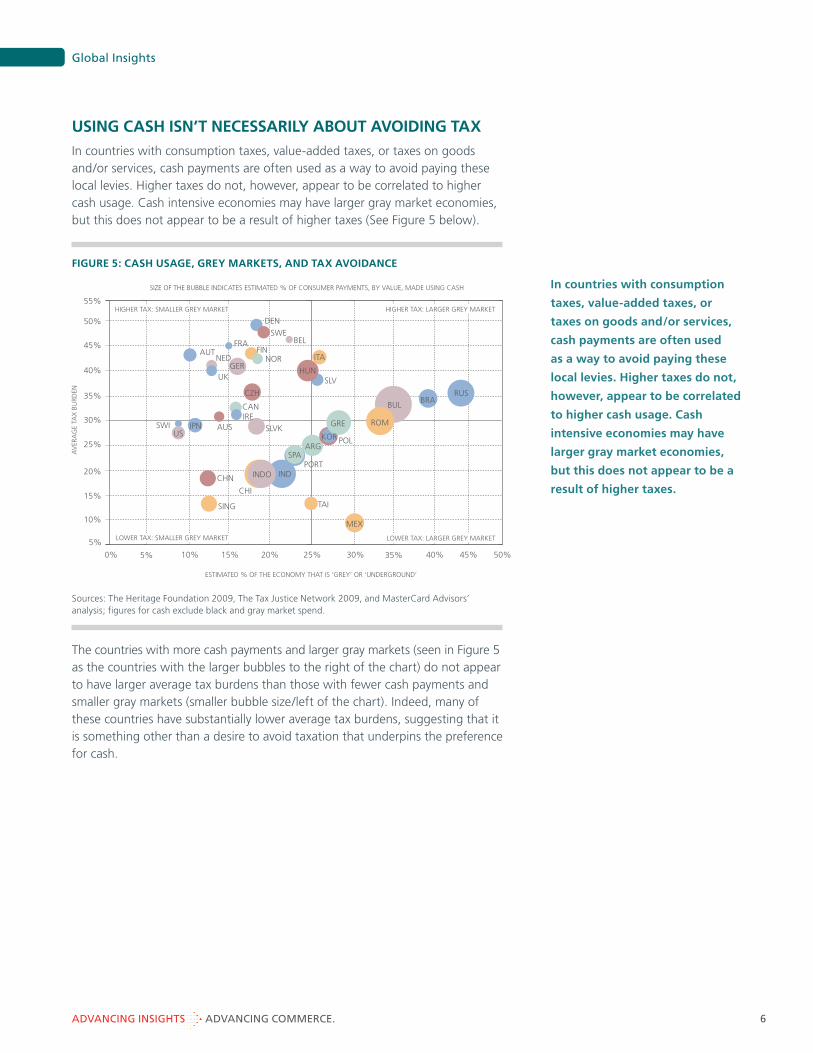

USING CASH ISN’T NECESSARILY ABOUT AVOIDING TAX

In countries with consumption taxes, value-added taxes, or taxes on goods and/or services, cash payments are often used as a way to avoid paying these local levies. Higher taxes do not, however, appear to be correlated to higher cash usage. Cash intensive economies may have larger gray market economies, but this does not appear to be a result of higher taxes (See Figure 5 below).

FIGURE 5: CASH USAGE, GREY MARKETS, AND TAX AVOIDANCE

Sources: The Heritage Foundation 2009, The Tax Justice Network 2009, and MasterCard Advisors’ analysis; figures for cash exclude black and gray market spend.

The countries with more cash payments and larger gray markets (seen in Figure 5 as the countries with the larger bubbles to the right of the chart) do not appear to have larger average tax burdens than those with fewer cash payments and smaller gray markets (smaller bubble size/left of the chart). Indeed, many of these countries have substantially lower average tax burdens, suggesting that it is something other than a desire to avoid taxation that underpins the preference for cash.

In countries with consumption

taxes, value-added taxes, or

taxes on goods and/or services,

cash payments are often used

as a way to avoid paying these

local levies. Higher taxes do not,

however, appear to be correlated

to higher cash usage. Cash

intensive economies may have

larger gray market economies,

but this does not appear to be a

result of higher taxes.

25%20%15%

ESTIMATED % OF THE ECONOMY THAT IS ‘GREY’ OR ‘UNDERGROUND’

SIZE OF THE BUBBLE INDICATES ESTIMATED % OF CONSUMER PAYMENTS, BY VALUE, MADE USING CASH

AV

ERA

GE

TAX

BU

RDEN

10%5%0% 45% 50%40%35%30%

55%

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

RUSBRA

BUL

ROMGRE

POLARG

SING

SWIUS

JPN AUS

CANIRE

SLVK

PORTSPA

TAI

MEX

IND

CHI

CHN

ITA

HUNSLV

DEN

SWEBEL

FINNOR

FRA

GER

CZH

NED

UK

AUT

KOR

INDO

HIGHER TAX: SMALLER GREY MARKET

LOWER TAX: SMALLER GREY MARKET LOWER TAX: LARGER GREY MARKET

HIGHER TAX: LARGER GREY MARKET

Global Insights

7ADVANCING INSIGHTS ADVANCING COMMERCE.

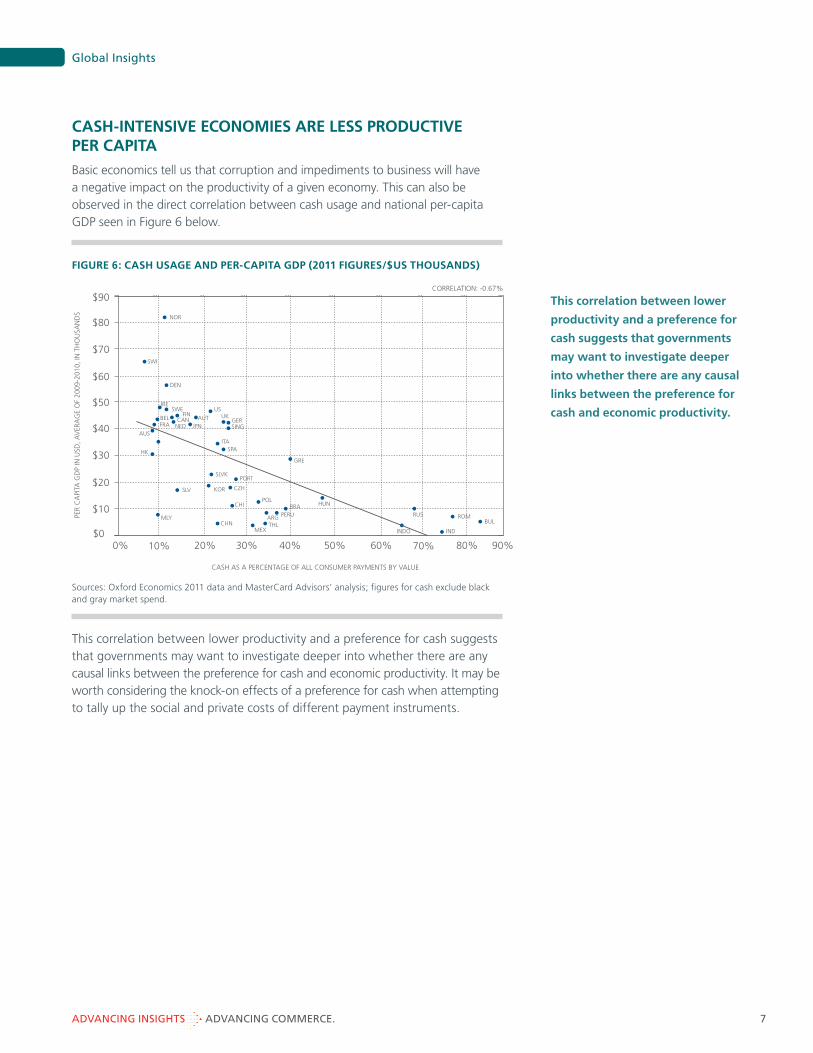

CASH-INTENSIVE ECONOMIES ARE LESS PRODUCTIVE PER CAPITA

Basic economics tell us that corruption and impediments to business will have a negative impact on the productivity of a given economy. This can also be observed in the direct correlation between cash usage and national per-capita GDP seen in Figure 6 below.

FIGURE 6: CASH USAGE AND PER-CAPITA GDP (2011 FIGURES/$US THOUSANDS)

Sources: Oxford Economics 2011 data and MasterCard Advisors’ analysis; figures for cash exclude black and gray market spend.

This correlation between lower productivity and a preference for cash suggests that governments may want to investigate deeper into whether there are any causal links between the preference for cash and economic productivity. It may be worth considering the knock-on effects of a preference for cash when attempting to tally up the social and private costs of different payment instruments.

This correlation between lower

productivity and a preference for

cash suggests that governments

may want to investigate deeper

into whether there are any causal

links between the preference for

cash and economic productivity.

50%40%30%

CORRELATION: -0.67%

20%10%0% 90%80%70%60%

NOR

SWI

DEN

IRE

KOR CZH

PORT

GRE

AUS

SWE

BEL CAN

POL

MEX

ARG PERU

FINAUT

FRA NED

BRA HUN

RUS

INDO

JPN

USUK

GER

ROM

IND

BULTHL

SING

ITASPA

SLVK

HK

SLV

MLYCHN

CHI

$80

$90

$70

$60

$50

$40

$30

$20

$10

$0

CASH AS A PERCENTAGE OF ALL CONSUMER PAYMENTS BY VALUE

PER

CA

PITA

GD

P IN

USD

, AV

ERA

GE

OF

2009

-201

0, IN

TH

OU

SAN

DS

Global Insights

8ADVANCING INSIGHTS ADVANCING COMMERCE.

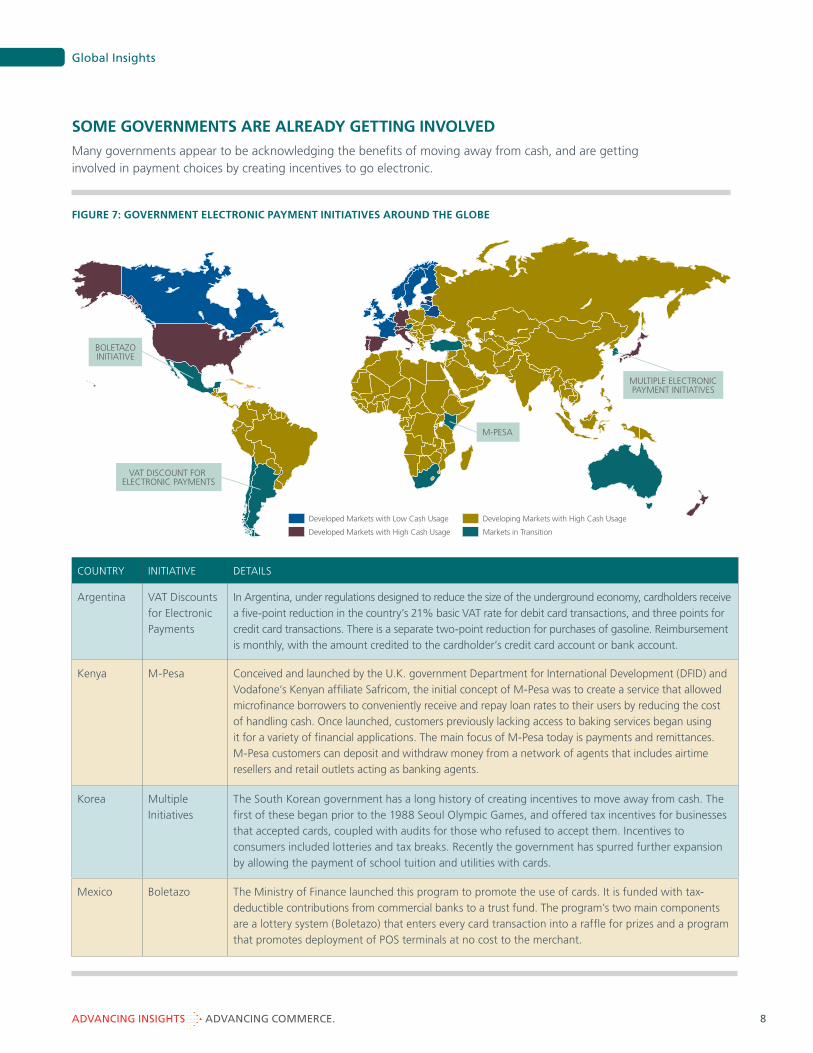

FIGURE 7: GOVERNMENT ELECTRONIC PAYMENT INITIATIVES AROUND THE GLOBE

MULTIPLE ELECTRONICPAYMENT INITIATIVES

M-PESA

VAT DISCOUNT FOR ELECTRONIC PAYMENTS

BOLETAZOINITIATIVE

Developed Markets with Low Cash Usage

Developed Markets with High Cash Usage

Developing Markets with High Cash Usage

Markets in Transition

SOME GOVERNMENTS ARE ALREADY GETTING INVOLVED

Many governments appear to be acknowledging the benefits of moving away from cash, and are getting involved in payment choices by creating incentives to go electronic.

COUNTRY INITIATIVE DETAILS

Argentina VAT Discounts

for Electronic

Payments

In Argentina, under regulations designed to reduce the size of the underground economy, cardholders receive

a five-point reduction in the country’s 21% basic VAT rate for debit card transactions, and three points for

credit card transactions. There is a separate two-point reduction for purchases of gasoline. Reimbursement

is monthly, with the amount credited to the cardholder’s credit card account or bank account.

Kenya M-Pesa Conceived and launched by the U.K. government Department for International Development (DFID) and

Vodafone’s Kenyan affiliate Safricom, the initial concept of M-Pesa was to create a service that allowed

microfinance borrowers to conveniently receive and repay loan rates to their users by reducing the cost

of handling cash. Once launched, customers previously lacking access to baking services began using

it for a variety of financial applications. The main focus of M-Pesa today is payments and remittances.

M-Pesa customers can deposit and withdraw money from a network of agents that includes airtime

resellers and retail outlets acting as banking agents.

Korea Multiple

Initiatives

The South Korean government has a long history of creating incentives to move away from cash. The

first of these began prior to the 1988 Seoul Olympic Games, and offered tax incentives for businesses

that accepted cards, coupled with audits for those who refused to accept them. Incentives to

consumers included lotteries and tax breaks. Recently the government has spurred further expansion

by allowing the payment of school tuition and utilities with cards.

Mexico Boletazo The Ministry of Finance launched this program to promote the use of cards. It is funded with tax-

deductible contributions from commercial banks to a trust fund. The program’s two main components

are a lottery system (Boletazo) that enters every card transaction into a raffle for prizes and a program

that promotes deployment of POS terminals at no cost to the merchant.

Global Insights

9ADVANCING INSIGHTS ADVANCING COMMERCE.

SUBJECT SUMMARY

The World Beyond Cash: Cash Transaction Pools

Delving still deeper into the pools of cash transactions identified in “Is There Such a Thing As Having Too Much Cash?” this short paper will provide estimates of the size of cash pools around the globe by payment locale (country and expenditure type) and offer ideas as to why these volumes persist as cash.

Factors Affecting Payment Choice

Cash is still used in a variety of situations where pure rational micro-economic considerations among stakeholders would suggest that other solutions would be preferred. This short paper offers a framework by which to think about all the considerations that go into stakeholder payment preference.

Merchant Considerations For Cash Usage

Cash is often perceived as the cheapest means by which to receive payment because it lacks any ad valorem element of cost (elements present in other methods of payment, such as credit and debit). This point of view only considers payment vehicles from a cost perspective, whereas a more balanced, P&L-type perspective is required. This study will flesh out the full list of factors to be considered as merchants seek to qualify the cost associated with different payment instruments.

CONCLUSIONS

There will always be a need for cash in some form. In places where infrastructures do not exist, or have been compromised, its portability and stored value can mean that cash is the only way to pay. Cash in some form is here to stay, whether we like it or not.

So while there may be good reasons to ensure that we are always able to use cash, its predominance in some economies suggests that cash usage feeds, and is being fed by, bad behavior. The estimates of cash usage prepared for this paper suggest that cash usage in many economies far outstrips what would be expected of consumers making rational micro-economic choices, and inasmuch as cash seems to be facilitating bad behavior, this preference for cash is not a good thing.

The information presented here can in no way be seen as implying any causation between cash usage and bad behavior. To blame bad behavior like corruption on a preference for cash would be like blaming high unemployment on too many job seekers. It would be blaming the symptoms for the disease. The most we can imply from the data reviewed is that a preference for cash appears, in many cases, to be symptomatic of broader economic problems and bad behavior. Data on the effect that reducing cash (i.e., through incentives such as M-Pesa or Boletazo) has had on this bad behavior are difficult to interpret and cannot be seen to imply a causal relationship between the two. This said, few governments that have undertaken initiatives to reduce the use of cash would question that they had had a positive overall effect on their economy.

NEXT STEPS

This is the first in a series of articles on the cost and consequences of cash. Planned future topics include:

The estimates of cash usage

prepared for this paper suggest

that cash usage in many

economies far outstrips what

would be expected of consumers

making rational micro-economic

choices, and inasmuch as cash

seems to be facilitating bad

behavior, this preference for cash

is not a good thing.

ADVANCING INSIGHTS ADVANCING COMMERCE.

For additional insights, please visit www.mastercardadvisors.com and insights.mastercard.com.

Global Insights

©2012 MasterCard. All rights reserved. Proprietary and Confidential.

Insights and recommendations are based on proprietary and third-party research, as well as MasterCard’s analysis and opinions, and are presented for your information only.

ABOUT THE AUTHORS

Hugh ThomasSenior Managing Consultant, MasterCard Advisors [email protected]

Kevin MellynPrincipal, MasterCard Advisors [email protected]