introduction on german long term care system on german long term care system ... • social...

TRANSCRIPT

Introduction on German

Long Term Care System

Prof. Dr. Heinz Rothgang

Centre for Social Policy Research

University of Bremen

Hamburg, 23rd October, 2013

Prof. Dr. Heinz Rothgang 2

Contents

I. Long-term care and healthcare in Germany

II. LTCI in Germany: Some Basic Facts

III. Issues of actual debate and for future reforms

IV. Lessons to be learned

Prof. Dr. Heinz Rothgang 3

Contents

I. Long-term care and healthcare in Germany

1. Health Care and Long-term care

2. Why was LTCI introduced?

II. LTCI in Germany: Some Basic Facts

III. Issues of actual debate and for future reforms

IV. Lessons to be learned

Prof. Dr. Heinz Rothgang 4

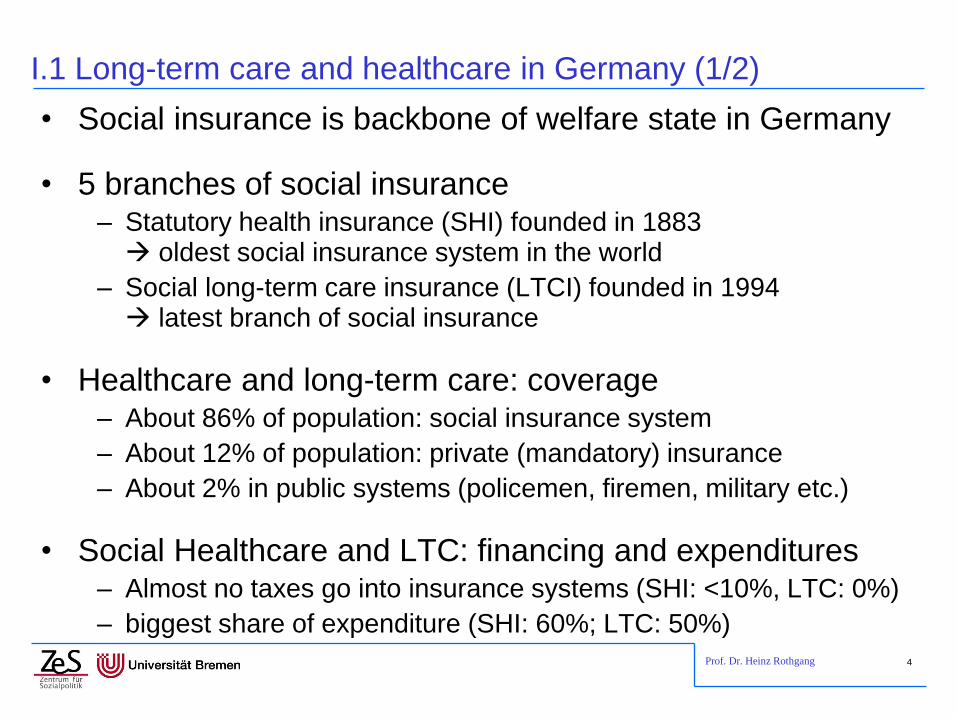

I.1 Long-term care and healthcare in Germany (1/2)

• Social insurance is backbone of welfare state in Germany

• 5 branches of social insurance – Statutory health insurance (SHI) founded in 1883 oldest social insurance system in the world

– Social long-term care insurance (LTCI) founded in 1994 latest branch of social insurance

• Healthcare and long-term care: coverage – About 86% of population: social insurance system

– About 12% of population: private (mandatory) insurance

– About 2% in public systems (policemen, firemen, military etc.)

• Social Healthcare and LTC: financing and expenditures – Almost no taxes go into insurance systems (SHI: <10%, LTC: 0%)

– biggest share of expenditure (SHI: 60%; LTC: 50%)

Prof. Dr. Heinz Rothgang 5

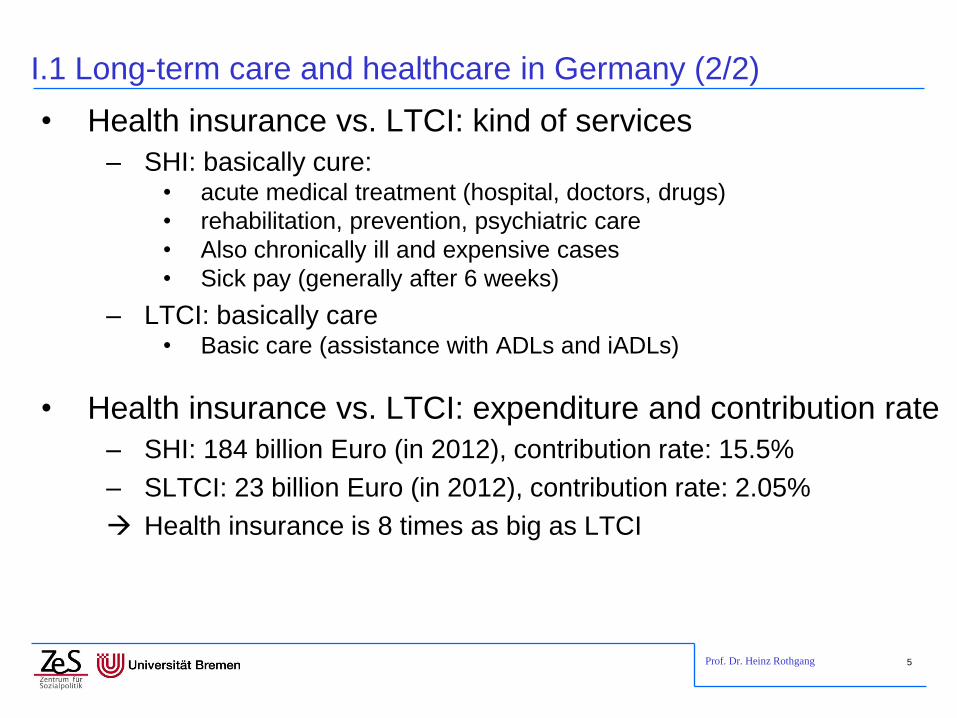

I.1 Long-term care and healthcare in Germany (2/2)

• Health insurance vs. LTCI: kind of services

– SHI: basically cure: • acute medical treatment (hospital, doctors, drugs)

• rehabilitation, prevention, psychiatric care

• Also chronically ill and expensive cases

• Sick pay (generally after 6 weeks)

– LTCI: basically care • Basic care (assistance with ADLs and iADLs)

• Health insurance vs. LTCI: expenditure and contribution rate

– SHI: 184 billion Euro (in 2012), contribution rate: 15.5%

– SLTCI: 23 billion Euro (in 2012), contribution rate: 2.05%

Health insurance is 8 times as big as LTCI

Prof. Dr. Heinz Rothgang 6

I.2 The introduction of LTC insurance: Goals and rationale (1/4)

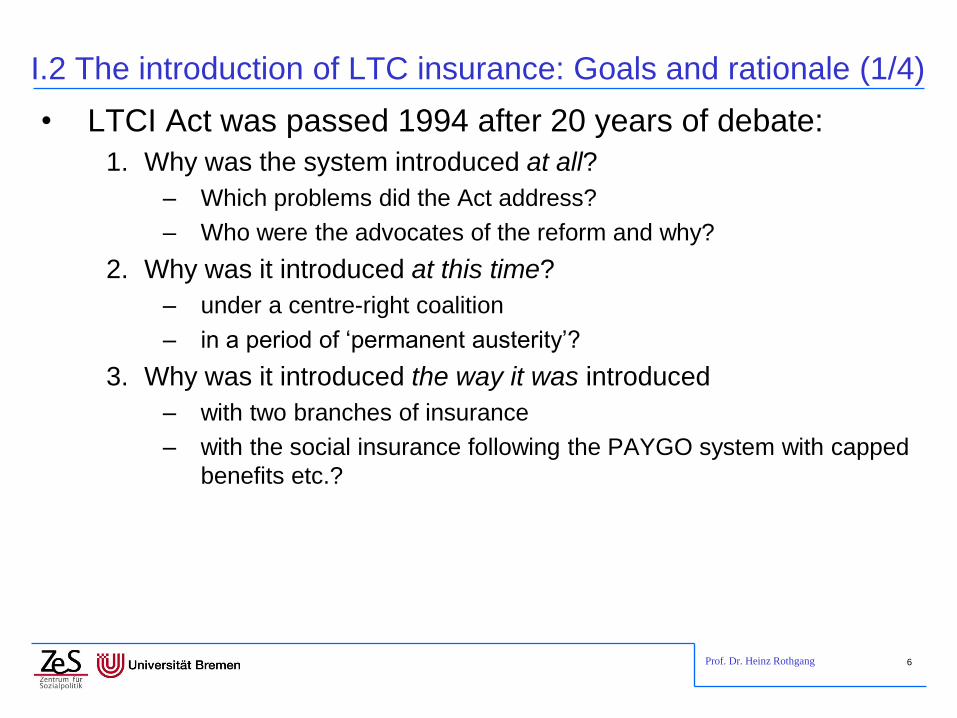

• LTCI Act was passed 1994 after 20 years of debate:

1. Why was the system introduced at all?

– Which problems did the Act address?

– Who were the advocates of the reform and why?

2. Why was it introduced at this time?

– under a centre-right coalition

– in a period of ‘permanent austerity’?

3. Why was it introduced the way it was introduced

– with two branches of insurance

– with the social insurance following the PAYGO system with capped

benefits etc.?

Prof. Dr. Heinz Rothgang 7

I.2 The introduction of LTC insurance: Goals and rationale (2/4)

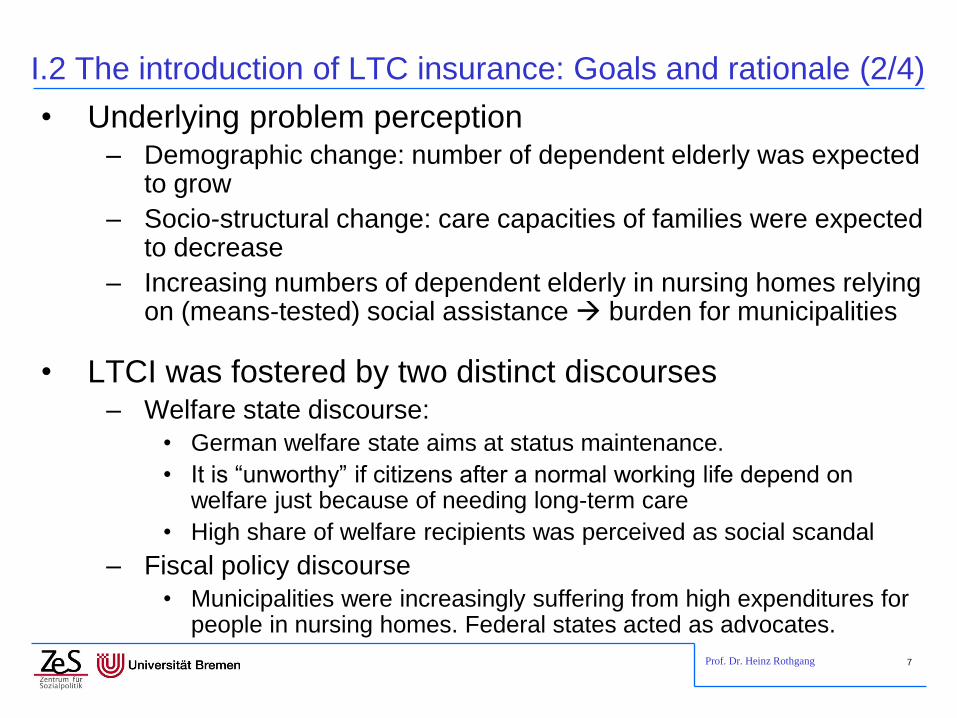

• Underlying problem perception – Demographic change: number of dependent elderly was expected

to grow

– Socio-structural change: care capacities of families were expected to decrease

– Increasing numbers of dependent elderly in nursing homes relying on (means-tested) social assistance burden for municipalities

• LTCI was fostered by two distinct discourses – Welfare state discourse:

• German welfare state aims at status maintenance.

• It is “unworthy” if citizens after a normal working life depend on welfare just because of needing long-term care

• High share of welfare recipients was perceived as social scandal

– Fiscal policy discourse

• Municipalities were increasingly suffering from high expenditures for people in nursing homes. Federal states acted as advocates.

Prof. Dr. Heinz Rothgang 8

I.2 The introduction of LTC insurance: Goals and rationale (3/4)

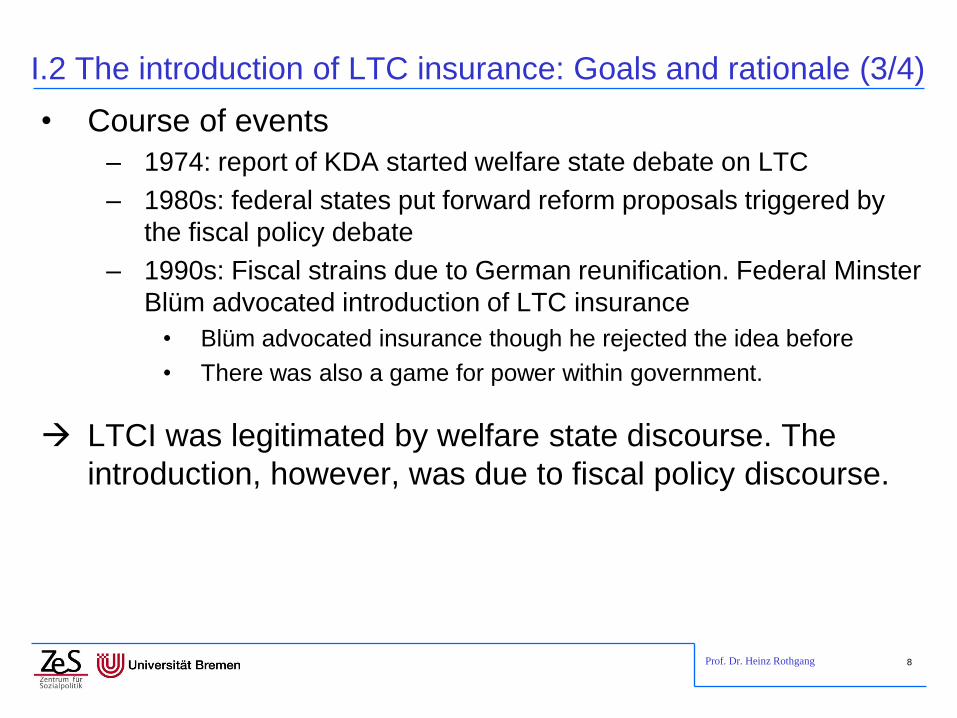

• Course of events

– 1974: report of KDA started welfare state debate on LTC

– 1980s: federal states put forward reform proposals triggered by

the fiscal policy debate

– 1990s: Fiscal strains due to German reunification. Federal Minster

Blüm advocated introduction of LTC insurance

• Blüm advocated insurance though he rejected the idea before

• There was also a game for power within government.

LTCI was legitimated by welfare state discourse. The

introduction, however, was due to fiscal policy discourse.

Prof. Dr. Heinz Rothgang 9

I.2 The introduction of LTC insurance: Goals and rationale (4/4)

• Reshaping of the welfare state rather than expansion:

– Introduction of LTCI was accompanied by cuts in other welfare

state areas

– LTCI marks break with German tradition of service provision

according to needs (as in health insurance)

– LTCI Act was shaped in order to prevent any “cost explosion”

thereafter

• tight definition of dependency

• capped benefits (nominally fixed)

• discretionary adjustment of benefits

• Compromise between Christian Democrats and Liberals:

two-pillar system with

– Social LTCI as PAYGO system, but

– Private mandatory insurance as funded system

Prof. Dr. Heinz Rothgang 10

Contents

I. Long-term care and healthcare in Germany

II. LTCI in Germany: Some Basic Facts

1. Basic institutional arrangements

2. Utilization: Extramural and intramural care

3. Benefits and co-payments

4. Remuneration and regional variations

5. Social Assistance

6. Overall financing

III. Issues of debate and for future reforms

IV. Lessons to be learned

Prof. Dr. Heinz Rothgang 11

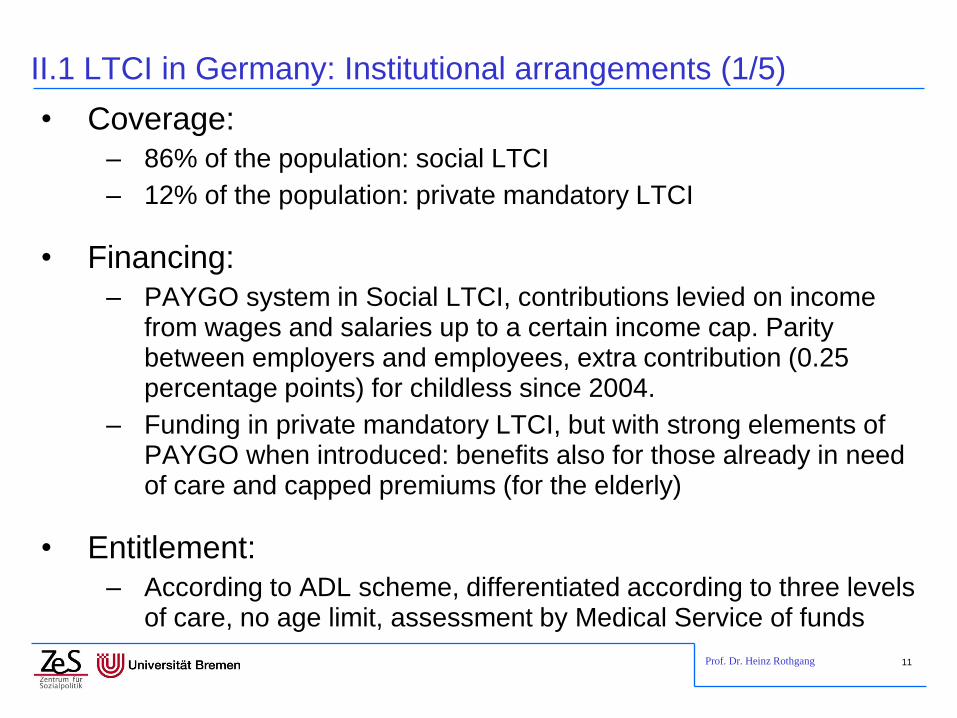

II.1 LTCI in Germany: Institutional arrangements (1/5)

• Coverage:

– 86% of the population: social LTCI

– 12% of the population: private mandatory LTCI

• Financing:

– PAYGO system in Social LTCI, contributions levied on income from wages and salaries up to a certain income cap. Parity between employers and employees, extra contribution (0.25 percentage points) for childless since 2004.

– Funding in private mandatory LTCI, but with strong elements of PAYGO when introduced: benefits also for those already in need of care and capped premiums (for the elderly)

• Entitlement:

– According to ADL scheme, differentiated according to three levels of care, no age limit, assessment by Medical Service of funds

Prof. Dr. Heinz Rothgang 12

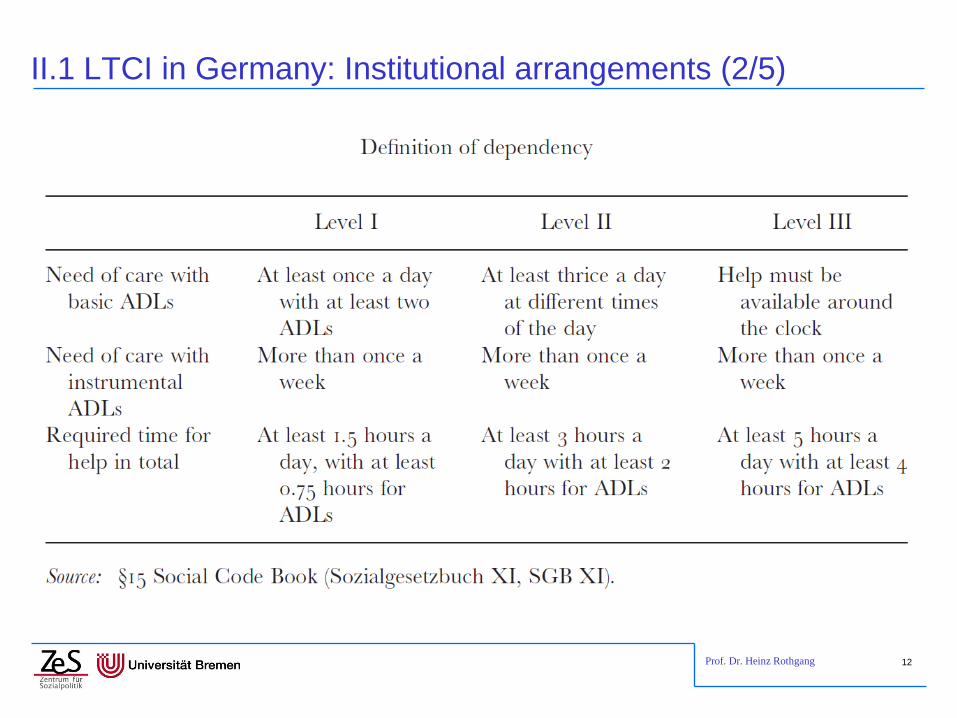

II.1 LTCI in Germany: Institutional arrangements (2/5)

Prof. Dr. Heinz Rothgang 13

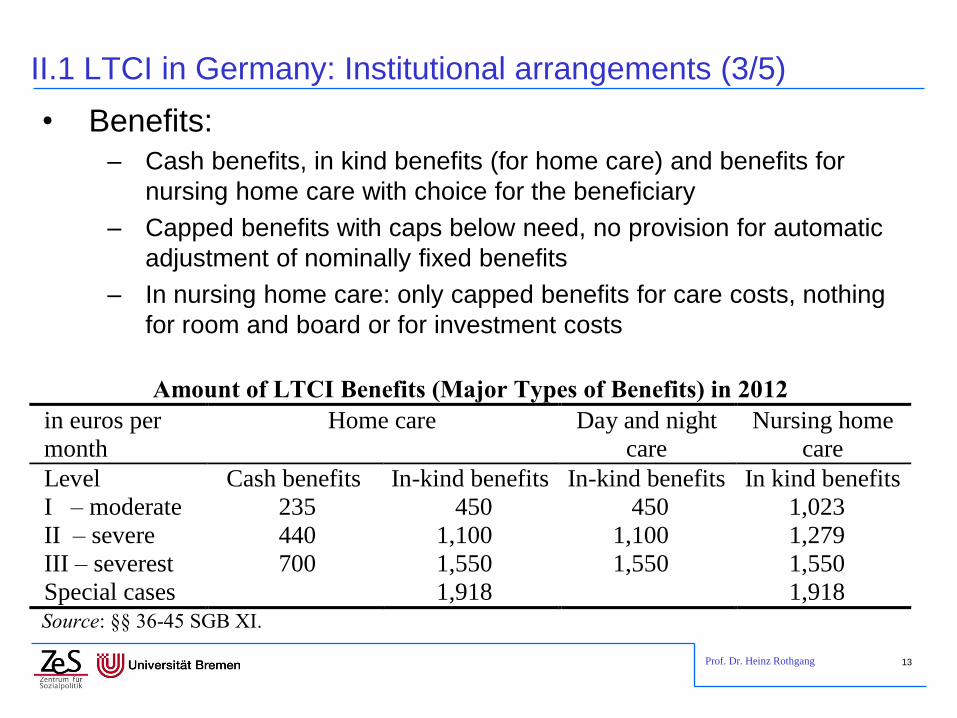

II.1 LTCI in Germany: Institutional arrangements (3/5)

• Benefits:

– Cash benefits, in kind benefits (for home care) and benefits for

nursing home care with choice for the beneficiary

– Capped benefits with caps below need, no provision for automatic

adjustment of nominally fixed benefits

– In nursing home care: only capped benefits for care costs, nothing

for room and board or for investment costs

Amount of LTCI Benefits (Major Types of Benefits) in 2012

in euros per

month

Home care Day and night

care

Nursing home

care

Level Cash benefits In-kind benefits In-kind benefits In kind benefits

I – moderate 235 450 450 1,023

II – severe 440 1,100 1,100 1,279

III – severest 700 1,550 1,550 1,550

Special cases 1,918 1,918 Source: §§ 36-45 SGB XI.

Prof. Dr. Heinz Rothgang 14

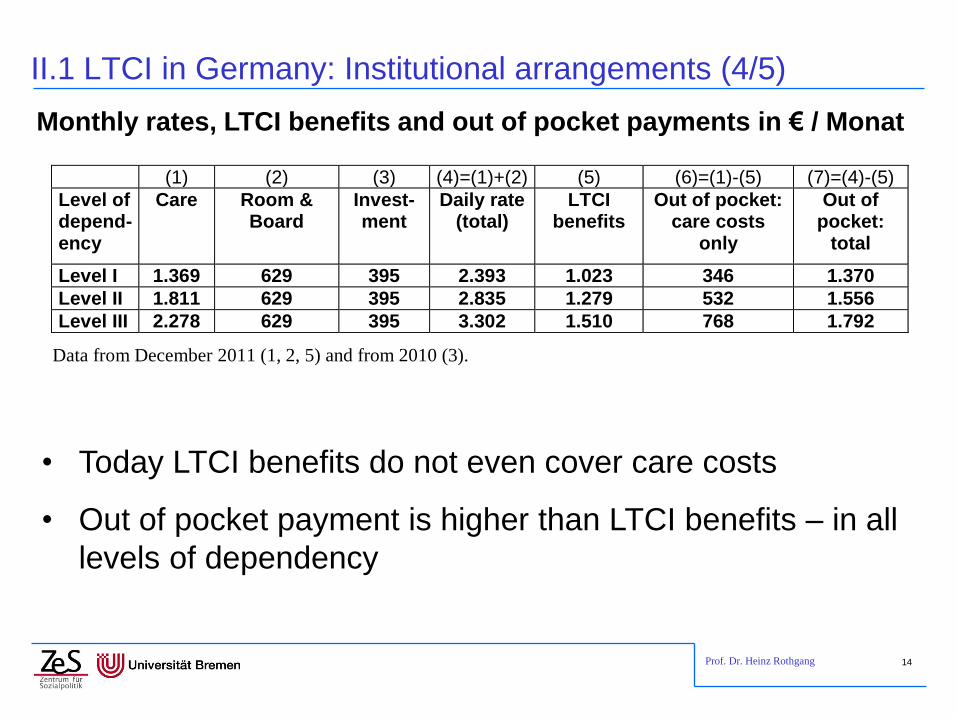

II.1 LTCI in Germany: Institutional arrangements (4/5)

• Today LTCI benefits do not even cover care costs

• Out of pocket payment is higher than LTCI benefits – in all

levels of dependency

(1) (2) (3) (4)=(1)+(2) (5) (6)=(1)-(5) (7)=(4)-(5)

Level of depend-ency

Care Room & Board

Invest-ment

Daily rate (total)

LTCI benefits

Out of pocket: care costs

only

Out of pocket:

total

Level I 1.369 629 395 2.393 1.023 346 1.370

Level II 1.811 629 395 2.835 1.279 532 1.556

Level III 2.278 629 395 3.302 1.510 768 1.792

Data from December 2011 (1, 2, 5) and from 2010 (3).

Monthly rates, LTCI benefits and out of pocket payments in € / Monat

Prof. Dr. Heinz Rothgang 15

II.1 LTCI in Germany: Institutional arrangements (5/5)

• Administration:

– Social LTCI is administered by LTCI funds founded as a branch of

the respective sickness fund. LTCI is independent but under the

umbrella of health insurance

– No competition between funds as all contributions go into one

fund which covers all expenditure

difference to health insurance

– Health Ministry oversees LTC but is not directly involved in

organizing it

– Providers have a legal right to contracts with funds if they fulfil

certain requirements no capacity planning!

Prof. Dr. Heinz Rothgang 16

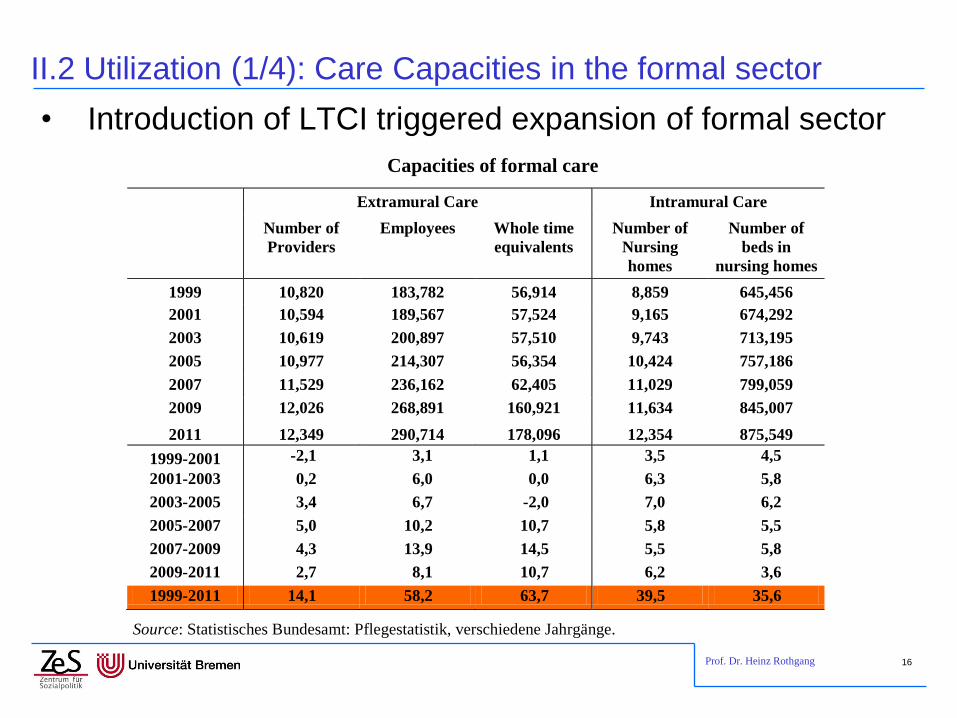

II.2 Utilization (1/4): Care Capacities in the formal sector

• Introduction of LTCI triggered expansion of formal sector

Capacities of formal care

Extramural Care Intramural Care

Number of

Providers

Employees Whole time

equivalents

Number of

Nursing

homes

Number of

beds in

nursing homes

1999 10,820 183,782 56,914 8,859 645,456

2001 10,594 189,567 57,524 9,165 674,292

2003 10,619 200,897 57,510 9,743 713,195

2005 10,977 214,307 56,354 10,424 757,186

2007 11,529 236,162 62,405 11,029 799,059

2009 12,026 268,891 160,921 11,634 845,007

2011 12,349 290,714 178,096 12,354 875,549

1999-2001 -2,1 3,1 1,1 3,5 4,5

2001-2003 0,2 6,0 0,0 6,3 5,8

2003-2005 3,4 6,7 -2,0 7,0 6,2

2005-2007 5,0 10,2 10,7 5,8 5,5

2007-2009 4,3 13,9 14,5 5,5 5,8

2009-2011 2,7 8,1 10,7 6,2 3,6

1999-2011 14,1 58,2 63,7 39,5 35,6

Source: Statistisches Bundesamt: Pflegestatistik, verschiedene Jahrgänge.

Prof. Dr. Heinz Rothgang 17

II.2 Utilization (2/4): Extramural vs. intramural care

• LTCI aims to favour family care over (formal) community care over nursing home care

• There are several measures favouring home care, e.g.

– Cash benefits for family care

– Pension benefits for informal care-givers

– Higher benefits for home care (in level I and II)

– Substitute caregivers for vacations

– Counselling

– Practical training (“Pflegekurse”)

• Nevertheless, there has been a trend towards formal care,

though the rate of the shift is declining

Prof. Dr. Heinz Rothgang 18

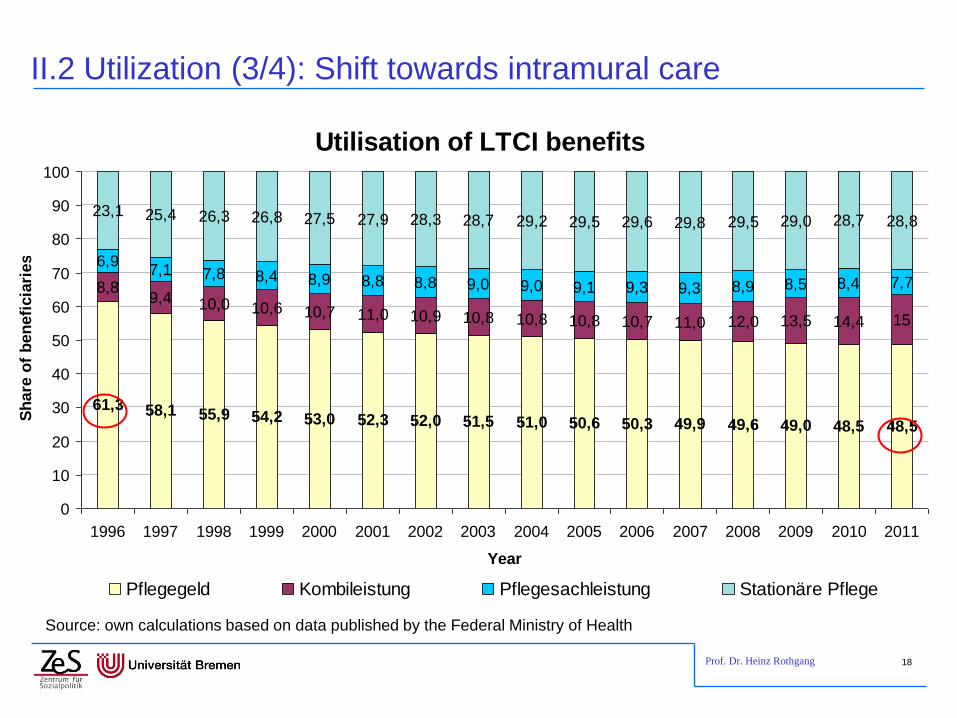

II.2 Utilization (3/4): Shift towards intramural care

Source: own calculations based on data published by the Federal Ministry of Health

Utilisation of LTCI benefits

61,3 58,1 55,9 54,2 53,0 52,3 52,0 51,5 51,0 50,6 50,3 49,9 49,6 49,0 48,5 48,5

8,89,4 10,0 10,6 10,7 11,0 10,9 10,8 10,8 10,8 10,7 11,0 12,0 13,5 14,4 15

6,97,1 7,8 8,4 8,9 8,8 8,8 9,0 9,0 9,1 9,3 9,3 8,9 8,5 8,4 7,7

23,1 25,4 26,3 26,8 27,5 27,9 28,3 28,7 29,2 29,5 29,6 29,8 29,5 29,0 28,7 28,8

0

10

20

30

40

50

60

70

80

90

100

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Year

Sh

are

of

ben

efi

cia

ries

Pflegegeld Kombileistung Pflegesachleistung Stationäre Pflege

Prof. Dr. Heinz Rothgang 19

II.2 Utilization (4/4): The Future

• There are good reasons to assume a continuation of this trend

– Demography: Decreasing share of informal caregivers per dependent elderly

– Socio-structural change: Increasing share of 1-person households among elderly; children live further away

– Increase female labour market participation higher opportunity costs of family care-giving

– Declining “duty to care” felt by families

Prof. Dr. Heinz Rothgang 20

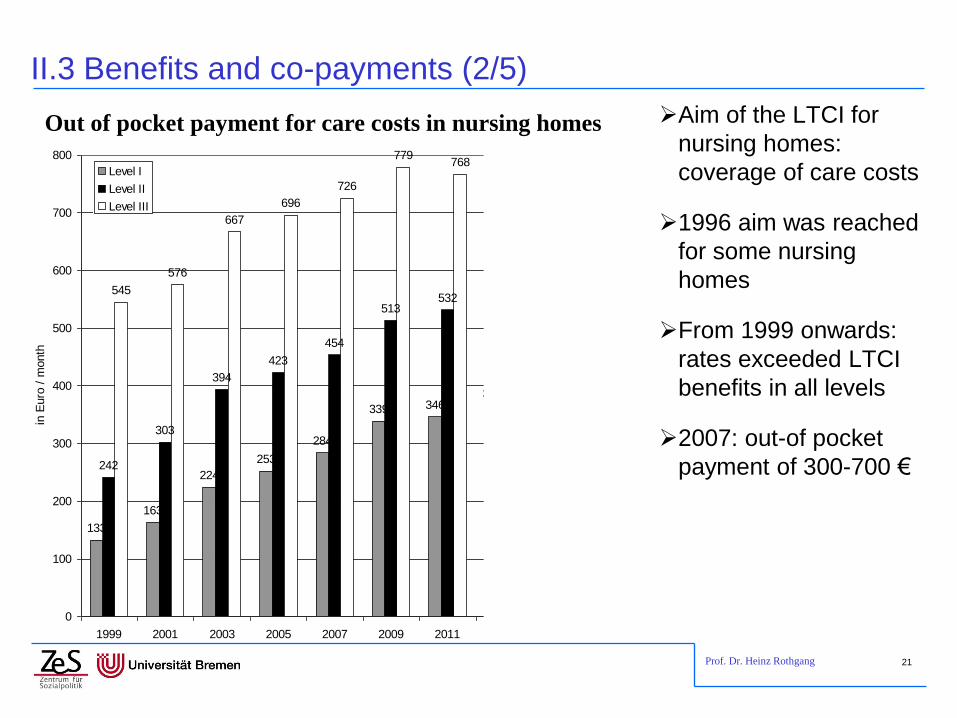

II.3 Benefits and co-payments (1/5)

• From 1994 to 2008 LTCI benefits have been kept constant

in nominal terms.

• Real purchasing power has been decreasing considerably

and out of pocket payments increased.

Prof. Dr. Heinz Rothgang 21

II.3 Benefits and co-payments (2/5)

Aim of the LTCI for

nursing homes:

coverage of care costs

1996 aim was reached

for some nursing

homes

From 1999 onwards:

rates exceeded LTCI

benefits in all levels

2007: out-of pocket

payment of 300-700 €

133

163

224

253

284

339 346365

385

242

303

394

423

454

513532

558

585

545

576

667

696

726

779768

755

782

0

100

200

300

400

500

600

700

800

1999 2001 2003 2005 2007 2009 2011 2013 2015

in E

uro

/ m

onth

Level I

Level II

Level III

Out of pocket payment for care costs in nursing homes

Prof. Dr. Heinz Rothgang 22

II.3 Benefits and co-payments (3/5)

• From 1994 to 2008 LTCI benefits have been kept constant in

nominal terms.

• Real purchasing power has been decreasing considerably

and out of pocket payments increased.

• Only 2008 a first adjustment was introduced

– Increase: 1.4 per cent per year for 2007-2012, about inflation rate

– Financed by an increase in contribution rate from 1.7 to 1.95 percent

– For some benefits there is no increase at all

Prof. Dr. Heinz Rothgang 23

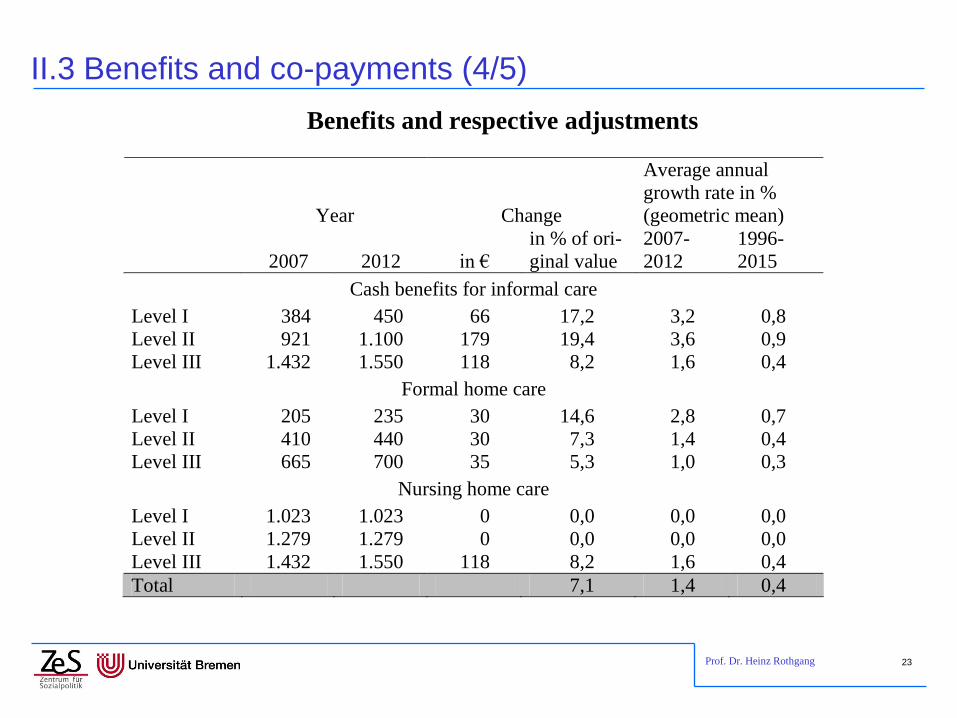

II.3 Benefits and co-payments (4/5)

Benefits and respective adjustments

Year Change

Average annual

growth rate in %

(geometric mean)

2007 2012 in €

in % of ori-

ginal value

2007-

2012

1996-

2015

Cash benefits for informal care

Level I 384 450 66 17,2 3,2 0,8

Level II 921 1.100 179 19,4 3,6 0,9

Level III 1.432 1.550 118 8,2 1,6 0,4

Formal home care

Level I 205 235 30 14,6 2,8 0,7

Level II 410 440 30 7,3 1,4 0,4

Level III 665 700 35 5,3 1,0 0,3

Nursing home care

Level I 1.023 1.023 0 0,0 0,0 0,0

Level II 1.279 1.279 0 0,0 0,0 0,0

Level III 1.432 1.550 118 8,2 1,6 0,4

Total 7,1 1,4 0,4

Prof. Dr. Heinz Rothgang 24

133

163

224

253

284

339 346365

385

242

303

394

423

454

513532

558

585

545

576

667

696

726

779768

755

782

0

100

200

300

400

500

600

700

800

1999 2001 2003 2005 2007 2009 2011 2013 2015

in E

uro

/ m

onth

Level I

Level II

Level III

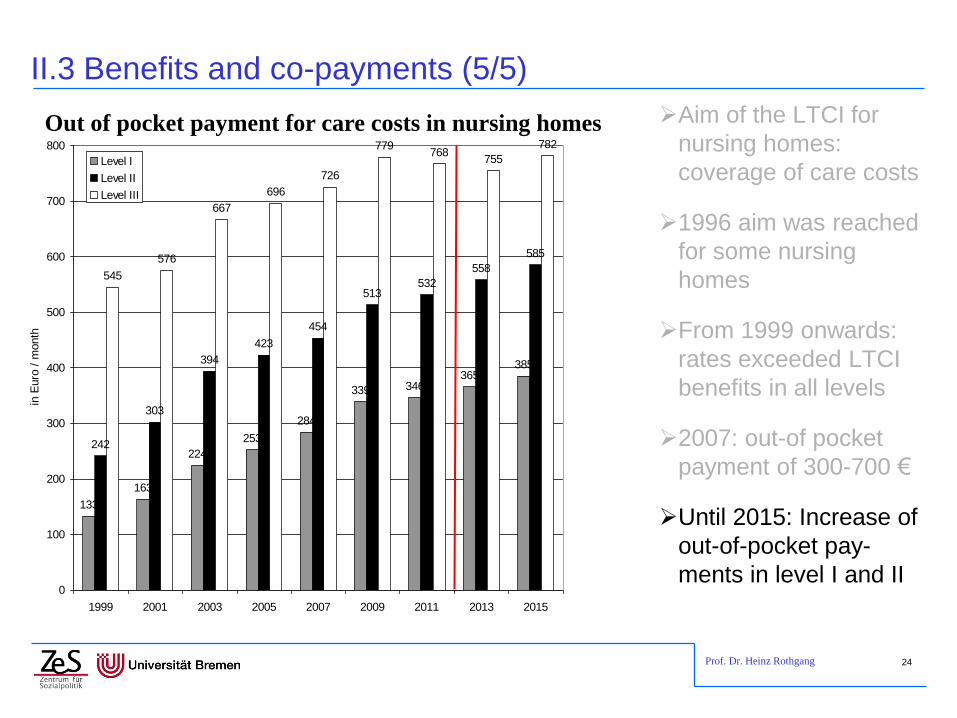

II.3 Benefits and co-payments (5/5)

Aim of the LTCI for

nursing homes:

coverage of care costs

1996 aim was reached

for some nursing

homes

From 1999 onwards:

rates exceeded LTCI

benefits in all levels

2007: out-of pocket

payment of 300-700 €

Until 2015: Increase of

out-of-pocket pay-

ments in level I and II

Out of pocket payment for care costs in nursing homes

Prof. Dr. Heinz Rothgang 25

II.4 Remuneration: Institutional arrangements

• Nursing homes

– are remunerated by daily rates for

• care costs,

• room & board and

• Investment cost (as far as not publicly financed)

– LTCI benefits are for care costs only,

– Room and board costs are for inhabitants (social assistant)

– Investment should be financed by provinces, uncovered

investment cost are for inhabitants (social assistance)

• Rates are negotiated between

– LTCI funds and social assistance

– Nursing homes

• Negotiations are based on external comparisons and

individual costs. Negotiations differ between provinces

Prof. Dr. Heinz Rothgang 26

II.4 Remuneration: Institutional arrangements

• Home care

– Remuneration is based on about two dozens of service packages

(“Leistungskomplexe”) which differ between provinces

– Relative prices (“points per complex”) are assigned to those

services

– This fee scale as well as the remuneration level (value of a

“point”) are negotiated on the “Länder” level.

– Due to different definitions of the service packages remuneration

levels are hard to compare between provinces

Prof. Dr. Heinz Rothgang 27

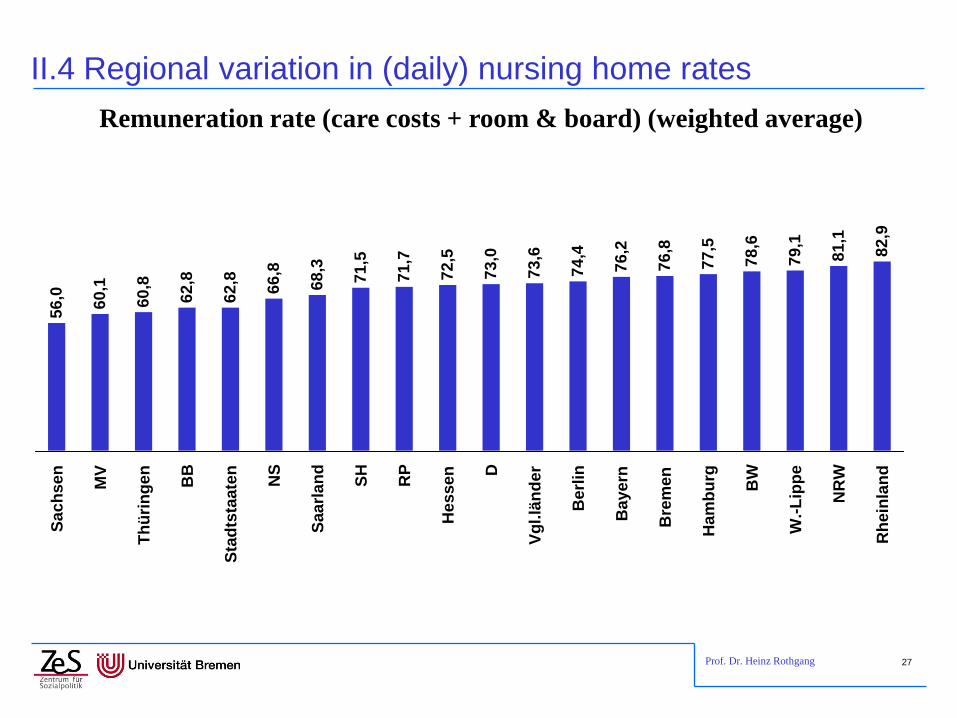

II.4 Regional variation in (daily) nursing home rates

Remuneration rate (care costs + room & board) (weighted average)

56,0

60,1

60,8

62,8

62,8

66,8

68,3

71,5

71,7

72,5

73,0

73,6

74,4

76,2

76,8

77,5

78,6

79,1

81,1

82,9

Sach

sen

MV

Th

üri

ng

en

BB

Sta

dts

taate

n

NS

Saarl

an

d

SH

RP

Hessen D

Vg

l.lä

nd

er

Berl

in

Bayern

Bre

men

Ham

bu

rg

BW

W.-

Lip

pe

NR

W

Rh

ein

lan

d

Prof. Dr. Heinz Rothgang 28

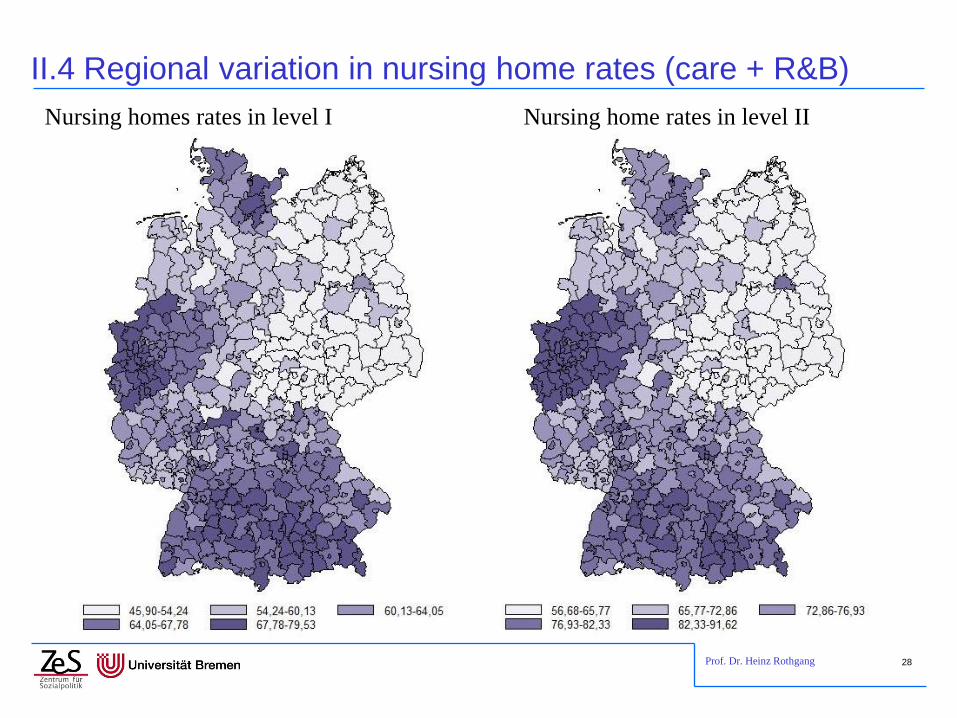

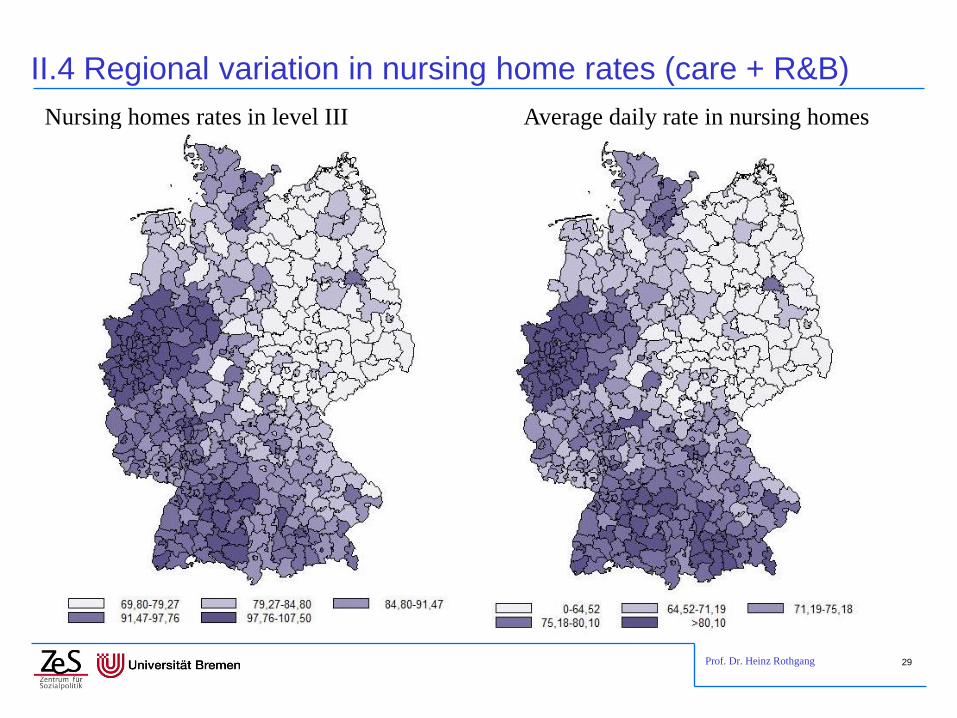

II.4 Regional variation in nursing home rates (care + R&B)

Nursing homes rates in level I Nursing home rates in level II

Prof. Dr. Heinz Rothgang 29

II.4 Regional variation in nursing home rates (care + R&B)

Nursing homes rates in level III Average daily rate in nursing homes

Prof. Dr. Heinz Rothgang 30

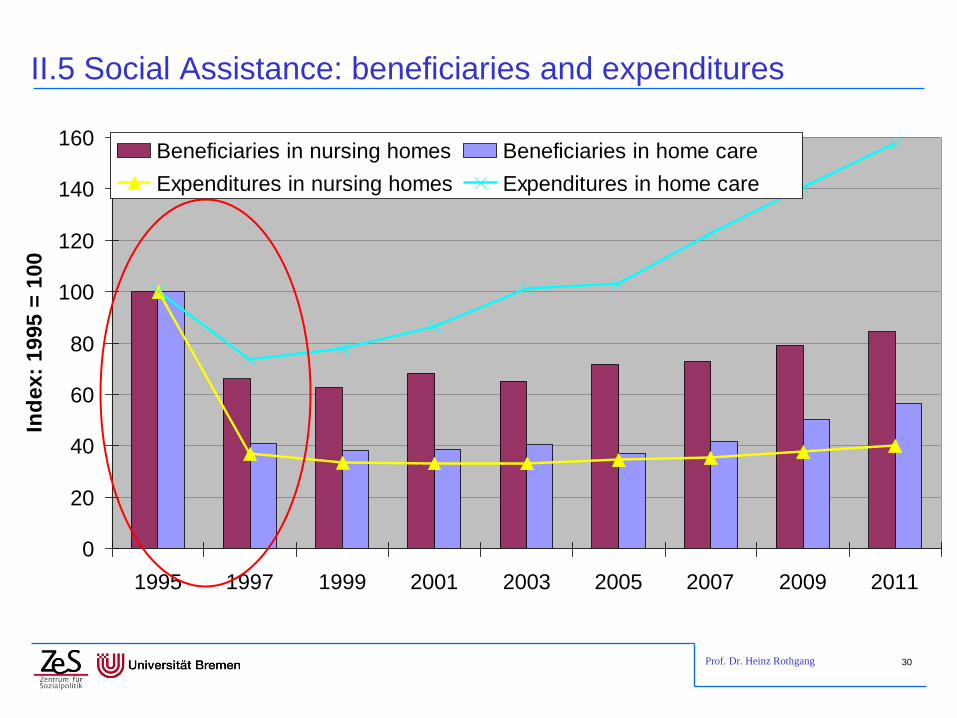

II.5 Social Assistance: beneficiaries and expenditures

0

20

40

60

80

100

120

140

160

1995 1997 1999 2001 2003 2005 2007 2009 2011

Ind

ex:

1995 =

100

Beneficiaries in nursing homes Beneficiaries in home care

Expenditures in nursing homes Expenditures in home care

Prof. Dr. Heinz Rothgang 31

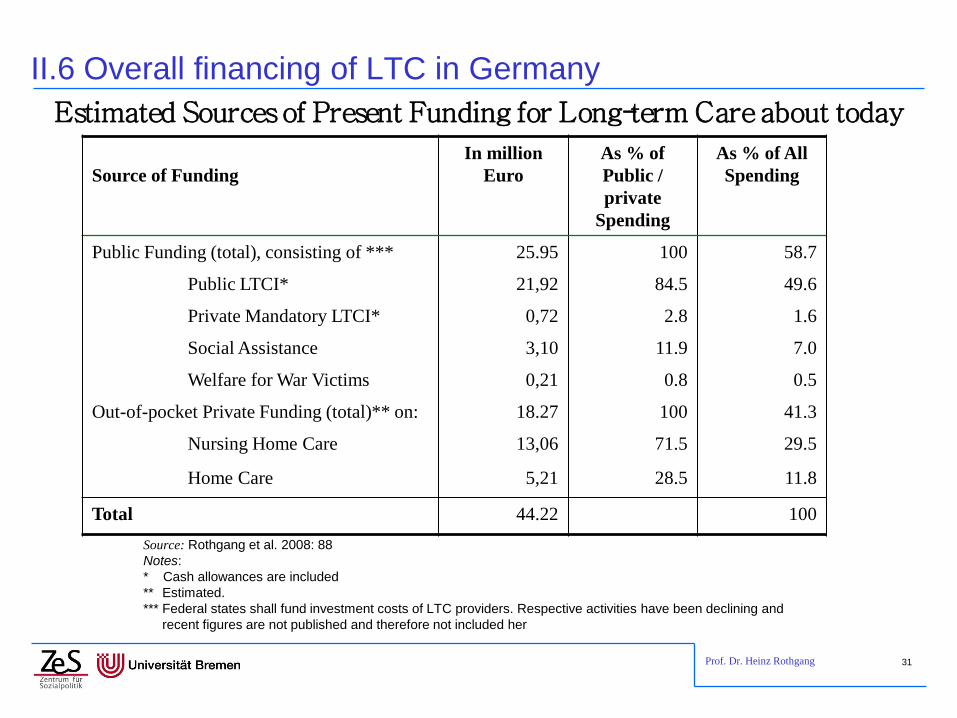

II.6 Overall financing of LTC in Germany

Estimated Sources of Present Funding for Long-term Care about today

Source of Funding

In million

Euro

As % of

Public /

private

Spending

As % of All

Spending

Public Funding (total), consisting of *** 25.95 100 58.7

Public LTCI* 21,92 84.5 49.6

Private Mandatory LTCI* 0,72 2.8 1.6

Social Assistance 3,10 11.9 7.0

Welfare for War Victims 0,21 0.8 0.5

Out-of-pocket Private Funding (total)** on: 18.27 100 41.3

Nursing Home Care 13,06 71.5 29.5

Home Care 5,21 28.5 11.8

Total 44.22 100

Source: Rothgang et al. 2008: 88

Notes:

* Cash allowances are included

** Estimated.

*** Federal states shall fund investment costs of LTC providers. Respective activities have been declining and

recent figures are not published and therefore not included her

Prof. Dr. Heinz Rothgang 32

Contents

I. Long-term care and healthcare in Germany

II. LTCI in Germany: Some Basic Facts

III. Issues of actual debate and for future reforms

1. Future financing

2. Needs assessment and entitlement

3. Quality of care, case and care management

4. Future Caregiving

IV. Lessons to be learned

Prof. Dr. Heinz Rothgang 33

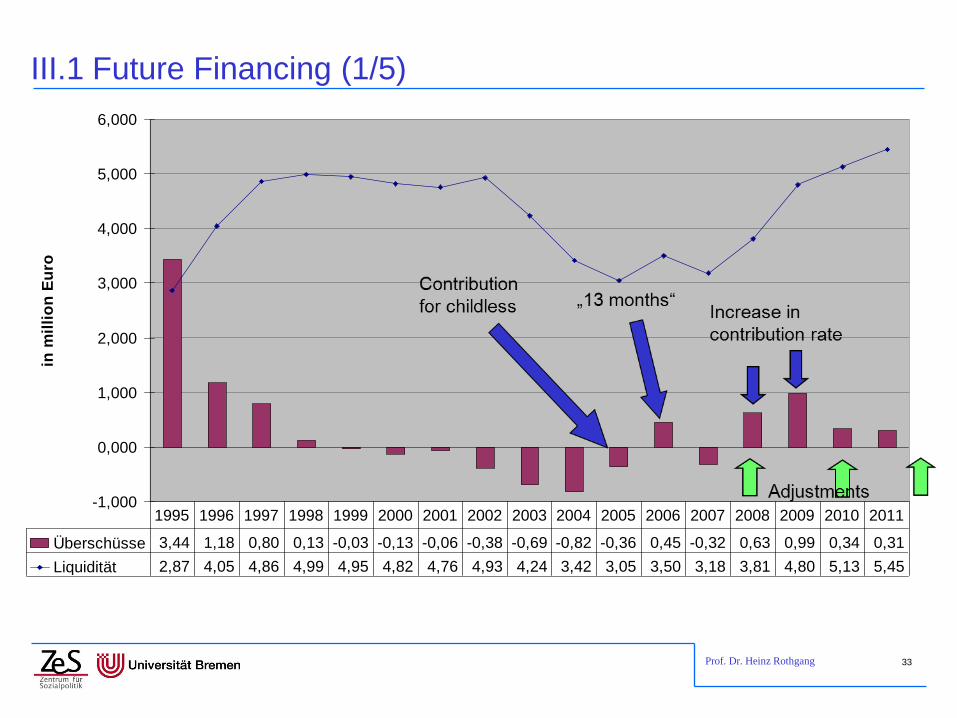

III.1 Future Financing (1/5)

-1,000

0,000

1,000

2,000

3,000

4,000

5,000

6,000

in m

illi

on

Eu

ro

Überschüsse 3,44 1,18 0,80 0,13 -0,03 -0,13 -0,06 -0,38 -0,69 -0,82 -0,36 0,45 -0,32 0,63 0,99 0,34 0,31

Liquidität 2,87 4,05 4,86 4,99 4,95 4,82 4,76 4,93 4,24 3,42 3,05 3,50 3,18 3,81 4,80 5,13 5,45

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Prof. Dr. Heinz Rothgang 34

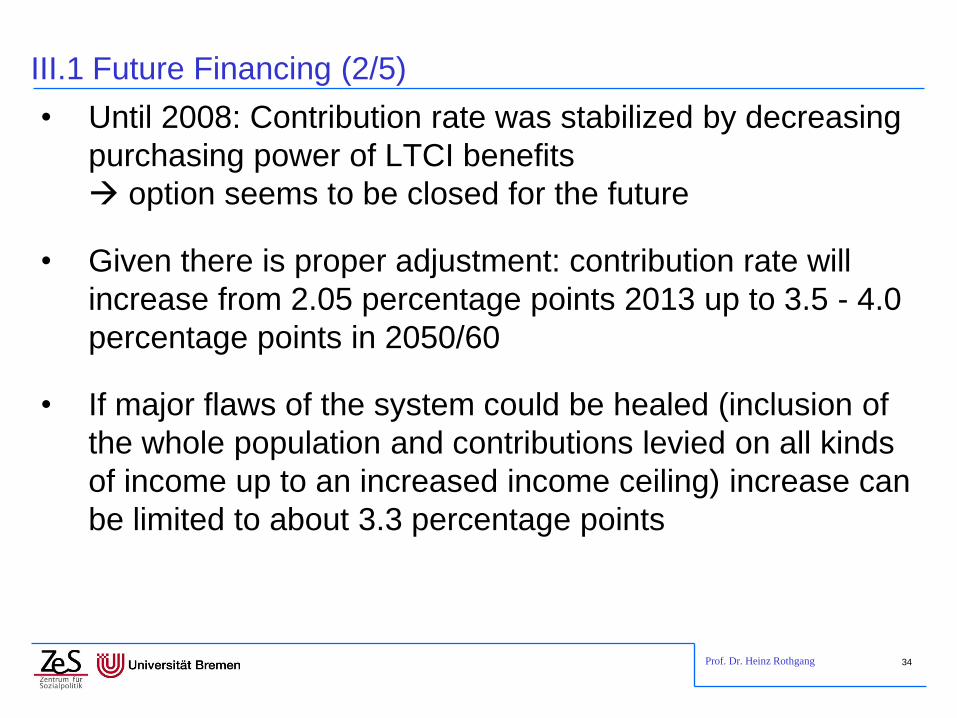

III.1 Future Financing (2/5)

• Until 2008: Contribution rate was stabilized by decreasing

purchasing power of LTCI benefits

option seems to be closed for the future

• Given there is proper adjustment: contribution rate will

increase from 2.05 percentage points 2013 up to 3.5 - 4.0

percentage points in 2050/60

• If major flaws of the system could be healed (inclusion of

the whole population and contributions levied on all kinds

of income up to an increased income ceiling) increase can

be limited to about 3.3 percentage points

Prof. Dr. Heinz Rothgang 35

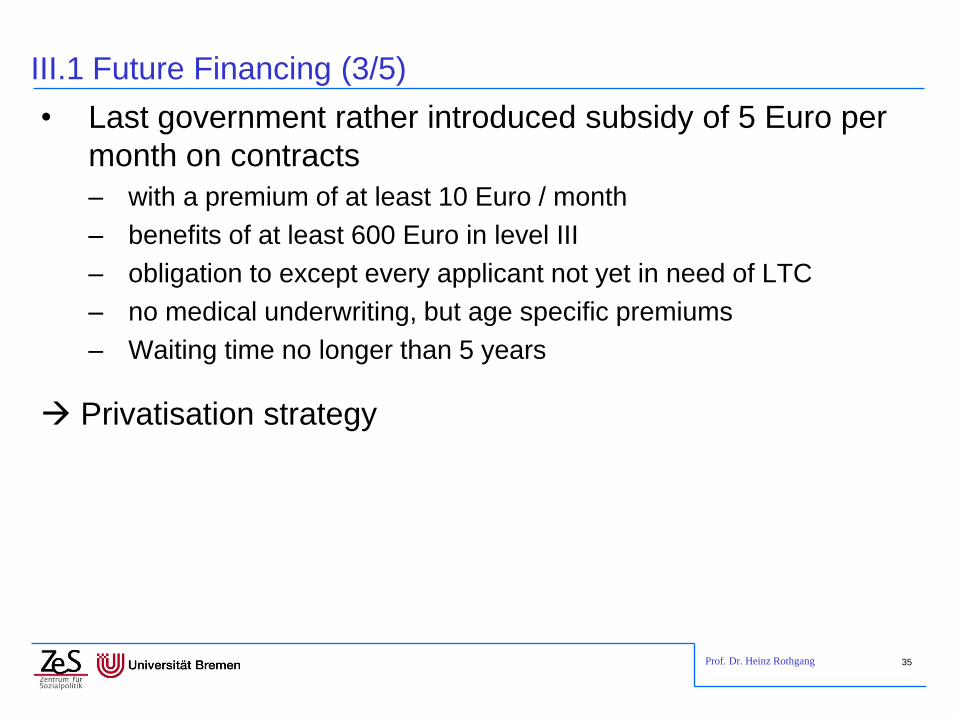

III.1 Future Financing (3/5)

• Last government rather introduced subsidy of 5 Euro per

month on contracts

– with a premium of at least 10 Euro / month

– benefits of at least 600 Euro in level III

– obligation to except every applicant not yet in need of LTC

– no medical underwriting, but age specific premiums

– Waiting time no longer than 5 years

Privatisation strategy

Prof. Dr. Heinz Rothgang 36

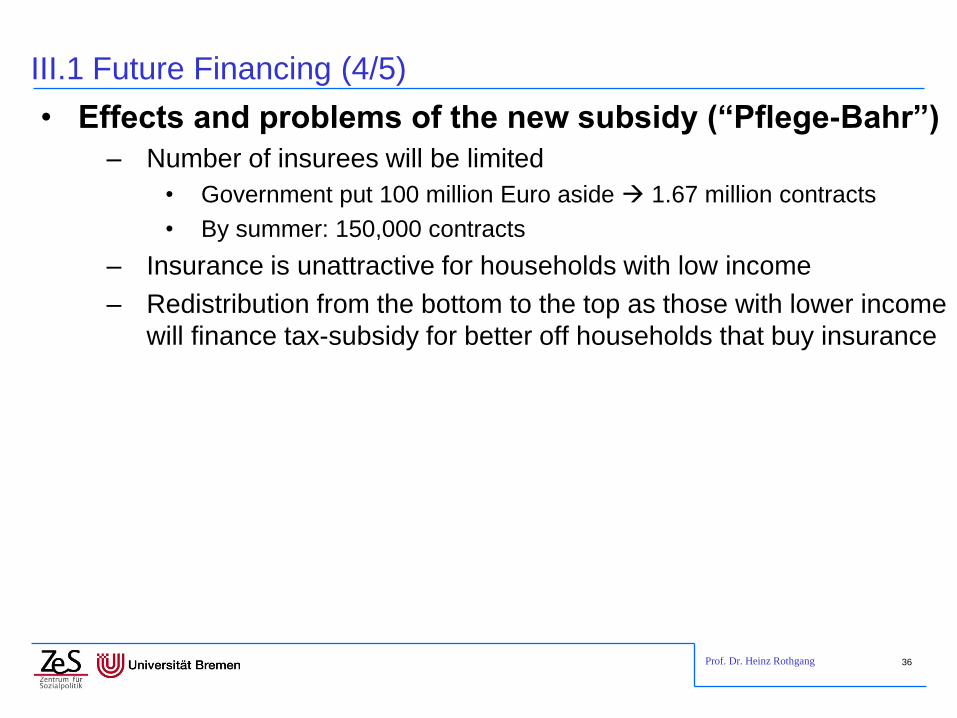

III.1 Future Financing (4/5)

• Effects and problems of the new subsidy (“Pflege-Bahr”)

– Number of insurees will be limited

• Government put 100 million Euro aside 1.67 million contracts

• By summer: 150,000 contracts

– Insurance is unattractive for households with low income

– Redistribution from the bottom to the top as those with lower income

will finance tax-subsidy for better off households that buy insurance

Prof. Dr. Heinz Rothgang 37

III.1 Future Financing (5/5)

• Effects and problems of the new subsidy (“Pflege-Bahr”)

cont.

– Problem of adverse selection

• New insurance is particularly attractive for those who could not buy

“normal” insurance

• Due to this risk selection premiums must be higher

• In the US a respective programme (CLASS Act) was stopped as

“unworkable” last year

• Insurance companies will nevertheless develop products as waiting time

works as a safety net for the first five years and premiums may be raised

thereafter.

– Overall problems result when Pflege-Bahr is used to stop proper

adjustments in Social LTCI

Prof. Dr. Heinz Rothgang 38

III.2 Needs assessment and entitlement (1/2)

• Definition of LTC is very strict, cognitive impairments and

not considered properly when LTC is measured

• Remedy I: Introduction of new benefits

– 2001: up to 460 € per year for people with cognitive impairments

– 2008: benefits up to 1,200 € or 2,400 € per year; benefits also for

people with care level 0; extra staff for people with dementia in

nursing homes

– 2013: additional benefits for people with cognitive impairments

(§ 123 SGB XI)

• Level 0: 120 / 225 € per month (cash benefits, in kind benefits)

• Level I: 70 / 215 € per month (cash benefits, in kind benefits )

• Level II: 85 / 150 € per month (cash benefits, in kind benefits)

Prof. Dr. Heinz Rothgang 39

III.2 Needs assessment and entitlement (2/2)

• Remedy II: Expert Commission for the developent of a

new entitlement

– 2006–09: Development of new definition and assessment

reports in Feb and June

– 2009–12: though positively perceived: nothing happens

– 2012: March re-establishment of expert commission, report in

spring 2013

– Plans to implement new assessment in next reform

Prof. Dr. Heinz Rothgang 40

III.3 Quality of care

• Introduction of LTCI has raised awareness more

scandals are revealed

• Quality improvement has been a major issue:

– 2002: Pflege-Qualitätsstärkungsgesetz (PQsG): attempt to enforce

control by contracts between funds and providers: never introduced

properly, failed

– 2008 reform

• Increased obligations for internal quality management

• Tenfold increased in frequency of quality controls by Medical Service

• Publication of reports from quality controls in a digestible way

introduction of competition based on quality

• Quality is still a major issue

Prof. Dr. Heinz Rothgang 41

III.3 Case and care management

• There is a lack of proper case and care management for people in need of long-term care

• The 2008 reform introduced the obligation to funds to provide case management and introduced “Pflegestützpunkte”, i.e. local centers providing counseling

• Implementation has been slow as neither Länder nor LTC funds are too enthusiastic

• Evaluations rather reveal “Pflegestützpunkte” as a failure as they are not just much

Prof. Dr. Heinz Rothgang 42

III.4 Future care-giving

• The problem:

– Family care-giving has been on the retreat

– For the future this trend is likely to continue

– With constant recruitment, retaining and return patterns the number

of professional care-workers is going to decline

– Projections show an (additional) gap of about 500,000 full-time

employees in care work by 2030

Who cares?

• Only solution: combined strategy

– Make a career in formal care-giving more attractive

– Stabilize family care via support for informal care-givers and

improved opportunities to combine care-giving and gainful

employment

– Mobilize the potential of community to care.

Prof. Dr. Heinz Rothgang 43

Contents

I. Long-term care and healthcare in Germany

II. LTCI in Germany: Some Basic Facts

III. Issues of debate and for future reforms

IV. Lessons to be learned

Prof. Dr. Heinz Rothgang 44

III. Lessons from the German Experience (1/3)

• Achievements – Acknowledging long-term care as a social risk

– Coverage of the whole population

– Increasing public spending: factor 2.5

– Reducing the number of people in nursing homes depending on welfare

– Huge reducing of expenditure on social assistant for people in nursing homes

– Improving care infrastructure (quantitative)

– Putting the quality issue on the agenda

– Work with a stable contribution rate for 15 years

Prof. Dr. Heinz Rothgang 45

III. Lessons from the German Experience (2/3)

• Room for improvement

– Benefits

• Definition of entitlement: better provision for dementia

• Too little rehabilitation

• Quality of care

• Future sustainable care structures

• Proper adjustment of benefits

– Financing: sustainable financing

Prof. Dr. Heinz Rothgang 46

III. Lessons from the German Experience (3/3)

• The German experience shows:

– A social insurance system should relate to the whole population.

– Contributions should be levied on all kinds of income, not just on income from gainful employment.

– Due to demographic and socio-demographic change over time the contribution rate necessarily goes up.

– Considerably co-payments are possible, but proper adjustment of benefits is vital.

– The definition of entitlement should be broad enough to include e.g. people suffering from dementia properly.

– Case and care management is necessary, particularly if beneficiaries may choose between different kinds of benefits.

– Support for family care is necessary if informal care has a role in care-giving

Prof. Dr. Heinz Rothgang 47

The end

Thank you for your attention!

Contact: [email protected]

See also:

Rothgang, Heinz (2010): Social Insurance for Long-Term Care: An Evaluation of the German

Model, in: Social Policy and Administration, Vol. 44, No. 4, August 2010, pp. 436–460