international energy agency world energy outlook strategic challenges hideshi emoto senior energy...

TRANSCRIPT

INTERNATIONAL ENERGY AGENCY

World Energy Outlook World Energy Outlook Strategic ChallengesStrategic Challenges

Hideshi EmotoHideshi EmotoSenior Energy Analyst Senior Energy Analyst

International Energy AgencyInternational Energy Agency

INTERNATIONALENERGY AGENCY

Energy Trends & Strategic ChallengesReference Scenario

INTERNATIONALENERGY AGENCY

World Primary Energy Demand

Fossil fuels account for more than 80% of the growth in energy demand between now and 2030

0

1 000

2 000

3 000

4 000

5 000

6 000

1970 1980 1990 2000 2010 2020 2030

Mto

eOil

Natural gas

Coal

Nuclear power

Hydro power

Other renewables

0

1 000

2 000

3 000

4 000

5 000

6 000

1970 1980 1990 2000 2010 2020 2030

Mto

eOil

Natural gas

Coal

Nuclear power

Hydro power

Other renewables

INTERNATIONALENERGY AGENCY

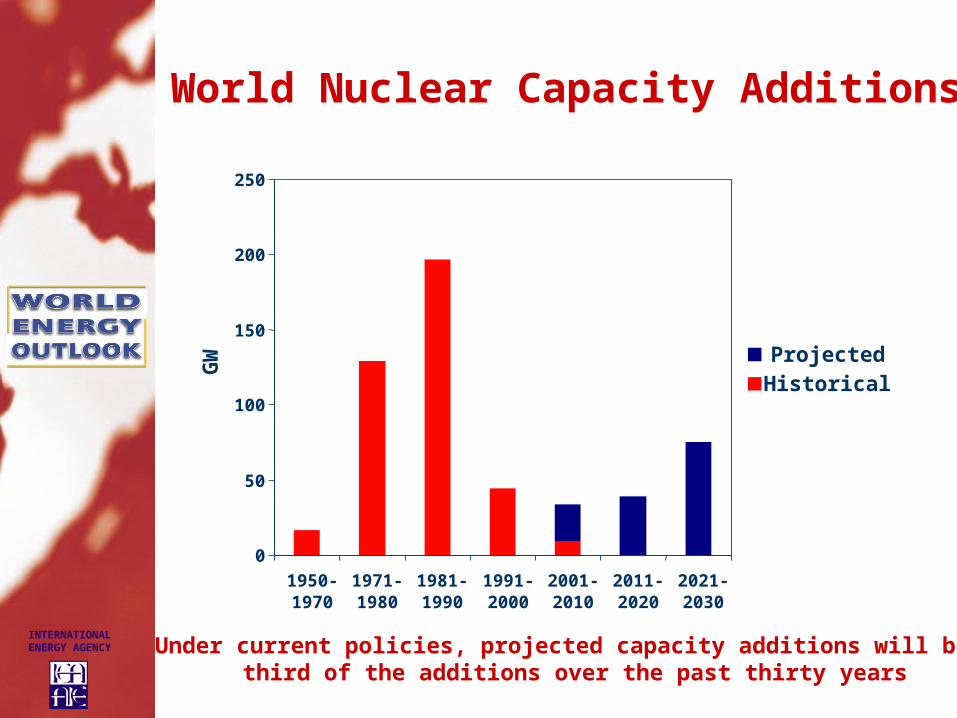

World Nuclear Capacity Additions

Under current policies, projected capacity additions will be a third of the additions over the past thirty years

0

50

100

150

200

250

1950-1970

1971-1980

1981-1990

1991-2000

2001-2010

2011-2020

2021-2030

GW Projected

Historical

INTERNATIONALENERGY AGENCY

Challenge 1:Security of

Supply

INTERNATIONALENERGY AGENCY

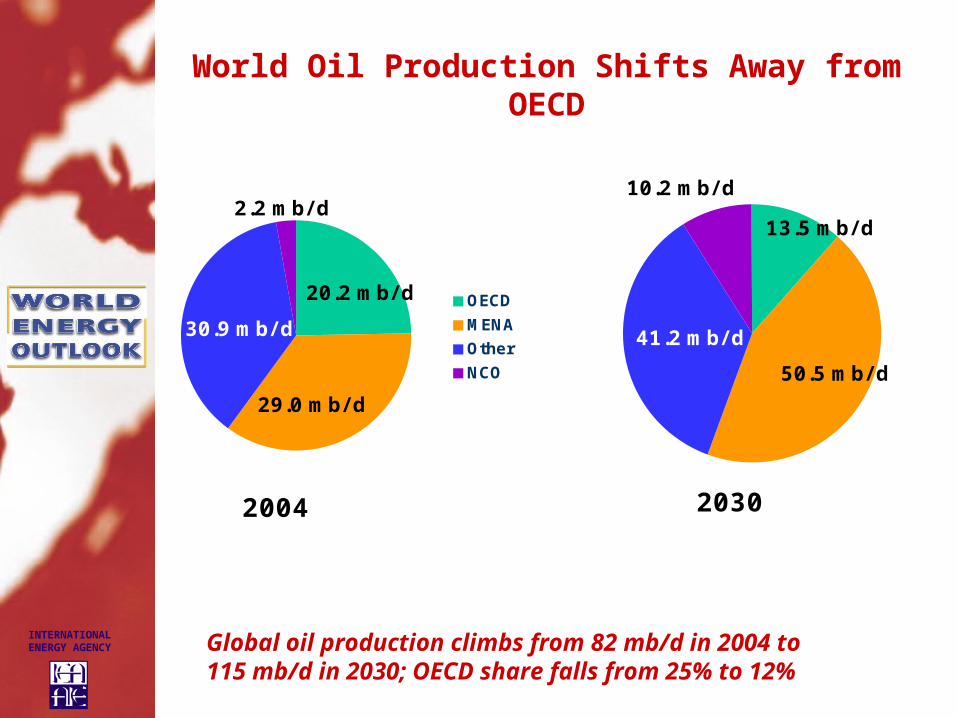

World Oil Production Shifts Away from OECD

Global oil production climbs from 82 mb/d in 2004 to 115 mb/d in 2030; OECD share falls from 25% to 12%

OECD

MENA

Other

NCO

41.2 mb/ d

50.5 mb/ d

13.5 mb/ d

30.9 mb/ d

29.0 mb/ d

20.2 mb/ d

2004 2030

2.2 mb/ d10.2 mb/ d

INTERNATIONALENERGY AGENCY

MENA Crude Oil & NGL Production by Country

MENA’s share of world oil production rises from 35% in 2004 to 44% in 2030 in the RS, with Saudi production rising to over 18

mb/d

0

10

20

30

40

50

1970 1980 1990 2000 2010 2020 2030

mb

/d

Iran Iraq Kuwait Other Middle East Saudi Arabia UAE North Africa

0

10

20

30

40

50

1970 1980 1990 2000 2010 2020 2030

mb

/d

Iran Iraq Kuwait Other Middle East Saudi Arabia UAE North Africa

INTERNATIONALENERGY AGENCY

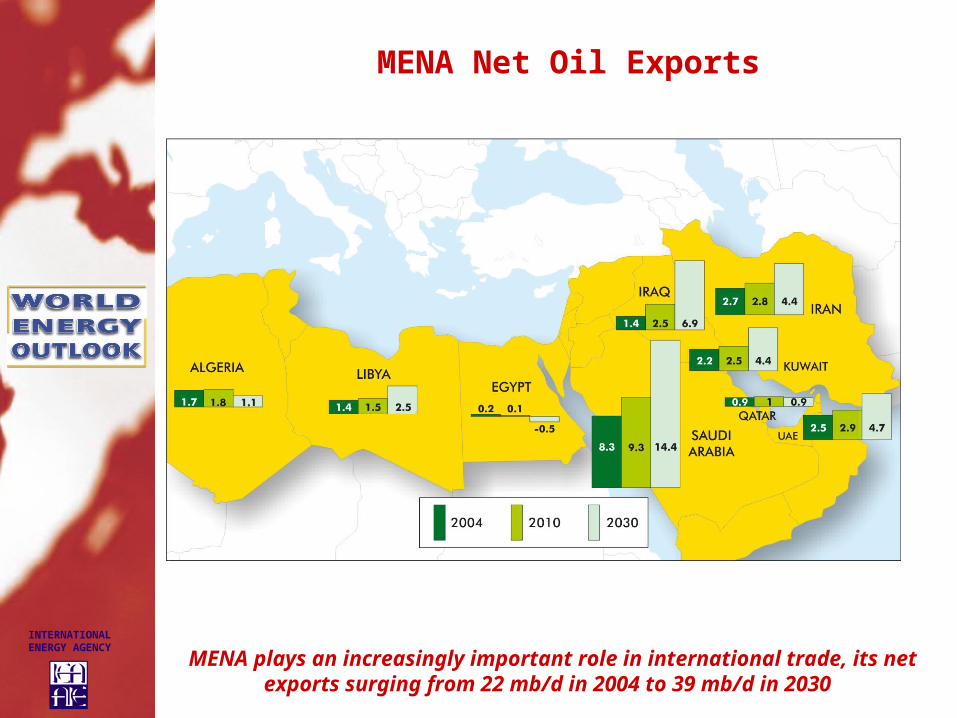

MENA Net Oil Exports

MENA plays an increasingly important role in international trade, its net exports surging from 22 mb/d in 2004 to 39 mb/d

in 2030

INTERNATIONALENERGY AGENCY

Saudi Arabia’s Oil Production by Source in the Reference Scenario

Based on its reserves and global demand trends, Saudi oil production is projected to reach 18 mb/d in 2030

0

4

8

12

16

20

1970 1980 1990 2000 2010 2020 2030

mb

/d

Currently producing fields Fields awaiting development

Reserve additions and new discoveries Total production

INTERNATIONALENERGY AGENCY

Iran’s Oil Balance in the Reference Scenario

Iran oil production reaches 6.8 mb/d in 2030, but exports increase

less rapidly due to strong growth in domestic demand

0

2

4

6

8

1970 1980 1990 2000 2010 2020 2030

mb

/d

Net exports Domestic demand

INTERNATIONALENERGY AGENCY

Oil Production Outlook in Iraq in the Reference Scenario

Oil production in Iraq is expected to reach around 3 mb/d in 2010 and

8 mb/d in 2030, provided that stability and security are restored

0

2

4

6

8

1970 1980 1990 2000 2010 2020 2030

mb

/d

Currently producing fields Fields awaiting development

Reserve additions and new discoveries Total production

INTERNATIONALENERGY AGENCY

Net Oil Imports by OECD Regions

OECD North America

OECD Europe OECD Pacific

0

3

6

9

12

15

18

2004 2030 2004 2030 2004 2030

mb/

d

MENA non MENA

OECD Europe will rely more on MENA oil – imports from MENA reach

8.5 mb/d, or nearly two-thirds of total imports in 2030

INTERNATIONALENERGY AGENCY

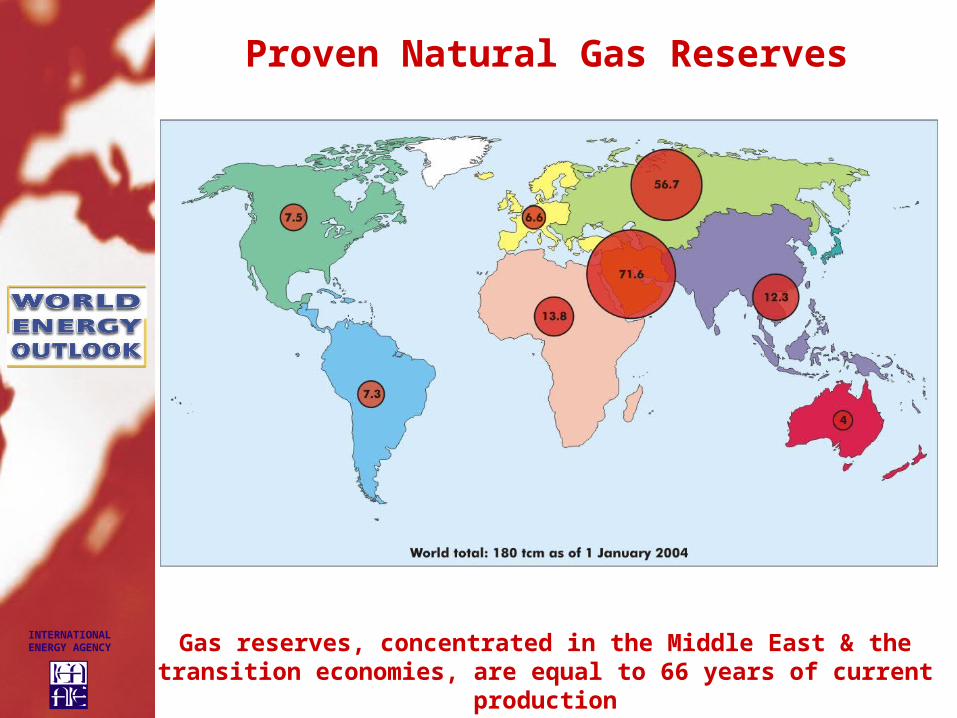

Proven Natural Gas Reserves

Gas reserves, concentrated in the Middle East & the transition economies, are equal to 66 years of current

production

INTERNATIONALENERGY AGENCY

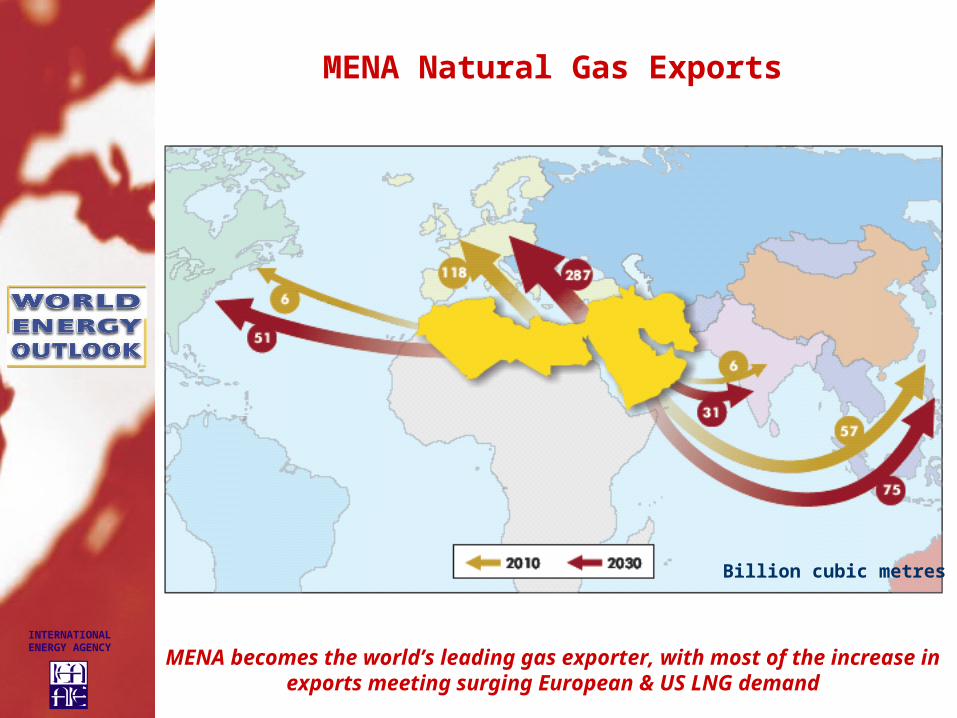

MENA Natural Gas Exports

MENA becomes the world’s leading gas exporter, with most of the increase in exports meeting surging European & US LNG

demand

Billion cubic metres

INTERNATIONALENERGY AGENCY

EU Gas Supply Balance

Rising demand – mainly for power generation – and declining output will cause net imports to surge

0

200

400

600

800

1980 1990 2004 2010 2020 2030

bcm

Production Net imports

INTERNATIONALENERGY AGENCY

Challenge 2:Carbon Dioxide Emissions

INTERNATIONALENERGY AGENCY

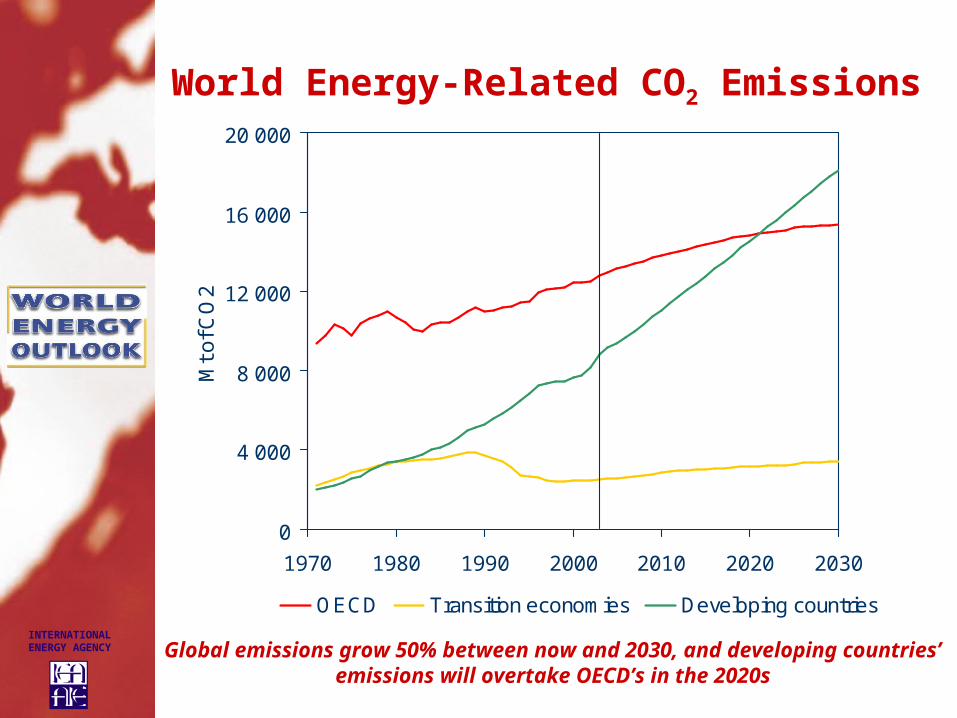

World Energy-Related CO2 Emissions

Global emissions grow 50% between now and 2030, and developing countries’ emissions will overtake OECD’s in the

2020s

0

4 000

8 000

12 000

16 000

20 000

1970 1980 1990 2000 2010 2020 2030

Mt o

f CO

2

OECD Transition economies Developing countries

INTERNATIONALENERGY AGENCY

CO2 Increase, 2004-2030

OECD CO2 additions equal to only three quarters of Chinese CO2 rise, but OECD emissions per capita still two times higher in

2030

0

1 000

2 000

3 000

4 000

China OECD

million

ton

nes

NorthAmerica

Pacific

Europe

0

3

6

9

12

15

ton

nes p

er c

ap

ita

2004

2030

2004

2030

INTERNATIONALENERGY AGENCY

World Alternative Policy Scenario

INTERNATIONALENERGY AGENCY

Key Policies in Alternative Scenario for European Union

Power generationRenewable energy directiveCombined Heat and Power directiveExtension of reactor useful lifetime

Transport sectorProlongation and tightening of Voluntary Agreement with car manufacturersBiofuels target

Residential and commercial sectorsEnergy performance in buildings directiveEnergy labelling

INTERNATIONALENERGY AGENCY

Reduction in Oil Demand in the Alternative vs. Reference Scenario,

2030

Oil savings in 2030 would be equivalent to the combined current production of Saudi Arabia and

the UAE

Oil savings = 12.1 mb/d

Transport64%

Other**4%

Industry13%

Power generation

8%

Residential and services

11%

INTERNATIONALENERGY AGENCY

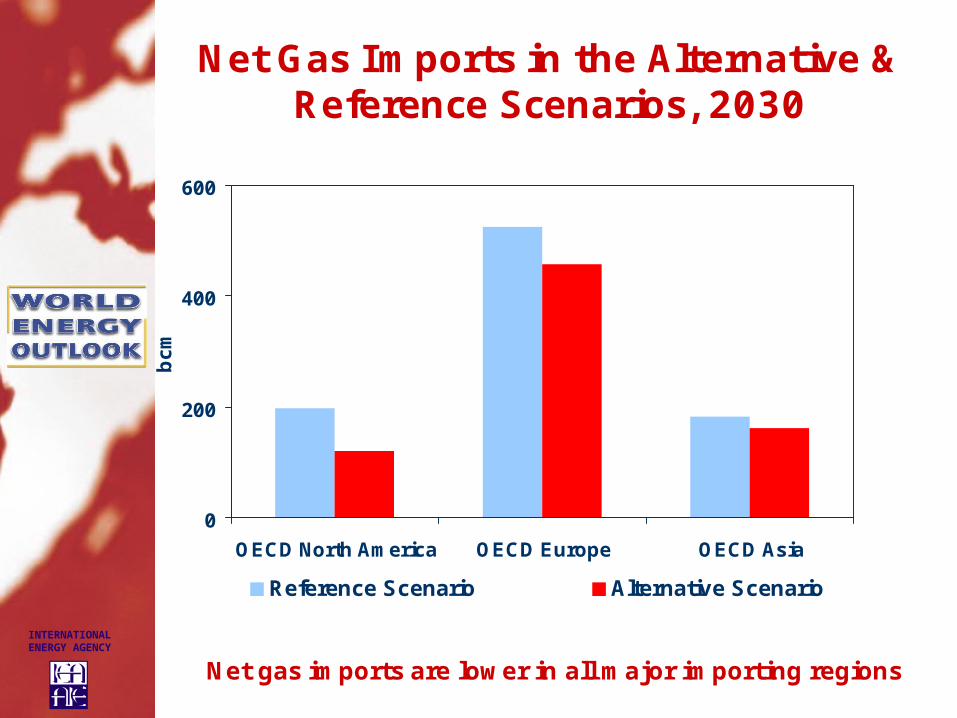

Net Gas Imports in the Alternative & Reference Scenarios, 2030

Net gas imports are lower in all major importing regions

0

200

400

600

OECD North America OECD Europe OECD Asia

bc

m

Reference Scenario Alternative Scenario

INTERNATIONALENERGY AGENCY

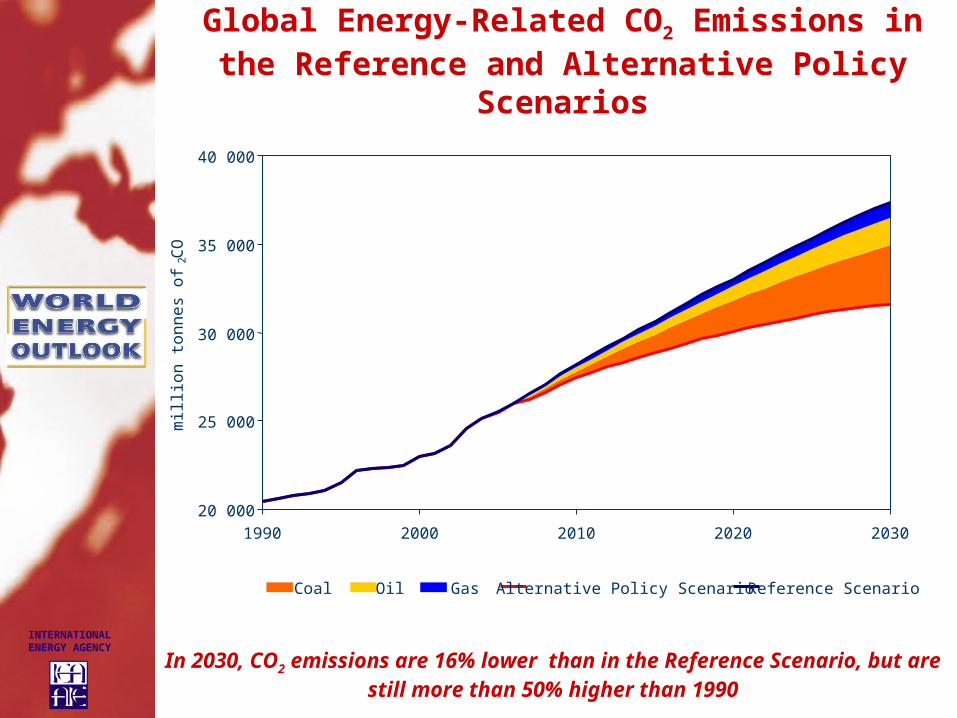

Global Energy-Related CO2 Emissions in the Reference and Alternative Policy

Scenarios

20 000

25 000

30 000

35 000

40 000

1990 2000 2010 2020 2030

mill

ion

to

nn

es

of

CO

2

Coal Oil Gas Alternative Policy Scenario Reference Scenario

In 2030, CO2 emissions are 16% lower than in the Reference Scenario, but are still more than 50% higher than 1990

INTERNATIONALENERGY AGENCY

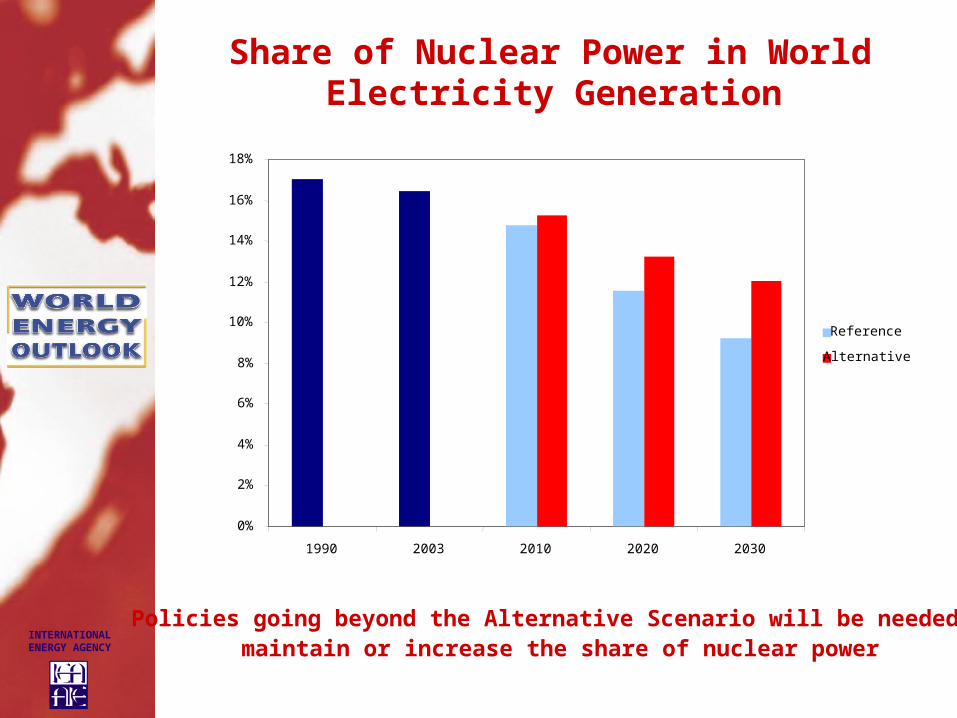

Share of Nuclear Power in World Electricity Generation

Policies going beyond the Alternative Scenario will be needed tomaintain or increase the share of nuclear power

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1990 2003 2010 2020 2030

Reference

Alternative

INTERNATIONALENERGY AGENCY

Summary & Conclusions

Projected market trends raise serious concerns Increased risk for energy security Rising environmental concerns

More vigorous policies would curb rate of increase in energy demand and emission significantly

Nuclear power can largely contribute toward meeting these challenges

Urgent and decisive government action needed

INTERNATIONALENERGY AGENCY

WEO 2006: Preliminary plan

World Alternative Policy Scenario a “tool for change” Deepening and broadening the analysis

Impact of high energy prices Impact of high oil, gas and electricity prices on

energy demand and macro economy Focus on developing Asia

Energy Investment Prospects Requirements vs. projects and plans

Role for Nuclear Availability of uranium and costs Nuclear investments in competitive markets