interest rates under till: after eight years, · pdf fileinterest rates under till: after...

TRANSCRIPT

INTEREST RATES UNDER TILL:

AFTER EIGHT YEARS, WHAT DOES TILL TELL US?

Reginald W. Jackson, Esq.* Vorys, Sater, Seymour and Pease LLP

52 E. Gay Street Columbus, OH 43215

The author acknowledges that the charts included with these materials are updated from materials originally prepared by Weil, Gotshal and Manges.

The Supreme Court’s Decision in Till v. SCS Credit Corp., 541 U.S. 465 (2004)

Till v. SCS Credit Corp. addressed the appropriate means to adduce the “cram-down” rate of interest to be applied in Chapter 13 plans. The “cram-down” provisions, both in Chapter 13 and Chapter 11 cases, allow a bankruptcy court to approve a plan over a secured claim-holder’s objection, but only if the creditor will receive the present value of its secured claim as of the effective date of the plan.

The Supreme Court granted certiorari in Till to resolve a four-way circuit split with regard to formulating this rate. Before Till, lower courts would use either: (1) The “coerced” loan method, which “focused on the interest rate that the creditor in question would obtain in making a new loan in the same industry to the debtor who is similarly situated, although not in bankruptcy”; (2) The “cost of funds method,” which charges “an interest rate equal to the creditor’s borrowing rate”; (3) the “formula” method, which adds a risk premium depending on the circumstances of the debtor to a “risk-free” base rate; or (4) the “presumptive contract approach,” which embraces the parties’ contractual rate with downward or upward adjustments as needed depending on evidence of risk.

In Till, the debtors had purchased a used truck subject to SCS’s purchase money security interest. The Chapter 13 plan provided that the Tills would pay interest on the $4,000 allowed secured claim at a rate of 9.5%, which was 1.5% above the national prime rate. SCS objected to the plan, arguing that the Tills would have to pay the contract rate of 21% in order to compensate them adequately under the Code. The Court upheld the 9.5% rate, but was divided as to the method that bankruptcy courts should use—

Stevens’s Plurality (Four Justices) applied the “formula approach,” using the national prime rate as a base. Because “bankruptcy debtors typically pose a greater risk of nonpayment than solvent commercial borrowers,” the plurality reasoned that courts must adjust the prime rate to the “prime-plus” rate, based on “the circumstances of the estate, the nature of the security, and the duration and feasibility of the reorganization plan.” The plurality praised the formula approach for its ease of use and responsiveness to changes in market conditions. It explained that the approach “obligates the court to compensate the creditor for its risk but not so much as to doom the plan. If the court determines that the likelihood of default is so high as to necessitate an eye-popping interest rate, the plan probably should not be confirmed.” The plurality added that, as an empirical matter, most risk adjustments will fall between one and three percent. Till, 541 U.S. at 480 (citing In re Valenti, 105 F.3d 55, 64 (2d Cir. 1997)). However, the creditor, who arguably has more access to relevant information, must ultimately prove risk of non-payment.

Thomas’s Concurrence agreed that a 9.5% rate would adequately compensate SCS, but disagreed with the Plurality’s use of an adjustment for risk. Thomas focused solely on the time-value of money. He would have upheld a “risk-free” rate.

Scalia’s Dissent (Four Justices) agreed that the appropriate cram-down rate must include a risk premium, but would have adopted the “presumptive contract approach,” with upward and downward adjustments based on the level of risk. Scalia identified additional factors that should inform a risk-premium adjustment: “(1) the probability of plan failure; (2) the rate of collateral depreciation; (3) the liquidity of the collateral market; and (4) the administrative expenses of enforcement.” Scalia noted that the contract rate had the advantage of already having incorporated such factors.

- 2 -

Chapter 13 Cases after Till: The Plurality’s “Formula Approach” Prevails, With Some Lingering Questions

1. What is the Precedential Value of Till in the Chapter 13 Context? Lower courts now follow the “formula approach” of Till’s Plurality with near uniformity in Chapter 13 cases. (See Ch. 13 Chart attached). In the last two years, every lower court to consider the appropriate cram-down interest rate in a Chapter 13 case has applied the formula approach, beginning with the national prime as a base and adjusting for risk. This is the case even for “910 vehicles” post-BAPCPA, although there was some initial uncertainty as to whether the “hanging paragraph affected interest rate modification as well as the bifurcation of claims. See Drive Fin. Servs., L.P. v. Jordan, 521 F.3d 343 (5th Cir. 2008) (holding that BAPCPA did not supersede Till, applying the formula method to creditor’s fully secured claim, arriving at a 7.5% interest rate); In re Jones, 530 F.3d 1284 (10th Cir. 2008) (same, but remanding to the bankruptcy court to determine the proper rate under Till for the creditor’s fully secured claim).

However, there is still some disagreement as to the precedential value of Till.

One line of authority has concluded that the Till decision results in “no binding precedent” because the plurality and the concurrence shared no common doctrinal ground, and agreed only on the result. See In re Cook, 322 B.R. 336, 343 (Bankr. N.D. Ohio 2005) (prime-plus is “confirmable,” but not binding); see also Marks v. United States, 430 U.S. 188 (for plurality opinions, lower courts can consider binding the narrowest doctrinal grounds on which the plurality and concurrence agree). Even so, In re Cook is the only known lower court decision to explicitly reject Till and apply a different test. 322 B.R. at 343 (applying coerced loan theory, which was the law of the Sixth Circuit prior to Till). Cf. In re Dimery, No. 11-60142, 2011 Bankr. LEXIS 2433 (Bankr. N.D. Ohio June 20, 2011) (applying the Till formula approach; noting that in In re Am. Homepatient, Inc., the Sixth Circuit explained in dicta that the formula method applies to Chapter 13 cases). Most lower courts have found the analysis in the Till plurality instructive, even if not binding.

Another line of authority has found Till to be more than instructive. Many lower courts treat Till as binding authority for Chapter 13 cases. See Drive Fin. Servs., L.P., 521 F.3d at 350 (“Since we are presented with facts indistinguishable from Till, we need not attempt to divine a narrowest grounds under Marks.”). District courts may overturn or remand a case where the bankruptcy court failed to apply the Till plurality’s prime-plus risk approach. In re Smith, 310 B.R. 631, 634 (D. Kan. 2004). Some courts have engaged in “vote counting” to arrive at the conclusion that Till “overruled” the former law of the circuit, even if it was only a plurality opinion. In re Princeton Office Park, LP, 423 B.R. 795, 807 (Bankr. D.N.J. 2010). In Princeton Office Park for example, the bankruptcy court held that the law of the Third Circuit, which had formerly embraced a coerced loan theory, was no longer applicable after Till—all nine of the justices rejected “coerced loan theory” and the “cost of funds approach,” and five justices rejected the “presumptive contract approach.” Eight of the justices agreed, however, that a cram-down interest rate must incorporate a premium for risk. Id.; see also Thomas J. Yerbich, “How Do You Count the Votes—or Did Till Tilt the Game?” 23 Am. Bankr. Inst. J. 10 (2004).

2. How Are Lower Courts Fashioning the “Prime-Plus” Rate?

In Chapter 13 cases, most lower courts have settled at a rate of 2% above the national prime at the time of plan confirmation. This percentage is in the middle of the 1% to 3% range that the Till plurality observed should be the average range of risk adjustment, with 1% representing an adjustment for a relatively low-

- 3 -

risk bankruptcy debtor, and 3% representing a higher level of risk. Most lower courts will consider a broad range of factors to determine the level of risk, including the pre-petition arrearage, the debtor’s history of making payments, the debtor’s income and occupation, the likelihood of depreciation in value, and the amount of equity that the creditor has in the collateral, if any. Some courts have also considered the administrative costs to the creditor in maintaining and enforcing the loan, and, even the parties’ contract rate.

Many lower courts have explicitly considered the Till plurality’s suggested range of risk adjustments in crafting a risk adjustment for a specific debtor. For example, in In re Johnson, 438 B.R. 854 (Bankr. D.S.C.), the bankruptcy court approved the 2% interest rate suggested by the debtors because it fell within the middle of the range suggested in Till. Bankruptcy courts in the Northern District of Ohio seem to have settled on a 2% adjustment for automobiles as standard practice, noting that the plurality in Till specifically selected the formula approach to avoid excessive evidentiary inquiry.

Courts will find that an adjustment factor lower than 1% applies where the contract rate is lower than the national prime rate, and the parties agree that the circumstances present minimal risk.

o Few bankruptcy courts have approved a prime rate adjustment of less than 2%—possibly because 2% tends to be the rate chosen by the debtor, and also because the rate is often uncontested. Two Eleventh Circuit courts have approved a prime rate with no upward adjustment. See In re Davis, No. 07-50761, 2007 Bankr. LEXIS 3175 (Bankr. M.D. Ga. Sept. 12, 2007); In re Yelverton, No. 06-10664, 2007 Bankr. LEXIS 1804 (Bankr. M.D. Ala. May 21, 2007). In each of these cases, however, the contract rate was lower than the current national prime rate of 8.25%. Holding that the formula approach applied even where the contract rate would be lower, the courts approved a rate equal to the national prime where the parties’ agreed that the risk of nonpayment was low.

Where circumstances indicate a high level of risk, it may be appropriate to adjust the prime rate by more than 3%.

o Although few lower courts have approved a rate adjustment above 3%, at least one district court has recently explained that the Till opinion does not require a rate adjustment within the “suggested” range. See In re Horny, No. 11-12508-BC, 2011 U.S. Dist LEXIS 146374 (E.D. Mich. Dec. 21, 2011). In In re Horny, the court approved an adjustment of 11.2%, for a total modified rate of 15.2%, where circumstances indicated significant risk of nonpayment. In that case, the debtor had purchased the vehicle only a few days before filing for bankruptcy protection, reporting a higher income on the credit application than on the bankruptcy schedules. The court held that, under these circumstances, the contract rate of 23.99% was relevant, because it incorporated the level of risk perceived at the time of purchase. The court reiterated that Till ultimately provided qualitative standards for determining the proper amount of adjustment that the bankruptcy court should make—i.e., the rate must be high enough to compensate the debtor, but not so high as to be “eye popping” or “doom the plan.”

3. When Does the Prime-Plus Rate Take Effect?

The prime-plus rate will take effect on the date of plan confirmation. First United Sec. Bank v. Garner (In re Garner), 663 F.3d 1218, 2011 U.S. App. LEXIS 23811 at *5-6 (11th Cir. 2011) (“The Ninth and Second Circuits have read Sections 506(b) and 1325 together to mean that interest accrues under 506(b) only until confirmation of the plan even though that section lacks an explicit temporal limitation.”). From the time of filing until the time of confirmation, the contract rate between the parties governs. Id. Courts will often apply the national prime rate at the time of hearing or confirmation when formulating a “prime-

- 4 -

plus” rate. See, e.g., In re Goggins, No. 05-42962, 2008 Bankr. LEXIS 1391 (Bankr. N.D. Ga. Mar. 20, 2008) (using a prime rate of 2%, even though the prime rate at the time of filing was 1.5%). Chapter 11 Cases after Till: The Lower Courts “Take a Cue” from Footnote 14, Applying a Two-Tiered Test

Although the Supreme Court was explicit in setting standards for approving an interest rate for a Chapter 13 plan, it left “seemingly contradictory” signals about the appropriate standard to use in a Chapter 11 case. See Gary W. Marsh & Matthew M. Weiss, Chapter 11 Interest Rates after Till, 84 AM. BANKR. L.J. 209, 212 (2010).

First, the plurality praised the formula approach, observing that it “entails a straightforward, familiar, and objective inquiry, and minimizes the need for potentially costly evidentiary hearings.” The plurality then suggested that the approach might apply to the entire Bankruptcy Code, referring to the Code’s “numerous provisions,” and commenting that “Congress intended bankruptcy judges to follow essentially the same approach when choosing an appropriate interest rate under any of these provisions.” Till, 541 U.S. at 474.

In footnote 14, however, the plurality distinguished Chapter 13 cases from Chapter 11 cases, noting that a market for exit financing often exists for Chapter 11 debtors, and “when picking a cram-down rate in a Chapter 11 case, it might make sense to ask what rate an efficient market would produce.” Id. at 476 n.14. Lower courts have observed additional distinctions between Chapter 13 and Chapter 11 cases that might limit the applicability of Till, including the type of collateral, loan term, type of debtor, and extent of court involvement. See In re Walkabout Creek Ltd., No. 09-00632, 2011 Bankr. LEXIS 4397 (Bankr. D.C. Nov. 14, 2011) (providing an overview of the relevant differences between Ch. 11 and Ch. 13 cases).

Under this rubric, the vast majority of lower courts apply the “two-tiered” approach in Chapter 11 cases to adduce cram-down interest rates, which was originally announced in In re American Homepatient, Inc., 420 F.3d 559 (6th Cir. 2005). Marsh & Weiss at 212. This approach requires the court to first determine whether there is an efficient market for the loan. If there is an efficient market, then the court will apply the market rate. If not, the Till formula approach applies. Other courts have modified the application of the formula method under the two-tiered approach to better account for long-term loans without the court oversight typically present in Chapter 13 cases. A minority of courts advocate a case-by-case or “market formula” approach, which considers the market rate under a more comprehensive coerced loan theory.

1. How Are Lower Courts Applying the Two-Tiered Test?

Since 2005, the “two-tiered” test has been the majority approach to Chapter 11 cram-down interest rates. See In re Prussia Assocs., 322 B.R. 572 (Bankr. E.D.Pa. 2005) (defaulting to the formula approach after finding an insufficient evidentiary basis about the availability of market financing). This approach attempts to reconcile the Till plurality with footnote 14 by first looking to whether an efficient market exists before applying the Till formula approach.

a. Tier One: Is There a Determinable Rate under an Efficient Market?

Under the two-tiered test, the burden is on the creditor to show the existence of an efficient market. In re VDG Chicken, LLC., No. NV-10-1278-HKiD, 2011 Bankr. LEXIS 1795 (BAP 9th Cir. April 11, 2011). Showing that an efficient market exists typically requires credible expert testimony showing that “traditional” lenders would be willing to provide post-petition financing to the debtor, considering the terms of the restructured debt, the type of collateral, the duration of the loan, and the amount of the loan. In re Brice Road Devs., LLC, 392 B.R. 274, 280-81 (BAP 6th Cir. 2008). In Brice Road, for example, the Bankruptcy Appellate Panel for the Sixth Circuit upheld the bankruptcy court’s determination that an

- 5 -

efficient market existed where the original lender to the debtor testified as to the loans similar to that which the debtor sought to confirm as part of its plan. Id. at 281 (finding that the efficient market rate was 6%).

In addition to the credibility of the parties’ expert testimony, lower courts will consider the following factors to determine whether an efficient market exists:

o The Status of the Market: The certainty and liquidity of the relevant market is one of the most important factors in determining whether an efficient market exists.

In Prussia Associates, the court accepted expert testimony of a strong “seller’s market,” supporting the existence of an efficient market for exit financing. In re Prussia Assocs., 322 B.R. 572, 589 (Bankr. E.D. Pa. 2005).

However, most courts in the past year have referenced the uncertain status of the real estate market in determining that no efficient market exists. In 2011, 12 bankruptcy courts purported to apply the “two-tiered” test, but only one found that an efficient market existed (In re Mace, 2011 Bankr. M.D. Tenn. Jan. 25, 2011)). Many of these are single-asset cases involving residential or commercial real property such as condominiums, apartment complexes, office space, retail shopping centers, or hotels. See In re Greenwood point, LP., 445 B.R. 885, 918-19 (Bankr. S.D. Ind. 2011) (noting that, “in today’s economic climate, lenders are not lending to borrowers like the Debtor due to its bankruptcy status and level of vacancies”). In some cases, the court has merely stated that there is “no efficient market” because of economic uncertainty, without exploring other factors in detail. In re DLH Master Land Holding, LLC, No. 10-30561-HDH-11, 2011 Bankr. LEXIS 4509 (Bankr. N.D. Tex. Nov. 23, 2011).

o The Risk Associated With the Loan: For creditors, the two-tiered test can act as a double-edged sword. The same evidence that a creditor will want to use to show that there is a high risk of non-payment under the formula approach will also undermine an argument in favor of an efficient market, as lenders are not generally willing to take extremely high risks.

In In re Smithville Crossing, LLC, for example, the court found that the creditor’s expert testimony regarding the uncertainty of the market and the risks associated with the loan was sound, but that the testimony itself was proof that no efficient market existed. No. 11-02573-8-JRL, 2011 Bankr. LEXIS 4605 (Bankr. E.D.N.C. Sept. 28, 2011).

Factors that add to the level of risk include the amount of the loan, the length of maturity, the debt-to-value ratio, the debtor’s creditworthiness, and whether there are negative market forecasts. See, e.g., In re 20 Bayard Views, LLC, 445 B.R. 83 (Bankr. E.D.N.Y. 2011) (finding that there was no efficient market for a 5 year, $20.5 million dollar loan with a 100% debt-to-value ratio in an unfavorable market); In re Inds. W. Commerce Cty., LLC, No. NC-10-JuHBa, 2011 Bankr. LEXIS 2090 (BAP 9th Cir. May 24, 2011) (citing the uncertain market both as the reason why there was no efficient market, and also as the primary risk adjustment factor).

o The Types of Loans That Would Be Available to the Debtor on the Market: Where only certain predatory or “eye-popping” interest rates would be available to the debtor on the market, courts have found that an efficient market does not exist. See Mercury Capital Corp. v. Millford Connecticut Assocs., 354 B.R. 1 (D. Conn. 2006) (finding that insufficient evidence of an efficient market existed, considering the testimony of the debtor’s president, indicating that the debtor would not be able to obtain a loan with less than 12.5% interest).

- 6 -

Likewise, showing that a debtor could obtain financing by mechanisms not actually being proposed in the bankruptcy case is not sufficient evidence of an efficient market.

Hard Money Loans: In In re American Trailer & Storage, Inc., 419 B.R. 412 (Bankr. W.D. Mo 2009), the creditor’s expert witness testified that, because of the negative market and the debtor’s financial position, a 5-year term, 10-year amortization loan could only be obtained through a “hard money lender,” charging a 10 to 18% interest rate, clearly expecting a default and foreclosure. The court criticized this evidence and moved to a Till analysis, explaining that such loans were not “appropriate options for debtors in bankruptcy.”

Blended Rate Loans: Several courts have also rejected evidence that a debtor would be able to procure a loan through tiered financing, including a blend of senior debt, mezzanine debt, and equity. See, e.g., In re Am. Homepatient, Inc., 420 F.3d at 568 (rejecting a 12.6% blended rate as a “purely hypothetical” new loan, where the debt was entirely senior); In re Red Mtn. Mach. Co., 448 B.R. 1 (Bankr. D. Ariz. 2011) (finding that no efficient market existed where the creditor relied on a blended rate). Cf. In re N. Valley Mall, LLC, 432 B.R. 825 (C.D. Cal. 2010) (applying an adjusted blended rate with three tranches under a market formula approach).

o Whether the Debtor Has Received Financing Offers from Willing Lenders: In determining whether an efficient market exists, it is not necessary to show an unsuccessful attempt at obtaining exit financing. SPCP Group, LLC v. Cypress Creek Assisted Living Residence, Inc., 434 B.R. 650 (M.D. Fla. 2010). However, where the debtor does have actual loan offers, this can be good evidence that an efficient market exists. In re Prussia Assocs., 322 B.R. at 590 (noting that an actual loan offer is “proof of the pudding” that an efficient market exists); see also In re Winn-Dixie Stores, Inc., 356 B.R. 239 (M.D. Fla. 2006) (finding that an efficient market existed where the debtor had 14 proposals among competing lending institutions for post-petition financing).

Courts are divided as to whether interest rates from loans to other debtors is good evidence that an efficient market exists. In In re Northwest Timberline Enterprises, the court rejected such evidence, explaining that “what two lenders allegedly agreed to in two other bankruptcy cases is not very persuasive.” 348 B.R. 412, 426 (Bankr. N.D. Tex. 2006). However, in In re Mace, another bankruptcy court was persuaded by the Trustee’s evidence that he had obtained the proposed terms for four other similarly situated debtors within the confirmation process. 2011 Bankr. LEXIS 280 (Bankr. M.D. Tenn. Jan. 25, 2011).

Formulating the Market Rate under Tier One:

o In formulating the market rate, courts will consider the figures and comparisons presented in expert testimony along with standard “commercial indicators” and the parties’ contract rate. Marsh & Weiss at 224-25; see also In re Am. Homepatient, Inc., 420 F.3d 559 (6th Cir. 2005) (using the 6-year treasury rate plus a basis for risk to determine that a market rate of 6.785% was appropriate for a 6 year loan secured by a health care company’s assets, valued at $250 million); In re Winn-Dixie Stores, Inc., 356 B.R. 239 (M.D. Fla. 2006) (using LIBOR and competing offers to determine the market rate). The pre-petition contract rate, by itself, is insufficient evidence to show that an efficient market exists. Mercury Capital Corp. v. Millford Connecticut Assocs., 354 B.R. 1 (D. Conn. 2006). However, courts have noted that the contract rate can be “informative” as to the proposed cram-down rate, especially where the market conditions are “substantially similar.” In re SW Boston Hotel Venture, LLC, No. 10-14535-JNF at *15.

- 7 -

b. Tier Two: Applying the Till Formula Approach

Under Tier Two, if no efficient market exists or the market rate is not determinable, then courts will apply the formula approach announced in Till. Some courts seem to apply the formula approach directly even in the Chapter 11 context, either because the parties did not present evidence of an efficient market, or because the court has determined that it is the only applicable test. (See Chapter 11 Case Chart). These cases are also analyzed herein.

Determining the Appropriate Base Rate in a Chapter 11 Context.

The formula method begins with using a “risk-free” base rate, and then adjusting the rate with a “risk premium” based on the circumstances of the case. Many courts will start with the national prime rate, as used and suggested in Till. The national prime rate, listed in the Wall Street Journal, “reflects the financial market's estimate of the amount a commercial bank should charge a creditworthy commercial borrower to compensate for the opportunity costs of the loan, the risk of inflation, and the relatively slight risk of default.” Till, 541 U.S. at 479. Courts using the prime rate have usually done so without discussion. However, other courts have noted that the prime rate tends to be more suitable for “short-term loans.” In re Walkabout Creek, Ltd., No. 09-00632, 2011 Bankr. LEXIS 4397 at *15-16 (explaining that the loan in Till had a 3-year term and that a Chapter 13 plan cannot provide for payments of a duration longer than 5 years).

o Applicable U.S. Treasury Bill Rate: Other courts have used the applicable U.S. Treasury Bill Rate, which is not used in Chapter 13 cases. In Walkabout Creek Limited, the Bankruptcy Court for the District of Columbia explained that the 30-year treasury yield was more appropriate where the debtors planed to re-amortize the loan over a period of 35 years, which is much longer than loans in the context of Chapter 13. No. 09-00632, 2011 Bankr. LEXIS 4397 at *15-16; see also In re VDG Chicken, LLC, No. NV—10-1278-HKiD, 2011 Bankr. LEXIS 1795 (BAP 9th Cir. April 11, 2011) (using the 10-year treasury yield for a 10-year loan). Cf. SPCP Group, LLC v. Cypress Creek Assisted Living Residence, Inc., 434 B.R. 650 (M.D. Fla. 2010) (approving a rate of 2% over prime for a loan of over $5.5 million, amortized over 20 years with a 6-year balloon feature, where the creditors were under-secured, but the debtors had ample cash flow ant a demonstrated ability to make timely payments).

o LIBOR: Other courts have used LIBOR as a base where testimony indicated that it was the prevailing rate for debt instruments. In re G-I Holdings, Inc., No. 09-CV-05031, 2009 U.S. Dist. LEXIS 108339 (D.N.J. Nov. 12, 2009).

Determining the Appropriate Risk Premium in Chapter 11 Cases

o As with Chapter 13 cases, lower courts tend to stay within 1 to 3% range for a risk premium adjustment to the base rate. However, although one court has mentioned the “suggested range” in Till as a factor for determining the appropriate risk adjustment, In re Lilo Props., LLC, No. 10-11303, 2011 Bankr. LEXIS 4407 (Bankr. D. Vt. Nov. 4, 2011), courts in the Chapter 11 context seem to be less focused on this range. There is more variety in rates both within the range and outside of it depending on the market, the nature of the collateral, the payment history of the debtor, the likelihood that the plan will succeed, the debt-to-value ratio, and the existence of a solvent guarantor. (See Chapter 11 Chart, comparing “Risk Factor Considerations” and “Rate Outcome”); see also In re Red Mtn Mach. Co., 448 B.R. 1 (Bankr. D. Ariz. 2011) (finding that positive risk factors included guaranty by a solvent guarantor, positive cash flow and projections, and significant amortization over 15 years;

- 8 -

negative factors included a 15-year term and a poor real estate market; approving a rate of 3.25% over prime).

For example, one court recently approved an adjustment of 1% over prime where it was a short-term loan, first in priority, and the creditor had $14 million in assets available to secure the loan. In re SW Boston Hotel Venture, LLC, No. 10-14535-JNF, 2011 Bankr. LEXIS 4384 (Bankr. D. Mass. Nov. 14, 2011).

By contrast, another court explained that an adjustment of “at least” 3-5% would be necessary, where there was a strong negative market forecast and a high debt-to-value ratio in a single-asset case. In re Smithville Crossing, LLC, No. 11-02573-8-JRL, 2011 Bankr. LEXIS 4605, at *24 (Bankr. E.D.N.C. Sept. 28, 2011).

o For both retail space and residential real estate, one of the primary factors that a court will consider is the amount of current vacancies and the feasibility of the debtor’s plan to generate new tenants and retain them. See, e.g., In re Riverbend Leasing LLC, 458 B.R. 520 (Bankr. S.D. Iowa 2011); In re 20 Bayard Views, LLC, 445 B.R. 83 (Bankr. E.D.N.Y. 2011) (finding that 1.5% over prime would not be appropriate for bulk, unsold condominium units in an unfavorable market; declining to adduce an appropriate rate).

o In the Chapter 11 context, courts have also noted that the costs associated with monitoring large, long-term loans is “not insignificant,” as compared with the typical Chapter 13 loan. See In re Walkabout Ltd., No. 09-00632, 2011 Bankr. LEXIS 4397 at *22 (“In this case, however, the debtors’ future income will not be paid (as it occurs in a chapter 13 case) to a trustee as necessary for execution of the plans.”).

2. Other Approaches, Post-Till, to Determining the Appropriate Interest Rate in the Chapter 11 Context

Although the Sixth Circuit’s “two tiered” approach is the majority test by far, some courts have fashioned different tests to adduce the appropriate cram-down interest rate in the Chapter 11 context. For example, one district court has upheld the use of the presumptive contract approach, and two bankruptcy courts have used a “market formula” approach, similar to the coerced loan theory. Other courts will apply the formula approach of Till, either directly or in conjunction with a number of other tests, considering “explicit findings” required under the pre-Till law of the circuit. See, e.g., In re Seasons Partners, LLC, 439 B.R. 505 (Bankr. D. Ariz. 2010).

a. The Presumptive Contract Approach

In Good v. RMR Investments, Inc., 428 B.R. 249 (E.D. Tex. Mar. 31, 2010), the district court upheld the bankruptcy court’s decision to apply the presumptive contract approach, over the objection of the debtor who argued that the Till formula approach should apply. Noting that Till is a plurality opinion, with limited precedential value in the context of Chapter 11 cases, the court listed the various methods of adducing cram-down interest rates and noted that the Fifth Circuit has “repeatedly declined” to require the application of a specific method. Id. at 254. In that case, the evidence at hearing showed that the debtor was solvent, the creditor was over-secured, and applying the contract rate of 15% would not harm distribution to other secured and unsecured creditors. Id. The court rejected a prime-plus rate of 5.25% for a loan secured by acres of unimproved land and mineral rights.

This opinion implies that, at least in the Fifth Circuit, the formula and two-tiered methods would be acceptable as well. See In re DLH Master Land Holding, LLC, No. 10-HDH-11, 2011 Bankr. LEXIS 4509 (Bankr. N.D. Tex. Nov. 23, 2011) (applying the two-tiered approach).

- 9 -

b. The Market Formula Approach

A few courts have applied a “market formula” approach, which is similar to coerced loan theory. This standard recognizes that there may be no actual market to provide financing for a particular debtor, but attempts to create a “proxy” for the market based on expert testimony and a discernable formula considering the nature of the collateral, the type of loan, and the risks associated with lending to the debtor.

In In re North Valley Mall, LLC, 432 B.R. 825 (Bankr. C.D. Cal. 2010), for example, the District Court for the Central District of California applied a “blended rate” after noting that the Till plurality opinion is but one attempt to find a “proxy” for a market where none exists. Id. at 831. The court found Till to be inapplicable, however, because the prime base rate is not appropriate for long-term loans, and because of the “world of difference” between the Tills’ truck, and the shopping center in North Valley valued at $30 million dollars. Id. Considering expert testimony, the court settled on a blended rate with a senior tranche, a mezzanine tranche, and an equity tranche. Id. at 833; see also In re SJT Ventures, LLC, 441 B.R. 248, 255 (Bankr. N.D. Tex. 2010) (following a similar approach and considering the 85% debt-to-value ratio as the most important factor).

AP

PE

ND

IX A

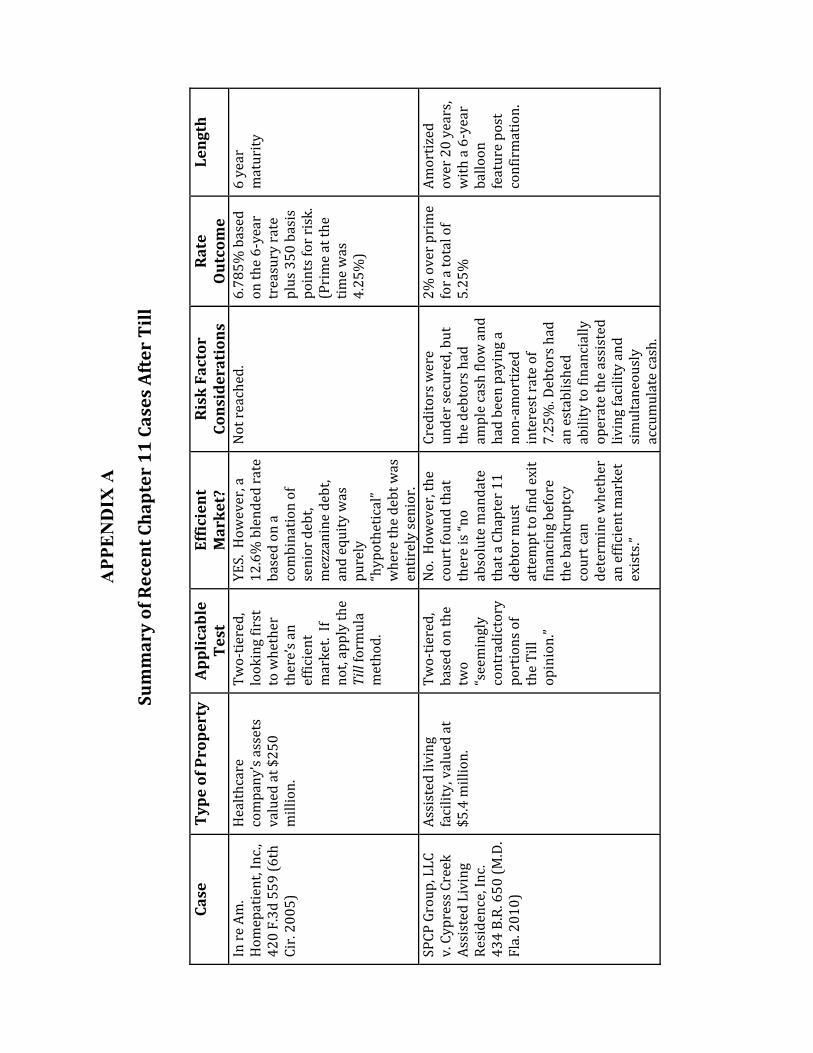

Summary of Recent Chapter 11 Cases After Till

Case

Type of Property

Applicable

Test

Efficient

Market?

Risk Factor

Considerations

Rate

Outcom

e Length

In re Am.

Hom

epatient, Inc.,

420 F.3d 559 (6th

Cir. 2005)

Healthcare

company’s assets

valued at $250

million.

Two‐tiered,

looking first

to whether

there’s an

efficient

market. If

not, apply the

Till formula

method.

YES. How

ever, a

12.6% blended rate

based on a

combination of

senior debt,

mezzanine debt,

and equity was

purely

“hypothetical”

where the debt was

entirely senior.

Not reached.

6.785%

based

on the 6‐year

treasury rate

plus 350 basis

points for risk.

(Prime at the

time was

4.25%)

6 year

maturity

SPCP Group, LLC

v. Cypress Creek

Assisted Living

Residence, Inc.

434 B.R. 650 (M

.D.

Fla. 2010)

Assisted living

facility, valued at

$5.4 million.

Two‐tiered,

based on the

two

“seemingly

contradictory

portions of

the Till

opinion.”

No. How

ever, the

court found that

there is “no

absolute mandate

that a Chapter 11

debtor must

attempt to find exit

financing before

the bankruptcy

court can

determ

ine whether

an efficient m

arket

exists.”

Creditors were

under secured, but

the debtors had

ample cash flow

and

had been paying a

non‐am

ortized

interest rate of

7.25%. Debtors had

an established

ability to financially

operate the assisted

living facility and

simultaneously

accumulate cash.

2% over prime

for a total of

5.25%

Amortized

over 20 years,

with a 6‐year

balloon

feature post

confirmation.

2

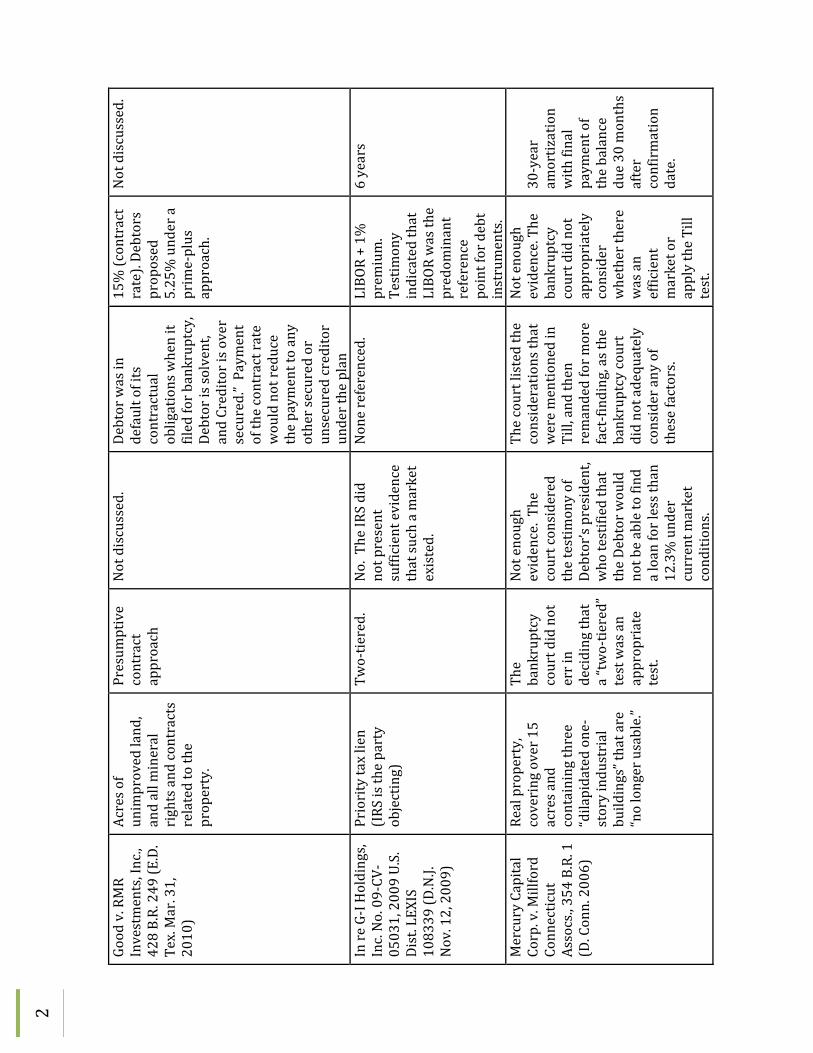

Good v. RMR

Investments, Inc.,

428 B.R. 249 (E.D.

Tex. Mar. 31,

2010)

Acres of

unimproved land,

and all m

ineral

rights and contracts

related to the

property.

Presum

ptive

contract

approach

Not discussed.

Debtor was in

default of its

contractual

obligations when it

filed for bankruptcy,

Debtor is solvent,

and Creditor is over

secured.” Paym

ent

of the contract rate

would not reduce

the paym

ent to any

other secured or

unsecured creditor

under the plan

15% (contract

rate). Debtors

proposed

5.25% under a

prime‐plus

approach.

Not discussed.

In re G‐I Holdings,

Inc. No. 09‐CV‐

05031, 2009 U.S.

Dist. LEXIS

108339 (D

.N.J.

Nov. 12, 2009)

Priority tax lien

(IRS is the party

objecting)

Two‐tiered.

No. The IRS did

not present

sufficient evidence

that such a market

existed.

None referenced.

LIBO

R + 1%

prem

ium.

Testimony

indicated that

LIBO

R was the

predom

inant

reference

point for debt

instruments.

6 years

Mercury Capital

Corp. v. Millford

Connecticut

Assocs., 354 B.R. 1

(D. Conn. 2006)

Real property,

covering over 15

acres and

containing three

“dilapidated one‐

story industrial

buildings” that are

“no longer usable.”

The

bankruptcy

court did not

err in

deciding that

a “two‐tiered”

test was an

appropriate

test.

Not enough

evidence. The

court considered

the testimony of

Debtor’s president,

who testified that

the Debtor would

not be able to find

a loan for less than

12.3% under

current m

arket

conditions.

The court listed the

considerations that

were mentioned in

Till, and then

remanded for m

ore

fact‐finding, as the

bankruptcy court

did not adequately

consider any of

these factors.

Not enough

evidence. The

bankruptcy

court did not

appropriately

consider

whether there

was an

efficient

market or

apply the Till

test.

30‐year

amortization

with final

paym

ent of

the balance

due 30 months

after

confirmation

date.

3

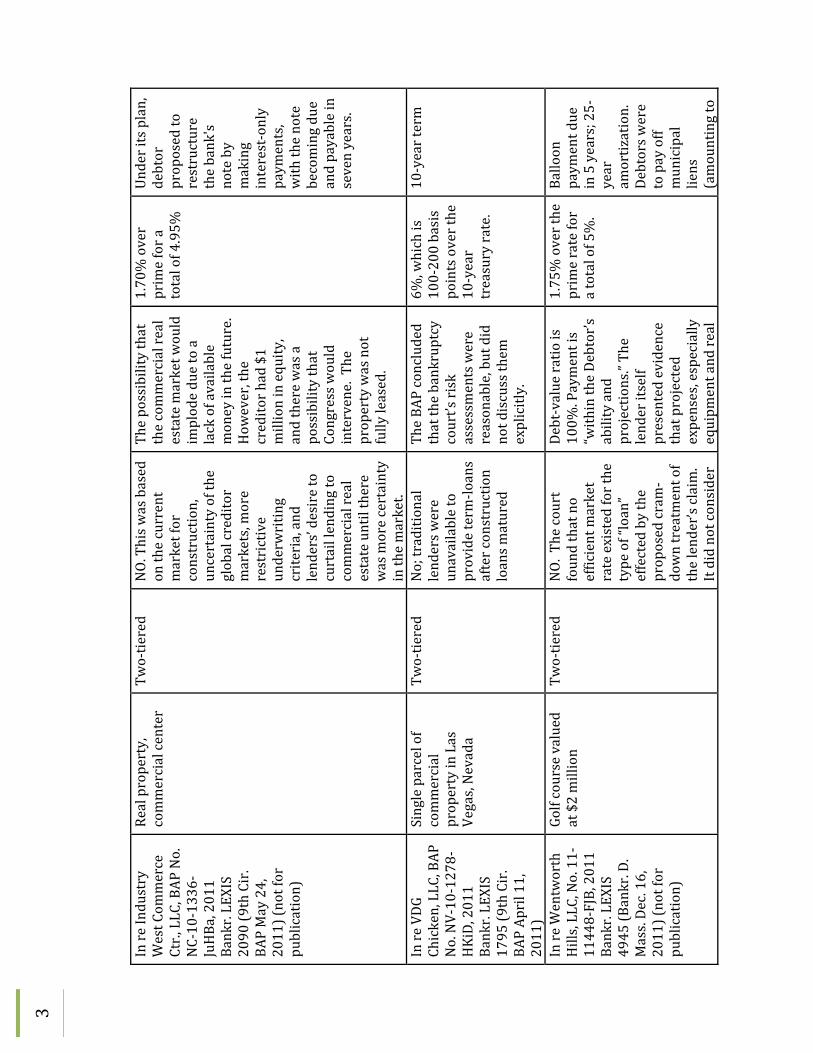

In re Industry

West Com

merce

Ctr., LLC, BAP No.

NC‐10‐1336‐

JuHBa, 2011

Bankr. LEXIS

2090 (9th Cir.

BAP May 24,

2011) (not for

publication)

Real property,

commercial center

Two‐tiered

NO. This w

as based

on the current

market for

construction,

uncertainty of the

global creditor

markets, m

ore

restrictive

underwriting

criteria, and

lenders’ desire to

curtail lending to

commercial real

estate until there

was more certainty

in the market.

The possibility that

the commercial real

estate market w

ould

implode due to a

lack of available

money in the future.

How

ever, the

creditor had $1

million in equity,

and there was a

possibility that

Congress would

intervene. The

property was not

fully leased.

1.70% over

prime for a

total of 4.95%

Under its plan,

debtor

proposed to

restructure

the bank's

note by

making

interest‐only

paym

ents,

with the note

becoming due

and payable in

seven years.

In re VDG

Chicken, LLC, BAP

No. NV‐10‐1278‐

HKiD, 2011

Bankr. LEXIS

1795 (9th Cir.

BAP April 11,

2011)

Single parcel of

commercial

property in Las

Vegas, Nevada

Two‐tiered

No; traditional

lenders w

ere

unavailable to

provide term

‐loans

after construction

loans m

atured

The BAP concluded

that the bankruptcy

court’s risk

assessments were

reasonable, but did

not discuss them

explicitly.

6%, which is

100‐200 basis

points over the

10‐year

treasury rate.

10‐year term

In re Wentworth

Hills, LLC, No. 11‐

11448‐FJB, 2011

Bankr. LEXIS

4945 (Bankr. D.

Mass. Dec. 16,

2011) (not for

publication)

Golf course valued

at $2 million

Two‐tiered

NO. The court

found that no

efficient market

rate existed for the

type of “loan”

effected by the

proposed cram

‐down treatment of

the lender’s claim.

It did not consider

Debt‐value ratio is

100%

. Payment is

“within the Debtor’s

ability and

projections.” The

lender itself

presented evidence

that projected

expenses, especially

equipm

ent and real

1.75% over the

prime rate for

a total of 5%.

Balloon

paym

ent due

in 5 years; 25‐

year

amortization.

Debtors w

ere

to pay off

municipal

liens

(amounting to

4

expert testimony

or other evidence.

estate tax

allocations, could be

significantly

reduced. Payment

on municipal liens

will im

prove

debtor’s position.

$47,000)

within 3 years.

In re DLH Master

Land Holding,

LLC, No. 10‐

30561‐HDH

‐11,

2011 Bankr.

LEXIS 4509

(Bankr. N.D. Tex.

Nov. 23, 2011)

real property

totaling

approximately

1,350 acres, valued

anyw

here from

$26.5 million to $86

million

Two‐tiered.

No. The court

merely stated that

there was no

efficient market.

The court noted that

the creditor w

as

over‐secured, but

did not discuss any

considerations at

length.

4% over prime

for a total of

7.25%

Due in full

after 5 years,

amortized

over 10

In re SW Boston

Hotel Venture,

LLC, No. 10‐

14535‐JNF, 2011

Bankr. LEXIS

4384 (Bankr. D.

Mass. Nov. 14,

2011)

Hotel, valued at

roughly $61.5

million

Two‐tiered

NO. Creditor

argued that the

market rate was

4.9%

. How

ever,

the court found the

Debtor’s expert to

be more credible.

Because of the

negative market,

and the size of the

loan, there was “no

interest.”

Short‐term loan;

first mortgage;

almost $10 million

in equity and an

additional $14

million in assets

available to secure

the loan. Creditor

did not present any

evidence on the

issue of risk

prem

ium.

1% over the

prime rate for

a total of

4.25%

To be paid in

full in less

than 4 years.

In re Walkabout

Creek, Ltd., N

o.

09‐00632, 2011

Bankr. LEXIS

4397 (Bankr. D.C.

Nov. 14, 2011)

low‐income

apartment

complexes financed

by a state housing

agency

Slightly

modified tw

o‐tiered: A

sophisticated

Ch. 11 debtor

has equal

access to data

and shares

the burden of

No. Neither the

debtor nor the

creditor w

ere able

to present credible

evidence of an

efficient market.

The court did not

reach this at length,

denying

confirmation based

on a low rate

compared to the 30‐

year treasury rate.

Creditor w

as fully

secured. The court

At least 5.24%

, which is a 1%

upward

adjustment on

the 30‐year

treasury rate.

Held that

prime is an

inappropriate

35‐year

maturity

5

proving the

risk

adjustment.

considered the

inherent risk

associated with

loans of this

magnitude and

length.

base, and

denied

confirmation

of the plan,

proposing 5%

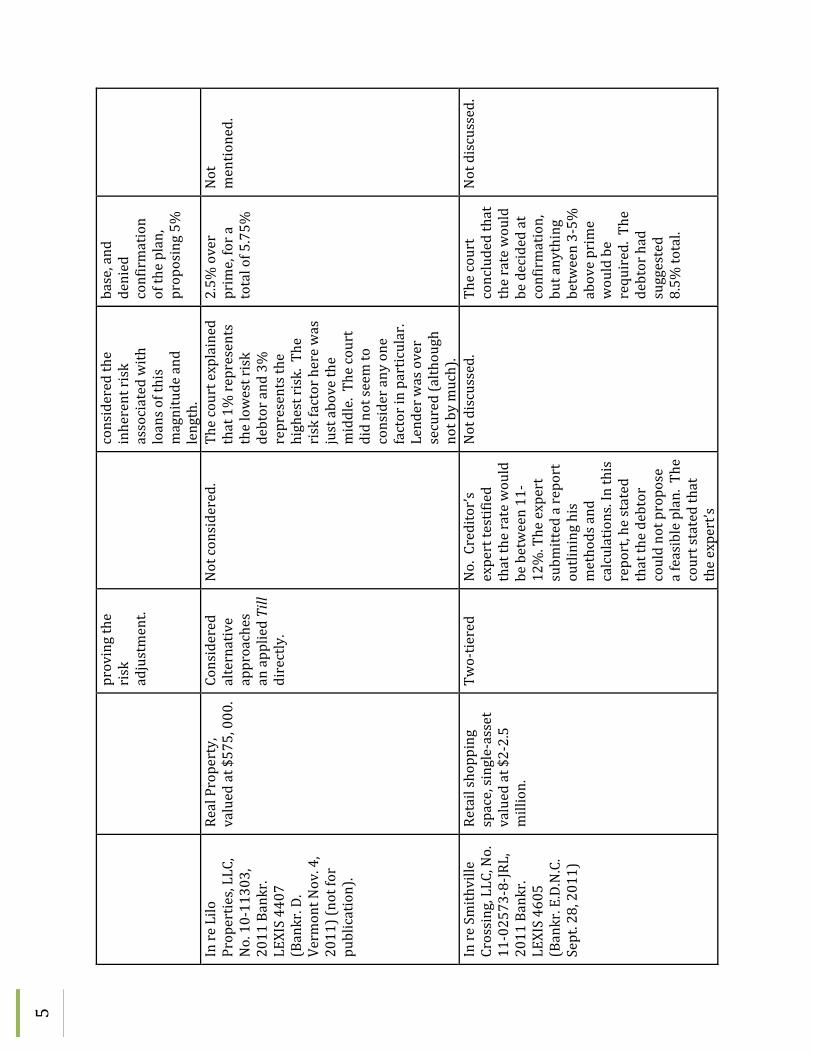

In re Lilo

Properties, LLC,

No. 10‐11303,

2011 Bankr.

LEXIS 4407

(Bankr. D.

Vermont N

ov. 4,

2011) (not for

publication).

Real Property,

valued at $575, 000.

Considered

alternative

approaches

an applied Till

directly.

Not considered.

The court explained

that 1% represents

the lowest risk

debtor and 3%

represents the

highest risk. The

risk factor here was

just above the

middle. The court

did not seem to

consider any one

factor in particular.

Lender was over

secured (although

not by much).

2.5%

over

prime, for a

total of 5.75%

Not

mentioned.

In re Smithville

Crossing, LLC, No.

11‐02573‐8‐JR

L,

2011 Bankr.

LEXIS 4605

(Bankr. E.D.N.C.

Sept. 28, 2011)

Retail shopping

space, single‐asset

valued at $2‐2.5

million.

Two‐tiered

No. Creditor’s

expert testified

that the rate would

be between 11‐

12%. The expert

subm

itted a report

outlining his

methods and

calculations. In this

report, he stated

that the debtor

could not propose

a feasible plan. The

court stated that

the expert’s

Not discussed.

The court

concluded that

the rate would

be decided at

confirmation,

but anything

between 3‐5%

above prime

would be

required. The

debtor had

suggested

8.5%

total.

Not discussed.

6

analysis was

sound, but show

ed

that there was no

effective market.

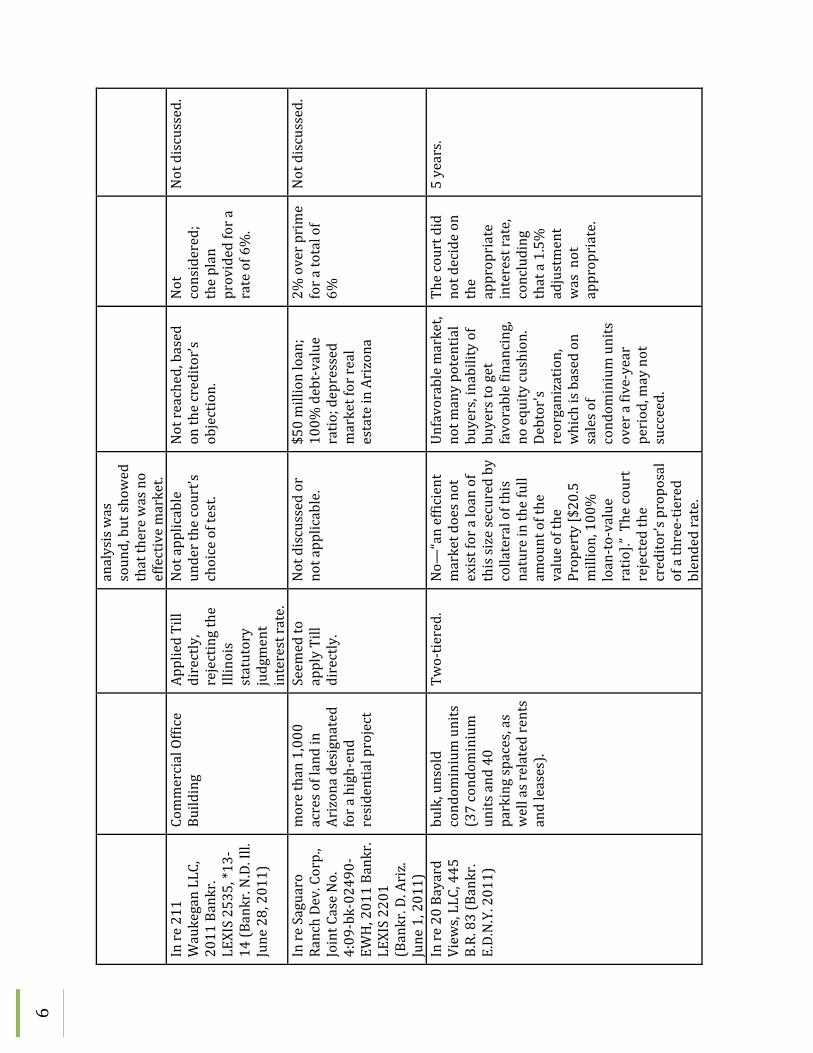

In re 211

Waukegan LLC,

2011 Bankr.

LEXIS 2535, *13‐

14 (Bankr. N.D. Ill.

June 28, 2011)

Commercial Office

Building

Applied Till

directly,

rejecting the

Illinois

statutory

judgment

interest rate.

Not applicable

under the court’s

choice of test.

Not reached, based

on the creditor’s

objection.

Not

considered;

the plan

provided for a

rate of 6%.

Not discussed.

In re Saguaro

Ranch Dev. Corp.,

Joint Case No.

4:09‐bk‐02490‐

EWH, 2011 Bankr.

LEXIS 2201

(Bankr. D. Ariz.

June 1, 2011)

more than 1,000

acres of land in

Arizona designated

for a high‐end

residential project

Seem

ed to

apply Till

directly.

Not discussed or

not applicable.

$50 million loan;

100%

debt‐value

ratio; depressed

market for real

estate in Arizona

2% over prime

for a total of

6%

Not discussed.

In re 20 Bayard

View

s, LLC, 445

B.R. 83 (Bankr.

E.D.N.Y. 2011)

bulk, unsold

condom

inium units

(37 condom

inium

units and 40

parking spaces, as

well as related rents

and leases).

Two‐tiered.

No—

“an efficient

market does not

exist for a loan of

this size secured by

collateral of this

nature in the full

amount of the

value of the

Property [$20.5

million, 100%

loan‐to‐value

ratio].” The court

rejected the

creditor’s proposal

of a three‐tiered

blended rate.

Unfavorable market,

not m

any potential

buyers, inability of

buyers to get

favorable financing,

no equity cushion.

Debtor's

reorganization,

which is based on

sales of

condom

inium units

over a five‐year

period, m

ay not

succeed.

The court did

not decide on

the

appropriate

interest rate,

concluding

that a 1.5%

adjustment

was not

appropriate.

5 years.

7

In re Riverbend

Leasing LLC, 458

B.R. 520 (Bankr.

S.D. Iowa 2011)

condom

inium

developm

ent, 112

units and five

vacant lots not yet

developed

Two‐tiered

The creditor

presented no

evidence of an

efficient market, so

the court did not

consider this

prong.

The creditor w

as

fully secured. The

court also

considered

historical data

regarding vacancies

and the debtor’s

projected earnings.

The tim

e‐value of

money, risk of non‐

paym

ent, and

inflation were also

relevant.

2.5%

over

prime for a

total of 5.75%

Paym

ent over

15 years,

amortized

over 30 years.

In re Red

Mountain

Machinery Co.,

448 B.R. 1 (Bankr.

D. Ariz. 2011)

Large earth‐moving

equipm

ent

(caterpillars),

valued at

approximately $10

million

Two‐tiered

No. Creditor relied

on a blended rate

and did not present

evidence regarding

an efficient m

arket.

Positive factors

included: guaranty

by a solvent

guarantor; positive

cash flow

and

projections;

significant

amortization over

15 years. Negative

factors included: 15‐

year term

and poor

real estate market.

3.25% over

prime for a

total of 6.5%

20 year

amortization,

with full

balance due in

15 years, 12

monthly

interest‐only

paym

ents for

the first year.

In re Greenwood

Point, LP, 445 B.R.

885, 918‐919

(Bankr. S.D. Ind.

2011)

Retail shopping

center containing

approximately

136,000 square feet

of gross leasable

space

Two‐tiered

No; in today's

econom

ic climate,

lenders are not

lending to

borrow

ers like the

Debtor due to its

bankruptcy status

and level of

vacancies.

fully collateralized;

the cash projections

were conservative

yet dem

onstrated

the ability to pay the

loan payments;

reserves were

maintained to

attract additional

tenants and to

maintain and

3% over prime

for a total of

6.25%

10‐year note

8

enhance the

collateral; the

collateral is likely to

go up in value over

the life of the loan;

Debtor's history of

always m

aking

timely debt

paym

ents

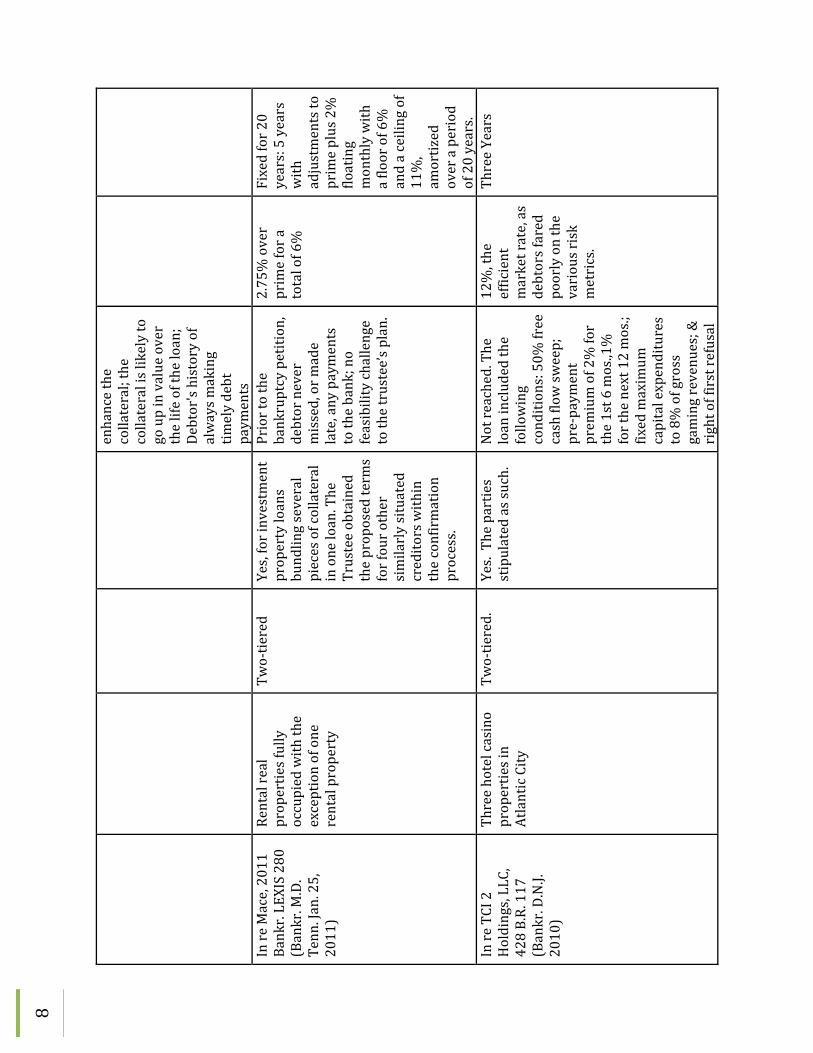

In re Mace, 2011

Bankr. LEXIS 280

(Bankr. M.D.

Tenn. Jan. 25,

2011)

Rental real

properties fully

occupied with the

exception of one

rental property

Two‐tiered

Yes, for investment

property loans

bundling several

pieces of collateral

in one loan. The

Trustee obtained

the proposed term

s for four other

similarly situated

creditors within

the confirmation

process.

Prior to the

bankruptcy petition,

debtor never

missed, or m

ade

late, any payments

to the bank; no

feasibility challenge

to the trustee’s plan.

2.75% over

prime for a

total of 6%

Fixed for 20

years: 5 years

with

adjustments to

prime plus 2%

floating

monthly with

a floor of 6%

and a ceiling of

11%,

amortized

over a period

of 20 years.

In re TCI 2

Holdings, LLC,

428 B.R. 117

(Bankr. D.N.J.

2010)

Three hotel casino

properties in

Atlantic City

Two‐tiered.

Yes. The parties

stipulated as such.

Not reached. The

loan included the

following

conditions: 50%

free

cash flow

sweep;

pre‐paym

ent

prem

ium of 2% for

the 1st 6 mos.,1%

for the next 12 mos.;

fixed maximum

capital expenditures

to 8% of gross

gaming revenues; &

right of first refusal

12%, the

efficient

market rate, as

debtors fared

poorly on the

various risk

metrics.

Three Years

9

before the Trum

p Marina can be sold.

In re Mayslake

Village‐Plainfield

Campus, Inc., 441

B.R. 309, 320

(Bankr. N.D. Ill.

2010)

real estate

improved with a

186‐unit senior

housing facility

valued at $13.4

million

Two‐tiered

No—

there was no

testimony that the

debtor could

obtain exit

financing.

Not reached.

The plan

proposed

3.25% (prime).

The court held

that some

upward

adjustment is

necessary.

20 years

In re Linda Vista

Cinemas, L.L.C.,

442 B.R. 724, 751

(Bankr. D. Ariz.

2010)

Multiplex theatre

Case‐by‐case,

considering

“explicit

findings”

relevant to a

variety of

tests.

Yes—

the court

states that the rate

proposed in the

plan “reflects a

market rate.”

The nature of the

real property is

predictable and

realizable. Monthly

paym

ents add

stability. The

collateral is w

ell‐

managed, and

there’s no evidence

of depreciation.

The Debtor has

stabilized itself from

past problem

s. The

guarantors are

financially stable.

1.5%

above

floating prime

rate

20 years

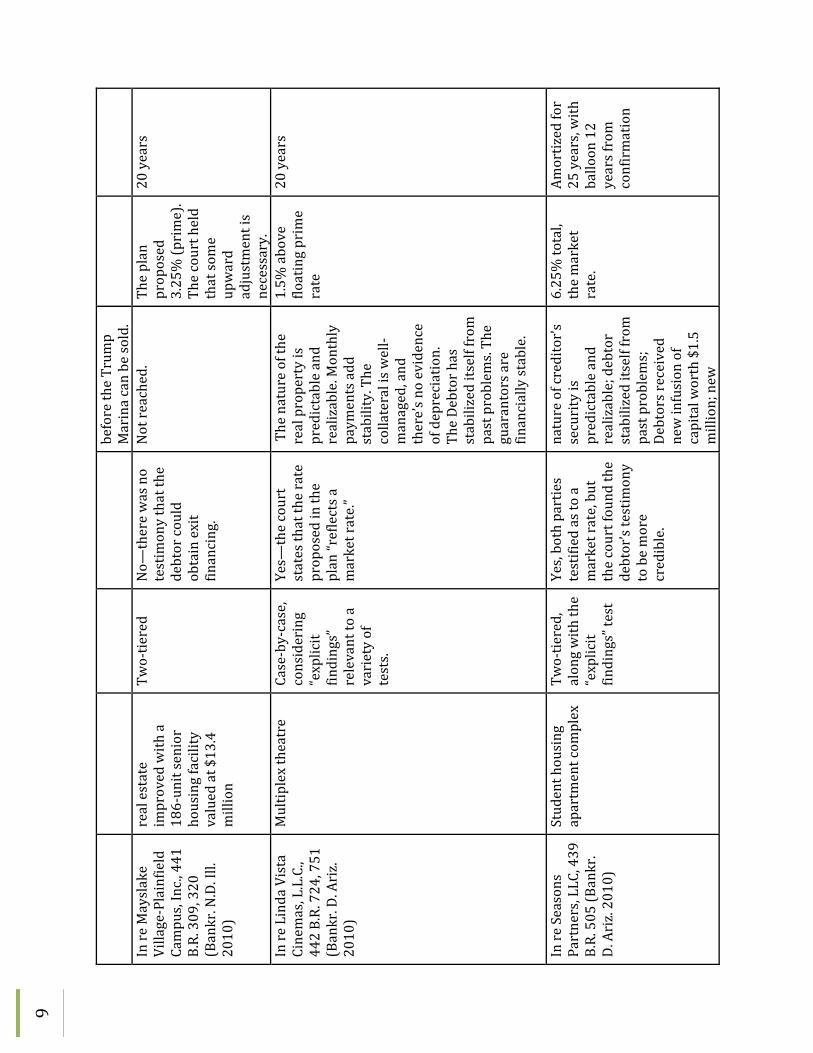

In re Seasons

Partners, LLC, 439

B.R. 505 (Bankr.

D. Ariz. 2010)

Student housing

apartment com

plex

Two‐tiered,

along with the

“explicit

findings” test

Yes, both parties

testified as to a

market rate, but

the court found the

debtor’s testimony

to be more

credible.

nature of creditor’s

security is

predictable and

realizable; debtor

stabilized itself from

past problem

s;

Debtors received

new infusion of

capital w

orth $1.5

million; new

6.25% total,

the market

rate.

Amortized for

25 years, with

balloon 12

years from

confirmation

10

managem

ent that

successfully raised

occupancy rate to

83%, pre‐petition

contract rate was

6.125%

In re S. Canaan

Cellular

Investments, Inc.,

427 B.R. 44

(Bankr. E.D. Pa.

2010)

Cell sites of

telecommunications

company

Two tiered.

NO. The creditor

bears the burden of

persuasion. The

lender had offered

some unconvincing

evidence that the

market rate was

10%.

The court

considered the

current revenues of

the debtor, its cash

reserves, and the

presence of its

parent company.

2.75% over

prime for a

total of 6%.

Not discussed.

In re Princeton

Office Park, LP,

423 B.R. 795

(Bankr. D.N.J.

2010)

Real Estate (office

park)

Applied Till

directly,

noting that 8

justices

agreed on an

adjustment

for risk.

Not considered.

Not considered; The

lender had bought a

municipal tax lien

from

the city at a

discount.

Not discussed;

remanded for

hearing.

Not discussed

In re Bryant, 439

B.R. 724 (Bankr.

E.D. Ark. 2010)

farm

land, 283 acres Tw

o‐tiered

No. No evidence

was before the

court. Court took

judicial notice that

less that Ch. 11

cases in Arkansas

account for less

than 1% of cases

filed.

Plan feasibility and

the actions taken by

the debtors to

ensure the success

of their farming

operations (cutting

costs, farm

ing closer

to hom

e, taking on

factory jobs, etc.)

2.25% over

prime for a

total of 5.5%

12 years

In re SJT

Ventures, LLC,

441 B.R. 248, 255

(Bankr. N.D. Tex.

2010)

Four‐story

commercial

building

“Market

formula”

approach,

using the

formula

Not considered.

Debt‐to‐value ratio

of 85%

, creating a

slim margin for

collateral that w

ill

possibly depreciate

6.35%, which

takes the 5‐

year treasury

rate, adds a

“spread” based

30‐year

amortization

with a 5‐year

balloon

paym

ent

11

ordinarily

used by the

market to

derive the

appropriate

interest rate

in value.

on debt‐to‐

value ratio,

with an

upward risk

adjustment.

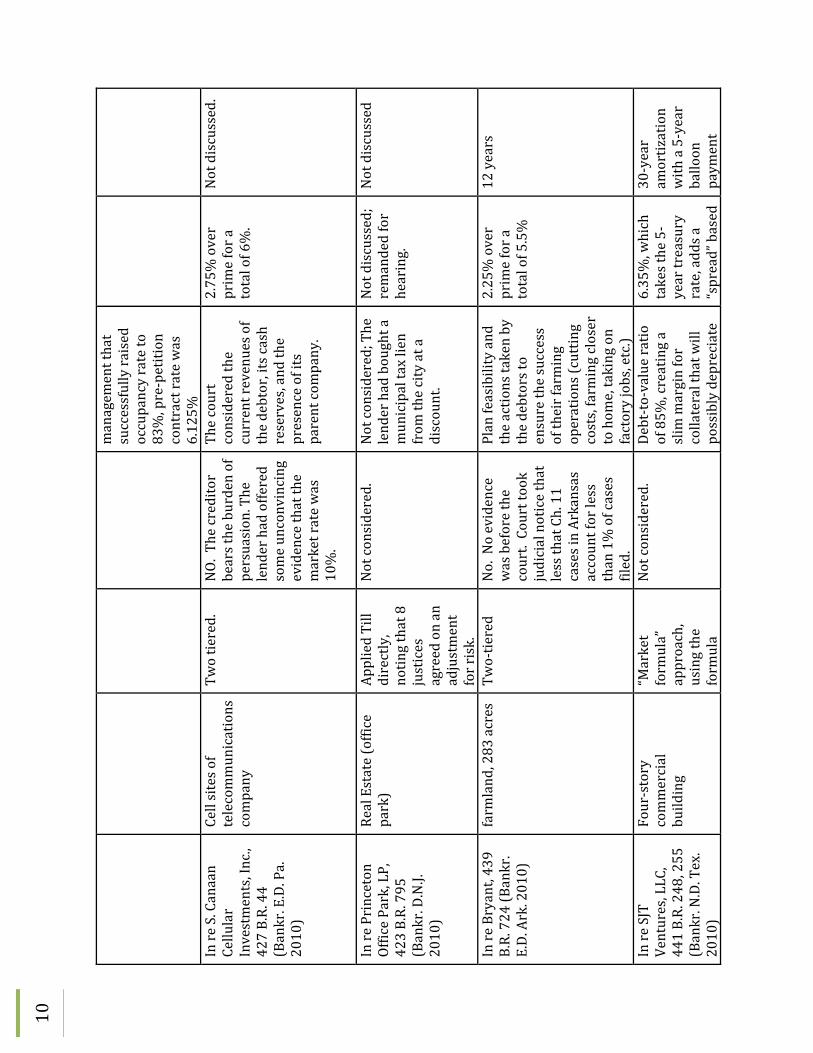

In re North Valley

Mall, LLC, 432 B.R.

825 (C.D. Cal.

2010)

Shopping center

Market

formula

approach

Not considered:

“markets such as

they exist are but

one reference point

among many in an

attempt to find a

suitable proxy

where no real

market exists”

Not discussed. The

blended rate was

based on expert

testimony regarding

the current m

arket

and yields on similar

property.

8.5%

blended

rate including

a senior

tranche, a

mezzanine

tranche, and

an equity

tranche. T

he

court found

that the prime

rate is not an

appropriate

base.

7 years

In re Mendoza,

No. 09‐11678,

2010 Bankr.

LEXIS 1308

(Bankr. N.D. Cal.

April 19, 2010)

60‐unit apartment

house

The parties

agreed that

the Till

formula

approach

applied.

Not applicable.

The interest rate

offered by the

debtor was accepted

by other similarly

situated lenders.

The vacancy was

zero, the loan was

short‐term, and the

cash flow

was more

than sufficient to

cover payments.

How

ever, the

debtors w

ere in

violation of a due‐

on‐encum

brance

clause.

1.15% over

prime for a

total of 4.4%

3 years

12

In re Am. Trailer

& Storage, Inc.,

419 B.R. 412

(Bankr. W

.D. Mo.

2009)

Portable container

units and trailers

Two‐tiered.

No. The parties

agreed that a

market exists only

among “hard

money lenders.”

“Hard money

lenders, charging

upwards of 12%

to

18%, generally are

not going to be

appropriate

options for debtors

in bankruptcy.”

Relatively stable

past payments;

projections were

realistic and had

historical support;

equity cushion of $3

million; collateral is

unlikely to decline

significantly in

value.

2.25% over

prime for a

total of 5.5%

Amortization

over 10 years,

with balloon

paym

ent at

the end of five

years

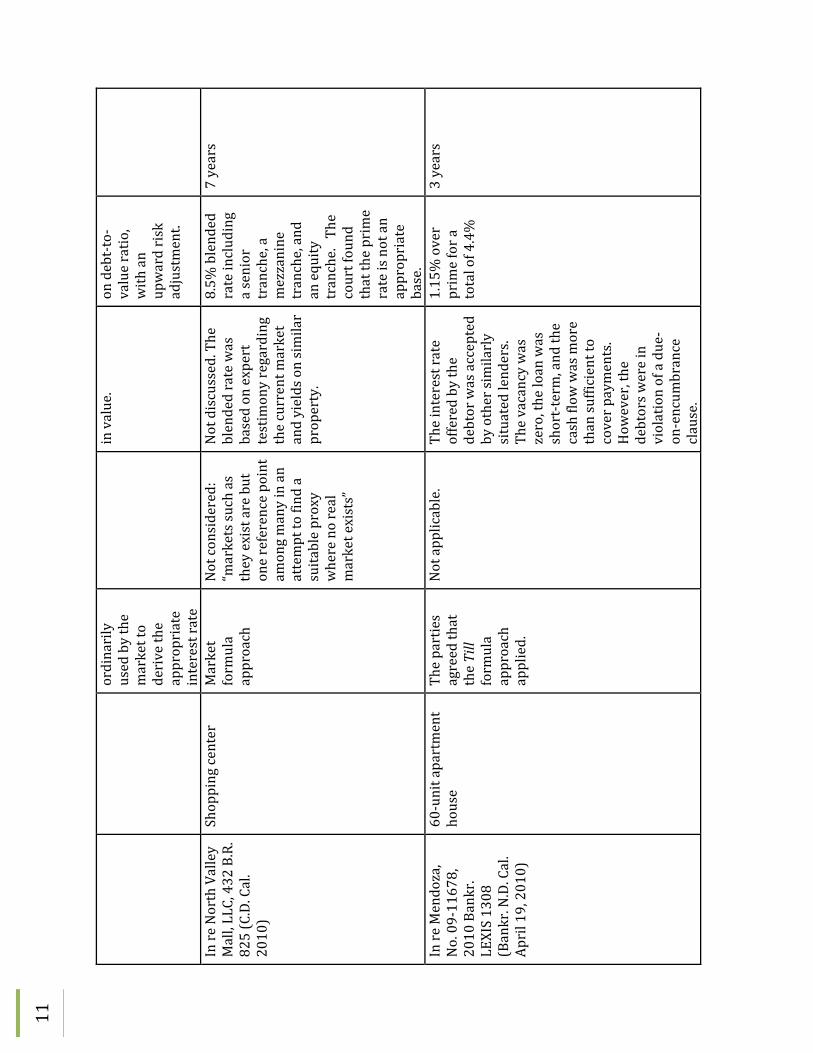

In re Winn‐Dixie

Stores, Inc., 356

B.R. 239 (M

.D. Fla.

2006)

Tax liens on

debtor’s property

Two‐tiered

Yes; Debtor w

ent

out and shopped

for post‐petition

financing, resulting

in 14 proposals

among competing

lending

institutions.

Not reached.

7%, m

arket

rate of LIBOR

plus 150

points.

Not discussed

In re Inv. Co. of

the Southw

est,

Inc., No. 11‐02‐

17878, 2004

Bankr. LEXIS

2582 (Bankr. D.

N.M. Sept. 28,

2004)

Real property

Two‐tiered

No. N

o testimony

from

either side

that any of the

national DIP

financing entities

would have any

interest in this

homegrown real

estate

sales/developm

ent

company. There

are “no closely

similar loans being

made.”

The court did not

consider the specific

risk factors, but

merely noted that

the proposed

interest rate was

within the range set

out in Till.

3% over prime

for a total of

7%

7 years

AP

PE

ND

IX B

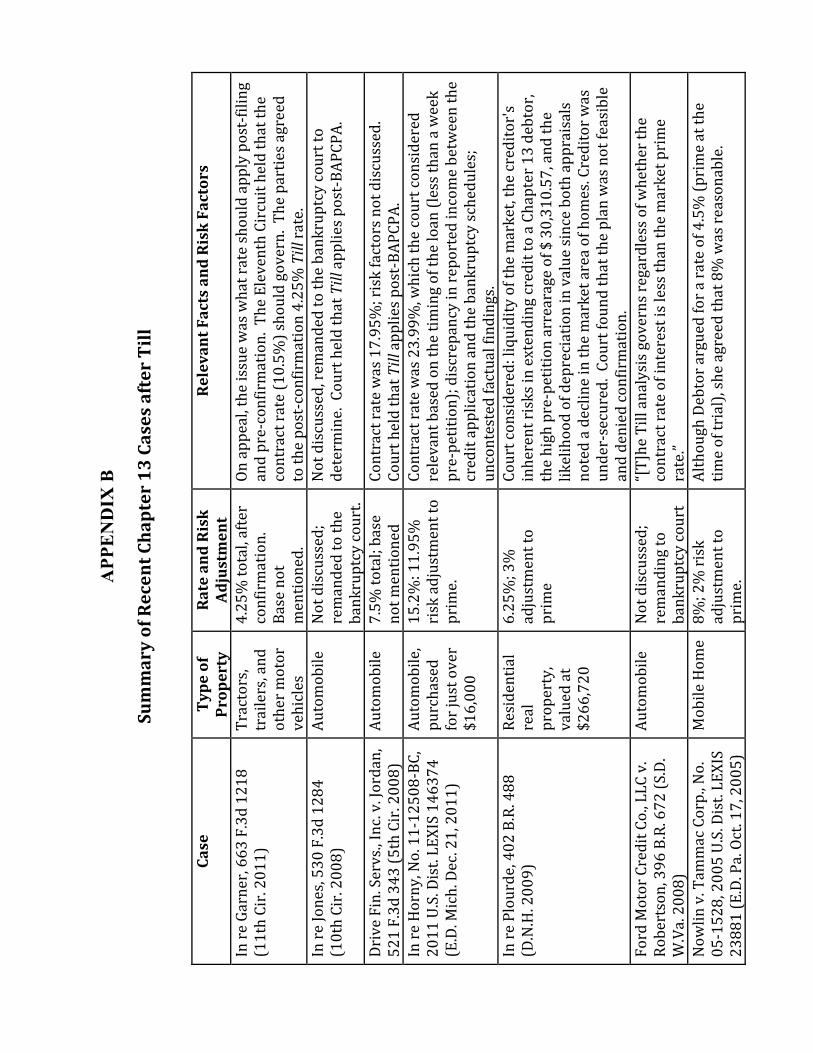

Summary of Recent Chapter 13 Cases after Till

Case

Type of

Property

Rate and Risk

Adjustment

Relevant Facts and Risk Factors

In re Garner, 663 F.3d 1218

(11th Cir. 2011)

Tractors,

trailers, and

other m

otor

vehicles

4.25% total, after

confirmation.

Base not

mentioned.

On appeal, the issue was what rate should apply post‐filing

and pre‐confirmation. The Eleventh Circuit held that the

contract rate (10.5%

) should govern. The parties agreed

to the post‐confirmation 4.25% Till rate.

In re Jones, 530 F.3d 1284

(10th Cir. 2008)

Automobile

Not discussed;

remanded to the

bankruptcy court.

Not discussed, rem

anded to the bankruptcy court to

determ

ine. Court held that Till applies post‐B

APCPA.

Drive Fin. Servs., Inc. v. Jordan,

521 F.3d 343 (5th Cir. 2008)

Automobile

7.5%

total; base

not m

entioned

Contract rate was 17.95%; risk factors not discussed.

Court held that Till applies post‐B

APCPA.

In re Horny, No. 11‐12508‐BC,

2011 U.S. Dist. LEXIS 146374

(E.D. Mich. Dec. 21, 2011)

Automobile,

purchased

for just over

$16,000

15.2%: 11.95%

risk adjustment to

prime.

Contract rate was 23.99%, which the court considered

relevant based on the tim

ing of the loan (less than a week

pre‐petition); discrepancy in reported income between the

credit application and the bankruptcy schedules;

uncontested factual findings.

In re Plourde, 402 B.R. 488

(D.N.H. 2009)

Residential

real

property,

valued at

$266,720

6.25%; 3%

adjustment to

prime

Court considered: liquidity of the market, the creditor's

inherent risks in extending credit to a Chapter 13 debtor,

the high pre‐petition arrearage of $ 30,310.57, and the

likelihood of depreciation in value since both appraisals

noted a decline in the market area of hom

es. Creditor w

as

under‐secured. Court found that the plan was not feasible

and denied confirmation.

Ford Motor Credit Co., LLC v.

Robertson, 396 B.R. 672 (S.D.

W.Va. 2008)

Automobile

Not discussed;

remanding to

bankruptcy court

“[T]he Till analysis governs regardless of w

hether the

contract rate of interest is less than the market prime

rate.”

Now

lin v. Tam

mac Corp., No.

05‐1528, 2005 U.S. Dist. LEXIS

23881 (E.D. Pa. Oct. 17, 2005)

Mobile Hom

e8%

; 2% risk

adjustment to

prime.

Although Debtor argued for a rate of 4.5% (prime at the

time of trial), she agreed that 8% was reasonable.

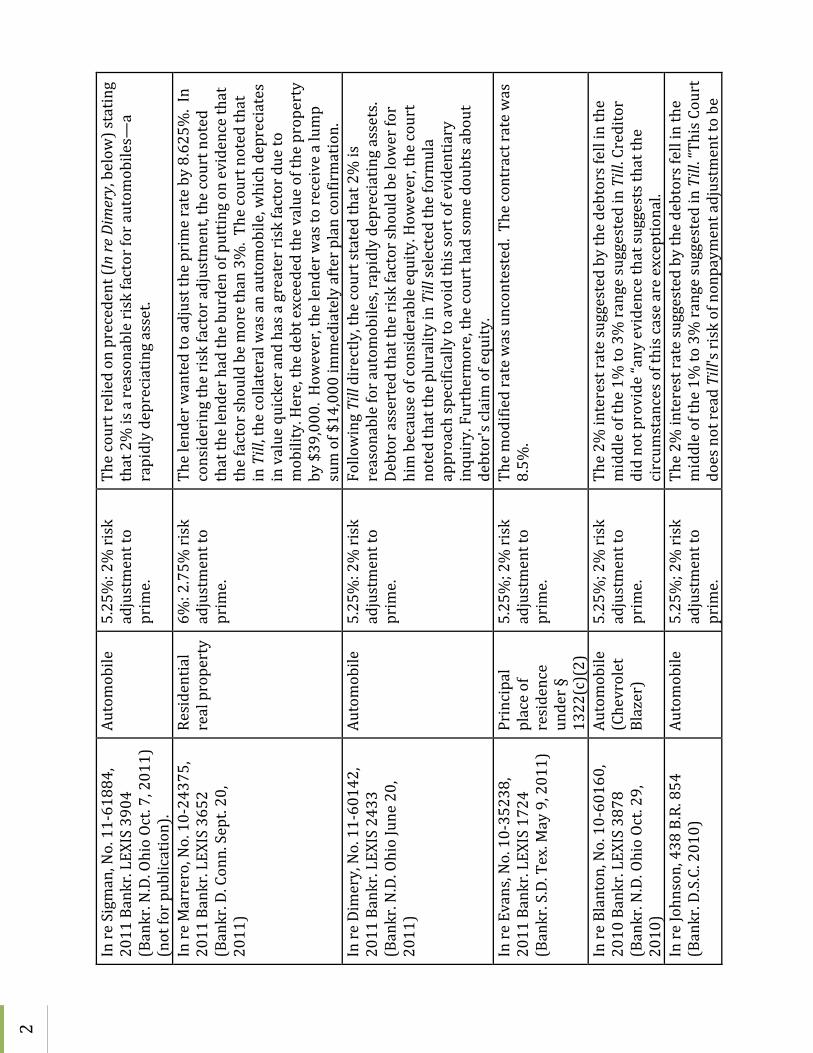

2

In re Sigman, No. 11‐61884,

2011 Bankr. LEXIS 3904

(Bankr. N.D. Ohio Oct. 7, 2011)

(not for publication).

Automobile

5.25%: 2% risk

adjustment to

prime.

The court relied on precedent (In re Dimery, below) stating

that 2% is a reasonable risk factor for autom

obiles—

a rapidly depreciating asset.

In re Marrero, No. 10‐24375,

2011 Bankr. LEXIS 3652

(Bankr. D. Conn. Sept. 20,

2011)

Residential

real property

6%: 2.75%

risk

adjustment to

prime.

The lender wanted to adjust the prime rate by 8.625%

. In

considering the risk factor adjustment, the court noted

that the lender had the burden of putting on evidence that

the factor should be more than 3%. The court noted that

in Till, the collateral w

as an automobile, which depreciates

in value quicker and has a greater risk factor due to

mobility. Here, the debt exceeded the value of the property

by $39,000. H

owever, the lender was to receive a lump

sum of $14,000 im

mediately after plan confirmation.

In re Dimery, No. 11‐60142,

2011 Bankr. LEXIS 2433

(Bankr. N.D. Ohio June 20,

2011)

Automobile

5.25%: 2% risk

adjustment to

prime.

Following Till directly, the court stated that 2% is

reasonable for autom

obiles, rapidly depreciating assets.

Debtor asserted that the risk factor should be lower for

him because of considerable equity. How

ever, the court

noted that the plurality in Till selected the formula

approach specifically to avoid this sort of evidentiary

inquiry. Furthermore, the court had some doubts about

debtor's claim of equity.

In re Evans, No. 10‐35238,

2011 Bankr. LEXIS 1724

(Bankr. S.D. Tex. May 9, 2011)

Principal

place of

residence

under §

1322(c)(2)

5.25%; 2% risk

adjustment to

prime.

The modified rate was uncontested. The contract rate was

8.5%

.

In re Blanton, No. 10‐60160,

2010 Bankr. LEXIS 3878

(Bankr. N.D. Ohio Oct. 29,

2010)

Automobile

(Chevrolet

Blazer)

5.25%; 2% risk

adjustment to

prime.

The 2%

interest rate suggested by the debtors fell in the

middle of the 1%

to 3% range suggested in Till. Creditor

did not provide “any evidence that suggests that the

circum

stances of this case are exceptional.

In re Johnson, 438 B.R. 854

(Bankr. D.S.C. 2010)

Automobile

5.25%; 2% risk

adjustment to

prime.

The 2%

interest rate suggested by the debtors fell in the

middle of the 1%

to 3% range suggested in Till. “This Court

does not read Till's risk of nonpaym

ent adjustment to be

3

the same as the creditw

orthiness factors that go into the

initial lending decision. Instead, . . . the risk of nonpaym

ent

referred to in Till is the risk that the chapter 13 debtor's

plan will not succeed.”

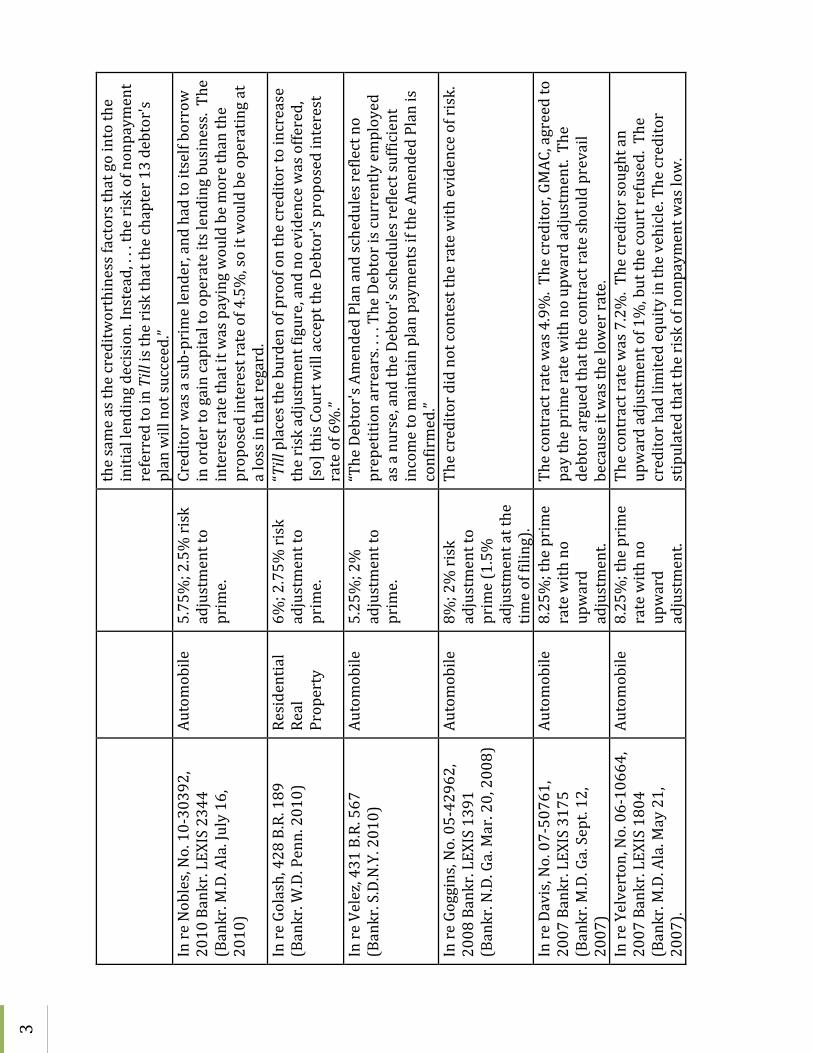

In re Nobles, No. 10‐30392,

2010 Bankr. LEXIS 2344

(Bankr. M.D. Ala. July 16,

2010)

Automobile

5.75%; 2.5% risk

adjustment to

prime.

Creditor w

as a sub‐prime lender, and had to itself borrow

in order to gain capital to operate its lending business. The

interest rate that it was paying would be more than the

proposed interest rate of 4.5%, so it would be operating at

a loss in that regard.

In re Golash, 428 B.R. 189

(Bankr. W

.D. Penn. 2010)

Residential

Real

Property

6%; 2.75%

risk

adjustment to

prime.

“Till places the burden of proof on the creditor to increase

the risk adjustment figure, and no evidence was offered,

[so] this Court will accept the Debtor's proposed interest

rate of 6%.”

In re Velez, 431 B.R. 567

(Bankr. S.D.N.Y. 2010)

Automobile

5.25%; 2%

adjustment to

prime.

“The Debtor's Amended Plan and schedules reflect no

prepetition arrears. . . . The Debtor is currently employed

as a nurse, and the Debtor's schedules reflect sufficient

income to maintain plan payments if the Am

ended Plan is

confirmed.”

In re Goggins, No. 05‐42962,

2008 Bankr. LEXIS 1391

(Bankr. N.D. Ga. Mar. 20, 2008)

Automobile

8%; 2% risk

adjustment to

prime (1.5%

adjustment at the

time of filing).

The creditor did not contest the rate with evidence of risk.

In re Davis, No. 07‐50761,

2007 Bankr. LEXIS 3175

(Bankr. M.D. Ga. Sept. 12,

2007)

Automobile

8.25%; the prime

rate with no

upward

adjustment.

The contract rate was 4.9%. The creditor, GM

AC, agreed to

pay the prime rate with no upward adjustment. The

debtor argued that the contract rate should prevail

because it was the lower rate.

In re Yelverton, No. 06‐10664,

2007 Bankr. LEXIS 1804

(Bankr. M.D. Ala. May 21,

2007).

Automobile

8.25%; the prime

rate with no

upward

adjustment.

The contract rate was 7.2%. The creditor sought an

upward adjustment of 1%, but the court refused. The

creditor had limited equity in the vehicle. The creditor

stipulated that the risk of nonpaym

ent w

as low.