intellectual capital governance and the knowledge...

TRANSCRIPT

Intellectual Capital Governance and the Knowledge Economy in Canada

Anthony Michael Hoffmann Faculty of Law, McGili University, Montréal

August, 2003

Athesis submitted to McGiII University in partial fulfilment of the requirements of the degree of Master of Laws

© Anthony Michael Hoffmann, 2003

1+1 Library and Archives Canada

Bibliothèque et Archives Canada

Published Heritage Branch

Direction du Patrimoine de l'édition

395 Wellington Street Ottawa ON K1A ON4 Canada

395, rue Wellington Ottawa ON K1A ON4 Canada

NOTICE: The author has granted a nonexclusive license allowing Library and Archives Canada to reproduce, publish, archive, preserve, conserve, communicate to the public by telecommunication or on the Internet, loan, distribute and sell th es es worldwide, for commercial or noncommercial purposes, in microform, paper, electronic and/or any other formats.

The author retains copyright ownership and moral rights in this thesis. Neither the thesis nor substantial extracts from it may be printed or otherwise reproduced without the author's permission.

ln compliance with the Canadian Privacy Act some supporting forms may have been removed from this thesis.

While these forms may be included in the document page count, their removal does not represent any loss of content from the thesis.

• •• Canada

AVIS:

Your file Votre référence ISBN: 0-612-98792-2 Our file Notre référence ISBN: 0-612-98792-2

L'auteur a accordé une licence non exclusive permettant à la Bibliothèque et Archives Canada de reproduire, publier, archiver, sauvegarder, conserver, transmettre au public par télécommunication ou par l'Internet, prêter, distribuer et vendre des thèses partout dans le monde, à des fins commerciales ou autres, sur support microforme, papier, électronique et/ou autres formats.

L'auteur conserve la propriété du droit d'auteur et des droits moraux qui protège cette thèse. Ni la thèse ni des extraits substantiels de celle-ci ne doivent être imprimés ou autrement reproduits sans son autorisation.

Conformément à la loi canadienne sur la protection de la vie privée, quelques formulaires secondaires ont été enlevés de cette thèse.

Bien que ces formulaires aient inclus dans la pagination, il n'y aura aucun contenu manquant.

Abstract

Intellectual capital, as opposed to traditional conceptions of intellectual property, is neither as simple to define nor as straightforward to protect and regulate. As companies in the financial services sector attempt the efficient management of increasingly voluminous and strategically important information and knowledge, governance mechanisms currently available in the Canadian context have not kept pace.

This thesis is at once a retrospective and prospective examination of the regulation and control of intellectual capital. The first two substantive sections of this thesis are primarily definitive and contextualizing - first defining the nature of contemporary legal and managerial concepts of intellectual capital and property, then examining the varied legal frameworks from which an intellectual capital governance scheme is distilled. The final chapter attempts a synthesis of these definitions and legal approaches to the governance of intellectual capital. The keystones of this synthesis are twofold: first, uniform Canadian legislation; and second, a more focused incorporation of 'property rights' in intellectual capital.

Résumé

Le capital intellectuel, à l'opposé des conceptions traditionnelles de la propriété intellectuelle, n'est pas aussi facile à définir, et sa réglementation ainsi que sa protection sont encore plus compliquées. Au fur et à mesure que les compagnies dans le secteur des services financiers tentent la gestion efficace d'un volume d'informations et de connaissances de plus en plus important, les procédures et les règlements actuellement disponibles au Canada n'ont pu se développer assez rapidement pour soutenir les exigences.

La présente thèse est un examen à la fois rétrospectif et prospectif de la réglementation et du contrôle du capital intellectuel. Les deux premiers chapitres de la présente thèse ont pour principal but la définition et la mise en contexte du problème - en premier lieu, la définition de la nature des concepts légaux et de gestion à la fois du capital et de la propriété intellectuelle, et, en deuxième lieu, l'examen de l'encadrement contemporain des lois qui créent le capital intellectuel. Le dernier chapitre constitue une synthèse de ces définitions et de ces approches juridiques afin d'obtenir une structure cohérente du capital intellectuel. Les clés de cette synthèse sont au nombre de deux: premièrement, l'uniformité de la législation canadienne; et deuxièmement, une synthèse plus ciblée des concepts de la propriété dans le capital intellectuel.

Acknowledgements

This thesis would not have been possible without the support and assistance of a number of individuals, ail of to whom 1 owe an immense debt of gratitude. The mental gymnastics 1 have tried to perform were with the certain knowledge that 1 would be caught without question before hitting the ground.

ln particular, 1 would like to express my gratitude ta my advisor, Professor David Lametti, for his patience, understanding, and critical and constructive eye, as weil as for his trust in my abilities. Professor Lametti never failed to let me do my own thing, and for that 1 am very grateful.

Equally important was the continued maintenance of my mental health by so many of my friends. Near or far, their ability to make me laugh when 1 least felt like laughing was more important than 1 can adequately express. Cheryl Plambeck, Nathalie Cousserans, Jono Kalles, Jon Greer and many others were ail an enormously important part of making this thesis possible.

At the last, there is no way 1 can thank my parents, Dr. Joan Eakin and Chris Hoffmann, and my sisters Willa and Marian enough. They gave me the opportunit y to get where 1 am today and their unconditional love and help along the way.

- Tony Hoffmann August, 2003

ii

Table of Contents

Acknowledgements ............................................................................................. ii Table of Contents ............................................................................................... iii Table of Figures .................................................................................................. iv Chapter 1 Thesis Overview ............................................................................ 1

1.1 Introduction ........................................................................................... 1 1.2 Intellectual Property & Intellectual Capital ......................................... 2 1.3 Thesis Objective: .................................................................................. 5 1.4 Thesis Methodology: ............................................................................ 6

1.4.1 Preliminary Definitions ..................................................................... 6 1.4.2 Current Legal Regimes .................................................................... 8 1.4.3 A Reconceptualization of Intellectual Capital Governance ............. 10

1.5 Applied Comparative Legal Methodology ......................................... 11 Chapter 2 Defining Terms in an Intellectual Capital Protection Regime .. 13

2.1 Introduction ......................................................................................... 13 2.2 Intellectual Capital .............................................................................. 13

2.2. 1 The Zurich Insurance Model .......................................................... 17 2.2.1.1 Human Capital ............................................................................................ 18 2.2.1.2 Structural Capital ........................................................................................ 21

2.3 Intellectual Property ........................................................................... 27 2.4 Conclusion .......................................................................................... 28

Chapter 3 Current Legal Regimes ................................................................ 30 3.1 Introduction ......................................................................................... 30 3.2 Intellectual Property in the Intellectual Capital Context .................. 31 3.3 Trade Secrets and Intellectual Capital Governance ......................... 39

3.3.1 Trade Secret in United States ....................................................... .42 3.3.2 NAFTA Treatment of Trade Secret ............................................... .45 3.3.3 World Trade Organization Treatment of Trade Secret .................. .48 3.3.4 Trade Secret in Canada ................................................................. 50

3.3.4.1 The Mutual Fund Industry Example ........................................................... 55 3.4 Persona"nformation Regulation Regimes ....................................... 59

3.4.1 Introduction .................................................................................... 59 3.4.2 Personal information and privacy in the commercial context ......... 61 3.4.3 Canadian Federal Treatment ......................................................... 64

3.4.3.1 Financiallnstitutions Regulation ................................................................. 69 3.4.4 Canadian Provincial Treatment ...................................................... 70 3.4.5 American Treatment ...................................................................... 75 3.4.6 Conclusion ..................................................................................... 78

3.5 The Employment Law Regime ........................................................... 79 3.5.1 Contractual Governance of Intellectual Capital .............................. 82

3.6 Civil Litigation and Criminal Law Regimes ....................................... 88 3.6. 1 The Civil Litigation Regime ............................................................ 89 3.6.2 The Criminal Law Regime .............................................................. 91

3.7 Conclusion .......................................................................................... 92

iii

Chapter 4 Toward Reconceptualizing Intellectual Capital Governance ... 94 4.1 Introduction ......................................................................................... 94 4.2 An Intellectual Capital Governance Framework ............................... 95 4.3 Intellectual Property Law Contributions ........................................... 97 4.4 Trade Secret Law Contributions ...................................................... 100 4.5 Personallnformation Protection Law Contributions ..................... 102 4.6 Employment Law Contributions ...................................................... 104 4.7 Civil Litigation Regime Contributions ............................................. 106 4.8 Conclusion ........................................................................................ 107

Bibliography .................................................................................................... 108 Legislation Cited .......................................................................................... 108 Jurisprudence Cited .................................................................................... 109 Books Cited .................................................................................................. 111 Articles Cited ............................................................................................... 113 Other Material Cited ..................................................................................... 116

Table of Figures

Figure 1: Intellectual Capital (IC) Management Continuum ................................. 16 Figure 2: Converting Knowledge to/from information .......................................... 33 Figure 3: Current Intellectual Capital Governance Framework ............................ 96

iv

Chapter 1 Thesis Overview

1.1 Introduction

The 21 st century is the age of the information economy. What you know,

and how you protect that knowledge from your competitors, is a critical aspect of

a successful business. Nowhere does this axiom ho Id more true than in the ser-

vice industry, where it is ideas, theories, and business methods that are bought,

sold, traded, and licensed. In their 2002 Annual Review, for example, the ac-

counting and consulting giant PriceWaterhouseCoopers stated that for the previ-

ous year, their revenue was $13.8 billion, not including $5 billion of revenue from

PWC Consulting, which was sold to IBM Inc., another giant 'idea company,.1

PWC states proudly not only these astronomical revenue figures, but also de

clares that it employs over 142,000 people in 142 countries worldwide.2 This is

not, however, the end of the story, since accounting and consulting firms, mas-

sive as they may be, are derivative industries - they rely on other organizations

for their bottom line. In the knowledge economy then, it seems reasonable to fol-

low the money trail. In the United States, as of the end of 2002, there were 3,672

commercial banks with assets of over $100 million, and the total assets of these

represented a staggering $6.6 trillion.3 ln Canada, though the figures are less

monumental given the smaller overall economy, they are nevertheless impres-

sive: Canada's 14 chartered banks manage $1.7 trillion dollars, which accounts

1 PriceWaterhouseCoopers, 2002 Global Annual Review, available online: www.pwc.com at 3. 2 Ibid. at 4. 3 United States Federal Reserve Board, "Insured U.S.-Chartered Commercial Banks that have Consolidated Assets of $100 million or more Ranked by consolidated assets", December 31, 2002, available online: http://www.federalreserve.gov/releases/lbr/currentllrg bnk Is1.tx1.

1

for more than 70 percent of the as sets of the financial services sector.4

But what is their product? What do they sell? The answer, very simply, is

their ideas and their expertise. But how do they leverage these ideas and this ex-

pertise and, more importantly, how do financial services firms, be they banks,

mutual fund companies, insurance companies, or any of the myriad players in the

'information economy' protect these ideas and expertise? This is particularly im-

portant in an environ ment which, from a regulatory and legislative point of view, is

more open and more onerous than ever?5 The answer is, as with so many others

in the field of legal academics, it depends.

1.2 Intellectual Property & Intellectual Capital

Companies founded on intellectual property and intellectual capital must

operate in an environ ment fraught with obstacles, both legislative and competi-

tive. On the one hand, financial services companies are heavily regulated, while

on the other, competition between industry players is fierce. In this environment,

financial services firms have been forced to keep pace, both from a regulatory

compliance point of view and from a competitive point of view. This business

paradigm is perhaps no more evident than in how the industry has dealt with both

rapidly developing technology and, as a consequence, rapidly developing ques-

tions of how a service industry can protect itself in a competitive market. A manu-

facturing company can protect itself quite weil with the use of copyright, patent,

4 Government of Canada, Department of Finance, "Canada's Banks - Fact Sheet", August 2002. available online: http://www.fin.gc.ca/access/fininste.html 5 For example, in response to the Enron disaster, the United States recently enacted the Sarbanes-Oxley Act, legislation designed to increase accountability and transparency for public corporations. See the Sarbanes-Oxley Act of 2002, H.Res. 3763. Available online: http://thomas.loc.gov/bss/d107guery.html.

2

and trademark law. A service company based on the provision of intellectual

capital, however, is less able to protect itself. This is primarily because while intel

lectual 'property' can be protected by the legal system, intellectual capital gov

ernance is a far more difficult problem.

To facilitate an understanding of the insufficiency of current intellectual capi

tal governance mechanisms, a parallel may be drawn with questions surrounding

the regulation and prohibition of hate speech and the policy goals of such regula

tion. Despite best intentions, regulating anything beyond the physical or literai

manifestation of hatred cannot seriously be considered. Disturbingly, the same

problem is faced by policy-makers and corporate citizens in attempting to protect

intellectual capital. The problem is as follows: as hateful thought is to acts of hate,

so intellectual capital is the primordial seed of intellectual property. However,

since it exists in the minds of employees or in the form of information that is not

physically manifest (or for which a property interest is not adequately defined), it

is in many respects as unprotectable as hateful thought is unpreventable.

Intellectual property regimes have traditionally dealt with the regulation of

'intellectually capitalized' firms on an almost ad hoc basis, and the result has

been a patchwork of statu te and jurisprudence pulled from numerous legal re

gimes. The jurisprudential and regulatory framework, therefore, is ineffective be

cause intellectual property governance is based on iII-defined precepts. The legal

notion of trade secrets, for example, relies simply on keeping something secret

and ultimately being able to maintain that confidentiality. This non sequitur re

veals an important logical flaw in intellectual capital governance: if, in defending a

3

claim of trade secret, one is to say "this information is a trade secret because it

was at ail times kept confidential, and should thus be protected", then one must

ask the question "if that information was kept secret, then how was that confi

dence breached?" The question that this thesis will attempt to resolve is: how can

the definitions and legal treatments of intellectual capital be clarified so that both

the legal and business participants have the most robust intellectual capital gov

ernance mechanisms at their disposai?

The above paradox further reveals inherent flaws in the governance regime.

If it can be shown that the secret information was divulged through nefarious

means, then a further problem arises: the governance of the unprotectable

amounts to the use of public resources (i.e., the enforcement of the Criminal

Code if theft can be shown) to enforce the interests of private citizens. While such

a structure is not uncommon, the question remains as to whether corrective jus

tice is the appropriate mechanism with which to govern the intellectual property

and intellectual capital landscapes.

Financial service firms including banks, investment firms, trust companies,

and mutual fund companies ail face an enormous challenge with respect to pro

tecting their assets. Why? Because such firms, despite their status as banks or

other sol id financial institutions, are to a large degree dependent not on 'what

they make' per se, but on 'how they interact with a client'. In order to be success

fui in the knowledge-based economy, such financial service institutions must

have a clear understanding of how their intellectual capital is protected by the le

gal system. They must also be aware of the system's limitations and the duties

4

placed on them. The definition of, and the maintenance of the integrity of, this 'in-

tellectual capital' and its application to the financial services sector is the focus of

this thesis.

1.3 Thesis Objective:

This thesis will examine how current legal regimes - ranging from employ-

ment law jurisprudence (a recent motion judgment denied an injunction restricting

a money manager's ability to move between two Canadian financial services

firms6) to copyrighf and patent8 law (traditional intellectual property regimes) to

the interaction of such regimes with privacy and consumer protection legislation -

are synthesized towards the efficient governance of intellectual capital. Though a

necessary precursor to any subsequent proposais, it is not the primary purpose

of this thesis merely to survey how legislation and jurisprudence can affect the

maintenance of a financial service~ firm's intellectual capital. Rather, the purpose

is to address a number of fundamental inconsistencies in intellectual capital gov-

ernance. Although the an artificial segregation of the components of intellectual

capital and intellectual property is not entirely realistic in the context of current

business models, it is the most effective method of examining the component

parts of the framework as a whole. The resulting questions, in their broadest

sense, are as follows9: what is the nature of the intellectual capital that financial

services firms wish to govern; how has this intellectual capital been protected to

6 TAL Global Asset Management Inc. v. Virginia Wai-Ping et al. (17 January 2003), Toronto 02-CV-00241164CM3 (Ont. S.C.). online: http://www.canliLorg/on/cas/onsc/2003/20030nsc10027.html(date accessed: 19 April 2003) ~herein~fter TAL].

Copyright Act, R.S.C. 1985, c. C-42. 8 Patent Act, R.S.C., c. P-4. 9 Note that each of these subdivisions will address more precise and concrete questions.

5

date in countries with weil developed intellectual property regimes (to wit, this

thesis will attempt to draw from the experiences of financial services firms across

Canada and in other common law jurisdictions.); and finally, having described the

state of the current governance framework, how can that structure, diverse and

disconnected as it is, be enunciated or restructured to reflect a more comprehen

sive treatment of intellectual capital in the modern financial services sector?

1.4 Thesis Methodology:

There are a number of crucial steps in the analysis. The analytical structure

will follow a fundamentally similar pattern to that of any other legal argument.

However, issues not explicitly legal in nature will inevitably be addressed. On a

very fundamental level, therefore, this thesis will proceed from a standard argu

mentative perspective with a view to accomplishing a number of milestones, each

of which will build a solid foundation for any proposed changes or improvements

that come to light as a consequence.

1.4.1 Preliminary Definitions

First and foremost, in order for the conclusion to logically follow from the

premises, it is necessary to understand what the 'object' of intellectual capital

governance is. That is, in order to understand how intellectual capital is treated

by the legal system, one must first understand precisely what intellectual capital

is. This thesis, the refore, will canvass the wide variety of intellectual capital in the

financial services sector. Such intellectual capital include business processes,

employees, client lists and personal information lists, investment and other profit

making strategies, and goodwill. The preliminary section will proceed from a

6

number of established definitions, both legal and extra-Iegal, of intellectual capi-

tal, property, and rights and interests.

The intention in basing the analysis on currently accepted conceptions of in-

tellectual property and capital is rooted in the desire to provide a 'jumping off

point' towards a re-conceptualization of how such capital and property can be

governed. In the context of this thesis, 'Intellectual Capital' can be generally de

fined as 'knowledge that can be converted into profit.,,1o There is no doubt that

this is a very inclusive definition, but two reasons militate against taking a nar-

rower view: first, if the goal is the effective governance of those aspects of intel-

lectual capital either totally unprotected or marginally protected by current legal

regimes, then it serves no purpose to exclude any su ch capital from the outset;

and second, it is precisely this unknown capital landscape that a new intellectual

capital protection regime should be addressing, and eliminating the object of

governance implicitly eliminates the need to govern them. If, at the outset, it is

averred that a particular piece of information or skill or knowledge is not intellec-

tuai capital, then the need to govern it evaporates. A further breakdown of the no-

tion of 'capital' in the legal and business contexts will also be made between hu-

man and structural capital. This parsing is based on the view that such artificial

distinctions, convenient as they may be, are detrimental to a robust governance

scheme.

Intellectual 'property' in this thesis is a legal term describing intellectual as-

sets for which legal protection has already been obtained. That is, this head of

10 Intellectual Capital Management Group, "Intellectual Capital", online: http://www.icmgroup.com/gp.asp?pld=4.

7

governance is comprised of knowledge for which there exists protections such as

those offered by the laws of copyright, patent, trade-mark etc. Importantly, this is

knowledge which has been fixed, as such fixation is a necessary precursor to

protection under the current system. Simple fixation, however, does not neces

sarily imply governability, and this 'fuzzification' of the boundaries of legal protec

tion offers the first indication that the foundation for knowledge and intellectual

capital governance may not be as solid as previously thought.

1.4.2 Current Legal Regimes

Chapter Three will address current intellectual property and other legal re

gimes which presently - or may in future - address intellectual capital and intel

lectual property governance. This thesis proposes that, as a first step, it is impor

tant to understand how current law protects such types of intellectual capital as

were defined in the previous canvass. That is, how do the intellectual property

regimes, employment law regimes, and civil liability regimes both in Canada and

in other countries, purport to both protect the players in the financial services sec

tor and maintain a manageable, fair, and practical governance structure.

With a view to simultaneously compartmentalizing and unifying the various

legal and jurisprudential regimes mentioned above, each will be addressed indi

vidually in the financial services context and in the context of the definitions more

clearly defined and expanded in Chapter Two. Accounting for what is established

as common financial services intellectual property, therefore, this section of

Chapter Two will examine how intellectual property as sets are governed by legal

mechanisms such as the Copyright Act and the Patent Act. It is important to note

8

that even at such a preliminary stage of the analysis, problems are expected,

since there are a number of areas in which the concept of property interests in

certain assets is unclear. Personal information, for example, is an area under

much debate. 11 While a business may have an interest in the physical manifesta-

tion - that is, the list itself - there is doubt as to who has the primary interest in

the personal information. If it is the client - the consumer - who owns the 'right' in

their own personal information (and this would seem to be the direction in which

legislation is moving on both a federal and provincial level), then copyright in the

'Iist' is not entirely an asset. Interestingly, there is more than a passing similarity

between such intellectual capital assets and certain objects of copyright law. It

can be argued, for example, that the various property interests in personal infor-

mation mirror the disparate interests in a compilation and the difficulties that the

courts have had in determining where the copyright lies. 12 ln the case of cus-

tomer lists, personal information protection legislation increases the complexity if

this definition since there is an underlying privacy right which must now be con-

sidered in addition to deciding copyright issues.

Governance of employees and other human capital is also a critical factor in

the overall governance of intellectual capital. In fact, since intellectual capital is

not explicitly protected by legislation, the human capital of a firm (defined, in gen-

eral, as the 'people element') may be inherently difficult to govern. Firms never-

11 See B. von Tigerstrom, "Protection of Health Information Privacy: The Challenges and Possibilities of Technology" (1998) 4 Appeal 44 [hereinafter Tigerstrom]. See also E. Paton-Simpson, "Privacy and the Reasonable Paranoid: The Protection of Privacy in Public Places" (2000) 50 Univ. of Toronto L.J. 305. 12 See, for example, Index Téléphonique (N.L.) de Notre Localité v. Imprimerie Garceau Ltée, (1987) 18 C.I.P.R. 133 (Que. S.C.). With respect to finding copyright in a compilation or business directory, see also Tele-Direct (Publications) Inc. v. American Business Information Inc. (1997) 76 C.P.R. (3d) 296 (Fed. CA) aff'ing (1996) 113 F.T.R. 123 (T.D.).

9

theless try to assert a type of 'ownership interest' in their personnel or staff. This

interest is expressed in the contracts that employees may be obliged to sign prior

to employment. Non-Disclosure Agreements (NDAs) and Non-Competition

Clauses (NCCs) are currently the preferred methods of controlling human capital,

yet even these mechanisms have limits. The goal of this section is to clarify the

limits of such contracts, and the limits of the control that firms can exert over cur

rent and former employees in governing their intellectual capital.

The civil liability mechanism of intellectual capital governance - that is, the

ability to sue for damages for copyright, patent, or trademark infringement, and

for damages in contracts and tort - is the traditional governance mechanism.

From a market efficiency as weil as a legal perspective, recourse to civil liability

and corrective justice is not necessarily the most effective way to regulate and

protect intellectual property and capital. Indeed, in the case of trade secrets

quantifying damages is highly complex; potential damage is extremely difficult to

predict, even after a trade secret has been revealed. The goal of this section will

to be examine how the civil liability regime has either contributed to, or detracted

from, the effective regulation and protection of intellectual capital.

1.4.3 A Reconceptualization of Intellectual Capital Govemance

Finally, Chapter Four will attempt to determine if the current legal structure,

in a decentralized and disparate form, is adequate for the fair and practical gov

ernance of intellectual capital in the financial services sector. Such a determina

tion should be very useful insomuch as it should both shed light on any deficien-

10

cies that currently affect the system and allow for the proposition of a more robust

governance mechanism.

1.5 Applied Comparative Legal Methodology

There are three levels of comparison inherent in the structure of this thesis,

and each level will contribute to the primary goal of governance improvement.

First, there are the implicit comparisons between the diverse legal, jurispruden

tial, and economic regimes which currently govern intellectual property and capi

tal. Each of the above regimes will be examined from a legal, theoretical, and

public policy perspective in the hope of extracting the most attractive, useful, and

efficient governance mechanisms. In this sense the comparison is descriptive.

However, given the disparate regimes involved in this area of law, it is the result

of this descriptive comparison that may le ad to a system with fewer gaps and less

complexity. In the latter sense, the analysis is also prescriptive.

Second, the globalization of both the financial services industry and the

laws which govern intellectual property and capital internationally necessitate an

examination of multiple jurisdictions to determine the level of protection and the

general framework of that jurisdiction. To that end, regard will be had as to how

the American legal framework compares to the Canadian model. This compari

son will suggest areas of cross-pollination between both legislation and jurispru

dence; these similarities and differences will be highlighted in an effort to find the

best of both worlds.

The third and final area of implicit comparative legal methodology is be

tween the conception of 'what we have now' and 'what we could have'. In order to

11

make this comparison - to be able to draw from existing systems and establish a

better governance structure - it remains critical to understand not only the legal

jurisdictions and the legal regimes, but also how they interact. This final level of

comparison will turn on the clarity of the analysis of the individual systems them

selves.

This methodology is, by necessity, a synthetic work - that is, it draws from

numerous sources of law towards the creation and the establishment of a more

fluid, more adaptable, and more robust intellectual capital regulation and protec

tion regime. The ultimate hope is that this thesis will encourage further thinking

with respect to intellectual capital governance in the Canadian financial services

sector and the knowledge economy.

12

Chapter 2 Defining Terms in an Intellectual Capital Protection Regime

2.1 Introduction

The most appropriate way to delineate the 'object' of a governance frame-

work is by reference to what that regime controls and what it does not control. In

the knowledge-based economy in general, and the financial services sector spe-

cifically, it is crucial to define what the participants control and what they do not

control vis-à-vis that knowledge. Control may be based on a number of govern-

ance mechanisms: the common law and jurisprudence, for example, generally

govern the intangible intellectual assets of the financial services sector; con-

versely, legislation, regulations, and international law and treaties - black-Ietter

law - are the governance mechanisms for the more tangible intellectual assets.

This chapter will attempt to define, survey, and categorize the tangible and intan-

gible intellectual assets of financial services sector participants with a view to pro-

viding a sound foundation for analysing how these assets are controlled by cur-

rent legal regimes.

2.2 Intellectual Capital

Intellectual capital is not a term easily described - indeed, opinions vary

widely as to its precise meaning. In general, intellectual capital is defined as

knowledge that can be converted into profit.13 Stewart and Edvinsson have dis-

tilled and defined the resource further to include the following:

• The sum of an enterprise's: o collective knowledge, experience, skills, competences, and ability to

acquire more; o work outcomes, services and other intangible manifestations of the

application of these to the strategic intent of the enterprise;

13 Supra note 10

13

o relationships and processes that facilitate this application, its delivery of value to the marketplace, and its delivery of strategic advantage back to the enterprise.

• An enterprise's competences; the artefacts and measurements of its intangible resources; the capabilities and interactions of its formai organizations, informai communities, customers, and partners; and the knowledge, skills, and potential of its employees and other stakeholders.14

Arian Ward, of the Community Intelligence Labs, offers another definition when

she says that it can be defined as "Intangible material and relationships that have

been or could be formalized, captured, and leveraged to produce a higher-valued

asset.,,15 ln their intellectual capital management model, which will be addressed

in more detail in a later section, Zurich Insurance (one of the world's largest in-

surance companies) defines intellectual capital in their organization as "the com-

bination of human capital, social capital, structural capital, and customer capi

tal.,,16 This breakdown of the umbrella term 'intellectual capital' is useful because

it offers a more practical understanding of the way in which a financial services

firm understands its own intangible intellectual assets.

One final categorization of intangible knowledge assets is offered by

Lewison, of the Institute of Management and Administration. Referring to knowl-

edge management, he breaks the field down into:

1. Explicit knowledge, which is a company's collective documents, files, policies, procedures, and training (such as the general ledger). It is explicit because it is tangible and readily identifiable.

2. Tacit knowledge, which actually may be more important to a company, is the collective wisdom within a company of learned ways of doing things on

14 L. Edvinsson & M.S. Malone, Intellectual Capital: realizing your company's true value by finding its hidden brainpower (New York: HarperBusiness, 1997). 15 Arian Ward, "Definition of Intellectual Capital and Knowledge", online: http://www.co-iLcom/coil/knowledge-garden/ic/arianic.shtml (Last modified: 02/26/00). 16 Zurich Insurance Company, "Zurich Financial Services Group Corporate Brochure 2000", online: http://www.zurich.com/about zurichlintellectual capitaLjhtmL

14

the job, as weil as life experiences learned inside and outside the company, and the sharing of those experiences.17

Right away, it is easy to see how a legal/regulatory framework might have great

difficulty establishing a standard treatment for intangible intellectual assets in the

same way as for a tangible asset like real estate or equipment. In Carpenter v.

U.S., for example, a court upheld a newspaper's property right in prepublication

confidentiality and exclusive use of the information compiled by its reporters. 18

The fact that the United States Supreme Court conferred a property right in the

notion of confidentiality is indicative of the extent to which courts in various juris-

dictions have so far been willing to go in extending private property interests to

intangibles. It must be noted that, by virtue of the economic value of intellectual

capital, the ability to profit from an asset must be distinguished from the simple

property interest in that asset. This distinction is made in Théberge v. Galerie

d'Art du Petit Champlain Inc. where the Court cites Professor Gendreau:

Unfortunately, the present text of the Copyright Act does little to help the promotion of the fusion of moral rights with the economic prerogatives of the law, since there is no comprehensive definition of copyright that embodies both. Section 3 of the Act, which is drafted as a definition of copyright, only refers to the economic dimension of copyright. Moral rights are defined and circumscribed in entirely distinct sections. This absence of cohesion leads to the separate mention of "copyright" and "moral rights" whenever Parliament wants to refer to both aspects of copyright law and to the near duplication of the provision on remedies for moral rights infringements. 19

17 J. Lewison, "How to Use Knowledge Management to Gain a Competitive Edge" (2001) Managing the General Ledger - The Institute of Management and Administration at 4. 18 Carpenterv. United States, 484 U.S. 19 (1987). 19 Y. Gendreau, "Moral Rights" in G. F. Henderson, ed., Copyright and Confidentiallnformation Law of Canada (Scarborough, Ont. : Ca rswe Il , 1994) , 161, at p. 171. As cited in Théberge v. Galerie d'Art du Petit Champlain Ine. [2002] S.C.C. 34 at para. 59.

15

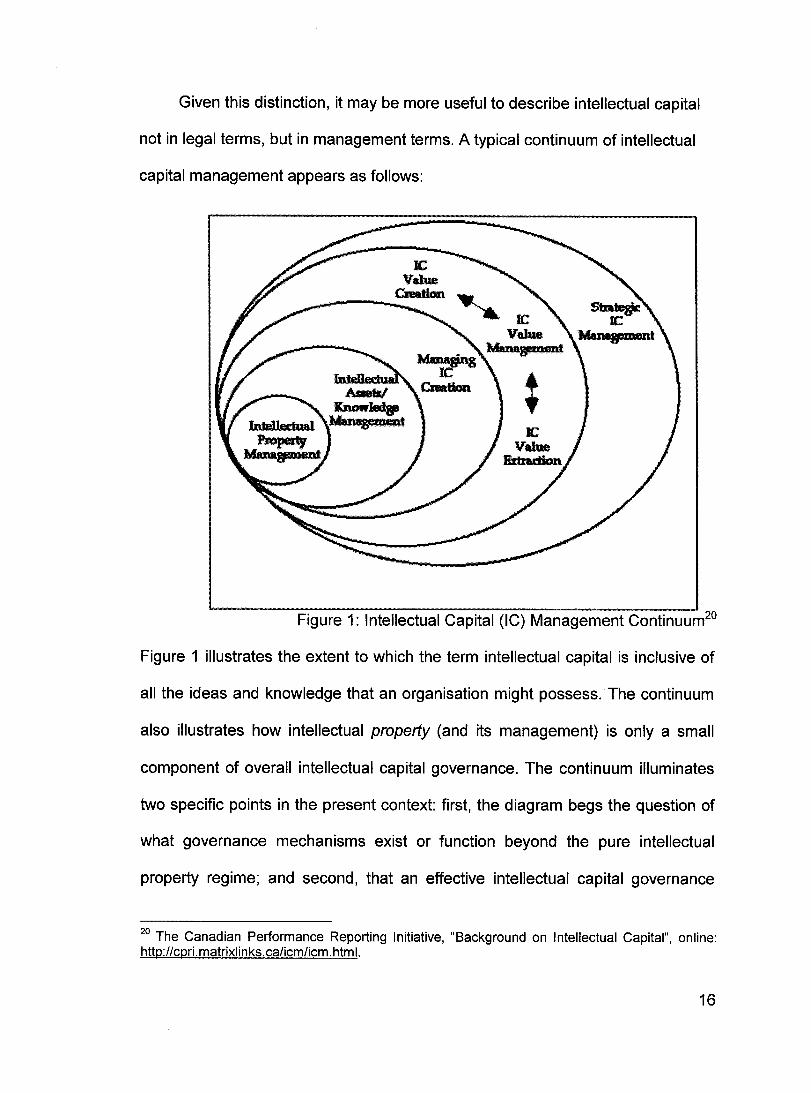

Given this distinction, it may be more useful to describe intellectual capital

not in legal terms, but in management terms. A typical continuum of intellectual

capital management appears as follows:

Figure 1: Intellectual Capital (IC) Management Continuum2o

Figure 1 iIIustrates the extent to which the term intellectual capital is inclusive of

ail the ideas and knowledge that an organisation might possess. The continuum

also iIIustrates how intellectual property (and its management) is only a small

component of overall intellectual capital governance. The continuum iIIuminates

two specifie points in the present context: first, the diagram begs the question of

what governance mechanisms exist or function beyond the pure intellectual

property regime; and second, that an effective intellectual capital governance

20 The Canadian Performance Reporting Initiative, "Background on Intellectual Capital", online: http://cprLmatrixlinks.ca/icmlicm.html.

16

framework requires the extension of sorne of theoretical underpinnings of the in

tellectual property regime. This thesis is, in part, an examination of the outer con

centric circles of the continuum, and an attempt to make sense of their govern

ance in light of existing legal treatments. In the financial services context specifi

cally, the question is what are the elements of intellectual capital that exist in

those outer rings, and how might they be legally classified in the absence of a

clear legal interest in, or treatment of, those elements?

2.2.1 The Zurich Insurance Model

The Zurich Insurance Group has broken intellectual capital down into four

subsets: human, social, structural, and customer capital. This breakdown is not

only useful fram a conceptual point of view, but also fram a legal point of view; to

a large degree, each of the subsets is governed by different legislation, regula

tion, and jurisprudence. The implication is that each subset may also have a dif

ferent interpretation of property rights and interests. In this model, it is human

capital that is the nexus for the other three subsets. In the context of the contin

uum in Figure 1, human capital forms a part of the outer three rings of the prac

ess. Financial capital (which refers to monetary inflow into an organization) is be

yond the scope of this analysis and as such, it can be assumed that an organiza

tion with the ability to leverage its intellectual capital - that is, its human and

structural capital - will have addressed the governance of its financial capital

elsewhere. For this thesis, the two most critical subsets are those of human and

structural capital, and each will be examined in turn.

17

2.2.1.1 Human Capital

One of the most important as sets that a financial services company draws

on is its people - its employees. A mutual fund management company, a bank,

or an investment company is based on the expertise that it can offer its clients.

Yet a company's personnel is not an asset in the traditional accounting or legal

sense of the word - it cannot easily be valued, and the law cannot easily affix

property rights or interests to it. It is, in the global sense, an almost limitless

spring, since ideas, knowledge and ability are not limited in the same sense as a

bank account or the sale value of equipment. In order to be able to protect this

fountainhead in a competitive and regulated market, a legal understanding of the

rights that attach to the 'asset' is imperative.

The way a financial services firm protects its rights to a person's mind is

generally focused on the product of that mind. That is work done in the course of

employment is generally considered to be the property of the employer. Ali as

pects of this relationship are usually governed by an employment contract which

stipulates that the product of an employees labour becomes the property of the

employer. However, the terms intellectual capital and human capital imply some

thing quite apart from ownership or property rights in the product of labour, and

establishing that characterization is more difficult because an individual em

ployee's ability, knowledge, and experience are intangible.

The motion judgment in TAL, for example, is an indication that a corpora

tion's 'ownership' of its personnel has limits and illustrates how employment law

and employment contracts can have a significant impact on the governance of

18

human intellectual capital. The judgment in TAL, which involved the enforceabil-

ity of the non-competition clause of an employment contract, ties the limits of

ownership to the potential for damage to the owner/corporation:

It appears to me that any damages which TAL may suffer by way of a loss of existing clients or business, as a result of Wai-Ping being employed by a competitor, can be quantified in monetary terms. The fact that it may be difficult to collect the necessary information and to do the calculation of such damages does not mean that they are damages which cannot be quantified in monetary terms. Damages resulting from a loss of potential new clients or business are, in my view, entirely based on speculation and do not satisfy the test of irreparable harm.21

Interestingly, the court in TAL cites the old case of Maguire v. Northland Drug

Company Limited, which established the original limits of a covenant in an em-

ployment contract. As Dysart J. stated in that case:

The practical question then is this, (1) what are the rights which the employer is entitled to protect by such a covenant, and (2) does the covenant not go beyond what is reasonably adequate in furnishing that protection. Proprietary rights, such as secrets of manufacturing pro cess and secret modes of merchandising, clearly come within the group of rights entitled to protection. So also is the right of an employer to preserve secret information ... (5). The information and training which an employer imparts to his employee become part of the equipment in skill and knowledge of the employee, and so are beyond the reach of such a covenant. .. The covenant in any event must not go further than is reasonably adequate to give the protection that is to be afforded [emphasis added].22

Despite their intangibility, these assets are valued differently for each employee

of a financial services firm. Variations in salaries and compensation packages

are often justified by the fact that the individual totality of a chief executive officer

is more valuable to a firm than that of a frontline customer service representa-

21 Supra note 6 at para. 10. 22 Maguire v. North/and Drug Company Limited (1935) S.C.R. 412 at 416.

19

tive. 23 Of course, higher compensation and responsibility within an organization

brings with it a higher degree of control over the employee or manager. That is,

the rights or interests that employers have in their employees and managers is

established by both contract and the common law. The judgment in Canadian

Aero Service Ltd. v. O'Malley4 was the first instance of this dut Y cum fiduciary

obligation. More recently, Felker v. Cunningham re-iterated the position of Cana-

dian law on the matter:

Since Canadian Aero it has been established law in Canada that high echelon managers and directors of an organization owe their employer a fiduciary obligation that transcends their implied dut Y of fidelity as a regular employee. Thus, an employee who stands in a fiduciary relationship to his or her employer has an equitable obligation of loyalty, good faith, honesty and avoidance of conflict of dut Y and selfinterest. The employee must act honestly, in ~ood faith and with a view to advancing the employer's best interests. 5

What is more, the governance of human capital - a company's employees,

personnel, and management - can be analogized to what amounts to a property

interest in that capital. This thesis argues in favour of finding this type of interest

because another characterization of the relationship, that of fiduciary duties,

does not do justice to the nature of intellectual capital. The strength of the prop-

erty-based analysis over the fiduciary duty-based analysis is that it accounts for

both the object and the relationship that are the component parts of intellectual

capital. Framing the relationship as simply a dut y, and not a dut Y with respect to

23 The Chairman & CEO of Toronto-Dominion Bank, for example, earned $1.3 million dollars in the year 2002. See 2002 Management Proxyllnformation Circular (25 February 2003), online: www.sedar.com. 24 Canadian Aero Service Ltd. v. O'Malley, [1974] S.C.R. 592. 25 Felkerv. Cunningham (2000) 191 D.L.R. (4th

) 734 (Ont. CA) at 739.

20

a parlicular object implicitly ignores the object itself. Lametti highlights the impor-

tance of this inclusive view when he writes that:

ln this understanding of property as both relationship and object, neither rights nor duties are prior to each other, as some rights or obligations may exist with specific resources but not with others. Of course, for most kinds of resources owners will have mainly rights and nonowners mainly duties, but recognizing the possibility of duties in rem for some resources is an important addition to a fuller understanding of this institution.26

Thus, the intellectual capital and the duties to which Lametti refers are

linked, and each is necessary in understanding the other. The proposed property

right in intellectual capital, unlike other more traditional property rights, is dy-

namic rather than static in nature, at least insomuch as it depends on the position

the employee holds or held within an organization. Further, the limits of this in-

terest, while initially created in contract, are subject to judicial scrutiny rather than

being enshrined in legislation or regulation. 27 As such they are effectively gov-

erned by common law. This effects-based approach to the limitation of the prop-

erty interest in human capital is cause for continued concern, as it permits for too

much uncertainty. The legal treatment and current protection of the pseudo-

property interest in human capital will be examined in more detail below in sec-

tion 3.5.

2.2.1.2 Structural Capital

Structural capital is a relatively new concept in the literature of business

management. Avramovich describes it as follows:

26 D. Lametti, "The Concept of Property: Relations through Objects of Social Wealth" (July, 2003) U. of T. L.J. [forthcoming]. 27 A notable exception to this observation, in the Canadian context, is section 122(1) of the Canada Business Corporations Act, R.S.C. 1985, c. C-44, as am.

21

Structural capital is a firm's organizational capabilities for meeting market requirements. It involves the organization's routines and structures that support employees' quests for optimum intellectual performance ... Structural capital allows intellectual capital to be measured at an organizational level. 28

As a general rule, structural capital refers to the physical and infrastructure sup-

port that financial services firms provide to their human capital - their employees

- in order to maximize their potential and take advantage of their knowledge and

skills. InteliectualCapital.org describes structural capital, paradoxically, as "tangi

ble intangibles,,29 such as product documentation databases, market analysis

models, and any of a myriad of other documentary-type assets. Such capital,

since it exists in a very real sense, is more conducive to categorization and, im-

plicitly, legal protection. While this remains a common-sense and straightforward

management definition of this type of intellectual capital, as a category for legal

and judicial treatment it is virtually ignored.

This situation begs the questions of if and how the component parts of

structural capital are defined in law. A closer examination reveals a thoroughly

inconsistent definition of what constitutes this subset of intellectual capital. Much

like the legal definition of human capital, structural capital is dependent on the

physical manifestation of that asset. Further, even physical, tangible manifesta-

tions remain legally ill-defined in certain cases. For example, to the extent that

such tangible intangibles can be shoe-horned into the definition of copyrightable

material in the Copyright Act, they are defined by necessity. An internai proce-

28 M.P. Avramovich, "The Protection of Internationallnvestment at the start of the twenty-first century: Will anachronistic notions of business render irrelevant the OECD's Multilateral Agreement on Investment?" (1998) 31 J. Marshall L. Rev. 1201 at 1274. 29 InteliectualCapital.org, "Exploring Intellectual Capital", online: http://www . i ntellectu alcap ital. org/intelcaplindex. htm 1.

22

durai guide or software library, for example, would fall under the definition of "Lit-

erary Work" as it appears in the Copyright Act, which "includes tables, computer

programs, and compilations of literary works."30 Patent, trade secret, and confi-

dential information law may also govern, at least in part, such structural capital.

The decision in Apple Computer Inc. V. Mackintosh Computers Ltd., for example,

affirms that the form of a literary work is irrelevant to its being covered by the

Copyright Act.31 Thus, legally speaking, this type of structural capital seems to be

nothing more than a literary work or computer programs as defined by legislation,

and the property interest vests in the author organization. Other aspects of struc-

tural capital, however, are not so amen able to having a property right or interest

attached.

ln the knowledge economy, one of the fundamental elements of structural

capital is a financial service company's client lists and files. While these lists may

only exist in customer relationship management software - that is in digital format

on an organization's systems - they quite clearly forms part of the structural capi-

tal. The ownership and property interest in the customer information contained in

these databases, however, is far more convoluted, as it involves a property inter-

est in information. The protection and regulation of personal information neces-

sarily imports questions dealing with the right of privacy. Interestingly, discussion

of the right to privacy has always used the language of property rights and, even

30 Supra note 7 at s. 2. 31 App/e Computer, Inc. V. Mackintosh Computers Ltd., [1988] 1 F.C. 673 (CA), aff'd [1990] 2 S.C.R. 209. See also Accusoft Corp. v. Pa/o, 923 F. Supp. 290; 1996 (U.S. Dist.), aff'd in part 237 F.3d 31, 2001 (U.S. App.).

23

in their differentiation from private property rights, legal scholars and jurists alike

employ what amounts to 'possessory' language.

Morgan, in a discussion of the expectation of privacy vis-à-vis electronic

mail, writes that:

[I)nformational privacy [has) come to be notionally distinguished from the concept of ownership over time. Rather than finding [a) basis in property rights, doctrinal writers, courts, and legislators in the United States and Canada have ail come to hold that the right of privacy is a "personality right". The very nature of a personality right is that it is held by everyone and that it cannot be alienated. It is extra-patrimonial. It is in part for this reason that it is inappropriate to suggest that ownership rights negate privacy rights. The two kinds of rights are each of a different nature; they overlap, they are not mutually exclusive.32

ln this sense, then, the notion of ownership of a database of customer informa-

tion, the property and ownership interest in which is protected by the Copyright

Act, is subordinate to an individual's right to the privacy of his or her personal in-

formation. The recently enacted Personal Information Protection and Electronic

Documents Acf3, a federal statute that addresses precisely this issue, requires

the consent of an individual for the collection, use or disclosure of personal infor-

mation. The statute appears to parallel Warren and Brandeis, who wrote of the

right of privacy that "[t)he rights, so protected, whatever their exact nature, are not

rights arising from contract or special trust, but are rights against the world;

and ... the principle which has been applied to protect these rights is in reality not

the principle of private property ... [but rather) the right of privacy.,,34

32 C. Morgan, "Employer Monitoring of Employee Electronic Mail and Internet Use" (1999) 44 McGiII L.J. 849 at 855. 33 Personallnformation Protection and Electronic Documents Act, R.S.C. 2000, c.5, s. 5 et seq. 34 S. Warren & L. Brandeis, "The Right to Privacy" (1890-91) 4 Harv. L. Rev. 193 at 213.

24

This brief introduction to privacy and personal information can be further

distilled: first, there is certainly a property interest in the compilation and collec-

tion of personal information - information that forms the structural capital of a fi-

nancial services organization; second, the right to privacy that resides in the

communication of personal information and - and the consent to that communi-

cation and collection - appears to outweigh the property interest he Id by the or-

ganization; third, that despite this trump card having many of the hallmarks of

property, it appears to have, per Warren and Brandeis, an even more inviolable

status as a 'personality right'; and finally, if the privacy right trumps the property

interest in personal information (and thus in structural capital), an organization's

assets can lose significant value.

It is the characterization of the right or interest in personal information that

results in the overlap of interests in that information. In this respect, it is useful to

examine the civil law concept of personality rights - rights which are attached to a

person and are 'extrapatrimonial'. In the Civil Law framework, these are rights

which cannot be detached from the individual. Deleury and Goubau describe

them as follows:

Ils sont intransmissibles, c'est-à-dire qu'ile s'éteignent avec la mort de la personne et ne passent pas, en principe, aux héritiers. Parce qu'ils ne mettent en jeu des intérêts d'ordre moral, donc non susceptibles d'évaluation pécuniare, ils échappent à l'emprise des mécanises économiques. Ils sont par le fait même incessibles: ils ne peuvent faire l'objet d'une convention, d'une cession ou d'une renonciation. N'ayant pas «d'attache matérielle et ne constituant pas des biens économiques», les droits de la personnalité sont également insaissisables. C'est pourquoi on dit généralement qu'ils sont hors com-

25

merce. Enfin, ce sont des droit imprescriptibles: le seul écoulement du temps ne peut entraîner la perte du droit.35

The problem in the case of the right of privacy and les droits extrapatrimoniaux is

that the reality of the knowledge economy is such that personal information as

described by both Warren and Brandeis and Deleury and Goubau does now

have economic value, and is valuable property. Declaring, therefore, that the pri-

vacy or extrapatrimonial right implicit in that personal information is sufficient to

establish a primacy of interests is false. Deleury and Goubau admit this weak-

ness in their characterization of personality rights, even admitting that in the

commercial context "ces droits peuvent donc, en quelque sort, se dédoubler,

pour comporter, à l'instar des droits d'auteur, un véritable caractère commercial,

à côté du droit extrapatrimonial. Le nom lui-même, lorsqu'il sert au ralliement

d'une clientèle commerciale, devient l'objet d'un véritable droit de propriété. ,,36 If

one accepts Deleury and Goubau's view, then, the civillaw has alreadyascribed

a property interest to an individual's name, creating a hybrid interest. This hybrid

property interest may be useful in a re-conceptualization of the property in per-

sonal information in the common law (see below, section 3.4).

If a bank, for example, wishes to spin off a subsidiary to deal with credit

cards currently held by its customers, the customer database (containing, per-

haps, the personal information of millions of individuals) would be valueless with-

out the required consent. Suddenly the structural capital, with its inherent poten-

tial to create profit is, for ail intents, handcuffed. The need for a more complete

35 E. Deleury & D. Goubau, Le Droit des Personnes Physiques (Montréal: Éditions Yvon Blais, 1994) at 72. 36 Supra note 35 at 74 [emphasis added].

26

definition of property in personal information is neatly outlined by Onyshko and

Owens, who wrote that

While the value of tangible property was a result of the ability of its owner to physically exclude others from possession, a single piece of information may be fully possessed by many different parties at the same time. In addition, there is a legitimate need for the circulation of sorne types of information about individuals; for example, information is necessary for government and business to make informed decisions about the treatment of individuals. Thus, there is a need for a more flexible conception of privacy.37

ln respect of financial services companies and their structural capital, there is a

very pressing need to re-examine the property interest in personal information.

This re-examination may ultimately result in an acceptance of a business reality

over an outdated legal fiction. As Douglas Adams put it "Even the sceptical mind

must be prepared to accept the unacceptable when there is no alternative. If it

looks like a duck, and quacks like a duck, we have at least to consider the possi

bility that we have a sm ail aquatic bird of the family Anatidae on our hands.,,38

2.3 Infellecfual Property

As the continuum in Figure 1 and the components of the Zurich Model iIIus-

trate, pure intellectual property is only a small component of the treatment of in-

tellectual capital in a financial services firm. In the financial services context,

however, intellectual property can nevertheless form the backbone of a com-

pany's business. Copyright law, for example, will protect ail literary works that an

investment firm produces for sale or for its clients. A bank or mutual fund com-

pany may own patents for business methods that are tangible insofar as they ex-

37 T.S. Onyshko & R.e. Owens, "Debit cards and stored value cards: legal regulation and privacy concerns" (1997) 16 Nat'I Banking L. Rev. 65. 38 D. Adams, Dirk Gent/y's Holistic Detective Agency, (New York: Simon and Schuster, 1987) at 216.

27

ist as computer programs being used in the context of business. The U.S. recent

case of State Street Bank & Trust Co. v. Signature Financial Group, Inc. 39, for

example, "established the viability of the current patent system as a vehicle to

protect software-related intellectual property.,,40 Financial services companies

also rely on legislative and regulatory protection for their trademarks41 and trade

secrets. This last is used to a certain extent in the protection of intellectual assets

and capital as they have been described above. To the extent that there is a well-

established, coherent, and consistent standard which has emerged in the treat-

ment of the property rights in intellectual assets, it is sufficient to say that, in con-

trast to the legal status of intellectual capital, intellectual property - in ail its vari-

ous forms and permutations - is weil defined. This is because while human capi-

tal - that is, the knowledge, experience, and skill that has the pofenfial to create

profit - is not weil defined in legal terms, the product of human capital is weil de-

fined and delineated by law. Given the established body of law that defines intel-

lectual property in the financial services sector, only the aspects of that regime

which relate to intellectual capital governance will be examined in more detail.

2.4 Conclusion

This chapter has attempted to outline the legal, as opposed to lay, defini-

tions of the various components of intellectual capital. As the investigation shows,

there are significant problems with the governance of intellectual assets that can-

39 State Street Bank & Trust Co. v. Signature Finaneial Group, Ine., 149 F.3d 1368, 1998 (U.S. App.). The case was concerned with whether the transformation of data through particular mathematical algorithms was a practical application eligible for patent protection on grounds of utility. It should be noted that the effects of this judgment are still being debated. 40 C. King, "Abort, Retry, Fail: Protection for software-related inventions in the wake of State Street Bank & Trust Co. v. Signature Finaneial Group, Ine." (2000) 85 Cornell L. Rev. 1118 at 1120. 41 Trade-marks Act, R.S. 1985, c. T-13.

28

not be qualified or defined as pure intellectual property. Further, even in cases

where an asset can adequately be defined as intellectual property, and the prop

erty interest established (as is the case for databases of personal information),

there remain unresolved issues with respect to the component parts of that prop

erty. Unless they can be resolved in the creation of standard legislative and judi

cial treatments of such hybrids, these inconsistencies threaten to upset the foun

dations of the information and knowledge economies. Chapter Three will ad

dress, in more detail, how current legal regimes have treated the components of

intellectual capital, including the human and structural subsets defined above and

will attempt to uncover a theoretical and practical foundation for a shift in the in

tellectual capital governance framework as a whole towards a property based

conception of this valuable resource.

29

Chapter 3 Current Legal Regimes

3.1 Introduction

The importance of intellectual capital governance lies in the fact that such

intellectual capital and intellectual property is in large part how the marketplace

values a company. Chapter Three will examine in more detail how current legal

regimes can and do govern the intellectual property and intellectual capital that

very often forms the backbone of a corporation's competitive viability. As Edvins

son says, U[w]hat is the true value of a company ... it is more than the tangible as

sets; the company's value is in its intangible intellectual assets as weil as its abil

ity to convert those assets into revenues.,,42 The purpose of this section is not to

present an in-depth method for the valuation of intangible intellectual assets -

that is a task better left to scholars and practitioners in the field of financial analy

sis. 1 nstead , the focus here is on how 'knowledge firms' - an economic sector

that includes financial services firms - have governed and can govern those core

elements of their business which, while intangible, are critical to economic suc

cess.

Chapter Two laid the framework of the elusive legal definitions towards

which the present argument progresses. This chapter, which builds a broad but

nevertheless detailed model of the various building blocks of a corporation's intel

lectual capital foundation, hopes to provide a more comprehensive survey and a

more robust understanding of those blocks. The four broadly defined legal re

gimes most responsible for intellectual capital governance in the financial ser

vices sector are examined here. The reader should recall that the intellectual

42 Supra note 14 at 356.

30

capital management continuum (Figure 1) and the Zurich Insu rance Model list

human capital and structural capital as the two key components of intellectual

capital. These models are based not in the principles of legal analysis but in the

practice of corporate management. The two categories can nevertheless be ex-

amined from a legal perspective and deconstructed to that end. Such an analysis,

however, requires the adoption of a goal beyond that of simple asset valuation.

Instead of valuing an intangible asset in monetary terms, this analysis values an

intangible asset from what might be termed the governance perspective. From

within the latter framework, structural and human capital can be pigeonholed into

the legal regimes mentioned above, and their value ascertained beyond simple

cash value on a balance sheet. The sections that follow are a comprehensive re-

view of how each legal regime creates value for intellectual capital via their effec-

tive governance and a shifting mentality with respect to the property interests in

intellectual capital.

3.2 Intellectual Property in the Intellectual Capital Context

The broad category of intellectual capital necessarily includes the more

specific notions of intellectual property (copyright, patent and trademark). Note

that while trade secret is considered a part of intellectual property, it is treated

separately in the intellectual capital context. The crucial problem with applying a

tradition view of intellectual property to the more ephemeral conception of intel-

lectual capital, however, is precisely the latter's lack of concreteness. This di-

lemma, from a management perspective, is pointed out by 8ertels and Savage:

Typically assets are recognized items of worth. We count our assets on our balance sheet, we put asset numbers on machinery

31

and we recognize that these assets depreciate. As we move into the knowledge era we are faced with more than just things. Ideas begin to take on major business significance. Yet, we hardly know how to put asset numbers on them, unless they be patents or trademarked items.43

From a legal perspective, this appears to be a non sequitur given the

idea/expression dichotomy in copyright law (or the analogous science/applied

science dichotomy in patent law), but it nevertheless speaks to the fallibility of the

current system. Copyright law, for example, is far more comfortable in the domain

of the tangible than in the uncharted waters of the intangible and, as such, has

traditionally concerned itself with the 'fixation' of a work or expression. There is

increasing recognition that fixation is no longer the necessity that it once was.

Vaver notes that though "The [Copyright1 Act nowhere specifies that fixation is a

general condition of protection ... [a]lIowing some flexibility on the fixation issue

may nevertheless sometimes be beneficial.,,44 Intellectual capital, however, can-

not neatly be fit into the traditional intellectual property categories, and not ail in-

tellectual property rights can be analogized. As Vaver states elsewhere,

[n]ot ail intellectual property rights can technically be called property. Even those that can may not everywhere have ail the usual attributes of property ... in short, we can talk about intellectual property as we talk about military intelligence: as useful shorthand for a phenomenon, but with no implication that its components - intellectual or property - do or should exist.45

The same conception of the dichotomy between what something appears to

be and what the law says it is can be found again with reference to busi-

43 T. Bertels & C.M. Savage, "Understanding knowledge in organizations" in G. von Krogh, J. Roos & D. Kleine, eds., Knowing in Firms: Understanding, Managing and Measuring Knowledge iLondon: SAGE Publications, 1998) at 9 [hereinafter von Krogh).

4 D. Vaver, Copyright Law (Toronto: Irwin Law, 2000) at 63. 45 D. Vaver, Intellectual Property Law (Toronto: Irwin Law, 1997) at 5.

32

ness/management theory. Marchand writes that "although knowledge and infor-

mation are often used interchangeably, most managers and scholars recognize

that knowledge is different from but directly linked to information.,,46 Marchand's

ideas in this area, however, neatly parallel the classical idea/expression dichot-

omy in copyright law. His hypothesis relates to the similar dichotomy of knowl-

edge versus information, but not in purely legal terms. If illustrated graphically

(see Figure 2, below) the cross-pollination becomes far clearer:

K Id nowe Ige to n orma Ion 1 f f

T acit to tacit T acit to explicit

Knowledge Information transfer A person transfers between people knowledge through (conversation) documents, messages,

data from

Explicit to tacit Explicit to explicit

Information Documents, data, mes- Information about infor-sages mation: documents, data,

Convey meaning to a per- messages are organized son into indexes, maps, rules

and repositories

Figure 2: Converting Knowledge to/from information47

A close examination of the components of this table reveals a clear parallel of the

dichotomy facing the underlying theory of much of copyright law in particular and

intellectual property law in general.48 This pola rit y is expressed by an English

court in, for example, Moreau v. St. Vincent:

46 DA Marchand, "Competing with Intellectual Capital" in von Krogh supra note 43 at 255. 47 Supra note 46 at 256. 48 Though the central hypothesis of this thesis is grounded in the view that the protection of intellectual capital will necessitate a re-evaluation of both law and business practice as regards the

33

It is ... an elementary principle of copyright law that an author has no copyright in ideas but only in his expression of them. The law of copyright does not give him any monopoly in the use of the ideas with which he deals or any property in them, even if they are original. His copyright is confined to the literary work in which he has expressed them. The ideas are public property, the literary work is his own. Every one may freely adopt and use the ideas but no one may copy his literary work without his consent.49

What is both interesting and problematic with the 'rights-based' discourse is that,

at least in the context of the valuation of knowledge-based companies such as

financial services firms, it has so far been obscenely difficult - and infinitely sub-

jective - to value rights as opposed to property. As Srooking points out,

Twenty years ago, we weren't bothered with intellectual capital. Its emerging importance reflects the organization's increasing dependence on intangible assets. New types of companies are born every day which have only intangible assets. Their products are intangible and can be distributed electronically in the 'market space' via Internet.50

How, then, can the need of knowledge-based businesses to value what

does not exist be reconciled with an intellectual property regime that does not

address the character of a business' most valuable asset? The business com-

munit y seems to have answered this question pragmatically through the liberal

use of the phrase 'ail rights reserved'. Intellectual property scholars and practitio-

ners commonly refer to only the right to exclude - that is, to the legislated mo-

nopoly that intellectual property laws create from thin air. They are, to a degree,

perfectly right. The Copyright Act, for example, states that:

so-called 'rights-based' interpretation of, for example, copyright law, it is nevertheless necessary to understand the opposition to this view. See, for example, A. Drassinower, "A Rights-Based View of the Idea/Expression Dichotomy in Copyright Law" (2003) 16 Cano J.L. & Jur. 3. 49 Moreau V. St. Vincent[1950] Ex. C.R. 198 at 203. 50 A. Brooking, Intellectual Capital: Core Asset for the Third Millennium Enterprise (London: International Thomson Business Press, 1996) at 17.

34

For the purposes of this Act, "copyright", in relation to a work, means the sole right to produce or reproduce the work or any substantial part thereof in any material form whatever, to perform the work or any substantial part thereof in public or, if the work is unpublished, to publish the work or any substantial part thereof ... 51

The Patent Act is also concerned with the rights of the patentee to control his or

her invention. Section 42 of the Patent Act states that: