insurance claims (risk management)

TRANSCRIPT

HEALTH INSURANCE

What is individual policy?Your health is precious to you - it enables you to live your life the way you please. But a sudden illness or accident can put a stop to your way of living and empty your savings. Protect yourself with Individual Health Guard - an all-round policy that covers you against medical expenses including hospitalization, in the event that you fall ill or have an accident. Now you don't ever have to worry about not having enough money for treatment in case things go wrong.

INDIVIDUAL POLICY

What are the coverage's?

• ALL medical expenses can be covered for individual benefit.• It covers many hospitals where you can do cashless claim.• It covers many types of critical diseases: Cataract (limited to 20,000 per eye) Lithotripsy Tonsillectomy Eye Surgery Dialysis Dilatation & Curettage Chemotherapy Radiotherapy Coronary Angiography Cardiac Catheterisation• Also covers OPD charges - Cover Room, Boarding Expenses as charged by the Hospital

Nursing Expenses Expenses related to Dental Treatment Surgeon, Anaesthetist, Medical Practitioner, Consultants, Specialist Fees Anaesthesia, Blood, Oxygen, Operation Theatre Charges, Surgical Consumables, Medicines and Drugs, Diagnostic Materials and X-ray, Dialysis, Chemotherapy, Radiotherapy, Cost of Pacemaker, Cost of Artificial Limbs External Medical Aids, Dental treatment charges, Ambulance charges etc.

• Pre-existing diseases can be covered after three continuous years of coverage withthe Company.

• Policies are covered subjected to terms & conditions.

Exclusions ?Some of the disease can only be covered after 2 years from the date of policy taken. The disease are following:• Cataract (limited to Rs 20,000 per eye)• Benign Prostatic Hypertrophy• Myomectomy, Hysterectomy unless because of malignancy• Hernia, Hydrocele• Fistula in Anus, Piles• Arthritis, Gout, Rheumatism• Joint replacement, unless due to accident• Sinusitis and related disorders• Stone in the urinary and biliary systems• Dilatation & Curettage• Skin and all internal tumors / cysts / nodules / polyps of any kind, including breast

lumps, unless malignant / adenoids and hemorrhoids• Dialysis required for chronic renal failure• Surgery on tonsils and sinuses• Gastric and duodenal ulcers• Deviated Nasal Septum

• Any disease contracted during the first 30 days of commencement of the policy will be excluded from coverage.

• Cosmetic, aesthetic or related treatments will not be covered.• Joint replacement surgery (other than due to accidents) shall have a waiting period of

4 years before it is covered.• All external equipments such as contact lenses, cochlear implants etc. will not get

covered.

Eligibility ?• Entry age for proposer is 18 years to 65 years. The policy can be renewed up to 80

years.• Children aged 3 months to 25 years can be covered under this policy.

Procedure for hospitalization ?Immediately on Hospitalization or within twenty four hours of such Hospitalization, please intimate the company or TPA of this fact, with details of Your Policy Number, Name of the Hospital and treatment undertaken. This is an important condition of the Policy that you need to comply with.

Key benefits… • Covers Outpatient Department (OPD) expenses, such as diagnostics tests, dental

treatment, medical bills, ambulance charges, etc.• Avail Cashless Claim facility at over 4,000+ network hospitals across India (Tip - Simply

use your Health ID card at any of our 4,000+ network hospitals and avail cashless service, a boon for those times when you need finance the most.)

• No sub-limits on room rent, doctor fees, and hospital charges or for any disease (Tip -Sub-limit means any limit or restriction put on the Sum Insured available for any treatment/ service/ disease/ covered under the policy. For example, a health policy may have sub-limits of 1% of Sum Insured on the Room rent on a per day basis, or a sub limit of 25% of Sum Insured on Doctor's fees. Sub-limits can be applied on the entire treatment of one illness, like Heart diseases may have a sub-limit of Rs. 50,000, i.e, a maximum of Rs. 50,000 can be claimed for the heart disease treatment)

• No co-payments for any disease or any Hospitalization expenses (Tip - Co-payment means a certain percentage of every claim amount which has to be borne by the insured person. For example a health policy may have co-pay of 20% on hospitalization expenses taken in a non network hospital then he will have to bear 20% of such claim amount out of his own pocket.

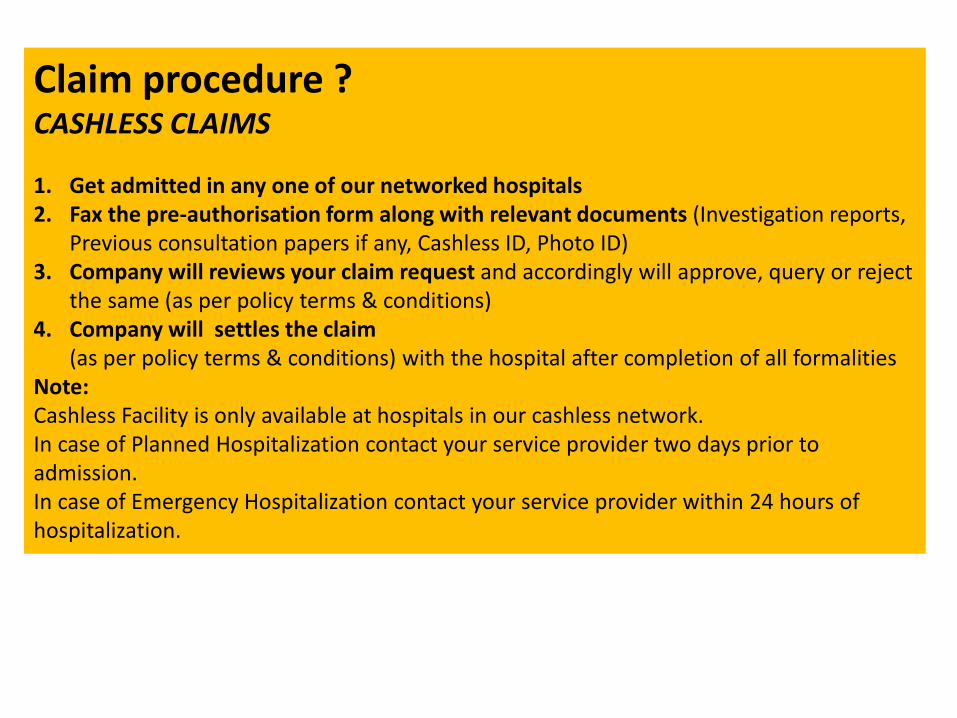

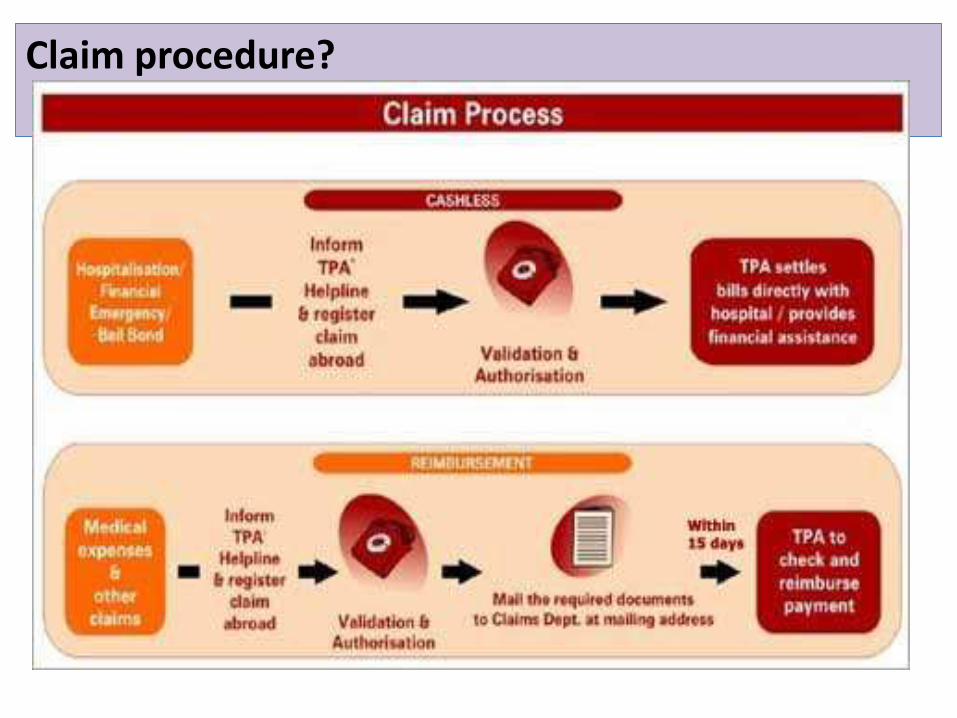

Claim procedure ?CASHLESS CLAIMS

1. Get admitted in any one of our networked hospitals2. Fax the pre-authorisation form along with relevant documents (Investigation reports,

Previous consultation papers if any, Cashless ID, Photo ID)3. Company will reviews your claim request and accordingly will approve, query or reject

the same (as per policy terms & conditions)4. Company will settles the claim

(as per policy terms & conditions) with the hospital after completion of all formalitiesNote:Cashless Facility is only available at hospitals in our cashless network.In case of Planned Hospitalization contact your service provider two days prior to admission.In case of Emergency Hospitalization contact your service provider within 24 hours of hospitalization.

REIMBURSEMENT CLAIMS1. Upon discharge, pay all hospital bills and collect all original documents of treatments

and expenses undergone2. Mail the duly filled (and signed by insured and treating doctor) claim form and required

documents to your service provider (Company or TPA)3. Company will reviews your claim request and accordingly will approve, query or reject

the same (as per policy terms & conditions)4. Company will settles the claim

(as per policy terms & conditions) and reimburses the approved amount.

OTHER’S TPA1. Get admitted in any one of the TPAs networked hospitals2. Fax the pre-authorisation form along with relevant documents (Investigation reports,

Previous consultation papers, Cashless ID, Photo ID)3. Your service provider reviews your claim request and accordingly will approve, query or

reject the same4. Your service provider settles the claim

(as per policy terms & conditions) with the hospital after completion of all formalities.

OPD claim procedure…Documents required1. The Insured shall be required to furnish the following documents in original for or in

support of a claim:2. Duly completed OPD claim form3. Discharge Card (if applicable) or OPD card of the Hospital4. Prescription of the treating Medical Practitioner, bills, receipts, etc.5. Bills from chemists supported by proper prescription6. Test reports and payment receipts7. Any other document as required by the Company

Payment of Claims• Claims pertaining to each Insured can be lodged only once during the Period of

Insurance• The Company shall not receive any claims prior to completion of 90 days of the

commencement of the Policy• Claims under OPD Benefit shall be payable only on re-imbursement basis• No claim shall be admissible under OPD Benefit 30 days after expiry of the Period

of Insurance• OPD HAP claims will be settled in 10 working days for cases where all the

required documents have been received

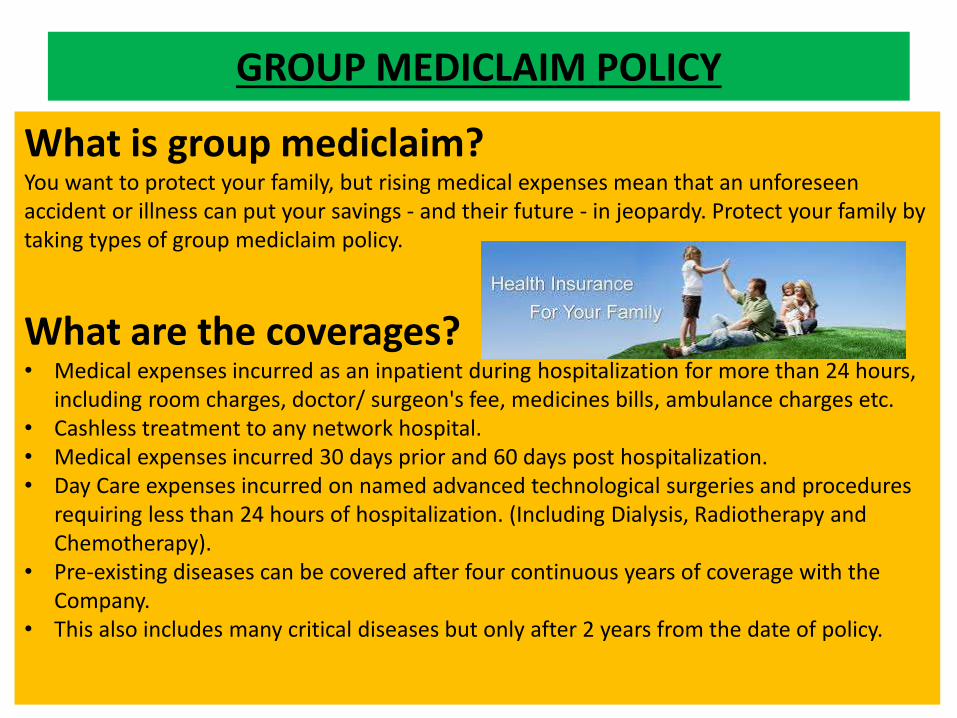

GROUP MEDICLAIM POLICY

What is group mediclaim?You want to protect your family, but rising medical expenses mean that an unforeseen accident or illness can put your savings - and their future - in jeopardy. Protect your family by taking types of group mediclaim policy.

What are the coverages?• Medical expenses incurred as an inpatient during hospitalization for more than 24 hours,

including room charges, doctor/ surgeon's fee, medicines bills, ambulance charges etc.• Cashless treatment to any network hospital.• Medical expenses incurred 30 days prior and 60 days post hospitalization.• Day Care expenses incurred on named advanced technological surgeries and procedures

requiring less than 24 hours of hospitalization. (Including Dialysis, Radiotherapy and Chemotherapy).

• Pre-existing diseases can be covered after four continuous years of coverage with the Company.

• This also includes many critical diseases but only after 2 years from the date of policy.

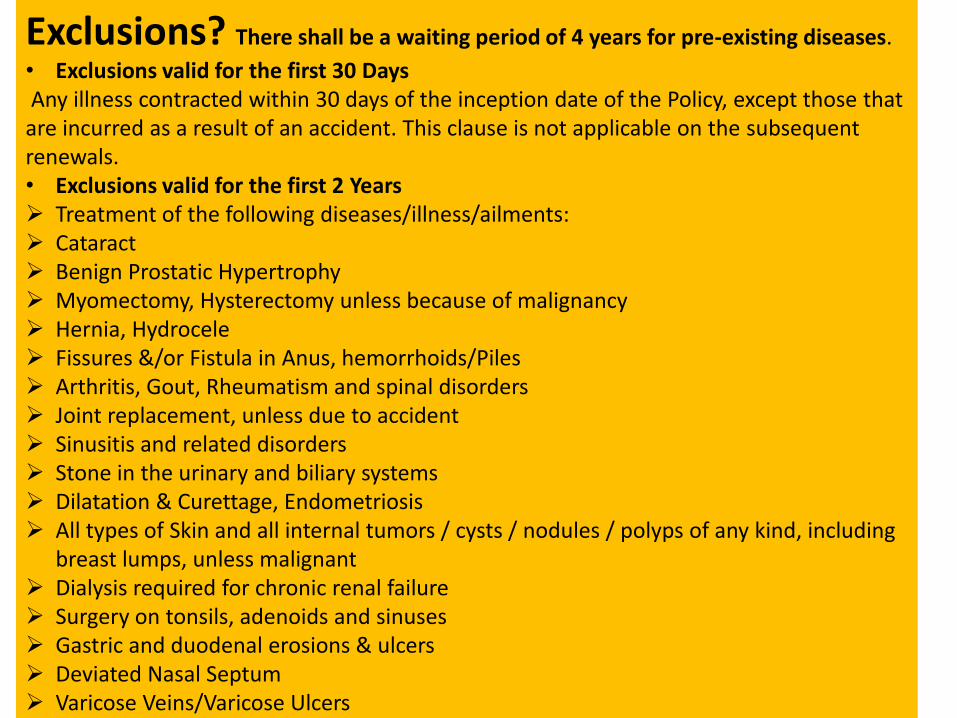

Exclusions? There shall be a waiting period of 4 years for pre-existing diseases.

• Exclusions valid for the first 30 DaysAny illness contracted within 30 days of the inception date of the Policy, except those that

are incurred as a result of an accident. This clause is not applicable on the subsequent renewals.• Exclusions valid for the first 2 Years Treatment of the following diseases/illness/ailments: Cataract Benign Prostatic Hypertrophy Myomectomy, Hysterectomy unless because of malignancy Hernia, Hydrocele Fissures &/or Fistula in Anus, hemorrhoids/Piles Arthritis, Gout, Rheumatism and spinal disorders Joint replacement, unless due to accident Sinusitis and related disorders Stone in the urinary and biliary systems Dilatation & Curettage, Endometriosis All types of Skin and all internal tumors / cysts / nodules / polyps of any kind, including

breast lumps, unless malignant Dialysis required for chronic renal failure Surgery on tonsils, adenoids and sinuses Gastric and duodenal erosions & ulcers Deviated Nasal Septum Varicose Veins/Varicose Ulcers

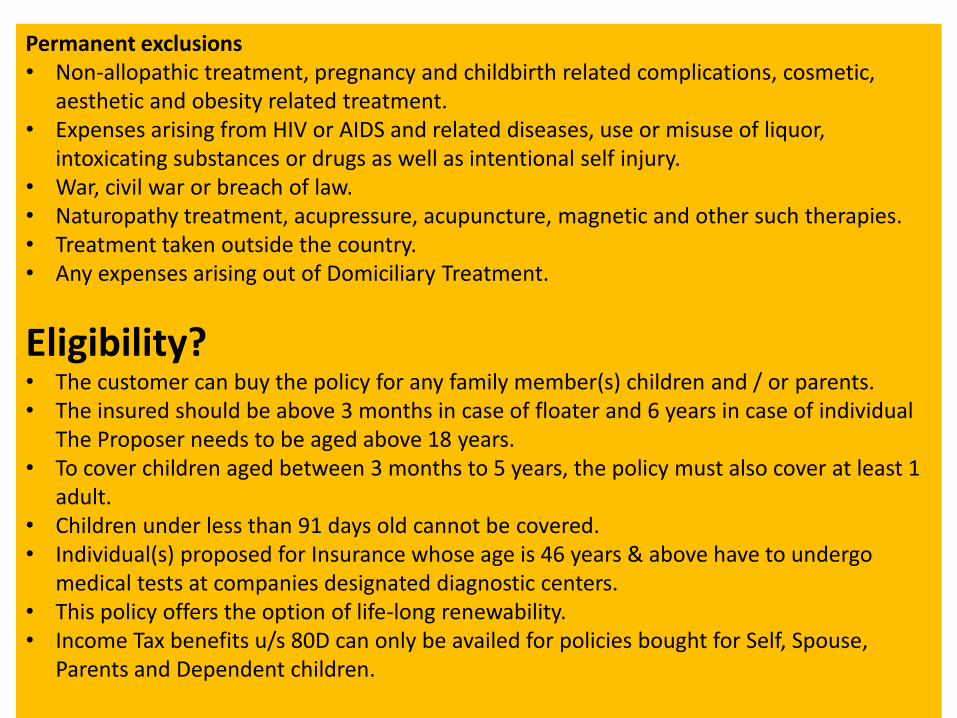

Permanent exclusions• Non-allopathic treatment, pregnancy and childbirth related complications, cosmetic,

aesthetic and obesity related treatment.• Expenses arising from HIV or AIDS and related diseases, use or misuse of liquor,

intoxicating substances or drugs as well as intentional self injury.• War, civil war or breach of law.• Naturopathy treatment, acupressure, acupuncture, magnetic and other such therapies.• Treatment taken outside the country.• Any expenses arising out of Domiciliary Treatment.

Eligibility?• The customer can buy the policy for any family member(s) children and / or parents.• The insured should be above 3 months in case of floater and 6 years in case of individual

The Proposer needs to be aged above 18 years.• To cover children aged between 3 months to 5 years, the policy must also cover at least 1

adult.• Children under less than 91 days old cannot be covered.• Individual(s) proposed for Insurance whose age is 46 years & above have to undergo

medical tests at companies designated diagnostic centers.• This policy offers the option of life-long renewability.• Income Tax benefits u/s 80D can only be availed for policies bought for Self, Spouse,

Parents and Dependent children.

Key benefits…

• Coverage up to Rs. 10 Lac. Multiple sum insured options• Get policy renewal facility for life time• No medical test required for policy holders below 46 years of age • No sublimit. But you can choose sublimit option as you please.• Cumulative bonus of 5% to your Limit of Indemnity for every claim free year.• 5% cumulative bonus benefit for each claim free year, maximum up to 50%. cumulative

bonus would be passed for sum insured Rs.2,00,000/- and above continuously renewed with us.

• No medical tests up to 45 years, subject to clean proposal form. • Medical tests (pre-policy check-up) are mandatory for members aged 46 years and above.• The pre-policy check up would be arranged at our empanelled diagnostic centers. • 100% cost of pre-policy check-up would be refunded if the proposal is accepted and

policy is issued. • In case the member opts for hospitals besides the empanelled ones, the expenses

incurred by him shall be reimbursed within 14 working days from submission of all documents.

Claim procedure ?CASHLESS CLAIMS

1. Get admitted in any one of our networked hospitals2. Fax the pre-authorisation form along with relevant documents (Investigation reports,

Previous consultation papers if any, Cashless ID, Photo ID)3. Company will reviews your claim request and accordingly will approve, query or reject

the same (as per policy terms & conditions)4. Company will settles the claim

(as per policy terms & conditions) with the hospital after completion of all formalitiesNote:Cashless Facility is only available at hospitals in our cashless network.In case of Planned Hospitalization contact your service provider two days prior to admission.In case of Emergency Hospitalization contact your service provider within 24 hours of hospitalization.

REIMBURSEMENT CLAIMS1. Upon discharge, pay all hospital bills and collect all original documents of treatments

and expenses undergone2. Mail the duly filled (and signed by insured and treating doctor) claim form and required

documents to your service provider (Company or TPA)3. Company will reviews your claim request and accordingly will approve, query or reject

the same (as per policy terms & conditions)4. Company will settles the claim

(as per policy terms & conditions) and reimburses the approved amount.

OTHER’S TPA1. Get admitted in any one of the TPAs networked hospitals2. Fax the pre-authorisation form along with relevant documents (Investigation reports,

Previous consultation papers, Cashless ID, Photo ID)3. Your service provider reviews your claim request and accordingly will approve, query

or reject the same4. Your service provider settles the claim

(as per policy terms & conditions) with the hospital after completion of all formalities

OPD claim procedure…Documents required1. The Insured shall be required to furnish the following documents in original for or in

support of a claim:2. Duly completed OPD claim form3. Discharge Card (if applicable) or OPD card of the Hospital4. Prescription of the treating Medical Practitioner, bills, receipts, etc.5. Bills from chemists supported by proper prescription6. Test reports and payment receipts7. Any other document as required by the Company

Payment of Claims• Claims pertaining to each Insured can be lodged only once during the Period of

Insurance• The Company shall not receive any claims prior to completion of 90 days of the

commencement of the Policy• Claims under OPD Benefit shall be payable only on re-imbursement basis• No claim shall be admissible under OPD Benefit 30 days after expiry of the Period

of Insurance• OPD HAP claims will be settled in 10 working days for cases where all the

required documents have been received

MOTOR INSURANCEWhat is motor insurance?As per the Motor Vehicles Act, 1988 it is mandatory for every owner of a vehicle plying on public roads, to take an insurance policy, to cover the amount, which the owner becomes legally liable to pay as damages to third parties as a result of accidental death, bodily injury or damage to property. A Certificate of Insurance must be carried in the vehicle as a proof of such insurance.

Highlights…This policy covers all types of vehicles plying on public roads such as:-Scooters & MotorcyclesPrivate carsAll types of commercial vehiclesMotor Trade (vehicles in show rooms and garages)

Eligibility?• Owners of the vehicle Financiers or Lessee who have insurable interest in a motor

vehicle.

What are coverages?• Motor vehicle which includes private cars Motorised Two wheelers and Commercial

vehicles excluding vehicles running on rails.• Loss or damage to accessories fitted in the vehicle such as stereos, fans, air-conditioners

etc.• Fire, explosion, self-ignition or lightning.• Burglary, housebreaking or theft.• Riot and Strike.• Malicious Act.• Terrorist Act.• Earthquake (Fire and Shock) Damage.• Flood, Typhoon, Hurricane, Storm, Tempest, Inundation, Cyclone and Hailstorm.• Accidental external means.• Whilst in transit by road, inland waterway, lift, elevator or air.• By landslide/Rockslide• Personal accident cover under private car policies for:

passengers paid driver

• Legal liability to employees.• Legal liability to non-fare paying passengers in commercial vehicles.

Exclusions?• Wear and tear, Mechanical/ electrical breakdowns• Consequential loss• Loss when driving with invalid driving license or under the influence of alcohol.• Loss due to war, civil war, etc.• Claims arising out of contractual liability.• Use of vehicle otherwise than in accordance with `limitations as to use ' (e.g. private car

being used as a taxi).• Depreciation or any consequential loss.• Damage to/ by a person driving the vehicle under the influence of drugs or liquor.

Key benefits… • Cashless servicing facility at network garages across India.• Immediate issuance of policy copy online Zero Depreciation Cover#. Avail coverage on

replaced parts with zero deduction for depreciation• Set Renewal Reminder to receive policy renewal reminders• Automobile Associations members can get up-to 5% discount.• Up-to 2.5% discount on ARAI Automobile Research Association of India approved anti

theft devices.• Multiple payment options including easy EMIs on car insurance policy • Avail of our 24x7 telephonic service for claims support and other assistance, even on

holidays.• Towing Facility in an event of a breakdown/accident.

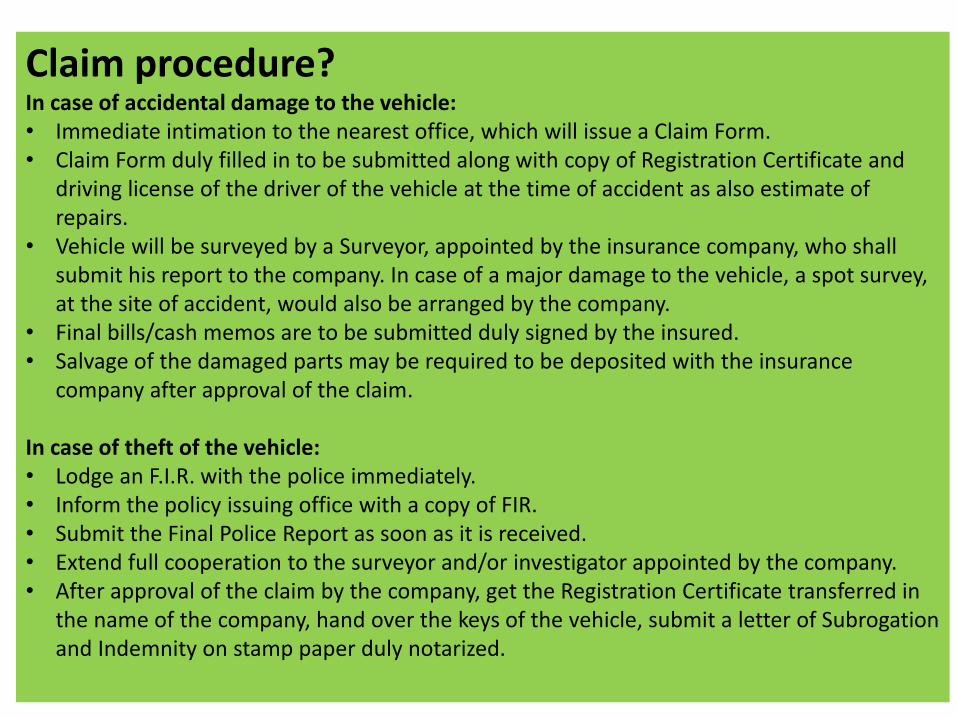

Claim procedure?In case of accidental damage to the vehicle:• Immediate intimation to the nearest office, which will issue a Claim Form.• Claim Form duly filled in to be submitted along with copy of Registration Certificate and

driving license of the driver of the vehicle at the time of accident as also estimate of repairs.

• Vehicle will be surveyed by a Surveyor, appointed by the insurance company, who shall submit his report to the company. In case of a major damage to the vehicle, a spot survey, at the site of accident, would also be arranged by the company.

• Final bills/cash memos are to be submitted duly signed by the insured.• Salvage of the damaged parts may be required to be deposited with the insurance

company after approval of the claim.

In case of theft of the vehicle:• Lodge an F.I.R. with the police immediately.• Inform the policy issuing office with a copy of FIR.• Submit the Final Police Report as soon as it is received.• Extend full cooperation to the surveyor and/or investigator appointed by the company.• After approval of the claim by the company, get the Registration Certificate transferred in

the name of the company, hand over the keys of the vehicle, submit a letter of Subrogation and Indemnity on stamp paper duly notarized.

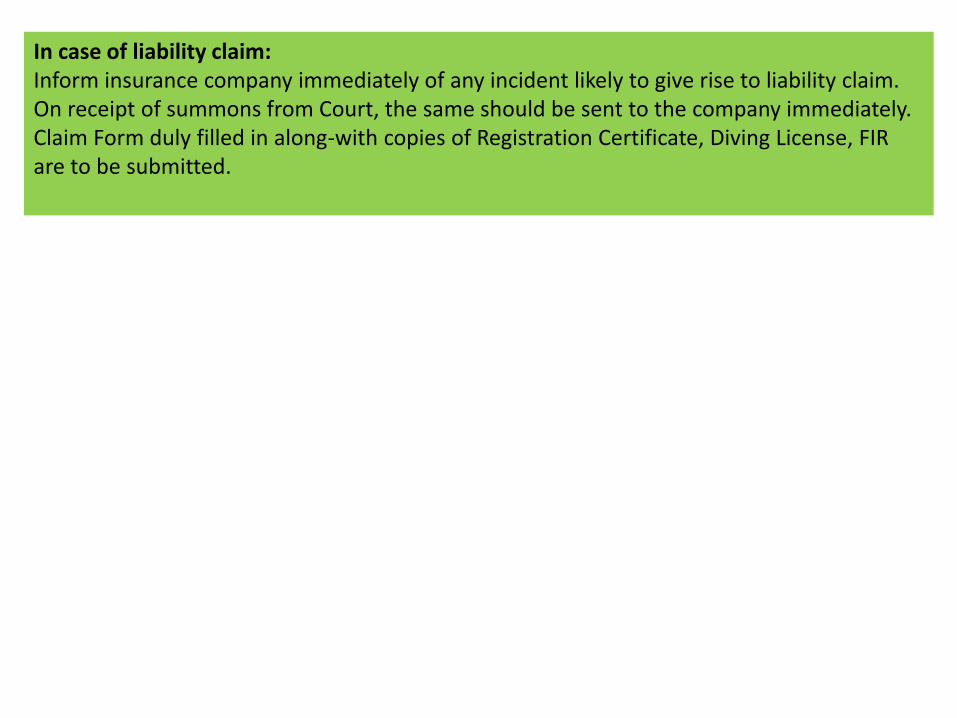

In case of liability claim:Inform insurance company immediately of any incident likely to give rise to liability claim.On receipt of summons from Court, the same should be sent to the company immediately.Claim Form duly filled in along-with copies of Registration Certificate, Diving License, FIR are to be submitted.

LIFE INSURANCE

Why life insurance?All of you knows your date of birth, but do you know your DATE OF DEATH.Who will take care of your family if you will die. Your children education, medical expenses, healthy food, and the most important is their dreams.You never know when you will die. So wakeup and take initiative for life insurance policy for better future of your precious family.Don’t be depend on others, because you are a king of your life. Life insurance will also give you benefit after your retirement.

There are many types of life insurance policy to secure your life as well as family also.1. Term plan2. Investment plan3. Retirement plan4. Child plan

TERM PLAN

Why is term plan?You always want to live a good life and provide same to family. But who knows when life is going good next what going to happen to you or your job. so keep a security by choosing term plan because it will help you when times going wrong.

Key features • Tax Exemption • Get the advantage of a level term cover at low cost, especially for larger sum assured.• Get rewarded for maintaining a healthy life-style, if applicable, with special premium rates

for non-smokers and medically fit non-smokers.• Benefit of attractive high sum assured rebate.• Flexibility to select your policy term of 10, 15, 20, 25 or 30 years depending on your

requirement.• Alter your premium payment frequency.• Include your spouse at a later date in your existing policy, if you are single at present.• Choose additional rider benefit(s) for enhanced protection.• Plan to meet recurring expenses of your loved ones by opting for payment of benefit in

annual installments.

• High cover at a very nominal cost - Your ideal life insurance cover should be about 10 times of your annual income

• No Medicals up to a cover of Rs. 75,00,000 • HDFC Life has a Claim Settlement Ratio of 96.17% - So that your family is provided the sum

assured when they need it the most• Enjoy tax benefits • Attractive premium rates for those do not consume tobacco

Flexibilities:• Additional Rider Benefits• Option to Take an Individual or a Joint Life Policy• Alteration of Premium Payment Frequency• Option to Take Death Benefit in Annual Installments

Eligibility:Entry level is 18 – 60 years.Policy term – 10,15,20,15,30 years.

Investment plan

Why investment plan?You have always given your family the very best. And there is no reason why they shouldn't get the very best in the future too. As a judicious family man, your priority is to secure the well-being of those who depend on you. More importantly, you have to ensure that your family's future expenses are taken care, even if something bad were to happen to you.

Features:• Tax Exemption • Inbuilt accidental death cover.• Option to select policy term of 10/15 or 20 years and premium paying term of 5 years to

policy term.• Automatic annual increase in sum assured from 6th policy anniversary to suit your needs.• Choice of 7 investment funds to invest in as per your risk appetite.• Two investment portfolio strategies to manage your investments better; including the

Wheel of Life portfolio strategy, which will help you to balance and safeguard your investment.

Key benefits:Surrender Benefit Tax benefitHigh Interest benefit Death benefit

RETIREMENT PLAN

Why retirement plans?Till the time you earning you feeding yourself and family also, and your family is dependent on you only. But what will happen after your retirement when you were unable to work, HAVE YOU PLANNED FOR BETTER OLD AGE FUTURE?

Key features:• Tax Exemption • Accumulated compound reversionary bonus on completion of premium payment term.• Cash Back benefit of 5% of the sum assured plus cash bonus, if any declared every year,

during the cash back period end.• Sum Assured plus terminal bonus, if any on maturity of the policy.• Select your policy term from 10 years to 65 years depending on your financial need.• Select your limited premium paying term (PPT) from 5 years to 30 years.• Pay your future premiums in advance and get benefit of appropriate discounts.

Types of Retirement Plans: Deferred Annuity:

A deferred annuity plan allows you to accumulate a corpus through regular premiums or single premiums over a policy term. After the policy term is over, pension will begin. Immediate Annuity:

In an immediate annuity plan, pension begins immediately. One has to deposit a lump sum amount and pension will begin instantly.

Child plan

Child Plans• A wise mom once said "Your child will keep building castles in the air; you better start buying

bricks for the castle today." • Loving your child is what comes naturally but as a responsible parent you have certain

obligations towards your child. Getting a Child Plan is one such obligation, might we add the most important one.

• If you are reading this, you’ve already proved that you are a concerned parent finding ways to secure your child’s future. Let us help you out in understanding what exactly a Child Plan is and how to go about it.

• Child Plan is insurance cum investment plan that serves 2 purposes – To financially secure your child’s future To finance the turning points in his life such as higher education and marriage

So, like a double-edged sword, a Child Plan protects the future of your child in case of your unfortunate demise and at the same time, builds a corpus over a term to be utilized to finance the prime moments in his life like higher education and marriage.

Key benefits and features:• Tax Exemption • Select up to no. of times your base sum assured as life cover-Super Cash Gain (according to

policy) • Option to select policy term of no. of years. E.g. 10, 12, 16, 24.• Benefit from shorter premium payment term as no premiums are payable for the last five

policy years.• Get 20% of the base sum assured as cash-back at regular intervals, which you may take as

cash or ask us to adjust against your due or future premium.• Flexibility to pay your future premiums in advance and avail discounts.• Option to

Keep your policy in force for full sum assured in case you miss paying your premiums on due dates, provided you have paid at least 3 years' premiums in full.

Convert your policy to a "single premium term cover with return of premium (ROP)"policy, if you miss paying your premiums on due dates provided you have paid at least 5 years' premiums in full.

• Get more value for your money with high sum assured rebate on premium.• Optional riders to enhance your protection.• Maturity benefit• Death benefit

ELIGIBLITY:• ENTRY LEVEL AGE 0-70 YEARS.

LIFE INSURANCE CLAIM PROCESS:

Filing a Life Insurance Claim

Claim settlement is one of the most important services that an insurance company can provide to its customers. Insurance companies have an obligation to settle claims promptly. You will need to fill a claim form and contact the financial advisor from whom you bought your policy. Submit all relevant documents such as original death certificate and policy bond to your insurer to support your claim. Most claims are settled by issuing a cheque within 7 days from the time they receive the documents. However, if your insurer is unable to deal with all or any part of your claim, you will be notified in writing.

Types of claims:Maturity Claim - On the date of maturity life insured is required to send maturity claim / discharge form and original policy bond well before maturity date to enable timely settlement. Most companies offer/issue post dated cheques and/ or make payment through ECS credit on the maturity date.

Death Claim (including rider claim) - In case of death claim or rider claim the following procedure should be followed.

Follow this four simple steps to file a claim:• Claim intimation / notification The claimant must submit the written intimation as soon as possible to enable the insurance company to initiate the claim processing. The claim intimation should consist of basic information such as policy number, name of the insured, date of death, cause of death, place of death, name of the claimant.The claimant can also get a claim intimation/notification form from the nearest local branch office of the insurance company or their insurance advisor/agent. Alternatively, some insurance companies also provide the facility of downloading the form from their website.

• Documents required for claim processing The claimant will be required to provide a claimant's statement, original policy document, death

certificate, police FIR and post mortem exam report (for accidental death), certificate and records

from the treating doctor/hospital (for death due to illness) and advance discharge form for claim

processing. Based on the sum at risk, cause of death and policy duration, insurance companies

may also request some additional documents

• Submission of required document for claim processingFor faster claim processing, it is essential that the claimant submits complete documentation as early as possible. A life insurer will not be able to take a decision until all the requirements are complete. Once all relevant documents, records and forms have been submitted, the life insurer can take a decision about the claim

• Settlement of claimAs per the regulation 8 of the IRDA (Policy holder's Interest) Regulations, 2002, the insurer is required to settle a claim within 30 days of receipt of all documents including clarification sought by the insurer. However, the insurance company can set a practice of settling the claim even earlier. If the claim requires further investigation, the insurer has to complete its procedures within six months from receiving the written intimation of claim

Claim intimation:In case a claim arises you should:• Contact the respective life insurance branch.• Contact your insurance advisor.• Call the respective customer headline.

Claim requirements:For death claim• Death certificate• Original policy bond• Claims forms issued by the new insurer along with supporting document

For accidental disability / critical illness claim• Copies of Medical Records, Test Reports, Discharge Summary, Admission Records of hospitals

and Laboratories• Original Policy Bond• Claim Forms along with supporting documents

For maturity claims:• Originally policy bond• Maturity claim form

HOME INSURANCE

What is home insurance?As a homeowner, you invest a lot of time, money and care into making your home look beautiful for the festival. But don't stop there - give your home the best possible protection from unforeseen incidents with Home Insurance plans.

This is a package policy specially designed to meet the insurance requirements of a householder by combining under a single policy, a number of our standard policies usually taken by householders.

What are coverages?Section I - Fire & Allied Perils• Coverage for building• Covers contents of the dwelling belonging to the proposer and his/her family members

permanently residing with him/her.• Allied Perils:• Fire, Lightening, Explosion of gas in domestic appliances• Bursting and overflowing of water tanks, apparatus or pipes.• Damage caused by Aircraft• Riot, Strike, Malicious or Terrorist Act• Earthquake, Fire and/or Shock, subsidence and Landslide (including Rockslide) damage• Flood, Inundation, Storm, Tempest, Typhoon, Hurricane, Tomado or Cyclone.• Impact damageSection II - Burglary & House Breaking including larceny and theft.• Covers contents of the dwelling against loss due to burglary, house breaking, larceny or

theft.Section III - All Risks (Jewellery & Valuables)• Covers loss or damage to your jewellery and valuables by accident or misfortune whilst

kept, worn or carried anywhere in India subject to the value declared in the schedule.

Section IV - Plate Glass• Loss or damage to fixed plate glass in the insured premises by accidental breakage subject

to limit of sum insuredSection V - Breakdown of Domestic appliances• Covers domestic appliances against unforeseen and sudden physical damage due to

mechanical or electrical breakdown.Section VI - T.V. Set including VCP/VCR (ALL RISKS)• Covers loss or damage to T.V.Set including VCP/VCR by fire and allied perils, burglary,

house breaking or theft, breakage due to accidental external means, mechanical or electrical breakdown. Any legal liability arising out of bodily injury or accidental death of any person other than insured's family members or employee as also damage to property not belonging to or in the custody of insured , caused by use of the T.V. Set is also covered up to a limit of Rs.25,000/-.

Section VII - Pedal Cycles (All Risks)• Covers loss or damage to pedal cycles by :• Fire & allied perils• Burglary, housebreaking, theft• Accidental external means• Third party personal injury or Third party property damage for Rs.10,000/-Section VII - Baggage Insurance• Covers loss or damage to insured's accompanied baggage by accident or misfortune whilst

the insured is traveling on tour or holiday anywhere in India.

Section IX - Personal Accident• Covers Death or bodily injury by accidental, violent, external and visible means to the

insured person named in the schedule and subject to limits specified therein.Section X - Public Liability• Covers Insured's legal liability for bodily injury or loss of or damage to property of third

party limited to amount specified in the schedule and workmen's compensation liability to domestic servants engaged in insured's premises.

• It is compulsory to opt for Section IB of the policy. A minimum of three sections including Section IB have to be taken for issuance of this policy.

Exclusions?• Consequential loss of any kind or description• Loss or damage caused by depreciation or wear and tear• Damage to contents of a consumable nature• Loss or damage to mobile phones or similar communication devices• Loss of or damage to valuables, jewellery or precious items• Other exclusions as listed in the policy wordings

Key benefits…• Provides protection for property, domestic and electronic appliances, interests of the

insured and their family members in a single policy• Affordable premium• Attractive rebates• Waiver of under-insurance• Comprehensive cover available, which covers both structure and / or contents of your

home • Coverage up to 10 years for only structure, 5 years for only contents and 5 years for

structure & content • Cover against Fire and allied perils, Burglary & Theft and Optional cover for Terrorism

and Additional expenses of rent for alternative accommodation.

Claim procedure?(I) Intimation –As soon as a claim occurs, please intimate immediately to our Help line numberWhile registering the claim through above help line number, please share the below details with our call centre executive1. Policy Number2. Insured name3. Location of loss4. Cause of loss and amount of loss (approx. estimation)5. Other relevant information like electronic breakdown, burglary details…..etc pertaining to your claim.Call centre executive will register your claim and you will receive claim intimation number which is unique claim identification number.

(II) Surveyor appointment –The company appoints a surveyor within 2 working days, who will assess the loss/damage, depending up the type of loss i.e. Fire/Burglary/electrical mechanical breakdown etc.

(III) Document submission –You need to submit the relevant documents as per the registered claim to the surveyor,

documents as below

1. Claim Form with complete details (policy number, insured name…..etc)Download Claim Form from RGICL website2. Purchase Invoice of the affected subject matter3. Estimates of Repairs/Replacements4. Replacement invoice & Payment Proofs5. First Information report & Final Investigation report from Police Authorities, if applicable6. Fire Brigade report, if applicable7. Service Report in case of Electronic & Mechanical breakdown claim8. Other supporting document as per Surveyor requirement based on case to case basis.

(IV) Claim Settlement –The surveyor would submit the final report along with the relevant documents to our Claims Authorities who would contact you if any additional information is required. The survey fee is paid by the insurance company and you need not pay anything to the surveyor.

Claim amount payment can be received through NEFT (National Electronic Funds Transfer) directly into your bank account. A cancelled cheque and an ID proof like PAN card may be submitted to the insurance company along with the claim form to avail this facility.On receipt of the documents, the claims department processes the claim without any further delay.

TRAVEL INSURANCE

What is travel insurance?Every one loves to travel with lots of fun. But the fact is that we have fear for our health, luggage, important documents etc. So if you want to get rid of all tensions and worries just sign a travel insurance policy and enjoy your happy moments. Travel insurance is both for family and individual.

what are the coverages?• Medical cover.• Repatriation of remains.• Daily allowance in case of hospitalization• Dental treatment• Total loss of checked in baggage• Delay of checked in baggage• Loss of passport• Accident• Hijack distress allowance• Emergency cash advance• Trip cancellation and interruption• Missed flight connection• Accidental death• Fire cover for building• Fire cover for home content• Return of minor child(ren)

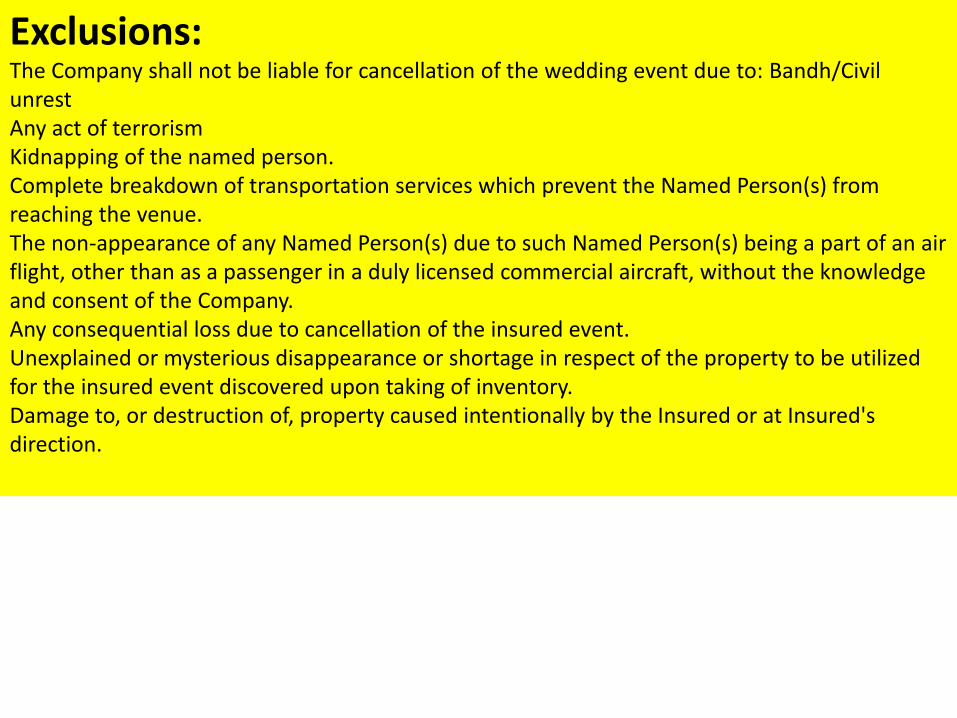

Exclusions?• Pre-existing conditions except in case of life-threatening situations.• Addiction to alcohol, drugs.• Mental disorder, anxiety, depression. • Venereal diseases. • Sexually transmitted diseases, AIDS, HIV. • Radiation, nuclear weapons induced. • Sporting activities. • Expenses arising out of loss of valuables, money, securities and tickets. • Naturopathy treatment, Ayurveda /homeopathic therapies. • Treatment relating to removal of physical flaws-cosmetic or plastic surgery. • Costs incurred relating to rest or recuperation at a spa or health resort.

Key benefits…• Get covered up to 85 years of age without medical check-up. • Avail cashless hospitalization facility worldwide.• Get covered on Pre-existing diseases under life-threatening situations.• For the very first time in India, with this policy you can get coverage for all baggage including

handbags.• Stay rest assured that your loved ones receive medical & nursing assistance back home.• Get support on car repairs even when you're away.• Get covered even against extended stay at hotel due to natural and man-made calamities.

Claim procedure?

How to file a Claim• In case of any event leading to a claim under the policy, Please call our Service Provider.• Our Claims Service Representative will guide you on the claim procedures and documents

required• A claim form will be forwarded to you by mail, email or fax• Complete the claim form relevant to the nature of loss as indicated below.• Attach the documents mentioned against the claim type

Documents required for claim:-For accidental injury claim:• Claim form• Police Report, if accident is reported to Police• Medical papers, pathology reports, X-ray reports, as applicable• For Permanent Disability Claims – disability certificate from reputed surgeon or Hospital• For Temporary Total Disability Claims-sick leave certificate from Employer• Attending Physician’s statement

For Emergency Medical Expenses/ Emergency Dental Treatment• Claim Form• Police FIR, if accident is reported to Police• Medical papers, pathology reports, X-ray reports, as applicable• Doctor’s prescription and line of treatment suggested• Bills and cash memos• Attending Physician’s statement

For Hospital Cash- Sickness Claim• Claim Form• Hospital Discharge Card• Doctor’s certificate and line of treatment suggested• Attending Physician’s statement as per ‘Form D’

For Hospital Cash – Accident Claim• Claim Form• Hospital Discharge Card• Doctor’s certificate and line of treatment suggested• Attending Physician’s statement.

For Accidental Death Claims• Claim Form• Police Report• Post-mortem Report or Coroner’s Report• Death Certificate• For payment to beneficiary – succession certificate or notarized affidavit certifying legal heir

status.• Where payment to beneficiary is through notarized affidavit, a letter of indemnity on Rs.200

stamp paper ( please contact us for the indemnity format)

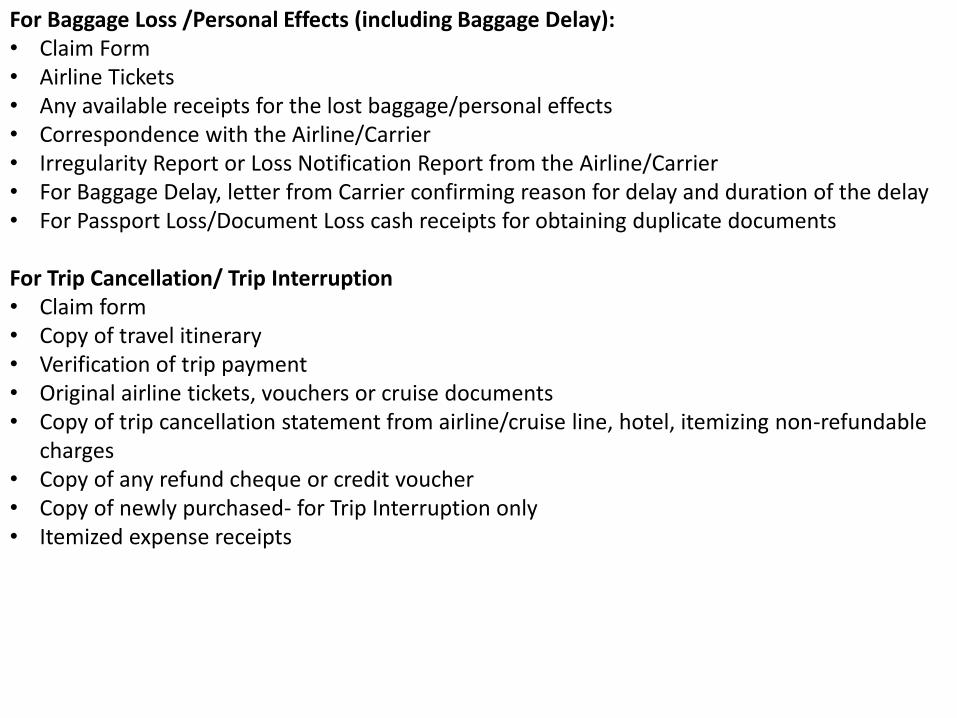

For Baggage Loss /Personal Effects (including Baggage Delay):• Claim Form• Airline Tickets• Any available receipts for the lost baggage/personal effects• Correspondence with the Airline/Carrier• Irregularity Report or Loss Notification Report from the Airline/Carrier• For Baggage Delay, letter from Carrier confirming reason for delay and duration of the delay• For Passport Loss/Document Loss cash receipts for obtaining duplicate documents

For Trip Cancellation/ Trip Interruption• Claim form• Copy of travel itinerary• Verification of trip payment• Original airline tickets, vouchers or cruise documents• Copy of trip cancellation statement from airline/cruise line, hotel, itemizing non-refundable

charges• Copy of any refund cheque or credit voucher• Copy of newly purchased- for Trip Interruption only• Itemized expense receipts

BUSINESS INSURANCE

Types of business insurance?• Shop/Shopkeeper insurance• Fire insurance• Marine insurance• Industrial insurance• Corporate insurance• Liability insurance• Event insurance• Money insurance• Burglary insurance• Credit insurance• All risk insurance policy

SHOPKEEPER INSURANCEWhy shopkeeper insurance?Shop keeping is an economic activity pursued with the aim of earning maximum profits within the limits of Government Rules & Regulations as well as social values. To ensure that one can focus on this primary activity, it is necessary that the mind should be free from other worries not related to trading such as accidents, which could hamper the business activity.

Coverages?• Fire• Housebreaking• Loss of money• Pedal cycle• Plate glass• Neon sign• Baggage• Personal accident• Fidelity guarantee• Electronic equipment insurance• Business interruption• Cheque forgery• Tenant’s legal liability

Exclusions?loss or damage caused by war and allied perils loss or damage by nuclear radiation and related causes. Restaurants / cafes may not be covered.Dry Cleaner shops may be covered provided no process is carried out in the shop premises. Jewellery shops may not be covered.

Benefits/features.• Lightening fast claims

Lots of additional optional covers available making it the most comprehensive policy.

How to claim?• In case of any incident giving rise to a claim under this policy, please take the following steps:• Take necessary steps to minimize the loss/damage.• In case of fire, inform fire brigade immediately.• In case of theft, larceny or burglary inform the police immediately along with a list of items

stolen and their approximate value.• Inform insurance company by phone or fax and in writing.• Extend full co-operation to the surveyor appointed by the insurance Co. and provide

necessary documents to substantiate the loss. A claim form issued by the company is also to be submitted.

• In case any rights of recovery exist against any other party responsible for the loss, your rights of recovery have to be subrogated to the insurance company on payment of claim.

FIRE INSURANCE

Coverages?• Buildings• Machinery and Accessories• Stock and stock in process• Contents including furniture• Lightning & explosion• Terrorism• Strom, tempest, floods & inundation• Industrial / Manufacturing Risks• Utilities located outside industrial/manufacturing risks• Tank farms / Gas holders located outside the compound of industrial risks• Bush fire• Bursting or overflowing of tanks.

Premium• Premium rate depends on construction of building and occupancy.• Discount/ loading in premium is given based on past claims experience for risks exceeding Rs.

50 crores sum Insured at any location and installation of Fire Extinguisher Appliances.

Exclusions?• Loss or damage to property due to :• Spontaneous combustion fermentation• Burning of property by order of any Public Authority• Its undergoing any heating or drying process• Explosion of boilers (other than domestic boilers)• Total or partial cessation of work• Permanent or temporary dispossession by order of Government• Burglary House breaking theft• Normal Cracking or settlement or bedding down of new structures• War or war like operations• Defective design workmanship defective materials• Pollution or contamination• Over-running short circuit etc.• Earthquake• Spoilage loss

Fire Insurance claim procedureIn case an unfortunate loss as covered in the policy occurs, so as to get prompt service we request you to take the following actions:a. Immediately inform the office concerned over phone and in writing the occurrence of the claim along with the correct policy number.b. Obtain the claim form from the office concerned, fill up the same in all respects and submit the same in our office.c. n case the loss is very large, prompt intimation is required to send a suitable surveyor to assist you in minimizing the loss and quick settlement of claim which helps to restart the business activity. Our officer may also visit the site of loss to have a first hand information of the loss.d. In order to help to prove your claim the surveyor or office may seek documentary evidence. You may handover photocopies of necessary documents and obtain acknowledgement.e. Fully cooperate with the surveyors and insurance officials visiting the site of loss to examine the cause of loss, to correctly estimate the extent of loss and to work towards a quick settlement of the loss. They should be helped to take photographs of the loss and obtain statements of witnesses.f. Necessary information, as if you are an uninsured, should be given to the local fire station, police authorities and other Civil authorities as per law and local practice. Copies of their reports should be obtained and handed over to the surveyor or office.g. Surveyor may also be given copies of licences, permits and certifications etc. in force to ensure that the operations are conducted as per law and as per the necessary safety standards.h. A copy of the survey report may be handed over to you if you so wish for your record so that you are aware of the assessment made.i. As soon as the survey report and copies of the document desired by the surveyor / insurer are complied with by you, you may keep in touch with our office for early disposal of the claim

MARINE INSURANCE

Marine hullCoverages?• ships tankers • bulk carriers • fishing boats • Hull or machinery• Freight• Builders risk• Loss of hire• Loss of profit• Fishing Vessels• Ocean Going Vessels.• Sailing Vessels.• Other Vessels .

Exclusions?• The exclusions will depend upon the type of cover availed and would be governed by

Institute Time clauses and Institute Voyage clauses.• Deliberate damage/destruction of the vessel by wrongful act of any person• Use of any weapon of war employing atomic / nuclear fission and or fusion• Insolvency or financial default of the vessel owner / operators / charterers.• War / civil war Strike Riot or Civil Commotion.• Any terrorist or person/s acting with political motive.

Sum insuredIt is an agreed value policy.

PremiumThe premium will depend on the following factors:• Type of vessel, trading limits, age, tonnage, technical aspects of machinery• Management and ownership consideration• Past claim experience• Valuation of vessel• Type of cover required• Size of deductible

Marine cargoCoverages?• Any loss or damage to goods in transit by rail sea road air or post.• Fire or explosion; stranding sinking etc.• Overturning derailment ( of land conveyance)• Collision• Discharge of cargo at port of distress• Jettison• General average sacrifice salvage charges• Earthquake lightning• Washing overboard• Sea lake river water• Total loss of package lost overboard or dropped in loading or unloading• War and SRCC is specifically covered

Premium Rating• The normal basis of valuation for ocean/air consignment will be CIF + incidentals up to a

percentage which is agreed upon at the inception of the policy ( normally this is 10 %)

Marine Cargo Insurance Claims Procedure

A. Duty of the Insured / Consignee / Its Agent or Representative

In case of any loss or damage to the cargo, it is a duty of the Insured / Consignee / Its Agent or Representative to take following procedures

1. Do no give clear receipt on the delivery order but to give such notice of loss or damage

2. In case of containerised cargo:- Check carefully condition of the containers if it was damaged or holed.- Check carefully condition of its seal if numbers is matched with the document or if it was damaged or cut.- If it was found damage, Give such notice of loss or damage on the delivery order.3. Immediately contact the carriers or its representative to do survey.

4. Immediately contact THE INSURANCE COMPANY to do joint - survey.

5. Immediately notify Police in case of traffic accident, theft or other malicious acts.

6. Take photographs showing details of container, its seal and numbers, its floor, wall and roof where it was damaged and condition of the cargo.

7. Write claim to the carriers holding them responsible for loss or damage.

B. Survey & Claim Reporting to THE INSURANCE COMPANY

Claim shall be reported immediately to THE INSURANCE COMPANY or Its survey agent in order to have the damage inspected to conclude the cause of loss or damage. Claim reporting shall not later than 7 days from the time loss or damage noticed.

It is a duty of the Insured to give THE INSURANCE COMPANY or Its survey agent an opportunity to inspect the damage, vessel, interview with the master and crews and other related parties.

C. Documentation

Claim FormOriginal Insurance Certificate / PolicyOriginal Bill of LadingInvoicePacking ListDelivery OrderOfficial damage / Survey ReportLetter of claim against the carriers and their replyEstimated cost of repairEIR (Equipment Interchange Receipt)Ship accident report and complete of its documentPolice report (in case of theft or traffic accident)Picture of damage

D. Salvage

1. It is a duty of the Insured / Consignee / Its Agent or Representative to mitigate the loss and secure the salvageable cargo safe, do not destroy or sell them without THE INSURANCE COMPANY’s written approval.

2. THE INSURANCE COMPANY for and on behalf of the Insured have a right to sell on tender the salvageable cargo and invite some buyers to quote.

3. The Insured or Consignee can participate on the above tender.

4. Terms and condition of the tender and to choose the winner are absolute right of THE INSURANCE COMPANY

5. Value of salvage is to be paid to the Insured and is to be deducted from amount of claim payable.

E. General Average

In case of GA the Insured / Consignee / Its Agent or Representative is not authorized to sign Average Guarantee or to pay cash deposit without THE INSURANCE COMPANY’s written approval.

INDUSTRIAL INSURANCE

Boiler and pressure plant insuranceCoverages?• Boilers like fire tube boilers/recovery boilers and unfired pressure vessels/steam pipes can be

covered.• The Policy broadly covers boilers and other pressure vessels, both fired and unfired against

losses due to explosion or collapse.

Exclusions?The policy does not cover loss and/or damage arising from:• Fire and allied perils• War and nuclear perils• Loss arising out of overload experiments• Gradual wear and tear of parts• Failure of individual tubes, loss due to chemical reaction• witful acts or gross negligence• Loss which is manufacture’s or repair’s responsibility• Act of God perils

Sum InsuredSum insured should be reinstatement cost of the Boiler.

PremiumPremium chargeable depends on the type of Boiler, type of fuel and the age of equipment. Discount is allowed for seasonal factories and stand by facilities

Electronics equipment's insurance policy

coverages?• Electronic equipments such as Computers Medical Bio-Medical Micro Processors Audio-visual

equipments etc.• Material damage to electronic equipment (which can include systems software) due to

sudden and unforeseen events• Cost of external data media, including cost of reconstruction of data

Exclusions?• Wear and tear.• War, witful act or wiful negligence.• Aesthetic defects and consequential loss.

Premium• Rate of Premium: 1 % For equipments valued more than Rs 1,00,000, a valid maintenance

agreement is required to be in force, failing which 100 % loading is attracted.

Claim procedure:1. Once you submitted all the required documents, we will acknowledge receipt of the

documents in writing.2. We will review the information provided and determine if it is sufficient for us to decide

whether the loss or damage can be indemnified under the policy coverage. During this process, we may request additional information or documentation.

3. We may appoint an investigator, loss adjuster or lawyer to investigate the events and circumstances that have lead to the claim.

4. If the information provided or discovered is sufficient, we will communicate our decision of coverage position and the proposed claim settlement to you in writing.

5. Claim payment will be executed upon receiving your confirmation of acceptance

Machinery breakdown insurance policy

Coverages?• Damage to foundation of machinery• Damage to oil in electrical apparatus• Express freight (excluding air freight), holiday rates, overtime charges• Air freight • Additional custom duty i.e the additional percentage of duty payable at the time of reimport

for replacement over and above the percentage of duty included in the original sum insured.• Own surrounding property i.e. damage to the insured's own existing property or property in

his custody or control (not included in the sum insured of the policy) due to any damage to the insured machines which is covered under the policy.

• Third party liability i.e. liability falling on the insured for bodily injury to any other party other than those covered by the policy or for property damage belonging to such other party.

Exclusions?• Fire and allied perils.• War and War like operations Nuclear perils.• Wilful act or gross negligence existing defects normal wear and tear and consequential loss.• Loss or damage falling under manufacturer's warranty.

Contractors plant and machinery policyCoverages?• This policy shall cover any unforeseen and sudden physical damage to the property by any

cause not specially excluded. This policy shall apply to the insured item whether:• They are at work• or at rest• or being dismantled for the purpose of cleaning or overhauling• or when being shifted within the premises• or subsequent re-erection• third party liability - personal injury and property damage.• damage to owner's surrounding property.

Exclusions?• Electrical or mechanical breakdown or boiler explosion• Replaceable parts like bits knives ropes & bolts chains etc. wear and tear corrosion damage

whilst in transit war and nuclear perils.• When undergoing test or while used for a purpose different from what was originally

intended .• Damage due to accidents to carrying vehicle /train/vessel/and craft.• Damage to plant&machinery working underground.• Contractual liability consequential loss existing defect inventory loss.

Contractors all risk policyThe policy is specially designed to give financial protection to the civil engineering contractors in the event of an accident to the civil engineering works under construction.

HighlightsThis policy is specially designed to give financial protection to the Civil Engineering Contractors in the event of an accident to the civil engineering works under construction.In case the policy period exceeds 12 months, the premium can be paid in quarterly installments with the first installment being more by 5% and the last installment being paid 6 months before expiry of the policy.

Scope• The policy comprises of 2 Sections :• Section I-Material Damage-covering physical loss, damage or destruction of the property

insured by any cause, other than those specifically excluded in the policy.• Section II-Third Party Liability-covering the legal liability falling on the insured contractor as a

result of bodily injury or property damage belonging to a third party.• The main exclusions under Section I for which no claim is payable, are loss or damage due to:

• faulty design• rectification of aesthetic defects of structure not relating to any physical loss or damage to

the structure due to any accident, or of material defect or of workmanship defect.The exclusion of defective material / workmanship is limited to the parts of the structure immediately affected and does not apply to any consequential loss to correctly executed items, arising out of the accident due to defective material or workmanship.

• loss or damage due to gradual deterioration, atmospheric condition, rusting etc.• loss discovered only at the time of taking inventory.• loss arising out of penalty for delay, non-fulfillment of terms of contract.

Add on covers• The policy can be extended to cover the following items :-• construction equipment like scaffolding, shuttering materials• construction equipment like scaffolding, shuttering materials• damage to surrounding property not forming part of the contract work.• maintenance visit / extended maintenance cover to cover accidental loss or damage whilst

carrying out any rectification during maintenance period and / or any amount incurred for rectification of such original defects or faults during construction.

Who can take the policy?The policy can be taken by the principal, contractor or sub contractor, jointly or separately.

How to select the sum insured?• The sum insured selected under section I should represent total contract value including the

estimated cost of labour charges and cost of materials but excluding profit. The cost of materials supplied by the principal is to be declared separately.

• In case of long term contracts, there is bound to be escalation in prices. The basic policy will pay only as per the original cost and prices. However escalation clause can be opted for, under which escalation upto 50%, can be selected to take care of such increase in prices.

• The sum insured under section II should represent the per accident limit (the maximum legal liability that may fall on the insured as a result of an accident in the insured's site). The limit per policy period should be fixed taking into account the maximum number of such accidents which can reasonably be expected to occur.

How to claim?In the event of any loss or damage giving rise to a claim under the policy, the following steps should be taken :-take necessary steps to minimise the loss.inform insurance company immediately.extend full cooperation to the surveyor deputed by the company.submit duly filled in claim form along with necessary documents to substantiate the financial loss suffered as a result of the accident.

Period of Insurance• Unlike other policies where the period of insurance is one year, in this policy the period of

insurance should be equivalent to the period of contract, commencing from the date of unloading of the first batch of material at the site of construction and expiring on the date of handing over of the contract work to the principal.

• Although it is possible to extend the policy period in case of delay in completion of contract, it is always advisable to choose a slightly longer period of insurance initially, to avoid paying the higher extension premium.

Erection all risk policyFor any construction project, erection is one of the most crucial phases. There are high risk elements associated with erection of machinery, plant etc which can bring about a heavy destruction and damage to property and contribute to huge financial losses to principal and contractors. The erection all risks/strong-cum-erection insurance policy offers a continuous over the various such project starting from the time the consignments leave the warehouse till they are received and erected at the site.

Key benefits:• Cover can be designed according to the specific needs of the project • Optional extensions which can be tailored to suit individual customer's needs • Specialized team of Engineers available to help in implementation of risk management

measures • Dedicated team of Claims specialists • Our presence across the length and breadth of GCC (except Kuwait) • It is also possible to have an annual policy issued for all work undertaken by a contractor

Summary of cover This policy (Section 1) covers risks associated with storage, assembly/erection and testing of Plant and Machinery. EAR insurance provides comprehensive cover. All perils are covered unless specifically excluded. Section 2 of the policy covers legal liability falling on the insured contractor as a result of bodily injury or property damage belonging to a third party.

Sum InsuredSum to be insured is the completely erected value of the plant and machinery inclusive of freight, customs duties and cost of erection.

Period of InsuranceThe cover starts on the unloading of the first consignment at site or commencement of work and continues to be in force as stated in the policy including the test run period. The policy ceases when the project is handed over to the principal or put into service.

On request the policy can be extended to cover various optional extensions viz. Transit to or from the site (excluding sea or air transit), testing and commissioning, maintenance cover, removal of debris costs, architects, surveyors fees for the reinstatement of damage, damage to surrounding property, etc

Corporate InsuranceCoverages?• Fire• Burglary• All risk functional equipment• Cost of data reinstatement• Cash-in-safe• Cash-in-transit• Glass breakage• All risks-non functional items• Fidelity• Cheque forgery• Personal accident• Mediclaim• Public liability• Professional indemnity• Employer’s liability• Tenant’s legal liability

Exclusions?• Under Insurance: In case the actual value of the insured property at the time of loss under

the Fire is found to be greater than the sum insured chosen by you, then, the claim would be proportionally reduced.Willful destruction of- property- loss- damage or destruction caused by war perils- wear and tear- atmospheric conditions.

Liability Insurance Policy

Product liabilitySafety and reliability of products are an important concern to consumers, sellers & manufacturers. Faulty products can be hazardous for the consumers' health & property. The manufacturer/ seller of faulty could be held liable for such damages, exposing themselves to financial losses

Scope of coverLegal liability of the Insured towards damages to the third party arising due to faulty products manufactured / sold by the insured, liability with respect to:• Accidental death• Bodily injury or disease• Loss or damage to property

Legal costs and expenses incurred with the prior consent of the Insurer and within the limit of indemnity.

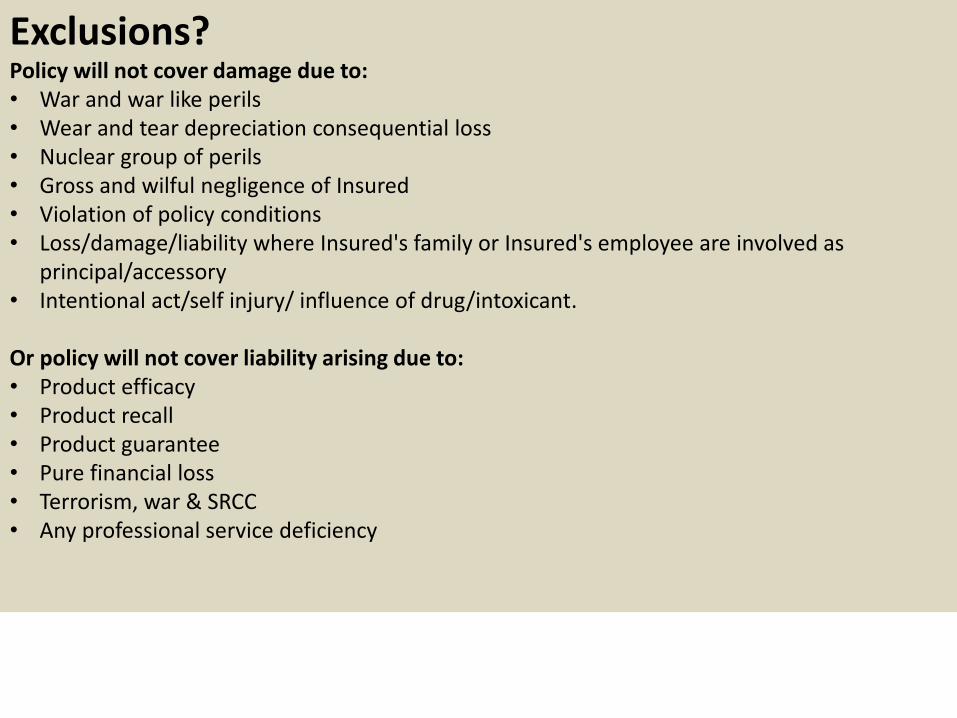

Exclusions?Policy will not cover damage due to:• War and war like perils• Wear and tear depreciation consequential loss• Nuclear group of perils• Gross and wilful negligence of Insured• Violation of policy conditions• Loss/damage/liability where Insured's family or Insured's employee are involved as

principal/accessory• Intentional act/self injury/ influence of drug/intoxicant.

Or policy will not cover liability arising due to:• Product efficacy• Product recall• Product guarantee• Pure financial loss• Terrorism, war & SRCC• Any professional service deficiency

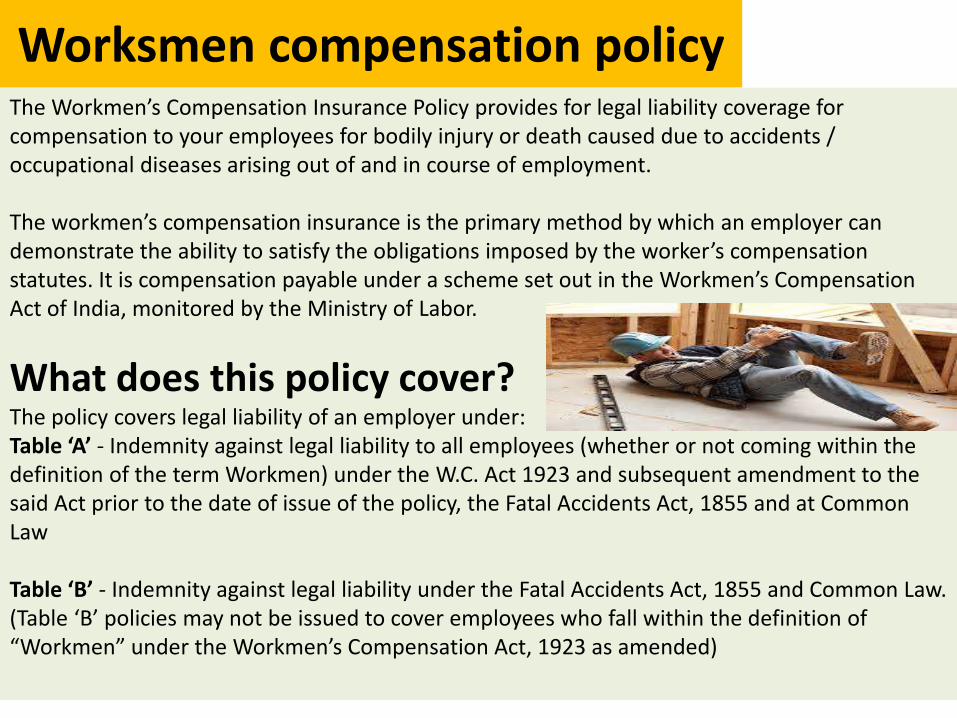

Worksmen compensation policyThe Workmen’s Compensation Insurance Policy provides for legal liability coverage for compensation to your employees for bodily injury or death caused due to accidents / occupational diseases arising out of and in course of employment.

The workmen’s compensation insurance is the primary method by which an employer can demonstrate the ability to satisfy the obligations imposed by the worker’s compensation statutes. It is compensation payable under a scheme set out in the Workmen’s Compensation Act of India, monitored by the Ministry of Labor.

What does this policy cover?The policy covers legal liability of an employer under:Table ‘A’ - Indemnity against legal liability to all employees (whether or not coming within the definition of the term Workmen) under the W.C. Act 1923 and subsequent amendment to the said Act prior to the date of issue of the policy, the Fatal Accidents Act, 1855 and at Common Law

Table ‘B’ - Indemnity against legal liability under the Fatal Accidents Act, 1855 and Common Law. (Table ‘B’ policies may not be issued to cover employees who fall within the definition of “Workmen” under the Workmen’s Compensation Act, 1923 as amended)

Exclusions?• Any injury which does not result in fatality or partial disablement for a period exceeding 3

days • The first 3 days of disablement where the total disablement is less than 28 days• Any non-fatal injury caused by any accident directly attributed to: Influence of drinks or drugs Willful disobedience of an order for securing safety to the workman Willful removal or disregard of a safety guard device War group and nuclear group of perils Liability to employees of contractors of the Insured (unless separately declared and covered) Liability of the Insured assumed under an agreement Occupational Diseases.

PremiumThe Premium rate depends on the Occupation and Wages of the workmen

Sum insuredThe sum insured is calculated on the basis of:• Earnings include wages, salaries, over time, board / lodging, and other perquisites.• No deductions for Pension / PF to be accounted• TA / traveling concessions not to be accounted• No deduction for IT deducted at source

Claim process:• Once you submitted all the required documents, we will acknowledge receipt of the

documents in writing.• We will review the information provided and determine if it is sufficient for us to decide

whether the event is indemnifiable under the policy coverage. During this process, we may request additional information or documentation.

• We may appoint an investigator, loss adjuster or lawyer to investigate the events and circumstances which leading to a claim.

• If the information provided or discovered is sufficient, we will communicate our decision of coverage position and the proposed claim settlement to you in writing.

• Claim payment will be executed upon receiving your confirmation of acceptance

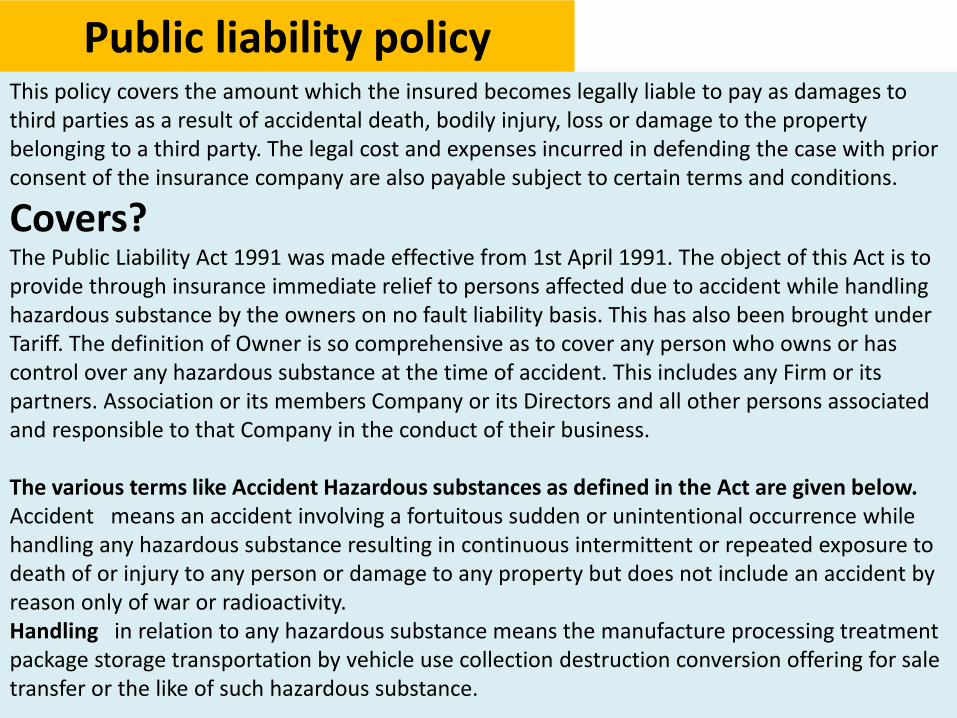

Public liability policyThis policy covers the amount which the insured becomes legally liable to pay as damages to third parties as a result of accidental death, bodily injury, loss or damage to the property belonging to a third party. The legal cost and expenses incurred in defending the case with prior consent of the insurance company are also payable subject to certain terms and conditions.

Covers?The Public Liability Act 1991 was made effective from 1st April 1991. The object of this Act is to provide through insurance immediate relief to persons affected due to accident while handling hazardous substance by the owners on no fault liability basis. This has also been brought under Tariff. The definition of Owner is so comprehensive as to cover any person who owns or has control over any hazardous substance at the time of accident. This includes any Firm or its partners. Association or its members Company or its Directors and all other persons associated and responsible to that Company in the conduct of their business.

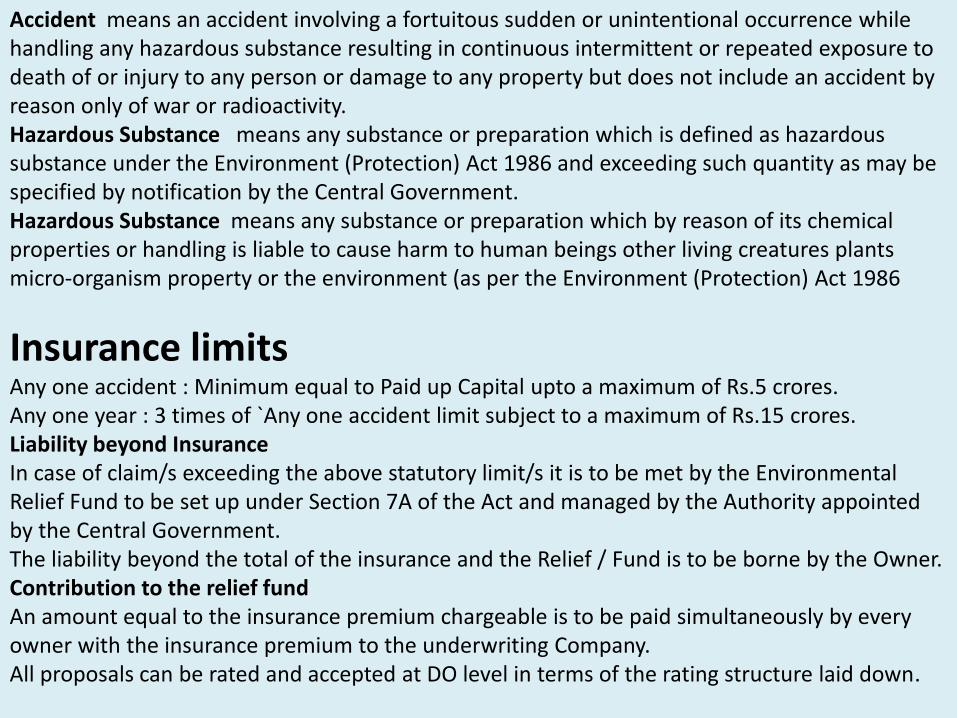

The various terms like Accident Hazardous substances as defined in the Act are given below.Accident means an accident involving a fortuitous sudden or unintentional occurrence while handling any hazardous substance resulting in continuous intermittent or repeated exposure to death of or injury to any person or damage to any property but does not include an accident by reason only of war or radioactivity.Handling in relation to any hazardous substance means the manufacture processing treatment package storage transportation by vehicle use collection destruction conversion offering for sale transfer or the like of such hazardous substance.

Accident means an accident involving a fortuitous sudden or unintentional occurrence while handling any hazardous substance resulting in continuous intermittent or repeated exposure to death of or injury to any person or damage to any property but does not include an accident by reason only of war or radioactivity.Hazardous Substance means any substance or preparation which is defined as hazardous substance under the Environment (Protection) Act 1986 and exceeding such quantity as may be specified by notification by the Central Government.Hazardous Substance means any substance or preparation which by reason of its chemical properties or handling is liable to cause harm to human beings other living creatures plants micro-organism property or the environment (as per the Environment (Protection) Act 1986

Insurance limitsAny one accident : Minimum equal to Paid up Capital upto a maximum of Rs.5 crores.Any one year : 3 times of `Any one accident limit subject to a maximum of Rs.15 crores.Liability beyond InsuranceIn case of claim/s exceeding the above statutory limit/s it is to be met by the Environmental Relief Fund to be set up under Section 7A of the Act and managed by the Authority appointed by the Central Government.The liability beyond the total of the insurance and the Relief / Fund is to be borne by the Owner.Contribution to the relief fundAn amount equal to the insurance premium chargeable is to be paid simultaneously by every owner with the insurance premium to the underwriting Company.All proposals can be rated and accepted at DO level in terms of the rating structure laid down.

Claim process:• Once you submitted all the required documents, we will acknowledge receipt of the

documents in writing.• We will review the information provided and determine if it is sufficient for us to decide

whether the loss or damage can be indemnified under the policy coverage. During this process, we may request additional information or documentation.

• We may appoint an investigator, loss adjuster or lawyer to investigate the events and circumstances that have lead to the claim.

• If the information provided or discovered is sufficient, we will communicate our decision of coverage position and the proposed claim settlement to you in writing.

• Claim payment will be executed upon receiving your confirmation of acceptance

Professional indemnityThis policy is meant for professionals to cover liability falling on them as a result of errors and omissions committed by them whilst rendering professional service.The policy offers a benefit of Retroactive period on continuous renewal of policy whereby claims reported in subsequent renewal but pertaining to earlier period after first inception of the policy, also become payable.Group policies can also be issued covering members of one profession. Group discount in premium is available depending upon the number of members covered.

Who can be Insured ?• Doctors• Medical Establishments• Engineers• Architects• Chartered Accountants• Lawyers

Covers?The cover granted under the policy provide indemnity for legal liability to third party arising out of errors and omissions or negligence in professional service rendered by the insuredPolicies will be issued for a period of 12 months (1 year).

Exclusions?Applicable in case of Doctors Policy• Any criminal act or violation of any Act of Statute• Services rendered under the influence of intoxicants or narcotics• Performance by Dentists under general anesthesia or any procedures carried out under

general anesthesia unless performed in a hospital.• Willful neglect or deliberate act• Third Party Public Liability• Pure financial loss due to loss of goodwill or loss of market• Acts committed under Influence of intoxicants / narcotics• Weight reduction• Criminal acts• Plastic surgery• HIV aids• Non compliance with statuotry provisions• Blood banks• Radioactivity• Punitive and exemplary damages

Claim procedure:• Once you submitted all the required documents, we will acknowledge receipt of the

documents in writing.• We will review the information provided and determine if it is sufficient for us to decide

whether the loss or damage can be indemnified under the policy coverage. During this process, we may request additional information or documentation.

• We may appoint an investigator, loss adjuster or lawyer to investigate the events and circumstances that have lead to the claim.

• If the information provided or discovered is sufficient, we will communicate our decision of coverage position and the proposed claim settlement to you in writing.

• Claim payment will be executed upon receiving your confirmation of acceptance.

Errors and omission (E&O)A professional liability insurance that protects companies and individuals against claims made by clients for inadequate work or negligent actions. Errors and omissions insurance often covers both court costs and any settlements up to the amount specified on the insurance contract.

What is covered? What is not covered?Alleged or actual negligence Bodily injury or property damageDefense costs Fraudulent actsPersonal injury (e.g., libel or slander) Employment mattersCopyright infringement False advertisingWorldwide errors and omissions insurance coverage

Patents and trade secrets

Temporary staff and independent contractors Personally identifiable information

Claims arising from services provided in the past

Other services

Claims and damages

Directors & officers liability insurance (D&O)

Directors and officers are fiduciaries of the corporation they serve and therefore, carry with them a host of legal obligations that can result in loss exposures for cor5porate wrong doing. They can be held personally and financially liable for actual or alleged breach of duty in the course of managing the affairs of a corporation and ensuring its compliance with the numerous loss and regulations that govern its operation.

Covers:• Against any loss that the Organization may incur, on account of mistaken actions taken in

their individual capacity as Directors & Officers in pursuance of their duties under Memorandum and Articles of Association.

• Against loss arising from claims made against them by reason of any wrongful Act in their Official capacity.

• Legal costs & expenses incurred with the written consent of the insurers arising out of prosecution (criminal or otherwise) of any Director/officer and attendance at any investigation, examination, inquiry or other proceedings by the authority empowered to do so.

• Expenses incurred by any shareholder of the Company in pursuance of a claim against any Director/Officer, which the Company is legally obliged to pay, pursuant to an order of a Court.

• Provide indemnity to the estate of, legal heirs or legal representatives of the Director / officer in the event of the Director / officer becoming insolvent.

Exclusion• Any bodily injury ,sickness, disease or death of any person or any damage to tangible

property• Dishonest, fraudulent, criminal or malicious act.• Personal guarantee.• Libel and slander• Personal injury and damage to property.• Pollution damage• Directly resulting from goods or products manufacture or sold by the company• Fines, penalties, punitive or exemplary damages.• Any circumstances existing prior to inception date of policy

PremiumPremium depends on profile of the client, the Sum Insured selected, present and past functioning of the company, information in the balance sheet and annual report, degree of exposure etc.

Special Conditions1.Directors and the Company shall give to underwriters immediate notice in writing of any claim.2.Directors and the Company shall not disclose to anyone the existence of the policy without underwrites' consent.3.Directors of the Company shall not be required to contest any legal proceedings Counsel shall advise that such proceedings should be contested.4.Underwriters shall not settle any claim without the consents of the Directors or the Company.

Claim procedure:• Once you submitted all the required documents, we will acknowledge receipt of the

documents in writing.• We will review the information provided and determine if it is sufficient for us to decide

whether the loss or damage can be indemnified under the policy coverage. During this process, we may request additional information or documentation.

• We may appoint an investigator, loss adjuster or lawyer to investigate the events and circumstances that have lead to the claim.

• If the information provided or discovered is sufficient, we will communicate our decision of coverage position and the proposed claim settlement to you in writing.

• Claim payment will be executed upon receiving your confirmation of acceptance

Money insurance

Scope of coverThe Insurance Policy broadly covers loss of money in transit by the insured or insured's authorized employee(s) occasioned by robbery, theft or any other fortuitous cause.

Sum InsuredSum insured should represent estimated total annual amount of the Money in transit.Separate Sum Insured also needs to be given for the maximum amount of money held in safe and in counter. Single carrying limit, which is the Company's limit of liability for any one loss, is also required to be specified in the policy.

PremiumPremium chargeable depends on single carrying limit, distance involved and security measures adopted

Significant ExclusionsThe Insurance Policy does not cover losses and /or damages due to floods, cyclones, earthquakes and other convulsions of nature, war and war like operations, civil commotion, riots and strikes and terrorist activities, shortage due to error, omission, by use of keys to safe(s) or strong room (unless such keys are obtained by force or threat), whilst being carried under contract of affreightment, theft from unattended vehicle and consequential loss.

Credit insuranceOur Credit Insurance (Globalliance) Policy is designed for companies that are selling their goods and/or services on credit to overseas buyers. This policy provides coverage to companies for outstanding receivables that are within approved credit terms, thereby protecting the Insured against non-payment risk by its buyers.

Scope of coverThe policy covers loss due to any or all of the following risks:

Commercial risk• Non payment by the buyer• Insolvency of the buyer

Political risk• Military or civil war, revolution, riot or insurrection• General moratorium on payment by the government of buyer's country• Cancellation of import license• Government decision preventing performance• Political events, economic difficulties, legislative or administrative measures preventing

payment• Non payment by government buyer

PremiumThe premium is expressed as in a rate in % of insurable turnover• Extent of courage sought• 70% / 80% / 90% of the individual bill• Risk taking of business sector• Countries included in the portfolio• Insured turnover• Trade losses of insured

Exclusions• Non payment arising due to trade disputes• Sales to a private individual who intends to use the goods or service for non-professional