instructional fs ipi curriculum development reportpkatia/fouryeararchives/_overview/final... ·...

TRANSCRIPT

i

Instructional FS‐IPI Curriculum Development Report (March 31, 2008)

© 2008 Dr. Katia Passerini, Dr. Asokan Anandarajan New Jersey Institute of Technology

ii

TABLE OF CONTENTS I. OVERVIEW..........................................................................................................................................................1

II. PROJECT BACKGROUND ..........................................................................................................................1

III. REQUIREMENTS DEFINITION ...................................................................................................................2 “SETTING THE STAGE”...............................................................................................................................................3 “REQUIREMENTS” ......................................................................................................................................................3

IV. APPROACH TO CURRICULUM DEVELOPMENT (4-YEAR COLLEGES) .........................................4

V. INSTRUCTIONS ON HOW TO USE THE MODULES..............................................................................6

VI. EVALUATION RESULTS..............................................................................................................................7

VII. CONCLUSIONS............................................................................................................................................16

VIII. PROJECT TEAM ..........................................................................................................................................16

IX. APPENDICES ...............................................................................................................................................17 APPENDIX A: NJ FINANCE CURRICULA BENCHMARK .............................................................................................17 APPENDIX B: SURVEY RESULTS AND CURRICULUM APPROACH............................................................................17 APPENDIX C: TEAM LEARNING MODULE AND ACTIVITIES ......................................................................................17 APPENDIX D: PROJECT MANAGEMENT MODULE AND ACTIVITIES..........................................................................17 APPENDIX E: FINANCIAL CONTROLS IN PROJECT MANAGEMENT MODULE AND ACTIVITIES ...................................17 APPENDIX F: BUSINESS ETHICS IN FINANCE MODULE AND ACTIVITIES ..................................................................17

1

I. Overview

Our team developed an integrated set of multidisciplinary learning modules for

teaching undergraduate students fundamental skills that are required for easing

an entry in financial industry job positions in New Jersey. Benefits of these

learning modules include:

Brief overview materials that can be easily integrated within existing courses

and curricula;

Enhancement of learning through simultaneous use of various media, within

a self-paced learning environment;

Easy replication and customization of the modules in various courses.

II. Project background

Governor Corzine announced an Economic Growth Strategy for New Jersey in

2007. The governor announced six key priority areas. Of the six, the area of

interest to this proposal relates to the governor’s initiative to improve the training

received by students in four year colleges in New Jersey. A Notice of Grant

Opportunity was issued by the New Jersey Commission on Higher Education

with funding from the state’s Department of Education and the Department of

Labor and Workforce Development to implement a strategy to (1) make NJ

colleges understand what is required of them, and (2) increase the soft and

creative thinking skills of students. Within the financial industry sector, a

curriculum development grant was awarded to a coalition including the New

Jersey Institute of Technology with the objective to develop new curricula that

offer students ways to improve vital skills of today’s job market.

This project is considered important because, currently, the chasm between

developments and innovation in the finance industry and the curriculum taught at

educational institutions in New Jersey is perceived to be gradually widening. For

this project, educational institutions are defined as high schools, community

2

colleges and four year colleges in this state. The finance industry is defined as

those companies involved in the creation, liquidation and protection of financial

assets. Based on this definition, the finance industry is assumed to comprise the

banking, insurance and commodities sectors. Developments in the finance

industry are characterized by continuously evolving technology, increasingly

complex laws and increased competition in the form of globalization. To meet

these changes, employers are now looking for personnel with high levels of

computerized technical skill, greater knowledge of the complex laws that govern

their activities and an ability to attract and enhance the customer base.

The purpose of this grant is to develop curricula at the high school, community

college, and four year college level that meets the increased skill demands of

industrialists. To attain this objective, we adopted a three step strategy:

• Study the current curricula offered by selected high schools, community

colleges and colleges offering four year programs with respect to finance and

finance related courses.

• Speak to industrialists and critically assess their specific needs and

requirements of potential new recruits.

• Develop curricula at the high school, community college and college level that

meets the heightened skill requirements of industry.

These steps are discussed in more detail in the next section.

III. Requirements Definition

The development of this project required a phased approach to curriculum

development. This approach started with some preliminary background research

(“setting the stage”) and continued through various phases of requirements

definition, refinement, curriculum design, feedback and testing.

3

“Setting the Stage”

During this initial phase, we conducted some background research to better

understand finance curricula across New Jersey 4-year institutions, and thus

identify potential gaps.

In summary, during this initial stage, our group

Identified a group of colleges offering financial programs to insert in a

quick benchmark.

Developed a preliminary list of the types of courses currently taught

(and the frequency by which they are taught) in NJ colleges.

The findings listed in Appendix A show that while many fundamental courses

are offered by multiple institutions; only a few colleges offered novel international

and financial ethics specialty courses.

“Requirements”

Several meetings were held with key partners in the financial sector in New

Jersey to identify recurrent needs that should be addressed by new curricula. At

least three focus groups were held to gather requirements and to obtain

feedback on proposed activities. In addition, a survey was developed to also

obtain information about curriculum needs by a larger audience. Appendix B

provides a list of the findings from the survey and focus groups activities. The

results of the survey mostly matched the information obtained in the focus

groups, and more specifically:

Key skills needed: The various financial services (FS) stakeholders

have provided feedback that specialized financial skills while vital, are

not as crucial, since such technical skills can be provided to new

recruits in the form of “on the job” training. However, “soft” skills are

more difficult to absorb in a “on the job rapid crash course”. Such soft

skills have to be nurtured over a period of time. Four year colleges in

New Jersey are in the best position to enhance the vital soft skills and

4

creative thinking ability required of new graduates. Currently

discussions with FS representatives reveal that there is an

“expectations gap” between what they, as potential employers expect

from new graduates, and the skills New Jersey colleges think they

should provide. The expectations of four year colleges with respect to

skill development do not come close to the expectations of employers

and this program is a preliminary milestone to achieve alignment. In

particular, FS spokespersons identified a set of crucial skills that they

would like be nurtured by academic institutions. These skills include:

(a) Communication skills, both oral and writing,

(b) Skills relating to conduct (including mode of dress and proper

business etiquette);

(c) Ability to deal with peers, superiors and subordinates;

(d) Ability to understand different cultures when dealing with people

of different international backgrounds;

(e) Ability to engage in critical thinking;

(f) Lateral thinking in problem solving;

(g) Knowing how to work effectively in a team; and

(h) Overall integrity in the work place environment

Reusability Of The Program. Another critical need established by the

grant was to prepare instructional materials that were generic enough

to be accessible and reusable by various institutions in NJ. Portability Of The Program. Accessibility and re-usability also

required that the program was accessible in multiple formats.

IV. Approach to Curriculum Development (4-year colleges)

To address the requirements, we developed four (4) short instructional modules

that could be easily integrated into existing curricula. The modules included:

5

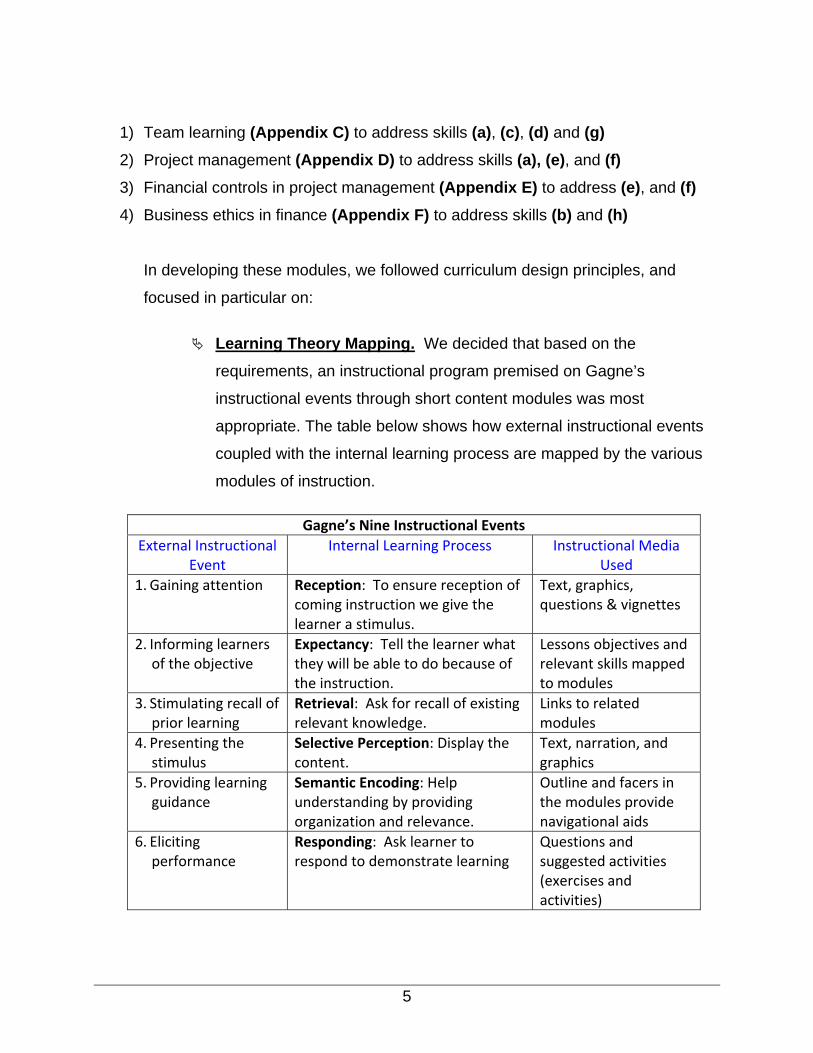

1) Team learning (Appendix C) to address skills (a), (c), (d) and (g) 2) Project management (Appendix D) to address skills (a), (e), and (f) 3) Financial controls in project management (Appendix E) to address (e), and (f) 4) Business ethics in finance (Appendix F) to address skills (b) and (h)

In developing these modules, we followed curriculum design principles, and

focused in particular on:

Learning Theory Mapping. We decided that based on the

requirements, an instructional program premised on Gagne’s

instructional events through short content modules was most

appropriate. The table below shows how external instructional events

coupled with the internal learning process are mapped by the various

modules of instruction.

Gagne’s Nine Instructional Events External Instructional

Event Internal Learning Process Instructional Media

Used 1. Gaining attention Reception: To ensure reception of

coming instruction we give the learner a stimulus.

Text, graphics, questions & vignettes

2. Informing learners of the objective

Expectancy: Tell the learner what they will be able to do because of the instruction.

Lessons objectives and relevant skills mapped to modules

3. Stimulating recall of prior learning

Retrieval: Ask for recall of existing relevant knowledge.

Links to related modules

4. Presenting the stimulus

Selective Perception: Display the content.

Text, narration, and graphics

5. Providing learning guidance

Semantic Encoding: Help understanding by providing organization and relevance.

Outline and facers in the modules provide navigational aids

6. Eliciting performance

Responding: Ask learner to respond to demonstrate learning

Questions and suggested activities (exercises and activities)

6

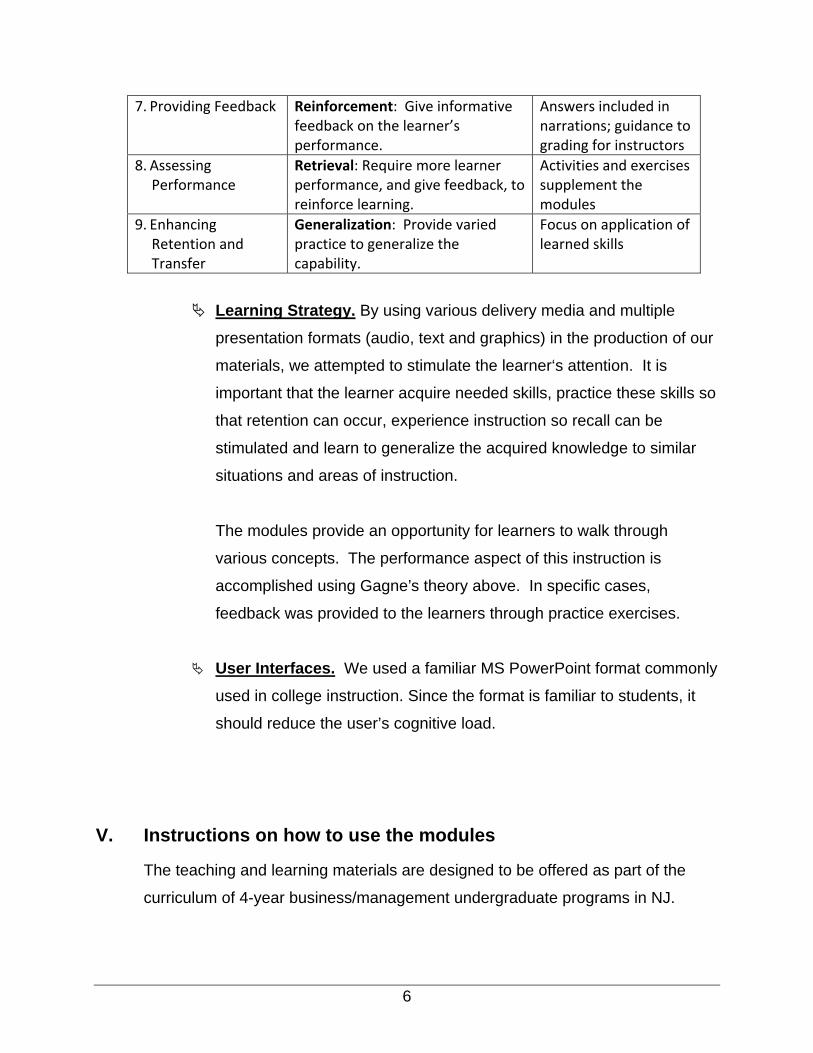

7. Providing Feedback Reinforcement: Give informative feedback on the learner’s performance.

Answers included in narrations; guidance to grading for instructors

8. Assessing Performance

Retrieval: Require more learner performance, and give feedback, to reinforce learning.

Activities and exercises supplement the modules

9. Enhancing Retention and Transfer

Generalization: Provide varied practice to generalize the capability.

Focus on application of learned skills

Learning Strategy. By using various delivery media and multiple

presentation formats (audio, text and graphics) in the production of our

materials, we attempted to stimulate the learner‘s attention. It is

important that the learner acquire needed skills, practice these skills so

that retention can occur, experience instruction so recall can be

stimulated and learn to generalize the acquired knowledge to similar

situations and areas of instruction.

The modules provide an opportunity for learners to walk through

various concepts. The performance aspect of this instruction is

accomplished using Gagne’s theory above. In specific cases,

feedback was provided to the learners through practice exercises.

User Interfaces. We used a familiar MS PowerPoint format commonly

used in college instruction. Since the format is familiar to students, it

should reduce the user’s cognitive load.

V. Instructions on how to use the modules

The teaching and learning materials are designed to be offered as part of the

curriculum of 4-year business/management undergraduate programs in NJ.

7

The short (elective) study modules can be integrated within existing courses to

increase access to concepts that are fundamental pre-requisites to a smooth

entry in the financial industry job market.

Each module consists of a ‘narrated lecture’ supported by a MS PowerPoint

presentation on the specific topic area. The narrations are roughly 30-minute

long and can be accessed on-line or can be downloaded and played off-line.

Multiple file formats allow interoperability across various platforms (i-tunes, MP3

and MP4-video and Windows Media Files .WMV)

The modules include supplementary materials such as case studies, exercises,

vignettes, and other activities. These activities are separate from the lecture

materials and instructors have the flexibility to select which activities are more

relevant to their courses.

Copies of the narrations, PowerPoint presentations and exercises are accessible

at http://web.njit.edu/~pkatia/FourYearArchives/ (3/31/2008)

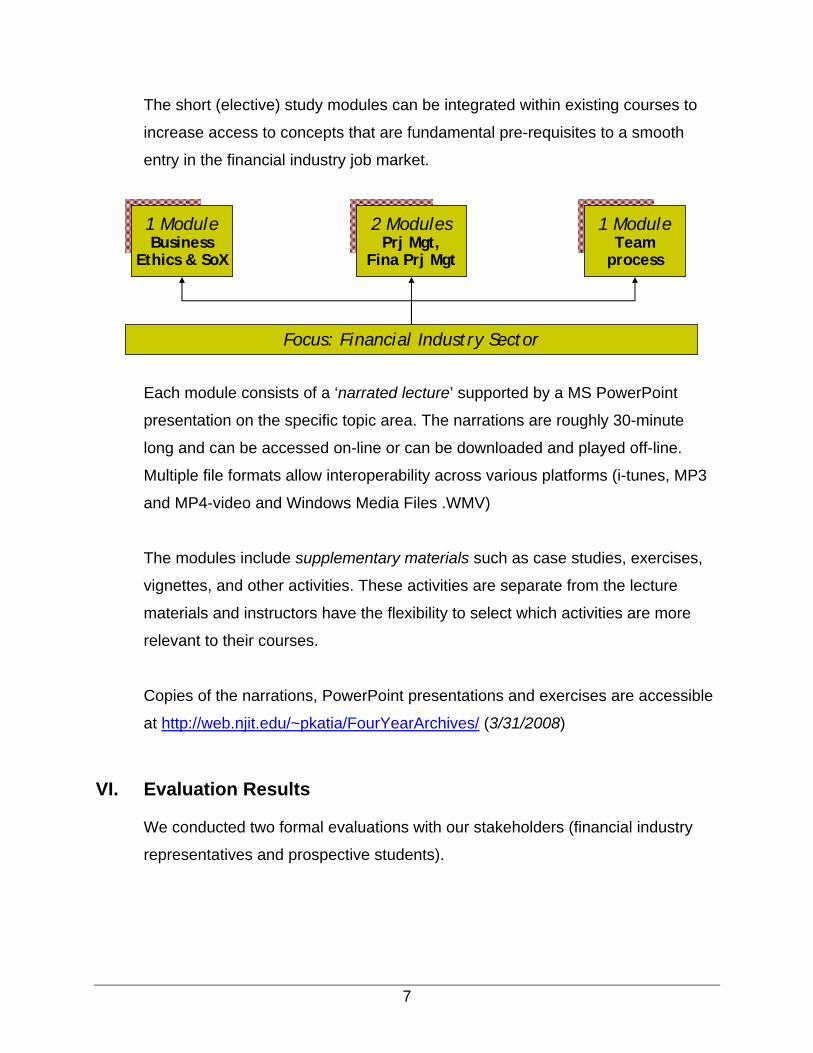

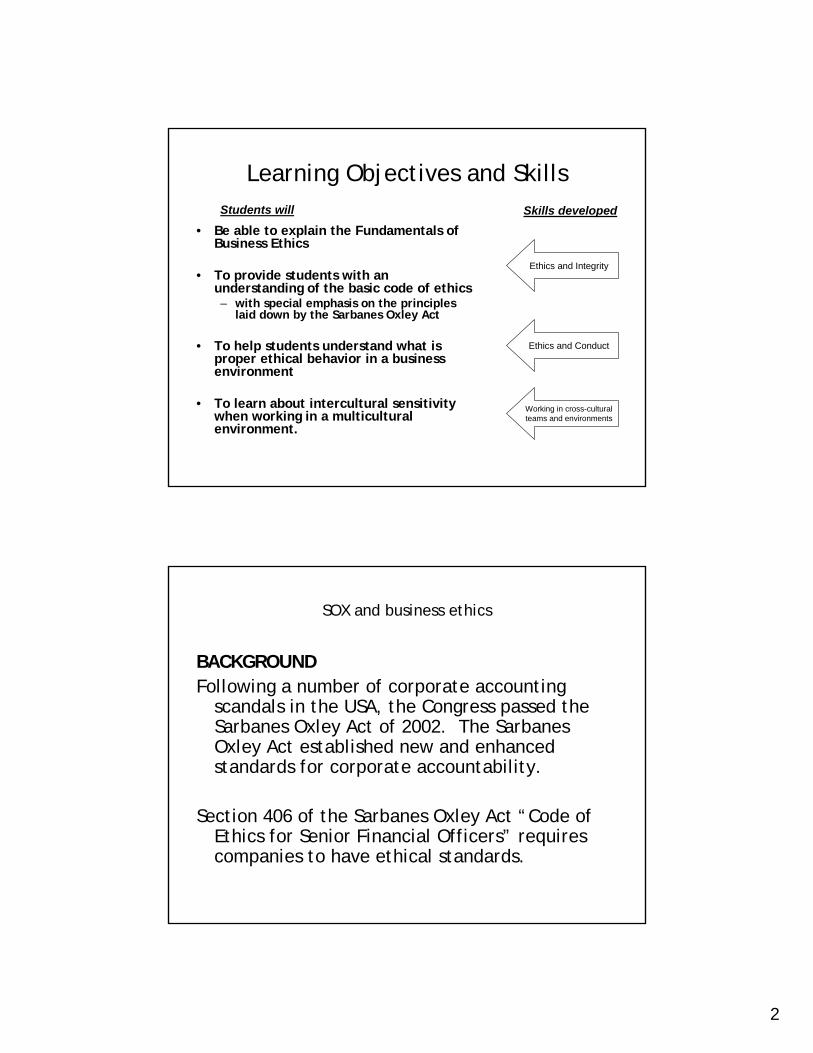

VI. Evaluation Results

We conducted two formal evaluations with our stakeholders (financial industry

representatives and prospective students).

1 ModuleBusiness

Ethics & SoX

1 ModuleTeam

process

2 ModulesPrj Mgt,

Fina Prj Mgt

Focus: Financial Industry Sector

8

1. Formative Evaluation. Feedback from the FS stakeholders

A meeting about curriculum proposals was held with FS stakeholders during Fall

2007. The participants expressed satisfaction with the progress of the project.

However, they also expressed concern whether, given the resources available

the project could be completed to the satisfaction of all parties. Gale Spak of the

New Jersey Institute of Technology stated that she would be applying for an

extension. In essence, the FS stakeholders noted that ethics was important and

using SoX, which, in their opinion, is one of the landmark legislation of our time,

was a good idea. This would provide students with an initial exposure to ethical

standards of behavior required by SoX and highlight the importance of this

legislation. It was also noted that some aspects of inter-cultural sensitivity should

be addressed as this was lacking in the presentation. FS stakeholders also

expressed satisfaction with the project management modules stating that it was

well developed, lucid and cogently worded.

In a follow up meeting that presented an almost final draft of the curriculum

(March 17, 2008), the FS stakeholders reviewed the curriculum and requested

minor changes to the materials presented. These changes have been included in

the final version of the instructional resources.

2. Summative Evaluation. Pilot tests outcomes (for three modules)

To test the impact of the instructional experience, the modules were presented to

students attending courses in the School of Management during Spring 2008. In

general, students reviewed the lectures, downloaded the instructional materials

(a copy of the MS PowerPoint) to support their review of the narrations, and

completed specific activities.

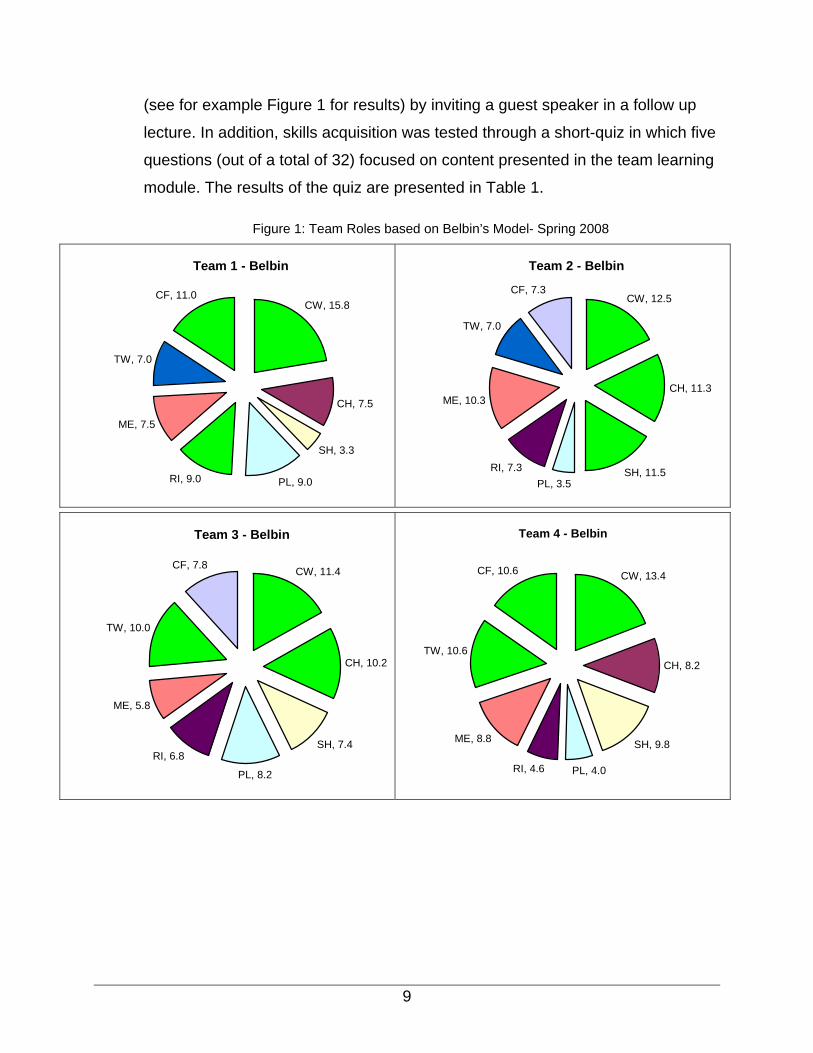

With regard to the Team Learning module, students identified their preferred

team-roles (through a sample Belbin profile activity) and discussed the results

with the instructor. The teams were highly engaged with the activities and an

additional class section was spent assessing the implications of the team-profiles

9

(see for example Figure 1 for results) by inviting a guest speaker in a follow up

lecture. In addition, skills acquisition was tested through a short-quiz in which five

questions (out of a total of 32) focused on content presented in the team learning

module. The results of the quiz are presented in Table 1.

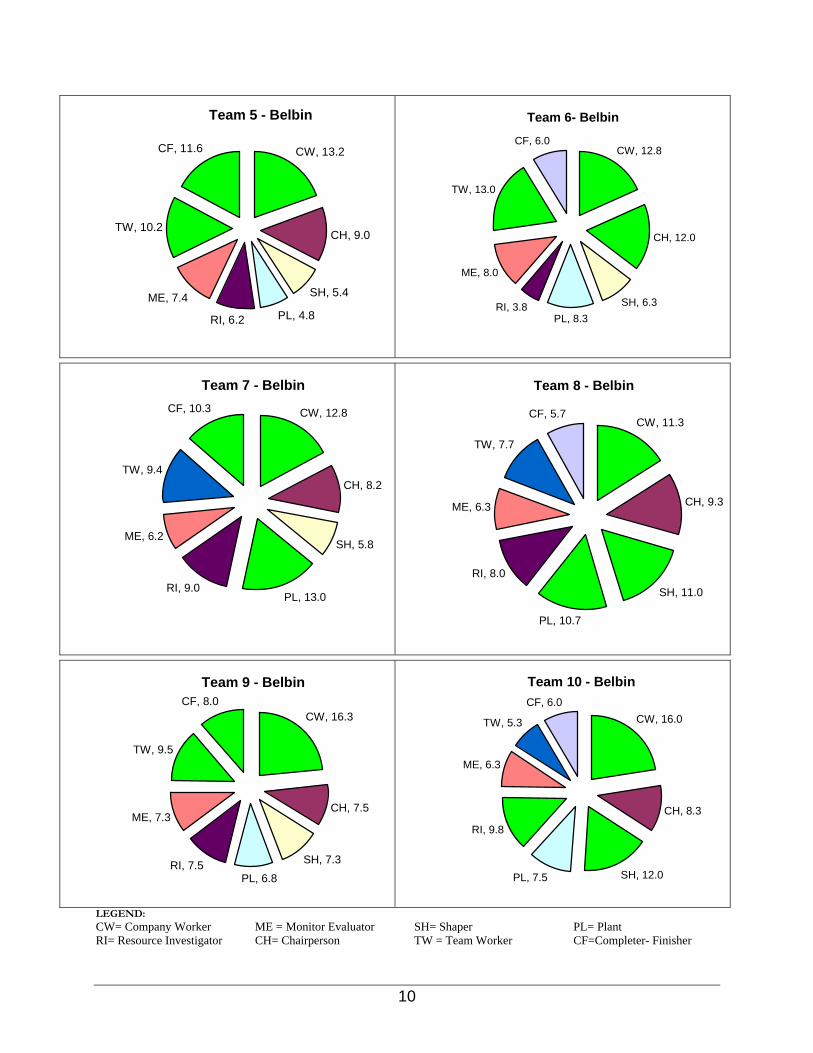

Figure 1: Team Roles based on Belbin’s Model- Spring 2008

Team 1 - Belbin

CW, 15.8

CH, 7.5

SH, 3.3

PL, 9.0RI, 9.0

ME, 7.5

TW, 7.0

CF, 11.0

Team 2 - Belbin

CW, 12.5

CH, 11.3

SH, 11.5PL, 3.5

RI, 7.3

ME, 10.3

TW, 7.0

CF, 7.3

Team 3 - Belbin

CW, 11.4

CH, 10.2

SH, 7.4

PL, 8.2

RI, 6.8

ME, 5.8

TW, 10.0

CF, 7.8

Team 4 - Belbin

CW, 13.4

CH, 8.2

SH, 9.8

PL, 4.0RI, 4.6

ME, 8.8

TW, 10.6

CF, 10.6

10

Team 5 - Belbin

CW, 13.2

CH, 9.0

SH, 5.4

PL, 4.8RI, 6.2

ME, 7.4

TW, 10.2

CF, 11.6

Team 6- Belbin

CW, 12.8

CH, 12.0

SH, 6.3PL, 8.3

RI, 3.8

ME, 8.0

TW, 13.0

CF, 6.0

Team 7 - Belbin

CW, 12.8

CH, 8.2

SH, 5.8

PL, 13.0RI, 9.0

ME, 6.2

TW, 9.4

CF, 10.3

Team 8 - Belbin

CW, 11.3

CH, 9.3

SH, 11.0

PL, 10.7

RI, 8.0

ME, 6.3

TW, 7.7

CF, 5.7

Team 9 - Belbin

CW, 16.3

CH, 7.5

SH, 7.3

PL, 6.8RI, 7.5

ME, 7.3

TW, 9.5

CF, 8.0

Team 10 - Belbin

CW, 16.0

CH, 8.3

SH, 12.0PL, 7.5

RI, 9.8

ME, 6.3

TW, 5.3

CF, 6.0

LEGEND: CW= Company Worker ME = Monitor Evaluator SH= Shaper PL= Plant RI= Resource Investigator CH= Chairperson TW = Team Worker CF=Completer- Finisher

11

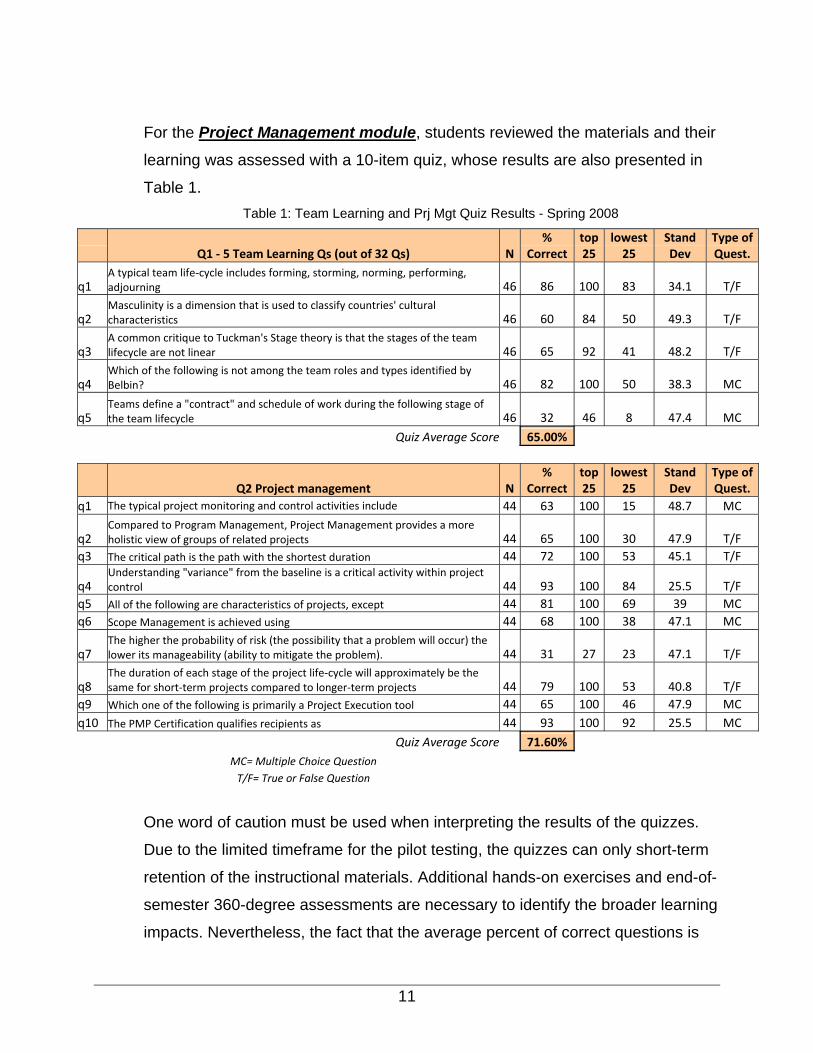

For the Project Management module, students reviewed the materials and their

learning was assessed with a 10-item quiz, whose results are also presented in

Table 1. Table 1: Team Learning and Prj Mgt Quiz Results - Spring 2008

Q1 ‐ 5 Team Learning Qs (out of 32 Qs) N%

Correcttop 25

lowest 25

Stand Dev

Type of Quest.

q1 A typical team life‐cycle includes forming, storming, norming, performing, adjourning 46 86 100 83 34.1 T/F

q2 Masculinity is a dimension that is used to classify countries' cultural characteristics 46 60 84 50 49.3 T/F

q3 A common critique to Tuckman's Stage theory is that the stages of the team lifecycle are not linear 46 65 92 41 48.2 T/F

q4 Which of the following is not among the team roles and types identified by Belbin? 46 82 100 50 38.3 MC

q5 Teams define a "contract" and schedule of work during the following stage of the team lifecycle 46 32 46 8 47.4 MC

Quiz Average Score 65.00%

Q2 Project management N%

Correcttop 25

lowest 25

Stand Dev

Type of Quest.

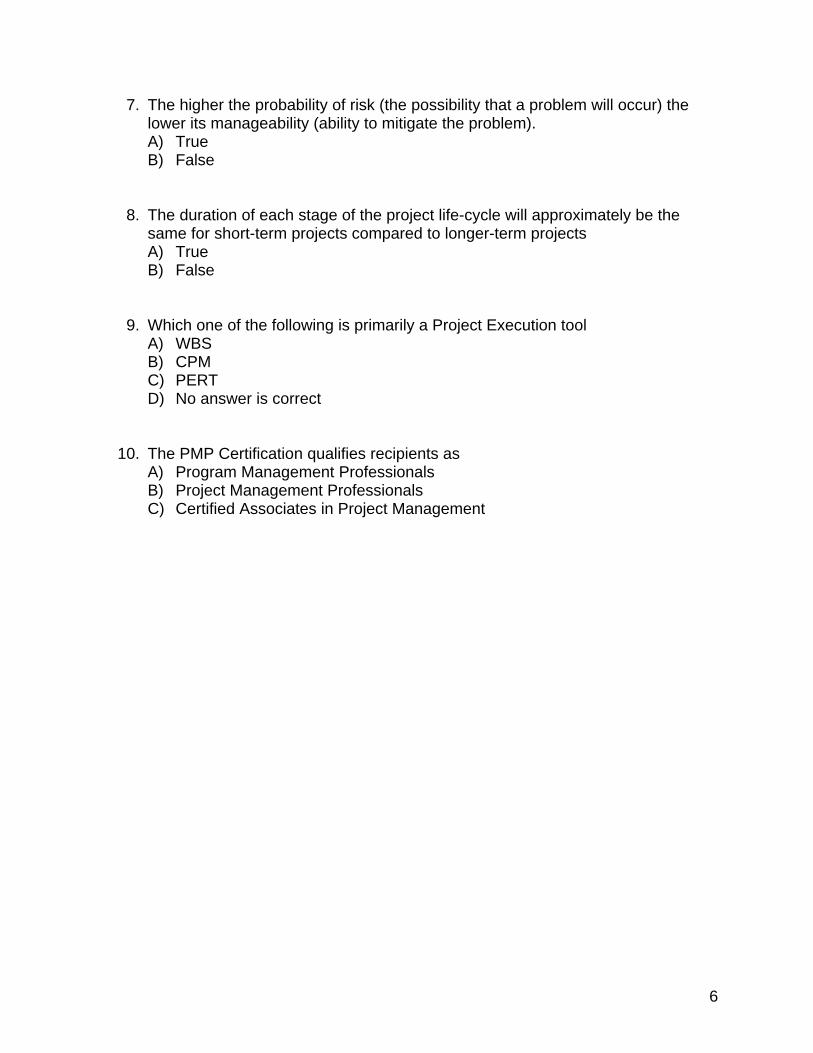

q1 The typical project monitoring and control activities include 44 63 100 15 48.7 MC

q2 Compared to Program Management, Project Management provides a more holistic view of groups of related projects 44 65 100 30 47.9 T/F

q3 The critical path is the path with the shortest duration 44 72 100 53 45.1 T/F

q4 Understanding "variance" from the baseline is a critical activity within project control 44 93 100 84 25.5 T/F

q5 All of the following are characteristics of projects, except 44 81 100 69 39 MC q6 Scope Management is achieved using 44 68 100 38 47.1 MC

q7 The higher the probability of risk (the possibility that a problem will occur) the lower its manageability (ability to mitigate the problem). 44 31 27 23 47.1 T/F

q8 The duration of each stage of the project life‐cycle will approximately be the same for short‐term projects compared to longer‐term projects 44 79 100 53 40.8 T/F

q9 Which one of the following is primarily a Project Execution tool 44 65 100 46 47.9 MC q10 The PMP Certification qualifies recipients as 44 93 100 92 25.5 MC

Quiz Average Score 71.60% MC= Multiple Choice Question T/F= True or False Question

One word of caution must be used when interpreting the results of the quizzes.

Due to the limited timeframe for the pilot testing, the quizzes can only short-term

retention of the instructional materials. Additional hands-on exercises and end-of-

semester 360-degree assessments are necessary to identify the broader learning

impacts. Nevertheless, the fact that the average percent of correct questions is

12

about 65 percent (for the team learning module) and 72 percent (for the project

management module) shows that the materials presented in these modules are a

necessary addition to the curriculum (as a few students continue to lack skills in

the area) and additional follow up and in-class discussion is needed to foster

long-term retention.

In the module Fundamentals of Business Ethics, students practiced with a

series of case studies in a classroom situation. The students who had

accounting classes previously were asked to respond and provide their answers

to the mini case studies in the module. The purpose was to examine if existing

accounting courses had provided the students with a basic understanding of

business ethics as espoused by the Sarbanes Oxley Act. The accounting

courses follow the same syllabi as courses conducted in other four year colleges.

So, the assumption is that the knowledge of the students who participated in this

survey is representative of the four year college population in general. The

results were as follows: Mini Case Study 1: A partner of the firm conducting an audit was provided a gift of

season tickets by the managers of the company he was auditing. Question: Does this

meet ethical standards?

Virtually all of the respondents (91%) answered correctly that this was not ethical

as it would create the impression that decisions could be improperly influenced.

Mini Case Study 2: A partner of the firm conducting an audit was paid in stock rather

than cash. Question: Does this meet ethical standards?

The respondents were split. However 54% said they did not see anything wrong

with this and hence, was not a violation of ethical standards. The rationale was

that the partner would now be very concerned with the company performance.

The answer was that this is now not allowed under SOX (section 206). The

partner would now be vulnerable to pressure from the client company since both

parties benefit if stock price increases.

Mini Case Study 3: In this case siblings of the partner of an audit firm had stock in the

company that their brother was auditing. Question: Does this meet ethical standards?

About 52% answered that they did not see anything wrong with this. Hence, the

class was split almost equally. The correct answer is that this is defined as

13

related third party transactions, which, under SOX, is not considered ethical and

not allowed.

Mini Case Study 4: An employee borrows a computer, uses it and returns it in extremely

good condition. Question: Does this meet ethical standards?

About 71% answered correctly that this was not ethical since she did not get

permission for using it. This comes under misuse of company assets by its

custodians. Use by an employee of physical assets for which the employee

might benefit is forbidden under SOX.

Mini Case Study 5: Same as before except that students were told that the employee

borrowed a computer with the permission of her immediate superior.

Question: Does this meet ethical standards?

About 98% of the respondents answered that this was now appropriate and

ethical since permission had been obtained. This was the question most

students answered incorrectly. Under SOX the use of assets for which an

employee is custodian, must be justified and approved by two levels of

management above the employee concerned. This is because the employee

may be friendly with the boss directly in charge of that person which could result

in “collusion”. This is more difficult when another level is involved.

Mini Case Study 6: A manager of a company tells friends who have stock in the

company about potential bad news regarding the company. The friends immediately sell

their stock. Question: Does this meet ethical standards?

The majority of students (78%) got this correct saying it was not ethical; 22%

thought it was still acceptable because the manager did not benefit personally.

SOX characterizes this as insider trading. Even though the manager did not

personally profit from disclosing information and hence, did not violate the law,

his action is still a violation of business ethic according to SOX.

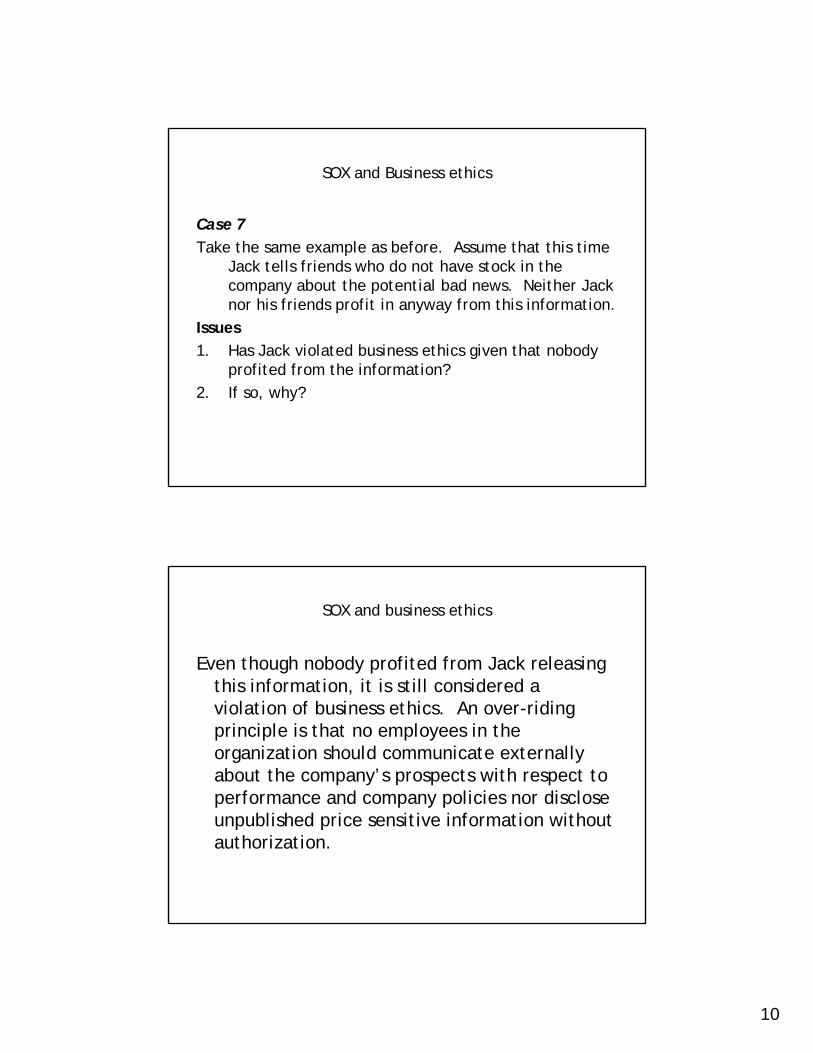

Mini Case Study 7: The manager tells students who do not have stock in the company

about the potential bad news. Nobody profited from the information

Question: Does this meet ethical standards?

Approximately 42% of the students got this correct and said this was

inappropriate while 58% said it was not a violation since nobody benefited. Even

though nobody profited from the manager releasing this information, it is still a

violation of ethics according to SOX since an over-riding principle in SOX is that

14

no employee in the organization should communicate externally with respect to

company performance or policy.

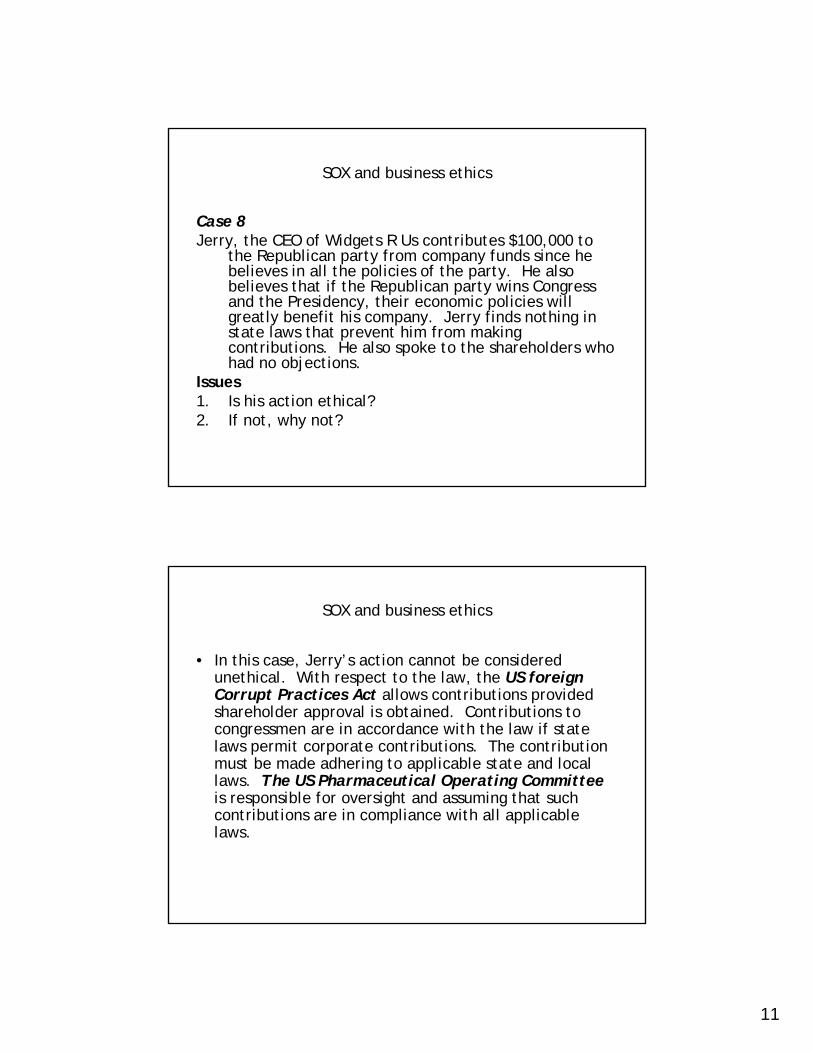

Mini Case Study 8: The CEO of a company contributes a donation to a political party.

The shareholders had no objections. Question: Does this meet ethical standards?

The overwhelming majority of students (88%) said that they saw nothing wrong

with this. They are correct; SOX mentions the US Foreign Practices Act which

allows contributions provided shareholder approval is obtained.

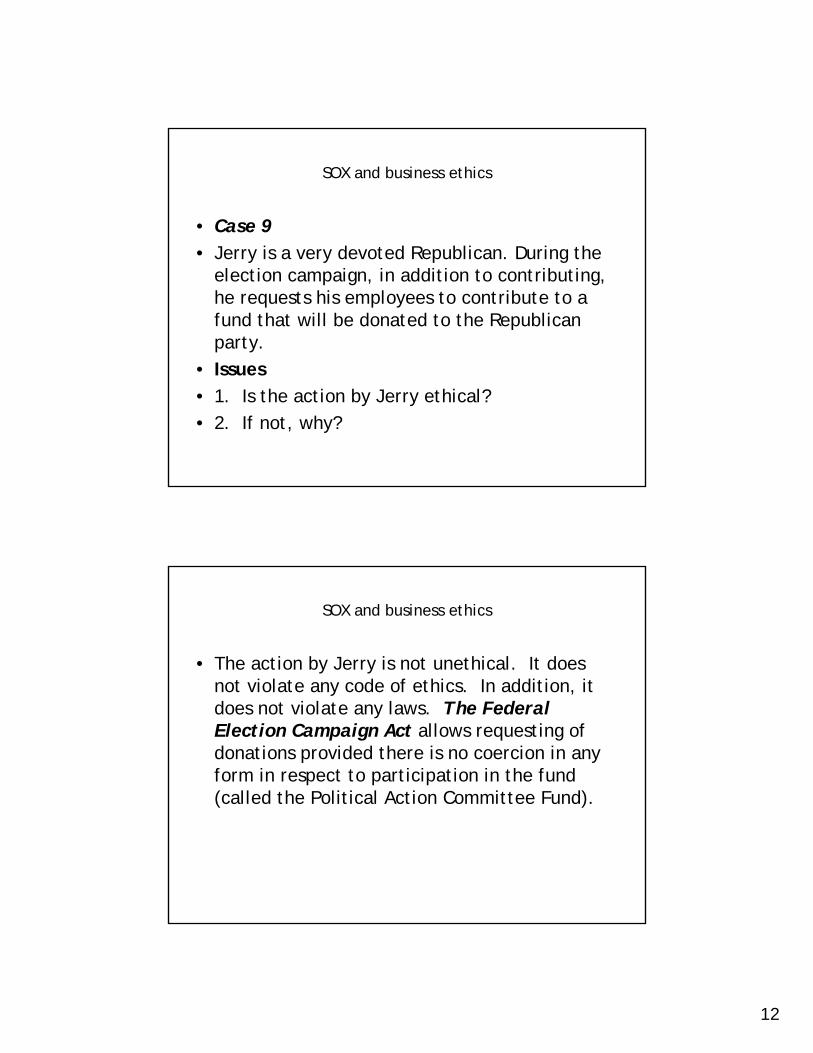

Mini Case Study 9: The manager, in addition to contributing to a political party also

requested his employees to contribute to a fund that will be donated to a political party.

Question: Does this meet ethical standards?

The majority of students thought that was not ethical (69%) while 31% said they

saw nothing wrong with it. In this instance the majority of students were incorrect.

SOX cites the Federal Election Campaign Act which allows requesting of

donations provided there is no coercion.

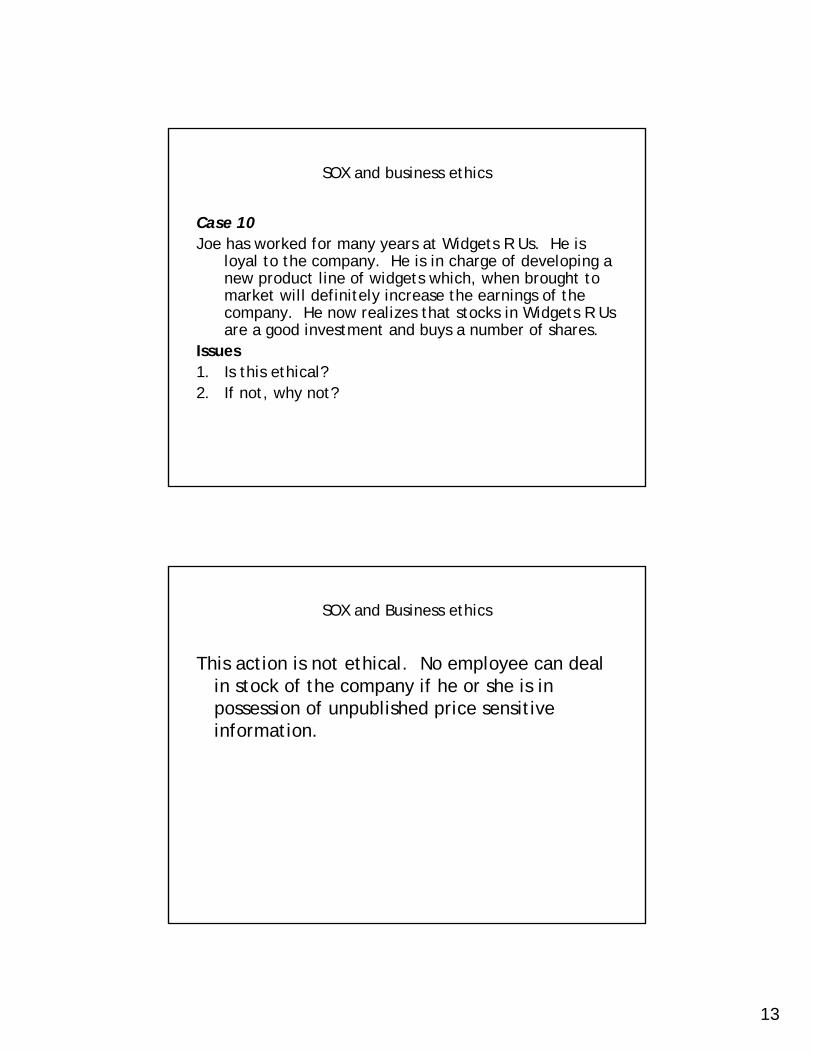

Mini Case Study 10: An employee knows about potential good news and buys stock in

the company. Question: Does this meet ethical standards?

About 78% of the students said this was not ethical. They were correct.

According to SOX, no employee can deal in stock of the company if he or she is

in possession of unpublished price sensitive information

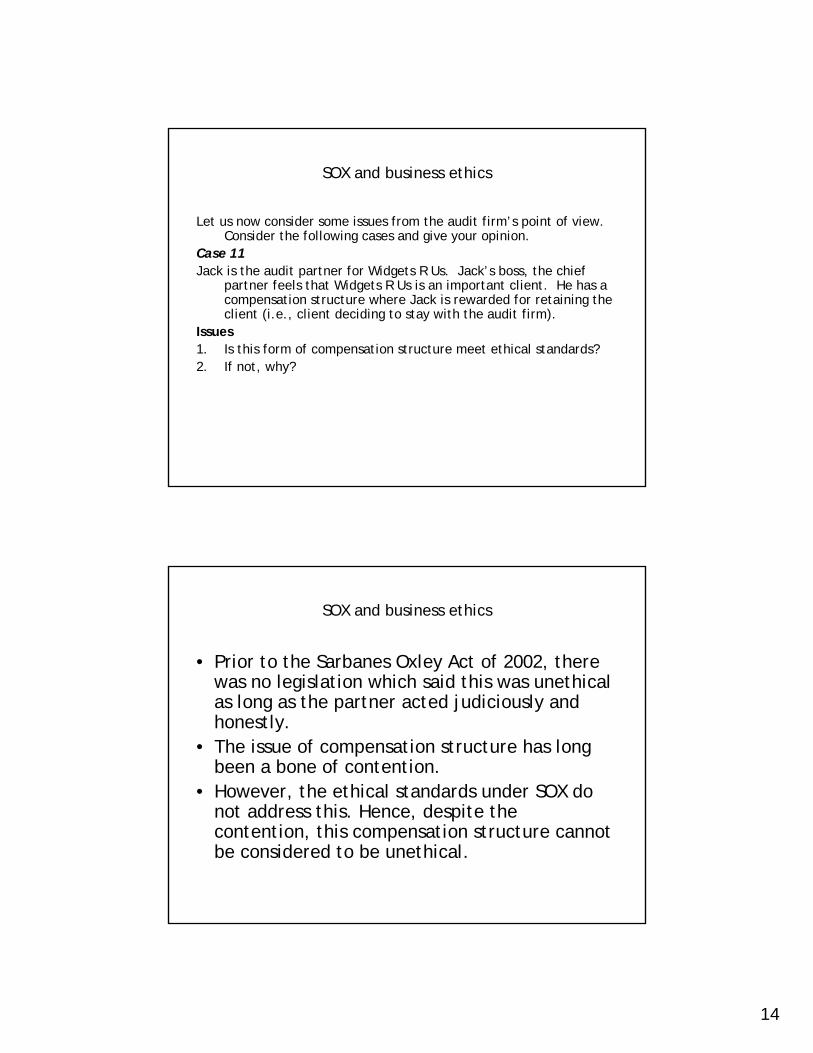

Mini Case Study 11: Audit partners have compensation structures where they are

rewarded for retaining the client. Question: Does this meet ethical standards?

About 71% of the students said they saw nothing wrong with this. They were

correct. This cannot be considered unethical as long as the partner acts

judiciously and honestly.

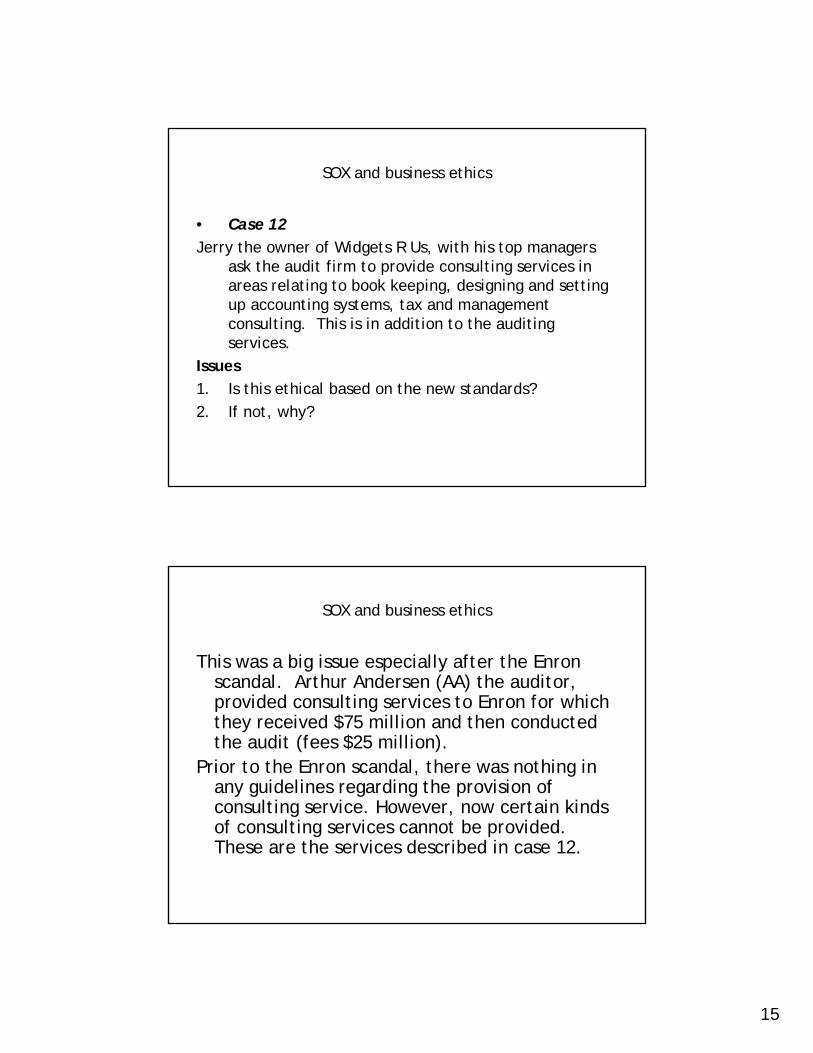

Mini Case Study 12: The auditors, in addition to the audit, also provide consulting

services to the client in areas relating to setting up accounting systems. Question: Does

this meet ethical standards?

About 80% said they saw nothing wrong with this. The justification was that if an

auditor was responsible for setting up accounting system, then they would be

able to do a better audit. These students were incorrect. SOX (section 206) now

prohibits certain kinds of consulting services if an auditor also conducts the audit.

This arose as a result of the Enron fiasco. Arthur Andersen, the audit partner

generated three times as much revenue from providing consulting services

relative to the audit. This made them susceptible to pressure from the client.

15

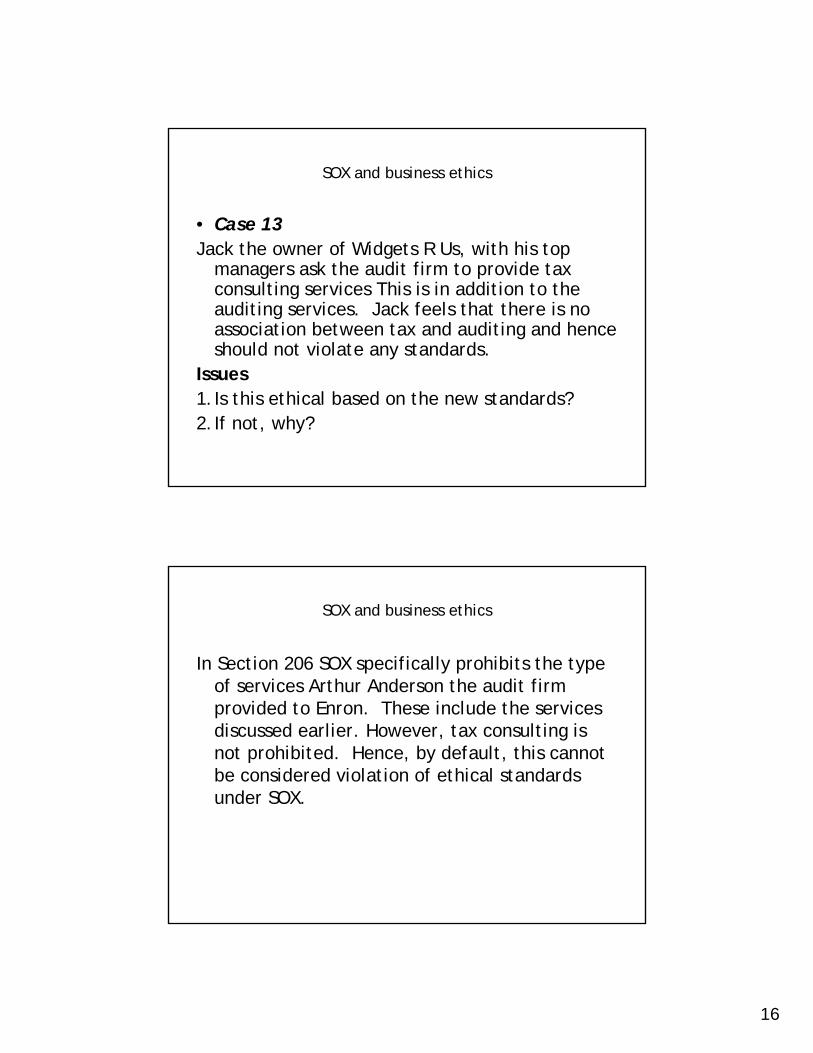

Mini Case Study 13: Same as above except that the auditor, in addition to the audit

provided tax services. Question: Does this meet ethical standards?

About 80% of the respondents said they saw nothing wrong with this. They were

correct. While SOX prohibits certain types of services, providing tax consulting is

not considered to be a violation of ethics.

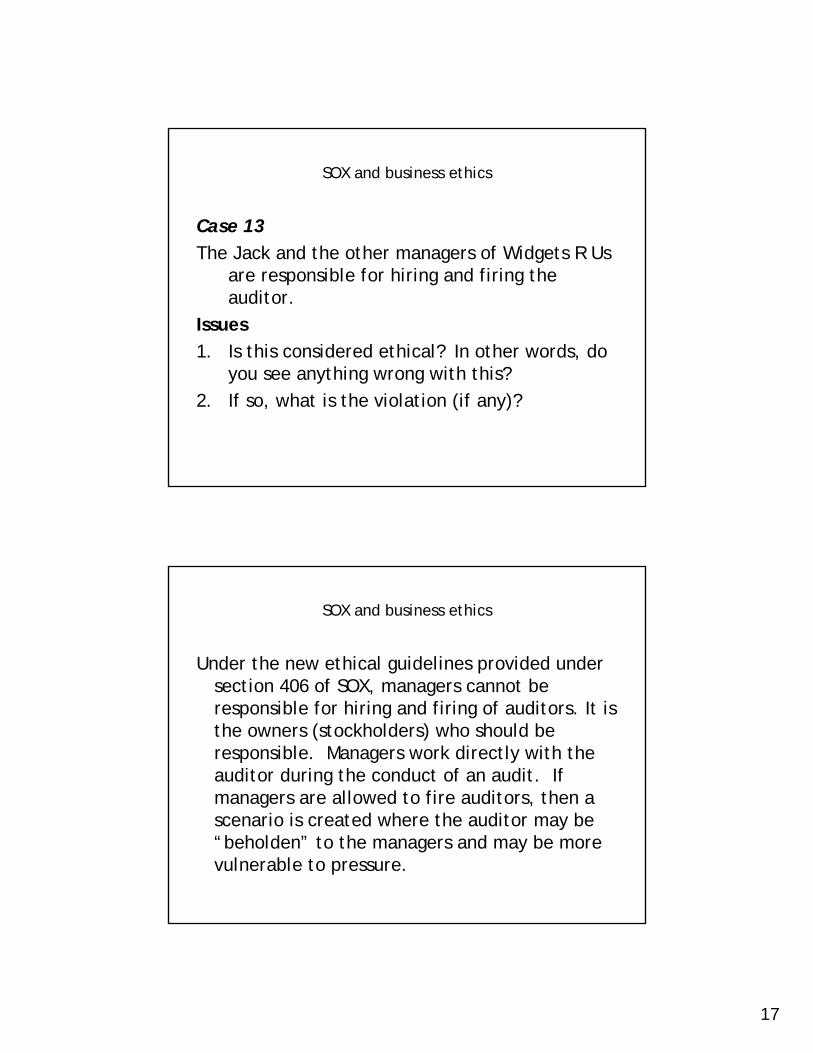

Mini Case Study 14: Managers of a company are responsible for hiring and firing the

auditor. Question: Does this meet ethical standards?

About 70% of the students said they was nothing wrong with this and hence,

there was no violation of ethics. However, under SOX managers cannot now be

responsible for hiring and firing the auditors. Since managers work directly with

the auditor they should not be put in a position of “strength”. Hiring and firing of

the auditor is now under the purview of the owners.

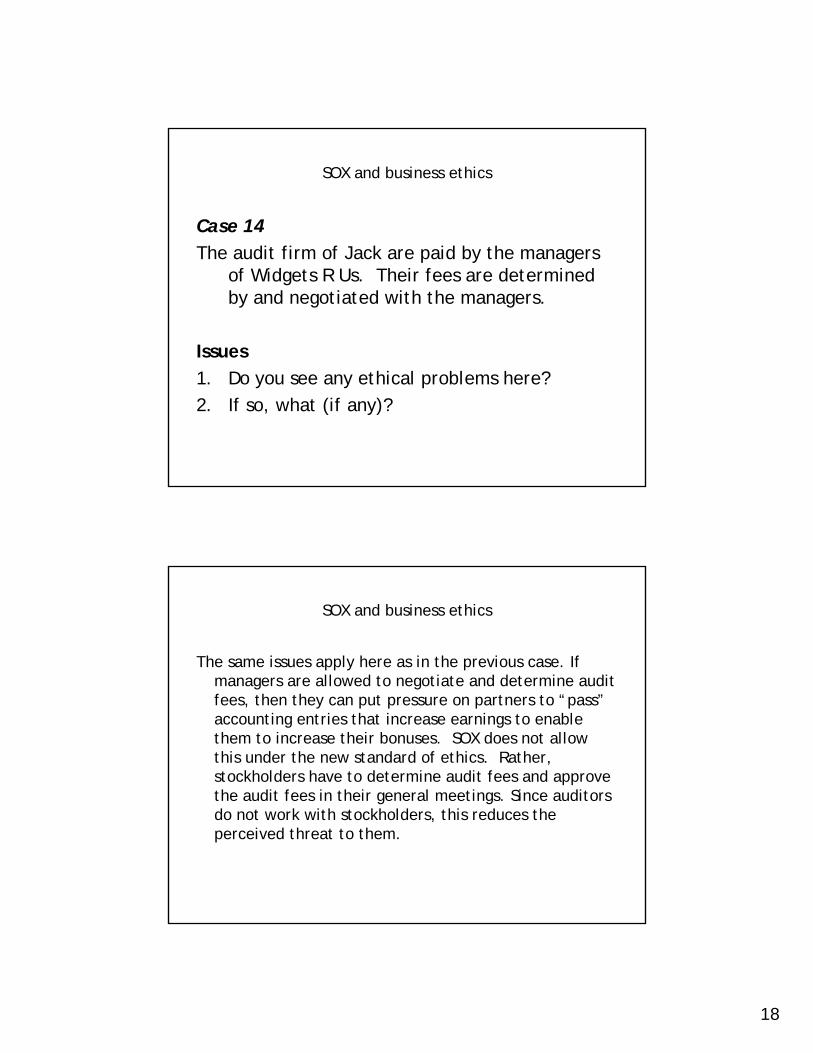

Mini Case Study 15: The fees of the audit firm are determined and negotiated by the

managers. Question: Does this meet ethical standards?

About 70% said there was nothing wrong with this. However, this does not meet

ethical standards for the same reasons noted above.

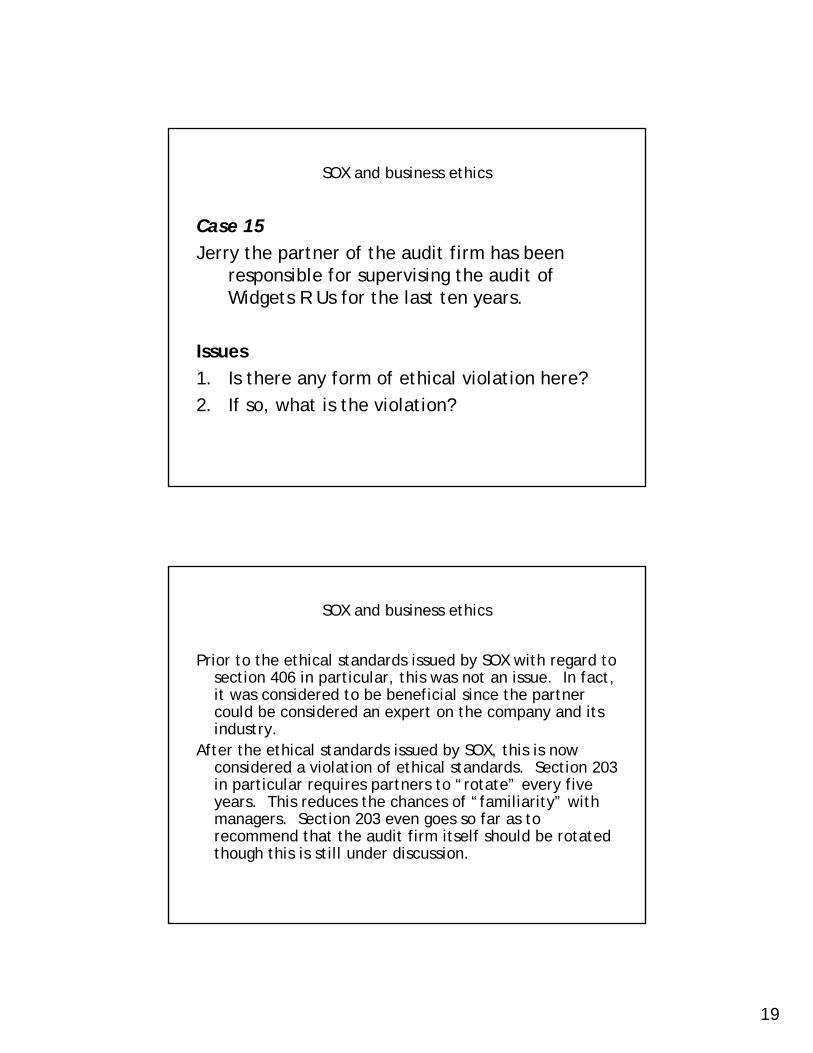

Mini Case Study 16: The partner of an audit firm has been responsible for supervising

the audit of a company for ten years. Question: Does this meet ethical standards?

Almost 90% of the students said there was nothing wrong with this. The

justification was that a partner who had a long experience of the client and the

industry would be in a better position to conduct the audit effectively. However,

according to SOX, (section 406) partners must be rotated and should not be in a

position to become too familiar with the client.

In general, students gave correct answers to 7 of the 16 case studies. They were

correct in situations which involved topics that are current news. For example, most

students showed an awareness of insider trading activities. However, the students used

“common sense” to answer case studies which, in 9 of the 16 cases, was not adequate.

For example, it makes sense to assume that a partner with many years experience of

the client would do a better job conducting the audit. However, this is a violation of

ethical standards under SOX because of the concept of “familiarity”. Partners are now

required to be rotated every five years. The survey shows that students are unfamiliar

with a lot of the concepts (ethical standards) introduced in SOX.

16

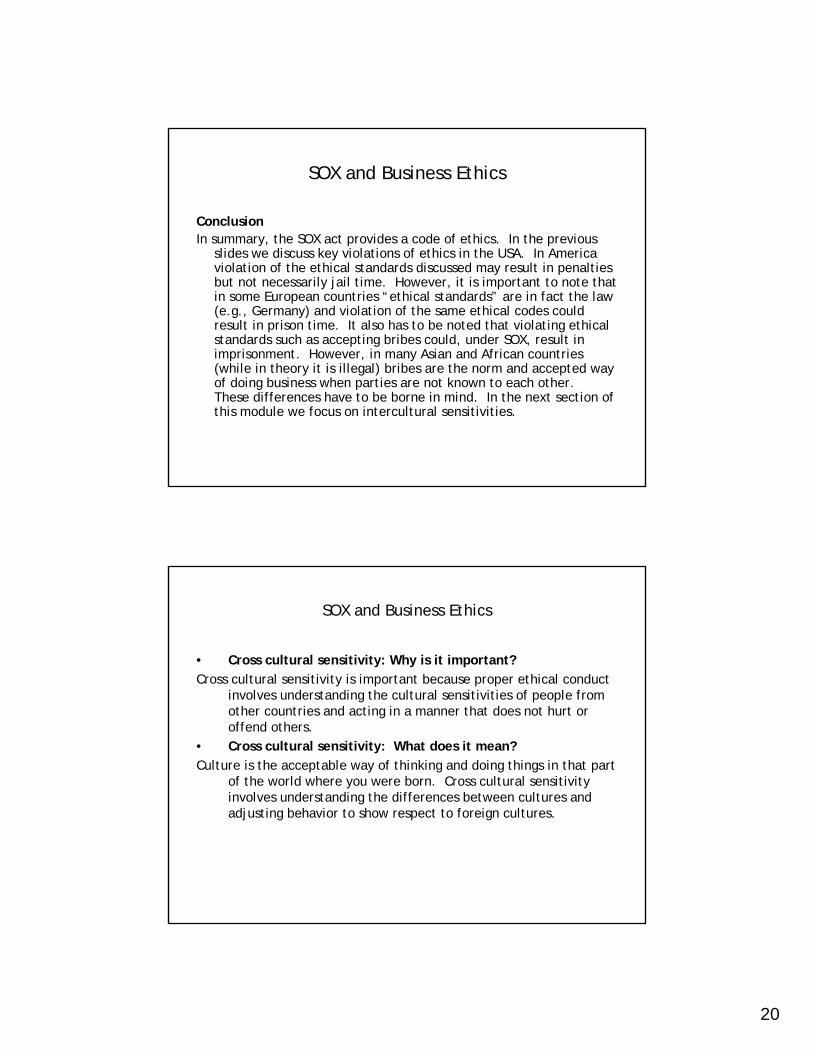

VII. Conclusions

This project started entailed an important and new challenge: enhance

educational curricula in the finance-related disciplines in New Jersey. To

accomplish this task, we started a review of finance programs in northern New

Jersey, intending to address emerging gaps in the curriculum. However, when

meeting with the finance industry stakeholders, we found that most of their

educational needs rotated around the development of ethical, interpersonal and

communication skills more than technical financial concepts. Based on this

findings, we developed modules that engaged students in communication,

working in teams, analytical and ethical reasoning while learning specific

concepts (such as project management, cost control, etc.). An analysis of the

preliminary results from the pilot tests shows that this approach is right on target:

total test scores were below standards or students asked more exposure to team

experiences as shown by their interest for the team-learning modules. Students

are not acquiring these skills within their programs, and hence need more

exposure to content and activities in these areas.

We designed these modules for easy and manageable replication by other

educational institutions. The length of the modules is appropriate for “ease of re-

use” and integration as lectures within existing courses. However, the materials

can be extended over various weeks through the use of sample exercises that

complement the lecture notes. The project team remains available for questions

or to provide guidance for replication at the email addresses listed in the next

section.

VIII. Project Team

The project team was composed of two lead curriculum developers from the

School of Management at NJIT. Since the spirit of the grant is to facilitate New

Jersey residents’ entry in the financial industry, we also funded two graduate

17

assistants who participated in selected activities (such as stakeholders’ needs

analysis and survey administration) and gained significant experiences. One of

such assistants, Marialisa Cisternino, was able to leverage her participation in

the grant and landed a position with Citi Smith Barney in NJ.

Asokan Anandarajan is a Professor of Accounting at the School of Management of the New Jersey Institute of Technology (NJIT) where he teaches courses in Accounting information systems, Financial accounting, Managerial accounting, Concepts of Finance, Business Valuation, and Insurance and Risk Management. He has published fifty five papers in refereed research journals including the top journals in accounting such as Auditing: A Journal of Practice and Theory, Accounting and Finance, Accounting Horizons, Behavioral Research in Accounting. International Journal of Intelligent Systems in Accounting, Finance and Management among others. Dr Anandarajan earned a double Master’s degree from Crainfield University in England and a Ph.D degree from Drexel University in Philadelphia. Email: [email protected]

Katia Passerini is an Assistant Professor and the Hurlburt Chair of Management Information Systems at the School of Management of the New Jersey Institute of Technology (NJIT) where she teaches courses in MIS, Knowledge Management and IT Strategy. She has published in refereed journals and proceedings (Communications of the ACM, CAIS, Society and Business Review, Journal of Knowledge Management, Computers & Education, Journal of Educational Hypermedia and Multimedia, IEEE Internet Computing) and professional journals (Project Management Network, Cutter IT Journal, Cutter Benchmark Review), particularly in the area of computer-mediated learning, IT productivity and knowledge management. Her professional experience includes multi-industry projects at Booz Allen Hamilton and the World Bank where she worked on information technology projects in Europe, North America and the South Pacific. Dr. Passerini earned both a MBA and a Ph.D. degree in Information & Decision Systems from the George Washington University, USA. Email: [email protected]

IX. Appendices Appendix A: NJ Finance Curricula Benchmark Appendix B: Survey Results and Curriculum Approach Appendix C: Team Learning Module and Activities Appendix D: Project Management Module and Activities Appendix E: Financial controls in project management module and Activities Appendix F: Business Ethics in finance module and Activities

Appendix A: NJ Finance Curricula Benchmark

Appendix A

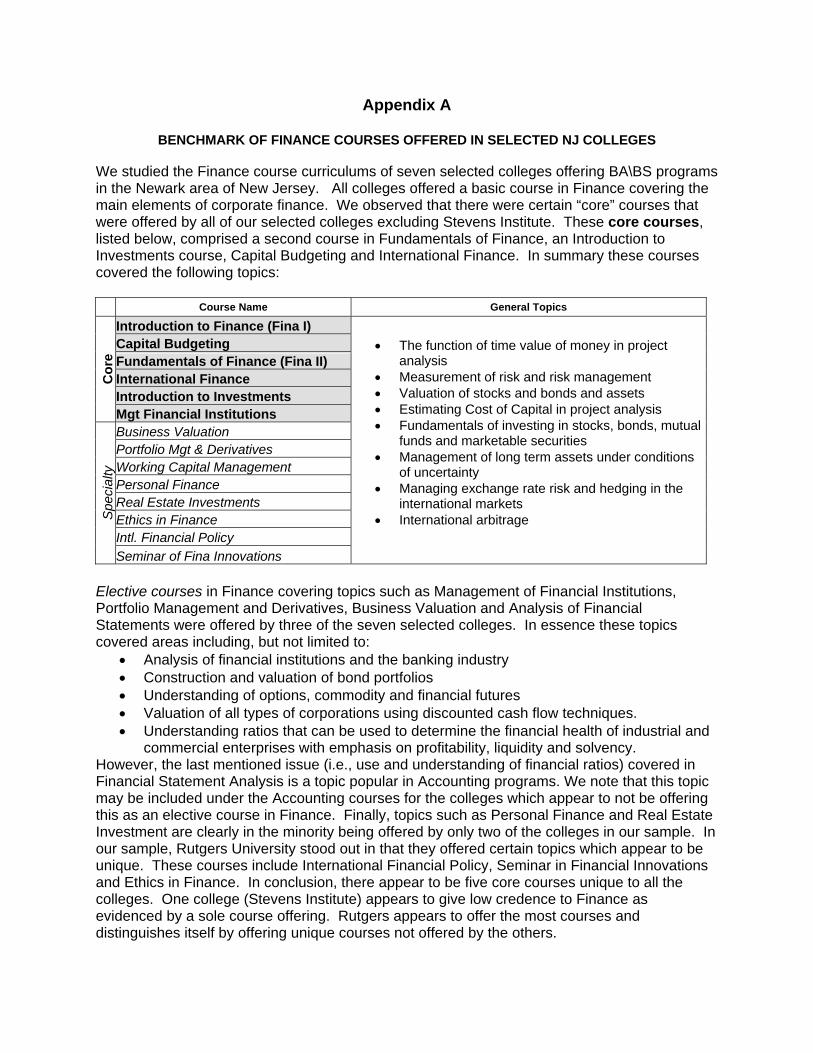

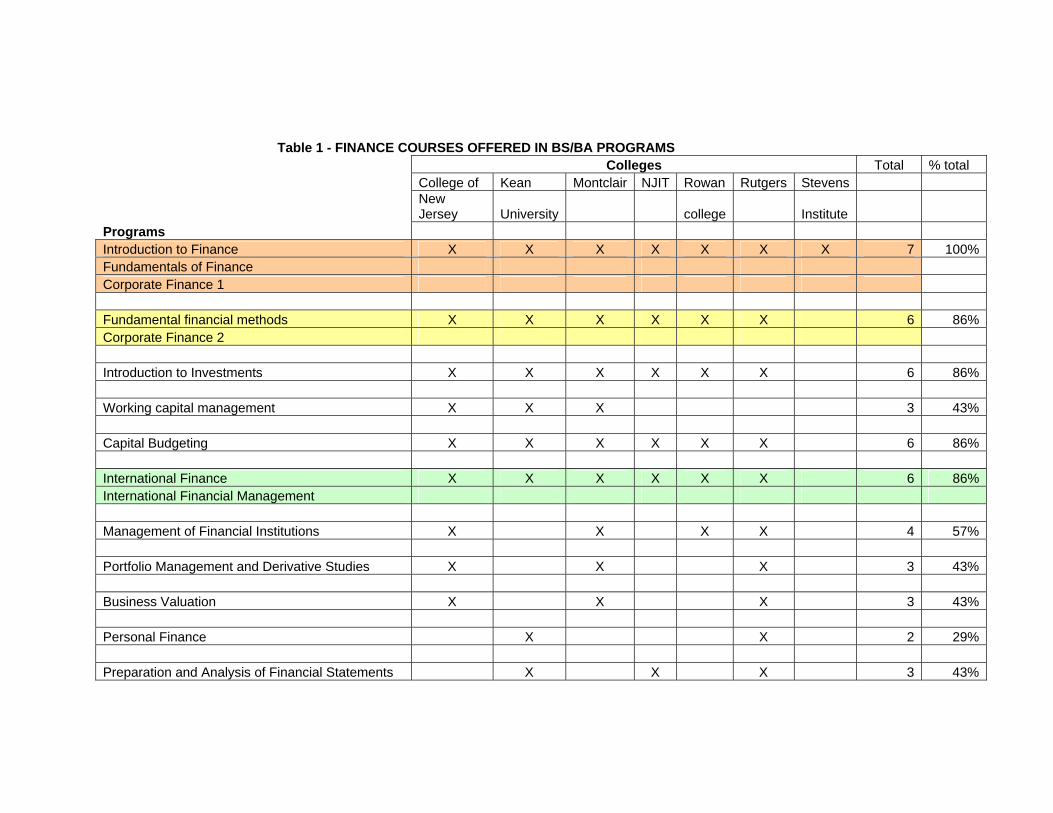

BENCHMARK OF FINANCE COURSES OFFERED IN SELECTED NJ COLLEGES

We studied the Finance course curriculums of seven selected colleges offering BA\BS programs in the Newark area of New Jersey. All colleges offered a basic course in Finance covering the main elements of corporate finance. We observed that there were certain “core” courses that were offered by all of our selected colleges excluding Stevens Institute. These core courses, listed below, comprised a second course in Fundamentals of Finance, an Introduction to Investments course, Capital Budgeting and International Finance. In summary these courses covered the following topics:

Course Name General Topics

Introduction to Finance (Fina I) Capital Budgeting Fundamentals of Finance (Fina II) International Finance Introduction to Investments

Cor

e

Mgt Financial Institutions Business Valuation Portfolio Mgt & Derivatives Working Capital Management Personal Finance Real Estate Investments Ethics in Finance Intl. Financial Policy

Spe

cial

ty

Seminar of Fina Innovations

• The function of time value of money in project analysis

• Measurement of risk and risk management • Valuation of stocks and bonds and assets • Estimating Cost of Capital in project analysis • Fundamentals of investing in stocks, bonds, mutual

funds and marketable securities • Management of long term assets under conditions

of uncertainty • Managing exchange rate risk and hedging in the

international markets • International arbitrage

Elective courses in Finance covering topics such as Management of Financial Institutions, Portfolio Management and Derivatives, Business Valuation and Analysis of Financial Statements were offered by three of the seven selected colleges. In essence these topics covered areas including, but not limited to:

• Analysis of financial institutions and the banking industry • Construction and valuation of bond portfolios • Understanding of options, commodity and financial futures • Valuation of all types of corporations using discounted cash flow techniques. • Understanding ratios that can be used to determine the financial health of industrial and

commercial enterprises with emphasis on profitability, liquidity and solvency. However, the last mentioned issue (i.e., use and understanding of financial ratios) covered in Financial Statement Analysis is a topic popular in Accounting programs. We note that this topic may be included under the Accounting courses for the colleges which appear to not be offering this as an elective course in Finance. Finally, topics such as Personal Finance and Real Estate Investment are clearly in the minority being offered by only two of the colleges in our sample. In our sample, Rutgers University stood out in that they offered certain topics which appear to be unique. These courses include International Financial Policy, Seminar in Financial Innovations and Ethics in Finance. In conclusion, there appear to be five core courses unique to all the colleges. One college (Stevens Institute) appears to give low credence to Finance as evidenced by a sole course offering. Rutgers appears to offer the most courses and distinguishes itself by offering unique courses not offered by the others.

Table 1 - FINANCE COURSES OFFERED IN BS/BA PROGRAMS

Colleges Total % total College of Kean Montclair NJIT Rowan Rutgers Stevens

New Jersey University college Institute

Programs Introduction to Finance X X X X X X X 7 100%Fundamentals of Finance Corporate Finance 1 Fundamental financial methods X X X X X X 6 86%Corporate Finance 2 Introduction to Investments X X X X X X 6 86% Working capital management X X X 3 43% Capital Budgeting X X X X X X 6 86% International Finance X X X X X X 6 86%International Financial Management Management of Financial Institutions X X X X 4 57% Portfolio Management and Derivative Studies X X X 3 43% Business Valuation X X X 3 43% Personal Finance X X 2 29% Preparation and Analysis of Financial Statements X X X 3 43%

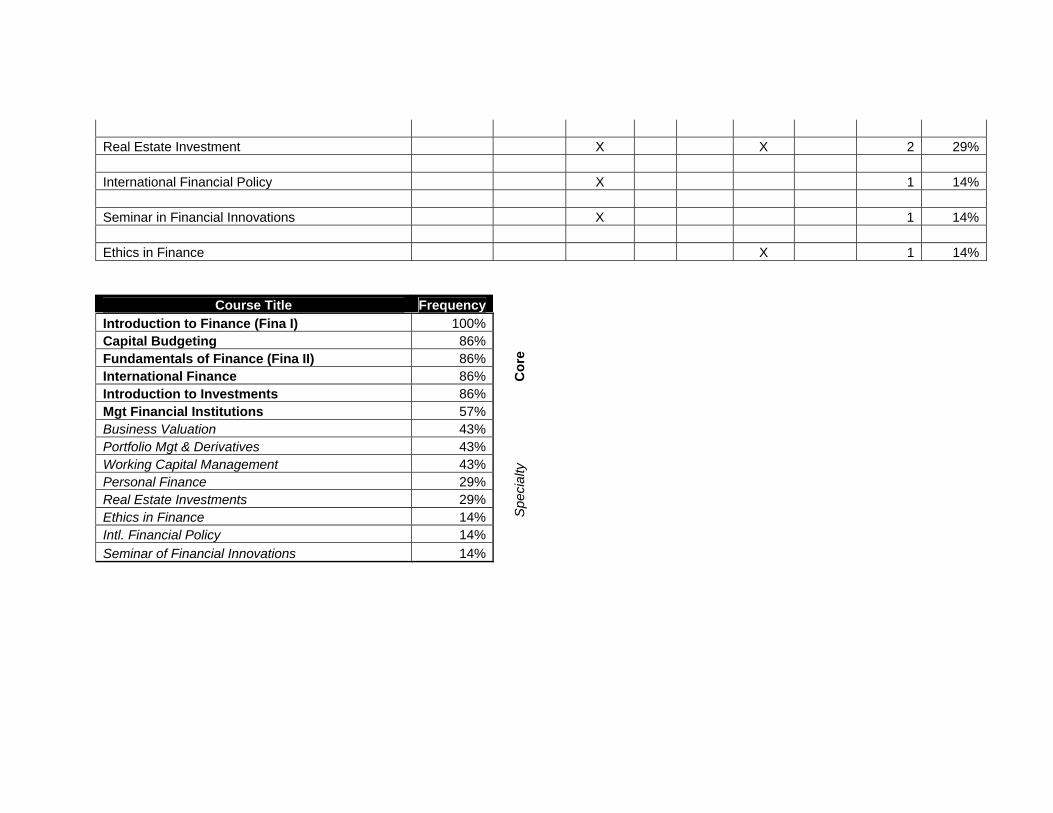

Real Estate Investment X X 2 29% International Financial Policy X 1 14% Seminar in Financial Innovations X 1 14% Ethics in Finance X 1 14%

Course Title Frequency Introduction to Finance (Fina I) 100% Capital Budgeting 86% Fundamentals of Finance (Fina II) 86% International Finance 86% Introduction to Investments 86% Mgt Financial Institutions 57%

Cor

e

Business Valuation 43% Portfolio Mgt & Derivatives 43% Working Capital Management 43% Personal Finance 29% Real Estate Investments 29% Ethics in Finance 14% Intl. Financial Policy 14% Seminar of Financial Innovations 14%

Spe

cial

ty

Appendix B: Survey Results and Curriculum Approach

1

1/16

Financial Industry Hiring Needs (2007)

Contact Katia Passerini - [email protected] Cisternino – [email protected] Anandarajan – [email protected]

http://www.surveymonkey.com/s.aspx?sm=I8wqAOX9WsEV2Z_2be5b1mQQ_3d_3d

2/16

Outline

Background: FS-IPIBackground: Feedback from IndustryKey Drivers & NeedsPreliminary Survey ResultsAction Areas

2

3/16

Financial Services Innovation Partnership Institute (FS-IPI)FS-IPI is a consortium of New Jersey’s education and workforce organizations created by Governor John Corzine as part of his Economic Growth Strategy.

• The Innovation Partnership Institute programs are administered as a collaboration among the NJ Commission on Higher Education, the Department of Labor and Workforce Development and the Department of Education.

The objective is to develop new study programs that better prepare students for occupations within the Financial Services SectorTo better reach our goal, we are seeking input from the FS industry

4/16

BackgroundThe FS-IPI member met with industry stakeholders to collect information about curriculum needs through• 2 co-located focus

groups • Ad hoc meetings @

company headquarters (Goldman Sachs recruiting meeting)

• 1 workforce needs survey (ongoing)

Survey URL:• http://www.surveymonkey.com/s.aspx?sm=I8

wqAOX9WsEV2Z_2be5b1mQQ_3d_3d

3

5/16

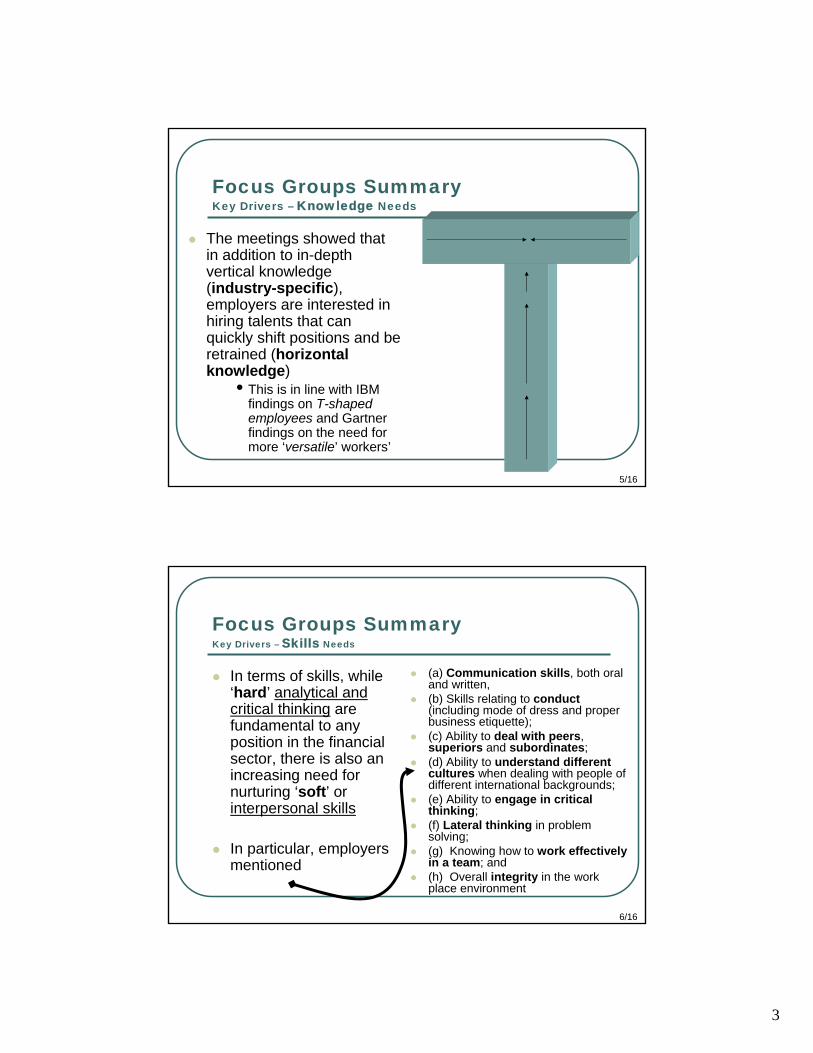

Focus Groups Summary Key Drivers – Knowledge Needs

The meetings showed that in addition to in-depth vertical knowledge (industry-specific), employers are interested in hiring talents that can quickly shift positions and be retrained (horizontal knowledge)

• This is in line with IBM findings on T-shaped employees and Gartner findings on the need for more ‘versatile’ workers’

6/16

Focus Groups Summary Key Drivers – Skills Needs

In terms of skills, while ‘hard’ analytical and critical thinking are fundamental to any position in the financial sector, there is also an increasing need for nurturing ‘soft’ or interpersonal skills

In particular, employers mentioned

(a) Communication skills, both oral and written,(b) Skills relating to conduct (including mode of dress and proper business etiquette);(c) Ability to deal with peers, superiors and subordinates;(d) Ability to understand different cultures when dealing with people of different international backgrounds; (e) Ability to engage in critical thinking;(f) Lateral thinking in problem solving;(g) Knowing how to work effectively in a team; and (h) Overall integrity in the work place environment

4

7/16

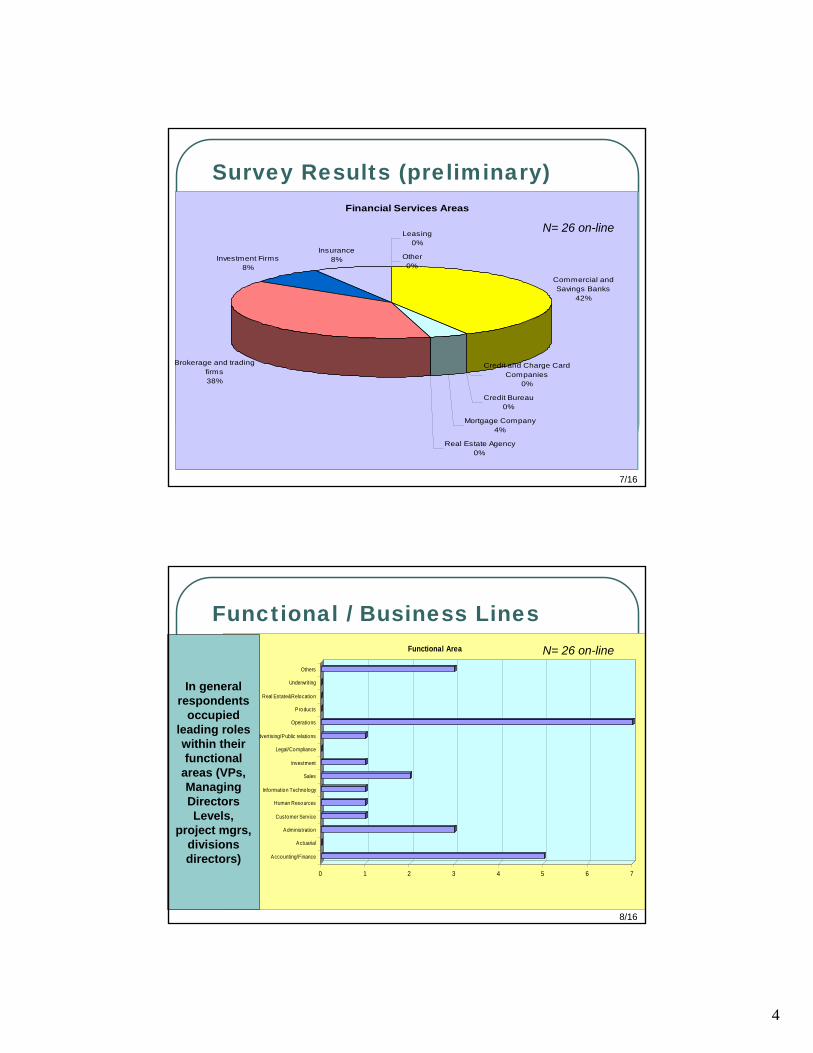

Financial Services Areas

Commercial and Savings Banks

42%

Credit and Charge Card Companies

0%

Credit Bureau0%

Mortgage Company4%

Real Estate Agency0%

Brokerage and trading firms38%

Investment Firms8%

Insurance8%

Leasing0%

Other0%

Survey Results (preliminary)

N= 26 on-line

8/16

Functional / Business Lines

0 1 2 3 4 5 6 7

Accounting/Finance

Actuarial

Administration

Customer Service

Human Resources

Information Technology

Sales

Investment

Legal/Compliance

M arketing/Advertising/Public relations

Operations

Products

Real Estate&Relocation

Underwriting

Others

Functional Area

In general respondents

occupied leading roles within their functional

areas (VPs, Managing Directors Levels,

project mgrs, divisions directors)

N= 26 on-line

5

9/16

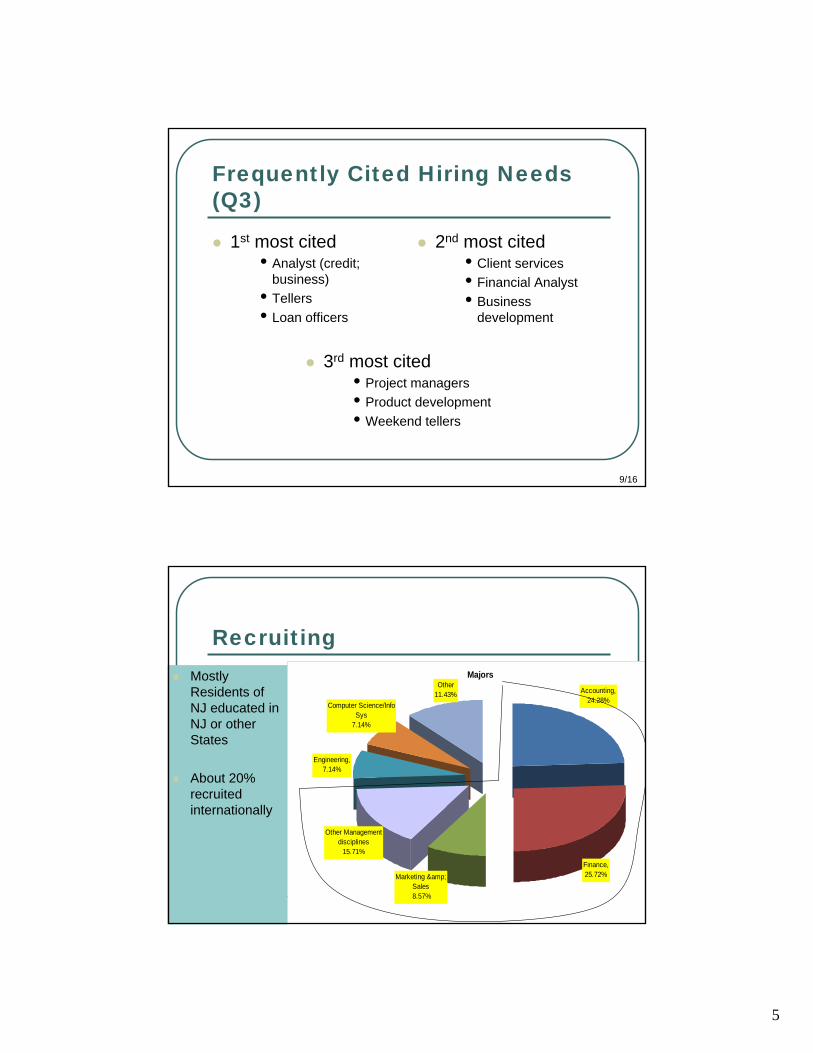

Frequently Cited Hiring Needs(Q3)

1st most cited• Analyst (credit;

business)• Tellers• Loan officers

2nd most cited• Client services • Financial Analyst• Business

development

3rd most cited• Project managers• Product development• Weekend tellers

10/16

RecruitingMostly Residents of NJ educated in NJ or other States

About 20% recruited internationally

MajorsOther

11.43%Computer Science/Info

Sys7.14%

Engineering,7.14%

Other Management disciplines

15.71%

Marketing & Sales

8.57%

Finance,25.72%

Accounting,24.28%

6

11/16

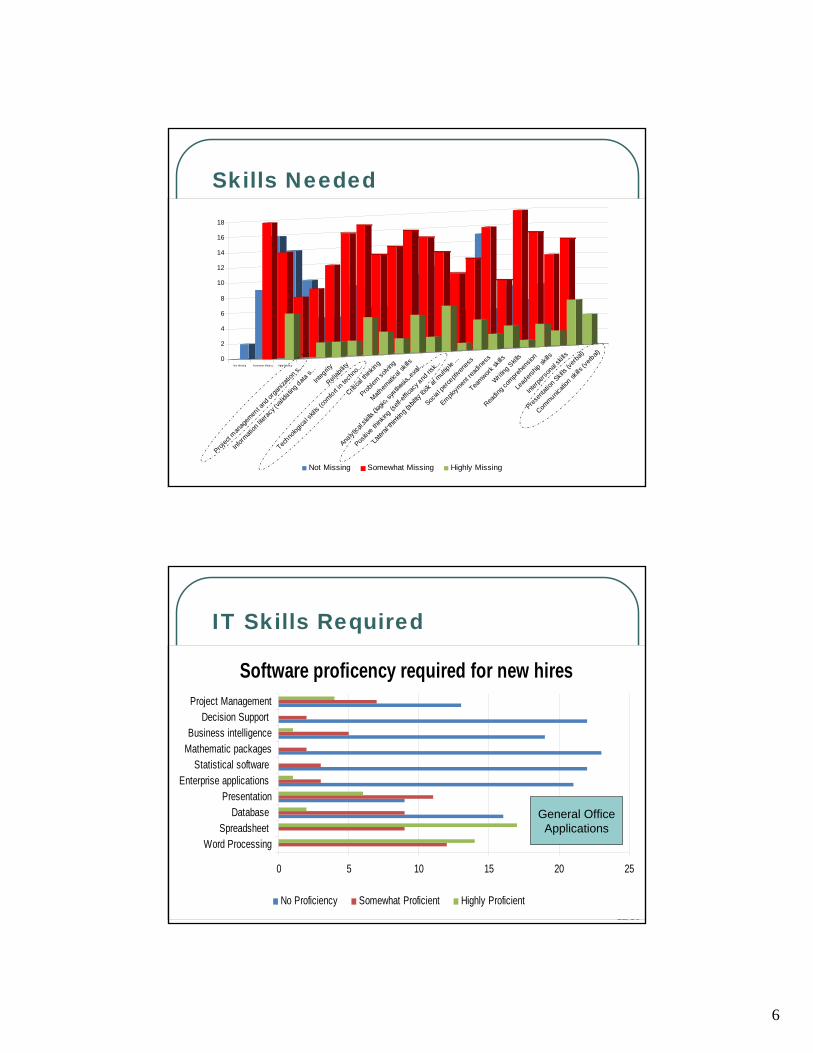

Skills Needed

0

2

4

6

8

10

12

14

16

18

Communic

ation

skills

(verb

al)

Presen

tation

Skills

(verba

l)

Interp

erson

al sk

ills

Lead

ership

skills

Readin

g com

prehe

nsion

Writing

Skill

s

Teamwork

skills

Employm

ent re

adine

ss

Social p

ercepti

vene

ss

Later

al thi

nking (

ability

look

at m

ultiple

...

Positiv

e think

ing (s

elf-ef

ficac

y and

risk..

.

Analyt

ical s

kills (

logic,

synthe

sis, e

val...

Mathem

atica

l skill

s

Problem

solvin

g

Critica

l think

ing

Techno

logica

l skill

s (co

mfort in t

echn

o...

Reliab

ility

Integ

rity

Inform

ation

litera

cy (v

alida

ting d

ata s.

. .

Projec

t man

agem

ent a

nd or

ganiz

ation

s...Not M issin g Somewhat M issin g Highly M issin g

Not Missing Somewhat Missing Highly Missing

12/16

IT Skills Required

Software proficency required for new hires

0 5 10 15 20 25

Word ProcessingSpreadsheet

Database Presentation

Enterprise applications Statistical software

Mathematic packagesBusiness intelligence

Decision Support Project Management

No Proficiency Somewhat Proficient Highly Proficient

General Office Applications

7

13/16

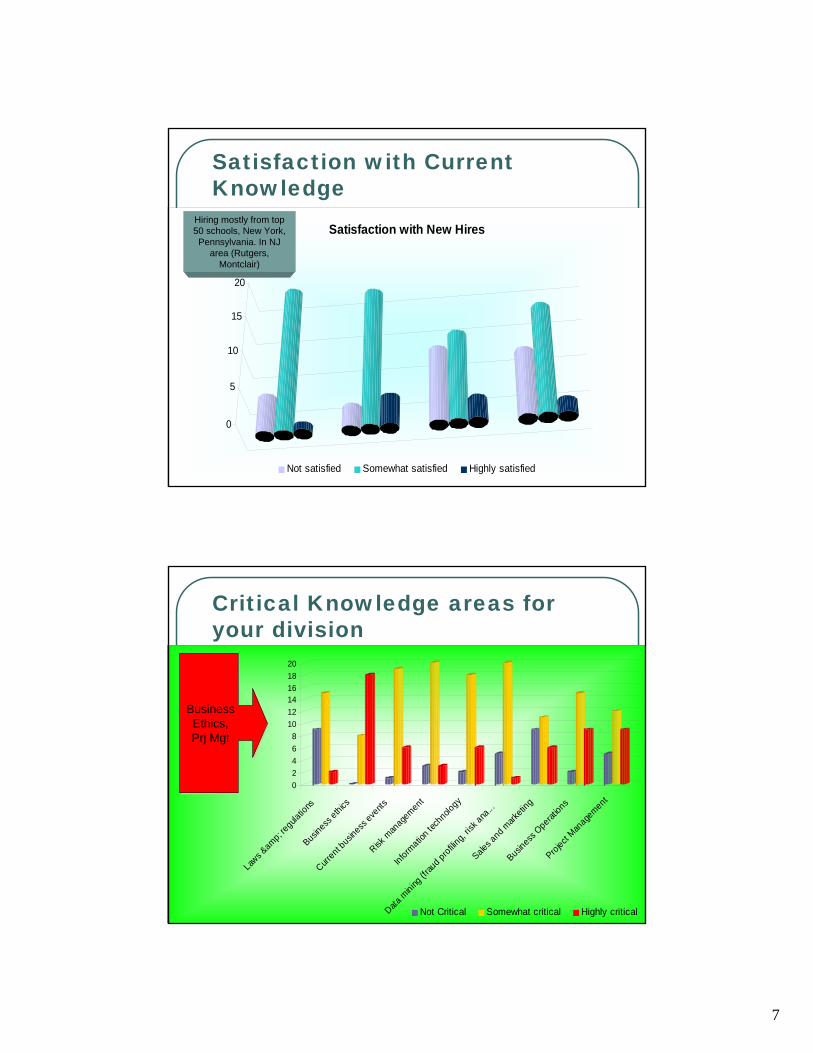

Satisfaction with Current Knowledge

0

5

10

15

20

Satisfaction with New Hires

Not satisfied Somewhat satisfied Highly satisfied

Hiring mostly from top 50 schools, New York, Pennsylvania. In NJ

area (Rutgers, Montclair)

14/16

Critical Knowledge areas for your division

02468

101214161820

Laws &

amp; regula

tions

Business

ethics

Current b

usiness

events

Risk m

anage

ment

Informatio

n tech

nology

Data m

ining (fr

aud profilin

g, ris

k ana

...

Sales and m

arketin

g

Business

Operat

ions

Project Man

agement

Not Critical Somewhat critical Highly critical

Business Ethics, Prj Mgt

Business Ethics, Prj Mgt

8

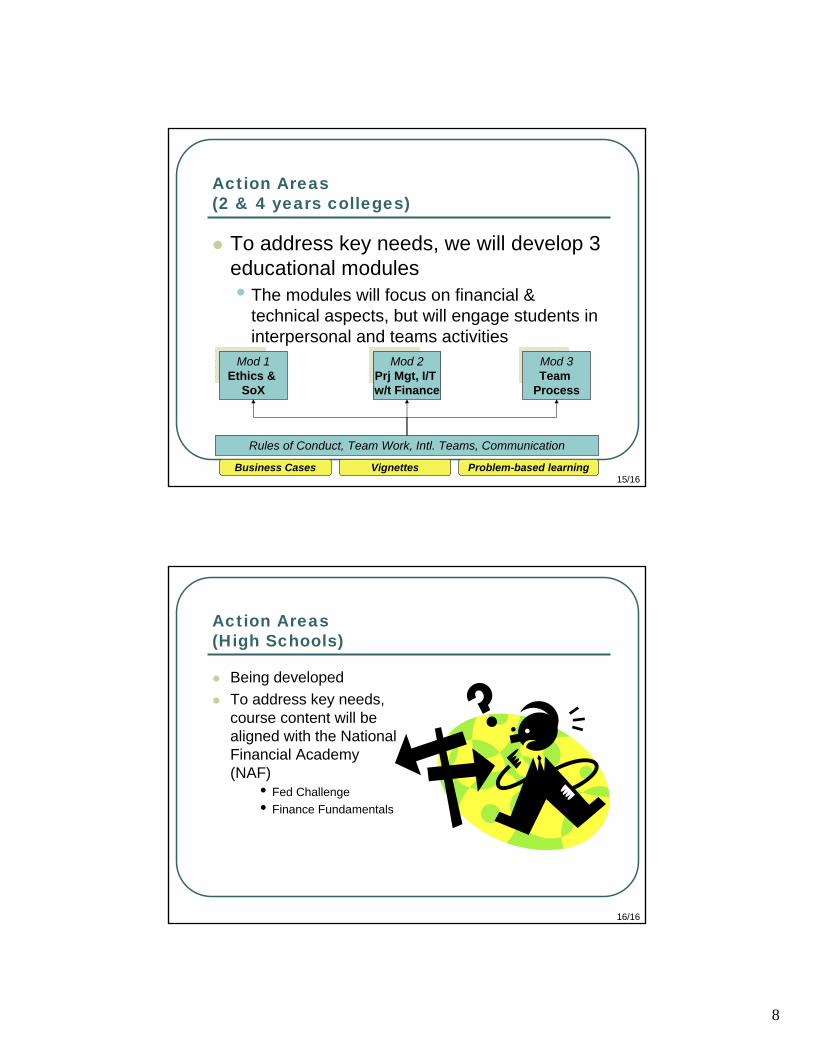

15/16

To address key needs, we will develop 3 educational modules• The modules will focus on financial &

technical aspects, but will engage students in interpersonal and teams activities

Action Areas (2 & 4 years colleges)

Mod 1Ethics &

SoX

Mod 3Team

Process

Mod 2Prj Mgt, I/T w/t Finance

Rules of Conduct, Team Work, Intl. Teams, Communication

Business Cases Vignettes Problem-based learning

16/16

Action Areas (High Schools)

Being developedTo address key needs, course content will be aligned with the National Financial Academy (NAF)

• Fed Challenge• Finance Fundamentals

1. Survey Purpose

To Financial Services Industry Professionals! We need your help! The FS-IPI* is conducting a survey to collect information on critical skills and knowledge gaps in the financial services industry in Northern New Jersey. The objective is to capture and aggregate responses from key financial industry players in order to develop new study programs that better prepare students for occupations within the Financial Services Sector. *The Financial Services Innovation Partnership Institute (FS-IPI) is a consortium of New Jersey’s education and workforce organizations created by Governor John Corzine as part of his Economic Growth Strategy. The Innovation Partnership Institute programs are administered as a collaboration among the NJ Commission on Higher Education, the Department of Labor and Workforce Development and the Department of Education. Results will be announced and made available on the FS-IPI web site in 2008. Aggregate results can also be mailed out earlier to all those that complete the survey and answer Question 20. By submitting this survey you confirm that you are over 18 years of age, you are volunteering your responses and will not be compensated. You have the right to withdraw your participation, if you wish to do so, by not completing the survey. The survey should take 5-10 minutes to complete and there are no required answers or comments.

1. Please click the next buttons to the industry you specifically represent:

Financial Service Business Functional area

.

Other (please specify)

2. What is your title / position in your company?

3. Please list your top three hiring needs / positions your division is looking for:

1st

2nd

3rd

4. Of the following list of occupations, please check which ones represent your hiring needs AND shortages in your division:

Not hiring

currentlyCurrently hiring

Will Hire (2-3

yrs)No shortage Some shortage High shortage

Bank Tellers gfedc gfedc gfedc gfedc gfedc gfedc

Customer service (from entry

level to management)gfedc gfedc gfedc gfedc gfedc gfedc

Call Center (from entry level

to management)gfedc gfedc gfedc gfedc gfedc gfedc

Insurance Claims and Policy

Processing Clerksgfedc gfedc gfedc gfedc gfedc gfedc

Senior Level Insurance

Managersgfedc gfedc gfedc gfedc gfedc gfedc

Accounting and compliance

specialistsgfedc gfedc gfedc gfedc gfedc gfedc

Security, Commodities and

Financial Services Sales

Agents

gfedc gfedc gfedc gfedc gfedc gfedc

Personal financial advisers gfedc gfedc gfedc gfedc gfedc gfedc

Sales and Marketing positions

(all levels)gfedc gfedc gfedc gfedc gfedc gfedc

Business services sales agents gfedc gfedc gfedc gfedc gfedc gfedc

Credit Analysts and Lenders gfedc gfedc gfedc gfedc gfedc gfedc

Financial Analysts gfedc gfedc gfedc gfedc gfedc gfedc

Senior Level financial

managersgfedc gfedc gfedc gfedc gfedc gfedc

Computer systems analysts gfedc gfedc gfedc gfedc gfedc gfedc

IT Project Managers gfedc gfedc gfedc gfedc gfedc gfedc

IT Networks Specialists gfedc gfedc gfedc gfedc gfedc gfedc

Others gfedc gfedc gfedc gfedc gfedc gfedc

Other (please specify)

5. Approximately, what percent of your hires in your division are:

1-20 21-40 41-60 61-80 81-100

Hired globally (i.e. international) nmlkj nmlkj nmlkj nmlkj nmlkj

Hired regionally (i.e. New York, PA) nmlkj nmlkj nmlkj nmlkj nmlkj

Residents of New Jersey, educated in NJ nmlkj nmlkj nmlkj nmlkj nmlkj

Residents and educated in other US States nmlkj nmlkj nmlkj nmlkj nmlkj

Other (please specify)

6. In general, what type of majors do you hire?

gfedc Accounting

gfedc Finance

gfedc Marketing & Sales

gfedc Other Management disciplines

gfedc Engineering

gfedc Computer Science/Info Sys

gfedc Other (please specify)

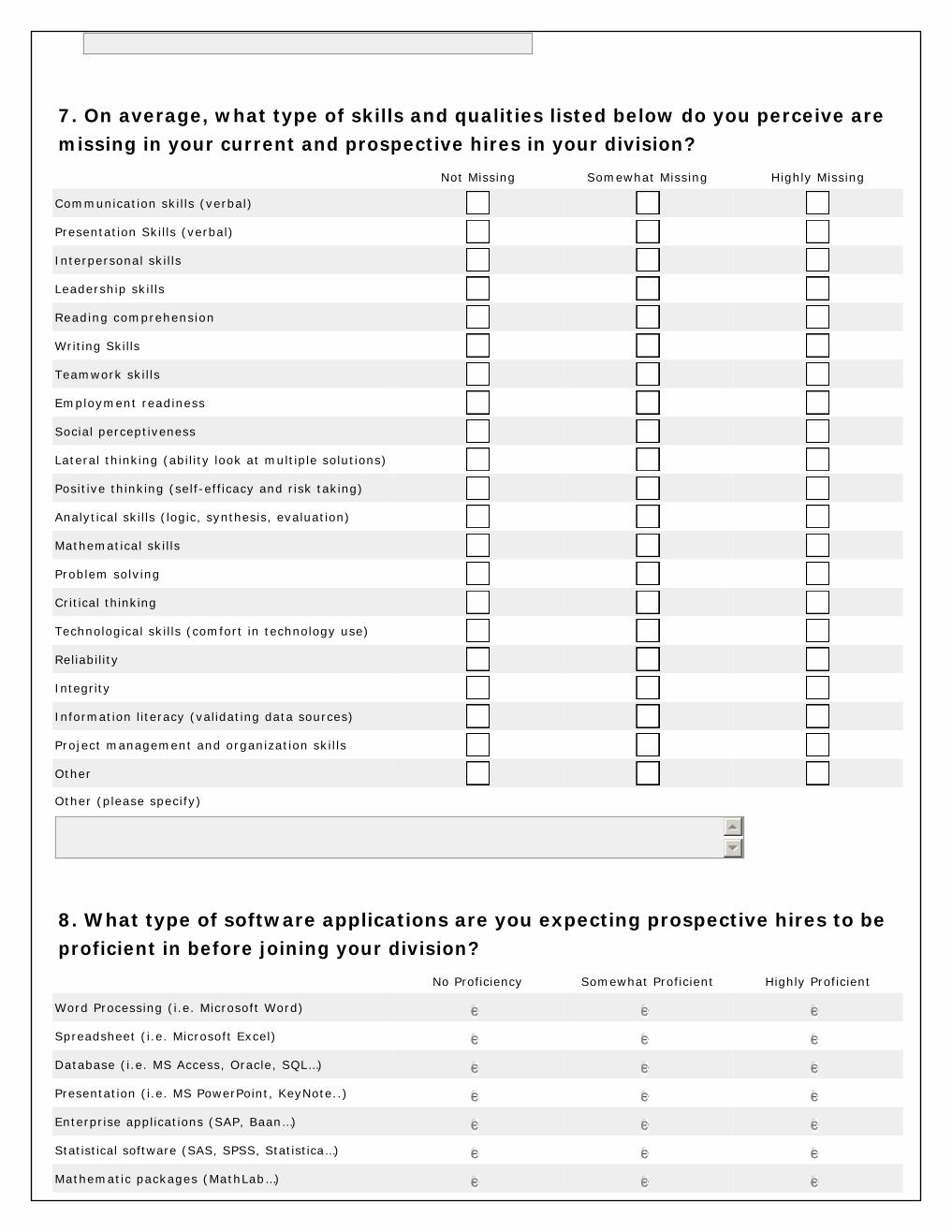

7. On average, what type of skills and qualities listed below do you perceive are missing in your current and prospective hires in your division?

Not Missing Somewhat Missing Highly Missing

Communication skills (verbal) gfedc gfedc gfedc

Presentation Skills (verbal) gfedc gfedc gfedc

Interpersonal skills gfedc gfedc gfedc

Leadership skills gfedc gfedc gfedc

Reading comprehension gfedc gfedc gfedc

Writing Skills gfedc gfedc gfedc

Teamwork skills gfedc gfedc gfedc

Employment readiness gfedc gfedc gfedc

Social perceptiveness gfedc gfedc gfedc

Lateral thinking (ability look at multiple solutions) gfedc gfedc gfedc

Positive thinking (self-efficacy and risk taking) gfedc gfedc gfedc

Analytical skills (logic, synthesis, evaluation) gfedc gfedc gfedc

Mathematical skills gfedc gfedc gfedc

Problem solving gfedc gfedc gfedc

Critical thinking gfedc gfedc gfedc

Technological skills (comfort in technology use) gfedc gfedc gfedc

Reliability gfedc gfedc gfedc

Integrity gfedc gfedc gfedc

Information literacy (validating data sources) gfedc gfedc gfedc

Project management and organization skills gfedc gfedc gfedc

Other gfedc gfedc gfedc

Other (please specify)

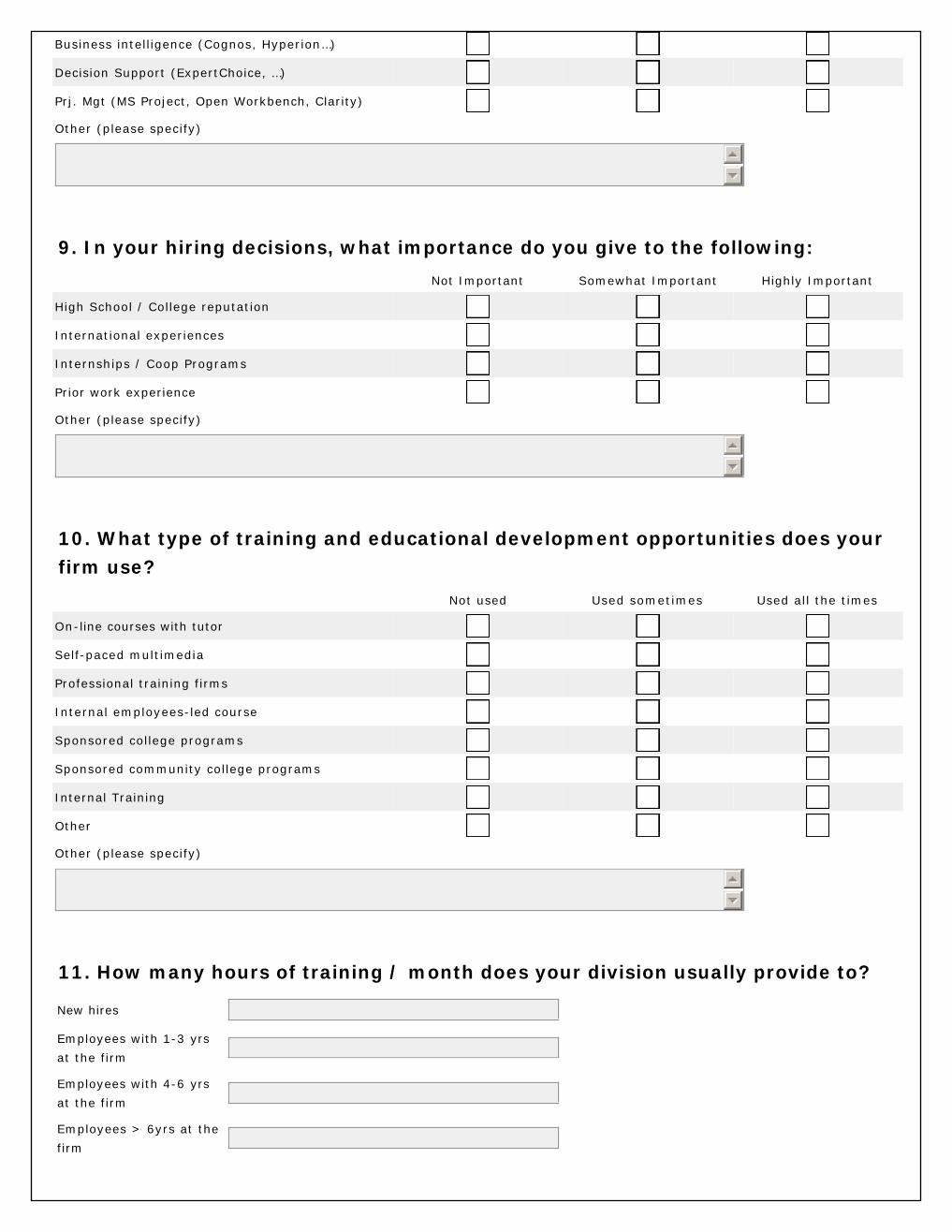

8. What type of software applications are you expecting prospective hires to be proficient in before joining your division?

No Proficiency Somewhat Proficient Highly Proficient

Word Processing (i.e. Microsoft Word) gfedc gfedc gfedc

Spreadsheet (i.e. Microsoft Excel) gfedc gfedc gfedc

Database (i.e. MS Access, Oracle, SQL…) gfedc gfedc gfedc

Presentation (i.e. MS PowerPoint, KeyNote..) gfedc gfedc gfedc

Enterprise applications (SAP, Baan…) gfedc gfedc gfedc

Statistical software (SAS, SPSS, Statistica…) gfedc gfedc gfedc

Mathematic packages (MathLab…) gfedc gfedc gfedc

Business intelligence (Cognos, Hyperion…) gfedc gfedc gfedc

Decision Support (ExpertChoice, …) gfedc gfedc gfedc

Prj. Mgt (MS Project, Open Workbench, Clarity) gfedc gfedc gfedc

Other (please specify)

9. In your hiring decisions, what importance do you give to the following:

Not Important Somewhat Important Highly Important

High School / College reputation gfedc gfedc gfedc

International experiences gfedc gfedc gfedc

Internships / Coop Programs gfedc gfedc gfedc

Prior work experience gfedc gfedc gfedc

Other (please specify)

10. What type of training and educational development opportunities does your firm use?

Not used Used sometimes Used all the times

On-line courses with tutor gfedc gfedc gfedc

Self-paced multimedia gfedc gfedc gfedc

Professional training firms gfedc gfedc gfedc

Internal employees-led course gfedc gfedc gfedc

Sponsored college programs gfedc gfedc gfedc

Sponsored community college programs gfedc gfedc gfedc

Internal Training gfedc gfedc gfedc

Other gfedc gfedc gfedc

Other (please specify)

11. How many hours of training / month does your division usually provide to?

New hires

Employees with 1-3 yrs

at the firm

Employees with 4-6 yrs

at the firm

Employees > 6yrs at the

firm

12. Are you satisfied with the knowledge of your new hires in your division?

Not satisfied Somewhat satisfied Highly satisfied

Generic business knowledge gfedc gfedc gfedc

Technical knowledge gfedc gfedc gfedc

Specialist financial knowledge gfedc gfedc gfedc

Industry-level knowledge gfedc gfedc gfedc

Other (please specify)

13. What are the most critical areas (other than finance) that a college-graduate should be proficient in to be successful in your division?

Not Critical Somewhat critical Highly critical

Laws & regulations gfedc gfedc gfedc

Business ethics gfedc gfedc gfedc

Current business events gfedc gfedc gfedc

Risk management gfedc gfedc gfedc

Information technology gfedc gfedc gfedc

Data mining (fraud profiling, risk analysis) gfedc gfedc gfedc

Sales and marketing gfedc gfedc gfedc

Business Operations gfedc gfedc gfedc

Project Management gfedc gfedc gfedc

Other gfedc gfedc gfedc

Other (please specify)

14. Please rate the level of proficiency in the following concepts that a college-graduate should demonstrate to be successful in your division?

No proficiency

12 3 4

High

proficiency 5

Measurement of risk and return nmlkj nmlkj nmlkj nmlkj nmlkj

Cost of capital and capital budgeting nmlkj nmlkj nmlkj nmlkj nmlkj

Knowledge of stocks and bonds nmlkj nmlkj nmlkj nmlkj nmlkj

Knowledge of mutual funds & securities nmlkj nmlkj nmlkj nmlkj nmlkj

Valuation of assets and business nmlkj nmlkj nmlkj nmlkj nmlkj

Financial statements analysis nmlkj nmlkj nmlkj nmlkj nmlkj

Financial products and services nmlkj nmlkj nmlkj nmlkj nmlkj

Mgt of short-term assets and liabilities nmlkj nmlkj nmlkj nmlkj nmlkj

Functioning of global markets nmlkj nmlkj nmlkj nmlkj nmlkj

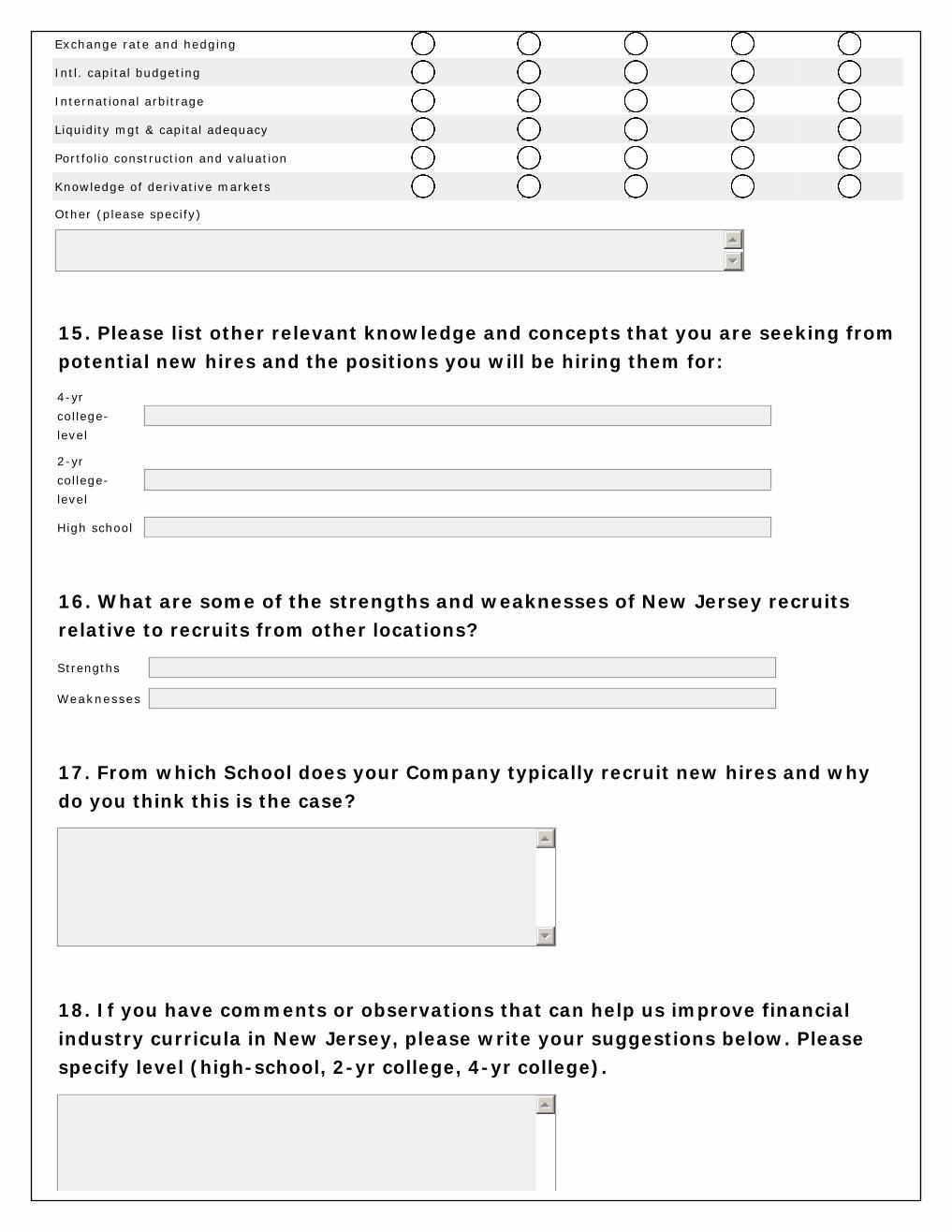

Exchange rate and hedging nmlkj nmlkj nmlkj nmlkj nmlkj

Intl. capital budgeting nmlkj nmlkj nmlkj nmlkj nmlkj

International arbitrage nmlkj nmlkj nmlkj nmlkj nmlkj

Liquidity mgt & capital adequacy nmlkj nmlkj nmlkj nmlkj nmlkj

Portfolio construction and valuation nmlkj nmlkj nmlkj nmlkj nmlkj

Knowledge of derivative markets nmlkj nmlkj nmlkj nmlkj nmlkj

Other (please specify)

15. Please list other relevant knowledge and concepts that you are seeking from potential new hires and the positions you will be hiring them for:

4-yr

college-

level

2-yr

college-

level

High school

16. What are some of the strengths and weaknesses of New Jersey recruits relative to recruits from other locations?

Strengths

Weaknesses

17. From which School does your Company typically recruit new hires and why do you think this is the case?

18. If you have comments or observations that can help us improve financial industry curricula in New Jersey, please write your suggestions below. Please specify level (high-school, 2-yr college, 4-yr college).

19. What is the size of your company with respect to the following indicators?

Number of Employees

Sales Revenue/ year

Assets

Net Profit

20. If you would like to receive a copy of the survey results, please provide your name and mailing address. (optional)

Name

Company Name

Address

City, State, Zip

e-Mail address

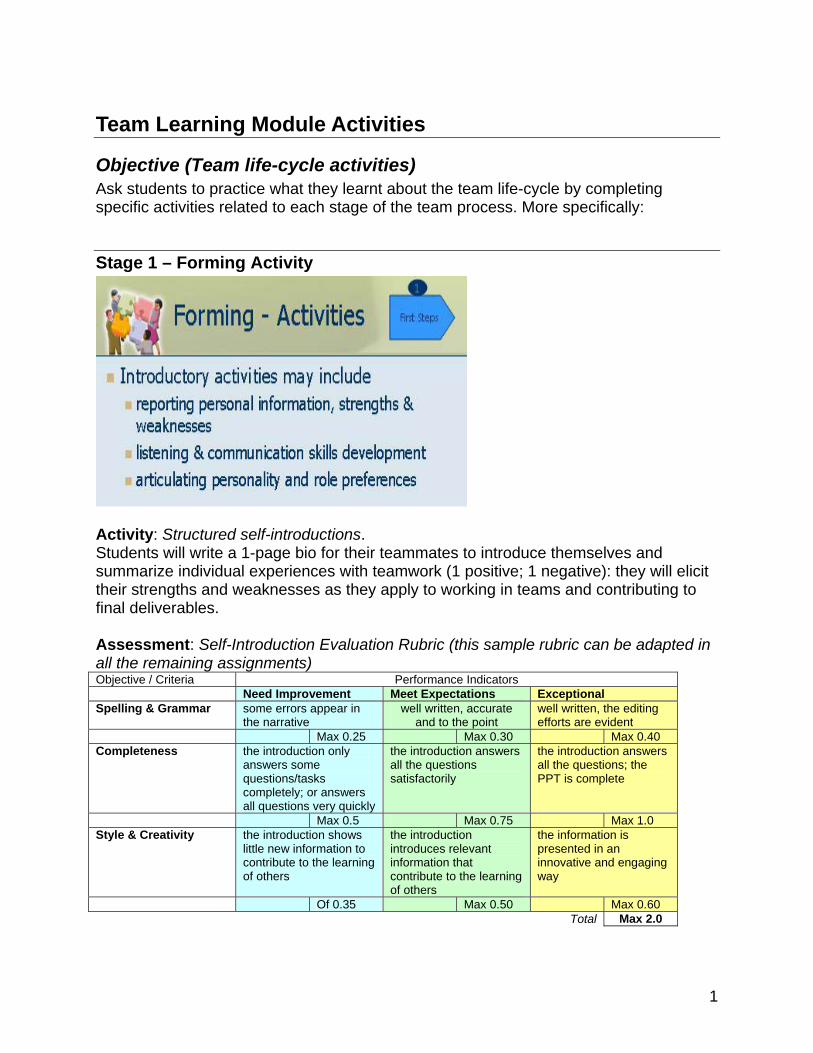

Appendix C: Team Learning Module and Activities

1

Working (and Learning) in Teams

© Dr. Katia Passerini , Dr. Asokan AnandarajanNew Jersey Institute of Technology

Outline

• Team Basics• The Life of A Team

• Forming, Storming, Norming, Performing, Adjourning

• Team Roles• Working in International Teams• Why Teams Fail• Reading List

Disclaimer: This is an overview module. We encourage learners to enroll in semester-long human resources management and organizational behavior

courses for a complete treatment of this topic.

2

Learning Objectives & Skills

• Be able to recognize key aspects of the team lifecycle

• Familiarize yourself with different roles in a team

• Understand the complexities of teamwork in international environments

• Recognize why teams fail

• Be introduced to specific software apps

Content-specific skills

Critical Thinking & Analytic skills

Skills developedStudents will

Teamwork skills

Communication skills

Technology skills

Outline

• Team Basics• The Life of A Team

• Forming, Storming, Norming, Performing, Adjourning

• Team Roles• Working in International Teams• Why Teams Fail• Reading List

3

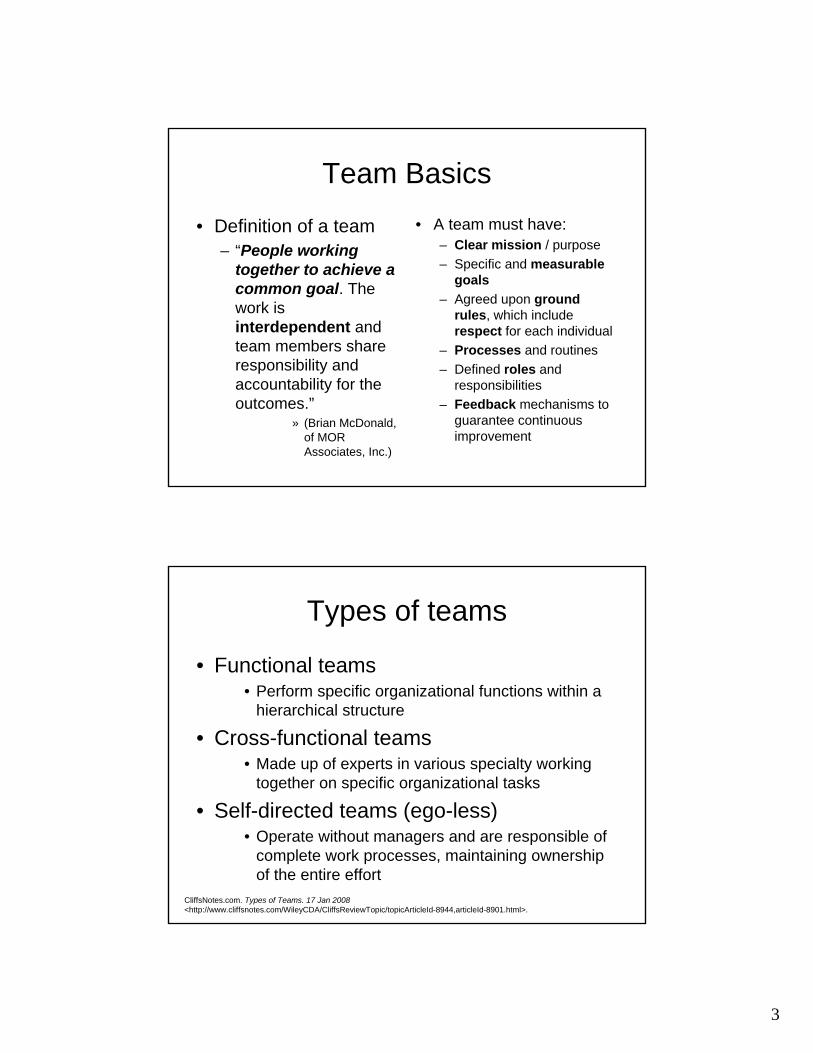

Team Basics

• Definition of a team– “People working

together to achieve a common goal. The work is interdependent and team members share responsibility and accountability for the outcomes.”

» (Brian McDonald, of MOR Associates, Inc.)

• A team must have:– Clear mission / purpose– Specific and measurable

goals– Agreed upon ground

rules, which include respect for each individual

– Processes and routines– Defined roles and

responsibilities– Feedback mechanisms to

guarantee continuous improvement

Types of teams

• Functional teams • Perform specific organizational functions within a

hierarchical structure

• Cross-functional teams• Made up of experts in various specialty working

together on specific organizational tasks

• Self-directed teams (ego-less)• Operate without managers and are responsible of

complete work processes, maintaining ownership of the entire effort

CliffsNotes.com. Types of Teams. 17 Jan 2008<http://www.cliffsnotes.com/WileyCDA/CliffsReviewTopic/topicArticleId-8944,articleId-8901.html>.

4

The importance of understanding the “team process”

Outline

• Team Basics• The Life of A Team

• Forming, Storming, Norming, Performing, Adjourning

• Team Roles• Working in International Teams• Why Teams Fail• Reading List

5

The Life of A Team

• The Team-Development Model (Forming, Storming, Norming, Performing, Adjourning)– Defined by Bruce Tuckman in 1965 (and then again in 1977 with

M.A Jensen)– Essentially explains how small teams evolve and behave (stage-

model)• The model has been used and adapted in many venues

– The Center for Team Learning, Boston University, adapted Tuckman’s model by building an interactive software (the Team Learning Assistant, TLA 3.0) to help manage the team development lifecycle

• (see reading list for more information)

First StepsTeam

contracts

Team & meeting

mgtPeer

Feedback

After action review

Evaluation

& closing

1 2 3 4 5 6

Forming Storming Norming Performing Adjourning

Stage 1: Forming•This is the beginningof team interactions which entail understanding/ orienting the team

•People are busy with routines related to organizing the team, gathering information and impressions

First Steps

1

• This is generally a comfortable stage where conflict is avoided, but it usually means that only basic operational tasks are initiated

• As team roles and responsibilities are still unclear, those who provide guidance and direction may emerge as leaders, and the team may rely on them for guidance

6

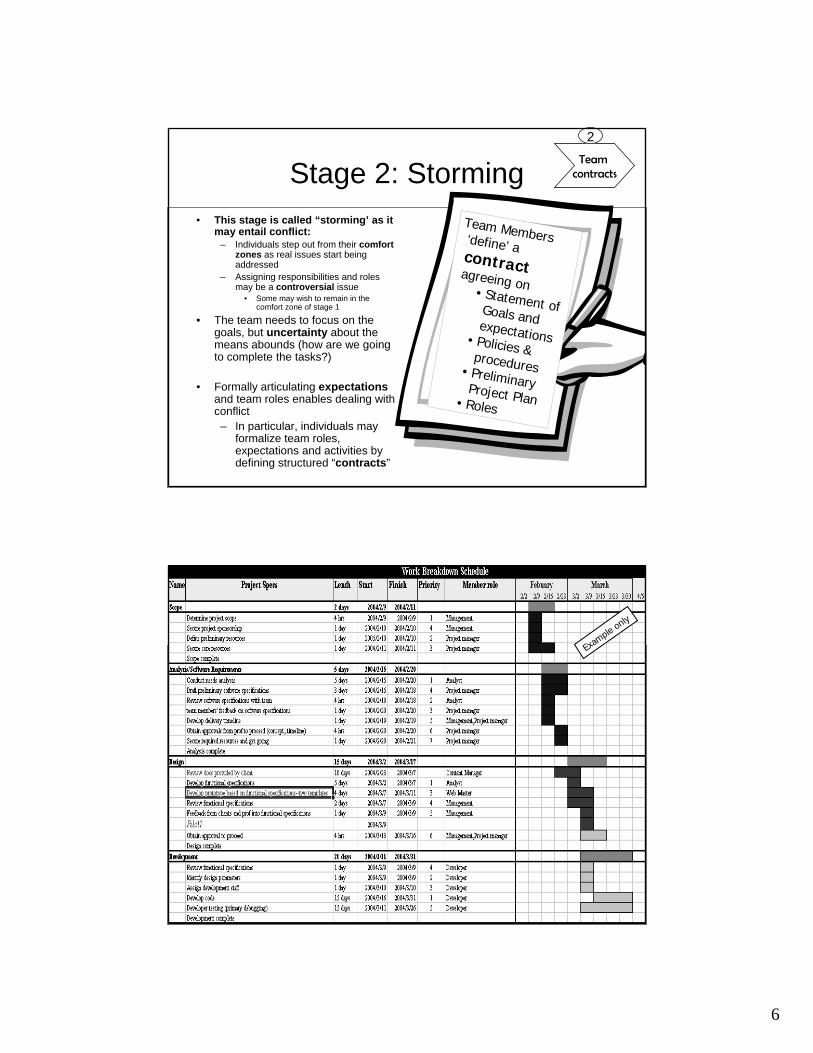

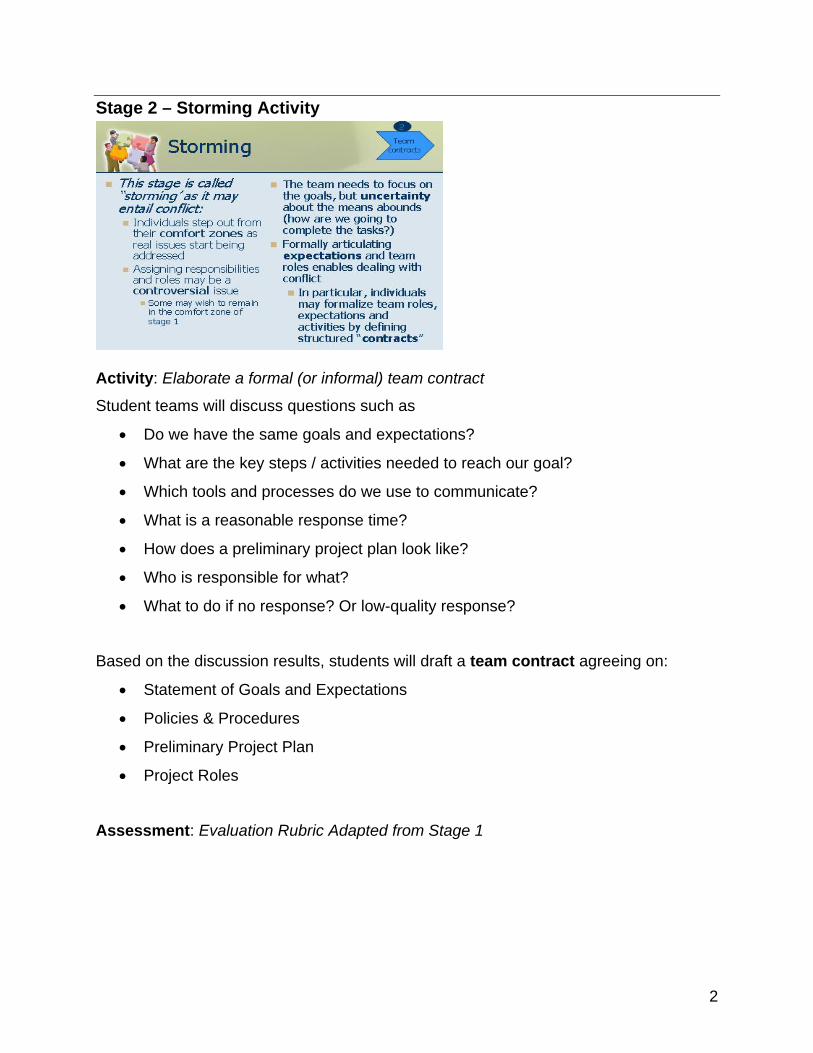

Stage 2: Storming• This stage is called “storming’ as it

may entail conflict:– Individuals step out from their comfort

zones as real issues start being addressed

– Assigning responsibilities and roles may be a controversial issue

• Some may wish to remain in the comfort zone of stage 1

• The team needs to focus on the goals, but uncertainty about the means abounds (how are we going to complete the tasks?)

• Formally articulating expectationsand team roles enables dealing with conflict– In particular, individuals may

formalize team roles, expectations and activities by defining structured “contracts”

Team contracts

2

Team Members ‘define’ a contractagreeing on• Statement of Goals and expectations• Policies & procedures• Preliminary Project Plan• Roles

Example

only

7

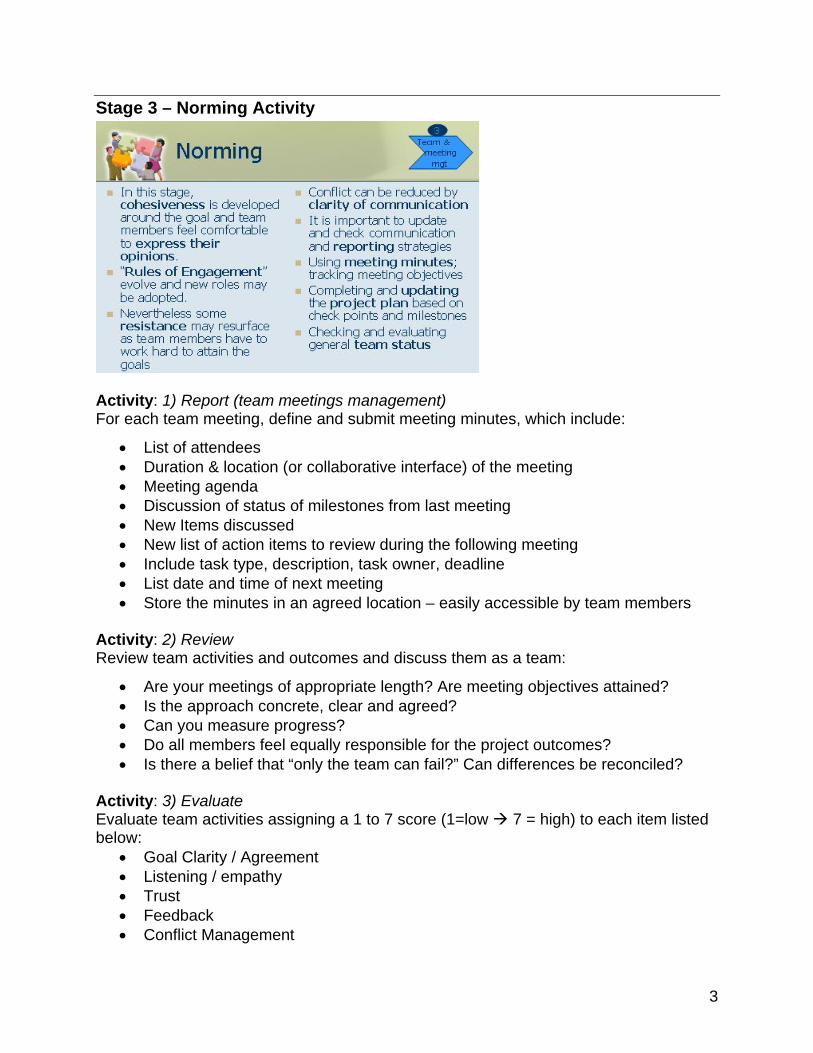

Stage 3: NormingTeam &

meeting mgt

3

• In this stage, cohesiveness is developed around the goal and team members feel comfortable to express their opinions.

• “Rules of Engagement”evolve and new roles may be adopted.

• Nevertheless some resistancemay resurface as team members have to work hard to attain the goals

• Conflict can be reduced by clarity of communication

• It is important to update and check communication and reporting strategies

• Using meeting minutes; tracking meeting objectives

• Completing and updating the project plan based on check points and milestones

• Checking and evaluating general team status

Norming (ctd)

Teamwork surveybased on Tuckman

http://www.nwlink.com/~donclark/leader/teamsuv.html

Enables understanding where your team is in terms of the stage process

– Are your meetings of appropriate length? Are meeting objectives attained?

– Is the approach concrete, clear and agreed?

– Can you measure progress? Do all members feel equally responsible for the project outcomes?

– Is there a belief that “only the team can fail?” Can differences be reconciled?

8

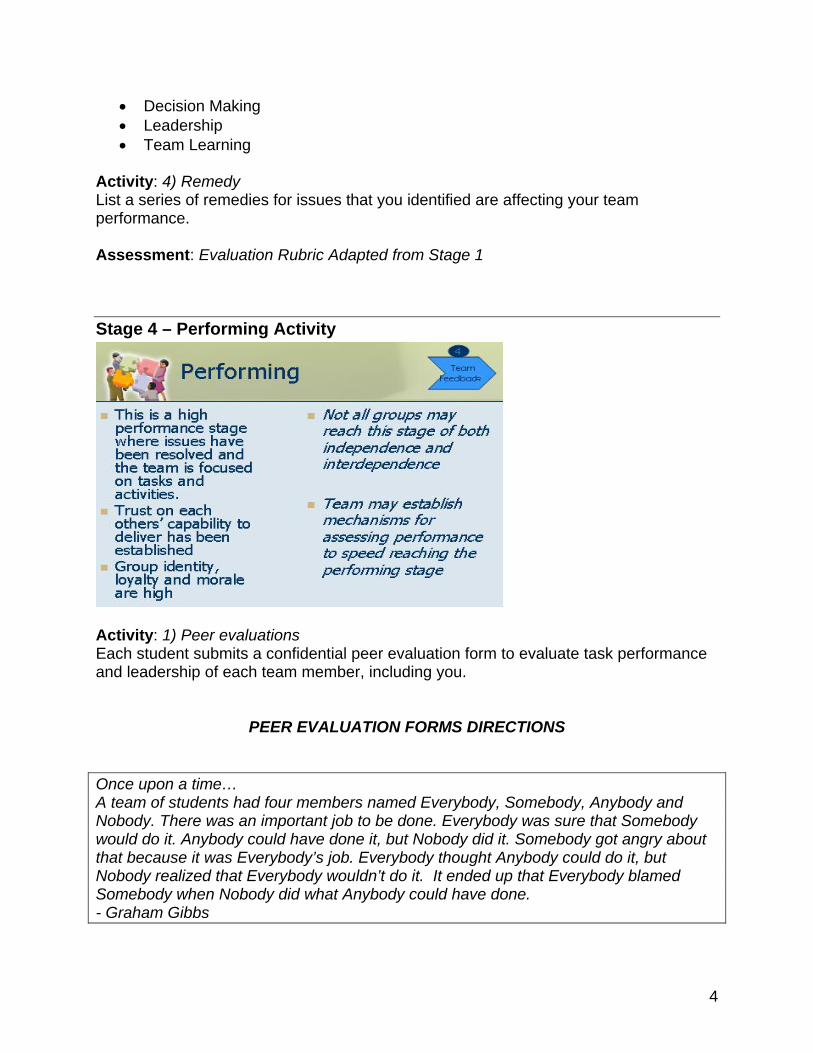

Stage 4: Performing

• This is a high performance stage where issues have been resolved and the team is focused on tasks and activities.

• Trust on each others’ capability to deliver has been established

• Group identity, loyalty and morale are high

• Not all groups may reach this stage of both independence and interdependence

• Team may establish mechanisms for assessing performance to speed reaching the performing stage

Team Feedback

4

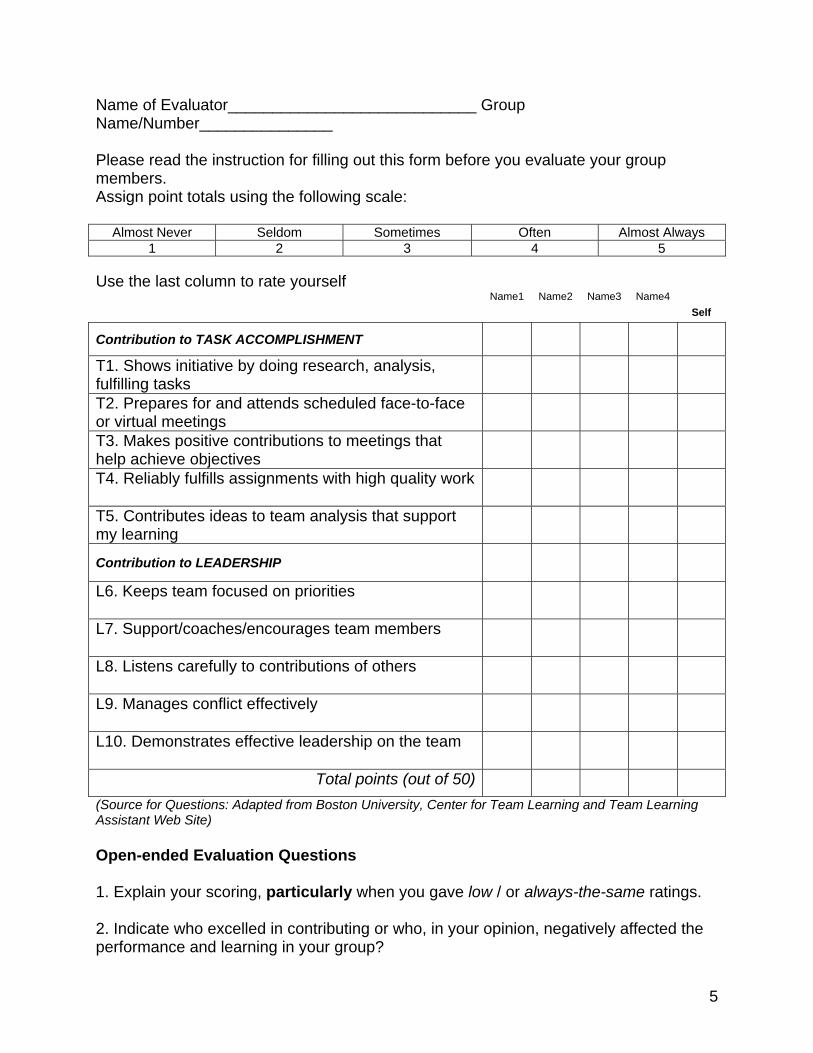

Peer Evaluation• Task-related questions

– Question 1: Shows initiative by doing research and analysis, takes on tasks.

– Question 2: Prepares for and attends scheduled meetings.

– Question 3: Makes positive contributions to meetings and helps team achieve objectives.

– Question 4: Reliably fulfills assignments and work is of high quality.

– Question 5: Contributes ideas to team's analysis and to my learning of course concepts.

• Leadership-related questions– Question 6: Keeps team

focused on priorities.– Question 7:

Supports/coaches/encourages team members.

– Question 8: Listens carefully to contributions of others.

– Question 9: Manages conflict effectively.

– Question 10: Demonstrates effective leadership on the team.

© Center for Team Learning Boston University School of Management

After action review

5

9

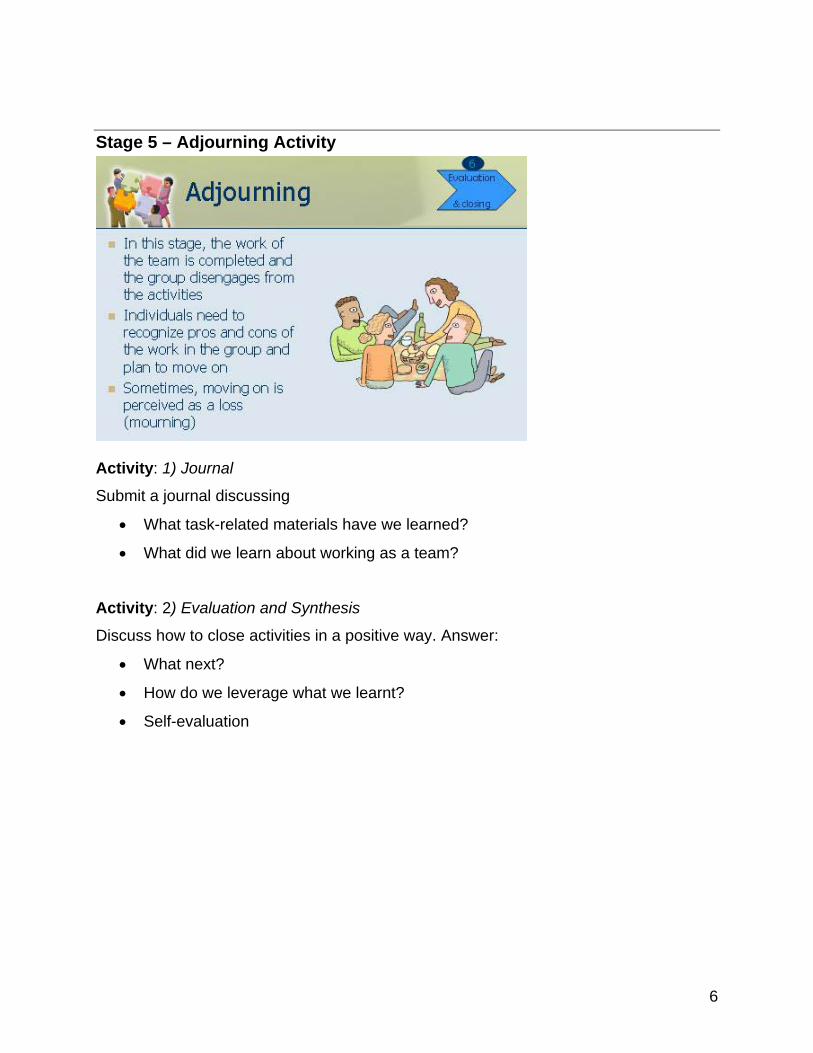

Stage 5: Adjourning • In this stage, the work of

the team is completed and the group disengages from the activities

• Individuals need to recognize pros and cons of the work in the group and plan to move on

• Sometimes, moving on is perceived as a loss (mourning)

Evaluation

& closing

6

Putting it all together: TLA 3.0

• The Team Learning Assistant (TLA 3.0) is an on-line system has been successfully tested in business and engineering courses.

• Developed by the Center for Team Learning Boston University School of Management (© 2001)

• Cost per student $20 (includes booklet and web site access)

– Responds to the need to enhance soft-skills(interpersonal and teamwork)

– Enables automating some of the aspects presented of the team-development process and facilitates the evaluation of learning outcomes trough peer review

10

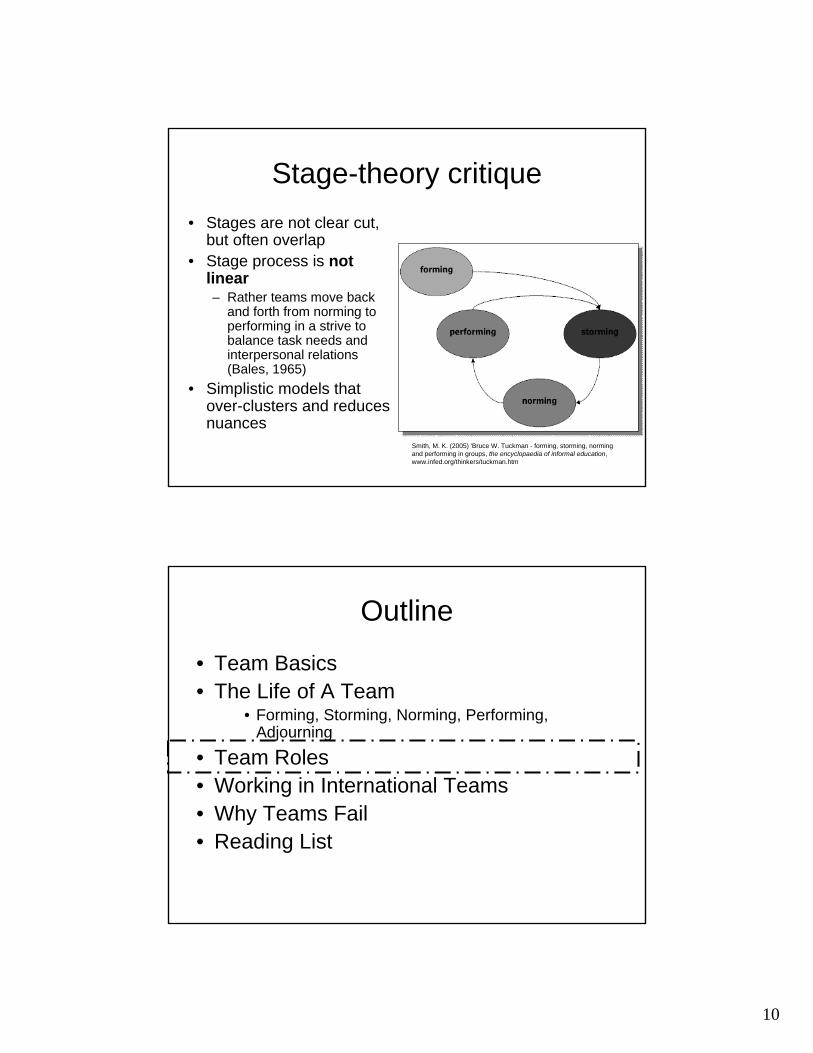

Stage-theory critique• Stages are not clear cut,

but often overlap• Stage process is not

linear– Rather teams move back

and forth from norming to performing in a strive to balance task needs and interpersonal relations (Bales, 1965)

• Simplistic models that over-clusters and reduces nuances

Smith, M. K. (2005) 'Bruce W. Tuckman - forming, storming, normingand performing in groups, the encyclopaedia of informal education, www.infed.org/thinkers/tuckman.htm

Outline

• Team Basics• The Life of A Team

• Forming, Storming, Norming, Performing, Adjourning

• Team Roles• Working in International Teams• Why Teams Fail• Reading List

11

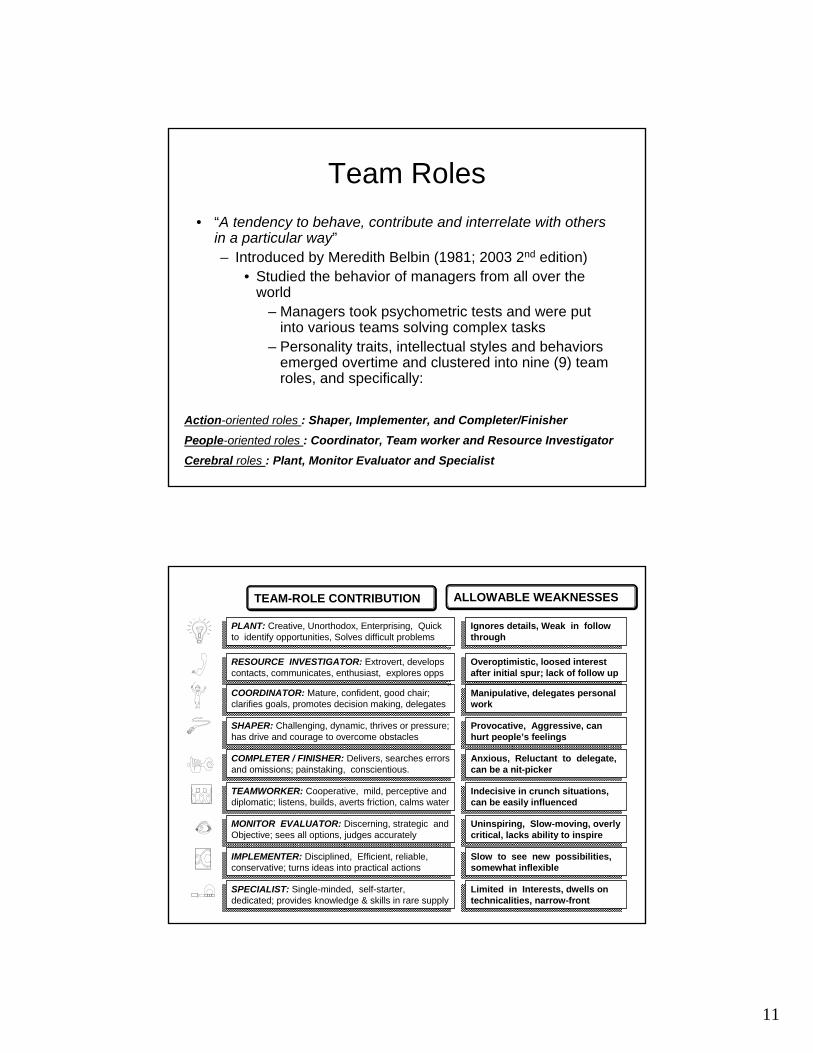

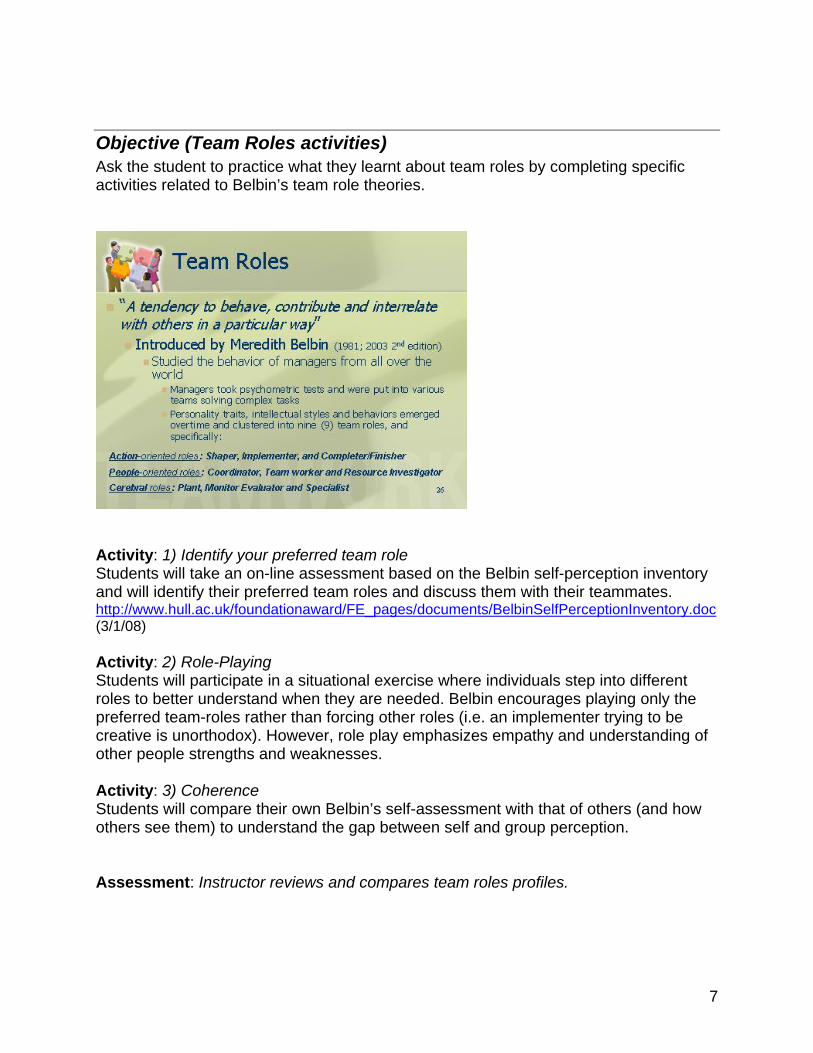

Team Roles• “A tendency to behave, contribute and interrelate with others

in a particular way”– Introduced by Meredith Belbin (1981; 2003 2nd edition)

• Studied the behavior of managers from all over the world

– Managers took psychometric tests and were put into various teams solving complex tasks

– Personality traits, intellectual styles and behaviors emerged overtime and clustered into nine (9) team roles, and specifically:

Action-oriented roles : Shaper, Implementer, and Completer/Finisher People-oriented roles : Coordinator, Team worker and Resource Investigator Cerebral roles : Plant, Monitor Evaluator and Specialist

TEAM-ROLE CONTRIBUTION ALLOWABLE WEAKNESSES

MONITOR EVALUATOR: Discerning, strategic and Objective; sees all options, judges accurately

Uninspiring, Slow-moving, overly critical, lacks ability to inspire

COORDINATOR: Mature, confident, good chair; clarifies goals, promotes decision making, delegates

Manipulative, delegates personal work

IMPLEMENTER: Disciplined, Efficient, reliable, conservative; turns ideas into practical actions

Slow to see new possibilities, somewhat inflexible

COMPLETER / FINISHER: Delivers, searches errors and omissions; painstaking, conscientious.

Anxious, Reluctant to delegate, can be a nit-picker

RESOURCE INVESTIGATOR: Extrovert, develops contacts, communicates, enthusiast, explores opps

Overoptimistic, loosed interest after initial spur; lack of follow up

SHAPER: Challenging, dynamic, thrives or pressure; has drive and courage to overcome obstacles

Provocative, Aggressive, can hurt people’s feelings

TEAMWORKER: Cooperative, mild, perceptive and diplomatic; listens, builds, averts friction, calms water

Indecisive in crunch situations, can be easily influenced

Limited in Interests, dwells on technicalities, narrow-front

SPECIALIST: Single-minded, self-starter, dedicated; provides knowledge & skills in rare supply

PLANT: Creative, Unorthodox, Enterprising, Quick to identify opportunities, Solves difficult problems

Ignores details, Weak in follow through

12

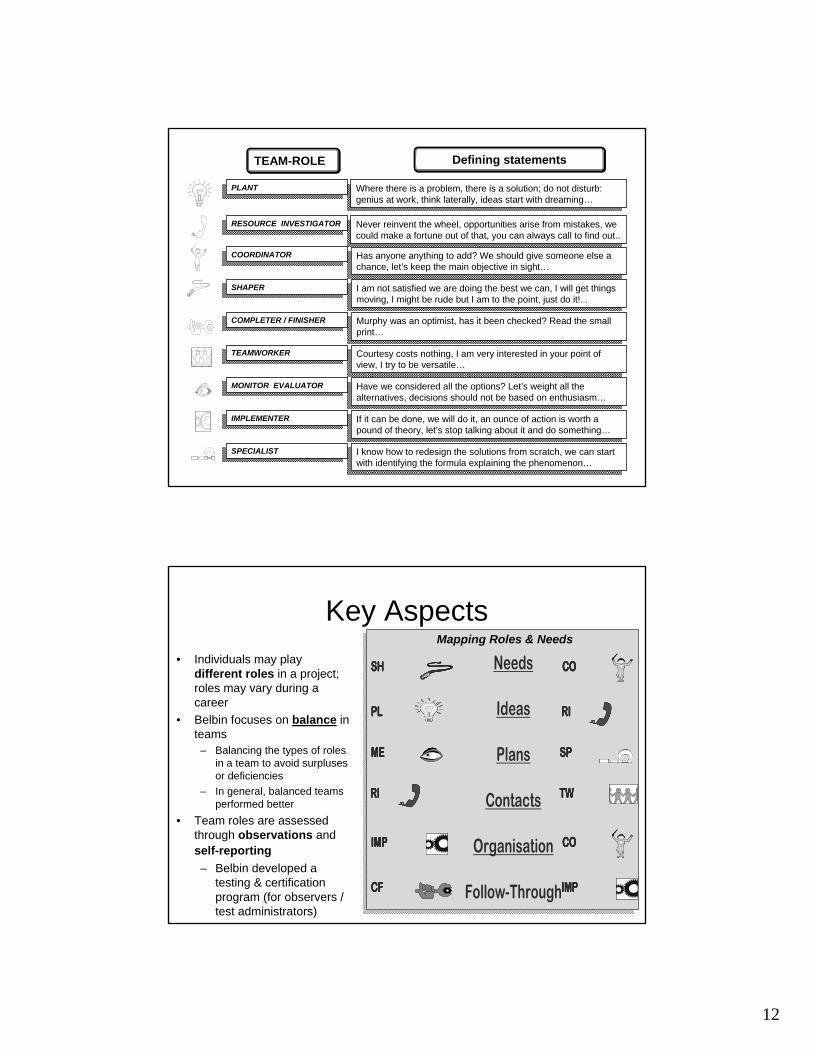

TEAM-ROLE Defining statements

MONITOR EVALUATOR Have we considered all the options? Let’s weight all the alternatives, decisions should not be based on enthusiasm…

COORDINATOR Has anyone anything to add? We should give someone else a chance, let’s keep the main objective in sight…

IMPLEMENTER If it can be done, we will do it, an ounce of action is worth a pound of theory, let’s stop talking about it and do something…

COMPLETER / FINISHER Murphy was an optimist, has it been checked? Read the small print…

RESOURCE INVESTIGATOR Never reinvent the wheel, opportunities arise from mistakes, we could make a fortune out of that, you can always call to find out..

SHAPER I am not satisfied we are doing the best we can, I will get things moving, I might be rude but I am to the point, just do it!...

TEAMWORKER Courtesy costs nothing, I am very interested in your point of view, I try to be versatile…

I know how to redesign the solutions from scratch, we can start with identifying the formula explaining the phenomenon…

SPECIALIST

PLANT Where there is a problem, there is a solution; do not disturb: genius at work, think laterally, ideas start with dreaming…

Key Aspects• Individuals may play

different roles in a project; roles may vary during a career

• Belbin focuses on balance in teams

– Balancing the types of roles in a team to avoid surpluses or deficiencies

– In general, balanced teams performed better

• Team roles are assessed through observations and self-reporting– Belbin developed a

testing & certification program (for observers / test administrators)

Needs

Ideas

Plans

Contacts

Organisation

Follow-Through

COSH

RI TW

ME SP

CF IMP

IMP CO

PL RI

COSH COCOSHSH

RI TWRIRI TWTW

ME SPMEME SPSP

CF IMPCFCF IMPIMP

IMP COIMPIMP COCO

PL RIPLPL RIRI

Mapping Roles & Needs

13

Team-Roles Activities• Role-Playing

• A situational exercise where individuals step into different roles to better understand when they are needed

» Belbin encourages to play your preferred team-roles rather than forcing other roles (i.e. an implementer trying to be creative is unorthodox), although role play emphasizes empathy

• Coherence• Define elements of your coherence, that is the degree to which you

see yourself as others see you; understand which characteristics are constantly defining your behavior by maximizing strengths

• Allowable weaknesses• Identify the context and levels where the allowable weaknesses

may be accepted or should be mitigated (i.e. continuing to be a plant when there is no implementer in a group)

Outline

• Team Basics• The Life of A Team

• Forming, Storming, Norming, Performing, Adjourning

• Team Roles• Working in International Teams• Why Teams Fail• Reading List

14

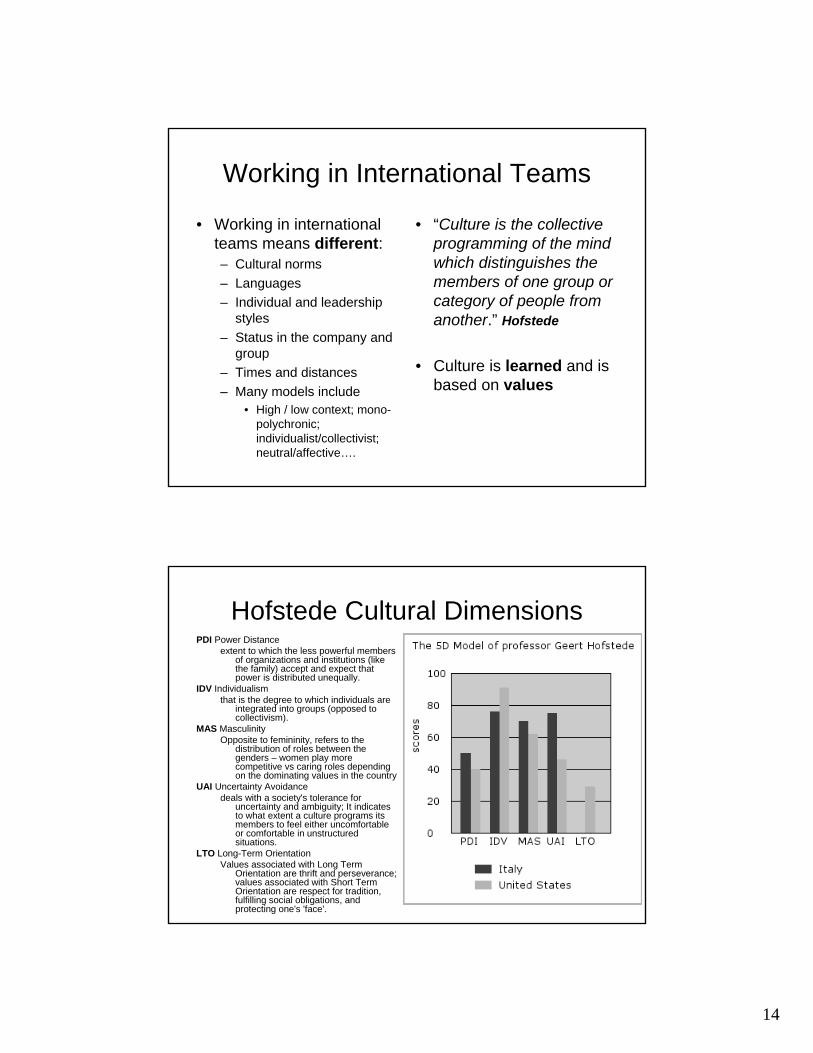

Working in International Teams

• Working in international teams means different:– Cultural norms– Languages– Individual and leadership

styles– Status in the company and

group– Times and distances– Many models include

• High / low context; mono-polychronic; individualist/collectivist; neutral/affective….

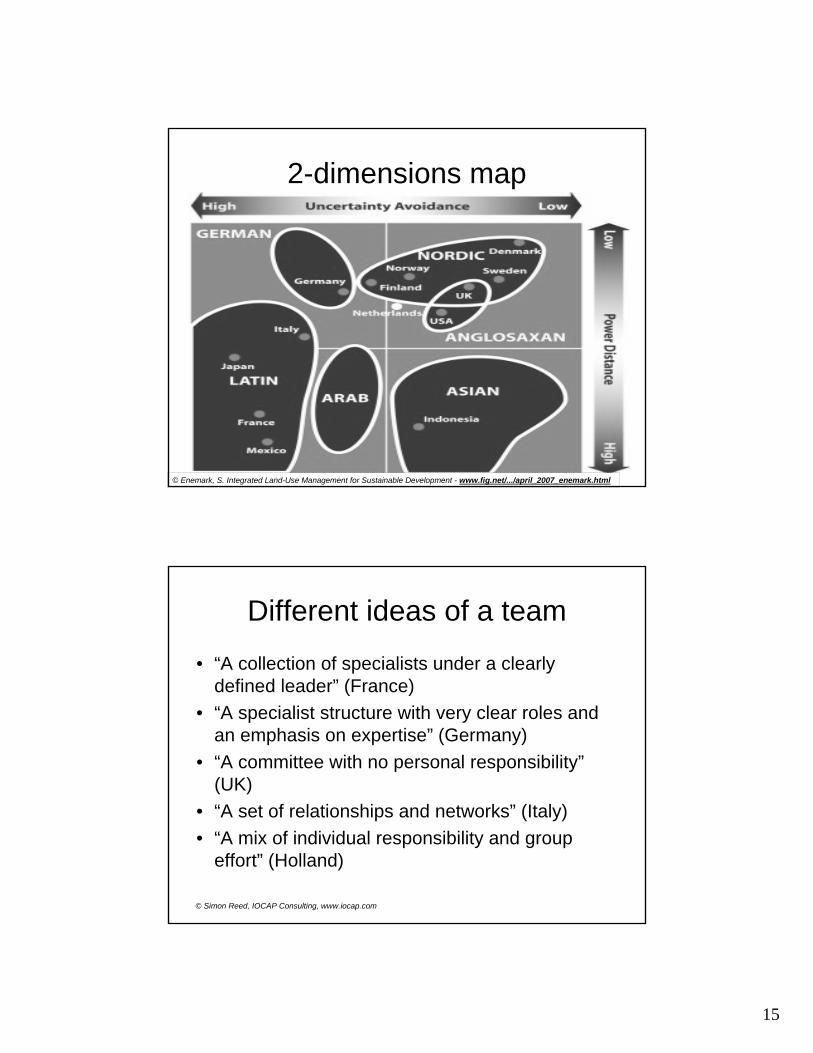

• “Culture is the collective programming of the mind which distinguishes the members of one group or category of people from another.” Hofstede

• Culture is learned and is based on values

Hofstede Cultural DimensionsPDI Power Distance

extent to which the less powerful members of organizations and institutions (like the family) accept and expect that power is distributed unequally.

IDV Individualismthat is the degree to which individuals are

integrated into groups (opposed to collectivism).

MAS MasculinityOpposite to femininity, refers to the

distribution of roles between the genders – women play more competitive vs caring roles depending on the dominating values in the country

UAI Uncertainty Avoidancedeals with a society's tolerance for

uncertainty and ambiguity; It indicates to what extent a culture programs its members to feel either uncomfortable or comfortable in unstructured situations.

LTO Long-Term OrientationValues associated with Long Term

Orientation are thrift and perseverance; values associated with Short Term Orientation are respect for tradition, fulfilling social obligations, and protecting one's 'face'.

15

2-dimensions map

© Enemark, S. Integrated Land-Use Management for Sustainable Development - www.fig.net/.../april_2007_enemark.html

Different ideas of a team

• “A collection of specialists under a clearly defined leader” (France)

• “A specialist structure with very clear roles and an emphasis on expertise” (Germany)

• “A committee with no personal responsibility”(UK)

• “A set of relationships and networks” (Italy)• “A mix of individual responsibility and group

effort” (Holland)

© Simon Reed, IOCAP Consulting, www.iocap.com

16

Outline

• Team Basics• The Life of A Team

• Forming, Storming, Norming, Performing, Adjourning

• Team Roles• Working in International Teams• Why Teams Fail• Reading List

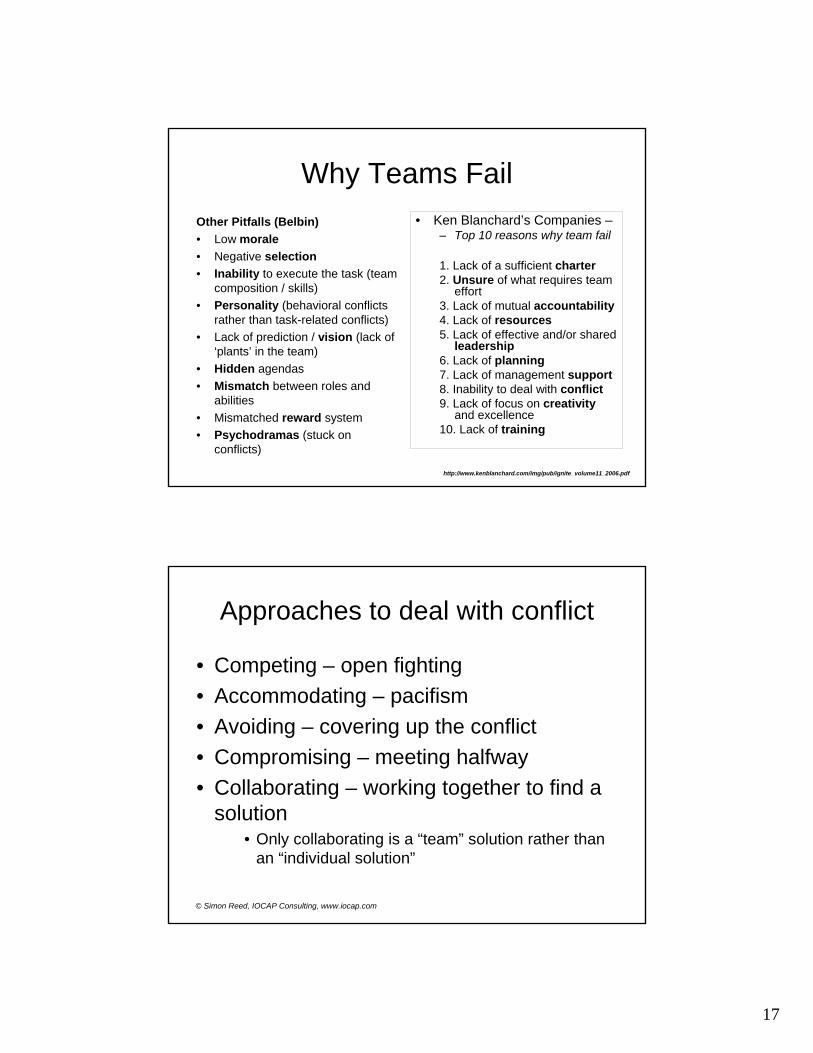

Why Teams FailPotential Pitfalls in Start-up

• Team leader or sponsor fails to explain the purpose

• No awareness of stakeholders • Team fails to establish or agree on

a mission – To capture the essence of why

they exist as a team • Goals and measurements not

established • Roles and responsibilities not well

defined • Expectations not clear• All the above my lead to

“scope creeps”» (Brian McDonald, of

MOR Associates, Inc.)

• Operational Pitfalls

• Lack of agendas in advance of meetings

• Lack of ground rules– Define how to deal with issues

• Limited use of templates to report progress and program status (what/who/by when?)

• Lack of delegation– Alienating team members

• Focusing on task without awareness of the process

• Assuming that the work is completed with a recommendations (and then ‘we are out of here’)

» (Brian McDonald, of MOR Associates, Inc.)

17

Why Teams FailOther Pitfalls (Belbin)• Low morale• Negative selection• Inability to execute the task (team

composition / skills)• Personality (behavioral conflicts

rather than task-related conflicts)• Lack of prediction / vision (lack of

‘plants’ in the team)• Hidden agendas• Mismatch between roles and

abilities• Mismatched reward system• Psychodramas (stuck on

conflicts)

• Ken Blanchard’s Companies –– Top 10 reasons why team fail

1. Lack of a sufficient charter2. Unsure of what requires team

effort 3. Lack of mutual accountability4. Lack of resources5. Lack of effective and/or shared

leadership6. Lack of planning7. Lack of management support8. Inability to deal with conflict9. Lack of focus on creativity

and excellence 10. Lack of training

http://www.kenblanchard.com/img/pub/ignite_volume11_2006.pdf

Approaches to deal with conflict

• Competing – open fighting• Accommodating – pacifism• Avoiding – covering up the conflict• Compromising – meeting halfway• Collaborating – working together to find a

solution • Only collaborating is a “team” solution rather than

an “individual solution”

© Simon Reed, IOCAP Consulting, www.iocap.com

18

Outline

• Team Basics• The Life of A Team

• Forming, Storming, Norming, Performing, Adjourning

• Team Roles• Working in International Teams• Why Teams Fail• Reading List

Reading List• Smith, M. K. (2005) 'Bruce W. Tuckman - forming, storming, norming and

performing in groups, the encyclopaedia of informal education, www.infed.org/thinkers/tuckman.htm