indas 109 : financial instruments · pdf fileindas 109 : financial instruments ... a financial...

TRANSCRIPT

IndAS 109 : Financial Instruments

CA Gautam Shah

WIRC – Intensive course on IndAS19 May 2017

Setting the Context

Lets go back to history of standard on Financial Instrument

Setting the Context

IAS 25 Accounting for Investments

IAS 39 Financial Instrument

IFRS 9 Financial Instrument

Setting the Context

One of the most challenging standards because it’s sooo

complex and complicated.

Setting the Context

NOT ALWAYS…….

Most of principles and concepts are logical. Only in

some exceptional cases, it becomes complex…..

We are not dealing with those exceptions…. We will be discussing Principles and Concepts

GOOD NEWs……

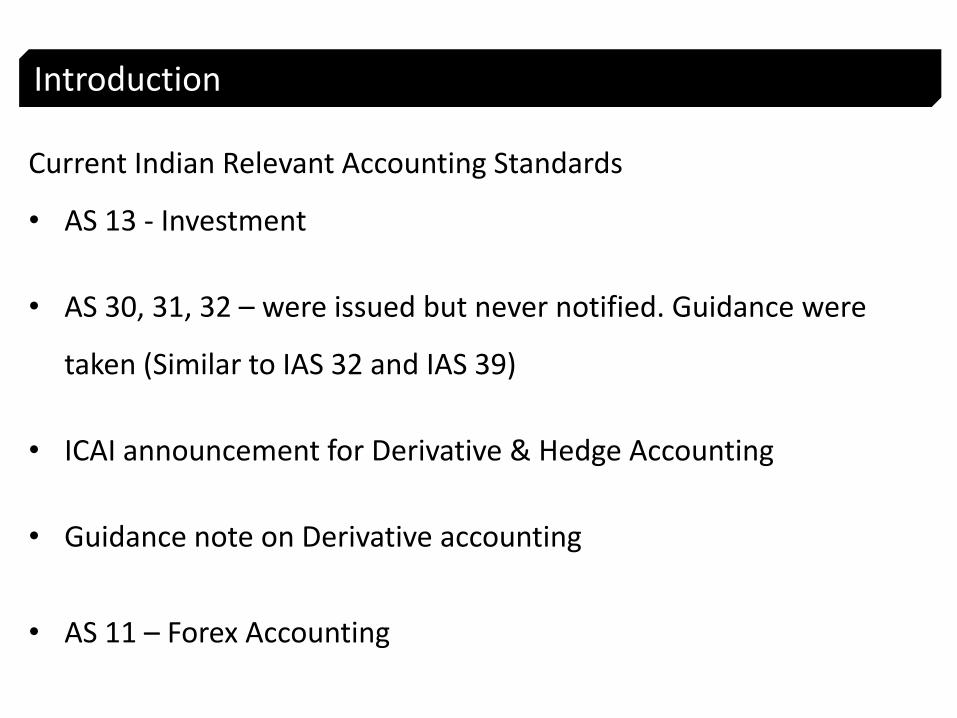

Current Indian Relevant Accounting Standards

• AS 13 - Investment

• AS 30, 31, 32 – were issued but never notified. Guidance were

taken (Similar to IAS 32 and IAS 39)

• ICAI announcement for Derivative & Hedge Accounting

• Guidance note on Derivative accounting

• AS 11 – Forex Accounting

Introduction

Currently no specific Accounting Standards

• Debtors or Receivables

• Creditors or Trade Payables

• Borrowings & Equity

• Loans & Advances

• Guarantees & Commitments

Introduction

What does Scope of IndAS 109 Cover:

Introduction

Only One Thing……………

“FINANCIAL INSTRUMENTS”

Hence It is important to first ensure whether particular

instrument falls within definition of “Financial Instrument”

• Interest in subsidiaries, associates and joint venture (Ind AS 110, 27,28)

• Leases (Ind AS 17)

• Employee Benefits (Ind AS 19)

• Rights and Obligations under an insurance contract or a contract (Ind AS 104)

• A forward contract resulting into a business combination (Ind AS 103)

• Share based payments (Ind AS 102)

• Rights and obligation within the scope of (Ind AS 115)

Exceptions to Ind AS 109

Flow of Presentation

Identification

Classification

Measurement

Reclassification

Derecognition

Impairment

Hedge Accounting

Identification

Financial Asset and Financial Liability :

• Contractual Arrangement• Settlement Terms

Equity : Residual interest in Entity

• Variable number of shares – hence consideration amount is fixed

• Fixed number of shares – hence consideration amount is dependingon performance of co, hence Equity.

Concepts

What is a Financial Instrument?

Any “contract”

o Giving rise to a “financial asset” of one entity and

o “financial liability” or “equity” of another entity

Equity

A financial instrument is an equity instrument only if:

• the instrument includes no contractual obligation to deliver cash oranother financial asset to another entity; and

• if the instrument will or may be settled in the issuer’s own equityinstruments, it is either:

✓ a non-derivative that includes no contractual obligation for the issuer to deliver avariable number of its own equity instruments; or

✓ a derivative that will be settled only by the issuer exchanging a fixed amount ofcash or another financial asset for a fixed number of its own equity instruments.

What is an equity instrument?An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities

a) Cash

b) An equity instrument of another entity

c) A contractual right:1. To receive cash or another financial asset from another entity, or2. To exchange financial asset or financial liabilities with another entity

under conditions that are potentially favourable to the entity

d) A contract that will or may be settled in the entity’s own equityinstruments and is:

1. A non derivative for which the entity is or maybe obliged to receive avariable number of the entity’s own equity instruments

2. A derivative that will or may be settled other than by the exchange of afixed amount of cash or another financial asset for a fixed number of theentity’s own equity instruments.

Financial Asset

a) A contractual obligation1. To deliver cash or another financial asset to another entity2. To exchange financial assets or financial liabilities with another

entity under conditions that are potentially unfavourable to theentity

b) A contract that will or may be settled in the entity’s own equityinstruments and is:1. A non-derivative for which the entity is or may be obliged to deliver

a variable number of the entity’s own equity instruments

2. A derivative that will or may be settled other than by the exchangeof a fixed amount of cash or another financial asset for a fixednumber of the entity’s own equity instruments

Financial Liability

a. Sale of Goods on Credit

b. Sale of Goods on Credit and Settlement in Own Equity Shares

c. Advance Given

d. Advance Given for Delivery of Goods

e. Warranty Given

f. Warranty Given – In case of default of X part, the Company will pay INR 500

g. Statutory Payment Liability

h. Convertible Debentures

Quiz

X Ltd Sold Goods to Y Ltd. Normal Credit period is 30 days.

1. Y Ltd made payment in advance.

2. Y Ltd will make payment after 90 days.

Case Analysis

X Ltd. issues 10,000 preference shares. The instrument contains a condition thatthe issuer has to transfer a property to the holder of the instrument if it fails tomake dividend payments.

Should the instrument be classified as an equity or a financial liability ?

Case Analysis

1. Further Info Needed on Redeemable or Convertible – That will decideclassification of principal amount to Equity or Debt

2. For Fixed dividend = not linked to residual interest in Co, hence not equity

A financial instrument may contain a non-financial obligation that must besettled, if and only if, the entity fails to make distributions or to redeem theinstrument. In case the entity can avoid transfer of cash or another financialasset only by settling the non-financial obligation, the financial instrument is afinancial liability.

In the given case of X Ltd., in case the entity fails to make dividend paymenton 10,000 preference shares, it has to transfer a property to the holder of theinstrument which becomes non-financial obligation. Hence, the instrument beclassified a financial liability.

Solution to Case Analysis

Classification

Concepts

AmortisedCost

Fair Value through Other Comprehensive income (FVOCI)

Certain Debt instruments

Certain equity instruments

Fair Value through profit or loss (FVTPL)

Test for Classification:➢ Business Model Tests➢ Contractual Cash flow Tests

Financial Assets

Debt Instrument• Terms of Instrument• Intention of the holder

• SPPI – Amorised Cost• SPPI + Sale – FVOCI• Others – FVTPL

Equity• Default – FVTPL• Can Elect – FVOCI (Realised gain/loss also in OCI)

Derivative• FVTPL, except Hedge accounting

Concepts

Financial Liabilities

Amortised CostExcept• Trading Liability

• Designated as FV

Classification of Financial Assets

Classification of Financial Assets

Debt

Business Model Test (at an aggregate level)

Held for Trading ?

Conditional Fair value option (FVO) elected ?

Contractual cash flow characteristics test (‘at instrument level’)

Hold to collect contractual cash flow

collect contractual cash flow & selling FA

Neither of the two

NoNo

Pass

Yes

Yes

Amortised Cost FVOCI (with recycling) FVTPL

• For any testing of classification of any financial asset, its contractual termsmust give rise on a specified date to the cash flows that are solely consist of:

A. PrincipalB. Interest on the Principal Amount Outstanding

• Definition:

Principal – Fair Value of asset on initial recognition

Interest – Consideration for time value of money, credit risk, other basic lending risk (Liquidity Risk), other associated cost (Admin cost) and profit margin.

Fair value of asset on initial recognition.

Contractual Cash Flow Characteristic Test

Hold the asset to collect contractual cash flow

Hold the asset to collect contractual cash flow and for sale

• The business model is determined at a level that reflects how groups of financial assets are managed together to achieve a particular business objective.

• The business model is determined by the entity’s key management personnel in the way that assets are managed and their performance is reported to them.

• Identification of Business Model is a subjective concept and shall vary from company to company. It cannot be identified on the basis of any single factor but needs to consider all the available evidences as on date.

Business Model Assessment Test

Meets the two requirements to be measured at amortisedcost or FVTOCI

Available OptionTo designate, at initial recognition, at FVTPL

if doing so eliminates or significantly reduces ameasurement or recognition inconsistency ('accountingmismatch') that would otherwise arise from measuringassets or liabilities or recognising the gains and losses onthem on different bases.

Fair Value Option (FVO)

Debt Instrument (Basic Loan features)- Example

Held to collect contractual cash flows

Not held to collect contractual cash flows

Amortised cost(FVO available if criteria are met)

Fair value through profit or loss

Debt Instrument (embedded derivative)- Example

Hybrid contract (as a whole) has basic loan features and is Held to collect contractual CFs

All other hybrid contracts with financial hosts

Whole instrument at amortised cost

Whole instrument at fair value through profit or loss

Classification of Financial Assets

Equity

Held for Trading ?

FVOCI option selected

Fail

Yes

Yes

No

No

FVOCI (no recycling)

FVTPL

Equity Instrument- Example

Held for trading

Not held for trading

Fair value - with changes recognised in profit or loss

Fair value – irrevocable choice of recognising

changes in profit or loss or OCI

Classification of Financial Liabilities

All financial liabilities

Amortised cost

FVO for mismatch,

managed on FV basis

Own credit in

OCI

Except

Held for tradingFair value through

P&L

Fair Value Designation:

• Doing so eliminates or significantly reduces accountingmismatch

• Part of group of assets which are evaluated on a fair valuebasis

• Embedded Derivatives

Classification of Financial Liabilities

What is ‘own credit’?➢ Fair value changes in liability arising from changes in the

issuer’s credit quality

What is the concern?➢ Gain when credit quality deteriorates, loss when credit quality

improves

FV change due to own credit - To recognise in OCI

Financial Liabilities (FVO and Own Credit)

Measurement

Concepts

Initial Measurement at Fair Value

Normally Transaction Value is Fair value, unless in exceptional cases

Transaction Cost – For FVTPL in PL, Other category, to be added to cost

Subsequent Measurement

Amortised Cost – IRR

Fair Value as at reporting date and gain/loss in OCI or PL

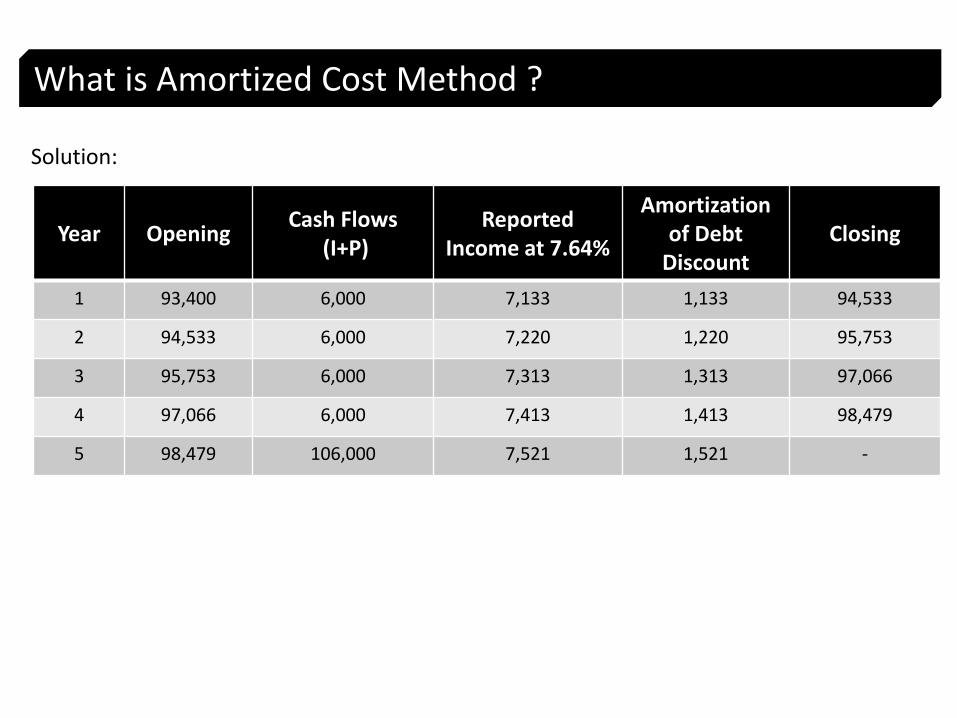

What is Amortized Cost Method ?

Amortized Cost is the cost of an asset or liability, as adjusted, to achieve a constant effective rate of interest over the life of the asset or a liability.

• In common parlance, Amortized Cost method involves calculation ofpresent value of all future cash flows (contracted cash flows) expectedfrom a particular instrument throughout its life at the market prevailingrate of interest or expected yield.

• Transaction Cost that are capitalized would also form a part the cash flowon Day 1 and would be considered for calculation of present value.

• The component that would finally be debited to the P&L would be theinterest calculated on the basis of above method.

What is Amortized Cost Method ?

Example:

A debt security has a FV of Rs. 100,000 which will be repaid at maturity in 5 years.

The coupon rate of the instrument is 6% payable annually at the end of each year until maturity.

X Ltd purchase the said security in market for Rs. 93,400 (including transaction cost of Rs.100)

Based on market rate of 7.64%, calculate amortized cost and reported interest income in each year.

What is Amortized Cost Method ?

Solution:

Year OpeningCash Flows

(I+P)Reported

Income at 7.64%

Amortization of Debt

DiscountClosing

1 93,400 6,000 7,133 1,133 94,533

2 94,533 6,000 7,220 1,220 95,753

3 95,753 6,000 7,313 1,313 97,066

4 97,066 6,000 7,413 1,413 98,479

5 98,479 106,000 7,521 1,521 -

Reclassification

Concepts

Reclassification

• Recognition and measurement is depending on classification of FA

• Classification is based on certain principles, hence if there is change in principles –reclassification need to be done

• On initial recognition, if entity has opted from FV, hence same can not be reclassified.

• Measurement to be done on date of reclassification

When can we reclassify?

Reclassification is possible:When and only when, an entity changes its business model for managing financial assets

What is NOT a change in business model?• A change in intention related to particular financial assets• A temporary disappearance of a particular market for financial assets• A transfer of financial assets between parts of the entity with different business

models

What is a change in business model?Management decides to sell portfolio of mortgages, which were hold initially till maturity

• No reclassification for financial liabilities

• No reclassification for FA or FL designated at Fair Value

• No reclassification for Equity Instrument – Designated as FVOCI – Can not be reclassified

– FVOCI designation only permitted at initial recognition, hence no reclassification of FVTPL

• To apply prospectively

Reclassification

Original Revised Treatment

Amortised Cost FVTPL FV on reclassification date. Difference in PL

FVTPL Amortised Cost FV on reclassification date becomes new carrying vale. EIR computed based on new carrying vale.

Amortised Cost FVOCI FV on reclassification date. Difference in OCI

FVOCI Amortised Cost FV on reclassification date becomes new carrying vale. Cumulative Gain/loss in OCI to be adjusted to fair value.

FVPL FVOCI Asset @ FV. No change to previous FV gain/loss.

FVOCI FVPL Asset @ FV. Cumulative Gain/loss in OCI to be adjusted to PL.

Measurement on reclassification

Derecognition

Concepts

Derecognition

Derecognition based on contractual terms

Need to assess substance of transaction – If entity continue to enjoy cashflows, may need to continue recognition of asset

Measurement of gain/loss on derecognition

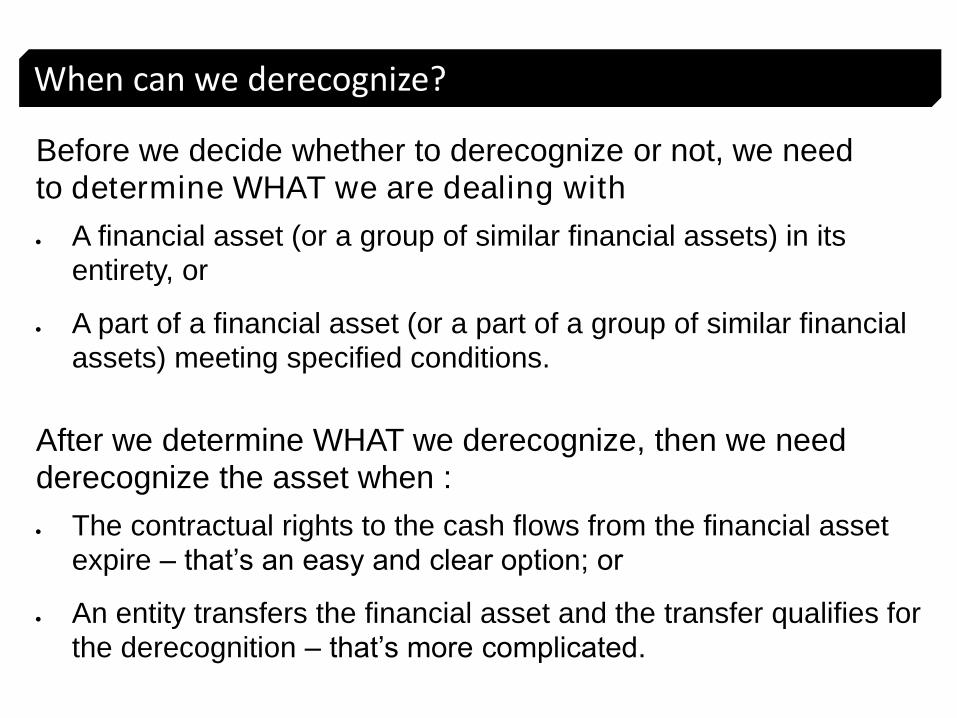

When can we derecognize?

Before we decide whether to derecognize or not, we need to determine WHAT we are dealing with

• A financial asset (or a group of similar financial assets) in its

entirety, or

• A part of a financial asset (or a part of a group of similar financial

assets) meeting specified conditions.

After we determine WHAT we derecognize, then we need derecognize the asset when :

• The contractual rights to the cash flows from the financial asset

expire – that’s an easy and clear option; or

• An entity transfers the financial asset and the transfer qualifies for

the derecognition – that’s more complicated.

Derecognition of Financial Assets

START

Entire asset or part?

DERECOGNIZE

Transfer of

rights?

Rights to cash flows

expired?

Risk/rewards transfer

?

Oblig-ation to pay CF?

Risk/rewards retaine

d?

Control retaine

d?

CONTINUE TO RECOGNIZE

DERECOGNIZE

CONTINUE TO RECOGNIZE

DERECOGNIZE

YES

NO NO YES NO NO

YESYES

YES

YESNO NO

Proceeds receivedCashOther Financial Assets received

Less: Carrying amount (measured at date of disposal)THUS: first have to restate balance

=Profit or loss on disposal recognized in P/L

Therefore, IF SOLD AT FV= no profit or loss

Derecognition Amount

Impairment - ECL

Concepts

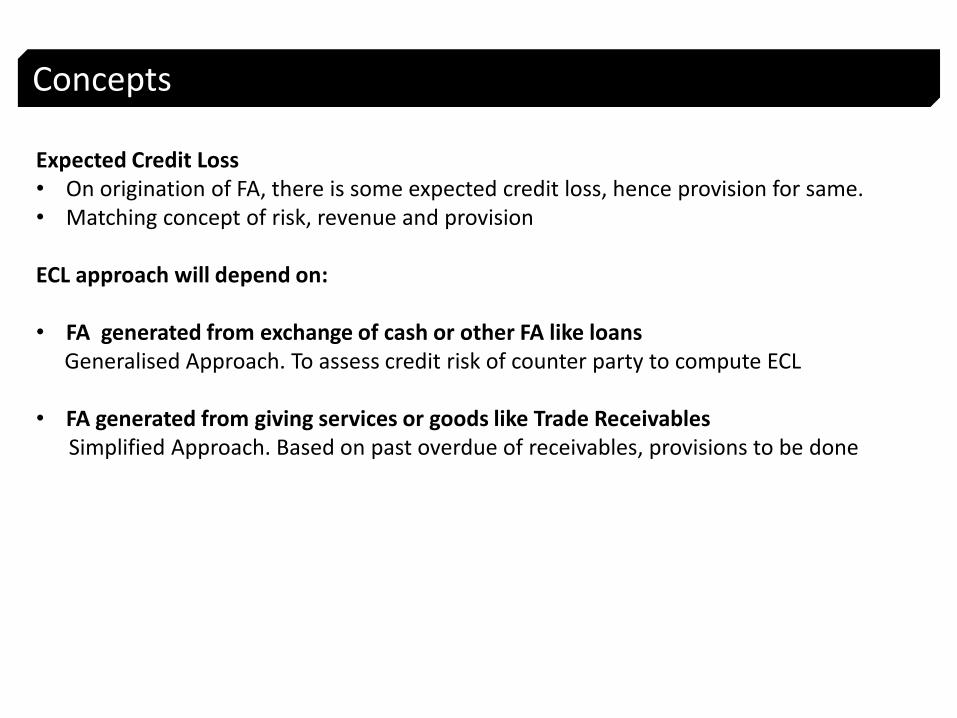

Expected Credit Loss• On origination of FA, there is some expected credit loss, hence provision for same. • Matching concept of risk, revenue and provision

ECL approach will depend on:

• FA generated from exchange of cash or other FA like loansGeneralised Approach. To assess credit risk of counter party to compute ECL

• FA generated from giving services or goods like Trade ReceivablesSimplified Approach. Based on past overdue of receivables, provisions to be done

Financial Asset IFRS 9 Classification Impairment TestingRequired?

Debt Instrument Amortised Cost Yes

FVOCI Yes

FVTPL No

Equity Any No

Lease receivable Yes

Trade Receivables Yes

Loan Commitment Yes

Financial Guarantees Yes

Impairment

Not applicable to any instrument measured at FVPL

Impairment

Approaches

General Approach• FA measured at Amortised Cost, FVOCI• Financial Guarantees• Loan Commitment

Simplified Approach• Trade Receivables• Lease Receivable

General Approach

EL = PD * LGD * EAD

Expected Loss (EL) as at reporting date

Probability of Default (PD) – Assessed based on External Rating, Past History of performance

Loss Given Default (LGD) - Amount of loss if there is Default. Normally Collateral Securities are considered

Exposure At Default (EAD) – The total exposure to credit risk is the amount that the borrower owes to the lending institution at the time of default

General Approach

This newly adopted standard lays down “Three-Stage” Model for impairment based on change in the credit quality since initial recognition:

12-month expected credit losses

Are a portion of the lifetime expected credit losses and represent the amount of expected credit losses that result from default events that are possible within 12 months after the reporting date.

Lifetime expected credit losses

The expected credit losses that result from all possible default events over the life of the financial instrument.

Credit loss Contractual Cashflows less Expected Cashflows

General Approach

Dual Measurement approach

Under the general principle, one of two measurementbases will apply:– 12-month expected credit losses; or– lifetime expected credit losses.

The measurement basis would depend on whether there has been a significant increase in credit risk since initial recognition.

Changes in operating results

Information to take into account for assessment of increased credit risk

Changes in external market

indicators

Changes in credit ratings

Changes in internal price

indicators

Changes in business

Other qualitative inputs

30 days past due

rebuttable presumption

However….

General Approach

Objective Evidence : Stage 3

Expected credit losses

Financial assets

• ECL represent a probability-weighted estimate of the difference over the remaining life of the financial instrument, between:

Undrawn loan commitments

• ECL represent a probability-weighted estimate of the difference over the remaining life of the financial instrument, between:

Present value of cash flows according to

contract

Present value of cash flows the entity

expects to receive

Present value of cash flows if holder draws

down

Present value of cash flows the entity

expects to receive if drawn down

General Approach

Banks – Regulatory PD and IndAS 109 PD

• Twelve-month expected credit losses used for regulatory purposesare normally based on ‘through the cycle’ (‘TTC’) probabilities of adefault (that is, probability of default in cycleneutral economicconditions) and can include an adjustment for prudence.

• PD used for IndAS 109 should be ‘point in time’ (‘PiT’)probabilities (that is, probability of default in current economicconditions) and do not contain adjustment for “prudence”.

• However, regulatory PDs might be a good starting point, providedthey can be reconciled to IndAS 109 PDs.

General Approach

Simplified Approach

The simplified approach does not require an entity to track thechanges in credit risk, but, instead, requires the entity to recognisea loss allowance based on lifetime ECLs at each reporting date,right from origination.

ECL provision can be done based on provision matrix. i.e. dayspass due.

Primarily applied to Trade Receivables, Lease Receivables

Trade and Lease Receivables and Contract Assets

Lease receivables Trade receivables and contract assets with a significant financing component

Trade receivables and contract assets without a significant financing component

Policy election to apply

General ApproachSimplified Approach

Loss allowance always equal to lifetime expected credit losses

On 31 December 20X1, Bank grants a loan to • A borrower with credit rating of A @ interest rate of 10%• B borrower with credit rating of BB @ interest rate of 12%

The price of the loan does not reflect incurred credit losses

Loss Allowance recognition - Illustration

Q: What loss allowance Bank should recognise in the statement of financial position at 31 December 20X1 for A Ltd and B Ltd

A. NoneB. 12-month expected credit lossesC. Lifetime expected credit losses

B. 12-month expected credit losses.

Loss Allowance recognition - Rationale

• Under the general model of IND AS 109, all assets need to have a loss allowance.

• Allowance covers either 12-month or lifetime expected credit losses depending on whether the asset’s credit risk has increased significantly.

• Since the loan has just been granted and there has not been a significant increase in credit risk, an allowance equal to 12-month expected credit losses is appropriate.

Hedge

Concepts

Hedge Accounting

Hedge Item – What Company wants to HedgeHedge Instrument – Instrument executed for Hedging, generally Derivatives.

Objective of Hedge – To cover RiskObjective of Hedge Accounting – To eliminate accounting mis-match due to hedge

Hedge Accounting is optional. If opted, need to comply with all required documentation and disclosures

Fair Value Hedge – To hedge fair value of existing assetExisting assets FV is accounted in PL, hence FV of Hedged instrument also in PL

Cash Value Hedge – To hedge future cashflowFuture cashflows i.e. no existing asset to hedge, hence FV of hedged instrument is parked in OCI. Recycled when actual cashflow happens.

Hedge accounting : To mitigate Accounting mis-match

Hedge accounting recognizes• the offsetting effects of changes in the fair values or

• the cash flows of the hedging instrument and the hedged item.

Strict conditions must be met before hedge accounting is possible:

• there must be formal designation and documentation of a hedge,including the risk management strategy for the hedge

• the hedging instrument must be expected to be highly effective inachieving offsetting changes in fair value or cash flows of thehedged item that are attributable to the hedged risk.

Hedge Accounting

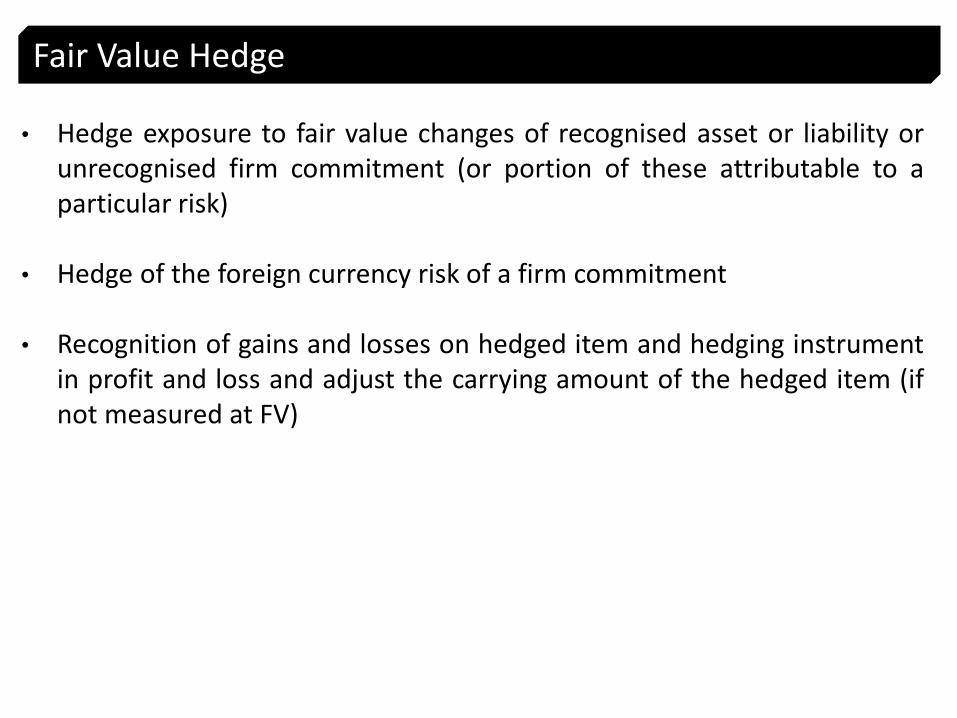

• Hedge exposure to fair value changes of recognised asset or liability orunrecognised firm commitment (or portion of these attributable to aparticular risk)

• Hedge of the foreign currency risk of a firm commitment

• Recognition of gains and losses on hedged item and hedging instrumentin profit and loss and adjust the carrying amount of the hedged item (ifnot measured at FV)

Fair Value Hedge

➢ Borrowing in FCY USD 10 Million

➢ Hedged with Currency Swap

Objective of Hedge is to Hedge Fair Value of Borrowings – Hence FVHedge

• FV of Borrowing and Swap in PL

• If Borrowing @ Amortised Cost, FV of Swap is in PL with similaradjustment to carrying value of Borrowing to eliminate accountingmis match

Fair Value Hedge Accounting - Example

Hedge of the exposure to variability in cash flows attributable to aparticular risk associated with

➢ a recognized asset or liability or➢ a highly probable forecast transaction

Hedge of the foreign currency risk of a firm commitment

Portion of hedge deemed to be effective:➢ gains and losses recognized in OCI

Portion of hedge deemed to be ineffective:➢ gains and losses recognized in profit or loss

Treatment of cumulative gains or losses differs based on what ‘type’of asset or liability is subsequently recognized

Cash Flow Hedge

▪ Entity intend to do Export after 2 months. Wants to hedge FCY riskon future cash flows

▪ Enters in to Forward contract

Objective is to hedge future cash flows

No existing asset on books, hence FV of forward is parked in OCI.When export happens, recycle FV gain/loss from OCI to PL

Cash Flow Hedge - Example

Hedge Accounting - Summary

QUIZ

CASE 1▪ A Ltd borrowed USD 10 million @ interest rate ‘LIBOR + 200bps’.

▪ Interest Rate Swap to convert floating cashflows to fixed cashflows

CASE 2▪ A Ltd borrowed USD 10 million @ interest rate 10%.

▪ Interest Rate Swap to convert fixed interest rate to floating interestrate linked to market.

CASE 3▪ A Ltd borrowed USD 10 million @ interest rate ‘LIBOR + 200bps’.

▪ Cross Currency Interest Rate Swap to hedge FCY and convertfloating cashflows to fixed cashflows

GAAP differences

AS Ind AS

Scope:

Only Investments under AS 13 Wider – All FI like investments, tradereceivables, loans & advances, borrowings..

Classification:

Current and Long term FI classified in 3 categories - Amortized Cost(AC), FVTOCI and FVTPL

Initial Recognition – at Cost Initial Recognition – at FV

Measurement:

• Current investment - lower of cost or FV

• Long term investment - cost less provisionfor diminution other than temporary.

• AC using EIR• FVTPL & FVTOCI at fair value with

changes routed through in PL or OCIrespectively

Measurement loss - charged to PL and gain isignored

Measurement gain or loss - charged as pertheir classification categories

No concept of fair value of FL FL – mainly at AC, if designated then FVTPL

Financial Instruments

AS Ind AS

• AS 11 – Covers forward exchangecontracts

• GN – Other derivative instruments(applicable from April 01, 2016)

• Ind AS 109 covers all derivativeinstruments

• Trade Forwards- marked to market onreporting date. Losses and Gains both tobe accounted in PL.

• Hedge - Premium to be amortized andcontract to be revalued on the reportingdate

• All derivatives should be fair valued.Losses and Gains both to be accounted inPL

• Hedge• Fair Value Hedge – PL• Cashflow Hedge – OCI

Impact

▪ Less guidance on derivatives (except Forwards) resulted in varied practices▪ Ind AS will lead to standard industry practices▪ Hedge (Cashflow Hedge & Fair Value Hedge) Documentations – For taking benefit of

hedged accounting, else transaction to be accounted as trading

Derivatives

Impact on Financials

Impact on Financials

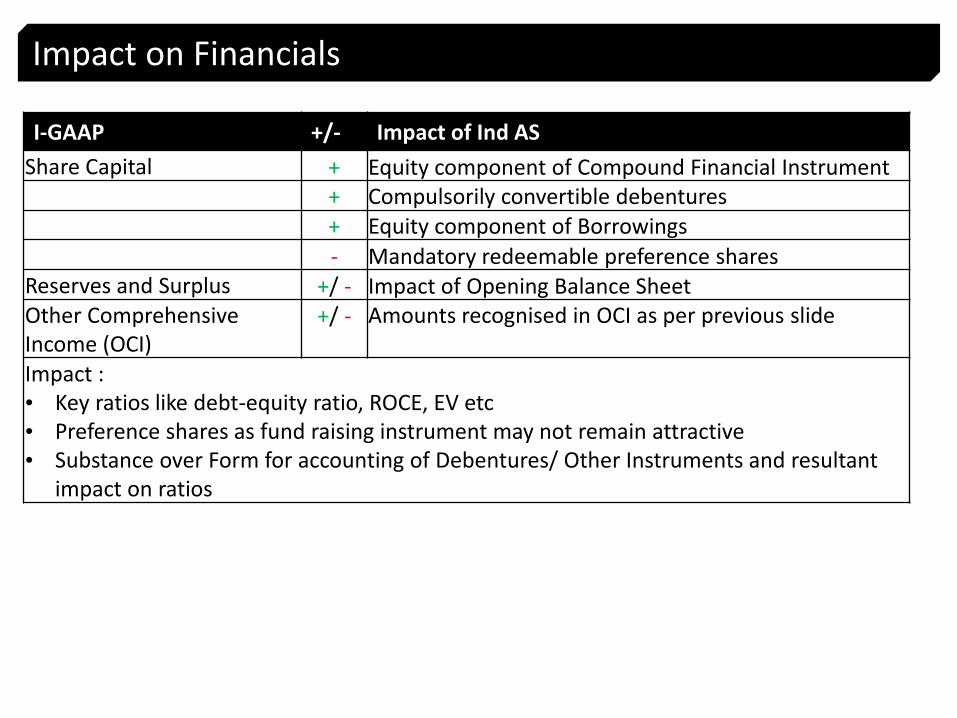

I-GAAP +/- Impact of Ind AS

Share Capital + Equity component of Compound Financial Instrument+ Compulsorily convertible debentures+ Equity component of Borrowings

- Mandatory redeemable preference sharesReserves and Surplus +/ - Impact of Opening Balance Sheet Other Comprehensive Income (OCI)

+/ - Amounts recognised in OCI as per previous slide

Impact :• Key ratios like debt-equity ratio, ROCE, EV etc• Preference shares as fund raising instrument may not remain attractive• Substance over Form for accounting of Debentures/ Other Instruments and resultant

impact on ratios

I-GAAP +/- Impact of Ind AS

Non Current Liabilities(i) Long-term borrowings +/ -

--

To be accounted at Amortized Cost. Interest to be accounted at Effective Interest RateEquity component of liability Puttable Equity

(ii) Long-term Liabilities - Initial Recognition at Fair Value (Discount to PV)Subsequently, to be recorded at Amortized Cost –May not have material impact

(iii) Long term provisions - Provisions to be recorded at present value

Current Liabilities(i) Short-term borrowings - Initial Recognition of FL at Fair Value.

Subsequent measurement at Amortized Cost, except for FL designated as FVTPLStatutory Dues are recorded at Carrying Value

(ii) Trade payables(iii) Other current liabilities

(iv) Short-term provisions No Material Impact

Impact on Financials

I-GAAP +/- Impact of Ind AS

Non Current Assets

Fixed Assets + Arrangement containing Finance Lease (IFRIC 4)

- Service Concession Agreement (IFRIC 12) De-recognition of Fixed Assets and Recognition of Financial Asset/ Intangible Asset

Impact on Financials

I-GAAP +/- Impact of Ind AS

Non Current Investments

Investment in Subsidiary/ JV/ Associate

+/ - Option:Cost under Ind AS 27FVTPLFVTOCI

Other Long Term Investments +/ - Classification, Recognition and Measurement as per Ind AS 109 i.e. @ Amortised Cost if satisfy conditions else @ Fair Value.

_ Transaction Cost to be charged to PL for FVTPL

Impact on Financials

I-GAAP +/- Impact of Ind AS

Long term loans and advances +/ - Financial Assets to be initially recognised at FV. Subsequent recognition at FV or Amortized Cost

Other non-current assets +/ -

Deferred tax assets (net) Impact as per previous slide on deferred tax

Impact on Financials

I-GAAP +/- Impact of Ind AS

Current Assets(a) Inventories + WIP for Service Companies(b) Current investments

(c) Trade receivables

(d) Cash and cash equivalents

(e) Short-term loans and advances

+/ -+/ -

+/ -

+/ -

All derivative transactions at FVAmortised cost or FV

Generally no impact. FV impact if different credit period. Impairment @ ECL

No Impact

No Material Impact

(f) Other current assets +/ - No Material Impact

Impact on Financials

Applicable to all most all Companies

What applies to most companies are – Logical and Not Complex

Complex Transactions – Complex Accounting Primarily for Financial Services and Banks

Most treatments in IndAS109 – Apply logic and reflect substance of transaction

Conclude…..

Thank You