inclusive growth: coalitions needed

DESCRIPTION

Presented by Roger van den Brink, World Bank Group Philippines lead economist and program manager, at the Kusog Mindanaw "Eminent Mindanawon Leaders Meeting", Marco Polo Davao, 5 October 2015TRANSCRIPT

Inclusive Growth:

Coalitions Needed

Rogier van den Brink Lead Economist and Program Leader

World Bank Group, Philippines

Eminent Mindanawon Leaders Meeting

October 5, 2015

Marco Polo Hotel, Davao

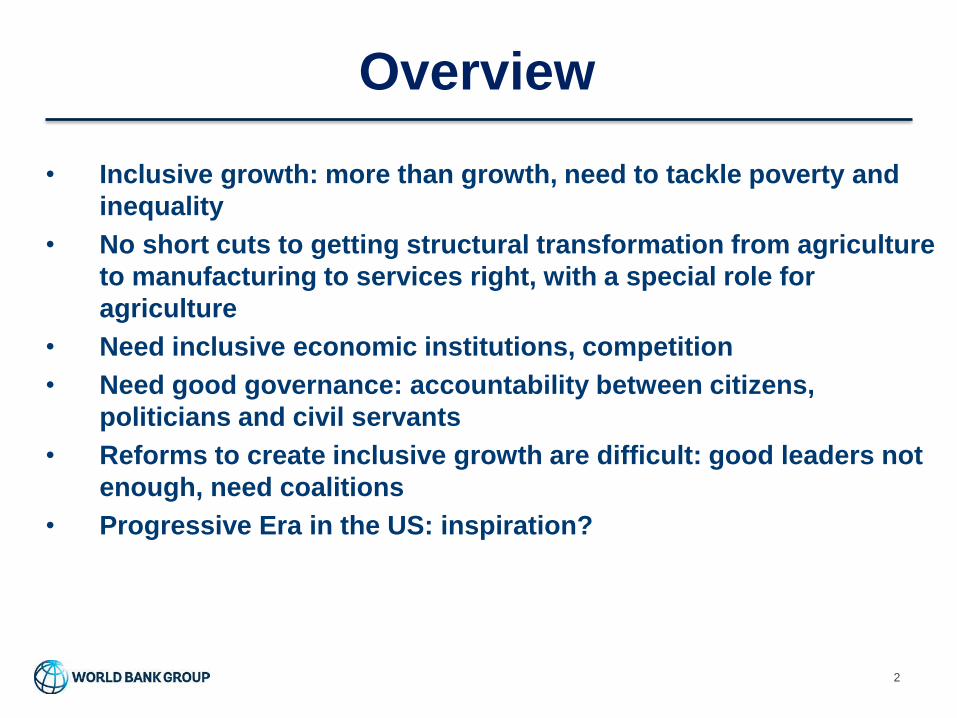

Overview

• Inclusive growth: more than growth, need to tackle poverty and

inequality

• No short cuts to getting structural transformation from agriculture

to manufacturing to services right, with a special role for

agriculture

• Need inclusive economic institutions, competition

• Need good governance: accountability between citizens,

politicians and civil servants

• Reforms to create inclusive growth are difficult: good leaders not

enough, need coalitions

• Progressive Era in the US: inspiration?

2

Inclusive growth: What is it? It is more than growth, but it

does start with growth, and growth

needs macroeconomic stability

Inclusive growth challenge: More than growth

Growth may be necessary but is not sufficient to ensure poverty reduction…

How broadly based growth is—i.e., how pro-poor the distribution of

growth is—also matters…

Raising the returns to labor—the main asset

of the poor—and securing the other

assets (land, savings)

…increasing value-added per worker

in agriculture

…while people move out of agriculture to higher value-added

activities in manufacturing and

services

…as does how resilient growth is and the extent to which poor and

vulnerable households are protected from shocks

Putting in place appropriate

social protection schemes

…and raising human capital

endowments

4

5

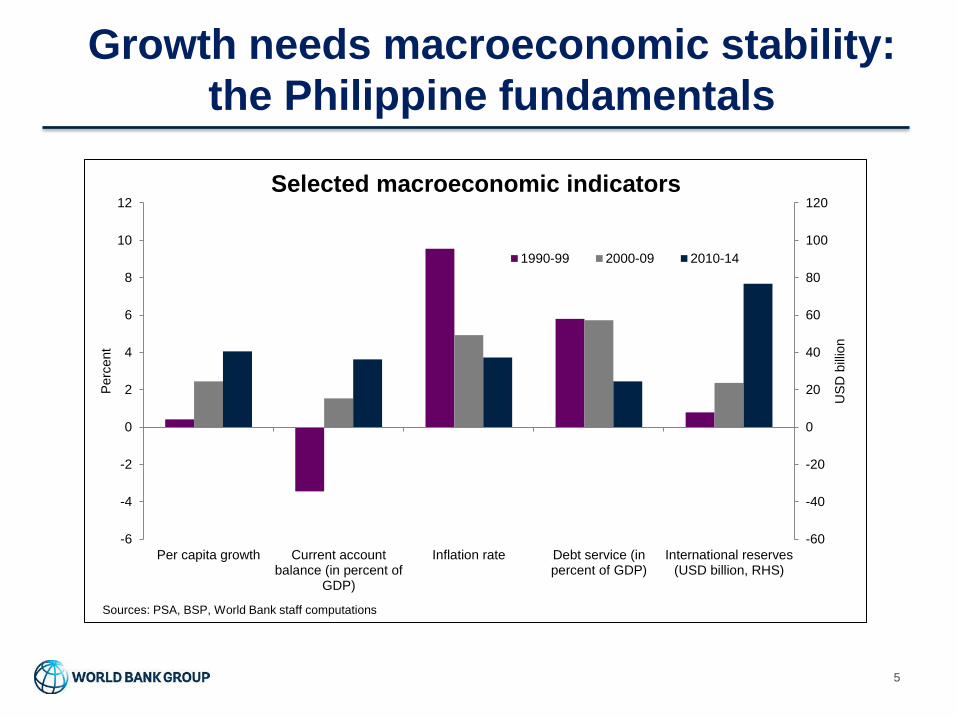

Growth needs macroeconomic stability:

the Philippine fundamentals

-60

-40

-20

0

20

40

60

80

100

120

-6

-4

-2

0

2

4

6

8

10

12

Per capita growth Current accountbalance (in percent of

GDP)

Inflation rate Debt service (inpercent of GDP)

International reserves(USD billion, RHS)

US

D b

illio

n

Perc

ent

Selected macroeconomic indicators

1990-99 2000-09 2010-14

Sources: PSA, BSP, World Bank staff computations

Inclusive Growth: inequality is the new growth agenda

Because growth is slow…

7

-4

-2

0

2

4

6

8

10

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

World High-income countries Developing countries(Percent)

GDP growth

Source: Global Economic Prospects, World Bank, June 2015

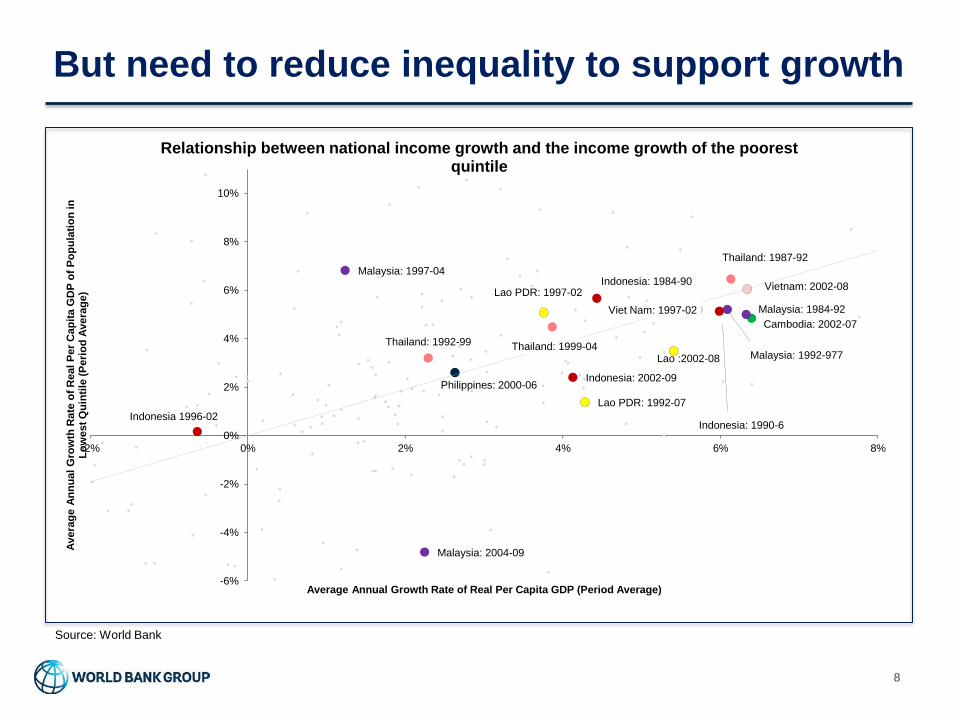

But need to reduce inequality to support growth

8

Philippines: 2000-06

Cambodia: 2002-07

Indonesia: 1984-90

Indonesia: 1990-6 Indonesia 1996-02

Indonesia: 2002-09

Lao PDR: 1992-07

Lao PDR: 1997-02

Lao :2002-08 Malaysia: 1992-977

Malaysia: 1984-92

Malaysia: 2004-09

Malaysia: 1997-04

Thailand: 1987-92

Thailand: 1992-99 Thailand: 1999-04

Viet Nam: 1997-02

Vietnam: 2002-08

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

-2% 0% 2% 4% 6% 8%

Avera

ge

An

nu

al

Gro

wth

Rate

of

Real

Per

Cap

ita G

DP

of

Po

pu

lati

on

in

L

ow

est

Qu

inti

le (

Peri

od

Avera

ge

)

Average Annual Growth Rate of Real Per Capita GDP (Period Average)

Relationship between national income growth and the income growth of the poorest quintile

Source: World Bank

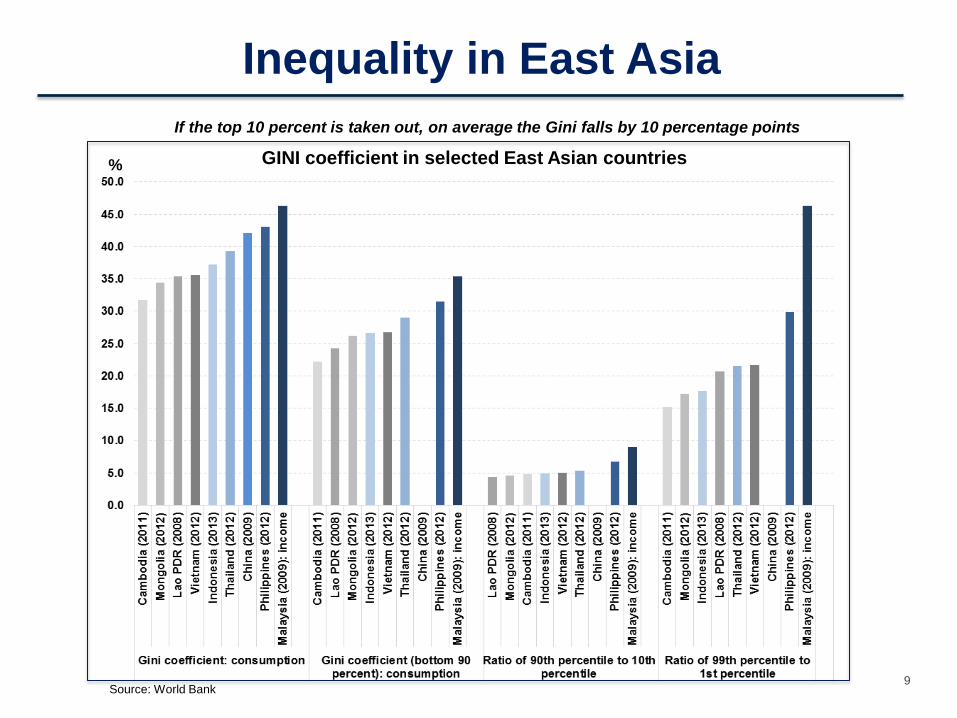

Inequality in East Asia

9

GINI coefficient in selected East Asian countries %

If the top 10 percent is taken out, on average the Gini falls by 10 percentage points

Source: World Bank

Inclusive Growth: the special role of agriculture

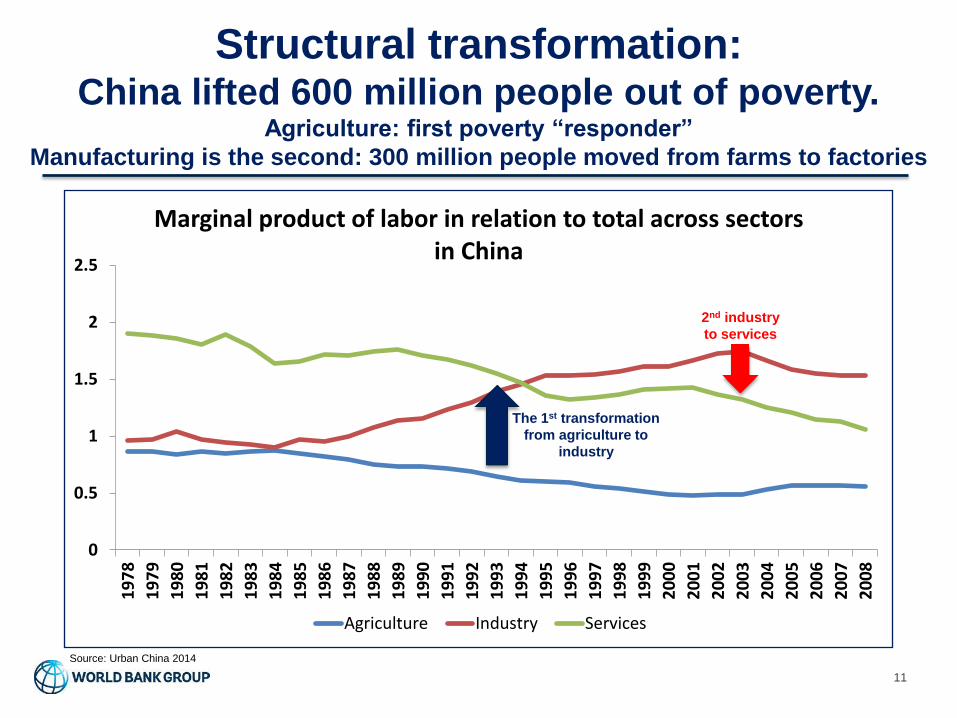

Structural transformation: China lifted 600 million people out of poverty.

Agriculture: first poverty “responder”

Manufacturing is the second: 300 million people moved from farms to factories

Source: Urban China 2014

0

0.5

1

1.5

2

2.5

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

Marginal product of labor in relation to total across sectors in China

Agriculture Industry Services

2nd industry

to services

The 1st transformation

from agriculture to

industry

11

The normal pattern of

economic transformation Before economic transformation takes off, agriculture:

– large shares in economic output and the labor force

– but the share in economic output less than its share in the labor force,

– lower productivity of labor than in industry and services.

Industrial growth takes off:

– industry, and in particular manufacturing, increases its share in the

economy

– pulls labor out of agriculture more or less rapidly.

In advanced economies, this transformation will reduce the

shares of agriculture in GDP and in the labor force to very

small numbers

This transformation is now taking longer and longer,

because manufacturing has become less labor-intensive Sources: Kuznets and Chenery, and Timmer, 2009

During the normal pattern, there is a

special role for agriculture:

poverty reduction

Global decline in the incidence of poverty (US$1/day):

– 28 percent in 1993 to 23 percent in 2002

Caused entirely by rural poverty reduction, while urban poverty has increased

More than 80 percent of the decline in rural poverty was due to improved conditions in rural areas

Migration was not the main instrument for rural, national and global poverty reduction

Improved rural conditions were, with agriculture as the main source of growth

Source: World Development Report on Agriculture 2008

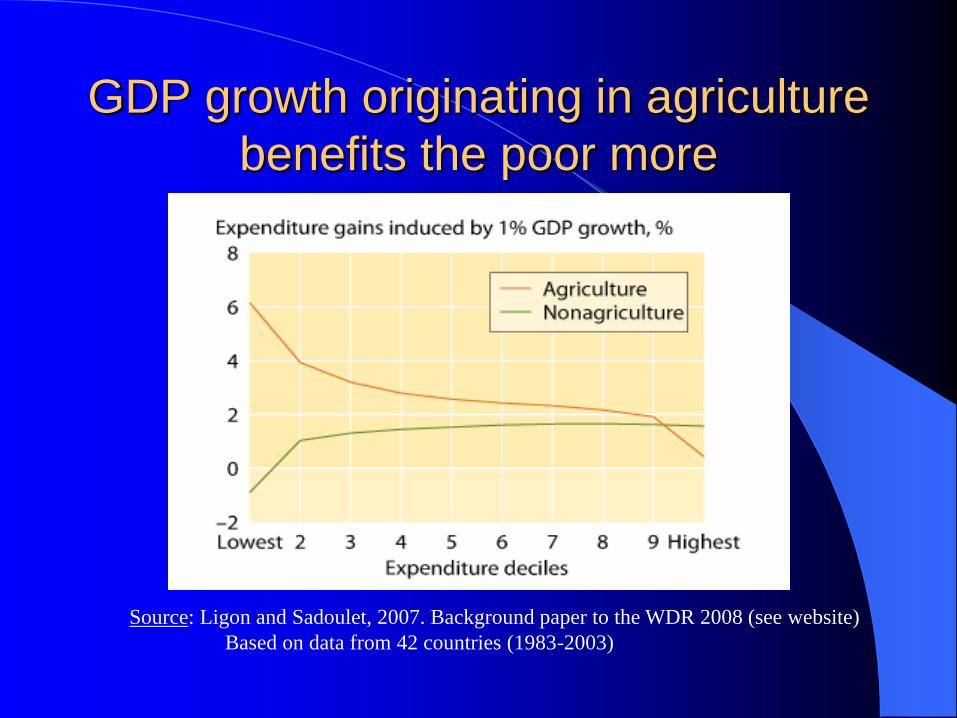

GDP growth originating in agriculture

benefits the poor more

Source: Ligon and Sadoulet, 2007. Background paper to the WDR 2008 (see website)

Based on data from 42 countries (1983-2003)

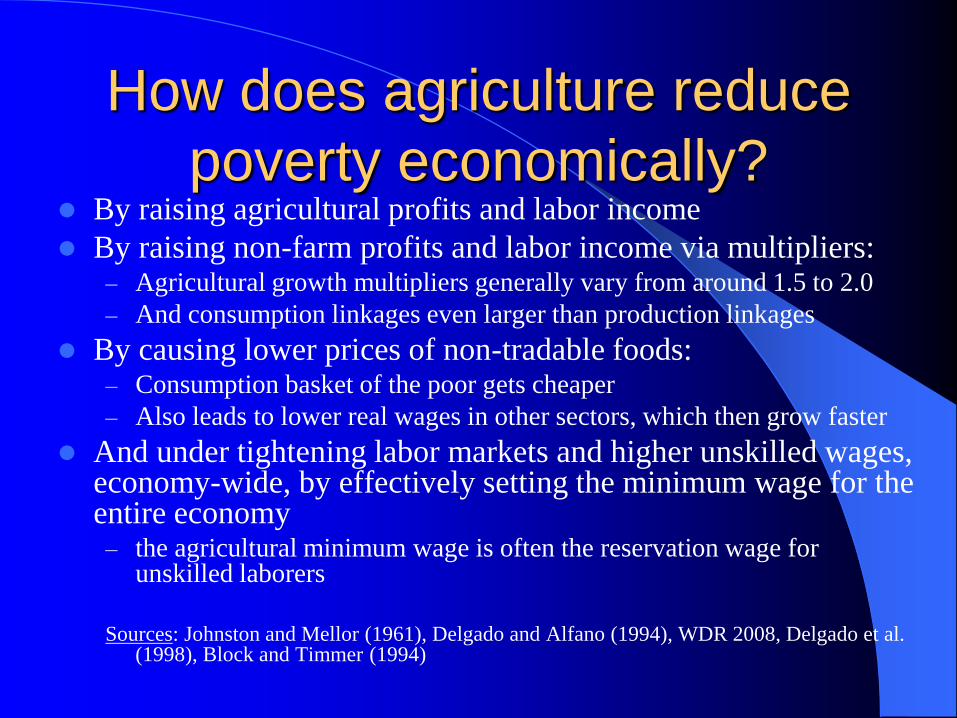

How does agriculture reduce

poverty economically? By raising agricultural profits and labor income

By raising non-farm profits and labor income via multipliers: – Agricultural growth multipliers generally vary from around 1.5 to 2.0

– And consumption linkages even larger than production linkages

By causing lower prices of non-tradable foods: – Consumption basket of the poor gets cheaper

– Also leads to lower real wages in other sectors, which then grow faster

And under tightening labor markets and higher unskilled wages, economy-wide, by effectively setting the minimum wage for the entire economy

– the agricultural minimum wage is often the reservation wage for unskilled laborers

Sources: Johnston and Mellor (1961), Delgado and Alfano (1994), WDR 2008, Delgado et al.

(1998), Block and Timmer (1994)

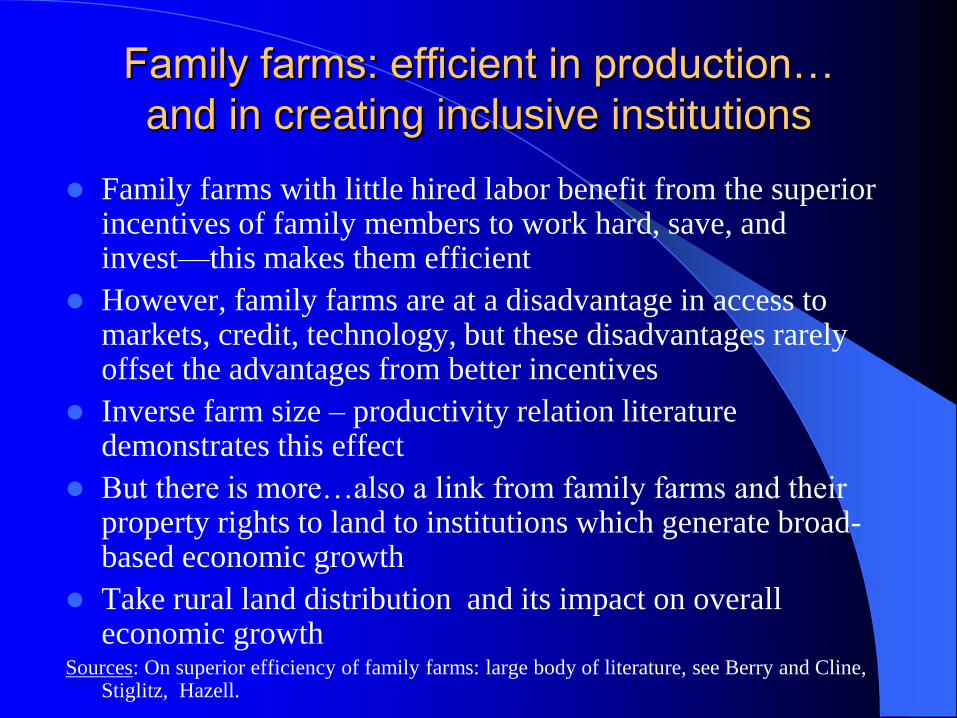

Family farms: efficient in production…

and in creating inclusive institutions

Family farms with little hired labor benefit from the superior incentives of family members to work hard, save, and invest—this makes them efficient

However, family farms are at a disadvantage in access to markets, credit, technology, but these disadvantages rarely offset the advantages from better incentives

Inverse farm size – productivity relation literature demonstrates this effect

But there is more…also a link from family farms and their property rights to land to institutions which generate broad-based economic growth

Take rural land distribution and its impact on overall economic growth

Sources: On superior efficiency of family farms: large body of literature, see Berry and Cline, Stiglitz, Hazell.

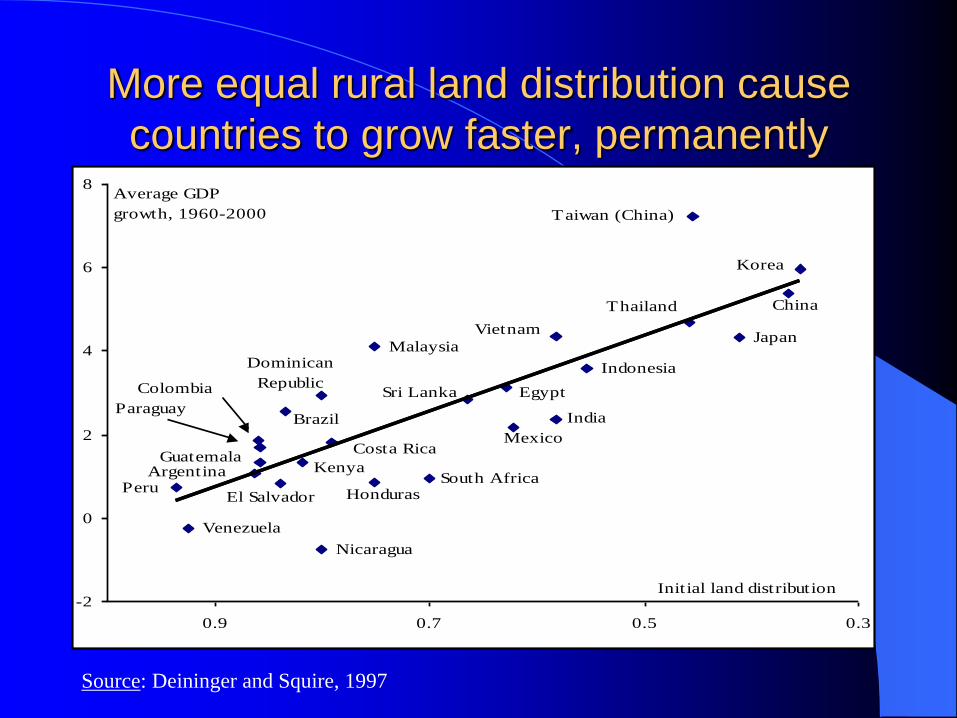

More equal rural land distribution cause

countries to grow faster, permanently

Guatemala

El Salvador

Argentina

Honduras

Dominican

RepublicSri Lanka

Vietnam

Colombia

Costa Rica

Paraguay

Kenya

Brazil

Thailand

Japan

Taiwan (China)

China

Korea

Malaysia

Indonesia

Egypt

India

Mexico

South AfricaPeru

Venezuela

Nicaragua

-2

0

2

4

6

8

0.30.50.70.9

Initial land distribution

Average GDP

growth, 1960-2000

Source: Deininger and Squire, 1997

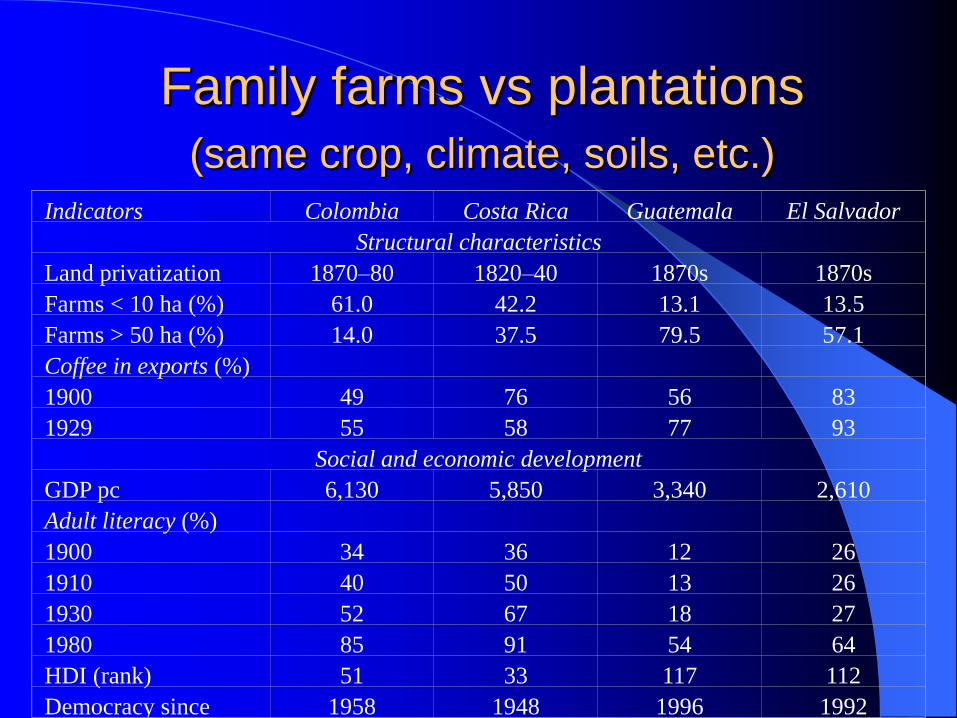

Family farms vs plantations

(same crop, climate, soils, etc.)

Indicators

Colombia

Costa Rica

Guatemala

El Salvador

Structural characteristics

Land privatization

1870–80

1820–40

1870s

1870s

Farms < 10 ha (%)

61.0

42.2

13.1

13.5

Farms > 50 ha (%)

14.0

37.5

79.5

57.1

Coffee in exports (%)

1900

49

76

56

83

1929

55

58

77

93

Social and economic development

GDP pc

6,130

5,850

3,340

2,610

Adult literacy (%)

1900

34

36

12

26

1910

40

50

13

26

1930

52

67

18

27

1980

85

91

54

64

HDI (rank)

51

33

117

112

Democracy since

1958

1948

1996

1992

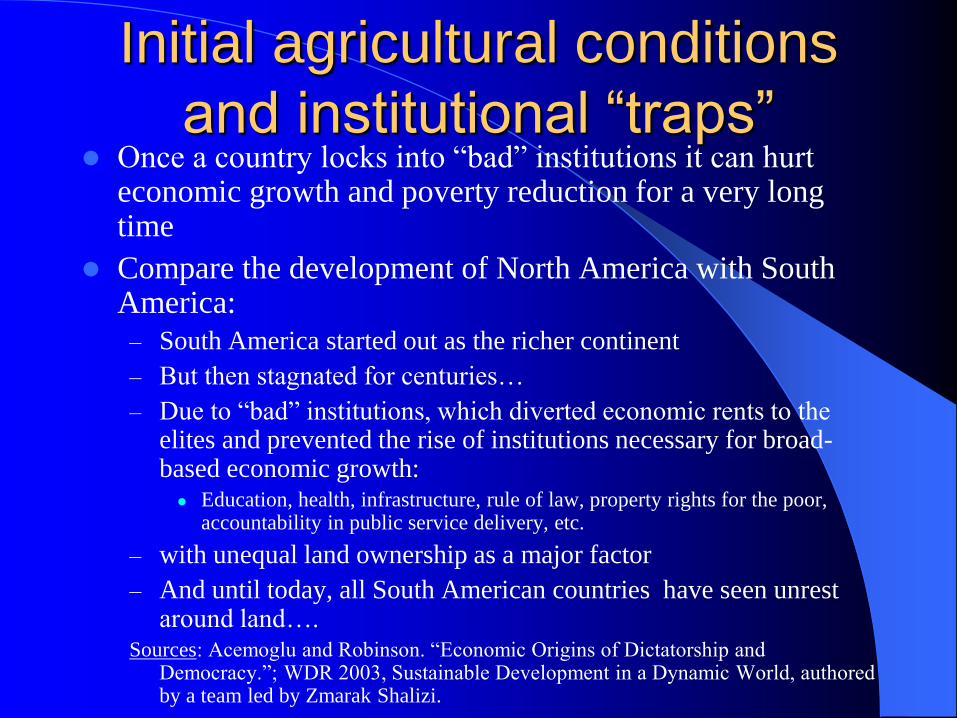

Initial agricultural conditions

and institutional “traps” Once a country locks into “bad” institutions it can hurt

economic growth and poverty reduction for a very long time

Compare the development of North America with South America:

– South America started out as the richer continent

– But then stagnated for centuries…

– Due to “bad” institutions, which diverted economic rents to the elites and prevented the rise of institutions necessary for broad-based economic growth:

Education, health, infrastructure, rule of law, property rights for the poor, accountability in public service delivery, etc.

– with unequal land ownership as a major factor

– And until today, all South American countries have seen unrest around land….

Sources: Acemoglu and Robinson. “Economic Origins of Dictatorship and Democracy.”; WDR 2003, Sustainable Development in a Dynamic World, authored by a team led by Zmarak Shalizi.

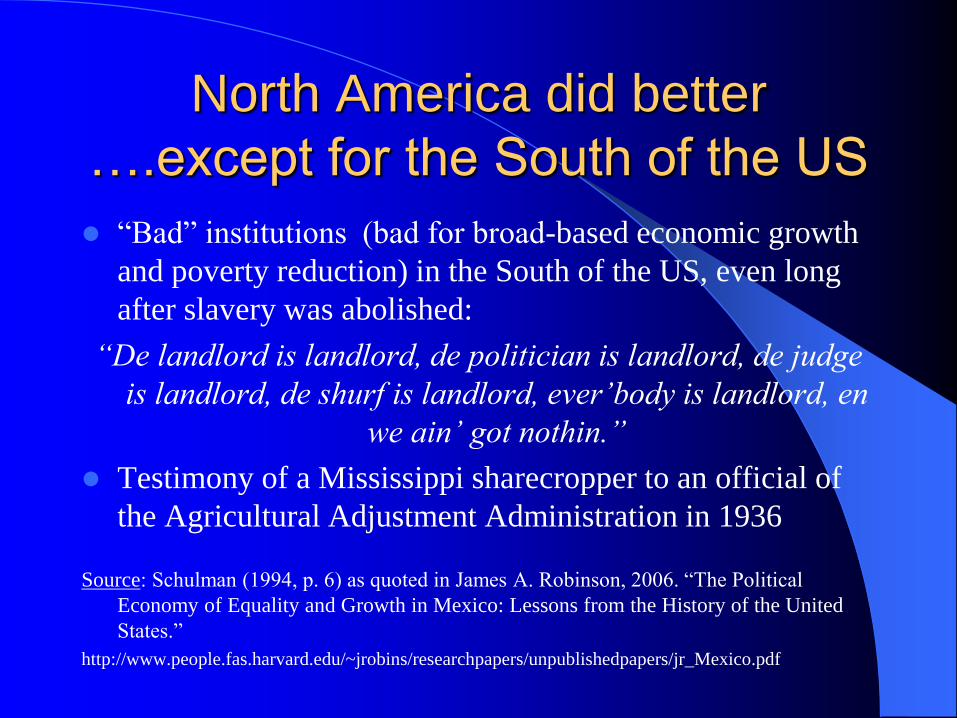

North America did better

….except for the South of the US

“Bad” institutions (bad for broad-based economic growth

and poverty reduction) in the South of the US, even long

after slavery was abolished:

“De landlord is landlord, de politician is landlord, de judge

is landlord, de shurf is landlord, ever’body is landlord, en

we ain’ got nothin.”

Testimony of a Mississippi sharecropper to an official of

the Agricultural Adjustment Administration in 1936

Source: Schulman (1994, p. 6) as quoted in James A. Robinson, 2006. “The Political

Economy of Equality and Growth in Mexico: Lessons from the History of the United

States.”

http://www.people.fas.harvard.edu/~jrobins/researchpapers/unpublishedpapers/jr_Mexico.pdf

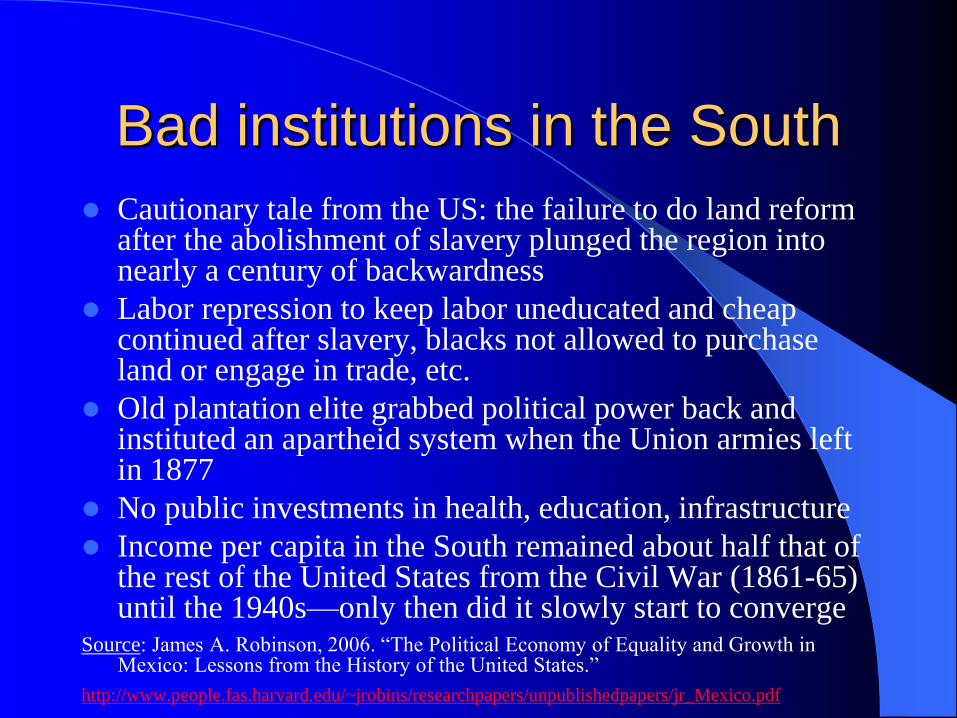

Bad institutions in the South

Cautionary tale from the US: the failure to do land reform after the abolishment of slavery plunged the region into nearly a century of backwardness

Labor repression to keep labor uneducated and cheap continued after slavery, blacks not allowed to purchase land or engage in trade, etc.

Old plantation elite grabbed political power back and instituted an apartheid system when the Union armies left in 1877

No public investments in health, education, infrastructure

Income per capita in the South remained about half that of the rest of the United States from the Civil War (1861-65) until the 1940s—only then did it slowly start to converge

Source: James A. Robinson, 2006. “The Political Economy of Equality and Growth in Mexico: Lessons from the History of the United States.”

http://www.people.fas.harvard.edu/~jrobins/researchpapers/unpublishedpapers/jr_Mexico.pdf

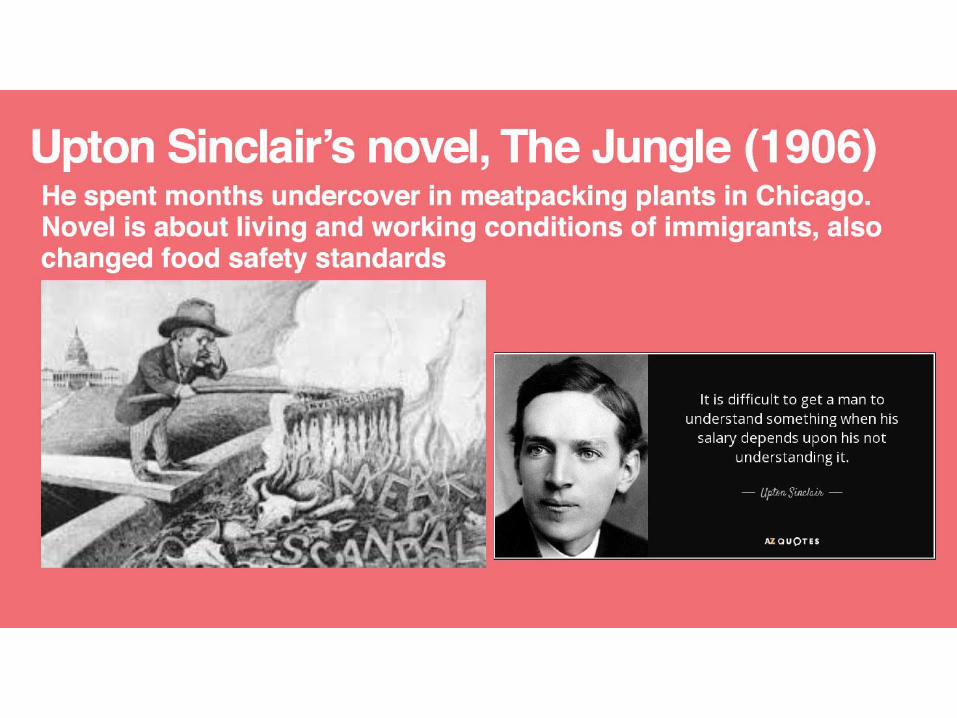

Better institutions in the North Whereas in the North, family farmers not only produced a

much more dynamic agricultural sector..

…but they also often successfully lobbied for economic

reforms:

– Farmers were the key reformers attacking the monopolies of the

Robber Barons

– Interstate Commerce Act, federal regulation of industry, Sherman

Ant-Trust Act, regulation of railroads

Helped by a vocal free press (the “muckrakers”)

Halted earlier concentration trend in industry, reduced

inequality, sustained economic growth Source: James A. Robinson, 2006. “The Political Economy of Equality and Growth in

Mexico: Lessons from the History of the United States.”

http://www.people.fas.harvard.edu/~jrobins/researchpapers/unpublishedpapers/jr_Mexico.pdf

So land reform became

cornerstone of US foreign

policy after WWII Following World War II, peaceful country-wide land

reforms were implemented in Japan, Korea and Taiwan, under strong external pressure from the United States.

US foreign policy position at the time: Dr. Lubin, its Ambassador to the United Nations, introduced a resolution which would make land reform a global economic program of the United Nations:

“A nation of insecure tenants and rootless laborers, who see little hope to better their lot, is an unstable society, subject to sporadic violence and easily persuaded to

follow false leaders.” Source: W.L. Lissner. American Journal of Economics and Sociology, Vol. 11, No. 1 (Oct.,

1951), pp. 53-54

Inclusive Growth: inclusive economic institutions,

competition

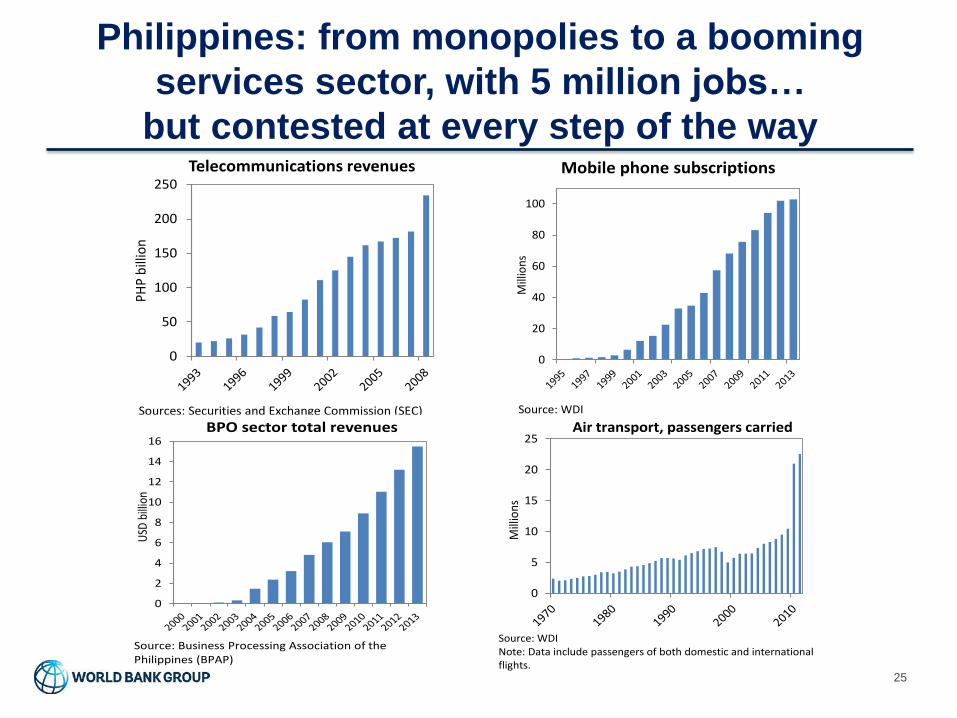

Philippines: from monopolies to a booming

services sector, with 5 million jobs…

but contested at every step of the way

0

50

100

150

200

250

PHP

bill

ion

Telecommunications revenues

Sources: Securities and Exchange Commission (SEC)

0

2

4

6

8

10

12

14

16

USD

bill

ion

BPO sector total revenues

Source: Business Processing Association of the Philippines (BPAP)

0

5

10

15

20

25

Mill

ions

Air transport, passengers carried

Source: WDINote: Data include passengers of both domestic and international flights.

0

20

40

60

80

100

Mill

ions

Mobile phone subscriptions

Source: WDI

ndicators

25

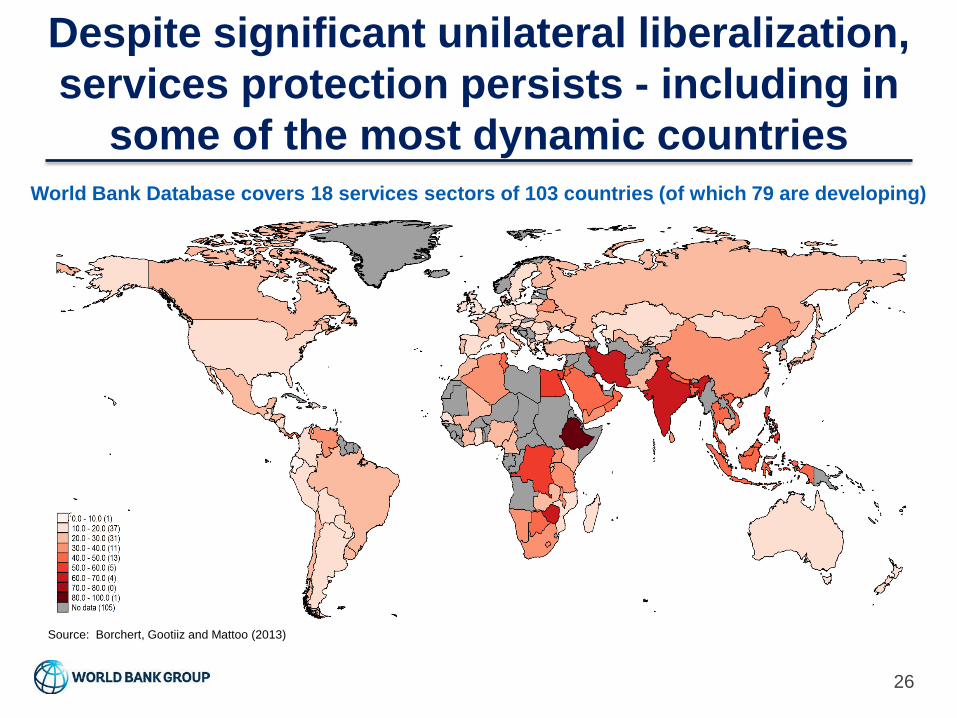

Despite significant unilateral liberalization,

services protection persists - including in

some of the most dynamic countries

26

World Bank Database covers 18 services sectors of 103 countries (of which 79 are developing)

Source: Borchert, Gootiiz and Mattoo (2013)

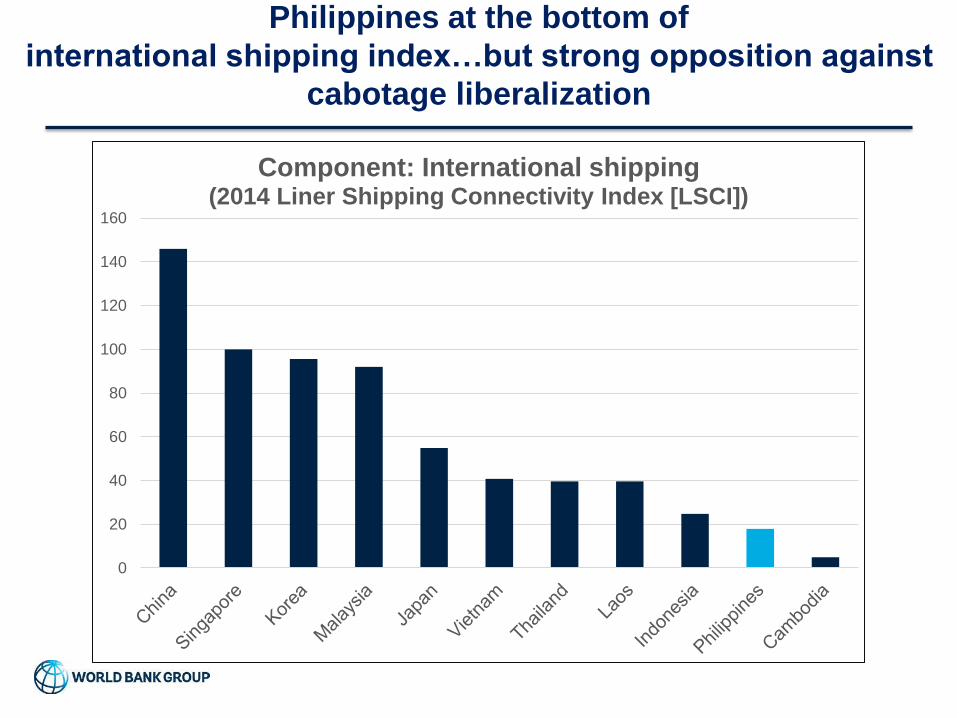

Philippines at the bottom of

international shipping index…but strong opposition against

cabotage liberalization

0

20

40

60

80

100

120

140

160

Component: International shipping (2014 Liner Shipping Connectivity Index [LSCI])

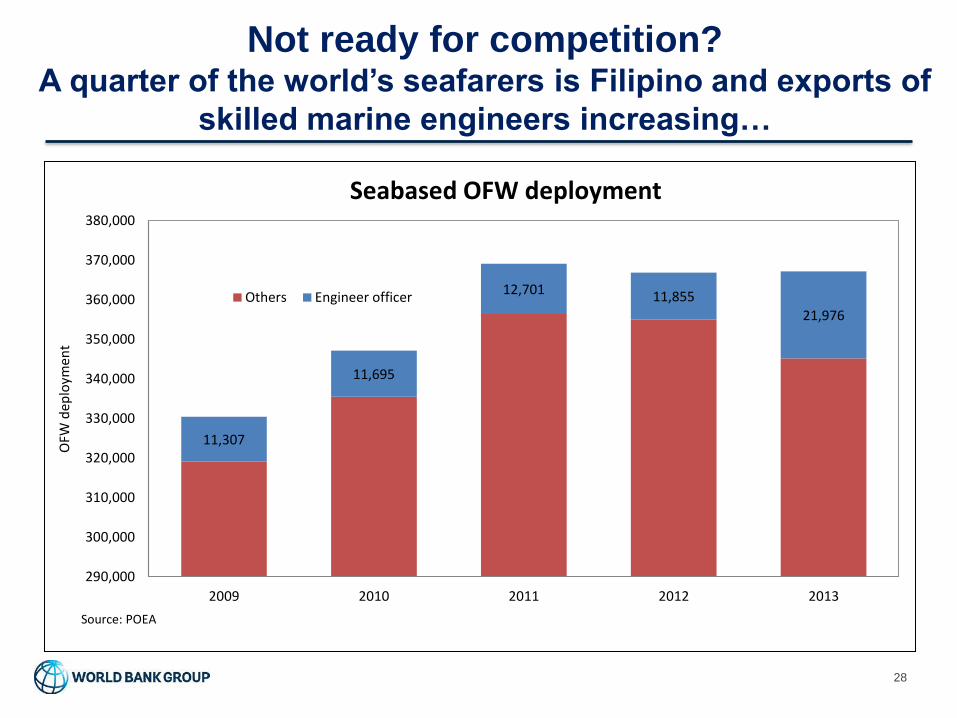

Not ready for competition? A quarter of the world’s seafarers is Filipino and exports of

skilled marine engineers increasing…

28

11,307

11,695

12,701 11,855

21,976

290,000

300,000

310,000

320,000

330,000

340,000

350,000

360,000

370,000

380,000

2009 2010 2011 2012 2013

OFW

dep

loym

ent

Seabased OFW deployment

Others Engineer officer

Source: POEA

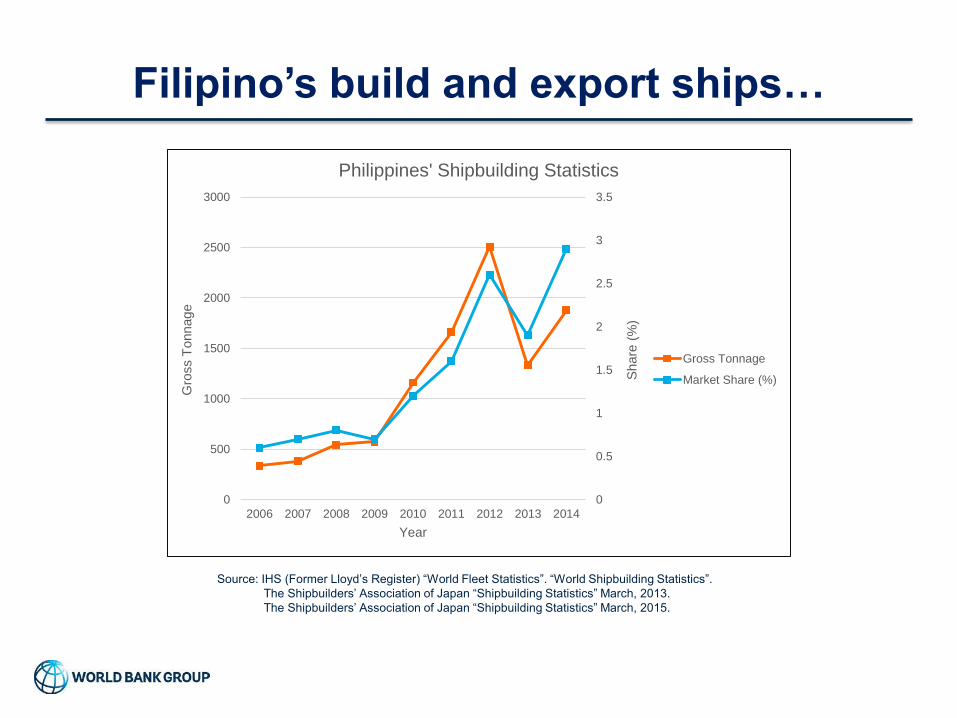

Filipino’s build and export ships…

0

0.5

1

1.5

2

2.5

3

3.5

0

500

1000

1500

2000

2500

3000

2006 2007 2008 2009 2010 2011 2012 2013 2014

Share

(%

)

Gro

ss T

onnage

Year

Philippines' Shipbuilding Statistics

Gross Tonnage

Market Share (%)

Source: IHS (Former Lloyd’s Register) “World Fleet Statistics”. “World Shipbuilding Statistics”.

The Shipbuilders’ Association of Japan “Shipbuilding Statistics” March, 2013.

The Shipbuilders’ Association of Japan “Shipbuilding Statistics” March, 2015.

30

The Foreign Ships Co-loading Act

• In July 21, 2015, the President signed RA 10668

into law.

• This is also known as the ‘The Foreign Ships Co-

loading Act’

• Move in the right direction: foreign ships can now

load and unload imports and exports along

domestic routes

• It will help reduce costs for importers and

exporters and it will also aid in decongesting ports

within the country

• But reform is incomplete…domestic shipping is

still protected…”not ready for competition”

31

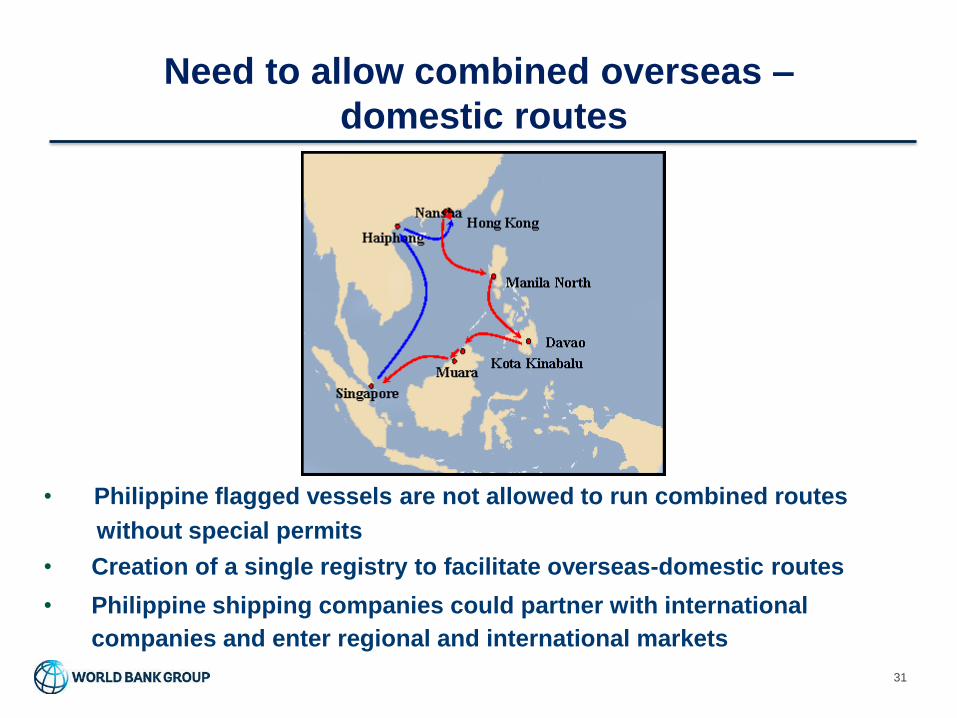

Need to allow combined overseas –

domestic routes

• Philippine flagged vessels are not allowed to run combined routes

without special permits

• Creation of a single registry to facilitate overseas-domestic routes

• Philippine shipping companies could partner with international

companies and enter regional and international markets

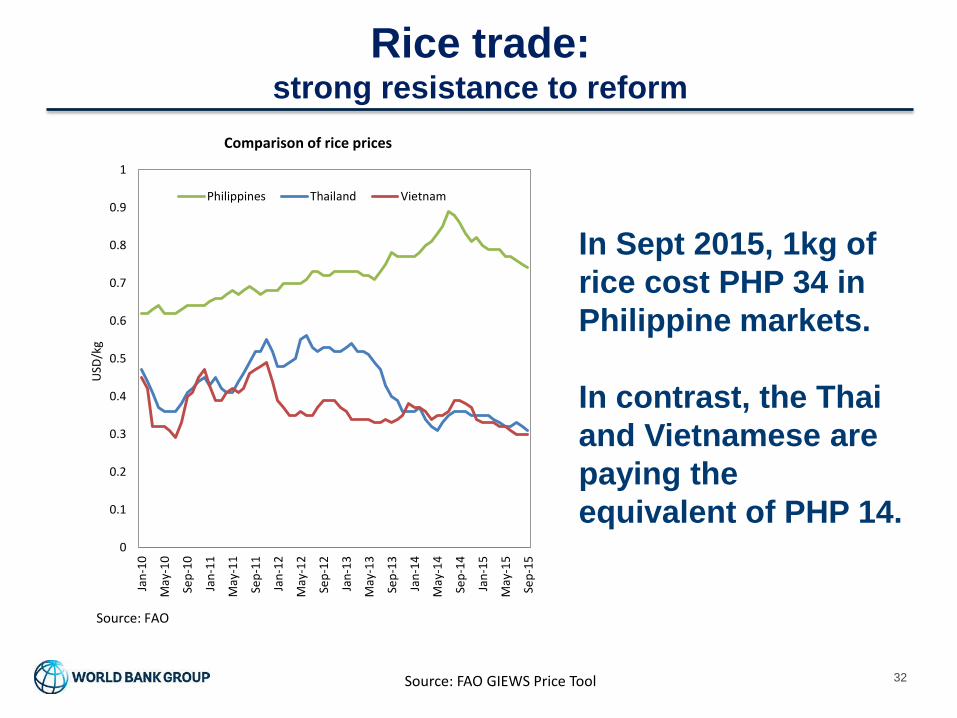

Rice trade: strong resistance to reform

Source: FAO GIEWS Price Tool 32

In Sept 2015, 1kg of

rice cost PHP 34 in

Philippine markets.

In contrast, the Thai

and Vietnamese are

paying the

equivalent of PHP 14. 0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

USD

/kg

Comparison of rice prices

Philippines Thailand Vietnam

Source: FAO

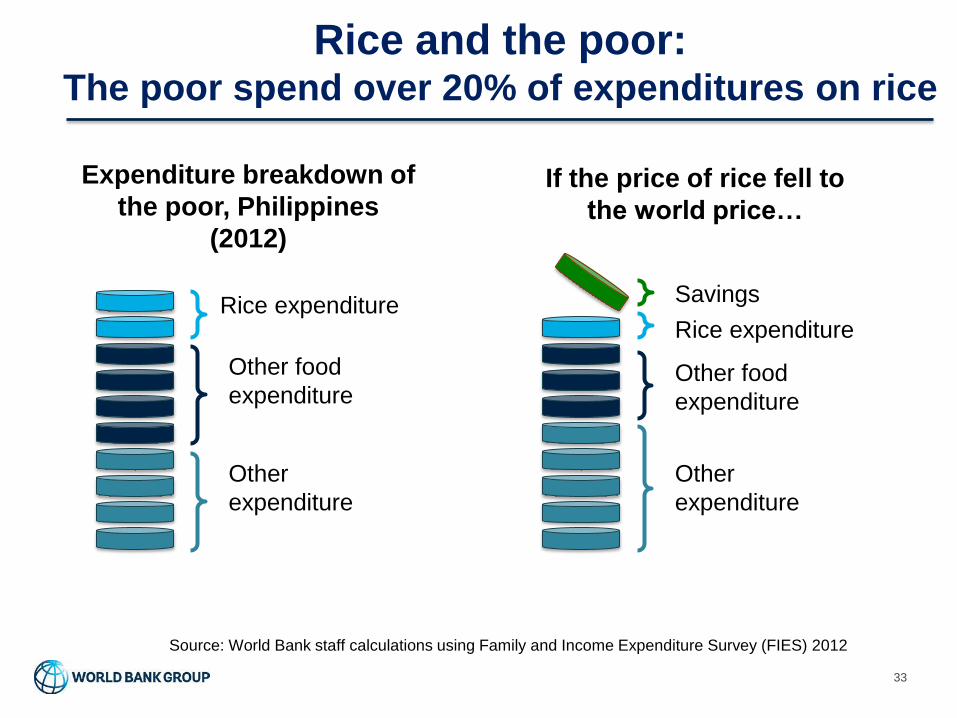

Rice and the poor: The poor spend over 20% of expenditures on rice

33

Other

expenditure

Other food

expenditure

Rice expenditure

Expenditure breakdown of

the poor, Philippines

(2012)

If the price of rice fell to

the world price…

Other

expenditure

Other food

expenditure

Savings

Source: World Bank staff calculations using Family and Income Expenditure Survey (FIES) 2012

Rice expenditure

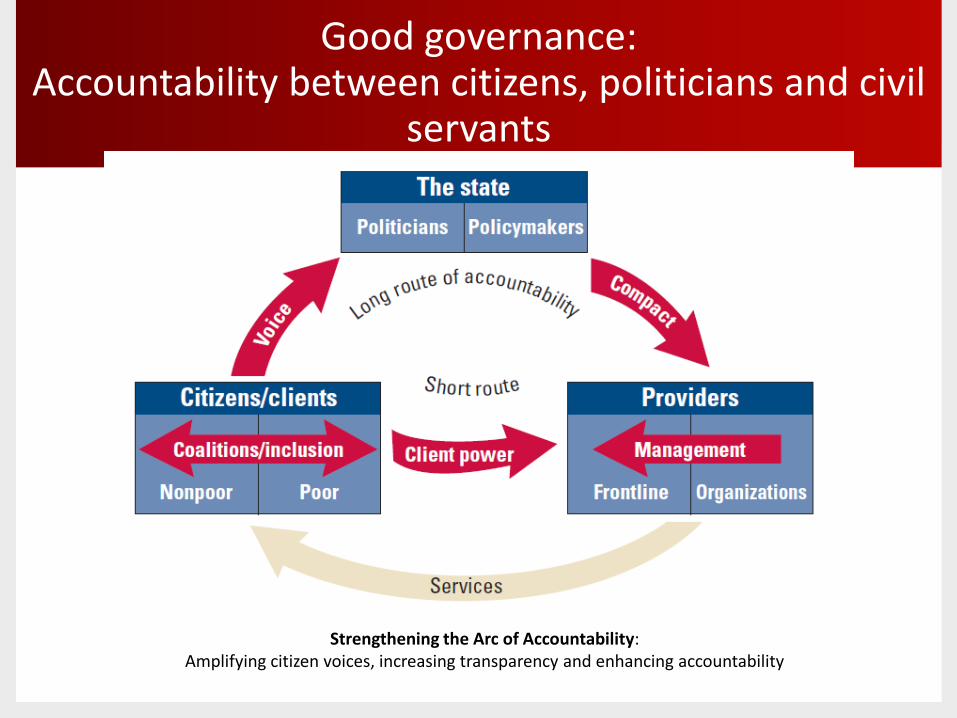

Inclusive Growth: good governance

Good governance: Accountability between citizens, politicians and civil

servants

Strengthening the Arc of Accountability: Amplifying citizen voices, increasing transparency and enhancing accountability

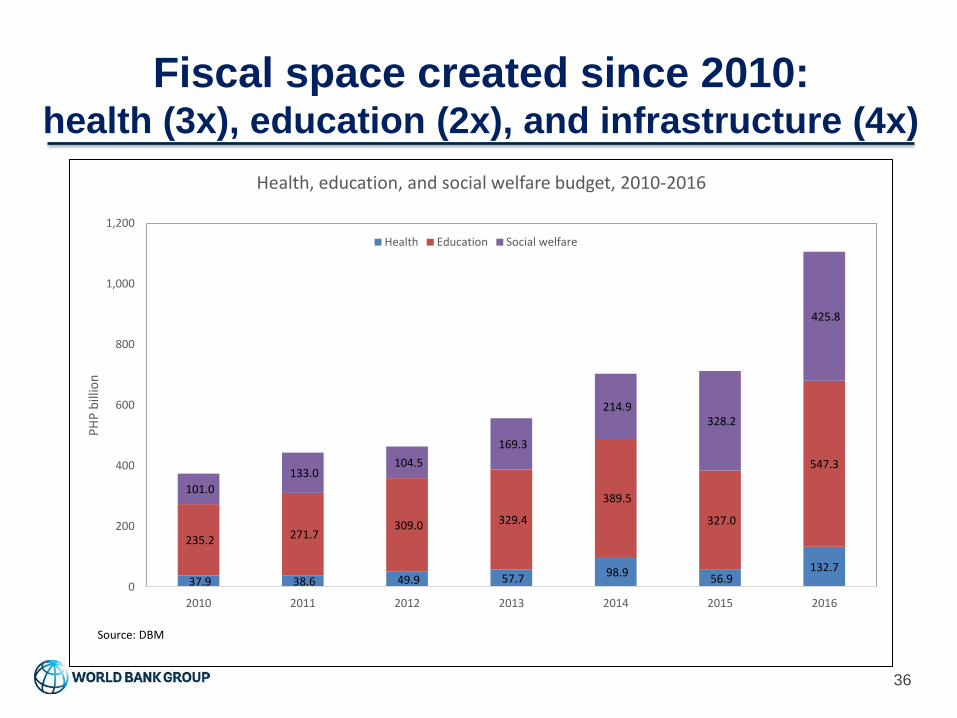

Fiscal space created since 2010: health (3x), education (2x), and infrastructure (4x)

36

37.9 38.6 49.9 57.7 98.9 56.9

132.7

235.2 271.7 309.0 329.4

389.5

327.0

547.3

101.0

133.0 104.5

169.3

214.9 328.2

425.8

0

200

400

600

800

1,000

1,200

2010 2011 2012 2013 2014 2015 2016

PH

P b

illio

n

Health, education, and social welfare budget, 2010-2016

Health Education Social welfare

Source: DBM

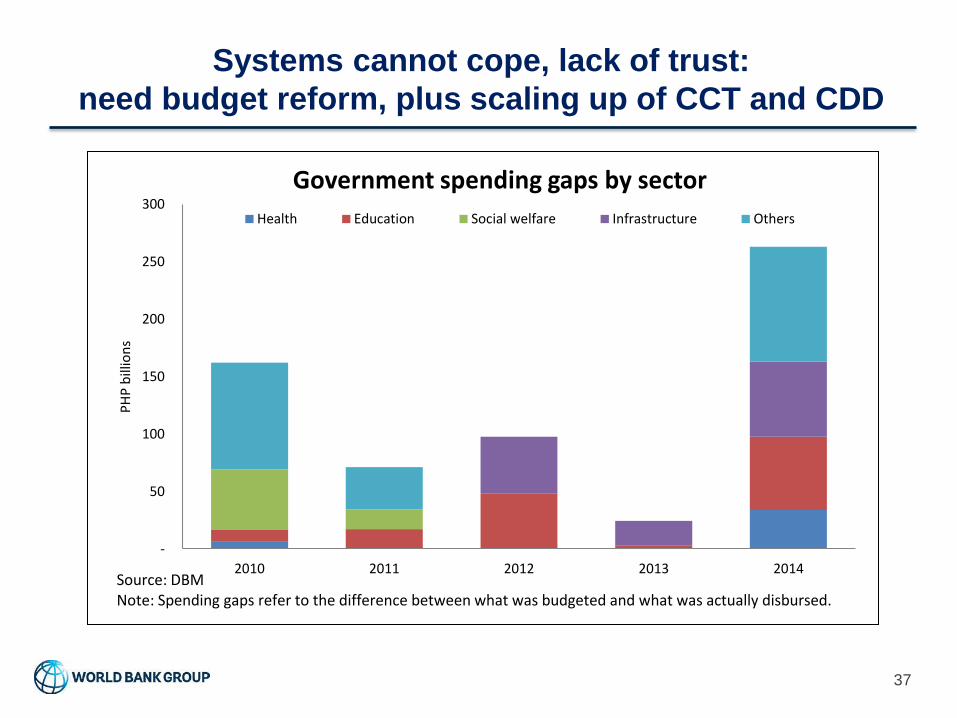

Systems cannot cope, lack of trust:

need budget reform, plus scaling up of CCT and CDD

37

-

50

100

150

200

250

300

2010 2011 2012 2013 2014

PH

P b

illio

ns

Government spending gaps by sector

Health Education Social welfare Infrastructure Others

Source: DBMNote: Spending gaps refer to the difference between what was budgeted and what was actually disbursed.

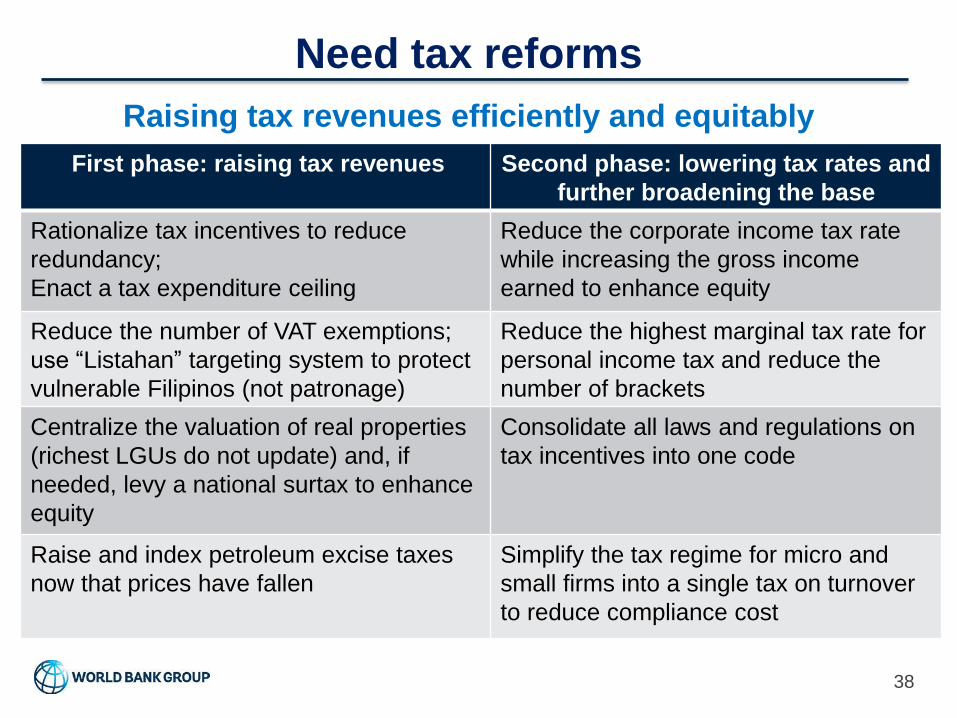

Need tax reforms

38

Raising tax revenues efficiently and equitably

First phase: raising tax revenues

Rationalize tax incentives to reduce

redundancy;

Enact a tax expenditure ceiling

Reduce the number of VAT exemptions;

use “Listahan” targeting system to protect

vulnerable Filipinos (not patronage)

Centralize the valuation of real properties

(richest LGUs do not update) and, if

needed, levy a national surtax to enhance

equity

Raise and index petroleum excise taxes

now that prices have fallen

Second phase: lowering tax rates and

further broadening the base

Reduce the corporate income tax rate

while increasing the gross income

earned to enhance equity

Reduce the highest marginal tax rate for

personal income tax and reduce the

number of brackets

Consolidate all laws and regulations on

tax incentives into one code

Simplify the tax regime for micro and

small firms into a single tax on turnover

to reduce compliance cost

39

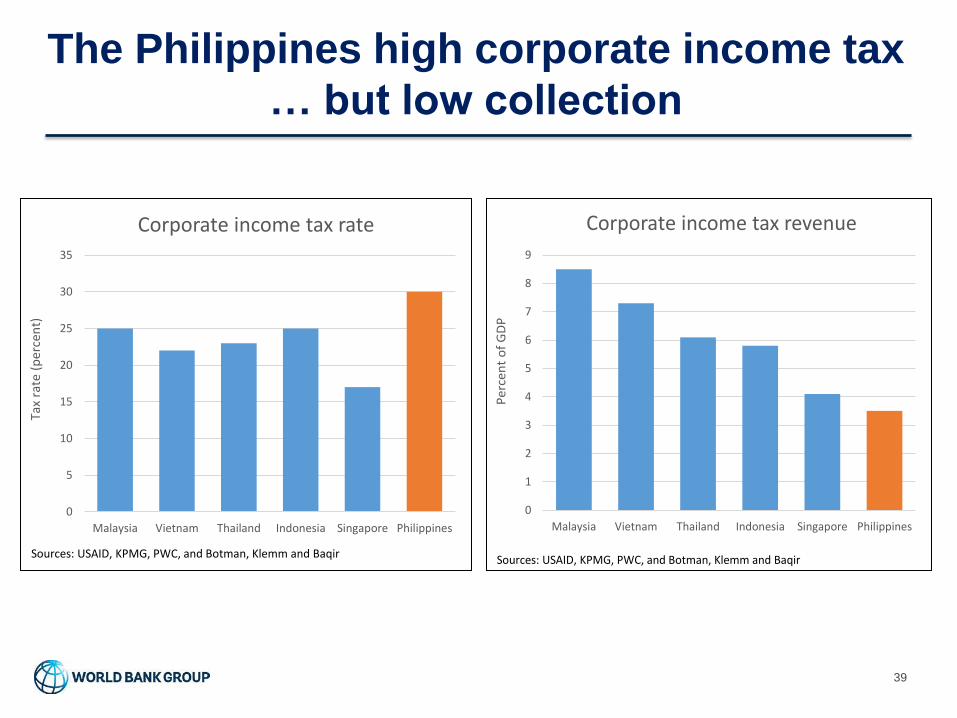

The Philippines high corporate income tax

… but low collection

0

5

10

15

20

25

30

35

Malaysia Vietnam Thailand Indonesia Singapore Philippines

Tax

rate

(p

erce

nt)

Corporate income tax rate

Sources: USAID, KPMG, PWC, and Botman, Klemm and Baqir

0

1

2

3

4

5

6

7

8

9

Malaysia Vietnam Thailand Indonesia Singapore Philippines

Pe

rce

nt

of

GD

P

Corporate income tax revenue

Sources: USAID, KPMG, PWC, and Botman, Klemm and Baqir

Citizens will demand more transparency

in return for paying more taxes

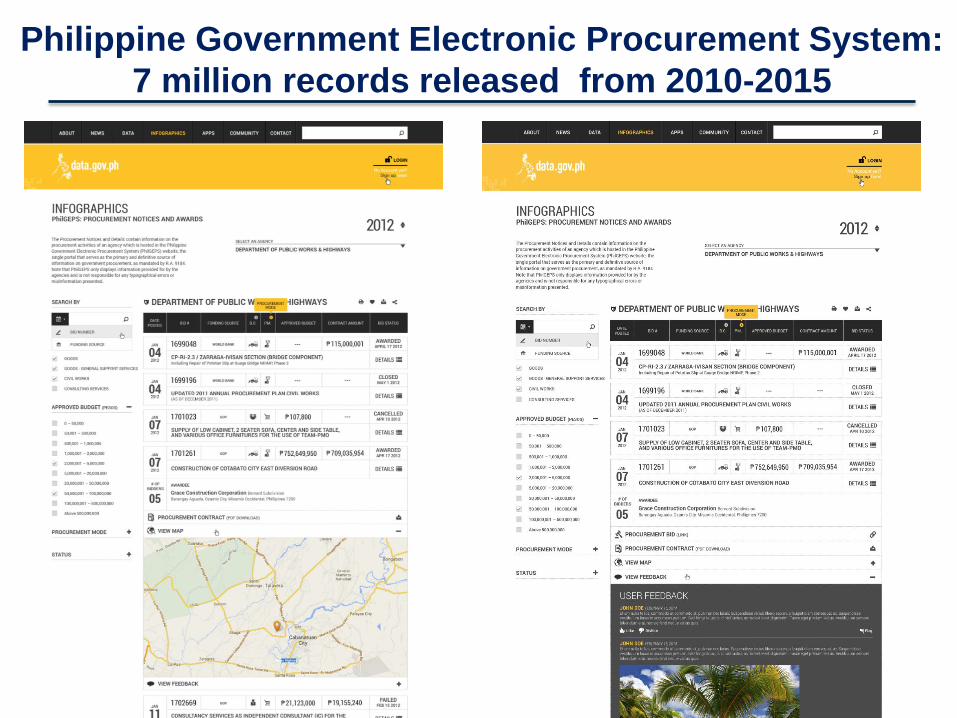

data.gov.ph – over 600 government

data sets are now public

40

Philippine Government Electronic Procurement System:

7 million records released from 2010-2015

Inclusive growth: good leaders not enough, coalitions

needed

• Structural reforms, say increased competition, often face strong

opposition from vested interests

• And the public needs to develop trust in public institutions

• The challenge is in fostering a broad coalition of stakeholders,

led by committed leaders, which supports a reform package,

because they anticipate that inclusive growth makes everybody

better off in the long run, even if some will face losses in the

short run

• These coalitions can form at many levels—sectorally, regionally,

and locally—and around many themes

• This can be done…..but it needs the stakeholders

For reforms to continue:

need coalitions

43