impulse route channel supermarket buying trends c&i...

TRANSCRIPT

Impulse Route Channel

Supermarket Buying Trends

C&I Show Breakfast Summary

The importance of stakeholder management is to support an organization in achieving its strategic objectives by interpreting and influencing both the external and internal environments and by creating positive relationships with stakeholders through the appropriate management of their expectations and agreed objectives. Stakeholder Management is a process and control that must be planned and guided by underlying Principles. Stakeholder management, within business or projects, prepares a strategy utilising information(or intelligence) gathered during the Survey that are common processes to them.

In this example we focus on the respondent “Decision Maker”

( Impulse Retailer ) and a face to face Rep. visitation

Stakeholder Management – Customer Satisfaction

FMCG Back Ground

Traditional Route & Impulse Reports

Report Contents

Traditional Route History

Store Profiles and Demographics

Call Cycle Satisfaction Levels – Coverage Percentage

Overall Satisfaction levels = Your Business Vs. Mean Average

Tailored Benchmarking against “like Suppliers / Distributors”

Key Category Promotions & Brand Marketing Awareness

National Wholesalers Satisfaction

Key Insights on better service requests

Executive summary

Traditional Route & Impulse History

The food-based route and convenience market in Australia is made

up of around 5,000 stores run by major and minor groups plus

another +16,000 largely independent stores. The 5,000 stores are

known as “Organised Convenience” and the +16,000 are

referred to generally as “The Traditional Route Market”.

According to two respected researchers, BIS Schrapnel and Nielsen,

these 16,000 stores make up two thirds of total convenience

business. These are independent convenience stores and mini

marts, corner stores, newsagents, and community stores.*

Traditional Route & Impulse History

* Quote from C&I magazine April 2013

Convenience & Impulse Break Downs 2013

Independent

Traditional Route

“Impulse Channel”

Organised Convenience

Independent Convenience

+16,000

+20,000

+22,000

*2015 C&I Magazine Mail out +27,000 outlets

Traditional Route & Impulse Languages

Where English is a second this requires skilled

language translations

Mandarin / Cantonese

Vietnamese

Korean

Arabic

Hindi

Other?

Traditional Route & Impulse

Methodology / Benchmarking

Impulse Research Methodology Our Biggest!

1st year of annual industry service satisfaction survey with

large number of 1203 respondents from across the country

Key Convenience Retailer, EDM and Magazine support

Mail out insertion into the C&I Magazine and via C.A.M.B.A

Attractive incentives – change to Win one of Five latest iPads

was offered to all respondents

Respondents had 12 weeks to complete and return survey –

Period March. to June 2013

SPSS statistical program has been utilised to professionally

analyse data and prepare tailored reports

“Industry Insights” and “Research Reports” will to be

published in C&I Magazine providing Respondents with

valuable feedback on the results of THEIR Survey

Traditional Route & Impulse Focus

At the C&I EXPO

Launch March 13

The IMPULSE Research enables the measurement of service and performance of the key market

ROUTE SUPPLIERS and their Traditional Brokers / WHOLESALERS who service Grocery &

Non Food, Telco, Beverage & Snacks, Tobacco & Cigarette, Chilled & Perishables categories

within the Impulse channel. Specifically measured are:

Representative Call Frequency

Representative Overall Satisfaction

Our First Route and Impulse Survey comprises these groups

Independent C –Stores / C-Store Buying groups

Service Stations / Corner Stores / Mixed Businesses / General

News agency / Liquor Stores / Tobacconists

Takeaway Food Outlets / Cafes / Bakery / Hot Bread Shops

Impulse Research Results = 1203 Respondents

Impulse Respondent Profile 2013

17%

16%

14%

12%

12%

12%

11%

7%

7%

4%

3%

3%

2%

2%

2%

2%

2%

1%

1%

Takeaway Food

Mixed Business

Convenience Store

Café/Industrial Work Place Eatery

Service Station

Corner Store

Newsagency

Bakery/Hot Bread Shop

General Business

Independent Grocery

Sporting Venue

Tobacconist

Specialty Food

Lucky 7

Liquor Store

Video/DVD Rental

Fruit & Veg.

Friendly Grocer

Retail Pharmacy

Primary Impulse Business Type

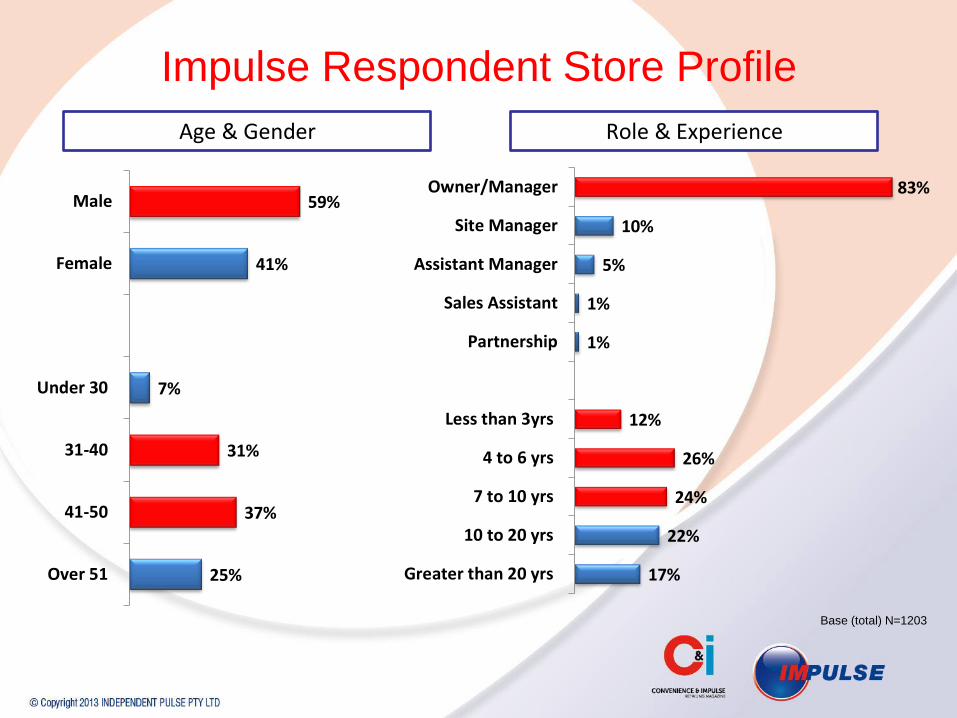

Impulse Respondent Store Profile

Base (total) N=1203

OVER +2000

individual

Traditional

Route

Businesses

Impulse Respondent Store Profile

1%

1%

8%

13%

13%

22%

42%

Australian Capital Territory(ACT)

Tasmania (TAS)

Western Australia (WA)

Queensland (QLD)

South Australia (SA)

Victoria (VIC)

New South Wales (NSW)

0% 10% 20% 30% 40% 50%

Metro 79%

Rural 21%

State Rural / Metro

Base (total) N=1203

Impulse Respondent Store Profile

54%

22%

11%

4%

3%

1%

1%

3%

Up to $1 million

$1.1 - $1.5 million

$1.6 - $2 million

$2.1 - $2.5 million

$2.6 - $3 million

$3.1 - $3.5 million

$3.6 - $4 million

Over $5 million

0% 10% 20% 30% 40% 50% 60%

Main Street 49%

Suburban Street 30%

Major Highway

11%

Shopping Centre

10%

Annual Turnover Store Location

Base (total) N=1203

59%

41%

7%

31%

37%

25%

Male

Female

Under 30

31-40

41-50

Over 51

Age & Gender Role & Experience

83%

10%

5%

1%

1%

12%

26%

24%

22%

17%

Owner/Manager

Site Manager

Assistant Manager

Sales Assistant

Partnership

Less than 3yrs

4 to 6 yrs

7 to 10 yrs

10 to 20 yrs

Greater than 20 yrs

Impulse Respondent Store Profile

Base (total) N=1203

Impulse Suppliers & Traditional Wholesalers

2013

British American Tobacco

Imperial Tobacco

Phillip Morris

AIDA Group C-Store, Metcash / Campbells Cash & Carry

Hollier Dicksons

Repco

Service Station Supplies – SSA

The Distributors – JB, Accredited

Austt. Convenience

Foods (ACF)

Battery Specialists

Ben & Jerry’s

Bundaberg Drinks Coca-Cola Amatil

Ferrero Aust.

Ferndale Confect.

Frucor

George Weston

Foods

Goodman Fielder

Go Natural

GlaxoSmithKline

Mondelez

International

Lion Co

Mars Confectionary

Mrs Mac’s

Nestlé Confectionary

Optus Prepaid

Pacific Optics Parmalat

Patties

Peters Ice Cream

Red Bull

Schweppes Aust.

Smith’s Sackfood Co.

Snack Brands Aust.

Superior Sales Force

Stuart Alexander

Unilever – Streets

Wrigley

MAJOR CONVENIENCE SERVICE PROVIDERS TOBACCO SERVICE PROVIDERS

WHOLESALER SERVICE PROVIDERS

Impulse Research Results – Breakdowns The Survey Results can be cross represented across a wide range of parameters which

helps Suppliers obtain a greater level of insight into key concerns of Impulse Retailers:

Data Breakouts Available

By State / Metro / Rural

By Impulse Business type ( Corner store, Take away, Service station, etc)

By Turnover

Tailored Benchmarking against like suppliers

Yearly Benchmarking available 2014

Individual supplier “Regular Call” satisfaction

Specialised Conference / State Managers Presentations

(Provided on request)

Satisfaction with Supplier Rep Call Cycle – CATEGORY AVERAGES

6%

7%

7%

10%

13%

10%

13%

18%

20%

27%

25%

20%

25%

27%

20%

21%

25%

20%

22%

22%

26%

8%

7%

5%

6%

12%

6%

7%

49%

45%

37%

39%

32%

38%

28%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

General Sundry

Confectionery

Snack foods

Ice Cream

Wholesalers

Beverages

Tobacco

Extremely Satisfied Very Satisfied Somewhat Satisfied Dissatisfied Very Dissatisfied

Base: Tobacco=1183,Beverages=1181, Ice cream=1168, General sundry=1144,Sncakfoods=1123, Confectionery=1169, wholesalers=1169

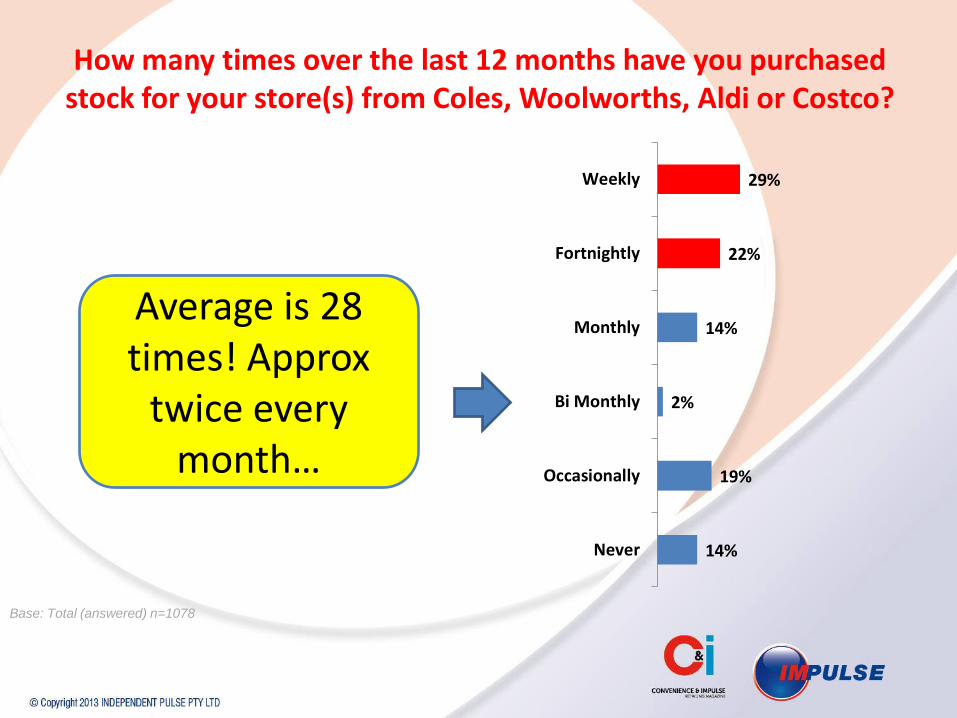

29%

22%

14%

2%

19%

14%

Weekly

Fortnightly

Monthly

Bi Monthly

Occasionally

Never

How many times over the last 12 months have you purchased

stock for your store(s) from Coles, Woolworths, Aldi or Costco?

Base: Total (answered) n=1078

Average is 28 times! Approx

twice every month…

30%

27%

16%

13%

7%

7%

Less than 5%

5 - 10%

11 - 15%

16 - 20%

21 - 30%

Over 30%

Over the past 12 months, what percentage of your shop

stock purchases have you spent at these outlets?

Base: Total (answered) n=1078

Average is 15% of shopping

87%

45%

35%

30%

29%

26%

23%

12%

12%

10%

2%

1%

1%

Soft drinks

Sport/Energy Drinks

Confectionary

Bar lines

General Merchandise

SnackFoods

Biscuits

Tobacco

Pet Food

Fresh Food (Milk, Bread, Veg etc)

Others

Chicken/Deli

Grocery (toiletries, tissues, Cleaning…

Top categories in supermarket buying

Base: Total (answered) n=1015

Most Purchase

Impulse Items For Quick

Resale

Copyright design and concept ©2012 Independent Pulse Pty Ltd.

Apart from any fair dealing for the purposes of study, research, criticism and review, as permitted under copyright

legislation, no part of the Content (all information, and data, including graphics) may be reproduced, published,

stored, reused, transmitted or redistributed by any person or entity (including Google, You Tube, Amazon or similar

organisations) in any form or by any means, electronic or mechanical, including photocopying, recording, scanning or

by any information storage and retrieval system for any purpose whatsoever, or distributed to a third party for any

purpose, without the written permission of Independent Pulse. For such purposes as are permitted, you must

acknowledge Independent Pulse as the source of information and include any copyright notice originally included

with the Content or as directed by Independent Pulse, in all copies. If permission is granted a link to

www.pulseplus.com.au and this document must be included on all reproduced material.

While every care is taken to ensure the accuracy of this data, Independent Pulse does not make any representations

or warranties about its accuracy, reliability, completeness or suitability for any particular purpose and, to the extent

permitted by law (but subject to any liability which cannot be excluded under the Competition and Consumer Act 2010

and equivalent State and Territory legislation), Independent Pulse disclaims all responsibility and all liability

(including without limitation, liability in negligence) for all expenses, losses, damages (including indirect or

consequential damage) and costs which might be incurred as a result of the data being inaccurate or incomplete in

any way and for any reason. You accept sole responsibility and risk associated with the use and results of information

presented.

Under no circumstances shall Independent Pulse be liable for any loss or damage (including special, indirect or

consequential damage) whatsoever which may arise from or in connection with the use of the Content.

This agreement will be administered under the laws of the State of New South Wales, Australia.

© 2012 Independent Pulse Pty Ltd

Independent Pulse reserves the right to change the Terms of Use without notification.

Impulse Terms & Conditions of Use

Thank You – [email protected]