impact of microfinance bank on standard of living of hairdresser … · impact of microfinance bank...

TRANSCRIPT

IOSR Journal of Humanities and Social Science (IOSRJHSS)

ISSN: 2279-0845 Volume 1, Issue 4 (Sep.-Oct. 2012), PP 26-35 www.iosrjournals.org

www.iosrjournals.org 26 | Page

Impact of Microfinance Bank on Standard Of Living of

Hairdresser in Oshodi-Isolo Local Government of Lagos State.

1Olusanya, Samuel Olumuyiwa,

2Oyebo Afees Oluwatosin

1lecturer Lagos State University External System. Economics Department.

2lecturer Lagos State University External System. Marketing Department

Abstract: The research study takes a look at the impact of Microfinance bank on standard of living of

hairdressers in Oshodi-Isolo local government area (LGA) of Lagos State as a Poverty eradication strategy

among the society. The objectives of the study examine how Microfinance bank in Oshodi-Isolo has impacted

greatly on the business of hairdressers in the local Government and to also examine the impact of Microfinance

on asset acquisition and savings of hairdressers in that LGA. A total of 120 hairdressers who registered with

Oshodi-Isolo LGA were used as study sample. However, primary data of questionnaire analysis was adopted

and Spearman’s rank correlation coefficient analysis was used as the estimation techniques. More so, the

hypotheses of the research were tested at 5% level of significance and the result revealed that there is a

significant relationship between Microfinance bank efforts and standard of living of hairdressers in Oshodi-

Isolo local Government area of Lagos state, and the implication of this is that due to the existence and help of

Microfinance bank, Poverty has reduced a little bit among the hairdressers association in Oshodi Isolo LGA. In conclusion, the study recommend that Government at Local, State and Federal levels through the Central bank

of Nigeria should ensure that Microfinance bank loans are easily obtainable and repayment should include a

grace period with reasonable schedule instead of weekly payment period that is commonly found among the

microfinance banks in Nigeria.

Keywords: Hairdressing, Liquidity, Micro-Credit, Micro Enterprises, Microfinance Bank, Standard of Living,

Poverty.

I. Introduction The issue of poverty has been a major concern to many nations, particularly the developing countries.

Poverty has been defined as a situation where a population or a section of the population is able to meet only its bare subsistence, the essentials of food, clothing and shelter, in order to maintain a minimum standard of living

(Balogun, 1999). The World Development Report (WDR) from the World Bank (1990) notes that conditions

could be described as poor if per capita income or consumption of the individual is below US $370 or very poor

if it is below US $275 at any time period.

Englama and Bamidele (1997) aptly summarized the definition of poverty, in both absolute and relative

terms as a state where an individual is not able to cater adequately for his/her basic needs of food, clothing and

shelter, meet social and economic obligations; lacks gainful employment, skills, assets and self-esteem; and has

limited access to social and economic infrastructures. In other words, the poor lacks basic infrastructure such as

education, health, potable water, and sanitation, and as a result has limited chance of advancing his/her welfare

to the limit of his/her limited access to social and economic infrastructures”. In other words, the poor lacks

capabilities The World Bank (1993) describe the poverty line as the value of income or consumption necessary for (a) the minimum standard of nutrition and (b) other “necessities.” The Human Development Index (HDI) of

the United Nations Development Programme (UNDP, 1996) introduced by the United Nations to give indication

of poverty or prosperity level within a society and globe, considers life expectancy at birth, adult literacy rate,

combined primary, secondary and tertiary enrolment ratio and the Real GDP per capita as factor indicators of

interest.

Oladunni (1999) notes that poverty is a worldwide phenomenon; however, Nigeria is one of the poorest

countries in the world. The situation has reached an alarming stage as more than 45% of the population lives

below the poverty line, while 67% of the poor are extremely poor. For example, the Bureau of Statistics‟ (BOS)

report for the period 1980-1996, indicates about 67 million Nigerians are living below the poverty level. The

report also indicates that from 1980 to 1985, the percentage of rural dwellers and urban inhabitants in the core

poverty bracket rose from 6.5 and 3.0 percent to 14.8 and 7.5 percent, respectively. Within the same period, the

percentage of moderately poor in the rural areas rose from 21.8 to 36.6 percent and 14.2 to 30.3 percent, respectively. Also the number of non-poor in both rural and urban areas dropped from 71.7 and 82.8 percent to

48.6 and 62.2 percent, respectively (Awoseyila, 1999; Okumadewa, 1999). The increasing incidence of poverty

in Nigeria within this period is not surprising. Going by the documentaries of Oladunni (1999) the overall

Impact Of Microfinance Bank On Standard Of Living Of Hairdresser In Oshodi-Isolo Local

www.iosrjournals.org 27 | Page

dependency ratio in Nigeria is 234 dependents per 100 gainfully employed persons. In the rural areas, it is 286

dependants per 100 workers, while in the urban centre it is 219 dependants per 100 workers. The

labor force age (between 15 and 64 years) dependant ratio is 259 dependants per 100 workers nationwide. It is

302 and 222 dependants per 100 workers in the rural and urban centers, respectively.. The above scenario works

concertedly to further reinforce the poverty syndrome of the average Nigerian employee, as each bears heavy

economic burden of over 200 non-workers. Poverty as noted earlier is not peculiar to Nigeria or developing nations alone, rather it has attracted worldwide

attention.

Egwuatu (2008) documents over 500 million of the world‟s population lives under very poor

conditions, but they are economically active. They lack access to basic necessities of life: food, shelter and

primary health care. They earn their livelihoods by being self employed as micro entrepreneurs or by working in

micro enterprises (very small businesses which may employ up to 5 people). This set of people has no hope for

expansion of their enterprise because of inability or incapability of accessing banks for credit.

More than 80 percent of all households in developing countries do not have access to institutional

banking services. This is because they lack the collateral to secure loans from formal financial institutions.

Besides, the technical backing needed for creativity and enhanced productivity is absent. Ehigiamusoe (2008)

notes that microfinance assumes the poor know what to do to enhance their economic condition, but they

operate from a slim economic base which can be strengthened by funds borrowed on affordable terms. In September 2005 at the World Summit, the 60th high-level plenary meeting of the United Nations General

Assembly gathered 151 Heads of State from all over the world at the UN Headquarters for the purpose of

getting the world leaders to review progress in reaching the targets of the Millennium Development Goals

(MDG), with the primary aim of eradicating extreme poverty by the year 2015. Microfinance was prominent on

the agenda of this historic gathering. The most significant recognition of its importance was made in the 2005

World Summit Outcome Document adopted by the gathering, which states, “We recognize the need for access

to financial services, in particular for the poor, including microfinance and microcredit” (Egwuatu, 2008). Thus,

microfinance has emerged as a growing industry to provide financial services to very poor people. It is premised

on the fact of economic relations, that the poor remain poor because they are deprived of access to life

transforming opportunities. Service users include artisans, small holder farmers, food processors, petty traders

and other persons who operate micro-enterprises. Sequel to the consolidation exercise by the CBN under the leadership Chukwuma Soludo and the emergence of

mega banks, the concept of microfinance banks, MFB, was introduced to provide a platform for the

underbanked segment of the economy that may not be able to meet the stringent requirements of the

conventional banks. It was also to be private sector driven. But this has already run into serious problems as

most MFBs are already facing one financial challenge or the other. From the above analysis, one can come to

the logical conclusion that government-driven poverty alleviation programs are viewed by the poor as largesse

while private sector-led programs are seen by promoters as avenues of mobilizing funds for their businesses. It

is apposite to examine why the MFBs are having problems. Therefore the research study will tend to examine

the following objectives; to examine how Microfinance bank in Oshodi Isolo has impacted greatly on the

business of hairdressers in the local Government and to also examine the impact of Microfinance on asset

acquisition and savings of hairdressers in that LGA.

II. Brief Literature Review The issue of poverty has been a major concern to many nations, particularly the developing countries.

Poverty has been defined as a situation where a population or a section of the population is able to meet only its

bare subsistence, the essentials of food, clothing and shelter, in order to maintain a minimum standard of living

(Balogun, 1999). The World Development Report (WDR) from the World Bank (1990) notes that conditions

could be described as poor if per capita income or consumption of the individual is below US $370 or very poor

if it is below US $275 at any time period. Englama and Bamidele (1997) aptly summarized the definition of

poverty, in both absolute and relative terms as a state where an individual is not able to cater adequately for

his/her basic needs of food, clothing and shelter, meet social and economic obligations; lacks gainful employment, skills, assets and self-esteem; and has limited access to social and economic infrastructures. In

other words, the poor lacks basic infrastructure such as education, health, potable water, and sanitation, and as a

result has limited chance of advancing his/her welfare to the limit of his/her limited access to social and

economic infrastructures”. In other words, the poor lacks capabilities. The World Bank (1993) describes the

poverty line as the value of income or consumption necessary for (a) the minimum standard of nutrition and (b)

other “necessities.” The Human Development Index (HDI) of the United Nations Development Programme

(UNDP, 1996) introduced by the United Nations to give indication of poverty or prosperity level within a

society and globe, considers life expectancy at birth, adult literacy rate, combined primary, secondary and

tertiary enrolment ratio and the Real GDP per capita as factor indicators of interest. Oladunni (1999) notes that

poverty is a worldwide phenomenon; however, Nigeria is one of the poorest countries in the world. The

Impact Of Microfinance Bank On Standard Of Living Of Hairdresser In Oshodi-Isolo Local

www.iosrjournals.org 28 | Page

situation has reached an alarming stage as more than 45% of the population lives below the poverty line, while

67% of the poor are extremely poor. For example, the Bureau of Statistics‟ (BOS) report for the period 1980-

1996, indicates about 67 million Nigerians are living below the poverty level. The report also indicates that from

1980 to 1985,

The percentage of rural dwellers and urban inhabitants in the core poverty bracket rose from 6.5 and

3.0 percent to 14.8 and 7.5 percent, respectively. Within the same period, the percentage of moderately poor in the rural areas rose from 21.8 to 36.6 percent and 14.2 to 30.3 percent, respectively. Also the number of non-

poor in both rural and urban areas dropped from 71.7 and 82.8 percent to 48.6 and 62.2 percent, respectively

(Awoseyila, 1999; Okumadewa, 1999). The increasing incidence of poverty in Nigeria within this period is not

surprising. Going by the documentaries of Oladunni (1999) the overall dependency ratio in Nigeria is 234

dependents per 100 gainfully employed persons. In the rural areas, it is 286 dependants per 100 workers, while

in the urban centre it is 219 dependants per 100 workers. The labor force age (between 15 and 64 years)

dependant ratio is 259 dependants per 100 workers nationwide. It is 302 and 222 dependants per 100 workers in

the rural and urban centers, respectively.. The above scenario works concertedly to further reinforce the poverty

syndrome of the average Nigerian employee, as each bears heavy economic burden of over 200 non-workers.

Poverty as noted earlier is not peculiar to Nigeria or developing nations alone, rather it has attracted

worldwide attention. Egwuatu (2008) documents over 500 million of the world‟s population lives under very

poor conditions, but they are economically active. They lack access to basic necessities of life: food, shelter and primary health care. They earn their livelihoods by being self employed as micro entrepreneurs or by working in

micro enterprises (very small businesses which may employ up to 5 people). This set of people has no hope for

expansion of their enterprise because of inability or incapability of accessing banks for credit.

More than 80 percent of all households in developing countries do not have access to institutional banking

services. This is because they lack the collateral to secure loans from formal financial institutions. Besides, the

technical backing needed for creativity and enhanced productivity is absent. Ehigiamusoe (2008) notes that

microfinance assumes the poor know what to do to enhance their economic condition, but they operate from a

slim economic base which can be strengthened by funds borrowed on affordable terms.

Microfinance in Nigeria, though on informal setting is as old as the nation itself. Though the informal system is

a rural unregulated and unofficial financial arrangement, it has highly respected modus operandi by which

individuals or groups relate in their various capacities as debtors and creditors outside the regimented and regulated markets. The informal financial market is classified into institutional and non-institutional markets. In

the non-institutional markets, the activities of savings and acquisition of credits are done by individuals on their

own or through person-to-person arrangement. The market includes self financing, financing by relations,

friends and well wishers, professional money lenders, jackpot, raffle and pool winnings, and trust system of

credit transactions. Institutional market on the other hand refers to any organizational or institutional

arrangement that aims at mobilizing savings and credits. Found in this market are the rotating savings and credit

associations (ROSCAs), thrift associations, savings mobilization groups (which are traditionally called Esusu,

bam bam, ajo, and adashi by different communities), daily savings or contribution organizations, co-operative

societies, religious organizations, social clubs and village or town unions. The informal system of advancing

credit irrespective of the meager amount it generates remains the major source of finance for the poor who see

the formal financial institution as being too bureaucratic, costly and cumbersome (Okpara, 1990). The

Government of Nigeria on its own has made several efforts at redressing the inadequate supply of financial services to the poor. In 1936, government in support of the cooperatives promulgated the cooperative society‟s

ordinance. This made the cooperatives have regular/compulsory savings as one of their goals while thrift and

credit societies combined regular savings of members with lending. The Commercial Bill Financing Scheme in

1962 and the Regional commodity Boards (later called National Commodity Boards in 1977) were among the

efforts made by government to improve the poor‟s access to lending. The Nigerian Agricultural and Cooperative

Bank (NACB) was established in 1972 to act as development finance institution extending loans to both small

and large-scale farmers. A similar institution, the Agricultural Credit Guarantee Scheme Fund (ACGSF) was

established in 1978 for the purpose of agricultural risk reduction. The bank guarantees up to 75% of the

principle in case of default due to natural events beyond the control of the farmers. Others are the Rural Banking

System of 1977, where banks were required to establish a specified number of branches in identified rural areas.

Export Financing Rediscount Facility in 1987, measured rural credit markets, including the sectoral allocation of credit, specified percentage of total deposits mobilized in the rural areas to be lent to borrowers in such areas,

concessional interest and grace periods on agricultural loans. However, some of these measures were abolished

with the introduction of liberal economic policies in 1989. The Peoples Bank established in 1989 for the same

purpose, was charged with the responsibility of taking deposits and lending to the poor. There was also licensing

of community banks in the 1990s for the provision of non-sophisticated loans to the community. Community

Bank metamorphosed into the recent Microfinance Bank in 2005. Some of these efforts were frustrated by lack

of managerial wherewithal, lack of supervision, mischannelling of credit facilities, bribery and corruption

(Olaitan 2001; Adeyemi, 2008).

Impact Of Microfinance Bank On Standard Of Living Of Hairdresser In Oshodi-Isolo Local

www.iosrjournals.org 29 | Page

III. Women Involvement And Micro-Finance In Nigeria. Nigerian is the seventy world largest exporter oil, yet ranks 158 out of the 188 countries of the world in

terms of quality of life (UNDP, 2007). Available statistics indicate that poverty has become endmic in Nigeria

and is on the increase. About two third of the Nigeria‟s population (about 150 million) are poor (UNDP, 2007). Out of these numbers of poor Nigerian, women represent greater proportion due largely to their ascribed and

acquired role: for instance, about 65 percent of active population, most of them women have been excluded

from formal financial institutions (Bamisile, 2006).

The increased focus on gender and development debate has been an important development of the last

three decades. According to UNECA (2005) cited in Yeshiareg (2009), one of the reasons why Africa is off

track in terms of meeting the millennium development goal targets, includes persistent gender inequality and

discrimination. The current challenge facing the cantment (Africa) and Nigeria in particular is how to achieve a

reversal of inequalities. Emergence of Micro Finance Bank was largely aggravated by the exclusion of the

informal sector by the formal financial system in Nigeria and indeed other developing countries. Thus, the

Micro Finance Banks are primarily established to fill the gap created by the formal financial institutions.

Anyanwu (2004), summarizing the objectives of Micro Finance Bank to include: improvement of the socioeconomic conditions of women, especially those in the rural areas through the provision of loan assistance.

This role has become necessary in Nigerian in order to foster the living standard of women that are heavily

disenfranchised by the formal banking system due largely to the perceived and real high risk and cost associated

with serving the poor. Corroborating this view, Anyanwu (2004) opined that a particular example in Nigeria is

that women suffer the disability of non access of bank credit, yet such credit removes constraints and poverty.

IV. Microfinance Bank And Standard Of Living Income is one of the important elements of living standard of the poor people as well as saving.

Mohammed and Mohammed (2007) The Microfinance Banks are to provide loans to the poor

not only the increase their income but also to mobilize their savings CBN, (2005). Apart from these other factors

that contribute to human development, like education, empowerment are also included as variables indicating a

level of standard of living. This study endeavor to explore and find out to what extent the standard of living of

hairdresser in Oshodi/Isolo Local Government has been influenced since they joined the microfinance program.

Microfinance programs target both economic and social poverty, and in essence it is important to assess the

success of Microfinance Bank. And according to Ghalid (2009), there need to measure the impact on borrowers,

whom in this study are the hairdresser in Oshodi/Isolo local Government. Mohammad and Mohammed (2007)

opined that Microfinance Bank interventions promote living condition of poor people by offering supportive

service. These supportive services are important indicators of the human development. Mohindra et al (2005), cited in Mohammad and Mohammed (2007) said Microfinance Banks micro credit helps to empower in society,

especially among the women clients. Traditionally, development initiatives are synonymous with raising

people‟s incomes, employment opportunities, consumption, building of assets and accumulating savings. Impact

assessment studies look for indicators and variables that measure prosperity no terms of material and tangible

assets that can be awarded numeric values such as increased income, greater employment ownership of physical

assets (Ghalid 2009).

V. Methodology

The data that would be generated for the purpose of this research study is be basically primary data that

would be used in generating questionnaire which will be administered to the members of hairdressers who

registered with Oshodi Isolo LGA.

However, the study population comprises 120 hairdressers who registered with Oshodi Isolo LGA and

it is made up of male and female altogether. More so, the population also has different material status from

single to married employees.

However, Spearman‟s rank correlation coefficient will be adopted in this study. Spearman's rank

correlation coefficient or Spearman's rho, named after Charles Spearman and often denoted by the Greek letter

(rho) or as, is a non-parametric measure of statistical dependence between two variables. It assesses how well

the relationship between two variables can be described using a monotonic function. If there are no repeated data values, a perfect Spearman correlation of +1 or −1 occurs when each of the variables is a perfect monotone

function of the other. Therefore Spearman's coefficient can be used when both dependent (outcome; response)

variable and independent (predictor) variable are ordinal numeric, or when one variable is a ordinal numeric and

the other is a continuous variable. However, it can also be appropriate to use Spearman's correlation when both

variables are continuous and the formular is as follows;

R = 1- 6∑d2

n (n2-1)

Where d = the difference between the ranks of each pair.

n = number of paired observations

Impact Of Microfinance Bank On Standard Of Living Of Hairdresser In Oshodi-Isolo Local

www.iosrjournals.org 30 | Page

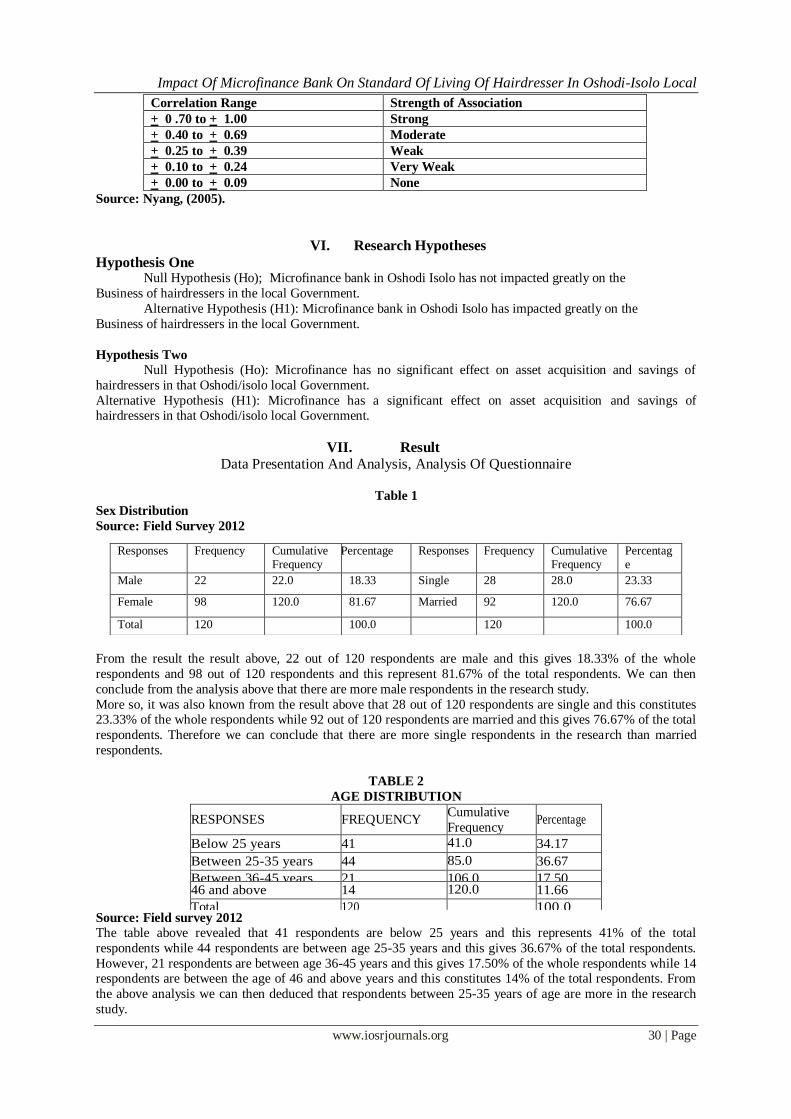

Correlation Range Strength of Association

+ 0 .70 to + 1.00 Strong

+ 0.40 to + 0.69 Moderate

+ 0.25 to + 0.39 Weak

+ 0.10 to + 0.24 Very Weak

+ 0.00 to + 0.09 None

Source: Nyang, (2005).

VI. Research Hypotheses

Hypothesis One Null Hypothesis (Ho); Microfinance bank in Oshodi Isolo has not impacted greatly on the

Business of hairdressers in the local Government.

Alternative Hypothesis (H1): Microfinance bank in Oshodi Isolo has impacted greatly on the

Business of hairdressers in the local Government.

Hypothesis Two

Null Hypothesis (Ho): Microfinance has no significant effect on asset acquisition and savings of

hairdressers in that Oshodi/isolo local Government.

Alternative Hypothesis (H1): Microfinance has a significant effect on asset acquisition and savings of hairdressers in that Oshodi/isolo local Government.

VII. Result

Data Presentation And Analysis, Analysis Of Questionnaire

Table 1

Sex Distribution

Source: Field Survey 2012

From the result the result above, 22 out of 120 respondents are male and this gives 18.33% of the whole

respondents and 98 out of 120 respondents and this represent 81.67% of the total respondents. We can then

conclude from the analysis above that there are more male respondents in the research study.

More so, it was also known from the result above that 28 out of 120 respondents are single and this constitutes 23.33% of the whole respondents while 92 out of 120 respondents are married and this gives 76.67% of the total

respondents. Therefore we can conclude that there are more single respondents in the research than married

respondents.

TABLE 2

AGE DISTRIBUTION

RESPONSES FREQUENCY Cumulative

Frequency Percentage

Below 25 years 41 41.0 34.17

Between 25-35 years 44 85.0 36.67

Between 36-45 years 21 106.0 17.50 46 and above 14 120.0 11.66

Total 120 100.0 Source: Field survey 2012

The table above revealed that 41 respondents are below 25 years and this represents 41% of the total

respondents while 44 respondents are between age 25-35 years and this gives 36.67% of the total respondents.

However, 21 respondents are between age 36-45 years and this gives 17.50% of the whole respondents while 14 respondents are between the age of 46 and above years and this constitutes 14% of the total respondents. From

the above analysis we can then deduced that respondents between 25-35 years of age are more in the research

study.

Responses Frequency Cumulative Frequency

Percentage Responses Frequency Cumulative Frequency

Percentage

Male 22 22.0 18.33 Single 28 28.0 23.33

Female 98 120.0 81.67 Married 92 120.0 76.67

Total 120 100.0 120 100.0

Impact Of Microfinance Bank On Standard Of Living Of Hairdresser In Oshodi-Isolo Local

www.iosrjournals.org 31 | Page

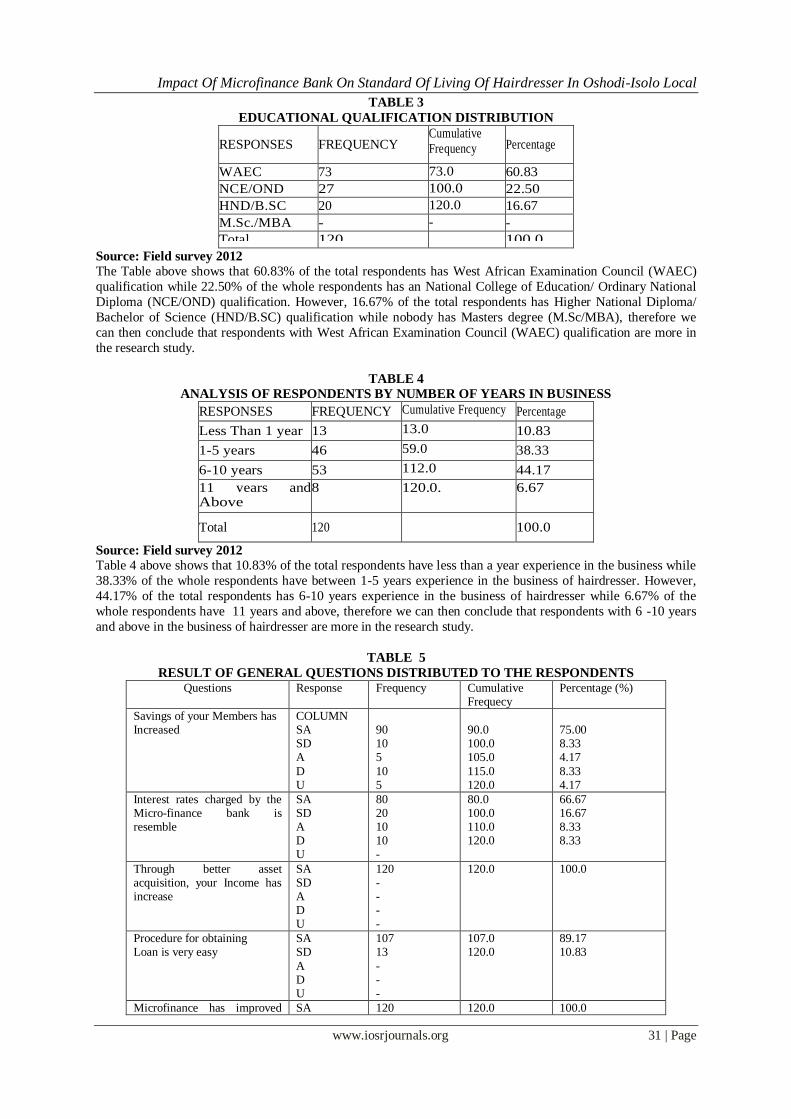

TABLE 3

EDUCATIONAL QUALIFICATION DISTRIBUTION

RESPONSES FREQUENCY Cumulative

Frequency Percentage

WAEC 73 73.0 60.83

NCE/OND 27 100.0 22.50

HND/B.SC 20 120.0 16.67

M.Sc./MBA - - -

Total 120 100.0 .

Source: Field survey 2012

The Table above shows that 60.83% of the total respondents has West African Examination Council (WAEC)

qualification while 22.50% of the whole respondents has an National College of Education/ Ordinary National

Diploma (NCE/OND) qualification. However, 16.67% of the total respondents has Higher National Diploma/

Bachelor of Science (HND/B.SC) qualification while nobody has Masters degree (M.Sc/MBA), therefore we

can then conclude that respondents with West African Examination Council (WAEC) qualification are more in

the research study.

TABLE 4

ANALYSIS OF RESPONDENTS BY NUMBER OF YEARS IN BUSINESS

RESPONSES FREQUENCY Cumulative Frequency Percentage

Less Than 1 year 13 13.0 10.83

1-5 years 46 59.0 38.33

6-10 years 53 112.0 44.17

11 years and

above

8 120.0. 6.67 Above

Total 120

100.0

Source: Field survey 2012

Table 4 above shows that 10.83% of the total respondents have less than a year experience in the business while

38.33% of the whole respondents have between 1-5 years experience in the business of hairdresser. However,

44.17% of the total respondents has 6-10 years experience in the business of hairdresser while 6.67% of the

whole respondents have 11 years and above, therefore we can then conclude that respondents with 6 -10 years

and above in the business of hairdresser are more in the research study.

TABLE 5

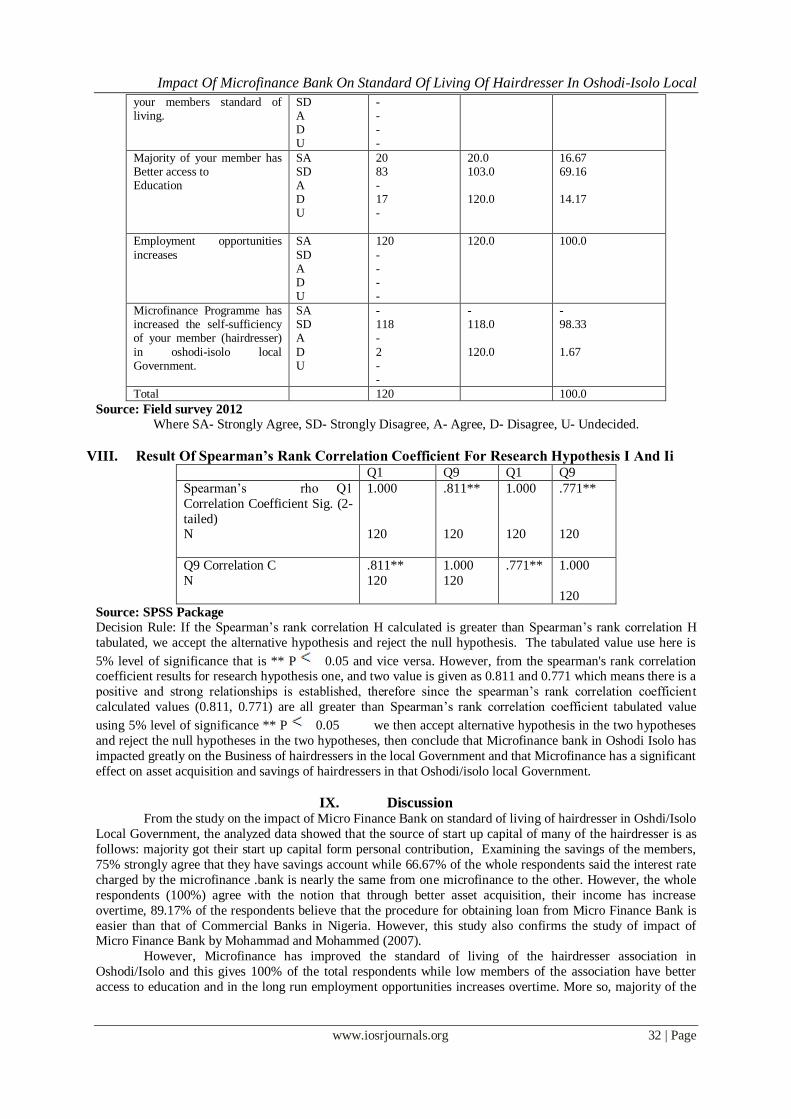

RESULT OF GENERAL QUESTIONS DISTRIBUTED TO THE RESPONDENTS Questions Response Frequency

Cumulative Frequecy

Percentage (%)

Savings of your Members has Increased

COLUMN SA SD A

D U

90 10 5

10 5

90.0 100.0 105.0

115.0 120.0

75.00 8.33 4.17

8.33 4.17

Interest rates charged by the Micro-finance bank is resemble

SA SD A D U

80 20 10 10 -

80.0 100.0 110.0 120.0

66.67 16.67 8.33 8.33

Through better asset acquisition, your Income has increase

SA SD A D U

120 - - - -

120.0 100.0

Procedure for obtaining Loan is very easy

SA SD

A D U

107 13

- - -

107.0 120.0

89.17 10.83

Microfinance has improved SA 120 120.0 100.0

Impact Of Microfinance Bank On Standard Of Living Of Hairdresser In Oshodi-Isolo Local

www.iosrjournals.org 32 | Page

your members standard of living.

SD A D U

- - - -

Majority of your member has Better access to Education

SA SD A D U

20 83 - 17 -

20.0 103.0 120.0

16.67 69.16 14.17

Employment opportunities

increases

SA

SD A D U

120

- - - -

120.0

100.0

Microfinance Programme has increased the self-sufficiency of your member (hairdresser)

in oshodi-isolo local Government.

SA SD A

D U

- 118 -

2 - -

- 118.0

120.0

- 98.33

1.67

Total 120 100.0

Source: Field survey 2012

Where SA- Strongly Agree, SD- Strongly Disagree, A- Agree, D- Disagree, U- Undecided.

VIII. Result Of Spearman’s Rank Correlation Coefficient For Research Hypothesis I And Ii Q1 Q9 Q1 Q9

Spearman‟s rho Q1

Correlation Coefficient Sig. (2-

tailed) N

1.000

120

.811**

120

1.000

120

.771**

120

Q9 Correlation C

N

.811**

120

1.000

120

.771** 1.000

120

Source: SPSS Package

Decision Rule: If the Spearman‟s rank correlation H calculated is greater than Spearman‟s rank correlation H

tabulated, we accept the alternative hypothesis and reject the null hypothesis. The tabulated value use here is

5% level of significance that is ** P 0.05 and vice versa. However, from the spearman's rank correlation coefficient results for research hypothesis one, and two value is given as 0.811 and 0.771 which means there is a

positive and strong relationships is established, therefore since the spearman‟s rank correlation coefficien t

calculated values (0.811, 0.771) are all greater than Spearman‟s rank correlation coefficient tabulated value

using 5% level of significance ** P 0.05 we then accept alternative hypothesis in the two hypotheses

and reject the null hypotheses in the two hypotheses, then conclude that Microfinance bank in Oshodi Isolo has

impacted greatly on the Business of hairdressers in the local Government and that Microfinance has a significant

effect on asset acquisition and savings of hairdressers in that Oshodi/isolo local Government.

IX. Discussion From the study on the impact of Micro Finance Bank on standard of living of hairdresser in Oshdi/Isolo

Local Government, the analyzed data showed that the source of start up capital of many of the hairdresser is as

follows: majority got their start up capital form personal contribution, Examining the savings of the members,

75% strongly agree that they have savings account while 66.67% of the whole respondents said the interest rate

charged by the microfinance .bank is nearly the same from one microfinance to the other. However, the whole

respondents (100%) agree with the notion that through better asset acquisition, their income has increase

overtime, 89.17% of the respondents believe that the procedure for obtaining loan from Micro Finance Bank is

easier than that of Commercial Banks in Nigeria. However, this study also confirms the study of impact of Micro Finance Bank by Mohammad and Mohammed (2007).

However, Microfinance has improved the standard of living of the hairdresser association in

Oshodi/Isolo and this gives 100% of the total respondents while low members of the association have better

access to education and in the long run employment opportunities increases overtime. More so, majority of the

Impact Of Microfinance Bank On Standard Of Living Of Hairdresser In Oshodi-Isolo Local

www.iosrjournals.org 33 | Page

respondents strongly agree that Microfinance programme has not increased the self-sufficiency of their member

(hairdresser) in Oshodi/Isolo local Government.

In conclusion, microfinance bank has given hope to the poor by improving their standard of living in

Nigeria than the commercial banks where in the case of paying the loan plus the capital out of the original

capital did not leave room for better access for education nor better financial situation of their family and hence

left many poorer than before collecting of the Micro Credit thereby reduced their standard of living.

X. Conclusion And Recommendations Despite the laudable impact of Micro Finance in many part of world, (Yunus, 1999; Kehinde, 2006;

Mohammad Mohammed, 2007) the impact was seriously felt a bit in Oshodi/Isolo local Government area of

Lagos state, and it has reduce the rate of poverty and standard of living has been enhanced to some certain

extent. In view of the problems encountered above, we recommend that the government through the Apex bank

(Central Bank of Nigeria) should ensure that Microfinance, Bank loans are extended to the poor without too

much strict deposit condition. However, the interest rate that will be charged on the loans should be lower than

that of commercial banks to enable them to be able to repay both interest and money borrowed and the repayment should include a grace period and reasonable schedule instead of weekly payment that is commonly

found among the Microfinance Bank.

References [1]. Adebola, O (2001) Judicial Administrative System and Microfinance policy in Nigeria, a textbook on Microfinance Bank, 1st

edition pages 121-133, Macmillian press limited, Nigeria.

[2]. Adeyemi, K. S. (2008). Institutional reforms for efficient microfinance operations in Nigeria. Central Bank of Nigeria Bullion,

32(1), 26-34.

[3]. Adewole E.A. (2008), The Contribution of Micro-Finance Bank to the Development of Nigerian Economy. An Unpublished

MBA Thesis, LAUTECH .

[4]. Armendariz de Aghion and Morduch, (2005) The Economics of Microfinance Cambridge M.A. The MIT Press Pg.14

[5]. Anyanwu, C.M (2004:5) Microfinance Instistutions in Nigeria policy, practice and potentials‟ Paper presented at the G24

workshop on constrictions to Growth in Sub Sahara, Africa, Pretoria, South Africa, November. Awoseyila, A. P. (1999).

[6]. The dimension of poverty in Nigeria (spatial, sectoral, gender, occupational, etc.). Central Bank of Nigeria Bullion, 23(4), 31-39

[7]. Ajayi, O.A. (2005) Role of Microfinance bank on small and medium enterprises in Nigeria, a Journal of social sciences

university of Lagos, Volume 4 pages 133-141, University of Lagos Press, Limited, Nigeria.

[8]. Aku, P.S; Ibrahim, M.T and Bulus, Y.D. (1997) Perspective on poverty Alleviation Strategies in Nigeria. Proceedings of the

Nigeria Economic Society, Ibadan.

[9]. Akanji O.O (2001), A paper presented on „‟Micro finance as a strategy for poverty reduction” Macmillan press publication page

4-10 (2001).

[10]. Amaratunga, D., Baldry, D., Sarshar, M. and Newton, R (2002), “Quantitative and qualitative research in the built environment”,

Work Study, Vol. 51, No.1.

[11]. Anyanwu C .M. (2004), A paper presented on “Micro finance institution in Nigeria: Police, practical and potential”, University

of Lagos Publication2004 page 4-12(2004)

[12]. Asa and Balogun A.W (1997),” Entrepreneurship Development Programme, A social science journal, page-5-10, topphill press

publication 1997.

[13]. Balogun, E. D. (1999). Analyzing poverty: Concepts and methods. Central Bank of Nigeria Bullion 23(4), 11-16.

[14]. Bamisile, A.S (2006) “Developing a long term sustainable microfinance sector in Nigeria: The way forward. Paper presented at

the mall enterprises educational promotion: Network (SEEP) Annual General meeting, Washington D.C Access (12/03/10).

[15]. Beranbach, Guzman, Gierameen, Hoit (1994) Group peer pressure contribution, a textbook, 6th edition, page 66-117 Grawhill

press limited, 1994.

[16]. Brody (2004) Micro finance a key strategy in reaching the millennium Development goal, a textbook 3rd edition pages 22-29,

Macgraw Publication limited, Sweden.

[17]. Burham M.(2005) A new micro finance Era, Ankasa Mlaysia Journa, vol 177,No 1 page 52-54, a university of Mallaya

publication.

[18]. Central bank of Nigeria (2005) Micro Finance Policy Regulation a Supervisory Framework of Nigeria.

[19]. Calescene (2005) High transaction cost and volume of Loans disbursement, a presentation of Association of Management

Student of University of Ghana, Ghana.

[20]. Chowdbury and Bhuiya (2004) Contribution Women in Loan disbursetment, a textbook, 1st edition, pages 334-383, Millwall

press limited, Togo.

[21]. Chowdhury, Mosley and Simanowitz (2004) Microfinance and social objectives of financial services, a Journal of University of

Lundbery, Social Sciences, Vol 4, pages 131-211, Swedish press limited, Sweden.

[22]. Chittaging District of Bangladesh, unpublished Master Thesis. Department of Business Administration. Accessed 13 -03 -10.

Convoy O (2003) micro finance success in Nigeria, A Macmillan press publication, 2003.

[23]. Dichter (1999) The Microfinance decade in Tailand, a presentation of Tailand association of Managers. Tailand publication

limited, Tailand.

[24]. Egwuatu, B. S. C. (2008). Reducing poverty through better credit delivery: The Asian experience Central Bank ofNigeria

Bullion, 32(1), 8-16 Ehigiamusoe, G. (2008). The role of microfinance institutions in the economic development of Nigeria.

Central Bank of Nigeria Bullion, 32(1), 17-24.

[25]. Englama, A. & Bamidele, A. (1997). Measurement issues in poverty. In Poverty Alleviation in Nigeria, Selected Papers for the

1997 Annual Conference of the Nigerian Economics Society (pp. 141-156).

[26]. Enugu Forum, (2006), impact of micro finance in Enugu State, Ebano press, an Enuge State university publication, Nigeria.

[27]. Fisher and Sriran (2002) saving and credit toward development in Sweden, a university of Lund publication, 4th edition, page

107-132, Lund university press Limited Sweden.

Impact Of Microfinance Bank On Standard Of Living Of Hairdresser In Oshodi-Isolo Local

www.iosrjournals.org 34 | Page

[28]. Global Development Research center, (2005) Loan with collateral, a textbook, 3rd edition page 66-103 GDRC press Limited,

Nigeria.

[29]. Grameen (1994 & 2000) Rotating Savings band Credit Allowance, a presentation on the woman savings initiative in Belgium,

Belg press limited, Belgium.

[30]. Guzman (1994) Pressure group peering in India, a presentation on international Pressure group association, Indiana press limited,

India

[31]. Ghalib, A.K (2007) Measuring the impact of microfinance intervention: A conceptual framework of social impact assessment

(Impact Assessment research centre (IARC) University of Manchester IARC working papers series No 24/2009

[32]. Hossain, F. (2002) Small Loan, Big Claims Journal of Foreign Policy, Vol 8 No. 5, Pp, 24- 26.

[33]. Harper, A (2002) saving and credit toward development in Sweden, a university of Lund Publication, 4th edition page 107-132,

Lund university press limited Sweden.

[34]. Hastemi (2003) Microfinance, a critical factor for development, a Journal of University of Hashamila, department of banking and

finance, Vol 3, page 111-142, Indian press limited, India.

[35]. Havers. A (1999) Microfinance Institution the cost and the benefit analysis, a textbook, 3rd

edition, pages 35-61, Millwall press

limited Newyork, U.S.A.

[36]. Holt, O. (1994) Non Governmental Organistion and financial Service delivery, a Journal of History and international relations of

University of Lagos, Vol 4 pages 57-68, GTBM press limited, London.

[37]. Helme (2001) Broad range financial Services through Microfinance bank, 2nd edition pages 44- 51, Macgrawhill Press limited,

Kinshasha.

[38]. Hulme and Mosle (1996)Micro finance and poverty in Africal, a journal of Africal journal consortium, vol 3 page 131 -162,

Africa journal press, Kinshasha.

[39]. Jeffery Scahs (2005) Population of Children in Bangladeshi a presentation of central bank of Bangladeshi, CBB Publication

limited, Bangladeshi.

[40]. Johnson (2004) Women participation in Microfinance project, a Journal of University of Jos, Social Sciences Vol 3, Page 1-5,

BMT press limited, Nigeria.

[41]. Johnson, Rogaly, K. (1997) microfinance and its impact on small and medium entarprises in Nigeria, a publication of social

science, university of Jos, Vol 2, page 33-49 University press Ibadan, Nigeria.

[42]. Kabeer .M (2003) Social impact assessment on Organisation performance, a Journal of India Economist Association, Indian

press limited,Indian.

[43]. Kasali T.A (2006) Financing small and medium scale industries for economic recovery. Journal of management and enterprise

Development. Vol 3 No 2.

[44]. Kehinde, O.J. (2006), Poverty Alleviation Strategies and the Challenges of Government in Nigeria. The way forward from

Legion of failed Policies, International Journal of social and policy Issues, Vol 4, No 1 and 2.

[45]. Kirkpatrick, C.H. Clarke R. Charles P (2003) Handbook on Development policy and management Edward Elgar publishing.,

[46]. Lashley, J.G (2004), Micro finance and poverty Alleviation in the Caribbea Journal of Micro Finance, Vol. 6, No 1, Pg 83-94.

[47]. Lawal, D.G (2005) Microfinance bank and Small Scale industry in Tanzania, Journal of University of Jos, Social sciences,

University of Ibadan Press Limited, Nigeria.

[48]. Ledger Wood(1999) Savings and Credit of small and Medium Scale enterprises in Sweden, a publication of Sweden Business

School, Vol 4 pages 161-182, Sweden Business School press limited, Sweden.

[49]. Ledgerwood, O. (1999) Loan disbursement in Belgiurnm a textbook, 2nd edition, page 142-171, Woodhill press limited 1999.

[50]. Levitsky, (1997) Banks and developing Countries, a publication of Rusian School of Economics,

[51]. Vol 4, pages 88-112, Levtschool press limited, Rusian.

[52]. Lindenbery M. (2002) Social Wellberg of a Community, the problems and prospects a textbook, 2nd edition, pages 299-304,

Wakhill publisher, limited,Ghana.

[53]. Little et al (2003) Microfinance, Income and Asset, a textbook on Microfinance, 4th edition, pages 31- 38, Moshprime press

limited, London.

[54]. Littlefield and Rosenbery(2004) Analysis of financial services sector in an Economy, Journal of Sweden business School, Vol 3,

page 44-81, Sweden press limited, Sweden.

[55]. Marko Wski (2002) Financial Services to large and how income earners, A textbook, 1st edition, pages 99-117 Macgrawhill

publication limited, Netherland.

[56]. Mc Gregor et al (2000) Social and Economic impact of labour market. A textbook, 2nd edition pages 39-61, Macgraw press

limited, England.

[57]. Mix M. (2005) Microfinance and its activities, Jurblin Publication page 50-88, university of New York press 2005.

[58]. Mosedale (2003) Loan Empowerment, and its importance, a textbook, 3rd edition, pages 1-9, Macgraw publication limited,

Kenyan.

[59]. Mohammad A.K and Mohammed, A.R (2007) Impact of Micro Finance on Living Standards, Empowerment and Poverty

Alleviation of poor people. A case study of Micro Finance in Mohundra, Katherine S. Haddad, S (2005) women‟s interlaced

freedoms a framework linking micro credit participation and Health “Pg 363

[60]. Mou, I.K (2007) Poverty, the challenges, the Imperatives (Zenith Economic Quaterly), vol 2, No 12.

[61]. Murray, U and Boros, R (2002) “ A Guide to Gender Sensitive Micro Finance”The socio- economic and Gender Analysis

(SEAGA) Programmes F.A.O

[62]. Navajas et al (2000) loans and economic development a textbook, 3rd edition page 113-161, Fresh wood press limited, France.

[63]. Neirh, M (2000) Banks and Loan disbursement a textbook, 2nd edition, pages 22-55, Macgraw Hill press limited, Sweden.

[64]. Noponen O. (2005) micro finance in broader perspective, a textbook, 2nd edition, page 88-142, Grawhill press Limited, Belgium.

[65]. Odoko, F. O. (2008). Beyond finance: Strategies for poverty reduction in Nigeria. Central Bank of Nigeria Bullion,31(1), 35-36.

[66]. Okpara, G. C. (1990). Informal financial system in economic development: The case of Nigeria. In I. C. Okonkwo et al (Eds.),

Issues in National Development (pp. 260-268).

[67]. Okpara, G. C.(2009) A Synthesis of the Critical Factors Affecting Performance of the Nigerian Banking System. European

Journal of Economics, Finance and Administrative Sciences, Issue 17:34-44.

[68]. Okumadewa, F. (1999). International agencies response to poverty situation in Nigeria. Central Bank of Nigeria Bullion,23(4),

66-70.

[69]. Oladunni, E. B. I. (1999). The dimension of poverty in Nigeria: Spatial, sectoral, gender, et al. Central Bank of Nigeria Bullion,

23(4) :17-30

[70]. Olaitan, M. A. (2001). Emerging issues on micro and rural financing in Nigeria. Central Bank of Nigeria Bullion 25(1), 64-71.

Impact Of Microfinance Bank On Standard Of Living Of Hairdresser In Oshodi-Isolo Local

www.iosrjournals.org 35 | Page

[71]. Okio credit (2005) Non credit financial services and Micro credit in Nigeria, a textbook, 2nd

endition pages 131-142,

Bolubestway Press limited, Nigeria.

[72]. Olowookere (2005) Small and Medium scale enterprises financing in the world, a textbook of SMSs financing pages 44-72, 2nd

edition, Multiple Publisher, Lagos, Nigeria.

[73]. Osmani (1998) Impact of credit and Bank performance, a presentation of Management School of Ghana, Macmillan press

publication, Ghana.

[74]. Osuala. (1993) Research methology in focus, a textbook on research methodology, pages 66- 102, Macmillian press limited,

Nigeria.

[75]. Otere, A (1999) The provision of financial services to low Income and self employed. A presentation workshop at Microfinance

activities in Nigeria, Macmilian press limited, Nigeria.

[76]. Otero A.O (1999), rovision of financial service a microfinance issue, university of Ibadan publication, sixth edition, page 66-110,

university of press, 1999.

[77]. Out et al (2003) The Pratice of Microfinance institutions, a presentation of Management students association of University of

Calabar, Macmilian Press limited, Nigeria.

[78]. Rigaly (1996) Major fault of Microfinance institution a textbook on Microfinance, 1st edition pages 34- 61, Wakhill publisher,

limited, Ghana.

[79]. Robinson A. (2001) Microfinance development in Africa, a broad perspectives, Michill college of social science journal third

edition, college press, South Africa, 2001.

[80]. Scheiner and Colomber (2001) microfinance bank, an attempt to improve access to small loan for poor. Macgraw journal, 10th

edition, macgraw press, 2001.

[81]. Schreiner and Combat (2001) Analysis of Microfinance, a presentation on the way forwards in the development of Microfinance

in Belgium School of Management study, Bell publisher limited, Belgium.

[82]. Sinha (1998) development and small and medium enterprises in Nigeria, a textbook in small scale management, page 122-136,

Macmillan press limited Nigeria.

[83]. Sinha (1998) Microcredit and Small loan disbursement a textbook, 3rd endition pages 53-59, Millwall Publication limited, China.

[84]. Sowunmi, O.A (2009) Microfinance Institute in broader Knowledge, a textbook on Microfinance, 1s edition pages 39-43,

University Press Ibadan.

[85]. Thomas, F (2004) Beyond Micro credit, putting development bank India, SW publication page 401- 409, university publication

press India 2004.

[86]. Von Pischke (1999) The survival of Microfinance Institution a textbook, 1st edition, pages 64-84, Poshken press limited

publication, Rusian.

[87]. UNCTAD(1995,2001,SBA,2000) Access to finance of SMES, a UNCTAD Presentation document, Vol 4 pages 108-121,

UNCTAD publication limited.

[88]. United Nations Development Programme [UNDP]. (1996). Human development indices. New York, Oxford University Press.

[89]. UNDF (2004) Financial Services to the poor, a blue print of UNDF, 2004, UNDF Publication limited.

[90]. Ukwu, U.I (2002) Towards Effective poverty Eradication Strategies NCEMA UNDP (2007) Human Development Report 2007-

2008, United Nation,Accessed 15 -10 -2009.

[91]. Wright, O. Gremeen Bank (2000) Micro finance tools as a way forward for small scale industry, in Africa, a journal of African

development economy, vol 4, page 222-316, African consorting press limited, Nairobi, Kenya. World Bank Retrieved on Nov

27:2009 from World bank website:

[92]. http://www.worldbank.org/nigeria). Walter (2002) Microfinance a social mission of analysis, a presentation of Chartered

Institutes of bankers, Nigeria, CIBN press limited.

[93]. Weirch, A(2000) Information Technology and portfolio management, a textbook, 3rd edition pages 33-69, Macgrawhill press

limited, Sweden.

[94]. World Bank. (1990). World development report 1990: Poverty. Oxford: Oxford University.

[95]. World Bnnk (1993) Poverty Reduction Handbook. The World Bank, Washington, D.C.

[96]. Yeshiareg, D (2009): Promoting Women‟s Economic Empowerment in Africa http://www.org/aee/documents Yeshiareg %20

Dejane pdf.

[97]. Yunus, Mohammad (1999) “Banker to the Poor-Microlending and the Battle against World Poverty.