ifrs news - grant thornton australia · international ifrs team. ifrs news offers a ... in...

TRANSCRIPT

IFRS News

Welcome to IFRS News – a quarterly update fromthe Grant ThorntonInternational IFRS team.IFRS News offers asummary of the moresignificant developments in International FinancialReporting Standards(IFRS) along with insightsinto topical issues andcomments and views from the Grant ThorntonInternational IFRS team.

Our first edition of 2013 starts with alook at the IASB’s recently publishedexception from consolidation forinvestment entities (itself the subject of aDecember 2012 special edition of IFRSNews) before looking at a host ofExposure Drafts that have been issued.

We go on to IFRS-related news atGrant Thornton before turning to amore general round-up of financialreporting developments relevant toIFRS preparers. We finish with theimplementation dates of newerStandards that are not yet mandatoryand a list of IASB publications that areout for comment.

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates

IFRS News Quarter 1 2013 1

Open for comment

IASB issues exception from consolidation for investment entities

At the end of October, the IASB issued‘Investment Entities – Amendments toIFRS 10, IFRS 12 and IAS 27’ (theAmendments), creating an exception forinvestment entities to the well-established principle that a parent entitymust consolidate all its subsidiaries.

The Amendments define aninvestment entity (see box) and providedetailed application guidance on thatdefinition. Private equity organisations,venture capital organisations, pensionfunds, sovereign wealth funds and otherinvestment funds are likely to beparticularly interested in theAmendments.

Entities that meet the definition arerequired to measure investments that arecontrolling interests in another entity (inother words, subsidiaries) at fair valuethrough profit or loss instead ofconsolidating them.

adopting the consolidation exceptionearly could spare affected entitiesmuch of the time and effort they will otherwise need to spend onreassessing control conclusions under IFRS 10

The publication is a response to concernsraised by many commentators thatconsolidating the financial statements ofan investment entity and its investees doesnot provide the most useful information,namely information on the value of theentity’s investments. The tablesummarises the key features of theAmendments.

IFRS News Quarter 1 2013 2

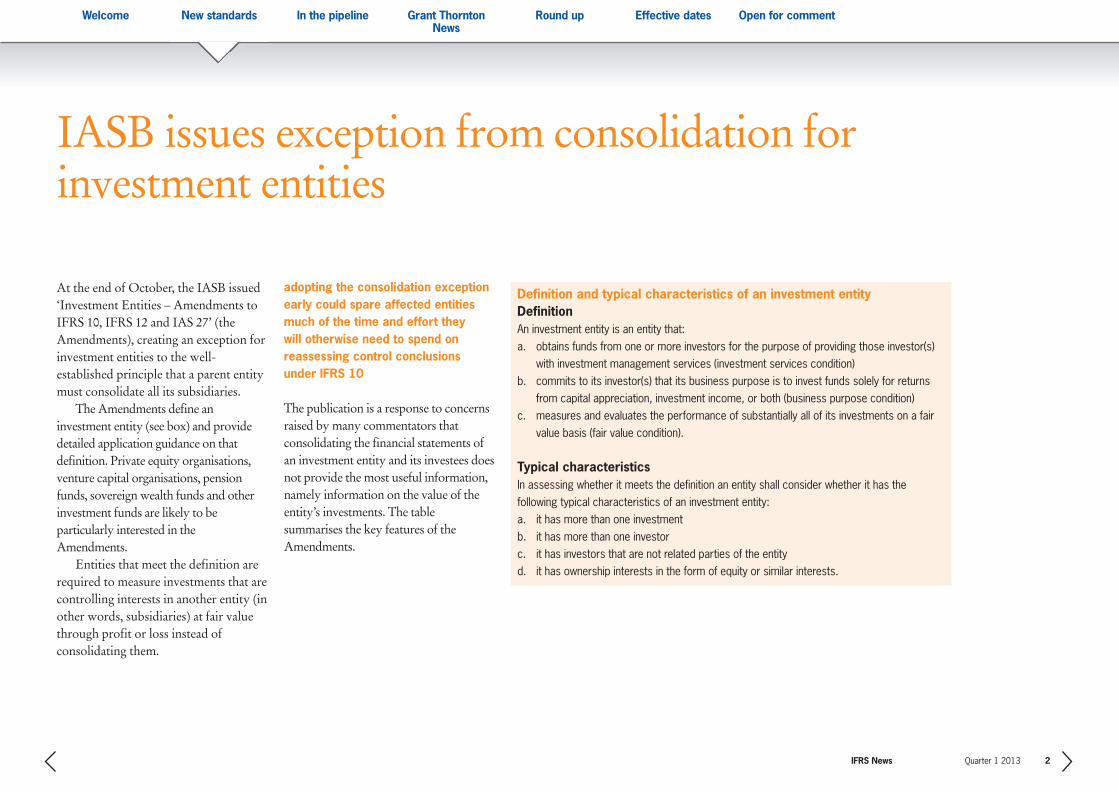

Definition and typical characteristics of an investment entity Definition An investment entity is an entity that:

a. obtains funds from one or more investors for the purpose of providing those investor(s)

with investment management services (investment services condition)

b. commits to its investor(s) that its business purpose is to invest funds solely for returns

from capital appreciation, investment income, or both (business purpose condition)

c. measures and evaluates the performance of substantially all of its investments on a fair

value basis (fair value condition).

Typical characteristics In assessing whether it meets the definition an entity shall consider whether it has the

following typical characteristics of an investment entity:

a. it has more than one investment

b. it has more than one investor

c. it has investors that are not related parties of the entity

d. it has ownership interests in the form of equity or similar interests.

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

The Amendments are effective forannual periods beginning on or after 1 January 2014, one year later than IFRS 10’s effective date. The IASB hashowever permitted early adoption inorder to allow investment entities toapply the Amendments at the same time they first apply the rest ofIFRS 10. Adopting the consolidationexception early could spare affectedentities from much of the time and effortthey would otherwise need to spend onreassessing their control conclusionsunder IFRS 10’s new requirements.

IFRS News Quarter 1 2013 3

The Amendments at a glance

Summary

Who’s affected? Entities that: • meet the new definition of ‘investment entity’ • hold one or more investments that are controlling interests in another entity

What is the impact? Investment entities will: • no longer consolidate investments that are controlling interests in another entity • make additional disclosures about these investments

Other key points • a non-investment parent entity that controls an investment entity will continue to consolidate its subsidiaries (the consolidation exemption does not ‘roll up’)

• an investment entity’s service subsidiaries (subsidiaries that are not ‘investments’) will continue to be consolidated

• if an investment entity has no non-investment subsidiaries it presents separate financial statements as its only financial statements

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

IASB proposes limited amendments to IFRS 9’sclassification and measurement provisions

The IASB has published an ExposureDraft titled ‘Classification andMeasurement: Limited Amendments to IFRS 9 – Proposed amendments to IFRS 9 (2010)’.

The table sets out the main changesproposed by the Exposure Draft. Whilethe proposed amendments are portrayedas limited in nature, they propose theintroduction of a fair value throughother comprehensive income (OCI)measurement category for debtinstruments that would be based on anentity’s business model – a major changeto IFRS 9’s current requirements.

IFRS News Quarter 1 2013 4

Issue Background Summary of proposals Summary of proposals

The Exposure Draft proposes:

• debt instruments held within a business model in which assets are managed both in order

to collect contractual cash flows and for sale should be mandatorily measured at fair

value through OCI

• interest revenue, credit impairment and any gain or loss on derecognition would be

recognised in profit or loss; all other gains or losses would be recognised in OCI

The Exposure Draft also contains:

• application guidance on how to determine whether the business model is to manage

assets both to collect contractual cash flows and to sell

• clarifications to the application guidance in IFRS 9 on what is a ‘hold to collect’ business

model

The Exposure Draft proposes amending the application guidance in IFRS 9 to clarify that:

• where a financial asset contains such an interest rate mismatch feature or leverage, an

entity shall assess the modification to determine whether the contractual cash flows

represent solely payments of principal and interest. This is done by reference to cash

flows on a ‘benchmark’ instrument

• if the modification could result in contractual cash flows that are more than insignificantly

different from the benchmark cash flows, the contractual cash flows are not solely

payments of principal and interest

Background

The proposals are a reaction to concerns from constituents, in

particular:

• insurers, who are concerned that IFRS 9 would result in an

accounting mismatch between some of their insurance

liabilities and the assets held to back them

• some banks, who are concerned that their liquidity

portfolios would be forced into the FVTPL category under

the existing version of IFRS 9

The proposals have been developed with the aim of providing

relief for certain types of financial assets which would be

classified at fair value under the current requirements:

• in particular, questions have been raised about financial

assets that contain interest rate mismatch features (ie the

interest rate is reset but the frequency of the reset does

not match the tenor of the interest rate).

• this has caused problems in certain regulated markets

where interest rates are set by a regulator or government

agency without regard to a market-based link between

interest rates and maturities, one prominent example

being Chinese mortgage bonds

Introduction of a ‘fair

value through other

comprehensive income’

measurement category

Clarification of

application issues

relating to the

‘contractual cash flow’

test

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

IFRS News Quarter 1 2013 5

Issue Background Summary of proposals Summary of proposals

• the Exposure Draft proposes that, going forward, only the completed version of IFRS 9

(ie including the Classification and Measurement, Impairment and General Hedge

Accounting chapters) can be newly applied prior to the mandatory effective date

• the proposed amendment would become effective six months after the completed

version of IFRS 9 is issued

• notwithstanding the proposed transition requirement above, once IFRS 9 is completed,

an entity will be permitted to early apply only the ‘own credit’ provisions in IFRS 9, which

require an entity to present in other comprehensive income fair value gains or losses

attributable to changes in the credit risk of financial liabilities designated as measured

at fair value through profit or loss, without otherwise changing the classification and

measurement of financial instruments.

Background

• at present, more than one version of IFRS 9 can be applied

early

• this means that entities can apply either the classification

and measurement requirements for financial assets only

(ie IFRS 9 issued in 2009) or the classification and

measurement requirements for both financial liabilities and

financial assets (ie IFRS 9 issued in 2010)

• in 2010, the IASB amended IFRS 9 to require the amount of

the change in fair value due to changes in the entity’s own

credit risk to be presented in other comprehensive income

• the change addressed the counter-intuitive way in which a

company in financial trouble was previously able to

recognise a gain based on its theoretical ability to buy

back its own debt at a reduced cost

Early adoption

Presentation of ‘own

credit’ gains or losses

on financial liabilities

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

Annual improvements proposals published

Proposed amendments addressnon-urgent (but necessary) minoramendmentsThe IASB has published an ExposureDraft ‘Annual Improvements to IFRSs2011–2013 Cycle’ which proposesminor amendments to four IFRSs. The proposals are the latest under theIASB’s annual improvements project, a process for making non-urgent, butnecessary, minor amendments to IFRSs.A summary of the issues, which reflectissues discussed by the IASB in a project cycle that began in 2011, is set out in the table.

IFRS News Quarter 1 2013 6

Proposals for 2011-2013 Annual Improvements Cycle

Standard affected Summary of proposed change

• amends the Basis for Conclusions to clarify that if a new IFRS is not yet mandatory but permits early

application, that IFRS is permitted, but not required, to be applied in the entity’s first IFRS financial

statements

• consequently, if a first-time adopter chooses to early apply a new IFRS, that new IFRS will be applied

throughout the periods presented in its first financial statements, unless IFRS 1 provides an exemption

or an exception that permits or requires otherwise

• amends the scope of IFRS 3 to exclude the formation of all types of joint arrangements

• clarifies that the scope exception only applies to the financial statements of the joint venture or the joint

operation itself

• amends the portfolio exception in IFRS 13 (the exception that permits an entity to measure the fair value

of a group of financial assets and financial liabilities on a net basis if the entity manages that group of

financial assets and financial liabilities on the basis of its net exposure to either market risk or credit risk) to

clarify that the exception applies to all contracts within the scope of IAS 39 ‘Financial Instruments:

Recognition and Measurement’ or IFRS 9 ‘Financial Instruments’, regardless of whether they meet the

definitions of financial assets or financial liabilities as defined in IAS 32 ‘Financial Instruments: Presentation’

• amends IAS 40 to clarify that:

a. judgement is required to determine whether the acquisition of investment property is the acquisition

of an asset, a group of assets or a business combination in the scope of IFRS 3

b. that this judgement is not based on paragraphs 7–15 of IAS 40 but is instead based on the guidance

in IFRS 3

Issue

Clarification of the meaning of

‘each IFRS effective at the end

of an entity’s first IFRS reporting

period’

Scope of IFRS 3

Scope of portfolio exception

The interrelationship of IFRS 3

and IAS 40 when classifying

investment property or

owner-occupied property

IFRS 1 First-time Adoption of

International Financial Reporting

Standards

IFRS 3 Business Combinations

IFRS 13 Fair Value

Measurement

IAS 40 Investment Property

Grant Thornton InternationalcommentOverall the changes are uncontroversial.

We do however have some concerns over

the proposed amendment to IAS 40, in

particular whether it would force even a

simple purchase of a single property with

in-place tenants and associated services

into the scope of IFRS 3.

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

Sale or contribution of assets between an investor andits associate or joint venture

The IASB has issued the Exposure Draft‘Sale or Contribution of Assets betweenan Investor and its Associate or JointVenture’. The Exposure Draft proposesamendments to IFRS 10 ‘ConsolidatedFinancial Statements’ and IAS 28‘Investments in Associates and JointVentures (Revised 2011)’.

The objective of the proposedamendments is to address anacknowledged inconsistency betweenthe requirements in IFRS 10 and those in IAS 28 in dealing with the sale orcontribution of a subsidiary.

The inconsistency stemmedoriginally from a conflict between therequirements of IAS 27 ‘Consolidatedand Separate Financial Statements(Revised 2008)’ and SIC-13 ‘JointlyControlled Entities – Non-Monetary

Contributions by Venturers’. While IAS 27 required the full gain or loss tobe recognised on the loss of control of asubsidiary, SIC-13 required a partial gain or loss recognition in transactionsbetween an investor and its associate or joint venture. Although IFRS 10supersedes IAS 27, and IAS 28 (2011)supersedes both IAS 28 and SIC-13, theconflict remains.

The Exposure Draft proposes torectify this problem by amending IAS 28 (2011) so that: • the current requirements for the

partial gain or loss recognition fortransactions between an investor andits associate or joint venture onlyapply to the gain or loss resultingfrom the sale or contribution ofassets that do not constitute abusiness, as defined in IFRS 3

IFRS News Quarter 1 2013 7

• the gain or loss from the sale orcontribution of assets that constitutea business between an investor andits associate or joint venture isrecognised in full

• when determining whether assetsthat are sold or contributedconstitute a business, an entity shallconsider whether the sale orcontribution of those assets is part ofmultiple arrangements that shouldbe accounted for as a singletransaction.

The Exposure Draft would also amendIFRS 10 so that:• the gain or loss resulting from the

sale or contribution of a subsidiarythat does not constitute a businessbetween an investor and its associateor joint venture is recognised only tothe extent of the unrelated investors’interests in the associate or jointventure.

The IASB proposes that theamendments would be appliedprospectively to sales or contributionsoccurring in annual periods beginningon or after the date that the proposedamendments would become effective(yet to be determined).

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

The IASB has finished its publicconsultation on its future agenda(initially reported on in the Q4 2011edition of IFRS News) by releasing aFeedback Statement that maps out itsfuture priorities.

The Feedback Statement sets out fivebroad themes that emerged from theconsultation in relation to the strategicdirection and overall balance of theIASB’s future work programme:

• respondents asked that a decade ofalmost continuous change in theIASB’s financial reportingrequirements should be followed bya period of relative calm

• there was unanimous support for theIASB to prioritise work on theConceptual Framework, in order toprovide a consistent and practicalbasis for standard setting

• the IASB was asked to make sometargeted improvements that respondto the needs of new adopters ofIFRSs

IFRS News Quarter 1 2013 8

• the IASB was asked to pay greaterattention to the implementation andmaintenance of its Standards

• the IASB was asked to improve theway in which it develops newStandards, by conducting morerigorous cost-benefit analysis andproblem definition earlier on in thestandard setting process.

IASB maps out future priorities following conclusionof public consultation

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

IASB looks to clarify acceptable methods ofdepreciation and amortisation

The IASB has issued the ‘ExposureDraft ‘Clarification of AcceptableMethods of Depreciation andAmortisation’. The proposedamendment:• seeks to clarify that when applying

the guidance in IAS 16.62 and IAS 38.98, a revenue-based methodshould not be used to calculate thecharge for depreciation and/oramortisation, because that methodreflects a pattern of economic benefitsbeing generated from the asset, ratherthan the expected pattern ofconsumption of the future economicbenefits embodied in the asset

• provides further guidance in theapplication of the diminishingbalance method.

IFRS News Quarter 1 2013 9

Grant Thornton InternationalcommentWe agree with the proposal to prohibit the

use of depreciation or amortisation

methods that are based on actual revenue

generated. We feel however that the final

amendments should acknowledge that for

some assets the expected future pattern of

revenue generation can serve as a valid

proxy for the expected consumption of

economic benefits in some circumstances.

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

IFRS News Quarter 1 2013 10

Recoverable amount disclosures for non-financial assets(proposed amendments to IAS 36)

The IASB has published an ExposureDraft of proposed modifications to thedisclosures in IAS 36 ‘Impairment ofAssets’ for the measurement of therecoverable amount of impaired assets.

Those disclosure requirements wereintroduced by IFRS 13 ‘Fair ValueMeasurement’. The IASB has noticedhowever that some of the amendmentsmade in introducing those requirementshave resulted in the requirement beingmore broadly applicable than the IASBintended. The Exposure Draft aims torectify this problem. In view of therelatively uncontroversial nature of theproposals, the Exposure Draft has asixty day comment period ending on 19 March.

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

IFRS News Quarter 1 2013 11

IASB proposes amendment to IFRS 11The IASB has issued ‘Acquisition of anInterest in a Joint Operation (Proposedamendment to IFRS 11). The ExposureDraft has been issued because neitherIFRS 11 ‘Joint Arrangements’ nor itspredecessor standard IAS 31 ‘Interests inJoint Ventures’ provided guidance onthe accounting by a joint operator forthe acquisition of an interest in a jointoperation in which the activity of thejoint operation constitutes a business. Asa result, significant diversity in practicehas arisen in venturers’ accounting forsuch transactions.

The Exposure Draft looks to remedythis problem. The proposedamendment:• changes IFRS 11 and IFRS 1 so that

a joint operator accounting for theacquisition of an interest in a jointoperation in which the activity of the joint operation constitutes abusiness, applies the relevantprinciples for business combinationsaccounting in IFRS 3 and otherStandards and discloses the relevantinformation required by thoseStandards for business combinations

• applies to the acquisition of aninterest in an existing joint operationand the acquisition of an interest in ajoint operation on its formation.

The IASB proposes that theamendments would be appliedprospectively to acquisitions of interestsin joint operations in which the activityof the joint operation constitutes abusiness, on or after the (yet to bedetermined) effective date of theproposed amendment.

Acquisition of an interest in a joint operation

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

Proposed amendments to IAS 28

The IASB has published the ExposureDraft ‘Equity Method: Share of OtherNet Asset Changes’. The aim of theExposure Draft is to provide additionalguidance to IAS 28 (revised 2011) on theapplication of the equity method (underwhich an investment is initiallyrecognised at cost and subsequentlyadjusted to reflect the change in theinvestor’s share of the investee’s netassets). The Exposure Draft proposes todo this by amending IAS 28 so that:

• an investor should recognise in theinvestor’s equity its share of thechanges in the net assets of theinvestee that are not recognised inprofit or loss or OCI of the investee,and that are not distributionsreceived

• that an investor shall reclassify toprofit or loss the cumulative amountof equity that the investor hadpreviously recognised when theinvestor discontinues the use of theequity method.

IFRS News Quarter 1 2013 12

Grant Thornton InternationalcommentWe welcome clarification of the issues

addressed in the Exposure Draft. We do

however have some concerns over the

effect of the proposals on transactions that

change an investor’s proportionate

ownership interest, and also on an

investor’s accounting for its share of an

equity-accounted investee’s equity-settled

share-based payment plan. We will look to

discuss these concerns in our comment

letter on the Exposure Draft.

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

Special edition of IFRS News on investment entities

The Grant Thornton International IFRSteam has published a special edition ofIFRS News on the IASB publication‘Investment Entities – Amendments toIFRS 10, IFRS 12, and IAS 27’ (featuredon page 2 of this newsletter).

The special edition takes readersthrough the key features of theconsolidation exception for investmententities and gives practical insights intohow its requirements may affect entities.It will be of particular interest to privateequity organisations, venture capitalorganisations, pension funds, sovereignwealth funds and other investmentfunds.

To obtain a copy of the specialedition, please get in touch with theIFRS contact in your local GrantThornton office.

IFRS News Quarter 1 2013 13

IFRS NewsSpecial EditionDecember 2012

The IASB has published ‘Investment Entities –Amendments to IFRS 10, IFRS 12 and IAS 27’ (theAmendments). The Amendments introduce an exception for investment entities to the well-established principle that a parent entity mustconsolidate all its subsidiaries. The Amendments: • define the term ‘investment entity’ and provide

supporting guidance• require investment entities to measure

investments in the form of controlling interestsin another entity (in other words, subsidiaries) at fair value through profit or loss in accordancewith IFRS 9 ‘Financial Instruments’ (or IAS 39‘Financial Instruments: Recognition andMeasurement’) instead of consolidating them

• specify disclosure requirements for entities thatapply the exception.

This special edition of IFRS News explains the keyfeatures of the Amendments and provides practicalinsights into their application and impact.

“Many commentators have long believed that consolidating thefinancial statements of an investment entity and its investeesdoes not provide the most useful information. Their concern isthat consolidation does not reflect the investment businessmodel and makes it harder for investors to understand whatthey are most interested in – the value of the entity’s investments.

We share these concerns and therefore welcome theseAmendments. Although consolidation normally provides themost relevant and useful information for a group, we believethere is a class of investment entity for which fair valueaccounting is significantly more useful. The IASB has workedhard to identify this class appropriately – aiming for a robustdefinition that still allows some flexibility and scope forreasonable judgement.

The timing of publication is significant given that IFRS 10 ‘Consolidated Financial Statements’ is effective from1 January 2013. The consolidation exception will have a hugeimpact on affected entities and, if adopted early, could sparethem from much time and effort on reassessing controlconclusions under IFRS 10.”

Andrew Watchman Executive Director of International Financial Reporting

A consolidation exception forinvestment entities

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

IFRS News Quarter 1 2013 14

Grant Thornton International guide to navigating thechanges to IFRS

The Grant Thornton International IFRSteam has published an updated versionof its guide ‘Navigating the changes toInternational Financial ReportingStandards: a briefing for Chief FinancialOfficers’.

The December 2012 edition of thepublication has been updated forchanges to International FinancialReporting Standards that have beenpublished between 1 December 2011and 30 November 2012.

The publication gives ChiefFinancial Officers a high-level awarenessof recent changes that will affectcompanies’ future financial reportingand their commercial significance. It hasbeen designed to help entities planningfor a specific financial reporting year endidentify:• changes mandatorily effective for the

first time • changes not yet effective• changes already in effect.

To obtain a copy of the publication,please get in touch with the IFRS contactin your local Grant Thornton office.

Navigating the changes to InternationalFinancial Reporting Standards: a briefing for Chief Financial Officers

DECEMBER 2012

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

IFRS News Quarter 1 2013 15

Now what? Considering IFRS for US issuers

US firm’s white paper outlines whyUS companies should not ignoreIFRS following SEC staff reportOur US member firm, Grant ThorntonLLP, has produced a white paper ‘Nowwhat? Considering IFRS for US issuers’.The paper reflects on the recent SECStaff Report on incorporating IFRS intothe US financial system and outlineswhy the SEC’s lack of a decision in thatreport does not mean that companies,either public or non-public, shouldsimply ignore IFRS.

Separately, Grant Thornton LLP haswritten to the SEC in reaction to theirStaff Report, setting out our US memberfirm’s continued belief that theoverarching goal for accounting and

financial reporting is to have a single setof high quality, globally acceptedaccounting standards and that IFRS isbest suited to be that set of standards.

The US firm’s comment letter alsodraws attention to the uncertainty in thefinancial reporting community that hasbeen created by the SEC’s delay inmaking a decision on the use of IFRS,noting that uncertainty is costly topreparers, users, investors, and others.The letter also observes that delaying adecision might also cause regulators,standard setters, and others in thefinancial reporting community in the USto have less influence in thedevelopment and application of IFRS.

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

IFRS News Quarter 1 2013 16

IFRS client presentation in Montreal, Canada

In November, Raymond Chabot GrantThornton, one of our member firms inCanada, hosted a client seminar onIFRS. The presentation, entitled ‘IFRS –the future is now!’, looked principally atthe new IFRSs on consolidation, jointarrangements and fair value which aredue to become effective in Canada.

The seminar also featured apresentation from a representative of theAutorité des Marchés Financiers (theQuebec Securities Commission) whichset out their expectations for IFRSfinancial statements in the comingreporting season. The seminar endedwith a presentation from arepresentative of the CanadianAccounting Standards Board, whosummarised the role of that Board in thecontext of applying IFRS in Canada anddiscussed the Board’s most importantcurrent projects.

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

IFRS News Quarter 1 2013 17

US white paper explores an alternative model for leasing

Our US member firm has released awhite paper ‘Rethinking the right-of-useasset’. The paper, written by John Heppand Mark Scoles, two partners in the USfirm’s Accounting PrinciplesConsultation Group, reconsiders theright-of-use asset proposed by the IASBand the US Financial AccountingStandards Board (FASB) in their originalExposure Draft ‘Leases’ issued inAugust 2010.

In the paper, which is available onthe US firm’s website(http://www.grantthornton.com), thetwo partners propose an alternativeapproach that calls for two types of leasecontracts, with classification contingenton whether the contract transferscontrol of the underlying asset to thelessee. The IASB and FASB are expectedto issue a second Exposure Draft onlease accounting in the early part of2013.

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

Spotlight on our IFRS Interpretations Group

Grant Thornton International’s IFRSInterpretations Group (IIG) consists of arepresentative from each of our memberfirms in the United States, Canada,Singapore, Australia, South Africa, India,the United Kingdom, France, Swedenand Germany as well as members of theGrant Thornton International IFRSteam. It meets in person twice a year todiscuss technical matters which arerelated to IFRS.

Each quarter we throw a spotlight onone of the members of the IIG. Thisquarter we focus on the UnitedKingdom’s representative:

Jake Green, United KingdomJake is the UK firm's director of financialreporting, having worked in itsaccounting technical department since2003. He is an active contributor to thefinancial reporting community;participating in a number of workingparties at the Institute of CharteredAccountants and attending theConfederation of British Industry’sFinancial Reporting Panel.

Jake is a keen contributor to a numberof accounting publications in the UK. Heprovides training seminars to clients andtargets of the UK firm on IFRS and otherfinancial reporting topics of interest. He isalso known for occasionally tweeting onthose topics. Twitter followers can readmore @jake_green_gtuk (the views are hisown!)

IFRS News Quarter 1 2013 18

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

Round-up

IASB turns its attention to theproblem of disclosure overloadThe IASB has responded to the growingclamour over disclosure overload infinancial statements by announcing that it isto hold a public ‘disclosure forum’ at the endof January 2013 to consider the problem.

IFRS News has featured a number ofinitiatives in recent quarters on the subject,including most recently the FASBdiscussion paper 'Disclosure Framework'and the EFRAG discussion paper 'Towardsa Disclosure Framework for the Notes'. Theforum will aim to further foster dialoguebetween preparers, auditors, regulators,users of financial statements and the IASBabout how to improve the usefulness andclarity of financial disclosures. Output fromthe forum will inform the IASB’s work on itsConceptual Framework.

IASB Chairman reiteratescommitment to its leasing projectHans Hoogervorst, has reiterated theIASB’s determination to complete itsleasing project and bring all leases ontothe balance sheet.

Speaking at the London School ofEconomics and Political Science, MrHoogervorst highlighted the extent towhich lease arrangements have becomeone of the greatest sources of off-balancesheet financing for many companies.

While acknowledging that the IASBfaces an uphill battle to overcomelobbying from vested interests, he voicedhis belief that completion of the projectwas essential if hidden leverage was to be uncovered.

IFRS Foundation issues first chapterof fair value measurementeducational materialThe IFRS Foundation has issued the first chapter of material to accompanyIFRS 13 ‘Fair Value Measurement’ underits Education Initiative.

The first chapter covers theapplication of the principles in IFRS 13when measuring the fair value ofunquoted equity instruments within thescope of IFRS 9 ‘Financial Instruments’and was developed with the assistance ofa valuation expert group.

Other chapters will be added in duecourse, the aim being for the material tocover the application of the principles inIFRS 13 across a number of topics. Thematerial has been published to assist inthe consistent application of IFRSs. It isnon-authoritative guidance however andhas not been approved by the IASB.

IFRS Foundation to create AccountingStandards Advisory ForumThe IFRS Foundation has publishedproposals to create a new advisory groupto the IASB. The main purpose of thegroup, which would consist of nationalaccounting standard-setters and regionalbodies with an interest in financialreporting, will be to provide technicaladvice and feedback to the IASB. Creationof such a group was recommended in lastyear’s Trustee’s strategy review.

IFRS News Quarter 1 2013 19

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

FASB publishes its impairmentproposalsThe US Financial Accounting StandardsBoard (FASB) has issued its impairmentproposals. Proposed AccountingStandards Update ‘Financial Instruments –Credit Losses (Subtopic 825-15)’,proposes a single ‘expected credit loss’measurement objective for therecognition of credit losses, replacing themultiple existing impairment models in USGAAP, which generally require that a lossbe ‘incurred’ before it is recognised.

Both the FASB and the IASB have beendeveloping expected loss models forimpairment of loans and other debtinstruments. Previously, the two Boardshad agreed on an approach that wouldtrack the deterioration of the credit risk ofloans and other financial assets in three‘buckets’ of severity. US preparers,auditors, investors, and regulatorsexpressed concerns about theunderstandability, operability, and

auditability of the ‘three-bucket’ creditimpairment model however, and whether itwould reflect an appropriate measure ofrisk. This led the FASB to revise itsapproach.

The key difference between the USproposals and the IASB’s expectedproposals (which are due to be publishedin the first quarter of 2013) relates to theIASB’s use of a different expected lossapproach for assets that have not yetexhibited significant deterioration in creditrisk; specifically, full recognition of anallowance for the expected credit losswould be deferred for financial assets forwhich a loss event is expected to occurbeyond 12 months. Under the FASBmodel, the entity would not limit itsestimate to losses that are expected tooccur in a particular time period; it wouldinstead always consider all availableinformation and recognise its currentestimate of cash flows not expected to becollected.

ACCA report on IFRS in the USThe Association of Chartered CertifiedAccountants (ACCA) has released a report'IFRS in the US: An investor's perspective'which discusses the findings of a surveyof US investors’ perceptions of IFRS andthe prospects for convergence.

The report finds that the generalperception among investors is that the USwill eventually adopt IFRS, and moreinvestors feel this will be beneficial for thedomestic economy than not (the report’sfindings were based on a survey of 493US-based investors). While many investorsare yet to be convinced of the merits ofthe standards, those most familiar withIFRS are very confident about the level ofdisclosures and the prospects for earlyadopters.

IFRS News Quarter 1 2013 20

ESMA announces enforcementpriorities for 2012 financialstatementsThe European Securities and MarketsAuthority (ESMA) has published a set ofpriority issues to be used by EUregulators in assessing listed companies’2012 financial statements.

The common financial reporting topics refer to the application of IFRS in relation to:• financial assets• impairment of non-financial assets• defined benefit obligations• provisions, contingent liabilities,

and contingent assets.

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

ICAEW report on the future of IFRS The Institute of Chartered Accountants ofEngland and Wales (ICAEW) has publisheda report ‘The Future of IFRS’. The reporttakes stock of the current state of IFRS,the benefits it offers and the challengesahead.

The report notes that the move toIFRS has arguably been transformationalfor international investors but emphasisesthat the organisation must continue tolisten and learn from constituents.Securing funding on a sustainable level isalso seen as an important challenge.More controversially, the report says thatit is time to end the era of convergencewith US GAAP and focus on completingsome of the IASB’s outstanding standardsprojects, such as financial instruments.

Reports on debt and cash flowdisclosureThe UK’s Financial Reporting Lab hasreleased two reports on ‘Debt terms andmaturity tables’ and ‘Operating andinvesting cash flows’.

The Financial Reporting Lab has beenset up by the UK’s Financial ReportingCouncil to improve the effectiveness ofcorporate reporting in the UK by providingan environment where investors andcompanies can come together. Much ofits work focuses on companies who useIFRS and its findings will therefore be ofinterest globally.

The two reports contain descriptionsof reporting practices that help investorsto understand debt obligations and theirrisks, and the drivers of cash flowmovements.

IVSC report on valuation uncertaintyThe International Valuation StandardsCouncil (IVSC) has released an ExposureDraft on valuation uncertainty.

The Exposure Draft has beenproduced in answer to calls from the G20(the Group of Twenty Finance Ministersand Central Bank Governors) and financialregulators around the world for improvedstandards of transparency and disclosureof valuation uncertainty factors.

The proposed guidance looks at howvaluation uncertainty can be identified,explained and disclosed in a way that isinformative to those relying on valuations.

Valuation guidance for commercialforestsThe IVSC has also published draftvaluation guidance for commercialforests. The publication is in part areaction to a lack of consistency arisingfrom the need for the tree crop to beaccounted for separately from the landunder IFRS. Particular concern has beenexpressed at the different approachesbeing taken to allocate value among the‘biological asset’, i.e. the living trees, andall the other elements that make up thetotal value of the forest. The guidance isdesigned to bring greater consistency tothis process.

IFRS News Quarter 1 2013 21

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

Effective dates of new standards and IFRIC interpretations

The table below lists new IFRSStandards and IFRIC Interpretationswith an effective date on or after 1January 2011. Companies are requiredto make certain disclosures in respect ofnew Standards and Interpretationsunder IAS 8 ‘Accounting Policies,Changes in Accounting Estimates andErrors’.

IFRS News Quarter 1 2013 22

New IFRS Standards and IFRIC Interpretations with an effective date on or after 1 January 2011

Title Full title of Standard or Interpretation Effective for accounting Early adoption permitted?

periods beginning on or after

IFRS 9 Financial Instruments 1 January 2015 Yes (extensive transitional rules apply)

IFRS 10, 12 Investment Entities (Amendments to IFRS 10, IFRS 12 and IAS 27) 1 January 2014 Yes

and IAS 27

IAS 32 Offsetting Financial Assets and Financial Liabilities (Amendments to 1 January 2014 Yes (but must also make the disclosures required by Disclosures

IAS 32) – Offsetting Financial Assets and Financial Liabilities)

IFRS 10, 11 Consolidated Financial Statements, Joint Arrangements and Disclosure of 1 January 2013 Yes

and 12 Interests in Other Entities: Transition Guidance – Amendments to IFRS 10,

IFRS 11 and IFRS 12

Various Annual Improvements 2009-2011 Cycle 1 January 2013 Yes

IFRS 1 Government Loans – Amendments to IFRS 1 1 January 2013 Yes

IFRS 7 Disclosures – Offsetting Financial Assets and Financial Liabilities 1 January 2013 Not stated (but we presume yes)

(Amendments to IFRS 7)

IFRIC 20 Stripping Costs in the Production Phase of a Surface Mine 1 January 2013 Yes

IFRS 13 Fair Value Measurement 1 January 2013 Yes

IFRS 12 Disclosure of Interests in Other Entities 1 January 2013 Yes

IFRS 11 Joint Arrangements 1 January 2013 Yes (but must apply IFRS 10, IFRS 12, IAS 27 and IAS 28 at

the same time)

IFRS 10 Consolidated Financial Statements 1 January 2013 Yes (but must apply IFRS 11, IFRS 12, IAS 27 and IAS 28 at

the same time)

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

Effective dates of new standards and IFRIC interpretations

IFRS News Quarter 1 2013 23

New IFRS Standards and IFRIC Interpretations with an effective date on or after 1 January 2011

Title Full title of Standard or Interpretation Effective for accounting Early adoption permitted?

periods beginning on or after

IAS 28 Investments in Associates and Joint Ventures 1 January 2013 Yes (but must apply IFRS 10, IFRS 11, IFRS 12 and IAS 27 at

the same time)

IAS 27 Separate Financial Statements 1 January 2013 Yes (but must apply IFRS 10, IFRS 11, IFRS 12 and IAS 28 at

the same time)

IFRS Practice Management Commentary: A framework for presentation No effective date as Not applicable

Statement non-mandatory guidance

IAS 19 Employee Benefits (Revised 2011) 1 January 2013 Yes

IAS 1 Presentation of Items of Other Comprehensive Income 1 July 2012 Yes

(Amendments to IAS 1).

IAS 12 Deferred Tax: Recovery of Underlying Assets (Amendments to IAS 12) 1 January 2012 Yes

IFRS 1 Severe Hyperinflation and Removal of Fixed Dates for 1 July 2011 Yes

First-time Adopters (Amendments to IFRS 1)

IFRS 7 Disclosures – Transfers of Financial Assets (Amendments to IFRS 7) 1 July 2011 Yes

Various Annual Improvements 2010 1 January 2011 unless otherwise Yes

stated (some are effective from

1 July 2010)

IFRIC 14 Prepayments of a Minimum Funding Requirement – Amendments to 1 January 2011 Yes

IFRIC 14

IAS 24 Related Party Disclosures 1 January 2011 Yes (either of the whole Standard or of the partial

exemption for government-related entities)

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment

Open for comment

This table lists the documents that theIASB currently has out to comment andthe comment deadline. Grant ThorntonInternational aims to respond to each ofthese publications.

IFRS News Quarter 1 2013 24

© 2013 Grant ThorntonInternational Ltd. All rightsreserved.References to “GrantThornton” are to the brandunder which the GrantThornton member firmsoperate and refer to one ormore member firms, as the context requires.Grant Thornton Internationaland the member firms arenot a worldwidepartnership. Services aredelivered independently bymember firms, which arenot responsible for theservices or activities of oneanother. Grant ThorntonInternational does notprovide services to clients.

Current IASB documents

Document type Title Comment deadline

Exposure Draft Annual Improvements to IFRSs 2011–2013 Cycle 18 February 2013

Exposure Draft Recoverable Amount Disclosures for Non-Financial 19 March 2013

Assets – Proposed Amendments to IAS 36

Exposure Draft Classification and Measurement: Limited Amendments 28 March 2013

to IFRS 9 – Proposed amendments to IFRS 9 (2010)

Exposure Draft Equity Method: Share of Other Net Asset Changes 22 March 2013

– Proposed amendments to IAS 28

Exposure Draft Clarification of Acceptable Methods of Depreciation 2 April 2013

and Amortisation – Proposed amendments to IAS 16

and IAS 38

Exposure Draft Exposure Draft: Acquisition of an Interest in a Joint 23 April 2013

Operation – Proposed amendment to IFRS 11

Exposure Draft Exposure Draft: Sale or Contribution of Assets between 23 April 2013

an Investor and its Associate or Joint Venture – Proposed

amendments to IFRS 10 and IAS 28

Welcome New standards In the pipeline Grant ThorntonNews

Round up Effective dates Open for comment