i’ve got my ppp loan, now what?...2020/05/06 · read my ebook, i've got my ppp loan, now...

TRANSCRIPT

I’ve got my PPP loan, now what?

simplicityHR.com

Supplement - Loan Reduction Computations5/6/20

simplicityHR.com

rev. 05/2020

Loan Forgiveness

Written by Barron Guss

5/6/20

1

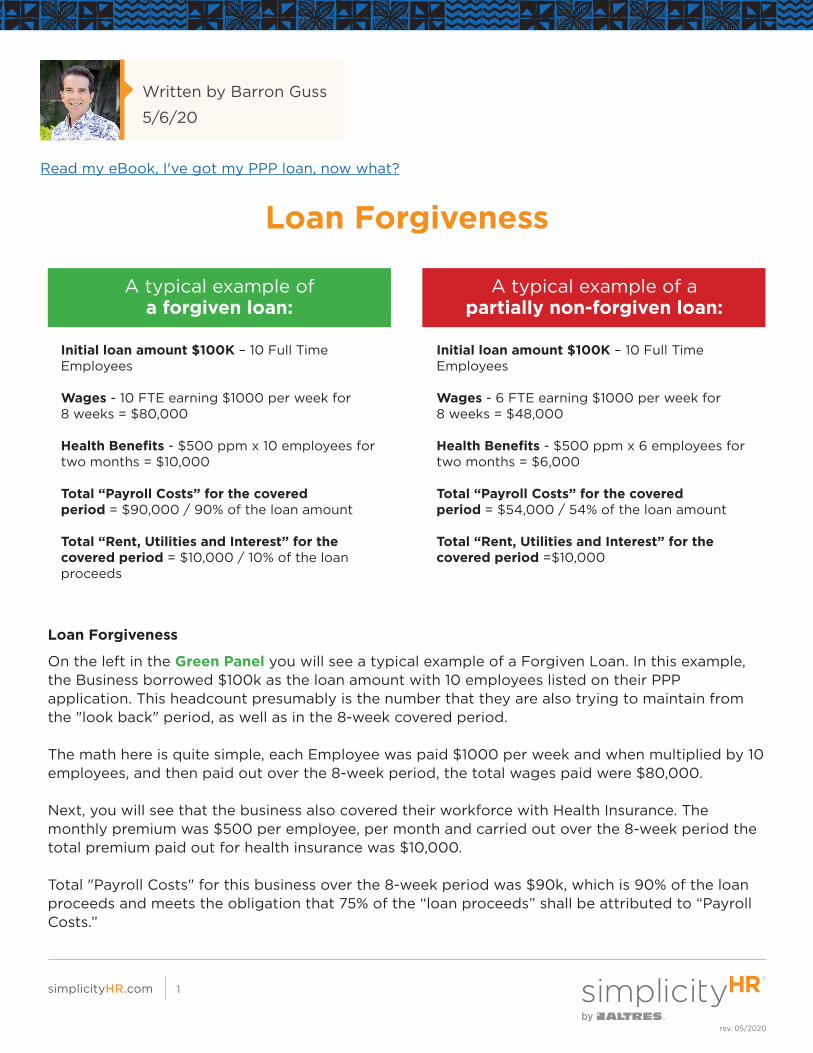

Initial loan amount $100K – 10 Full Time Employees

Wages - 10 FTE earning $1000 per week for 8 weeks = $80,000

Health Benefits - $500 ppm x 10 employees for two months = $10,000

Total “Payroll Costs” for the covered period = $90,000 / 90% of the loan amount

Total “Rent, Utilities and Interest” for the covered period = $10,000 / 10% of the loan proceeds

A typical example of a forgiven loan:

A typical example of a partially non-forgiven loan:

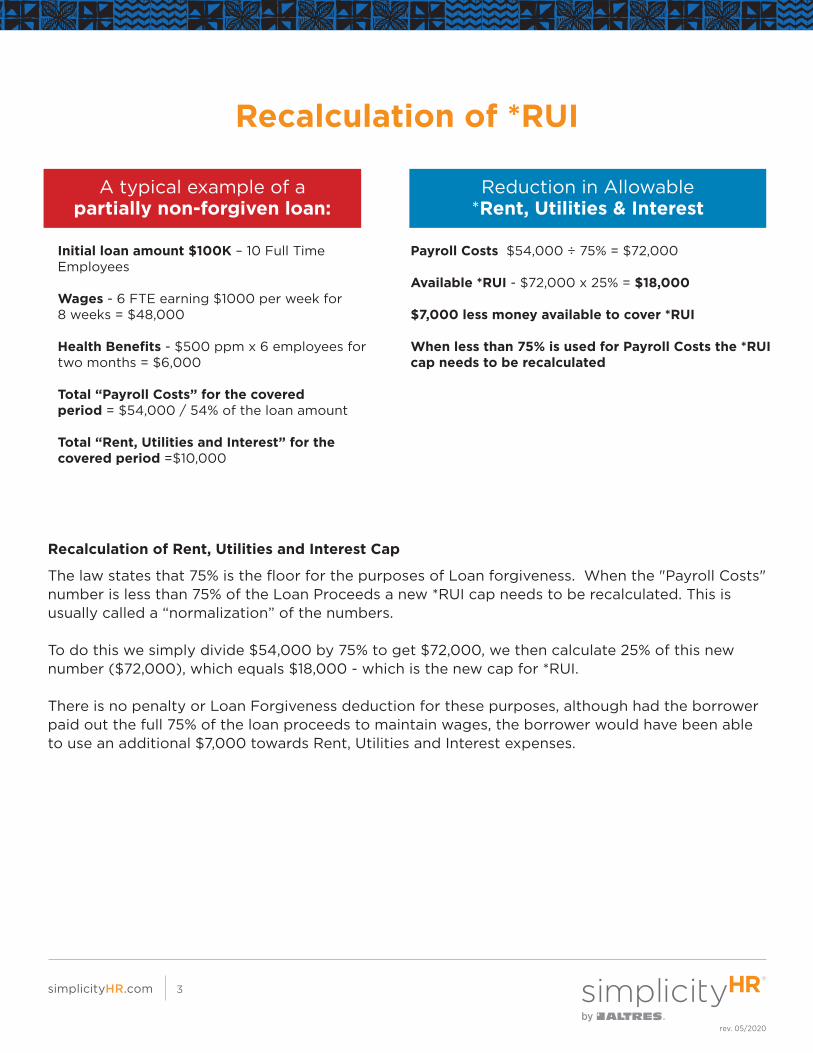

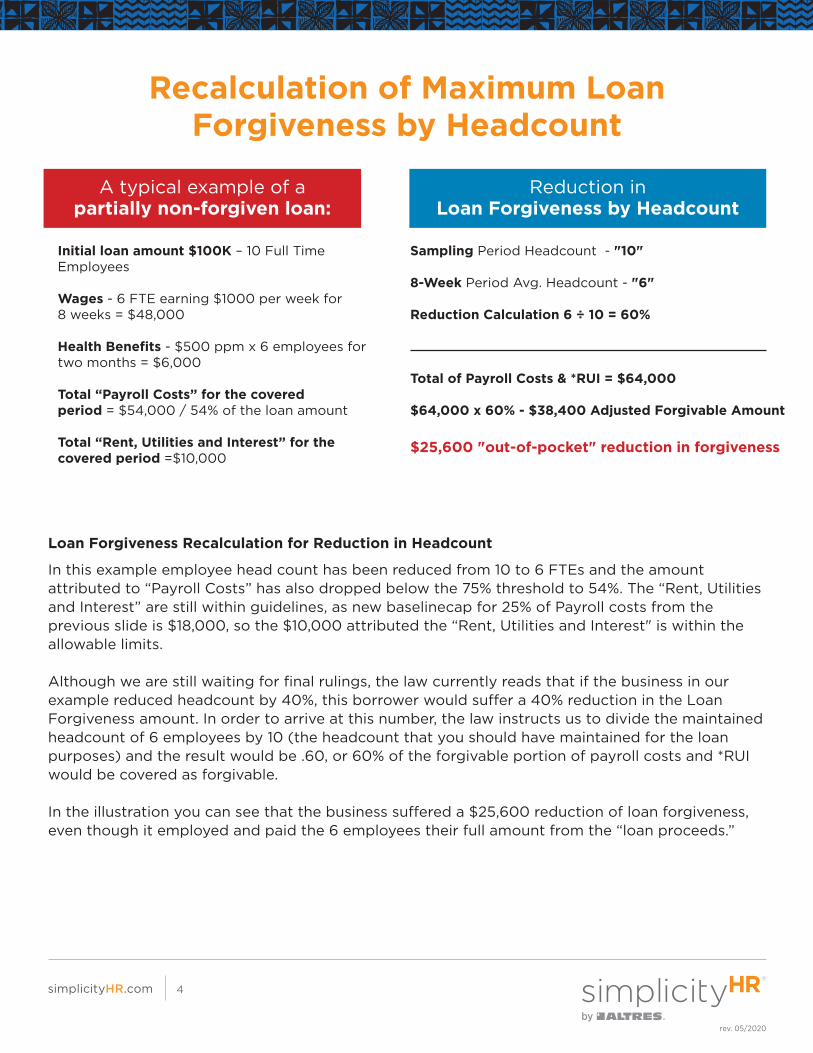

Initial loan amount $100K – 10 Full Time Employees

Wages - 6 FTE earning $1000 per week for 8 weeks = $48,000

Health Benefits - $500 ppm x 6 employees for two months = $6,000

Total “Payroll Costs” for the covered period = $54,000 / 54% of the loan amount

Total “Rent, Utilities and Interest” for the covered period =$10,000

Loan Forgiveness

On the left in the Green Panel you will see a typical example of a Forgiven Loan. In this example, the Business borrowed $100k as the loan amount with 10 employees listed on their PPP application. This headcount presumably is the number that they are also trying to maintain from the "look back" period, as well as in the 8-week covered period.

The math here is quite simple, each Employee was paid $1000 per week and when multiplied by 10 employees, and then paid out over the 8-week period, the total wages paid were $80,000.

Next, you will see that the business also covered their workforce with Health Insurance. The monthly premium was $500 per employee, per month and carried out over the 8-week period the total premium paid out for health insurance was $10,000.

Total "Payroll Costs" for this business over the 8-week period was $90k, which is 90% of the loan proceeds and meets the obligation that 75% of the “loan proceeds” shall be attributed to “Payroll Costs.”

Read my eBook, I've got my PPP loan, now what?

simplicityHR.com

rev. 05/2020

2

In addition, you can see that this business then paid $10,000 for *Rent, Utilities, and Interest, which is less than 25% of the allowable allocation for *RUI

In this example you can see that all the utilizations fall within the allowable 75/25 split and therefore, the borrower can expect the entire loan to be forgiven.

On the right in the Red Panel you will see a typical example of a partially non-forgiven loan.

In this example, the employee head count has been reduced from 10 full time employees to 6 and the amount attributed to “Payroll Costs” has also dropped below the 75% threshold to 54%. The “*Rent, Utilities and Interest” appear to be within guidelines, but because the payroll cost have been reduced, there will need to be a new 25% cap calculated for the *RUI.

For the purposes of maintaining headcount, the borrower will do its computation for Full-time Employee Equivalents - FTEs are based on a sampling time period prior to the downturn (February 15, 2019 -June 30, 2019 or for January 1, 2020 - February 29, 2020, at the borrower's choice) and the "determination" period (8-week "covered" period for which loan forgiveness is based upon).

On a special note: although the regulations are not yet clear it seems that the current law does allow that if the discrepancy was to be discovered prior to June 30, 2020, there would be a possible “fix.” The “fix” would be to rehire four workers and to quickly adjust the compensation of the of the entire 10-person workforce (for the 8-week period) up to minimally 75% of the loan amount or, in this case, $75,000, prior to June 30, 2020.

simplicityHR.com

rev. 05/2020

3

Recalculation of *RUI

Recalculation of Rent, Utilities and Interest Cap

The law states that 75% is the floor for the purposes of Loan forgiveness. When the "Payroll Costs" number is less than 75% of the Loan Proceeds a new *RUI cap needs to be recalculated. This is usually called a “normalization” of the numbers.

To do this we simply divide $54,000 by 75% to get $72,000, we then calculate 25% of this new number ($72,000), which equals $18,000 - which is the new cap for *RUI.

There is no penalty or Loan Forgiveness deduction for these purposes, although had the borrower paid out the full 75% of the loan proceeds to maintain wages, the borrower would have been able to use an additional $7,000 towards Rent, Utilities and Interest expenses.

A typical example of a partially non-forgiven loan:

Reduction in Allowable*Rent, Utilities & Interest

Initial loan amount $100K – 10 Full Time Employees

Wages - 6 FTE earning $1000 per week for 8 weeks = $48,000

Health Benefits - $500 ppm x 6 employees for two months = $6,000

Total “Payroll Costs” for the covered period = $54,000 / 54% of the loan amount

Total “Rent, Utilities and Interest” for the covered period =$10,000

Payroll Costs $54,000 ÷ 75% = $72,000

Available *RUI - $72,000 x 25% = $18,000

$7,000 less money available to cover *RUI

When less than 75% is used for Payroll Costs the *RUI cap needs to be recalculated

simplicityHR.com

rev. 05/2020

4

Recalculation of Maximum Loan Forgiveness by Headcount

Loan Forgiveness Recalculation for Reduction in Headcount

In this example employee head count has been reduced from 10 to 6 FTEs and the amount attributed to “Payroll Costs” has also dropped below the 75% threshold to 54%. The “Rent, Utilities and Interest” are still within guidelines, as new baselinecap for 25% of Payroll costs from the previous slide is $18,000, so the $10,000 attributed the “Rent, Utilities and Interest" is within the allowable limits.

Although we are still waiting for final rulings, the law currently reads that if the business in our example reduced headcount by 40%, this borrower would suffer a 40% reduction in the Loan Forgiveness amount. In order to arrive at this number, the law instructs us to divide the maintained headcount of 6 employees by 10 (the headcount that you should have maintained for the loan purposes) and the result would be .60, or 60% of the forgivable portion of payroll costs and *RUI would be covered as forgivable.

In the illustration you can see that the business suffered a $25,600 reduction of loan forgiveness, even though it employed and paid the 6 employees their full amount from the “loan proceeds.”

Reduction in Loan Forgiveness by Headcount

A typical example of a partially non-forgiven loan:

Initial loan amount $100K – 10 Full Time Employees

Wages - 6 FTE earning $1000 per week for 8 weeks = $48,000

Health Benefits - $500 ppm x 6 employees for two months = $6,000

Total “Payroll Costs” for the covered period = $54,000 / 54% of the loan amount

Total “Rent, Utilities and Interest” for the covered period =$10,000

Sampling Period Headcount - "10"

8-Week Period Avg. Headcount - "6"

Reduction Calculation 6 ÷ 10 = 60%

Total of Payroll Costs & *RUI = $64,000

$64,000 x 60% - $38,400 Adjusted Forgivable Amount

$25,600 "out-of-pocket" reduction in forgiveness

simplicityHR.com

rev. 05/2020

5

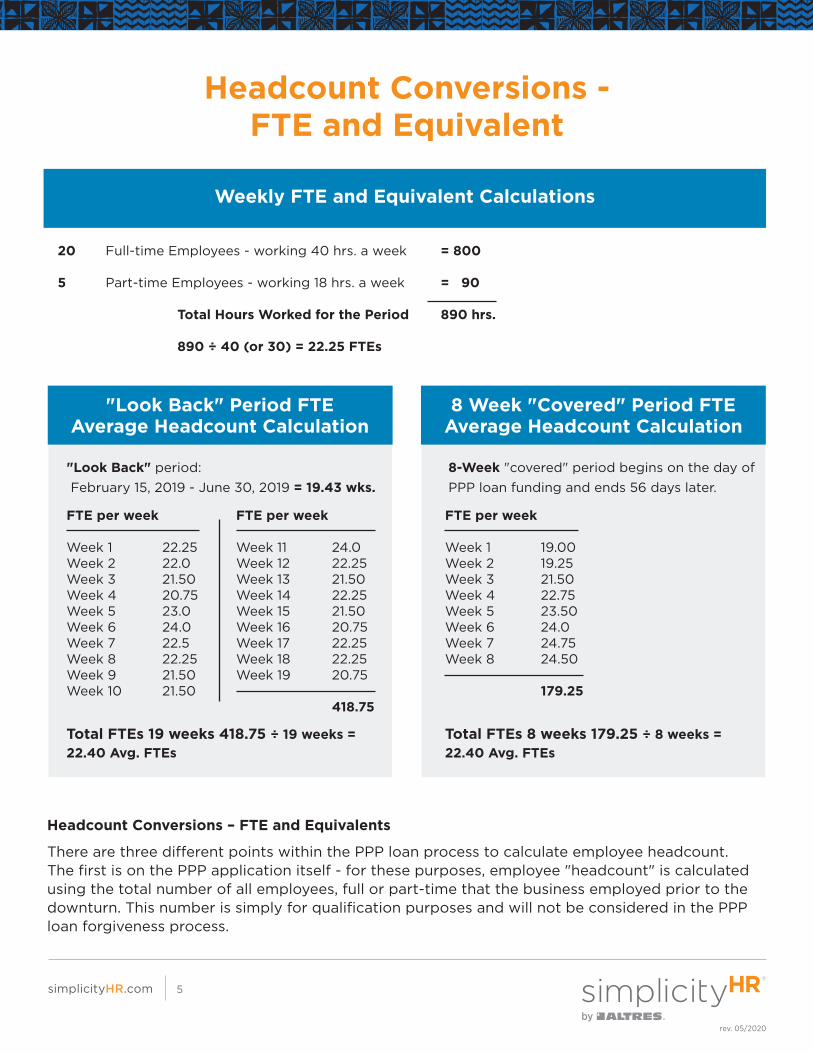

Headcount Conversions - FTE and Equivalent

Headcount Conversions – FTE and Equivalents

There are three different points within the PPP loan process to calculate employee headcount. The first is on the PPP application itself - for these purposes, employee "headcount" is calculated using the total number of all employees, full or part-time that the business employed prior to the downturn. This number is simply for qualification purposes and will not be considered in the PPP loan forgiveness process.

Weekly FTE and Equivalent Calculations

"Look Back" Period FTE Average Headcount Calculation

8 Week "Covered" Period FTE Average Headcount Calculation

20 Full-time Employees - working 40 hrs. a week = 800

5 Part-time Employees - working 18 hrs. a week = 90

Total Hours Worked for the Period 890 hrs.

890 ÷ 40 (or 30) = 22.25 FTEs

"Look Back" period: February 15, 2019 - June 30, 2019 = 19.43 wks.

8-Week "covered" period begins on the day ofPPP loan funding and ends 56 days later.

FTE per week

Week 1 22.25Week 2 22.0Week 3 21.50Week 4 20.75Week 5 23.0Week 6 24.0Week 7 22.5Week 8 22.25Week 9 21.50Week 10 21.50

FTE per week

Week 1 19.00 Week 2 19.25Week 3 21.50Week 4 22.75 Week 5 23.50Week 6 24.0Week 7 24.75Week 8 24.50

179.25

FTE per week

Week 11 24.0Week 12 22.25Week 13 21.50Week 14 22.25Week 15 21.50Week 16 20.75Week 17 22.25Week 18 22.25Week 19 20.75

418.75

Total FTEs 19 weeks 418.75 ÷ 19 weeks = 22.40 Avg. FTEs

Total FTEs 8 weeks 179.25 ÷ 8 weeks = 22.40 Avg. FTEs

simplicityHR.com

rev. 05/2020

FTEs will come into consideration during the "look back" period (February 15, 2019 - June 30, 2019 or for January 1, 2020 - February 29, 2020, at the borrower's choice) and the "determination" period (8-week "covered" period for which loan forgiveness is based upon).

Note: It does not matter if you use 30 or 40 hours during the conversion process of combining full and part-time employees into FTEs, the important thing is that you are consistent in the use of either number for calculation for both the "look back" and determination periods. For the purposes of loan forgiveness, the number of calculated FTEs is simply an “index," and the number you need to manage to for the 8-week determination period.

In order to perform the conversion of full-time and part-time workers into FTEs, calculate the total number of hours worked by your full and part-time employees each week and then divide by 40 (or 30) hours, which is traditionally the number of hours worked in a week by a full-time employee. For example, if you had 25 employees comprised of both full-time and part-time employees with hours worked by all employees totaling 890, your FTE would be 22.25 (890 divided by 40).

"Look Back" Average FTE Calculation

In order to calculate the “average” number of FTEs for the “look back” period, you simply calculate the FTEs for each week (you can do a monthly calculation if preferred), total the number of FTEs for the period of measurement and then divide by the number of sampling periods. In the illustration above, we chose to sample 19 weeks since there are 19.43 weeks in the “look back” period from February 15, 2019 - June 30, 2019. The calculation is 418.75 FTEs ÷ 19 weeks = 22.40 Avg. FTEs for the “look back” period.

8-Week "Covered" Period Average FTE Calculation

A similar calculation is used for the 8–week “covered” period. Sample eight individual weeks, total the number of FTEs and then divide by “8” in order to determine the “average” number of FTEs that were employed in the period.

6

simplicityHR.com

rev. 05/2020

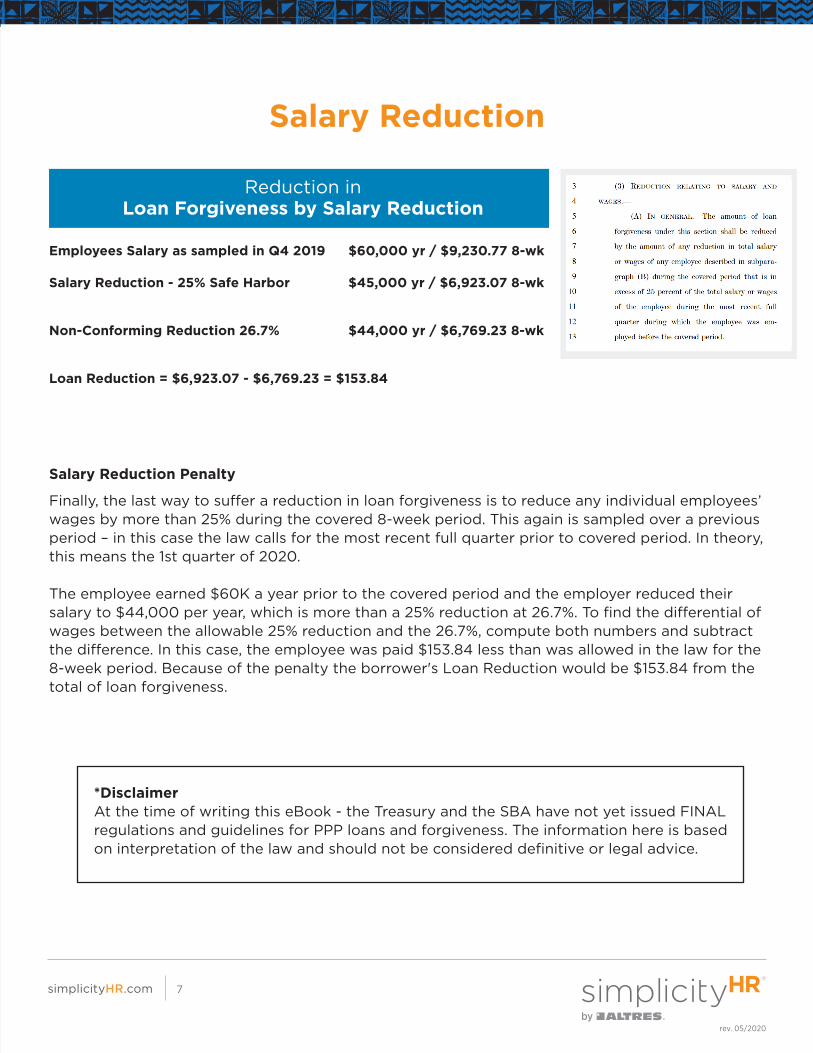

Salary Reduction

Salary Reduction Penalty

Finally, the last way to suffer a reduction in loan forgiveness is to reduce any individual employees’ wages by more than 25% during the covered 8-week period. This again is sampled over a previous period – in this case the law calls for the most recent full quarter prior to covered period. In theory, this means the 1st quarter of 2020.

The employee earned $60K a year prior to the covered period and the employer reduced their salary to $44,000 per year, which is more than a 25% reduction at 26.7%. To find the differential of wages between the allowable 25% reduction and the 26.7%, compute both numbers and subtract the difference. In this case, the employee was paid $153.84 less than was allowed in the law for the 8-week period. Because of the penalty the borrower's Loan Reduction would be $153.84 from the total of loan forgiveness.

*DisclaimerAt the time of writing this eBook - the Treasury and the SBA have not yet issued FINAL regulations and guidelines for PPP loans and forgiveness. The information here is based on interpretation of the law and should not be considered definitive or legal advice.

Reduction inLoan Forgiveness by Salary Reduction

Employees Salary as sampled in Q4 2019 $60,000 yr / $9,230.77 8-wk

Salary Reduction - 25% Safe Harbor $45,000 yr / $6,923.07 8-wk

Non-Conforming Reduction 26.7% $44,000 yr / $6,769.23 8-wk

Loan Reduction = $6,923.07 - $6,769.23 = $153.84

simplicityHR.com

rev. 05/2020

7

simplicityHR.com

rev. 05/2020

To our clients and members of our business community,

COVID-19 has changed the physiological, psychological, and financial landscape of the world almost overnight. Each of us has been affected and no one has been spared.

The constant flow and volume of information regarding this crisis can be overwhelming and difficult for all of us to understand. We have done our best to simplify and explain all the information found in this guide, and I hope that you find our expertise useful and insightful.

We have taken to heart our responsibility to serve our clients and our community for the last 50 years, and while tomorrow’s business landscape may look and feel different, our commitment will remain the same; to be with you today, tomorrow and the next 50 years.

Sincerely,

Barron L. Guss President and CEO

About Us

simplicityHR by ALTRES

serves as the human

resources “back office”

for more than 2,200 local

businesses. We provide

expert payroll processing,

HR administration,

workers’ compensation

coverage and claims

management, health care

plans and exceptional

employee benefits

packages, as well as

training for managers

and staff.

From the Remote Desk of Barron Guss