how to stockpile $100,000 in 15 years

DESCRIPTION

How much money have you saved over the last 5, 10, or even 15 years? If you're like most people, you probably haven't done as well as you would have liked. But the fact is it's relatively easy to amass a considerable amount of money in a reasonable amount of time. All it requires is consistency – unwavering consistency. But like anything else, to be successful over the long haul, you'll need a realistic plan that you can live with. What does it take to save $100,000 in 15 years?TRANSCRIPT

How to Stockpile$100,000 in 15 Years

Saving $100,000 – A Walk in the Park?

Reaching $100,000 in 15 years requires investing $300 per month.

The best way to reach that 15-year goal is to increase income, decrease expenses and increase assets.

Even though the process might sound complicated or out of reach for you, we’ll show you how it’s easier than you think!

Formula for Saving $100,000 in 15 Years

Decrease DebtIncrease Income &

Assets

What is an Asset?

An asset is anything that is purchased or acquired for the purpose of generating income in the future.

For example, a car would not be considered an asset because it will de-value as the years go by.

Your home might or might not be an asset. Did you purchase it to live in the rest of your life? Will you be selling it before it can gain equity?

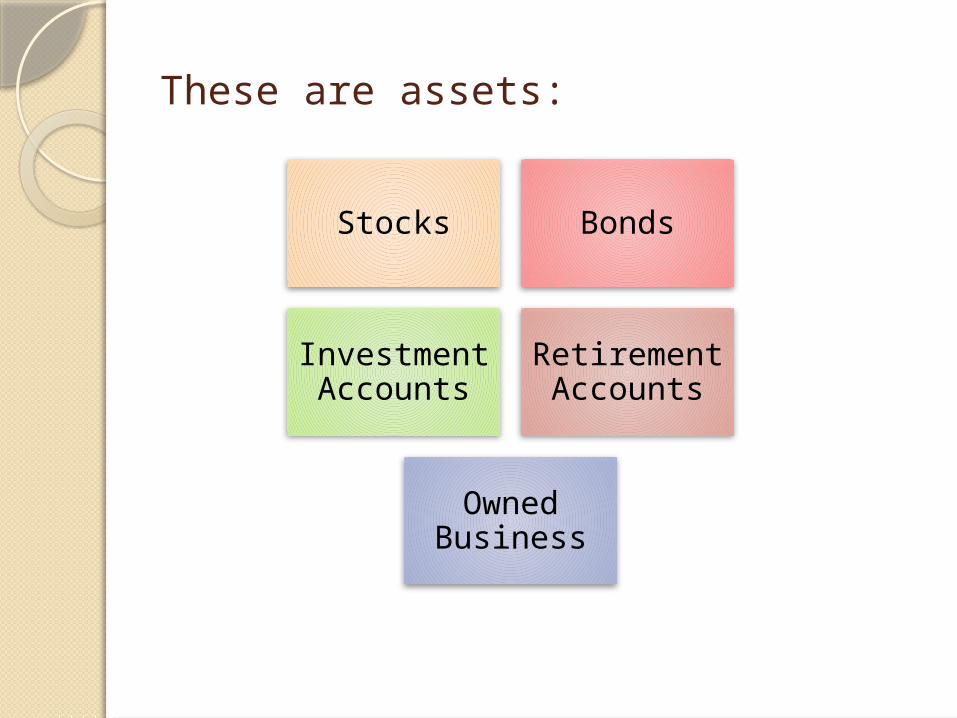

These are assets:

Stocks Bonds

Investment Accounts

Retirement Accounts

Owned Business

What is Debt?

Debt is the total amount of money that is owed.

Having $1 million in assets puts you in a better position than having $1 million in assets and $2 million in debt.

The solution is to possess Net Assets.

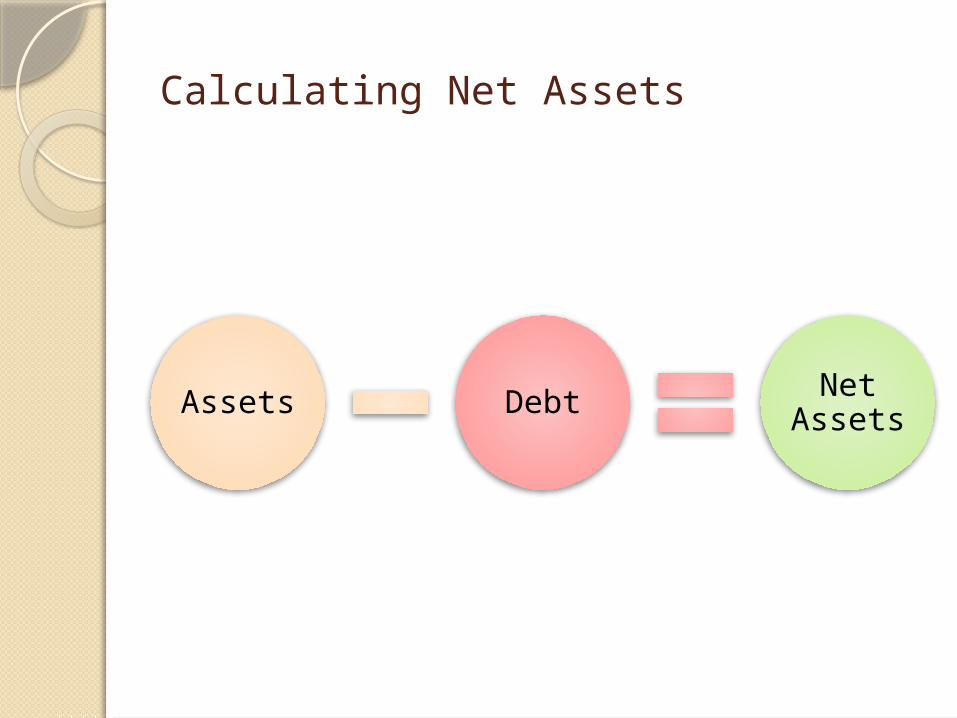

Calculating Net Assets

Assets Debt Net Assets

Strategies: Achieve Your $100,000 Goal

Budgeting & Saving

Investing

Managing Debt

Minimizing the Effect of Taxes

Protecting Wealth

Budgeting & Saving

Tips for Budgeting

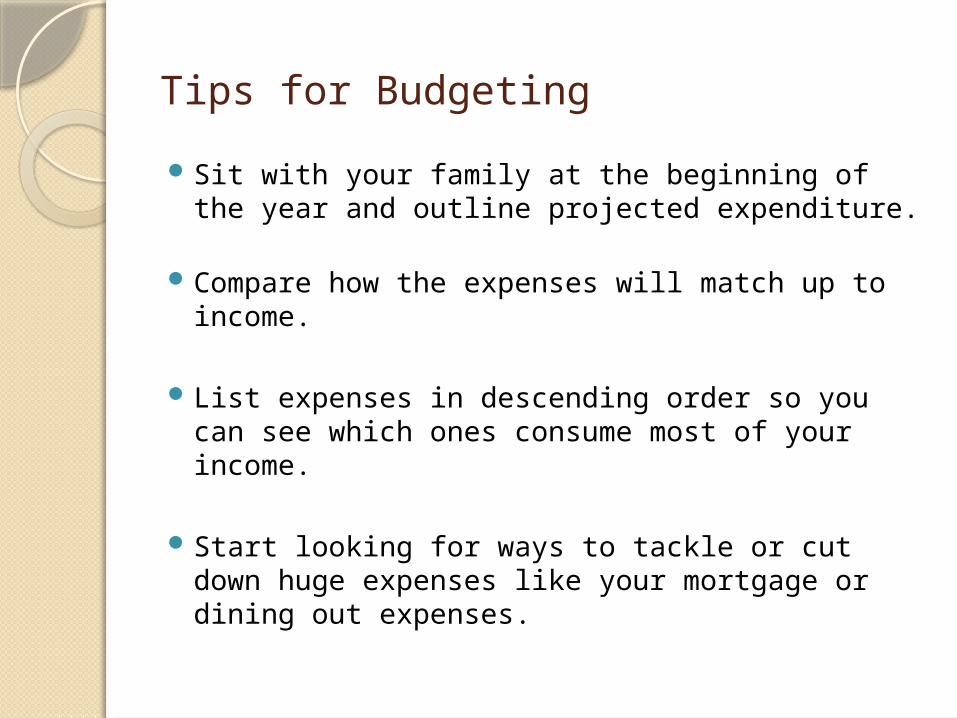

Sit with your family at the beginning of the year and outline projected expenditure.

Compare how the expenses will match up to income.

List expenses in descending order so you can see which ones consume most of your income.

Start looking for ways to tackle or cut down huge expenses like your mortgage or dining out expenses.

Things to Consider when Budgeting

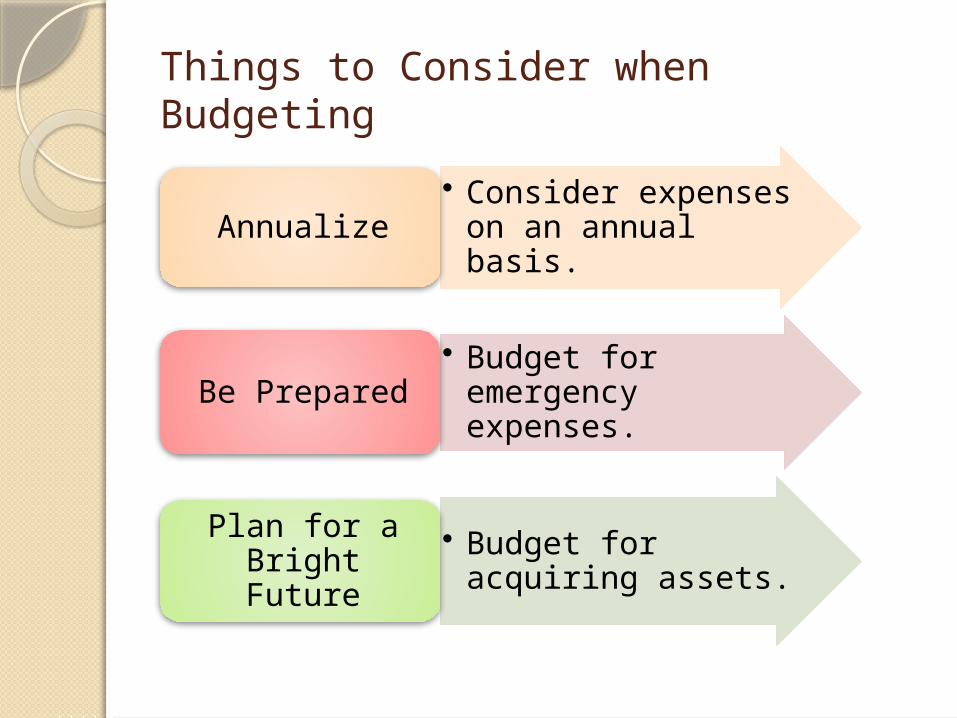

• Consider expenses on an annual basis.Annualize

• Budget for emergency expenses.

Be Prepared

• Budget for acquiring assets.

Plan for a Bright Future

Finding the Funds: $3600/yr.

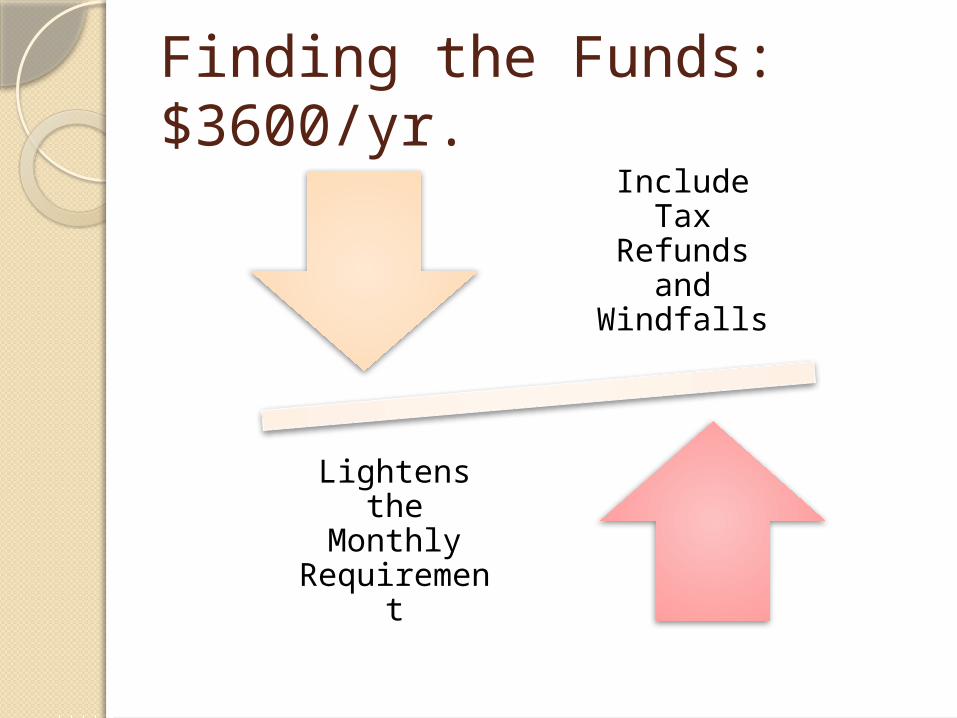

Include Tax Refunds and

Windfalls

Lightens the Monthly

Requirement

Finding the Funds: $300/mo.Use savings that you discovered

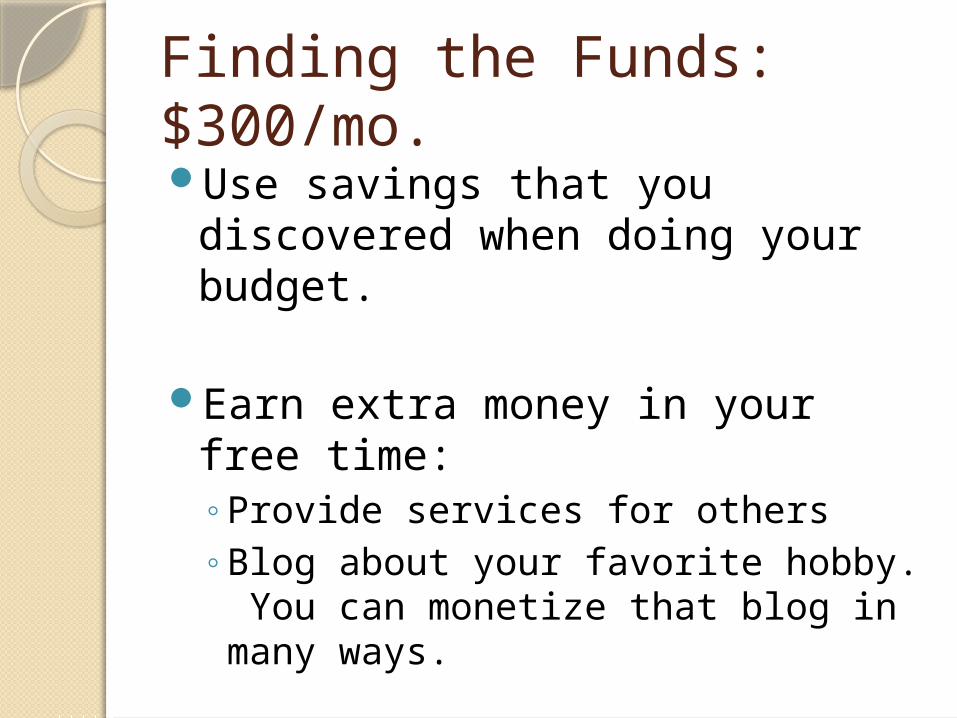

when doing your budget.

Earn extra money in your free time:◦Provide services for others◦Blog about your favorite hobby. You

can monetize that blog in many ways.

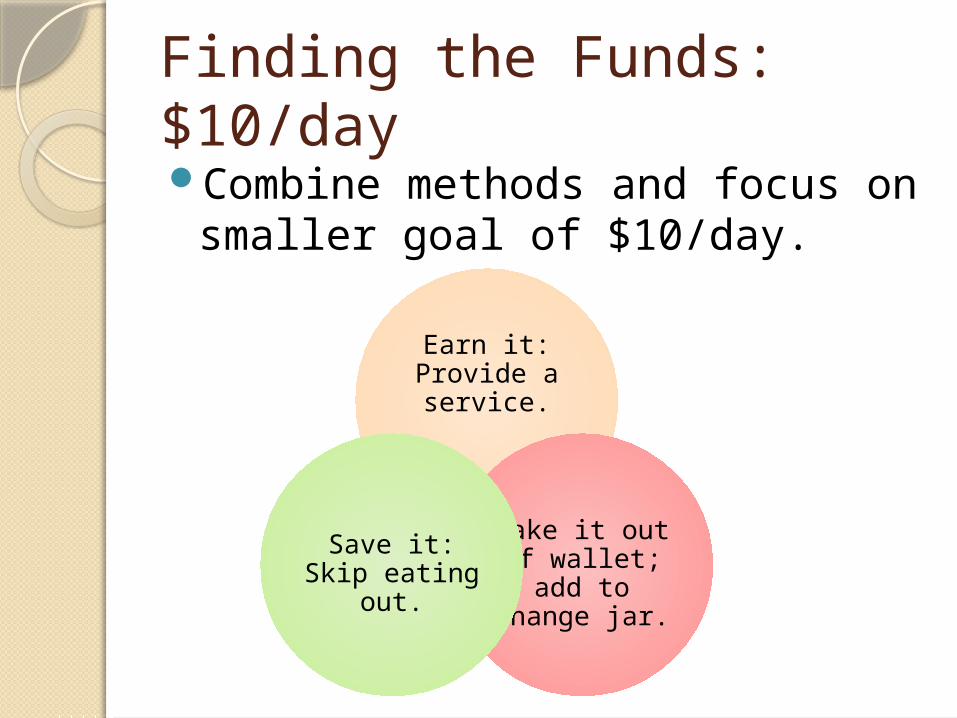

Finding the Funds: $10/dayCombine methods and focus on

smaller goal of $10/day.

Earn it: Provide a service.

Take it out of wallet;

add to change jar.

Save it: Skip eating

out.

Investing

Tips for Investing

Investing is putting your money to work for you; it is thinking about the best way to make more money.

The more money you spend in your lifetime on income producing assets, the wealthier you will ultimately become.

The sooner you get started, the harder your money can work for you.

Things to Consider when Investing

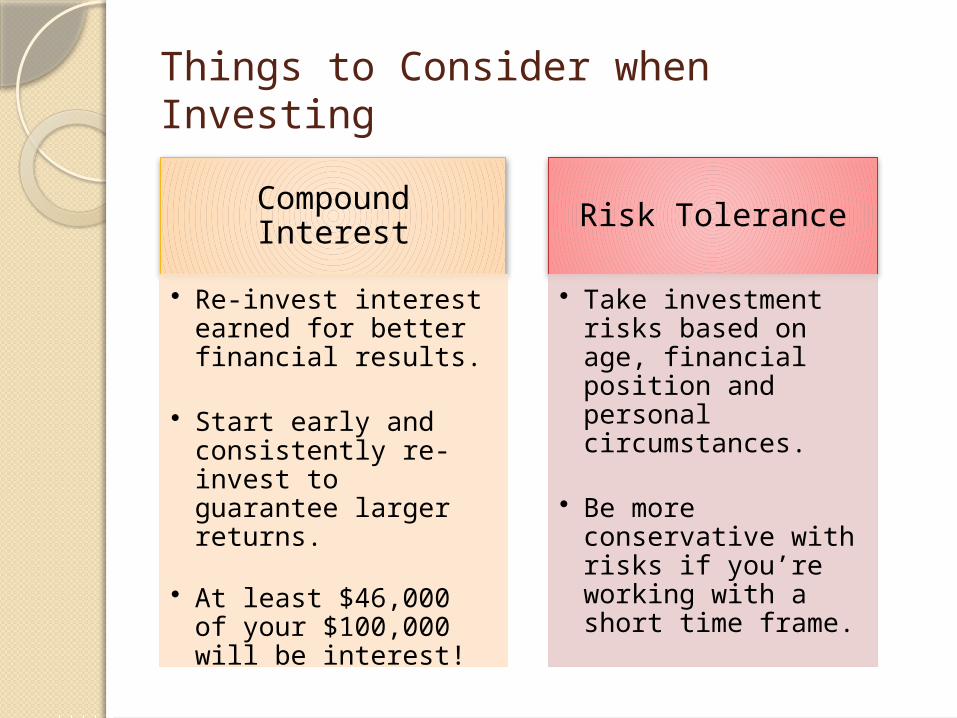

Compound Interest

• Re-invest interest earned for better financial results.

• Start early and consistently re-invest to guarantee larger returns.

• At least $46,000 of your $100,000 will be interest!

Risk Tolerance

• Take investment risks based on age, financial position and personal circumstances.

• Be more conservative with risks if you’re working with a short time frame.

Things to Consider when Investing

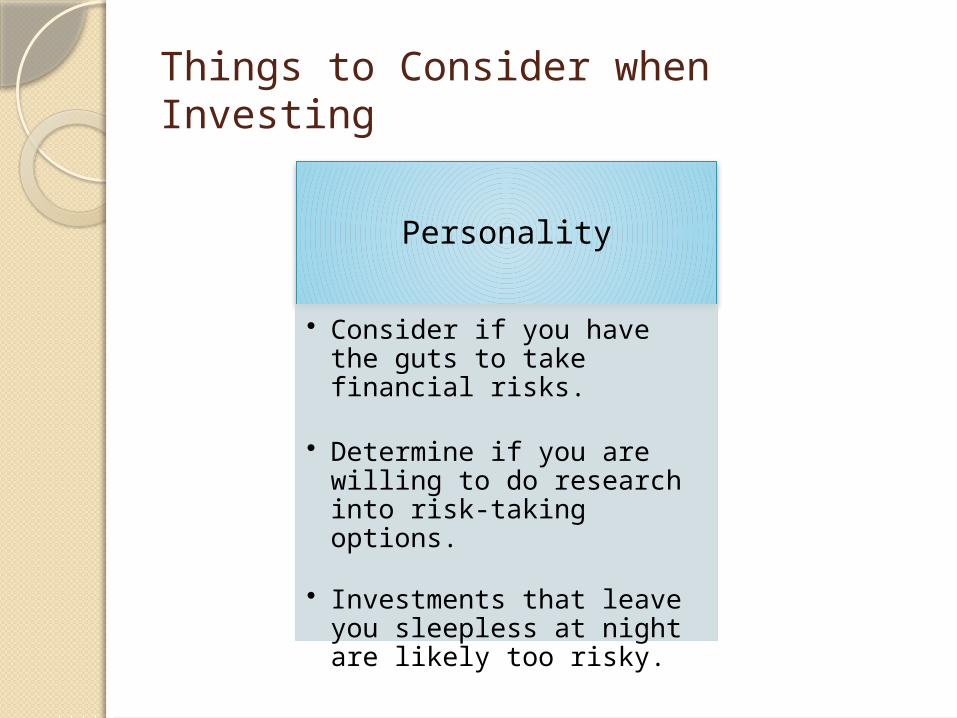

Personality

• Consider if you have the guts to take financial risks.

• Determine if you are willing to do research into risk-taking options.

• Investments that leave you sleepless at night are likely too risky.

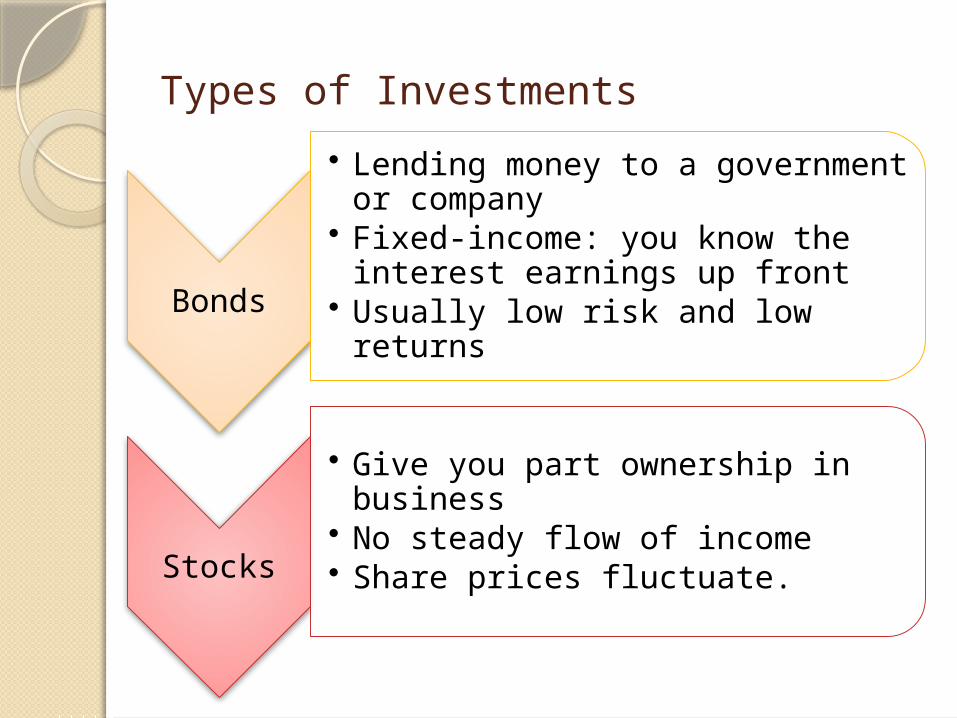

Types of Investments

Bonds

• Lending money to a government or company

• Fixed-income: you know the interest earnings up front

• Usually low risk and low returns

Stocks

• Give you part ownership in business

• No steady flow of income• Share prices fluctuate.

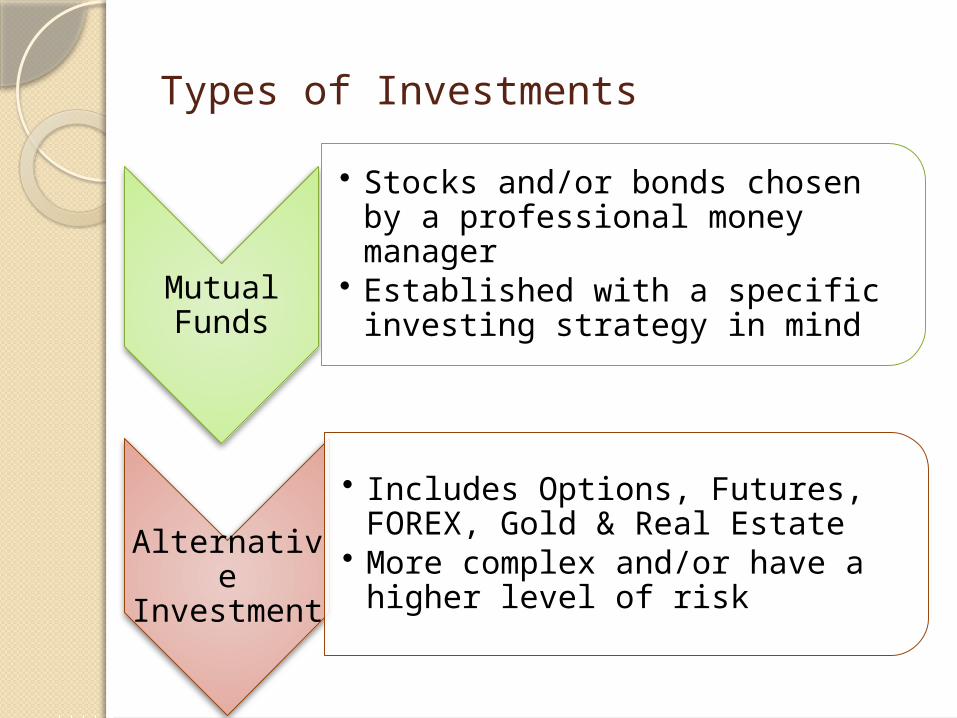

Types of Investments

Mutual

Funds

• Stocks and/or bonds chosen by a professional money manager

• Established with a specific investing strategy in mind

Alternative

Investment

• Includes Options, Futures, FOREX, Gold & Real Estate

• More complex and/or have a higher level of risk

Managing Debt

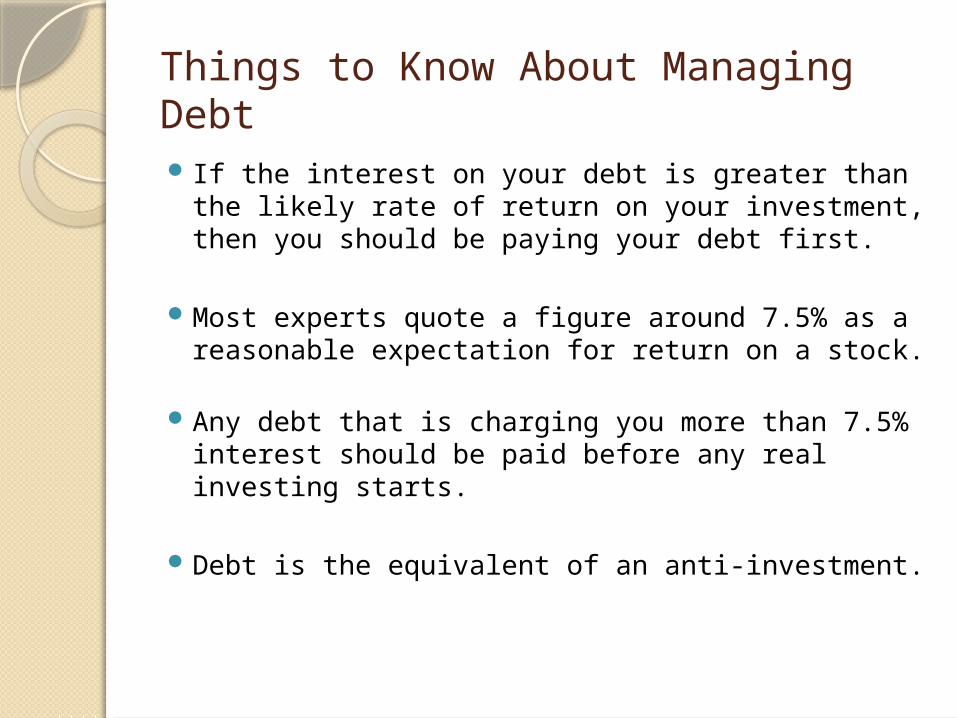

Things to Know About Managing Debt

If the interest on your debt is greater than the likely rate of return on your investment, then you should be paying your debt first.

Most experts quote a figure around 7.5% as a reasonable expectation for return on a stock.

Any debt that is charging you more than 7.5% interest should be paid before any real investing starts.

Debt is the equivalent of an anti-investment.

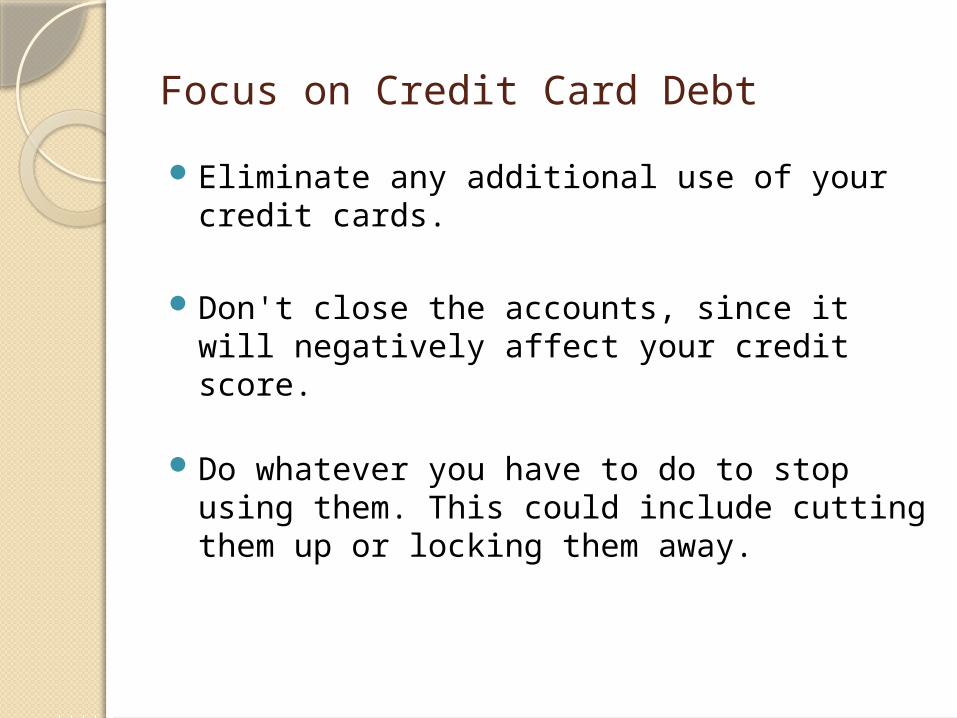

Focus on Credit Card Debt

Eliminate any additional use of your credit cards.

Don't close the accounts, since it will negatively affect your credit score.

Do whatever you have to do to stop using them. This could include cutting them up or locking them away.

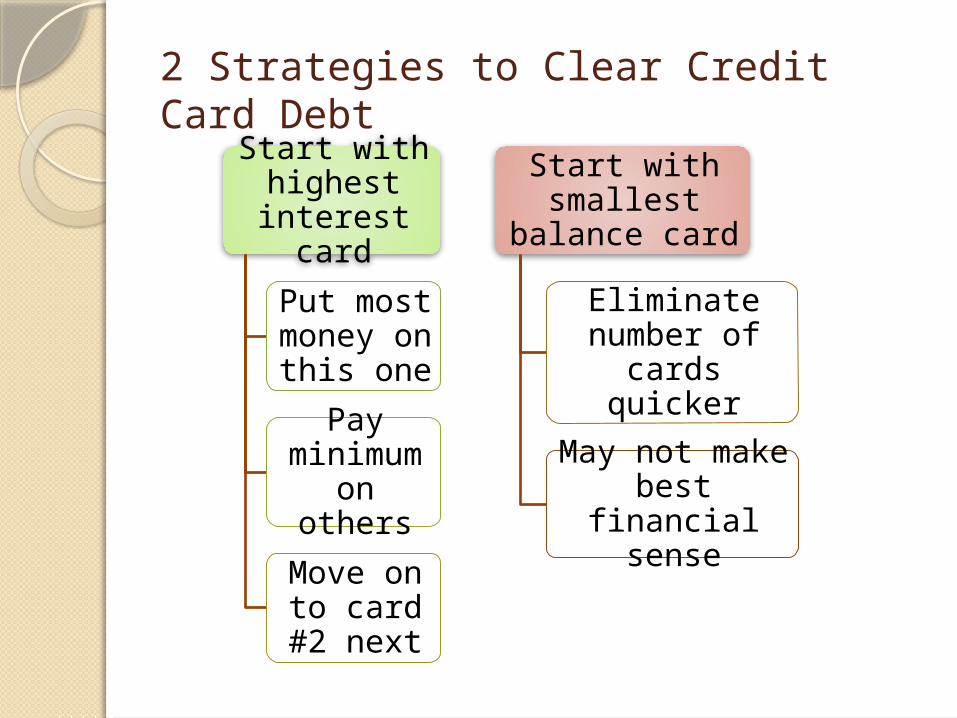

2 Strategies to Clear Credit Card DebtStart with highest interest

cardPut most money on this

one

Pay minimum on others

Move on to card #2 next

Start with smallest

balance card

Eliminate number of

cards quicker

May not make best financial

sense

Minimizing the Effect of Taxes

Strategies for Minimizing the Effect of Taxes

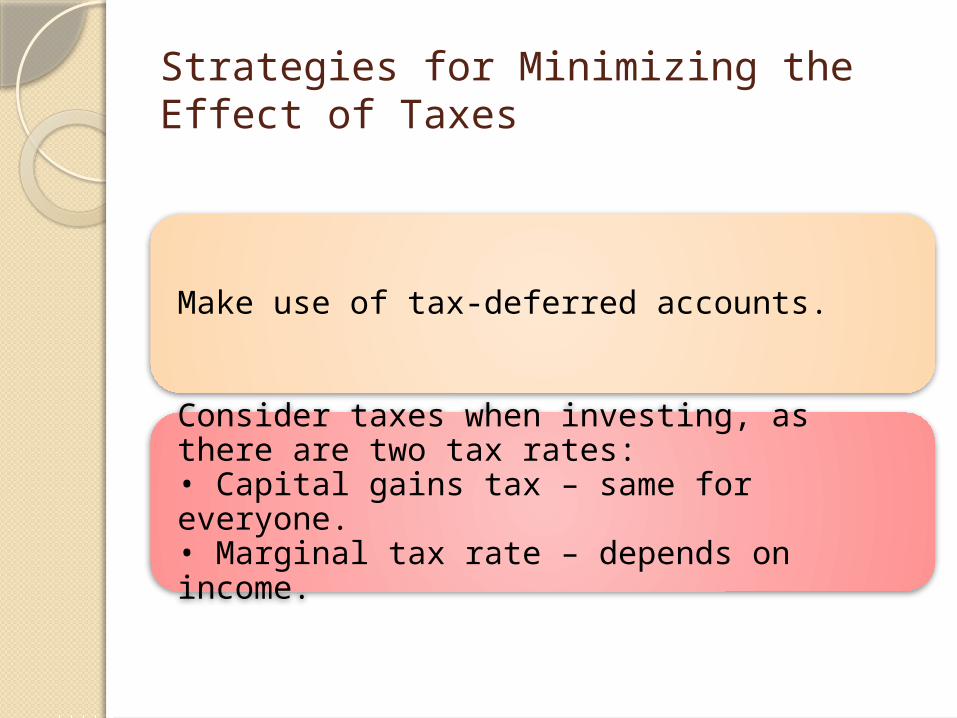

Make use of tax-deferred accounts.

Consider taxes when investing, as there are two tax rates:• Capital gains tax – same for everyone.• Marginal tax rate – depends on income.

Planning Investments Around Taxes

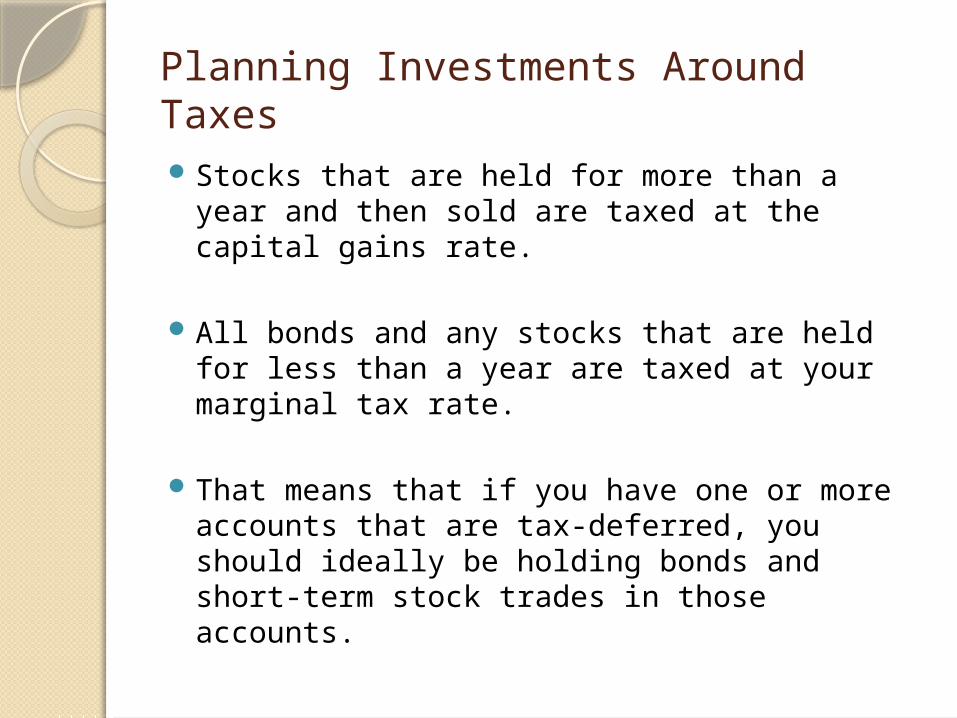

Stocks that are held for more than a year and then sold are taxed at the capital gains rate.

All bonds and any stocks that are held for less than a year are taxed at your marginal tax rate.

That means that if you have one or more accounts that are tax-deferred, you should ideally be holding bonds and short-term stock trades in those accounts.

Protecting Wealth

Looking Into Protecting Wealth

There are several aspects that go into protecting your assets and your wealth.

Set up protection from potential legal actions against you.

Avoid the temptation to spend your wealth before you're done needing or accumulating your assets.

Conclusion

Building assets is really just a function of budgeting/saving, investing, reducing debt, and then protecting those assets.

Eliminate the waste from your financial life, increase your income slightly, and invest consistently.

Building savings of over $100,000 in 15 years is well within the capabilities of anyone with the necessary discipline.

We hope you enjoyed your Special Report!

Curtis Roese is an experienced professional with extensive experience in personal finance and small business matters. Curtis writes and publishes articles, courses, guides and special reports on his personal finance blog.

Common Cents Wisdom is a website with hundreds of informative articles, special reports, resources to assist you with all of your financial concerns and a free monthly newsletter.

Sign up to receive your free eBook "Common Cents" and get started today on the road to financial freedom!

This Free Course Includes:

A Complete 80+ Page, 16-Module Home Study Course in PDF format

Companion Worksheets and Cheat Sheets

Budget Helpers, Worksheets, and Trackers

Bonus Audio Interviews with Financial Experts

My Secret Resource List of Helpful Money Sites, Tools, and Calculators

Bonus #1: Boosting Your Value Without a Formal Education

Bonus #2: Building a Wealth and Prosperity Mindset

Bonus #3: 25 Ways To Protect Your Identity

Don’t Delay! Get Your Free Course Now!

Sign Up ~ FREE Personal Finance Newsletter “Finally… A High-Quality, Content Rich, No BS NewsletterWritten Specifically For Those Interested In Personal Finance” What you can expect to receive EVERY Month by signing up: Special Report – 10 to 20 page in-depth report on Personal Finance topics important to you! Articles to keep you informed on a variety of topics relevant to your financial freedom. Action Guides, Worksheets, Resources & Buyer Guides! Monthly Financial Calendar to keep you organized and current with managing your personal finances. Periodic reviews of Products and Services – Real Financial Solutions ~ Real Fast!

http://www.commoncentswisdom.com/newsletter/