how to pay for news?

DESCRIPTION

Presentation by Valérie-Anne Bleyen and Leo Van Hove. FLEET-workshop Paying For News, 19th of March, 2009.http://www.fleetproject.be/nl/home/paying-for-news-workshop/TRANSCRIPT

19 MARCH 2009

VRIJE UNIVERSITEIT BRUSSEL

PA¥ING FOR N€W$INTERACTIVE WORKSHOP ON FLEMISH E-PUBLISHING TRENDS

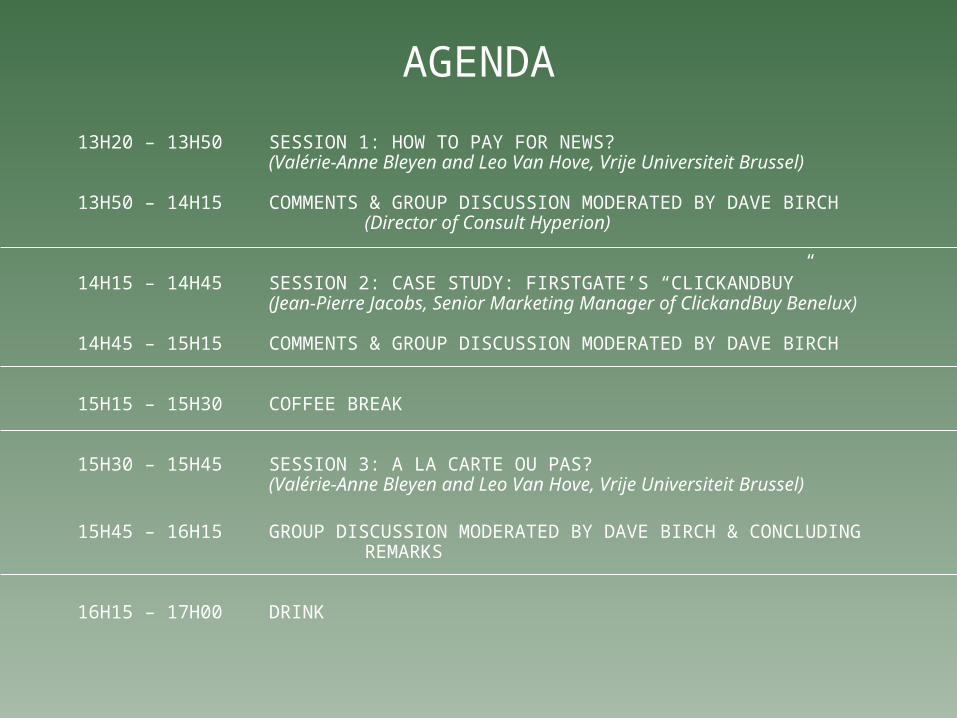

AGENDA

13H20 – 13H50 SESSION 1: HOW TO PAY FOR NEWS? (Valérie-Anne Bleyen and Leo Van Hove, Vrije Universiteit Brussel)

13H50 – 14H15 COMMENTS & GROUP DISCUSSION MODERATED BY DAVE BIRCH (Director of Consult Hyperion)

14H15 – 14H45 SESSION 2: CASE STUDY: FIRSTGATE’S “CLICKANDBUY”(Jean-Pierre Jacobs, Senior Marketing Manager of ClickandBuy Benelux)

14H45 – 15H15 COMMENTS & GROUP DISCUSSION MODERATED BY DAVE BIRCH

15H15 – 15H30 COFFEE BREAK

15H30 – 15H45 SESSION 3: A LA CARTE OU PAS? (Valérie-Anne Bleyen and Leo Van Hove, Vrije Universiteit Brussel)

15H45 – 16H15 GROUP DISCUSSION MODERATED BY DAVE BIRCH & CONCLUDING REMARKS

16H15 – 17H00 DRINK

Valérie-Anne Bleyen - Leo Van Hove

19 March 2009

Vrije Universiteit Brussel

SESSION 1: HOW TO PA¥ FOR N€W$?

-2/26-

INTRO: WHY PAYMENT INSTRUMENTS?

1. PAYMENTS MARKET = DYNAMIC AND TURBULENT

=> CLASSIFICATION OVERVIEW

2. PI ~ REVENUE MODEL

=> SWOT ANALYSIS INSIGHT

-3/26-

AGENDA

I. CLASSIFYING PIS: A MATRYOSHKA APPROACH

II. PIS OFFERED BY NP SITES: 2008 VS. 2006

III. SWOT-ANALYSIS

IV. CONCLUSION

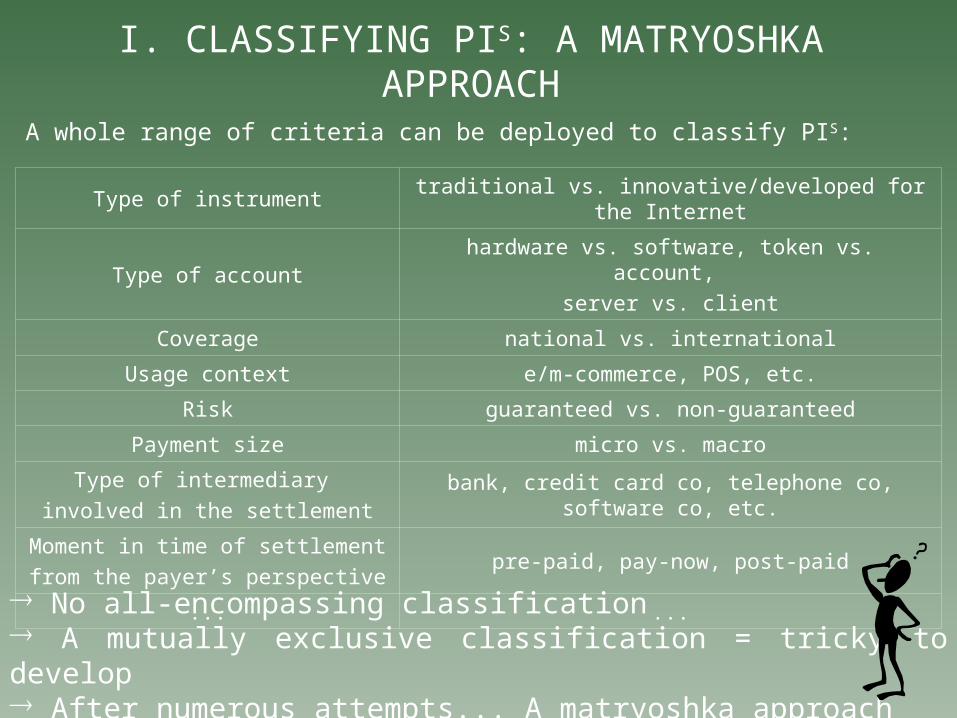

I. CLASSIFYING PIS: A MATRYOSHKA APPROACH

A whole range of criteria can be deployed to classify PIS:

No all-encompassing classification A mutually exclusive classification = tricky to develop After numerous attempts... A matryoshka approach

Type of instrument traditional vs. innovative/developed for the Internet

Type of accounthardware vs. software, token vs. account,

server vs. client

Coverage national vs. international

Usage context e/m-commerce, POS, etc.

Risk guaranteed vs. non-guaranteed

Payment size micro vs. macro

Type of intermediary

involved in the settlementbank, credit card co, telephone co, software co, etc.

Moment in time of settlement

from the payer’s perspectivepre-paid, pay-now, post-paid

... ...

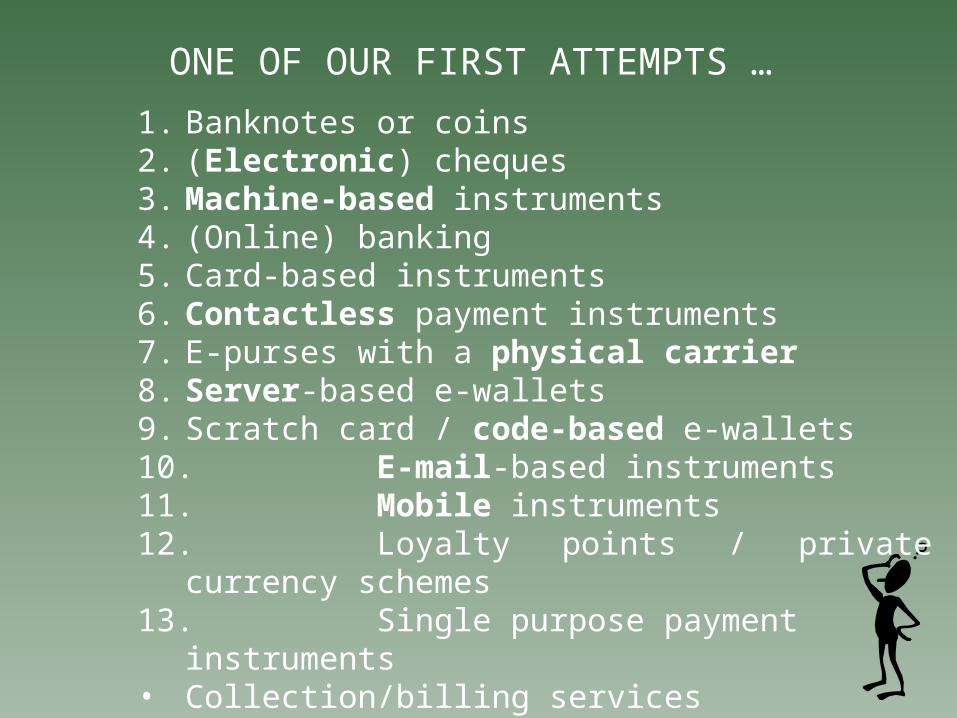

ONE OF OUR FIRST ATTEMPTS …

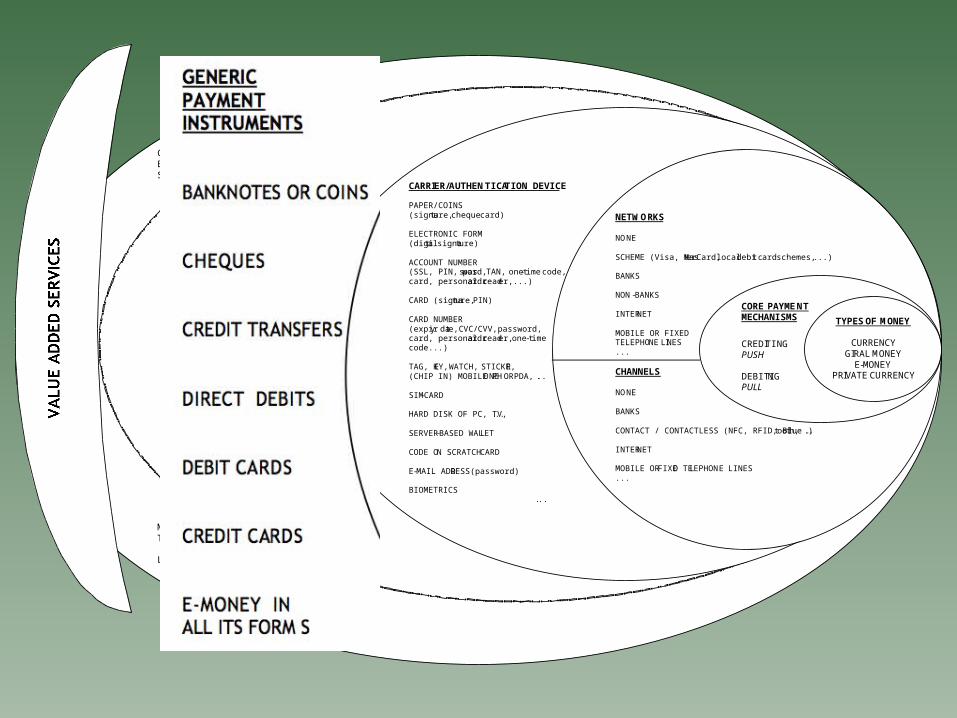

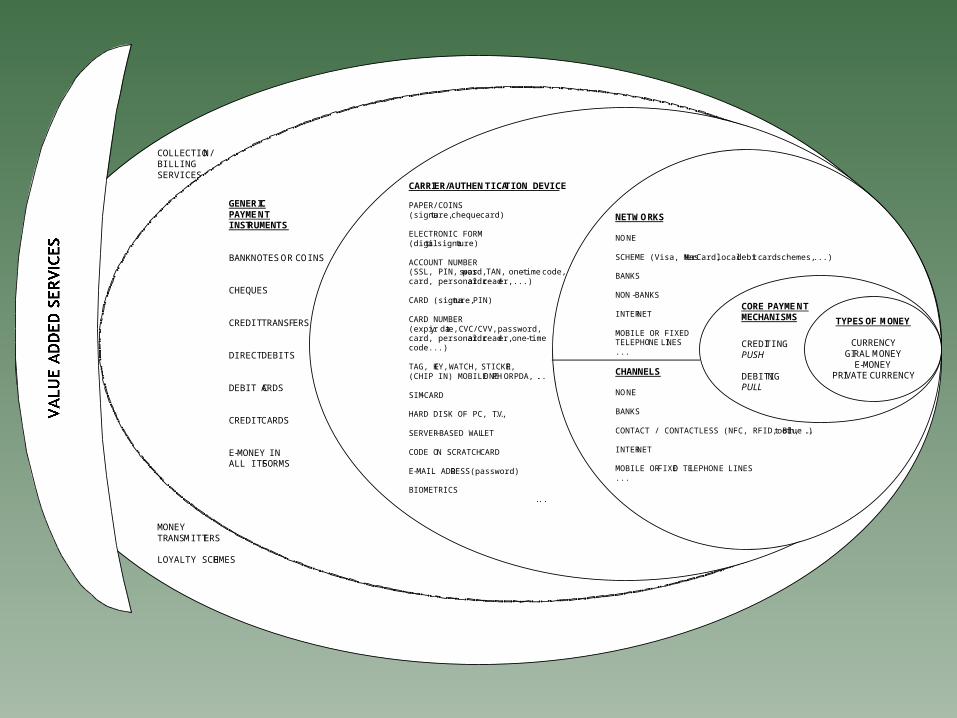

1. Banknotes or coins2. (Electronic) cheques3. Machine-based instruments4. (Online) banking5. Card-based instruments6. Contactless payment instruments7. E-purses with a physical carrier8. Server-based e-wallets9. Scratch card / code-based e-wallets10.E-mail-based instruments11.Mobile instruments12.Loyalty points / private currency schemes13.Single purpose payment instruments• Collection/billing services• Money transmitters

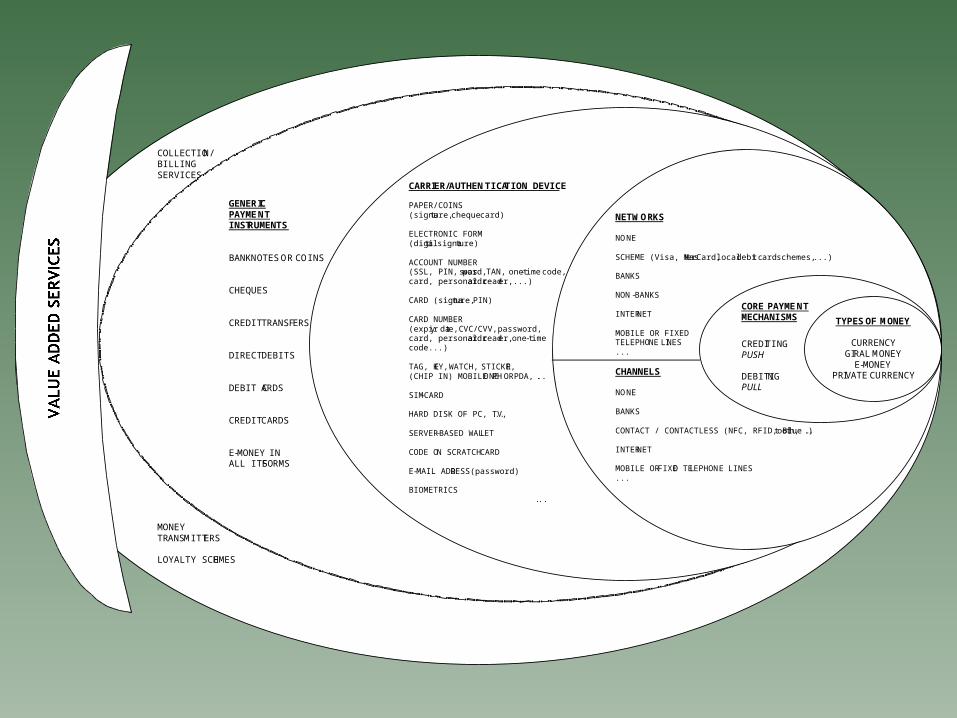

COLLECTION/ BILLING SERVICES MONEY TRANSMITTERS LOYALTY SCHEMES

GENER IC PAYME NT INST RUMENTS BANK NOTES OR COINS CHEQUES CREDIT TRANSFERS DIRECT DEBITS DEBIT C ARDS CREDIT CARDS E-MONEY IN ALL ITS FORMS

VALUE ADDED SERVICES

CARRI ER/ AUTHEN T ICAT ION DEVICE PAPER/COINS (signa t ure, cheque card) ELECTRONIC FORM (digi t al signa t ure) ACCOUNT NUMBER (SSL, PIN, pas sword, TAN , one - t ime code, card, personal c ard read e r,...) CARD (signa t ure, PIN) CARD NUMBER (expir y da t e, CVC/ CVV, password, card, personal c ard read e r, one - t ime code...) TAG, K EY, WATCH, STICKE R, (CHIP IN) MOBILE PH ONE OR PDA, . .. SIM-CARD HARD DISK OF PC, TV, . .. SERVER-BASED WAL LET CODE O N SCRATCH CARD E-MAIL ADD RESS (password)

BIOMETRICS

. ..

NETW ORKS NO NE SCHEME (Visa, Mas t erCard, local debi t card schemes, ...) BANKS NON -BANKS INTER NET MOBILE OR FIXED TELEPHO NE LINES ... CHANNELS NO NE BANKS CONTACT / CONTACTLESS (NFC, RFID, Blue t oo t h, .. . ) INTER NET MOBILE OR FIXED TE LEPHON E LINES ...

CORE PAYME NT MECHANISMS

CREDIT ING PUSH DEBITI NG PULL

TYPES OF MONEY

CURRENCY GIRAL MONEY

E-MONEY PRIVATE CURRENCY

COLLECTION/ BILLING SERVICES MONEY TRANSMITTERS LOYALTY SCHEMES

GENER IC PAYME NT INST RUMENTS BANK NOTES OR COINS CHEQUES CREDIT TRANSFERS DIRECT DEBITS DEBIT C ARDS CREDIT CARDS E-MONEY IN ALL ITS FORMS

VALUE ADDED SERVICES

CARRI ER/ AUTHEN T ICAT ION DEVICE PAPER/COINS (signa t ure, cheque card) ELECTRONIC FORM (digi t al signa t ure) ACCOUNT NUMBER (SSL, PIN, pas sword, TAN , one - t ime code, card, personal c ard read e r,...) CARD (signa t ure, PIN) CARD NUMBER (expir y da t e, CVC/ CVV, password, card, personal c ard read e r, one - t ime code...) TAG, K EY, WATCH, STICKE R, (CHIP IN) MOBILE PH ONE OR PDA, . .. SIM-CARD HARD DISK OF PC, TV, . .. SERVER-BASED WAL LET CODE O N SCRATCH CARD E-MAIL ADD RESS (password)

BIOMETRICS

. ..

NETW ORKS NO NE SCHEME (Visa, Mas t erCard, local debi t card schemes, ...) BANKS NON -BANKS INTER NET MOBILE OR FIXED TELEPHO NE LINES ... CHANNELS NO NE BANKS CONTACT / CONTACTLESS (NFC, RFID, Blue t oo t h, .. . ) INTER NET MOBILE OR FIXED TE LEPHON E LINES ...

CORE PAYME NT MECHANISMS

CREDIT ING PUSH DEBITI NG PULL

TYPES OF MONEY

CURRENCY GIRAL MONEY

E-MONEY PRIVATE CURRENCY

COLLECTION/ BILLING SERVICES MONEY TRANSMITTERS LOYALTY SCHEMES

GENER IC PAYME NT INST RUMENTS BANK NOTES OR COINS CHEQUES CREDIT TRANSFERS DIRECT DEBITS DEBIT C ARDS CREDIT CARDS E-MONEY IN ALL ITS FORMS

VALUE ADDED SERVICES

CARRI ER/ AUTHEN T ICAT ION DEVICE PAPER/COINS (signa t ure, cheque card) ELECTRONIC FORM (digi t al signa t ure) ACCOUNT NUMBER (SSL, PIN, pas sword, TAN , one - t ime code, card, personal c ard read e r,...) CARD (signa t ure, PIN) CARD NUMBER (expir y da t e, CVC/ CVV, password, card, personal c ard read e r, one - t ime code...) TAG, K EY, WATCH, STICKE R, (CHIP IN) MOBILE PH ONE OR PDA, . .. SIM-CARD HARD DISK OF PC, TV, . .. SERVER-BASED WAL LET CODE O N SCRATCH CARD E-MAIL ADD RESS (password)

BIOMETRICS

. ..

NETW ORKS NO NE SCHEME (Visa, Mas t erCard, local debi t card schemes, ...) BANKS NON -BANKS INTER NET MOBILE OR FIXED TELEPHO NE LINES ... CHANNELS NO NE BANKS CONTACT / CONTACTLESS (NFC, RFID, Blue t oo t h, .. . ) INTER NET MOBILE OR FIXED TE LEPHON E LINES ...

CORE PAYME NT MECHANISMS

CREDIT ING PUSH DEBITI NG PULL

TYPES OF MONEY

CURRENCY GIRAL MONEY

E-MONEY PRIVATE CURRENCY

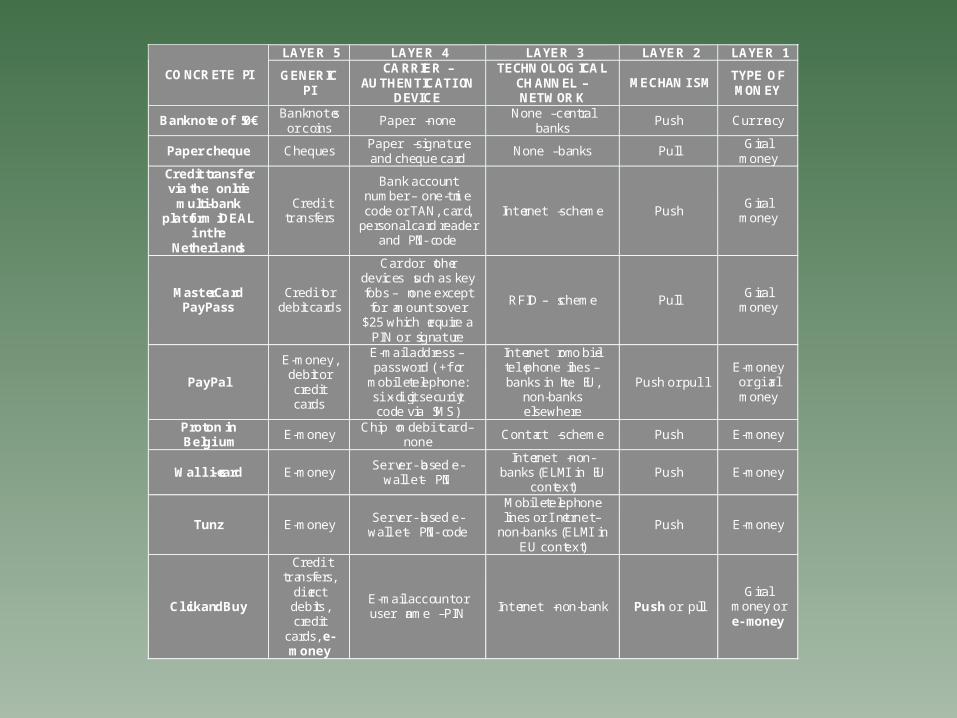

LAYER 5 LAYER 4 LAYER 3 LAYER 2 LAYER 1

CONCRETE PI GENERICPI

CARRIER –AUTHENTICATION

DEVICE

TECHNOLOGICALCHANNEL –NETWORK

MECHANISMTYPE OFMONEY

Banknote of 50€Banknotes

or coinsPaper – none

None – centralbanks

Push Currency

Paper cheque ChequesPaper – signatureand cheque card

None – banks PullGiral

moneyCredit transfervia the online

multi-bankplatform iDEAL

in theNetherlands

Credittransfers

Bank accountnumber – one-timecode or TAN, card,

personal card readerand PIN-code

Internet – scheme PushGiral

money

MasterCardPayPass

Credit ordebit cards

Card or otherdevices such as keyfobs – none exceptfor amounts over

$25 which require aPIN or signature

RFID – scheme PullGiral

money

PayPal

E-money,debit orcreditcards

E-mail address –password (+ for

mobile telephone:six-digit securitycode via SMS)

Internet or mobiletelephone lines –banks in the EU,

non-bankselsewhere

Push or pullE-moneyor giralmoney

Proton inBelgium

E-moneyChip on debit card –

noneContact – scheme Push E-money

Wallie-card E-moneyServer-based e-

wallet – PIN

Internet – non-banks (ELMI in EU

context)Push E-money

Tunz E-moneyServer-based e-

wallet – PIN-code

Mobile telephonelines or Internet –

non-banks (ELMI inEU context)

Push E-money

ClickandBuy

Credittransfers,

directdebits,credit

cards, e-money

E-mail account oruser name – PIN Internet – non-bank Push or pull

Giralmoney ore-money

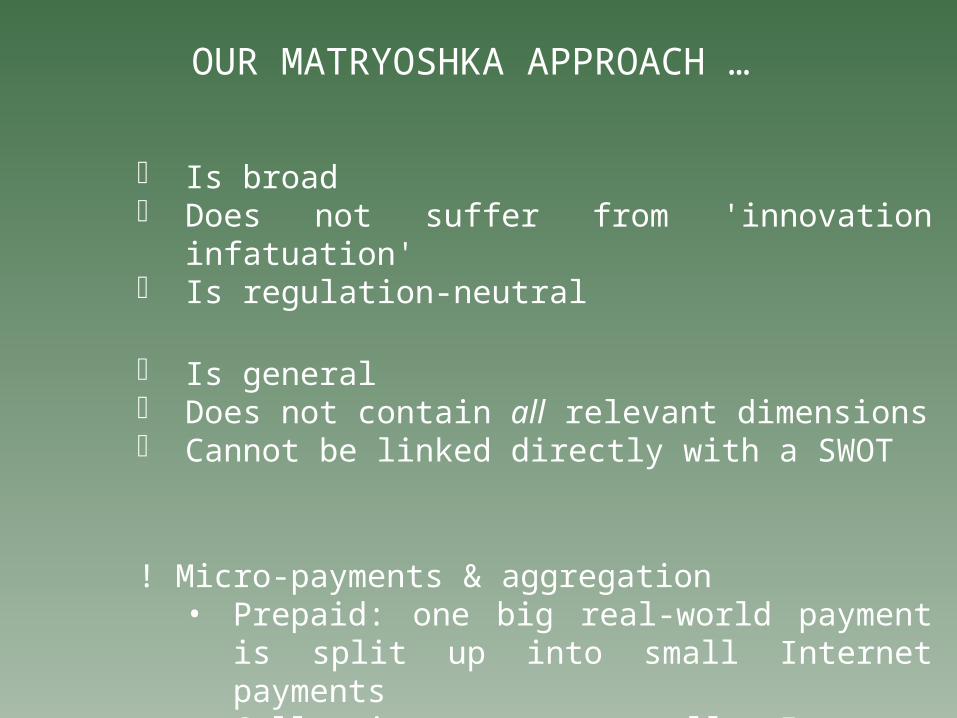

OUR MATRYOSHKA APPROACH …

Is broad Does not suffer from 'innovation infatuation' Is regulation-neutral

Is general Does not contain all relevant dimensions Cannot be linked directly with a SWOT

! Micro-payments & aggregation• Prepaid: one big real-world payment is split up

into small Internet payments• Collection: many small Internet payments are

aggregated into one big real-world payment

-11/26-

AGENDA

I. CLASSIFYING PIS: A MATRYOSHKA APPROACH

II. PIS OFFERED BY NP SITES: 2008 VS. 2006

III. SWOT-ANALYSIS

IV. CONCLUSION

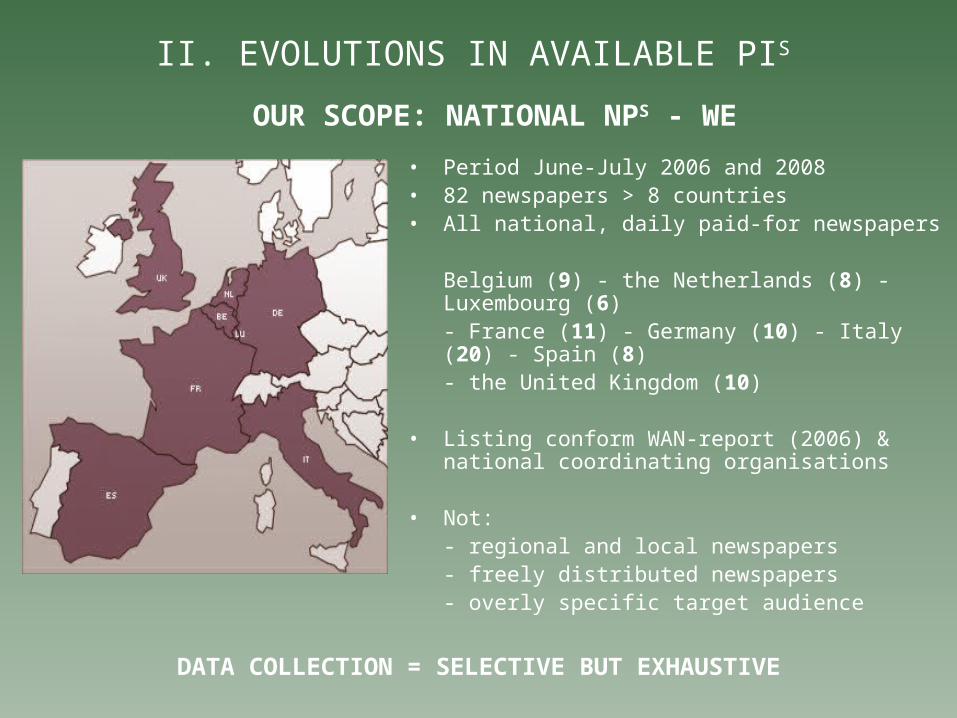

II. EVOLUTIONS IN AVAILABLE PIS

OUR SCOPE: NATIONAL NPS - WE

• Period June-July 2006 and 2008• 82 newspapers > 8 countries• All national, daily paid-for newspapers

Belgium (9) - the Netherlands (8) - Luxembourg (6)- France (11) - Germany (10) - Italy (20) - Spain (8)- the United Kingdom (10)

• Listing conform WAN-report (2006) & national coordinating organisations

• Not: - regional and local newspapers- freely distributed newspapers - overly specific target audience

DATA COLLECTION = SELECTIVE BUT EXHAUSTIVE

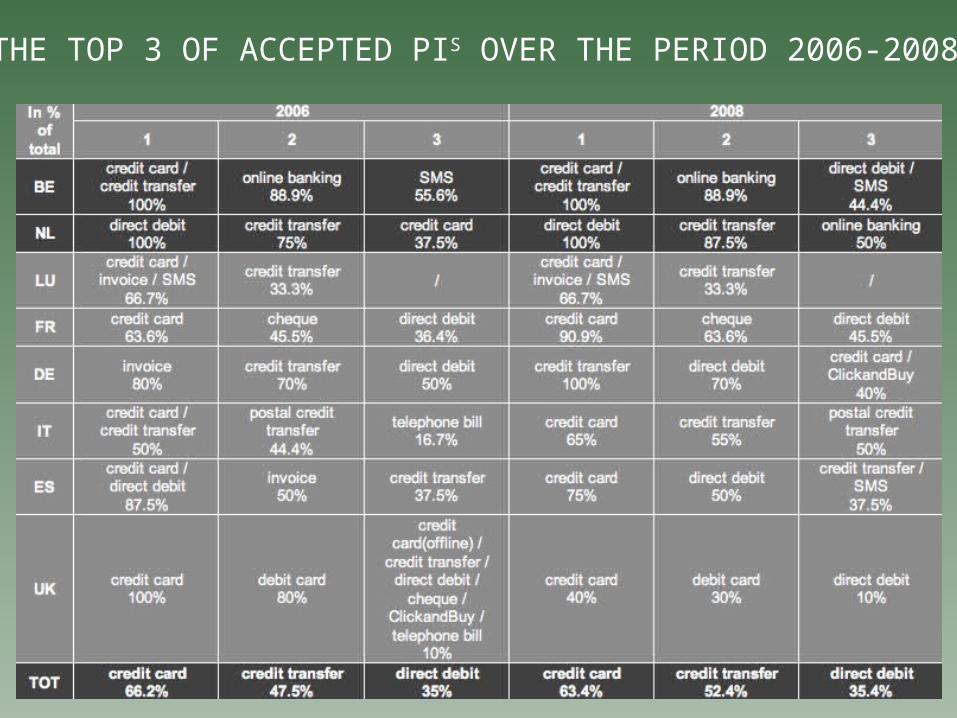

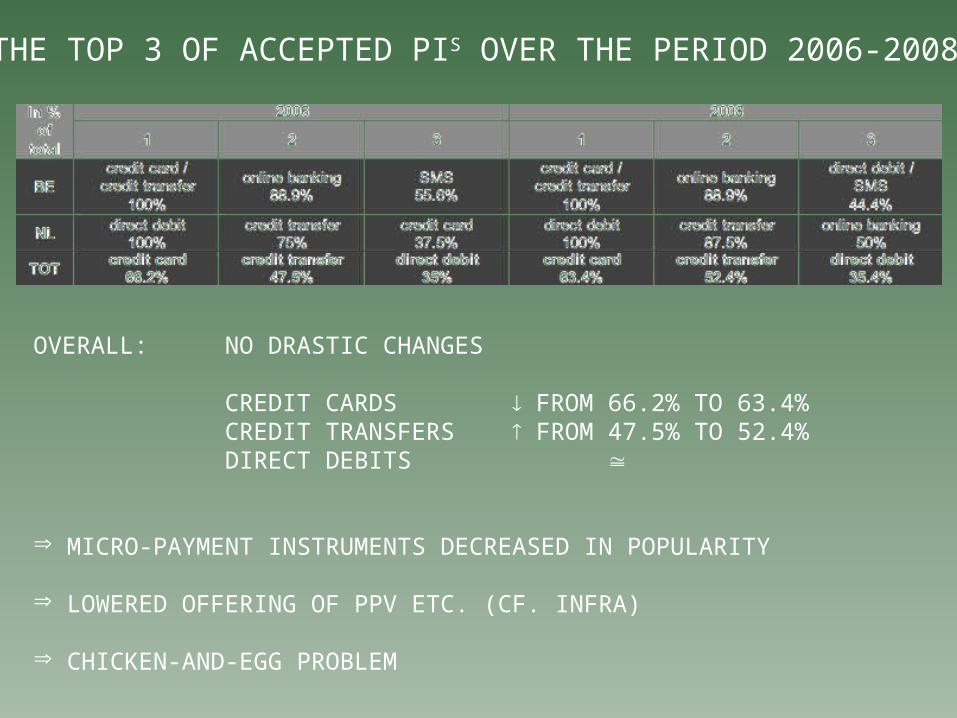

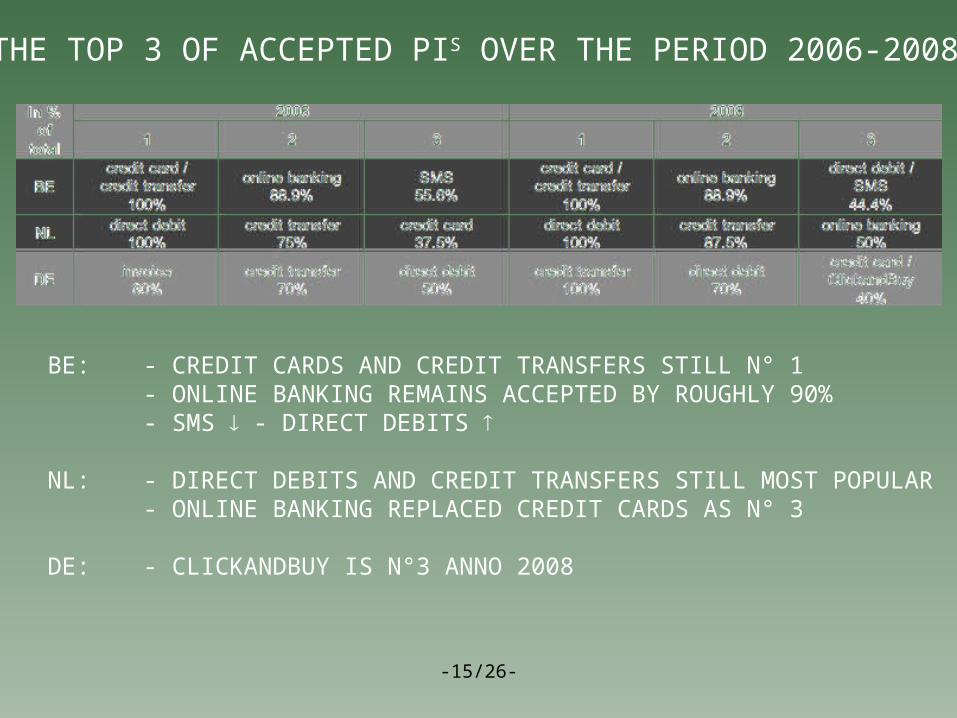

THE TOP 3 OF ACCEPTED PIS OVER THE PERIOD 2006-2008

THE TOP 3 OF ACCEPTED PIS OVER THE PERIOD 2006-2008

OVERALL: NO DRASTIC CHANGES

CREDIT CARDS FROM 66.2% TO 63.4%CREDIT TRANSFERS FROM 47.5% TO 52.4%DIRECT DEBITS

MICRO-PAYMENT INSTRUMENTS DECREASED IN POPULARITY

LOWERED OFFERING OF PPV ETC. (CF. INFRA)

CHICKEN-AND-EGG PROBLEM

-15/26-

THE TOP 3 OF ACCEPTED PIS OVER THE PERIOD 2006-2008

BE: - CREDIT CARDS AND CREDIT TRANSFERS STILL N° 1- ONLINE BANKING REMAINS ACCEPTED BY ROUGHLY 90%- SMS - DIRECT DEBITS

NL: - DIRECT DEBITS AND CREDIT TRANSFERS STILL MOST POPULAR- ONLINE BANKING REPLACED CREDIT CARDS AS N° 3

DE: - CLICKANDBUY IS N°3 ANNO 2008

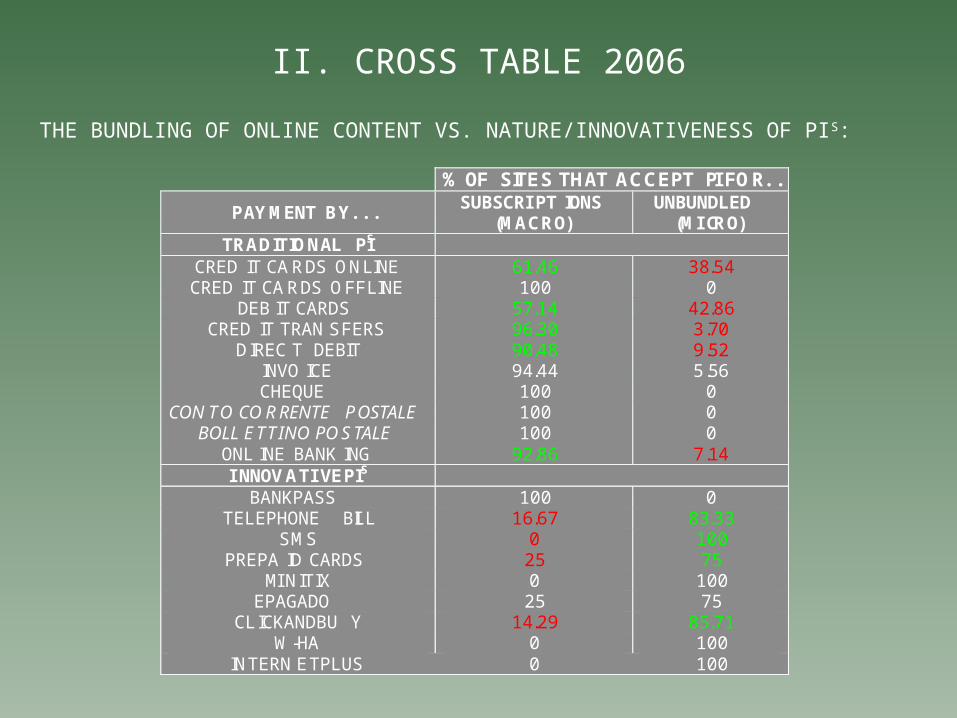

II. CROSS TABLE 2006

% OF SITES THAT ACCEPT PI FOR...

PAYMENT BY... SUBSCRIPTIONS

(MACRO) UNBUNDLED

(MICRO) TRADITIONAL PIS

CREDIT CARDS ONLINE 61.46 38.54 CREDIT CARDS OFFLINE 100 0

DEBIT CARDS 57.14 42.86 CREDIT TRANSFERS 96.30 3.70

DIRECT DEBIT 90.48 9.52 INVOICE 94.44 5.56 CHEQUE 100 0

CONTO CORRENTE POSTALE 100 0 BOLLETTINO POSTALE 100 0

ONLINE BANKING 92.86 7.14 INNOVATIVE PIS

BANKPASS 100 0 TELEPHONE BILL 16.67 83.33

SMS 0 100 PREPAID CARDS 25 75

MINITIX 0 100 EPAGADO 25 75

CLICKANDBUY 14.29 85.71 W-HA 0 100

INTERNETPLUS 0 100

THE BUNDLING OF ONLINE CONTENT VS. NATURE/INNOVATIVENESS OF PIS:

-17/26-

AGENDA

I. CLASSIFYING PIS: A MATRYOSHKA APPROACH

II. PIS OFFERED BY NP SITES: 2008 VS. 2006

III. SWOT-ANALYSIS

IV. CONCLUSION

-18/26-

III. SWOT-ANALYSIS OF THE MOST PREVALENT PIS

III.1 CREDIT CARDS

III.2 CREDIT TRANSFERS

III.3 DIRECT DEBITS

III.4 ONLINE BANKING

III.5 SMS

-19/26-

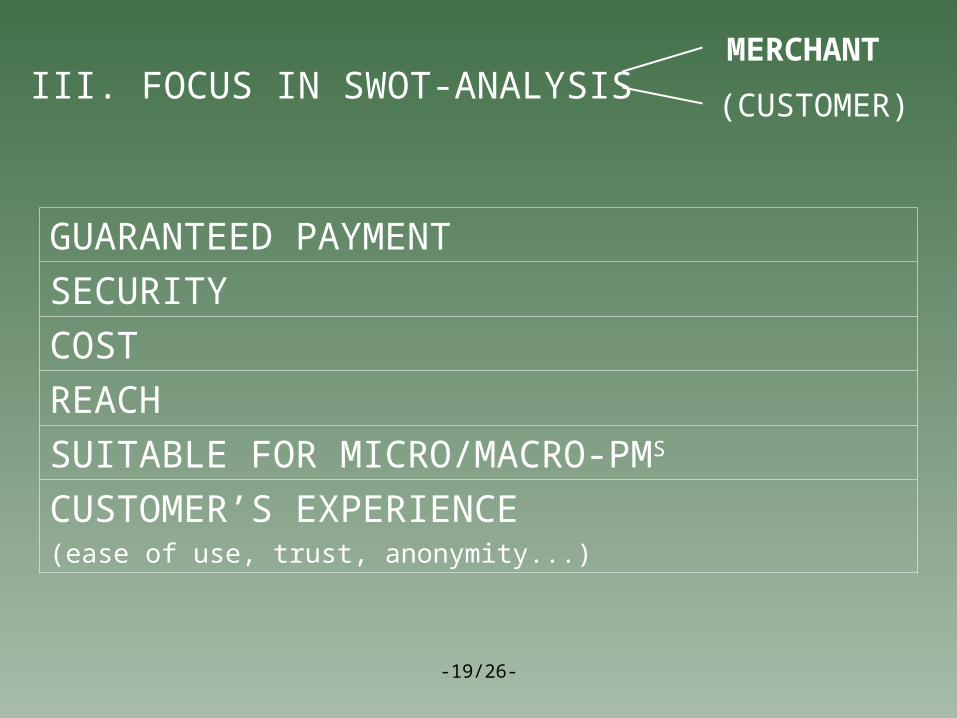

III. FOCUS IN SWOT-ANALYSIS

GUARANTEED PAYMENT

SECURITY

COST

REACH

SUITABLE FOR MICRO/MACRO-PMS

CUSTOMER’S EXPERIENCE (ease of use, trust, anonymity...)

MERCHANT

(CUSTOMER)

-20/26-

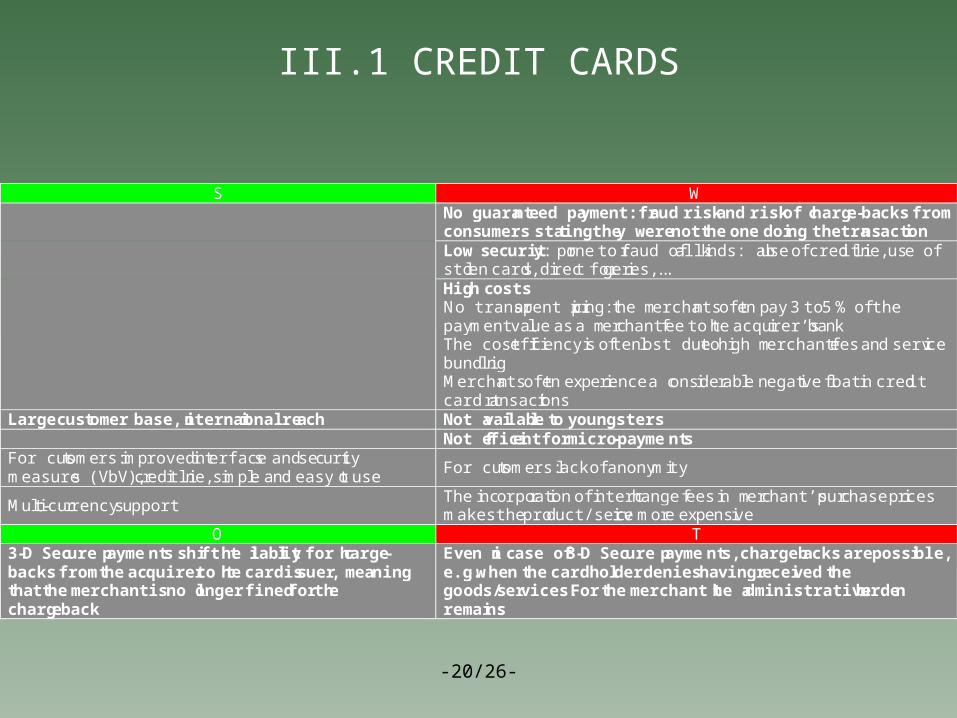

III.1 CREDIT CARDS

S W

No guara n teed pa yment: fr au d risk an d risk of c h arg e-b acks from co n su mers sta ting the y were n ot th e one doi n g the tra n sact io n

Low sec u rit y : pr one to f raud of a ll k inds: ab use of cred it line, us e of sto len card s, d irec t for ger ies, ...

Hig h costs N o transp arent pr ic ing: the m ercha nts oft en pay 3 to 5 % of the pay m ent va lue as a m er chant fee to the acqu irer’s ba nk The cost eff ic iency is o ften lost due to h igh m erchant fees and serv ice bund ling M ercha nts oft en experience a c ons ide rab le negat ive float in cred it card t ransact ions

Large cu stomer base, in ternat io n al re ach Not a va ilab le to you ngsters Not e ffici en t for micro -payme n ts For cus tom ers: im proved in terface s and se curi ty m easure s (VbV), cred it line, s im p le and easy to use For cus tom ers: lack of anony m ity

M u lti-cu rrency support The inc orpo rat ion of interc hange fees in m er chant’s pur chase prices m akes the pro duct/serv ice m ore expens ive

O T 3-D Sec u re p ayme n ts sh ift t h e l iabi lit y for c h arge -backs from th e ac qu irer to t h e card is su er , mea n ing th at th e merc h ant is n o longer fined for th e ch arg eback

Even in case of 3-D Sec u re p ayme n ts, chargeb acks are poss ible, e.g. w h en th e card hol der denies ha v ing recei ved th e go ods/ ser v ices. For th e merc h ant th e a dmi n istrative b u rde n remai n s

-21/26-

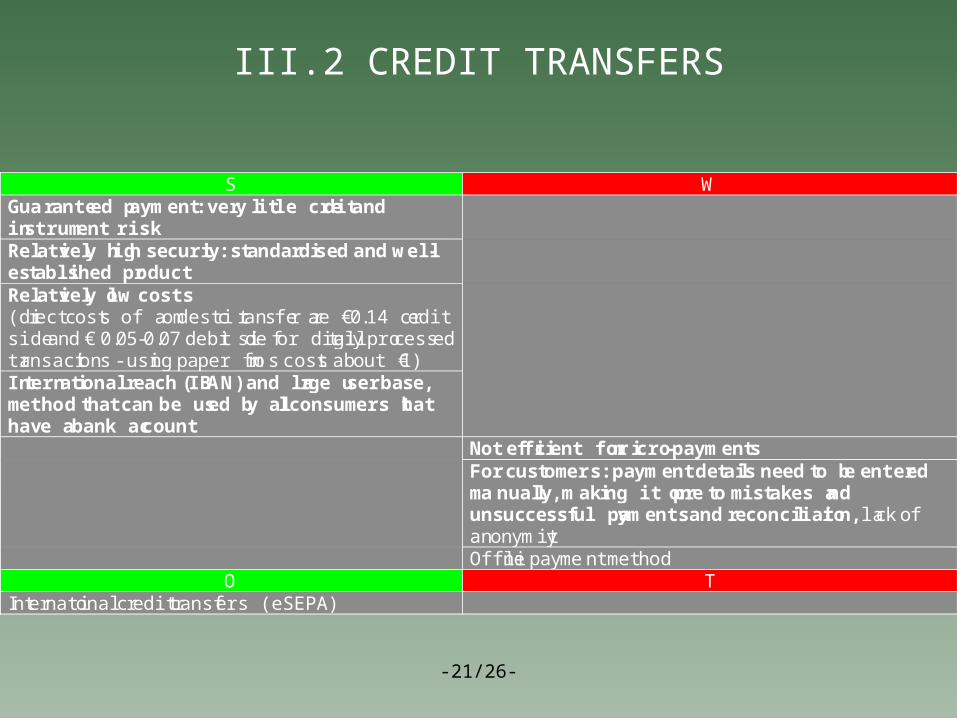

III.2 CREDIT TRANSFERS

S W Gua ran te ed p aym ent: ver y lit tle cre d it an d in s trum ent risk

Rel a tivel y h ig h securi ty: s tan da rdi se d an d w ell -es tab lished pr o du ct

Rel a tivel y lo w co sts (di rect cost s of a d om esti c t ran s fe r a re € 0 .14 cr edit side and € 0. 05-0. 07 debi t si de for digi tall y p ro cess ed transact ion s - usi ng paper fo rm s cost s ab out € 1 )

In tern a tion al reach (IB A N ) and la rge u ser base , met ho d tha t can b e us ed b y al l cons umers t h at hav e a ba nk ac co un t

Not effic ient for m icro -paym ents

For cu stomer s : p aym en t d etai ls n eed to b e en ter ed ma n ual ly , m ak ing it pr on e to mi s tak es a n d un su ccessful pa ym en ts and recon ci liat io n, la ck o f an onym ity

Offli ne payme n t met hod O T

Int e rnati onal c redit transf e rs (eSEPA)

-22/26-

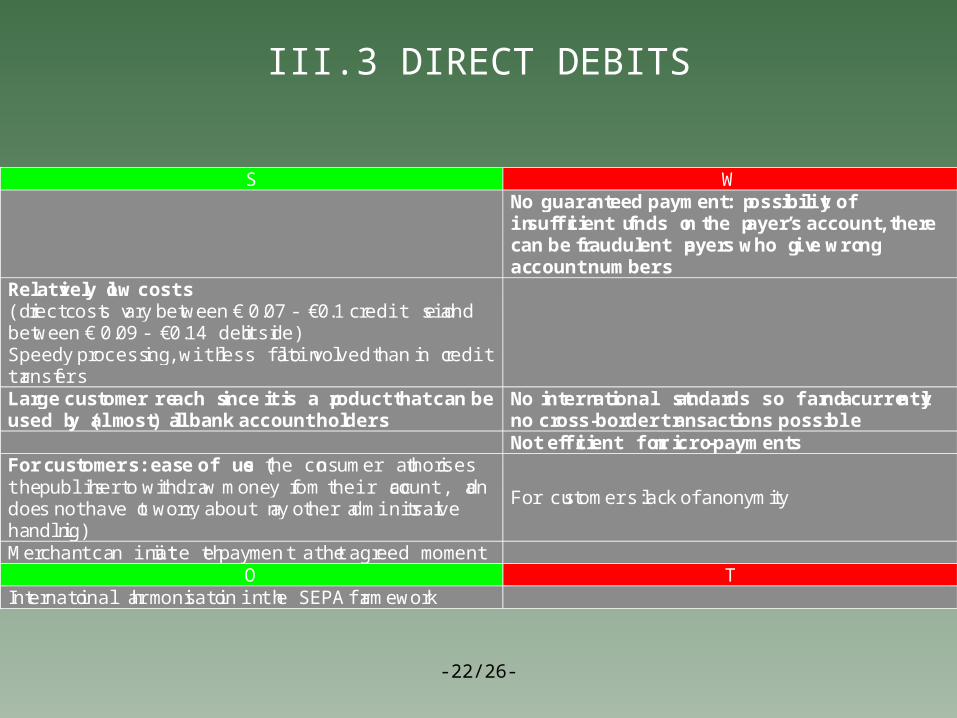

III.3 DIRECT DEBITS

S W

No gu ara n teed p aym ent: p o ss ibi lity of in suffic ient f un ds o n the p ayer ’s accou nt, ther e can b e frau du lent p ayer s w ho g iv e w ro n g ac co un t n um bers

Rel a tivel y lo w co sts (di rect cost s v a ry bet w een € 0. 07 - € 0 .1 credit sid e and bet w een € 0. 09 - € 0. 14 deb it si de) Spe edy p rocess ing , w ith less flo a t in vo lved than in c redit transf e rs

Lar g e cu stomer re ach s ince it is a p rod uc t tha t ca n b e used b y (a lm o st ) a ll b an k acco un t h ol d ers

No in tern a tion al st an dar d s so far a n d curre n tly no cr o ss -b or d er tr ans actio ns p ossi b le

Not effic ient for m icro -paym ents For cu stomer s : eas e o f us e ( the co ns um er au thor ises the publis her to w ithd ra w m one y f rom their ac count, an d doe s not hav e to w orry about a ny o ther a dm inis trat ive ha ndli ng)

Fo r cu s tom ers: lac k o f anonym ity

M erchan t ca n init iate th e paymen t at t he agr eed moment O T

Int e rnati onal h a rmoni sati on in th e SEPA fram ew or k

-23/26-

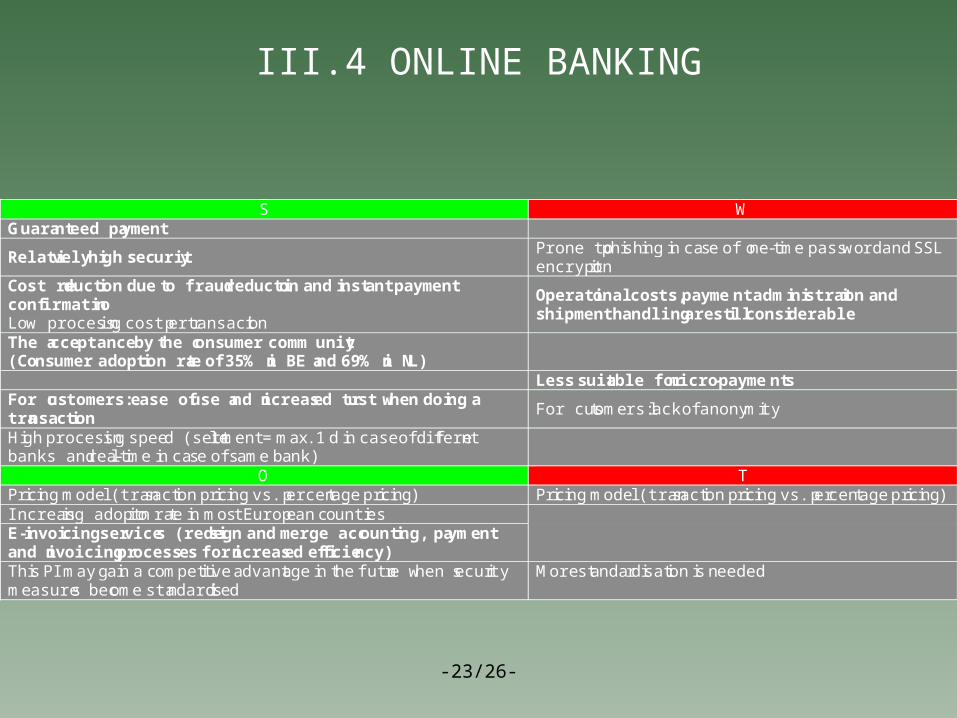

III.4 ONLINE BANKING

S W G u ara n teed pa yment

Relati vely h ig h sec u rit y Prone to ph ish ing in ca se of o ne -tim e pass w ord and SSL encrypt ion

Cost re du ct io n due to fraud reducti on an d in st an t pa yment co n firmatio n Lo w process in g cost p er transact ion

Operati on al co sts, payme n t adm in istrat ion an d sh ipment ha n dling are st ill con s iderable

T h e a cce ptance by th e c o n su mer comm u nit y (Co n su mer ad opt io n ra te of 35 % in BE a n d 69 % in N L)

Less su it able for micro -pa yme n ts For c u stomers: ease of u se a n d in creas ed tr u st w h en do in g a tra n sa ction

For cus tom ers: lack of anony m ity

H igh process in g spee d (sett le m ent = m ax. 1 d in case of d if fere nt banks and rea l-tim e in ca se of sam e bank)

O T Pr ic ing m ode l (tran sact ion pric ing vs. p ercen tage pr ic ing) Pr ic ing m ode l (tran sact ion pric ing vs. p er cen tage pr ic ing) Increas ing adopt io n ra te in m ost Europ ean countr ies E-inv oi cing ser v ice s (rede sign and merge acc oun tin g , pa ym en t an d inv oicing pr ocess es for in creas ed e fficie n cy)

Th is PI m ay ga in a com pet itive advant age in the futu re w hen s ecur ity m easure s bec om e sta ndard ised

M ore st anda rd isat ion is needed

-24/26-

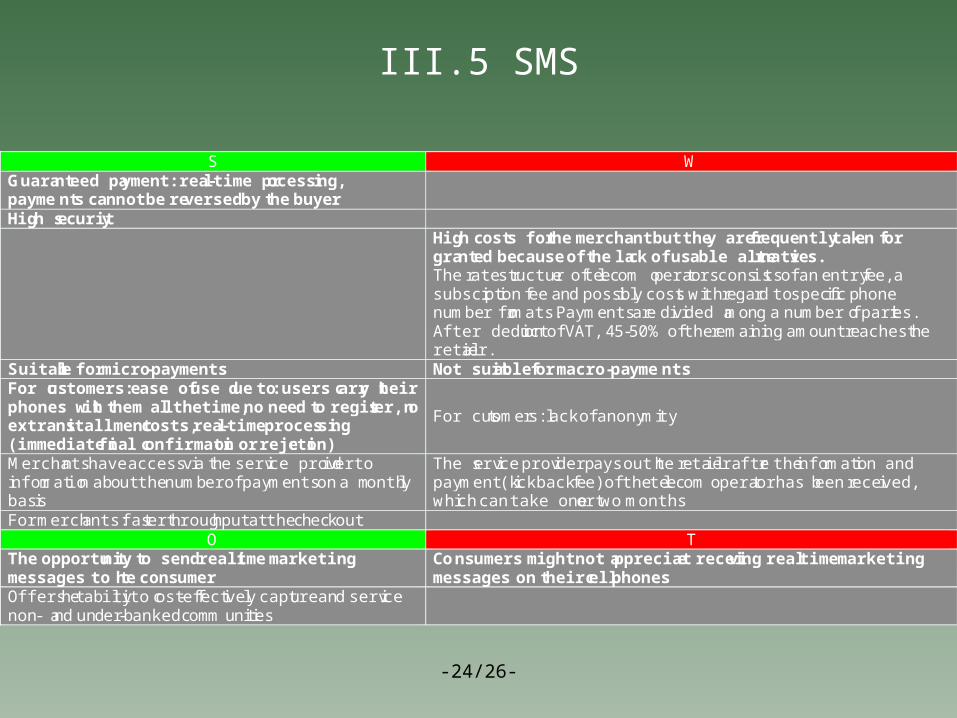

III.5 SMS

S W G u ara n teed pa yment: rea l-time pr ocess in g, pa yme n ts cann ot be re versed b y th e b uy er

Hig h s ecu rit y

Hig h cost s for th e merc h an t but the y are freq u en tly tak en for gra n ted b ecause of th e la ck o f u sable alte rn ati ves. The rate st ructur e of te lecom o pera tors cons is ts of an entry fee, a subscr ipt ion fee and poss ib ly cost s w ith rega rd to spec ific phone nu m be r fo rm ats. Pay m ents a re d iv ided a m ong a nu m ber o f part ies. After deduct ion of VAT, 45 -50% of the rem a in ing am ount reaches the reta iler.

Su itab le for mi cro -pa yments Not suit able for macro -p ayme n ts For c u stomers: ease of u se d u e to : u sers c arr y t h eir p h on es w it h th em a ll the time, n o n eed to regis ter, n o extra i n stallment costs, rea l-time proces si n g (immediate fi n a l c on firmati on or reje cti on )

For cus tom ers: lack of anony m ity

M ercha nts have access v ia the serv ice prov id er to infor m at io n ab out the nu m ber of pay m ents on a m onth ly bas is

The s erv ice prov ider pays out the reta iler afte r the info rm at ion and pay m ent (k ickback fee) of the te lecom opera tor has b een rece ived, w h ich can take one or tw o m onths

For m erch ants: fas ter throug hput at the chec kout O T

T h e o pportu n ity to send real t ime marketing messages to t h e cons u mer

Co n su mers mi gh t n o t a ppreciat e recei v in g real time marketing messages o n th eir c ell ph on es

Offers t he ab ili ty to c ost -ef fect ive ly capt ure an d serv ice non - a nd un der -banked comm un ities

-25/26-

III. TO SUM UP...

CREDIT CARDCREDIT

TRANSFERDIRECT DEBIT

ONLINE BANKING

SMS

GUARANTEED

PM X X SECURITY X ~

COST X ~ XREACH ~

MICRO-PMS X X X X ATTRACTIVE

TO CUSTOMERS ~

IV. CONCLUSION

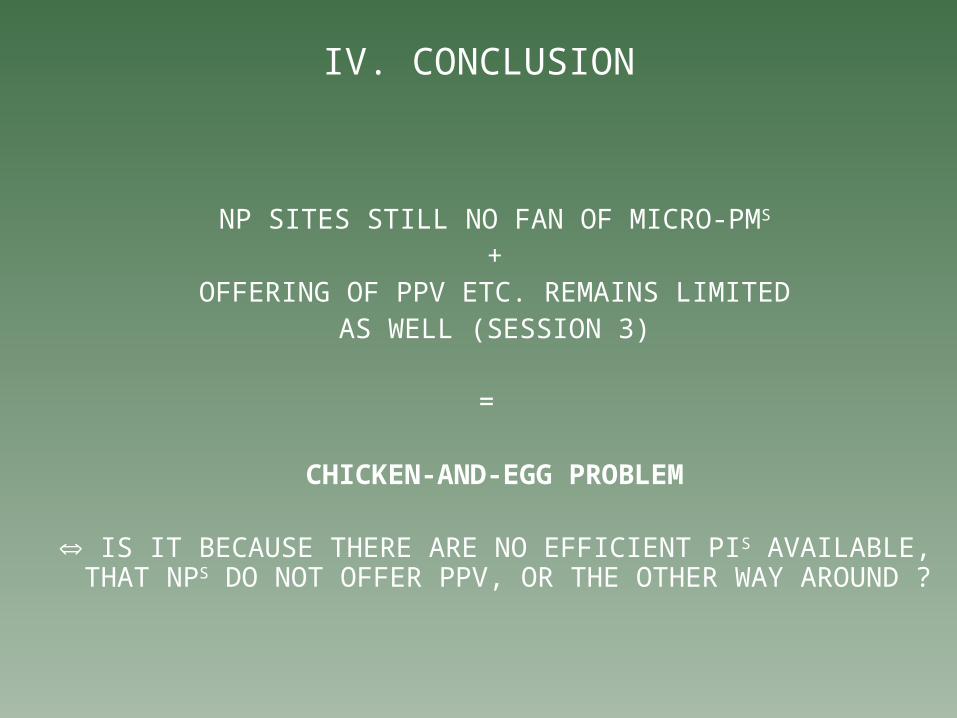

NP SITES STILL NO FAN OF MICRO-PMS

+OFFERING OF PPV ETC. REMAINS LIMITED

AS WELL (SESSION 3)

=

CHICKEN-AND-EGG PROBLEM

IS IT BECAUSE THERE ARE NO EFFICIENT PIS AVAILABLE, THAT NPS DO NOT OFFER PPV, OR THE OTHER WAY

AROUND ?