horizon asia opportunity q4 2016...

TRANSCRIPT

MARKET COMMENTARY

© 2017 Horizon Kinetics LLC ®

Horizon Asia Opportunity Q4 2016 Commentary February 2017

MARKET COMMENTARY 4th Quarter 2016 February 2017

© 2016 Horizon Kinetics LLC ® 1

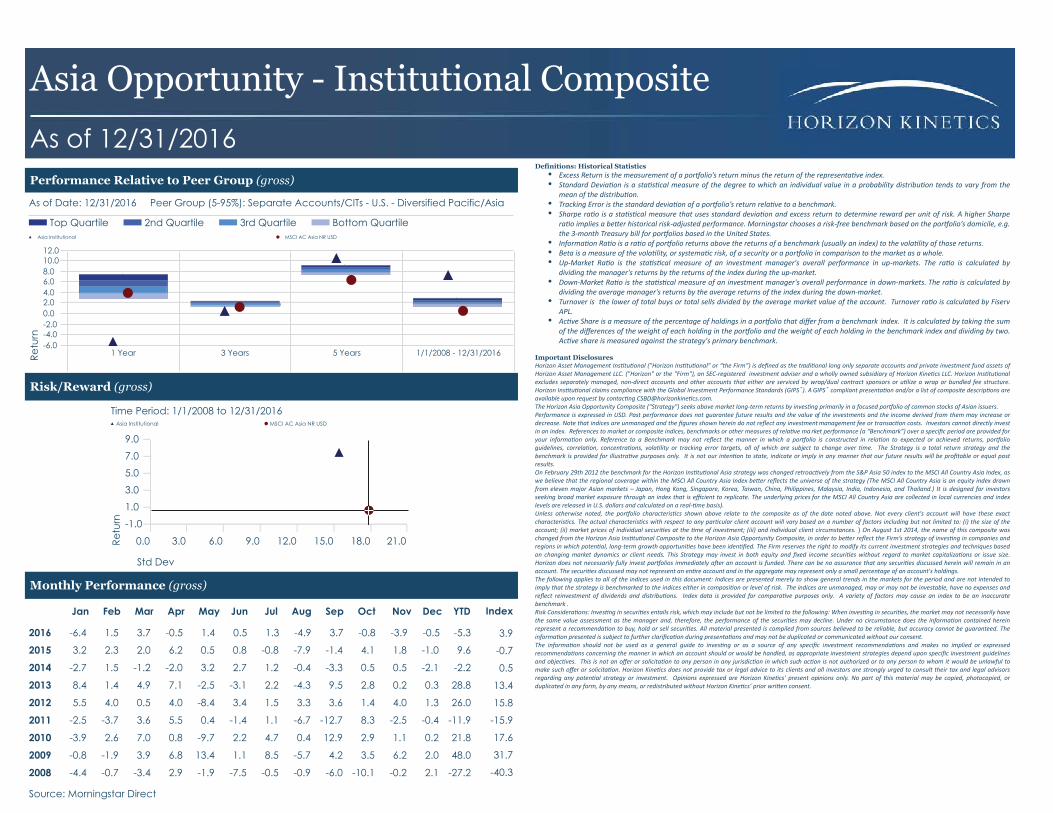

In the fourth quarter of 2016, the Horizon Asia Opportunity Institutional Composite (the “Strategy”) declined

5.4%, net of fees, compared to the MSCI All Countries Asia Index (the “Index”), which declined 3.5%. The

Strategy’s holdings in Asian gaming companies contributed positively. The consumer staples and information

technology names in Japan detracted from performance. In 2016, the Strategy declined 6.2%, net of fees, as

compared to a gain of 3.9% for the Index.

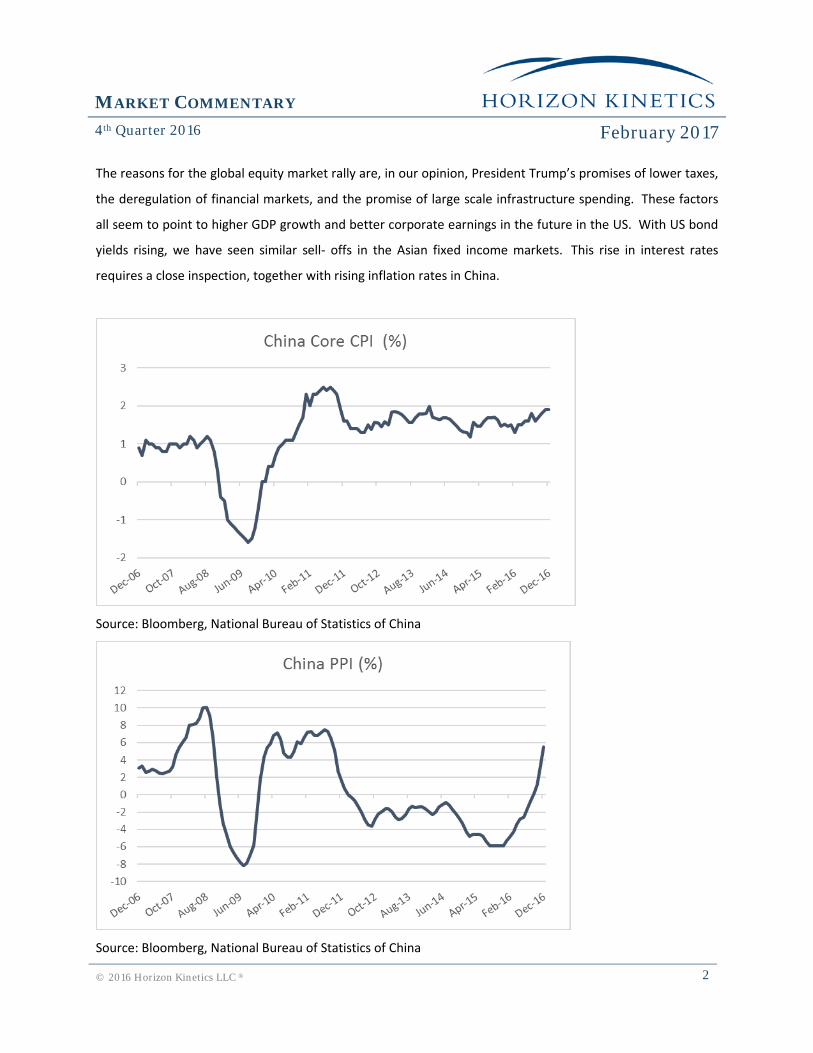

Donald Trump's unexpected presidential election victory brought a very substantial change of direction in the

global financial markets. After the initial sell off, the US equity market engineered one of its best rallies since

2008, rising 4.6%, as measured by the S&P 500 Index. The US Dollar index also rose by 4.4%. On the other

hand, the global fixed income markets retreated sharply, and negative yields in some developed government

bond markets disappeared. The bond market reversal ended a 30+ year bull market, which had pushed the

long term bond yield from 1.85% to 2.44%, as measured by US 10 year government bonds. The financial

markets lost the biggest tail- wind which had existed since the early 1980s.

Source: Bloomberg

MARKET COMMENTARY 4th Quarter 2016 February 2017

© 2016 Horizon Kinetics LLC ® 2

The reasons for the global equity market rally are, in our opinion, President Trump’s promises of lower taxes,

the deregulation of financial markets, and the promise of large scale infrastructure spending. These factors

all seem to point to higher GDP growth and better corporate earnings in the future in the US. With US bond

yields rising, we have seen similar sell- offs in the Asian fixed income markets. This rise in interest rates

requires a close inspection, together with rising inflation rates in China.

Source: Bloomberg, National Bureau of Statistics of China

Source: Bloomberg, National Bureau of Statistics of China

MARKET COMMENTARY 4th Quarter 2016 February 2017

© 2016 Horizon Kinetics LLC ® 3

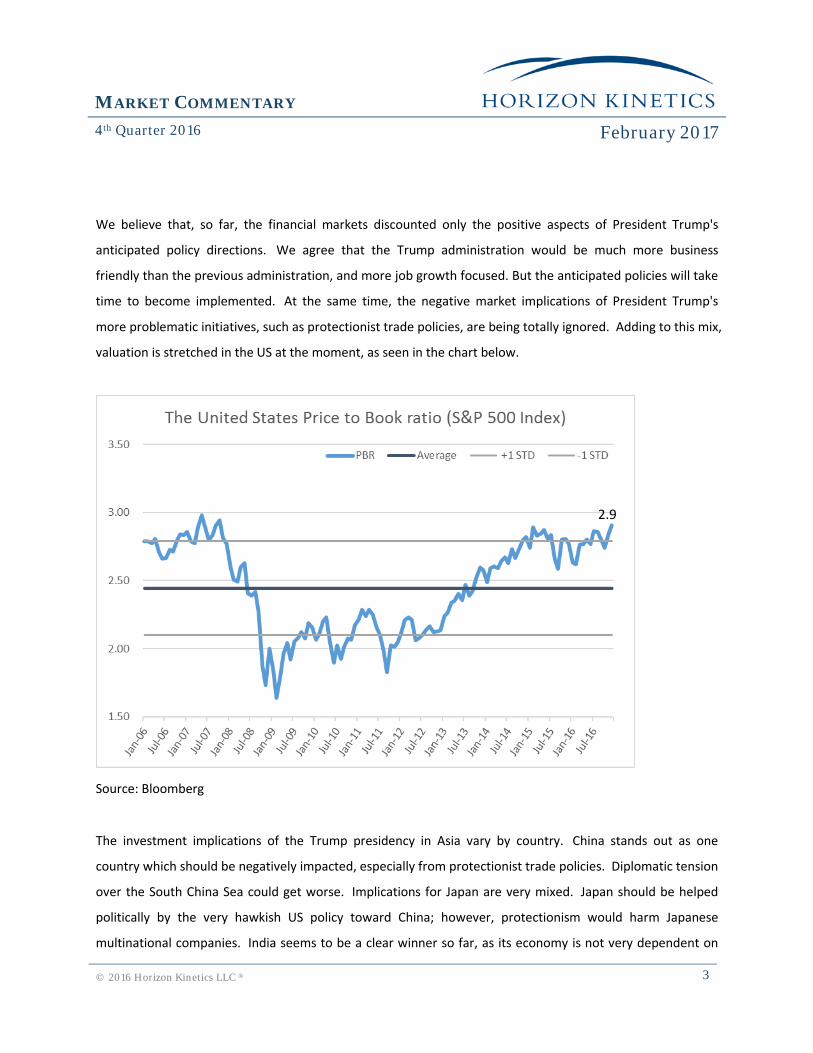

We believe that, so far, the financial markets discounted only the positive aspects of President Trump's

anticipated policy directions. We agree that the Trump administration would be much more business

friendly than the previous administration, and more job growth focused. But the anticipated policies will take

time to become implemented. At the same time, the negative market implications of President Trump's

more problematic initiatives, such as protectionist trade policies, are being totally ignored. Adding to this mix,

valuation is stretched in the US at the moment, as seen in the chart below.

Source: Bloomberg

The investment implications of the Trump presidency in Asia vary by country. China stands out as one

country which should be negatively impacted, especially from protectionist trade policies. Diplomatic tension

over the South China Sea could get worse. Implications for Japan are very mixed. Japan should be helped

politically by the very hawkish US policy toward China; however, protectionism would harm Japanese

multinational companies. India seems to be a clear winner so far, as its economy is not very dependent on

2.9

MARKET COMMENTARY 4th Quarter 2016 February 2017

© 2016 Horizon Kinetics LLC ® 4

trade, and is more affected by domestic consumption. Also, President Trump has reaffirmed US

commitments to the Indo-US political alliance.

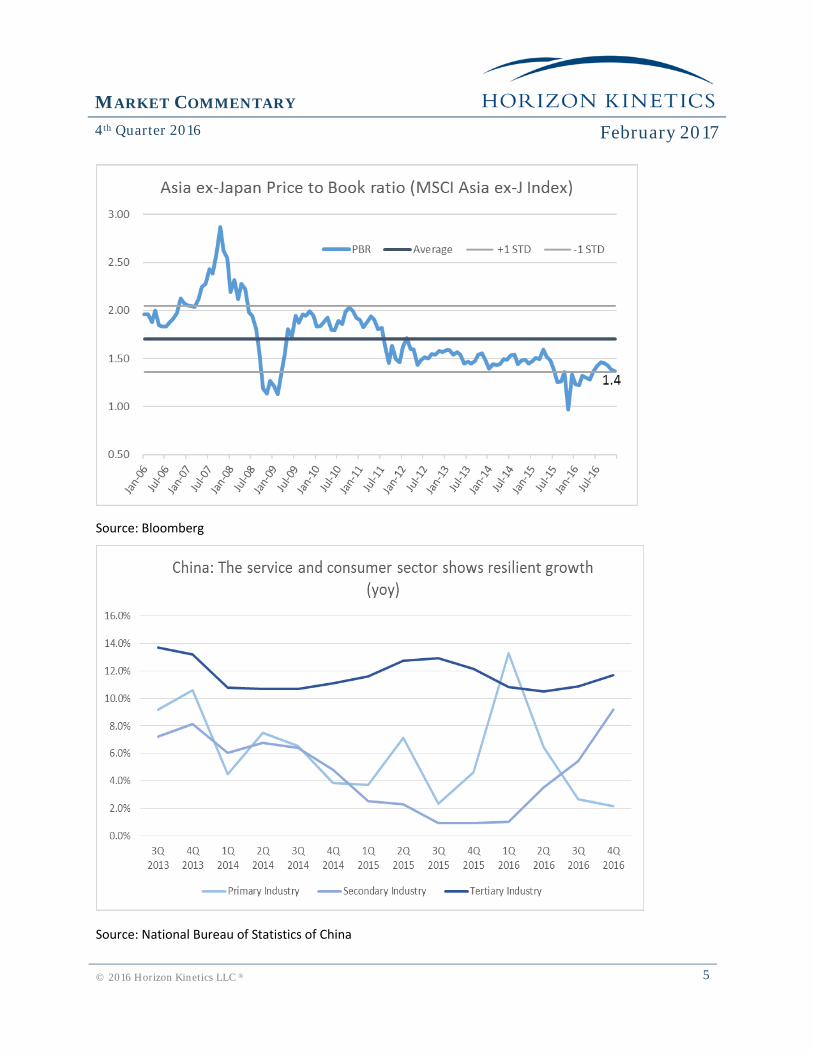

Near term, the most constructive aspects of the Asian equity markets are their very attractive valuation

parameters. (Please see the attached charts). At the same time, most Asian economies are entering a cyclical

recovery phase, as reflected in the most recent governmental economic statistics, which bodes well for the

corporate earnings outlook. We are especially encouraged by consumer spending trends in China. After

going through a major contraction caused by President Xi's campaign against corruption, consumption

spending seems to have stabilized. Also, once troubling capital flight from China seems to be stabilizing as

well. The Chinese Government's more decisive and draconian capital control measures in the past few

months are finally succeeding in stopping illegal capital outflow from the country. For the first time, we have

seen growth in spending on luxury items such as watches. We have seen both sales and profits growth from

European luxury brands companies such as Richmond and LVMH in the most recent quarterly

earnings. Macau’s casinos are seeing renewed sales and earnings growth as well.

Source: Bloomberg

MARKET COMMENTARY 4th Quarter 2016 February 2017

© 2016 Horizon Kinetics LLC ® 5

Source: Bloomberg

Source: National Bureau of Statistics of China

MARKET COMMENTARY 4th Quarter 2016 February 2017

© 2016 Horizon Kinetics LLC ® 6

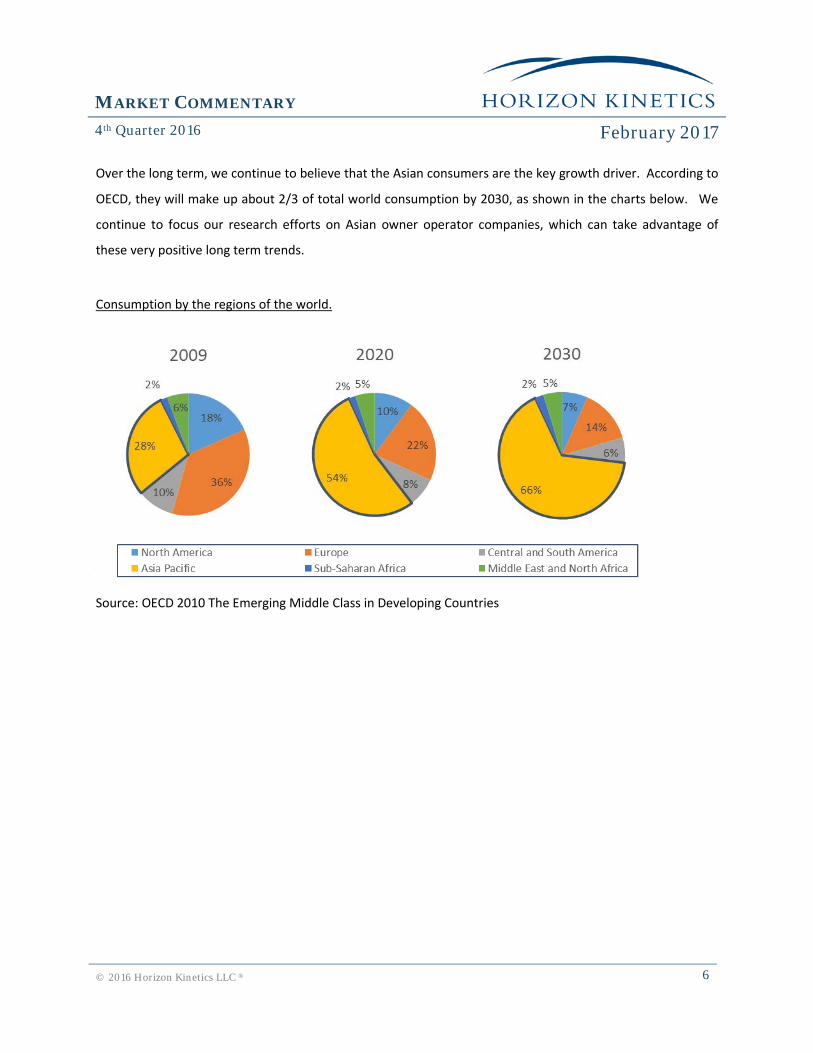

Over the long term, we continue to believe that the Asian consumers are the key growth driver. According to

OECD, they will make up about 2/3 of total world consumption by 2030, as shown in the charts below. We

continue to focus our research efforts on Asian owner operator companies, which can take advantage of

these very positive long term trends.

Consumption by the regions of the world.

\

Source: OECD 2010 The Emerging Middle Class in Developing Countries

MARKET COMMENTARY 4th Quarter 2016 February 2017

© 2016 Horizon Kinetics LLC ® 7

DISCLOSURES

Past performance is not indicative of future returns. This information should not be used as a general guide to investing or as a source of any specific investment recommendations, and makes no implied or expressed recommendations concerning the manner in which an account should or would be handled, as appropriate investment strategies depend upon specific investment guidelines and objectives. This is not an offer to sell or a solicitation to invest.

This information is intended solely to report on the investment strategies of Horizon Kinetics LLC. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. There are risks associated with purchasing and selling securities and options thereon, and investments can lose money.

The MSCI All Countries Asia Index® captures large and mid-cap companies represented across 3 Developed Markets countries and 8 Emerging Markets countries in Asia. With 930 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

TOPIX is a free-float adjusted market capitalization-weighted index that is calculated based on all the domestic common stocks listed on the TSE First Section. TOPIX shows the measure of current market capitalization, assuming that market capitalization as of the base date (January 4, 1968) is 100 points. This is a measure of the overall trend in the stock market, and is used as a benchmark for investments in Japanese stocks.

Note that indices are unmanaged, and the figures shown herein do not reflect any investment management fee or transaction costs. Investors cannot directly invest in an index. References to market or composite indices, benchmarks or other measures of relative market performance (a “Benchmark”) over a specific period are provided for your information only. Reference to a Benchmark may not reflect the manner in which a portfolio is constructed in relation to expected or achieved returns, portfolio guidelines, correlations, concentrations, volatility, or tracking error targets, all of which are subject to change over time. The strategy is a total return strategy, and the benchmark is provided for illustrative purposes only. It is not our intention to state, indicate or imply in any manner that our future results will be profitable or equal to past results.

Horizon Kinetics LLC is the parent company to several US-registered investment advisers, including Horizon Asset Management LLC (“Horizon”) and Kinetics Asset Management LLC (“Kinetics”). Horizon and Kinetics manage separate accounts and pooled products that may hold certain of the securities mentioned herein. Horizon is the investment manager to the strategy referenced herein. For more information on Horizon Kinetics, you may visit our website at www.horizonkinetics.com.

No part of this material may be reproduced or distributed, in whole or in part, without Horizon Kinetics’ prior written consent.

2017 copyright Horizon Kinetics LLC®. All rights reserved.