head office: 71 tulip street cheltenham melbourne offices in capital cities across australia. sydney...

TRANSCRIPT

Head Office: 71 Tulip Street Cheltenham Melbourne

Offices in capital cities across Australia.Sydney | Melbourne | Perth | Brisbane | Adelaide

MY COLLEAGUES

Want to learn more?

• www.mcmasters.com.au• User name sydney123

• Password sydney123

Keep in touch

This is not the Commissioner of Taxation

This is the Commissioner of TaxationMr Michael D’Ascenzo

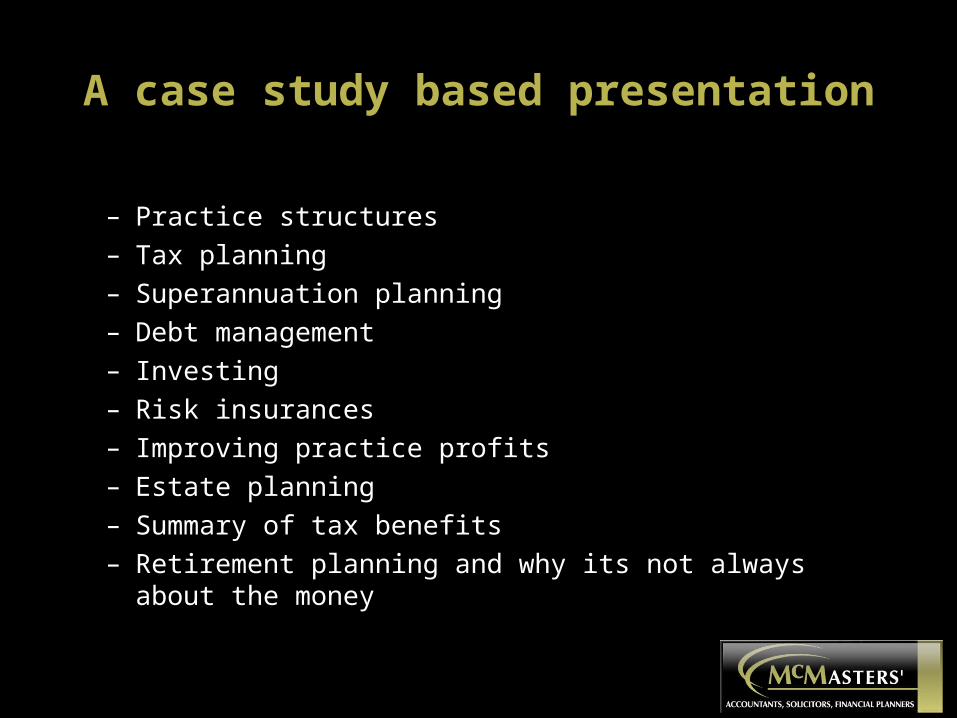

A case study based presentation

– Practice structures– Tax planning– Superannuation planning– Debt management– Investing– Risk insurances– Improving practice profits– Estate planning– Summary of tax benefits– Retirement planning and why its not always about the money

Lucy 28 year old hospital employee

Brad Recently qualified GP

Denzel The 45 year old IMG GP practice owner

NicoleThe 50 year old cardiologist

HelenThe 50 year old employee specialist

MickeyThe tired 60 year old GP

Structures

Structures

Structures

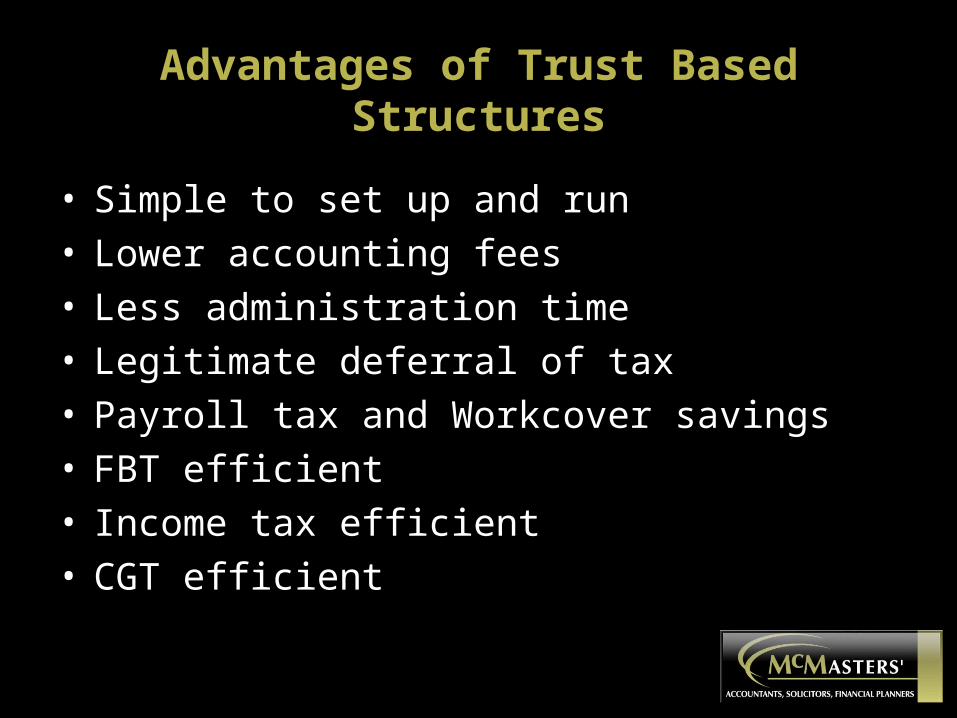

Advantages of Trust Based Structures

• Simple to set up and run• Lower accounting fees• Less administration time• Legitimate deferral of tax• Payroll tax and Workcover savings• FBT efficient• Income tax efficient• CGT efficient

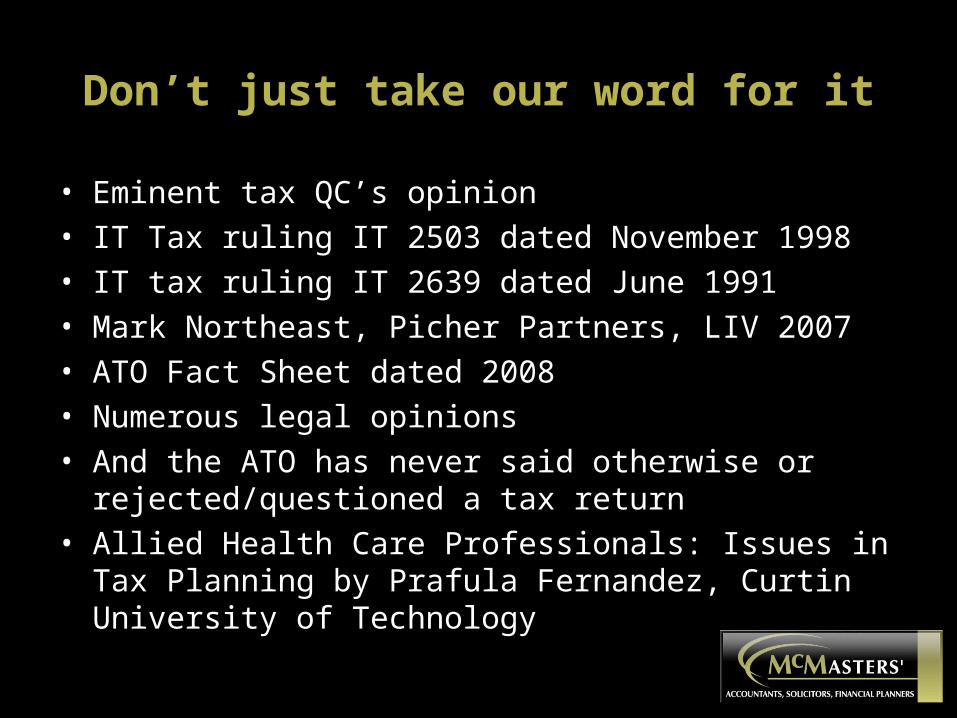

Don’t just take our word for it

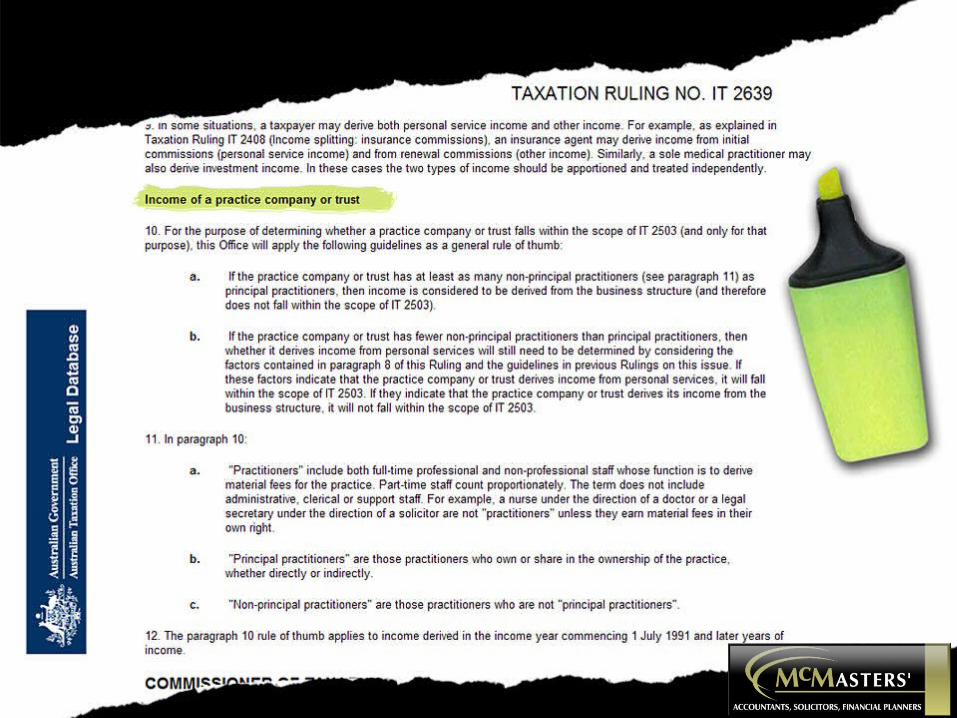

• Eminent tax QC’s opinion• IT Tax ruling IT 2503 dated November 1998• IT tax ruling IT 2639 dated June 1991• Mark Northeast, Picher Partners, LIV 2007• ATO Fact Sheet dated 2008• Numerous legal opinions • And the ATO has never said otherwise or

rejected/questioned a tax return• Allied Health Care Professionals: Issues in Tax Planning

by Prafula Fernandez, Curtin University of Technology

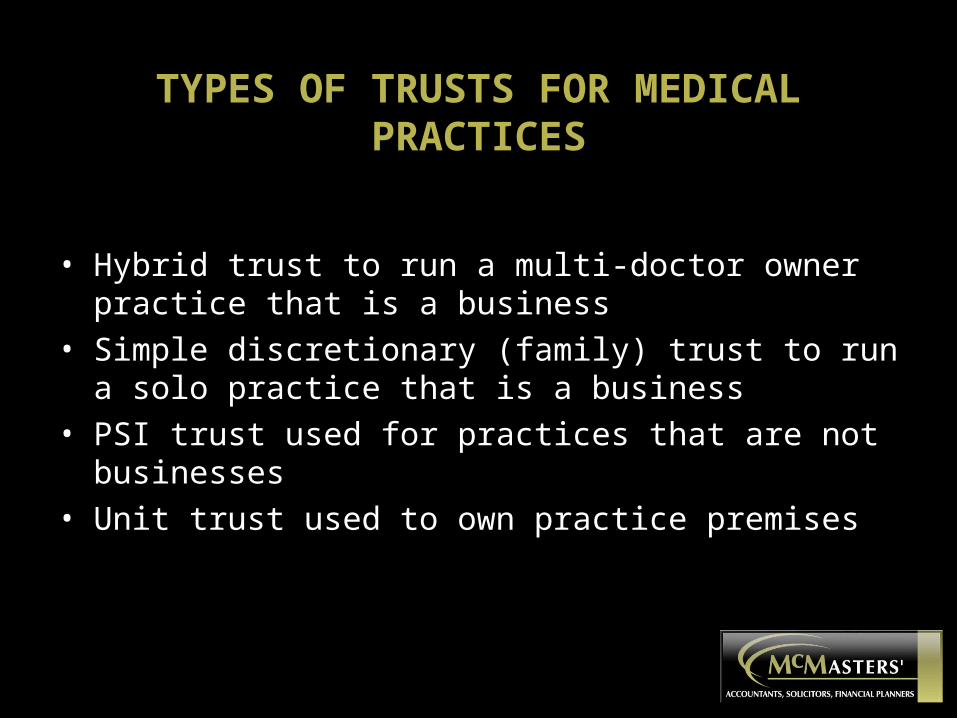

TYPES OF TRUSTS FOR MEDICAL PRACTICES

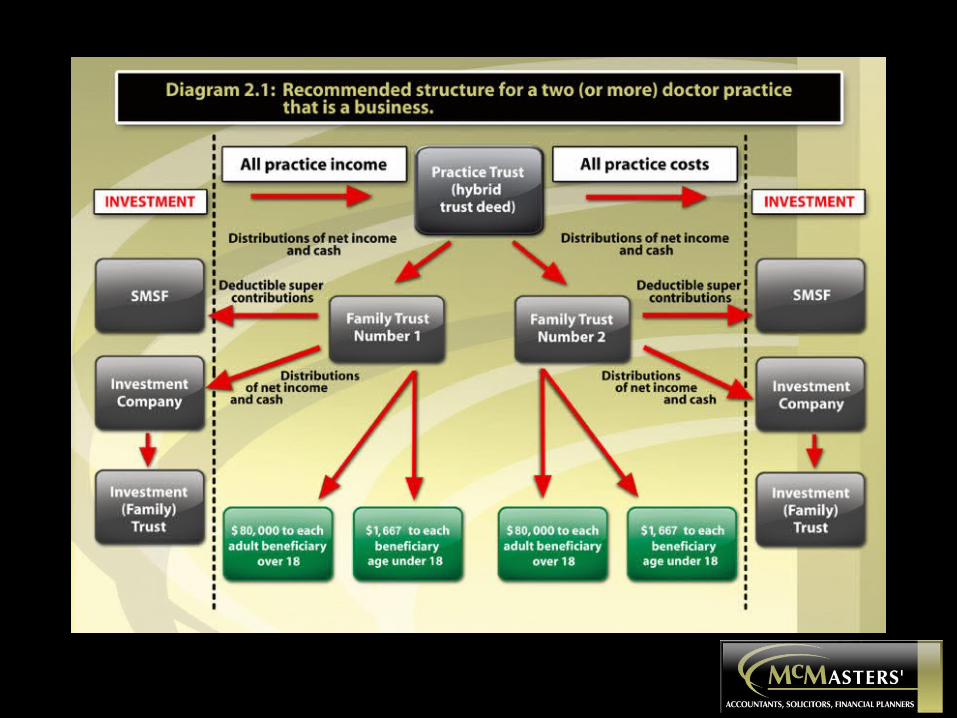

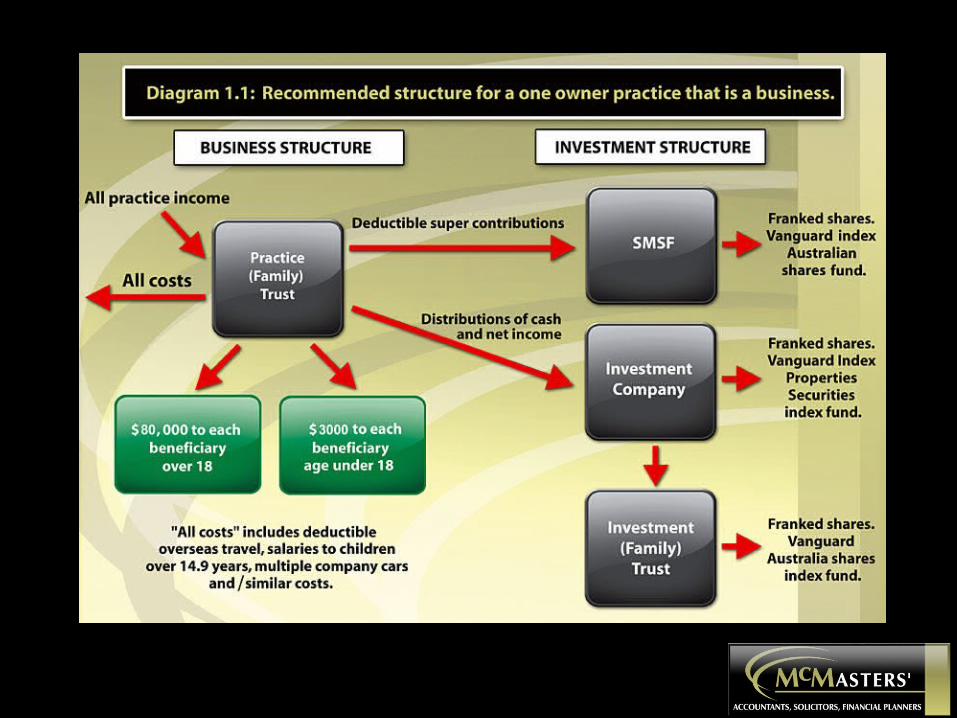

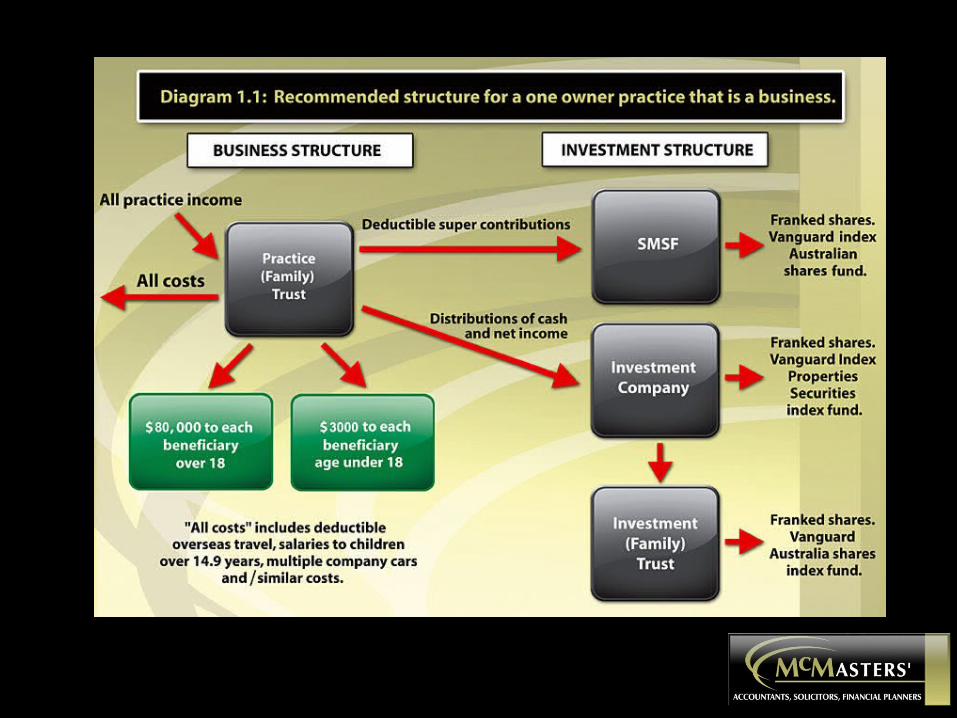

• Hybrid trust to run a multi-doctor owner practice that is a business

• Simple discretionary (family) trust to run a solo practice that is a business

• PSI trust used for practices that are not businesses• Unit trust used to own practice premises

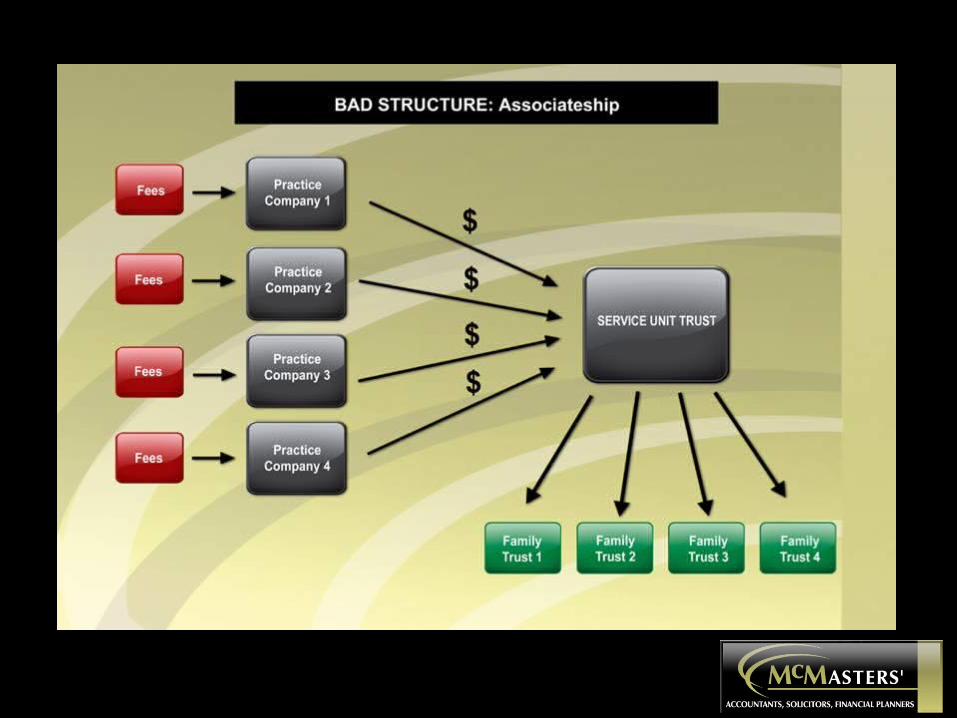

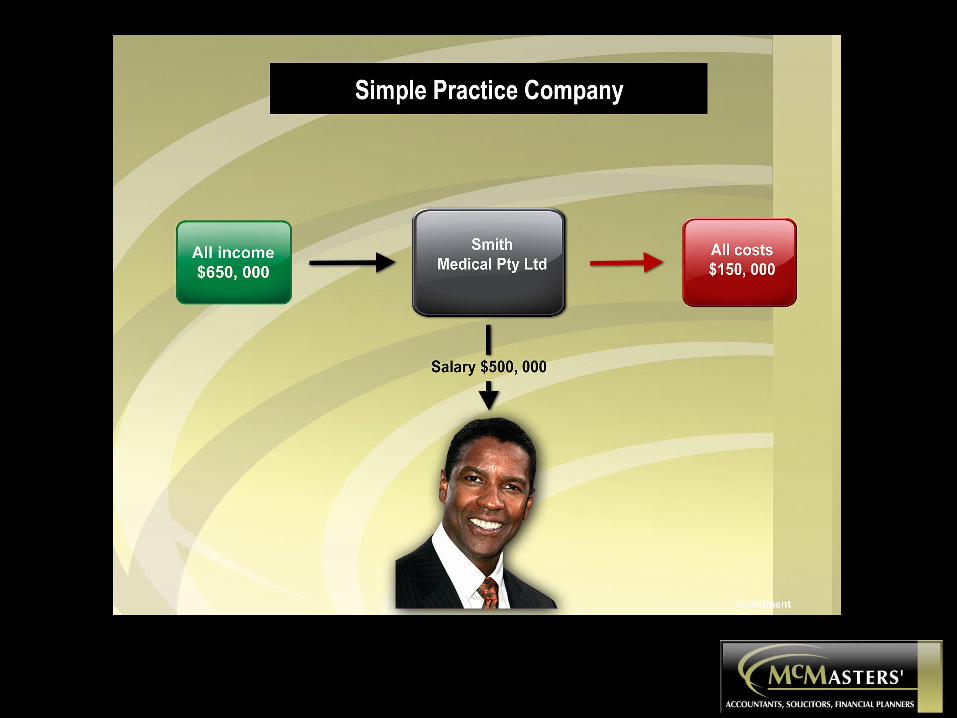

Dr Mickey’s Costley and Kumbersum Practice

• Four doctors practice in an associateship

• Each doctor uses a practice company

• The practice companies pay each doctor a salary

• Each practice company pays a management fee to a service trust

• The service trust distributes its net income to the doctors’ family

trusts

• The family trusts distribute net income to low tax rate related

persons

• The Practice engages a total of 4 equivalent full time material

fee earners

Problems with Dr Mickey’s Costly and Kumbersum Structure

– Complexity – 5 BAS’s, many inter-practice transactions– Expensive to maintain: 9 sets of accounts, 9 bank statements– Tax benefits very limited, ie only profit on services shifted to low

tax rate related parties– Payroll tax and Workcover on doctors’ salaries (?)– Compliance with service entity ruling– 45% tax rate on doctor’s earnings, ie very limited tax planning

compared to alternatives– Doctors’ rewards are taxed very inefficiently, ie as salaries– CGT inefficient with use of practice companies– Practice manager stressed out

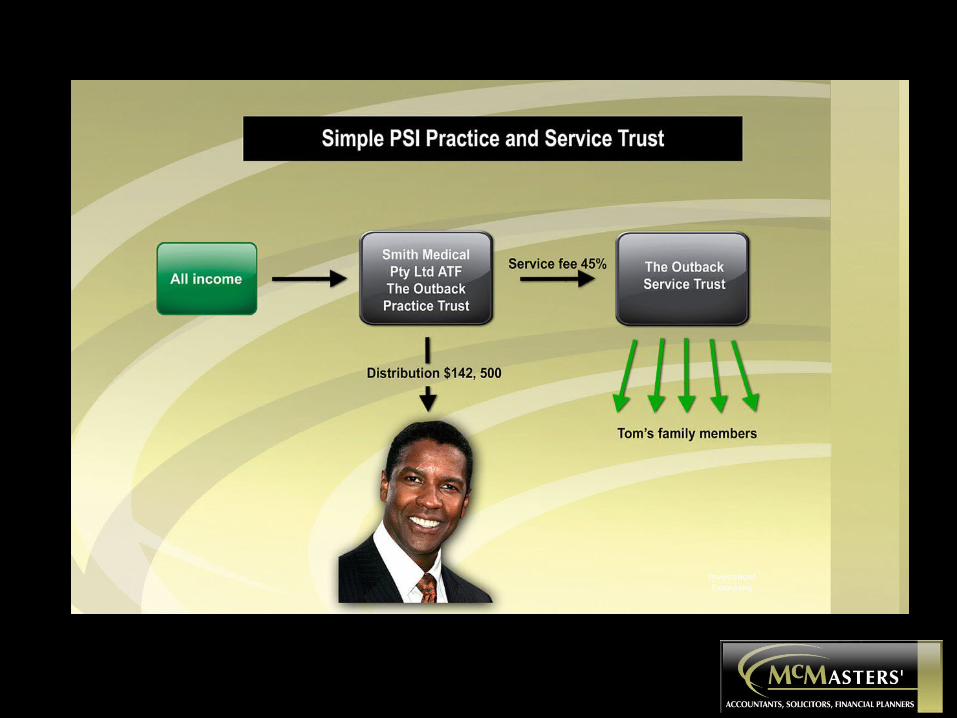

What are the advantages of the new structure?

– Simple just one BAS and no inter-practice transactions– Cheap to maintain: 1 sets of accounts, 1 bank statement– Tax benefits : income shifted to low tax rate related parties– Payroll tax and Workcover on doctors’ salaries eliminated– Compliance with service entity ruling not necessary– 30% tax rate on doctor’s earnings, ie strong tax planning

compared to alternatives– Doctors’ rewards taxed very efficiently,– CGT efficient– FBT efficient– Practice manager smiling (and now working on important matters!)

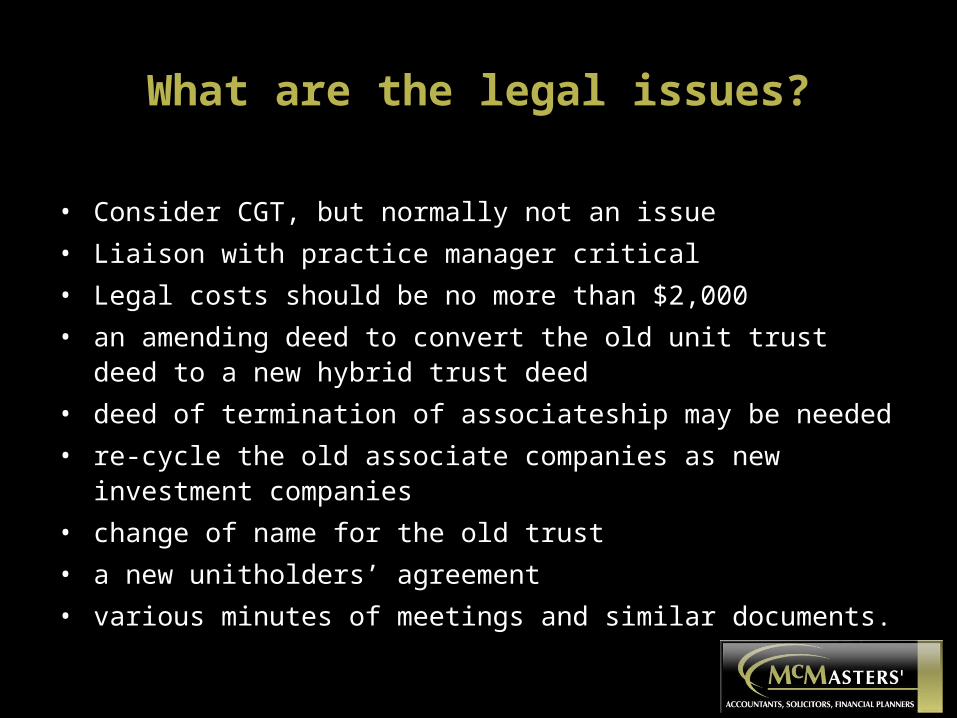

What are the legal issues?

• Consider CGT, but normally not an issue

• Liaison with practice manager critical

• Legal costs should be no more than $2,000

• an amending deed to convert the old unit trust deed to a new hybrid trust deed

• deed of termination of associateship may be needed

• re-cycle the old associate companies as new investment companies

• change of name for the old trust

• a new unitholders’ agreement

• various minutes of meetings and similar documents.

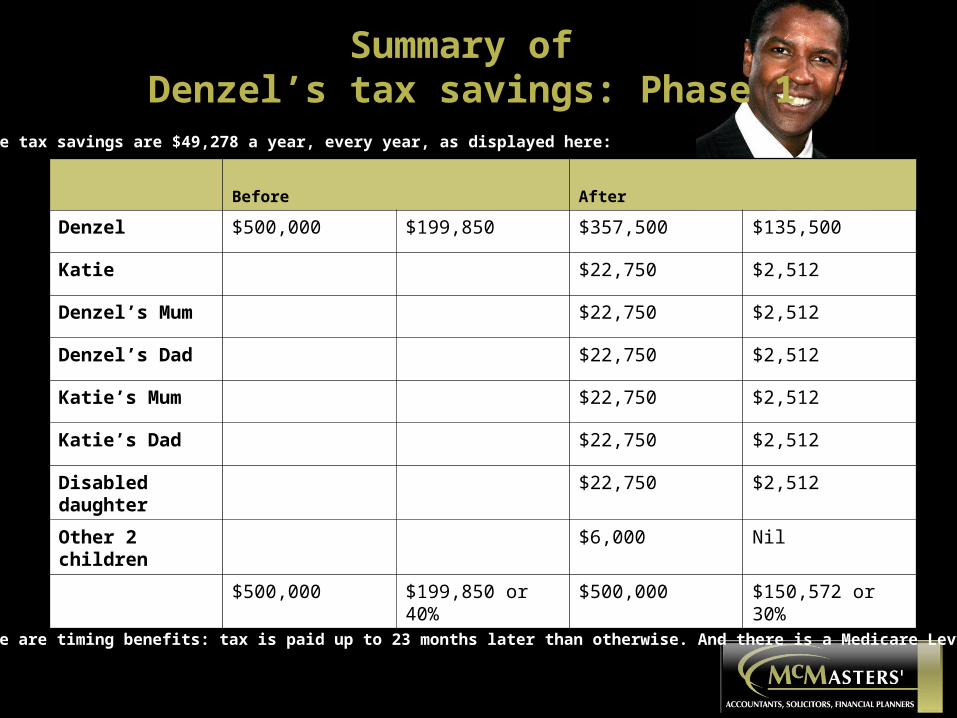

Summary of Denzel’s tax savings: Phase 1

Before After

Denzel $500,000 $199,850 $357,500 $135,500

Katie $22,750 $2,512

Denzel’s Mum $22,750 $2,512

Denzel’s Dad $22,750 $2,512

Katie’s Mum $22,750 $2,512

Katie’s Dad $22,750 $2,512

Disabled daughter

$22,750 $2,512

Other 2 children $6,000 Nil

$500,000 $199,850 or 40% $500,000 $150,572 or 30%

The tax savings are $49,278 a year, every year, as displayed here:

And there are timing benefits: tax is paid up to 23 months later than otherwise. And there is a Medicare Levy saving.

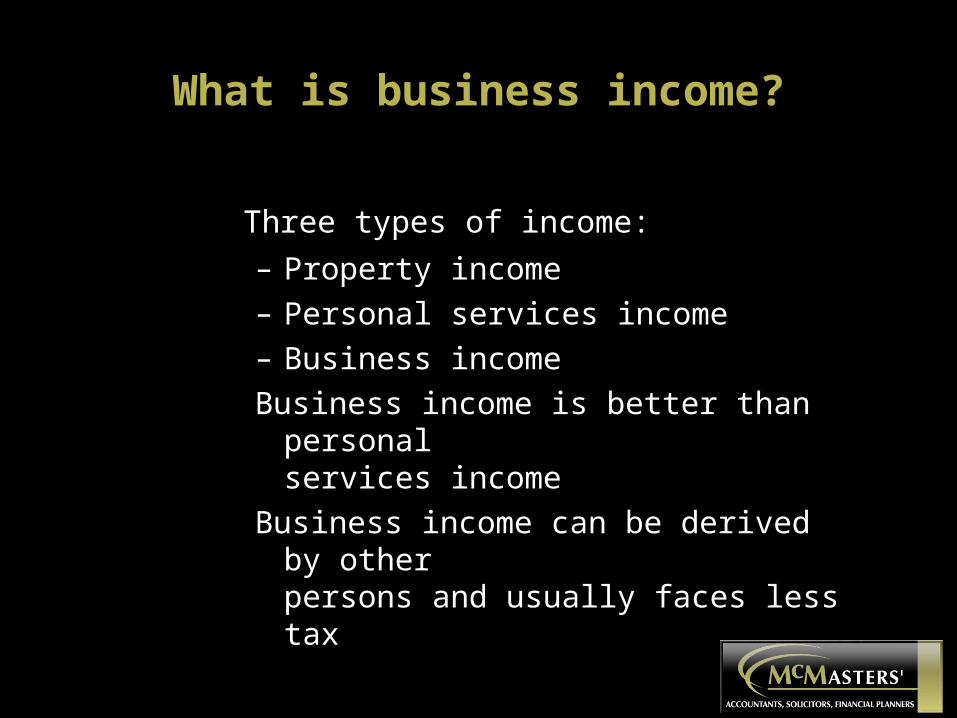

What is business income?

Three types of income:

– Property income– Personal services income– Business income

Business income is better than personal services income

Business income can be derived by other persons and usually faces less tax

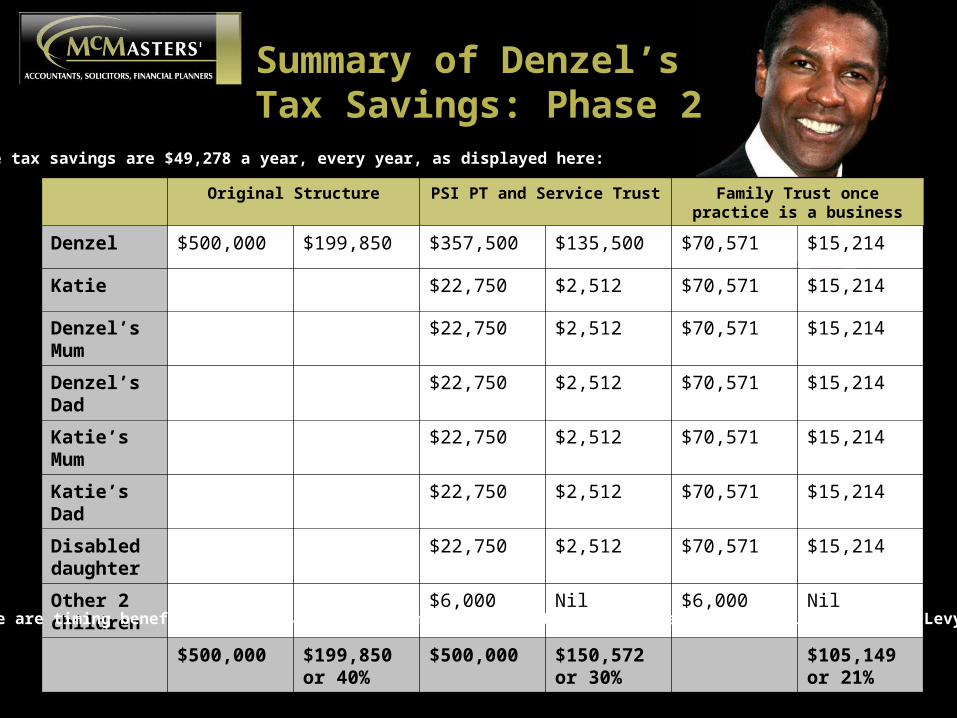

Summary of Denzel’s Tax Savings: Phase 2

Original Structure PSI PT and Service Trust Family Trust once practice is a business

Denzel $500,000 $199,850 $357,500 $135,500 $70,571 $15,214

Katie $22,750 $2,512 $70,571 $15,214

Denzel’s Mum

$22,750 $2,512 $70,571 $15,214

Denzel’s Dad

$22,750 $2,512 $70,571 $15,214

Katie’s Mum

$22,750 $2,512 $70,571 $15,214

Katie’s Dad $22,750 $2,512 $70,571 $15,214

Disabled daughter

$22,750 $2,512 $70,571 $15,214

Other 2 children

$6,000 Nil $6,000 Nil

$500,000 $199,850 or 40%

$500,000 $150,572 or 30%

$105,149 or 21%

The tax savings are $49,278 a year, every year, as displayed here:

And there are timing benefits: tax is paid up to 23 months later than otherwise. And there is a Medicare Levy saving.

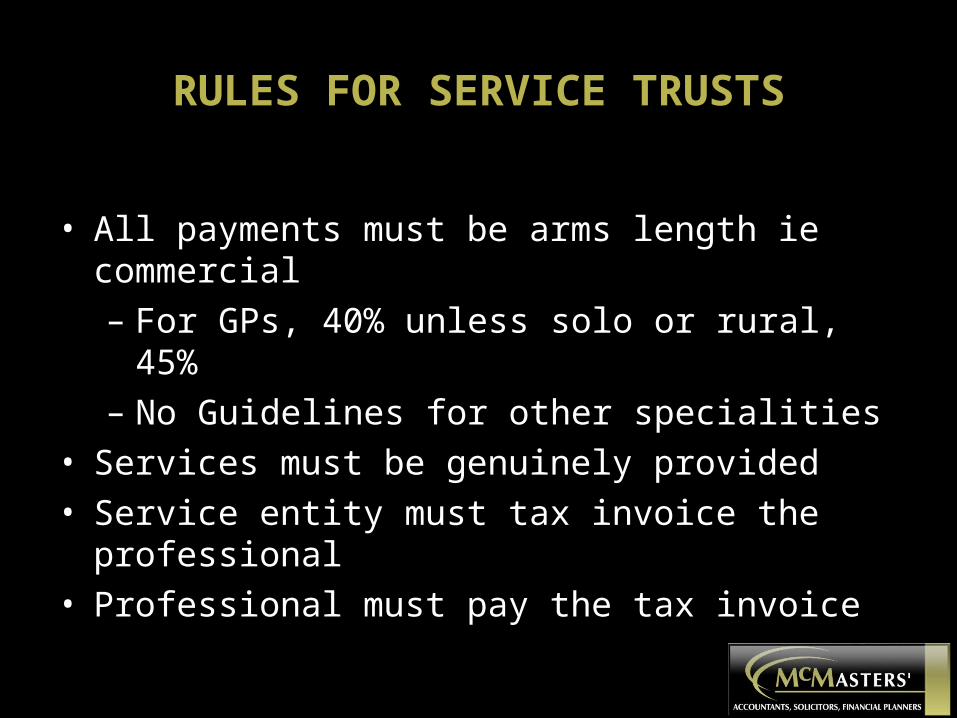

RULES FOR SERVICE TRUSTS

• All payments must be arms length ie commercial

– For GPs, 40% unless solo or rural, 45%

– No Guidelines for other specialities

• Services must be genuinely provided

• Service entity must tax invoice the professional

• Professional must pay the tax invoice

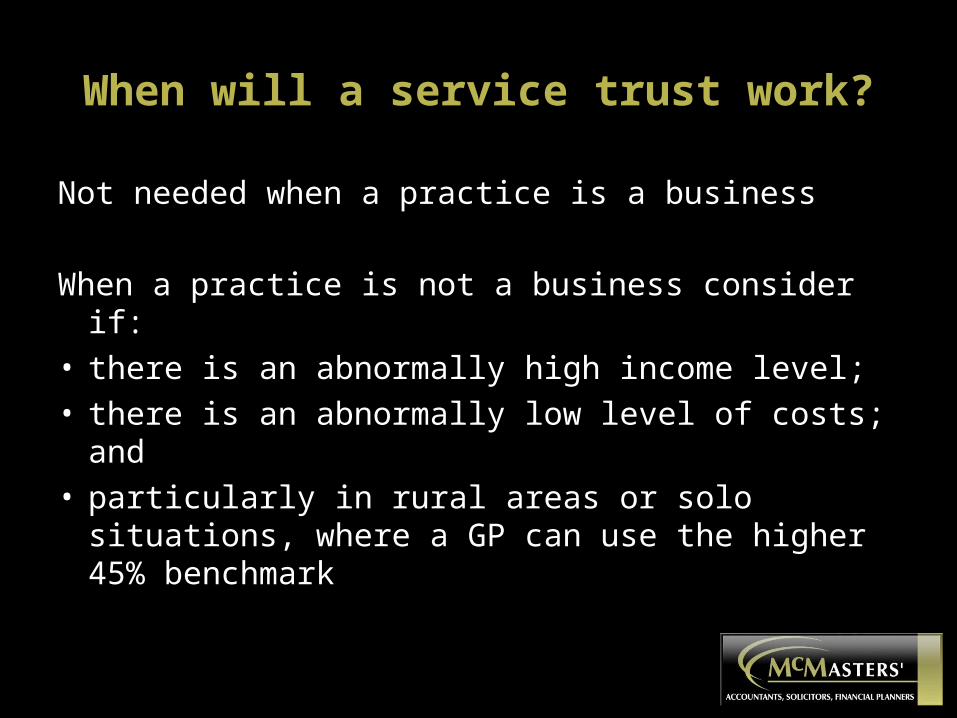

When will a service trust work?

Not needed when a practice is a business

When a practice is not a business consider if:• there is an abnormally high income level;• there is an abnormally low level of costs; and• particularly in rural areas or solo situations,

where a GP can use the higher 45% benchmark

McMasters’ Dox4Dox

Banklink

A reminder: someone is listening

The Supa Dupa(TM) Medical Centre

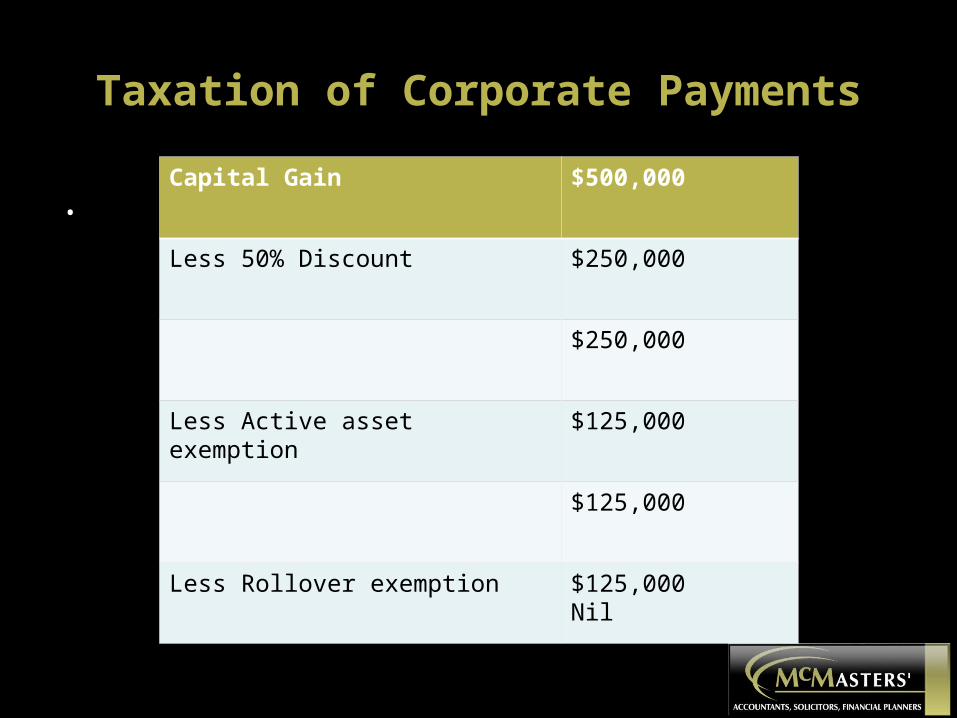

Taxation of Corporate Payments

.Capital Gain $500,000

Less 50% Discount $250,000

$250,000

Less Active asset exemption $125,000

$125,000

Less Rollover exemption $125,000Nil

Home to work travel, log books and bulky medical equipment

• Ballesty v FCT

(1977) 7 ATR 411

• FCT v Vogt

(1975) 4 ATR 274

• AAT Case 9235

(1994) 27 ATR 127

18 year old daughter’s car

18 year old son’s car

Mother in law’s car

50% investment allowance and cars

• 50% one off deduction on the cost of a new car• Luxury car rule limit applies• Must be ordered before 31 December 2010• Turnover less than $2,000,000 per annum• GST credits apply too• A persuasive case for bringing forward planned

car up-grades• Up to about 60% of the cost of a new car is in

effect paid for by tax benefits

Going somewhere?

Deductible overseas travel

What are the rules?

Must be for the purpose of maintaining or advancing an existing body of knowledge used to produce assessable income

Purpose determines deductibility

Paper proves purpose

Document, document, document

Before, after and during the trip

Dual purpose trips = part deductions

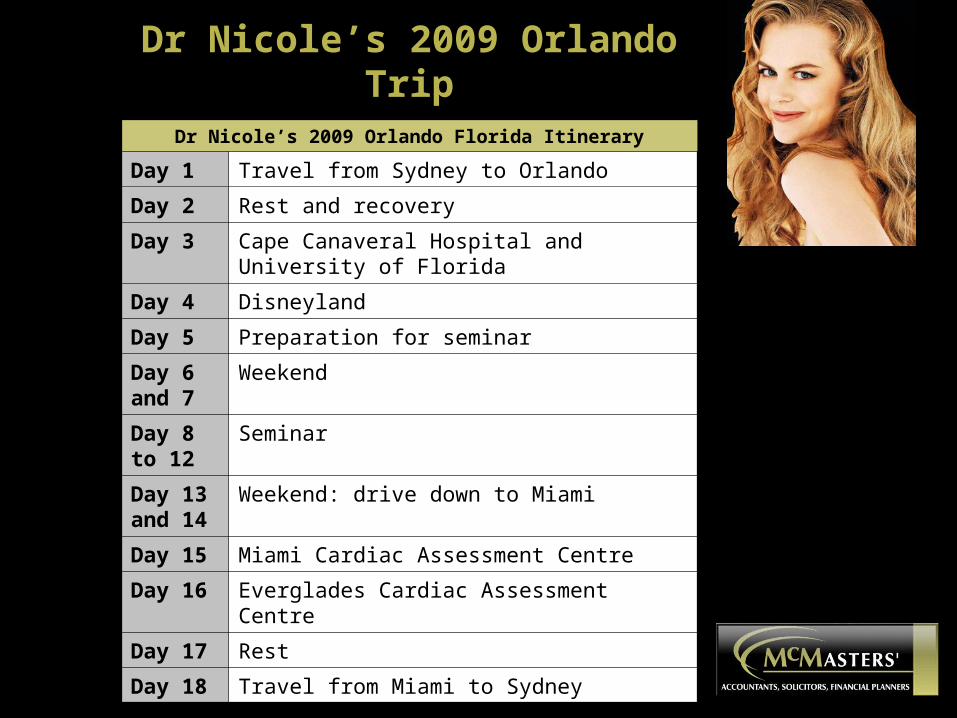

Dr Nicole’s 2009 Orlando Trip

Dr Nicole’s 2009 Orlando Florida Itinerary

Day 1 Travel from Sydney to Orlando

Day 2 Rest and recovery

Day 3 Cape Canaveral Hospital and University of Florida

Day 4 Disneyland

Day 5 Preparation for seminar

Day 6 and 7

Weekend

Day 8 to 12

Seminar

Day 13 and 14

Weekend: drive down to Miami

Day 15 Miami Cardiac Assessment Centre

Day 16 Everglades Cardiac Assessment Centre

Day 17 Rest

Day 18 Travel from Miami to Sydney

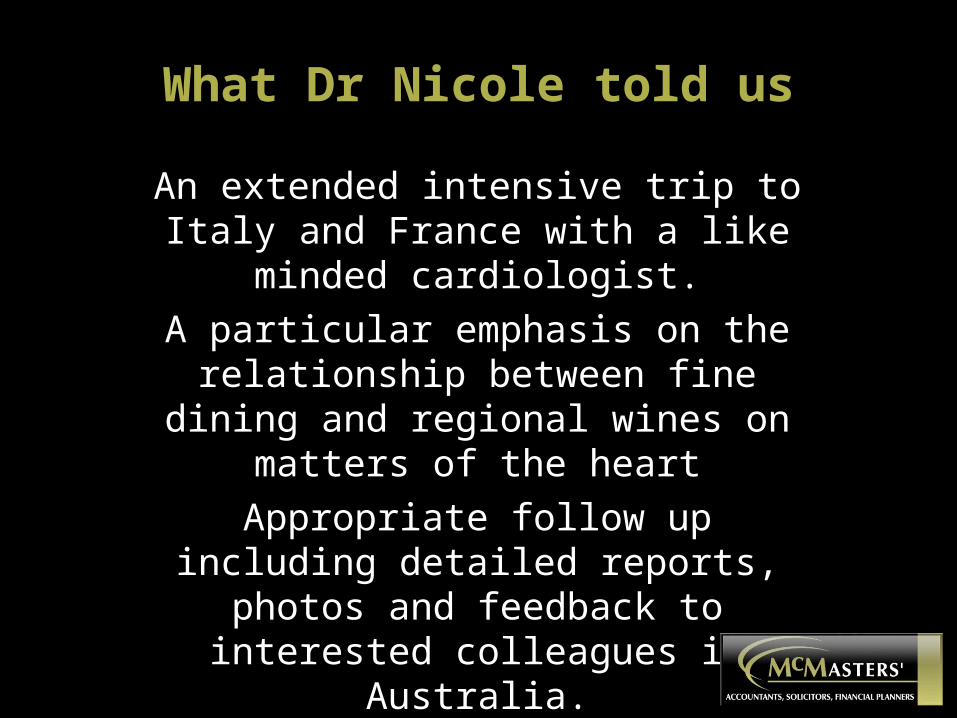

What Dr Nicole told us

An extended intensive trip to Italy and France with a like minded cardiologist.

A particular emphasis on the relationship between fine dining and

regional wines on matters of the heart

Appropriate follow up including detailed reports, photos and feedback to

interested colleagues in Australia.

What Dr Nicole really meant

Dr Brad’s Bright Idea

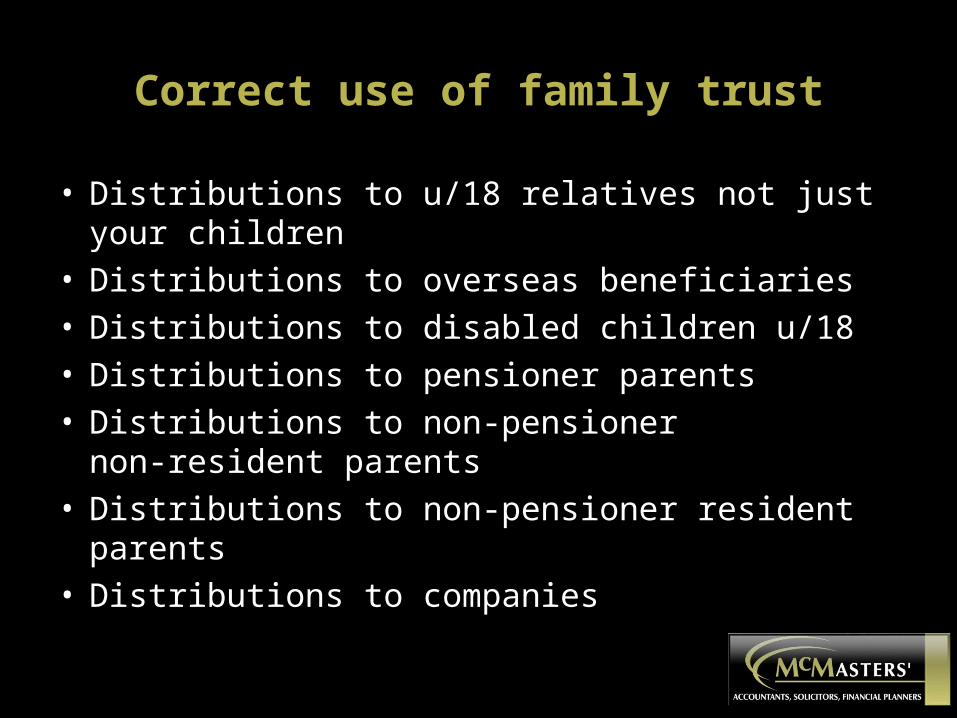

Correct use of family trust

• Distributions to u/18 relatives not just your children

• Distributions to overseas beneficiaries• Distributions to disabled children u/18• Distributions to pensioner parents• Distributions to non-pensioner

non-resident parents• Distributions to non-pensioner resident parents• Distributions to companies

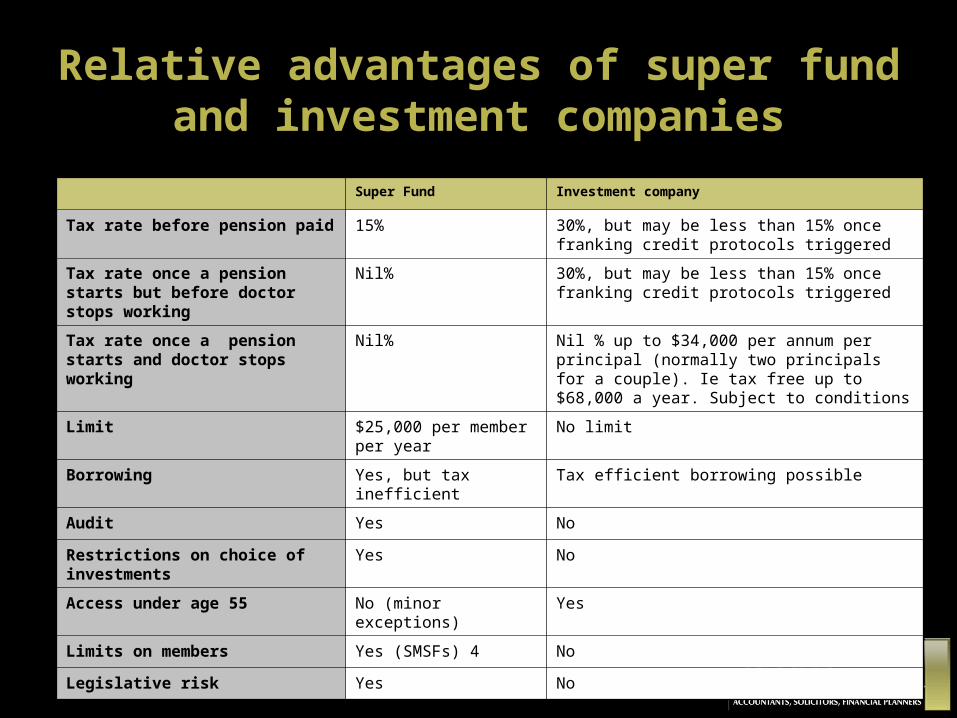

Relative advantages of super fund and investment companies

Super Fund Investment company

Tax rate before pension paid 15% 30%, but may be less than 15% once franking credit protocols triggered

Tax rate once a pension starts but before doctor stops working

Nil% 30%, but may be less than 15% once franking credit protocols triggered

Tax rate once a pension starts and doctor stops working

Nil% Nil % up to $34,000 per annum per principal (normally two principals for a couple). Ie tax free up to $68,000 a year. Subject to conditions

Limit $25,000 per member per year

No limit

Borrowing Yes, but tax inefficient Tax efficient borrowing possible

Audit Yes No

Restrictions on choice of investments

Yes No

Access under age 55 No (minor exceptions) Yes

Limits on members Yes (SMSFs) 4 No

Legislative risk Yes No

Tax planning for employee doctors

Tax Planning for Corporate Doctors

Tax planning for IMGs

www.mcmasterssuper.com.au

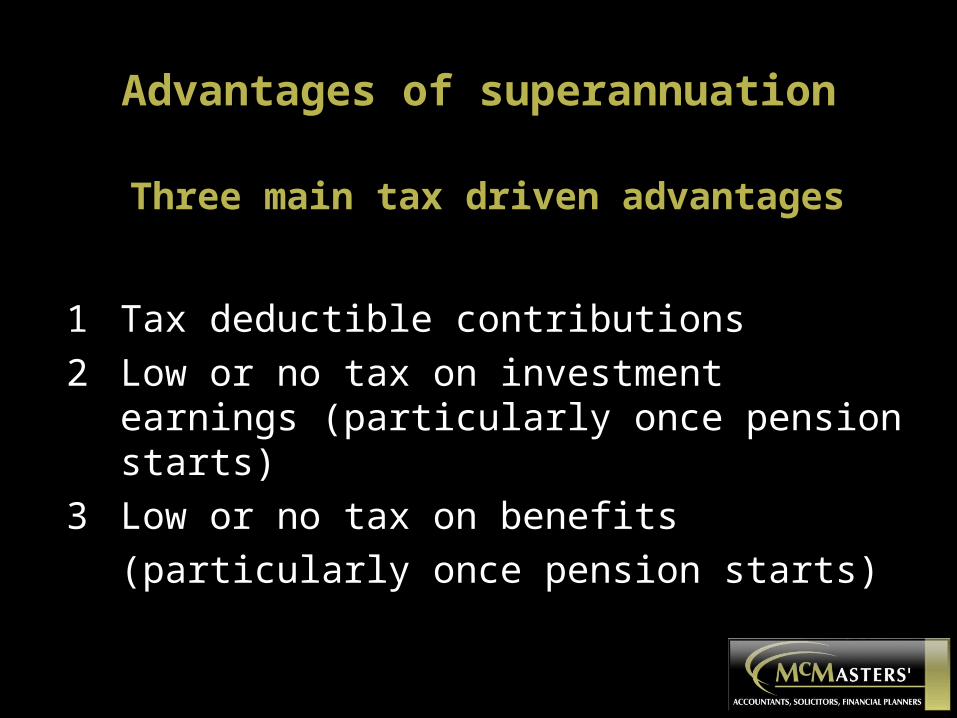

Advantages of superannuation

Three main tax driven advantages

1 Tax deductible contributions

2 Low or no tax on investment earnings (particularly once pension starts)

3 Low or no tax on benefits

(particularly once pension starts)

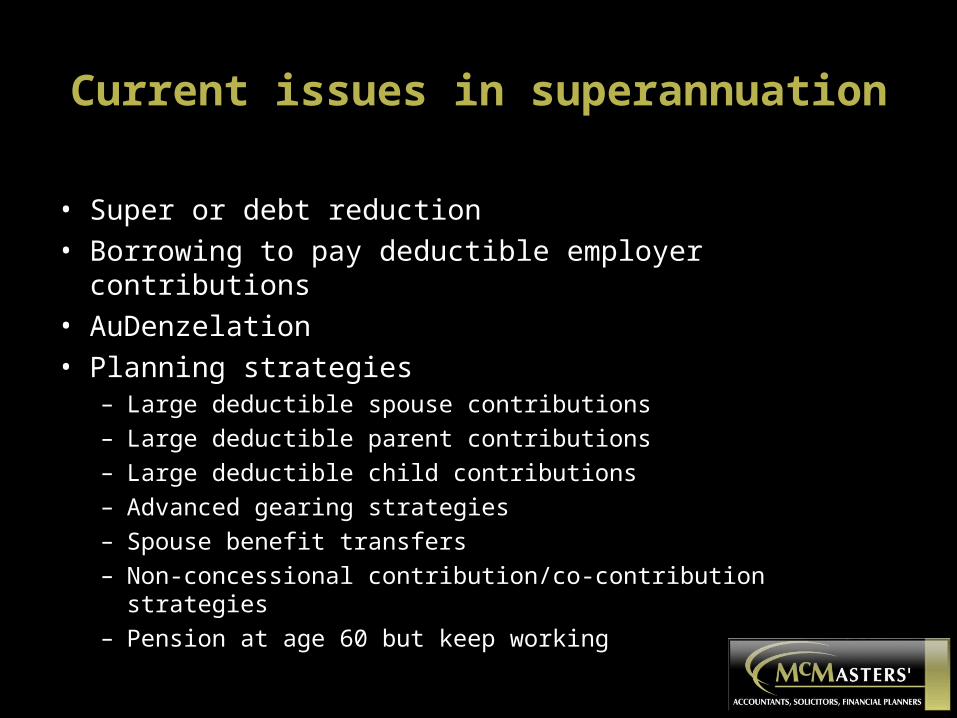

Current issues in superannuation

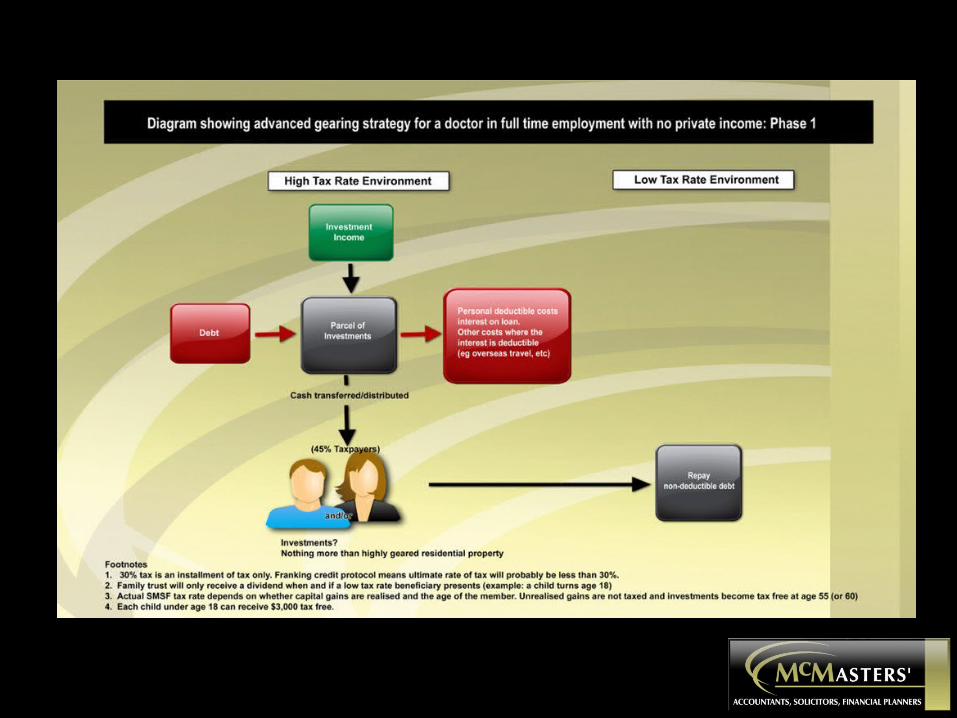

• Super or debt reduction• Borrowing to pay deductible employer contributions• AuDenzelation• Planning strategies

– Large deductible spouse contributions– Large deductible parent contributions– Large deductible child contributions– Advanced gearing strategies– Spouse benefit transfers– Non-concessional contribution/co-contribution strategies– Pension at age 60 but keep working

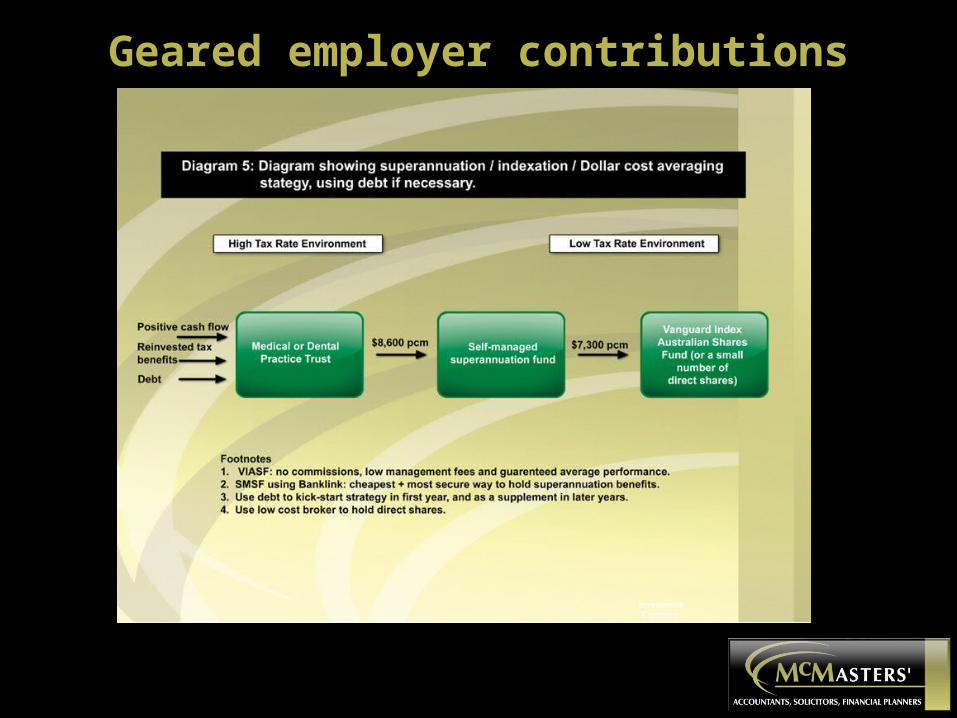

Geared employer contributions

Industry Super Funds

Why are SMSFs so good?

• Control

• Better investment performance

• Coordination with other aspects of your financial plan

• Cost are very low

– No commission investment strategies

– No wraps or other investment platforms

– Simple investment strategies

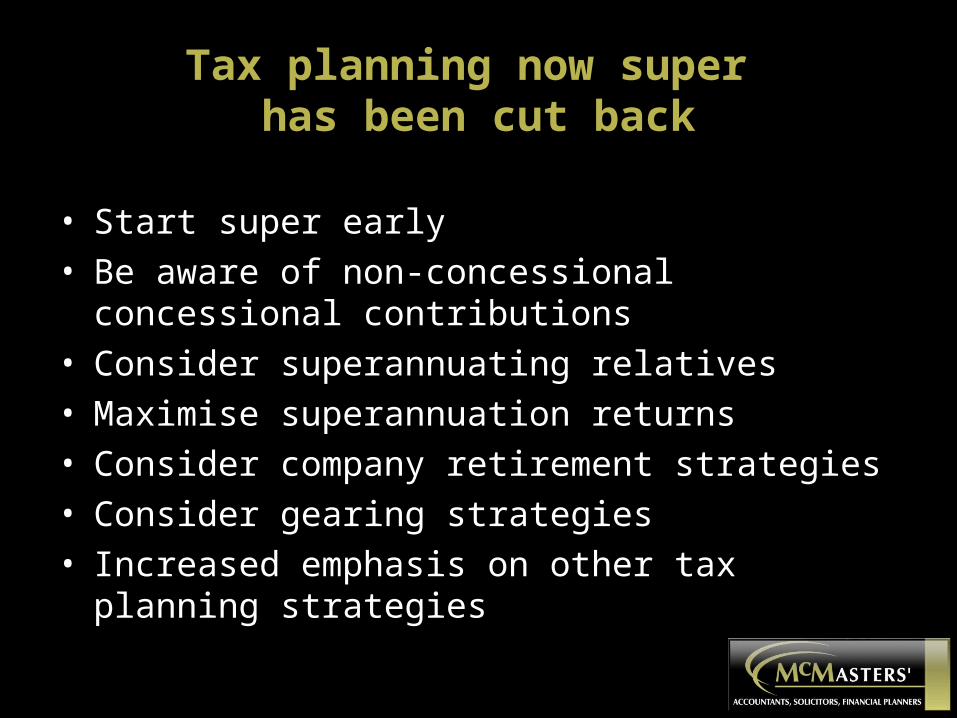

Tax planning now super has been cut back

• Start super early

• Be aware of non-concessional concessional contributions

• Consider superannuating relatives

• Maximise superannuation returns

• Consider company retirement strategies

• Consider gearing strategies

• Increased emphasis on other tax planning strategies

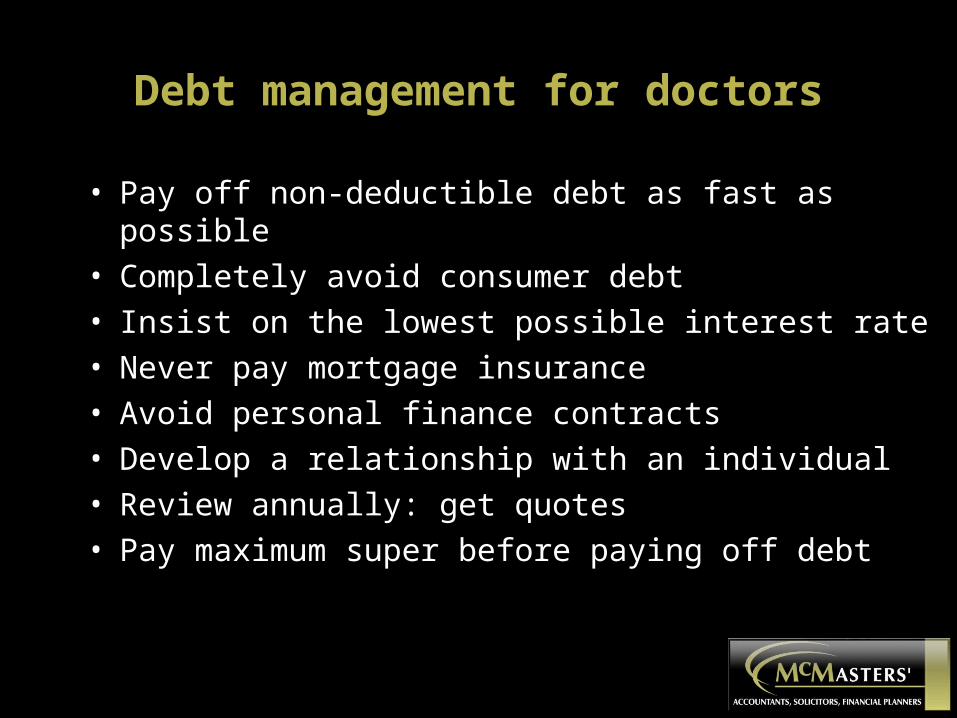

Debt management for doctors

• Pay off non-deductible debt as fast as possible

• Completely avoid consumer debt

• Insist on the lowest possible interest rate

• Never pay mortgage insurance

• Avoid personal finance contracts

• Develop a relationship with an individual

• Review annually: get quotes

• Pay maximum super before paying off debt

Your bank manager is not your friend

Two credit cards

Banklink, again

The Doctors’ Guide to Investingavailable at: www.mcmasters.com.au

McMasters’ Investment Maxims

• Never invest in anything that pays anyone a commission

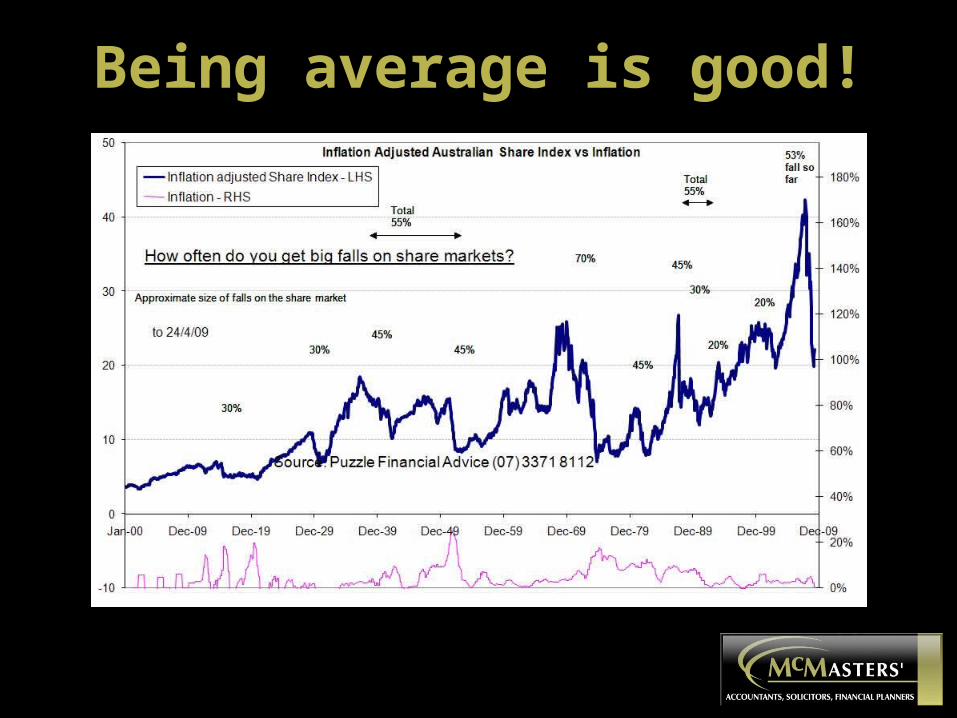

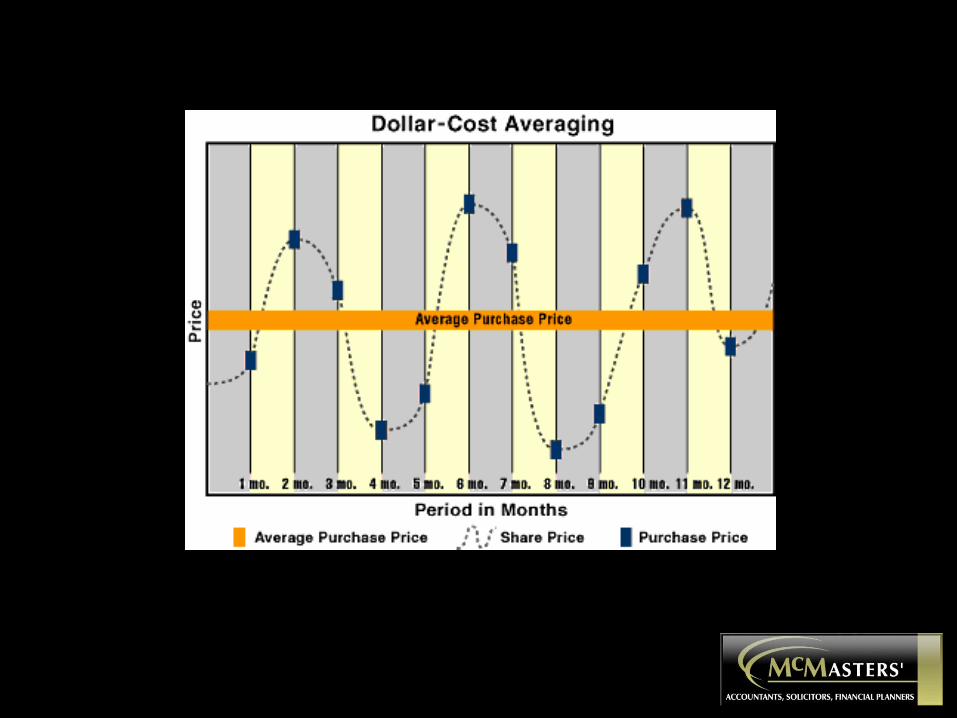

• Never let anyone else control your money• The best investment is your practice• Invest through a tax efficient structure• Being average is good (most aren’t)• Dollar cost averaging is good• Do not use wraps or other expensive platforms

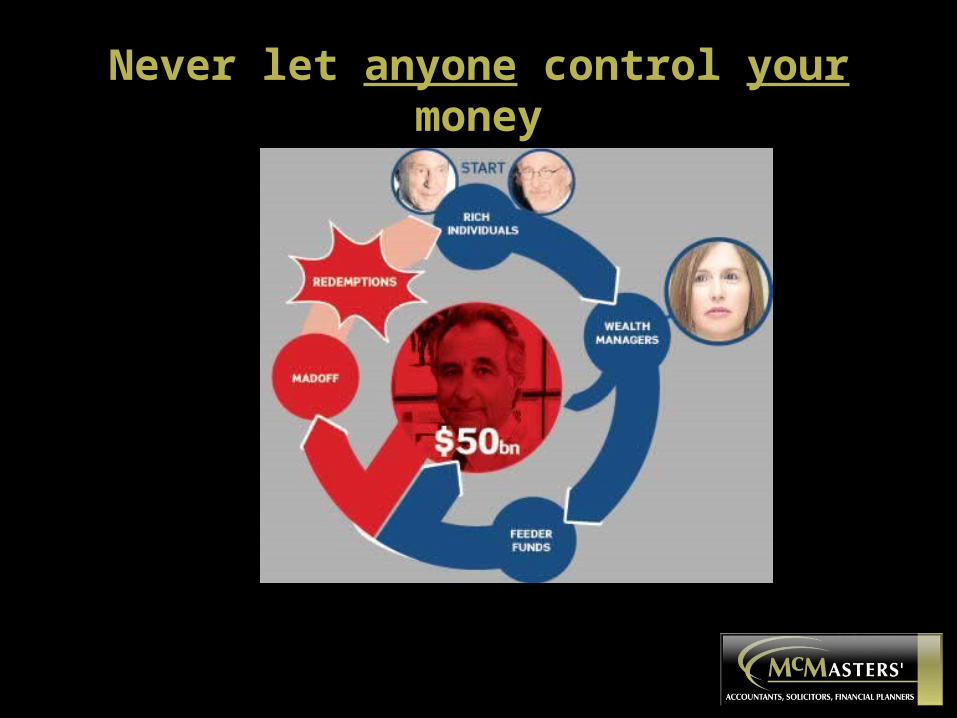

Never let anyone control your money

Your best investment: your practice

Tax Efficient Structures

Being average is good!

Do what he says, not what he does

Investors who use wraps

Sensible investments for doctors

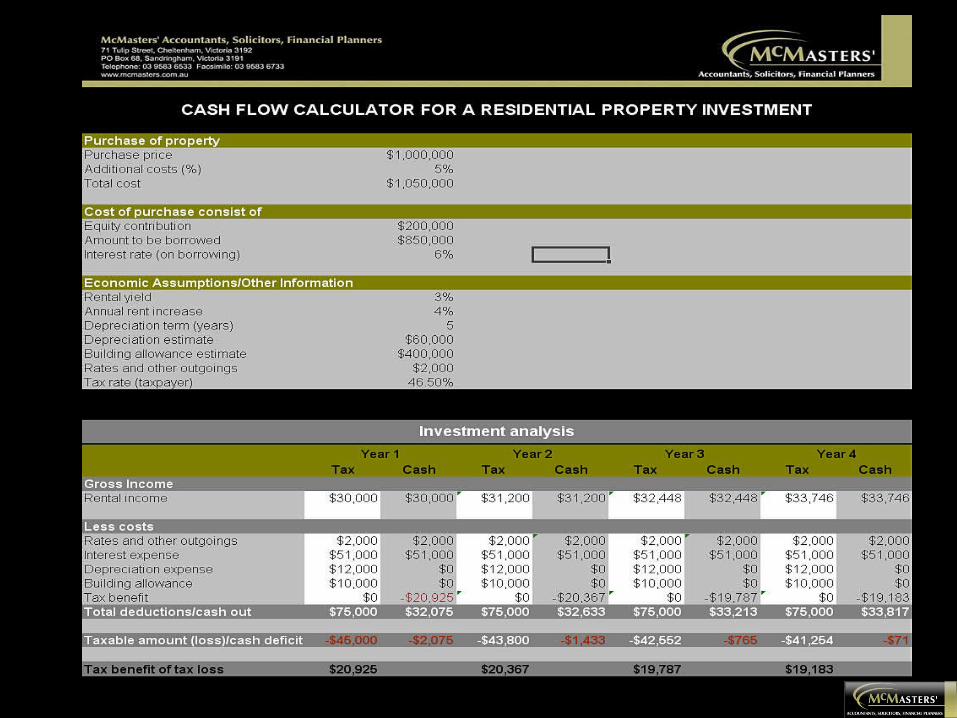

• Cash deposits and fixed interest securities• Residential property• Surgery premises• Other commercial property• Index funds and similar vehicles• Direct share investments• Other businesses

Safe as a bank

Safe as bricks and mortar

The Surgery Building

Commercial property

- No commissions- Low operating costs- No wasted time- Average performance guaranteed - Research shows most professional advisors cannot beat the average: costs and commissions drag them down- Do you really think your advisor is that good?

Share investing

• Use a low cost broker• Do not own more than 15 shares• Hold the shares directly• Do not use a wrap service• Do not trade• Do not hold values less than $20,000• Do not pay commissions

.

Adult kids still at home?

Insurances: a necessary evil

Commission Rebate Scheme

The ground rules for risk insurances

• Rebate all commissions• Do not over insure• Make sure insurances are tax effective• Do not bother with trauma/crisis cover• Be prepared to cut back $ as you get older• Industry super funds are the cheapest• Multiple universal no-medical cover?

Wills and estate planning

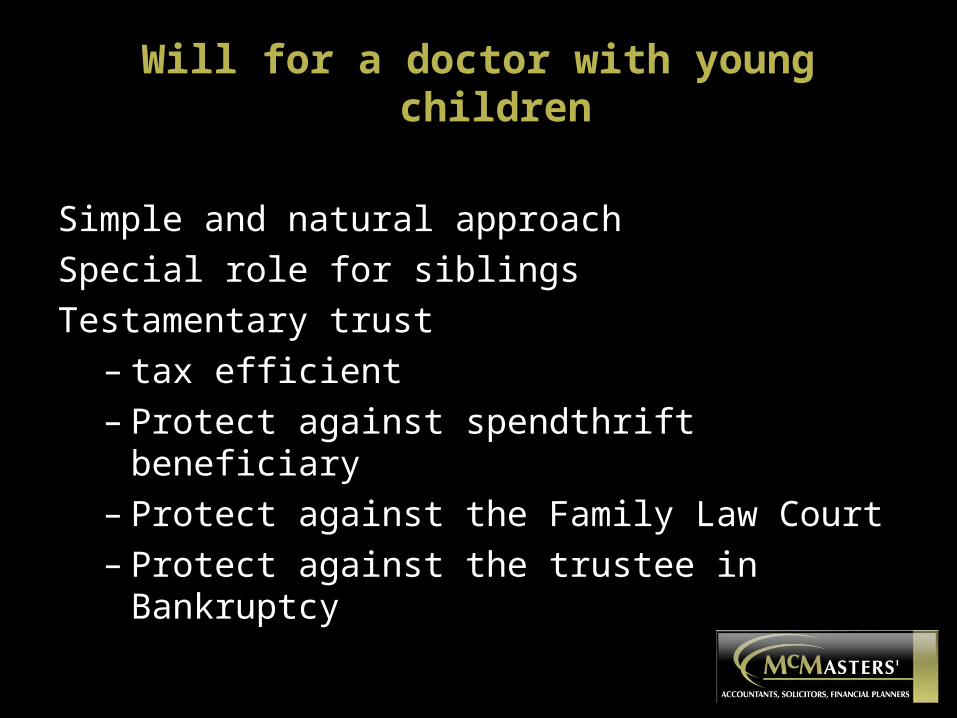

Will for a doctor with young children

Simple and natural approach

Special role for siblings

Testamentary trust– tax efficient– Protect against spendthrift beneficiary– Protect against the Family Law Court– Protect against the trustee in Bankruptcy

How to increase your profits

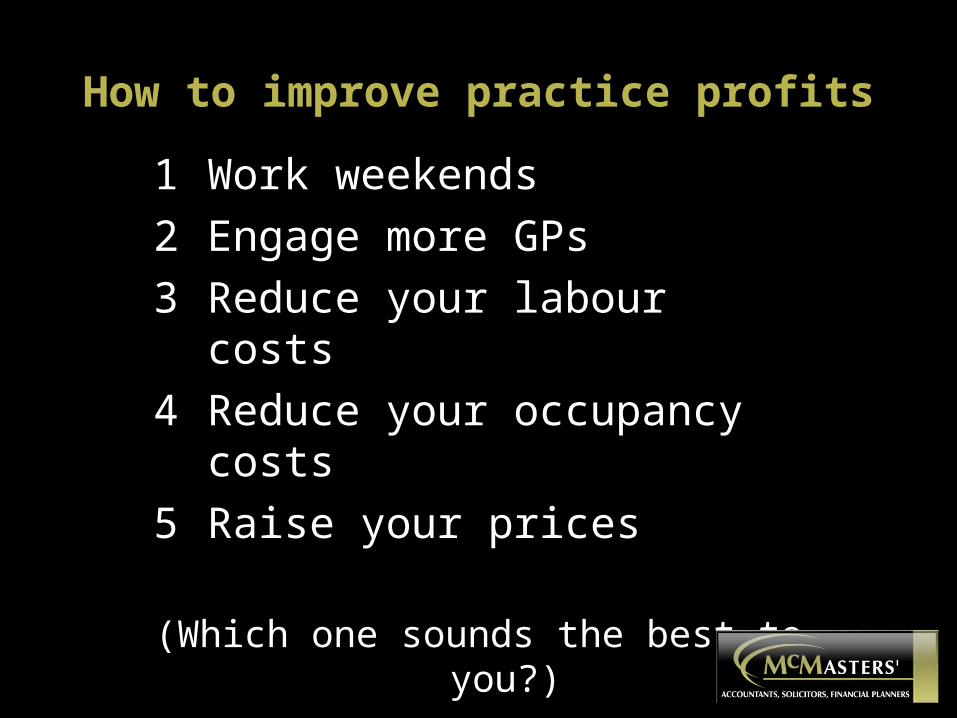

How to improve practice profits

1 Work weekends

2 Engage more GPs

3 Reduce your labour costs

4 Reduce your occupancy costs

5 Raise your prices

(Which one sounds the best to you?)

To summarise $$$$$$$$

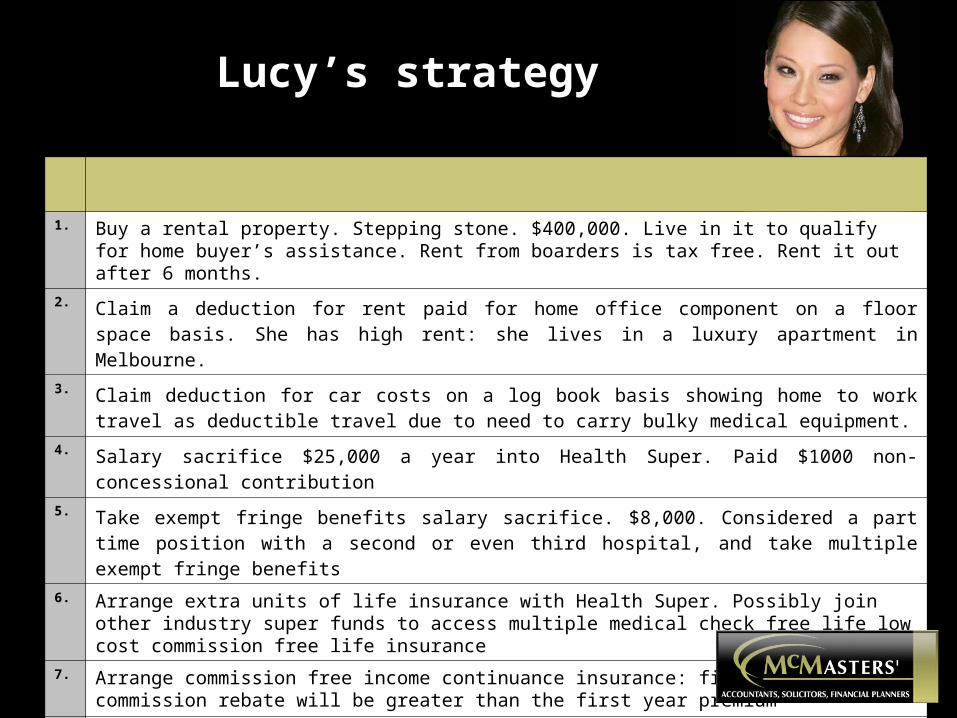

Lucy’s strategy

1. Buy a rental property. Stepping stone. $400,000. Live in it to qualify for home buyer’s assistance. Rent from boarders is tax free. Rent it out after 6 months.

2. Claim a deduction for rent paid for home office component on a floor space basis. She has high rent: she lives in a luxury apartment in Melbourne.

3. Claim deduction for car costs on a log book basis showing home to work travel as deductible travel due to need to carry bulky medical equipment.

4. Salary sacrifice $25,000 a year into Health Super. Paid $1000 non-concessional contribution

5. Take exempt fringe benefits salary sacrifice. $8,000. Considered a part time position with a second or even third hospital, and take multiple exempt fringe benefits

6. Arrange extra units of life insurance with Health Super. Possibly join other industry super funds to access multiple medical check free life low cost commission free life insurance

7. Arrange commission free income continuance insurance: first year commission rebate will be greater than the first year premium

8. Deductible overseas travel

9. Lodge PAYGW variation to get benefit of lower tax amounts straight away

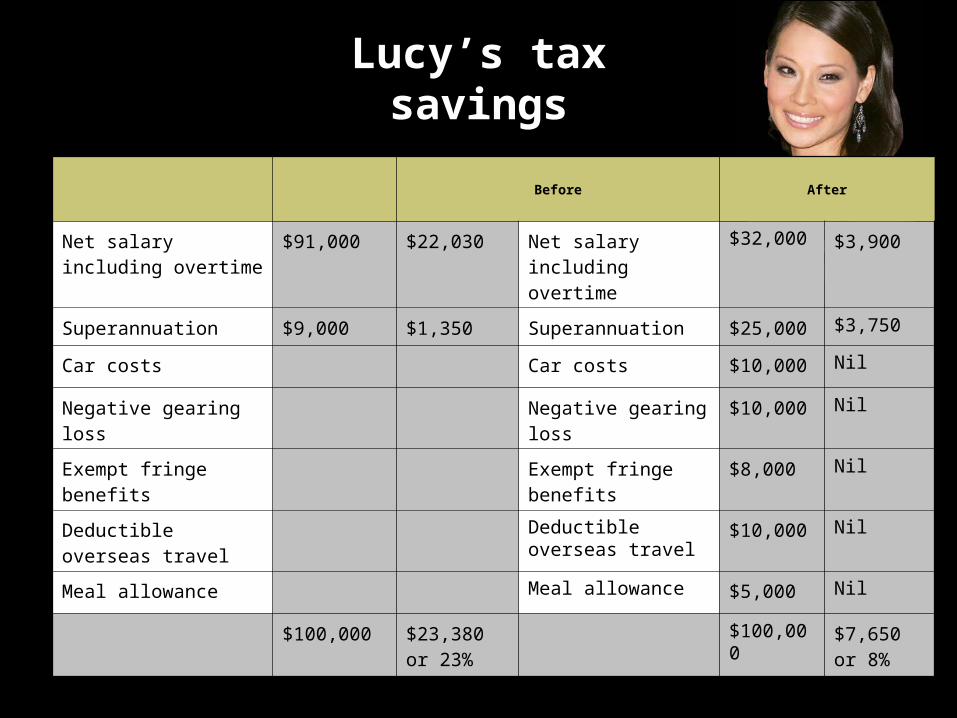

Lucy’s tax savings

Before After

Net salary including overtime

$91,000 $22,030 Net salary including overtime

$32,000 $3,900

Superannuation $9,000 $1,350 Superannuation $25,000 $3,750

Car costs Car costs $10,000 Nil

Negative gearing loss Negative gearing loss $10,000 Nil

Exempt fringe benefits Exempt fringe benefits

$8,000 Nil

Deductible overseas travel

Deductible overseas travel

$10,000 Nil

Meal allowance Meal allowance $5,000 Nil

$100,000 $23,380 or 23%

$100,000 $7,650 or 8%

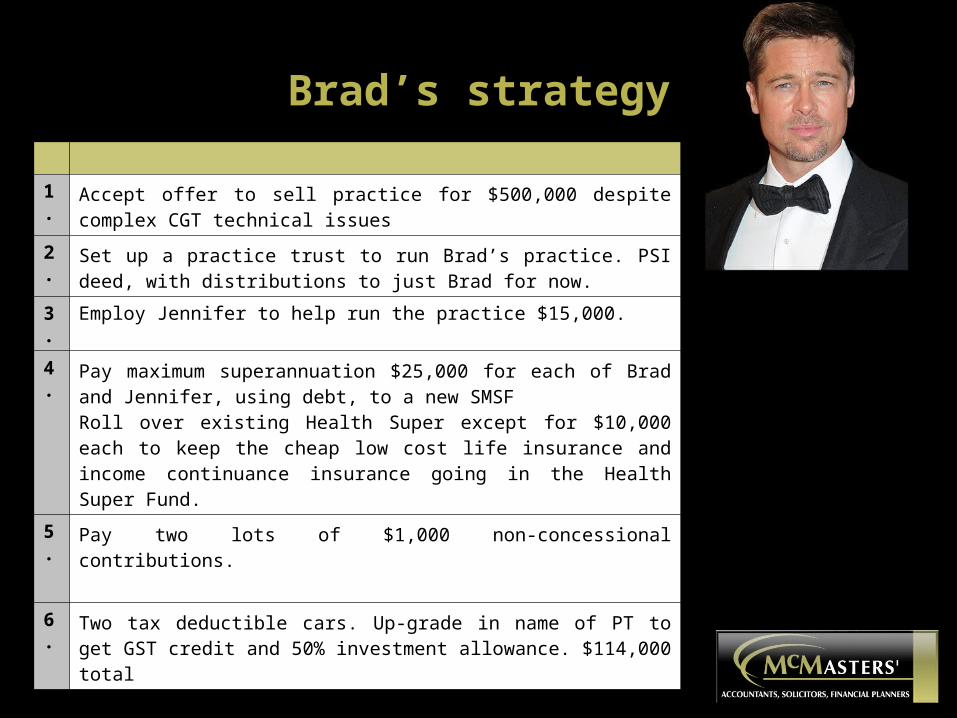

Brad’s strategy

1. Accept offer to sell practice for $500,000 despite complex CGT technical issues

2. Set up a practice trust to run Brad’s practice. PSI deed, with distributions to just Brad for now.

3. Employ Jennifer to help run the practice $15,000.

4. Pay maximum superannuation $25,000 for each of Brad and Jennifer, using debt, to a new SMSF Roll over existing Health Super except for $10,000 each to keep the cheap low cost life insurance and income continuance insurance going in the Health Super Fund.

5. Pay two lots of $1,000 non-concessional contributions.

6. Two tax deductible cars. Up-grade in name of PT to get GST credit and 50% investment allowance. $114,000 total

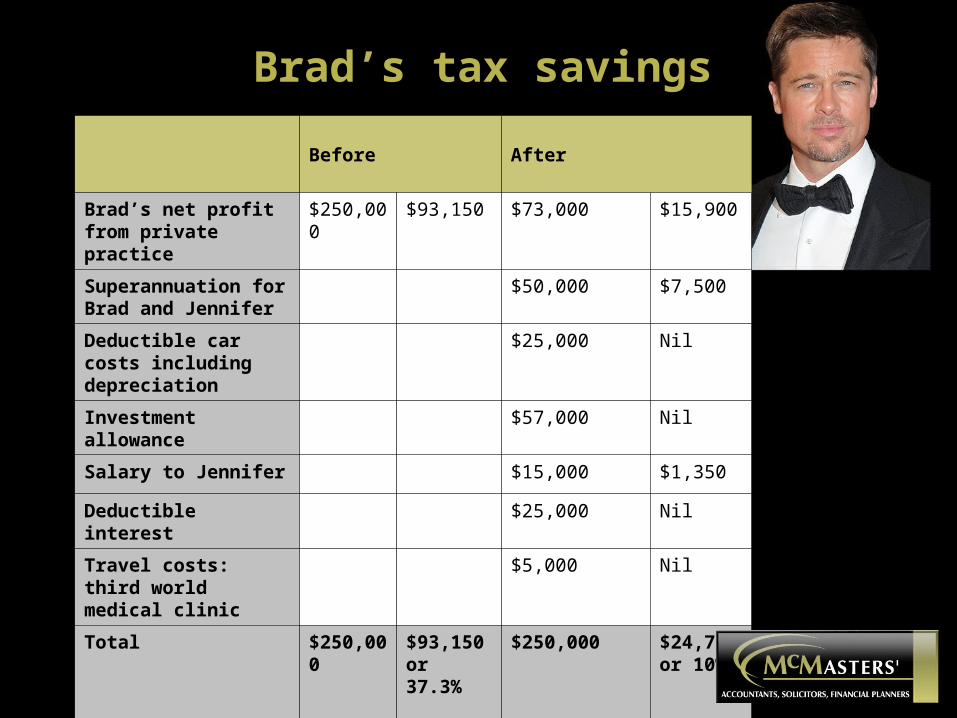

Before After

Brad’s net profit from private practice

$250,000 $93,150 $73,000 $15,900

Superannuation for Brad and Jennifer

$50,000 $7,500

Deductible car costs including depreciation

$25,000 Nil

Investment allowance $57,000 Nil

Salary to Jennifer $15,000 $1,350

Deductible interest $25,000 Nil

Travel costs: third world medical clinic

$5,000 Nil

Total $250,000 $93,150 or 37.3%

$250,000 $24,750 or 10%

Brad’s tax savings

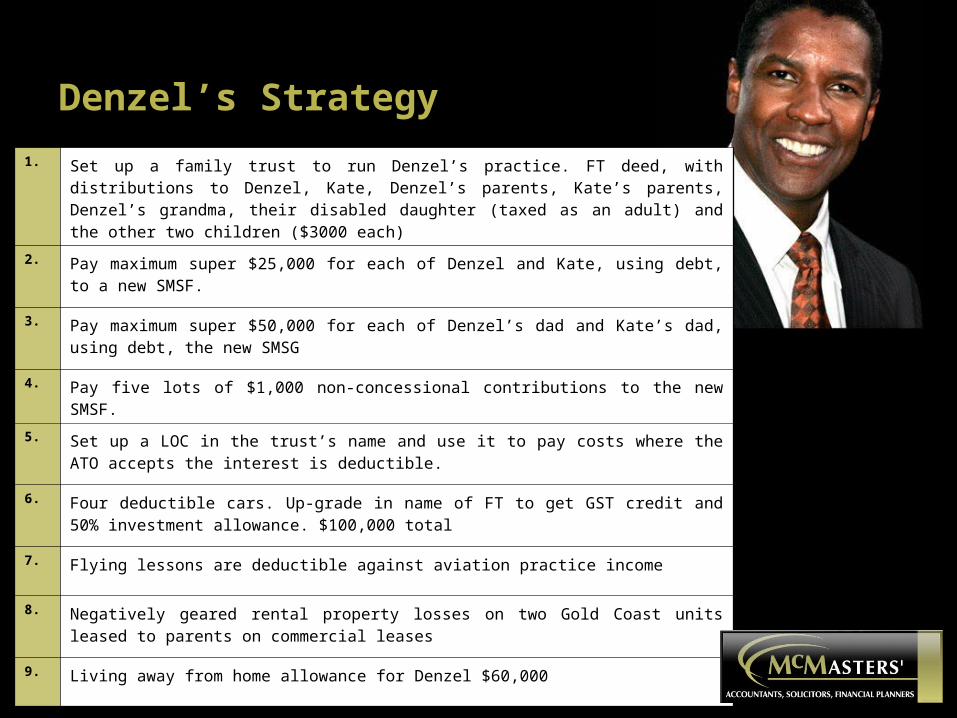

Denzel’s Strategy

1. Set up a family trust to run Denzel’s practice. FT deed, with distributions to Denzel, Kate, Denzel’s parents, Kate’s parents, Denzel’s grandma, their disabled daughter (taxed as an adult) and the other two children ($3000 each)

2. Pay maximum super $25,000 for each of Denzel and Kate, using debt, to a new SMSF.

3. Pay maximum super $50,000 for each of Denzel’s dad and Kate’s dad, using debt, the new SMSG

4. Pay five lots of $1,000 non-concessional contributions to the new SMSF.

5. Set up a LOC in the trust’s name and use it to pay costs where the ATO accepts the interest is deductible.

6. Four deductible cars. Up-grade in name of FT to get GST credit and 50% investment allowance. $100,000 total

7. Flying lessons are deductible against aviation practice income

8. Negatively geared rental property losses on two Gold Coast units leased to parents on commercial leases

9. Living away from home allowance for Denzel $60,000

Before After

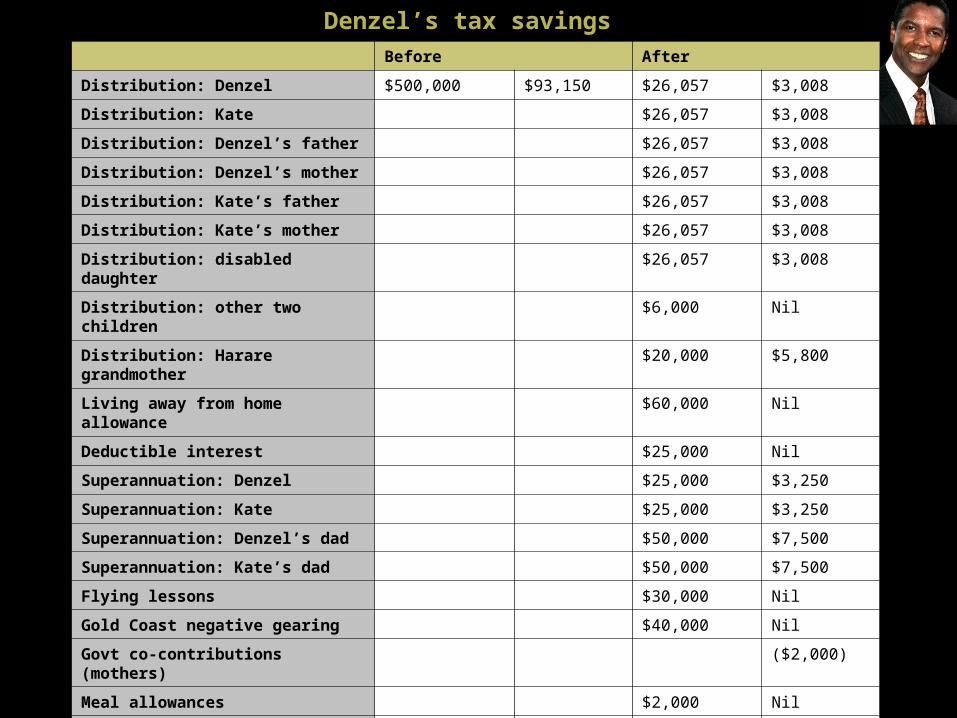

Distribution: Denzel $500,000 $93,150 $26,057 $3,008

Distribution: Kate $26,057 $3,008

Distribution: Denzel’s father $26,057 $3,008

Distribution: Denzel’s mother $26,057 $3,008

Distribution: Kate’s father $26,057 $3,008

Distribution: Kate’s mother $26,057 $3,008

Distribution: disabled daughter $26,057 $3,008

Distribution: other two children $6,000 Nil

Distribution: Harare grandmother $20,000 $5,800

Living away from home allowance $60,000 Nil

Deductible interest $25,000 Nil

Superannuation: Denzel $25,000 $3,250

Superannuation: Kate $25,000 $3,250

Superannuation: Denzel’s dad $50,000 $7,500

Superannuation: Kate’s dad $50,000 $7,500

Flying lessons $30,000 Nil

Gold Coast negative gearing $40,000 Nil

Govt co-contributions (mothers) ($2,000)

Meal allowances $2,000 Nil

Small irregular fringe benefits $1,000 Nil

Investment allowance $50,000 Nil

Total $500,000 $93,150 or 37.3%

$500,000 $46,356 or 9%

Denzel’s tax savings

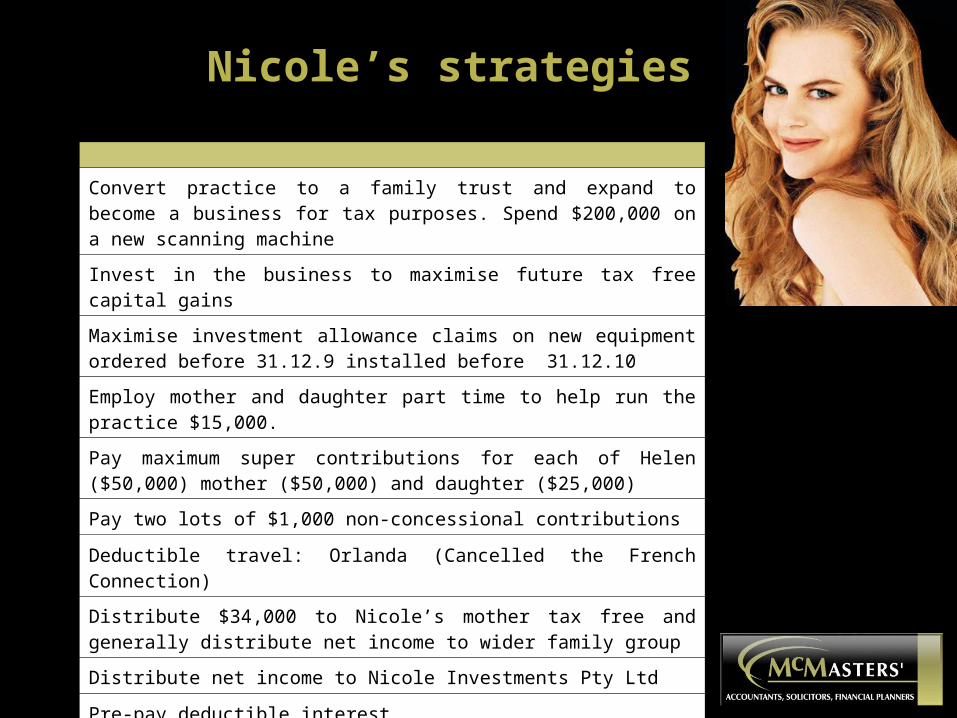

Nicole’s strategies

Convert practice to a family trust and expand to become a business for tax purposes. Spend $200,000 on a new scanning machine

Invest in the business to maximise future tax free capital gains

Maximise investment allowance claims on new equipment ordered before 31.12.9 installed before 31.12.10

Employ mother and daughter part time to help run the practice $15,000.

Pay maximum super contributions for each of Helen ($50,000) mother ($50,000) and daughter ($25,000)

Pay two lots of $1,000 non-concessional contributions

Deductible travel: Orlanda (Cancelled the French Connection)

Distribute $34,000 to Nicole’s mother tax free and generally distribute net income to wider family group

Distribute net income to Nicole Investments Pty Ltd

Pre-pay deductible interest

Pay daughter’s education costs (business management course)

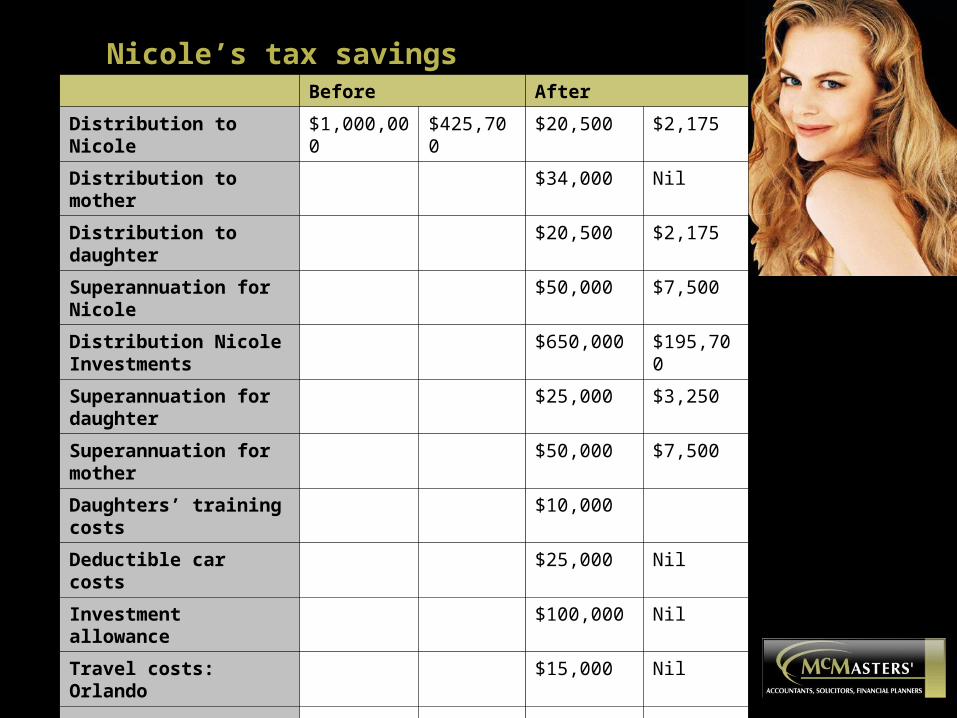

Before After

Distribution to Nicole $1,000,000 $425,700 $20,500 $2,175

Distribution to mother $34,000 Nil

Distribution to daughter $20,500 $2,175

Superannuation for Nicole

$50,000 $7,500

Distribution Nicole Investments

$650,000 $195,700

Superannuation for daughter

$25,000 $3,250

Superannuation for mother

$50,000 $7,500

Daughters’ training costs

$10,000

Deductible car costs $25,000 Nil

Investment allowance $100,000 Nil

Travel costs: Orlando $15,000 Nil

Total $1,000,000 $425,700 or 42.5%

$1,000,000 $218,300 or 22%

Nicole’s tax savings

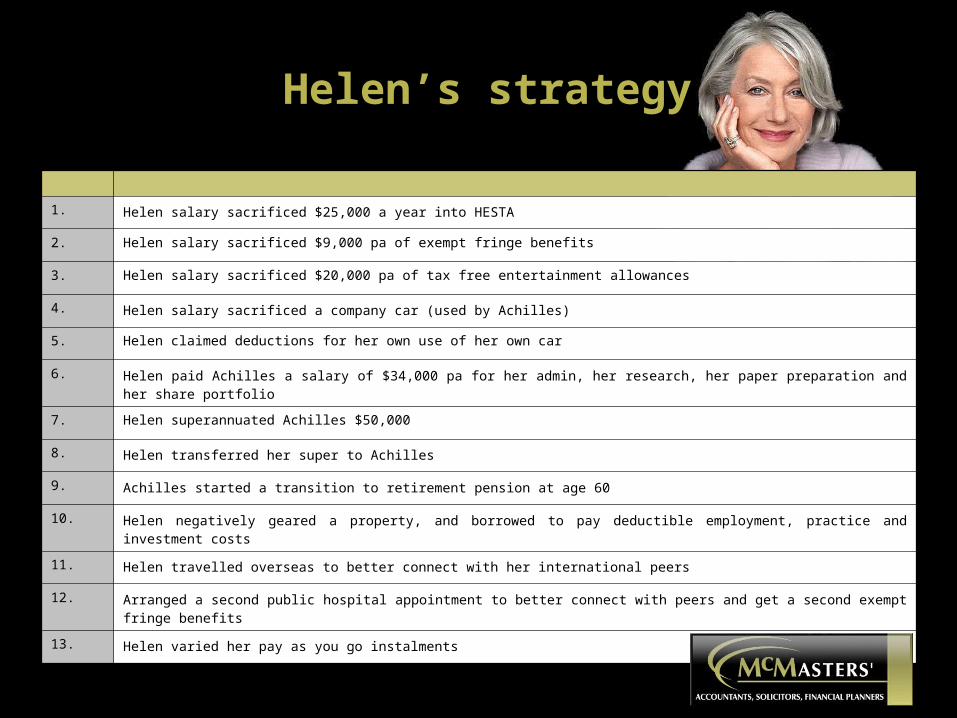

Helen’s strategy

1. Helen salary sacrificed $25,000 a year into HESTA

2. Helen salary sacrificed $9,000 pa of exempt fringe benefits

3. Helen salary sacrificed $20,000 pa of tax free entertainment allowances

4. Helen salary sacrificed a company car (used by Achilles)

5. Helen claimed deductions for her own use of her own car

6. Helen paid Achilles a salary of $34,000 pa for her admin, her research, her paper preparation and her share portfolio

7. Helen superannuated Achilles $50,000

8. Helen transferred her super to Achilles

9. Achilles started a transition to retirement pension at age 60

10. Helen negatively geared a property, and borrowed to pay deductible employment, practice and investment costs

11. Helen travelled overseas to better connect with her international peers

12. Arranged a second public hospital appointment to better connect with peers and get a second exempt fringe benefits

13. Helen varied her pay as you go instalments

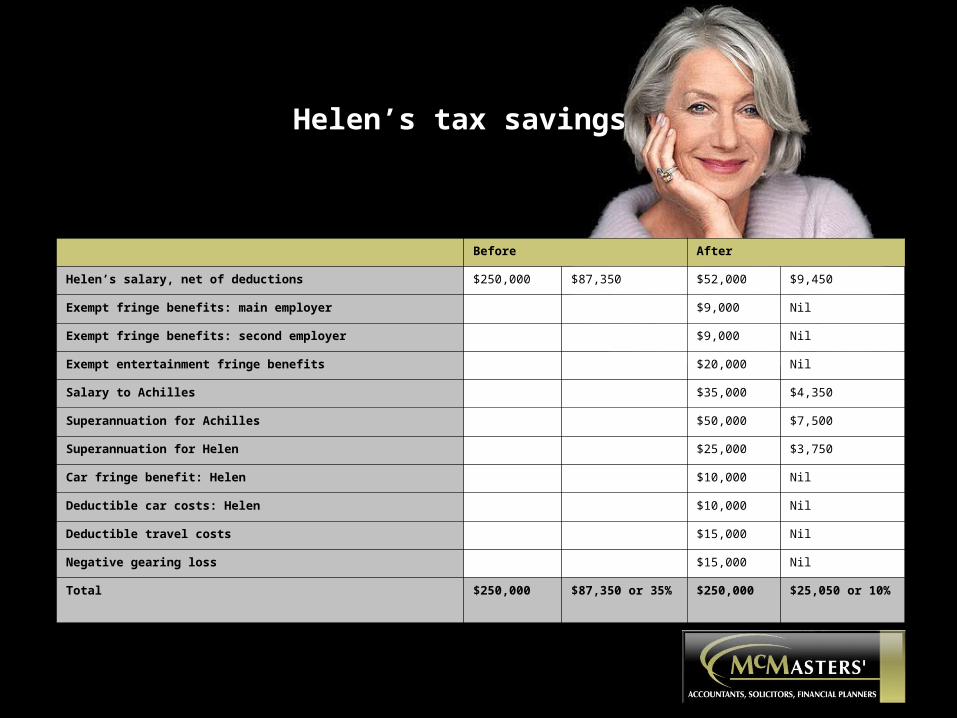

Before After

Helen’s salary, net of deductions $250,000 $87,350 $52,000 $9,450

Exempt fringe benefits: main employer $9,000 Nil

Exempt fringe benefits: second employer $9,000 Nil

Exempt entertainment fringe benefits $20,000 Nil

Salary to Achilles $35,000 $4,350

Superannuation for Achilles $50,000 $7,500

Superannuation for Helen $25,000 $3,750

Car fringe benefit: Helen $10,000 Nil

Deductible car costs: Helen $10,000 Nil

Deductible travel costs $15,000 Nil

Negative gearing loss $15,000 Nil

Total $250,000 $87,350 or 35% $250,000 $25,050 or 10%

Helen’s tax savings

MickeyThe tired 60 year old GP

Retirement Planning: The Problem

• Burn out is a real issue for older doctors, particularly males• At age 40 most doctors have completed a normal working life

– Ie [(40-15)*1.3*1.3] or 42 years work

• At age 60 most doctors have completed two normal working lives– Ie [60-15)*1.3*1.3] or 76 years work

• High pressure#• Heath problems#• High morbidity#• Marital and other relationship stresses#

#Source: Emotional Health. The Conspiracy of Silence Among Medical Practitioners. A review of the literature for the RACGP by Dr Danielle Clode University of Melbourne 2004 (accessible on www.mcmasters.com.au)

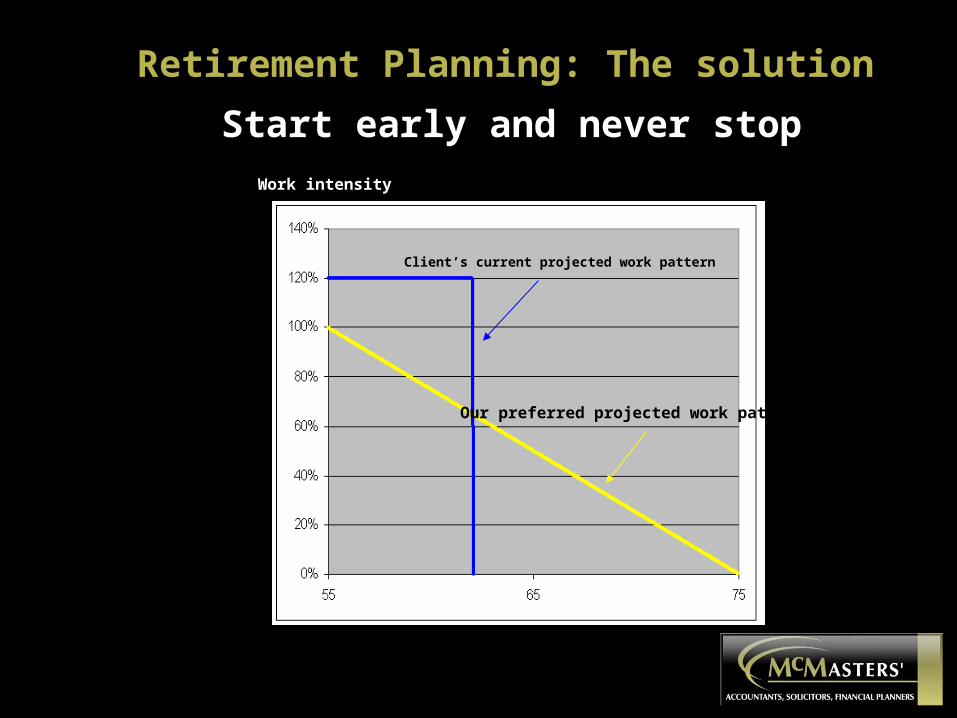

Client’s current projected work pattern

Our preferred projected work pattern

Work intensity

Start early and never stop

Retirement Planning: The solution

• Start early and never stop

• Live longer

• Have more fun

• Do more good

• Make more money

• Pay less tax

• And if you die, even better

Retirement Planning: The solution

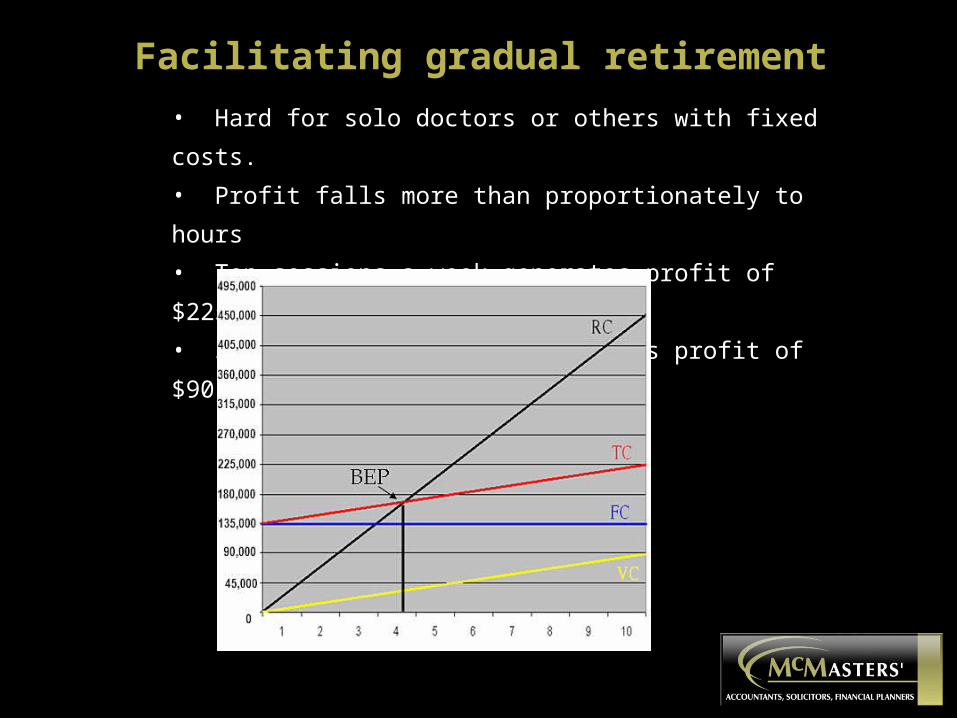

BEP

Facilitating gradual retirement

• Hard for solo doctors or others with fixed costs.

• Profit falls more than proportionately to hours

• Ten sessions a week generates profit of $225,000 pa

• Seven sessions a week generates profit of $90,000 pa

Retirement Planning

• Solution for solo doctors?

• Sell your practice

• Amalgamate your practice and negotiate a lower

management fee on own patients and reducing hours

• ensure continuity of care

• CGT exemptions on surgery

• If all else fails, abandon your practice and go

somewhere else

The Good News

• Serious shortage of GPs right around Australia

• Most practices are desperate for assistance

• Age is not an issue if you are a GP

• You are interviewing them, they are not interviewing you, and

will be flexible on working hours and related issues

• No reason why any doctor in good health cannot start to retire

at age 55 and finish at age 75, earning a very high income in a

very tax efficient form each year