handheld devices and handsets - ey - united states · 56 speeding ahead on the telecom and digital...

TRANSCRIPT

56 | Speeding ahead on the telecom and digital economy highway

4. Handheld devices and handsets

57Speeding ahead on the telecom and digital economy highway |

4.1. Introduction

Mobile handsets have played an integral part in the overall evolution of the mobile ecosystem in the country and have become agents of socio-economic transformation. Reduction of handset prices and increased affordability of services can be deemed critical success factors for the bourgeoning growth of wireless telephony. Currently, mobile handsets have evolved from communication-centric devices to all-encompassing communication devices that are no longer considered a luxury.

In future, mobile handsets and mobile tablets are expected to play a significant role in bridging the digital divide and connecting the country. Apart from being the primary communication medium for people, mobile devices are finding numerous uses across various domains. They are being used for banking transactions, making payments, as an educational and multi-media tool and for spreading governance. In addition, a mobile device is also an information dispersal platform across verticals such as agriculture and health care.

4.1.1. Size and evolution of Indian handset market

During the initial years of wireless telephony in India, customers had limited choice in terms of handsets, since the majority of devices were imported by a handful of global players. Moreover, the handsets and mobile services were both very costly and beyond the reach of low-income users. Over the years, the scenario has changed dramatically with a rapidly expanding telecom market, reducing tariffs, declining production costs and rising number of domestic players. Currently, the mobile handset and mobile tablet market in India has several players with varied offerings across all price points.

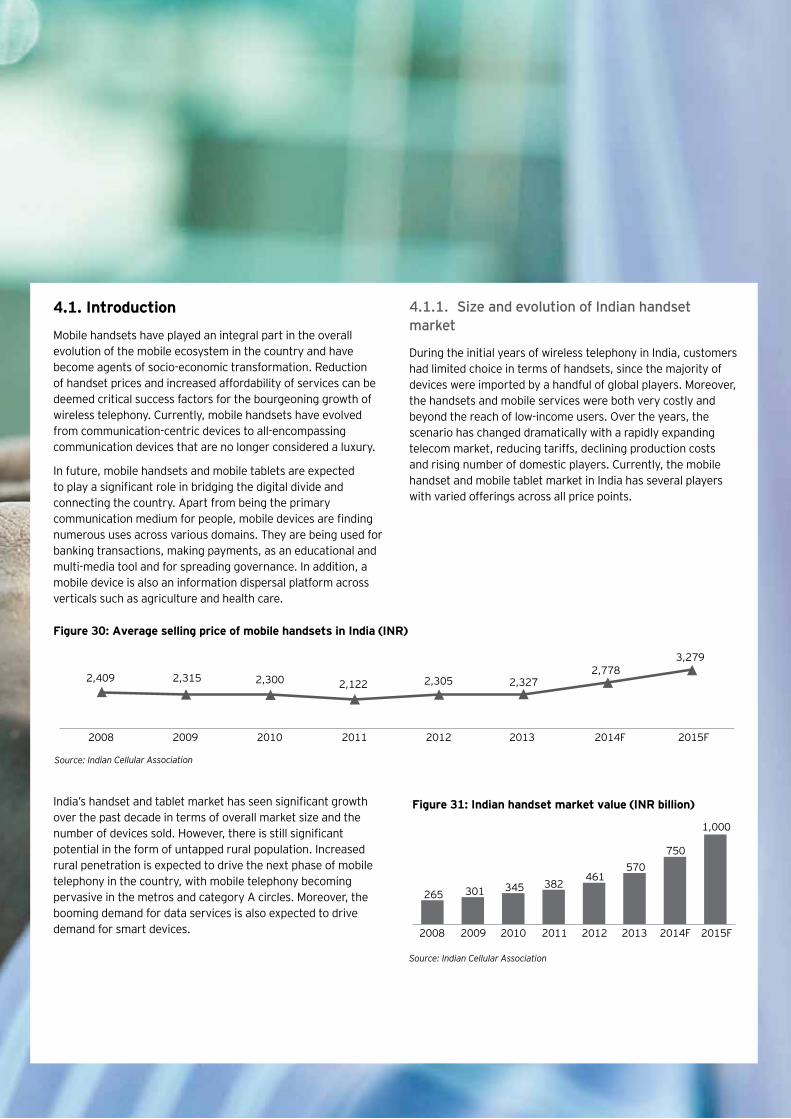

Figure 30: Average selling price of mobile handsets in India (INR)

2,409 2,315 2,300 2,122 2,305 2,327 2,778

3,279

2008 2009 2010 2011 2012 2013 2014F 2015F

Source: Indian Cellular Association

India’s handset and tablet market has seen significant growth over the past decade in terms of overall market size and the number of devices sold. However, there is still significant potential in the form of untapped rural population. Increased rural penetration is expected to drive the next phase of mobile telephony in the country, with mobile telephony becoming pervasive in the metros and category A circles. Moreover, the booming demand for data services is also expected to drive demand for smart devices.

Figure 31: Indian handset market value (INR billion)

265 301 345 382461

570750

1,000

2008 2009 2010 2011 2012 2013 2014F 2015F

Source: Indian Cellular Association

58 | Speeding ahead on the telecom and digital economy highway

Figure 32: Indian handset market volume (million)

110 130 150180 200

245 270305

2008 2009 2010 2011 2012 2013 2014F 2015F

Source: Indian Cellular Association

4.2. Indian handset market: key trends and drivers

Mobile devices are at the center of most things people do, from entertainment to communication and from banking to commuting; several factors are at play in shaping the demand for these devices.

Emergence of dual-SIM handsets: The emergence of dual-SIM handsets has been a game-changer for the Indian handset industry, since these phones allow consumers to take advantage of price arbitrage in tariffs offered by different operators. Furthermore, these handsets enable consumers to do away with the need to carry two handsets. First introduced by Indian manufacturers, the concept has found wide acceptance and has now become a standard feature in most handsets.

Figure 33: Smartphone market in India

0

300

600

900

1200

1500

0

50

100

150

200

250

2011 2012 2013 2014F 2015F 2016F 2017F 2018F 2019F 2020F

Value (billion)Volume (million)

Smartphone sale by volume (million) Smartphone sale by value (INR billion)

Growth of smartphones: In recent years, there has been an increasing trend of consumers opting for smartphones, since these offer a compelling user experience, with access to social media, emails and the internet. The boost in the demand for smartphones has been driven by the falling average selling prices of devices and a dip in data prices. Furthermore, with low penetration of PCs and a deficient fixed broadband network, smartphones are expected to drive the next phase of internet growth in the country.

The uptake of smartphones in India has been revolutionized by players that focus on introducing premium smartphones at affordable prices. These players have adopted innovative branding and marketing strategies to change the consumer preference toward smartphones.

Source: Indian Cellular Association

59Speeding ahead on the telecom and digital economy highway |

Demand for data and 3G/4G services: The demand for mobile data has grown exponentially, with ~92.6% of the total 254.4 million internet subscribers in the country accessing data from mobile devices.52 Moreover, with the country’s large population becoming “keypad literate,” and demand for internet becoming ubiquitous, the appetite for internet-enabled handsets and tablets is expected to improve further.

Adoption of 3G services is expected to be another driver of the demand for handsets. Although current 3G penetration remains low, the demand for the service has gained pace, and the prices of the service have come down sharply. All these are expected to drive adoption of the service. Additionally, operators are making considerable investments to roll out 3G sites and are aggressively promoting the service to monetize it. India is also expected to witness large scale rollout of 4G services this year.

Changing consumer preferences: The Indian market has seen a marked shift in consumers’ preferences. Consumers are willing to spend more than earlier to buy mobile devices, and are demanding fully loaded feature-phones and smartphones.

India’s handset market has also evolved in terms of consumer behavior. The frequency with which users change their devices has increased significantly. Going forward, the replacement market is expected to account for the bulk of handset sales in the country. In 2013, the handset replacement market was estimated to be around 80% of the total market.53

Innovative sales strategies: Innovative sales strategies such as EMI schemes and exchange offers have increased the affordability of high-end smartphones for consumers. There is also an increasing trend of handset manufacturers partnering with online retail platforms to help increase sales and reduce time to market.

52Telecom Regulatory Authority of India53“85% of Mobile Shipments to be Smartphones in India by 2016,” Telecom Circle Website, http://www.telecomcircle.com/2013/07/85-of-mobiles-to-be/, accessed 4 March 2014.

60 | Speeding ahead on the telecom and digital economy highway

4.3. Challenges in the current scenario and the way forward

4.3.1. Irrational structure of taxes and levies

In India, the importance of mobile devices has grown significantly, both in terms of contribution toward socio-economic development and the revenue generated in the form of taxes and levies. However, there is a need to strike the right balance regarding taxes levies imposed, ensuring end-user affordability and ensuring the vitality of the industry.

Inconsistent Value Added Tax (VAT) regime across states

Currently, there is an inconsistency in VAT on mobile handsets in the country, with different states in India charging different rates. This difference leads to price arbitrage and in the longer

run a parallel grey market. The emergence of a grey market, in turn, negatively impacts the tax collection of individual states. Similarly, the VAT rates in case of mobile accessories also vary from state to state, which leads to growth in sale of unbranded/sub-standard accessories. There is a need to address this ambiguity and bring in consistent guidelines.

Bringing handsets under the provisions of “Goods of Special Importance” under the Central Excise Tax Act, 1956 will cap the maximum VAT that can be levied by states at 5%. Department of Electronics and Information Technology (DeitY) has also highlighted the need to bring handsets under this category in the National Policy on Electronics 2012 (NPE 2012).54

Figure 34: VAT rate prevalent across states

State Rate as on 1 Apr’15 State Rate as on 1 Apr’15

Andaman & Nicobar (UT) NIL Kerala 5.00%

Andhra Pradesh 5.00% Lakshadweep (UT) NIL

Arunachal Pradesh 4.00% Madhya Pradesh 13.00%

Assam < INR15,000 5.00% Maharashtra 12.50%

Assam > INR15,000 14.50% Manipur 5.00%

Bihar 5.00% Meghalaya 5.00%

Chandigarh (UT) 5.00% Mizoram 5.00%

Chhattisgarh < INR3,000 5.00% Nagaland 5.00%

Chhattisgarh > INR3,000 14.00% Odisha < INR5,000 4.00%

Dadra and Nagar Haveli (UT) 4.00% Odisha > INR5,000 13.50%

Daman and Diu (UT) 4.00% Puducherry (UT) 5.00%

Delhi < INR10,000 5.00% Punjab 9.35%

Delhi > INR10,000 12.50% Rajasthan 8.00%

Goa 5.00% Sikkim 4.00%

Gujarat 15.00% Tamil Nadu 5.00%

Haryana < INR10,000 5.25% Tripura 5.00%

Haryana > INR10,000 8.00% Uttar Pradesh < INR10,000 5.00%

Himachal Pradesh 5.00% Uttar Pradesh > INR10,000 14.00%

Jammu & Kashmir 5.00% Uttarakhand 4.50%

Jharkhand 5.00% West Bengal < INR3,000 5.00%

Karnataka 5.50% West Bengal > INR3,000 14.50%Source: Indian Cellular Association

54Indian Cellular Association

61Speeding ahead on the telecom and digital economy highway |

Imposition of NCCD charge on mobile phones

National Calamity Contingent Duty (NCCD) of 1% of maximum retail price/retail selling price (MRP/RSP) was imposed on import of mobile phones in the Union Budget 2008–09.55 The proceeds of NCCD are aimed to be used for relief and rehabilitation in areas struck by natural disaster.

The NCCD charge on mobile handset was shifted from polyester filament yarn, which is now exempted. It is recommended that NCCD of 1% be shifted to other high volume goods, since the charge has been imposed on mobile handsets for several years now, to rotate the incidence on other industries in the interest of equity.

Charge for allocation of IMEI numbers

Mobile Standards Alliance of India (MSAI) is the authorized body for allocation of International Mobile Station Equipment Identity (IMEI) numbers in India and charges a fee from the mobile device importer/brand owner for allotment of these numbers. Given the importance of IMEI number in identifying individual mobile devices and the role it plays in tracking or blocking of a device in case of theft, this fee should be removed.

4.3.2. Weak ecosystem for local manufacturing

In spite of India’s handset market growing at a robust rate, almost 83% of the demand is met via imports, while domestic production and manufacturing continues to lag.56 It is imperative that measures are taken to address this mismatch and reduce the dependence on imports. Correcting this imbalance will not only lead to saving of foreign exchange, but also result in build-up of local capabilities and job creation.

The Government has recognized the need to bolster telecom equipment manufacturing in the country, and subsequent National Telecom Policies have also acknowledged telecom manufacturing as critical to the overall economic growth of the country. In the Union Budget for 2015–16, the Government rationalized duty on import of mobile phones and mobile tablets in the country, a move aimed to provide a fillip to the local manufacturing of these devices in the country.

Furthermore, electronic systems or the electronics system design and manufacturing (ESDM) industry has been identified as one of the focus sectors under the Make in India program. Given the pivotal role of mobile handsets and tablets in enabling the dream of a Digital India, favorable policies for manufacturing of these devices need to be instituted.

To further the efforts under the Make in India program, DeitY has established a joint task force of industry representatives and government officials with an aim to achieve production of 500 million handsets by 2019.57 The task force aims to rejuvenate the mobile handset and component manufacturing ecosystem in the country and targets to create additional employment opportunities for 1.5 million people.58

• Make VAT rates uniform for mobile handset and mobile accessories across states.

• Bring handsets under provisions of “Goods of Special Importance” under the Central Excise Tax Act, 1956; therefore, capping the maximum VAT that can be levied by states at 5%.

• Shift NCCD charge of 1% from mobile phones to other goods, to share the levy equitably among industries.

• Do away with imposition of a fee for allocation of IMEI numbers, since such a practice is not followed by other countries.

Key recommendations

55“Budget 2008 – 2009,” India Budget website, http://indiabudget.nic.in/ub2008-09/bs/speecha.htm, accessed 20 March 2014.56Indian Cellular Association57“Government sets up task force to revive domestic mobile manufacturing,” India in Business website, http://indiainbusiness.nic.in/newdesign/index.php?param=newsdetail/10473, accessed on 24 April, 2015. 58Ibid.

62 | Speeding ahead on the telecom and digital economy highway

Figure 36. Mobile handset market — value imported and exported (INR billion)

133 154258 252

346422

585.5

757.5

115 125 153 120 120 118.524.5 0

2008 2009 2010 2011 2012 2013 2014F 2015F

Import value Export value

While the service sector in India has evolved at a frantic pace, the manufacturing sector has failed to keep pace. Development of manufacturing ecosystem has been hampered by lack of investor friendly policies, flux in taxation policies, and the lack of effective labor reforms. To overcome these challenges and to encourage companies to manufacture in India, Government of India launched a flagship program — Make in India.

The program, launched in September 2014, aims to strengthen the manufacturing ecosystem in the country by promoting investment, fostering innovation and enhancing skill development. Under the initiative, 25 priority sectors have been identified, which will receive special focus from the Government.

• Automobiles

• Automobile component

• Aviation

• Biotechnology

• Chemicals

• Construction

• Defence manufacturing

• Electrical machinery

• Electronics systems

• Food processing

• IT and BPM

• Leather

• Mining

• Oil and gas

• Pharmaceuticals

• Ports

• Railways

• Renewable energy

• Roads and highways

• Space

Identified sectors:

• Textile and garments

• Thermal power

• Tourism and hospitality

• Wellness

• Media and entertainment

Indian ESDM industry, which is expected to be ~US$94 billion in 201559 has been identified as one of the focus sectors under the Make in India program.

• The ESDM sector within India is already of considerable size; in years to come, more growth is expected, and ESDM’s contribution to India’s GDP is expected to grow.

• Fueled by considerable planned government investments (such as the NPE 2012 and Digital India program) India’s ESDM sector will accelerate in years to come.

• Market potential is fueled by high market readiness, with a pattern of significant increases in consumption and high demand for all sub-segments of the ESDM sector.

• The rising penetration rate of mobile phones, along with growing internet usage, will boost the development of India’s ESDM sector.

• The large low-cost labor force and considerable domestic market combine to make India an attractive manufacturing base for the ESDM sector.

Mobile handset industry, which accounts for the largest share of electronic products sold in the country is expected to benefit due to policies instituted for the ESDM industry.

Figure 35. Mobile handset market — units imported and exported (million)

50 7090

130 130

188225

259

55 68 80105

85.0 73

14 0

2008 2009 2010 2011 2012 2013 2014F 2015F

Import Export

Source: Indian Cellular Association Source: Indian Cellular Association

Make in India

59“Electronic Systems,” Make in India website, http://www.makeinindia.com/sector/electronic-systems-design/, accessed 25 April 2015.

63Speeding ahead on the telecom and digital economy highway |

Tax holiday for new units entering manufacturing of handsets and tablets

The domestic market for mobile handsets is expected to cross 300 million devices in 2015, while the number of devices being manufactured locally is expected to be only 46 million. This schism highlights the need for provision of incentives for the setting up of new handsets and tablets manufacturing units in the country.60 Vietnam is a prime example of a country, which has witnessed a sharp increase in its electronics manufacturing industry, with big ticket investments from some of the leading global players.

Vietnam has emerged as a global hub for manufacturing of mobile handsets, supported by a stable regulatory environment and favorable incentive schemes. The country offers 30 years of tax holiday window at just 10% tax on mobile manufacturing. This further goes down to 100% exemption in the first four years and reduction of 50% in the next nine years.61

India needs to consider providing a 10-year tax holiday on a block of 15 years on all profits and gains from manufacturing or rendering of services in or in relation to the mobile phone industry. This benefit should be provided to all fresh investment made in plant and machinery and other equipment of a durable nature for special economic zones (SEZ), domestic tariff areas (DTAs) and export-oriented units (EOUs).

Interest subsidy on fixed capital investment

The National Policy on Electronics 2012 (NPE 2012) has called for a favorable tax regime that promotes investments, given the burgeoning demand for ESDM in India. To capitalize on this demand, and promote domestic manufacturing, providing interest subsidy on fixed capital investment needs to be evaluated.

Under the current duty structure, no interest subsides are available for the ESDM sector, while similar incentives are available to other sectors. The Technology Upgradation Fund Scheme (TUFS) provides for interest subsidy of 5% for the textile and jute industries in India.

Deemed export benefit for domestically manufactured handsets

Local handset manufacturers have been affected by the Information Technology Agreement (ITA 1) with the World Trade Organization and the governments of certain countries. Manufacturers, who import handsets under the ITA 1 agreement, enjoy concessional Basic Custom Duty (BCD) of 0%. To incentivize manufacturing and create a level playing field for Indian manufacturers, domestically manufactured ITA 1 products should be treated as “deemed exports” in terms of the provisions of the Foreign Trade Policy (FTP) 2015–2020.62

Extending the benefits under the FPS

The global demand for mobile handsets is increasing strongly and creation of strong ecosystem for local manufacturing will stand India in good stead. Currently, push button mobile phones are entitled to duty credit scrip equivalent to 5% of FOB (free on board) value of exports (in free foreign exchange) under the FPS.63 To further incentivize local manufacturing of handsets in India, the Government should consider extending this benefit to touch phones, smartphones and tablets.

Moreover, extending the 5% FPS benefit to all handset parts and components will provide a fillip to the industry and help attract investments for manufacturing of these items. Currently, handset parts such as camera, battery, charger, and hands-free kit etc., get a benefit of 2% under the scheme.

Reformulation of the export incentive policy for zero duty ITA goods

Currently, supplies into domestic tariff area from SEZs and EOUs are recognized as exports only for the purpose of calculation of export obligation. However, other export benefits such as refund of taxes on inputs used in the manufacture of ITA goods for the DTA are not available.

In order to make the industry competitive in an ITA zero duty environment, it is suggested that all manufacturing of ITA items should be treated fully at par with physical export for the purpose of incentives.

60Ibid.61Ibid.62Indian Cellular Association63Ibid.

64 | Speeding ahead on the telecom and digital economy highway

Income tax exemption on mobile phone exports/sales to DTA

ITA goods have to compete in a zero duty environment in the world market. Income tax on the profit derived from exports make the industry less competitive.

It is suggested that the Electronic Hardware Technology Park (EHTP)/SEZ schemes should have a special chapter on ITA goods with the following incentives:

• Income tax holiday on export from SEZ should continue as envisioned in the SEZ Act 2005 passed by the Parliament. Subsequent amendments, which detract from the tax holiday such as Minimum Alternate Tax (MAT), may be done away with, at least in the case of IT goods exports.

• The same regime should be adopted for the parallel EHTP scheme as well as export from DTA to compete with major electronic exporting countries particularly China and Vietnam, where exports enjoy special dispensation in their direct tax regime.

State-level daughter policies on ESDM manufacturing

Electronics hardware industry is the largest and the fastest growing manufacturing industry in the world, and stood at US$1.75 trillion in 2012, and is expected to grow to US$2.4 trillion in 2020.64 The industry comprises semiconductor design, high-tech manufacturing, electronic components and electronic system design for consumer products, telecom products and equipment, and IT systems and hardware.

India is one of the fastest-growing markets for electronics in the world. There is a considerable potential to develop the ESDM sector in India to meet our domestic demand, and also to use the capabilities thus developed to successfully export these products from the country. The NPE 2012 aims to address the issue with the explicit goal of transforming India into an ESDM hub. It is recommended that the respective state governments come up with daughter policies, in sync with NPE, for establishing conducive policies for growth of the ESDM sector in the states.

Case study: Andhra Pradesh Electronics Policy 2014–2020

Government of Andhra Pradesh aims to develop the electronics industry as an important growth engine for the state through effective use of the talent pool, skill enhancement, promotion of innovation and future technologies, as well as creation of infrastructure. The policy aims to attract investments to the tune of US$5 billion in the ESDM sector and create employment for 400,000 people by 2020.

Key strategies and incentives:

• The Government of Andhra Pradesh proposes to promote the development of 20 electronic manufacturing clusters (EMC) across the state. The EMC scheme intends to create infrastructure highly suited to electronics units by providing a subsidy of 50%.

• The Government will make efforts to attract investments to the tune of INR300 billion (US$5 billion) and facilitate the units to get the 25% capex subsidy under the MSIPS.

• It will provide 10% subsidy on new capital equipment for technology upgrading, limited to INR2.5 million as one time availment by the eligible company.

• The Government intends to provide power subsidy of 50% to micro, 40% to small, 25% to medium and 10% to large-scale industry limited to INR5 million.

• The electronics industry will be exempt from the purview of statutory power cuts.

• There will be 100% tax reimbursement of VAT/CST, for the new units started for a period of 5 years from the date of commencement of production for products manufactured and sold in Andhra Pradesh.

Source: Andhra Pradesh State Portal

64National Policy on Electronics 2012

65Speeding ahead on the telecom and digital economy highway |

Case study: Uttar Pradesh Electronics Manufacturing Policy 2014

Government of Uttar Pradesh has adopted the “Uttar Pradesh Electronics Manufacturing Policy 2014” with an aim to promote and develop the electronics manufacturing industry within the state, thereby, making Uttar Pradesh a globally competitive and industry friendly state for electronics design and manufacturing.

Key strategies and incentives:

• Single window clearance unit to work closely with the investors to efficiently and smoothly assist the investors in processing incentives claims as laid down under the policy; to facilitate investors in obtaining statutory clearances such as pollution control, shop and establishment act, power allocation etc.

• Capital subsidy of 15% on fixed capital, other than land, subject to maximum of INR50 million.

• Interest subsidy of 5% per annum for a period of seven years on the rate of interest paid on the loans obtained from scheduled banks/financial institutions will be reimbursed subject to a maximum of INR10 million per annum per unit.

• 100% tax reimbursement on VAT/CST subject to a maximum of 100% of fixed capital investment other than land (such as building, plant, machinery, testing equipment) for a period of 10 years.

• A memorandum of understanding for uninterrupted power supply, which will ensure commitment of reliable and quality power.

Source: Department of Information Technology and Electronics, Uttar Pradesh

Case study: Draft Electronics Hardware Manufacturing (ESDM) Policy, Government of Maharashtra

The Government of Maharashtra has drafted the “Draft Electronics Hardware Manufacturing Policy” with an aim to establish the state as the hub of ESDM manufacturing in India. The State Government envisions that via favorable investment policies the state will be able to attract investments to the tune of U$15 billion, and help generate employment for 3.6 million people. The State Government also anticipates that the ESDM sector will have a turnover of US$60 billion by 2020.

Key objectives of the policy:

• To strengthen the chip design, VLSI and embedded software industry and achieve a turnover of US$2 billion by 2020.

• To increase ESDM exports to US$6 billion by 2020.

• To promote creation of intellectual property in the ESDM sector by providing an impetus to research and development, start-up ESDM units and nanoelectronics sector.

• To create special financing dispensation to arrange soft loans to set up ESDM units.

• To create specialized departments/governance structures within the state government to cater to specific needs of the ESDM sector.

Source: Indian Cellular Association

66 | Speeding ahead on the telecom and digital economy highway

4.3.3. Presence of grey market and the lack of implementation of standards

Grey market comprises transactions, which are done outside authorized channels of trade and mainly includes counterfeiting, smuggling and tax evaded goods. There exists a considerable grey market for unbranded mobile phones in India. The presence of grey market deters mobile device players’

from investing in business growth and, future research and development (R&D), while causing significant revenue loss for the industry. Moreover, the sale of such handsets causes loss to the exchequer in the form of foregone direct and indirect taxes. It is estimated that branded devices have a total disability of 21%–30% against grey market devices, which includes outgo on taxes, quality compliance, and warranty and after sales.65

Figure 37: Gray market of mobile handsets India

0

50

100

150

200

0

20

40

60

2008 2009 2010 2011 2012 2013 2014F 2015F

Value (billion)Volume (million)

Sale by volume (million) Smartphone sale by value (INR billion)

• Ten-year tax holiday on a block of 15 years on all profits and gains from manufacturing or rendering of services in or in relation to the mobile phone industry.

• Minimum interest subsidy of 5% on all fixed capital investments for the entire ESDM sector on the lines of benefits given under TUFS.

• Domestically manufactured ITA 1 products should be treated as “deemed exports” in terms of the provisions of the FTP 2015–2020 to incentivize local manufacturing.

• The Government should consider extending the 5% FPS benefit accorded to push button mobile phones, to touch phones, smartphones and tablets as well.

• There is a need to increase FPS benefits for handset parts and accessories (memory/external memory, camera, battery, charger etc.) from 2% to 5%.

Key recommendations

• Incentive available to exports should also be extended to SEZs, EOUs and EHDPs.

• EHTP/SEZ schemes should have a special chapter for ITA goods with the following benefits:

• Income tax holiday on export from SEZ should continue as envisaged in the SEZ Act 2005 and subsequent amendments, which detract from the tax holiday, need to be done away with.

• The same regime needs to be put in place for EHTP scheme and export from DTA.

• State governments should come up with daughter policies on ESDM manufacturing in sync with National Policy on Electronics 2012.

Source: Indian Cellular Association

67Speeding ahead on the telecom and digital economy highway |

Figure 38: Revenue loss to government from sale of mobile phones in grey market, 2014

Loss to the exchequer (INR billion)

Direct tax loss Indirect tax loss Total Loss

10.4 56.6 67

Source: FICCI CASCADE

Issues arising from non-adherence to standards such as SAR and RoHS: Counterfeit handsets do not adhere to the health and safety standards as laid down by the government such as those pertaining to specific absorption rate (SAR) guidelines and the use of non-hazardous substances.

Another issue plaguing the industry has been the increase in the import of unbranded and substandard mobile device chargers. These chargers, which currently account for approximately 25% of the total market, lead to health and safety related threats due to power leakage and non-compliance to Restriction of Hazardous Substances (RoHS) limits.66 The proliferation of unbranded chargers also results in increased power consumption. These chargers, which are not subject to any standards, take increased amount of time to charge handsets. This leads to increase in gross power consumption straining the limited energy resource of the country.

Other tangential issues: Illegally imported handset and other telecommunications equipment also pose a threat to national security, as these can be misused by non-state actors. Furthermore, there is evidence that money generated from piracy and smuggling of goods has been used to fund terrorist activities.

• The industry for counterfeit handsets and chargers continues to thrive due to the absence of a concerted strategy and the lack of definite guidelines to manage the issue. Moreover, the implementation of existent rules pertaining to safety standards of these devices continues to be weak, especially those relating to mobile phone batteries.

• Inclusion of mobile handsets, mobile adaptors and mobile phone batteries in the list of products under DeitY’s compulsory registration scheme for electronic products. Currently, 15 items including mobile tablets are a part of this list.

• Stringent implementation of rules relating to reduction in the use of hazardous substances in manufactured/ imported electrical and electronic equipment. Rules relating to RoHS were enacted in 2012, and came into effect from 1 May 2014.

• Protecting customer interests by assuring quality through establishment of Bureau of Indian Standards (BIS) standards for mobile phones sold in the country.

• A Bureau of Energy Efficiency (BEE) rating for mobile device chargers needs to be adopted. This will not only help consumers identify energy-efficient chargers but also help conserve energy in the long run.

Key recommendations

65Indian Cellular Association66FICCI Communications and Digital Economy Committee

68 | Speeding ahead on the telecom and digital economy highway

4.3.4. IPv6 compliance for mobile handsets

The future of the internet lies in an efficient numbering and addressing system, and the transition to Internet Protocol version 6 (IPv6) is a welcome step. The Government has taken progressive steps through NTP 2012 in recognizing the importance of IPv6 and its subsequent role in supporting innovative IP-based applications in different sectors of the economy.

Given the recommendations laid down by DoT, all new devices launched after July 2014 are capable of carrying IPv6 traffic; however, the ecosystem for testing and compliance remains deficient.

• Telecommunication Engineering Center’s (TEC) lab for testing of mobile handsets is not ready.

• The RFCs are defined according to the TEC IR document but do not identify the relevant test specification, which makes IPv6 compliance a challenge.

FICCI CASCADE

In 2011, FICCI established “FICCI Committee Against Smuggling and Counterfeiting Activities (FICCI CASCADE),” a dedicated forum to address the industry’s concerns of counterfeit products.

Aims of FICCI CASCADE

• Generating awareness on the hazardous impact of smuggled, contraband and counterfeit products among consumers and citizens

• Capacity building of law enforcement agencies including judges, police and customs officers

• Researching and proposing law reforms

• Interacting with law enforcement authorities to emphasize on the importance of continued awareness and seriousness of the impact of counterfeit goods

• Enforcing IP-related laws

• Systematically disseminating enforcement techniques, procedure and strategy through regular workshops for the guidance of its members

• Sharing best practices followed globally for combating contraband, smuggled and counterfeit product

• Providing knowledge support to industry members

Source: FICCI CASCADE website

• ► Standards and labs for testing and compliance of IPv6 need to be established.

Key recommendations

“All mobile phone handsets/ data card dongles/ tablets and similar devices used for internet access supporting GSM/CDMA version 2.5G and above sold in India on or after 30-06-2014 shall be capable of carrying IPv6 traffic either on dual stack (IPv4v6) or on native IPv6.”

– DoT recommendation on IPv6

69Speeding ahead on the telecom and digital economy highway |

88 | Speeding ahead on the telecom and digital economy highway

6. Emerging opportunities: Cloud and M2M

89Speeding ahead on the telecom and digital economy highway |

6.1. Cloud services

6.1.1. Introduction

Over the last few years, cloud computing has emerged as one of the most defining secular trends and it is believed that its effects are beginning to be felt across various industries. Cloud services are finally taking off because technology advances, particularly ubiquitous high-speed internet connectivity and the ever-decreasing cost of storage, have finally enabled service providers to meet buyers’ needs for simplicity, cost and flexibility.

For consumers, the recent proliferation of smart mobile devices, that are actually handheld wireless computers, has accelerated the development of cloud services that provide application functionality to those devices. This is an example of why consumers have been such rapid adopters of the cloud — cloud computing has the potential to instantly deliver simple, easy-to-use, sophisticated and high-powered computer applications and information that consumers could not otherwise access.

Organizations are using the cloud technology to increase operational efficiency, improve collaboration, and gain competitive edge by delivering differentiated services. The shift to cloud helps organizations in achieving business agility and scalability, which enables them to be more responsive in the rapidly changing market.

Figure 47: How companies are using cloud today?

Transform infrastructure by changing application

delivery method.

Deliver a new service, or existing service to

a new market.

Arming your people with the best tools to

increase productivity.

Efficiency and Transparency Channel Startegy Workforce Innovation

Undergoing a major IT TransformationAging Infrastructure/workforceTransparency in cost, and cost reduction

Drive new revenueExpand client baseReach new customersExpand market footprint

Implement new technology applications based on user requirements and increasing mobility demandImprove end user driven collaboration(maximize productivity)

►► ►

►

►

►

►

►

►

Source: EY analysis

90 | Speeding ahead on the telecom and digital economy highway

6.1.2. Cloud computing spanning across industries

Cloud computing has the power to transform traditional operations of a business, and is bringing about significant changes across several sectors. It is acting as a catalyst for growth to bring about robust value additions across verticals.

Some industries are adopting cloud to reduce their capital expenditure on IT while others are utilizing cloud to better collaborate and deliver high-value add to its customers. For example, financial institutions and the banking sector are adopting cloud technology to reduce upfront IT cost, whereas health care companies are exploring cloud technology to enable better patient reach and care.

As enterprises are becoming increasingly aware, this technology is gaining popularity across various industries, since they operate in an evolving and highly competitive marketplace. According to a research report, the number of cloud applications used by various industries is expected to increase by 36% between 2011 and 2014.77

Figure 48: Global average number of cloud applications per company

10.8

10.9

12.4

13.2

13.3

13.6

14.3

17.6

18.0

19.4

9.34.8

3.4

4.5

4.4

5.7

5.1

5.5

5.7

6.8

6.2

8.5

Media and entertainment

Health care services

Energy and utilities

Metals and Mining

Consumer productmanufacturing

Pharmaceuticals

Retail

Transport

Banking and Insurance

Telecom services

Communicationequipment manufacturer

2011 2014Source: TCS website

Figure 49: Cloud services across verticals

6.1.3. Clouds offer full range of computing services

Cloud computing is becoming a business-changing technology, which has not only affected the IT industry considerably, but is also transforming the business models of telecoms operators across the globe. Cloud computing services are available across the entire computing spectrum.

• Infrastructure-as-a-Service (IaaS) is a provision model in which an organization outsources equipment used to support operations, including storage, hardware, servers and networking components.

• Software-as-a-Service (SaaS) is a software distribution model in which applications are hosted by a vendor and made available to customers over a network, typically the internet. Applications both general, such as word processing, email and spreadsheet, and specialized, such as customer relationship management (CRM) and enterprise resource management (ERM) are the typical service offerings.

• Platform-as-a-Service (PaaS) is another upcoming area highlighted in the survey, and is used to develop and deploy applications on the cloud. It typically includes databases, development tools and other components required to support the delivery of custom applications.

77“Differences in Cloud Adoption Across Global Industries,” TCS website, sites.tcs.com/cloudstudy/differences-in-cloud-adoption-across-global-industries#.UhxkJTssUhU, accessed on 27August 2013.

Source: EY analysis

91Speeding ahead on the telecom and digital economy highway |

• Communication-as-a-Service (CaaS) is increasingly being used to describe a suite of cloud-based unified communication applications, which include audio and web conferencing, desktop conferencing, email, instant messaging, mobility features, voice, document sharing and enterprise-grade social networking.

• Network-as-a-Service (NaaS) is a category where cloud-based service users are provided network connectivity services on a pay-as-you-use model. In this, the mobile network, billing and informational assets are bundled together.78

Indian government emphasizes the need for cloud computing

The NTP-2012 emphasizes on the need for cloud computing with the following objectives:

• To recognize that cloud computing will significantly speed up design and roll out of services, enable social networking and participative governance and e-Commerce on a scale, which was not possible with traditional technology solutions.

• To take new policy initiatives to ensure rapid expansion of new services and technologies at globally competitive prices by addressing concerns of cloud users and other stakeholders including specific steps that need to be taken for lowering the cost of service delivery.

• To identify areas where existing regulations may impose unnecessary burden and take consequential remedial steps in line with international best practices for propelling the country to emerge as a global leader in the development and provision of cloud services to benefit enterprises, consumers and Central and state governments.

The TRAI is working on a paper on cloud. Separately, a working group at DeitY is also working on enabling cloud services in India covering aspects such as jurisdiction, cross-border data flow, data security, data location and much more.

There is a need for a coordinated effort and a uniform cloud policy from the Ministry of Communications and Information Technology

6.1.4. Challenges and the way forward

6.1.5.1 Data center location

In line with the nature of cloud architecture, it is possible that consumer data is split and stored at multiple locations. As data sometimes falls under more than one legal jurisdiction, there is no clarity on how inconsistencies across jurisdictions can be resolved. Governments are concerned about weakening or redeeming their “legal controls” due to jurisdictional compliance and to “oversee” data on the cloud and apply their laws to the cloud.

• Free flow of non-critical data across borders: A majority of Indian industries involved in IT-enabled services (ITeS) benefit substantially from cross-border flow of networks and data-based services; the ITeS sector is likely to be at a disadvantage if India adopts policies that limit the country’s ability to move data on a cross-border basis. Any restrictions that India imposes are likely to become restrictive precedents that other countries adopt, which will restrict the movement of data to Indian BPOs or data centers. With this in mind, the default position should be that cloud-based services can utilize data centers either within or outside India.

• Mission critical data to be stored in India: There will be certain narrowly tailored instances where Government’s mission-critical data is best secured within the geographical boundaries of the country. In these narrowly tailored instances, findings should be made on a case-to-case basis, rather than adopt a blanket rule that may unnecessarily compromise India’s role in a global information economy. The Government should frame policies to keep mission-critical data within the geographical boundaries of the country, such as data for sectors of national importance such as defence should reside within India. Non-critical data/applications can be stored outside the country. However, the Government should retain the rights to access the data if needed.

78“Network as a Service,” DSG website, www.dsg.co.za/Default.aspx?TabID=54, accessed on 25 July 2013.

Source: DeitY, NTP-2012

92 | Speeding ahead on the telecom and digital economy highway

• No separate statewide regulations: The Government should avoid varying regulations across states and formulate a single nationwide policy. It should avoid localizing mandates or any policies that give preference to data processors using only local facilities or operating locally. Any sweeping restriction on data center location or on cross-border data flow restriction will create a precedent, which may be adopted by other countries that could be devastating to the Indian BPO industry, which is entirely dependent on the ability of cross-border data flow into India.

If India were to adopt overly broad restrictions, other countries will follow this lead and this will directly harm the services economy. With this in mind, the default position should be that cloud-based services utilize data centers either in India or outside India.

6.1.5.2. Security and risk of data loss

Customers are concerned that transmitting and storing data over a public internet, as opposed to storing it entirely within an exclusive corporate network, is likely to increase data vulnerability and expose it to unauthorized users. As the cloud aggregates data and services of multiple users on the same platform, it becomes an easy target for cyber-attacks. If encryption standards are not strong, it will be vulnerable to store and transmit data over the network.

6.1.5.3. Data privacy

Since data on the cloud is stored on remote machines, which are shared with other users, customers are concerned about the potential of competitors accessing their data. Even though concern over privacy is secondary to its concern over security for cloud sharing, the storage space with its competitors definitely poses a concern for the cloud customer.

6.1.5.4. Requirement of robust interoperability standards

The ability of clients to move data across various cloud providers is restricted due to the “vendor lock-in” function; use of proprietary architecture; or unique application model employed by a cloud provider. Standards are required to simplify interoperability among cloud providers and between enterprise systems and cloud-based services, since very few exist currently. The lack of standards may also pose as an obstacle in recovering data for the purpose of legal discovery or for migrating from one cloud-based service provider to another.

• It is suggested that the Government could frame policies to expand the scope of a narrowly tailored view of mission-critical government data or national security-related data that is recommended for storage within Indian boundaries.

• The default position should be that cloud computing services utilize data centers either in India or outside India. The Government could contemplate formulating a single nation-wide policy avoiding regional/state-wise difference in regulations.

Key recommendations

• Government policy should adopt strengthened encryption standards rather than continue with 40-bit encryption.

• The Government should identify best practices such as ISO 27001 and SAS 70 for the audit process of a cloud-based service provider to provide assurance to its customers.

Key recommendations

• Bring cloud-based service providers under the purview of the Information Technology Act of 2000.

• The Government needs to spread awareness among consumers, especially its own departments, by educating them on data privacy legislations that apply to cloud-based service providers.

Key recommendations

93Speeding ahead on the telecom and digital economy highway |

6.1.5.5. Reliability

Typically, in a competitive market such as cloud computing, competition will deliver a range of service level agreements (SLAs) at various price points. This will deliver extra-high SLAs for mission critical cloud applications to businesses that will pay a premium. Furthermore, it will deliver services with low ensured SLA for cloud applications where a customer wants a value service and is willing to experience some service quality trade off. The Government could set some indicative benchmarks, but in a competitive market, it should also consider its role as a facilitator and not stifle business model innovation by imposing rigid SLA requirements.

6.1.5.6. Cross-border flow of data

Currently, there is a lack of clarity under which legal jurisdiction data on the cloud falls. Related concerns are about legal compliance issues such as whether laws in the jurisdiction where the data was collected apply or whether the laws at the user’s destination apply. As a result, constraints on trans-border flow of sensitive data are a key area of discussion while framing policies and regulations around data security.

6.1.5.7. Lack of credibility

Organizations using cloud-based services do not have complete visibility if the vendors are ensuring 100% compliance, which may result in oversight of privacy policies and procedures. Cloud computing increases the need for service providers to implement and adhere to the agreed service level agreements.

• The Government may work in collaboration with the MCIT and the industry to promote open standards-based cloud infrastructure and documented interfaces. These standards are expected to help increase software and data interoperability.

Key recommendations

• The Government should have a registration mechanism through a single window to approve cloud providers in the market. For this, the Government should collaborate with the industry to define minimum technical standards required to set up a cloud infrastructure.

Key recommendations

• The Government may work with the industry to set benchmark standards for SLAs, defining minimum commitment levels for critical service parameters such as uptime, response times and bandwidth. Furthermore, it should also consider its role as a facilitator and not stifle business model innovation by imposing rigid SLA requirements.

Key recommendations

• The Government should try to ensure that the necessary legal regulation of the country in which data originates is applicable to data controllers and data processors. There is a need to encourage accountability rules governing data flow and ensuring that consumers do not lose protection when their data is stored or processed in any remote computing environment outside the country.

Key recommendations

Compliance involves conformity with laws, regulations and standards regarding data security. A major compliance issue is the location of data storage. If the data resides within the premise of an organization, it can ensure that safeguards are in place to protect the data. Most cloud-based service provider do not disclose the location of data storage to their customers, which results in uncertainty pertaining to whether adequate safeguards are in place and whether legal and regulatory compliance requirements are being met.

94 | Speeding ahead on the telecom and digital economy highway

6.1.5.8. Clarity on taxation

Currently, there are no specific tax rules in the Indian taxation regime, since cloud computing-based services are nascent in the country. According to the current tax regime, the direct tax of cloud-based services depends on the residential status of the service provider, while the indirect tax depends on whether the cloud is classified as a service or as transfer of right to use property. There needs to be clarity on classification of the category of cloud services for taxation applicability.

6.2. Machine-to-machine (M2M)

6.2.1. M2M and IoT market overview

The evolution of internet in recent times has led to more devices being connected to each other. In future, these devices are expected to generate majority of the internet traffic. The interaction of these devices with each other and other static non-intelligent objects is termed as “internet of things” (IoT). To ensure such interaction, mobile technology is expected to play a transformational role in the future.

Figure 50: M2M and IoT as enablers for various industries

M2M is a subset of IoT and refers to machines communicating with the application infrastructure using network resources for purpose of monitoring or control, either of the machine itself or the surrounding environment. Additional services, along with M2M services, which involve physical world to merge with digital world together, form IoT.

IoT is fast becoming a reality globally. The use of connected devices and systems to leverage data from a range of physical objects is growing rapidly, transforming societies and economies in many new ways. Technology and services revenue from IoT are expected to expand from US$1.3 trillion in 2013 to US$3.04 trillion in 2020 with a compound annual growth rate of 13%.79 By the end of the decade, nearly 30 billion connected devices are estimated worldwide, with all regions experiencing growth.80

The upside represented by IoT remains highly promising — with use cases as diverse as home automation services, logistics tracking, pay-as-you-drive car insurance and much more. Partnerships are a key success factor for these emerging IoT service propositions. Go-to-market approaches for such initiatives remain flexible, with operators considering offering such services either directly to customers or via white-label platforms.

Application areas Automotive Logistics and fleet management

Monitoring/ automation

Remote sales and payments

Security/ surveillance

Health care

Applications

(examples)

• Infotainment and positioning services

• Active security• Post-crash

systems• Pay-as-the-

drive solutions• Remote

diagnostics• Traffic control

systems

• Logistics planning and optimization

• Fleet vehicle management

• Navigation• Fuel

Management• Sensors• Carbon

footprint

• Smart metering

• Smart grid• Field

equipment management

• Facility management

• Public surveillance and safety

• Remote sales management

• Remote credit card applications

• Mobile point of sales, e.g., taxis and vending machines

• E-commerce

• Cameras• Alarms and

surveillance systems

• Telemedicine• Remote

monitoring

Potential industry alliances

(examples)

• Automotive• Diversified

industrial products

• Safety• Media and

entertainment• Insurance

• Transportation• Construction• Diversified

industrial products

• Car leasing companies

• Utilities• Real estate• Chemicals• Oil and Gas• Retail• Government

and public sector

• Retail• Banking

• Security • Government

and public sector

• Heath care providers

• Life sciences• Insurance

Source: EY analysis

95Speeding ahead on the telecom and digital economy highway |

6.2.1.1. Snapshot of global and Indian M2M market

Global M2M market

According to industry estimates, around 61% of connected devices globally are expected to be categorized as M2M by 2022.81 The total number of global M2M connections is likely to reach 18 billion by 2022.82

The growth in the number of M2M connections is expected to result in significant revenue opportunity for all players in the ecosystem. By 2022, the total M2M revenue opportunity is expected to increase at a CAGR of approximately 20.5% to reach US$1.2 trillion, up from US$200 billion in 2011.83

Figure 51: Current status of global M2M connections

Indian M2M market

Currently, the Indian M2M market is at a nascent stage but offers high growth opportunities. Enterprises have realized the incremental benefits of M2M and have gradually started adopting these solutions. M2M solutions have already started gaining prominence in industries such as utilities, logistics and automotive and are in early deployment stages.

Figure 52: India M2M market growth Revenue in US$ million

22.9

98.4

2011 2016F

CAGR33.8%

Global M2M connections

Growth rate: 38% CAGR from 2010 to 2013

• Current status: 195 million connections in 2013.

• M2M connections account for 2.8% of all global mobile connections.

M2M adoption by operators

Growing momentum of M2M service offering by service providers

• As of January 2014, 428 mobile operators offered M2M services across 187 countries; equivalent to 40% of world's mobile operators.

• Growth is stronger in developing markets over the last three years — six out of ten operators offering M2M are located in developing countries.

Source: GSMA

Source: 6Wresearch

79“Finding Success in the New IoT Ecosystem: Market to Reach $3.04 Trillion and 30 Billion Connected ‘Things’ in 2020, IDC Says,” IDC, 7 November 2014.80“Finding Success in the New IoT Ecosystem: Market to Reach $3.04 Trillion and 30 Billion Connected ‘Things’ in 2020, IDC Says,” IDC, 7 November 2014.81“The Global M2M Market in 2013,” Machina Research white paper, January 2013.82Ibid.83Ibid.

96 | Speeding ahead on the telecom and digital economy highway

Figure 54: Government departments’ initiatives toward IoT and M2M

Figure 53: Key drivers of M2M services

Standardization and adoption of IPV6 technology

Government mandates and regulatory compliances

Improved network coverage and high speed data services

Cloud-based offerings

Declining technology and component costs

New revenue streams and differentiated service

offerings

Environmental sustainability Operational efficiency and cost savings

Key drivers ofM2M services

2014: The DeitY comes out with a draft IoT policy

• The policy focuses on the following objectives:• ► Create a US$15 billion IoT industry in India by 2020.

India is assumed to have a share of 5%–6% of global IoT industry

• ► Undertake capacity development (human and technology) for IoT specific skill-sets for domestic and international markets

• ► Undertake research and development for all assisting technologies

• ► Develop IoT products specific to Indian needs in all possible domains

The IoT policy framework is proposed to be implemented via a multi-pillar approach. The approach comprises five vertical pillars — demonstration centers, capacity building and incubation, R&D and innovation, incentives and engagements, human resource development; and two horizontal supports — standards and governance structure.

2015: DoT comes out with a draft National Telecom M2M roadmap

The document puts together various standards, policy and regulatory requirements and approach for the industry on how to look forward for M2M.

It provides the following:

► ► Overview of M2M, applications, opportunities and future of M2M

► ► Communication technologies and infrastructure for the last mile

► ► Global scenario for M2M standards and regulations ► ► DoT activities towards policy formulation and

development of standards ► ► M2M adoption supporting Make in India ► ► M2M’s influence on various sectors such as smart

cities, automobile, energy, utilities and much moreThe roadmap is expected to be reference document for all M2M ecosystem stakeholders and help in proliferation of M2M services in the country.

Need for synergy between DeitY’s draft IoT policy and DoT’s M2M roadmap

Source: DeitY, DoT.

Source: EY analysis

97Speeding ahead on the telecom and digital economy highway |

6.2.2. M2M: challenges in the current scenario and the way forward

The lucrative M2M market comes with a host of challenges, which may deter the segment’s growth potential. Given that this market is at a nascent stage not only in India, it is best to set up a strong policy framework, which ensures a conducive environment for the service to grow in future. Moreover, collaboration among the industry, government agencies, academia and global agencies on M2M will help in better planning for the concerns, which may arise as the market matures.

6.2.2.1. Lack of standardization and interoperability

The M2M market operates in a fragmented ecosystem where various players are offering similar solution with different technical specifications. With numerous M2M connections, integration of data from various nodes poses a unique challenge. Increased standardization is required to encourage investment and development in the M2M market. Protocols for interoperability, security, and performance need to be defined to enable the M2M market to grow. Such initiatives are also vital to contain product development costs and generate economies of scale.

Apart from the basic communication or “service layer” architecture of M2M devices, there is also a need for a standard protocol for communication between these devices and the central server. Similar to HTTP, which is the de facto protocol for World Wide Web, standards need to be produced for M2M/IoT connectivity protocols.

In line with this requirement, open standardization bodies such as Organization for the Advancement of Structured Information Standards (OASIS) are leading efforts for producing standards for protocols such as Message Queuing Telemetry Transport (MQTT). It is critical to adopt such measures toward an open, standardized communication protocol to ensure easy connectivity of devices to a central server and transmission of data with a reliable quality of service.

Globally, there are various groups, alliances and trade bodies such as the M2M Standardization Task Force (MSTF) and GSMA, which are working toward achieving standardization. In India as well, DoT, through its various arms such as the

Telecommunication Engineering Center (TEC) and the Centre for Development of Telematics (C-DOT), is partnering with One M2M Alliance (an alliance of leading global standardization bodies) to take care of India-specific requirements for M2M standards development. TEC has made five working groups to meet this objective.

• ► Coordination between government, industry and related global standards bodies to establish protocols for standardization, interoperability and performance, which are in line with global practices.

• ► National M2M standards should cover architecture, gateway, communication protocol/standards, vertical specific requirements and interoperability guidelines. White goods should be an additional category in standards formulation.

Key recommendations

6.2.2.2. Numbering scheme

On the M2M policy front, provisioning of numbering schemes for M2M services is one of the most significant aspects requiring regulatory clarity. Traditionally, most M2M devices are allocated numbers from the existing numbering schemes meant for mobile and fixed numbers. However, given that the M2M devices and services follow a different business model, usage of existing numbering schemes comes with its set of challenges.

Business models followed by M2M devices and services are considerably different from typical handsets and mobile services. The value chain for provisioning of M2M service includes mobile network operators providing wireless connectivity to M2M device manufacturers, who in turn provide M2M devices and services to end customers. The wireless connectivity is integrated within the M2M device meant for specific functions (such as smart metering, etc.) and the end customer is not charged separately for usage of a communications service. Moreover, M2M devices have low data consumption and low ARPU as compared to mobile phones and tablets. Due to these reasons, building economies of scale by developing standardized products is one of the main objectives of M2M device manufacturers.

98 | Speeding ahead on the telecom and digital economy highway

With such a view to curtail input costs, M2M device ecosystem will not flourish if country-specific numbering schemes are made mandatory. In such a case, the M2M device manufacturer will need a SIM card embedded with the country-specific International Mobile Subscriber Identity (IMSI) code for each M2M device to be distributed in that particular country, leading to increased inventory management costs. Moreover, requiring M2M device manufacturers to conform to country-specific E.16484 numbers, which are addressing schemes used to route calls to the appropriate destination in each country where they seek to distribute products, will substantially increase their costs.

Usage of country-specific numbering resources also means that the M2M device manufacturer will need to forecast customer demand with high accuracy in order to avoid cases where there are too many M2M devices with a SIM card properly coded for one country, but not enough devices for another country. Given the global scope of M2M services, the administrative costs and operational complexities of manufacturing will therefore, become overwhelming. With each individual country requiring reservation of numbering blocks, such a scenario is likely to result in unused part of blocks, leading to inefficient use of numbering resources.

Additionally, from the perspective of potential market for device manufacturers, country-specific numbering policy for M2M will undermine the proliferation of M2M services developed by global players in India, as well as deter global prospects for providing M2M services developed and originated in India.

In light of these challenges, an M2M system should be flexible to support more than one naming scheme. The M2M policy should enable the use of global numbering resources, and allow for global use of IMSIs and E.164 numbers. In this respect, the addressing schemes should include IP address of connected objects, IP address of group of connected objects (including multicast address), and E.164 addresses of connected objects.

Moreover, the ITU Recommendation E.21285 should be followed, which establishes a three-tiered plan for identification of geographic areas, networks and subscriptions. The E.212 standard makes roaming of devices possible by identifying the subscriber, the subscriber’s carrier and the carrier’s country, which, in turn, enables the visited network operator to authenticate the subscriber as an authorized roamer and to bill the home network operator appropriately.

Another aspect to be considered in M2M systems relates to the time of allocating numbers to devices. The Mobile Subscriber Integrated Services Digital Network (MSISDN), which follows the numbering plan defined in ITU’s E.164 recommendation, is used to uniquely identify a device.

Traditionally, each SIM card, associated with its IMSI, is allocated an MSISDN during manufacture and testing phase itself, thereby, pre-provisioning the subscriptions in the network. Given that M2M devices may actually not require permanent wireless connectivity or may be static, i.e., only operating in one geographic region, hence, such devices do not require unique provisioning of the subscription.

Accordingly, M2M policy should allow for MSISDN less subscriptions or dummy MSISDN-based subscriptions. Even in cases where there is a requirement for unique identifier, such as when M2M devices require permanent wireless connectivity and are mobile in nature, then the unique MSISDN can be dynamically provisioned when they are first used. Such a policy will enable efficient utilization of MSISDNs and save costs.

In recent years, several countries have started to realize the challenge posed by scarcity of numbering ranges to address the substantial number of M2M devices. This issue can be resolved by designating specific numbering ranges to M2M devices.

Telecoms regulators in some European Union countries (such as Ireland and Spain) have deliberated on allocating long 15 digit numbers for M2M devices

• A welcome step, since it addresses the demand for a large number of M2M devices.

• Additionally, the length of the numbering scheme does not pose a problem since these numbers are not designed for dialing by humans.

Source: Ovum

84Note: ITU-T E.164 provides for the international public telecommunication numbering plan; “Recommendation E.164,” ITU, http://www.itu.int/rec/T-REC-E.164/en, accessed 2 May 2014.85Note: ITU-T E.164 provides for the international identification plan for public networks and subscriptions; “Recommendation E.212,” ITU, https://www.itu.int/rec/T-REC-E.212/en, accessed 2 May 2014.86Cisco6lab, http://6lab.cisco.com/stats/index.php, accessed 19 March 2014.

99Speeding ahead on the telecom and digital economy highway |

• While framing its policy for numbering scheme for M2M services, the Government should consider the following:

• Formulate an M2M policy enabling the use of global numbering resources. In this respect, global use of IMSIs and E.164 numbers should be facilitated

• Supporting more than one naming scheme

• Adoption of ITU E.212 recommendation

• MSISDN less subscription/dummy MSISDN-based subscription

Key recommendations

Mandatory IP/IPv6 in transport network

In addition to forming a specific numbering scheme for M2M devices, availability of adequate IP addresses is also important. Since the IPv4 addresses have been officially depleted, timely transition to IPv6 protocol is necessary. India’s overall IPv6 deployment currently stands at 20.8%, which is much behind Belgium, the global leader with 39.3% IPv6 deployment.86 The Government has laid out a national roadmap for IPv6 deployment and in the first phase mandated Government-based organizations to migrate to IPv6 networks by end of 2017. The challenges in implementation withstanding, it is a positive step from the Government and India should further promote uptake of IPv6 in M2M network architecture.

6.2.2.3. SIM-related issues and know your customer (KYC) requirements

Policy aspects pertaining to SIM and KYC norms form another area of concern likely to deter the growth of M2M services. The scope of M2M devices differs from traditional communication devices and the policies should be framed accordingly. In several instances, M2M devices may not be directly associated with a specific user; may be located remotely; transferred from one jurisdiction to another; and may require change in ownership. In such scenarios, laying stringent norms can pose a challenge to the propagation of M2M services in the country.

Accordingly, a light regulatory approach needs to be adopted for M2M SIMs, which operate in a controlled and secure environment, i.e., where the M2M SIM can communicate with only a server or an emergency number. On the KYC aspect, all redundant requirements for M2M SIMs should be removed.

6.2.2.4. Roaming issues

Another area of concern requiring policy back-up for seamless execution of M2M services are the roaming norms. These include issues pertaining to inter-circle roaming, inter-network (including 2G-3G, GSM-CDMA), home network roaming as well as permissions to international roaming.

Most M2M devices such as health care equipment, smart utility meters, components of smart vehicles, etc., are manufactured in one country and later distributed globally. Therefore, the business model of M2M market inherently results in a large number of devices to be roaming on a permanent basis. Since embedded SIMs cannot be manually replaced with a local SIM, the M2M devices are connected to the visited mobile network in the foreign country, as a roaming device. This leads to increased costs for operators due to additional outlay to cover signaling.

Global associations such as the GSMA have suggested the use of specific standards/templates for facilitating roaming of M2M devices. For instance, GSMA adopted an “M2M Annex” template in 2012 for international M2M roaming. Among other things, this contract template mandates transparency in the provision of M2M services by requiring the parties to the agreement to identify their M2M traffic separately from other traffic (via a dedicated IMSI code, Access Point Names (APNs), or other agreed means). Taken together, international roaming agreements and the M2M Annex provide an industry-wide standard contractual structure for supporting M2M services globally.

• ► Have IPv4/IPv6 mandatory in transport network

Key recommendations

• ►► Adopt a very light touch regulatory approach for M2M SIMs.

• ► No new KYC requirements are needed for M2M services; norms, which limit SIM transfers, necessitate tele-verification of the user and require the maintenance of a list of user identities should be discouraged.

Key recommendations

100 | Speeding ahead on the telecom and digital economy highway

Despite its significance, most regulators across the globe have not come up with a firm view on provision of permanent roaming by operators. Given the opportunity of M2M services at a global level, inability to roam permanently is likely to hinder the growth of M2M business models significantly. There is a need for regulators, including the Indian counterparts, to bring clarity on the roaming aspects.

6.2.2.5. Privacy and security concern

M2M is expected to enable billions of connected devices to interact with each other. In such a market, there is significant potential to generate economic value from personal data collected. However, the use of this data also poses issues on the security and privacy front. Security lapses and misuse of personal data need to be addressed by adopting appropriate safety measures.

It is critical to maintain security at the device end, at the transport layer as well as while connecting to central enterprise server. Unauthorized device clients connecting to the enterprise server can cause serious security breach. In countries such as the US, standards such as Federal Information Processing Standard (FIPS) 140-2 are enforced to provide multi-level security. Such initiatives are important to maintain the confidentiality and integrity of information.

• Put in place a policy framework on security issues including:

• Data ownership, sharing and protection

• Broad data retention policy

• Basic security and privacy framework

• M2M data encryption policy

• M2M data accessibility for lawful interception

• Define security features (for instance, multiple independent levels of security; safety for embedded sensors)

Key recommendations

• Develop a policy framework to avoid issues pertaining to inter-network (including 2G-3G, GSM-CDMA), home network and inter-circle roaming; permitting of international roaming by default.

Key recommendations

Case study: Regulation of M2M services in Singapore

Over the years, the telecoms regulator of Singapore has focused on regulations for M2M services. Accordingly, there is more certainty on some M2M policy guidelines in Singapore as compared to other countries globally.

Positive regulatory regime to boost development of

M2M market

SIM card/roaming rules• Currently, there are no permanent roaming restrictions• License is needed for sale of foreign SIM cards

Spectrum allocation and management

Though separate spectrum has not been awarded for M2M; but the regulator has deliberated on use of white spaces since 2009. Trails have been launched in collaboration with private companies.

Numbering policy

The telecoms regulator encourages adoption of 13-digit M2M numbering address scheme; has proposed for a five-digit access code format for M2M.

Source: Infocomm Development Authority of Singapore; Ovum

101Speeding ahead on the telecom and digital economy highway |

Actions expected from the industry:

In addition to the government’s initiatives to support future uptake of M2M from a regulatory policy standpoint, industry participation is equally important to ensure mass and faster rollout of M2M-based services. For this, the industry should in parallel take up the following steps:

• Collate M2M status in India in terms of industry wise/telco wise number of M2M connections

• Collate M2M-related issues industry wise/segment wise

• Collate details of M2M support activities initiated by various government and industry bodies

• On the enterprise end, develop an M2M gateway solution, which can scale to millions of concurrent connections, process millions of messages per second and ensure secure access to the central services. This is essential to enable multiple connected devices communicate to the enterprise server, including many scenarios requiring real time communication.

• Establish a National M2M Forum

• Create awareness among SME to adopt production of M2M products and services

• Identify manufacturing hub or clusters dedicated to M2M

• Form an inter-ministerial task force for M2M proliferation

Case study: Brazilian Government’s regulatory support to drive uptake of M2M services

Brazil has significant demand for M2M services in security application and industry sectors. There were a total 9.9 million M2M connections by December 2014, with significant future growth potential.

Regulatory support to push uptake of M2M services:

Impact:

• With the regulatory changes, the number of M2M connections is expected to be 35 million in 2018, growing at a CAGR of 32% from 2012 to 2018.

• Telematics and fleet management sector in Brazil is expected to grow from BRL2.2b in 2014 to BRL4.2b in 2019, at a 14.5% CAGR. The sector is expected to account for 49% of total M2M revenue by 2019.

Regulatory support

Source: Analysys Mason, Pyramid Research, M2M World News, Teleco website, Factiva

Tax cutsReduced installation inspection fee — paid by operator for each active terminal as part of telecommunications fund from BRL26.7 to BRL5.6. Also, reduced operation inspection fee from BRL8.9 to BRL1.9, which is charged to carriers annually for each active telecommunications chip.

Mandatory installation in vehiclesBy 2015, all new vehicles produced for the domestic market must have M2M device to allow vehicle tracking and remote blocking services.