global technology quantum computing – weird science · pdf filefoundation global...

TRANSCRIPT

tion

lity n.

Founda Global Technology

Quantum computing – weirdscience or the next computingrevolution?With more companies moving quantum computers from the lab to commercialactivities, we believe widespread quantum computing is about to become a reaand holds the key to double the high-end computing market from $5bn to $10b

August 23, 2017 09:00 PM GMT

of interest

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report. + = Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to NASD/NYSE restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Foundation

g

, Google, in the dis- as impor-ompanies ockheed

ctor, with ation) and

g is not b servers . We think ost 2025, gines and ed. In the PUs (pos-upercom-ulate the ventually uting sys-the valua- our view.

Quantum computing – weirdscience or the next computinrevolution? Quantum computing is at an inflection point - moving from funda-mental theoretical research to an engineering development phase, including commercial experiments. That said, in the medium term, we see a transition period during which classical computers will simulate quantum algorithms, while genuine quantum computers are custom-ised to fit those algorithms.

While the classical computer is very good at calculus, the quantum computer is even better at sorting, finding prime num-bers, simulating molecules, and optimisation, and thus could open the door to a new computing era. Moore's Law was the main driver of the digital revolution; we believe quantum computing could trigger the beginning of a fourth industrial revolution, with far-reaching consequences for many sectors where computing power is becoming a limitation for R&D, such as Financials, Pharma (drug dis-covery), Oil & Gas (well data analysis), Utilities (nuclear fusion), Chemicals (polymer design), Aerospace & Defense (plane design), Capital Goods (digital manufacturing and predictive maintenance), Artificial Intelligence, and Big Data search in general.

It is hard to discern among currently evolving hardware platforms, which will be resilient enough to beat classical supercomputers in the next few years, but in our view the listed companies with the most

credible internal quantum computing roadmaps are IBMMicrosoft and Nokia Bell Labs. We also believe that withruption path there is room for new companies to emergetant players, such as D-Wave and Rigetti. Outside of tech, chaving led the charge for several years include Airbus, LMartin, and Raytheon in the aerospace and defence serecent interest by Amgen and Biogen (for molecule simulVolkswagen (traffic optimisation).

Life beyond transistors? Because quantum computinsuited to all compute tasks, smartphones, PCs, and westoring data will continue to run on current technologythe high-end compute platforms could see a transition psimilar to how steam engines coexisted with combustion enelectric motors for decades before being decommissionmedium term, we see incremental demand for FPGAs and Gsibly benefiting Xilinx, nVidia, and maybe Intel) as more sputers from Atos and Fujitsu are developed to simbehaviour of quantum computers. If quantum computers edo become ubiquitous, then the growth of high-end comptems that emulate them could be affected, hence limiting tions of those stocks, but this is more a post 2020 event, in

Global Technology

ation

m

ey.com

y.com

Found Contributors

Morgan Stanley & Co. International plc

Francois A MeunierEquity Analyst

+4420 7425-6603

Morgan Stanley & Co. LLC

Katy L. Huberty, CFAEquity Analyst

+1212 761-6249

Morgan Stanley & Co. LLC

Keith Weiss, CFAEquity Analyst

+1212 761-4149

Morgan Stanley & Co. LLC

Joseph MooreEquity Analyst

+1212 761-7516

Morgan Stanley & Co. LLC

Brian Nowak, CFAEquity Analyst

+1212 761-3365

Morgan Stanley & Co. LLC

James E FaucetteEquity Analyst

+1212 296-5771

James.Faucette@morganstanl

Morgan Stanley & Co. International plc

Adam WoodEquity Analyst

+4420 7425-4450

Morgan Stanley & Co. LLC

Vinayak Rao, CFAResearch Associate

+1212 761-4669

Morgan Stanley & Co. LLC

Elizabeth Elliott, CFAResearch Associate

+1212 761-3632

Elizabeth.Elliott@morganstanle

Morgan Stanley & Co. LLC

Erik W WoodringResearch Associate

+1212 296-8083

oundation

tion

rse - " for

phase

ck

F Contents

5 Executive summary

11 The world needs more (affordable) computing power – disrupneeded

14 Price reduction in classic computing has potentially run its couthe quantum computer is not a "nice to have" but a "must haveglobal productivity

15 Potential $10bn addressable market for quantum computing

16 Quantum computing moving to the engineering development

25 What is the potential impact of quantum computing to the stomarket and the economy?

27 Glossary of Terms

4

Foundation

Morgan Stanley Research 5

Quantum Computing at a GlanceWhat is quantum computing? While classical computers use the laws of mathematics, quantum computers use the laws of physics. We can describe the difference between classical computing and quantum computing with the image of a coin. In classical computing, information is stored in bits with two states, 0 or 1 – or heads or tails. In quantum computing, information is stored in quantum bits ("qubits") that can be any state between 0 and 1 – similar to a spinning coin that can be both heads and tails at the same time. The information contained in qubit is much richer than the information contained in a classical bit.

Every time you look at a spinning coin it takes on a different state, i.e. 75% heads and 25% tails, depending on where in the rotation you look at it. This is similar to a qubit that has a very fragile state, which can change each time you look at it. To search potential solutions to a problem, a classical computer individually tests different combinations of 0s and 1s. Meanwhile, quantum computing can test all combinations at once because a qubit represents all combinations of states between 0 and 1 at the same time.

In a quantum computer, qubits are interconnected by logic gates, like in a classical computer, but the available operands are more diverse and more complicated.

What is the holy grail of quantum computing? Exponential acceleration. In other words, a quantum computer would be able to compute at a much faster speed (exponentially faster) than a classical computer. This implies that classical algorithms, which would take years to solve on a current supercomputer, could take just hours or minutes on a quantum computer.

What are the hurdles to achieve quantum computing? Qubits are fragile and the state of a qubit can always change, therefore a significant challenge in quantum computing is maintaining a stable state of qubits in order to read the information. Quantum computers must operate at extremely low temperatures to slow the movement of qubits and are much larger in size than classical computers. Maintaining a stable state of qubits and correcting for the "noise" of high error rates as the number of qubits scale are some of the largest hurdles in quantum computing, which companies are solving in different ways. It is also difficult to read the result of an experiment without damaging the quantum state of a qubit. As a result, the read-out of a quantum experiment is not always the same - it gives a "probabilistic" answer, while a classical computer gives a deterministic' "answer (always the same and predictable).

What are the use cases? In order to be practical, quantum computers should have at least >50 qubits, relative to 16 [units?] today, and with a lower level of noise. Early applications are expected to be used in the chemistry and pharmaceutical industries, where scientists can decrease the time to discover new materials, for example new catalysts to produce fertilizer with much less energy than today. With the addition of more qubits, applications are expected to grow into the finance (i.e. portfolio optimization) and machine learning spaces.

What is the time line? Google, IBM, and others have achieved 16+ qubit systems, while others have simulated quantum computing with more than 40 qubits. That said, quantum computers are measured by not only the number of qubits but also by the amount of interconnection (the more interconnection, the more flexible) and the noise level (the lower the better). Google is tight-lipped about its efforts, but IBM has talked about having a 50-qubit system within the next few years. We believe that there will be a two- to three-year period during which simulations and real quantum hardware systems will coexist before quantum computers reach more than 50 qubits and simulators become less relevant. Beyond that, it is all about "scaling" the number of qubits at an acceptable level of noise, similar to what the computer/semiconductor industry experienced by doubling the number of transistor every 18 to 24 months for the same production cost (which is known as Moore's Law).

Executive summary

Foundation

6

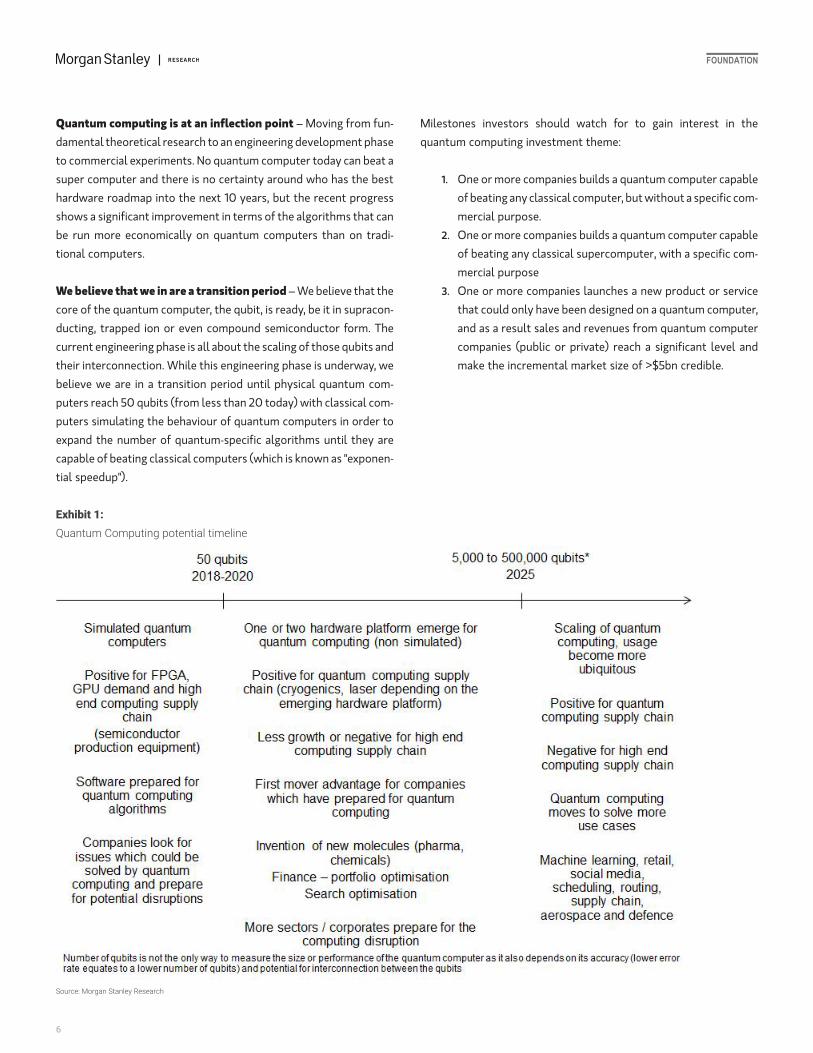

Quantum computing is at an inflection point – Moving from fun-damental theoretical research to an engineering development phase to commercial experiments. No quantum computer today can beat a super computer and there is no certainty around who has the best hardware roadmap into the next 10 years, but the recent progress shows a significant improvement in terms of the algorithms that can be run more economically on quantum computers than on tradi-tional computers.

We believe that we in are a transition period – We believe that the core of the quantum computer, the qubit, is ready, be it in supracon-ducting, trapped ion or even compound semiconductor form. The current engineering phase is all about the scaling of those qubits and their interconnection. While this engineering phase is underway, we believe we are in a transition period until physical quantum com-puters reach 50 qubits (from less than 20 today) with classical com-puters simulating the behaviour of quantum computers in order to expand the number of quantum-specific algorithms until they are capable of beating classical computers (which is known as "exponen-tial speedup").

Milestones investors should watch for to gain interest in the quantum computing investment theme:

1. One or more companies builds a quantum computer capable of beating any classical computer, but without a specific com-mercial purpose.

2. One or more companies builds a quantum computer capable of beating any classical supercomputer, with a specific com-mercial purpose

3. One or more companies launches a new product or service that could only have been designed on a quantum computer, and as a result sales and revenues from quantum computer companies (public or private) reach a significant level and make the incremental market size of >$5bn credible.

Exhibit 1:Quantum Computing potential timeline

Source: Morgan Stanley Research

Foundation

Morgan Stanley Research 7

The world economy needs more computer power, but poten-tially of a different kind. We see an increasing need for supercom-puting power amongst many verticals (financials, chemicals, oil & gas, pharma, nuclear fusion) and AI/Big Data search in general. As the digitalization of the economy continues, the need for a different form of computing is accelerating. More and more devices and systems are being connected to collect data (the Internet of Things),. Artificial intelligence chips are finding correlation levels or making inferences in large quantities of data but there is also enough evidence to sug-gest that large companies are looking for larger levels of computing power, or computing of a different kind. The classical computer is a large calculator that is very good at calculus and step-by-step ana-lytics, whereas the quantum computer looks at solving problems from a higher point of view.

Exhibit 2:Comparing classical computers with quantum computers at a high level

Source: Morgan Stanley Research

Quantum computing does not make the classic computer irrelevant – smartphones and laptops will still use transistors for the foresee-able future and the transition might take several years. As explained in our digital revolution blue paper (Technology: Disruptions and pro-ductivity growth in the next decade of the digital revolution), quantum computing could be a key driving element of a fourth indus-trial revolution as it could, for example, help invent new molecules for drugs and materials that could not be invented before with tradi-tional computers.

Foundation

8

Exhibit 3:Quantum Computing in the Industrial Revolution time scale

Source: Morgan Stanley Research

Quantum computing opens up new markets for computing. It may not be able to solve everything but it could solve issues that conven-tional computers either cannot, or struggle to solve.

Exhibit 4:Classical computers are great at calculus, quantum com-puters could open new horizons

Source: Morgan Stanley Research

Foundation

Morgan Stanley Research 9

How big could Quantum Computing be?

The market for high end computing is $5-6bn a year, according to IBM, and according to our discussions could increase to $10bn with poten-tial upside should quantum computing be used for many algorithms in many industries. The size of the market will also depend on the business model used (one-off hardware sales vs. cloud-based, the latter being the most likely, in our view, as the hardware needs to run at a very low temperature (below 1 degree Kelvin) in a very stable radio frequency environment, and as such is more likely used as a shared asset).

Exhibit 5:How big could quantum computing be?

Source: Morgan Stanley Research estimates

Our discussions with industry specialists at or involved with IBM, D-Wave, Lockheed Martin, Microsoft, Rigetti, BluFors, Google, Intel, Atos, 1Qbit, Nokia Bell Labs and Morgan Stanley IT, show that quantum computing is moving from white papers and fundamental research to engineering developments, including roadmaps to full functioning quantum computers with hundreds or thousands of qubits. The range of effort varies by company - from several key scien-tists at the Bell Labs to hundreds of engineers at IBM. According to The Economist, there is $1,500bn of public funding dedicated to quantum computing in the next several years.

In terms of landscape, in the exhibit below, we divide the technology road maps into three categories:

1) Companies looking to build universal quantum computers. There are three main subcategories, based on the material/technique used to create the qubits, i.e. supraconducting, ions trapped with lasers, and compound semiconductors. The three road maps are explained in more detail later in this report.

2) Companies which have built a task-specific quantum computer - D-Wave and its partners in particular. While the level of noise is higher than average and the level of connectivity is lower than for universal quantum computers, D-Wave has generated revenues for several years with task-specific computers containing up to 2,048 qubits.

3) Companies offering simulating platforms for quantum computers, i.e. classical computers able to simulate quantum bits and quantum gates, with varying degrees of accuracy. The largest simulators could simulate quantum computers with a number of quantum bits in the high 40s. The best simulators can simulate accurate levels of noise.

There are also software companies working on quantum algorithms that could be used on any platform and are currently designed using simulators.

We have also identified a few suppliers of key hardware components to the nascent quantum computing industry such as cryogenics equipment (as most hardware road maps need to "freeze" the qubits at close to absolute zero) and radiofrequency equipment (a signal at several gigahertz is used to maintain the qubit in a quantum state).

Foundation

10

Exhibit 6:Quantum computing – technology and company landscape

Source: Morgan Stanley Research

Foundation

Morgan Stanley Research 11

With an abundance of computing power in our pockets, it does not feel like more computing power is needed. That said, this abundance is only related to personal productivity and we are gathering enough evidence to convince us that several large companies and sectors are looking for more computing power at an affordable price.

Moore's Law is becoming more difficult to achieve, i.e. the cost per transistor does not halve every 18 months as it used to. ASML's EUV is expected to bring some relief for the next 5 years but beyond that the size of the transistor is getting so small that Moore's Law is likely to reach a limit.

The classic computer architecture cannot solve all problems. The classic computer architecture should be viewed as a large calculator, e.g. very good at calculus ; however there are problems that are not naturally suited for a classic computer's architecture. Hence, we have seen the emergence of more specialized chips for graphics (GPUs), and specific calculations (DSPs, TCUs, FPGAs). But there are numerous tasks where quantum computers can thrive naturally, such as the factoring of large numbers, sorting numbers, artificial intelligence, solving optimization problems such as supply chain optimization, and vehicle routing problems as well as the simulation of quantum mechanics.

The world needs more (affordable) computing power – disruption needed

Exhibit 7:Quantum computing has a much larger reach than a classic computer – and thus a much larger potential addressable market, in our view

Source: Morgan Stanley Research

While quantum computers are still mostly in the lab and slowly moving to the cloud, companies and scientists are looking for evidence that quantum computers can beat classical computers:

Quantum computing could prove more efficient than today's com-puters for sorting and searching. Today's best algorithms for sorting n numbers can achieve a full result in n.log(n) steps while a quantum computing cans sort in a square root of n , i.e. it takes many more computing steps for the classic computer to solve the same problem. Moore's Law has allowed those computing steps to become signifi-cantly quicker and cheaper but with Moore's Law slowing, the bene-fits of quantum computing become more apparent. To sort a billion numbers, a quantum computer would require 3.5 million fewer com-puting steps than a traditional computer and would find the solution in only 31,623 steps. This gain would be particularly interesting for companies involved in databases, big data analytics and search engines.

Exhibit 8:A quantum computer is much more efficient at sorting numbers than a classic computer for a range of applications ("exponential speedup")The number of computing steps required to sort a large list of numbers is exponentially higher for a classic computer than for a quantum com-puter

1.E+00

1.E+02

1.E+04

1.E+06

1.E+08

1.E+10

1.E+12

1.E+14

1.E+16

1.E+18

1.E+20

Classic Computer

Quantum Computer

Source: Morgan Stanley Research estimates

Foundation

12

In Financial Services, discussions with quantum computing soft-ware company 1Qbit show that the most promising applications could be in: 1) collateral optimization (managing stock of collateral to optimize profits); and 2) portfolio construction optimization con-strained by transaction cost. For the moment, 1Qbit suggests the best available hardware platform is actually based on traditional transistors (a cluster of FPGA chips simulating a quantum computer) but when quantum computing power is high enough, the software would switch to the new generation hardware, potentially custom-ised to those specific algorithms for financial services. Goldman Sachs is an early investor in D-Wave.

In Chemicals, Paul Walsh and team believes this is the first time that a large company like BASF has announced a plan to set up a supercomputer in order to design polymers with pre-defined properties. The goal for BASF is to simulate the quantum mechanics and therefore the properties of a molecule - while today the simula-tions are made with a traditional cluster of computers, we believe that quantum computers are more naturally able to solve such prob-lems. BASF and HewlettPackard announced that the companies will collaborate to develop one of the world’s largest supercomputers for industrial chemical research at BASF's Ludwigshafen headquar-ters this year. Based on the latest generation of HPE Apollo 6000 systems, themselves based on Intel Xeon chips, the new supercom-puter will drive the digitalization of BASF's worldwide research. “The new supercomputer will promote the application and development of complex modeling and simulation approaches, opening up completely new avenues for our research at BASF,” according to Dr. Martin Brud-ermueller, Vice Chairman of the Board of Executive Directors and Chief Technology Officer at BASF (press release by BASF published on the 17th March 2017). “The supercomputer was designed and developed jointly by experts from HPE and BASF to precisely meet our needs.” The new system will make it possible to answer complex questions and reduce the time required to obtain results from sev-eral months to days across all research areas. As part of BASF’s digi-talization strategy, the company plans to significantly expand its capabilities to run virtual experiments with the supercomputer. It will help BASF reduce time to market and costs by, for example, simu-lating processes on catalyst surfaces more precisely or accelerating the design of new polymers with pre-defined properties.

We believe that quantum computing could help in the Chemicals industry with the design of new chemicals and materials, and Dow Chemicals announced a collaboration with quantum computing software company 1Qbit on June 21, 2017, in order to create new molecules. A quantum computer is naturally suited to simulate the quantum physics linking atoms in a molecule (i.e. Schroedinger's equation) especially as the number of atoms grows. Our discussion

with IBM show simulation of molecules with 5 atoms already, but this is something which can be done with a laptop computer as well. The promise of quantum computers is the simulation of much larger mol-ecules which cannot be simulated by a supercomputer (above 50 atoms), represented by 5 qubits.

In Pharma, Biogen announced in June 2017 a collaboration with quantum computing software company 1QBit and Accenture to design new molecules. Morgan Stanley analyst Matthew Harrison believes Amgen is also working on quantum computing experiments. As with chemicals, the quantum computers appears very well suited to simulate a whole molecule.

In Oil & Gas, Martijn Rats and team have identified BP as a strong user of computing power to optimize oil extraction. Today, it holds more than 1 petabyte - a billion million bytes - of data. ARGUS, the wells data platform of BP, contains 2,458 wells – or 99.5% of all BP’s well stock.

APEX is the system optimizer. It enables BP to optimise production in real time by monitoring and modelling physical constraints across the production system live. It will be installed in all operated assets by 2018.

SIRAAJ is BP’s field development platform – it was pioneered in Oman. It enables live updating of the development plan as results stream in from new drilling data. BP can now monitor and analyse drilling operations and wells, from remote centres around the world. BP highlights that this will improve its decision making and make the organisation more efficient.

Another system, The Plant Operations Advisor, is in pilot testing on a facility in the Gulf of Mexico. At the moment it is running over 20 million calculations per day and assesses the operational state of 150 pieces of equipment, every 2 seconds. By end 2018, BP expects to have it fully deployed.

Eni fired up its new HPC3 (High Performance Computing) in the Green Data Center in Ferrera Erbognone (PV). HPC3 allows Eni to fully support all the activities in the Exploration and Production sector. The High Performance Computing HPC3, together with the coexisting HPC2 system, will provide Eni with a sustained 5.8 Peta-FLOPS, and 8.4 PetaFLOPS of peak computing capacity.

The new cluster continues along Eni’s HPC philosophy based on hybrid architectures, by using top end GP-GPUs as computational accelerators. Driven by Eni’s internal research activity, the cluster design targets both the most efficient energy solution and the

Foundation

Morgan Stanley Research 13

delivery of the maximum computational power required by the most advanced proprietary algorithms. HPC3 records a remarkable energy efficiency consumption of 3.66 gigaFLOPS/Watt; moreover, overall efficiency is also maximized by the direct free-cooling solution pro-vided by the hosting Eni Green Data Center.

HPC3 is an intermediate step towards the next evolution, the HPC4, expected at the beginning of 2018. With HPC4, Eni’s target is to over-come the barrier of 10 PetaFLOPS.

In aerospace and defence, companies have been early to see the advantages of quantum computing with Lockheed Martin and NASA being early partners of D-Wave (since 2010 for Lockheed) and Ray-theon with IBM.

In May 2017, Scientists from IBM Research and Raytheon BBN demon-strated one of the first proven examples of a quantum computer’s advantage over a classical computer. By probing a black box con-

taining an unknown string of bits, they showed that just a few super-conducting qubits can discover the hidden string faster and more efficiently than today’s computers. Their research was published in the paper, “Demonstration of quantum advantage in machine learning” (Nature article published on the 13th April 2017)

According to a report by CBInsight, Airbus Group established a team to tackle quantum computing at the end of 2015 at its site in New-port, Wales. Airbus wants to adapt existing quantum machines to specific problems within the aerospace industry, namely those requiring the handling and storage of large amounts of data, including sorting and analyzing images streamed by satellites, or cre-ating ultra-durable materials for aircrafts.

In transportation, Volkswagen announced a partnership in March 2017 with D-Wave to optimize traffic flow. The constant quest for more computing at an affordable cost sets the scene for a potential technology disruption.

oundation

t

ssic tran-ay to put wer com-n the past h? , Semi-er targets

ower is in nificantly ting tech-cades but

F

We believe one of the main drivers of each of the three industrial revolutions is a cost curve. The first industrial revolution was driven by an increase in efficiency for the steam engine, hence the cost of producing mechanical force was reduced by a factor of 5 over time. The same occurred during the second industrial revolution when the cost of producing mechanical force was reduced by a factor of 14 over time. Moore's Law drove the cost of computing power down by a factor of 100 million during the digital revolution. That said, the diffi-culty in driving Moore's Law further in terms of cost reduction is well documented (Blue Paper: Global Semiconductors: Chipping Away at Returns ,Technology - Semiconductors: Global Insight: Moore's law slowdown – temporary or terminal? and could be summarized by the following exhibit.

Price reduction in classic computing has potentially run its course - the quantum computer is not a "nice to have" but a "mushave" for global productivity

Exhibit 9:Classical computers do not scale as fast as they have in the past

With only incremental cost reduction available from clasistor based computers, the tech industry has found a wresources in common in the form of public cloud and thus loputing cost at a higher rate than Moore's Law would allow idecade. (Global Technology: Public Cloud, What’s It Wortconductors: Making the case for Intel to lower its data cent)

Once a large part of the globally available computing ppublic clouds, it is difficult to lower computing power sigfurther, hence the need to work harder on quantum compunologies, which have actually been well documented for dehave not moved to the engineering phase yet.

14

Source: Morgan Stanley Research

oundation

mmercial to solve

uming the ame, then mputing,

view. Any rcial com- forecast.

omputing

7 2027

5

0

5

0 872

5 185

0 89

5 10

0 283

1 3.1

F Potential $10bn addressable market for quantum computing The high-end computing market is worth around $5bn today. It is dwarfed by the overall commercial and consumer computing market. The consumer computing market is 3x as large as the commercial computing market as the past 10 years have seen smartphones emerging as the leading computing platform (the iPhone was launched in 2007). IBM thinks quantum computing can target the high end computing market and potentially double it as commercial applications emerge. We believe that the potential could be larger when quantum computing starts scaling like classical computers scaled from 1980 onwards.

Exhibit 10:How big could quantum computing be?

We expect the next 10 years to see a rebalancing favoring covs consumer computing as quantum computers are ablemany problems that could not be solved up until now. Assratio of consumer vs commercial spending remains the sthe high end computing market, including quantum cocould comfortably reach $10bn in the next ten years, in ourrebalancing of spending, between consumer and commeputing could lead to further upside to that $10bn revenue

Exhibit 11:The market for high end computing including Quantum Ccould double in the next ten years $bn 201

smartphones 41

tablets 5

PCs consumer 12

total consumer computing 59

PCs commercial 12

Servers 6

High End and Quantum Computing

total commercial computing 19

consumer vs commercial computing 3.

Source: Morgan Stanley Research estimates

Morgan Stanley Research 15

Source: Morgan Stanley Research estimates

Foundation

16

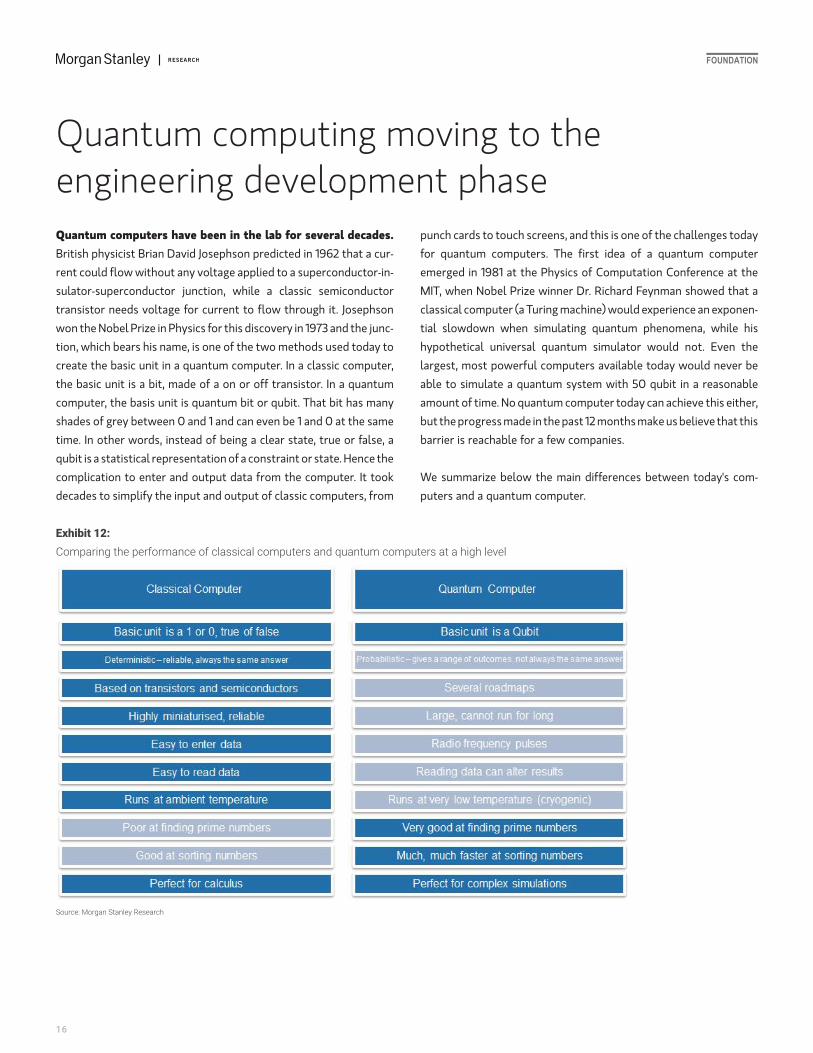

Quantum computers have been in the lab for several decades. British physicist Brian David Josephson predicted in 1962 that a cur-rent could flow without any voltage applied to a superconductor-in-sulator-superconductor junction, while a classic semiconductor transistor needs voltage for current to flow through it. Josephson won the Nobel Prize in Physics for this discovery in 1973 and the junc-tion, which bears his name, is one of the two methods used today to create the basic unit in a quantum computer. In a classic computer, the basic unit is a bit, made of a on or off transistor. In a quantum computer, the basis unit is quantum bit or qubit. That bit has many shades of grey between 0 and 1 and can even be 1 and 0 at the same time. In other words, instead of being a clear state, true or false, a qubit is a statistical representation of a constraint or state. Hence the complication to enter and output data from the computer. It took decades to simplify the input and output of classic computers, from

Quantum computing moving to the engineering development phase

punch cards to touch screens, and this is one of the challenges today for quantum computers. The first idea of a quantum computer emerged in 1981 at the Physics of Computation Conference at the MIT, when Nobel Prize winner Dr. Richard Feynman showed that a classical computer (a Turing machine) would experience an exponen-tial slowdown when simulating quantum phenomena, while his hypothetical universal quantum simulator would not. Even the largest, most powerful computers available today would never be able to simulate a quantum system with 50 qubit in a reasonable amount of time. No quantum computer today can achieve this either, but the progress made in the past 12 months make us believe that this barrier is reachable for a few companies.

We summarize below the main differences between today's com-puters and a quantum computer.

Exhibit 12:Comparing the performance of classical computers and quantum computers at a high level

Source: Morgan Stanley Research

Foundation

Morgan Stanley Research 17

Meanwhile, IBM has announced significant improvements, with 16-17 qubits now available on its cloud platform, ahead of schedule and with a roadmap to 50 qubits in the next few years and up to 1,000 qubits longer-term. Google keeps its progress internal but a report by futurism.com shows that Google is also working on a similar archi-tecture, but with a particular focus on reducing the number of "errors" made by the quantum computer up to 9 qubits (according to the last Google quantum publication) and has been reported by futurism.com to test a 20 qubit chip this year with a goal to achieve 50 qubit by the end of 2017.

There are currently three different road maps to create a universal computer with no established winners, but the progress made in the past 12 months, at IBM for instance, is notable and makes us believe that quantum computers could be at an inflection point.

Supraconductor roadmap, the most visible so far - The supracon-ducting route chosen by IBM, Google, D-Wave and Rigetti seems to be making more progress at the moment, even if it is limited by the number of radio frequency drivers it can handle, and taking the system to a temperature below that of outer space is not an easy task. That said, discussion with the main supplier of cryogenic devices, BluFors Cryogenics, show that a triple stage cooling equip-ment works well with enough radio frequency coaxial cables feeding to the core of the supraconducting chip. Also, the supraconducting quantum computer can run 10,000x faster than the trapped ion-based quantum computer, i.e. up to 100MHz, but it makes more mis-takes. That is why the leaders in this road map are working to improve not only the number qubits but also the error rate.

D-Wave has sold quantum computers since 2010 and IBM delivers its 5 and 16/17 qubit quantum computer as a free cloud service (in exchange for access to the code). Google, in our view, will keep its research internal and it would make sense to stay that way if Google finds a way to lower the cost of sorting, searching, and machine learning with a quantum computer.

There are some clear positives about the supraconducting roadmap - the qubits are well identified, with a good level of coherence and fidelity with a road map to improve the error rate.

There are, however, some outstanding issues:

1) The need for very low temperature, below 1 Kelvin. But the progress made by cryogenics companies like Blufors is impressive.

2) Scalability of the system as current qubits are fairly large, in the range of 1um, which means that a chip with 1 million qubits with the current dimensions would require a million RF generators and their associated multiplexers. That would fill an area as large as a football pitch.

3) The material used for the Josephson junction, which could be made of either the very exotic material Niobium or the very common mate-rial aluminum.

Trapped ion roadmap, promising but still in Universities - Recent improvements have been made around a different way to make a qubit-based computer, not with supraconductors, but with lasers and electromagnetic fields, as described with the Paul ion trap. The ion trap was conceived of in the 1950s by Wolfgang Paul, who was awarded the Nobel Prize in Physics in 1989, and it was first imple-mented in 1995 by J. Cirac and P. Zoller. While this road map is inter-esting in terms of its lower error rate, the speed of the computer is lower than with supraconductors and the lack of backing by large corporates could be a headwind. The efforts for this road map are led more at a University level (such as the University of West Sussex, England, and the University of Maryland, with a start-up spin-off called IonQ).

A team of scientists, including Austin Fowler from Google Research, have published a blueprint for a quantum computer, with a modular approach based on ion trapped qubits and solving many engineering issues to build it and interconnect the different modules. We have seen the core of the quantum computer, with lasers and magnetic fields, at the University of West Sussex (Brighton, England) headed by Winfried Hensinger. Hensinger has enough funding to actually make a first >10 qubit prototype and is currently looking for $100m funding to build a larger scale prototype with over 1,000 qubits.

While the core of the quantum computer seems to work correctly, the team of scientists have also solved several practical issues such as interconnecting the trapped ions qubits between each other. Inter-connection with photons used to be the limiting factor, with a max-imum frequency of 7 Hertz (7 times per second) due to the interfacing between the trapped ions and the photons emitter/detector. The paper suggests to use ions, the same ones that are used in the ion trap, as interconnection between the different modules, increasing the speed by a factor of 100,000 and thus reaching 700kHz. This sounds very low compared to a clock speed in most personal com-puters around 3GHz, but each qubit can do so much more than a classic bit that the clock speed does not matter so much, according to Hensinger.

Foundation

18

Traditional industrial chips will be used to control the magnetic fields that shift ions in and out of the traps - digital to analog converters with 16 bit precision and 1MHz refresh rate, which could typically be sourced from Analog Devices. Commercial silicon based photon counters would be used to read the quantum states with an effi-ciency of 30% could be sourced from Hamamatsu. Each microfabri-cated junction (with a qubit) would be manufactured on a traditional Silicon wafer substrate, with traditional etching and deposition tech-niques - that said the prototype we saw in the lab was all hand made so there is lots of potential for miniaturisation down to 1,296 junc-tions per 4-inch wafer in a first stage. Aligning the modules and inter-connects in the order of 3 to 5nm is likely to be a technical challenge but, not surprisingly, ASML is suggested as the supplier of equipment to achieve this.

An experimental comparison of the two leading quantum computer architectures above (supraconducting junction and trapped ions) has been established by a team of scientists including Christopher Monroe of the University of Maryland in 2016. While the two archi-tectures have different ways of being programmed, the team has established that the ion trapped architecture was slower but more precise. Also the trapped ion roadmap does not require sub 1 Kelvin

temperature (i.e., colder than deep space) and could scale up with no need for hundreds of radio frequency generators to maintain the ion in entanglement - but the scaling of trapped ions qubits is currently only at the blueprint stage.

Compound semiconductor road map could be the wild card. We believe that the Bell Labs (owned by Nokia) have an aggressive road map for 2017 for delivering working gates (functions) around already working qubits based on a very thin layer of gallium arsenide running at very low temperature (below 1 Kelvin) - a recent Bell Labs paper in Nature and our discussion with CTO of Bell Labs Marcus Weldon shows strong confidence in reaching the target to demonstrate the gates by the end of 2017 and to then scale the qubits with a manufac-turing partner and an IP licensing programme for Nokia. The qubits last longer and thus have much lower error rates than with the other materials according to Nokia Bell Labs. Compound semis is also researched by the University of Delft QuTech with a $50m invest-ment programme from Intel since 2015, and the University of Purdue, with backing from Microsoft. NTT Basic Research Laborato-ries also has researchers working on this road map.

Exhibit 13:Technology and company landscapes

Source: Morgan Stanley Research

Foundation

Morgan Stanley Research 19

The core of the quantum computer thus already exists and is well understood, be it a Josephson junction or a trapped ion. The real ques-tion now is a how to scale and miniaturize those qubits. Referring back to the invention of the transistor effect in 1925 by Julius Edgar Lilienfeld, it took more than 20 years to implement it in real life in 1947 at the Bell Labs. The team lead by William Shockley won the Nobel Prize in Physics in 1956. In took another decade, for Jack Kilby at Texas Instruments to make the first integrated circuit chip, in 1958 (Kilby won the Nobel Prize in Physics in 2000). But this is a team of engineers moving from Fairchild to Intel, which created the largest semiconductor company of the past century. Hence, it is interesting to note that this is the company that industrialized the process that created the most value, not the one that invented the concept.

Exhibit 14:First transistor designed at the Bell Labs in 1948

Source: Wikicommons

Exhibit 15:First integrated circuit (replica of the Texas Instruments Kilby proto-type)

Source: Wikicommons

While this is a team of scientists/physicists in one lab, larger compa-nies like IBM, Intel, Google and Microsoft are also looking at the quantum computing opportunity.

IBM and quantum computing - first commercially available small scale universal quantum computer

We met with Dr. Arvind Krishna, Senior Vice President and director of IBM Research.

IBM is dedicating considerable resources to the area of quantum computing. With a team of 100s of engineers, a long history in micro-electronics, systems, and software, and strong relationships with large enterprises and governments, IBM is well positioned to lead in commercializing quantum computing. The company views the $5-6 billion high-end computing market as the initial target but sees the potential for new use cases to grow the addressable market for quantum computing to $10 billion-plus.

Foundation

20

In 2016, IBM launched Quantum Experience (now called IBM Q Expe-rience) with a 5 qubit universal quantum processor that is freely accessible on the IBM Cloud, which was upgraded to a 16 qubit proc-essor in 2017. IBM also developed a 17 qubit commercial processor prototype which will be the basis for the first IBM Q early-access commercial systems. IBM Q is an industry-first initiative to build com-mercially available universal quantum computers and services for business and science which will be delivered via the IBM Cloud plat-form. The company is on the path to achieve a 50 qubit system within the next few years which it believes represents the point quantum computing can solve a wider range of complex problems far better than a classical computer. Already, 50,000 users executed more than half a million trials on IBM Q Experience. Significant interest in the scientific community supports the view that the technology com-munity will embrace the platform as it scales.

Already, use cases are emerging. At IBM's investor briefing in March 2017, management explained that quantum computing will "enable a range of computation which would take more than the age of the universe to do on classical computers," including for medicine and materials, machine learning, and searching big data. According to IBM, a quantum computer with 10-30 qubits could beat any classical computer for molecule simulation (chemistry, pharma), and 1,000 qubits could supersede GPU-based inference calculations for artifi-cial intelligence.

Exhibit 16:Why quantum computing matters, according to IBM

Source: IBM

In particular, IBM explained that a laptop can simulate a molecule with 25 electrons but no classical computer could ever be built to simulate a 50-electron system as the problem is exponential by nature. A quantum computer with 50 qubits could simulate that mol-ecule easily and IBM has already demonstrated the simulation of H2, LiH, and BeH2 molecules with 2, 4, and 6 qubits, respectively.

Supporting quantum software development is key. IBM provides standard software wording (APIs) such that anyone can create quantum algorithms and call them from a standard language (Python), hence reducing the time for a software engineer to retrain to quantum computing. IBM is also supporting early customers. IBM is working with Raytheon to demonstrate the first proven examples of quantum computers' advantage over a classical computer. With only a 5 supercomputing qubits process, the quantum algorithm con-sistently identified an unknown string of bits in a black box in 100-fold fewer steps and was more tolerant to noise than the classical binary computing architecture. In layman's terms, the classical binary computer was trying every possible combination, one by one, in a very orderly but slow manner, while the quantum computer quickly converged toward the right solution as if it was guessing the answer. This is a strong step towards artificial intelligence as the human brain would also start with an informed guess.

Foundation

Morgan Stanley Research 21

Cloud delivery is the future of quantum computing. In 2017, IBM announced the IBM Q initiative to build commercially available uni-versal quantum computing systems delivered via the IBM Cloud Plat-form. Following Watson and blockchain, the company believes quantum computing could form the next set of services delivered via IBM Cloud. Beyond the typical cloud advantages of cost and agility, quantum computing delivered via the cloud addresses a number of bottlenecks, including the need to operate in a very low temperature which requires specialized technology and resource constrained liquid helium.

Exhibit 17:How to reach close to absolute zero temperature to slow down mole-cules and take control of quantum properties of molecules

Source: Blufors Cryogenics

Exhibit 18:IBM 5 qubits chip

Source: IBM

Exhibit 19:IBM 16 qubits chip

Source: IBM

Foundation

22

Intel and quantum computing - partnership with Delft Univer-sity and report to the US President

We spoke with Jim Clarke, who heads Intel's quantum computing efforts.

Intel CEO Brian Krzanich is very excited about quantum computing and, like us, believes "it has the potential to augment the capabilities of tomorrow's high performance computers." Intel's CEO recognises the challenges including how to fabricate, connect and control many more qubits

When US semiconductor companies wrote to the US President at the beginning of 2017, they highlighted research in quantum computing as one of the ways to leapfrog China's $100bn plan to build a semi-conductor industry of its own (Semiconductors: Report to the Presi-dent – Ensuring Long Term US leadership in Semiconductors ). The quantum computer would develop "a pilot version of a high scale, zero carbon, cost-competitive energy system," which we believe refers to the nuclear fusion system that many countries have been working on for several decades but failed to achieve because of the lack of computing power with the current computer architecture.

Intel launched its quantum computing program in 2015 in partner-ship with Netherlands' Delft University of Technology. The company is hedging its bets by working on two different quantum computing approaches simultaneously: 1) superconducting qubits (similar to efforts by other companies in this space); and 2) silicon spin qubit (unique to Intel but something that is behind the progress made on the superconducting qubit front). Having said that, the company has little to publically show for its efforts to date with its silicon-based efforts around only 2-3 qubits currently. The company expects to progress to 50 qubits in two years and 1000 qubits in 5-6 years, while targeting commercial quantum applications in a decade from now. In addition, the company is focussed on developing complete quantum system that would include qubit chips and custom control elec-tronics, while data processing could be boosted by high end FPGA/custom core.

Google and quantum computing - the Quantum Ai Lab and collabo-ration with UCSB.

Google Research has a Quantum Ai Lab and has also worked with the D-Wave computer (not a universal quantum computer). Google has not communicated to the public for more than a year on its quantum computing research but given the potential cost savings on sorting and searching algorithms we believe this is critical for Google's long-term position and gross margin.

According to a report by Futurism.com, Google has improved its cur-rent quantum computer from 9 qubits (last official publication in 2015) to a 20 qubit chip currently under test and working to deliver a 50 qubit chip by the end of 2017. The last publication regarding the 9 qubit chip was particularly interesting regarding the reduction of errors in the qubits vs other companies, down to 99.5%. Should this quantum computer based on 50 qubit have customised hardware then it is reasonable to believe it could be dedicated to number sorting and searching functions, thus at the core of Google business and that quantum computing could very well stay internal to Google.

Microsoft – Looking to Build the Full Quantum Stack

Microsoft has been investing in quantum computing research for over 10 years. The appointment of Todd Holmdahl to head Micro-soft's efforts in quantum computing in November 2016 marked the transition of this research effort, into the realm of engineering and development. In Todd's words, Microsoft saw the research, "at an inflection point, in which we are now ready to go from research to engineering" with a clear road map to a scalable quantum computer. A twenty year Microsoft veteran, Todd had previously led efforts to bring the Xbox, Kinect, and Hololens to market. The game plan at Mic-rosoft is to develop the entire stack for the scalable quantum com-puter, starting from the people pioneering the science, to manufacturing the quantum hardware, to developing the software language with which new algorithms and program will be written. All these efforts are occurring in parallel, with a software language already in place (LiquiI>), the first qubit of Microsoft's topological quantum computer coming online imminently, and an existing ser-vice delivery model in Azure the most likely route to market. Our esti-mate is a commercial quantum computing service (a system of ~100 logical qubits) available from Microsoft within 5 years.

Foundation

Morgan Stanley Research 23

The People Through direct hires and collaboration, Microsoft has brought together the following quantum computing researchers:

l Michael Freedman – Head of Station Q Santa Barbara: A renowned mathematician and Fields Medal winner, Freedman heads up a Microsoft Research lab located at the University of Santa Barbara. Freedman has pioneered much of the fundamental work of topological quantum computing, a differentiated approach to leveraging quantum effects for computing.

l Leo Kouwenhoven - Technical University of Delft: A Professor of Physics at TU Delft, Kouwenhoven was the founding director of QuTech, an Advanced Research Center on Quantum Technologies, and leads research efforts around potential quantum structures like semiconducting nanowires and carbon nanotubes.

l Charles Marcus - Niels Bohr Institute: The Villum Kann Ras-mussen Professor at NBI and a Center Director at the Center for Quantum Devices, Charles Marcus' research interests include fractional Hall systems (which give rise to topological qubits).

l Matthias Troyer - Professor of Computational Physics at ETH Zurich: A professor at ETH Zurich, Troyer develops simula-tion algorithms for quantum systems.

l David Reilly - Experimental Physicist at the Center for Quantum Machines at the University of Sydney: Professor Reilly leads research efforts on enabling technologies to con-trol condensed matter systems at the quantum level.

The Technology – Pursuing Higher Fidelity with Topological QubitsMore traditional quantum computer architectures look to store and manipulate information by capturing a particle in a localized space, for example capturing an electron to measure its spin. These systems are very sensitive to the external environment, which introduces errors into the system (causes decoherence of the qubit). Microsoft's quantum computing efforts base around the idea of a topological quantum computer, where the information is contained in an inher-ently more stable topological space – the interaction of field lines from multiple particles called Marojana fermions into what physi-cists refer to as braids. Todd Holmdahl sees the stronger inherent fidelity of the topological architecture as the key to vaulting Micro-soft's efforts ahead of competitors. Thought of simply, traditional quantum computers necessitate multiple physical qubits in a system to error correct against one logical qubit, which actually does the computational work. The inherent stability of the topological

quantum state means each physical qubit represents a logical qubit, or said another way, competing systems need an order of magnitude more qubits to do the same amount of work as Microsoft's qubits.

Microsoft is currently pursuing three parallel development paths for manufacturing the physical quantum computer. These include semi-conducting nanowires, carbon nanotubes, and a CMOS based system (possibly with a superconducting layer on top of a compound semi-conductor substrate). The first qubits are expected to be online 'imminently', with a roadmap to 10's and 10,000's qubits well plotted ahead.

The Software – Already Coding Algorithms to Harness Quantum AbilitiesIn line with the hardware efforts at Microsoft's Quantum Architec-tures and Computation Group (QuArc), is the development of a soft-ware platform for quantum computing called LIQUil> (pronounced liquid). LIQUil> includes a programming language, optimization and scheduling algorithms, quantum simulators and compilers for trans-lating high-level programs into low-level machine instructions for quantum computers. The LIQUil> platform enables researchers and students to simulate quantum circuits, and use recently developed quantum algorithms to begin writing programs utilizing quantum computing power even before the actual quantum computers are available.

D-Wave has been selling quantum computers since 2010 to part-ners including Lockheed Martin, Nasa and Google. Whilst D-Wave is not a universal quantum computer, i.e. it does not work with every workload/algorithm, its quantum computer has the largest claimed number of qubit (2,048) and is best suited for the following tasks according the company: Optimization, Machine learning, Sampling / Monte Carlo, Pattern recognition and anomaly detection, Cyber security, Image analysis, Financial analysis, Software / hardware veri-fication and validation, Bioinformatics / cancer research. While the D-Wave quantum computer is not universal, D-Wave is the only com-pany to have sold quantum computers for several years to reputable customers at a cost of over $10m per machine depending on the con-figuration. Like IBM, the D-Wave computer is based on a supracon-ducting chip made of Niobium and there is a roadmap to make it with Aluminum, according to an industry specialist who has been using the D-Wave computer for many years in a US University. Discussion with industry specialists show, however, that inputting data into the com-puter has proved difficult and the results were very noisy, i.e. with a high error rate

Foundation

24

Rigetti, a private company with $69m in funding formed by Chad Rigetti, who previously worked at IBM Quantum Computing Group, announced in June 2017 an 8 qubit computer based on a supraconductor chip (aluminum) and a software environment linked to that chip called Forest. Rigetti has also launched a simulation plat-form (36 qubits with accurate noise simulation) running on classical computer chips, thus competing with Atos and Fujitsu. In terms of roadmap, Rigetti believes it can scale its quantum computer hard-ware to above 50 qubits in 2018.

Alibaba In 2015, AliCloud/Aliyun announced a breakthrough in artifi-cial intelligence and set up a Quantum Computing Laboratory with the Chinese Academy of Sciences (we have not soken with them).

Atos - Paris-based Quantum research lab

Atos has launched a quantum specific emulator based on classical computer architecture (CPUs, GPUs, FPGAs and ASICs) able to simu-late 30 to 40 qubits at an affordable cost ($100k to $1m). The com-puter can be attached to a real physical quantum computer to offload some calculations. We believe this is a good approach for companies and universities willing to look at the opportunity to develop new algorithms and customise the attached quantum computing hard-ware.

Exhibit 20:Atos quantum computer simulator using classical computer architec-ture

Source: Atos

Foundation

Morgan Stanley Research 25

Each industrial revolution has created large new sectors by market cap. The first industrial revolution created the financial and transpor-tation sectors. The second one created the oil & gas, chemicals, pharma, and autos sectors. The third one created the tech and media sectors, with new companies such as Amazon, Apple, IBM, Intel, Mic-rosoft, Google, Samsung Electronics. If history repeats itself, then the fourth Industrial Revolution would create new companies and new sectors.

That said, current large companies such as Google, IBM, Intel, and Microsoft have already positioned themselves into quantum com-puting, but that does not mean they will succeed. There are also a few private companies, with different levels of funding like D-Wave or Professor Monroe's IonQ start-up, working on different types of quantum computing as well as IdQuantique working on hack-proof transmission of data thanks for quantum physics principles.

Technological disruptions are both risks and opportunities for sec-tors and companies. The financial sector continued to thrive in the second and third/digital revolution, the autos, oil&gas and chemicals sectors continued to thrive in the digital revolution. But the train companies / transportation sector did not do so well as the combus-tion engine gained share during the second industrial revolution. Even during the digital revolution, Intel and to a lesser extent Micro-soft did very well until the launch of Windows 95 but have underper-formed since.

In all scenarios, we believe that quantum computing will not super-sede all current forms of computing. Like when combustion engines started to gain traction, steam engines were still used for several dec-ades for manufacturing applications and mass transportation. Based on the prototypes we have seen, using lasers, we believe that quantum computing will not be miniaturized to the point that it can be used in any portable applications, i.e. a laptop, tablet, smartphone. Nor does it make much sense to use it for a basic server and to store data. But there could be a handful very large quantum computers by the end of the decade, available to share, in the cloud, or not, held by private companies for their own use or large States. Like the very first

What is the potential impact of quantum computing to the stock market and the economy?

computer used to decode messages during WWII, there was only one and it was kept secret for a long time.

At this stage, we view two main applications for quantum computers - a useful one and a less so useful one.

A quantum computer could be used to solve physical problems that humans and supercomputers struggle to solve today, because they are exponentially complex by nature. We view BASF's aim to create bespoke polymers as a good example, but it could be used to simulate nuclear reactions like nuclear fusion reactors, which have proved dif-ficult to design in the past several decades (Super Phoenix and Iter reactors). It could also be used to design new molecules in the Pharma sector. In summary, it could be beneficial to any company looking for more affordable computing power today.

A quantum computer could be used to decode most types of cryptog-raphy keys used today. Current computers can multiply several prime numbers easily, say 3*7*23*67=32,361 - even a pocket calcu-lator could do that. But a computer would take much more time to find the prime numbers making a large number like 32,361. Obviously most cryptography system would use many more prime numbers to make finding the prime numbers very difficult. Your credit card secu-rity, the sim card in your smartphone, the cryptography in your com-puter are all based on this. A quantum computer would crack the code more easily and there could in theory be a transition period where cybersecurity/payment companies could become irrelevant unless they find quantum proof cryptography systems.

That does not look like very many use cases, but this is only the begin-ning and use cases might increase as research into the field continues to progress. Who would have thought that the computer used to decode messages during WWII or the microcontroller used to guide the Apollo rocket to the moon could be used to send messages in your pocket, turn on and off the lights at home, and measure the dis-tance to the car in front etc.

Foundation

26

Could, for instance, quantum computing be used for Artificial Intelli-gence applications? NASA, Universities Space Research Association and Google Research set up the Quantum AI Lab in 2013 and pub-lished reports comparing their efforts based on a D-Wave quantum annealing computer in 2014. That said, reports from the lab have been scarce since 2015. nVidia has stolen the show with so much progress made in AI thanks to AI specific chip architecture and an easy to learn language (Kuda). Google has a Quantum AI Lab and IBM's Director of Research Dr. Arvind Krishna has stated publically at its 2017 Investor Briefing 2017 that quantum computers could be used for Machine Learning (and Big Data searching).

Machine learning requires a significant amount of processing power and thus quantum, at least theoretically, should be a prime candidate to take AI beyond the current state-of-the-art calculation of infer-ences, as shown in the most recent demonstration made by IBM and Raytheon that a quantum computer would guess an unknow string of bits in a black box in 100 times fewer steps than a classical binary computer using "if, then, else" loops.

There are different paths of development shown in the following quadrant chart. On the x-axis, the speed of development from here, fast or slow. On the y-axis, if the technology will remain public or be widely available as a cloud service

Exhibit 21:Potential outcomes of the quantum computing depending on take up and on business model (cloud vs internal)

Source: Morgan Stanley Research estimates

oundation

ce whose ke copper duct elec-der other veral ele- (Se), can omposed s is called

el of com-ctor tran-

mplify or or is a the n

requency eating or ound 5 to

f several put into a

r of light light.

ckness or an uncon-

material, anometer between e aspect

F Quantum Bits (“qubits”): the basic unit of information in a quantum computer; similar to a "bit" in a classical computer.

Quantum gates: While a classical computer is based on logical operand or gates like NOT, NOR, AND, NAND, which assembled together can compute numbers like a + b, quantum computers have their own operands or gates, which assembled together can "com-pute" much more complicated algorithms than classical computers. Quantum gates can include Hadamard gates and Pauli gates which have the properties to 'move' the qubits in three dimensions.

Entanglement: a quantum state whereby two qubits act in a very similar manner even though they can be many meters apart

Quantum coherence: a quantum state is coherent when the qubits used in the system interfere in a stable manner. The longer the quantum coherence, the better for the quantum computer.

Fidelity: The measure of the "closeness" of two quantum states. A loss of fidelity would result in a higher level of noise

Josephson junction: quantum junction created with a piece of insu-lator linked between two superconductors, where electrons can flow in both directions at the same time

Supraconductor/Supraconducting: material where electrons can move without any resistance (superconductivity), usually created a super low temperature (see cryogenics below)

Cryogenics : Ultra low temperature, lower than refrigeration. While a deep freezer can be used a -20 to -30 degrees Celsius, cryogenics start with a minus -150 degree Celsius. Ultra low temperatures are measured in Kelvin. 0 degrees Kelvin is -273 degrees Celsius or -460 degrees Fahrenheit. For perspective, water freezes at 273 degrees Kelvin (i.e. 0 degrees Celsius and 32 degrees Fahrenheit). Most quantum computers need to be maintained at very low temperature, below the temperature of deep space, or below 0.02 Kelvin.

Liquid helium: helium gas exists in a liquid form at extremely low temperatures (4 Kelvin or -452 Fahrenheit) and is used as a cryogenic

Glossary of TermsCompound Semiconductor: A semiconductor is a substanelectrical conductivity lies between that of a conductor lior aluminum and an insulator like rubber or glass. It can contricity under some conditions but insulate electricity unconditions. Of the 92 elements existing on the earth, only sements, including silicon (Si), germanium (Ge) and seleniumbehave as semiconductors. In contrast to a semiconductor cof a single element, one composed of two or more elementa compound semiconductor.

Super computer/computing: A computer with a high levputing performance and capabilities, based on semicondusistors

Transistor: A transistor is a semiconductor device used to aswitch electronic signals and electrical power. The transistcore of the classical computer and of the digital revolutio

RF Generator: Also known as a signal generator, a radio f(RF) generator is an electronic device that generates repnon-repeating electronic signals a very high frequencies (ar6 GHz for quantum computers)

Multiplexer: A multiplexer is a device that selects one oanalog or digital input signals and forwards the selected insingle line.

Photon Counting: a technique for measuring the numbeparticles (photons) by utilizing the particle properties of

Semiconducting Nanowires: Structures that have a thidiameter constrained to tens of nanometers or less and strained length.

Carbon Nanotubes: A carbon nanotube is a tube-shapedmade of carbon, having a diameter measuring on the nscale. Carbon nanotubes are unique because the bondingthe atoms is very strong and the tubes can have extremratios.

Morgan Stanley Research 27

refrigerant in the study of qubit behaviour at very low temperatures

Foundation

28

Disclosure SectionThe information and opinions in Morgan Stanley Research were prepared or are disseminated by Morgan Stanley & Co. LLC and/or Morgan Stanley C.T.V.M. S.A. and/or Morgan Stanley México, Casa de Bolsa, S.A. de C.V. and/or Morgan Stanley Canada Limited and/or Morgan Stanley & Co. International plc and/or RMB Morgan Stanley Proprietary Limited and/or Morgan Stanley MUFG Securities Co., Ltd. and/or Morgan Stanley Capital Group Japan Co., Ltd. and/or Morgan Stanley Asia Limited and/or Morgan Stanley Asia (Singapore) Pte. (Registration number 199206298Z) and/or Morgan Stanley Asia (Singapore) Securities Pte Ltd (Registration number 200008434H), regulated by the Monetary Authority of Singapore (which accepts legal responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with, Morgan Stanley Research) and/or Morgan Stanley Taiwan Limited and/or Morgan Stanley & Co International plc, Seoul Branch, and/or Morgan Stanley Australia Limited (A.B.N. 67 003 734 576, holder of Australian financial services license No. 233742, which accepts responsibility for its contents), and/or Morgan Stanley Wealth Management Australia Pty Ltd (A.B.N. 19 009 145 555, holder of Australian financial services license No. 240813, which accepts responsibility for its contents), and/or Morgan Stanley India Company Private Limited, regulated by the Securities and Exchange Board of India (“SEBI”) and holder of licenses as a Research Analyst (SEBI Registration No. INH000001105), Stock Broker (BSE Registration No. INB011054237 and NSE Registration No. INB/INF231054231), Merchant Banker (SEBI Registration No. INM000011203), and depository participant with National Securities Depository Limited (SEBI Registration No. IN-DP-NSDL-372-2014) which accepts the responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with, Morgan Stanley Research, and/or PT. Morgan Stanley Sekuritas Indonesia and their affiliates (collectively, "Morgan Stanley").

For important disclosures, stock price charts and equity rating histories regarding companies that are the subject of this report, please see the Morgan Stanley Research Disclosure Website at www.morganstanley.com/researchdisclosures, or contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY, 10036 USA.

For valuation methodology and risks associated with any recommendation, rating or price target referenced in this research report, please contact the Client Support Team as follows: US/Canada +1 800 303-2495; Hong Kong +852 2848-5999; Latin America +1 718 754-5444 (U.S.); London +44 (0)20-7425-8169; Singapore +65 6834-6860; Sydney +61 (0)2-9770-1505; Tokyo +81 (0)3-6836-9000. Alternatively you may contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY 10036 USA.

Analyst Certification

The following analysts hereby certify that their views about the companies and their securities discussed in this report are accurately expressed and that they have not received and will not receive direct or indirect compensation in exchange for expressing specific recommendations or views in this report: James E Faucette; Katy L. Huberty, CFA; Francois A Meunier; Joseph Moore; Brian Nowak, CFA; Keith Weiss, CFA; Adam Wood.

Unless otherwise stated, the individuals listed on the cover page of this report are research analysts.

Global Research Conflict Management Policy

Morgan Stanley Research has been published in accordance with our conflict management policy, which is available at www.morganstanley.com/institutional/research/conflictpolicies.

Important US Regulatory Disclosures on Subject Companies

As of July 31, 2017, Morgan Stanley beneficially owned 1% or more of a class of common equity securities of the following companies covered in Morgan Stanley Research: Gemalto N.V., Logitech, Technicolor SA, TomTom NV.

Within the last 12 months, Morgan Stanley has received compensation for investment banking services from Technicolor SA.

In the next 3 months, Morgan Stanley expects to receive or intends to seek compensation for investment banking services from Gemalto N.V., Logitech, Technicolor SA, Telit Communications PLC, TomTom NV.

Within the last 12 months, Morgan Stanley has received compensation for products and services other than investment banking services from Gemalto N.V., Technicolor SA.

Within the last 12 months, Morgan Stanley has provided or is providing investment banking services to, or has an investment banking client relationship with, the following company: Gemalto N.V., Logitech, Technicolor SA, Telit Communications PLC, TomTom NV.

Within the last 12 months, Morgan Stanley has either provided or is providing non-investment banking, securities-related services to and/or in the past has entered into an agreement to provide services or has a client relationship with the following company: Gemalto N.V., Technicolor SA, TomTom NV.

Morgan Stanley & Co. LLC makes a market in the securities of Logitech.

The equity research analysts or strategists principally responsible for the preparation of Morgan Stanley Research have received compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues and overall investment banking revenues. Equity Research analysts' or strategists' compensation is not linked to investment banking or capital markets transactions performed by Morgan Stanley or the profitability or revenues of particular trading desks.

Morgan Stanley and its affiliates do business that relates to companies/instruments covered in Morgan Stanley Research, including market making, providing liquidity, fund management, commercial banking, extension of credit, investment services and investment banking. Morgan Stanley sells to and buys from customers the securities/instruments of companies covered in Morgan Stanley Research on a principal basis. Morgan Stanley may have a position in the debt of the Company or instruments discussed in this report. Morgan Stanley trades or may trade as principal in the debt securities (or in related derivatives) that are the subject of the debt research report.

Certain disclosures listed above are also for compliance with applicable regulations in non-US jurisdictions.

STOCK RATINGS

Morgan Stanley uses a relative rating system using terms such as Overweight, Equal-weight, Not-Rated or Underweight (see definitions below). Morgan Stanley does not assign ratings of Buy,

Foundation

Morgan Stanley Research 29

Hold or Sell to the stocks we cover. Overweight, Equal-weight, Not-Rated and Underweight are not the equivalent of buy, hold and sell. Investors should carefully read the definitions of all ratings used in Morgan Stanley Research. In addition, since Morgan Stanley Research contains more complete information concerning the analyst's views, investors should carefully read Morgan Stanley Research, in its entirety, and not infer the contents from the rating alone. In any case, ratings (or research) should not be used or relied upon as investment advice. An investor's decision to buy or sell a stock should depend on individual circumstances (such as the investor's existing holdings) and other considerations.

Global Stock Ratings Distribution

(as of July 31, 2017)

The Stock Ratings described below apply to Morgan Stanley's Fundamental Equity Research and do not apply to Debt Research produced by the Firm.

For disclosure purposes only (in accordance with NASD and NYSE requirements), we include the category headings of Buy, Hold, and Sell alongside our ratings of Overweight, Equal-weight, Not-Rated and Underweight. Morgan Stanley does not assign ratings of Buy, Hold or Sell to the stocks we cover. Overweight, Equal-weight, Not-Rated and Underweight are not the equivalent of buy, hold, and sell but represent recommended relative weightings (see definitions below). To satisfy regulatory requirements, we correspond Overweight, our most positive stock rating, with a buy recommendation; we correspond Equal-weight and Not-Rated to hold and Underweight to sell recommendations, respectively.

Coverage Universe Investment Banking Clients (IBC)Other Material Investment Services Clients

(MISC)Stock Rating Cate-

goryCount % of Total Count % of Total IBC % of Rating Category Count % of Total Other MISC

Overweight/Buy 1150 36% 299 40% 26% 556 37%Equal-weight/Hold 1413 44% 349 47% 25% 692 46%

Not-Rated/Hold 61 2% 7 1% 11% 10 1%Underweight/Sell 607 19% 93 12% 15% 242 16%

Total 3,231 748 1500

Data include common stock and ADRs currently assigned ratings. Investment Banking Clients are companies from whom Morgan Stanley received investment banking compensation in the last 12 months.

Analyst Stock Ratings

Overweight (O or Over) - The stock's total return is expected to exceed the total return of the relevant country MSCI Index or the average total return of the analyst's industry (or industry team's) coverage universe, on a risk-adjusted basis over the next 12-18 months.

Equal-weight (E or Equal) - The stock's total return is expected to be in line with the total return of the relevant country MSCI Index or the average total return of the analyst's industry (or industry team's) coverage universe, on a risk-adjusted basis over the next 12-18 months.

Not-Rated (NR) - Currently the analyst does not have adequate conviction about the stock's total return relative to the relevant country MSCI Index or the average total return of the analyst's industry (or industry team's) coverage universe, on a risk-adjusted basis, over the next 12-18 months.

Underweight (U or Under) - The stock's total return is expected to be below the total return of the relevant country MSCI Index or the average total return of the analyst's industry (or industry team's) coverage universe, on a risk-adjusted basis, over the next 12-18 months.

Unless otherwise specified, the time frame for price targets included in Morgan Stanley Research is 12 to 18 months.

Analyst Industry Views

Attractive (A): The analyst expects the performance of his or her industry coverage universe over the next 12-18 months to be attractive vs. the relevant broad market benchmark, as indicated below.

In-Line (I): The analyst expects the performance of his or her industry coverage universe over the next 12-18 months to be in line with the relevant broad market benchmark, as indicated below.