global tea production & consumption trends

TRANSCRIPT

February , 2014

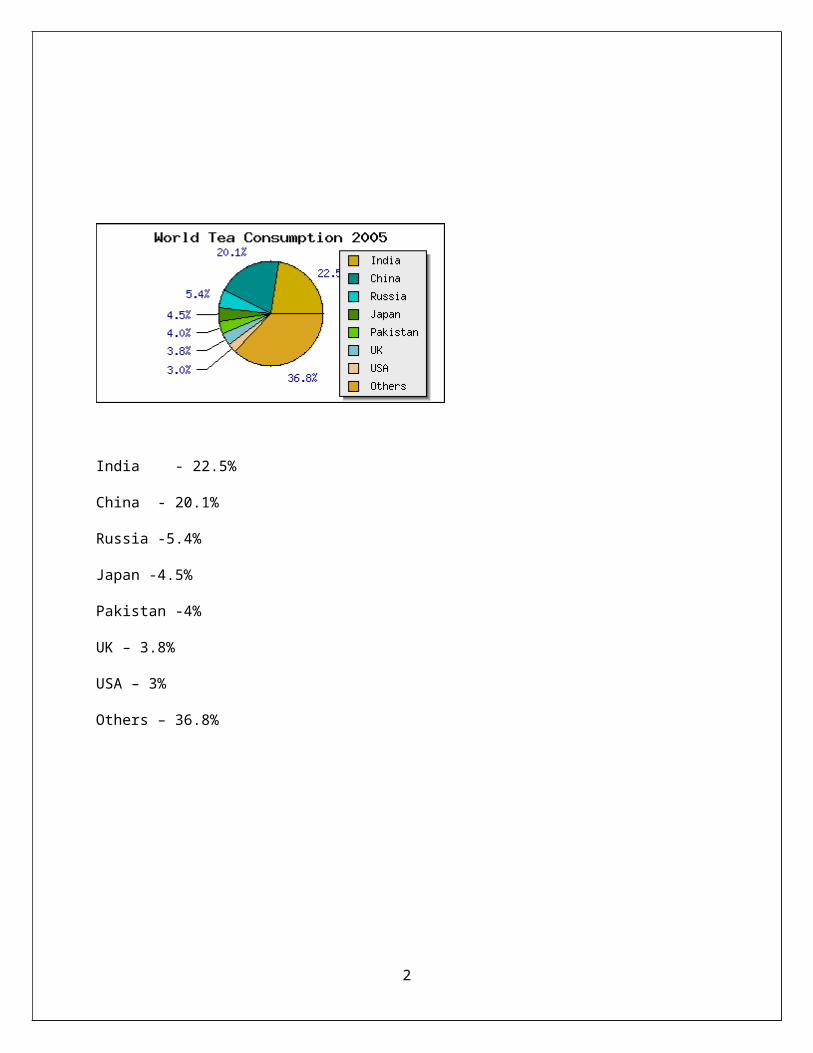

India - 22.5%

China - 20.1%

Russia -5.4%

Japan -4.5%

Pakistan -4%

UK – 3.8%

USA – 3%

Others – 36.8%

2

Tea

http://www.fao.org/docrep/006/y5143e/y5143e0z.htm

Introduction

The production and trade projections presented in this section are derived from a dynamic times series model of the world tea market. This model quantifies key market relationships on the basis of observations on the past behaviour of volumes produced and traded, prices, and population and income growth. This projection methodology is a development of a former one used to provide projections for the FAO Intergovernmental Group meetings. By exploiting additional information concerning the economics of market behaviour, the revised methodology should provide a sounder basis for projections, and allow a wider range of alternative scenarios to be explored.

The projections presented here also include a first attempt at providing separate results for black and green tea. While the differences in demand and price trends make this a useful distinction, data limitations mean that the analysis of green tea markets is less detailed.

Black tea production

World black tea production is projected to increase to 2.4 million tonnes in 2010, an annual average growth rate of 1.2 percent from 2.15 million tonnes in 2000. This growth would result largely from the improvement in yields.

Most African producers are likely to see significant production growth as tea bushes reach optimum production age, and production skills of small growers improve. For example, production in Kenya would grow by 2.3 percent a year from 236 300 tonnes in 2000 to 304 000 tonnes in 2010, while growth rates in Tanzania and Uganda are expected to be 1.7 percent and 2.7 percent, respectively.[15]

3

Most producers in Asia would experience a steady growth in production. Indonesia is expected to achieve an annual growth of 1.1 percent, from 130 600 tonnes in 2000 to 147 000 tonnes in 2010. Over the same period, production in India, the world’s largest black tea producing country, is projected to grow by 2.5 percent to 1.07 million tonnes, accounting for nearly 44 percent of global production, compared to 38 percent in 2000. Tea production in Sri Lanka is projected to reach 329 000 tonnes by 2010, an annual average growth rate of 0.7 percent. Black tea production in China is expected to continue to decline to 54 000 tonnes as the balance of production shifts to other teas with stronger market prospects.

The three largest black tea producing countries, India, Kenya and Sri Lanka, are expected to account for 70 percent of the world tea production in 2010, compared to 63 percent in 2000.

Black tea exports

World black tea exports in 2010 are projected at 1.14 million tonnes, reflecting an average annual increase of 1.1 percent from 1 million tonnes in 2000.

Most of this increase would take place in Africa, where production is likely to continue to grow while domestic consumption remains small. Exports from Kenya would increase by 2.6 percent annually from 208 200 tonnes in 2000 to 275 000 tonnes in 2010, giving Kenya 32 percent of global exports. Over the same period, export availability in Malawi would remain unchanged at 38 000 tonnes.

Most major tea exporting countries in Asia are expected to experience slight declines in exports in line with expected growth in income and population that would foster domestic consumption. For example, exports from India and Indonesia would decrease by 2.4 percent to 150 890 tonnes and by 1.1 percent to 87 000 tonnes, respectively. Conversely, exports from Sri Lanka would increase from 281 000 tonnes to 293 400 tonnes, an annual average growth rate of 0.4 percent.

4

Black tea consumption

In 2010 world net imports of black tea, a proxy for consumption, would amount to 1.15 million tonnes, reflecting an average annual increase of 0.6 percent from 1.08 million tonnes in 2000. Net imports in the countries of the former Soviet Union would increase from 223 600 tonnes to 315 200 tonnes, an annual average growth rate of 3 percent. Pakistan would increase its net imports by 2.9 percent per year from 109 400 tonnes to 150 000 tonnes. The United States is expected to increase net imports by 1.4 percent a year to 94 300 tonnes, while Japan would increase its net imports from 18 000 to 22 000 tonnes, an annual average growth rate of 1.8 percent. On the contrary, net imports by the United Kingdom are expected to decrease by 0.6 percent annually to 125 500 tonnes. These major importers together would account for about 60 percent of global net imports.

The model does not take into account stock levels. Hence, the difference between production and exports is treated as a proxy for domestic consumption in producing countries. In 2010, the quantity of black tea production that would be consumed in these countries is expected to reach 1.27 million tonnes, or 52 percent of global black tea production, compared to 1.14 million tonnes in 2000. Domestic consumption of black tea in India is expected to increase by an average annual rate of 3.7 percent to 919 300 tonnes by 2010, or 86 percent of the black tea produced in the country. During the same period, Indonesia is expected to increase its domestic consumption at an average annual rate of 4.0 percent from 33 100 tonnes to 51 000 tonnes. Domestic consumption in Bangladesh and Sri Lanka would grow by 2.0 percent and 3.8 percent to reach 45 000 tonnes and 36 000 tonnes, respectively.

Green tea market trends

Projections for green tea are provided only for production and exports due to data limitations. World green tea production is forecast to increase from 680 700 tonnes in 2000 to 900 000 tonnes in 2010, reflecting an annual average growth rate of 2.6 percent. During this period, production in China would grow by 2.7 percent per annum from 500 000 tonnes to 671 000

5

tonnes, accounting for 75 percent of global green tea production in 2010, compared to 73.5 percent in 2000. Production in Japan would grow by an average rate of 0.1 percent to 90 800 tonnes, while production in Viet Nam is expected to increase by an average rate of 2.5 percent to 50 000 tonnes. Output in Indonesia would grow by 2.3 percent annually to reach 49 000 tonnes.

Green tea exports are expected to exhibit a significant upward trend in keeping with production. Total exports would increase by 2.8 percent annually from 186 800 tonnes in 2000 to 254 000 tonnes in 2010. China would continue to be the world’s dominant green tea exporter, with shipments reaching 210 000 tonnes by 2010, reflecting an annual average growth rate of 2.7 percent. During the same period, exports from Indonesia are expected to increase by 3.8 percent per annum to 12 000 tonnes, while exports from Viet Nam would increase by 2.5 percent a year to 25 000 tonnes. Japan would consume most of its domestic production.

Morocco, the world’s leading green tea importer, is expected to increase imports from 35 200 tonnes in 2000 to 57 100 tonnes in 2010, an annual average growth rate of 4.5 percent.

Issues and uncertainties

The projections indicate that over the next decade exports of black tea would increase at an annual growth rate of a little over one percent, mirroring a similar growth in production. However, the world market is expected to remain broadly in balance. In consequence, price levels should be maintained.

In contrast, with consumption outstripping the production of green tea, an upward trend would persist in the medium-term.

Several actions can be taken to enhance returns from black tea production. On the supply side, by reducing unit costs through productivity gains, building capacity of small growers, streamlining marketing channels and improving infrastructure, improved returns to growers may result.

6

On the demand side, consumption can be raised through effective marketing. Variations in demand among countries suggest that marketing activities need to be tailored to individual markets. Successful market-specific activities require in-depth knowledge and understanding of the target market, including consumers’ preference and market structures. In addition, worldwide marketing efforts, such as the generic promotion of tea using the Tea Mark, could have a significant impact, if planned and implemented appropriately.

It is important that any action taken is done holistically to improve longer-term price prospects. Forming such a strategy requires better understanding of markets. Exchanging information and views between producers and consumers, as well as public and private sectors, could promote greater market transparency.

7

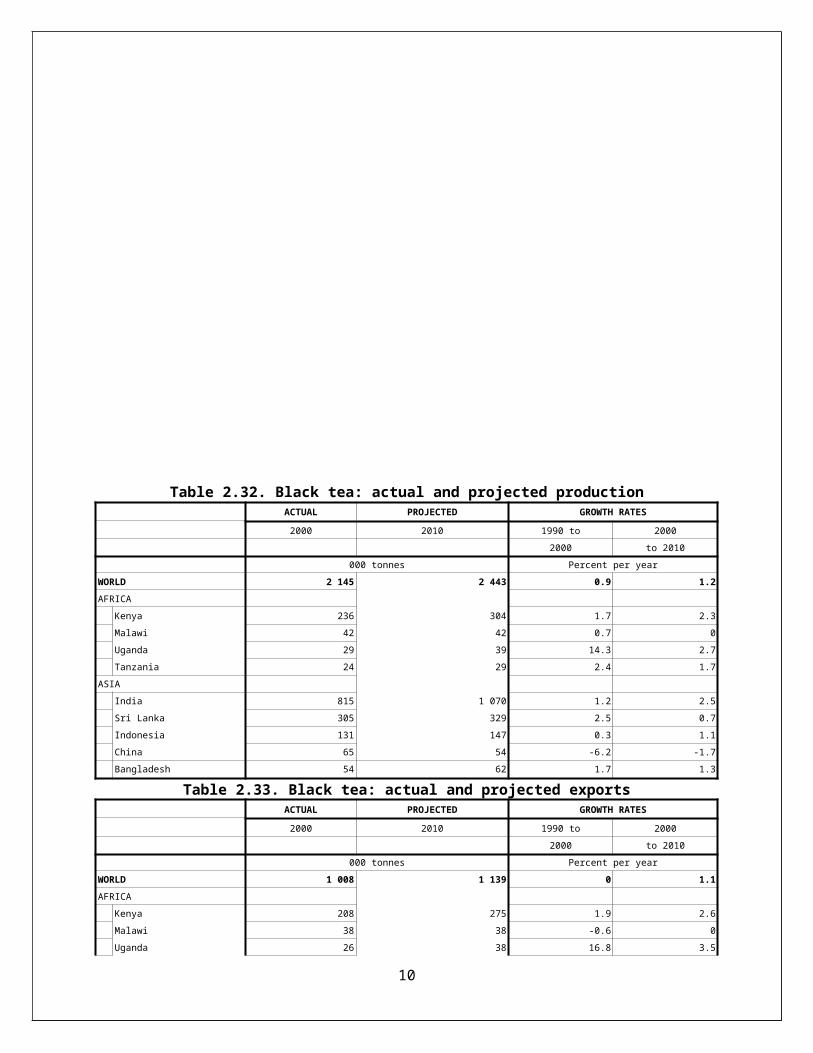

Table 2.32. Black tea: actual and projected productionACTUAL PROJECTED GROWTH RATES

2000 2010 1990 to 2000

2000 to 2010

000 tonnes Percent per year

WORLD 2 145 2 443 0.9 1.2

AFRICA

Kenya 236 304 1.7 2.3

Malawi 42 42 0.7 0

Uganda 29 39 14.3 2.7

Tanzania 24 29 2.4 1.7

ASIA

India 815 1 070 1.2 2.5

Sri Lanka 305 329 2.5 0.7

Indonesia 131 147 0.3 1.1

China 65 54 -6.2 -1.7

Bangladesh 54 62 1.7 1.3

Table 2.33. Black tea: actual and projected exportsACTUAL PROJECTED GROWTH RATES

2000 2010 1990 to 2000

2000 to 2010

000 tonnes Percent per year

WORLD 1 008 1 139 0 1.1

AFRICA

Kenya 208 275 1.9 2.6

Malawi 38 38 -0.6 0

Uganda 26 38 16.8 3.5

Tanzania 22 28 3.8 2.2

ASIA

Sri Lanka 281 293 2.5 0.4

India 198 151 -0.4 -2.4

Indonesia 98 87 -1 -1.1

China 28 21 -10.1 -2.6

Bangladesh 18 17 -3.6 -0.5

8

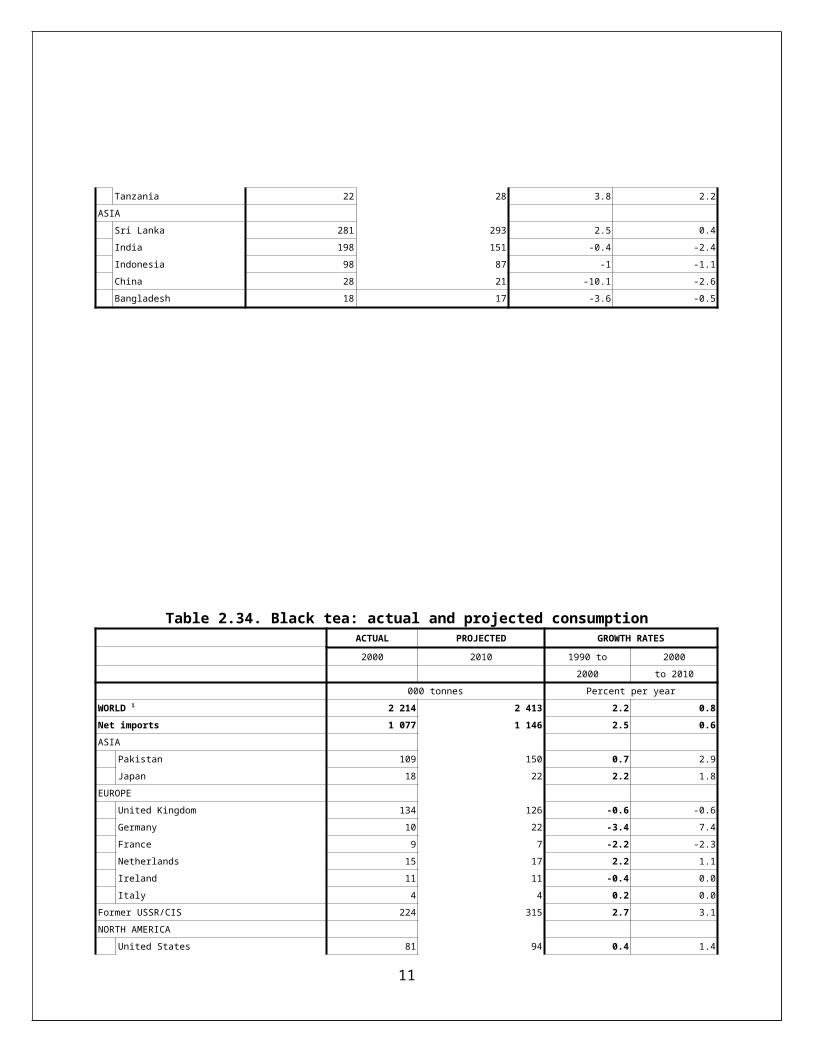

Table 2.34. Black tea: actual and projected consumptionACTUAL PROJECTED GROWTH RATES

2000 2010 1990 to 2000

2000 to 2010

000 tonnes Percent per year

WORLD 1 2 214 2 413 2.2 0.8

Net imports 1 077 1 146 2.5 0.6

ASIA

Pakistan 109 150 0.7 2.9

Japan 18 22 2.2 1.8

EUROPE

United Kingdom 134 126 -0.6 -0.6

Germany 10 22 -3.4 7.4

France 9 7 -2.2 -2.3

Netherlands 15 17 2.2 1.1

Ireland 11 11 -0.4 0.0

Italy 4 4 0.2 0.0

Former USSR/CIS 224 315 2.7 3.1

NORTH AMERICA

United States 81 94 0.4 1.4

Canada 15 19 1 2.2

OCEANIA

Australia 14 11 -1.5 -2.2

Domestic consumption2 1 137 1 267 1.9 1.0

AFRICA

Uganda 3 1 3.9 -9.5

Tanzania 1 1 0 0.0

Malawi 4 4 0 0.2

Kenya 28 29 0.2 0.3

ASIA

India 617 919 1.8 3.7

Indonesia 33 51 6.1 4.0

China 37 31 -1.1 -1.6

Bangladesh 36 45 2.4 2.0

Sri Lanka 24 36 2.6 3.8

1/ Net imports plus domestic consumption2/ Production minus exports

9

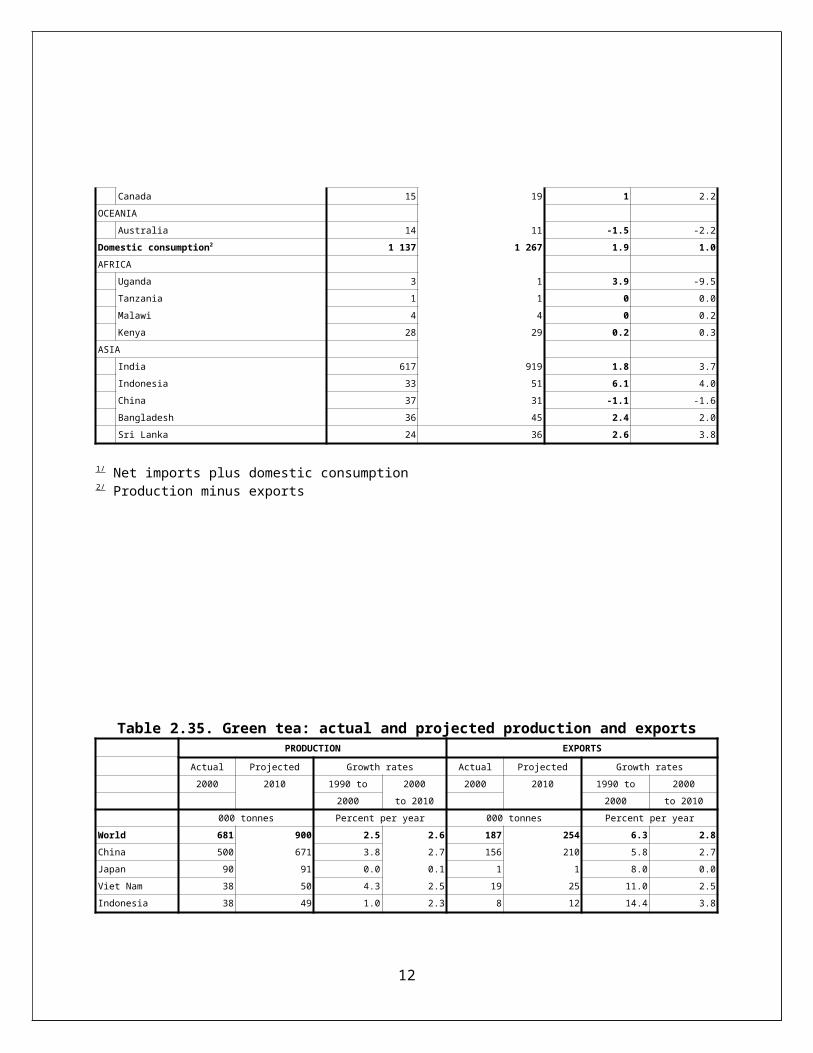

Table 2.35. Green tea: actual and projected production and exportsPRODUCTION EXPORTS

Actual Projected Growth rates Actual Projected Growth rates

2000 2010 1990 to 2000 2000 2010 1990 to 2000

2000 to 2010 2000 to 2010

000 tonnes Percent per year 000 tonnes Percent per year

World 681 900 2.5 2.6 187 254 6.3 2.8

China 500 671 3.8 2.7 156 210 5.8 2.7

Japan 90 91 0.0 0.1 1 1 8.0 0.0

Viet Nam 38 50 4.3 2.5 19 25 11.0 2.5

Indonesia 38 49 1.0 2.3 8 12 14.4 3.8

Black Tea

Key Production Points :

Asia –India, Sri Lanka, Indonesia , China , Bangladesh

10

Africa – Kenya, Uganda, Malawi , Tanzania

Key Consumption Points:

Asia - India , Pakistan , Japan ,Indonesia , China , Bangladesh , Sri Lanka

Europe – UK, Germany, France , Netherlands , Ireland , Italy

North America – USA, Canada

Africa – Kenya

India- India has also consistently been a major hub of tea production in the world. Amounting to 23% of global production, India produces 966,733 metric tonnes of tea every year, and exports around 203,207 metric tonnes of tea, worth $867,143,000, annually – a 12% share in the international market. Several farmlands in Darjeeling and Assam have become famous all around the world thanks to Tata tea; one of the major commercial tea brands in India. Indian tea is considered by some to be the best in the world, thanks to good processing and strategic market expansion.

China - Tea is incredibly important in China, which is the largest tea-producing country in the world. China dominated the international market in tea exports until the 1880s, and ranks third on the list today. However, most of the tea grown in China is consumed within the country, and so only a small portion is exported internationally. With annual production of 1,640,310 metric tonnes annually, only 299,789 metric tons, worth $965,080,000, are exported in the international market. All told, China contributes about 35% of the total amount of tea grown around the world.

11

Sri Lanka - Tea production and export has been the major source of this Asian country’s economy, and accounts for around 2% of the GDP of Sri Lanka. The tea industry got its commercial start in the country in 1847, thriving in Sri Lanka’s cool and humid environment. Overally, it’s the fourth-largest tea producing country in the world, and second on the list of the largest exporters. Producing a total of 327,500 metric tonnes of tea, 318,329 tonnes are exported to the international community, accounting for roughly $1.48 billion annually. About 23% of the total export of tea in the international market is provided by Sri Lanka alone, and the product accounts for roughly 60% of Srilanka’s export profit.

Kenya - With more than 111,000 hectors of land for tea production, Kenya ranks highest on the list of the largest exporters of tea around the world. Contributing from 17-20% of the country’s total export revenue, Kenya exports 396,641 metric tonnes of tea annually, a number that has grown by about 39% over a decade. 80% of the total tea produced in Kenya comes from small scale farmers, with the remaining a product of large scale operations. The product is collected, processed, and refined for exports worth $858,250,000, a contribution of around 28% of the total tea exported in the international market.

12

Green Tea

Key Production Points :

China, Japan, Vietnam , Indonesia

Vietnam - Tea in Vietnam is produced mostly on a commercial and industrial scale, and around 174,900 metric tonnes of tea is produced each year, worth $204,018,000 in the international market. The average price of tea exported from Vietnam is worth $1,340 per tonne, which is very high in comparison to other countries. However, Vietnamese tea is exported to 61 countries in the world, of which a very low amount is exported to European and American nations. Taiwan and Pakistan import almost all of their tea supplies from Vietnam.

13

TEA CONSUMPTION :

Egypt ranks among the top importers of tea in Africa, and imports around 23% of its tea supply from Kenya. Tea is the national drink of Egypt, which makes it one of the most highly-imported goods in its economic market. About 107,586 metric tonnes of tea, worth $308,452,000, is imported annually in the country, mostly from Kenya and Sri Lanka. The Egyptian government considers it a strategic crop, and runs tea plantations in Kenya as well. With the increasing demand of high quality and low priced tea in Egypt, India marketers have stepped up in exporting CTC tea to Egypt.

The United Arab Emirates ranks fourth on the list of the biggest tea importers, but is also the world’s leading country in tea re-exporting. Tea is brought into the country in raw form, and the industries in the country refine, polish, package and sell the product back to the international market at a higher price. Around 108,575 metric tonnes of tea is imported annually in this country – about 10% higher than the imports in the last decade. Annually, an amount of tea worth $485,768,000 is brought into the country, mostly from India and China, and then re-exported to countries like Iran and Oman after the product is refined and packaged.

Tea, in various sweetened and unsweetened forms, is one of the most popular drinks in the United States and the consumption has been increasing at a very high rate after the 90s. With the invention of tea bags, consumption in the United States has grown. Several varieties of tea, flavored and unflavored, blended and premium, have been imported from various parts of the world. The United States imports a total of 116,746 metric tonnes of tea every year to supply its demand, and also as part of the tea bag

14

packaging industry. About $ 318,535,000 worth of tea is brought in every year.

Since the British Empire was at its peak, tea has been regarded as a very high class drink in the United Kingdom. Because of that, the United Kingdom has been one of the largest tea-consuming countries in the world, with an average person consuming around 1.9 kg of tea per year. The invention of tea bags further increased the consumption of tea in the country. Around 165 million cups of tea is consumed each day in the United Kingdom, and around 157,593 metric tonnes of tea is imported annually, mostly coming from China and India. The country imports tea to the tune of $367,564,000.

Russia is one of the global leaders in tea consumption, and the country that imports the highest amount of tea in the world. According to KPMG analysts, people in Russia drink around four cups of tea daily, driving up the domestic value of the tea industry to $510,872,000 each year. Russia imports around 181,859 metric tonnes of tea annually from several international tea traders. Kenya and Srilanka have been the major countries to export tea to Russia, while the high cost of tea in India has caused a minimum amount of tea to be imported from India.

15

Japan

Japanese green tea consumptionJapanese green tea has took root in Japanese society as taste drink as well as indispensable product.

Consumed green teas are various.These teas are different dependent on production areas and plantation as well as production method and distribution

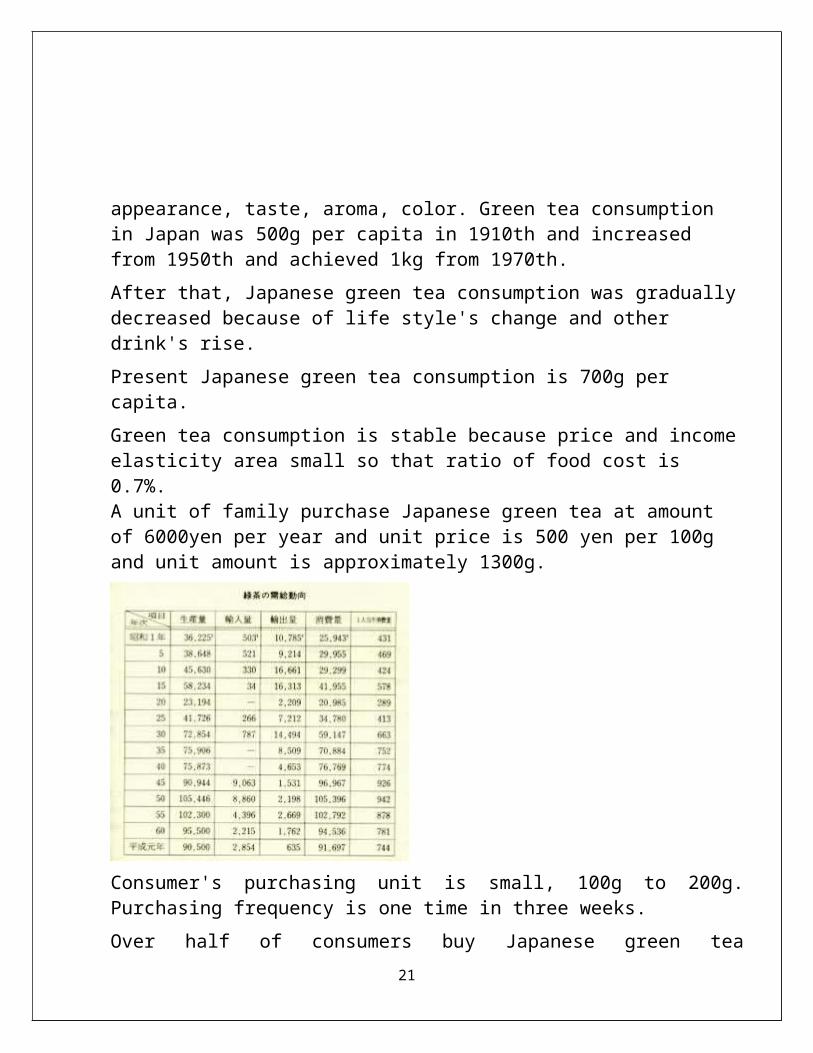

Therefore kinds of Japanese green teas are countless. However, these teas are judged by same 4 criteria, appearance, taste, aroma, color. Green tea consumption in Japan was 500g per capita in 1910th and increased from 1950th and achieved 1kg from 1970th.

After that, Japanese green tea consumption was gradually decreased because of life style's change and other drink's rise.

Present Japanese green tea consumption is 700g per capita.

Green tea consumption is stable because price and income elasticity area small so that ratio of food cost is 0.7%. A unit of family purchase Japanese green tea at amount of 6000yen per year and unit price is 500 yen per 100g and unit amount is approximately 1300g.

16

Consumer's purchasing unit is small, 100g to 200g. Purchasing frequency is one time in three weeks.

Over half of consumers buy Japanese green tea specialized shops. Next 30% of consumers buy Japanese green tea in supermarkets.

Recently Tokyo Japanese green tea association has made campaign that " Let customer buy Japanese green tea in Japanese green tea specialized shop.

http://www.japan-guide.com/e/e2041.html

Tea is the most commonly drunk beverage in Japan and an important part of Japanese food culture. Various types of tea are widely available and consumed at any point of the day. Green tea is the most common type of tea, and when someone mentions "tea" (お茶, ocha) without specifying the type, it is green tea to which is referred. Green tea is also the central element of the tea ceremony. Among the most well-known places for tea cultivation in Japan are Shizuoka, Kagoshima and Uji.

The following is a list of the main varieties of tea that are popularly consumed in Japan:

17

Tea from tea plant

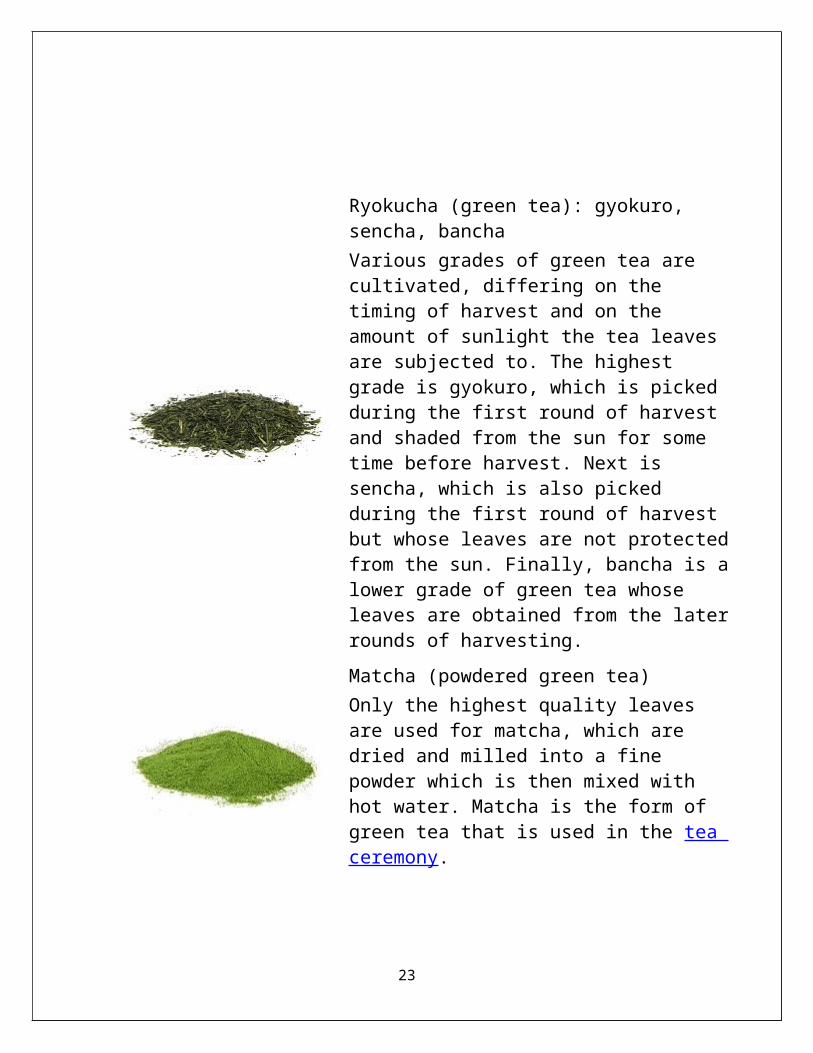

Ryokucha (green tea): gyokuro, sencha, banchaVarious grades of green tea are cultivated, differing on the timing of harvest and on the amount of sunlight the tea leaves are subjected to. The highest grade is gyokuro, which is picked during the first round of harvest and shaded from the sun for some time before harvest. Next is sencha, which is also picked during the first round of harvest but whose leaves are not protected from the sun. Finally, bancha is a lower grade of green tea whose leaves are obtained from the later rounds of harvesting.

Matcha (powdered green tea)Only the highest quality leaves are used for matcha, which are dried and milled into a fine powder which is then mixed with hot water. Matcha is the form of green tea that is used in the tea ceremony.

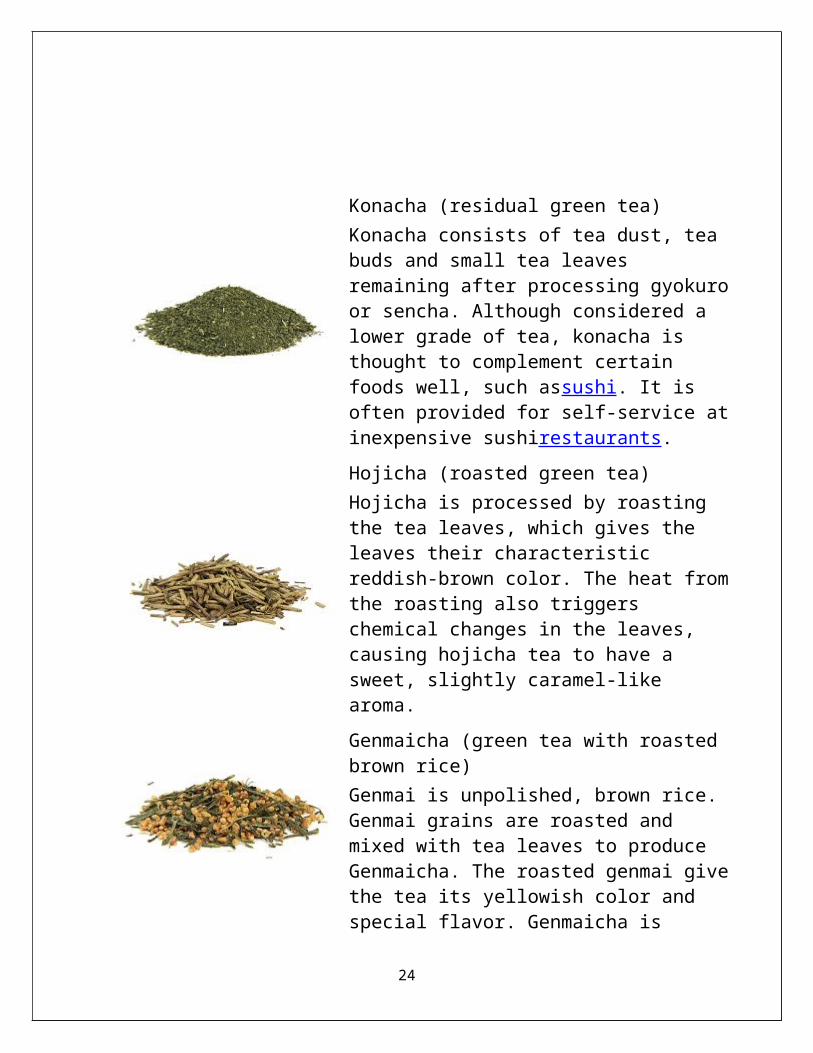

Konacha (residual green tea)Konacha consists of tea dust, tea buds and small tea leaves remaining after processing gyokuro or sencha. Although considered a lower grade of tea, konacha is thought to complement certain foods well, such assushi. It is often provided for self-service at inexpensive sushirestaurants.

18

Hojicha (roasted green tea)Hojicha is processed by roasting the tea leaves, which gives the leaves their characteristic reddish-brown color. The heat from the roasting also triggers chemical changes in the leaves, causing hojicha tea to have a sweet, slightly caramel-like aroma.

Genmaicha (green tea with roasted brown rice)Genmai is unpolished, brown rice. Genmai grains are roasted and mixed with tea leaves to produce Genmaicha. The roasted genmai give the tea its yellowish color and special flavor. Genmaicha is popularly served as an alternative to the standard green tea.

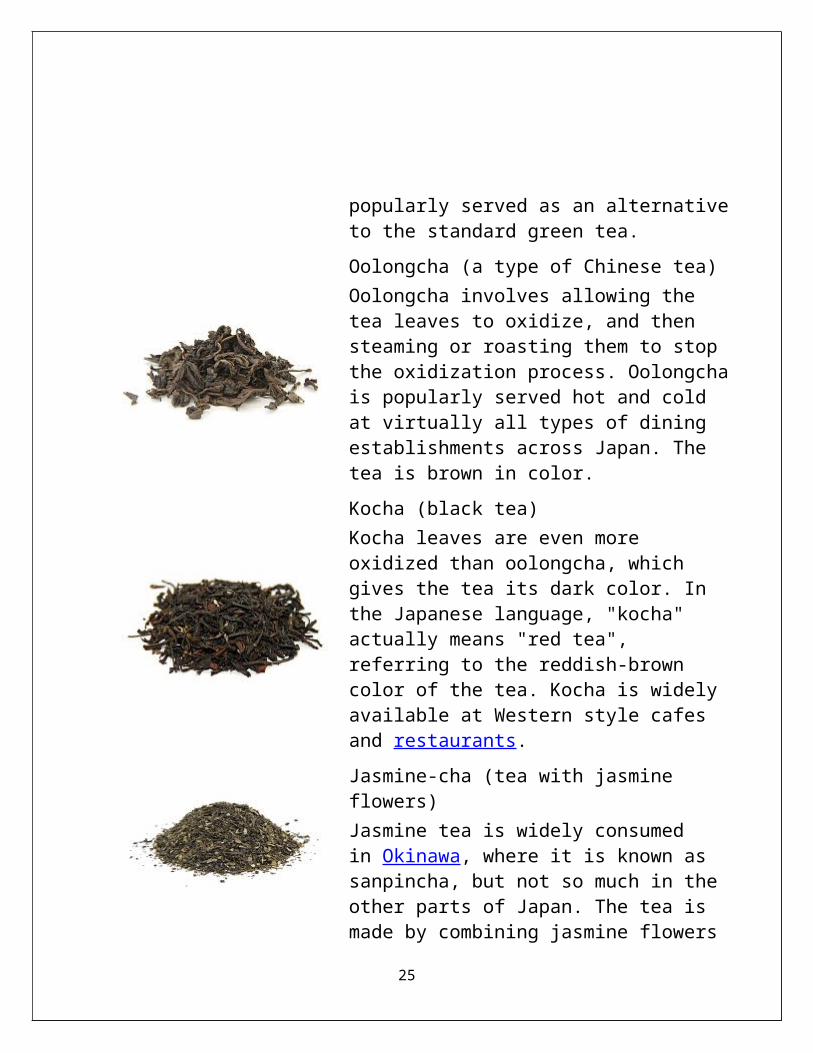

Oolongcha (a type of Chinese tea)Oolongcha involves allowing the tea leaves to oxidize, and then steaming or roasting them to stop the oxidization process. Oolongcha is popularly served hot and cold at virtually all types of dining establishments across Japan. The tea is brown in color.

Kocha (black tea)Kocha leaves are even more oxidized than oolongcha, which gives the tea its dark color. In the Japanese language, "kocha" actually means "red tea", referring to the reddish-brown color of the tea. Kocha is widely available at Western style cafes and restaurants.

19

Jasmine-cha (tea with jasmine flowers)Jasmine tea is widely consumed in Okinawa, where it is known as sanpincha, but not so much in the other parts of Japan. The tea is made by combining jasmine flowers with a green tea or sometimes oolong tea base.

Tea not from tea plant

Mugicha (barley tea)Mugicha is made by infusing roasted barley into water. The drink is popularly served cold in summer, and some consider it more suitable for consumption by children because it does not contain caffeine from the tea leaves.

Kombucha (kelp tea)Kombucha is a beverage made by mixing ground or sliced kombu seaweed into hot water. The drink has a salty taste and is sometimes served as a welcome drink at ryokan.

Where tea can be found

Tea of one kind or another, hot or cold, can be found practically at all restaurants, vending machines, kiosks,convenience stores and supermarkets

At restaurants, green tea is often served with or at the end of a meal for free. At lower end restaurants, green tea or mugicha tend to be available free for self-service, while konacha is commonly provided at inexpensive sushirestaurants. Kocha is usually available alongside coffee at

20

cafes and Western restaurants.

At some temples and gardens, tea (usually ryokucha or matcha) is served to tourists. The tea is typically served in a tranquil tatami room with views onto beautiful scenery, often together with an accompanying Japanese sweet. While the tea is sometimes included in the temple's or garden's admission fee, it more often requires a separate fee of a few hundred yen.

Last but not least, many types of tea are sold in PET bottles and cans at stores and vending machines across Japan. They are available both hot or cold, although hot tea is less widely available during the summer months, especially at vending machines.

Having tea with a garden view at Tottori's Kannonin Temple

Japanese tea and a brief history

Tea was first introduced to Japan from China in the 700s. During the Nara Period (710-794), tea was a luxury product available in small amounts to priests and noblemen as a medicinal beverage.

Around the beginning of the Kamakura Period (1192-1333), Eisai, the founder of Japanese Zen Buddhism, brought back from China the custom of making tea from powdered leaves. Subsequently, the cultivation of tea spread across Japan, notably at Kozanji Temple in Takao and in Uji.

During the Muromachi Period (1333-1573), tea gained popularity among people of all social classes. People gathered in big tea drinking parties and played a guessing game, whereby participants, after drinking from cups of tea being passed along, guessed the names of tea and where they came from. Collecting and showing off prized tea utensils was also popular among the affluent.

At about the same time, a more refined version of tea parties, with Zen-inspired simplicity and a greater emphasis on etiquette and spirituality

21

developed. These gatherings were attended by only a few people in a small room where the host served the guests tea, allowing greater intimacy. It is from these gatherings that the tea ceremony has its origins.

Inside the Joan Teahouse in Inuyama

22

Pakistan - Tea

In Pakistan, tea is popular all over the country and holds an integral significance in local culture; it is one of the most consumed beverages in Pakistani cuisine. The local name for tea, in Urdu, is Chai. While Pakistan does not produce tea, it is a major tea-consuming country, being ranked as the third largest importer of tea in the world. In 2003, as much as 109,000 tons of tea was consumed in Pakistan, placing it as the seventh largest tea-consuming country in the world.

Doodh pati

Masala chai

Green tea

Kawah

Varieties

Different regions throughout the country have their own different flavours and varieties, giving Pakistani tea culture a diverse blend. In Karachi, the strong presence of Muhajir cuisine has allowed the Masala Chai version to be very popular while the thick and milky Doodh Pati Chai is more preferred in Punjab. Biscuits and paan are common delicacies and staples enjoyed with tea. In the northern and western parts of the country, including Khyber Pakhtunkhwa, Balochistan and much of Kashmir, the popular green tea Kahwah is predominant. In the further north Chitral and Gilgit-Baltistan regions, Central Asian variants such as salty buttered Tibetan style tea are consumed.

23

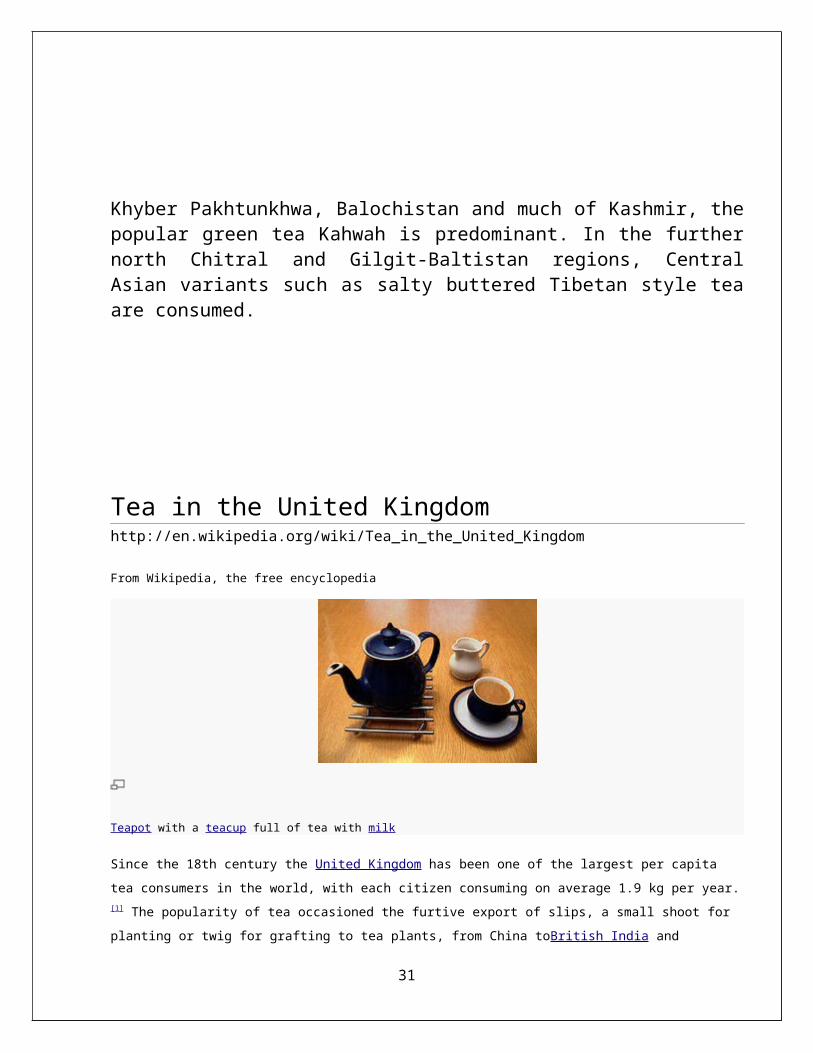

Tea in the United Kingdomhttp://en.wikipedia.org/wiki/Tea_in_the_United_Kingdom

From Wikipedia, the free encyclopedia

Teapot with a teacup full of tea with milk

Since the 18th century the United Kingdom has been one of the largest per capita tea consumers in the world,

with each citizen consuming on average 1.9 kg per year.[1] The popularity of tea occasioned the furtive export of

slips, a small shoot for planting or twig for grafting to tea plants, from China toBritish India and its commercial

culture there, beginning in 1840; British interests controlled tea production in the subcontinent. Tea, which was an

upper-class drink in Europe, became the infusion of every class in Great Britain in the course of the 18th century

and has remained so.

In Britain, the drinking of tea is so varied that it is quite hard to generalise, but usually it is served with milk and

sometimes with lemon. Strong tea can be served with milk and occasionally one or two teaspoons of sugar in

a mug, and is commonly referred to as builder's tea. The expression "cream tea" does not refer to cream mixed

into the beverage but to a meal in which tea is taken along with scones and clotted cream, and usually strawberry

jam as well. (This tradition originated from Devon and Cornwall.)

Much of the time in the United Kingdom, tea drinking is not the delicate, refined cultural expression that some

might imagine: a cup (or commonly a mug) of tea is something drunk often.

24

History[edit]

Tea with milk that has not yet been stirred

Before it became Britain's number one drink, China tea was introduced in the coffeehouses of London

shortly before the Stuart Restoration (1660); about that time Thomas Garraway, a coffeehouse owner in

London, had to explain the new beverage in pamphlet and an advertisement in Mercurius Politicusfor 30

September 1658 offered "That Excellent, and by all Physicians approved, China drink, called by

the Chinese, Tcha, by other nations Tay alias Tee, ...sold at the Sultaness-head, ye Cophee-house in

Sweetings-Rents, by the Royal Exchange, London". [2] In London "Coffee, chocolate and a kind of drink

called tee" were "sold in almost every street in 1659", according to Thomas Rugge's Diurnall.[3] Tea was

mainly consumed by the fashionably rich: Samuel Pepys, curious for every novelty, tasted the new drink in

1660: [25 September] "I did send for a cup of tee, (a China drink) of which I had never had drunk before".

Two pounds, two ounces were formally presented to Charles II by the British East India Company that

same year.[4] The tea had been imported to Portugal from its possessions in Asia as well as through the

trade merchants maintained with China and Japan. In 1662 Charles II's Portuguese queen, Catherine of

Braganza, introduced the act of drinking tea, which quickly spread throughout court and country and to the

English bourgeoisie. The British East India company, which had been supplied with tea at the Dutch factory

of Batavia imported it directly from China from 1669.[5] In 1672, a servant of Baron Herbert in London sent

his instructions for tea making, and warming the delicate cups, to Shropshire;

"The directions for the tea are: a quart of spring water just boiled, to which put a spoonful of tea, and

sweeten to the palate with candy sugar. As soon as the tea and sugar are in, the steam must be kept in as

much as may be, and let it lie half or quarter of an hour in the heat of the fire but not boil. The little cups

must be held over the steam before the liquid be put in."[6]

Between 1720 and 1750 the imports of tea to Britain through the British East India Company more than

quadrupled.[7] Fernand Braudel queried, "is it true to say the new drink replaced gin in England?"[8] By 1766,

exports from Canton stood at 6 million pounds on British boats, compared with 4.5 on Dutch ships, 2.4 on

Swedish, 2.1 on French.[9] Veritable "tea fleets" grew up. Tea was particularly interesting to the Atlantic

25

world not only because it was easy to cultivate but also because of how easy it was to prepare and its

ability to revive the spirits and cure mild colds:[10]"Home, and there find my wife making of tea", Pepys

recorded under 28 June 1667, "a drink which Mr. Pelling the Pottecary tells her is good for her colds and

defluxions".

The earliest English equipages for making tea date to the 1660s. Small porcelain tea bowls were used by

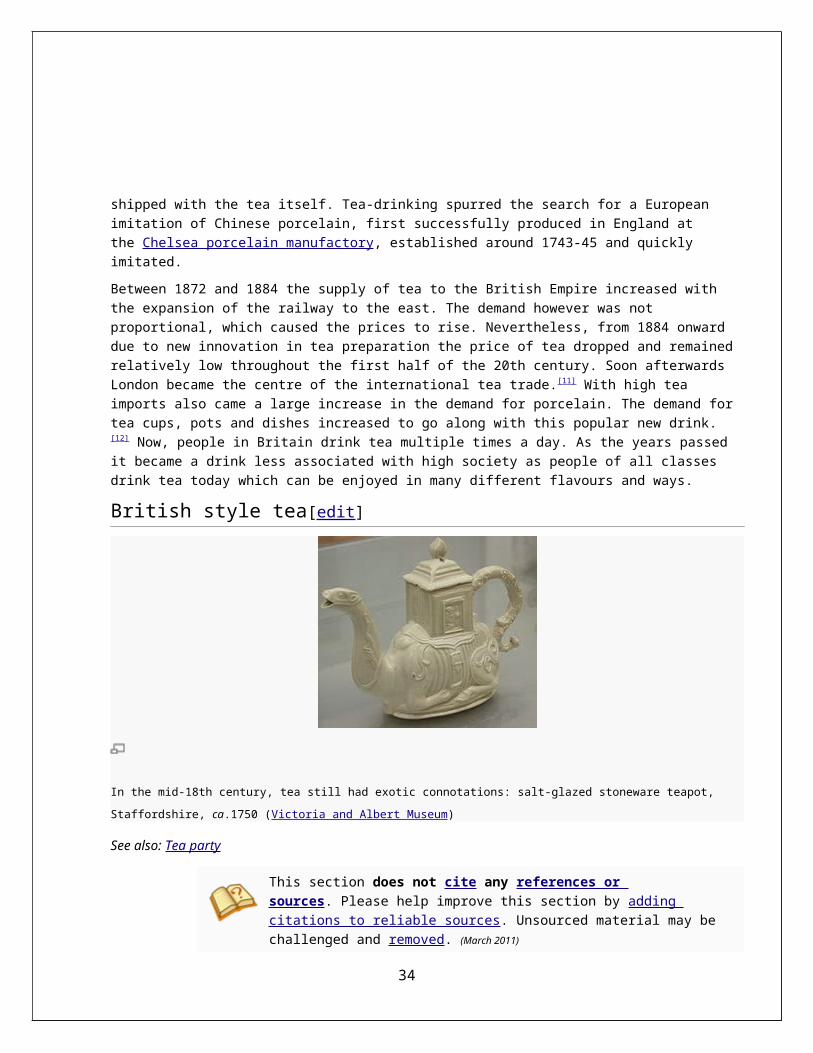

the fashionable; they were occasionally shipped with the tea itself. Tea-drinking spurred the search for a

European imitation of Chinese porcelain, first successfully produced in England at the Chelsea porcelain

manufactory, established around 1743-45 and quickly imitated.

Between 1872 and 1884 the supply of tea to the British Empire increased with the expansion of the railway

to the east. The demand however was not proportional, which caused the prices to rise. Nevertheless, from

1884 onward due to new innovation in tea preparation the price of tea dropped and remained relatively low

throughout the first half of the 20th century. Soon afterwards London became the centre of the international

tea trade.[11] With high tea imports also came a large increase in the demand for porcelain. The demand for

tea cups, pots and dishes increased to go along with this popular new drink.[12] Now, people in Britain drink

tea multiple times a day. As the years passed it became a drink less associated with high society as people

of all classes drink tea today which can be enjoyed in many different flavours and ways.

British style tea[edit]

In the mid-18th century, tea still had exotic connotations: salt-glazed stoneware teapot, Staffordshire, ca.1750 (Victoria and

Albert Museum)

See also: Tea party

This section does not cite any references or sources. Please help improve

this section by adding citations to reliable sources. Unsourced material may be

challenged and removed. (March 2011)

26

This section possibly contains original research. Please improve

it by verifying the claims made and adding inline citations. Statements consisting

only of original research may be removed. (March 2011)

Even very slightly formal events can be a cause for cups and saucers to be used instead of mugs. A typical

semi-formal British tea ritual might run as follows (the host performing all actions unless noted):[13]

1. The kettle, with fresh water, is brought to a rolling boil.

2. Enough boiling water is swirled around the teapot to warm it and then poured out.

3. Add loose tea leaves, (usually black tea) or tea bags, always added before the boiled water.

4. Fresh boiling water is poured over the tea in the pot and allowed to brew for 2 to 5 minutes while

a tea cosy may be placed on the pot to keep the tea warm. If the tea is allowed to brew for too

long, for example, more than 10 minutes, it will become "over-steeped",or "stewed", resulting in a

very bitter, astringent taste.

5. Milk may be added to the tea cup, the host asking the guest if milk is wanted, although milk may

alternatively be added after the tea is poured.

6. A tea strainer is placed over the top of the cup and the tea poured in, unless tea bags are used.

Tea bags may be removed, if desired, once desired strength is attained.

7. Fresh milk and white sugar is added according to individual taste. Most people have milk with their

tea, many without sugar.

8. The pot will normally hold enough tea so as not to be empty after filling the cups of all the guests. If

this is the case, the tea cosy is replaced after everyone has been served. Hot water may be

provided in a separate pot, and is used only for topping up the pot, never the cup.

Whether to put milk into the cup before or after the tea is, and has been since at least the late 20th century,

a matter of some debate with claims that adding milk at the different times alters the flavour of the tea.[citation

needed] The heating of milk above 75 degrees Celsius (adding milk after the tea is poured, not before) does

cause denaturation of the lactalbumin and lactoglobulin.[14] This may affect the flavour. In addition to

considerations of flavour, the order of these steps is thought to have been, historically, an indication of

class. Only those wealthy enough to afford good qualityporcelain would be confident of its being able to

cope with being exposed to boiling water unadulterated with milk.[15]

There is also a proper manner in which to drink tea when using a cup and saucer.[citation needed] If one is seated

at a table, the proper manner to drink tea is to raise the teacup only, placing it back into the saucer in

between sips. When standing or sitting in a chair without a table, one holds the tea saucer with the off hand

and the tea cup in the dominant hand. When not in use, the tea cup is placed back in the tea saucer and

held in one's lap or at waist height. In either event, the tea cup should never be held or waved in the air.

Fingers should be curled inwards, no finger should extend away from the handle of the cup.[13]

Drinking tea from the saucer (poured from the cup in order to cool it) was not uncommon at one time but is

now almost universally considered a breach of etiquette.

27

Tea as a meal[edit]

Main article: Tea (meal)

Tea is not only the name of the beverage, but of a late afternoon light meal at four o'clock, irrespective of

the beverage consumed. Anna Russell, Duchess of Bedford is credited with the creation of the meal circa

1800. She thought of the idea to ward off hunger between luncheon and dinner, which was served later and

later. The tradition continues to this day.

There used to be a tradition of tea rooms in the UK which provided the traditional fare

of cream and jam on scones, a combination commonly known as cream tea. However, these

establishments have declined in popularity since World War II. In Devon and Cornwall particularly, cream

teas are a speciality. A.B.C. tea shops and Lyons Corner Houses were a successful chain of such

establishments. In Yorkshire the company Bettys and Taylors of Harrogate, run their own

Tearooms. Bettys Café Tearooms, established in 1919, is now classed as a British Institution. In America it

is a common misconception that cream tea refers to tea served with cream (as opposed to milk). This is

certainly not the case. It simply means that tea is served with a scone with clotted cream and jam.

An English tea caddy, a box to store loose tea leaves

Industrial Revolution[edit]

Some scholars suggest that tea played a role in British Industrial Revolution. Afternoon tea possibly

became a way to increase the number of hourslabourers could work in factories (e.g. trolley service); the

stimulants in the tea, accompanied by sugary snacks (such as cream horns) would give workers energy to

finish out the day's work. Further, tea helped alleviate some of the consequences of the urbanization that

accompanied the industrial revolution: drinking tea required boiling one's water, thereby killing water-

borne diseases like dysentery, cholera, and typhoid.[16]

Tea cards[edit]

In the United Kingdom, and to a certain extent, Canada, a number of varieties of loose tea sold in packets

28

from the 1940s to the 1980s contained tea cards. These were illustrated cards roughly the same size

as cigarette cards and intended to be collected by children. Perhaps the best known wereTyphoo

tea and Brooke Bond (manufacturer of PG Tips), the latter of whom also provided albums for collectors to

keep their cards in. Some renowned artists were commissioned to illustrate the cards including Charles

Tunnicliffe. Many of these card collections are now valuable collectors' items.

A related phenomenon arose in the early 1990s when PG Tips released a series of tea-based Pogs, with

pictures of cups of tea and chimpanzees on them. Tetley's tea released competing pogs but never matched

the popularity of the PG Tips variety.

Tea today[edit]

In 2003, DataMonitor reported that regular tea drinking in the United Kingdom was on the decline.[17] There

was a 10.25 percent decline in the purchase of normal teabags in Britain between 1997 and 2002.[17] Sales

of ground coffee also fell during the same period.[17] Britons were instead drinking health-oriented beverages

like fruit and/or herbal teas, consumption of which increased 50 percent from 1997 to 2002.[17] A further,

unexpected, statistic is that the sales of decaffeinated tea and coffee fell even faster during this period than

the sale of the more common varieties.[17] In 2011, espresso sales were higher than tea sales.[18]

See also[edit]

A Nice Cup of Tea

Brown Betty (teapot) , an iconic type of teapot made from British red clay, known for being rotund and

glazed with brown manganese

Cube teapot , a heavy duty type of teapot invented for making tea on ships

Earl Grey tea , a classic English blended tea, flavored with Bergamot citrus oil

English breakfast tea

Gunfire (drink) , a cocktail made of tea and rum served in the British Army

List of tea companies#United Kingdom

London Tea Auction

Prince of Wales tea blend

Rich tea , an early form of tea biscuit, created as a light between meal snack to be served with tea

Teacake

Tea sandwich

Teasmade , an English appliance that combines a kettle and a teapot to make tea automatically by

alarm clock

TV pickup , a daily spike in power consumption in the UK due to the use of electric kettles

http://www.tea.co.uk/page.php?id=237

29

With 66% of the British population drinking tea every day there is an understandable thirst for knowledge on all aspects

of tea. Here are a few answers to some of the most popular questions asked about tea. If your question is not answered

here then drop us an e-mail.

A: 165 million cups daily or 60.2 billion per year.

A: No, the number of cups of coffee drunk each day is estimated at 70 million.

A: Republic of Ireland followed by Britain.

A: China with 1,359,000 tonnes, India is second with 979,000 tonnes (2009 production).

A: 96%

A: 98%

A: Simply by "washing" the tea leaves towards the end of the production process in an organic solvent. The method is

strictly governed by legal limits.

Britain’s growing appreciation for green and herbal tea hits sales of builder’s brew

http://www.mintel.com/press-centre/food-and-drink/britains-growing-appreciation-for-green-and-herbal-tea-hits-sales-of-

builders-brew

“Once a cup of builder’s tea was enough to drown the nation’s sorrows, but new research from Mintel finds Brits are

increasingly turning to alternative varieties, as sales of green tea bags have shot up an impressive 83% in past two

30

years alone.

Indeed, the strain is showing for good old-fashioned English Breakfast tea. Although accounting for the biggest share of

the tea market (70%), sales of ordinary English Breakfast tea bags dropped by 1.5% from £470 million to £463 million

between 2010 and 2011. Since 2009, the share of ordinary bags as a percentage of all in home tea sales has declined

from 73% in 2009 to 70% in 2011. What is more, the number of Brits using English Breakfast tea in the past 12 months

has fallen from 87% in 2010 to 83% in 2011.

Meanwhile, other more exotic varieties have shown more positive performances, indeed, between 2009 and 2011,

sales of”"Fruit and Herbal bags”"(valued at £54 million in 2011) increased 10%, while”"Speciality bags”"(£52 million)

and”"Decaffeinated bags”"(£36 million) grew by 8% and 16% respectively. But it was the”"Green bags”"sector which

was the real star performer of the home tea sector. Sales of Green bags grew a sensational 83% between 2009 and

2011, the market almost doubling from £12 million in 2009 to £22 million in 2011. Today, as many as 12% of Brits drink

Green tea on a weekly basis.

Alex Beckett, Senior Food Analyst at Mintel, said:

“”While English Breakfast tea is fondly regarded, the expansion of coffee chains and the exotic flavours of fruit, herbal

and green teas are encouraging consumers to diversify their consumption habits, prompting fewer cups of standard tea

to be drunk. Though the segment continues to play only a niche role in the market, Green tea, like Fruit and Herbal

teas, has benefited from positive associations with healthiness. Green tea extracts are increasingly found in cosmetic

beauty products, raising the profile of Green tea among women in particular.”"

Overall, retail value sales of tea in the UK jumped by 22% to £655 million between 2006 and 2011. Annual sales growth

had rapidly accelerated to 11.9% in 2009 when the market was valued at £610 million. This was largely fuelled by price

inflation, which also remained high in 2010 when the total value hit £660 million. The tea market then declined in 2011,

when value fell 1% to £655 million. Today, tea is drunk by almost nine in ten (87%) Brits.

“”When faced with adversity, Britons have historically reached for a cup of tea. And the state of the current economic

climate should in theory provide bountiful times for tea brands, considering three quarters of users describe it as

comforting. However, diversity appears to be impacting tea consumption more than adversity these days. With usage

rates falling and value sales growth all but reliant on commodity inflation, it could be forgiven for disregarding the long-

established motto to ‘Keep calm and carry on’.”"Alex continues.

Meanwhile, sales of loose leaf tea dropped by 11% between 2009 and 2011, to record £16 million, accounting for just

2% of overall tea sales. While usage of loose leaf remained flat over the period, with 9% of tea users choosing this

format, sales have declined slightly in recent years, with the higher price of loose tea making it more vulnerable to

consumer cut backs in the recession. Surprisingly, the biggest users of loose tea are aged between 25-34 at 12%

31

rather than those aged 65 and over (10%) who were more likely to have grown up using loose leaf rather than tea bags.

“”Most people would think over-55s are the biggest users of loose leaf tea, but it is actually those aged 25-34. Tea has

an increasingly cool image. With many of the nation’s younger consumers’ having a keener interest in food, as well as

quality coffee, this group are more likely to be more open to discovering the benefits of loose leaf, such as the full

flavour of the larger leaves.”"adds Alex.

With a strong possibility that the economy will head back into a recession, the outlook for consumer confidence in the

UK is bleak. However, as a household staple rather than a luxury item, tea sales are unlikely to be strongly adversely

affected. The overall tea market is forecast to grow by 8% to £708 million between 2011 and 2016, as global wholesale

tea prices rebound, forcing manufacturers to pass on the costs. “

TEA CONSUMPTION PATTERN IN THE NETHERLANDS

Coffee and tea drinkers may not need to worry about indulging -- high and moderate consumption of tea and moderate coffee consumption are linked with reduced heart disease, according to a study published in Arteriosclerosis, Thrombosis, and Vascular Biology: Journal of the American Heart Association.Researchers in The Netherlands found:

Drinking more than six cups of tea per day was associated with a 36 percent lower risk of heart disease compared to those who drank less than one cup of tea per day.

32

Drinking three to six cups of tea per day was associated with a 45 percent reduced risk of death from heart disease, compared to consumption of less than one cup per day.

And for coffee they found:

Coffee drinkers with a modest intake, two to four cups per day, had a 20 percent lower risk of heart disease compared to those drinking less than two cups or more than four cups.

Although not considered significant, moderate coffee consumption slightly reduced the risk of heart disease death and deaths from all causes.

Researchers also found that neither coffee nor tea consumption affected stroke risk."While previous studies have shown that coffee and tea seem to reduce the risk of heart disease, evidence on stroke risk and the risk of death from heart disease was not conclusive," said Yvonne T. van der Schouw, Ph.D., study senior author and professor of chronic disease epidemiology, Julius Center for Health Sciences and Primary Care, University Medical Center Utrecht, The Netherlands. "Our results found the benefits of drinking coffee and tea occur without increasing risk of stroke or death from all causes.Van der Schouw and colleagues used a questionnaire to evaluate coffee and tea consumption among 37,514 participants. They followed the participants for 13 years for occurrences of cardiovascular disease and death.Study limitations included self-reported tea and coffee consumption, and the lack of specific information on the type of tea participants drank. However, black tea accounts for 78 percent of the total tea consumed in The Netherlands and green tea accounts for 4.6 percent. Coffee and tea drinkers have very different health behaviors, researchers note. Many coffee drinkers tend to also smoke and have a less healthy diet compared to tea drinkers.Researchers suggest that the cardiovascular benefit of drinking tea may be explained by antioxidants. Flavonoids in tea are thought to contribute to reduced risk, but the underlying mechanism is still not known.Co-authors are: J. Margot de Koning Gans, M.D.; Cuno S.P.M. Uiterwaal, M.D., Ph.D.; Joline W.J. Beulens, Ph.D.; Jolanda M.A. Boer, Ph.D.; Diederick E. Grobbee, M.D., Ph.D.; and W.M. Monique Verschuren, Ph.D. Author disclosures and funding sources are in the study.

Story Source:The above story is based on materials provided by American Heart Association.Note: Materials may be edited for content and length.

Drinking Tea and Coffee in France

http://www.livinglanguage.com/blog/2013/01/24/tea-and-coffee-in-france-and-italy/

33

By Sev

It would be difficult to argue that coffee and tea do not hold a similar importance for French people. After all, cafés are commonplace in

cities, towns and villages of France; and while these establishments serve tea, the most common (and often cheapest) drink indeed is the café (kah-fay) – a plain coffee brewed like espresso. A café sérré is especially strong.For a little more sophistication, there exists some variations:

34

Café au lait (kah-fay oh-lay) is a very popular French coffee with

steamed milk. At home, it is often served in a bol (bowl). To the dismay of foreigners, some French

people like to dip their bread (a slice of baguette, spread with butter) in it.

Café crème (kah-fay khremm) is a coffee served in a large cup with hot cream. Of course, you can

always ask for a Café décafféiné (kah-fay day-kah-fay-uhn-ay) - decaffeinated coffee.

French also drink tea occasionally, but later in the day, and especially in the evening, people enjoy

a tisane (herbal tea). The most common ones

are verveine (verbena), camomille (chamomile), tilleul (tilia, linden), menthe (mint).

Tea in Italy (What?)By Max

Notwithstanding its ancient ties to China — remember Marco Polo and the Jesuits-educated Chinese elite of the Middle ages? — Italy is not exactly known for tea consumption or culture. Even the uber-Italian spaghetti seems to have been imported from China via Marco

35

Polo, however Italy has remained a little resistant to tea so much so that the Italian spelling for tea is in itself is mysterious: the. Italy is a coffee-importer and consumer powerhouse, with leading brands like Illy (from Trieste), Lavazza (Torino), Segafredo (Bologna), and Kimbo (Napoli). Espresso is possibly the most Italian of all beverages.

Of course you can buy tea almost everywhere

and there are people who drink it regularly, but it is not a staple beverage like coffee. In Italy, tea is mostly associated with the flu (influenza) or a cold (raffreddore). Hot tea and honey (miele) are popular during flu season, but that is it. Italians do however enjoy tea

while in the UK, Asia, Middle East, and North Africa. For instance, the author of this post — an Italian — still recalls that, while living in Morocco, he would sip about ten glasses a day of hot tea with mint while lazily watching people walking in the socco.- See more at: http://www.livinglanguage.com/blog/2013/01/24/tea-and-coffee-in-france-and-italy/#sthash.95kt52EE.dpuf

36

TEA CONSUMPTION IN THE U.S.

http://www.teausa.com/14655/tea-fact-sheet

Tea is the most widely consumed beverage in the world next to water, and can be found in almost 80% of all U.S. households. It is the only beverage commonly served hot or iced, anytime, anywhere, for any

occasion. On any given day, over 158 million Americans are drinking tea.

Annual Consumption:

(U.S.)

In 2012, Americans consumed well over 79 billion servings of tea, or over 3.60 billion gallons. About 84% of all tea consumed was Black Tea, 15% was Green Tea, and a small remaining amount was Oolong and White Tea.

Daily Consumption:

(U.S.)

On any given day, over one half of the American population drinks tea. On a regional basis, the South and Northeast have the greatest concentration of tea drinkers.

Iced Tea Consumption: Approximately 85% of tea consumed in America is iced.

Ready-To-Drink Iced Teas:Over the last ten years, Ready-To-Drink Tea has grown more than 15 fold. In 2012, Ready-To-Drink sales were conservatively estimated at $4.8 billion and this trend continues in 2013.

Tea Bags, Loose Tea & Iced Tea Mixes:

In 2012, over 65% of the tea brewed in the United States was prepared using tea bags. Ready-to-Drink and iced tea mix comprises about one fourth of all tea prepared in the U.S., with instant and loose tea accounting for the balance. Instant tea is declining and loose tea is gaining in popularity, especially in Specialty Tea and coffee outlets.

Current Sales:

2012 continued the trend of increased consumer purchases of tea. Retail supermarket sales alone surpassed the $2.25 billion dollar mark. Away-from-home consumption has been increasing by at least 10% annually over the last decade. Total sales have increased 16% since over the last 5 years.

Anticipated Sales:

(U.S.)

The industry anticipates strong, continuous growth over the next five years. This growth will come from all segments driven by convenience, interest in the healthy properties of tea, and through the continued discovery and appreciation of unique, flavorful and high-end Specialty Tea.

Varieties:Black, Green, Oolong and White teas all come from the same plant, a warm-weather evergreen named Camellia sinensis. Differences among the four types of tea result from the various degrees of processing and the level of oxidization. Black tea is oxidized for up to 4 hours and Oolong teas are oxidized for 2-3 hours. As a result, the tea leaves undergo natural chemical reactions, which result in taste and color changes, and allow for distinguishing characteristics. Green & White teas are not oxidized after leaf harvesting, so they most closely resemble the

37

look and chemical composition of the fresh tea leaf. Oolong tea is midway between Black and Green teas in strength and color.

38